georgia department of audits and accounts march 12, 2015 department of natural resources uniform...

TRANSCRIPT

GEORGIA DEPARTMENT OF AUDITS AND ACCOUNTS

March 12, 2015Department of Natural Resources

Uniform Guidance:

What you need to know

Uniform Guidance

Superseded OMB Circulars: A-21 – Cost Principles for Educational Institutions A-50 – Single Audit Act Follow-up A-87 – Cost Principles for State, Local, and Indian Tribal Governments A-89 – Catalog of Federal Domestic Assistance A-102 – Grants and Cooperative Agreements with State and Local

Governments A-110 – Uniform Administrative Requirements for Grants and Other

Agreements with Institutions of Higher Education, Hospitals, and Other Nonprofit Organizations

A-122 – Cost Principles for Non-Profit Organizations A-133- Audits of States, Local Governments and Non-Profit Organizations

2

Uniform Guidance Eight different OMB guidance streamlined into one. Eliminating overlapping

duplicative and conflicting guidance.

A-21 A-50 A-87 2 CFR Part 200 A-89 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST

PRINCIPLES,

A-102 AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS

A-110 (Uniform Guidance) A-122 A-133

33

Uniform Guidance

Intended Outcomes

• Reduce administrative burden for non-Federal entities

• Reduce the risk of waste, fraud and abuse

44

Effective Dates section 200.110

December 26, 2014

Uniform Guidance is effective for all Federal awards and for additional funding to existing awards (funding increments) made on or after this date.

Procurement requirements - The Federal Government will provide non-Federal entities a grace period for one full fiscal year after the effective date of the Uniform Guidance with certain requirements. (FAQ .110-6) Beginning FY 2017 Full Compliance with Procurement

Requirements

5

Effective Dates section 200.110

December 26, 2014 through June 30, 2015

Non-federal entities must adopt new administrative requirements and cost principles for all new Federal awards and funding increments to existing awards.• Auditor compliance testing will be effected if an entity

has new awards or funding increments made on or after the effective date of the guidance

• Read and understand the terms and conditions of your Federal award (FAQ .110-6)

6

Effective Dates section 200.110

Fiscal year-end June 30, 2016 and beyond

New single audit requirements will apply

Auditors may have to continue testing some awards under the “old” regulations and some under the Uniform Guidance

Testing under the “old” regulations and “new” guidance may continue for several years

7

Effective Dates section 200.110

Fiscal year-end June 30, 2017

Non-federal entities who chose to take advantage of the one full fiscal year grace period must comply with procurement requirements under the uniform guidance.

8

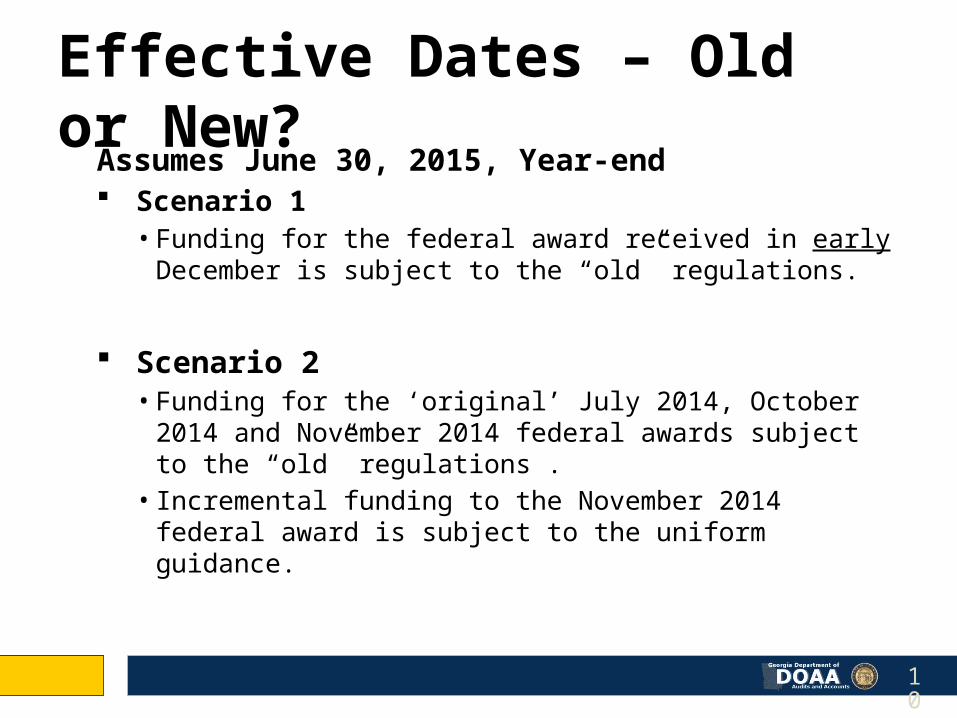

Effective Dates – Old or New?Assumes June 30, 2015, Year-end Scenario 1

• Entity expended funds from a new federal award, which was awarded in early December.

