genivi alliance: smartphone connectivity · genivi alliance: smartphone connectivity means and...

TRANSCRIPT

GENIVI Alliance:Smartphone ConnectivitySmartphone ConnectivityMeans and Outlook

Roger C. Lanctot, Associate DirectorGl b l A t ti P tiGlobal Automotive PracticeStrategy Analytics

October 2012October 2012

New policyNew policy

Has unfortunate consequencesHas unfortunate consequences

Hopefully vehicle connectivity will be part of the solution, not part of the problem!the problem!

Global Safety Outlook, OpportunityGlobal Safety Outlook, Opportunity

5

Connecting the Car: The Big PictureConnecting the Car: The Big Picture

Drives – OUT; Displays ‐ INDrives OUT; Displays IN3G/LTE Connectivity on the way for CRMSmartphone accommodation to sellSmartphone accommodation to sell carsDigital radio for low cost, low distraction content delivery

6

distraction content delivery

Connectivity ECU ‐ OEM:Regional ShipmentsRegional Shipments

35 000

40,000Rest Of the World

20 000

25,000

30,000

35,000

000'

s)

BrazilRussiaIndiaChi

5 000

10,000

15,000

20,000

Uni

ts (0 China

JapanSouth KoreaEurope

0

5,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

North America

• Connectivity ECU growth opportunity 2011 vs 2019:• Connectivity ECU growth opportunity 2011 vs. 2019:

– ECU Shipments: 4.5 mil units in 2011 to 38.7 million units in 2019 (CAGR 31%)

– ECU Revenues: $460 mil in 2011 to $2.9 Billion in 2019 (CAGR 26%)

A S lli P i– Average Selling Price:

– $100/unit in 2011 $75/unit in 2019

Source: Automotive Multimedia & Communications ‐ AMCS

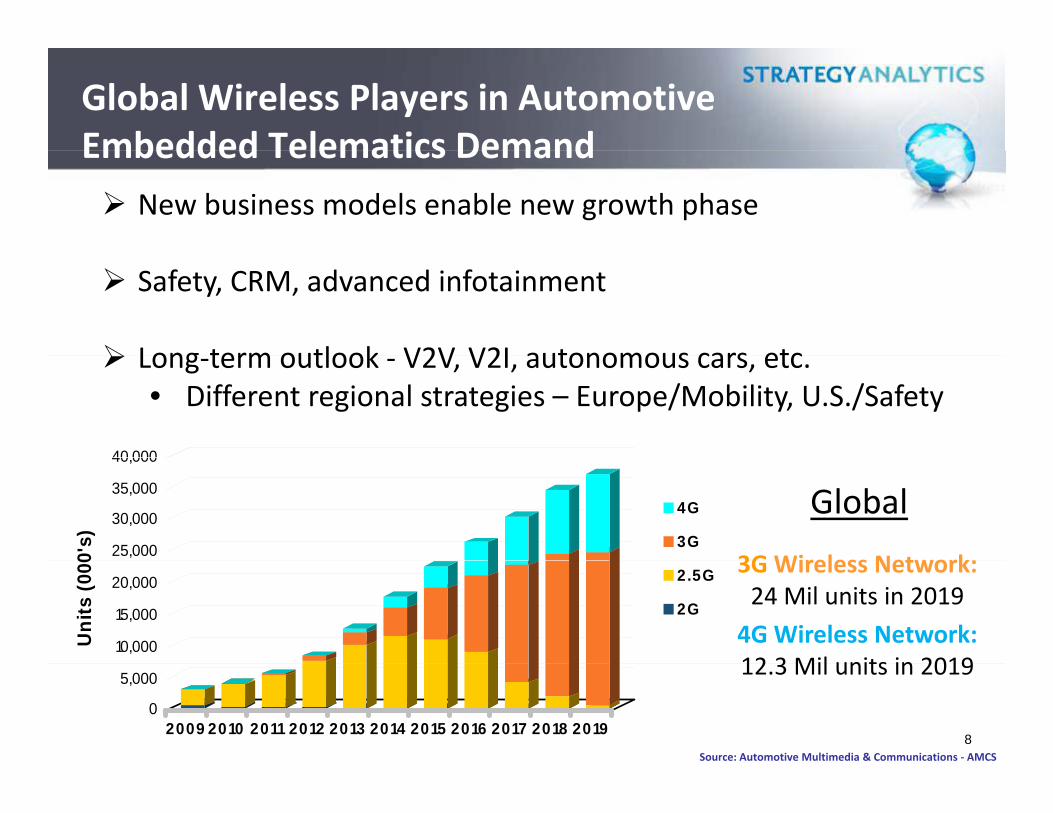

Global Wireless Players in Automotive Embedded Telematics DemandEmbedded Telematics Demand

