george o. gamble - tscpa's version 1--2009.pptconferences.tscpa.org/cpefamily/materials/george...

TRANSCRIPT

6/9/2009

1

Convergence Between IFRSs and U.S. GAAP

Presented toPresented to Houston TSCPA Foundation

byDr. George O. GambleRobert Grinaker Professor ofAccountancy & Taxation

C.T. Bauer College of Business AdministrationUniversity of Houston

Convergence Between IFRSs and U.S. GAAP

FASB and IASB In February 2006, the FASB and IASB issued a Memorandum of Understanding (MoU). This document set forth the relative priorities within the FASB-IASB joint work program in the form of specific milestones reached by 2008. The MoU was based on three principles:

(1) Convergence of accounting standards can best be (1) Convergence of accounting standards can best be achieved through the development of high quality, common standards over time.

(2) Trying to eliminate differences between standards that are in need of significant improvement is not the best use of the FASB’s and the IASB’s resources—instead, a new common standard should be developed that improves the financial information to investors.

(3) Serving the needs of investors means that the Boards should seek convergence by replacing standards in need of improvement with jointly developed new standards.

2

Convergence Between IFRSs and U.S. GAAP

FASB and IASB (Cont.)In developing the MoU published in 2006, the Boards agreed on priorities and established milestones only to 2008. The Boards agreed-upon pathway for completing the MoU was to establish short-term convergence projects and major joint projects.

Short-term Convergence

Projects completed: The FASB and the IASB issued standards on a number of short-term convergence projects. The FASB issued new or amended standards that introduced a fair value option (SFAS 157) and adopted the IFRS approach to accounting for research and development assets acquired in a business combination (SFAS 141R). The IASB published new standards on borrowing costs (IAS 23 revised) and segment reporting (IFRS 8).

3

6/9/2009

2

Convergence Between IFRSs and U.S. GAAP

FASB and IASB (Cont.)

Ongoing short-term convergence: The IASB published an Exposure Draft on Joint arrangements (joint ventures) They expect to release the final standard at the beginning of 2009. The IASB also issued a proposal for improvements to financial instruments disclosures and amended IAS 39 (Financial Instruments: Recognition and Measurement and IFRS 7 (Financial Instruments). The FASB is g ( )considering the adoption of IFRS that would eliminate differences in the accounting for taxes (IAS 12 as revised), investment properties (IAS 40) and research and development (IAS 38).

Short-term convergence work deferred: The Boards have chosen to defer projects on government grants and impairment until other work is completed.

Major Joint Projects: The MoU identified 11 milestones to be achieved on major joint projects by 2008. The below table presents the 11 milestones, their current status and estimated completion date.

4

Convergence Between IFRSs and U.S. GAAP

Convergence topic Current status Estimated Completion date

1. Business Combinations completed FAS 141R (2007) &revisions to IFRS 3 (2008)

2. Financial instruments IASB Discussion Paper (2008); FASB issued Exposure Draft to simplify

To be determined

Exposure Draft to simplify hedge accounting

3. Financial Statement Presentation

IASB issued a revision to IAS 1 (2007); IASB & FASB issued Discussion Papers (2008)

2011

4. Intangible assets Inactive-the boards decided in 2007 not to add a project to their joint agenda

Not part of joint agenda

5. Leases Boards plan to issue DP in March 2009

2011

6. Liabilities and equity distinctions

Discussion Paper issued 2011

Convergence Between IFRSs and U.S. GAAP

Convergence topic Current status Estimated completion date

7. Revenue recognition Boards issued DP 2011

8. Consolidations IASB issued Exposure Draft in 2008; FASB has completed a stage of its consolidations project with the issuance of Exposure

2009-1010

the issuance of Exposure Draft, Amendments to FASB Interpretation 46(R).

9. Derecognition Both Boards to publish Exposure Drafts in early 2009.

2009-2010

10. Fair value FASB completed first stage of FASB defined project

IASB: 2011

11. Post employment benefits (including pensions)

FASB: Completed first stage of FASB-defined project; IASB: Discussion paper issued in March 2008

IASB:2011

6

6/9/2009

3

Convergence Between IFRSs and U.S. GAAP

FASB and IASB (Cont.)Conceptual Framework: In setting this work programe initially in 2006, the Boards noted that the major joint projects will take account of the ongoing work of the FASB and the IASB on their joint project to improve and to bring about convergence of their respective Conceptual Framework. The Boards are proposing the following objective of Framework. The Boards are proposing the following objective of general purpose financial statements:

The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to present and potential equity investors, lenders and other creditors in making decisions in their capacity as capital providers. Information that is decision-useful to capital providers may also be useful to other users of financial reporting who are not capital providers.

7

Convergence Between IFRSs and U.S. GAAP

Background (Cont.)The Boards are considering the following workable definition of an

asset and a liability: A liability of an entity is a present economic obligation that is enforceable against the entity.

P t th t th i bli ti i t th Present means that the economic obligation exists on the date of the financial statements.An economic obligation is something that is capable of resulting in cash outflows or reduced cash inflows, directly or indirectly, alone or together with other economic obligations.Obligations link the entity with what it has to do because obligations are enforceable against the entity by legal or equivalent means.

8

Convergence Between IFRSs and U.S. GAAP

FASB and IASB (Concluded)An asset of an entity is a present economic resource to which, through an enforceable right or other means, the entity has access or can limit the access of others.

Present means that both the economic resource and the enforceable right or other means by which the entity has access or

li it th f th i t th d t f th fi i l can limit the access of others exist on the date of the financial statements.An economic resource is something that is scarce and capable of producing cash inflows or reducing cash outflows, directly or indirectly, alone or together with other economic resources.An enforceable right is legally enforceable or enforceable by equivalent means (such as by a professional association), and it enables the entity to use the present economic resource directly or indirectly and precludes or limits its use by others.

9

6/9/2009

4

SEC

On August 27, 2008, the SEC approved for public comment its “Roadmap” for the eventual adoption of International Financial Reporting Standards (IFRS) by US issuers. This “Roadmap” anticipates mandatory reporting under IFRS beginning 2014 for

Convergence Between IFRSs and U.S. GAAP

anticipates mandatory reporting under IFRS beginning 2014 for large accelerated filers, 2015 for accelerated filers and 2016 for non-accelerated filers. US issuers currently use US Generally Accepted Accounting Principles (US GAAP) in their SEC filings.

10

SEC (Cont.)The SEC will make a decision in 2011 on whether or not to adopt IFRS. That decision will include consideration of the progress on seven milestones identified by the SEC which including:

Improvement of accounting standards—The SEC expects the

Convergence Between IFRSs and U.S. GAAP

Improvement of accounting standards The SEC expects the FASB and the IASB to continue to work together and progress towards convergence of IFRS and U.S. GAAP. An updated MOU between the FASB and the IASB is expected to be completed through 2011.

