getting more ethanol to consumers

TRANSCRIPT

Getting More Ethanol to

Consumers

Kennedy & Coe Ethanol Summit

2014

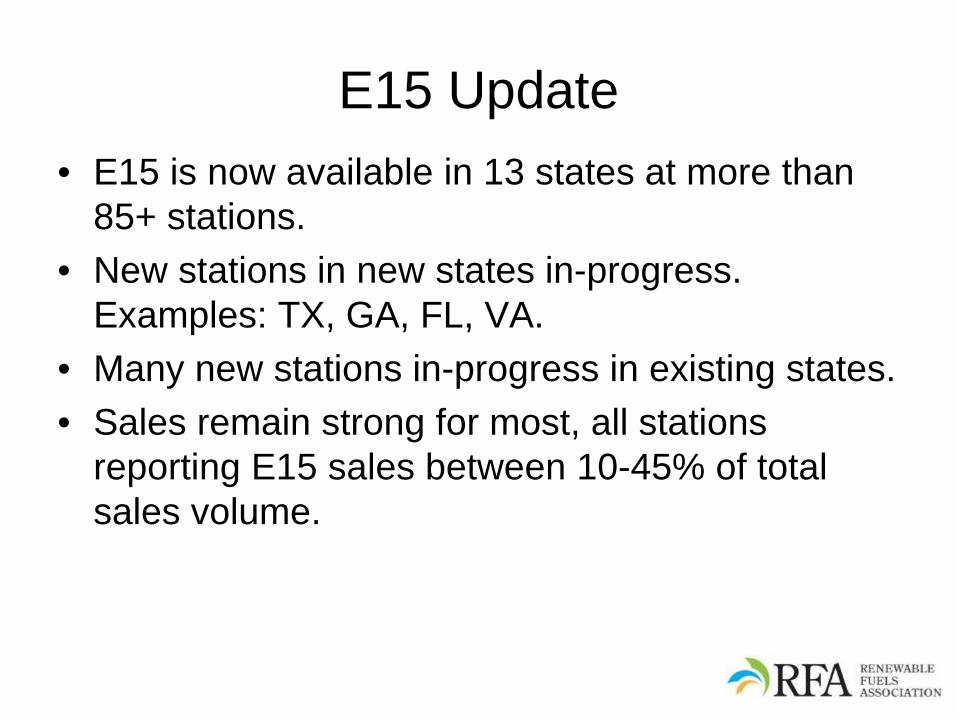

E15 Update • E15 is now available in 13 states at more than

85+ stations. • New stations in new states in-progress.

Examples: TX, GA, FL, VA. • Many new stations in-progress in existing states. • Sales remain strong for most, all stations

reporting E15 sales between 10-45% of total sales volume.

E15 Update • Continuing to explore options in RFG markets.

Know of companies in those areas exploring equipment options.

• Conversations continue with all retailers across the country that will listen.

• Terminals looking at offering blended E15 – until terminals start offering, can’t do E15 w/o E85.

• Prime the Pump. • Chicago E15 Mandate. • Summer volatility season remains biggest hurdle

– presses importance of RFG markets.

