global economic outlook - sifm.org · u.s. outlook: no more fat pitches june 2019 constance l....

TRANSCRIPT

U.S. Outlook: No More Fat Pitches June 2019

Constance L. Hunter, CBEChief Economist @[email protected]

KPMG Economics

2© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Economic activity firms in 2018

Source: KPMG Economics, BEA, Haver Analytics

2017 2018

GDP 2.2 2.9

Consumption 2.5 2.6

Business Investment 5.3 7.0

Residential Investment 3.3 -0.2

Federal Gov't 0.7 2.6

Exports 3.0 3.9

Imports 4.6 4.6

Growth Rates (Annual %)

3© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

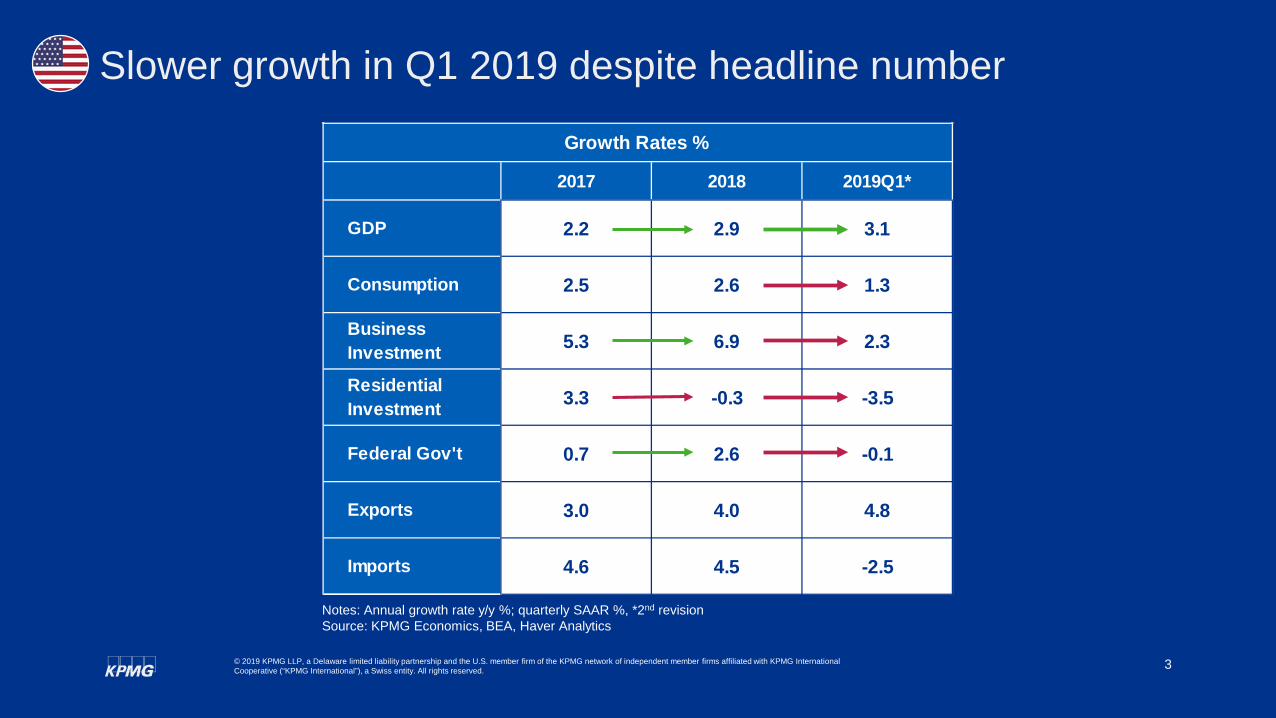

2017 2018 2019Q1*

GDP 2.2 2.9 3.1

Consumption 2.5 2.6 1.3

Business Investment 5.3 6.9 2.3

Residential Investment 3.3 -0.3 -3.5

Federal Gov't 0.7 2.6 -0.1

Exports 3.0 4.0 4.8

Imports 4.6 4.5 -2.5

Growth Rates %

Slower growth in Q1 2019 despite headline number

Notes: Annual growth rate y/y %; quarterly SAAR %, *2nd revisionSource: KPMG Economics, BEA, Haver Analytics

4© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Notes: Annual growth rate y/y %; quarterly SAAR %, *2nd revisionSource: KPMG Economics, BEA, Haver Analytics

2017 2018 2019Q1*

GDP 2.2 2.9 3.1

Consumption 2.5 2.6 1.3

Business Investment 5.3 6.9 2.3

Residential Investment 3.3 -0.3 -3.5

Federal Gov't 0.7 2.6 -0.1

Exports 3.0 4.0 4.8

Imports 4.6 4.5 -2.5

Growth Rates %

Trade developments added to GDP but are not good news

5© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Notes: Annual growth rate y/y %; quarterly SAAR %, *2nd revisionSource: KPMG Economics, BEA, Haver Analytics