Improvement in the structure and funding of the International Accounting Standards Board—To date, the International Accounting Standards Committee Foundation (IASCF) has financed IASB operations largely through voluntary contributions from companies, accounting firms, international

11

SEC Seven Milestones(Cont.)

organizations and central banks. The roadmap contains a milestone that requires the IASCF to develop a funding mechanism that will enable it to remain a stand-alone, private -sector organization with the necessary resources to conduct

Convergence Between IFRSs and U.S. GAAP

-sector organization with the necessary resources to conduct its work in a timely fashion. The SEC staff stated that the IASCF has made significant progress towards the development of such mechanism.

Improvements in the use of Interactive data (XBRL) for IFRS—The SEC has invested in heavily in XBRL and expects that IFRS information will be capable of being provided to the SEC in interactive format. The IASCF has issued a version of an IFRS taxonomy, which the SEC would consider in evaluating

12

6/9/2009

5

SEC Seven Milestones(Cont.)IASB’s ability to provide interactive data.

Improvements in IFRS education and training—Before making a final decision to move towards IFRS, the SEC would consider the state of preparedness of U.S. issuers, auditors and users including the extent and availability of IFRS education

Convergence Between IFRSs and U.S. GAAP

users, including the extent and availability of IFRS education and training. The SEC commented that it is aware of efforts being made by public accounting firms and academia in this regard.

Experience of voluntary early adopters—The Roadmap contains a provision that permits certain U.S. companies meeting specified criteria to file IFRS financial statements with the SEC for years ending on or after 15 December 2009. Based on a preliminary assessment, the SEC staff stated that

13

SEC Seven Milestones(Cont.)approximately 110 companies across 34 industries would qualify for this provision. In order to be eligible for this provision, a U.S. issuer must meet the following Criteria.

1) be one of the 20 largest companies (based on global market cap) in its industry

Convergence Between IFRSs and U.S. GAAP

2) Participate in an industry in which the use of IFRS is more prevalent than any other basis of accounting

For companies that meet these criteria, the SEC is also expected to require either a one-year reconciliation of the issuer’s financial statements from IFRS to U.S. GAAP in accordance with IFRS 1, or an unaudited three-year reconciliation of the issuers financial statements from IFRS to U.S. GAAP until such time as the use of IFRS becomes mandatory.

14

SEC Seven Milestones(Completed)

Anticipated timing of future rulemaking—The SEC will make its final decision regarding the mandatory use of IFRS in 2011 based on whether the adoption of IFRS is in the public interest and would benefit investors The SEC believes this

Convergence Between IFRSs and U.S. GAAP

interest and would benefit investors. The SEC believes this timing would give companies sufficient notice to begin producing IFRS information for internal purposes in2012.

Sequencing mandatory use of IFRS—mandatory use of IFRS beginning with filings for 2014 for large accelerated filers. Smaller filers would follow in 2015 and 2016. The SEC would later decide to permit other companies to early adopt IFRS prior to the mandatory date of adoption.

15

6/9/2009

6

Convergence Between IFRSs and U.S. GAAP

The FASB’s Response to the Roadmap

1 The FASB supports the Roadmap’s call for a study by the Office of the 1. The FASB supports the Roadmap s call for a study by the Office of the Chief Accountant on the implications for investors and other market participants of implementing IFRS for U.S. issuers. The study is a necessary step in reaching a timely and well supported conclusion on the most advantageous approach the U.S. should take in moving toward the ultimate goal of a single set of high-quality global accounting standards.

2. The FASB recommends that the SEC form a broad-based Advisory Committee, comprising representatives of the many different parties that have a stake, or interest, in the U.S. financial reporting system, to provide one source of valuable input to the study. That group would be charged with identifying, from each of those varying perspectives, the implications of possible changes in the U.S. financial reporting system.

16

Convergence Between IFRSs and U.S. GAAP

3. the Roadmap has appropriately identified the achievement of importantmilestones as essential to the decision about whether to adopt IFRS and the timing of any such adoption. Among the milestones identified is the continued improvement of accounting standards.

4. With respect to the milestone addressing the accountability and funding of the global standard setter, The FASB believes that realizing the benefits of a possible move to global accounting standards requires a sufficiently robust sustainable move to global accounting standards requires a sufficiently robust, sustainable, and independent standard-setting structure. Recent events have demonstrated the significant pressure that can be brought to bear on standard setters and the adverse consequences such pressure can cause, such as suspension of established due process procedures.

5. With respect to the proposal for limited early use of IFRS in certain circumstances, The FASB continues to believe that the SEC should not permit an option unless and until there is a decision that all U.S. public companies will ultimately be required to adopt IFRS. They believe that permitting choice before that decision would create the potential for a two-GAAP system for an extended period of time, resulting in unnecessary complexity and additional costs for investors and other capital market participants.

17

Convergence Between IFRSs and U.S. GAAP

6. While the Roadmap has helped to stimulate debate about the potential use of IFRS by U.S. issuers, it has also contributed to significant uncertainty for all participants in the U.S. financial reporting system about whether, when, and how U.S. financial reporting might change.

18

6/9/2009

7

Accounting Examples

Inventories (IAS No. 2)The accounting treatment for inventory is the same as US GAAP except for the use of LIFO. Standard 2 does not permit the use of the LIFO formula to measure the cost of inventories

Convergence Between IFRSs and U.S. GAAP

formula to measure the cost of inventories.

26 November 2004 the FASB issued SFAS 151, “Inventory Costs an amendment of ARB No. 43, Chapter 4”. This Standard clarifies that abnormal amounts of idle facility expense, freight, handling costs, and wasted materials (spoilage) should be recognised as current-period charges and to require the allocation of fixed production overheads to inventory based on the normal capacity of the production facilities. This Standard is the result of the FASB working with the IASB in trying to eliminate differences between their standards.

19

Interests in Joint Ventures (IAS 31)

Definition of Joint Venture

IAS 31, Interest in a Joint Venture, defines a joint venture as, “a contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control.

l h ll d h f l

Convergence Between IFRSs and U.S. GAAP

Joint control is the contractually agreed sharing of control over an economic activity, and exists only when the strategic financial and operating decisions relating to the activity require the unanimous consent of the parties sharing control (the venturers). Control is the power to govern the financial and operating policies of an economic activity so as to obtain benefits from it.”

IAS 31 identifies three broad types of joint ventures—jointly controlled operations, jointly controlled assets and jointly controlled entities.