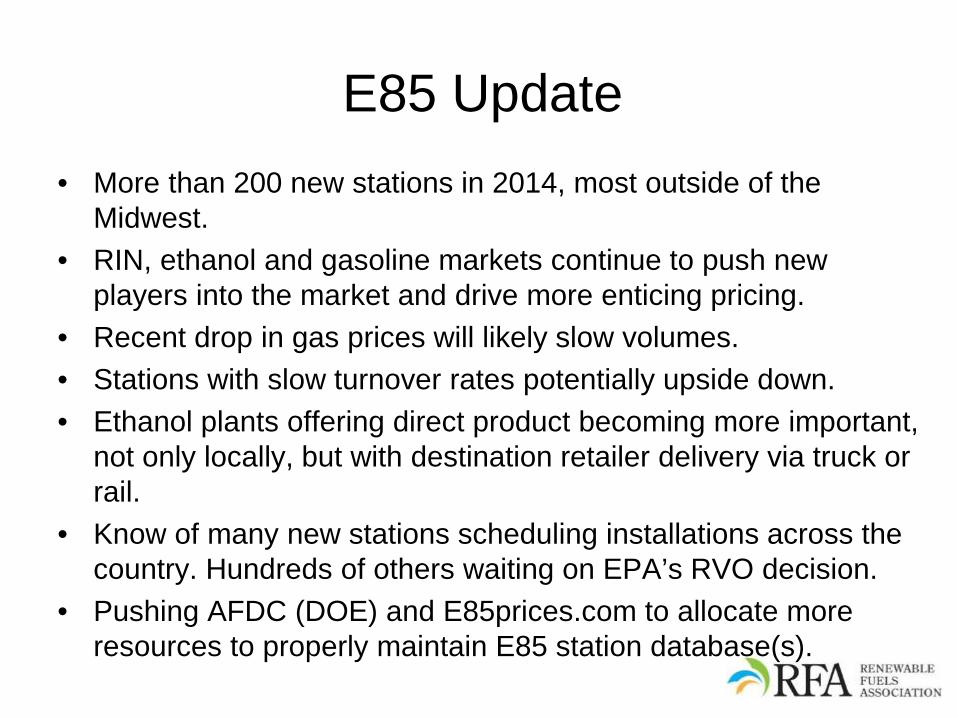

E85 Update • More than 200 new stations in 2014, most outside of the

Midwest. • RIN, ethanol and gasoline markets continue to push new

players into the market and drive more enticing pricing. • Recent drop in gas prices will likely slow volumes. • Stations with slow turnover rates potentially upside down. • Ethanol plants offering direct product becoming more important,

not only locally, but with destination retailer delivery via truck or rail.

• Know of many new stations scheduling installations across the country. Hundreds of others waiting on EPA’s RVO decision.

• Pushing AFDC (DOE) and E85prices.com to allocate more resources to properly maintain E85 station database(s).

E85 Pricing

• Both pictures taken Saturday, December 6th. • Left: E85 $.50/gal more; Right: $1/gal less.

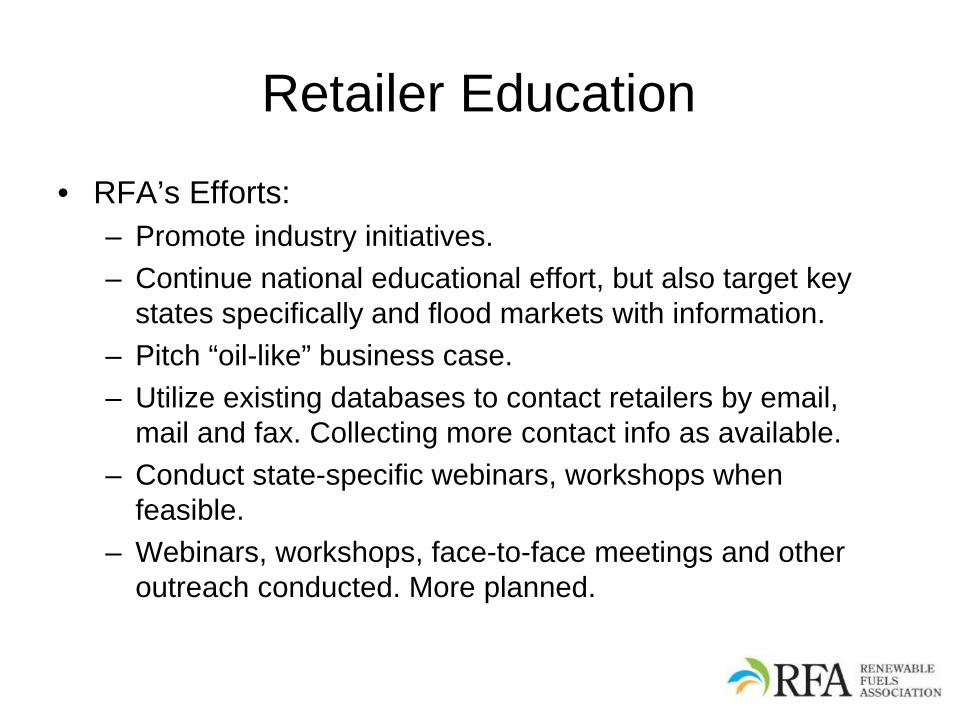

Retailer Education

• RFA’s Efforts: – Promote industry initiatives. – Continue national educational effort, but also target key

