getting more bang for your public investment buck - richard hugues, imf

TRANSCRIPT

Getting More Bank for Your Public Investment Buck: Outline of the Presentation

I. Public Investment and Infrastructure Quality

II. Estimating Public Investment Efficiency

III. Assessing Public Investment Management

IV. Explaining Public Investment Performance

V. Conclusions, Recommendations, and Next Steps

2

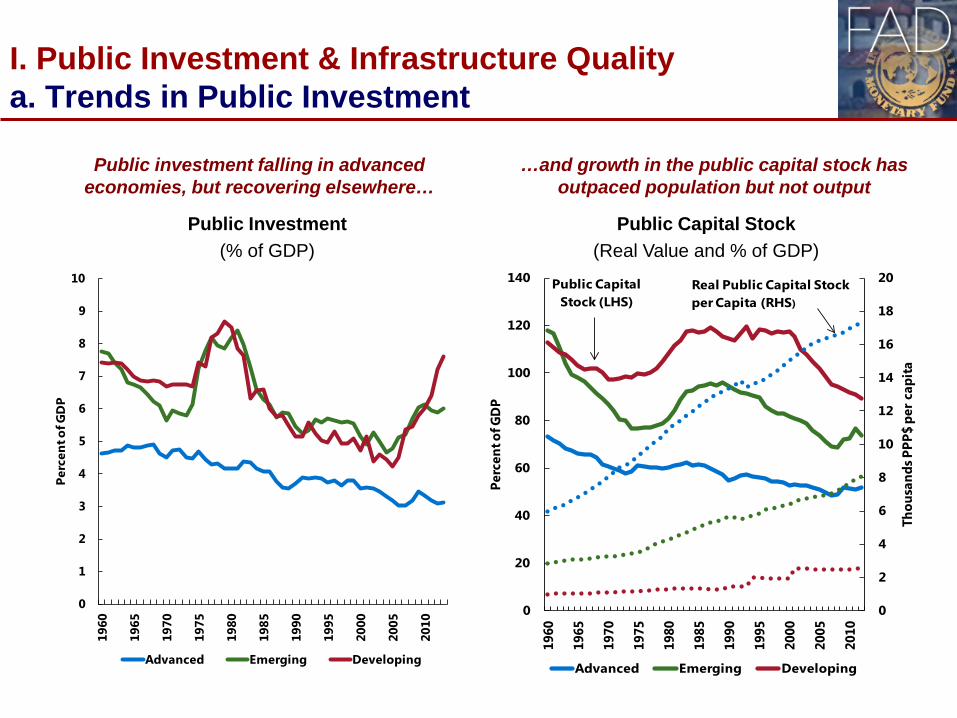

I. Public Investment & Infrastructure Quality a. Trends in Public Investment

Public investment falling in advanced economies, but recovering elsewhere…

…and growth in the public capital stock has outpaced population but not output

3

0

1

2

3

4

5

6

7

8

9

10

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Perc

ent o

f GD

P

Advanced Emerging Developing

Public Investment (% of GDP)

0

2

4

6

8

10

12

14

16

18

20

0

20

40

60

80

100

120

140

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Thou

sand

s PPP

$ pe

r cap

ita

Perc

ent o

f GD

P

Advanced Emerging Developing

Real Public Capital Stock per Capita (RHS)

Public Capital Stock (LHS)

Public Capital Stock (Real Value and % of GDP)

