geos confidential - geos energy consulting, calgary ab, canada no portion of this presentation may...

TRANSCRIPT

GEOS

CONFIDENTIAL - GEOS Energy Consulting, Calgary AB, Canada No portion of this presentation may be reproduced in any form without prior written consent

The Future of Oil & Gas in North America…

The Canadian Perspective

George Eynon

GEOS Energy Consulting, Calgary

GCAGS, Austin TX — Nov 1, 2002

GEOS

Outline

Production >> Consumption = Exports Resource base changing

— Deeper-, Tighter-, Coalbed- Gas; Heavier Barrel; More Remote

Wells, drilling season, rig fleet, etc.— Limitations on resource development

WCSB conventional & unconventional Gas Coalbed methane Heavy oil & oilsands Frontiers

— Newfoundland, Scotian Shelf, Arctic, West Coast, Gas Hydrates.

Pace of E&P?— E&P structure, economics, infrastructure & Kyoto

GEOS

Production, Demand & Exports

GEOS

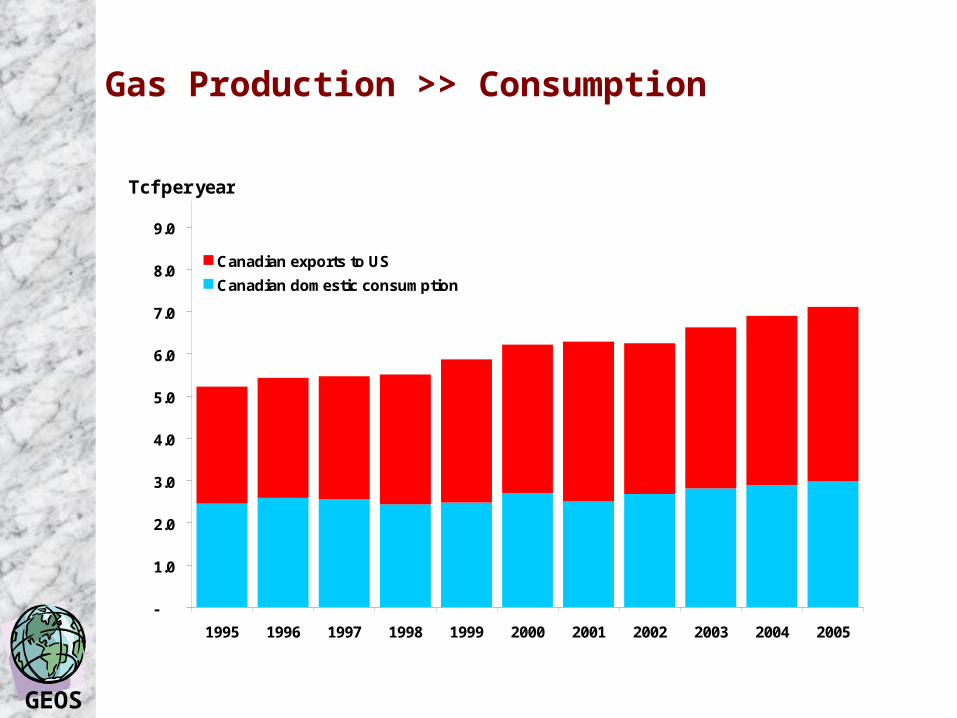

US is Canada’s Export Market

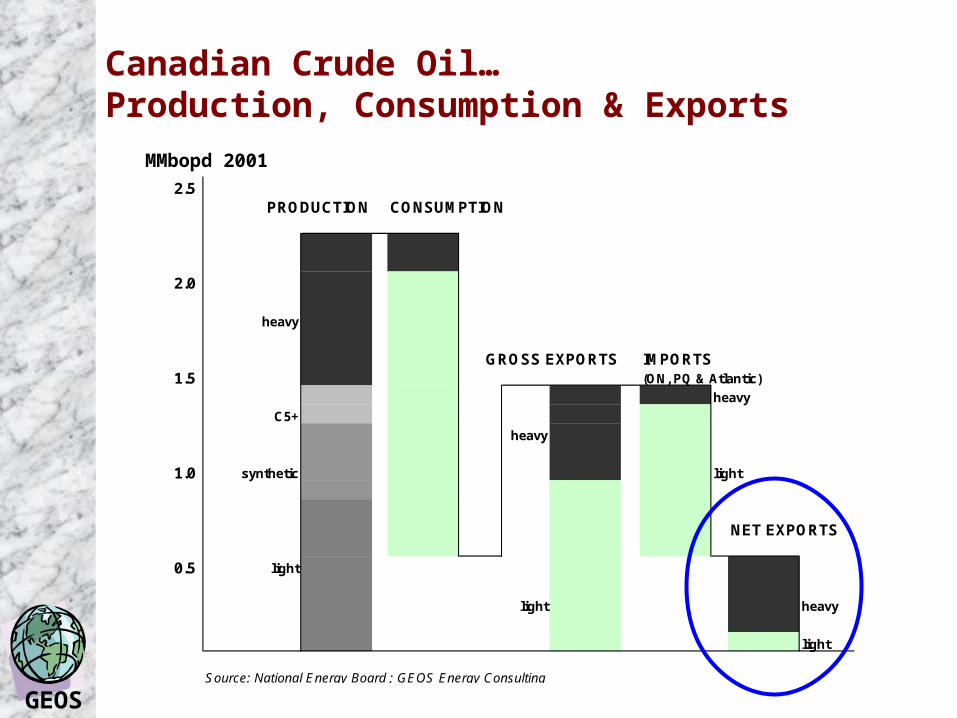

Canada’s production >> domestic consumption— Gas: North American market + North American pricing— Crude oil: US market + World pricing

Gas production increasing since mid-80s— Domestic consumption increasing only marginally— Now export almost 60%

Oil production increasing, but heavier barrel— Light oil in decline; except offshore Newfoundland— Heavy oil and steam-assisted in situ bitumen— Oil sands mining— Upgraded & synthetic crude oil exported

GEOS

Gas Production >> Consumption

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Tcf per year

Canadian exports to US

Canadian domestic consumption

GEOS

Canadian Crude Oil…Production, Consumption & Exports

2.5 PRODUCTION CONSUMPTION

2.0

heavy

GROSS EXPORTS IMPORTS1.5 (ON, PQ & Atlantic)

heavy

C5+

heavy

1.0 synthetic light

NET EXPORTS

0.5 light

light heavy

light

Source: National Energy Board ; GEOS Energy Consulting

MMbopd 2001

GEOS

Resources & Supply Regions

GEOS

Resource Base Not the Problem

Increasing conventional gas Adding unconventional (deep/tight gas, CBM, oilsands) Frontier regions oil & gas Gas hydrates – commerciality 15 years away

GEOS

Gas Production & R/P RatioWCSB - Production & R/P Ratio

-

1

2

3

4

5

6

7

1975 1980 1985 1990 1995

Tcf Per year

-

5

10

15

20

25

30

35R/P ratio

Export pipe expansion& developing the treadmill

Deregulation &working off inventory

Domestic consumption

Exports

GEOS

Gas Pipeline Connected Area 1990…

60ºN

90

80

6M

49ºN

120

100

110

70

60

50

80

60

70

40

50

90

100

120

110

10

1

20

30

5M

3M4M

Fort Nelson

Grande Prairie

Fort St. John

Lethbridge

Calgary

Hinton

Swift Current

Medicine Hat

Saskatoon

Lloydminster

Edmonton

Fort McMurray

110

20

10

30

40

50

70

60

90

80

100

120

126

1

Period Township Connected Onstream

No 1990-1999 Additions to Pre-1990 Township (355)Township Connected 1990 - 1999 (1925)Township Connected Pre-1990 (1943)

Natural Gas Supply Trends 1990-1999

Period TownshipConnected OnstreamEarliest Gas Production in Township

© Forward Energy Group Inc., 2002

60ºN

90

80

6M

49ºN

120

100

110

70

60

50

80

60

70

40

50

90

100

120

110

10

1

20

30

5M

3M4M

Fort Nelson

Grande Prairie

Fort St. John

Lethbridge

Calgary

Hinton

Swift Current

Medicine Hat

Saskatoon

Lloydminster

Edmonton

Fort McMurray

110

20

10

30

40

50

70

60

90

80

100

120

126

1

Period Township Connected Onstream

No 1990-1999 Additions to Pre-1990 Township (355)Township Connected 1990 - 1999 (1925)Township Connected Pre-1990 (1943)

Natural Gas Supply Trends 1990-1999

Period TownshipConnected OnstreamEarliest Gas Production in Township

© Forward Energy Group Inc., 2002

Western Canada Sedimentary basin under-exploited

GEOS

…Doubled by 2000

60ºN

90

80

6M

49ºN

120

100

110

70

60

50

80

60

70

40

50

90

100

120

110

10

1

20

30

5M

3M4M

Fort Nelson

Grande Prairie

Fort St. John

Lethbridge

Calgary

Hinton

Swift Current

Medicine Hat

Saskatoon

Lloydminster

Edmonton

Fort McMurray

110

20

10

30

40

50

70

60

90

80

100

120

126

1

Period Township Connected Onstream

No 1990-1999 Additions to Pre-1990 Township (355)Township Connected 1990 - 1999 (1925)Township Connected Pre-1990 (1943)

Natural Gas Supply Trends 1990-1999

Period TownshipConnected OnstreamEarliest Gas Production in Township

© Forward Energy Group Inc., 2002

60ºN

90

80

6M

49ºN

120

100

110

70

60

50

80

60

70

40

50

90

100

120

110

10

1

20

30

5M

3M4M

Fort Nelson

Grande Prairie

Fort St. John

Lethbridge

Calgary

Hinton

Swift Current

Medicine Hat

Saskatoon

Lloydminster

Edmonton

Fort McMurray

110

20

10

30

40

50

70

60

90

80

100

120

126

1

Period Township Connected Onstream

No 1990-1999 Additions to Pre-1990 Township (355)Township Connected 1990 - 1999 (1925)Township Connected Pre-1990 (1943)

Natural Gas Supply Trends 1990-1999

Period TownshipConnected OnstreamEarliest Gas Production in Township

© Forward Energy Group Inc., 2002

Large areas still not connected

GEOS

Wells, Drilling Season, Rig Fleet ...