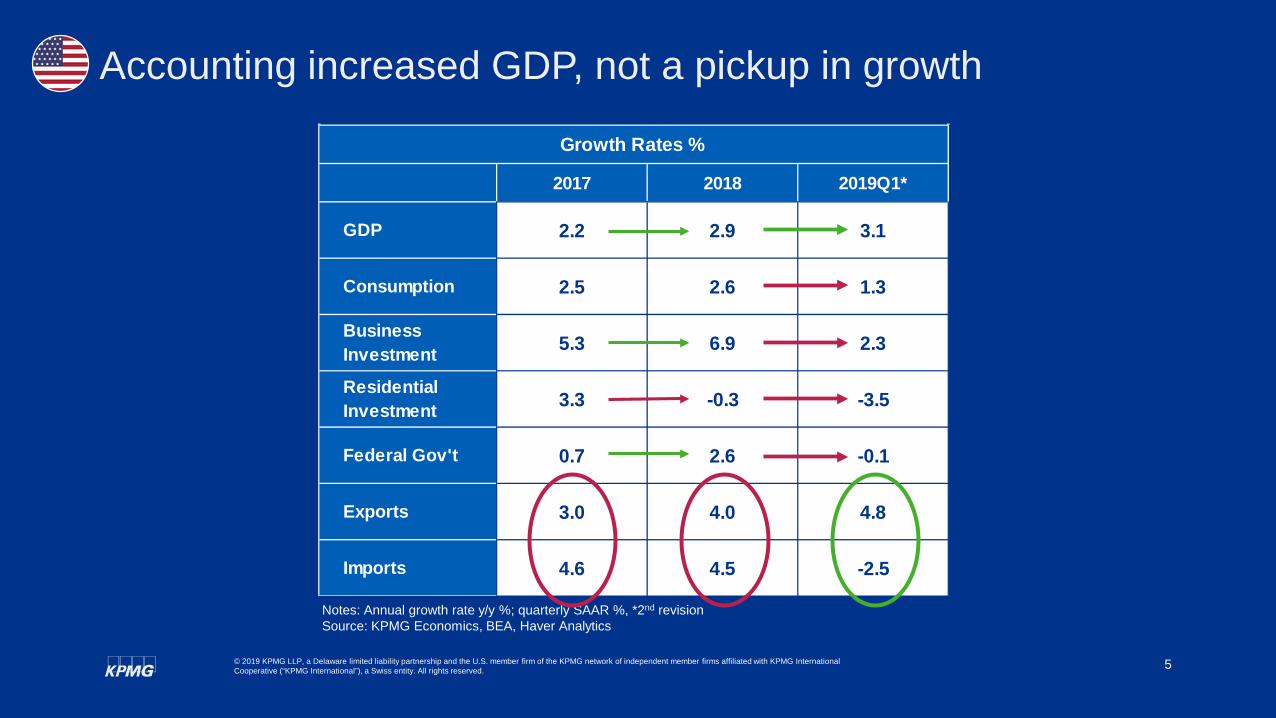

2017 2018 2019Q1*

GDP 2.2 2.9 3.1

Consumption 2.5 2.6 1.3

Business Investment 5.3 6.9 2.3

Residential Investment 3.3 -0.3 -3.5

Federal Gov't 0.7 2.6 -0.1

Exports 3.0 4.0 4.8

Imports 4.6 4.5 -2.5

Growth Rates %

Accounting increased GDP, not a pickup in growth

6© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

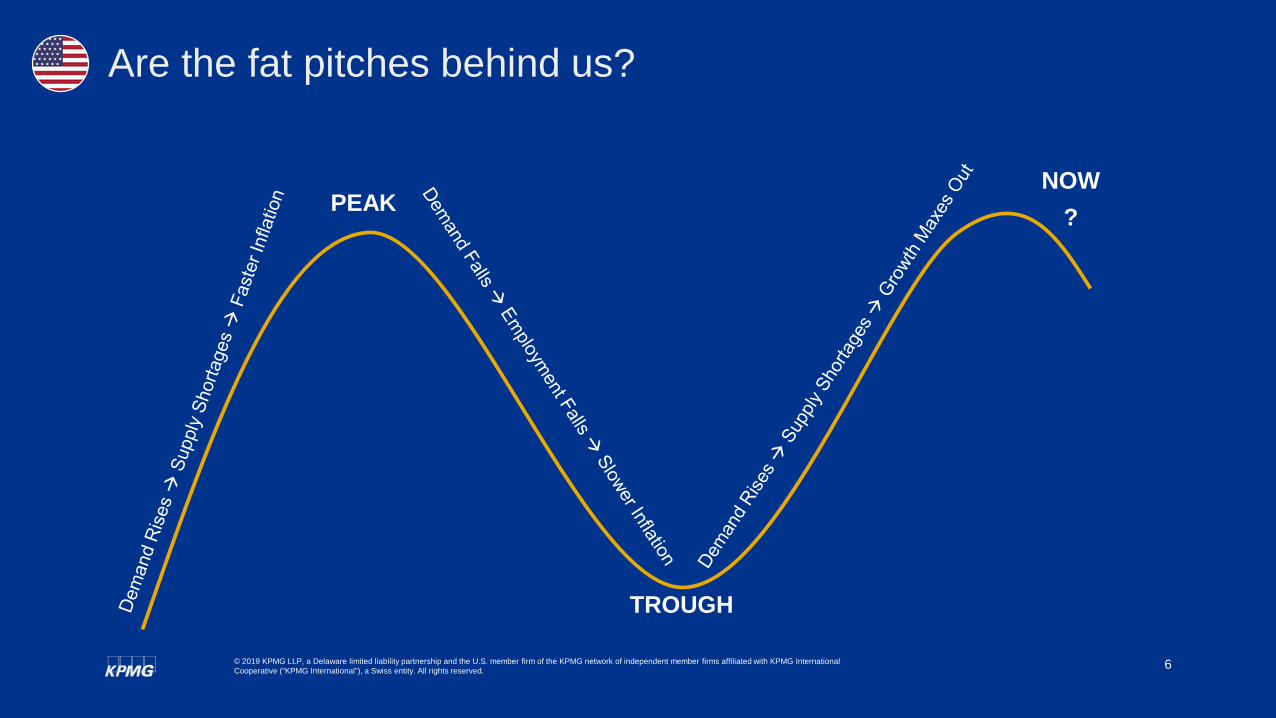

Are the fat pitches behind us?

PEAK

TROUGH

NOW?

7© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Bond market signaling a recession is on the way