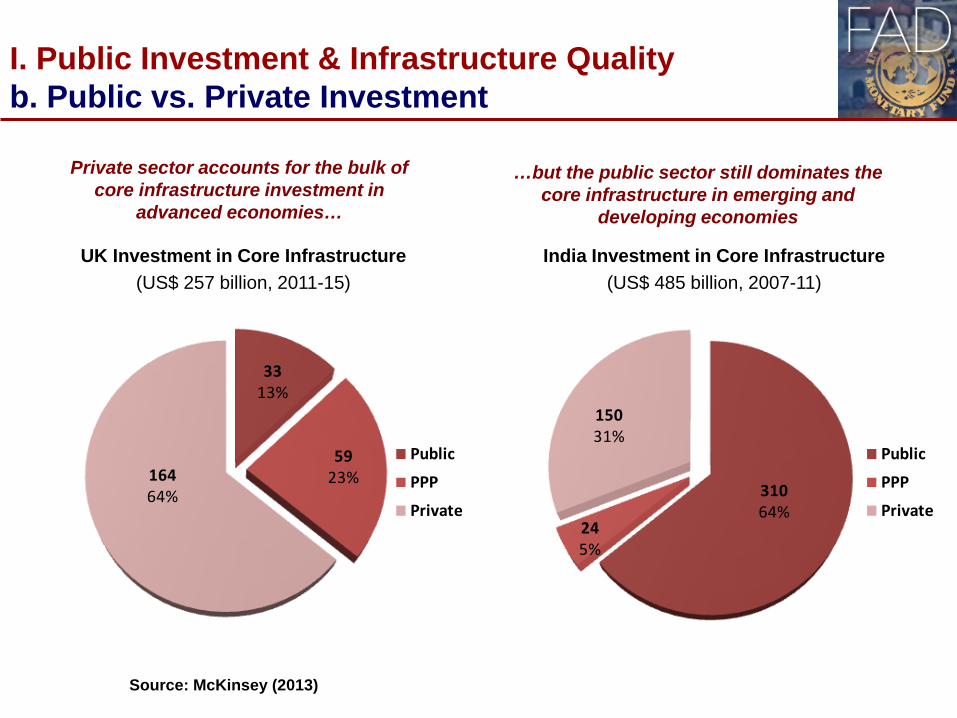

I. Public Investment & Infrastructure Quality b. Public vs. Private Investment

Private sector accounts for the bulk of core infrastructure investment in

advanced economies…

…but the public sector still dominates the core infrastructure in emerging and

developing economies

4

UK Investment in Core Infrastructure (US$ 257 billion, 2011-15)

3313%

5923%164

64%

Public

PPP

Private31064%

245%

15031%

Public

PPP

Private

India Investment in Core Infrastructure (US$ 485 billion, 2007-11)

Source: McKinsey (2013)

I. Public Investment & Infrastructure Quality c. Trends in Infrastructure Quality

Survey measures suggest some convergence in infrastructure quality

between rich & poor countries….

…but physical measures highlight the large and persistent disparities in infrastructure

access & quality between rich and poor

5

0

1

2

3

4

5

6

2006

2007

2008

2009

2010

2011

2012

2013

2014

AdvancedEmergingDeveloping

Perceptions of Infrastructure Quality (2006-14)

Measures of Infrastructure Access (Latest year)

0102030405060708090100

02468

1012141618

Road

s per

capi

ta

Publ

ic e

duca

tion

infr

astr

uctu

re

Publ

ic h

ealth

in

fras

truc

ture

Elec

tric

ity p

er

capi

ta

Acce

ss to

wat

er

(RHS

)

AdvancedEmergingDeveloping

II. Estimating Public Investment Efficiency a. Public Investment Efficiency Index

6

Sizeable public investment efficiency gaps both across and with different income groups

0

20

40

60

80

100

120

140

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

Phys

ical

infr

astr

uctu

re sc

ore

(100

=AE a

vera

ge)

Public capital stock per capita, PPP US$

Advanced Emerging Developing Frontier line

Public Capital Stock vs. Infrastructure Quality

0.0

0.2

0.4

0.6

0.8

1.0

Advanced Emerging Low-Income All Countries

Effic

ienc

y sc

ores

Average efficiency gap

of 40%

II. Estimating Public Investment Efficiency b. Public Investment Efficiency Gap

7

Variation in Public Investment Efficiency

Average country is 40% below efficiency frontier with largest efficiency gaps among low income countries