New business models enable new growth phase

Safety, CRM, advanced infotainment

Long term outlook V2V V2I autonomous cars etcLong‐term outlook ‐ V2V, V2I, autonomous cars, etc.• Different regional strategies – Europe/Mobility, U.S./Safety

40 000

25,000

30,000

35,000

40,000

0's)

4G

3G3GWireless Network:

Global

10,000

15,000

20,000

Uni

ts (0

00 2 .5G

2G

3GWireless Network: 24 Mil units in 2019

4G Wireless Network: 12 3 Mil units in 2019

8Source: Automotive Multimedia & Communications ‐ AMCS

0

5,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

12.3 Mil units in 2019

Telematics ECU: OEM Regional Shipment ViewOEM Regional Shipment View

35,000

40,000Rest Of the World

20,000

25,000

30,000

(000

's)

BrazilRussiaIndiaChina

5 000

10,000

15,000

,

Uni

ts China

JapanSouth KoreaEurope

• North America: eCall/Telematics highly dependent on car maker strategies

0

5,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

North America

• North America: eCall/Telematics highly dependent on car maker strategies

• Europe: eCall telematics highly dependent on regulatory activity and selected OEMs

• Japan: Navigation is still dominant, Telematics roll‐out is lead by Toyota

• China: Forecast to be #3 Player in embedded Telematics ECU Globally by 2014

Source: Automotive Multimedia & Communications ‐ AMCS

Automotive HMI: The Rise of the Display – 2012 updateThe Rise of the Display 2012 update