states specifically and flood markets with information. – Pitch “oil-like” business case. – Utilize existing databases to contact retailers by email,

mail and fax. Collecting more contact info as available. – Conduct state-specific webinars, workshops when

feasible. – Webinars, workshops, face-to-face meetings and other

outreach conducted. More planned.

Retailer Education

• Fuel retailers compete on RUL, which is 87.2% of their business.

• Premium sales are between 1.5-5%. Keep in mind how much of this is midgrade.

• Now more vehicles have favorable E15 language & warranty than FFVs for E85 or vehicles that require premium!

• Need all of ethanol industry to help push their local retailers to explore options.

BYO Ethanol Campaign

• Extend key elements of program for next 3 years: – Continue hosting webinars and educational

seminars/workshops. – Maintain website: www.BYOethanol.com. – Attend and exhibit at “Top 5” petroleum marketer events.

• Fund infrastructure compatibility review to assist retailers and regulators for all E10+ blends. – Project underway, will be complete in less than 4 months. – Includes compatibility review of Chicago stations for E15 mandate

discussion.

• Fund infrastructure. – Funding effort in KS to collect data for business case. – Stations “in the works” in outside of Midwest.

Dispenser News

• EMV changes coming soon, dispensers must be compatible by 2017, or retailers accept liability for fraudulent transactions.

• UL is dragging their feet on elimination of 87 listing protocol, which would eliminate E10 only dispensers.

• Wayne made announcement at end of July that one of their most popular dispensers, the Ovation 2, will be E25 compatible, eliminating E10 only option.

• Gilbarco discussing similar options. • Efforts underway to determine cost to switch early. But,

doesn’t guarantee E10+ blends are sold, just that infrastructure is there.

Infrastructure Funding Efforts

• Prime the Pump. • Other industry initiatives. • State Incentives:

– Tax Credits. – Grant Programs. – Motor Fuels Tax Rates.

• Local Incentives: – Gilbarco/Corn Growers. – American Lung Association. – Individual Ethanol Plants. – State Corn Growers. – Clean Cities Coalitions. – MN E15 Coalition.