GEOS

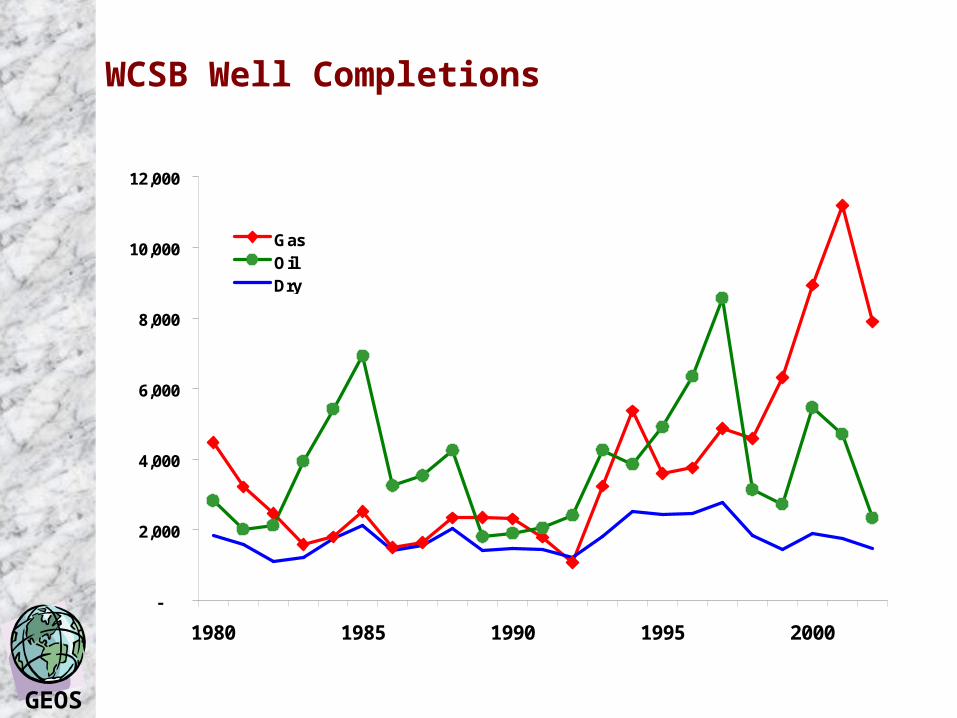

WCSB Well Completions

-

2,000

4,000

6,000

8,000

10,000

12,000

1980 1985 1990 1995 2000

GasOilDry

GEOS

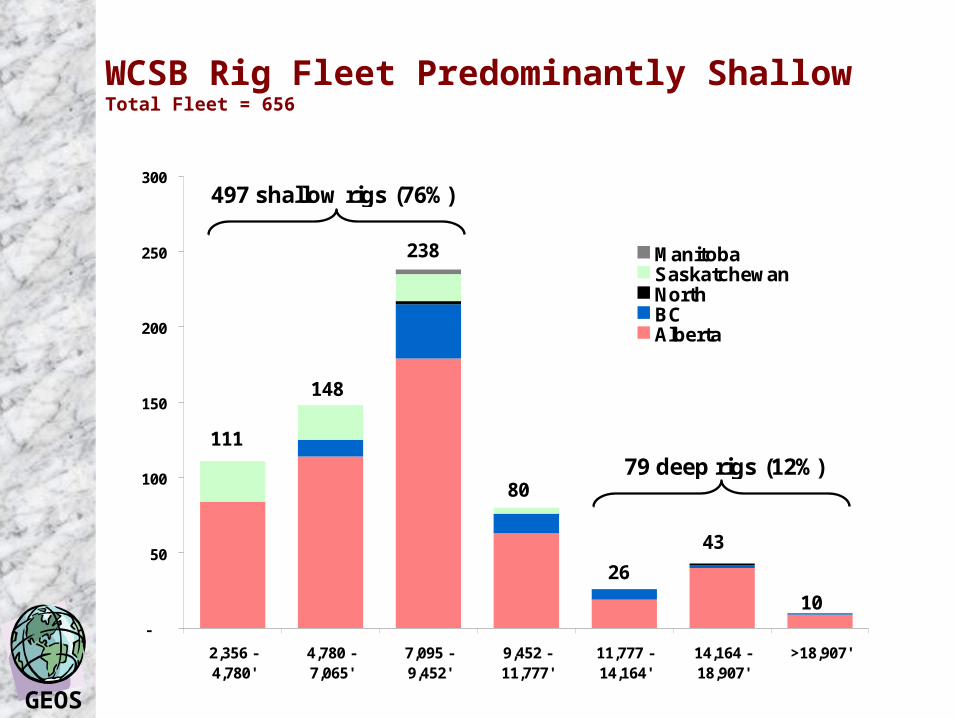

WCSB Rig Fleet Predominantly ShallowTotal Fleet = 656

-

50

100

150

200

250

300

2,356 -4,780'

4,780 -7,065'

7,095 -9,452'

9,452 -11,777'

11,777 -14,164'

14,164 -18,907'

>18,907'

ManitobaSaskatchewanNorthBCAlberta

111

148

238

80

26

43

10

79 deep rigs (12%)

497 shallow rigs (76%)