Recession

Source: KPMG Economics, Federal Reserve Board (June 7, 2019), Haver Analytics

8© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

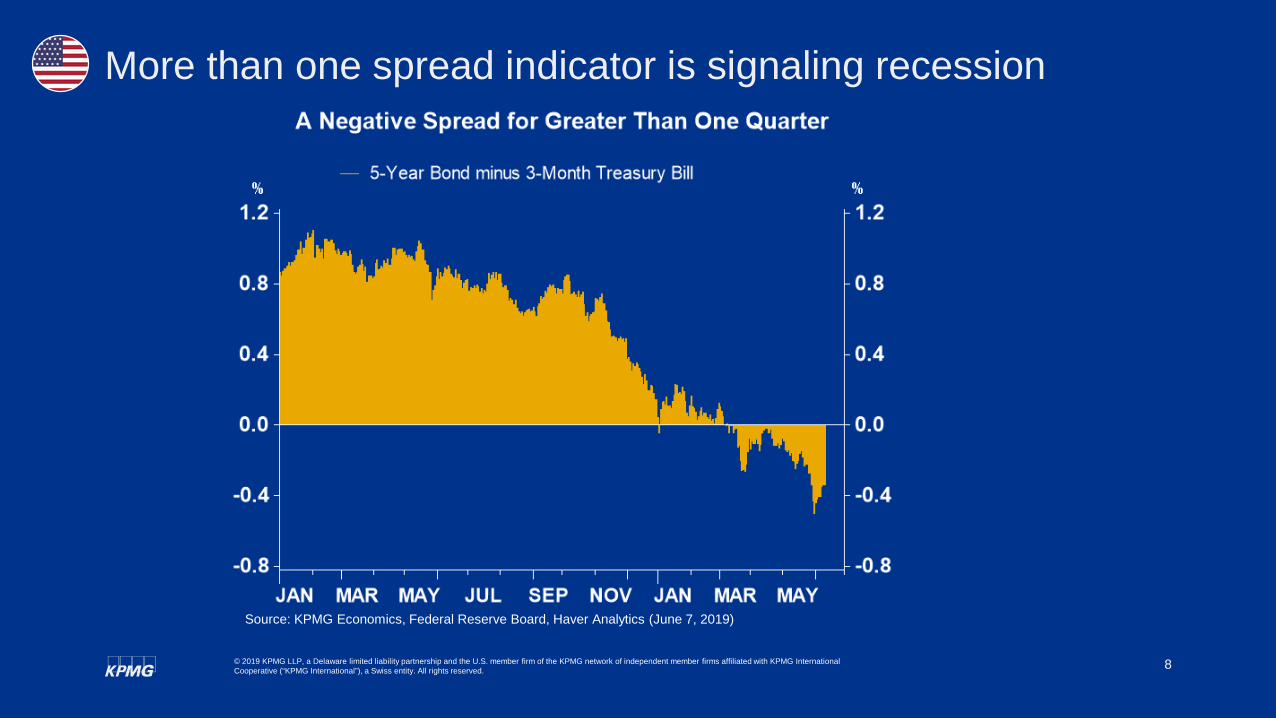

More than one spread indicator is signaling recession

Source: KPMG Economics, Federal Reserve Board, Haver Analytics (June 7, 2019)

9© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

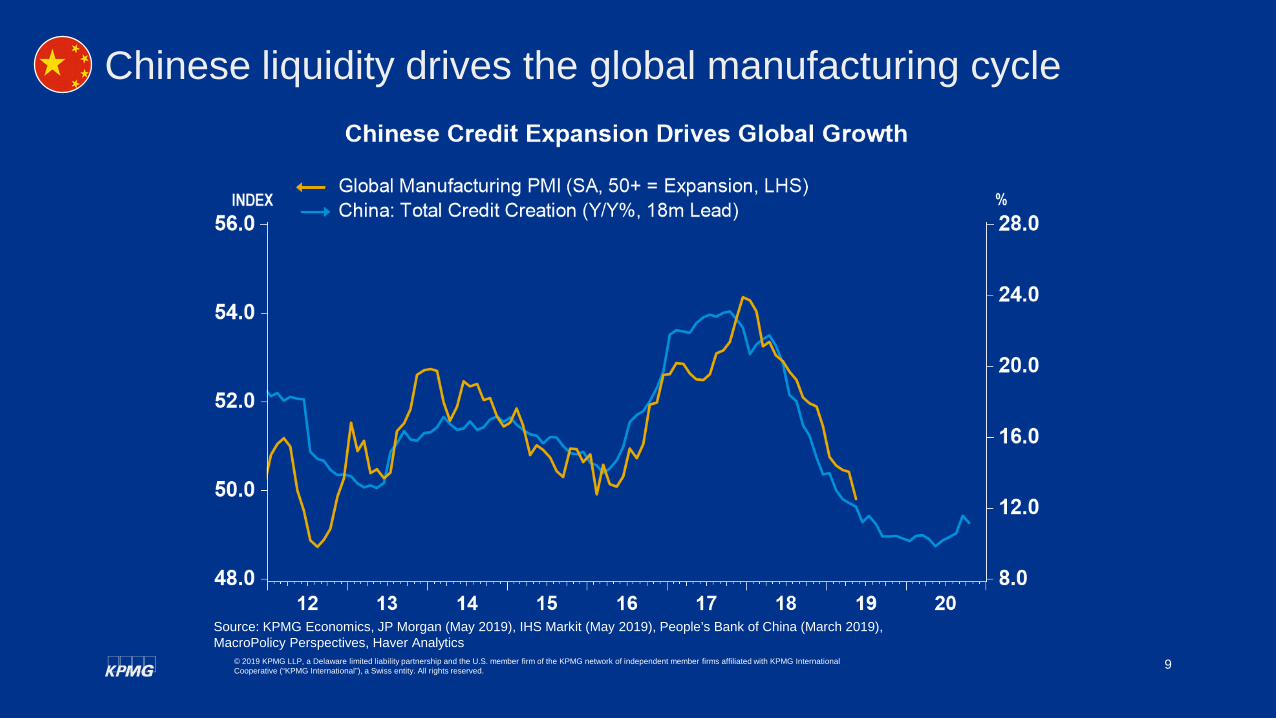

Chinese liquidity drives the global manufacturing cycle

Source: KPMG Economics, JP Morgan (May 2019), IHS Markit (May 2019), People’s Bank of China (March 2019), MacroPolicy Perspectives, Haver Analytics

10© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The global manufacturing cycle is under stress

PMIDeveloped Markets Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19Australia 54.0 54.5 54.6 54.0 53.9 52.9 52.0 50.9 51.0Canada 54.8 53.9 54.9 53.6 53.0 52.6 50.5 49.7 49.1France 52.5 51.2 50.8 49.7 51.2 51.5 49.7 50.0 50.6Germany 53.7 52.2 51.8 51.5 49.7 47.6 44.1 44.4 44.3Greece 53.6 53.1 54.0 53.8 53.7 54.2 54.7 56.6 54.2Ireland 56.3 54.9 55.4 54.5 52.6 54.0 53.9 52.5 50.4Italy 50.0 49.2 48.6 49.2 47.8 47.7 47.4 49.1 49.7Japan 52.5 52.9 52.2 52.6 50.3 48.9 49.2 50.2 49.8Korea 51.3 51.0 48.6 49.8 48.3 47.2 48.8 50.2 48.4Spain 51.4 51.8 52.6 51.1 52.4 49.9 50.9 51.8 50.1UK 53.7 51.1 53.3 54.3 52.8 52.1 55.1 53.1 49.4US 55.6 55.7 55.3 53.8 54.9 53.0 52.4 52.6 50.5Emerging MarketsChina 50.0 50.1 50.2 49.7 48.3 49.9 50.8 50.2 50.2Brazil 50.9 51.1 52.7 52.6 52.7 53.4 52.8 51.5 50.2India 52.2 53.1 54.0 53.2 53.9 54.3 52.6 51.8 52.7Mexico 51.7 50.7 49.7 49.7 50.9 52.6 49.8 50.1 50.0Source: KPMG Economics, IHS Markit (May 2019), Haver Analytics

11© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Slow car sales suggests a weaker consumer in the EU

Source: KPMG Economics, Verban der Automobilindustrie (May 2019), Asociacion Espanola de Fabricanes de Automoviles y Camiones (April 2019), Associazione Nazionale Fra Industrie Automobilistiche (April 2019), Haver Analytics

12© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

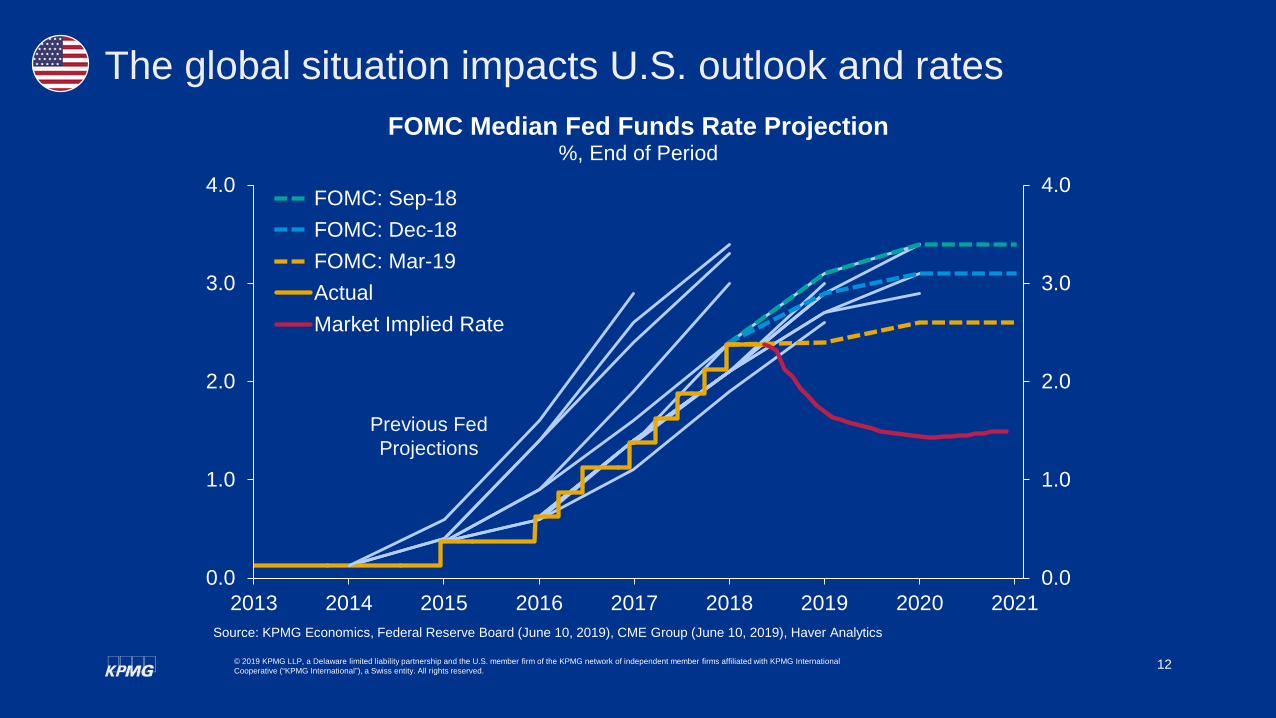

The global situation impacts U.S. outlook and rates

0.0

1.0

2.0

3.0

4.0

0.0

1.0

2.0

3.0

4.0

2013 2014 2015 2016 2017 2018 2019 2020 2021

FOMC Median Fed Funds Rate Projection%, End of Period

FOMC: Sep-18FOMC: Dec-18FOMC: Mar-19ActualMarket Implied Rate

Source: KPMG Economics, Federal Reserve Board (June 10, 2019), CME Group (June 10, 2019), Haver Analytics