Scenario 2• Entity expended funds from three new federal awards –

These were awarded in July 2014, October 2014 and November 2014.

• In February 2015, the cognizant agency provided incremental funding to the November 2014 federal award and noted the uniform guidance applied.

9

Effective Dates – Old or New?Assumes June 30, 2015, Year-end Scenario 1

• Funding for the federal award received in early December is subject to the “old” regulations.

Scenario 2• Funding for the ‘original’ July 2014, October 2014 and

November 2014 federal awards subject to the “old” regulations .

• Incremental funding to the November 2014 federal award is subject to the uniform guidance.

10

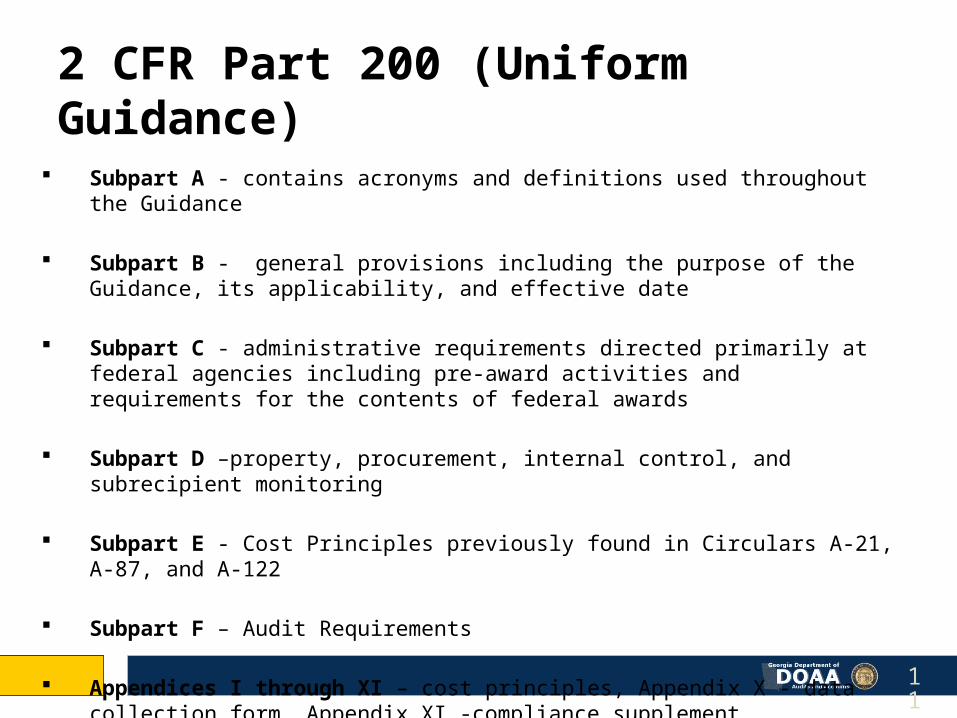

2 CFR Part 200 (Uniform Guidance) Subpart A - contains acronyms and definitions used throughout the Guidance

Subpart B - general provisions including the purpose of the Guidance, its applicability, and effective date

Subpart C - administrative requirements directed primarily at federal agencies including pre-award activities and requirements for the contents of federal awards

Subpart D –property, procurement, internal control, and subrecipient monitoring

Subpart E - Cost Principles previously found in Circulars A-21, A-87, and A-122

Subpart F – Audit Requirements

Appendices I through XI – cost principles, Appendix X - data collection form, Appendix XI -compliance supplement

11

What you need to know – Subpart A Key Acronyms and Definitions

Use of “SHOULD” and “MUST”.• Should = best practice or recommended approach.• Must = required• OMB has identified all SHOULDs and MUSTs in the “interim final rule” published on