GEOS

Canada & US Rig Fleets – Depth Capability

69%

22%

7%2% 0%

30%28%

20% 19%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

<3,750'Shallow

3,750-7,500'Medium

7,500-10,000'Deep

10,000-15,000'Very Deep

>15,000'Ultra deep

Canada

USA

GEOS

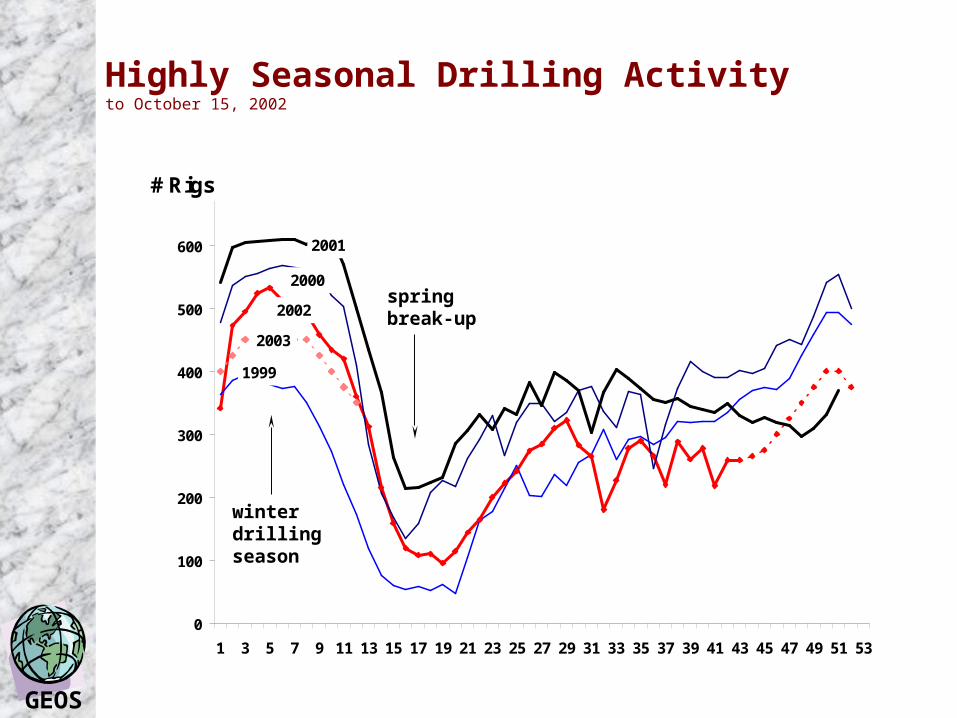

Highly Seasonal Drilling Activity to October 15, 2002

winter drilling season

spring break-up

0

100

200

300

400

500

600

700

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53

# Rigs

2001

2002

2000

1999

2003

GEOS

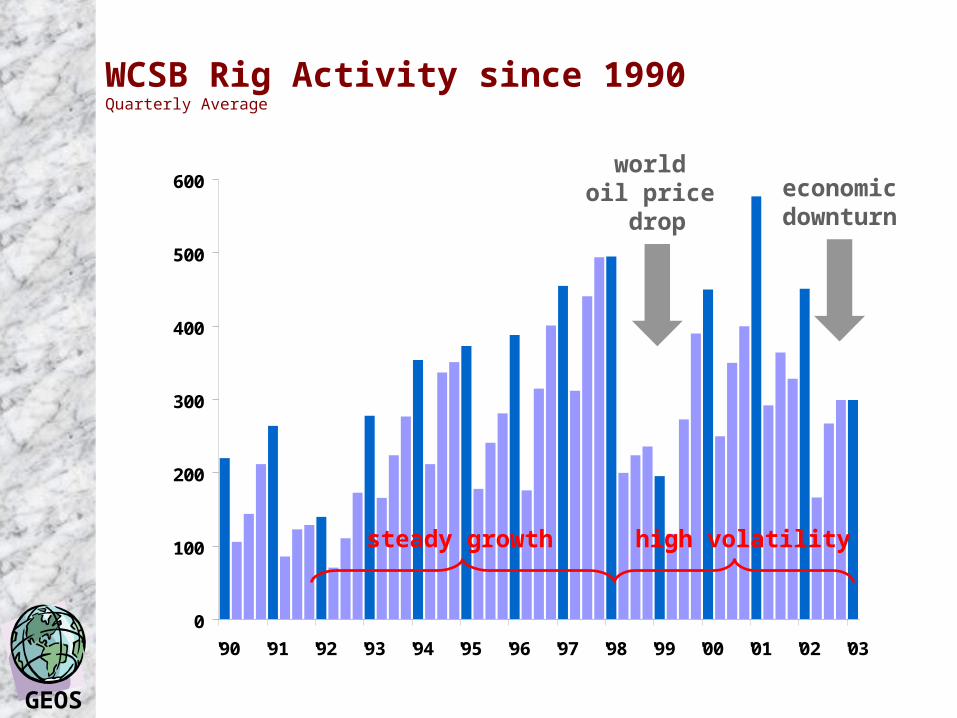

WCSB Rig Activity since 1990 Quarterly Average

0

100

200

300

400

500

600

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03

world oil price

drop

economicdownturn

high volatilitysteady growth

GEOS

WCSB Natural Gas –Shallow, Deep & Tight, Structured

GEOS

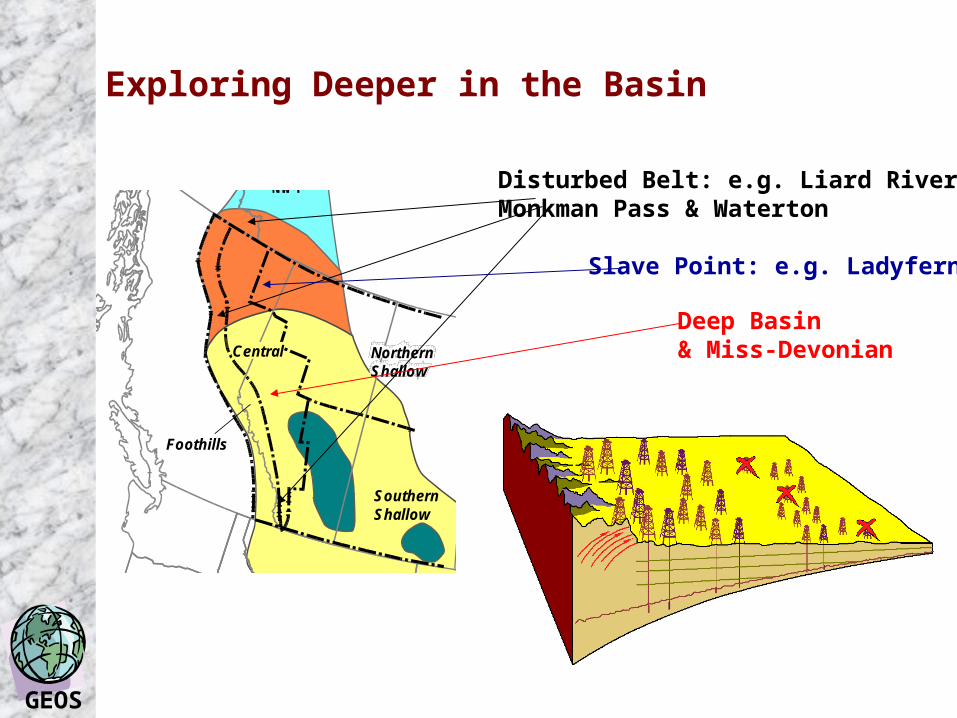

Exploring Deeper in the Basin

Undeveloped

Known Gas Area

Underdeveloped

Relatively Mature

SouthernNWT

SouthernShallow

Central NorthernShallow

Foothills

Disturbed Belt: e.g. Liard River, Monkman Pass & Waterton

Deep Basin & Miss-Devonian

Slave Point: e.g. Ladyfern

GEOS

Annual Decline Rate Flattened Out

Western Canada Region-Wide Annual Decline Rate

15.9%

-1.2%

9.5% 9.8%

14.2%

13.8% 14.0%

16.9% 16.8%18.0%

-5%

0%

5%

10%

15%

20%

25%

1990 1995 2000 2005

Percent Decline

Increase from 10% in early 90sto >15% by 2000then slower increase

GEOS

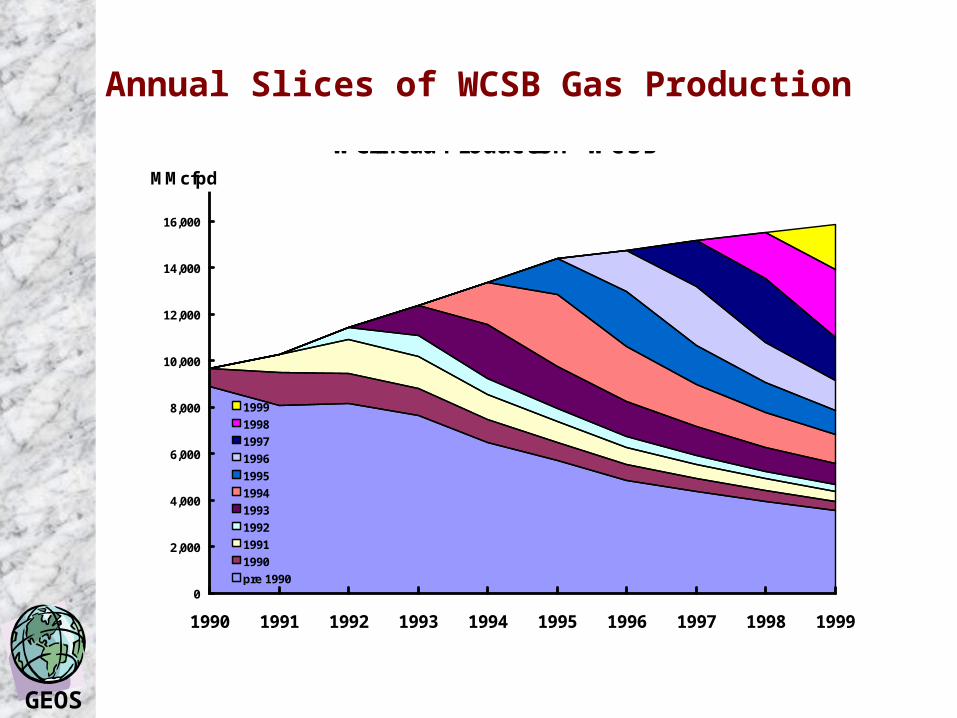

Annual Slices of WCSB Gas Production

Wellhead Production - WCSB

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

MMcfpd

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

pre 1990

GEOS

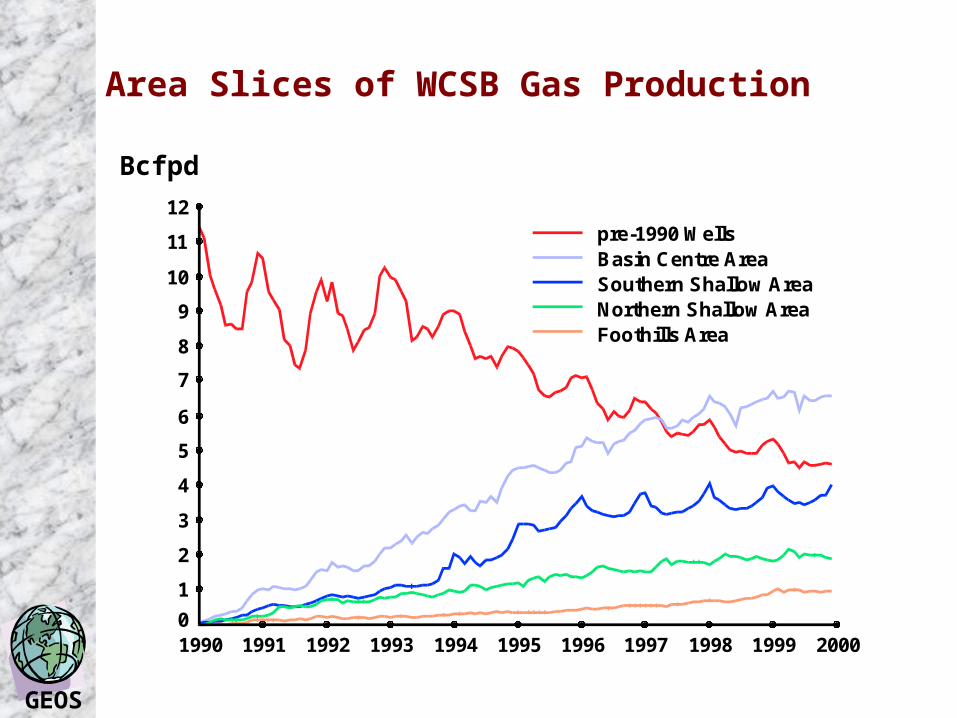

Area Slices of WCSB Gas Production

12

19921990

8

7

6

5

1

01993 1994 1995 1996 1997 1998 1999

2

3

9

10

pre-1990 WellsBasin Centre AreaSouthern Shallow AreaNorthern Shallow AreaFoothills Area

1991 2000

4

11

SalesGas

(BillionCubic

Feetper

Day)

