global market update - the ciatti company · ciatti global market update | january 2017 2 volume...

TRANSCRIPT

GLOBAL MARKET UPDATE

2016 REVIEW / 2017 PREVIEW Volume 8 Issue No. 1

Fax (415)

458- 5160

CIATTI GLOBAL WINE & GRAPE BROKERS

1101 Fifth Avenue #170

San Rafael, CA 94901

Phone (415) 458-5150

Ciatti Global Market Update | January 2017

2

Volume 08, Issue No. 1, January 2017

As 2017 begins, the team at Ciatti wishes all of our clients,

friends and business associates a very happy and prosperous

year to come. We thank you for your continued support.

It being January, this month’s report reviews the old year on

the bulk market and assesses what the new one may bring. The

two talking points that are likely to reoccur throughout 2017 are: 1)

will (what we believe to be) a pretty much balanced market slip

into undersupply if harvests continue to come in average or below,

and 2) how will political events affect exchange rates?

Last year’s currency turbulence (illustrated on pages 15-16)

could be a foretaste of what is to come this year: Donald Trump is

sworn in as US president on 20th January and the Dutch general

election (15th March), French presidential election (23rd April) and

German federal election (sometime in August-October) are all

slated to occur in 2017. All the while, from the end of March, the

Brexit process will be underway.

As for the coming Southern Hemisphere harvests: the

beleaguered Argentine industry really needs a strong 2017 harvest

to uplift it, but is – like neighbour Chile – experiencing growing

conditions still not fully normalised after El Niño. Argentina’s 2017

grape market is very active; in Chile some 80% of 2017 grapes have

already been allocated. On the flip-side, other than the intense

November storm in Australia’s Riverland and Sunraysia regions, the

Antipodean growing seasons are proceeding smoothly. And while

South Africa continues to battle drought, its record 2015/16

carryover stock is interesting international buyers.

Ciatti looks forward to helping you navigate the twists and

turns of the 2017 market, whatever it may bring, and once again

wishes you a Happy New Year!

Robert Selby

Argentina 2

Australia 3

California 4

Chile 5

France 6

Germany 7

Italy 8

New Zealand 9

South Africa 10

Spain 11

Market profile:

Scandinavia 12

Craft Beer 13

California 3

Argentina 5

Chile 7

France 9

Spain 10

Italy 11

South Africa 12

Australia 13

New Zealand 14

Concentrate Update 6

2016 Currency Review 15

Contacts 17

Ciatti Global Market Update | January 2017

3

CALIFORNIA

Harvest 2016: good in quality,

approximately 4 million tons in size

2016: The Year That Was

Following a 2015 harvest that – at 3.69 million tons – was down 5% on 2014 and one of the smallest

since 2011, calendar year 2016 began with continued price increases on the market as buyers

scrambled to secure ever-scarce supply. The lighter yields from the 2015 vintage in the coastal

vineyards – whose premium offerings have been in rapidly growing demand – created demand of an

intensity not seen for 4-5 years. Meanwhile, yields in the bulk wine powerhouse areas of the interior

and Central Valley were better, and there remained inventory in tank, including for generic and

value-level wines.

By mid-2016, spot market sales for reds – especially Cabernet – were fast, with many sale prices at

historic highs, especially for coastal region high-end and sub-appellation varietal wine and grapes. Ciatti –

deeply involved as it is in the sourcing and sales of many high-end grapes and wines sold domestically –

saw how prices increased significantly on these: high-end Napa Valley Cabernet was going for USD10.50-

13.20/litre by October (up from USD9.25-12.00 in October 2015). In the US consumer market,

premiumization is the buzzword: price categories over USD10 are seeing the strongest growth.

Chardonnay’s 2015 volumes coming in 11.8% down on 2014’s meant that carryover Chardonnay

from past vintages was largely gone by April 2016, while other whites such as Pinot Grigio and Sauvignon

Blanc were also getting short. Thus sales of 2016 grapes on these – and all other varietals, really – were brisk

by mid-year, with higher prices and longer-term contracts being written. Prices remained firm and – on

some varieties – near or above historic highs. Cabernet and Pinot Noir led the demand.

By May it was a case of ‘if we had more, we could sell more’ on 2015 vintage wines – though, again,

value-end wines and older vintages (with buyers increasingly reluctant to move backwards on vintage)

proved tougher to move.

The 2016 harvest’s growing season experienced mercifully few dramas when it came to climate and

disease. The official harvest figure is pending but it is expected at or around 4 million tons – big enough to

replenish the supply pipeline but not enough to create any long positions or soften prices. It was straight

down the middle both in terms of quality and volume on the key varieties: Chardonnay, Pinot Grigio,

Sauvignon Blanc, Cabernet, and Pinot Noir all came in better than in 2016 to varying degrees, but none was

bumper. Other grapes such as Merlot and Petite Syrah are increasingly going into ‘heavy red’ or ‘black red’

proprietary blends like Gallo’s ‘Apothic’ – brand extensions targeted at millennial males.

By the end of the year, buyers were beginning to set themselves up as they normally do on all

varieties, prices looked very similar to last campaign for both domestic and export, and deals were

happening. International buyers were, as every year, mainly prospecting Red Zinfandel, White Zinfandel and

some Cabernet, though some were interested in California’s small Malbec output due to Argentina’s

difficulties. Brexit is a concern for the big Californian exporters: the UK takes 25% of California’s wine export

volumes, and some UK buyers are trying to pass on the cost of a weakened pound sterling to the sellers

(see pages 15-16). The strong US dollar and the attractiveness of the domestic US market – both in terms of

volume demand and its increasing thirst for premium – is serving to reduce exports.

