geopolitical risk in port multi asset · » bloomberg port includes state- of-the-art portfolio...

TRANSCRIPT

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

GEOPOLITICAL RISK IN PORT MULTI ASSET RISK MODEL

ADVANCED PORTFOLIO RISK AND ANALYTICS TOOLS TO BUILD BETTER PORTFOLIOS IN PORT<GO> SEP// 16 // 2014

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

SUMMARY 2

» Webinar details

» What are risk factor models and why use them

» Bloomberg multi-asset class risk models

» Model coverage

» Geopolitical risk example

» Identifying sources of portfolio risk and return:

• Factor based performance attribution (FBA)

• Tracking Error breakdown

» How to reduce the major sources of geopolitical risk

» Q&A

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

WEBINAR DETAILS

» On Demand • This webinar will be available ON DEMAND starting on

9/18/14 and available for 90 days » Slide availability

• The slides will be available through the ON DEMAND link to view this webinar; they will also be attached to the post webinar mailing

» Q&A • We will attempt to answer as many questions as possible • Additional answers to questions asked during today’s webinar

will be aggregated and part of the post-mailing sent out the following week

» Inviting a colleague • If you’d like to invite a colleague to view the ON DEMAND

version of this presentation, they may register at www.bloomberglp.com/PORTgeorisk

3

GEO

POLI

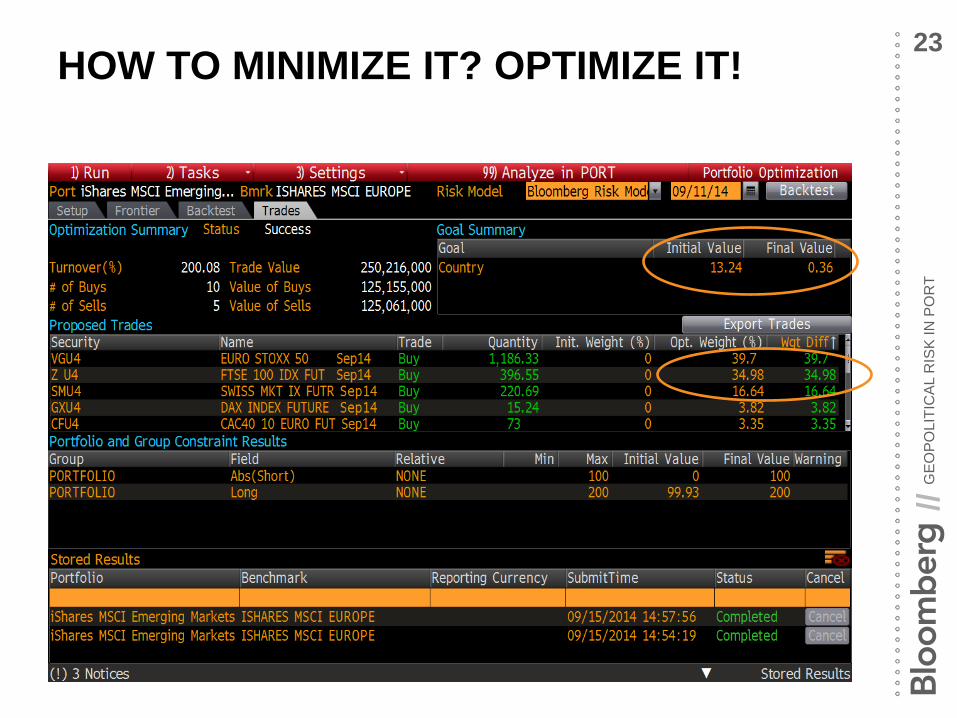

TIC

AL R

ISK

IN P

OR

T //

PORTFOLIO & RISK ANALYTICS OVERVIEW

4

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

A PREVIEW 5

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

WHAT ARE FACTOR MODELS? 6

itktkttit fbfbfbr ε++++= ...2211

Factor Returns Non-Factor Returns

Security Returns

Factor Exposures (sensitivities)

This return decomposition also allows easy risk decomposition: • Need exposures, b • Factor covariances • Non-factor risk magnitudes

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

WHY USE FUNDAMENTAL FACTOR MODELS?