‘Pre‐iPhone’ Phase

Source: Automotive Multimedia & Communications ‐ AMCS

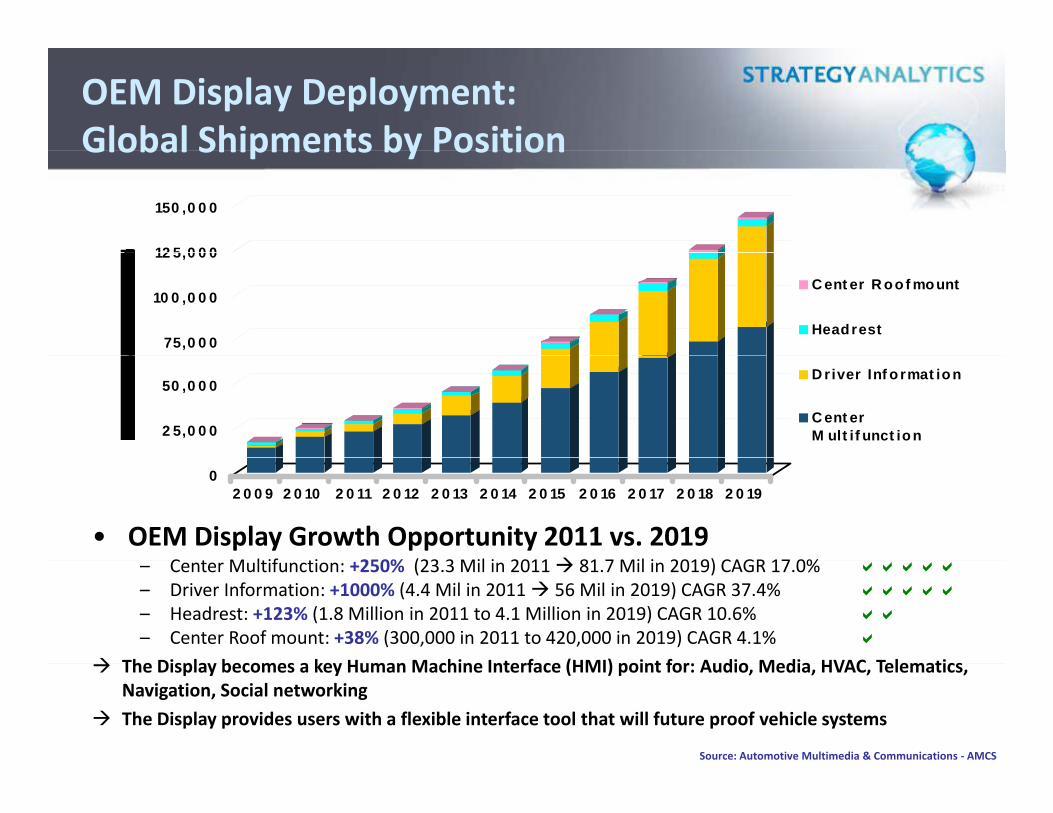

OEM Display Deployment: Global Shipments by PositionGlobal Shipments by Position

12 5 0 0 0

150 ,0 0 0

75,0 0 0

10 0 ,0 0 0

12 5,0 0 0

C ent er R oo f mount

Headrest

2 5,0 0 0

50 ,0 0 0D river Inf o rmat io n

C ent erM ult if unct ion

02 0 0 9 2 0 10 2 0 11 2 0 12 2 0 13 2 0 14 2 0 15 2 0 16 2 0 17 2 0 18 2 0 19

• OEM Display Growth Opportunity 2011 vs. 2019C t M ltif ti 250% (23 3 Mil i 2011 81 7 Mil i 2019) CAGR 17 0%– Center Multifunction: +250% (23.3 Mil in 2011 81.7 Mil in 2019) CAGR 17.0%

– Driver Information: +1000% (4.4 Mil in 2011 56 Mil in 2019) CAGR 37.4% – Headrest: +123% (1.8 Million in 2011 to 4.1 Million in 2019) CAGR 10.6%– Center Roof mount: +38% (300,000 in 2011 to 420,000 in 2019) CAGR 4.1%

The Display becomes a key Human Machine Interface (HMI) point for Audio Media HVAC TelematicsThe Display becomes a key Human Machine Interface (HMI) point for: Audio, Media, HVAC, Telematics, Navigation, Social networking

The Display provides users with a flexible interface tool that will future proof vehicle systems

Source: Automotive Multimedia & Communications ‐ AMCS

OEM Headunit: Prem. & Branded Audio ShipmentsPrem. & Branded Audio Shipments

20 000

25,000

s)

15,000

20,000

Uni

ts (0

00's

Premium Audio

Branded Audio

5,000

10,000

Glo

bal U Surround (5.1/7.1)

• Feature Trend/Opportunity: 2011 vs. 2019

02009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

– Premium Audio: Growing interest in midrange vehicle segment

• Market Shipments: 9.0 Mil to 21 Mil units (130% Growth, CAGR 11%)

– Branded Audio: OEM’s are adopting ‘Brands’ to add value to Premium audio

M k Shi 6 4 Mil 16 4 Mil i (156% G h CAGR 12 5%)• Market Shipments: 6.4 Mil to 16.4 Mil units (156% Growth, CAGR 12.5%)

– Surround Sound (5.1/7.1): Currently low penetration across all vehicle segments

• Market Shipments: 4 Mil to 15.1 Mil units (270% growth, CAGR 17.9%)Source: Automotive Multimedia & Communications ‐ AMCS

OEM Headunit: Optical Media and StorageOptical Media and Storage

70 000

80,000

90,000

40 000

50,000

60,000

70,000

Uni

ts (0

00's

) Mechless

CD/DVD (Single)

CD/DVD (Changer)

10 000

20,000

30,000

40,000

Glo

bal Blu- ray

HDD

Flash Slot

0

10,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

• Headunit Feature Trend/Opportunity: 2011 vs. 2019Headunit Feature Trend/Opportunity: 2011 vs. 2019Mechless: 69% of vehicles worldwide will be ‘solid‐state’ by 2019 (2.6% in 2011)

– CD/DVD Changer: Headunit availability falls to 1.9% WW by 2019 (29% in 2011)

– Blu‐ray: Compatible drive in 1.0% of headunits WW by 2019 (0% in 2011)

– HDD: Available on 1.1% of headunits WW by 2019 (7.6% in 2011)