Bcfpd

GEOS

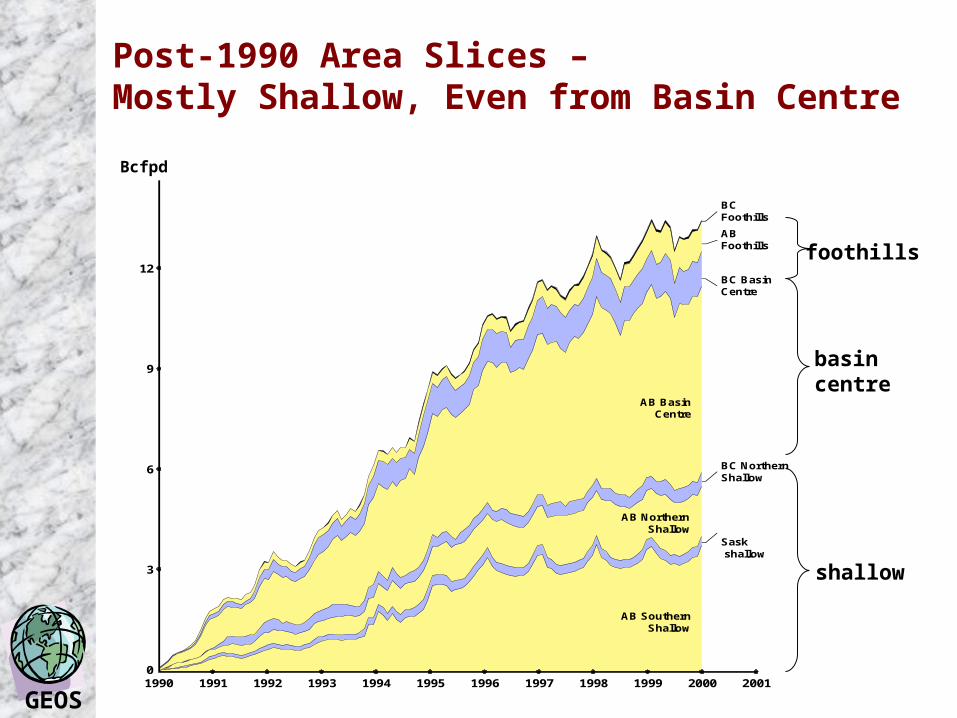

Post-1990 Area Slices – Mostly Shallow, Even from Basin Centre

BillionCubic

FeetperDay

2000

15

1999199719961994199319911990

12

01992 1995 1998

3

6

9

BCFoothills

ABFoothills

BC BasinCentre

AB BasinCentre

BC NorthernShallow

AB NorthernShallow

Sask shallow

AB SouthernShallow

2001

shallow

basin centre

foothills

Bcfpd

GEOS

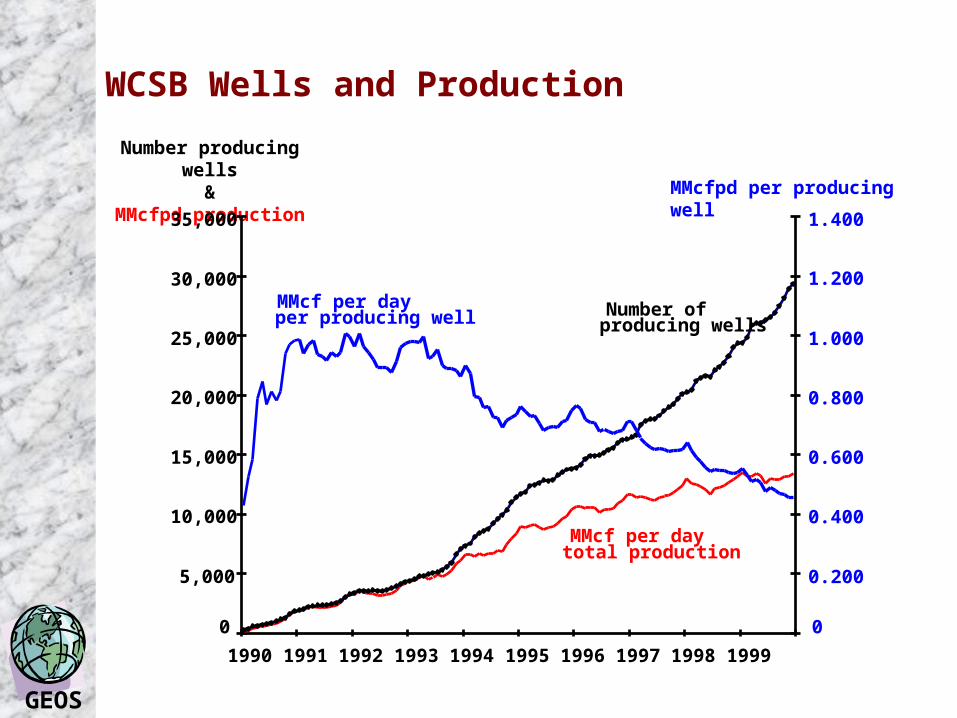

WCSB Wells and Production

Number producing wells &

MMcfpd production MMcfpd per producing well

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

0

0.200

0.400

0.600

0.800

1.000

1.200

1.400

Number of producing wells

MMcf per day per producing well

MMcf per day total production

GEOS

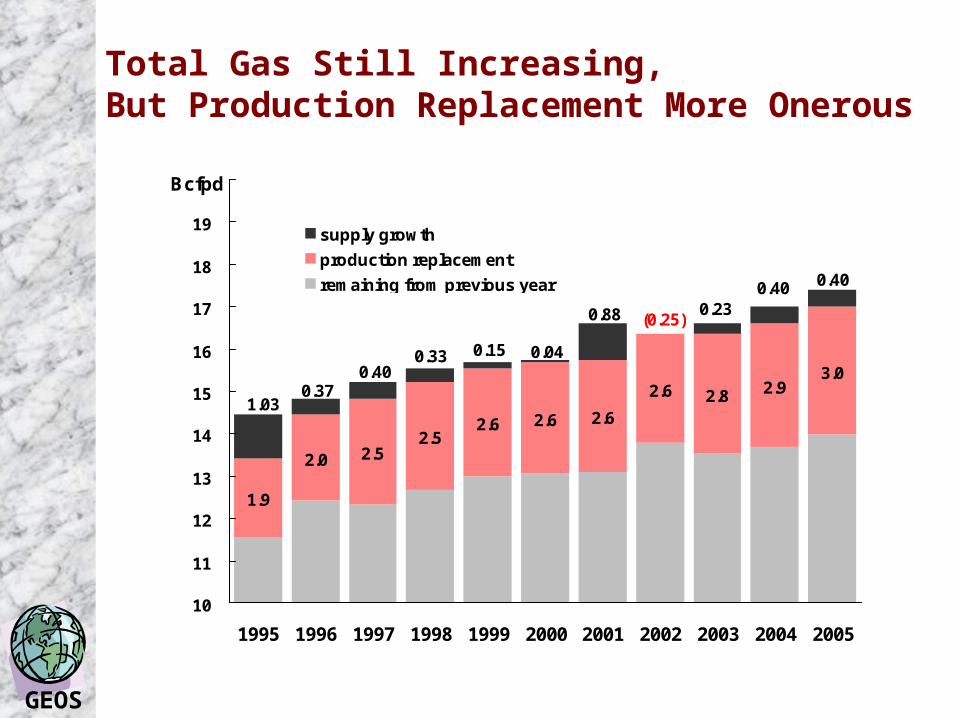

Total Gas Still Increasing,But Production Replacement More Onerous

1.9

2.0 2.52.5

2.6 2.6 2.6

2.6 2.8 2.93.0

1.03

0.40

0.040.150.330.40

0.37

0.400.23

(0.25)0.88

10

11

12

13

14

15

16

17

18

19

20

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Bcfpd

supply growth

production replacement

remaining from previous year

GEOS

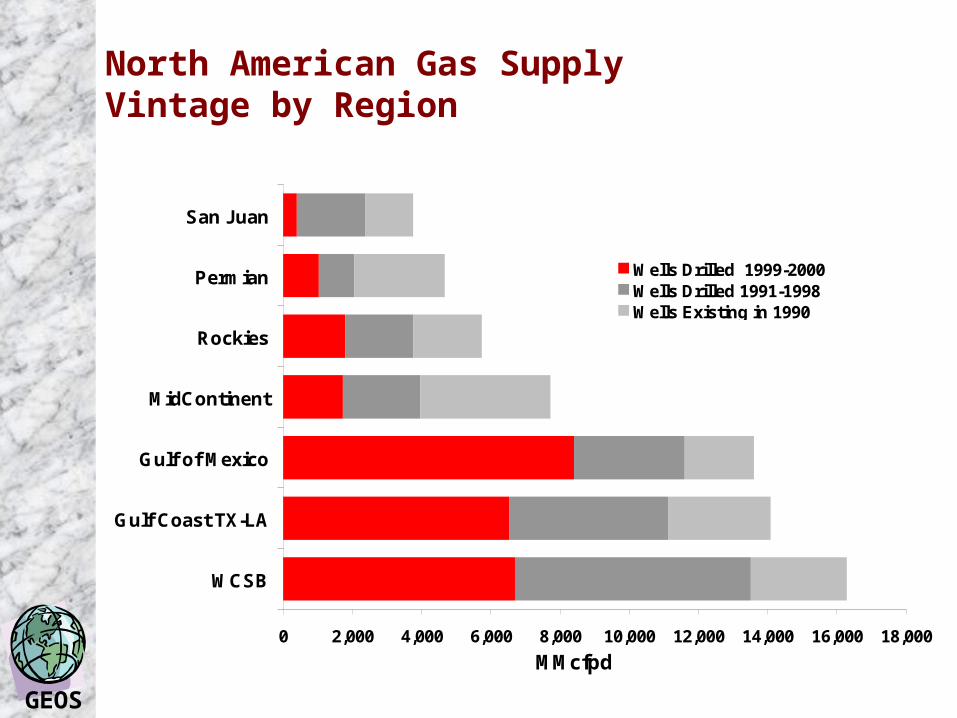

North American Gas Supply Vintage by Region

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000

WCSB

Gulf Coast TX-LA

Gulf of Mexico

MidContinent

Rockies

Permian

San Juan

Wells Drilled 1999-2000Wells Drilled 1991-1998Wells Existing in 1990

MMcfpd

GEOS

Canada’s Coalbed Methane -A Sleeping Giant?

GEOS

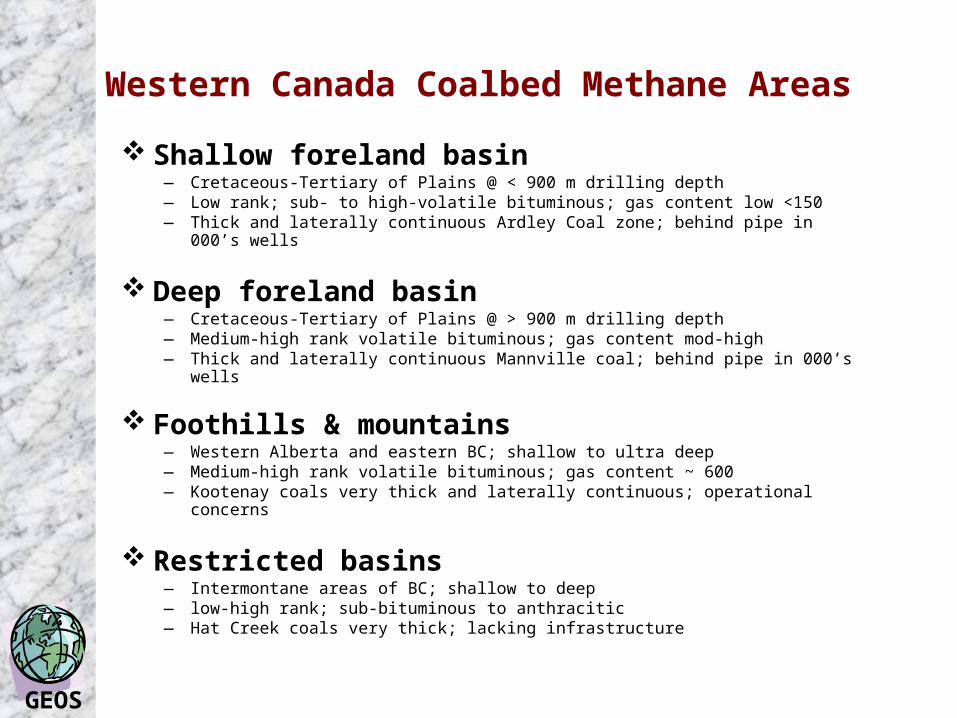

Western Canada Coalbed Methane Areas Shallow foreland basin

— Cretaceous-Tertiary of Plains @ < 900 m drilling depth— Low rank; sub- to high-volatile bituminous; gas content low <150— Thick and laterally continuous Ardley Coal zone; behind pipe in 000’s wells

