george akello regional credit officer, africa standard chartered bank making credit decisions using...

TRANSCRIPT

George Akello

Regional Credit Officer, Africa

Standard Chartered Bank

Making Credit Decisions Using Credit Reports

1

2

Discussion points

Getting to the destination model

Creating efficiency and scale

Essential elements – Industry wide

Essential elements – bank wide

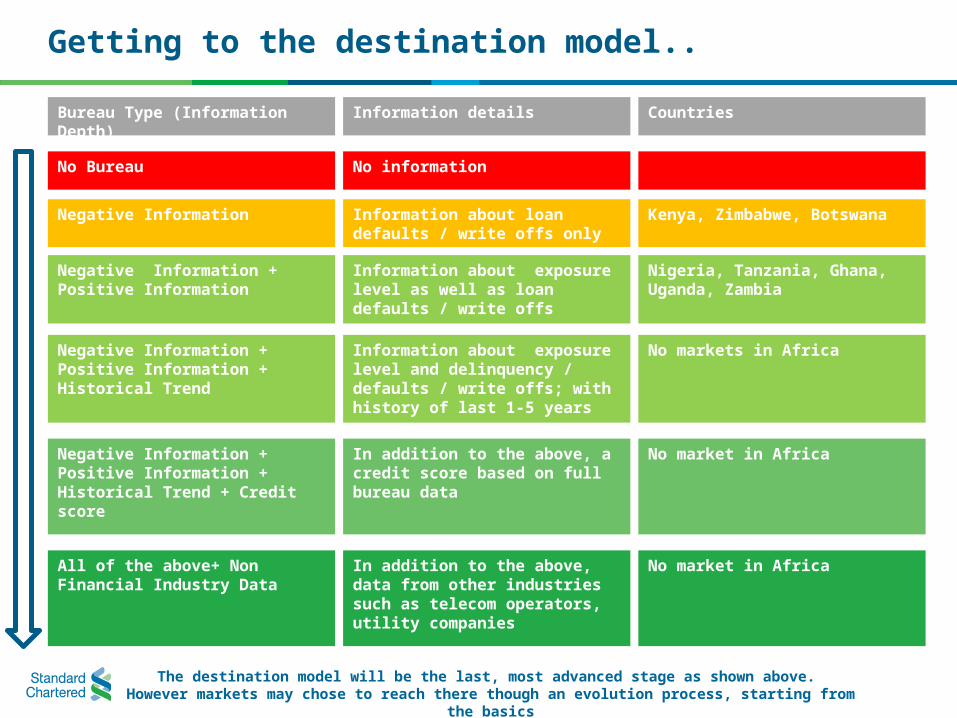

Getting to the destination model..

Negative Information Information about loan defaults / write offs only

Kenya, Zimbabwe, Botswana

Negative Information + Positive Information

Information about exposure level as well as loan defaults / write offs

Nigeria, Tanzania, Ghana, Uganda, Zambia

Negative Information + Positive Information + Historical Trend

Information about exposure level and delinquency / defaults / write offs; with history of last 1-5 years

No markets in Africa

Negative Information + Positive Information + Historical Trend + Credit score

In addition to the above, a credit score based on full bureau data

No market in Africa

All of the above+ Non Financial Industry Data

In addition to the above, data from other industries such as telecom operators, utility companies

No market in Africa

No Bureau No information

Bureau Type (Information Depth) Information details Countries

The destination model will be the last, most advanced stage as shown above. However markets may chose to reach there though an evolution process, starting from the basics