– Flash card slot: Available on 25% of headunits WW by 2019 (8.3% in 2011)

Source: Automotive Multimedia & Communications ‐ AMCS

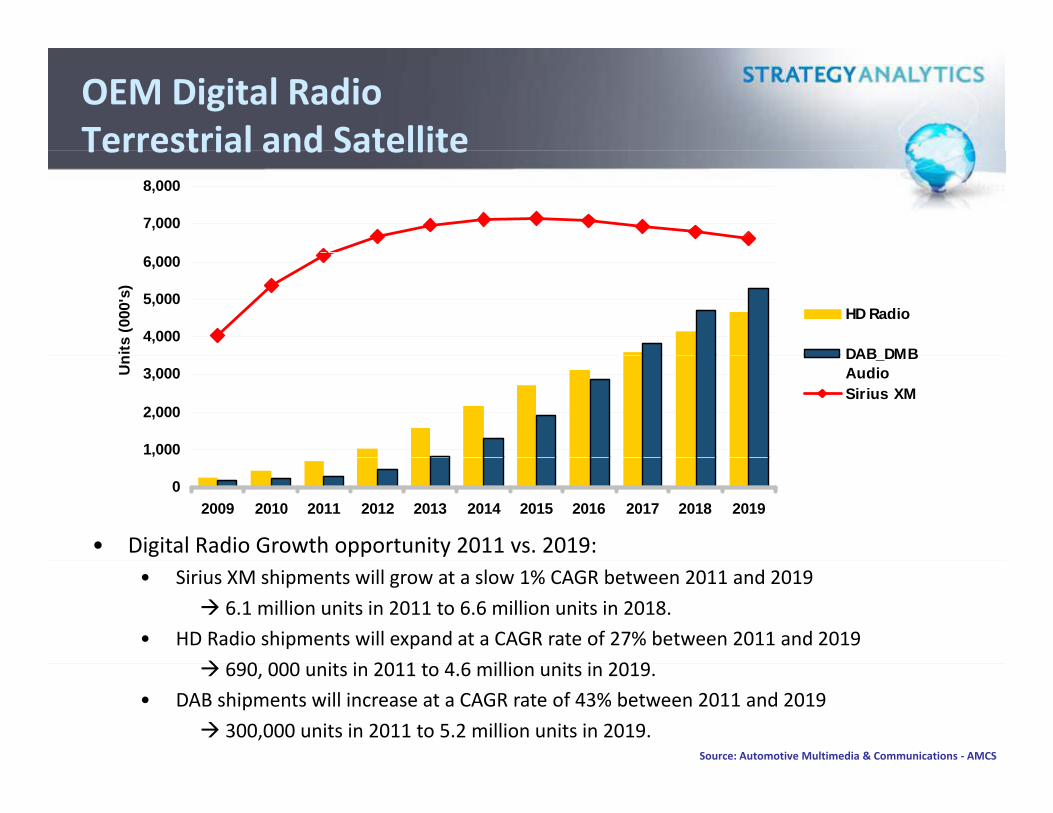

OEM Digital RadioTerrestrial and SatelliteTerrestrial and Satellite

7,000

8,000

4,000

5,000

6,000

its (0

00's

)

HD Radio

DAB DMB

1,000

2,000

3,000 Un DAB_DMB

AudioSirius XM

02009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

• Digital Radio Growth opportunity 2011 vs. 2019:• Sirius XM shipments will grow at a slow 1% CAGR between 2011 and 2019

6.1 million units in 2011 to 6.6 million units in 2018.• HD Radio shipments will expand at a CAGR rate of 27% between 2011 and 2019

690 000 i i 2011 4 6 illi i i 2019690, 000 units in 2011 to 4.6 million units in 2019. • DAB shipments will increase at a CAGR rate of 43% between 2011 and 2019

300,000 units in 2011 to 5.2 million units in 2019. Source: Automotive Multimedia & Communications ‐ AMCS