Bottled wine imports into the US are up, assisted by the growing popularity of – among others –

Italian sparkling, Provencal rosé, and New Zealand Sauvignon Blanc. Bulk imports are at okay levels; the

level is very reactionary to market conditions and domestic supply availability. Things have slowed in bulk

but not going away. The bulk imports are filling the holes from declining production and vineyard removal

Ciatti Global Market Update | January 2017

4

in the south of the Central Valley: bulk import remain a cost-effective sourcing strategy. Most bulk is being

sold into labels that are deploying the newer packaging tends: 750ml bottles instead of 1.5 liter, and 3-liter

bag-in-box instead of 4-5 liter.

2017: Looking Ahead

Premiumization is where the action and focus of most wineries in the US is right now. These profitable sales

are driving the activity in grape contracting and new plantings, pre-harvest custom wine contracts and spot

bulk sales. Ciatti expects this to continue.

It seems that some of the steep declines seen in the purchasing of generic or value wines may be

levelling off. There seems to be price increases or reduced discounting on some generics; these generic

programs may be more profitable today. There has been a switch in some of the packaging and bottle sizes

that have affected volumes. For example, there are fewer wines in 1.5 liter glass bottles as more have moved

into 750ml bottles. Also, the growth in 3-liter bag-in-boxes may be affecting 4-5 liter boxes. The 4 and 5

liter glass packages have all but gone away. Wine in cans is getting a lot of hype right now.

There were more consolidations in 2016 than in previous years. As an example, coming in quick

succession mid-year was Gallo’s purchase of Orin Swift Cellars; Jackson Family’s purchase of Copain Wines;

Constellation’s purchase of Prisoner; and the acquisition of Far Niente Estates by GI Partners. Most of the

M&A activity is taking place in the premium segments and for big dollar amounts: this will continue in 2017.

KEY TAKEAWAYS

The 2016 harvest was bigger than 2015’s,

but still not bumper.

Prices for this 2016/17 buying campaign

look very similar to 2015/16 both for

domestic and export.

The premiumization trend is set to continue

in 2017, as is the M&A activity in the

premium wine segment.

That said, there are signs of a pick-up in

interest in generic and value-end wines.

Contacts Contacts

CALIFORNIA – IMPORT / EXPORT

T. +415 458-5150

Greg Livengood (CEO) – [email protected]

Steve Dorfman – [email protected]

CALIFORNIA – DOMESTIC

T. +415 458-5150

John Ciatti – [email protected]

Glenn Proctor – [email protected]

John White – [email protected]

Chris Welch – [email protected]

Ciatti Global Market Update | January 2017

5

ARGENTINA

Harvest watch: continuing abnormal growing

conditions could hit crop size

2016: The Year That Was

Due to El Niño weather, Argentina’s 2016 harvest was 35% down on the 10-year average at 1.75

million metric tonnes. The prior, 2015 crop was ‘small’ at 2.4 million metric tonnes, showing what a

poor harvest 2016 was. Malbec volumes came in 50% lower than the average. The bulk wine market

thus became very active, domestically and for export. The prices for 2016 grapes and carryover stock

rose sharply, and continued to firm-up when 2016 wines came online: most pricing – on bulk Malbec

and generic reds – increased by 100% or more on the previous year. Malbec at USD1.50/litre and

below quickly became short, with higher-end Malbec at USD1.70-2.50 available for longer.

This pricing dissuaded some traditional international bulk wine buyers from sourcing from Argentina

this time. Bulk wine exports were thus down 32% in January-August 2016, from 51.2 million litres to 34.7

million litres, due mainly to the loss of US and Canadian custom. Domestic players were impacted by the

high price and short supply of generic red, passing on some of the cost to Argentine consumers already

labouring under high inflation and a recession (the new government began the rollback of the previous

government’s energy subsidies: some people’s energy bills rose as much as 400%). The pressure on the

consumer price in Argentina has been intense: a 1-litre Tetra Pak of entry-level wine costing 15 pesos

(USD1) at the start of 2016 cost closer to 28 pesos (US1.87) by September, a nigh-100% price hike.

From October, Argentina’s domestic big three players began shipping in generic bulk wine from

Chile to cover their Christmas and New Year needs. Some 17 million litres was imported in October and

November combined. The Argentine buyers braved a Chilean market likewise affected by El Niño, and

forced to pay a bulk price of approximately USD0.65/litre, up from USD0.40-50 some weeks before. By the

end of the year, there was very little wine in Argentina to interest international buyers. Grape juice

concentrate prices remains at their high level of USD1,300-1,400/MT, up from USD800/MT a year before,

and sales are slow (see page 6).

Argentine growers have been facing severe headwinds: the cost of all the spraying that was required

on the small 2016 harvest, combined with increased energy bills throughout 2016 – and interest rates at 40-

50% making borrowing unrealistic – mean that some will have endured a year without income, and longing

for a decent 2017 harvest.

Growing conditions for the 2017 harvest have not been ideal; it seems the weather has not fully

returned to normal after El Niño passed. Heavy spring frosts and October hailstorms were experienced in

Mendoza. The wine industry needs a good 2017 harvest so that it can harness the new government’s fiscal

encouragement of exports and agriculture: the Argentine president, Mauricio Macri, wants his country to

become “the supermarket of the world”.

2017: Looking Ahead

For 2017 in Argentina, Ciatti expects another tough year depending on the harvest result. Argentina will

need a fantastic crop size but – due to the weather events already experienced – Ciatti is not very optimistic

about that. Prices will remain high for the first half of the year due to lack of stock and high demand.