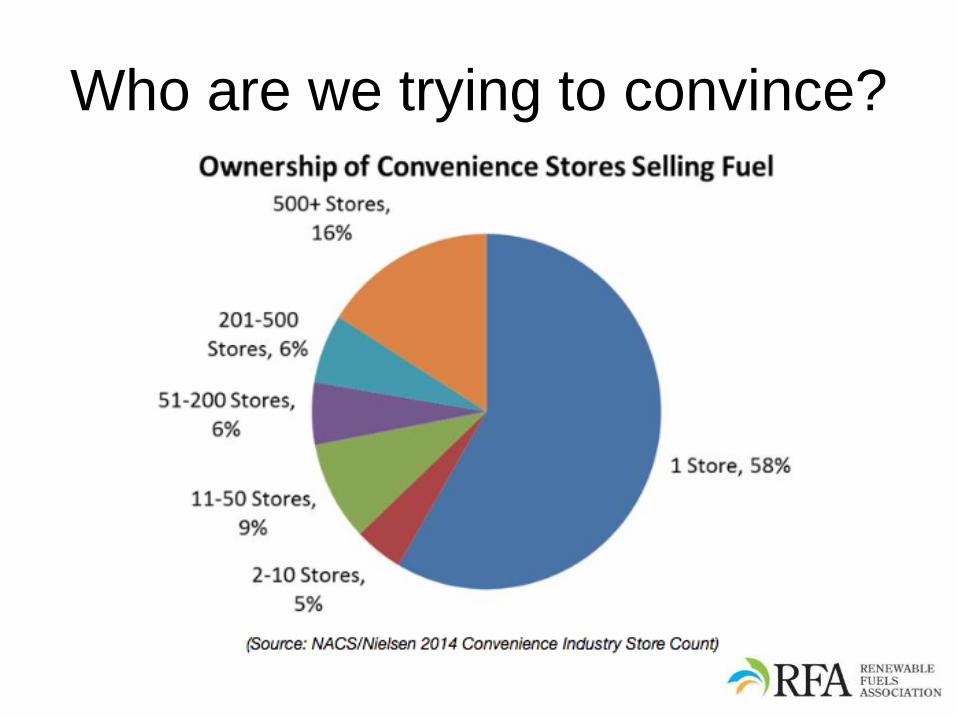

Who are we trying to convince?

Why does that matter?

• The typical station owner today doesn’t have deep pockets.

• Investment is typically focused elsewhere on higher margin items (think coffee, etc.).

• Belief in need of franchises remains high with the “I don’t want to worry about that” mentality.

• If you want to push infrastructure, we will need to invest.

Big Oil Influence

• Top 5 oil companies now own just 424 stations.

• Top 5 oil companies control 47,928 stations OR 31% of all stations.

• Major refiner-branded outlets total 29,938 OR 19% of all stations.

• Combined 50% of all stations.

Why Big Oil Influence Matters?

• Control the decisions. • Control the fuel supply. • Control the dispensers purchased. • …all while having zero liability.

Contractual Terms

• Length. • Volume Requirements. • Image Requirements. • Wholesale Price Requirements.

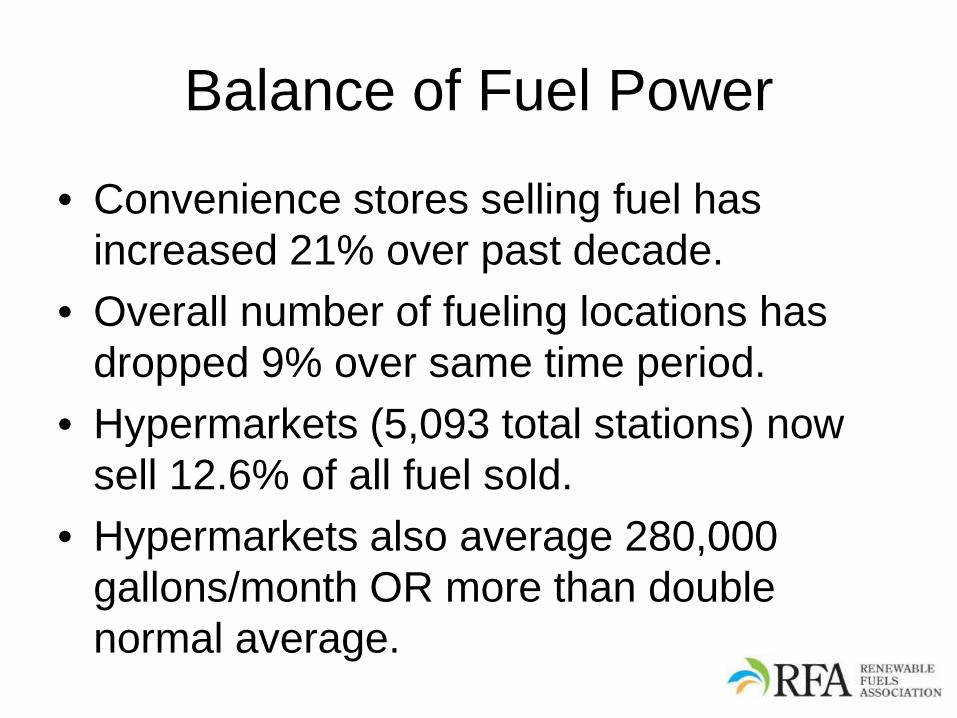

Balance of Fuel Power

• Convenience stores selling fuel has increased 21% over past decade.

• Overall number of fueling locations has dropped 9% over same time period.

• Hypermarkets (5,093 total stations) now sell 12.6% of all fuel sold.