20

Jointly Controlled Operations

DefinitionJointly controlled operations involves the use of the assets and th f th t th th th t bli h t f

Convergence Between IFRSs and U.S. GAAP

other resources of the venturers rather than the establishment of a separate entity. Each venturer uses its own assets, incurs it own expenses and liabilities, and raises its own finance.

Accounting TreatmentIAS No.31 requires that the venturer should recognize in its financial statements the assets that it controls, the liabilities that it incurs, the expenses that it incurs, and its share of the income that it earns from the sale of goods or services by the joint venture.

21

6/9/2009

8

Jointly Controlled Assets

DefinitionJointly controlled assets involve the joint control, and often the joint ownership, of assets dedicated to the joint venture. Each venturer may

Convergence Between IFRSs and U.S. GAAP

p, j ytake a share of the output from the assets and each bears an agreed share of the expenses incurred.

Accounting TreatmentIAS 31 requires that the venturer should recognize in its financial statements its share of the joint assets, any liabilities that it has incurred directly and its share of any liabilities incurred jointly with the other venturers, income from the sale or use of its share of the output of the joint venture, its share of any expenses incurred by the joint venture, and expenses that it incurred directly in respect of its interest in the joint venture.

22

Jointly Controlled Entities

DefinitionA jointly controlled entity is a corporation, partnership or other entity in which each venturer has an interest, under contractual arrangement that establishes joint control over the entity.Each venturer usually contributes cash or other resources to the jointly controlled entity. Those contributions are included in the accounting records of the venturer and recognized in the venturer’s financial statements as an investment in the jointly controlled entity.

Convergence Between IFRSs and U.S. GAAP

Accounting TreatmentIAS 31 allows two treatments of accounting for an investment in jointly controlled entities: proportionate consolidation and the equity method.

Proportionate consolidation is a method of accounting whereby a venturer’s share of each of the assets, liabilities, income and expenses of a jointly controlled entity is combined line by line with similar items in the venturer’s financial statements or reported as separate line items in the venturer’s financial statements.

The equity method is a method of accounting whereby an interest in a jointly controlled entity is initially recorded at cost and adjusted thereafter for the post-acquisition change in the venturer’s share of net assets of the jointly controlled entity. The profit or loss of the venturer includes the venturer’s share of the profit or loss of the jointly controlled entity.

23

Example of Proportional Consolidation Method

24

6/9/2009

9

US GAAP vs. IFRS Accounting Treatmentsfor Different Types of Joint Venture Interests Table

Joint Venture Interest Types

Unincorporated EntitiesJointly Controlled Assets or Operations and

Undivided Interests

Comparison of US GAAP vs. IFRS Accounting Treatments

25

IncorporatedEntities

Unincorporated Entities Undivided Interests

Specialized Industries Other Industries

Real EstateUnder Joint Control Others

USGAAP

Equity Method

(APB 18)

ProportionateConsolidation(EITF 00-1)

Equity Method(EITF 00-1)

Equity Method(EITF 00-1 /SOP 78-9)

Share of Assets/Liabilities

(EITF 00-1)

IFRS(IAS 31)

Equity Method/

ProportionateConsolidation

Equity Method/ProportionateConsolidation

Equity Method/ProportionateConsolidation

Share of Assets/Liabilities

Share of Assets/Liabilities

Proposed Changes to Accounting for Joint Ventures

Problems

The accounting requirements of IAS 31 can lead to the recognition of assets that are not controlled and liabilities that are not obligations.

Convergence Between IFRSs and U.S. GAAP

gWhen a party to an arrangement has joint control of an entity, it shares control of the activities of the entity. It does not, however, control each asset nor does it have a present obligation for each liability of the jointly controlled entity. Rather, each party has control over its investment in the entity. If the party uses proportionate consolidation to account for its interest in a jointly controlled entity, it recognizes as assets and liabilities a proportion of items that it does not control or for which it has no obligation. These supported assets and liabilities do not meet the definition of assets and liabilities in the conceptual framework. The framework defines an asset as “a resource

26

Proposed Changes to Accounting for Joint Ventures (Cont.)

Problems (Cont.)

Controlled by the entity…” and a liability as a present obligation of the entity…”

Convergence Between IFRSs and U.S. GAAP

y

IAS 31 can also lead to an entity not recognizing its assets and liabilities. When a jointly controlled entity is similar in substance to jointly controlled operations or jointly controlled assets, a party controls assets and has obligations relating to the activities of the joint arrangement. These assets and liabilities should be recognized in the party’s financial statements. However, if the party accounts for such jointly controlled entities using the equity method, because IAS 31 emphasizes the form of the arrangement, the party does not recognize the assets that it controls and its liabilities.

27

6/9/2009

10

On 13 September 2007, the IASB published for public comment Exposure Draft (ED) 9 proposing to replace Interest in Joint Ventures with a new Standard to be titled Joint Arrangements.

A joint arrangement is a contractual arrangement whereby two or more parties undertake an economic activity together and share d i i ki l ti t th t ti it J i t ti j i t t

Convergence Between IFRSs and U.S. GAAP

decision-making relating to that activity. Joint operation, joint asset, and joint venture are the three forms of arrangements contemplated by ED 9. The following table summarizes those three forms of joint arrangements.

28

Type Characteristics Ownership of assets

Summary of accounting required

Joint operation Involves the use of the assets and other resources of the parties, often to manufacture and sell a joint product.

Each party generally owns its own assets that it uses to create the joint product.

Recognize controlled assets and incurred liabilities, expenses incurred and share of revenues and expenses from the sale of goods or

Convergence Between IFRSs and U.S. GAAP

29

services by the joint arrangement

Joint asset Each party takes a share of the output from the asset and bears an agreed share of the costs incurred to operate the asset.

Each party has rights, and often has joint ownership of the assets used to generate the output

Recognize share of joint assets, classified according to the nature of the asset, liabilities incurred (including those jointly incurred) revenuefrom the sale of share of output and expenses incurred.

Type Characteristics Ownership of assets

Summary of accounting required

Joint venture Joint arrangement that is jointly controlled by the ventuers. Each

l d

Venturers do not have rights to individual assets or obligations for

f h

Recognize theinterest in the joint venture using the equity method

l

Convergence Between IFRSs and U.S. GAAP

venturer is entitled to a share of the outcome of the activities of the joint venture.

expenses of the venture.

unless an exemption applies (held for sale, exemption from equity accounting)

30

6/9/2009

11

Proposed Changes to Accounting for Joint Ventures (Cont.)