December 19, 2014

Contractor will be used instead of “vendor”. • These terms have the same meaning

Personally Identifiable Information (PII) and Protected Personally Identifiable Information (PPII).• Definitions can be found in sections 200.79 (PII) and 200.82 (PPII)• Auditors and auditees must ensure that no protected personally identifiable

information is included in their respective parts of the reporting package

12

What you need to know – Subpart A Improper Payments 200.53

Payment should not have been made Payment for incorrect amount Improper payments

• Ineligible party, goods or services• Goods or services not received• Duplicate• Does not account for credits or discounts• Lack of documentation

13

What you need to know – Subpart B

Conflict of Interest section 200.112

• Federal awarding agencies must establish conflict of interest policies for federal awards. Non-federal entities must disclose in writing to federal awarding agency or pass-through any potential conflict of interest.

14

What you need to know – Subpart B

Mandatory Disclosures section 200.113

• Non-federal entity must disclose, in a timely manner, in writing to federal awarding agency or pass-through all violations of federal criminal law involving fraud, bribery, or gratuity violations potentially affecting the federal award.

• Failure to make required disclosures can result in any of the remedies described in section 200.338. (e.g. temporarily withhold cash payments, disallow, wholly or partly suspend or terminate the Federal award)

15

What you need to know – Subpart D Internal Controls section 200.303

The uniform grant guidance defines internal control as a process that provides reasonable assurance that the Non-Federal entity is managing the Federal award in compliance with Federal statute, regulations and the terms and conditions of the Federal award.

The non-Federal entity must establish and maintain effective internal controls over the Federal award and also:

Comply with Federal statutes, regulations, and the terms and conditions of the Federal award Evaluate and monitor its compliance with statue, regulations and terms and conditions of the

Federal award Take prompt action when instances of noncompliance are identified including noncompliance

identified in audit findings Take reasonable measures to safeguard protected personally identifying information and

other sensitive information

16

What you need to know – Subpart D Internal Controls section 200.303

Source documents for Best Practices • Standards for Internal Control In the Federal Government

(Green Book) – Recently updated, September 2014

• Committee on Sponsoring Organizations (COSO)The COSO 1992 framework was superseded by the COSO 2013 framework on December 15, 2014

• Appendix XI to Part 200—Compliance SupplementWill consider COSO in the 2015 updateWill consider both Green Book and COSO in the 2016 update

17

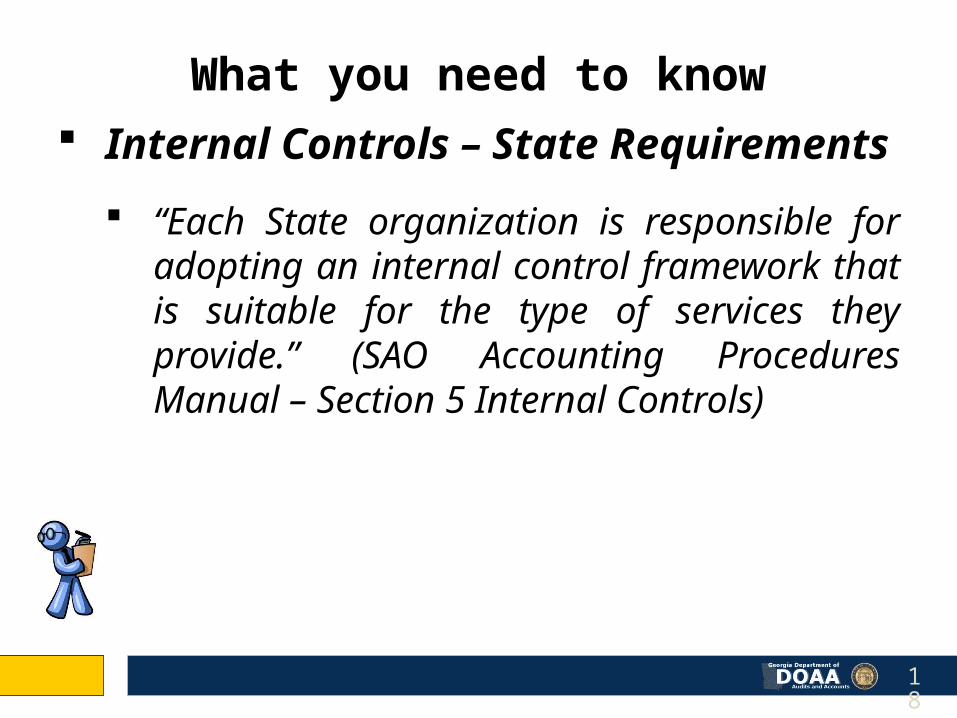

What you need to know Internal Controls – State Requirements

“Each State organization is responsible for adopting an internal control framework that is suitable for the type of services they provide.” (SAO Accounting Procedures Manual – Section 5 Internal Controls)

