global economic outlook - finance.si -

TRANSCRIPT

GLOBAL ECONOMIC OUTLOOK

GRZEGORZ SIELEWICZEconomist Central & Eastern Europe

Country Risk Conference

Ljubljana, 5th June 2019

INDUSTRY IN THE EUROZONE: THE END OF A VERY LONG EXPANSION CYCLE

COFACE, THE MOST AGILE GLOBAL TRADE CREDIT PARTNER IN THE INDUSTRY2

Euro Area: Industrial Production(3 month moving average, year-over-year change in percent)

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

growth period industrial production

60 months22

months56

months27

months30

months25

months

Source: Eurostat, Datastream, Coface

GLOOMY OUTLOOK IN BUSINESS SURVEYS

COFACE, THE MOST AGILE GLOBAL TRADE CREDIT PARTNER IN THE INDUSTRY3

Business confidence (Manufacturing Purchasing Manager Index in points)

Source: Markit

COFACE. THE MOST AGILE GLOBAL TRADE CREDIT PARTNER IN THE INDUSTRY4

UK: POLITICAL UNCERTAINTIES AFFECT BUSINESSES

19,485

17,709

16,293

14,58814,716 14,631

16,090

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

2012 2013 2014 2015 2016 2017 2018

Company insolvencies

Underlying company insolvencies

Growth (rhs)

Source: Insolvency Service's National Statistics

-2%

1%

9%

12%

18%

24%

10%

-5% 0% 5% 10% 15% 20% 25% 30%

Manufacturing

ICT

Retail trade

Construction

Food services

Personal services (excl. foodservices)

Total insolvencies

Growth in insolvencies in 2018

Source: Insolvency Service's National Statistics

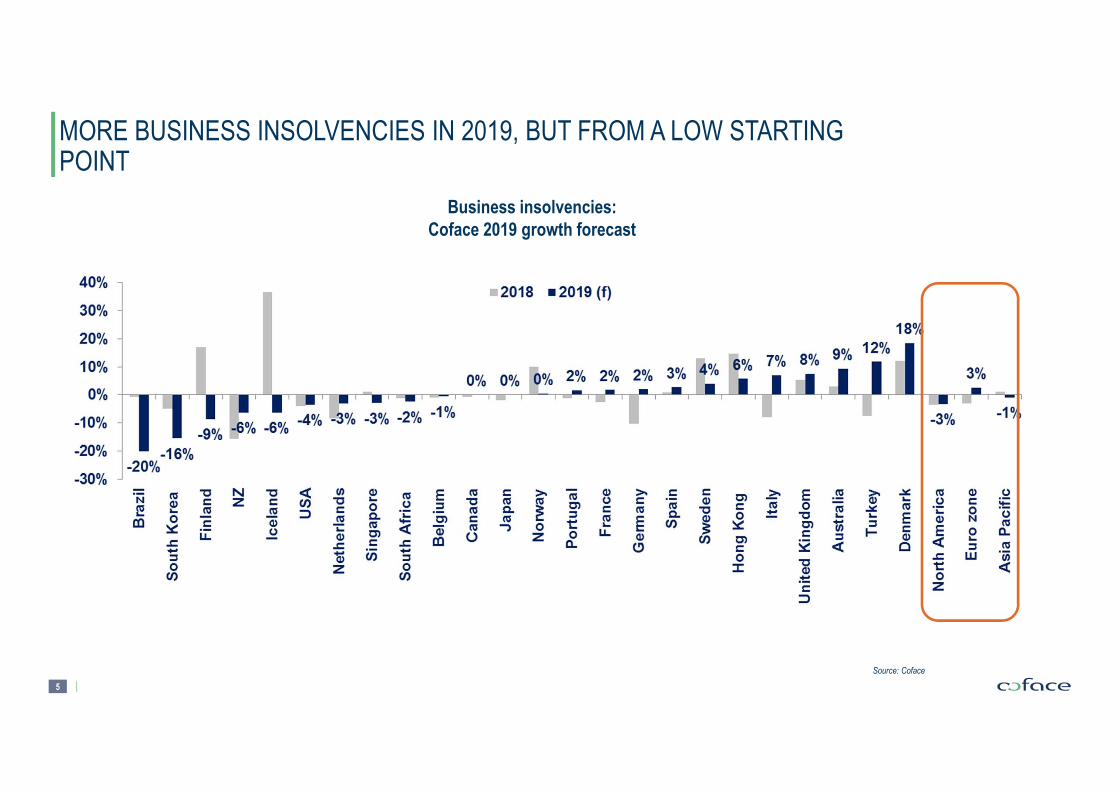

5

MORE BUSINESS INSOLVENCIES IN 2019, BUT FROM A LOW STARTING POINT

Business insolvencies:

Coface 2019 growth forecast

Source: Coface

6

UNITED STATES: BUSINESS INVESTMENT WILL SLOW DOWN IN A LESS FAVOURABLE FISCAL AND EXTERNAL ENVIRONMENT

43

45

47

49

51

53

55

57

59

61

63

65

67

69

2016 2017 2018 2019

ISM Manufacturing PMI

New orders New export orders Manufacturing PMI

Source: ISM

2.2%

1.8%

2.5%

2.9%

1.4%

2.2%

2.9%

2.5%

-2%

-1%

0%

1%

2%

3%

4%

2012 2013 2014 2015 2016 2017 2018 2019f

Contribution to GDP growth

Household consumption Government spending

GFCG Net exports

Inventories GDP

Sources: BEA,Coface forecast

7

PROTECTIONISM AND THE INDUSTRY CYCLE BOTH CAUSE GLOBAL TRADE DOWNTURN

Emerging markets: GDP growth tracker

(quarter on quarter SAAR, %)

World trade

(year on year % change)

Sources: IIF, Coface

f: forecast

Source: Coface

-8

-6

-4

-2

0

2

4

6

8

10

12

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

COFACE, THE MOST AGILE GLOBAL TRADE CREDIT PARTNER IN THE INDUSTRY8

EMERGING MARKETS – RISK #1: RISING CORPORATE CREDIT RISK IN CHINA

Coface’s Corporate Payment Survey:

China’s GDP growth will increase in 2019

China: Coface Corporate Payment Survey

(credit terms, number of days)

Sources: Bloomberg, Coface Source: Coface

60

55

5957 56

68

76

86

40

60

80

100

2011 2012 2013 2014 2015 2016 2017 2018

COFACE, THE MOST AGILE GLOBAL TRADE CREDIT PARTNER IN THE INDUSTRY9

EMERGING MARKETS – RISK #2: CAPITAL FLOWS AND EXTERNAL VULNERABILITY

-30

-20

-10

0

10

20

30

40

50

60

70

01/0

1/15

01/0

1/16

01/0

1/17

01/0

1/18

01/0

1/19

Net non-resident purchases of EM stocks and bonds (in USD bn, source: IIF)

Local currency versus USD (YTD in %, 17 May 2019, source: Reuters)

COFACE, THE MOST AGILE GLOBAL TRADE CREDIT PARTNER IN THE INDUSTRY10

EMERGING MARKETS – RISK #3: OIL PRICES

157%

118%

9%

261%

114%

57%

154%

64%

125%

Angola Kuwait Nigeria SaudiArabia

UAE Russia OPEC Non-OPEC10

Total

Compliance to 2019 output deal(in % of pledged cut)