The most significant changes proposed are:To shift the focus in accounting for joint arrangements away from the legal form of the arrangements and onto the contractual rights and obligations agreed by the parties and

Convergence Between IFRSs and U.S. GAAP

to remove the choice currently available for jointly controlled entities (equity method or proportionate consolidation) by requiring parties to recognize both individual assets to which they have rights and the liabilities for which they are responsible, even if the joint arrangement operates in a separate legal entity. If the parties only have a right to a share of the outcome of the activities, their net interest in the arrangement would be recognized using the equity method.

31

Proposed Changes to Accounting for Joint Ventures (Cont.)

The ED effectively requires an entity to take a holistic view of its joint arrangements. Thus, one arrangement can have multiple aspects and those aspects may be separately accounted for in some cases. For example, where joint arrangements are conducted through an entity, ll i t d t ill d t b id d h i

Convergence Between IFRSs and U.S. GAAP

all associated agreements will need to be considered when assessing how to account for the arrangement –this could include leases granted or other rights afforded to one or more of the venturers, or guarantees provided effectively making venturers liable for liabilities. These contractual rights and obligations considered in the context of the overall arrangement may bring some assets and liabilities directly into the balance sheet of the venturers

The following flowchart illustrates how a party to a joint arrangement recognizes its interests in the arrangement.

32

Outside the scope of IFRS X

Identify the assets and liabilities (and income and expense) relating to the joint arrangement.

Does the contractual arrangement establish shared decision-making over the joint activities?

No

Yes

Convergence Between IFRSs and U.S. GAAP

33

Recognize each asset and liability (and related income and expense) in accordance with applicable IFRSs.

Recognize any remaining assets and liabilities [interest in a joint venture] using the equity method, ie the assets and liabilities of the joint arrangement for which the parties have an interest only in a share of the outcome of the activities carried on by those assets and

liabilities, and the parties jointly control the activities.

No

Does the party have contractual rights to individual assets (and related benefits) or contractual obligations for expenses or financing [ie interest in a joint asset or

joint operation]?

Yes

6/9/2009

12

Problem 1Four companies jointly buy a 12-floor office building. Each floor inthe building has a separate legal title, which allows a floorto be sold separately. Each company takes title of three of thefloors, one of which it uses for its own purposes. Each has a right

Convergence Between IFRSs and U.S. GAAP

to use that one floor for whatever purpose it chooses. The venturers set up a company and each transfers its ownership of four floors of the building to the company. The 8 floors are rented to third parties. The company employs a management team to manage the rental business. The company is controlled jointly by the venturers. The venturers are not liable for any costs of the company.

34

Problem 2Suppose that the venturers set up the company to purchase all 12 floors. Financing for the acquisition of the building is arranged in the name of the company, secured by the building. Each venturer leases one floor from the company. Each has the right to use that floor for its own purposes or to sublease it

Convergence Between IFRSs and U.S. GAAP

right to use that floor for its own purposes or to sublease it independently to third parties. The lease term is for all of the expected useful life of the building. The company rents the remaining 8 floors to third parties and employs a management team as detailed in paragraph. The venturers jointly control the company.

35

Leases (IAS 17)Definition

According to IAS 17, a lease is an agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of time.

Convergence Between IFRSs and U.S. GAAP

Classification of LeasesThe classification of leases is based on the extent to which risks and rewards incidental to ownership of a leased asset lie with the lessor or the lessee. Risks include the possibilities of losses from idle capacity or technological obsolescence and of variations in returns because of changing economic conditions. Rewards maybe represented by the expectations of profitable operations over the asset’s economic life and of gain from appreciation in value or realization of a residual value.

36

6/9/2009

13

A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease if it does not transfer substantially all the risks and rewards incidental to ownership.

Finance Leases -- Initial Recognition by Lessee

Convergence Between IFRSs and U.S. GAAP

At the start of the lease term, lessees shall recognize finance leases as assets and liabilities at amounts equal to the fair value of the leased property, or, if lower, the present value of the minimum lease payments . The discount rate to be used in calculating the present value of minimum lease payments is the interest rate implicit in the lease, if practicable; if not, the lessee’s incremental borrowing rate shall be used. Any initial direct costs of the lessee are added to the amount recognized as an asset. Contingent rental payments are recognized as expenses in periods incurred.

37

Finance Leases-- Initial Recognition by Lessor

Lessors shall recognize assets held under a finance lease in their balance sheets and present them as a receivable at an amount equal to the net investment in the lease.N t i t t i th l i th i t t i th

Convergence Between IFRSs and U.S. GAAP

Net investment in the lease is the gross investment in the lease discounted at the interest rate implicit in the lease.Gross investment in the lease is the aggregate of the minimum lease payments plus any unguaranteed residual.

38

IAS 17 U.S. GAAP

Finance lease YES Yes (direct financing lease)