• Intuitive decomposition of portfolio return and risk into exposures and factors

• Actionable: e.g. “I need to increase my Korea exposure” or “I want to lower exposure to the long end of the swap curve”

• A relatively small number of key factors explain risk/return of millions of securities=> on-the-fly risk calculations even for very large portfolios

• Can cover securities with (almost) no data: EM assets, IPOs, new issues

• High predictive ability, good at separating signal from noise

7

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

BLOOMBERG REGIONAL MODEL: FACTOR HIERARCHY

Regional Model

USD FI

Curve

6m

1 yr

2 yr

…

Conv

Vol

Spread

Sov

Agcy

Corp

EUR FI

Curve

6m

1 yr

2 yr

…

Conv

Vol

Spread

Sov

Corp

Agency

EM FI

Local currency

Hard currency

EU Equity

Market Country

Germany

UK

…

Industry

Auto

Media

…

Style

Value

Growth

Size

Momentum

…

FX

EUR

JPY

CAD

GBP

…

Commodity

Agri

Energy

Nat Gas

Metals

…

Greeks

Vega

Gamma

8

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

BLOOMBERG REGIONAL MODEL: ~1500+ FACTORS

• EQUITY: ~400 FACTORS • (100 Market/Country + 200 Industry + 100 Style)

• FIXED INCOME: ~720 FACTORS • (450 curve + 270 Spread)

• FX: ~160 FACTORS • COMMODITY: ~220 FACTORS

• (60 Agri + 10 Coal + 70 Crude + 15 Electricity + 30 Metals +

• 15 Nat Gas + 20 Shipping)

• GREEKS ~20 FACTORS

SEE MORE DETAILS ON HELP PORT<GO>

9

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

RISK MODEL ASSET TYPE COVERAGE • Equities: REITs, ADR, GDR, NVDR, ordinary and preferred classes, 80,000+ issues

• Sovereign, agency, corporate bonds in almost all developed and emerging markets

• Securitized: ABS, CMBs, RMBS, ARMs, TBAs, Agency CMOs, pools

• Sovereign inflation linked bonds

• Municipal bonds

• Bank loans

• Money market securities

• Convertible bonds

• Preferred and hybrid preferred

• CDS/CDX

• IRS

• Equity, single stock, commodity and volatility (VIX) futures

• Bond futures, STIR futures

• Options on equity futures, options on VIX ETF

• Equity, FI, commodity and balanced ETFs

• Listed equity, index, and commodity options

• FX futures and forwards

• Equity, FI, commodity and balanced funds without holdings

10

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

EXAMPLE: SAMSUNG STOCK IN A REGIONAL MODEL

11

$

:$

Pr

11112.22 0.530.71 0.47

... 0.70

Asia

Korea

KRW

Semicond

Size Value

ofit Growth

Leverage

r fffx

ff ff f

fε

= ∗

+ ∗+ ∗∆

+ ∗+ ∗ + ∗+ ∗ + ∗

− ∗

+

Market return

Country return

Currency return

Industry return

Style returns

Factor returns

Non-Factor return

As of: 10/30/13

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

EXAMPLE: SAMSUNG STOCK IN A REGIONAL MODEL

12

$

:$

Pr

11112.22 0.530.71 0.47

... 0.70

Asia

Korea

KRW

Semicond

Size Value

ofit Growth

Leverage

r fffx

ff ff f

fε

= ∗

+ ∗+ ∗∆

+ ∗+ ∗ + ∗+ ∗ + ∗

− ∗

+

Market return

Country return

Currency return

Industry return

Style returns

Factor returns

Non-Factor return

As of: 10/30/13

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

GEOPOLITICAL RISK EXAMPLE 13

Look at Eastern Europe ETF vs Europe ETF: ESR US vs IMEU LN

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

GEO POLITICAL RISK EXAMPLE • LOOK AT EASTERN EUROPE ETF VS EUROPE ETF:

