global fashion & luxury market private equity and investors survey

TRANSCRIPT

Global Fashion & Luxury marketPrivate Equity and investors survey 2016

Contents

Executive Summary 3

Key market trends 7

M&A Deal Monitor 2015 15

Private Equity and investors survey 2016 22

About Deloitte and its Fashion & Luxury practice 34

Private Equity and investors survey 2016 3

Executive summary

goods. The factors that negatively impact on the

sector performance are the drop in Leather Goods

sales, the increasingly strong competitive pressure

of Premium Fashion Brands and a slowdown in the

expansion of the Retail channel.

• Luxury jewelry is the best performing sector in the

Fashion & Luxury industry as a result of a growing

interest of high-worth consumers and thanks to

the positive performance achieved in the Branded

Jewelry segment, which offset the drop in sales

recorded in the Watches segment.

• The Cosmetics & Fragrances sector is growing,

mainly thanks to the development of cosmetics in

the Make-up category, especially for the High-End

segment. The Fragrances sector is characterized by

a positive trend driven by increasing prices.

• The Automotive industry is showing signs of

recovery; this phenomenon is particularly evident

in North America and Western Europe and is

linked to the expansion of the High-End segment

which takes away significant market shares from

the Premium segment. The recent economic

and financial turbulence has slowed down the

development of the Asian and Russian markets.

• The demand for Luxury accommodation is growing

in Europe, especially in large cities.

• Performance is stable in the Furniture sector, as

it is driven by the European market performance.

Growth opportunities have been identified in the

Asia-Pacific area and in the Middle-East, where

global players are scarcely present.

• The Private long-range Jets segment is expanding.

The North American market is recording the best

results in this segment.

• The demand for new Yachts is showing a slight

increase; the segment of custom-built yachts is

growing and the American market is showing signs

of recovery. The high-performance yacht segment

is still suffering; yacht demand shows a limited

penetration, especially in emerging markets.

• A positive performance is expected for Luxury

Cruise sector, driven by an increase in production

capacity in 2016.

Global Fashion & Luxury market: Private Equity and Investors Outlook 2016

• The “Global Fashion & Luxury Market: Private

Equity and Investors Outlook 2016” survey

conducted by Deloitte Financial Advisory analyzes

the main trends that, according to the interviewed

investors, are expected to characterize the

performance of this industry in 2016.

• In general, prospects are very good for players in

the Fashion & Luxury market; as a matter of fact,

also merger & acquisition deals show signs of

recovery in all areas of the luxury goods industry

that have been considered.

Global Fashion & Luxury market: Key market trends

• In 2015, sales in the Luxury market reached US$

~1.2 trillion, growing by 14.8% (+5% at constant

rates) over the last year mainly thanks to the Hotels

and Cars sectors.

• The Personal Luxury Goods sector, which accounts

for 28.2% of the total market, has grown by

12.9% (2.0% at constant rates).

• The average turnover of Fashion and Luxury

companies is US$ 3.6 billion, excluding the Car

sector (avg. US$ ~33 billion).

• Players in the Personal Luxury Goods sector record

average sales of around US$ 5 billion per year.

• The Personal Luxury Goods sector is the best

performing area of the Fashion & Luxury industry:

its average margins account for 22.5% of sales

compared to an average performance of 17.3%

in Fashion & Luxury. The worst-faring companies

are those operating in the Yachts sector as their

margins are far below the general average (~2.5%).

• In 2016, the four main trends that characterize

this sector and are impacting on the evolution

of the reference industry are as follows: digital

revolution, craftsmanship, contemporary fashion,

and consolidation of the new fashion capitals.

• The positive performance of the Apparel &

Accessories sector is driven by Shoes segment as

well as by the stable growth of Ready-to-Wear

4

Fashion & Luxury M&A deals in 2015

• In 2015, around 141 M&A deals focused on the

larger Fashion & Luxury industry were carried out,

of which 48% (67 deals) were finalized in the

Personal Luxury goods sector.

• The sectors that recorded the highest number

of deals are: Hotels (51), Apparel & Accessories

(33), Cosmetics & Fragrances (19) and Watches &

Jewelry (15). The remaining 23 transactions took

place in the Yachts & Private Jets and Furniture

sectors.

• In 2015, 47% of the finalized deals had an average

value below US$ 100 million, whereas it exceeded

US$ 500 million in 18% of cases. The average value

per transaction was US$ 426 million.

• The largest transactions – value above US$ 500

million – were finalized in the Private Jets, Hotels

and Cosmetics & Fragrances sectors. The average

value per transaction in the Personal Luxury Goods

sector was US$ 278 million.

• 81 deals (57%) were finalized in Europe, mainly in

the Apparel & Accessories (27 deals) and Hotels (24

deals) sectors. 35 transactions (25%) were carried

out in North America, of which 15 in the Hotels

sector. 13 transactions (9%) were finalized in the

Asia Pacific region, of which 6 in the Hotels sector

and 5 in the Watches & Jewelry sector.

• In 2015, around 70% of the acquired companies

recorded sales below US$ 100 million, whereas

10% recorded sales above US$ 500 million.

• The average sales of the companies acquired in

2015 amounted to US$ 425 million. The largest

players operated in the Apparel & Accessories (avg

US$ 663 million) and Hotels (avg US$ 572 million)

sectors, whereas the target companies operating in

the Furniture and Yachts sectors were smaller (avg

US$ 67 million and US$ 34 million, respectively).

• In 2015, 50% of the deals were executed by

Financial Investors, who are generally more inclined

to invest in the Personal Luxury Goods sector;

the remaining half of deals were carried out by

strategic investors operating in the Apparel &

Accessories, Fragrance & Cosmetics, Hotels and

Yachts sectors and more interested in consolidating

their position in their respective sectors.

• In 2015, 66% of exits were carried out by Strategic

Sellers who sold their business to investment funds;

Financial Sellers finalized 64% of transactions with

strategic investors.

• The main strategies adopted by Financial Bidders

were Growth Capital (49%) and Buyout (64%)

strategies, whereas Business Consolidation

strategies (used in 6.6% of all transactions) were

adopted almost exclusively by Strategic Investors.

• Overall, 77% of all finalized transactions resulted

in the acquisition of a majority stake in the target

company.

• 35% of the finalized deals achieved a 15x EBITDA

multiple, mostly in the Hotels sector (driven also by

the presence of property assets), whereas 20% of

the deals achieved a 5-10x EBITDA multiple.

Private Equity and investors survey 2016 5

Fashion & Luxury Private Equity and Investors Outlook 2016

• Around 60% of investors maintain they own assets

in the Fashion & Luxury industry characterized by

a majority stake and an average duration generally

below 5 years.

• In 2015, the main strategies developed to support

the creation of economic value from owned

Fashion & Luxury assets were as follows:

– development of new distribution channels - 60%;

– penetration of new geographical markets - 51%;

– improvement of operational performance through

actions to increase efficiency - 37%;

– development of new products - 29%.

• 44% of investors foresee at least one exit from

their F&L portfolio in 2016, mainly driven by

the opportunity to achieve high returns on the

investment made.

• 53% of all respondents forecast an increase of over

5% (of which 15% with double-digit growth) in

the Fashion & Luxury market in 2016, driven by the

positive trends predicted in the following sectors:

Cosmetics & Fragrances (on the increase according

to 69% of investors), Furniture (60% of investors),

Apparel & Accessories (59%), Cars (54%):

– the sectors which attract the highest percentage

of negative forecasts – although they are fewer

than positive forecasts – are as follows: Yachts

(25% predicting a decrease vs 30% predicting

an increase), Private Jets (22% - decrease vs 39%

- increase), Cruises (21% - decrease vs 41% -

increase) and Selective Retailing (21% - decrease

vs 69% - increase);

– investors with assets in the F&L industry have

better expectations, compared to potential

investors who do not own F&L assets, as regards

the Cosmetic & Fragrances and the Apparel &

Accessories sectors.

• The geographies where investors expect growth in

2016 are the Asia-Pacific region (excluding Japan),

the Middle East and North America, whereas

Europe should remain stable. Investors forecast a

negative trend for Latin America and Japan.

• In 2016, 76% of respondents plan to make at least

one investment in the Fashion & Luxury industry,

more specifically in the following sectors: Apparel &

Accessories (75%), Cosmetics & Fragrances (48%),

Furniture (39%).

• Investors interested in F&L maintain:

– in 72% of cases, that they intend to acquire

target companies with a turnover below US$ 100

million; 10% of investors plan on investing in

companies with sales above US$ 500 million;

– that they intend to carry out new transactions in

this industry through Expansion Capital strategies

(63%), Leverage buy-out strategies (61%)

and Management buy-out strategies (54%),

mainly acquiring a majority stake in the target

organization;

– that they intend to fund the investment using

mainly senior debt (80%).

• The average return expected from investments in

the Fashion & Luxury industry is very high; 70%

of respondents expect investments to have an

IRR exceeding 20%. The Personal Luxury Goods

sectors are considered as the most profitable

ones by investors, as confirmed by the business

performance of the companies analyzed.