The 2017 grape market will be very active: the most important players are already talking to the

growers to secure their needs so strong pricing can be expected. Even though the availability situation

could improve on some wine varietals, Malbec pricing will remain strong.

Domestic consumption in 2017 will be down from 24 litres per capita to 20-21 litres per capita, so

demand could be softened by the second half of the year. SEE NEXT PAGE FOR KEY TAKEAWAYS

Ciatti Global Market Update | January 2017

6

GRAPE JUICE CONCENTRATE: UPDATE

TIME ON TARGET

California’s 2016 generic grape harvest for white grape juice concentrate (GJC) will probably go down as

one of the lowest in the state’s history. Unsustainable growing costs and more profitable alternative crops

continue to cause massive pull-outs of generic grapes. Despite this fact, there is still product available as

demand has dwindled in a food and beverage industry plagued by the ongoing war on sugar.

Rubired grapes used in standard and high color red GJC continue to sell at a premium as winery

demand and the food/beverage market demand for natural colors continues to grow. While the volume of

this year’s crop was average, the color levels in the grape were very low, causing higher production pricing

and lower yields in finished product.

The 2016 harvest of grapes for concentrate in Argentina was considerably down because of poor

weather conditions throughout the growing season. Most generic grapes that could be harvested went to

wineries. What product was available to the concentrate marketplace was higher-priced and of less than

desired quality. The industry is anticipating a much better harvest in 2017 which should bring pricing and

volumes back into a competitive position.

Spain’s generic harvest was shorter than anticipated because of the lingering drought in the

growing regions. Most of the generic grapes went into wine, leaving the white GJC market short. For this

reason pricing has increased and most of the product has been sold for the season. Current stock pricing

may drop depending on what the 2017 Argentina harvest brings.

On the red GJC front, Spain pulled out of the market as EU demand soared for the red grapes in

Spain’s wine industry. This demand increase occurred because availability of Chilean product was

diminished due to Chile’s very poor 2016 harvest. Massive rains at the end of Chile’s harvest meant that all

available red grapes went to wineries in 2016: Chile’s red GJC is thus very limited and expensive at this time.

Ciatti is anticipating product availability as the 2017 harvest nears, barring another weather problem.

KEY TAKEAWAYS

The 2017 grape market will be very active following

a very short 2016 crop and with another short crop

feared for this year. A continued output shortfall

could be partially offset by domestic consumption

declines as Argentine consumers rein in spending.

Ciatti Contact

Eduardo Conill

T. + 54 261 420 3434

KEY TAKEAWAYS

Lower yields in Argentina, Spain and Chile – due to

adverse weather conditions – have raised GJC

prices in those markets. A low white GJC yield in

California, the result of ongoing pull-outs of

generic grapes, has been offset by the war on

sugar. The state’s red GJC volume is low due to

very low color levels in the grapes.

Ciatti Contact

Grape & fruit juices, concentrates,

natural colorants

John Ciatti

T. +415 458-5150

Ciatti Global Market Update | January 2017

7

CHILE

Harvest watch: abnormal weather possibly

causing lighter, not uniform bunches

2016: The Year That Was

El Niño weather conditions reduced the 2016 Chilean harvest to 1.014 billion litres, down 21% from

1.2 billion litres in 2015 (an average year) but in-line with the frost-hit year of 2014. The 2016

volume figure was better than previously feared – an earlier estimate had the harvest at 800-900

million litres – because the wineries tried to crush as much as possible, accepting grapes affected by

the El Niño rains. Thus, unlike in the earthquake-impacted year of 2010 for example, quality was

down as well as volume. DOC reds came in at 590 million litres, with DOC Carmenere (-36%), Merlot

(-28%) and Cabernet (-27%) well down on 2015.

The harvest was late, as growers waited for sugars and colours to materialise due to the abnormally

cool conditions. These cool conditions were conducive for the whites (Valle Central Sauvignon Blanc quality,

for example, was better than ever), but the quality of the reds was more affected. The reds were further

impacted as they were still on the vines when late heavy rains came: Carmenere and Syrah, then Cabernet

and Merlot, were worst hit. By August it was pretty clear that if buyers needed good quality wines in large

volumes – particularly reds – they would need to step into the market immediately if they hadn’t already

done so. On the flip-side, there would be some very aggressively-priced low-end red wines available on the

spot market.

The industry ensured its prices did not get out of control like they did in 2010; varietal Cabernet for

international buyers increased to USD0.85-90/litre, but not upwards of USD1.30/litre as in 2010. Because

pricing increased less markedly than in 2010, some buyers disbelieved reports of the severity of the year’s

production shortfall, and held off – some for too long.

Tintorera for colour was in great demand. Tintorera, Sauvignon Blanc – both down 17-20% in output

– and Pinot Noir grapes were almost completely pre-harvest allocated and sold out before the crush. After

crush in May and June there was a market frenzy on all wines as domestic and international bulk buyers

sought to cover their needs.

Before the late rains, Chile was visited by Spanish and Argentinian buyers who held off as prices

remained firm; when the rains came and prices firmed-up even more, these buyers went away. Argentinian

buyers, however, were back prospecting the market in August and September as Argentina’s tight market

situation grew more acute. From October, Argentina’s domestic big three players began shipping in generic

bulk wine from Chile to cover their Christmas and New Year needs. Some 17 million litres of Chilean bulk

wine was imported into Argentina in October and November combined. The Argentinian buyers were

paying USD0.65/litre, up from the USD0.40/litre they could have paid a couple of months earlier.

2017: Looking Ahead

Looking forward, the market could potentially be stable. Unfortunately this has never happened in Chile,

and there will likely continue to be its characteristic volatility. Currency exchange, increasingly unpredictable

weather and the small domestic market will normally cause price fluctuations in this market.