18

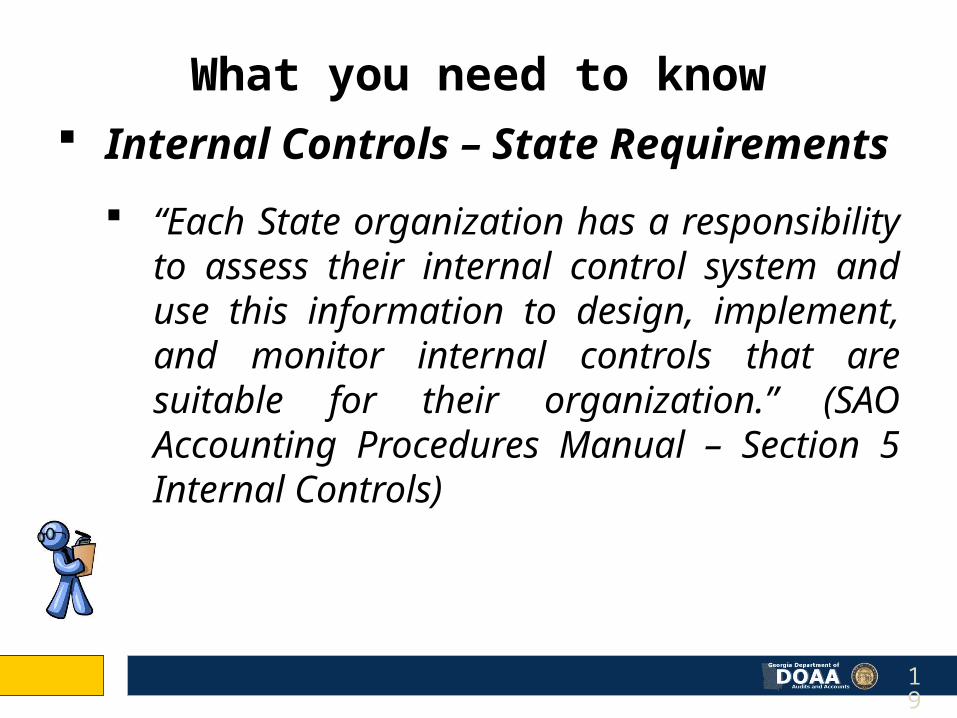

What you need to know Internal Controls – State Requirements

“Each State organization has a responsibility to assess their internal control system and use this information to design, implement, and monitor internal controls that are suitable for their organization.” (SAO Accounting Procedures Manual – Section 5 Internal Controls)

19

What you need to know Internal Controls – State Requirements

All State organizations should evaluate their internal controls. Large State organizations with complex operations should formally document their controls…. (SAO Accounting Procedures Manual – Section 5 Internal Controls Conclusion)

20

What you need to know Internal Controls

Determine an appropriate framework or review existing framework based on your agency’s needs. An internal control framework serves as a way to:

Effectively apply internal controls Identify and analyze risks Develop and manage responses to risks

21

What you need to know Internal Control Components

Internal control consists of five integrated components:

Control environment: Tone at the top

Risk assessment: Determining what could go wrong

Control activities: Actual internal control policies and procedures that are put in place

Information and Communication: Set requirements, expectations and responsibility for carrying out the internal control environment

Monitoring: Process of ensuring that controls are operating effectively

22

What you need to know Internal Controls Components

An effective internal control environment requires that all five components are:

Placed in operationEffectively designedOperating as intended

23

What you need to know Internal Controls - Why?

An entity’s failure to implement effective internal controls could result in noncompliance.