ESR US VS IMEU LN

14

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

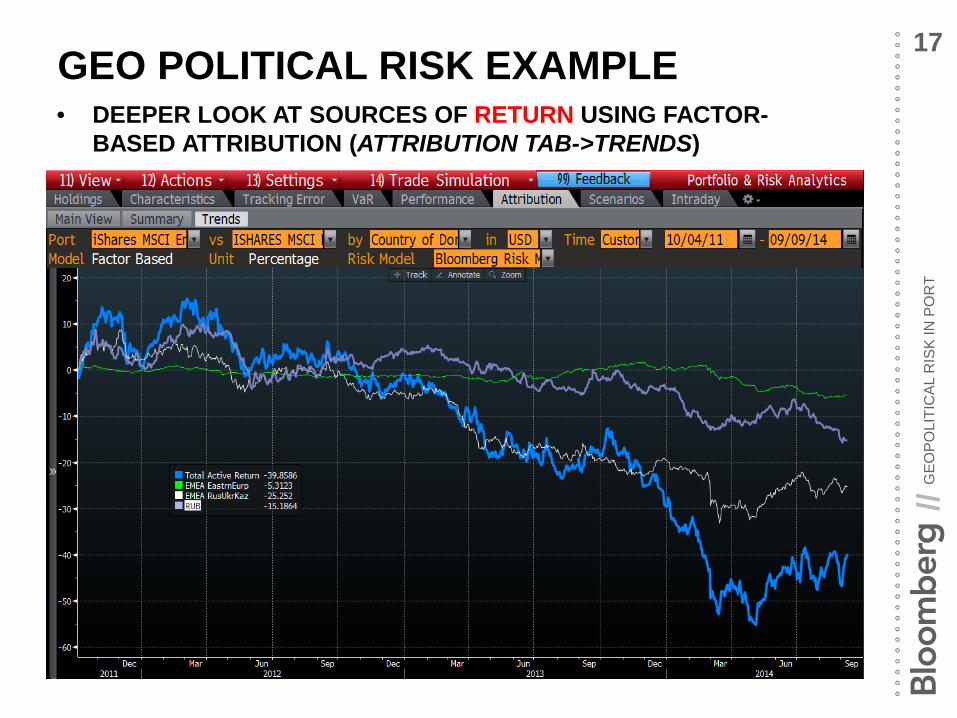

GEO POLITICAL RISK EXAMPLE • DEEPER LOOK AT SOURCES OF RETURN USING FACTOR-

BASED ATTRIBUTION (ATTRIBUTION TAB->SUMMARY)

15

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

GEO POLITICAL RISK EXAMPLE • DEEPER LOOK AT SOURCES OF RETURN USING FACTOR-

BASED ATTRIBUTION (ATTRIBUTION TAB->SUMMARY)

16

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

GEO POLITICAL RISK EXAMPLE • DEEPER LOOK AT SOURCES OF RETURN USING FACTOR-

BASED ATTRIBUTION (ATTRIBUTION TAB->TRENDS)

17

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

DID THE MODEL SEE THIS IN 2011? • DEEPER LOOK AT SOURCES OF RISK USING FACTOR-

BASED RISK (TRACKING ERROR TAB->SUMMARY)

