global commercial solutions cost segregation overview

TRANSCRIPT

GLOBAL Commercial Solutions Cost Segregation Overview

Cost SegregationCost Segregation

How Does It Work?

What’s Your Benefit?

What Is It?

The IRS approved method for accelerating building depreciation for Commercial and Residential Rental properties. It is a detailed process which includes identifying the building components that should be properly classified as tangible personal property or land improvements, rather than real property that is depreciated over 39 years (or 27.5 for Residential Rental).

Cost Segregation Is:

What is Cost Segregation?

The US Treasury Department States:

“Cost Segregation is a lucrative tax strategy that

should be used in almost every major

purchase of Commercial Real Estate.”

Wall Street Journal – June‚2003

• A cost segregation study is an in-depth analysis of the cost incurred to build, acquire or renovate a real estate holding.

• The primary goal is to identify all construction related costs that qualify for accelerated income tax depreciation.

• A true engineering based cost segregation study will identify and assign costs to all building components including those in the 39 year depreciation category.

Cost Segregation Defined:

Why Use Cost Segregation?• Taxes are one of the largest expenses for commercial

property owners.

• Significant federal income tax benefits can be derived from utilizing shorter recovery periods.

• Engineering-based cost segregation studies allow commercial real estate owners to take what would otherwise be classified as 1250 property for depreciation purposes and reclassify it as more rapidly depreciating 1245 property.

• This reclassification results in substantial cash flow benefits in both current and future years through substantially shorter depreciable tax lives and accelerated depreciation methods.

Standard Depreciation• Traditionally, a building’s actual cost is

divided between land and building. For example:

– 20% to Land (which is Non Depreciable) and

– 80% to Building

• The 80% allocated to the building is then typically depreciated using 39 year straight line depreciation.

Accelerated Depreciation

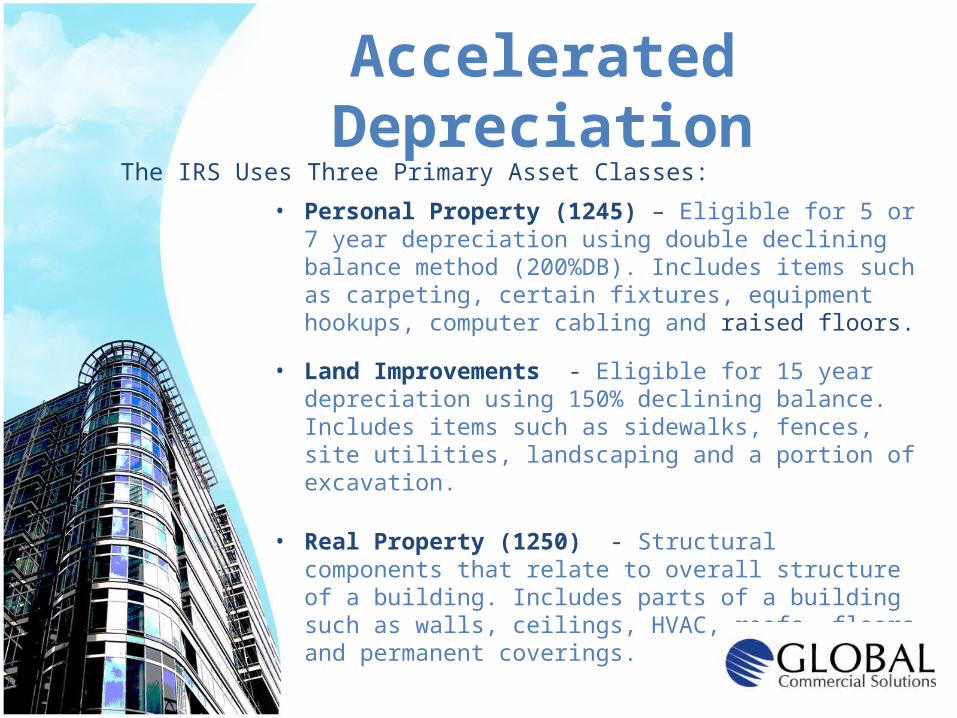

• Personal Property (1245) – Eligible for 5 or 7 year depreciation using double declining balance method (200%DB). Includes items such as carpeting, certain fixtures, equipment hookups, computer cabling and raised floors.

• Land Improvements - Eligible for 15 year depreciation using 150% declining balance. Includes items such as sidewalks, fences, site utilities, landscaping and a portion of excavation.

• Real Property (1250) - Structural components that relate to overall structure of a building. Includes parts of a building such as walls, ceilings, HVAC, roofs, floors and permanent coverings.

The IRS Uses Three Primary Asset Classes:

Typically, only 3% of a buildings cost is classified to reap the

greatest tax benefit.

Assets such as furniture, fixtures, and equipmenthave properly been classified and claimed as

“personal property”.

The remainder of the building is assigned a depreciable life of 39 years.