Previous Fed Projections

13© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

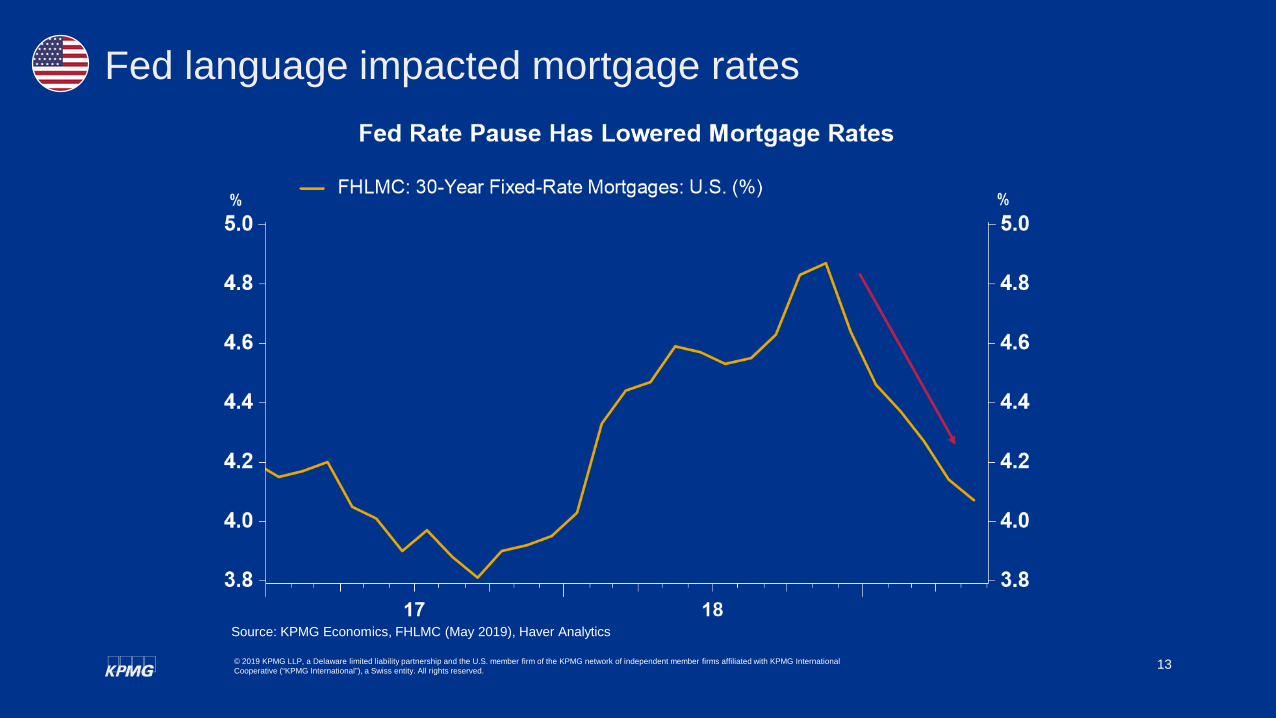

Fed language impacted mortgage rates

Source: KPMG Economics, FHLMC (May 2019), Haver Analytics

14© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

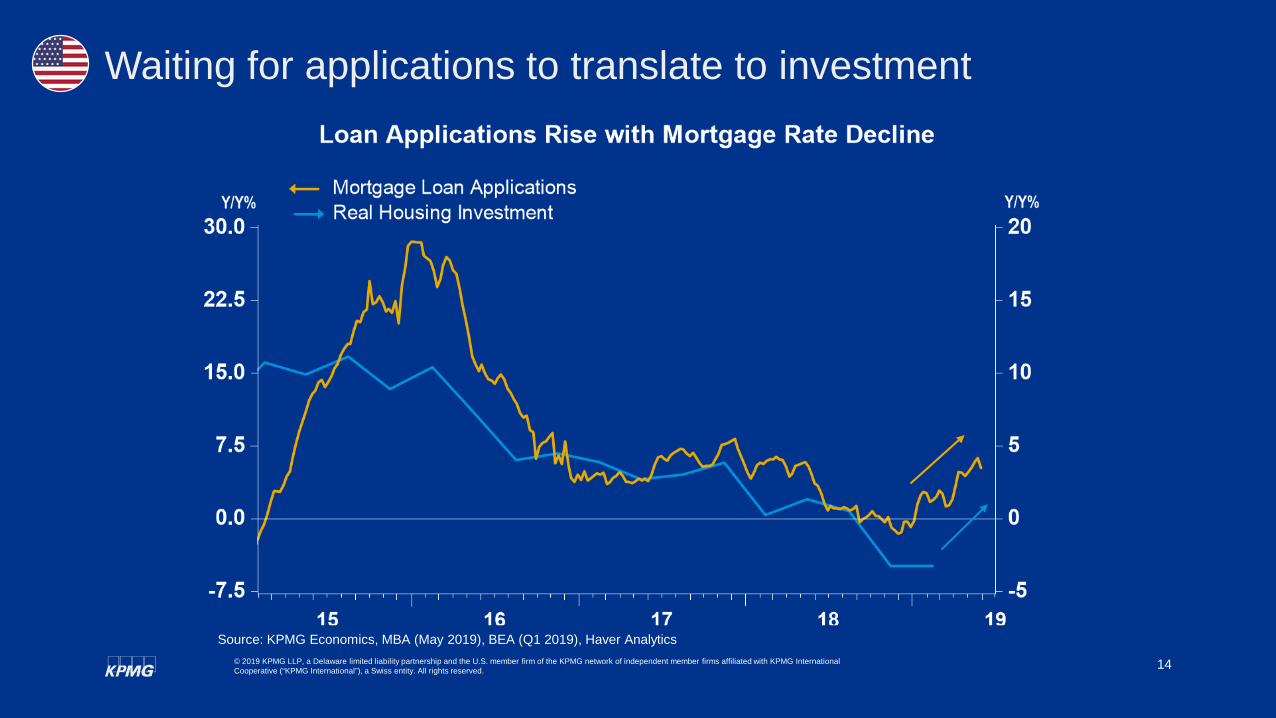

Waiting for applications to translate to investment

Source: KPMG Economics, MBA (May 2019), BEA (Q1 2019), Haver Analytics

15© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

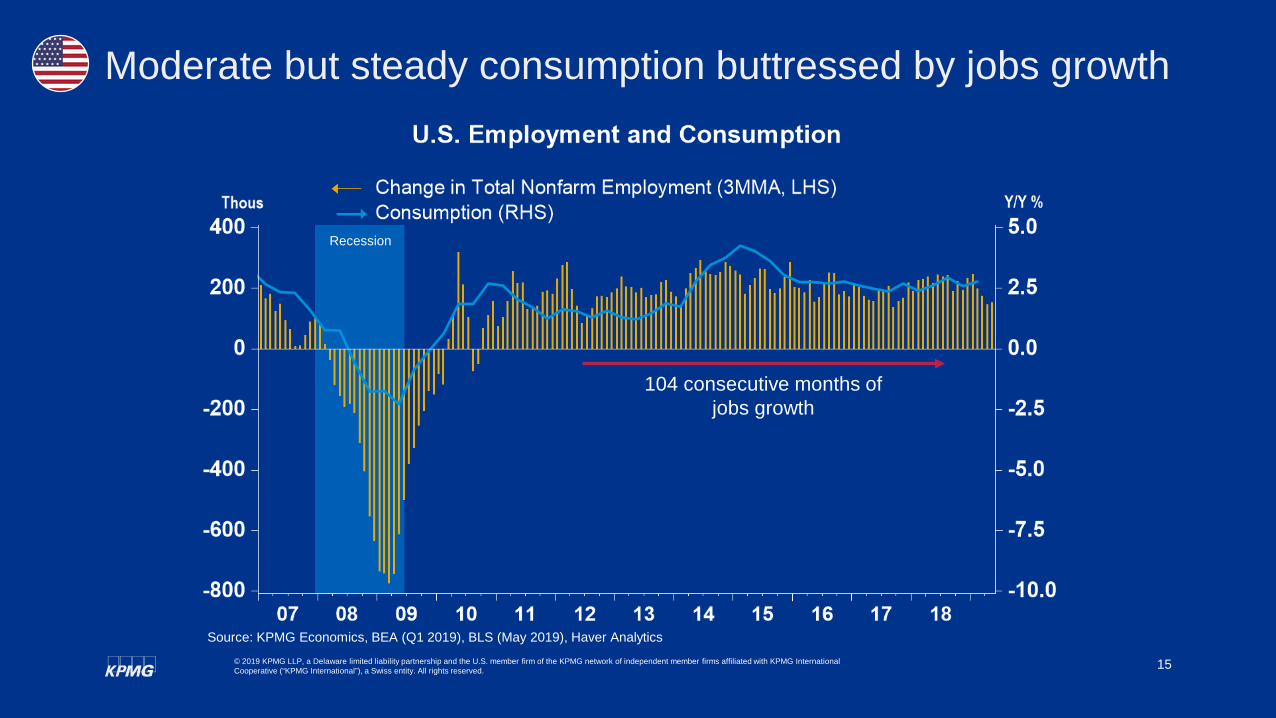

Moderate but steady consumption buttressed by jobs growth

Recession

104 consecutive months of jobs growth

Source: KPMG Economics, BEA (Q1 2019), BLS (May 2019), Haver Analytics

16© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Inflation persistently low despite long expansion and jobs growth

Recession Target Rate

Source: KPMG Economics, Bureau of Economic Analysis (May 2019), Haver AnalyticsNote: Core PCE Index is smoothed using a 3-month moving average of the year to year growth rate