Sales type lease No Yes

Convergence Between IFRSs and U.S. GAAP

Sales-type lease No Yes

Operating lease Yes Yes

Leveraged Lease No Yes

39

6/9/2009

14

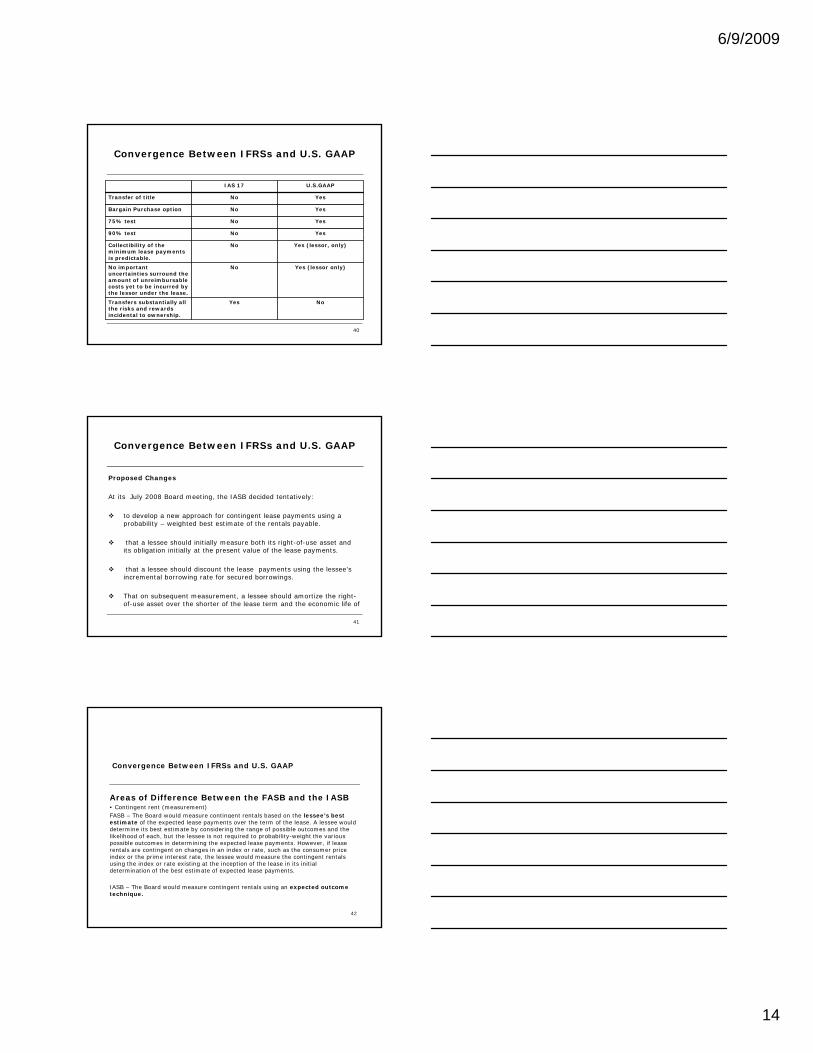

IAS 17 U.S.GAAP

Transfer of title No Yes

Bargain Purchase option No Yes

75% test No Yes

90% test No Yes

Convergence Between IFRSs and U.S. GAAP

90% test No Yes

Collectibility of the minimum lease payments is predictable.

No Yes (lessor, only)

No important uncertainties surround the amount of unreimbursable costs yet to be incurred by the lessor under the lease.

No Yes (lessor only)

Transfers substantially all the risks and rewards incidental to ownership.

Yes No

40

Proposed Changes

At its July 2008 Board meeting, the IASB decided tentatively:

to develop a new approach for contingent lease payments using a probability – weighted best estimate of the rentals payable.

Convergence Between IFRSs and U.S. GAAP

p y g p y

that a lessee should initially measure both its right-of-use asset and its obligation initially at the present value of the lease payments.

that a lessee should discount the lease payments using the lessee’s incremental borrowing rate for secured borrowings.

That on subsequent measurement, a lessee should amortize the right-of-use asset over the shorter of the lease term and the economic life of

41

Convergence Between IFRSs and U.S. GAAP

Areas of Difference Between the FASB and the IASB • Contingent rent (measurement) FASB – The Board would measure contingent rentals based on the lessee’s best gestimate of the expected lease payments over the term of the lease. A lessee would determine its best estimate by considering the range of possible outcomes and the likelihood of each, but the lessee is not required to probability-weight the various possible outcomes in determining the expected lease payments. However, if lease rentals are contingent on changes in an index or rate, such as the consumer price index or the prime interest rate, the lessee would measure the contingent rentals using the index or rate existing at the inception of the lease in its initial determination of the best estimate of expected lease payments.

IASB – The Board would measure contingent rentals using an expected outcome technique.

42

6/9/2009

15

Convergence Between IFRSs and U.S. GAAP

Subsequent measurement of assets and liabilities: FASB – The Board believes that there are differences between leases that are in-

substance purchases and leases that only convey a right to use that may merit differences in the subsequent measurement or presentation.

IASB - Amortize/depreciate the right-of-use asset, apportion the lease payments between a finance charge and a reduction of the outstanding obligation, and present interest expense and amortization/depreciation in the income statement. No difference between leases that are in-substance purchases and a right to use.

Changes in cash flow estimates (method and rate): FASB – The Board would like to account for changes in cash flow estimates using a

catch-up approach using the original incremental borrowing rate.

IASB - The Board would like to account for changes in cash flow estimates using a catch-up approach using the current interest rate.

43

Convergence Between IFRSs and U.S. GAAP

IAS 16—Property, Plant and Equipment

ObjectiveThe objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of the financial statements can discern information about an entity’s investment in its property, plant and equipment and the changes in such investment.

DefinitionsCarrying amount is the amount at which an asset is recognized after deducting any accumulated depreciation and accumulated impairment losses.Cost is the amount of cash or cash equivalents paid or the fair value of the other consideration given to acquire an asset at the time of its acquisition or construction or, where applicable, the amount attributed to that asset when initially recognized in accordance with the specific requirements of other IFRSs.

44

Convergence Between IFRSs and U.S. GAAP

Definitions Cont.

Depreciable amount is the cost of an asset, or other amount substituted for cost, less its residual value.Entity-specific value is the present value of the cash flows an entity expects to arise from the continuing use of an asset and from its disposal at the end of its useful life or expects to incur when settling a liability.Fair value is the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm’s length transaction.

Property, plant and equipment are tangible items that:(a) are held for use in the production or supply of goods or

services, for rental to others, or for administrative purposes; and(b) are expected to be used during more than one period.

45

6/9/2009

16

Convergence Between IFRSs and U.S. GAAP

Definitions (Concluded)

Recoverable amount is the higher of an asset’s net selling price and its value in use.

The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life.

46

Convergence Between IFRSs and U.S. GAAP

Recognition

The cost of an item of property, plant and equipment shall be recognized as an asset if, and only if:(a) it is probable that future economic benefits associated

with the item will flow to the entity; and(b) the cost of the item can be measured reliably.

Measurement at Recognition

An item of property, plant and equipment that qualifies for recognition as an asset shall be measured at its cost.

47

Convergence Between IFRSs and U.S. GAAP

Elements of Cost

The cost of an item of property, plant and equipment comprises:(a) its purchase price, including import duties and non-refundable

purchase taxes, after deducting trade discounts and rebates.

(b) any costs directly attributable to bringing the asset to the location and condition necessary for it to be capable of operating in the manner intended by management.

(c) the initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located, the obligation for which an entity incurs either when the item is acquired or as a consequence of having used the item during a particular period for purposes other than to produce inventories during that period.

48

6/9/2009

17

Convergence Between IFRSs and U.S. GAAP

Elements of Cost (Cont.)

The cost of a self-constructed asset is determined using the same principles as for an acquired asset. If an entity makes similar assets for sale in the normal course of business, the cost of the asset is usually the same as the cost of constructing an asset for

l Th f i t l fit li i t d i i i t h sale. Therefore, any internal profits are eliminated in arriving at such costs. Similarly, the cost of abnormal amounts of wasted material, labor, or other resources incurred in self-constructing an asset is not included in the cost of the asset. IAS 23 Borrowing Costs establishes criteria for the recognition of interest as a component of the carrying amount of a self-constructed item of property, plant and equipment.

49

Convergence Between IFRSs and U.S. GAAP

Measurement of Cost (Cont.)