Remedies for noncompliance (200.338) stipulates Specific Conditions (200.207) or actions the Federal agency or pass-through entity may take if a non-Federal entity fails to comply with Federal statutes, regulations or the terms and conditions of the award

24

What you need to know – Subpart D Procurement sections 200.317 through 200.326

Procurement standards are modeled after A-102• State agencies will follow the same policies and procedures they use

for procurements from non-federal funds

Five procurement methods• Micro-purchases ( < $3,000)• Small purchases (> $3,000 and < $150,000)• Sealed bids (> $150,000)• Competitive proposals (> $150,000)• Noncompetitive purchases: special circumstances applicable to all purchase levels

25

What you need to know – Subpart D

Procurement sections 200.317 through 200.326

All procurement methods must comply with the following standards:

Documented polices and proceduresPurchases are necessaryFull and open competitionConflict of Interest policyProper documentation

26

What you need to know – Subpart D

Procurement - FAQ .110-6 Effective Dates and Grace Period

The Federal Government will provide non-Federal entities (NFEs) a grace period for one full fiscal year after the effective date of the Uniform Guidance:

NFEs must comply with terms and conditions of their Federal award

NFEs must document whether in compliance with old or new standard and must meet the documented standard

The Single Audit Supplement will instruct auditors to review procurement policies and procedures based on the documented standard

NFEs must comply fully with the uniform guidance beginning in fiscal years 2017 and beyond

27

What you need to know – Subpart D

Procurement – Identified State Impact

Geographical preferences The uniform guidance is clear that if utilizing federal

funds to procure goods/services the nonfederal entity must conduct procurements in a manner that prohibits the use of statutorily or administratively imposed state or local geographical preferences (see supplementary information in the 12/26/14 final guidance – 200.319)

No other known impacts as of today

28

Subrecipient Monitoring and Management Requirements

200.330 Subrecipient and Contractor Determinations

200.331 Requirements of Pass-Through Entities

29

What you need to know – Subpart D

What you need to know – Subpart D Subrecipient and Contractor Determinations 200.330

(a) Subrecipients (b) Contractors (c) Use of Judgment

DNR must make case-by-case determinations whether each agreement it makes for the disbursement of Federal program funds casts the party receiving the funds in the role of a subrecipient or a contractor. (In the new guidance, contractor is used instead of vendor)

30

What you need to know – Subpart D

(a) Subrecipients A subaward is for the purpose of carrying out a

portion of a Federal award and creates a Federal assistance relationship with the subrecipient.

Characteristics of a Subrecipient:1. Determines who is eligible to receive what Federal assistance2. Has its performance measured in relation to whether objectives of a Federal

program were met3. Has responsibility for programmatic decision making4. Is responsible for adherence to applicable Federal program requirements

specified in the Federal award5. In accordance with its agreement, uses the Federal funds to carry out a

program for a public purpose specified in authorizing statute, as opposed to providing goods or services for the benefit of the pass-through entity

31

What you need to know – Subpart D

(b) Contractors A contract is for the purpose of obtaining goods and

services for DNR’s own use and creates a procurement relationship with the contractor.

Characteristics of a Contractor:1. Provides the goods and services within normal business operations2. Provides similar goods or services to many different purchasers3. Normally operates in a competitive environment4. Provides goods or services that are ancillary to the operation of the

Federal program5. Is not subject to compliance requirements of the Federal program as

a result of the agreement, though similar requirements may apply for other reasons

32

What you need to know – Subpart D(c) Use of Judgment In determining whether an agreement between a pass-

through entity (DNR) and another non-Federal entity casts the latter as a subrecipient or contractor, the substance of the relationship is more important than the form of the agreement.

All of the characteristics listed above may not be present in all cases, and the pass-through entity must use judgment in classifying each agreement as a subaward or a procurement contract.

33

What you need to know – Subpart DRequirements for Pass-Through Entities 200.331 DNR MUST:

(a) Ensure that every subaward is clearly identified to the subrecipient as a subaward and include all required information at the time of the subaward

(b) Evaluate each subrecipient’s risk of noncompliance with Federal statutes, regulations, and the terms and conditions of the subaward for purposes of determining the appropriate subrecipient monitoring

(c) Consider imposing specific subaward conditions upon a subrecipient if appropriate

(d) Monitor the activities of the subrecipient as necessary to ensure that the subaward is used for authorized purposes, in compliance with Federal statutes, regulations, and the terms and conditions of the subaward; and that the subaward performance goals are achieved

34

What you need to know – Subpart DRequirements for Pass-Through Entities 200.331 DNR MUST:

(e) Depending on DNR’s assessment of risk posed by the subrecipient, determine which monitoring tools will be used to ensure proper accountability and compliance with program requirements and achievement of performance goals(f) Verify that subrecipients who are expected to expend $750,000 or

more in Federal funds obtain the required audits(g) Consider whether results of subrecipient monitoring procedures

necessitate adjustments to DNR’s records(h) Consider taking enforcement action against noncompliant

subrecipients

35

What you need to know – Subpart D(a) Ensure that every subaward is clearly identified to the subrecipient as

a subaward and includes all required information at the time of the subaward.