Deep foreland basin— Cretaceous-Tertiary of Plains @ > 900 m drilling depth— Medium-high rank volatile bituminous; gas content mod-high— Thick and laterally continuous Mannville coal; behind pipe in 000’s wells

Foothills & mountains— Western Alberta and eastern BC; shallow to ultra deep— Medium-high rank volatile bituminous; gas content ~ 600— Kootenay coals very thick and laterally continuous; operational concerns

Restricted basins— Intermontane areas of BC; shallow to deep— low-high rank; sub-bituminous to anthracitic— Hat Creek coals very thick; lacking infrastructure

GEOS

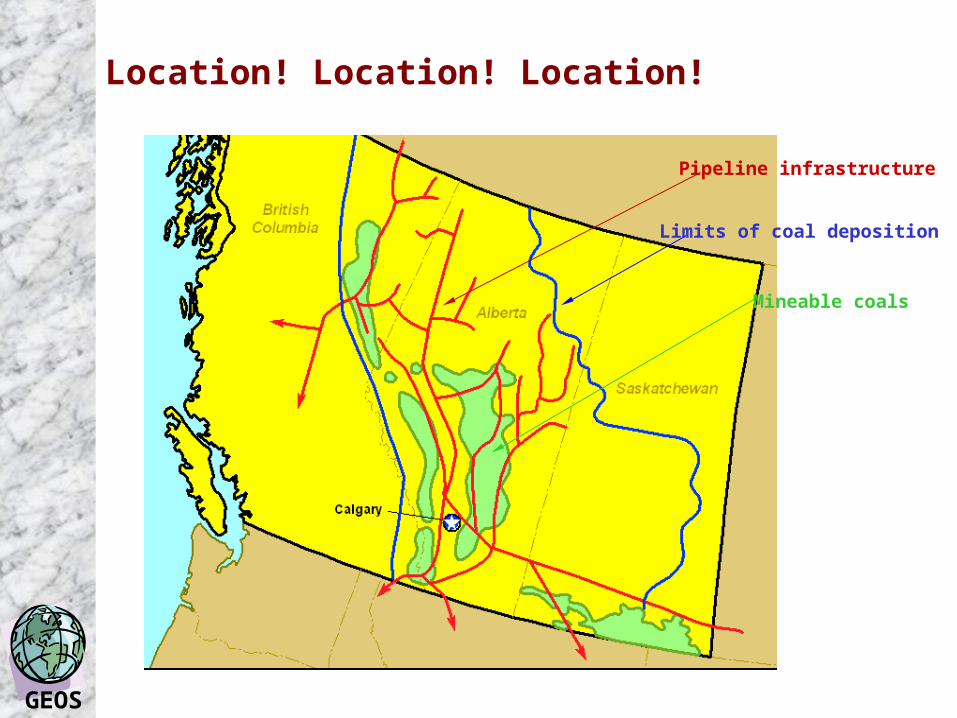

Location! Location! Location!

Limits of coal deposition

Mineable coals

Pipeline infrastructure

GEOS

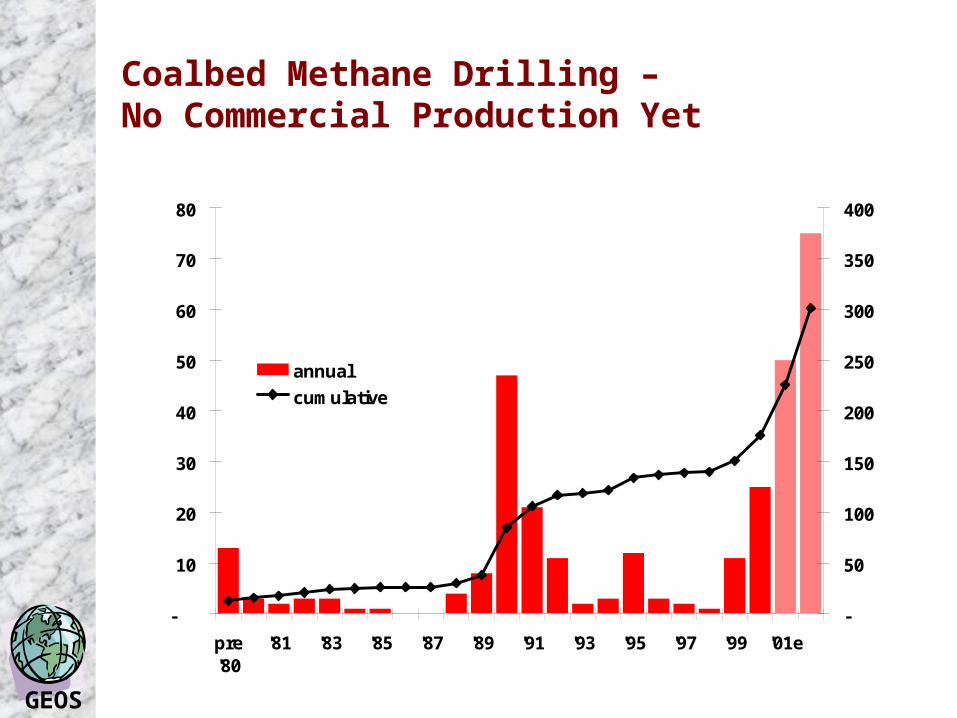

Coalbed Methane Drilling – No Commercial Production Yet

-

10

20

30

40

50

60

70

80

pre'80

'81 '83 '85 '87 '89 '91 '93 '95 '97 '99 '01e

-

50

100

150

200

250

300

350

400

annual

cumulative

GEOS

Western Canada OilsandsThe Future is Now!

