gerald brady managing director silicon valley bank

TRANSCRIPT

Gerald BradyManaging DirectorSilicon Valley Bank

Banking the Innovation Economy

Our Mission:

Build Deep RelationshipsGive AdviceMake It Easy to Do Business with UsSolve Problems

To increase our clients’probability of success

To be the premier provider of financial services and thought leadership to innovation companies, of all sizes, and their investors, world-wide

5

Vision

Differentiated

Focus on “innovation” marketsMainly balance sheet lenderStrong deposit franchiseDiversified revenue streamsGlobal reach

Leader

THE bank for innovation companies

More than 600 venture/ PE firm clients

Global reputation

Established

30 years of supporting innovation

26 U.S. and 7 international offices

$20.0 billion in total assets

$35.5 billion in total client funds

~50% Market Share <15% Market Share <10% Market Share

We work with start-ups to global corportions

Innovation: Macro-themes

10

• 2008-2010: Developed economies slow down / corporate growth impacted

• Company EPS maintained through RIFs, operational excellence programs and increased productivity – little or no focus on innovation

• The pace of innovation continues to accelerate – largely driven by start-ups

• Corporates have more cash on their balance sheet than at any other time

• Established leaders stumble - i.e. Nokia, Microsoft, Pfizer etc

The CEO’s agenda – looking beyond 2012

11

• Technology impact and business model shift across all industries

• Technology driven disruption of existing supply chains

• Non-traditional alliances & partnerships accelerate i.e. GE & Google, P&G & Inverness

• Chinese corporates go from local to regional to global champions

• Innovation becomes driver for competiveness

Innovation is back on the CEO’s agenda

12

• Capital market stabilization results in investors shifting focus from cost management to growth:

- “where is long-term revenue growth going to coming from?”

• Innovation returns to the CEO agenda – as a driver of growth

• Increasingly, corporate venturing goes beyond “open innovation” to include:

- Internal & external innovation initiatives - Corporate ventures- Licensing- Partnering- JVs- M&A

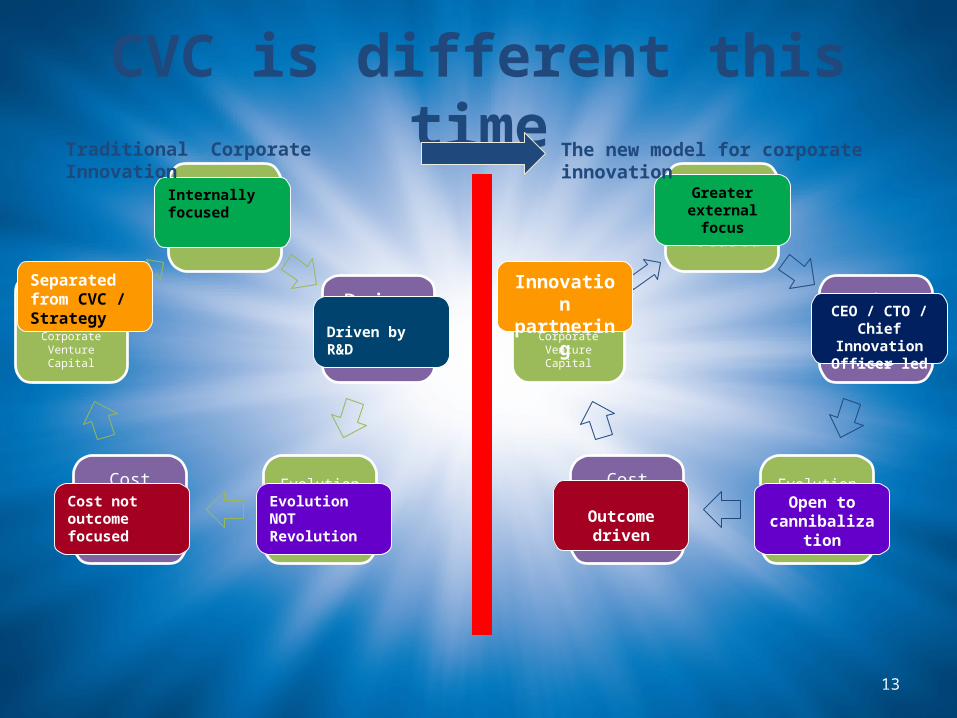

CVC is different this time

13

Internally

focused

Driven by

R&D

EvolutionNOT

Revolution

Cost not outcome focused

Little correlation

with Corporate Venture Capital

Internally focused

Separated from CVC / Strategy

Cost not outcome focused

Evolution NOT Revolution

Driven by R&D

Internally

focused

Driven by

R&D

EvolutionNOT

Revolution

Cost not outcome focused

Little correlation

with Corporate Venture Capital

Greater external focus

Innovation partnering

Outcome drivenOpen to

cannibalization

CEO / CTO / Chief Innovation Officer led

Traditional Corporate Innovation The new model for corporate innovation

The corporate ecosystem: growth is driving the need for innovation

14

MediaInternetLife

Sciences

F&BFMCG

CleantechSemisEnterprise Software

Fin Services

Comms

Automotive

Disney, Hearst, News Corp, WB

Amazon, eBay, Google

Glaxo, Pfizer, Roche, Takeda

Pepsi, Coke, Gen Mills, Nestle

Best Buy, Ikea, P&G, Unilever

ABB, HON, GE, Siemens, Vestas

App Mat, Arm, Intel, Nat Semi

Adobe, IBM, MSoft, SAP

Cisco, Juniper, Huawei, Mot

BMW, GM, Honda, VW

Allianz, Citi, CS, Hartford, Visa

Corporate innovation intersects all company stages

15

Mature

Disruptive trends,white spaces& roadmaps

CorporateInnovation

M&APartneringDistributionVenture Portfolio:

Segmentation bycompany stage Growth

Start-ups

SVB’s role: At the center of the innovation economy

SVB

16

SVB’s Role• Positioned like Switzerland

• Neutral about:- Investors- Location- Stage- Sector

• Able to connect:

Corporate CompaniesCorporate VCsCorporate Corporate