17

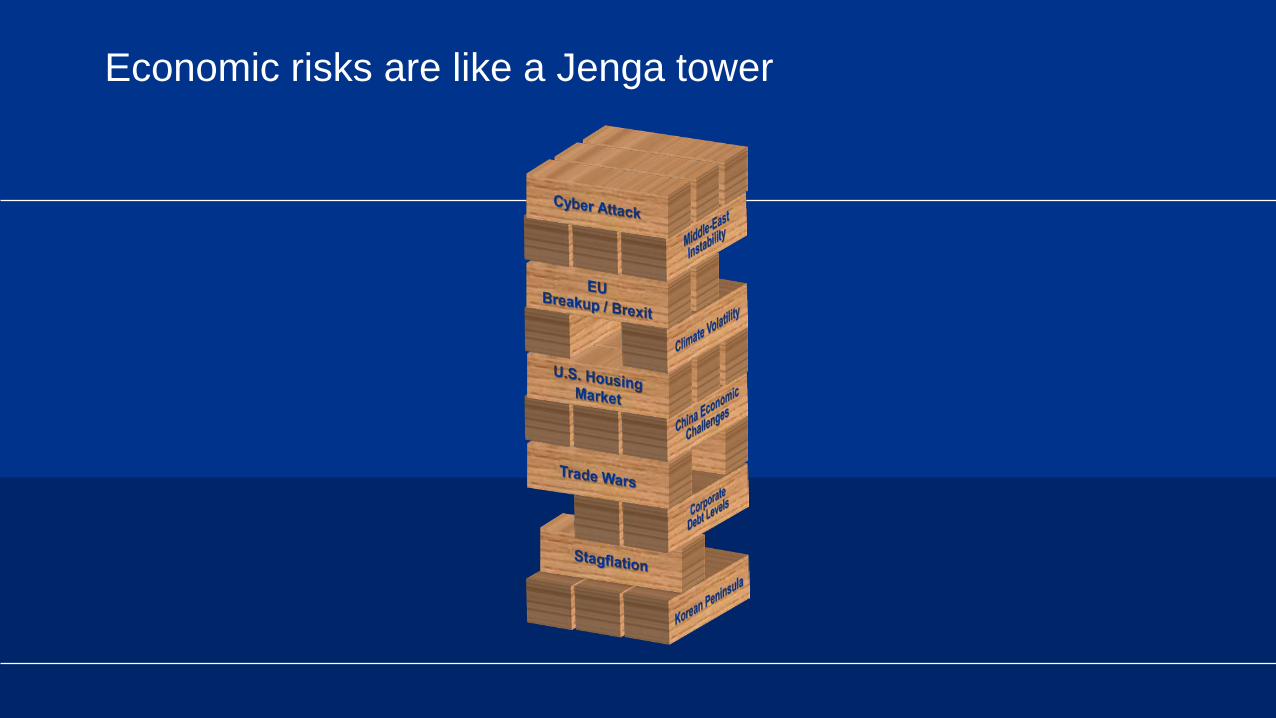

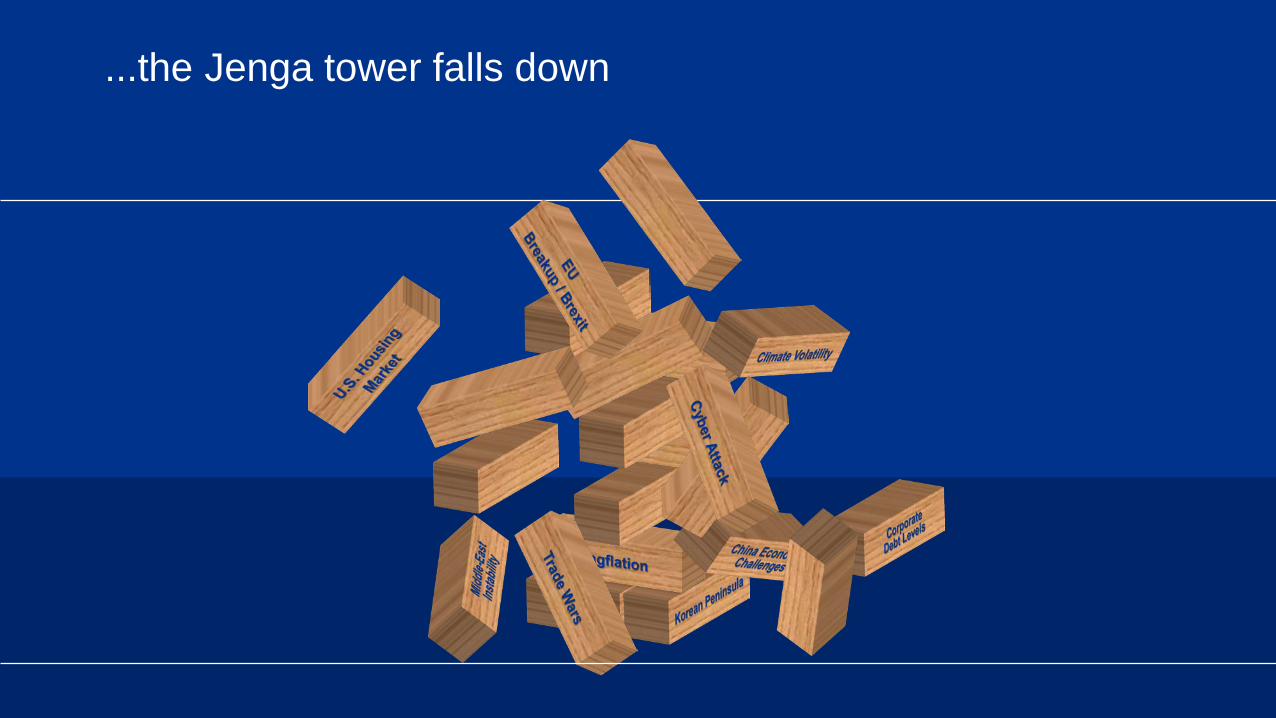

Economic risks are like a Jenga tower

18

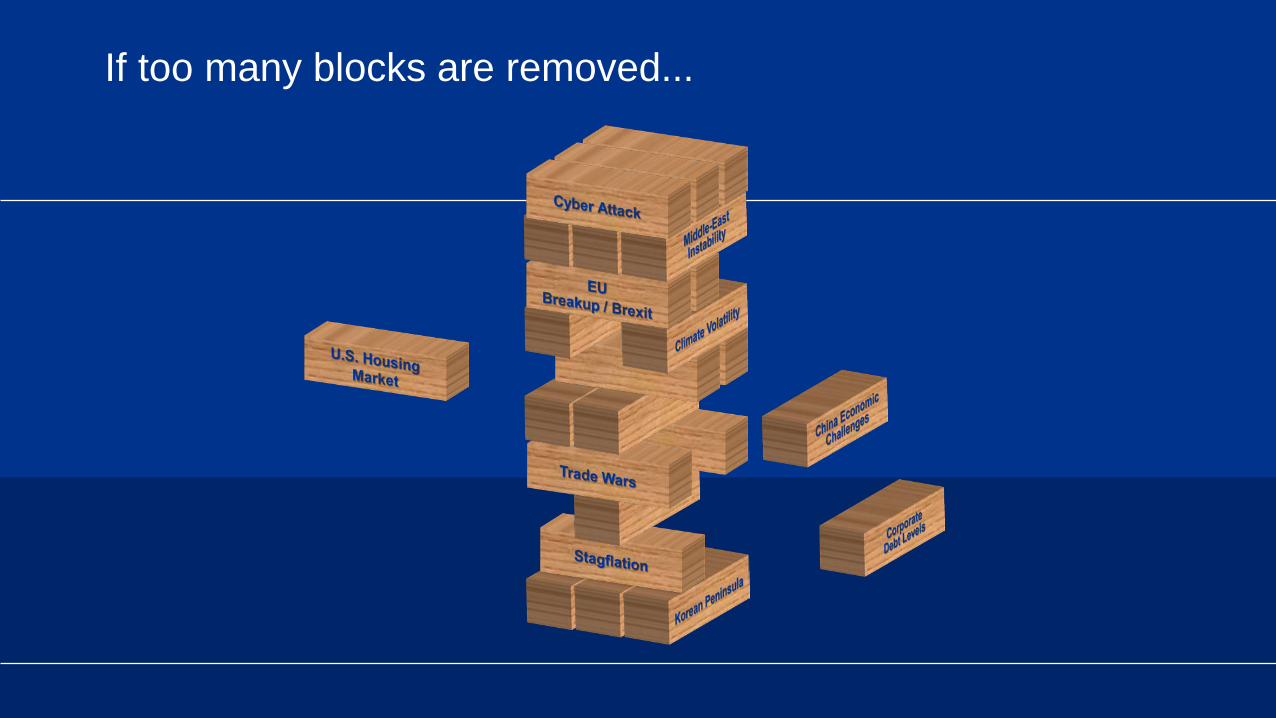

If too many blocks are removed...

19

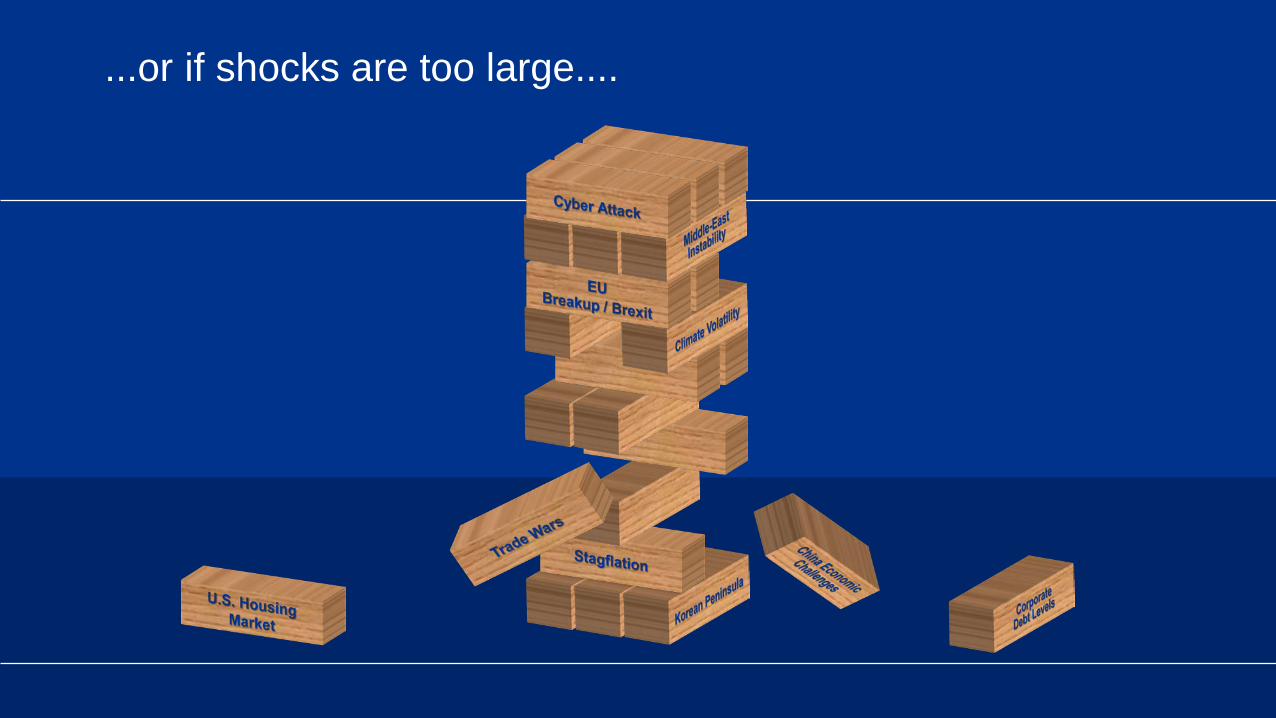

...or if shocks are too large....

20

...the Jenga tower falls down

21© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

-1

0

1

2

3

4

5

2016 2017 2018 2019 2020

%

Real GDP% Change, Annual Rate

Soft Landing Mild Recession

Historical Data Forecast

Near term growth outlook – a tale of two scenarios

Source: KPMG Economics, Macroeconomic Advisers by IHS (April 2019), BEA (Q1 2019)Note: Real GDP is GDP adjusted for inflation; Real GDP reported at a seasonally adjusted annualized rate

22© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Consumption can keep growing during normal recessions

Source: KPMG Economics, BEA (Q1 2019), Haver Analytics

23© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Consumption has changed with millennial influences