18

This is risk forecast as of Oct 2011

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

HOW TO MINIMIZE IT? OPTIMIZE IT! 19

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

HOW TO MINIMIZE IT? OPTIMIZE IT! 20

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

HOW TO MINIMIZE IT? OPTIMIZE IT! 21

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

HOW TO MINIMIZE IT? OPTIMIZE IT! 22

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

HOW TO MINIMIZE IT? OPTIMIZE IT! 23

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

HOW TO MINIMIZE IT? OPTIMIZE IT! 24

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

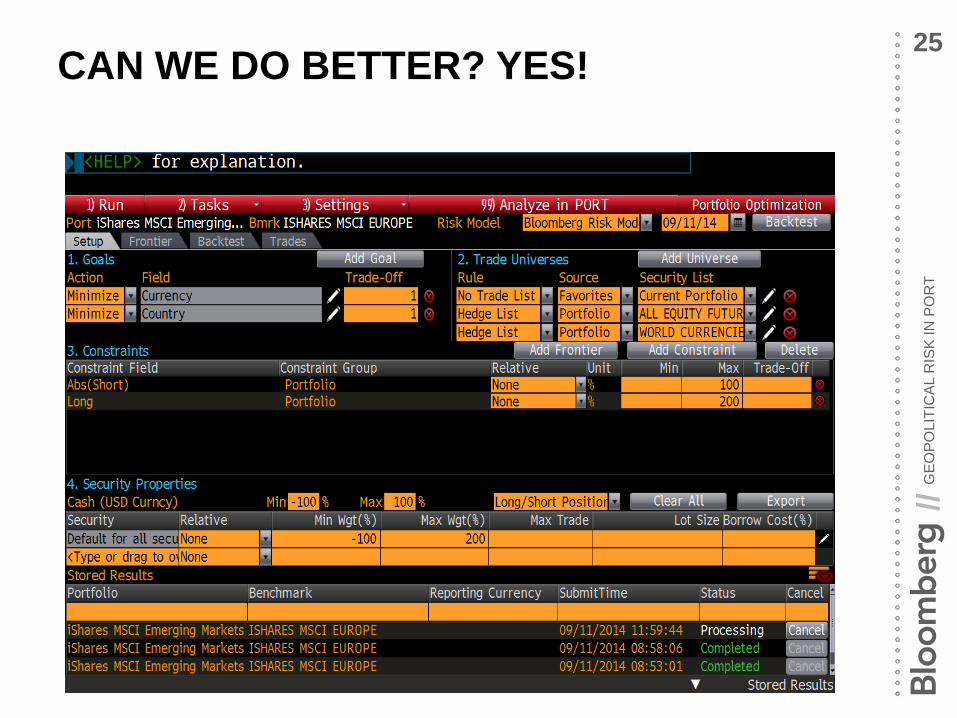

CAN WE DO BETTER? YES! 25

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

CAN WE DO BETTER? YES! 26

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

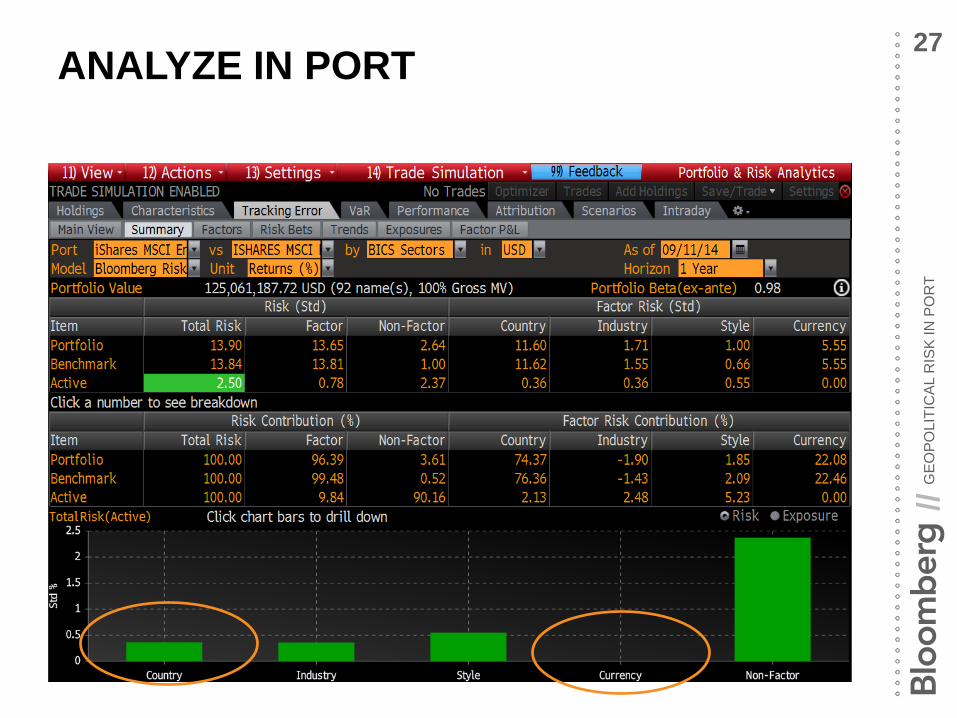

ANALYZE IN PORT 27

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

CONCLUSION 28

» Factor models help analyze risk and return sources

» Country and currency factors are significant sources of risk and return that is commonly known as geopolitical risk

» Bloomberg PORT includes state-of-the-art portfolio construction tools which help investors construct better portfolios through hedging of unwanted risk sources and retain exposure to desired risk factors

» For more information on PORT type HELP PORT<go>

GEO

POLI

TIC

AL R

ISK

IN P

OR

T //

WEBINAR DETAILS - RECAP

» On Demand • This webinar will be available ON DEMAND starting on

9/18/14 and available for 90 days » Slide availability

• The slides will be available through the ON DEMAND link to view this webinar; they will also be attached to the post webinar mailing

» Q&A • We will attempt to answer as many questions as possible • Additional answers to questions asked during today’s webinar

will be aggregated and part of the post-mailing sent out the following week

» Inviting a colleague • If you’d like to invite a colleague to view the ON DEMAND

version of this presentation, they may register at www.bloomberglp.com/PORTgeorisk

29

//

>>>>>>>>>>>>>> CONTACT [email protected] New York +1 212 617 7070 London +44 20 7330 7099 Singapore +65 6212 9798