More than 80% of Chile’s 2017 grapes have been allocated: their prices have been high, and

continue to rise. The grape prices are the base for the wine price calculations, and the result of current

market prices. The first grapes to be allocated were those grown on vertical trellis systems. Until December’s

start there was very low demand for the pergola grapes; transactions for these are happening now.

Chile is still receiving good demand for its wine, and Ciatti believes all the traditional buying

countries will continue with their normal needs. Argentina, not a traditional buyer, may continue to be a

Ciatti Global Market Update | January 2017

8

buyer for the 2017 crop, but its demand pressure should reduce; China is always a big player, though bigger

in some years than others.

Weather remains abnormal. Last month the Central Region received record rain levels for the month

of December, as well as record highest temperatures. Harvest seems to be coming earlier than normal,

which potentially decreases the level of rain damage on the grapes. Viticulturists speak of lighter and not

uniform bunches being the reason for a potentially smaller 2017 crop. One potential crop forecast figure

appears to be 1.1 billion litres. As mentioned, prices should remain stable for a while. The crop size and

demand will dictate the market, especially by the end of the year when wineries need to have their wines

allocated in order to receive the next crush.

KEY TAKEAWAYS

More than 80% of Chile’s 2017 grapes have already

been allocated. Their prices have been high, and

continue to rise. Transactions on pergola grapes

are happening now. Prospect of the harvest’s

bunch weights being affected by abnormal weather

is intensifying transactions.

Ciatti Contact

Marco Adam

T. +56 2 2363 9206 – or – T. +56 2 2363 9207

Chilean Export Figures Wine

Export Figures

January 2015 – November 2015 January 2016 – November 2016 Volume

Million Liters

Million US$ FOB

Average Price

Million Liters

Million US$ FOB

Average Price

Variance %

Bottled 437,04 1.386,04 3,17 444,83 1.376,01 3,09 1,78

Bulk 337,85 235,44 0,70 351,07 239,97 0,68 3,91

Sparkling Wines

4,03 16,49 4,09 4,81 19,33 4,02 19,34

Packed Wines

25,98 44,19 1,70 29,39 49,25 1,68 13,13

Total 804,90 1.682,16 2,42 830,11 1.684,55 2,37 3,13

Ciatti Global Market Update | January 2017

9

FRANCE

Harvest 2016: at 43.2 million hectolitres,

down 8% on five-year average

2016: The Year That Was

With almost 48 million hectolitres of wine produced, France’s 2015 vintage was larger than the five‐

year average, with more volumes produced in Languedoc (+1 million hectolitres versus 2014), the

Southwest and Bordeaux, and less in the eastern regions (Burgundy, Alsace and Champagne).

The overall market pricing for varietal and AOP wines had remained firm and steady, accompanied

by smooth and regular loadings until the end of winter 2015-16. However, the market experienced an

important slowdown from then on, with less demand and a slow loading pace. Rosé was the most impacted

category with an important unsold carryover stock until the beginning of the 2016-17 buying campaign.

This led to the emergence in 2016 of protest groups organised by southern French growers, who

attributed slow sales and large carryover stocks to the growing level of foreign wine imports (mainly from

Spain and Italy and also from Chile and South Africa). These protest groups carried out such actions as

forcing Spanish trucks to dump their Spanish wine cargo at the border.

The explanation for the increase in imports is price: France losing share to Spain and other countries

on 3-litre or 5-litre bag-in-box programmes – due to being uncompetitive on price – has exaggerated

French wine’s market share loss in terms of volumes. French supermarkets are sourcing foreign wines not

only to make a bigger margin but also to maintain the retailing pricing: French wine prices have simply

exceeded the maximum that retailers can absorb. The problem regarding export sales is the disparity

between the price and the quality offered by French wines, with French wines’ price-quality ratio having

struggled to adapt to international buyers’ increasing expectations.

In contrast to 2015-16, the current, 2016-17 buying campaign got underway with smaller 2016 crop

results for most of the producing regions (except Bordeaux and Côtes du Rhône), together with a slow kick-

off. The harvest is reported at 46.5 million hectolitres. At the beginning of summer 2016, hopes for a good-

sized crop were strong but the southern European heatwave, combined with sporadic hailstorm episodes,

impacted growers’ expectations. In the end the 2016 crop was characterised by an important heterogeneity

in terms of quality: red wines are better than whites and rosés (lacking acidity and aromaticity). Due to the

slow-moving market for the old carryover stock, growers’ price expectations have steadily been reduced

until the beginning of 2017 – also due to the slower than usual buying activity (specially for varietal wines).

2017: Looking Ahead

Pricing on the 2016 vintage now seems to have stabilised and should remain at current levels for the next

couple of month at least. Of course, the inventory on the best qualities is getting lower faster.

Although French producers have seen important market share losses in export markets over the last

couples of years, the national market remains active and shows steady demand. This demonstrates the

home market’s predominance and importance, remaining as it is the first destination for French wines. The

problem for French producers is that good demand from the bag-in-box segment – currently representing

40% of overall sales – provides comfort, but it is also the segment least attached to country of origin, thus

French IGP wines are potentially always under threat of being replaced. With a much-needed price adjustment

and a price hierarchization starting to take place, slower but still good activity overall should be assured.

KEY TAKEAWAYS

Slow activity on 2015 carryover and 2016 vintage

has served to reduce prices. France’s much-needed

price adjustment is seen to be taking place.