GEOS

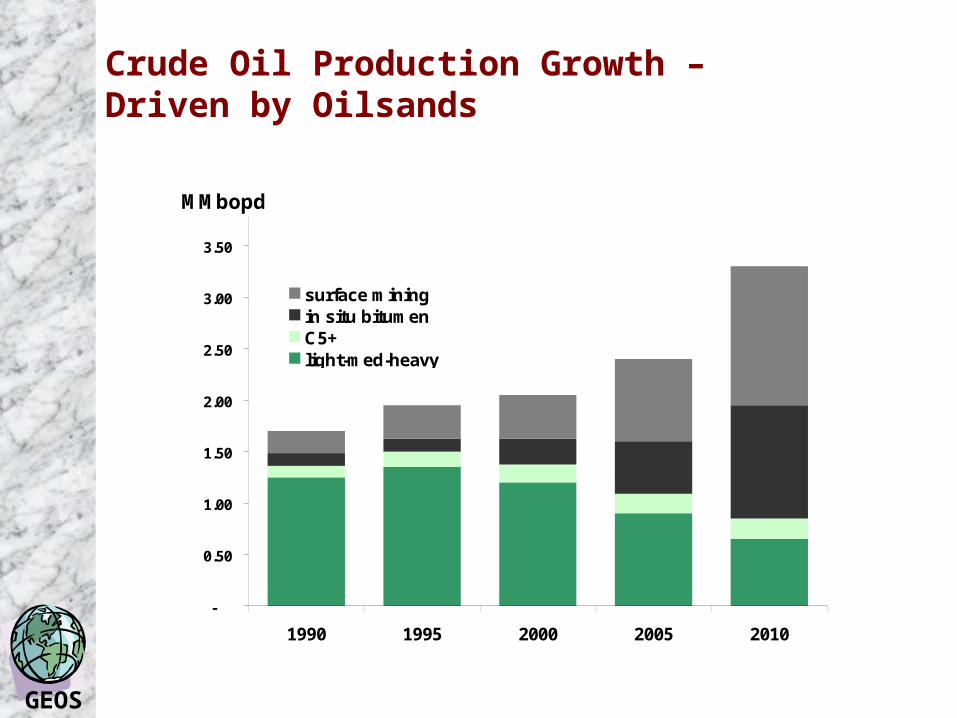

Crude Oil Production Growth – Driven by Oilsands

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

1990 1995 2000 2005 2010

MMbopd

surface miningin situ bitumen C5+ light-med-heavy

GEOS

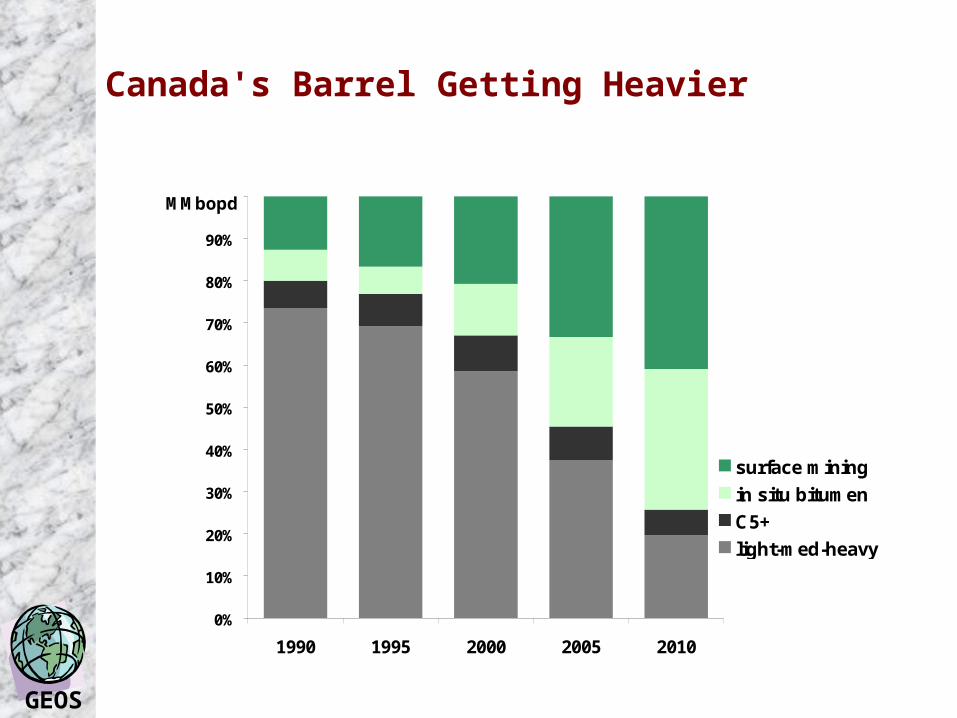

Canada's Barrel Getting Heavier

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 1995 2000 2005 2010

MMbopd

surface mining

in situ bitumen

C5+

light-med-heavy

GEOS

Oilsands Mining Capacity

-

250

500

750

1,000

1,250

1,500

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Mbopd

OthersShellSyncrudeSuncor

GEOS

Diluent requirements –Lagging in situ Bitumen Production

-

0.25

0.50

0.75

1.00

1.25

1.50

1990 1995 2000 2005 2010

MMbopd

in situ bitumen production

C5+ production

GEOS

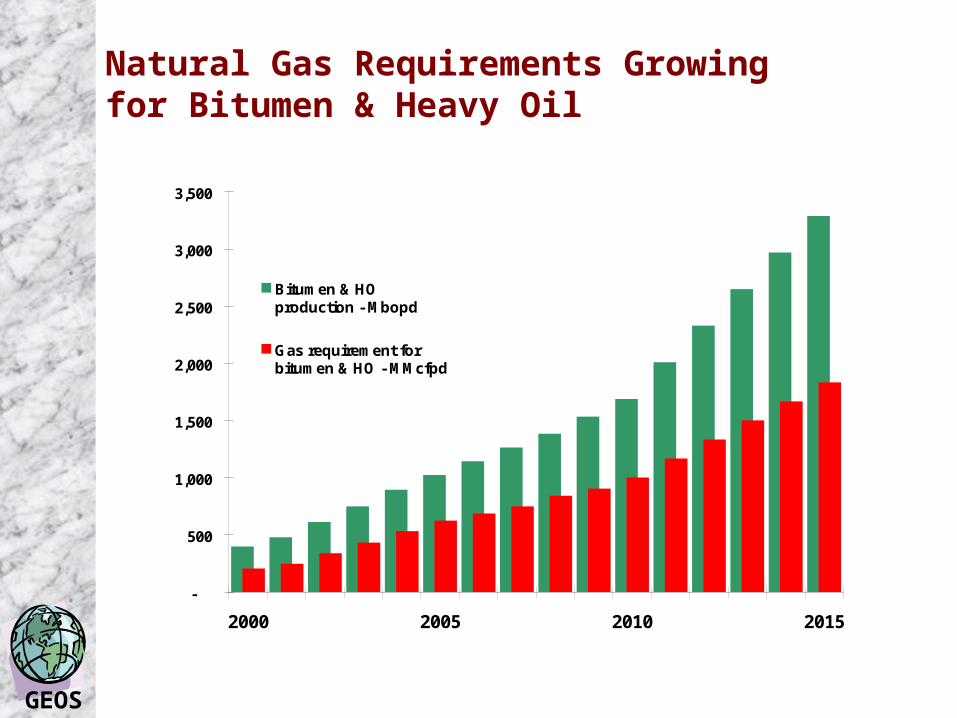

Natural Gas Requirements Growingfor Bitumen & Heavy Oil

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2005 2010 2015

Bitumen & HOproduction - Mbopd

Gas requirement forbitumen & HO - MMcfpd

GEOS

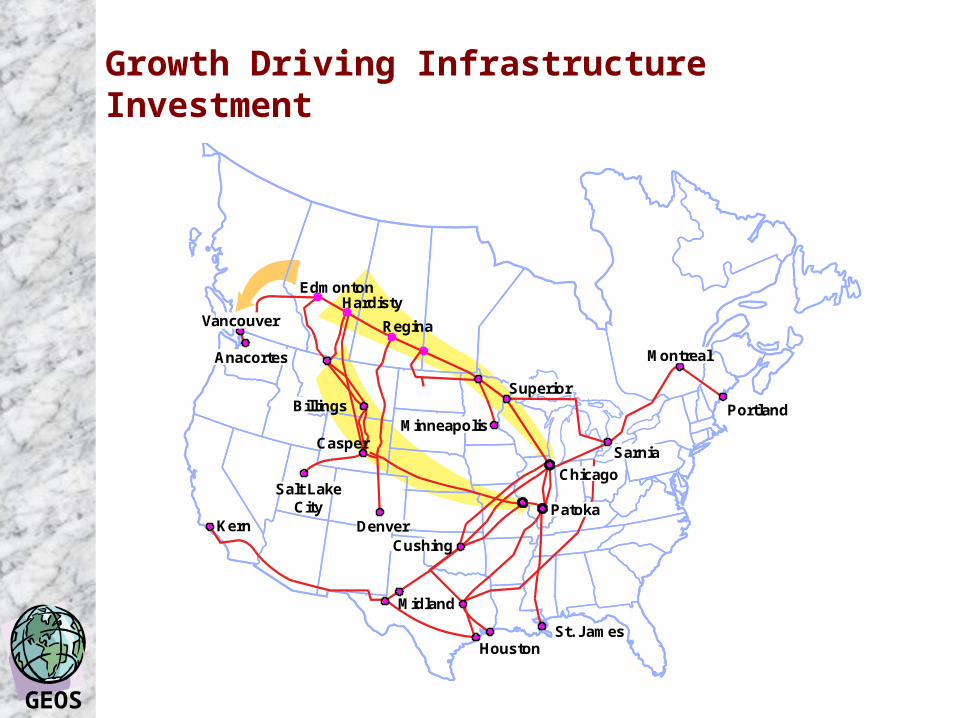

Growth Driving Infrastructure Investment

EdmontonHardisty

Regina

Portland

St. JamesHouston

Midland

Kern

Casper

Salt LakeCity

Superior

Montreal

MinneapolisBillings

Vancouver

Anacortes

DenverCushing

Patoka

Chicago

Sarnia

GEOS

Canadian Frontier Supply Regions…

GEOS

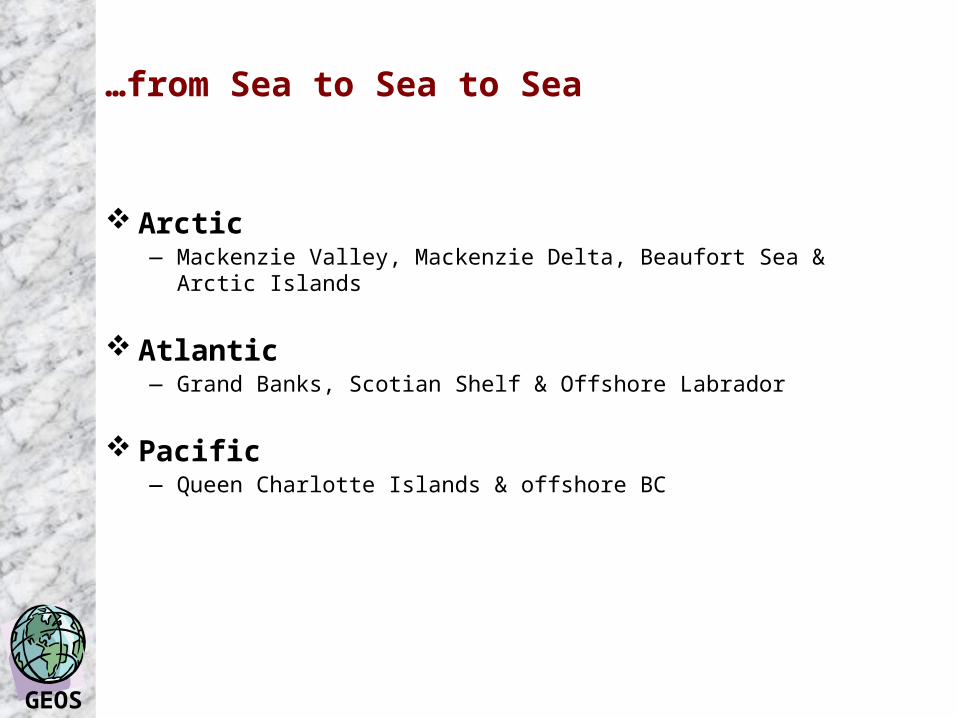

…from Sea to Sea to Sea

Arctic— Mackenzie Valley, Mackenzie Delta, Beaufort Sea & Arctic Islands

Atlantic— Grand Banks, Scotian Shelf & Offshore Labrador

Pacific— Queen Charlotte Islands & offshore BC

GEOS

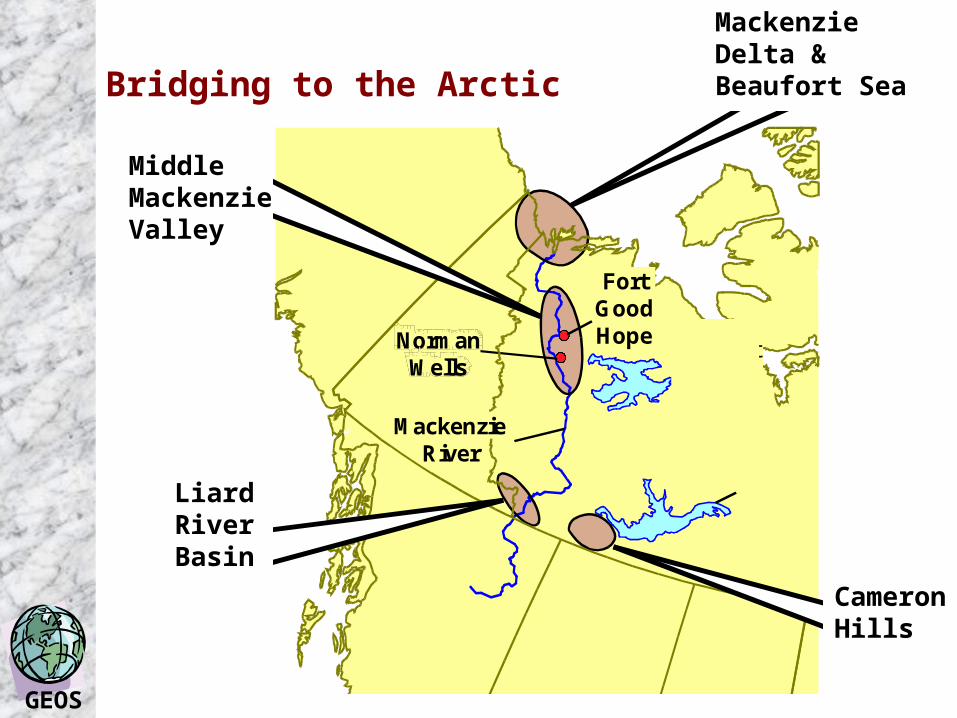

Bridging to the Arctic

NormanWells

GreatSlaveLake

NorthwestTerrotories

GreatBearLake

FortGoodHope

MackenzieRiver

Fort Liard

ParamountCanadian Forest Oil

BP Amoco CanadaPanCandian Petroleum

Suncor Energy

Chevron CanadaRanger Oil

148,15646,241

27,54013,025

5,622

5,1105,090

Undiscovered Potential: 20 Tcf

Beaufort Sea and Mackenzie Delta

BP Amoco CanadaAEC

Talisman EnergyPetro-Canada

Burlington Ranada

Imperial OilGulf Canada

Shell CanadaSuncor Energy

Ikhil ResourcesChevron Canada

425,632214,088

175,810147,822

145,629

100,73792,838

20,5734,843

3,1322,738

Undiscovered Potential: 45 Tcf

Mackenzie Valley

Grand River ResourcesAEC

Ranger OilFoxboro

Inter. Frontier Res.