• Hypermarkets also average 280,000 gallons/month OR more than double normal average.

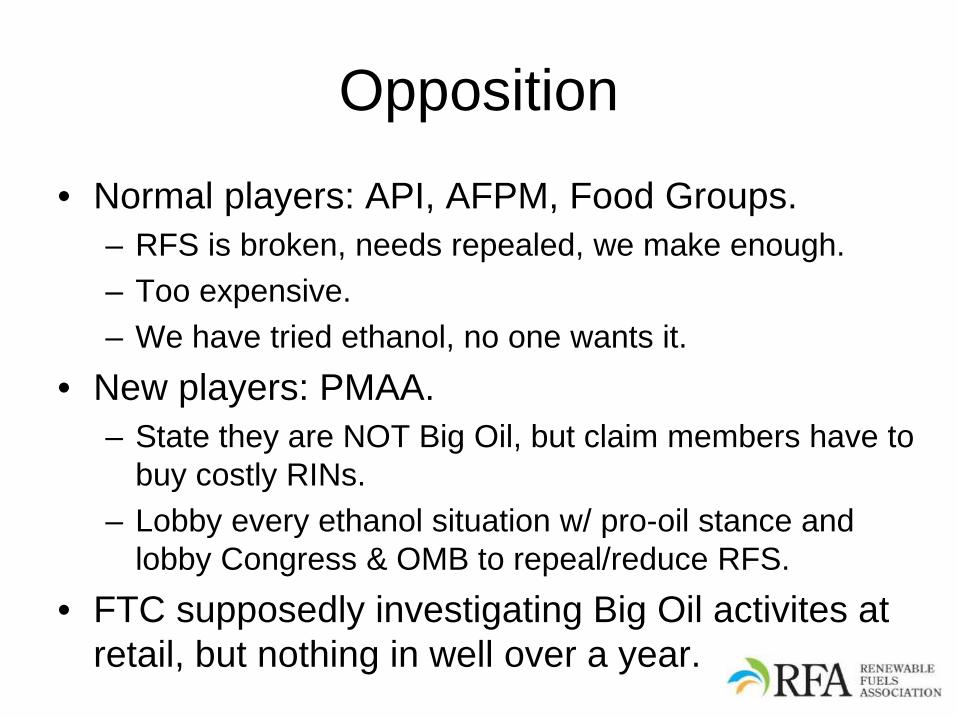

Opposition

• Normal players: API, AFPM, Food Groups. – RFS is broken, needs repealed, we make enough. – Too expensive. – We have tried ethanol, no one wants it.

• New players: PMAA. – State they are NOT Big Oil, but claim members have to

buy costly RINs. – Lobby every ethanol situation w/ pro-oil stance and

lobby Congress & OMB to repeal/reduce RFS. • FTC supposedly investigating Big Oil activites at

retail, but nothing in well over a year.

Consumers

• Want cheap fuel. • Interest in alternative fuel technology declines w/

gas prices. • Why do they consider alt fuel vehicles?

– 51% of consumers would consider an alternative vehicle to protect the environment .

– 45% to reduce American dependence on foreign oil. – 42% to reduce their carbon footprint. – 41% to increase their driving range. Source: NACS

Recent Example: Florida • New stations in Florida have been open ~10

days. • E15 is averaging ~17% of total volume. • E85 is averaging ~18% of total volume. • Proving once again, if priced as market allows,

ethanol-blended fuel will sell. • Stations have lowered their RUL competition to

65% from 87%.

Conclusion

• Multiple efforts will continue with same end game, we need more infrastructure to get our product to consumers.

• There are stations that can add E15 and E85 at a relatively low price point. RFA has hundreds at the ready, could be online in less than 6 months.

• Dispenser changes can lead to quicker adoption in the field.

• If part of the ethanol industry, find your preferred way to invest.

Questions?

Robert White, VP of Industry Relations Renewable Fuels Association (RFA)

425 Third St, SW, Suite 1150 Washington, DC 20024

(202) 289-3835 Twitter: @fuelinggood

www.ChooseEthanol.com www.BYOethanol.com www.EthanolRFA.org