Ciatti Contact

Florian Ceschi

T. +33 4 67 913532 E. [email protected]

Ciatti Global Market Update | January 2017

10

SPAIN

Harvest 2016: volumes reportedly in-line

with 2015; rosé down

2016: The Year That Was

Calendar year 2016 began active following a 2015 crop – at 41-42 million hectolitres – down some 8-

10% on 2014. Although the white grape crop in the powerhouse Castilla La Mancha region had come

in 15-20% down, this was compensated for by lower GJC production (see page 6) and satisfactory

wine inventories were maintained. The red grape crop came in larger than the year before, thanks to

higher production in the south-eastern regions of Manchuela, Jumilla, and Valencia.

Carryover stock from 2014 helped soften the overall price increase on the Spanish market.

International varietal wine inventories were starting to get low during 2016, especially for Chardonnay,

Sauvignon Blanc and Merlot, but good opportunities remained for Muscat, Cabernet Sauvignon, and Syrah.

In generic wines, the market reacted differently, with domestic and international buyers buying aromatic

blenders, high alcohol wines and colour enhancers, in order to cover only their short- to mid-term needs as

part of a wait-and-see strategy.

Following a very hot and dry summer, the 2016 harvest season started with huge uncertainty about

the crop potential. Non-irrigated vineyards suffered the most from the dry conditions (seeing a 30% drop)

whereas irrigated/trained vineyards coped better to moderate the final average loss. The actual crop size is

not yet known, but it is believed to be roughly 42-43 million hectolitres, roughly in line with the year before.

The quality was very good overall, the only issue being the low average alcohol degree (especially for white

wines) and a low acidity on whites/rosés.

Due to the inability to assess the real crop size, the beginning of the harvest season saw a rapid and

regular grape price increase (+10-15%), mainly led by Spain’s top three players in an attempt to secure the

supply for their case goods programs. Automatically, the average market price for bulk increased by

approximately 10% on all kind of wines as co-ops and private wineries had to reflect the grape price

increase in their bulk wine offers.

Even though 2015 vintage carryover was moderate, the 2016-17 campaign started very slowly (with

mainly domestic activity) as most of the international buyers maintained a wait-and-see position until more

precise crop figures appeared. In fact, according to the latest figures published by the Spanish Ministry of

Agriculture, the 2016-17 campaign started with an initial inventory of 40.59 million hectolitres of wine and

almost 4.52 million hectolitres of non-concentrated must (45.11 million hectolitres in total).

2017: Looking Ahead

Ciatti considers the Spanish market to be in a balanced situation with enough supply for a smooth bulk

wine campaign. International buyers know perfectly well the situation and are only covering their immediate

to mid-term needs, waiting for better opportunities to arise. As a consequence, Ciatti has seen the market

price slowly but surely decrease from the high peaks of October, especially on the white wines. The price

drop on the reds is moderate whereas the rosé pricing remains stable due to the fact that wineries

produced their 2016 volumes based on the level of volume sold of the 2015 vintage, plus a balanced

inventory.

KEY TAKEAWAYS

A slow start to the 2016-17 buying campaign has

seen prices fall since October. Rosé pricing is stable

as 2016 production was significantly down.

Ciatti Contact

Nicolas Pacouil

T. +33 4 67 913531 E. [email protected]

Ciatti Global Market Update | January 2017

11

ITALY

Harvest 2016: at 46-47 million hectolitres,

the world’s largest

2016: The Year That Was

Although world production in 2016 was one of the lowest in recent years, Italy had a normal crop

and you can see this on the market. In theory Italy’s market should have been more active, with

prices rising. Instead the market was simply staying more or less level with the last vintage. The year

saw an increase in demand from Germany and Eastern Europe but not enough to raise prices.

The Prosecco market in 2016 was still growing and the varietal was slowly stealing shelf space from

Pinot Grigio, which was suffering a little, mainly due to the confusion created during 2016 regarding the

possible transition to the DOC for the main production area of the north-east.

International varietals, especially of the higher quality, were still in good demand and – in general –

demand was increasing for the high-level wines. Entry level wine was always in competition with Spain’s:

often the buyer’s final decision was based upon a simple calculation of the difference in transport costs. For

some countries such as Russia and those in Eastern Europe, Italy seemed to be the more competitive

solution. For France and Germany the final calculation was very close and the decision was made on the

quality and commercial condition, but the feeling was that lots of companies were still waiting for prices to

lower on the entry-level qualities. In the nine months until the end of September 2016, Italy was regaining

market share in Germany but its overall exports to the German market was down by approximately 6%.

2017: Looking Ahead

Ciatti won’t be surprised if 2017 will bring a general increase in the bulk wine price. Lots of large European

companies, given the fact that a lot of supermarkets were delaying some big tenders, still have to finalise

their purchasing. If this happens during the coming months the market could change a little and there may

be a shortage in some wine categories like the good sparkling bases and the good red wines in general.

It is very improbable that Spain will downgrade its prices soon; it will wait to get more information

regarding the 2017 South Hemisphere harvests.

The impression is that consumption around Europe is changing: sparkling is on the rise, as is

sparkling wine mixers. Some cheap wine of very low quality will be very hard to sell in future.

Regarding the global economic environment, it is probable that the euro will weaken against all the

main currencies throughout the year, assisting exports. But inflation may rise off the back of the oil price

and this would not be good for consumption levels. The new US president’s policies should in theory help

the purchasing power of US workers, but a round of protectionist measures might hinder European exports

to the US. China is still a very small market for Italy but with a different approach maybe it can become a

more important player.

KEY TAKEAWAYS

Italy’s buying campaign has commenced slower

than expected. Italian sellers are keeping a close

eye on the important UK and US markets; an

unconducive exchange rate with the former and

potential protectionist measures in the latter could

make things harder for Italian imports.