Source: KPMG Economics, BEA (Q1-2019), UN Population Statistics, Haver Analytics

24© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

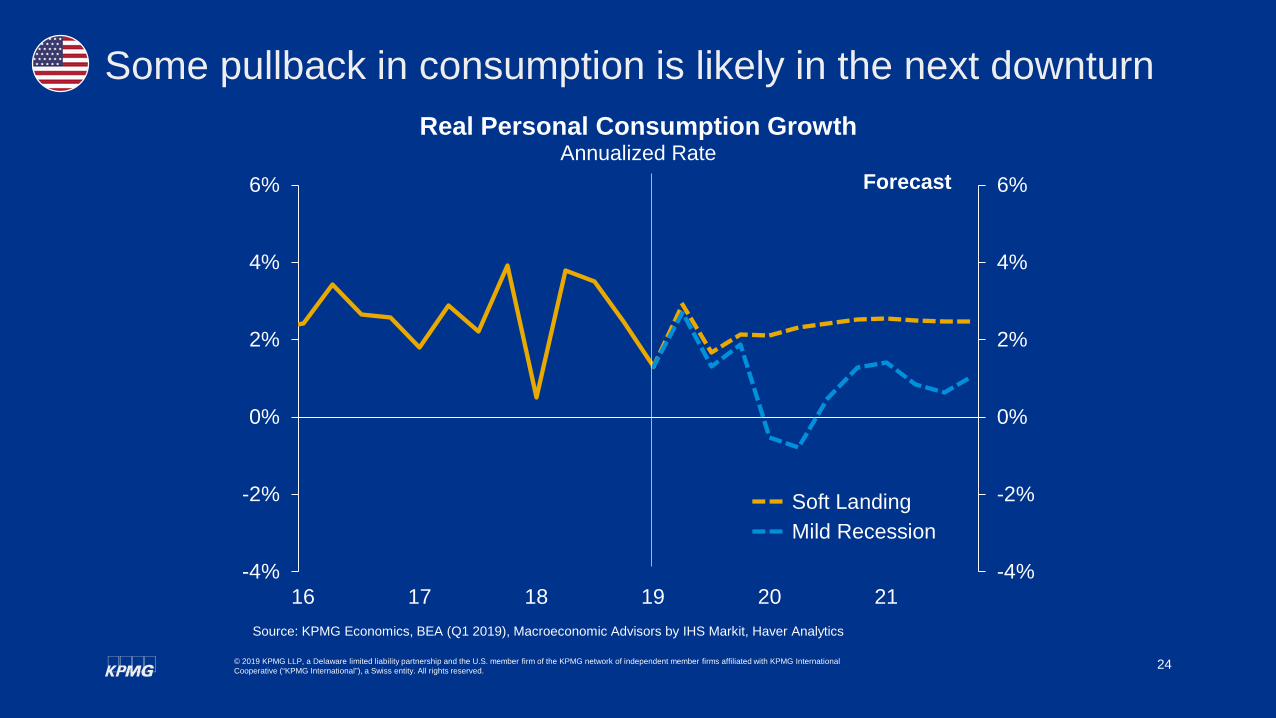

Some pullback in consumption is likely in the next downturn

-4%

-2%

0%

2%

4%

6%

-4%

-2%

0%

2%

4%

6%

16 17 18 19 20 21

Real Personal Consumption GrowthAnnualized Rate

Soft LandingMild Recession

Forecast

Source: KPMG Economics, BEA (Q1 2019), Macroeconomic Advisors by IHS Markit, Haver Analytics

25© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

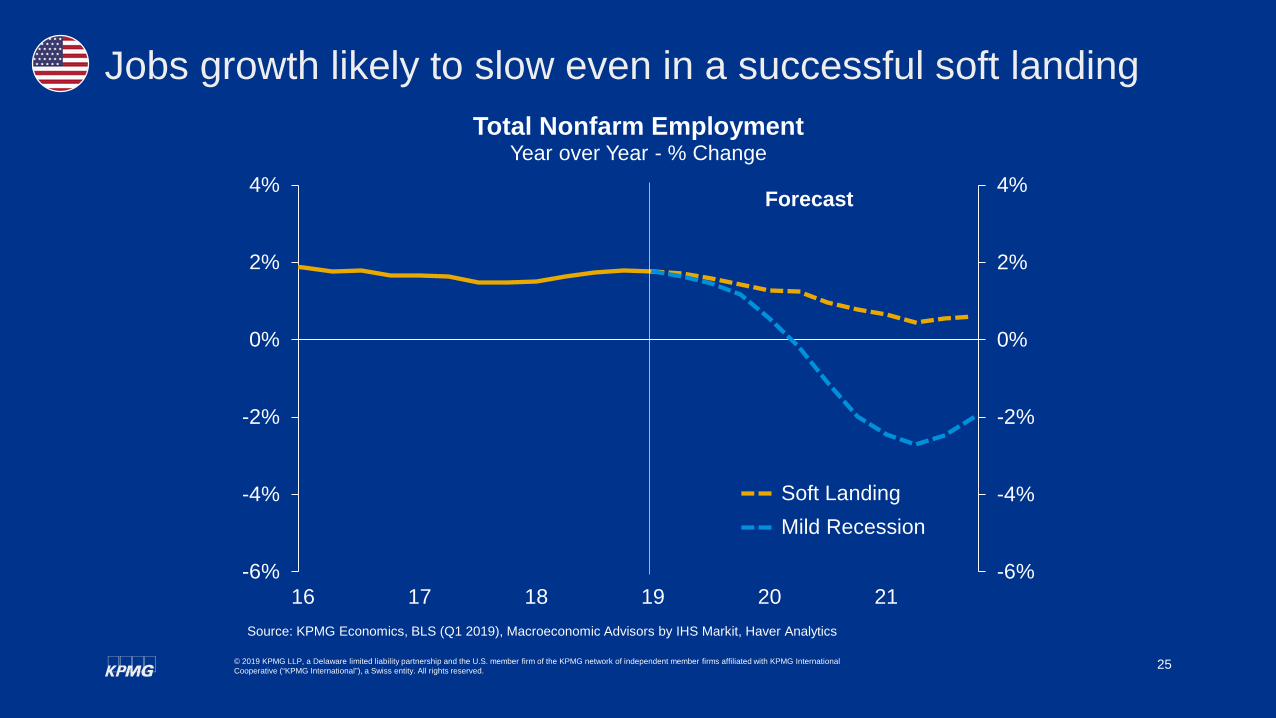

Jobs growth likely to slow even in a successful soft landing

-6%

-4%

-2%

0%

2%

4%

-6%

-4%

-2%

0%

2%

4%

16 17 18 19 20 21

Total Nonfarm EmploymentYear over Year - % Change

Soft LandingMild Recession

Forecast

Source: KPMG Economics, BLS (Q1 2019), Macroeconomic Advisors by IHS Markit, Haver Analytics

26© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• A slowdown in growth is likely even with a soft landing

• A normal business cycle recession is not as severe as 2008/2009

• A dip in consumption is to be expected

• A decline in jobs growth will impact the insurance industry

• Rates are unlikely to rise until after the trough of the next recession

Concluding Thoughts

Thank you

© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia

Some or all of the services described herein may not be permissible for KPMG audit clients and their affiliates.