• The highest returns are expected from large-sized

organizations; as a matter of fact, around 35%

of investors expecting an IRR above 20% plan on

acquiring companies with sales above US$ 100

million.

6

Methodological approach

Sectors covered

Apparel & Accessories | Watches & Jewelry | Cosmetics & Fragrances | Cars | Hotels | Furniture | Private Jets | Yachts | Cruises

Market segments

The survey focuses on the «Premium» segments in the sector, defined on the basis of quantitative (e.g. price point) and qualitative (e.g. interviews with industry experts) parameters.

Key market trends M&A deal monitor PE & investors survey

Main contents

Size of global market in 2015Size of M&A deals in 2015 classi-

fied by sector

Analysis of the current portfolio of

assets operating in the reference

market

Analysis of market trends by sector Analysis of target company profiles

Analysis of the main guidelines

implemented with reference to

the existing portfolio to create

economic value

State of the market in 1Q 2016 Analysis of investor profiles Analysis of the exit strategies fore-

casted for 2016

2016 market outlookAnalysis of the characteristics of

deals carried out at global level

Outlook and investment strategies

for 2016

Analysis of the business perfor-

mance of the major market players

classified by sector

Sources

Altagamma Foundation Merger Market

Online survey based on CAWI

(Computer Assisted Web Inter-

viewing)

Annual financial report and pre-

sentation of major players Thomson M&A

Interviews with executives operat-

ing in the PE sector

Interviews with opinion leaders in

the industryOne Source

Mint Global

Company press releases

Geographical footprint

Primary data level

Global scope

Private Equity and investors survey 2016 7

Key market trends

Global Luxury Market in 2015

In 2015, sales in the Luxury market reached US$ ~1.2 trillion, growing by 14.8% (+5% at constant rates) over

the last year mainly thanks to the Hotels and Cars sectors.

Key Fashion Business Trends in 2016

Four key trends are influencing the Fashion industry and consequently the strategic and operational choices of

organizations.

6.7%

Yachts

Watches & Jewelry

Furniture

Cosmetics & Fragrances

Apparel & Accessories

4.5%

1.3%

4.6%

6.0%

Cruises 7.2%

11.5%

Private Jets

Cars

9.5%

Total luxury market

10.6%

Hotels

9.1%

+7.0%

+8.0%

-1.0%

+4.0%

+2.6%

+1.0%

+4.0%

-3.0%

+5.0%

+17.3%

+15.4%

+16.7%

+14.3%

+14.7%

+13.6%

+10.3%

+8.0%

+14.8%

-1.0% +2.0%

1,188

5.6%

6.2%

2015

3.6%

16.4%

19.6%

45.2%

Cruises

Private Jets

Furniture

Yachts

Apparel & Accessories

Watches & Jewelry

Cosmetics & Fragrances

Hotels

Cars

0.2%0.8% 2,3%

Global Luxury Market 2015 (B$; %)

Luxury market trend (CAGR 12-15; %)

YoY 14-15

YoY @k 14-15

The booming of digital is modifying companies’ distribution channels for the

front-end market and business models for product development and supply

chain.

The research of quality and exclusivity from end users encourages fashion

luxury corporations to invest in craftsmanship, influencing production and

design competencies and skills.

The upsurge of “Contemporary Fashion” segment, represented by emerging

designers launching their own start-ups.

The global growth of mature and emergent fashion capitals, driven by the

economic growth of emerging markets, offering the possibility of geographical

expansion to key players in the industry.

Digital Revolution

Craftsmanship

Contemporary fashion

Fashion capitals

Key business trends Highlights

Source: Data from Altagamma Worldwide Luxury Market Monitor.

8

Global Luxury Market Outlook

Apparel & Accessories

Key attractions: This sector benefits from the positive

trend of the «shoes» category, particularly in the US

and China, which is driven by increasing consumer

demand in the high-end market segment.

Stable growth in the Ready-to-Wear sector, driven

by the by now consolidated performance of the

Womenswear segment.

«Lifestyle» and «Iconic» brands are growing strongly

and achieving positive results in all goods categories

The off-price channel continues on its development

path; it is used by industry players as a strategic tool

to differentiate their offering based on different

demand segments.

Key concerns: Leather Goods are losing market

shares because of greater consumer loyalty volatility

in the aspirational goods segment, which results

from the sharp price increases recorded over the last

few years. Increase in competitive pressure among

Premium Fashion Brands in the High-End segment.

Expansion slowdown in the Retail sector. In many

cases, players limit themselves to the acquisition

of distribution networks managed through joint

ventures in Asian markets.

Cosmetics & Fragrances

Key attractions: The ongoing development of the

Make-up category drives growth in the Cosmetics

sector, thus offsetting the poor performance

of Skincare products. The positive trend in the

Fragrances segment is supported by the good

performance of the high-end segment; especially

handcrafted products are on the increase.

What stands out is the expansion of Asian players

- that take market shares away from large groups

in the local markets - coupled with increasing

demand, therefore attracting potential private capital

investment.

Key concerns: Despite the significant role of

promotional initiatives, the main growth driver in the

Fragrances segment is represented by price increases

in mature markets, which are somewhat resistant to

product innovation.

Cars

Key attractions: Luxury Cars continue on their

growth path, driven by progressive recovery in the

automotive industry. The performance of the U.S.

market and recovery in Western Europe stand out as

particularly positive.

The high-end segment (2.2% of all automotive

sales) is strongly expanding, driven by an extension

of the range of products and services offered: new

entry-level models (bridge categories) launched to

take away market shares from premium players and

greater customer service differentiation in order to

maximize operating margins.

Key concerns: The Asian market is under scrutiny

because of its unsatisfactory results, which are

a direct consequence of economic and financial

turbulence. The Russian market has still not been

recovered.

+3.5%Outlook 2016

+8.0%Outlook 2016

+4.0%Outlook 2016

Source: Data from Altagamma Worldwide Luxury Market Monitor.

Private Equity and investors survey 2016 9

Hotels

Key attractions: The European market is driving

the sector’s performance, which is characterized

by a significant increase in the demand for luxury

accommodation in large cities.

Service differentiation according to different cultural

and generational needs may represent a potential

lever for business expansion in the future.

Key concerns: Declining performance in the United

States and the Asian market, which is struggling to

find a path towards sustainable development.

Competitive pressure is increasing in the sector as a

result of the entry of new players and the emergence

and consolidation of new online accommodation

platforms, which are becoming more and more

widespread in the high-end segment.

Private Jets

Key attractions: The long-range Jets segment (54%

of the total market) is growing and drives the

performance of the entire sector.

North America is the main market showing signs of

strong expansion.

Key concerns: The performance of the small- and

medium-sized Jets segment is stable.

Competitive pressure is increasing in strongly

developing markets, especially in Emerging Countries.

Cruises

Key attractions: The increase in production capacity

expected to take place in 2016, as a result of

the delivery of new cruise ships, will be a key

development driver for this sector.

In particular, the «slow cruises» - i.e. cruises on

smaller ships offering alternative routes to larger

ships - segment looks promising.

The expectations as to demographic and income

trends support the growth expected in this sector.

Key concerns: Potential market risk associated with

a failure to saturate the new capacity expected for

2016.

Furniture

Key attractions: This sector has a not yet fully

exploited growth potential in the Asia-Pacific and

Middle-East market.

The Living & Bedroom and Lighting categories are

showing an interesting performance, whereas the

Kitchens segment is recovering.

Key concerns: The performance of the entire sector is

influenced by the by now stable trend in Europe, i.e.

the major market worldwide

Concentration in the European market is a potential

risk factor for private capital investments.

+2.5%Outlook 2016

+5.0%Outlook 2016

+5.0%Outlook 2016

+6.0%Outlook 2016

Source: Data from Altagamma Worldwide Luxury Market Monitor.