Ciatti Contact

Florian Ceschi

T. +33 4 67 913532

Ciatti Global Market Update | January 2017

12

SOUTH AFRICA

Harvest watch: drought may affect

the 2017 crop size

2016: The Year That Was

South Africa’s 2016 harvest started two weeks earlier than normal, due to eight very dry, preceding

months, which made it possibly the driest ripening season in 40 years. The crop was predicted to be

10-12% smaller; it in fact came in only 6.7% down on 2015, though still the smallest crop since 2012.

Already by the end of February, predictions were that varietals like Cabernet, Sauvignon Blanc and

Chardonnay would be short; after Q1 2016, Merlot and even possible Chenin Blanc shortages were

predicted. Following the largest-ever carryover stock (46%) from 2015 to 2016, this gave producers new

confidence. By the start of Q2, pricing showed increases on short varietals and exports showed an 8%

growth year-on-year.

Good rains in late April and early May and increased contracting and shipments over that period

bolstered producers further, especially after a disastrous depreciation in the SA Rand over the previous 15-

18 months. The Rand weakened from January 2014 to Jan 2015 by a shocking 40%+, rallied again quickly,

but was still 27% down on that 2014 base by end of Q1 2016. At year-end 2016, the Rand was still 20%

down on that 2014 base.

Following a dry spell in June, further cold spells with good rain and snow in July and August raised

hopes for 2017, but catchment dams were still only around 55% full. Shortages in Chile and corresponding

price increases there raised expectations of a buyer influx into South Africa, but that was only realised

around October. Domestic sales grew exponentially month-on-month, but were mostly driven by bag-in-

box sales; value, therefore, didn’t show the same domestic growth as volume. On the export front, exports

to the UK and Germany showed a decline by the end of Q3, while France is now South Africa’s third-largest

export client-country after a very short history of importing South African product. This has been driven

mostly by Cinsaut Rosé and varietals Sauvignon Blanc, French Colombard and/or blends of these varietals.

Brexit raised major concerns in July: even though South African producers sell in Rand, a much-

depreciated UK pound sterling raised concerns of decreased UK consumer spending. That was fairly short-

lived as, by the end of September, consumer confidence in the UK had already returned.

By October, dry conditions again returned, compounding the effect of last year’s drought. Producers

had to start irrigating much earlier than usual, on top of low catchment dam levels. At the time of writing –

Christmas 2016 – that drought still persists and strict water restrictions are in force even in the cities,

carrying heavy penalties. October also brought a spell of Black Frost to the important Worcester and

Breedekloof bulk wine areas, which will affect the 2017 crop to some extent.

2017: Looking Ahead

The last quarter of 2016 brought the sudden influx of buyers that was expected to have arrived by midyear.

Russian, Chinese, EU and US buyers are contracting everything, including generic reds and whites, with

shipments planned ASAP in the New Year. This has brought welcome relief from that record 2015/16

carryover and also resulted in price increases at all levels on all products. The continuing drought may result

in another small 2017 crop and with lower starting-stock levels, the higher demand and expected pricing

will bring welcome relief to a country where sustainability has been at extreme risk for many years.

KEY TAKEAWAYS

South Africa is receiving a lot of interest from

international buyers on all categories, including

generic reds and whites, denting the carryover stock

and increasing pricing at all levels on all products.

Ciatti Contacts

Vic Gentis

T. +27 21 880 2515

-or-

Petré Morkel

T. +27 82 338 8123

Ciatti Global Market Update | January 2017

13

AUSTRALIA

Harvest watch: early indications point

to a harvest average-sized

2016: The Year That Was

Australia’s 2016 crush figure came in at 1.81 million tonnes as per the Winemaker’s Federation of

Australia (WFA). This figure is a 6% increase on the 2015 crush of 1.67 million tonnes. The main

increase came from a surge in volume of cool climate fruit. Prices firmed as the average purchase

price increased 14% to AUD526/ tonne. Ciatti has seen slight upward pressure on pricing throughout

the year, not only due to higher fruit prices but the cost of water earlier in the season, as well as

increased demand from China. Australia saw additional interest due to the smaller volumes available

in Chile and Argentina. Pricing pressure has also occurred due to an increase in the amount of

vineyards and agricultural land being converted to almonds: the potential for larger incomes and

profitability from these crops has enticed many farmers to convert.

As at September, Australia’s wine exports have seen an overall increase in value to AUD2.17 billion,

up 10% in the last 12 months and a 0.2% increase in volume to 734 million litres. White varieties such as

Pinot Gris and Sauvignon Blanc were popular from early in the year with irrigated parcels of Shiraz and

Cabernet being the main red wines of interest. The quality level of 2016 fruit was very good with no disease

pressure.

China’s interest in Australian wine has increased exponentially in 2016. In January, the US was

Australia’s No.1 export country by value whilst China was third. By September, China had risen to pole

position with 90 million litres of wine being shipped there at a value of AUD474 million. This was an

increase of 52% in volume and 51% in value in the past 12 months. Chinese interest in wine continues to

grow as we see more foreign parties looking to purchase vineyards, winery infrastructure and brands. Many

wonder where the Australian wine industry would be without this Chinese interest.

The Wine Equalisation Tax Rebate (WET) has been a continuous debate throughout 2016 with a

number of potential amendments considered for the ruling. The WET Rebate was originally initiated to help

small wine producers offset the tax’s cost to them. The government has finally opted to remove the WET

Rebate from bulk wine and cleanskins as of 31st July 2018. This removal will ensure a consistent price

offered for bulk wine versus two set prices.