Must Have Infotainment – Western EuropeMust Have Infotainment Western Europe

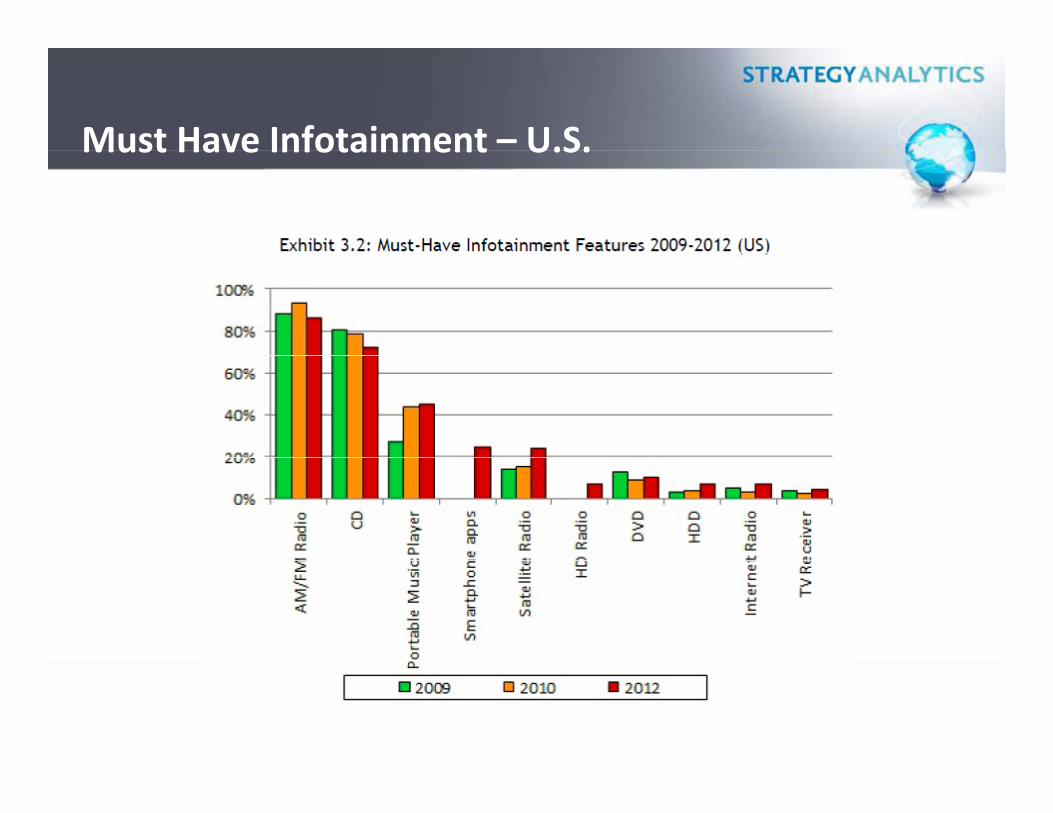

Must Have Infotainment – U.S.Must Have Infotainment U.S.

Connecting the Car to the InternetConnecting the Car to the Internet

H ?How?Why?Why?

17

Connecting the Car to the InternetConnecting the Car to the Internet

How?Consumer’s phoneE b dd d dEmbedded modem

18

Connecting the Car to the InternetConnecting the Car to the Internet

Why?yTo sell content, applications and servicesTo enhance safety and security (mandates)To enhance navigationTo enhance drivingT h i hi l t t i tTo enhance in‐vehicle entertainmentTo sell more carsTo capture more of aftersales opportunity:To capture more of aftersales opportunity:

For OEMs, aftersales represents ~15% of

19

For OEMs, aftersales represents 15% of revenue and 70% of profits

Connecting the Car to the InternetConnecting the Car to the Internet

Other reasons to connect?Cost avoidance – limit warranty exposureAnticipate/diagnose system failuresSuperior customer service experienceChanging ownership scenarios – ride sharing,

h i l tcar sharing, lease, rentAlternative powertrain requirements – ie. EV

chargingchargingNew insurance models – usage‐based insuranceITS, traffic mgmt, V2X, tolling

20

To sell more cars!