Required information includes:

(1) Federal Award Identification (i) Subrecipient name (which must match the name associated with its unique

entity identifier (DUNS number) (ii) Subrecipient’s unique entity identifier (DUNS number) (iii) Federal Award Identification Number (FAIN) (iv) Federal Award Date (see 200.39 for more information) (v) Subaward Period of Performance Start and End Date (vi) Amount of Federal Funds Obligated by this action (vii) Total Amount of Federal Funds Obligated to the subrecipient (viii) Total Amount of the Federal Award (ix) Federal award project description, as required to be responsive to the Federal Funding Accountability and Transparency Act (FFATA) 36

What you need to know – Subpart D(a) Ensure that every subaward is clearly identified to the subrecipient as a

subaward and includes all required information at the time of the subaward. (continued)

Required information includes:

(x) Name of Federal awarding agency, pass-through entity, and contact information for awarding official (xi) CFDA Number and Name; the pass-through entity must identify the dollar amount made available under each Federal award and the CFDA number at time of disbursement (xii) Identification of whether the award is Research and Development (R&D) (xiii) Indirect cost rate for the Federal award

(2) All requirements imposed by the pass-through entity on the subrecipient so that the Federal award is used in accordance with Federal statutes, regulations and the terms and conditions of the Federal award (3) Any additional requirements that the pass-through entity imposes on the subrecipient in order for the pass-through entity to meet its on responsibility to the Federal awarding agency including identification of any required financial and performance reports

37

What you need to know – Subpart D(a) Ensure that every subaward is clearly identified to the

subrecipient as a subaward and includes all required information at the time of the subaward. (continued)

(4) An approved federally recognized indirect cost rate negotiated between the subrecipient and the Federal Government or, if no such rate exists, either a rate negotiated between the pass-through entity and the subrecipient or a de minimus indirect cost rate as defined in 200.414

(5) A requirement that the subrecipient permit the pass-through entity and auditors to have access to the subrecipients records and financial statements as necessary

(6) Appropriate terms and conditions concerning closeout of the subaward

38

What you need to know – Subpart D(b) Evaluate each subrecipient’s risk of noncompliance with Federal

statutes, regulations, and the terms and conditions of the subaward for purposes of determining the appropriate subrecipient monitoring

The new Uniform Guidance give the following examples of factors that may be considered in the evaluations.

(1) The subrecipient’s prior experience with the same or similar subawards (2) The results of previous audits of the subrecipient and the extent to

which the same or similar subaward has been audited as a major program

(3) Whether the subrecipient has new personnel or new or substantially changed systems

(4) The extent and results of Federal awarding agency monitoring. For example, if the subrecipient also receives Federal awards directly from a Federal awarding agency

39

What you need to know – Subpart D(b) Evaluate each subrecipient’s risk of noncompliance with Federal

statutes, regulations, and the terms and conditions of the subaward for purposes of determining the appropriate subrecipient monitoring. (continued)

Other possible considerations (not in the guidance). (1) The size of the subaward (risk follows the expenditures) (2) Subject to a single audit (3) The complexity of the program (4) Significant changes that could effect the Federal risk (5) Newly formed organization

(6) Complaints against the subrecipient(7) Timeliness of required reports within the past 12 months

40

What you need to know – Subpart D(c) Consider imposing specific subaward conditions

upon a subrecipient if appropriate.

See 200.207 Specific Conditions for details of what these conditions might be

41

What you need to know – Subpart D(d) Monitor the activities of the subrecipient as necessary to ensure that the

subaward is used for authorized purposes, in compliance with Federal statutes, regulations, and the terms and conditions of the subaward; and that the subaward performance goals are achieved.