Water availability at the beginning of 2016 was in short supply and high in cost – some growers

were forced to pay as high as AUD300 per megalitre in order to sustain their vineyards. Growers were

initially advised that they would only receive 36% of their allocations from 1st July and were grateful when

the winter period provided decent rainfall which flowed through to spring. Growers now have 100% of their

allocation for the upcoming summer period. Aside from November’s hail and wind event, which affected

the Riverland and Sunraysia areas, the growing period has been smooth.

2017: Looking Ahead

Demand for Australian wine has been strong and Ciatti expects this to continue into 2017. Domestic buyers

for next year’s irrigated fruit have been active in the market to obtain the material required early in the

season. Chinese interest is expected to continue with further demand for reds such as Shiraz and Cabernet

from both irrigated and cool climate regions. White varieties such as Pinot Gris and Sauvignon Blanc are

expected to be in high demand with a good amount of material to be signed up in pre-harvest

contracts. Early indications point to an average-sized harvest but this will be dependent on any future

weather conditions. Growers have access to a good supply of water and expect a dry summer period (with

no disease pressure). SEE NEXT PAGE FOR KEY TAKEAWAYS

Ciatti Global Market Update | January 2017

14

NEW ZEALAND

Harvest watch: early indications point

to a harvest average-sized, smaller than 2016

2016: The Year That Was

The 2016 crush figure for New Zealand came in at 436,000 tonnes, up 34% from 2015. The main

variety, Sauvignon Blanc, accounted for over 303,000 tonnes of this amount. The start of the season

was very dry with limited rain before wet weather commenced in March, causing disease pressure for

many growers. The larger volume of grapes available saw downward pressure on bulk pricing for

Sauvignon Blanc – from NZD4.00-5.00/litre to mid-high NZD3/litre.

It was revealed in mid-2016 that the value of New Zealand wine exports increased to NZD1.54

billion in 2015, up from NZD1.42 billion in 2014. Wine is currently the country’s sixth-largest export with the

majority of material being shipped to the US and Australia. Can New Zealand meet the world’s demand for

Sauvignon Blanc? The availability of suitable land for vineyard development to either purchase or lease is

becoming in short supply with potential buyers now looking to develop terraced-style vineyards. Some

36,192 hectares of vineyards are currently planted with an average yield of 12.0 tonnes per hectare, a

production capacity of 313 million litres of wine. The average price for fruit from 2016 was looking to reach

NZD1,800 per tonne – in the past prices have fluctuated heavily from as low as NZD1,239 per tonne in 2011

to NZD2,161/tonne in 2008.

November’s 7.8 magnitude earthquake on the South Island caused a 2% loss in volume and varying

damage on 20% of the storage tanks. Many wineries are looking to have these repairs fixed as soon as

possible in the lead up to vintage. Others are also looking into repairs for their irrigation systems. This could

have some effect on the 2017 crush, but the size of the impact is still unknown.

2017: Looking Ahead

The demand for Marlborough Sauvignon Blanc is expected to continue as market activity remains

strong. Sales to the US and Australia continue to grow. Good-size inventories remain of the 2016 material

and prices are staying firm at their current level. Aside from the earthquake, there has been minimal impact

on the growing season this year. Early indications are for an average year, lower than the large crush of

2016 – but there is still five months to go before vintage commences.

AU & NZ KEY TAKEAWAYS

Australian wine remains in strong demand, with

increased Chinese interest putting pressure on

prices and pre-harvest 2017 contracts being made.

Shiraz, Cabernet, Pinot Gris and Sauvignon Blanc

particularly are in demand. Due to its big 2016

crop, NZ’s prices are steady; Sauvignon Blanc will

remain in strong demand and suitable space for

increasing production is growing scarce.