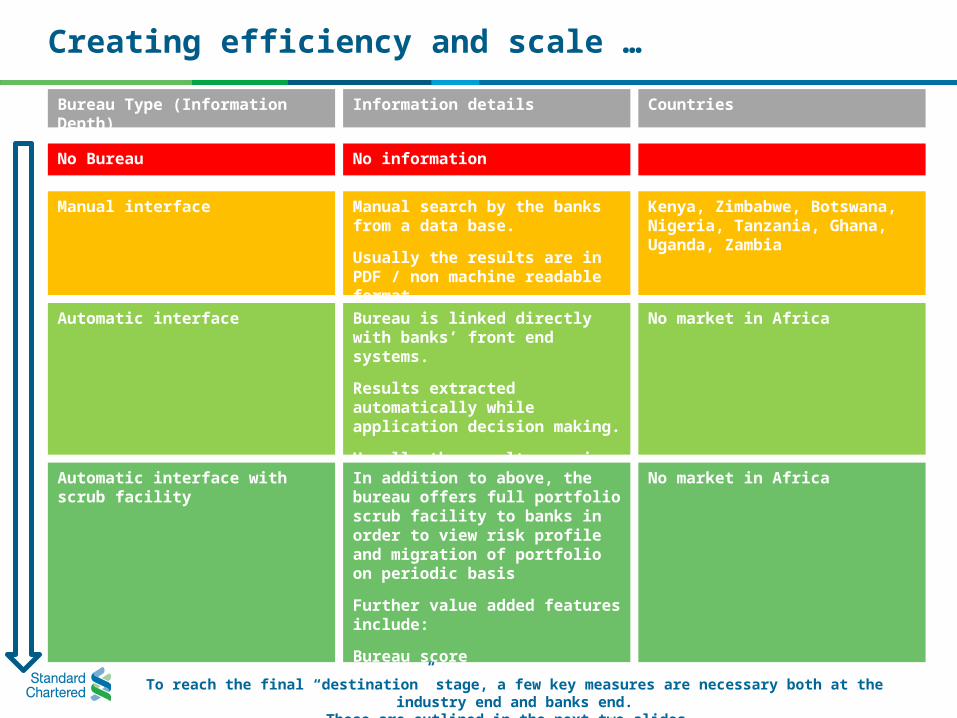

Manual interface Manual search by the banks from a data base.

Usually the results are in PDF / non machine readable format

Kenya, Zimbabwe, Botswana, Nigeria, Tanzania, Ghana, Uganda, Zambia

Automatic interface Bureau is linked directly with banks’ front end systems.

Results extracted automatically while application decision making.

Usually the results are in machine readable format.

No market in Africa

Automatic interface with scrub facility In addition to above, the bureau offers full portfolio scrub facility to banks in order to view risk profile and migration of portfolio on periodic basis

Further value added features include:

Bureau score

Default triggers

No market in Africa

No Bureau No information

Creating efficiency and scale …

Bureau Type (Information Depth) Information details Countries

To reach the final “destination” stage, a few key measures are necessary both at the industry end and banks end.These are outlined in the next two slides.