For ALL subrecipients, monitoring MUST include:

(1) Reviewing financial and performance reports required by DNR (2) Following-up and ensuring that the subrecipient takes

timely and appropriate action on all deficiencies detected through audits, on-site reviews, and other means

(3) Issuing a management decision for audit findings pertaining to the Federal award provided to the subrecipient from DNR as required by 200.521 Management decision

42

What you need to know – Subpart D(e) Depending on DNR’s assessment of risk posed by the

subrecipient, determine which monitoring tools will be used to ensure proper accountability and compliance with program requirements and achievement of performance goals.

These are monitoring options listed in the new guidance and could be incorporated for the subrecipients that are deemed to have higher risk through the risk assessment process:

(1) Providing subrecipients with training and technical assistance on program-related matters

(2) Performing on-site reviews of the subrecipient’s program operations (3) Arranging for agreed-upon-procedures engagements as described in 200.425 Audit services

43

What you need to know – Subpart D

(f) Verify that subrecipients who are expected to expend $750,000 or more in Federal funds obtain the required single audit.

The $500,000 threshold has been increased to $750,000 in the new guidance

(g) Consider whether results of subrecipient monitoring procedures necessitate adjustments to DNR’s records.

Should any issues noted be reflected in DNR’s records?

(h) Consider taking enforcement action against noncompliant subrecipients.

See 200.338 Remedies for noncompliance for further information

44

Good morning, I’m the auditor and I’m your friend. (its okay to laugh, hiss, or boo at this slide)

How to make the auditor happy…. What will the auditor want? Documentation, documentation,

documentation…

45

What you can anticipate – Audit Requests

The following items are likely to be asked for by the auditor: (not all inclusive) Listing of all subawards by Federal program (CFDA) made

during the current state fiscal year which includes the amounts of the subawards.• Some agencies post all their subawards separately in a single

account or accounts in TeamWorks. If that is the case, then auditor could pull population from TeamWorks. If DNR does not do this, the auditor must rely on listings provided to us by DNR.

46

What you can anticipate – Audit Requests

The following items are likely to be asked for by the auditor: (not all inclusive) Your program’s policies and procedures (plan) for

subrecipient monitoring.• This plan should include an understanding of the scope, frequency,

and timeliness of monitoring activities and the number, size, and complexity of awards to subrecipients, including, as applicable, to subawards to for-profit entities.

47

What you can anticipate – Audit Requests

The following items are likely to be asked for by the auditor: (not all inclusive) Copies of selected subaward agreements and the

Contractor/Subrecipient determination worksheets.• We will check for all required information to be included in the

agreement/contract and verification of subrecipient determination.

48

What you can anticipate – Audit Requests

The following items are likely to be asked for by the auditor: (not all inclusive) Current year risk assessments for the following subrecipients

and documentation of the during-the-award monitoring that should correspond to the assessed risk as indicated in the risk assessment document.

49

What you can anticipate – Audit Requests

The following items are likely to be asked for by the auditor: (not all inclusive) Documentation of corrective action for deficiencies noted in

during-the-award monitoring

50

What you can anticipate – Audit Requests

The following items are likely to be asked for by the auditor: (not all inclusive) We will request a list of subrecipients and review for

documentation that supports the following:• Required audits were completed for selected subrecipients• DNR issued management decisions on audit findings within six

months after receipt of the audit report• Subrecipients took appropriate and timely corrective action on all

audit findings.

51

What you can anticipate – Audit Requests

What you need to know – Subpart E

Cost Principles – What is new and how is this applicable to subrecipients?

Uniform Guidance clarifies that indirect costs are now allowable.

Federal agencies are now required to accept and apply the approved indirect cost rate as established by the cognizant agency for the non-federal entity (200.414(c)(1)).• Two exceptions to not using the approved negotiated rate:

When the rate is required by federal statute or regulation When awarding agency head has documented justification for applying

another rate

52

What you need to know – Subpart E

Cost Principles – What is new?

OMB has authorized a new de minimis rate equivalent to 10 percent of the modified total direct costs (200.414(f)). This rate does not apply if: • The entity has received a negotiated indirect cost rate.• The entity is a state public assistance agency in accordance with Appendix VI to

Part 200 (e.g. TANF, Medicaid)

The de minimis rate:• Can be used indefinitely or until an indirect cost rate is negotiated• Does not require review of actual costs• Must be applied consistently for all federal awards• Restricted from use if an entity’s direct federal funding is greater than $35

million (appendix VII.D.1.b)

53

What you need to know – Subpart E

Cost Principles – What is new?

Salaries of administrative and clerical staff should be considered indirect costs unless they can be considered direct costs (200.413).

