global healthcare it consulting · as was the case with the us market ... natalie jamison ......

TRANSCRIPT

GLOBAL HEALTHCARE IT CONSULTING

WHICH FIRMS ARE CONSIDERED FOR IMPLEMENTATION AND ADVISORY WORK?

| A U G U S T 2 0 1 7 | P E R C E P T I O N R E P O R T

GLOBAL HEALTHCARE IT CONSULTINGWHICH FIRMS ARE CONSIDERED FOR IMPLEMENTATION AND ADVISORY WORK?

Implementation Services

Both IT Advisory & Implementation

IT Advisory Services

Deloitte, PwC Most Broadly Considered Firms for HIT Work

Deloitte and PwC headline the list of 89 unique firms that provider organizations indicate they would consider for HIT consulting work. Deloitte is widely considered and respected for their advisory and implementation work. PwC is looked at almost exclusively for IT advisory engagements; infrequently, they are considered a strong option for hospital-led implementation projects. Thanks to expertise in UK and Middle East EMR implementations, The HCI Group (a relatively new multiregional firm) is the only smaller firm to break into the ranks of the large multiregional consulting firms in terms of total considerations. KPMG, Accenture, and EY round out the list of top 6 firms considered. Looking to the future, about 40% of provider organizations have plans to engage a consulting firm in the next two years. As was the case with the US market 7–10 years ago, large-scale EMR deployments are the single biggest driver of consulting engagements due to the strategy, advisory, and implementation work they require.

With EMR implementations outside the US on the rise, many provider organizations have asked KLAS which firms they can turn to for help in planning for or implementing an EMR. Within healthcare organizations, resources for strategizing and implementing are often stretched thin, and this report—KLAS’ first on consulting firms outside the US—highlights how these organizations perceive healthcare IT (HIT) consulting firms. Who are they considering for upcoming projects, for what purpose, and who has mindshare?

1

Firms Under Consideration, with Regional Breakout

Regional Mindshare of Consulting Firms

Plans to Use Consulting Services in the Next Two Years

Deloitte

(n=100†)

Neither

Accenture

NTT DATA (Dell Services)

DXC Technology (CSC)

The HCI Group

IBM

Healthtech Consultants

Other—Multiregional

PwC

EY

McKinsey

HQS Plus

KPMG

Gartner

Other—Regional

Canada(n=17)

Asia/Oceania(n=12)

Latin America(n=14)

Europe(n=38)

Middle East

(n=16)

0% 70%

19%

17%

6%

58%

4+ Mentions

Project-Specific Considerations

† Note: 3% of providers are considering engaging a firm for technical services and 3% are considering a firm for IT outsourcing.

1–3 Mentions

Overall Mindshare

34%

29%

18%

16%

15%

15%

9%

8%

6%

5%

30%

60%

4%

3%

3%

(n=97)

REPORTS 2017

For complete list of firms included in "Other" see figure 7 on page 15.