The cost of an item of property, plant and equipment is the cash price equivalent at the recognition date. If payment is deferred beyond normal credit terms, the difference between the cash price equivalent and the total payment is recognized as interest over the period of

dit l h i t t i it li d i d ith IAS 23credit unless such interest is capitalized in accordance with IAS 23.

One or more items of property, plant and equipment may be acquired in exchange for a non-monetary asset or assets, or a combination of monetary and non-monetary assets. The cost of such an item of property, plant and equipment is measured at fair value unless (a) the exchange transaction lacks commercial substance or (b) the fair value of neither the asset received nor the asset given up is reliably measurable. If the acquired item is not measured at fair value, its cost is measured at the carrying amount of the asset given up.

50

Convergence Between IFRSs and U.S. GAAP

Measurement of Cost (Cont.)An entity determines whether an exchange transaction has commercial substance by considering the extent to which its future cash flows are expected to change as a result of the transaction. An exchange transaction has commercial substance if:

(a) the configuration (risk, timing and amount) of the cash flows of the asset received differs from the configuration of the cash flows of the asset transferred; or

(b) the entity-specific value of the portion of the entity’s operations affected by the transaction changes as a result of the exchange; and

(c) the difference in (a) or (b) is significant relative to the fair value of the assets exchanged.

For determining whether an exchange transaction has commercial substance, the entity-specific value of the portion of the entity’s operations affected by the transaction shall reflect post-tax cash flows.

51

6/9/2009

18

Convergence Between IFRSs and U.S. GAAP

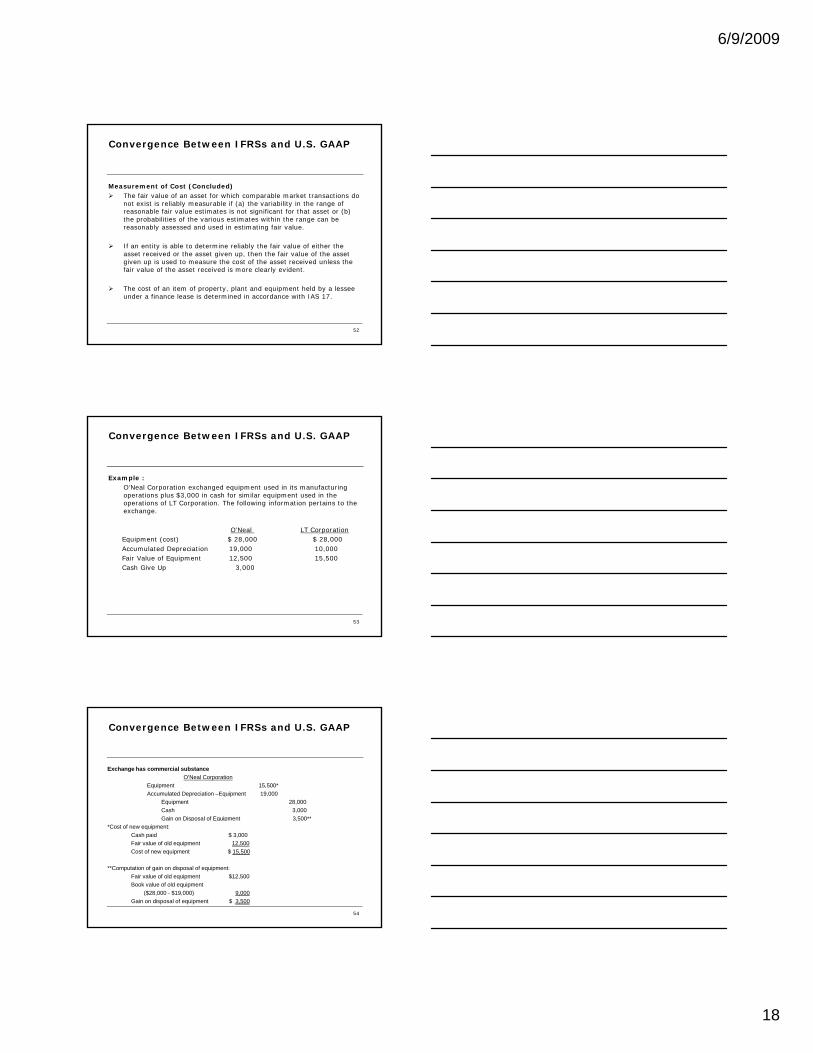

Measurement of Cost (Concluded)The fair value of an asset for which comparable market transactions do not exist is reliably measurable if (a) the variability in the range of reasonable fair value estimates is not significant for that asset or (b)the probabilities of the various estimates within the range can be reasonably assessed and used in estimating fair value.

If an entity is able to determine reliably the fair value of either the asset received or the asset given up, then the fair value of the asset given up is used to measure the cost of the asset received unless the fair value of the asset received is more clearly evident.

The cost of an item of property, plant and equipment held by a lessee under a finance lease is determined in accordance with IAS 17.

52

Convergence Between IFRSs and U.S. GAAP

Example :O’Neal Corporation exchanged equipment used in its manufacturing operations plus $3,000 in cash for similar equipment used in the operations of LT Corporation. The following information pertains to the exchange.

O’Neal LT Corporation Equipment (cost) $ 28,000 $ 28,000 Accumulated Depreciation 19,000 10,000Fair Value of Equipment 12,500 15,500Cash Give Up 3,000

53

Convergence Between IFRSs and U.S. GAAP

Exchange has commercial substanceO’Neal Corporation

Equipment 15,500*Accumulated Depreciation –Equipment 19,000

Equipment 28,000Cash 3,000Gain on Disposal of Equipment 3 500**Gain on Disposal of Equipment 3,500**

*Cost of new equipment:Cash paid $ 3,000Fair value of old equipment 12,500Cost of new equipment $ 15,500