Canadian AbraxasMurphy Oil

Petro-CanadaBP Amoco Canada

Imperial Oil

352,467262,093

139,63175,196

71,816

46,73834,204

29,6879,391

3,603

Undiscovered Potential: 5–10 Tcf

Cameron Hills

ParamountPhillips

BP Amoco Canada

34,4893,771

321

Undiscovered Potential: 1 Tcf

Mackenzie Delta & Beaufort Sea

Middle Mackenzie Valley

LiardRiverBasin

CameronHills

GEOS

Arctic Gas Pipeline Alternatives

Pipeline toLNG Plant

ARCProposal

ANGTSProject

MackenzieProposal

PacificOcean

Gulf ofAlaska

BeringSea

BeaufortSea

ArcticOcean

AK

BC

AL

AlliancePipeline Foothills

Pipeline

West CoastTransmission

NOVA/TransCanada

Pipeline

United Statesof America

SW

YT

Alaska toMackenzie Valley

“over the top” proposal

Mackenzie Valley Pipe by late 2008?

GEOS

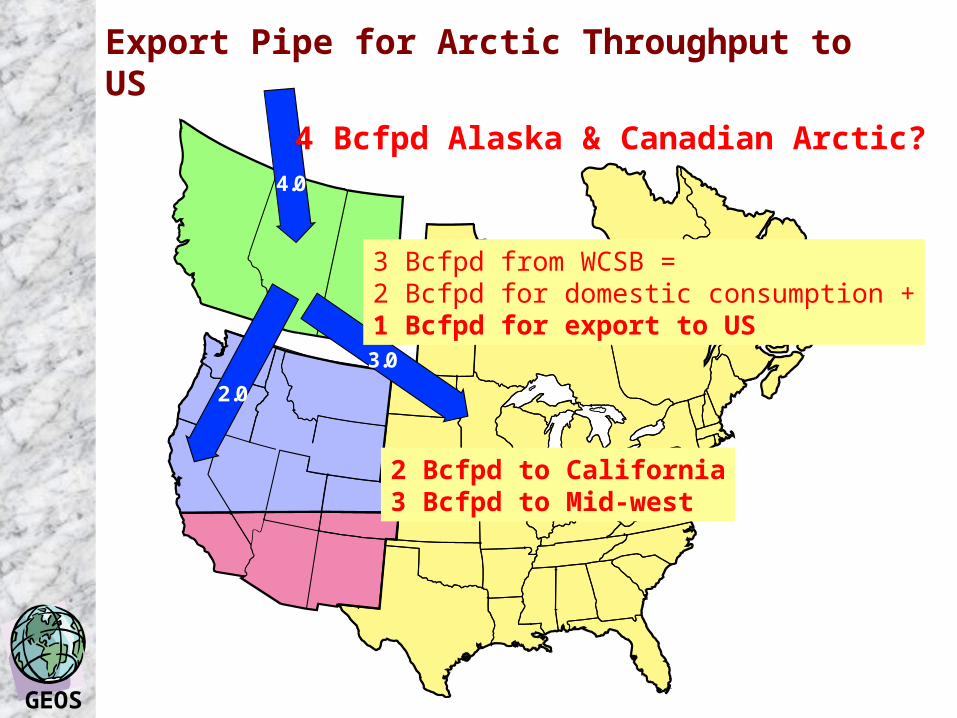

Export Pipe for Arctic Throughput to US

4.0

3.0

2.0

4 Bcfpd Alaska & Canadian Arctic?

3 Bcfpd from WCSB =2 Bcfpd for domestic consumption +1 Bcfpd for export to US

2 Bcfpd to California3 Bcfpd to Mid-west

GEOS

Atlantic Canada Geography

SCOTIAN SHELFSCOTIAN SHELF

GRAND BANKS GRAND BANKS Sable IslandSable Island

150 km150 km

HiberniaHibernia

Terra NovaTerra NovaSt. JohnSt. John

HalifaxHalifax

CharlottetownCharlottetown

St. John’sSt. John’s

SCOTIAN SHELFSCOTIAN SHELF

GRAND BANKS GRAND BANKS Sable IslandSable IslandSable IslandSable Island

150 km150 km150 km150 km

HiberniaHiberniaHiberniaHibernia

Terra NovaTerra NovaTerra NovaTerra NovaSt. JohnSt. JohnSt. JohnSt. John

HalifaxHalifaxHalifaxHalifax

CharlottetownCharlottetownCharlottetownCharlottetown

St. John’sSt. John’sSt. John’sSt. John’s

GEOS

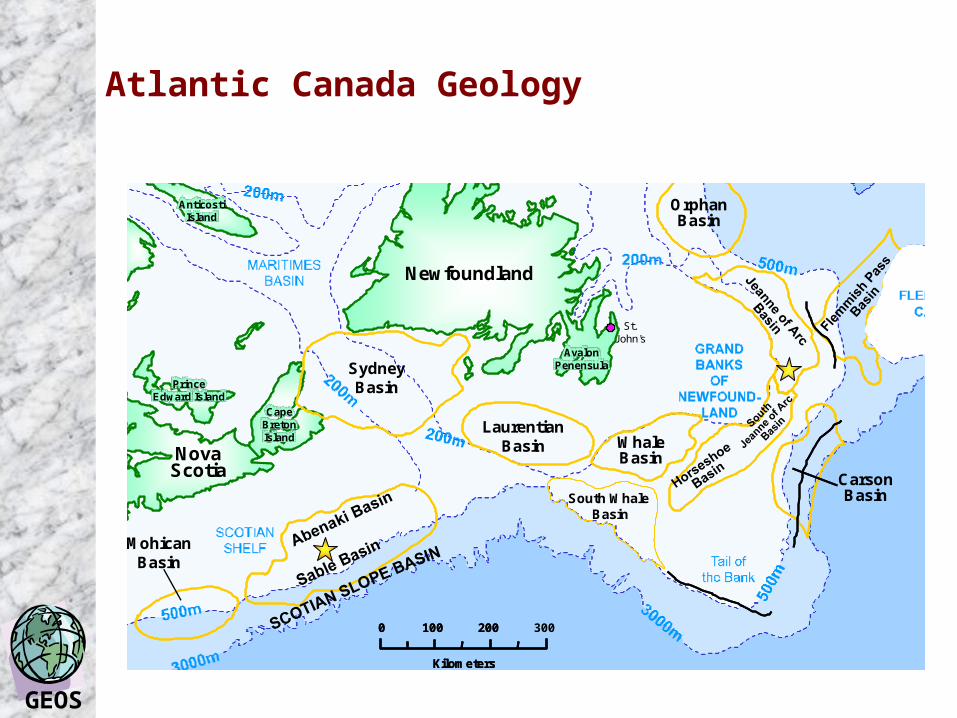

Atlantic Canada Geology

Kilometers

0 100 200 300

NovaScotia

PrinceEdward Island

CapeBretonIsland

AnticostiIsland

Newfoundland

AvalonPenensula

St.John's

MohicanBasin

SydneyBasin

LaurentianBasin Whale

Basin

South Whale Basin

OrphanBasin

CarsonBasin

Kilometers

0 100 200

Kilometers

0 100 200 300

NovaScotia

PrinceEdward Island

CapeBretonIsland

AnticostiIsland

Newfoundland

AvalonPenensula

St.John's

MohicanBasin

SydneyBasin

LaurentianBasin Whale

Basin

South Whale Basin

OrphanBasin

CarsonBasin

GEOS

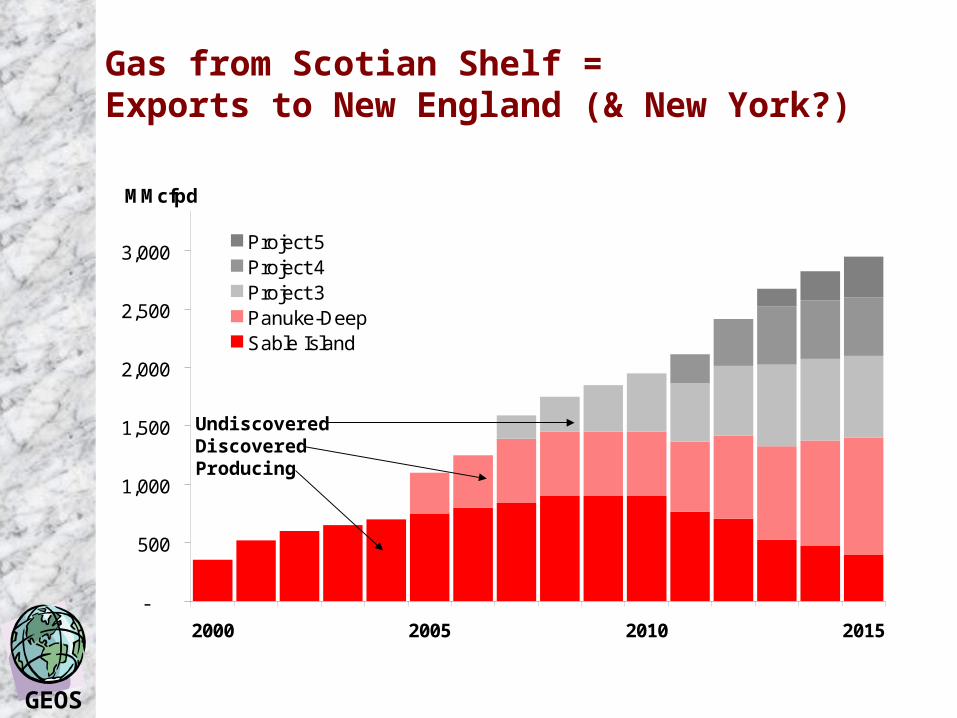

Gas from Scotian Shelf = Exports to New England (& New York?)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2005 2010 2015