10

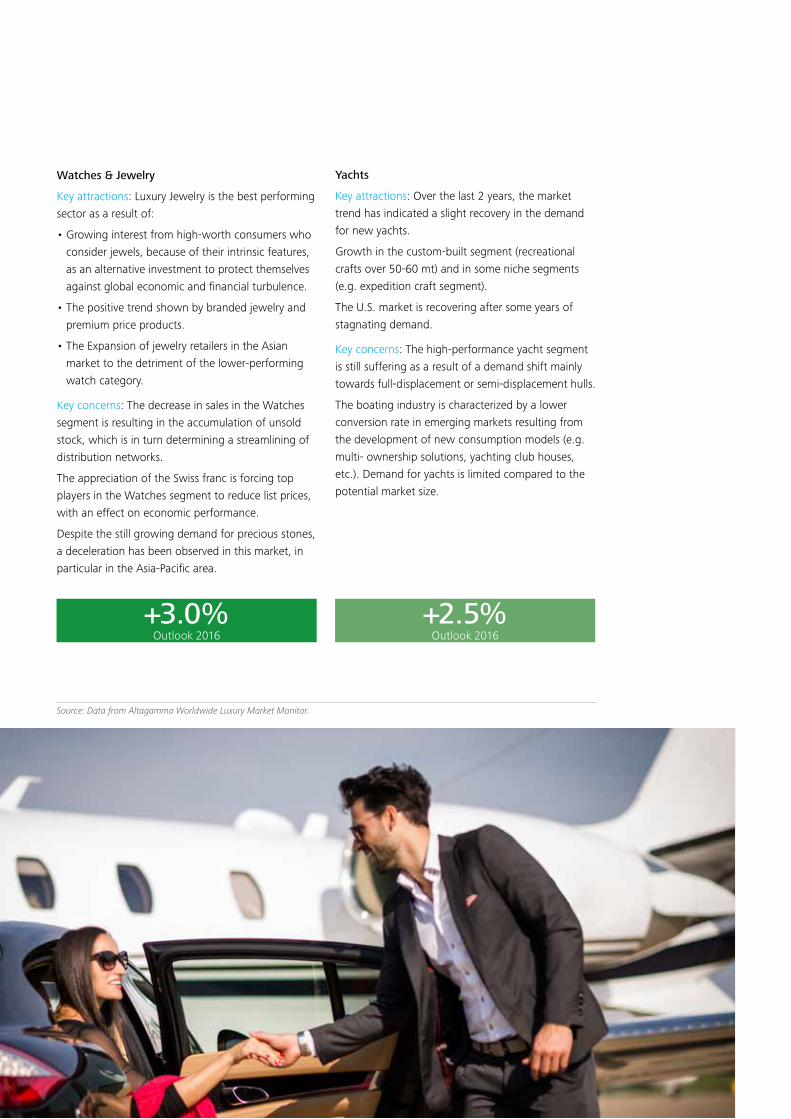

Watches & Jewelry

Key attractions: Luxury Jewelry is the best performing

sector as a result of:

• Growing interest from high-worth consumers who

consider jewels, because of their intrinsic features,

as an alternative investment to protect themselves

against global economic and financial turbulence.

• The positive trend shown by branded jewelry and

premium price products.

• The Expansion of jewelry retailers in the Asian

market to the detriment of the lower-performing

watch category.

Key concerns: The decrease in sales in the Watches

segment is resulting in the accumulation of unsold

stock, which is in turn determining a streamlining of

distribution networks.

The appreciation of the Swiss franc is forcing top

players in the Watches segment to reduce list prices,

with an effect on economic performance.

Despite the still growing demand for precious stones,

a deceleration has been observed in this market, in

particular in the Asia-Pacific area.

Yachts

Key attractions: Over the last 2 years, the market

trend has indicated a slight recovery in the demand

for new yachts.

Growth in the custom-built segment (recreational

crafts over 50-60 mt) and in some niche segments

(e.g. expedition craft segment).

The U.S. market is recovering after some years of

stagnating demand.

Key concerns: The high-performance yacht segment

is still suffering as a result of a demand shift mainly

towards full-displacement or semi-displacement hulls.

The boating industry is characterized by a lower

conversion rate in emerging markets resulting from

the development of new consumption models (e.g.

multi- ownership solutions, yachting club houses,

etc.). Demand for yachts is limited compared to the

potential market size.

+3.0%Outlook 2016

+2.5%Outlook 2016

Source: Data from Altagamma Worldwide Luxury Market Monitor.

Private Equity and investors survey 2016 11

Business Performance Analysis: Scope of Top Players

The analysis of business performance in the Fashion & Luxury industry was conducted on a panel of 73

companies.

Business Performance Analysis: Revenues of Top Players

F&L top players accounted for around 55% of the total market; Cars and Personal Luxury Goods made up 90%

of the total revenues of F&L top players.

In order to analyze the business performance of the main players in the Fashion & Luxury industry, summary economic and financial data was collected from a panel of 73 companies.

The panel has been selected considering the size of total revenues of each player and its representativeness in the analyzed sectors (covered market share). The organizations are mostly based in Europe and North America, but they generally have a global business scope.

In 2014, the total revenues recorded by the industry top players equaled around US$ 553 billion, of which 60% was represented by Luxury Cars and 32% by Personal Luxury Goods.

An analysis of the market shares held by the selected top players has highlighted the high level of concentration characterizing Fashion & Luxury sectors, where some organizations hold over 50% of the global market share. The Furniture sector appears to be highly fragmented.

Note: Consolidated data on the main corporate groups operating in the reference market are reported, segmented by business area. The collected data refer only to brands with a ‘premium’ market positioning.Source: Data from Altagamma Worldwide Luxury Market Monitor and company financial reports.

Source: Data from Altagamma Worldwide Luxury Market Monitor and company financial reports.

60% 80% 100%

20%

40%

60%

40%

20% 0%

80%

0%

100%

Apparel & Accessories

20

Watches & Jewelry

10

20.0%

30.0% 20.0%

20.0%

50.0% 60.0%

20.0%

50,0%

Furniture

87.5%

7

16.7%

5

20.0%

10

90.0%

10.0% 12.5%

Hotels Cosmetics & Fragrances

6

Yachts

14.3%

66.7%

Cruises Cars

16.7%

85.7%

Private Jets

2

50.0%

8 5

60.0%

20.0%

80.0%

Europe

North America

Asia-Pacific 7%

Break (%) 27.4% 8.2% 6.8% 11.0% 6.8% 13.7% 9.6% 13.7% 2.7%

Break %

26%

67%

73 player

Panel of top players – breakdown by sector and geographical area (# ; %)

Total revenues of top players in 2014 – breakdown by sector (B$; %)

326.7

50.9

87.8

375.8 (68%)

Furniture

Personal Luxury Goods

3.4

Yachts Total

176.7 (32%)

33.5 552.5

Cruises

1.8

Private Jets

6.1

38.1

Apparel & Accessories

Cosmetics & Fragrances

Watches & Jewelry

Cars Hotels

4.2

Other Luxury markets

Break (%)

Top players Mkt Share (%)

15.9% 9.2% 6.9% 59.1% 6.1% 0.6% 1.1% 0.8% 0.3% 100.0%

51.5% 74.5% 65.3% 70.2% 16.9% 25.6% 44.4% 8.9% 96.8% 53.4%

503B$ - 91%

Key Findings

Key Findings

12

Business Performance Analysis: Average Sales per Top Player

Average sales reported by Fashion & Luxury companies equaled US$ 3.6 billion, excluding the Cars sector (avg.

US$ ~33billion). Personal Luxury Goods players reported an average yearly turnover of around US$ 5 billion.

Business Performance Analysis: Profit Pool of Top Players

Personal Luxury Goods were the most profitable industry sector, with margins averaging 22.5% of sales. The

situation in the Yachts sector proved more difficult as players reported margins way below the general average

(2.5%).

Fashion & Luxury top players reported a turnover of US$ 7.6 billion; the average figure was significantly influenced by the size of holdings in the Cars sector, where the average turnover was US$ 32.7 billion; if this sector is excluded, then the average drops to US$ 3,6 billion.

The companies operating in the Yachts, Furniture and Cruises sectors were generally small-sized (average sales around US$ 500 million). On average, companies in the Personal Luxury Goods sector had a turnover of around US$ 5 billion.

Profitability in Personal Luxury Goods companies was around 5 percentage points higher than the general Fashion & Luxury average. The best performing sectors were Apparel & Accessories (24.8%) and Watches & Jewelry (22.5%). Yacht shipyards reported margins that were clearly lower than those reached in the other sectors, with a 2.5% average operating profit.

Source: Data from company financial reports.

Source: Data from company financial reports.

Average sales of F&L top players in 2014 – breakdown by sector (B$)

Average operating profit of F&L top players in 2014 – breakdown by sector (%)

0.40.40.6

3.1

6.7

4.45.1

6.3

Hotels

32.7

Cars Cosmetics & Fragrances

Private Jets Watches & Jewelry

Yachts Apparel & Accessories

Avg. PLG 4.9B$

Avg. F&L 3.6B$ (cars excl.)

Avg. F&L 7.6B$

Furniture Cruises

Personal Luxury Goods (PLG)

Other Luxury markets

Avg. PLG 22.5%

Avg. F&L 17.3%

Apparel & Accessories

22.5%

8.9%

Cruises Yachts Furniture Cosmetics & Fragrances

13.9% 12.4%

Watches & Jewelry

Private Jets

15.3%

2.5%

8.8%

Hotels

24.8%

Cars

16.9%

Other Luxury markets

Personal Luxury Goods (PLG)

+5 pp

Key Findings

Key Findings

Private Equity and investors survey 2016 13

Attractiveness of Fashion & Luxury Sectors

Apparel & Accessories and Watches & Jewelry are the top performing Fashion & Luxury sectors, both in terms

of average turnover growth (+7.6%) and operating margins (24%). The Cars sector is recovering; strong

growth in the Private Jets sector.

Source: Data from company financial reports.