**Computation of gain on disposal of equipment:Fair value of old equipment $12,500Book value of old equipment

($28,000 - $19,000) 9,000Gain on disposal of equipment $ 3,500

54

6/9/2009

19

Convergence Between IFRSs and U.S. GAAP

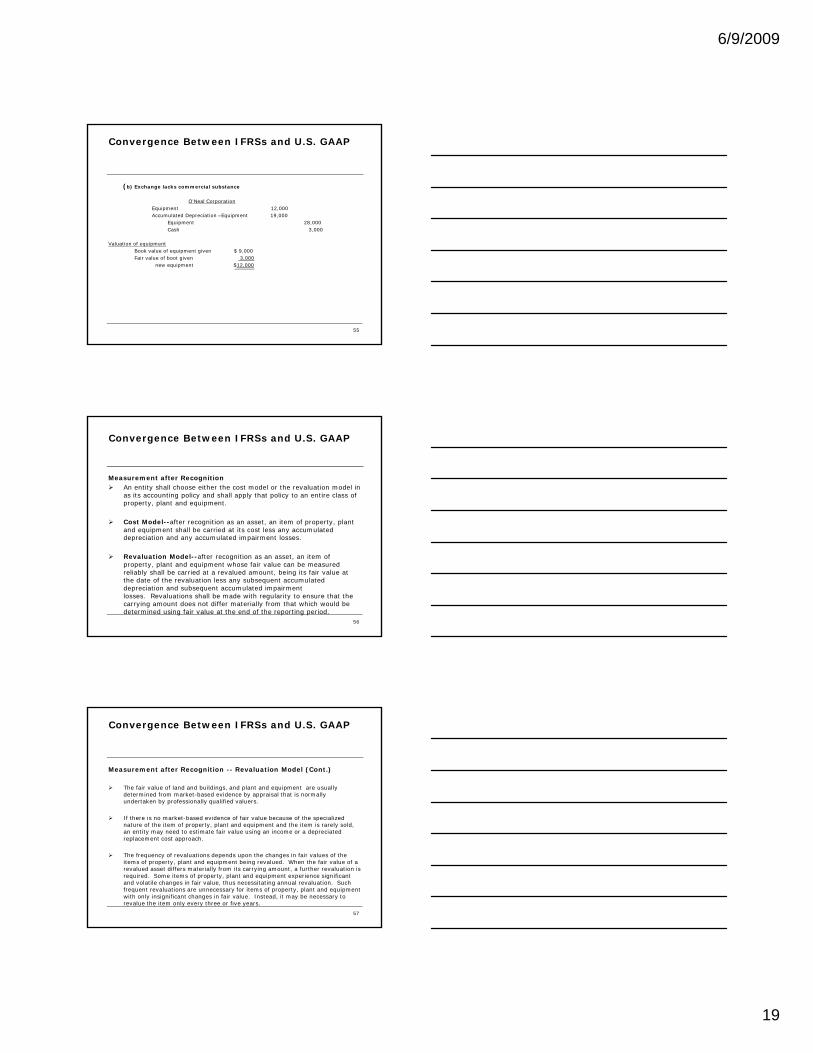

(b) Exchange lacks commercial substance

O’Neal CorporationEquipment 12,000Accumulated Depreciation –Equipment 19,000

Equipment 28,000Cash 3,000

Valuation of equipmentBook value of equipment given $ 9,000Fair value of boot given 3,000

new equipment $12,000

55

Convergence Between IFRSs and U.S. GAAP

Measurement after RecognitionAn entity shall choose either the cost model or the revaluation model in as its accounting policy and shall apply that policy to an entire class of property, plant and equipment.

Cost Model--after recognition as an asset, an item of property, plant and equipment shall be carried at its cost less any accumulated depreciation and any accumulated impairment losses.

Revaluation Model--after recognition as an asset, an item of property, plant and equipment whose fair value can be measured reliably shall be carried at a revalued amount, being its fair value at the date of the revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses. Revaluations shall be made with regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the end of the reporting period.

56

Convergence Between IFRSs and U.S. GAAP

Measurement after Recognition -- Revaluation Model (Cont.)

The fair value of land and buildings, and plant and equipment are usually determined from market-based evidence by appraisal that is normally undertaken by professionally qualified valuers.

If there is no market based evidence of fair value because of the specialized If there is no market-based evidence of fair value because of the specialized nature of the item of property, plant and equipment and the item is rarely sold, an entity may need to estimate fair value using an income or a depreciated replacement cost approach.

The frequency of revaluations depends upon the changes in fair values of the items of property, plant and equipment being revalued. When the fair value of a revalued asset differs materially from its carrying amount, a further revaluation is required. Some items of property, plant and equipment experience significant and volatile changes in fair value, thus necessitating annual revaluation. Such frequent revaluations are unnecessary for items of property, plant and equipment with only insignificant changes in fair value. Instead, it may be necessary to revalue the item only every three or five years.

57

6/9/2009

20

Convergence Between IFRSs and U.S. GAAP

Measurement after Recognition -- Revaluation Model(Cont.)

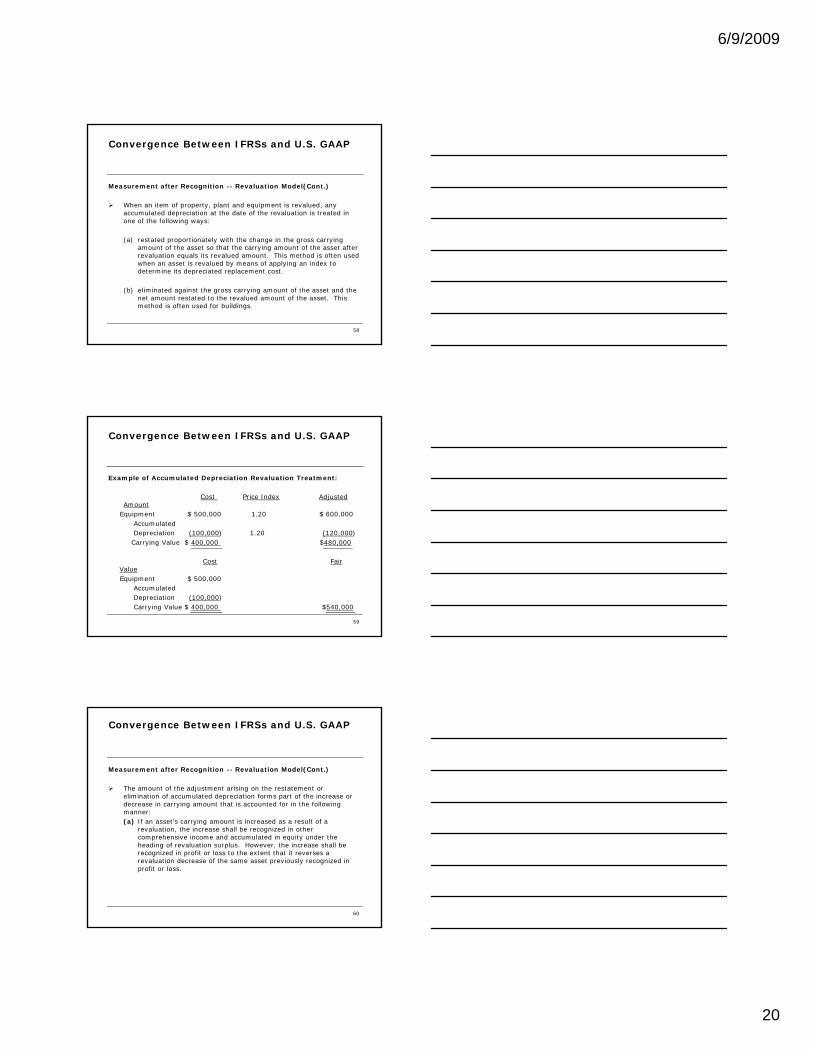

When an item of property, plant and equipment is revalued, any accumulated depreciation at the date of the revaluation is treated in one of the following ways:

(a) restated proportionately with the change in the gross carrying amount of the asset so that the carrying amount of the asset after revaluation equals its revalued amount. This method is often used when an asset is revalued by means of applying an index to determine its depreciated replacement cost.