MMcfpd

Project 5Project 4Project 3Panuke-DeepSable Island

UndiscoveredDiscoveredProducing

GEOS

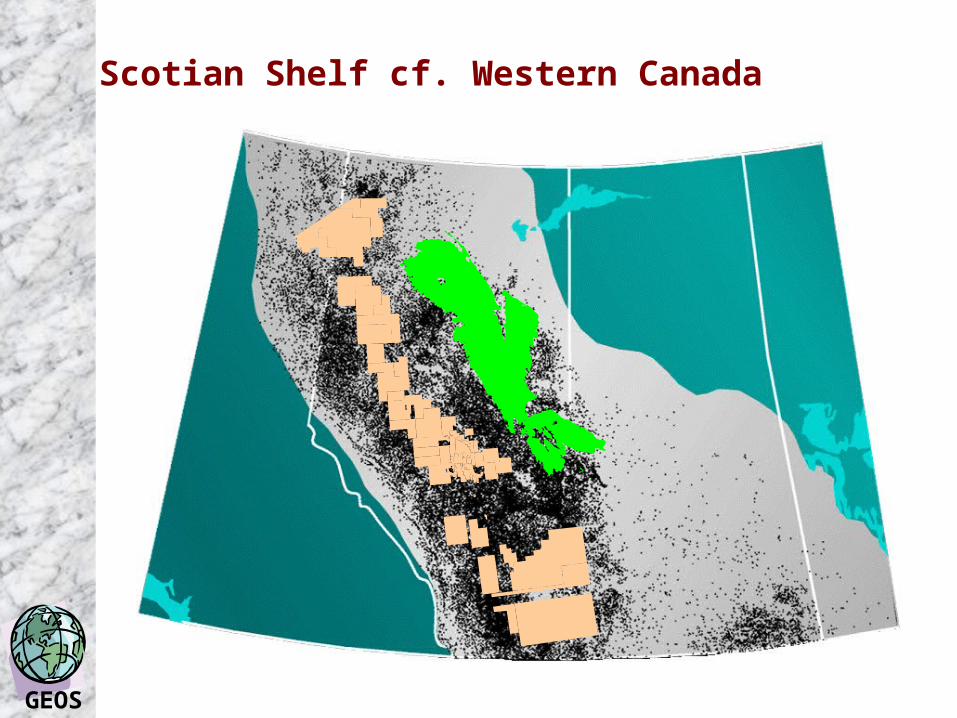

Scotian Shelf cf. Western Canada

GEOS

Canadian Oil & Gas into US

GEOS

4 Bcfpd More Canadian Gas by 2010?(1-2 Bcfpd more by 2015?)

154350

477

905

1,4501,660

1,829

2,324 2,420

3,500

(1,102) (827) (104)

(2,000)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Mid

Co

nti

nen

t

San

Ju

an

Per

mia

n

Wes

t C

oas

t

Eas

tern

US

Gu

lf C

oas

t

Un

des

ig L

48

Sco

tian

Sh

elf

Wes

tern

Can

ada

Gu

lf o

f M

exic

o

Ro

ckie

s

LN

G

Arc

tic

MMcfpd

~1,000

GEOS

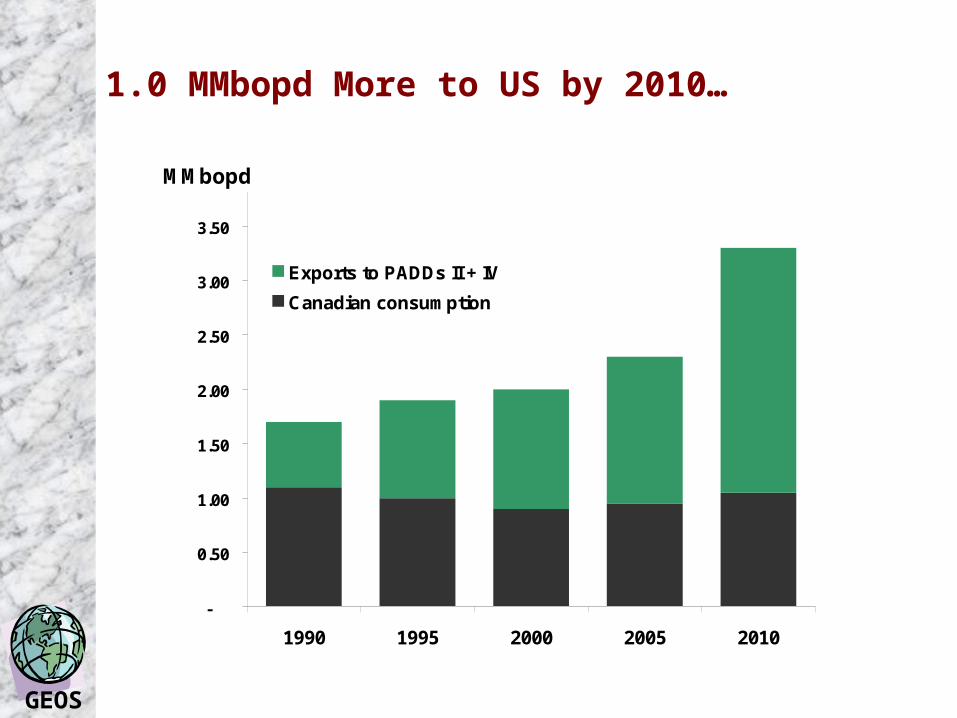

1.0 MMbopd More to US by 2010…

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

1990 1995 2000 2005 2010

MMbopd

Exports to PADDs II + IV

Canadian consumption

GEOS

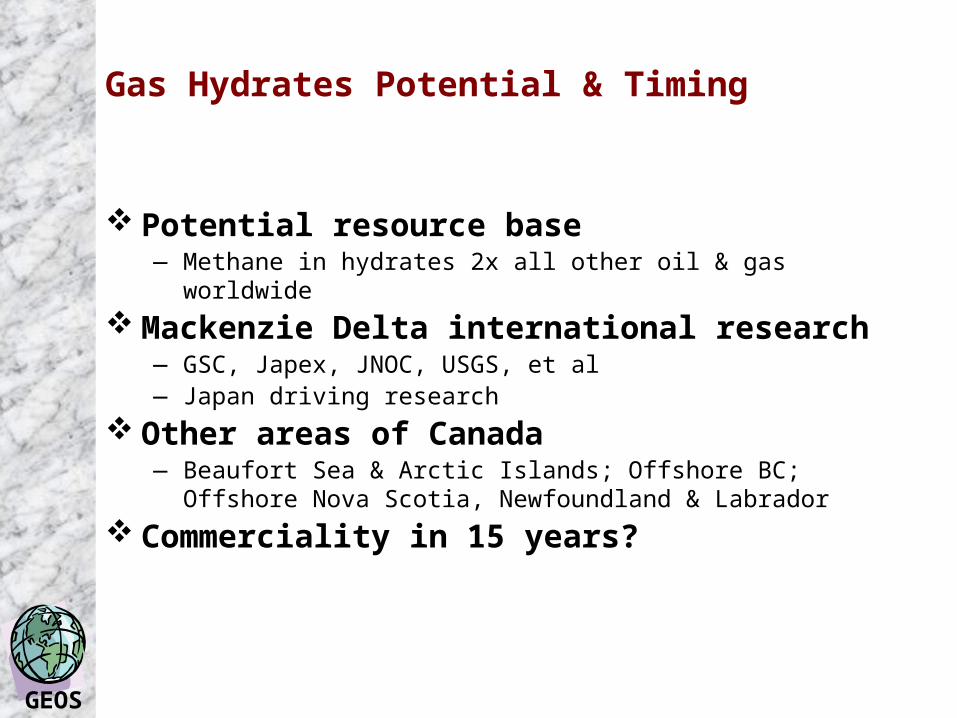

Gas Hydrates Potential & Timing

Potential resource base — Methane in hydrates 2x all other oil & gas worldwide

Mackenzie Delta international research — GSC, Japex, JNOC, USGS, et al— Japan driving research

Other areas of Canada— Beaufort Sea & Arctic Islands; Offshore BC; Offshore Nova Scotia,

Newfoundland & Labrador

Commerciality in 15 years?

GEOS

Future of Canadian E&P Activity

GEOS

Impacting the Pace of Canada’s E&P

Structure of Canada’s E&P sector — M&A: “invasion of the body snatchers”; Mid-size companies swallowed-up— Limited real exploration by US companies in Canada— “Start-ups” small and privately funded— Producing assets in Royalty Income Trusts — Cash flow not fully reinvested; Large dividends to shareholders

Economic recession & recovery in US— Market slowdown; Gas demand restructured

Infrastructure requirements— Arctic gas through Alberta to Midwest & California— Scotian shelf gas to Boston & New York— refineries & upgraders— Canadian producers lack vertical integration

Politics - the Kyoto quagmire— Doing some of the right things for the wrong reasons?