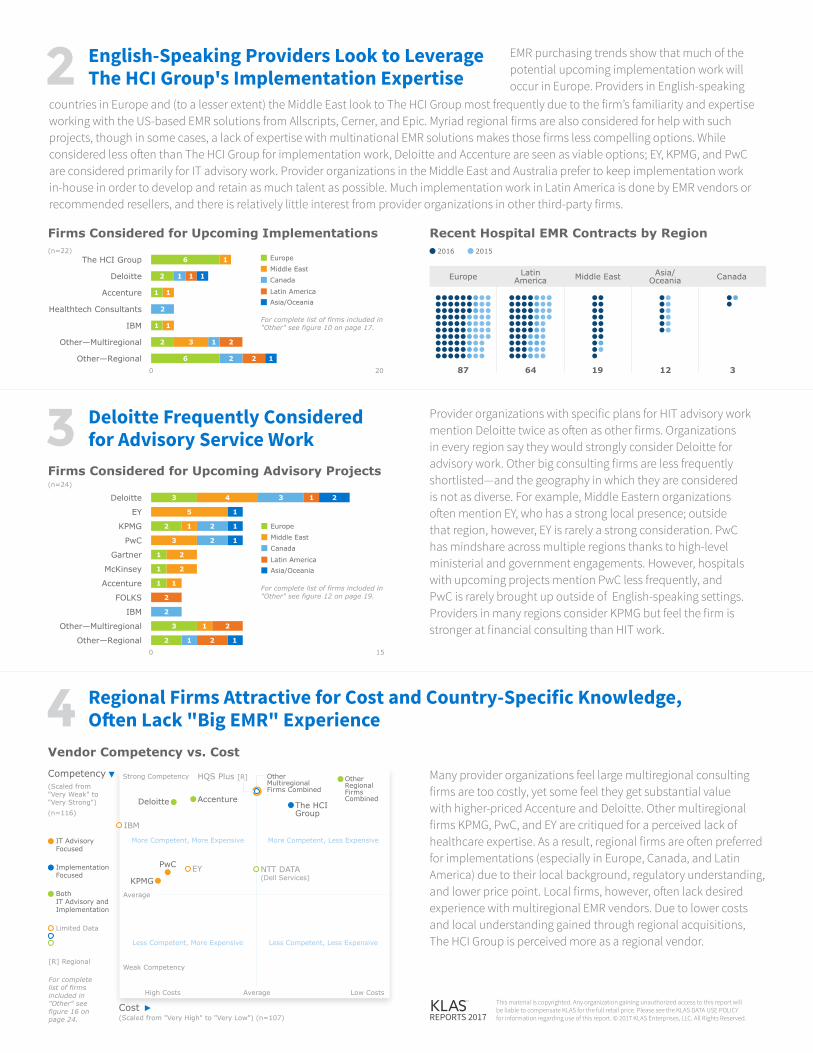

English-Speaking Providers Look to Leverage The HCI Group's Implementation Expertise

Deloitte Frequently Considered for Advisory Service Work

Regional Firms Attractive for Cost and Country-Specific Knowledge, Often Lack "Big EMR" Experience

EMR purchasing trends show that much of the potential upcoming implementation work will occur in Europe. Providers in English-speaking

Provider organizations with specific plans for HIT advisory work mention Deloitte twice as often as other firms. Organizations in every region say they would strongly consider Deloitte for advisory work. Other big consulting firms are less frequently shortlisted—and the geography in which they are considered is not as diverse. For example, Middle Eastern organizations often mention EY, who has a strong local presence; outside that region, however, EY is rarely a strong consideration. PwC has mindshare across multiple regions thanks to high-level ministerial and government engagements. However, hospitals with upcoming projects mention PwC less frequently, and PwC is rarely brought up outside of English-speaking settings. Providers in many regions consider KPMG but feel the firm is stronger at financial consulting than HIT work.

Many provider organizations feel large multiregional consulting firms are too costly, yet some feel they get substantial value with higher-priced Accenture and Deloitte. Other multiregional firms KPMG, PwC, and EY are critiqued for a perceived lack of healthcare expertise. As a result, regional firms are often preferred for implementations (especially in Europe, Canada, and Latin America) due to their local background, regulatory understanding, and lower price point. Local firms, however, often lack desired experience with multiregional EMR vendors. Due to lower costs and local understanding gained through regional acquisitions, The HCI Group is perceived more as a regional vendor.

2

3

4

This material is copyrighted. Any organization gaining unauthorized access to this report will be liable to compensate KLAS for the full retail price. Please see the KLAS DATA USE POLICY for information regarding use of this report. © 2017 KLAS Enterprises, LLC. All Rights Reserved.REPORTS 2017

Firms Considered for Upcoming Advisory Projects

Vendor Competency vs. CostCompetency(Scaled from "Very Weak" to "Very Strong")(n=116)

Cost(Scaled from "Very High" to "Very Low") (n=107)

Strong Competency

More Competent, More Expensive

Less Competent, More Expensive

More Competent, Less Expensive

Less Competent, Less Expensive

IT Advisory Focused

Implementation Focused

Limited Data

Regional[R]

Both IT Advisory and Implementation

Low Costs

Weak Competency

High Costs Average

Average

The HCI Group

AccentureDeloitte

PwC

KPMGEY

HQS Plus [R]

IBM

NTT DATA (Dell Services)

0

(n=24)

15

Firms Considered for Upcoming Implementations Recent Hospital EMR Contracts by Region

The HCI Group

IBM

Other—Multiregional

Other—Regional

Accenture

Deloitte

Healthtech Consultants

0

(n=22) 2016 2015

For complete list of firms included in "Other" see figure 10 on page 17.