Source: OPEC, IEA, Coface

0,0

0,5

1,0

1,5

2,0

2,5

3,0

Mb/

d

OPEC: Unplanned production outages

Source: EIA

11

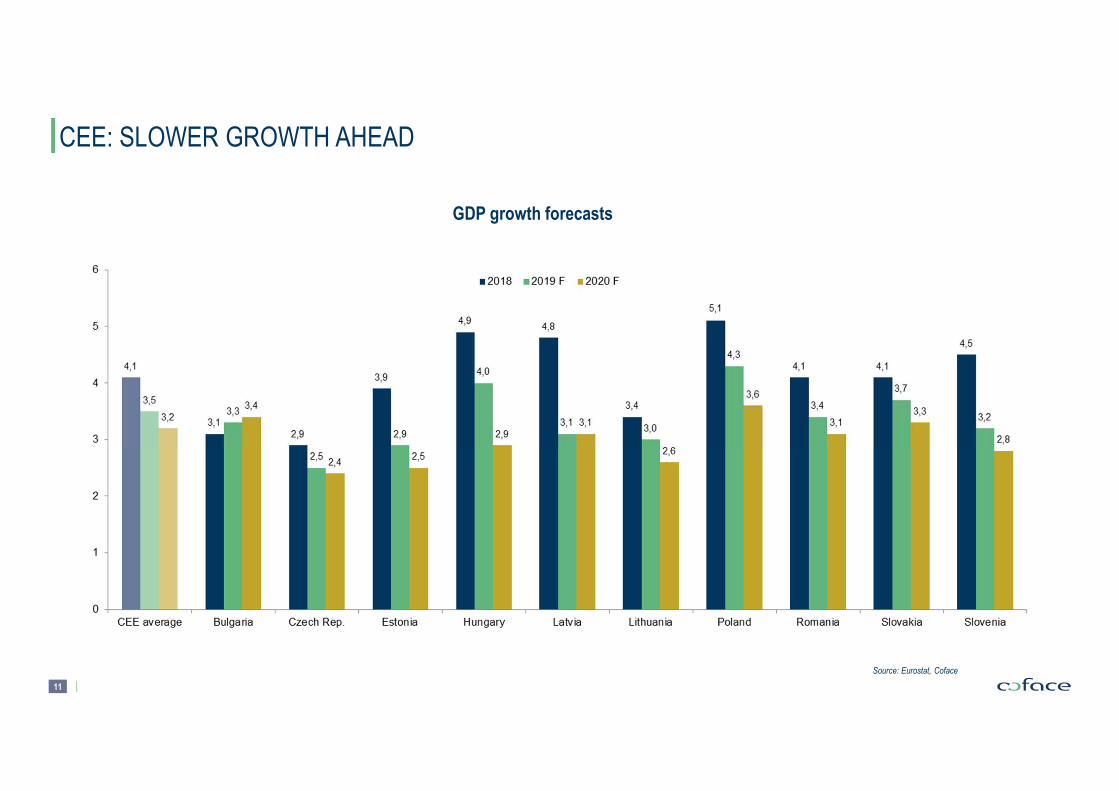

CEE: SLOWER GROWTH AHEAD

GDP growth forecasts

Source: Eurostat, Coface

12

CEE: HOUSEHOLD CONSUMPTION REMAINS GROWTH DRIVER

Source: Eurostat

Labour shortages as a factor

limiting the production (business survey)

Unemployment rate (%)

Source: Eurostat

13

WHO’S AFRAID OF GLOBAL SLOWDOWN?

Exports of goods and services as % of GDP (%, 2018)

Source: Eurostat

14

RUSSIA: WEAK ECONOMIC ACTIVITY

Source: Rostat

Industrial production (y/y changes)Dynamics of retail sales and disposable income

(%, y/y changes)

Source: Rostat

15

COFACE COUNTRY RISK ASSESSMENTS

16

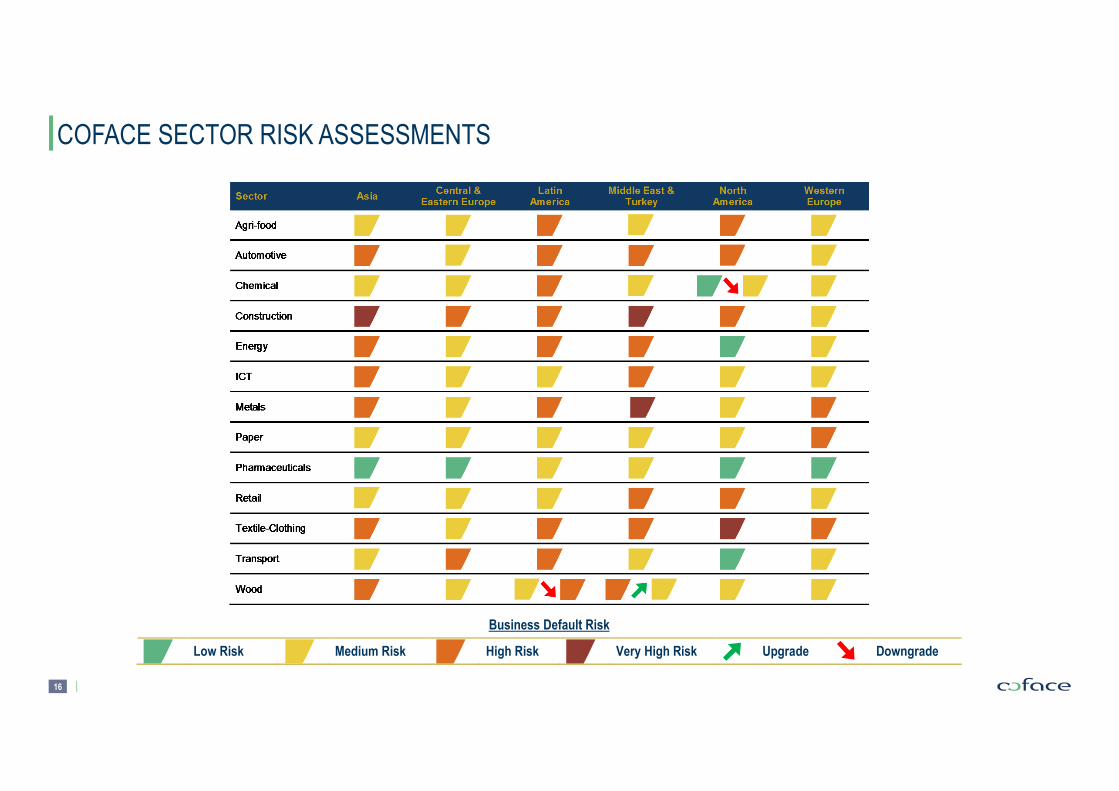

COFACE SECTOR RISK ASSESSMENTS

Low Risk

Medium Risk

High Risk

Very High Risk

Upgrade

Downgrade

Business Default Risk