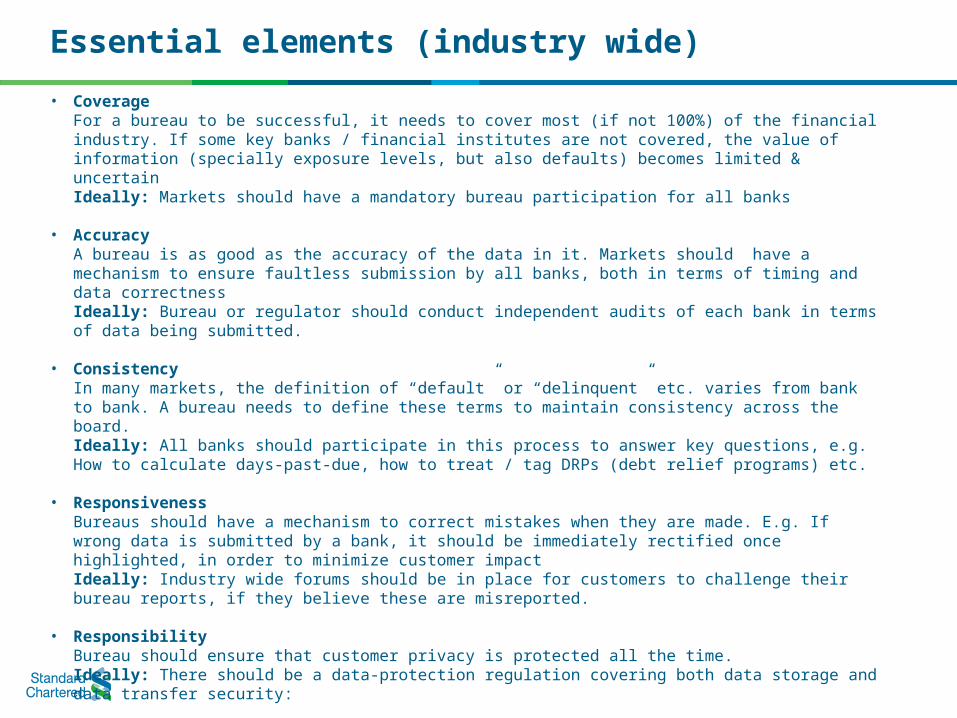

• CoverageFor a bureau to be successful, it needs to cover most (if not 100%) of the financial industry. If some key banks / financial institutes are not covered, the value of information (specially exposure levels, but also defaults) becomes limited & uncertainIdeally: Markets should have a mandatory bureau participation for all banks

• AccuracyA bureau is as good as the accuracy of the data in it. Markets should have a mechanism to ensure faultless submission by all banks, both in terms of timing and data correctnessIdeally: Bureau or regulator should conduct independent audits of each bank in terms of data being submitted.

• ConsistencyIn many markets, the definition of “default” or “delinquent” etc. varies from bank to bank. A bureau needs to define these terms to maintain consistency across the board. Ideally: All banks should participate in this process to answer key questions, e.g. How to calculate days-past-due, how to treat / tag DRPs (debt relief programs) etc.

• ResponsivenessBureaus should have a mechanism to correct mistakes when they are made. E.g. If wrong data is submitted by a bank, it should be immediately rectified once highlighted, in order to minimize customer impactIdeally: Industry wide forums should be in place for customers to challenge their bureau reports, if they believe these are misreported.

• ResponsibilityBureau should ensure that customer privacy is protected all the time.Ideally: There should be a data-protection regulation covering both data storage and data transfer security:

• Reach abilityWhile the bureau service has its cost, the pricing of these services should be managed to ensure that its not too high for bank’s to consider bureau participation unviable. Nor it should be too low for bureau to be unable to sustain itself.Ideally: Industry should jointly determine the optimal pricing level for bureau services, acceptable by all stake holders

Essential elements (industry wide)

• AwarenessBanks should make sure that their customers are aware of dynamics of the bureau, and the fact that their information will be shared. If mandated by regulator, customer consent before information sharing is essential.Ideally: Before participating in a bureau, banks should run a customer, as well as staff, awareness campaign on above lines

• Data AccuracyBanks should make a concrete effort to make sure their data (including historical delinquency info) is accurate. This also includes consistency of definitions with industry & bureauIdeally: Before participating in bureau, a data clean up exercise should be done

• Data SecurityTechnology should be in place to ensure transfer and storage of data is secure and fool proof.Ideally: Bank’s tech team should be in the loop to ensure latest security mechanism is in place

• Resources & FundingEvery bank participating in the bureau needs to have dedicated resources including staff who will report to the bureau, or extract bureau info, as well as technology to transmit the data to and from the bureau.Ideally: Technology team should be in the loop at all stages of bureau participation.

• Policy ChangesOnce credit information sharing becomes a norm, and bureau is fully operational, the banks should have robust policies in place to benefit from these elements. These may include

• DBR policies capturing full industry exposure• Bureau score usage for TTD as well as portfolio actions• Proactive line management actions in the event of off-us performance deterioration• Incorporating bureau variables in in-house scoring models,• Verification process based on customer contact details given in the bureau

Essential elements (bank wide)