(b) eliminated against the gross carrying amount of the asset and the net amount restated to the revalued amount of the asset. This method is often used for buildings.

58

Convergence Between IFRSs and U.S. GAAP

Example of Accumulated Depreciation Revaluation Treatment:

Cost Price Index Adjusted Amount

Equipment $ 500,000 1.20 $ 600,000Accumulated Depreciation (100,000) 1.20 (120,000)

Carrying Value $ 400,000 $480,000

Cost Fair Value Equipment $ 500,000

Accumulated Depreciation (100,000)Carrying Value $ 400,000 $540,000

59

Convergence Between IFRSs and U.S. GAAP

Measurement after Recognition -- Revaluation Model(Cont.)

The amount of the adjustment arising on the restatement or elimination of accumulated depreciation forms part of the increase or decrease in carrying amount that is accounted for in the following manner:(a) If an asset’s carrying amount is increased as a result of a

revaluation, the increase shall be recognized in other comprehensive income and accumulated in equity under the heading of revaluation surplus. However, the increase shall be recognized in profit or loss to the extent that it reverses a revaluation decrease of the same asset previously recognized in profit or loss.

60

6/9/2009

21

Convergence Between IFRSs and U.S. GAAP

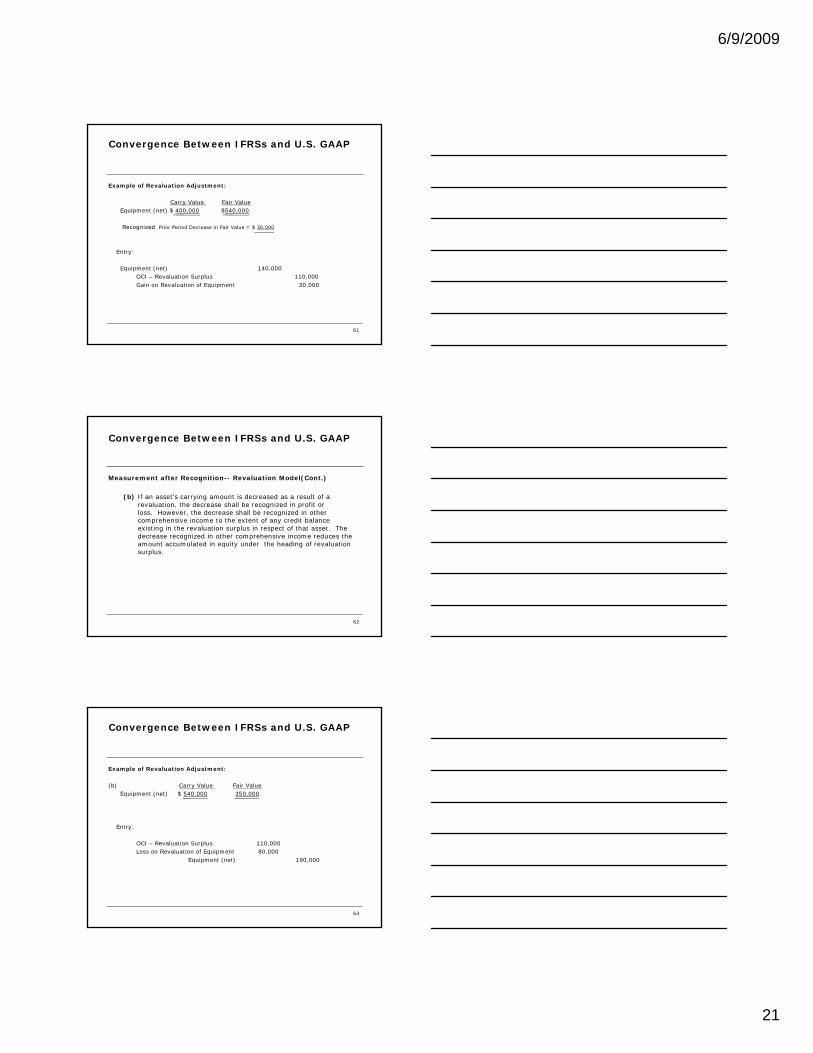

Example of Revaluation Adjustment:

Carry Value Fair ValueEquipment (net) $ 400,000 $540,000

Recognized Prior Period Decrease in Fair Value = $ 30,000

Entry:

Equipment (net) 140,000OCI – Revaluation Surplus 110,000Gain on Revaluation of Equipment 30,000

61

Convergence Between IFRSs and U.S. GAAP

Measurement after Recognition-- Revaluation Model(Cont.)

(b) If an asset’s carrying amount is decreased as a result of a revaluation, the decrease shall be recognized in profit or loss. However, the decrease shall be recognized in other comprehensive income to the extent of any credit balance

i ti i th l ti l i t f th t t Th existing in the revaluation surplus in respect of that asset. The decrease recognized in other comprehensive income reduces the amount accumulated in equity under the heading of revaluation surplus.

62

Convergence Between IFRSs and U.S. GAAP

Example of Revaluation Adjustment:

(b) Carry Value Fair ValueEquipment (net) $ 540,000 350,000

Entry:

OCI – Revaluation Surplus 110,000Loss on Revaluation of Equipment 80,000

Equipment (net) 190,000

63

6/9/2009

22

Convergence Between IFRSs and U.S. GAAP

Measurement after Recognition -- Revaluation Model(Concluded)

The revaluation surplus included in equity in respect of an item of property, plant and equipment may be transferred directly to retained earnings when the asset is derecognized. This may involve transferring the whole of the surplus when the asset is retired or di d f H f th l b t f d th disposed of. However, some of the surplus may be transferred as the asset is used by an entity. In such a case, the amount of the surplus transferred would be the difference between depreciation based on the revalued carrying amount of the asset and depreciation based on the asset’s original cost. Transfers from revaluation surplus to retained earnings are not made through profit or loss.

64

Outline for Convergence Between IFRSs and U.S. GAAP

I. Historical Background

II. Inventory

III. Interests in Joint Ventures (IAS 31)

IV. Leases (IAS 17)

V. IAS 16—Property, Plant and Equipment