Mapping of Luxury sectors by business performance

30%

18

3

6

0

15

9

15 10 25 20 5 0

Hotels

Cars

Cosmetics & Fragrances

Apparel & Accessories

Watches & Jewelry

Cruises

Average operating profit FY14 (Percentage | avg. 17.3%)

Turn

over

gro

wth

201

2 -

14(C

AG

R %

| av

g. 7

.3%

)

Yachts

Private Jets

Furniture

Personal Luxury Goods

Other Luxury markets

Starsmarkets

High growth markets

Mature markets

Lower performer sectors

Market size

14

Private Equity and investors survey 2016 15

M&A Deal Monitor 2015

Overview by sector

Overview by geography

Relevant deals in 2015

Global

100%141 deals

Apparel & Accessories

23%33 deals

Watches & Jewelry

11%15 deals

Yachts

6%9 deals

Furniture

5%7 deals

Cosmetics & Fragrances

13%19 deals

Hotels

36%51 deals

Private jets

5%7 deals

North America

Cos&Fra

43% Hotels

100%

17%

29% Other

11%

2015

App&Acc 35 deals (25%)

Rest of the World

Hotels

2015

100%

75%

25% Yachts

4 deals (3%)

Europe

2015

100%

33%

25%

Hotels 30%

12% Cos&Fra

App&Acc

Other

81 deals (57%)

Middle East

50%

2015

100%

Private Jets 50%

Furniture 2 deals (1%)

Japan

Cos&Fra 17% Wat&Jew

33%

2015

100%

Hotels

App&Acc 33%

16%

6 deals (5%)

Asia-Pacific

Wat&Jew

100%

Cos&Fra

46% Hotels

2015

38%

15%

13 deals (9%)

Overview of global M&A deals in Fashion & Luxury - 2015

Date November July April June June December September December March January

TargetStarwood

hotelsP&G Coroin Ltd

Center Parcs

Douglas Holding

FRHI HotelsLandmark aviation

Pepe Jeans HypermarcasThe Net-A-Porter

Group Ltd

BidderMarriot Intern.

CotyConstellation

HotelsBrookfield partners

CVC AccorBBA

aviationM1 Group Coty YOOX SpA

Value (B$) ~12 ~12 ~4.7 ~3.7 ~3 ~3 ~2 ~1 ~1 ~0.8

Note: In the «Relevant deals in 2015» list are included both announced and closed deals.

16

Size of the Main M&A Deals

In 2015, the Fashion & Luxury industry recorded around 141 M&A deals globally, of which 48% focused on

Personal Luxury Goods and 36% on the Hotels sector.

Breakdown of Deals by Average Deal Value

In 2015, 47% of deals had an average unit value below US$ 100M. The deals with a unit value above US$

500M represented 18% of all transactions, of which 2/3 with a value exceeding US$ 1B.

Note: The analysis includes the main M&A deals finalized in the Fashion & Luxury industry during 2015, excluding IPOs; the analysis takes into consideration also transactions aimed at acquiring players in the Fashion & Luxury value chain as strategic suppliers and selective retailers;(1) The analysis does not include deals having the purchase of tangible assets (real estate) as sole purposeSource: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

Note: The average deal value has been calculated excluding the transactions for which no specific condition details are availableSource: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases,

33

1519

51

Other Luxury markets

Personal Luxury Goods

Apparel & Accessories

Yachts Hotels 1 Watches & Jewelry

Cosmetics & Fragrances

67 (48%)

74 (52%)

141

Furniture Total Fashion & Luxury

Private Jets

9 77

Break (%) 23.4% 10.6% 13.5% 36.2% 6.4% 5.0% 5.0% 100.0%

Number of deals in 2015 – breakdown by sector (# ; %)

Breakdown of deals by deal value (%)

During 2015, around 141 M&A transactions focused on the larger Fashion & Luxury sector were carried out globally; 48% of these deals (67 deals) involved Personal Luxury Goods companies.

Because of the uncertainty characterizing global markets, investors turned to companies with substantial property assets, i.e. Hotels (representing 36% of total transactions), in order to protect themselves against economic and currency fluctuations. Deals were distributed as follows among the remaining sectors: Yachts 6.4% (9 deals), Private Jets 5.0% (7 deals) and Furniture 5.0% (7 deals).

In 2015, around 47% of M&A transactions had an overall value below US$ 100M. 50% of these deals focused on target companies operating in Personal Luxury Goods sectors. The deals with a unit value above US$ 500 million accounted for 18% of all transactions. In 2015, top deals – i.e. deals with value exceeding US$ 1 billion – represented 11% of transactions and were concentrated in the Hotels sector (65% of deals). The high deal value in this sector results from the very features of the transaction, which focuses on the acquisition of the business AND the purchase of the property assets owned by the target company

100%

34%

Total Fashion & Luxury

> 1B$ 500M$ - 1B$ 100-500M$ < 100M$

47%

11%

7%

Key Findings

Key Findings

Private Equity and investors survey 2016 17

Average Value of Main Deals by Sector

In 2015, the average value per deal equaled US$ 426M; the deals with a value above average were finalized in

the Private Jets (US$ 2B), Hotels (US$ 573M) and Cosmetics & Fragrances (US$ 498M) sectors.

Geographical Distribution of Deals

In 2015, 57% of deals (81) were finalized in Europe, 25% (35) in North America and 9.2% (13) in the Asia-

Pacific region.

Note: The average deal value has been calculated excluding the transactions for which no specific condition details are available; the analysis excludes some deals which represented outliers, as they would not allow a reliable analysis of sector averages.(1) The value reported for the Private Jets sector refers to a single transaction, for which economic and financial details are available.Source: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

Average value per deal in 2015 – breakdown by sector (M$)

Deals finalized in 2015 – breakdown by sector and geographical area (# ; %)

In 2015, the most sizable acquisition deals were finalized in the Private Jets and Hotels sectors, with an average value per deal greater than US$ 500 million.

The average deal value in the Apparel & Accessories sector equaled US$ 297 million - i.e. 0.7 times the average value of the whole Fashion & Luxury industry; this was mainly a consequence of the strong focus of investors on small-sized (low-turnover), fast-growing target companies. The same applies to the Watches & Jewelry sector.

18

100

573

182

297

498

Avg. PLG 278M$

Avg . F&L 426M$

Yachts Cosmetics & Fragrances

Hotels

2,065

Watches & Jewelry

Furniture Apparel & Accessories

Private Jets 1

Personal Luxury Goods (PLG)

Other Luxury markets

Source: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

Europe North

America

15

644

35 3 3

Deal per settore

Hotels

App & Acc Wat & Jew

Cos & Fra

27

24

10

Deal per settore

81

5

3 5

7

Asia-Pacific

6

5

213

Deal per settore

Hotels

Wat & Jew

Cos & Fra

24.8% 57.4% 9.2%

Middle East

Rest of the World

3

1

Hotels

4

Deal per settore

Yachts

1

1

Furniture

Deal per settore

2

Private Jets

Japan

2

2

1

1

Hotels

Cos & Fra

Wat & Jew

6

Deal per settore

App & Acc

2.8% 1.4% 4.3%

Hotels Furniture Yachts Private Jets

Apparel & Accessories Cosmetics & Fragrances Watches & Jewelry

App & Acc

Hotels

Cos & Fra Wat & Jew

Key Findings

18

Average Size of Target Companies

In 2015, around 70% of the acquired companies reported sales below US$ 100 million and 10% exceeded

US$ 500M.

In 2015, the average turnover reported by the acquired companies equaled US$ 425M; most deals involving

big companies were executed in the Apparel & Accessories and Hotels sectors.

Note: The analysis is based on a sample of target companies for which official turnover figures as at the end of FY 2014 were available.Source: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

Note: The analysis is based on a sample of target companies for which official turnover figures as at the end of FY 2014 were available.Source: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

Distribution of target companies across revenue classes (%)

Average turnover of the acquired companies by sector (M$)

In 2015, investments in the Fashion & Luxury industry were focused mainly on smaller-sized organizations: around 67% of the target companies had a turnover below US$ 100 million

Only 10% of the total number of deals involved organizations with sales exceeding US$ 500 million. The main ‘giant deals’ were as follows:

• Acquisition of Starwood Hotels by Marriot International (deal value ~12-13B$).

• Agreement between Procter&Gamble and Coty concerning the transfer of 43 haircare brands to the multinational Perfumes company (deal value ~12.5B$).

• Acquisition of the Douglas perfumery chain by the CVC Capital Partners private equity fund (deal value ~3B US$).

The average turnover reported by the companies acquired in 2015 equaled around US$ 425M, or US$ 453M if only Personal Luxury Goods companies are considered.

Large-sized target companies were concentrated in the Apparel & Accessories (avg. US$ 663M) and Hotels (avg. US$ 572M) sectors.

6.0%

9.6%

14.5%

101-250M$

32.5%

16.9%

501-1,000M$

4.8%

15.7%

51-100M$ 251-500M$ 25-50M$ <25M$ >1,000M$ Total Fashion & Luxury

100.0% 67% under 100 M$

10% over 500 M$

3467

276

572

214227

663

Furniture Watches & Jewelry

Apparel & Accessories

Cosmetics & Fragrances

Private Jets Hotels

Avg. F&L 425M$

Yachts

Avg. PLG 453M$

Other Luxury markets

Personal Luxury Goods (PLG)

Key Findings

Key Findings

Private Equity and investors survey 2016 19

Bidder Profile

In 2015, 50% of deals were executed by Financial Investors, of which around 90% were Private Equity

investors; the remaining half of deals were carried out by Corporate investors operating in the Fashion & Luxury

industry...