Salaries for administrative and clerical staff must meet four conditions to be classified as direct costs: Must be integral to a project or activity; Individuals should be specifically identified with the activity; Should be explicitly included in the budget; and Costs should not be recovered as indirect costs.

54

What you need to know – Subpart E

Cost Principles – What is new?

Annual and fiscal reports or vouchers requesting payment must include a certification by an official who is authorized to legally bind the non-Federal entity. (200.415)• Certification language has been strengthened to include specific

language acknowledging the statutory consequences of false certifications

• Certification of cost allocation plan or indirect cost rate proposal is required

Requirements for public assistance cost allocation plans can be found at Appendix VI to Part 200 and Subpart E of 45 CFR Part 95.

55

What you need to know – Subpart E

Compensation (200.430) Costs of compensation are allowable to the extent that they

satisfy the specific requirements of section 200.430 and that the total compensation for individual employees:Is reasonable for the services rendered and conforms to the established

written policy of the non-Federal entity consistently applied to both Federal and non-Federal activities;

Follows an appointment made in accordance with a non-Federal entity’s laws and/or rules or written policies and meets the requirements of Federal statutes, were applicable; and

Is determined and supported as provided in paragraph (1); Standards for Documentation of Personnel Expenses, when applicable. These standards are described below.

56

What you need to know – Subpart E

Compensation (200.430) Standards for documentation of personnel expenses:

• Must be based on records that accurately reflect the work performed• Be supported by a system of internal control • Be incorporated into the official records of the non-Federal entity • Reflect the total activity for which the employee is compensated not

exceeding 100% of compensated activities• Encompass both federally assisted and all other activities compensated by

non-Federal entity • Comply with the established accounting policies and practices of the non-

federal entity• Support the distribution of the employee’s salary or wages among specific

activities or cost objectives if the employee works on more than one Federal award

57

What you need to know – Subpart E

Compensation (200.430(i)(1)(x)(5)(i)) Substitute processes or systems of allocating

salaries and wages to Federal awards may be used in place of or in addition to the records described above if approved by the cognizant agency.• Systems may include but are not limited to:

Random moment sampling “rolling” time studies Case counts; or Quantifiable measures of work performed.

58

What you need to know – Subpart E

Compensation – Fringe Benefits (200.431) The cost of fringe benefits in the form of regular

compensation paid to employees during periods of authorized absences from the job, such as for annual leave … are allowable if all of the following criteria are met:• They are provided under established written leave policies; • The costs are equitably allocated to all related activities,

including Federal awards; and, • The accounting basis (cash or accrual) selected for costing

each type of leave is consistently followed by the non-Federal entity or specified grouping of employees.

59

What you need to know – Subpart F

Audit Requirements – What is new?

Nonfederal entities that expend $750,000 or more in federal awards during the entity’s fiscal year must have a single or program specific audit performed (200.501).

Nonfederal entities that expend less than $750,000 in federal awards during the entity’s fiscal year are not required to perform a single or program specific audit (200.501). Some exceptions apply as noted in section 200.503 Records must be available for review or audit

60

What you need to know – Subpart F

Audit Requirements – What is new?

Audit Findings (200.516)• Known and likely questioned costs have been increased from

$10,000 to those greater than $25,000

Audit requirements under part 200 are applicable to both recipients and subrecipients.

Possible changes to the 2015 compliance requirements.

61

What you should do now Obtain an Understanding of the New

Requirements • Office of Management and Budget - UNIFORM

ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS. http://www.whitehouse.gov/omb/grants_docs

• Council on Financial Assistance Reform (COFAR) - Frequently Asked Questions (FAQs)

https://cfo.gov/cofar/

62

What’s next “Interim Final Rule” was published on December 19, 2014

and all comments were due on February 17, 2015

OMB is in the process of reviewing comments in coordination with Federal awarding agencies

Understand Effective Dates - December 26, 2014

63

What you should do now Set Tone at the Top Develop a Plan to become Compliant• Determine Policy and Procedure Changes• Establish or Update Internal Controls• Establish Action Items and Item Owners• Establish a Training Program • Establish Deadlines

64

65

Questions?

Pete Sheffield, Audit SupervisorState Government Division

Jessica Parent, Director Roger Boyd, DirectorDivision of Professional Standards and Practices Information Technology Services

[email protected] [email protected] 404-657-5116