Ciatti Contacts

Matt Tydeman

Simone George

T. +61 8 8361 9600

Ciatti Global Market Update | January 2017 15

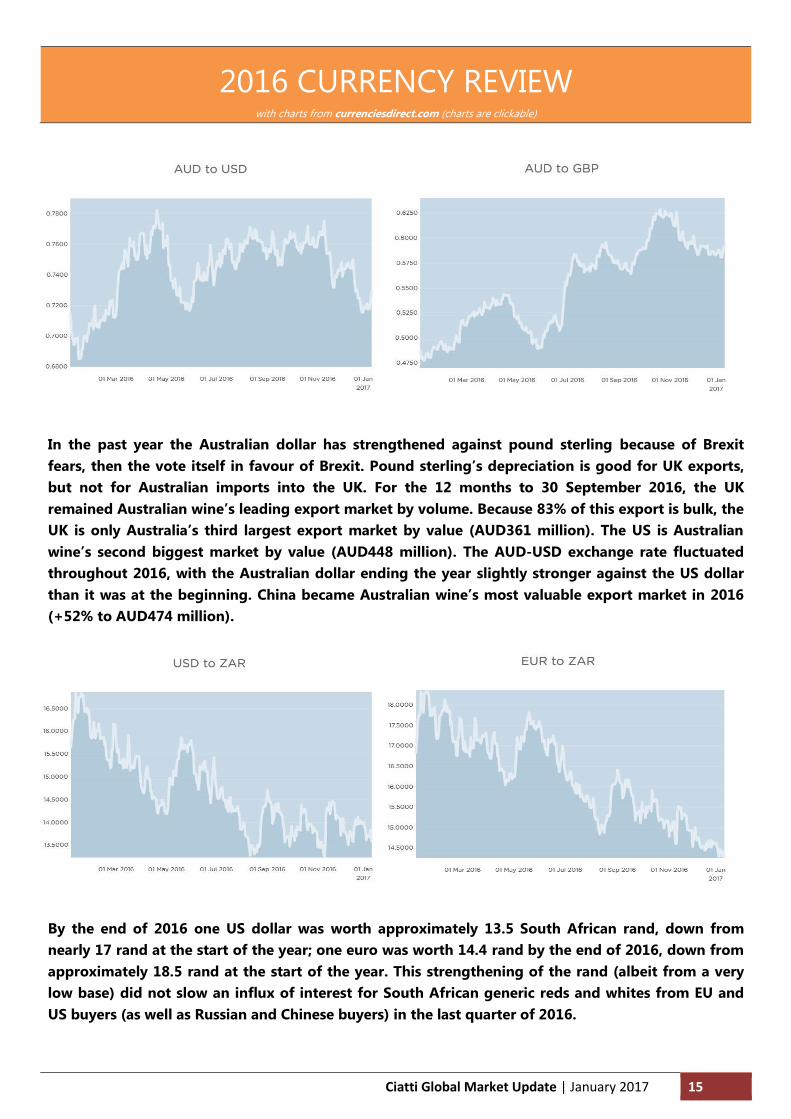

2016 CURRENCY REVIEW with charts from currenciesdirect.com (charts are clickable)

In the past year the Australian dollar has strengthened against pound sterling because of Brexit

fears, then the vote itself in favour of Brexit. Pound sterling’s depreciation is good for UK exports,

but not for Australian imports into the UK. For the 12 months to 30 September 2016, the UK

remained Australian wine’s leading export market by volume. Because 83% of this export is bulk, the

UK is only Australia’s third largest export market by value (AUD361 million). The US is Australian

wine’s second biggest market by value (AUD448 million). The AUD-USD exchange rate fluctuated

throughout 2016, with the Australian dollar ending the year slightly stronger against the US dollar

than it was at the beginning. China became Australian wine’s most valuable export market in 2016

(+52% to AUD474 million).

By the end of 2016 one US dollar was worth approximately 13.5 South African rand, down from

nearly 17 rand at the start of the year; one euro was worth 14.4 rand by the end of 2016, down from

approximately 18.5 rand at the start of the year. This strengthening of the rand (albeit from a very

low base) did not slow an influx of interest for South African generic reds and whites from EU and

US buyers (as well as Russian and Chinese buyers) in the last quarter of 2016.

Ciatti Global Market Update | January 2017 16

Brexit fears, then the result of the referendum on 23rd June, saw pound sterling slump against the

euro in 2016. The UK market has become a concern for European wine traders with a UK focus, such

as Italy’s Prosecco and Pinot Grigio producers and France’s Côtes du Rhône region. Suppliers to the

UK are being asked by UK buyers to absorb the cost of the weakened pound. However, UK

consumers are repeatedly being prepared – by government and through media – to expect higher

prices in 2017, which may allow some space for price rises to be passed on to the consumer without

sales being unduly shocked. On the flip-side, the US dollar has fluctuated with but strengthened

against the euro, assisting imports into the US of French and Italian sparkling wines, and French rosé.

Brexit saw pound sterling weaken substantially against the US dollar in 2016. At the start of the year

one dollar was worth approximately GBP0.68; by the end it was worth over GBP0.80. The dollar’s

strengthening relative to the pound is placing some strain on some big US brands with a UK focus.

As European suppliers are finding out, some UK buyers are essentially asking sellers to discount

their prices at the rate the pound has fallen. The UK received 25% of US wine export volume in

2015. Canada, meanwhile, is the second biggest destination for US wine exports after the EU-28 (in

2015, US wine sales surpassed wines from France and Italy for the first time to claim the largest share

of imported table wines in the Canadian market). At the start of 2016, one US dollar was worth over

CAD1.45; however, the Canadian dollar rallied in relation to the US dollar by mid-year following a

poor 2015, and ended the year at CAD1.32.

Ciatti Global Market Update | January 2017 17

CONTACT US

ARGENTINA Eduardo Conill

T. +54 261 420 3434 E. [email protected]

AUSTRALIA / NEW ZEALAND

Matt Tydeman Simone George

T. +61 8 8361 9600 E. [email protected]

CALIFORNIA – IMPORT / EXPORT CEO – Greg Livengood

Steve Dorfman T. +415 458-5150

E. [email protected] E. [email protected]

CALIFORNIA – DOMESTIC

T. +415 458-5150 John Ciatti – [email protected]

Glenn Proctor – [email protected] John White – [email protected] Chris Welch – [email protected]

CONCENTRATE

John Ciatti T. +415 458-5150

CANADA & US CLIENTS OUTSIDE OF CALIFORNIA

Dennis Schrapp T. 905/354-7878

CHILE Marco Adam

T. +56 2 2363 9206 or T. +56 2 2363 9207

CHINA / ASIA PACIFIC Simone George

T. +61 8 8361 9600 E. [email protected]

FRANCE / ITALY Florian Ceschi

T. +33 4 67 913532 E. [email protected]

GERMANY

Christian Jungbluth T. +49 6531 9734 555 E. [email protected]

SPAIN

Nicolas Pacouil T. +33 4 67 913531 E. [email protected]

UK / SCANDINAVIA / HOLLAND

Catherine Mendoza T. +33 4 67 913533

SOUTH AFRICA Vic Gentis

T. +27 21 880 2515 E: [email protected]

-or- Petré Morkel

T. +27 82 338 8123 E. [email protected]

JOHN FEARLESS CO. CRAFT HOPS & PROVISIONS

CEO - Rob Bolch T. + 1 800 288 5056

johnfearless.com