...in particular, an analysis of investment strategies shows that PE investors were mostly interested in Personal

Luxury Goods companies, whereas large corporations tended to invest in their own sector.

Note: A deal with undisclosed Bidder name has been excluded from this analysis.Source: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

Note: The propensity index has been calculated by comparing the exit strategy mix in each sector with the general average observed in the analyzed sample, weighted according to deal concentration in that sector in 2015.Source: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

Investor profile in PE exits (%)

Type of exit broken down by target company sector (propensity idx)

Investor profile in Strategic exits (%)

The analysis of acquisition strategies confirms that Private Equity funds – despite an increased focus on experiential luxury sectors (e.g. Hotels) – still show a propensity to invest in Personal Luxury Goods companies. The most significant deals included: The acquisition of Pepe Jeans, - the Spanish premium jeans brand - by M1 Group and L Capital Asia; The acquisition of Twin-Set – an Italian player in the premium App&Acc sector - by The Carlyle Group.

The remaining Fashion & Luxury sectors mainly attracted Strategic Investors adopting consolidation and/or business growth strategies.

In 2015, the main bidders in 50% of the executed deals were Financial Investors, represented by Private Equity funds in ~90% of cases. 50% of transactions were carried out by Strategic Investors, of which 25.7% were large corporate investors operating in the Apparel & Accessories sector, 10.0% were investors operating in the Fragrance & Cosmetics business, and 20.0% specialized in the Hotels sector. 8.6% of deals were executed by investors operating in sectors external to the Fashion & Luxury industry.

85.7%

10.0%

50.0%

50.0%

Financial investor

Bidder type

Venture Capital/ Private Equity

Other investors

Bidder sector

Real Estate

4.3%

Strategic investor

100.0% 100.0%

25.7%

10.0%

20.0%

10.0%

25.7%

8.6%

50.0%

50.0%

100.0%

Strategic investor

Bidder type

Apparel & Accessories

Bidder sector

Fragrances & Cosmetics

100.0%

Hotels

Other F&L sectors

Other industries

Financial investor

Yachts

Strategic investor Propensity (Idx 100)

Financial investor propensity (Idx 100)

Cruises

Furniture

Yachts

Private Jets

Hotels

Watches & Jewelry

Apparel & Accessories

Fragrances & Cosmetics

Key Findings

Key Findings

20

Exits by Seller Type

In 2015, 66% of exits were executed by Strategic Sellers selling their business to investment funds; Financial

Sellers executed 64% of transactions with strategic investors.

Main Investment Strategies of Bidders

Most finalized deals were based either on a «Growth Capital» or a «Buyout» strategy as underlying logic and

were mainly aimed at the acquisition of a majority stake.

Note: A deal with undisclosed Bidder name has been excluded from this analysis.Source: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

Note: This analysis is based on a sample of 91 target companies for which information about the equity stake in the target company acquired through the transaction was available.Source: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

M&A market by investor type (%)

Deal breakdown by investment strategy (%) Deal breakdown by sector and equity stake (%)

In 2015, 66% of exit transactions were executed by Strategic Sellers; in 57% of these deals, the counterparty was a Financial Investor (Strategic to Sponsor), whereas in 43% of deals the counterparty was a Strategic Investor (Strategic to Strategic). Financial Sellers executed most deals with strategic investors; 30 Sponsor-to-Strategic transactions were finalized (representing 64% of Financial Sellers).

In 2015, 64.2% of deals were based on a «growth capital» strategy, followed by 20.4% based on a «buyout» logic, of which 64% were executed by Private Equity funds. «Business consolidation» strategies accounted only for 6.6% of all deals mainly executed by Strategic Investors (around 90%). 80% of turnaround and recapitalization deals were executed by Private Equity funds.

Overall, 77% of the finalized deals were aimed at the acquisition of a majority stake in the target company; deals aimed exclusively at the acquisition of a majority stake were executed in some sectors, such as Furniture, Private Jets and Yachts.

It should be noted that 56% of the deals finalized in the Watches & Jewelry sector resulted in the acquisition of a minority stake.

Strategic Investor 66 deals

Sponsor to Sponsor 17 deals (36%)

Financial Investor 71 deals

50%

50%

Strategic to Strategic 40 deals (43%)

Sponsor to Strategic

Strategic to

Sponsor

53 deals (57%)

30 deals (64%)

Financial Seller 45 deals

Strategic Seller 92 deals

Seller Buyer

34%

66%

Weight on total deals per seller type

6.6%

3.6% 1.5% 3.6%

20.4%

64.2%

Merger

Recapitalisation

Turnaround

Consolidation

Buyout

Growth capital

% Financial investor

49%

64%

11%

80%

80%

0%

63%44%

89% 81%100% 100% 100%

77%

37%56%

11% 19% 23%

100%

Cosmetics& Fragrances

100%

Watches& Jewelry

100%

Apparel& Accessories

100%

Total Fashion& Luxury

Yachts

100%

PrivateJets

100%

Furniture

100%

Hotels

100%

Minority

Majority

Key Findings

Key Findings

Private Equity and investors survey 2016 21

Analysis of EBITDA Multiples Achieved on the Main Deals

An analysis of the EBITDA multiples achieved in this industry confirms the premium value assigned by investors

to Fashion & Luxury companies; an EBITDA multiple greater than 15x was achieved on 36% of transactions.

Note: This analysis is based on a sample of 31 companies for which information about the EV/EBITDA multiple assigned to the target company was available.Source: Data from Merger Market, Thomson M&A, One Source, Mint Global and company press releases.

Deal breakdown by EBITDA multiple in 2015 (%)

An analysis of the Enterprise value/EBITDA multiple achieved on a sample of deals for which transaction details had been disclosed, confirms the premium value assigned by investors to Fashion & Luxury players: 36% of all deals were closed with a multiple greater than 15x.

The companies operating in the Hotels sector proved to be the best performing ones in 2015. 50% of target companies were valued above 15x, mainly thanks to the mark-up associated with property assets

A 5-10x EBITDA multiple was achieved on 36% of deals.

50% inHotels sector

>15x Total Fashion & Luxury

<5x

8.0%

5-10x

20.0%

36.0%

11-15x

100.0%

36.0%

Key Findings

Private Equity and Investors Survey 2016

Private Equity and investors survey 2016 23

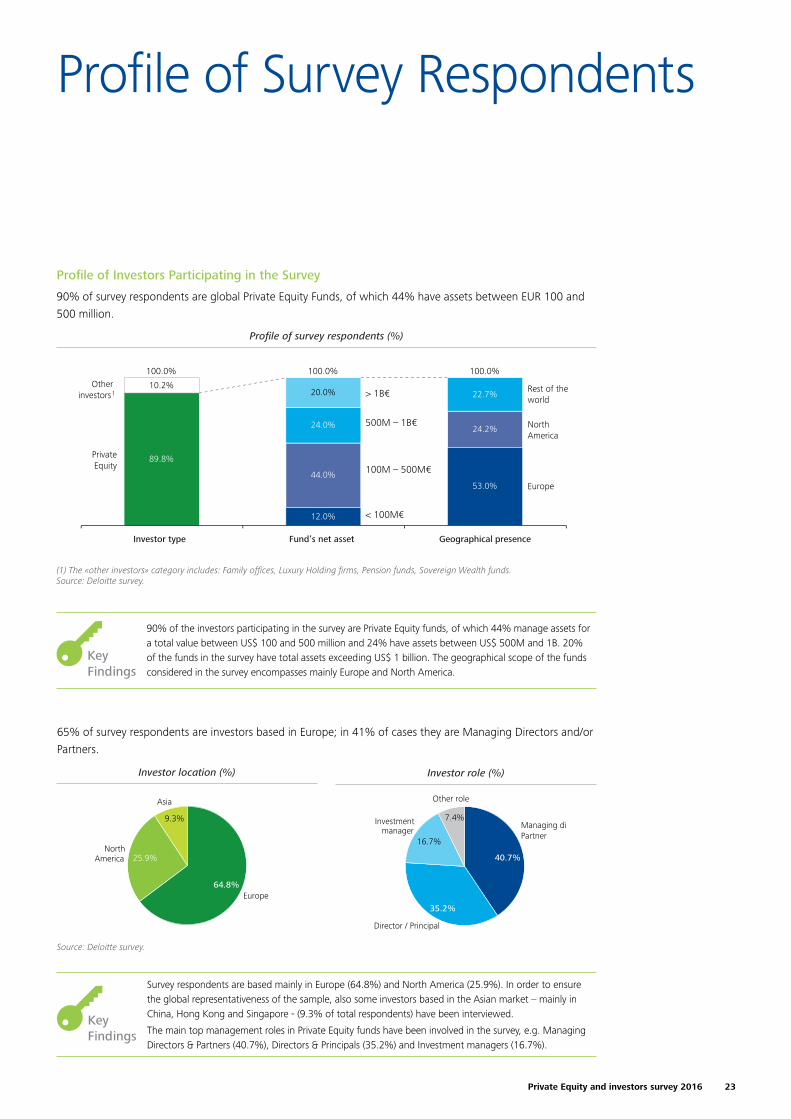

Profile of Survey Respondents

Profile of Investors Participating in the Survey

90% of survey respondents are global Private Equity Funds, of which 44% have assets between EUR 100 and

500 million.