EuropeMiddle EastCanada

Latin AmericaAsia/Oceania

20

6

6

3 1 2

2 2 1

1

111

1

1

2

1

1

2

2

EY 5 1

Accenture 1 1

PwC 3 12

Gartner 1 2

McKinsey 1 2

FOLKS 2

IBM 2

KPMG 11 22

Other—Multiregional 1 23

Other—Regional 1 2 12

Deloitte 3 4 3 1 2

countries in Europe and (to a lesser extent) the Middle East look to The HCI Group most frequently due to the firm’s familiarity and expertise working with the US-based EMR solutions from Allscripts, Cerner, and Epic. Myriad regional firms are also considered for help with such projects, though in some cases, a lack of expertise with multinational EMR solutions makes those firms less compelling options. While considered less often than The HCI Group for implementation work, Deloitte and Accenture are seen as viable options; EY, KPMG, and PwC are considered primarily for IT advisory work. Provider organizations in the Middle East and Australia prefer to keep implementation work in-house in order to develop and retain as much talent as possible. Much implementation work in Latin America is done by EMR vendors or recommended resellers, and there is relatively little interest from provider organizations in other third-party firms.

Europe

87 64 19 12 3

Middle East CanadaLatin America

Asia/Oceania

Other Multiregional Firms Combined

Other Regional Firms Combined

EuropeMiddle EastCanada

Latin AmericaAsia/Oceania

For complete list of firms included in "Other" see figure 12 on page 19.

For complete list of firms included in "Other" see figure 16 on page 24.

630 E. Technology Ave. Orem, UT 84097Ph: (800) 920-4109 | Fax: (801) 377-6345

www.KLASresearch.com

AuthorJeremy [email protected]

CoauthorJon Christensen

AnalystMichael [email protected]

DesignerNatalie Jamison

Project ManagerJenna Zidel

REPORT INFORMATIONREADER RESPONSIBILITY:KLAS’ website and reports are a compilation of research gathered from websites, healthcare industry reports, interviews with healthcare provider executives and managers, and interviews with vendor and consultant organizations. Data gathered from these sources includes strong opinions (which should not be interpreted as actual facts) reflecting the emotion of exceptional success and, at times, failure. The information is intended solely as a catalyst for a more meaningful and effective investigation on your organization’s part and is not intended, nor should it be used, to replace your organization’s due diligence.

KLAS data and reports represent the combined opinions of actual people from provider organizations comparing how their vendors, products, and/or services performed when measured against participants’ objectives and expectations. KLAS findings are a unique compilation of candid opinions and are real measurements representing those individuals interviewed. The findings presented are not meant to be conclusive data for an entire client base. Significant variables including organization/hospital type (rural, teaching, specialty, etc.), organization size, depth/breadth of software use, software version, role in the organization, provider objectives, and system infrastructure/network impact participants’ opinions and preclude an exact apples-to-apples vendor/product comparison or a finely tuned statistical analysis.

We encourage our clients, friends, and partners using KLAS research data to take into account these variables as they include KLAS data with their own due diligence. For frequently asked questions about KLAS methodology, please refer to the KLAS FAQs.

COPYRIGHT INFRINGEMENT WARNING:This report and its contents are copyright-protected works and are intended solely for your organization. Any other organization, consultant, investment company, or vendor enabling or obtaining unauthorized access to this report will be liable for all damages associated with copyright infringement, which may include the full price of the report and/or attorney’s fees. For information regarding your specific obligations, please refer to the KLAS Data Use Policy.

ABOUT KLAS:For more information about KLAS, please visit our website.

OUR MISSION:KLAS’ mission is to improve the delivery of healthcare technology by independently measuring and reporting on vendor performance.

NOTE: Performance scores may change significantly when including newly interviewed provider organizations, especially when added to a smaller sample size like in emerging markets with a small number of live clients. The findings presented are not meant to be conclusive data for an entire client base.

5