(27.5 Years for residential rental property)

Cost Segregation Breakdown

Before

Cost Seg

After

39 years*

5 Years

7 Years

15 years

39 years*

* 39 Years for Commercial Property and/or 27.5 Years for Residential Rental Property

S1245Personal Property

200%DBDouble Declining Balance Method

Land Improvements

150% DB

S1250 Real Property

Straight Line

Class

Segregate

Types of Components We Segregate and Reclassify In Our Studies: Communication Systems Computer Data / Power Data Outlets Electrical Outlets Distribution Wiring Distribution Panels High Voltage Switchgear Emergency Power Supply / Exhaust Systems Removable HVAC

Systems Specialized Fire

Protection Specialized Air Filtration Humidity / Temp. Control Security Access & -

Monitoring Systems Audio / Visual Systems Communications

Conduit / Wiring to Special Systems

Demountable Power Systems

Specialty Gas / Compressed Air Systems

Millwork Floor Coverings Window Treatments Wall Coverings Demountable Walls Decorative Lighting Signage Sidewalk & Curbing Parking Lots & Curbing Site Utilities Sewer & Drainage Landscaping Site Lighting

““Our engineers look beyond the obvious Our engineers look beyond the obvious items and evaluate every single key items and evaluate every single key component associated with a property.”component associated with a property.”

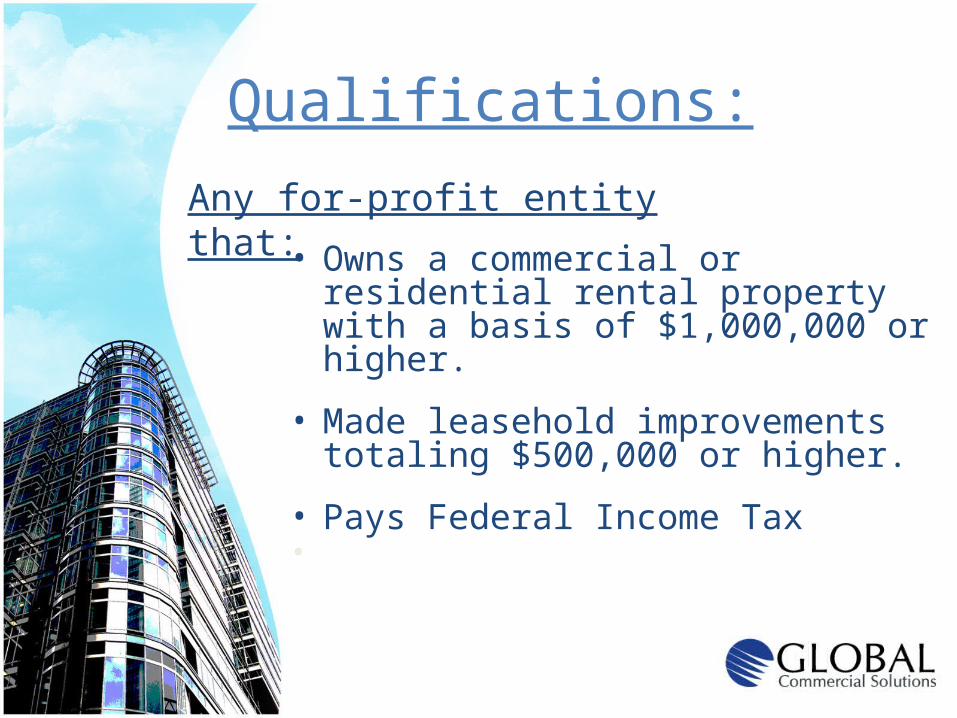

• Owns a commercial or residential rental property with a basis of $1,000,000 or higher.

• Made leasehold improvements totaling $500,000 or higher.

• Pays Federal Income Tax•

Qualifications:

Any for-profit entity that:

Properties That Qualify• Existing property acquired after 1986.• New Construction or Future

Construction.• Existing buildings undergoing

renovations or expansion.• Leasehold Improvements, both past

and future.• Commercial Property about to be

acquired.

• We provide a free Cost-Benefit Analysis for each and every property.

• In the analysis we will provide our flat fee to complete the study along with a conservative estimate of benefits.

• This provides the owner the ability to make an educated decision whether or not to go forward with the study based upon the anticipated return on investment.

We Provide Free Property Evaluations

Service Highlights

• Our studies are conducted using a Unique Detailed Engineering Approach. Our Engineers visit the site and assign both a depreciable life and a project cost to every asset in a property. All short life items, as well as all 39 year assets are accounted for. Our study allows the property owner to realize the greatest tax benefit from a front loaded depreciation schedule while keeping within all guidelines required by the IRS.

Service Highlights

Our Studies Are Different

Most providers of cost segregation do not provide the detail necessary to retire long life s1250 – “Real Property”. This often results in a property having “Ghost” assets on the depreciation schedule.

Our studies allow the property owner to write off long life assets in the years following the study.

– For example: If a roof needs to be replaced ten years after the property is placed in service, the owner can write off the remaining depreciable balance of that roof all in one year.

This can amount to hundreds of thousands of dollars in tax benefits.

Service Highlights

Retirement of Assets

Our comprehensive engineering studies maximize the benefit for our clients and contain all of the supporting documentation necessary to support our findings. Our final reports stand on their own.

In the event of an IRS Audit and/or if any questions or raised, we will defend our findings at no additional charge.

Service Highlights

We Will Support Our Findings

Contact Us Today for your Free Cost-Benefit Analysis!

Why provide the Federal Government with an Interest Free Loan for the remaining 39 years of your buildings’ depreciable life?

OROR

YourselfYourselfIRSIRS

Who would you rather pay?