65% of survey respondents are investors based in Europe; in 41% of cases they are Managing Directors and/or

Partners.

(1) The «other investors» category includes: Family offices, Luxury Holding firms, Pension funds, Sovereign Wealth funds.Source: Deloitte survey.

Source: Deloitte survey.

Profile of survey respondents (%)

Investor location (%) Investor role (%)

90% of the investors participating in the survey are Private Equity funds, of which 44% manage assets for a total value between US$ 100 and 500 million and 24% have assets between US$ 500M and 1B. 20% of the funds in the survey have total assets exceeding US$ 1 billion. The geographical scope of the funds considered in the survey encompasses mainly Europe and North America.

Survey respondents are based mainly in Europe (64.8%) and North America (25.9%). In order to ensure the global representativeness of the sample, also some investors based in the Asian market – mainly in China, Hong Kong and Singapore - (9.3% of total respondents) have been interviewed.

The main top management roles in Private Equity funds have been involved in the survey, e.g. Managing Directors & Partners (40.7%), Directors & Principals (35.2%) and Investment managers (16.7%).

53.0%

24.2%

22.7%

12.0%

44.0%

24.0%

20.0%

89.8%

10.2%

100.0%

North America

Other investors1

Fund’s net asset

PrivateEquity

Rest of the world

Investor type Geographical presence

100.0% 100.0%

Europe

> 1B€

500M – 1B€

100M – 500M€

< 100M€

25.9%

64.8%

North America

Asia

9.3%

Europe

7.4%

Other role

40.7%

35.2%

Director / Principal

Managing director / Partner

16.7%

Investment manager

25.9%

64.8%

North America

Asia

9.3%

Europe

7.4%

Other role

40.7%

35.2%

Director / Principal

Managing director / Partner

16.7%

Investment manager

Key Findings

Key Findings

24

Profile of Investors Participating in the Survey

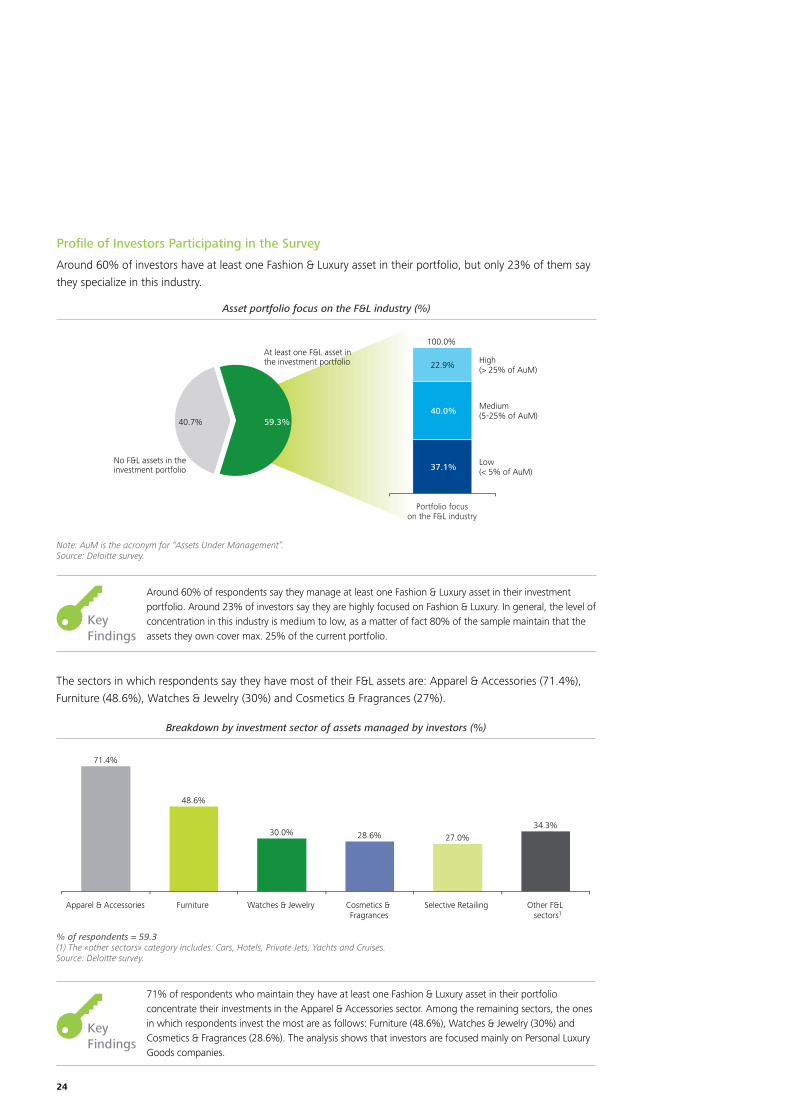

Around 60% of investors have at least one Fashion & Luxury asset in their portfolio, but only 23% of them say

they specialize in this industry.

The sectors in which respondents say they have most of their F&L assets are: Apparel & Accessories (71.4%),

Furniture (48.6%), Watches & Jewelry (30%) and Cosmetics & Fragrances (27%).

Note: AuM is the acronym for “Assets Under Management”. Source: Deloitte survey.

% of respondents = 59.3(1) The «other sectors» category includes: Cars, Hotels, Private Jets, Yachts and Cruises.Source: Deloitte survey.

Asset portfolio focus on the F&L industry (%)

Breakdown by investment sector of assets managed by investors (%)

Around 60% of respondents say they manage at least one Fashion & Luxury asset in their investment portfolio. Around 23% of investors say they are highly focused on Fashion & Luxury. In general, the level of concentration in this industry is medium to low, as a matter of fact 80% of the sample maintain that the assets they own cover max. 25% of the current portfolio.

71% of respondents who maintain they have at least one Fashion & Luxury asset in their portfolio concentrate their investments in the Apparel & Accessories sector. Among the remaining sectors, the ones in which respondents invest the most are as follows: Furniture (48.6%), Watches & Jewelry (30%) and Cosmetics & Fragrances (28.6%). The analysis shows that investors are focused mainly on Personal Luxury Goods companies.

22.9%

40.0%

100.0%

37.1%

Medium (5-25% of AuM)

Low (< 5% of AuM)

High (> 25% of AuM)

Portfolio focuson the F&L industry

59.3%

40.7%

At least one F&L asset in the investment portfolio

No F&L assets in theinvestment portfolio

Furniture

48.6%

34.3% 27.0%

Cosmetics & Fragrances

Other F&L sectors1

28.6%

Watches & Jewelry

30.0%

Apparel & Accessories

71.4%

Selective Retailing

Key Findings

Key Findings

Private Equity and investors survey 2016 25

Investors maintain that in ~72% of cases the Fashion & Luxury assets in their portfolio have sales below US$

100M, whereas 20% of them own medium-sized assets (companies with sales between US$ 100 and 250M).

% of respondents = 59.3Source: Deloitte survey.

Average turnover of Fashion & Luxury assets in investors’ portfolios (%)

71.4% of the assets in the current portfolio of investors have a turnover below US$ 100 million

Only 20% of the considered sample invests in medium-sized companies, whereas only 8% has stakes in large-sized organizations.

100.00% 2.86%

251-500M$

51-100M$

25-50M$

28.57%

<25M$

20.00%

Total F&L Investors

>500 M$

5.71%

101-250M$

20.00%

22.86%

71.4%

Key Findings

26

2016 Market Outlook

Features of the Current F&L Portfolio

Around 60% of investors say they own one Fashion & Luxury asset characterized by a majority stake and an

average duration below 5 years.

The development of distribution channels, internationalization, and performance improvement are the main

strategies adopted by investors to promote the growth of their Fashion & Luxury assets.

Source: Deloitte survey.

% of respondents = 59.3Source: Deloitte survey.

Equity stake and average duration of Fashion & Luxury assets (%)

Adoption of main key strategic drivers (%)

71.4% of respondents maintain they have a majority stake in the Fashion & Luxury companies present in their investment portfolio; this figure is in line with data referring to deals finalized in 2015 (77%).

In most cases (68.6%), the average duration of Fashion & Luxury assets present in the current portfolio of investors is below 5 years.

In 2015, the main strategies used to create economic value from the assets owned were:• «Development of new distribution channels» - 60% • «Penetration of new geographical markets» - 51%• «Improvement of operational performance through actions to increase efficiency» - 37%• «Development of new products» - 29%

Key Findings

71.4% 28.6%

Majority

Minority

> 5 years

< 5 years

68.6% 31.4%

100.0%

59.3%

40.7%

At least one F&L asset in the investment portfolio

No F&L assets in the investment portfolio

Investors with F&L assets in their portfolio

Mai

n dr

iver

s

11.4%

14.3%

20.0%

22.9%

22.9%

28.6%

37.1%

51.4%

60.0%

Value chain vertical expansion

Financial restructuringand/or leverage

Brand lineExtension

Internationalization strategy

Creation of a new distribution channel

Change inmanagement

New Product Development

Performance improvement

Brandre-positioning

Key Findings

Private Equity and investors survey 2016 27

Exit Strategy for 2016

In 2016, 44% of investors foresee at least one exit from their F&L portfolio in 2016, mainly driven by the

opportunity to achieve high returns on the investment made.