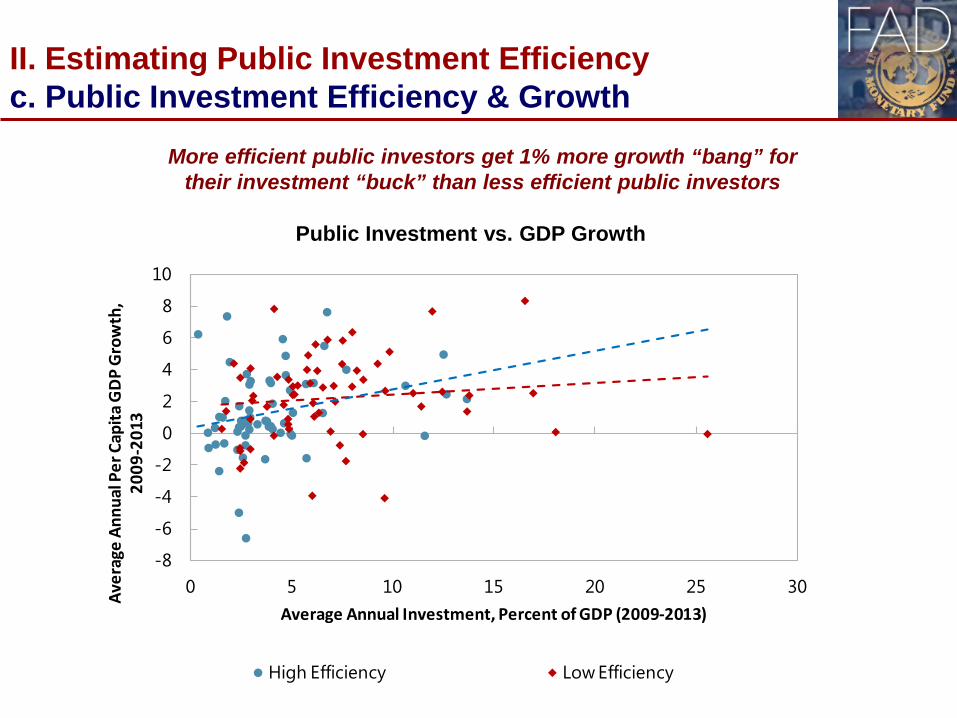

II. Estimating Public Investment Efficiency c. Public Investment Efficiency & Growth

8

-8

-6

-4

-2

0

2

4

6

8

10

0 5 10 15 20 25 30Aver

age

Annu

al P

er C

apita

GD

P G

row

th,

2009

-201

3

Average Annual Investment, Percent of GDP (2009-2013)

High Efficiency Low Efficiency

Public Investment vs. GDP Growth

More efficient public investors get 1% more growth “bang” for their investment “buck” than less efficient public investors

III. Evaluating Public Investment Management a. Public Investment Management Assessment (PIMA)

The PIMA Framework

9

Planning1. Fiscal rules2. National & Sectoral Plans3. Central-Local Coordination4. Management of PPPs5. Regulation of Infra. Corps.

Allocating6. Multi-year budgeting7. Budget Comprehensiveness8. Budget Unity9. Project Appraisal10. Project Selection

Implementing11. Protection of Investment12. Availability of Funding13. Transparency of Execution14. Project Management15. Monitoring of Assets