% of respondents = 58(1) The «other strategies» category includes: Change in investment strategy and Mismatch of Market Trends versus the investment thesis scenario.Source: Deloitte survey.

Exit drivers (%) Exit strategy (%) Expected multiple (%)

44% of investors maintain they intend to sell some of the Fashion & Luxury assets currently in their portfolio during 2016. Moreover, the respondents say that the possibility of maximizing the return on their investment (according to 52.6% of the sample) – as a matter of fact, 73% of investors expect to achieve EBITDA multiples above 10x – and the completion of the investment cycle (26.3%) will be the main incentives to exit in 2016. Trade sales (54.2%) and secondary buy-outs (37.5%) are likely to be the most popular exit strategies.

Key Findings

52.6%

26.3%

21.1%

44.1%

55.9%

High returns opportunity

Exit driver

Other strategies1

No exit in 2016

100.0% 100.0%

At least oneexit in 2016

Closing investment period

Divestmentsin 2016

Divestmentsin 2016

Divestmentsin 2016

54.2%

37.5%

8.3%

44.1%

55.9% Secondary buyout

100.0% 100.0%

IPO

Exit strategy

Trade sale

26.7%

73.3%

44.1%

55.9%> 10x

100.0% 100.0%

ExpectedEBITDA multiple

< 10x

28

2016 Fashion & Luxury Market Outlook by Sector

53% of respondents forecast an increase of over 5% in the Fashion & Luxury market in 2016. The best growth

expectations are observed in the Cosmetics & Fragrances and Furniture sectors.

Investors with assets in the F&L industry anticipate better results in the Apparel & Accessories, Cosmetic &

Fragrances and Cars sectors.

% of respondents = 100Source: Deloitte survey.

Note: The positive sentiment delta represents the difference expressed as a percentage between investors operating, and those not operating, in the F&L industry who expect a market growth.Fonte: Deloitte Survey.

Expected market trends in 2016 - breakdown by sector (%)

Expected market trends in 2016 - breakdown by sector (%)

53% of all respondents forecast a growth in the Fashion & Luxury market during 2016; 15% of them (i.e. 8% of all respondents) predict the increase will exceed 10%.

According to over 50% of respondents, the Cosmetics & Fragrances, Furniture, Apparel & Accessories, Cars and Hotels sectors will grow by over 5%, whereas around 10% of them forecast a double-digit trend.

Some difficulties are expected in the Yachts and Private Jets sectors, in which according to 25% of respondents a negative trend will develop over the next year.

Key Findings

16% 21% 22% 25% 21%

37%38%

27%

33%39% 43% 32%

39%45%

38%38%

49%42%

55%

40%45%

48%49%

29%23% 36%

45%

10% 14% 9% 11% 10%

9%9%

100%

Cruises

5% 100%

7%

Furniture

7%

Hotels

100% 100%

Private Jets

100% 100%

Cosmetics & Fragrances

Yachts

100%

Cars

2% 6%

7%

100%

Watches & Jewelry

100% 100%

4%

4%

Apparel & Accessories

4%

Total F&L market

100%

8%

Selective Retailing

Strong increase (>10%) Increase (5-10%)

Decrease (<0%)

Stable (0-5%)

Positive sentiment

59% 46% 69% 46% 54% 60% 39% 30% 53%41% 50%

17% 27% 23%11%

29%40%

17%

38%32% 48% 39%

36% 50%43%

52%

47%

69%

41%48%

40%39%

32%23%

38%46%

14%11%12%13%

35%

11%14%13%

100% 4% 7%

100% 100% 5% 5%

100% 100% 8%

100% 100% 100% 4%

100% 100% 3%

100%

8% 6%

35% 26% 28% 28%50%

20%

40%26%

47% 37%21%

42%39% 33%

40%

45% 35% 35% 37% 42% 58%

63%

26%22% 33%

44%

10% 15% 11% 11% 11% 16% 11%

16%10%

Total F&Lmarket

Cruises

8%

Yachts

8% 100% 100%

6% 100%

Private Jets

100% 100% 100%

5% 5%

Cosmetics& Fragrances

Cars Hotels Furniture

100% 100%

SelectiveRetailing

100%

Watches& Jewelry

5% 100% 100%

Apparel &Accessories

Investors withassets in theFashion &Luxury industry

Investors notoperating in theFashion &Luxury industry

+15% Delta positive sentiment +2% +33% -4% +3% -14% -24% -5% -6% +4% +1%

Stable (0-5%) Strong increase (>10%) Increase (5-10%) Decrease (<0%)

Private Equity and investors survey 2016 29

2016 Fashion & Luxury Market Outlook by Geographical Area

Asia, the Middle East and North America will be the main growth markets in 2016, driving the performance of

the entire industry; the trend is expected to remain mainly stable in Europe.

Investors with assets in the F&L industry anticipate better results in Europe and Latin America.

% of respondents = 100Source: Deloitte survey.

Note: The positive sentiment delta represents the difference expressed as a percentage between investors operating, and those not operating, in the F&L industry who expect a market growth.Fonte: Deloitte Survey.

Expected market trends in 2016 - breakdown by geographical area (%)

Expected market trends in 2016 - breakdown by geographical area (%)

The geographical areas that are expected to experience the strongest growth in 2016 are Asia, the Middle-East and North America: over 60% of respondents expect that growth will exceed 5% in these areas. The best performances are expected in the Asian market, where 30% of investors predict a double-digit growth. The respondents do not seem to agree on Japan: 28% of them predict a positive trend for 2016 and 24% expect a contraction of the market.

The majority of respondents expect the trend to remain stable in Europe over the next year.

Key Findings

23% 24%15% 16%

51%

36%

33%47%

11%20% 47% 38%

33%

52%

37%24%

45%44%

47%45%

12%30%

20%8%

9%14%

Middle East

Global F&L market

100% 100%

Rest of

the World

3%

3%

100%

Asia

100%

North America

Japan

2%

100% 100%

Latin America

100%

4% 7%

Europe

100%

Increase (5-10%)

Decrease (<0%)

Strong increase (>10%)

Stable (0-5%)

Positive sentiment

35% 64% 44% 28% 75% 50% 53% 64%

+33% Delta Positive sentiment

22%10%

39%

34%

36%

52%

14%29% 52% 35%

45%

52%36%

22%

52%36%

43% 46%

14% 12%24% 25%

11%11%16%13%

100% 100% 100% 100% 100% 100% 7% 4% 4%

100% 3%

100%

33% 28% 22% 24%

70%

38%

28% 39%

40% 40%

15%

52%

39% 28%

33%

59%

53% 44%

15%

12%

39%

10% 8% 100%

8%

100%

Rest ofthe World

7%

Middle East

100%

Europe Asia

100% 100% 100%

6%

Japan North America

100%

6%

6%

Latin America

100%

+4% +9% -8% +4% -10% -6% +1%

Total F&Lmarket

Stable (0-5%)Strong increase (>10%) Increase (5-10%) Decrease (<0%)

Investors withassets in theFashion &Luxury industry

Investors notoperating in theFashion &Luxury industry

30

2016 Investment Strategy

Expected Investments in F&L in 2016

In 2016, 76% of investors plan to carry out new transactions in the Fashion & Luxury industry. Personal Luxury

Goods will remain the most attractive target thanks to higher growth performance and margins than the rest

of the industry.

Propensity to invest in the various F&L sectors tends to be similar among investors with or without assets in the

F&L industry.

% of respondents = 98(1) The «other F&L sectors» category includes: Cars, Hotels, Private Jets, Yachts and Cruises.Source: Deloitte survey.

(1) The «other sectors» category includes: Cars, Hotels, Private Jets, Yachts and Cruises.Source: Deloitte survey.

Propensity to invest in Fashion & Luxury assets in 2016 and main target sectors (%)

Propensity to invest in Fashion & Luxury assets in 2016 and main target sectors (%)

The respondents who plan to invest in the Fashion & Luxury industry (76% of all respondents) will focus on the Apparel & Accessories sector (75% of respondents).

Investors show strong interest also in the Cosmetics & Fragrances sector, where around 50% of the sample plans to finalize at least one deal. The main sectors expected to attract investments over the next year include Furniture, Selective Retailing and Watches & Jewelry; the latter draws a large number of investors from different industries (other than F&L) who are attracted by the increase in sales and operating margins characterizing this sector. General propensity to invest in Personal Luxury Goods companies.

Key Findings

75.9%

24.1%

Apparel & Accessories

75.0%

Watches & Jewelry

20.5%

Other F&Lsectors 1

Furniture

38.6%

Cosmetics & Fragrances

34.1%

47.7%

Selective Retailing

25.0%

Current investorin F&L

New investorin F&L

69.7%

30.3%

71.4%

28.6%

64.7%

35.3%

66.7%

33.3%

44.4%

55.6%

54.5%

45.5%

At least one F&L asset in the investment portfolio

No F&L assets in theinvestment portfolio

76.7%

33.3%

13.3% 20.0%

50.0% 36.7%

Other F&L sectors 1Furniture Selective Retailing

Cosmetics & Fragrances

Apparel & Accessories

Watches & Jewelry

71.4%

35.7% 35.7% 35.7% 42.9% 42.9%

Other F&L sectors 1 Furniture Selective Retailing

Cosmetics & Fragrances

Apparel & Accessories

Watches & Jewelry

Investors withassets in theFashion &Luxury industry

Investors notoperating in theFashion &Luxury industry

Private Equity and investors survey 2016 31

Size of Potential Investments in F&L

Investments in the Apparel & Accessories sector will target large-sized organizations in 27% of cases, whereas

deals in the other sectors will focus mainly on mid-market companies.

Deal Characteristics: Deal Type and Equity Stake

Around 60% of investors plan to carry out new transactions in the market using Expansion Capital, Leverage

Buy-out and Management Buy-out strategies to acquire a majority stake in the target company.

% of respondents = 75(1) The «other sectors» category includes: Cars, Hotels, Private Jets, Yachts and Cruises.Source: Deloitte survey.

% of respondents = 75(1) The «other strategies» category includes: Turnarounds and Start-up Financing.Source: Deloitte survey.

Average sales of potential target companies – breakdown by sector (%)

New investments – breakdown by deal type and equity stake (%)

The survey shows an investor propensity to acquire large organizations in the Apparel & Accessories sector, which will be the main target sector in 2016; more specifically, 27% of respondents plan to invest in companies with sales over US$ 100M. 80% of respondents planning to carry out M&A deals in the Cosmetics & Fragrances, Watches & Jewelry and Furniture sectors will select small to medium-sized target companies with a turnover below US$ 100M.

Over 50% of respondents plan to finalize new acquisitions in the Fashion & Luxury industry through Expansion Capital, Leverage Buyout and Management Buyout strategies.

Investors anticipate acquiring a majority stake in the target company through most of the transactions carried out.

Key Findings

Key Findings

14%

44%21%

14%29%

20% 27%

45%33%

44% 47%

53%

9%

15%29%

13%

55%

10% 11% 7% 9%

7%12% 11%

20%

41%

19%

8%

Total F&Lmarket

100%

Furniture

100%

Watches & Jewelry

100% 100%

Apparel & Accessories

6%

6% 6%

6% 6%

Cosmetics & Fragrances

2%

Other F&LSectors

1

100% 100%

Selective Retailing

100%

25 - 50M€

101 - 250M€

500 - 1B€

< 25M€

51 - 100M€

251 - 500M€

20.5%

Support to MBO/MB

LBO or Replacement

54.5% 61.4%

Expansion capital

63.2%

18.2%

Other strategies 1

Corporate carve-out

Minority stake

Majority stake

37.0%

63.0%

18.5%

81.5%

16.7%

83.3%

33.3%

66.7%

8.3%

91.7%

32

Deal Characteristics: Financing Strategy

67.5% of respondents say they will buy a stake greater than 40%, using mainly senior debt to fund the

transaction.

% of respondents = 100(1) The «other types» category includes: Junior Debt, Unitranche and Equity.Source: Deloitte survey.

Equity stake to be acquired in the new asset (%) Funding sources (%)

~67% of transactions will result in the acquisition of a stake of more than 40% in the target company.

Senior debt will be the main funding source for acquisition deals in the Fashion & Luxury industry.

The other main funding sources mentioned by investors include Shareholders’ loans (43%), Vendor’s notes or convertible bonds (27%) and Mezzanine Financing (23%).

Key Findings

Vendor’s notes or convertible

bonds

Mezzanine financing

23%

80%

Other types 1 Shareholders’loan

43%

9%

Senior debt

27%

Total

100.0%

> 60%

23.3%

21 - 40% 41 - 60% 0 - 20%

18.6%

14.0%

44.2%

Private Equity and investors survey 2016 33

Return Expected From New Investments

The IRR expected from new investments in the Fashion & Luxury industry is between 20% and 30%, as

confirmed by the past business performance of top players in this industry.

The highest returns are expected from large-sized organizations; 35% of the investors who forecast an IRR

above 20% plan to invest in companies with sales above US$ 100M.

% of respondents = 75(1) The «other sectors» category includes: Cars, Hotels, Private Jets, Yachts and Cruises.Source: Deloitte survey.

% of respondents = 100Source: Deloitte survey.

Internal Return Rate expected from new F&L investments – breakdown by sector (%)

Internal Return Rate expected from new F&L investments – breakdown by target company size (%)

On average, investors expect the new investments in the Fashion & Luxury industry to have an IRR between 21% and 30%. The best performing sector – in terms of average profitability - is expected to be Watches & Jewelry, for which around 20% of respondents forecast an IRR greater than 30%, as confirmed by an analysis of the business performance of top players.

Key Findings

23% 30% 30% 31% 33%50%

68% 60%50%

56% 56%40%

9% 10%20% 13% 11% 10%

31%

57%

12%

100%

Total F&L market Other F&Lsectors

1

100%

Selective retailing

100% 100%

Furniture Apparel & Accessories

Watches & Jewelry

Cosmetics & Fragrances

100% 100% 100%

> 30%

< 20%

21-30%

< 20%

12.9%

35.5%

Expected IRR (%)

70.5%

16.1%

19.4%

> 20%

6.5%

Targ

et t

urno

ver

size

(M$)

9.7%

29.5%

15.4%

23.1%

38.5%

23.1% Big Companies account for35.6% of highreturn investments

51 - 100M$

< 25M$

251 - 500M$

500 - 1B$

25 - 50M$

101 - 250M$

34

About Deloitte and its Fashion & Luxury Practice

Deloitte EMEA Fashion & Luxury Center of Excellence

A Network of 65 cross-functional Subject Matter

Experts (SME) with competence in the Fashion &

Luxury industry able to suit diverse client needs.

Countries involved

France - Germany - Italy - Netherlands - Spain -

Switzerland - Turkey - United Kingdom.

Main Objective

Cross-border cooperation to leverage on specific local

expertise to deliver high level services to Fashion &

Luxury clients and targets across Europe.

Our Top Offerings

• Core business transformation & Global retail

Transformation

• CRM & Digital Transformation

• Marketing & Sales Strategy Operations

• Contract Risk and Compliance

• Risk Analytics

• Internal Controls

• Internal Audit Services

• Sustainability

• Corporate Finance Advisory

• Strategy & Business Planning

• Transaction Services

• Forensic

• Transfer prices – supply chain

• Custom duties/vat/logistic tax issues – supply chain

• Data privacy

• Personal planning for private family

Global Fashion & Luxury: Glossary

Personal Luxury Goods Personal Luxury Goods include the following

sectors: Apparel & Accessories, Cosmetics &

Fragrances and Watches & Jewelry

F&L Abbreviation for Fashion & Luxury

App&Acc Abbreviation for Apparel & Accessories

Cos&Fra Abbreviation for Cosmetics & Fragrances

Wat&Jew Abbreviation for Watches & Jewelry

PLG Acronym for Personal Luxury Goods

IRR Acronym for Internal Return Rate

PE Acronym for Private Equity

M&A Acronym for Merger & Acquisition

Il nome Deloitte si riferisce a una o più delle seguenti entità: Deloitte Touche Tohmatsu Limited, una società inglese a responsabilità limitata (“DTTL”), le member firm aderenti al suo network, e le loro entità correlate. DTTL e ciascuna delle sue member firm è un’entità giuridicamente separata e indipendente dalle altre. DTTL (descritta anche come “Deloitte Global”) non fornisce servizi ai clienti. Si invita a leggere l’informativa completa relativa alla descrizione della struttura legale di Deloitte Touche Tohmatsu Limited e delle sue member firm all’indirizzo www.deloitte.com/about.

© 2016 Deloitte Touche Tohmatsu LimitedStudio Grafico Deloitte, Italia - SG.051.16

Contacts

Deloitte Fashion & Luxury Leaders Deloitte Financial Advisory contacts

EMEA Fashion & Luxury LeaderPatrizia Arienti | [email protected]

FranceBenedicte Sabadie | [email protected]

Germany Karsten Hollasch | [email protected]

ItalyPatrizia Arienti | [email protected]

NetherlandsVictor Hoong | [email protected]

SpainJuan José Peso | [email protected] Lopez Tellez | [email protected]

SwitzerlandKarine Szegedi | [email protected]

TurkeyHakan Gol | [email protected]

UKNick Pope | [email protected]

ChinaIvan Man Kit Wong | [email protected] Fantacci | [email protected]

FranceClaire Deguerry | [email protected]

Germany Karsten Hollasch | [email protected]

ItalyElio Milantoni | [email protected] Nastasi | [email protected]

SpainRoberto Martinez Roldan | [email protected]

SwitzerlandHoward Da Silva | [email protected] Gehre | [email protected] UKRichard Lloyd-Owen | [email protected] Pacitti | [email protected]

USLorin DeMordaunt | [email protected]

SingaporeJiak See Ng | [email protected] Snyder | [email protected]