III. Evaluating Public Investment Management b. PIM Strengths and Weaknesses

10

PIMA Score by Institution

1. Fiscal rules2. Natl/Sectoral Planning

3. Central-Local Coord.

4. PPP

5. Infrastructure Company Regulation

6. Multi-year Budgeting

7. Budget Comprehensiveness8. Budget Unity9. Project Appraisal

10. Project Selection

11. Investment Protection

12. Funding Availability

13. Budget Execution Transparency

14. Mgmt. of Project Implementation

15. Monitoring of Public Assets

Advanced

Emerging

Developing 1 - 5: Planning

6 - 10: Allocating

1 - 5: Planning

6 - 10: Allocation

IV. Explaining Public Investment Performance a. Public Investment Efficiency & Productivity

Stronger PIM institutions associated with more efficient investment…

…and (more weakly) associated with more productive investment

11

PIMA Score vs. PI Efficiency PIMA Score vs. PICOR

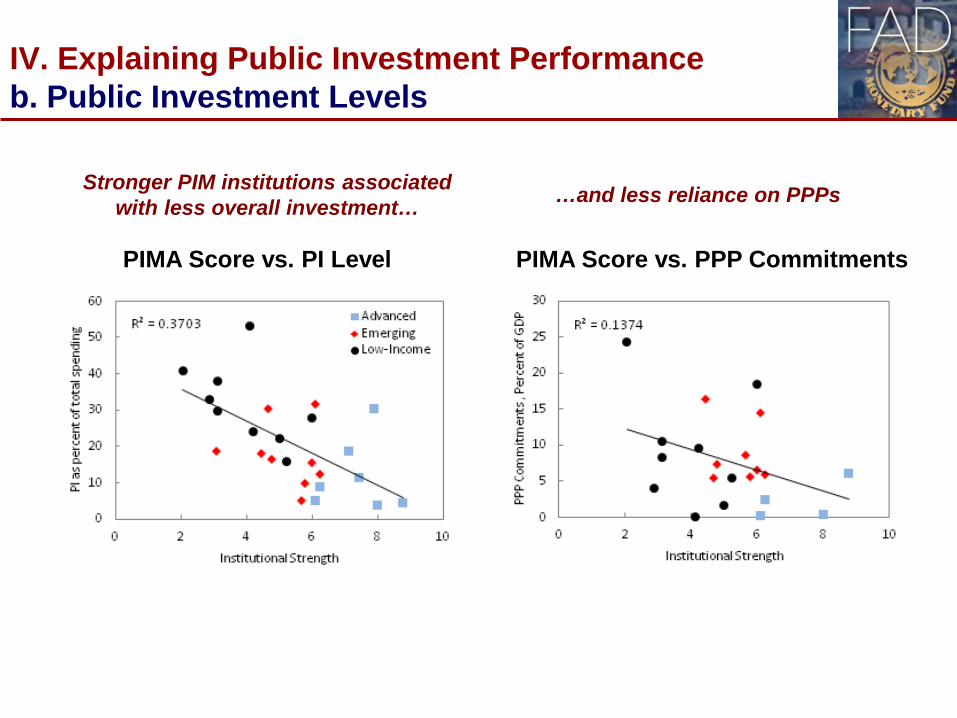

IV. Explaining Public Investment Performance b. Public Investment Levels

Stronger PIM institutions associated with less overall investment… …and less reliance on PPPs

12

PIMA Score vs. PI Level PIMA Score vs. PPP Commitments

IV. Explaining Public Investment Performance c. Public Investment Stability

Stronger PIM institutions associated with more stable levels of investment…

…and more stability in the allocation of investment between sectors

13

PIMA Score vs. Overall PI Volatility

0

5

10

15

20

25

30

35

40

45

0 2 4 6 8 10

Vola

tility

Institutional Strength

Correlation Coef: -0.59

0

1

2

3

4

5

6

7

0 2 4 6 8 10

Chur

n

Institutional Strength

Correlation Coef: -0.57

PIMA Score vs. PI “Churn”

Advanced Emerging

Low Income

IV. Explaining Public Investment Performance c. Public Investment Execution

Stronger PIM institutions associated with more credible capital budgets…

…and lower perceptions of government corruption.

14

0

10

20

30

40

50

60

70

80

90

0 2 4 6 8 10

Impl

emen

tatio

n

Institutional Strength

Correlation Coef: -0.53

0

1

2

3

4

5

6

0 2 4 6 8 10

ICRG

Inte

grity

Sco

re

Institutional Strength

Correlation Coef: 0.60

PIMA Score vs. PI Over/Under Execution PIMA Score vs. Government Integrity

Advanced Emerging

Low Income

V. Conclusions, Recommendations, and Next Steps: a. Preliminary Conclusions

1. Scope to improve public investment efficiency by 40 percent on average across 25 sample countries

2. Higher efficiency countries get 1 percent of GDP more growth “bang” for their investment than lower efficiency countries

3. Strengthening public investment management (PIM) practices can reduce the “efficiency gap” by almost half

4. Stronger PIM practices improve efficiency by ensuring: – More sustainable levels of investment and PPPs – More stable profile and allocation of investment spending – Less overspending during project execution – Lower levels of rent-seeking

5. Stronger PIM practices positively (but weakly) associated with more economically productive public infrastructure (PICOR) 15

V. Conclusions, Recommendations, and Next Steps: b. Tentative Recommendations

1. Advanced economies need to introduce more investment-friendly fiscal frameworks, strengthen central-local coordination, and adopt more binding MTBFs

2. Emerging economies should unify current and capital budgets and adopt more rigorous and transparent mechanisms for investment project appraisal, selection, and management

3. Developing countries should focus on strengthening investment project execution and management of risks associated with rapid growth in PPPs

4. All countries would benefit from integrating strategic investment planning and budgeting

16

V. Conclusions, Recommendations, and Next Steps: c. Next Steps in Conjunction with Other IFIs

17

Date Milestone

May 2015 Publication of IMF Policy Paper Making Public Investment More Efficient

Summer 2015 Release of cross-country data set on capital stocks public investment quality (PIQ-X) and efficiency (PIE-X)

Autumn 2015 Piloting of Public Investment Management Assessment (PIMA) diagnostic

Winter 2015 Launch of IMF PPP Fiscal Risk Analysis and Management (P-FRAM) tool

Spring 2016 Finalization of PIMA in light of lessons from pilots

Ongoing Greater emphasis in IMF technical assistance on strengthening public investment management