Connecting the Car to the InternetConnecting the Car to the Internet

H t t?How to connect?Easy way: embedded modemEasy way: embedded modemHard way: customer’s phone

Reality:Reality:Nothing is easy

21

Everything is expensive

Connecting the Car to the InternetConnecting the Car to the Internet

Customer’s phone scenario:Customer s phone scenario: BYOC: Bring Your Own Connection

Leverage customer’s data planEnable access to customer’s:Enable access to customer s:

Preferred apps, contacts, content, POIs routes social networkPOIs, routes, social network

Potentially superior network, connections

E bl i ti bil t22

Enable existing mobile payments

Connecting the Car to the InternetConnecting the Car to the Internet

BYOC: The DownsideBYOC: The DownsideLoss of customer controlS ti lti l OSSupporting multiple OSesMaintaining software APIsP idi d i f i hi l i t fProviding drive‐safe in‐vehicle interfacesSupporting third‐party navigation, voice

iti l ti irecognition, location services

23

Barbarians in the DashboardBarbarians in the Dashboard

24

GENIVI’s contribution to the discussionGENIVI s contribution to the discussion

Highlighted proliferation of openHighlighted proliferation of open source software

HighlightedHighlighted virtualization/hypervisoryp

25

GENIVI’s contribution to the discussionGENIVI s contribution to the discussion

Examples

26

Toyota Entune (Denso)Toyota Entune (Denso)

BingOpen Table

MT.com IHRgTable

UIEngine

Nav AM/FM

UIEngine

OSBus

OS

TCP/IP/

WiFi BluetoothTelematics

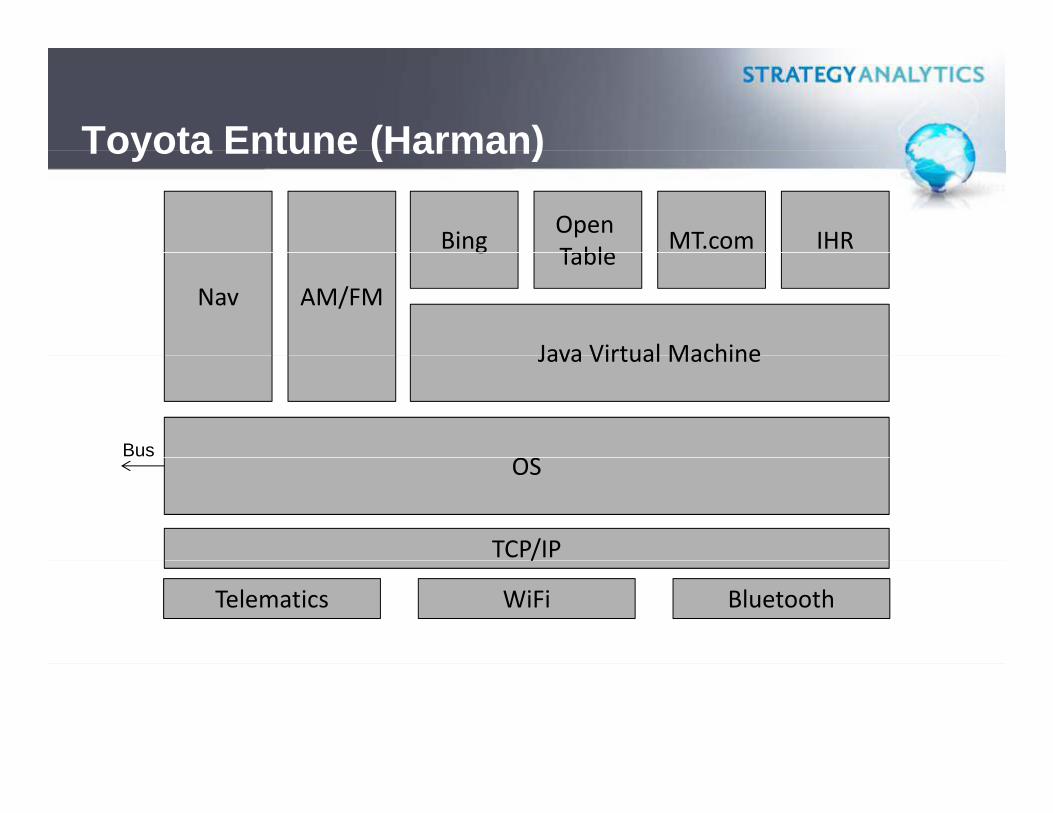

Toyota Entune (Harman)

BingOpen Table

MT.com IHR

Toyota Entune (Harman)

gTable

Java Virtual Machine

Nav AM/FM

Java Virtual Machine

OSBus

OS

TCP/IP/

WiFi BluetoothTelematics

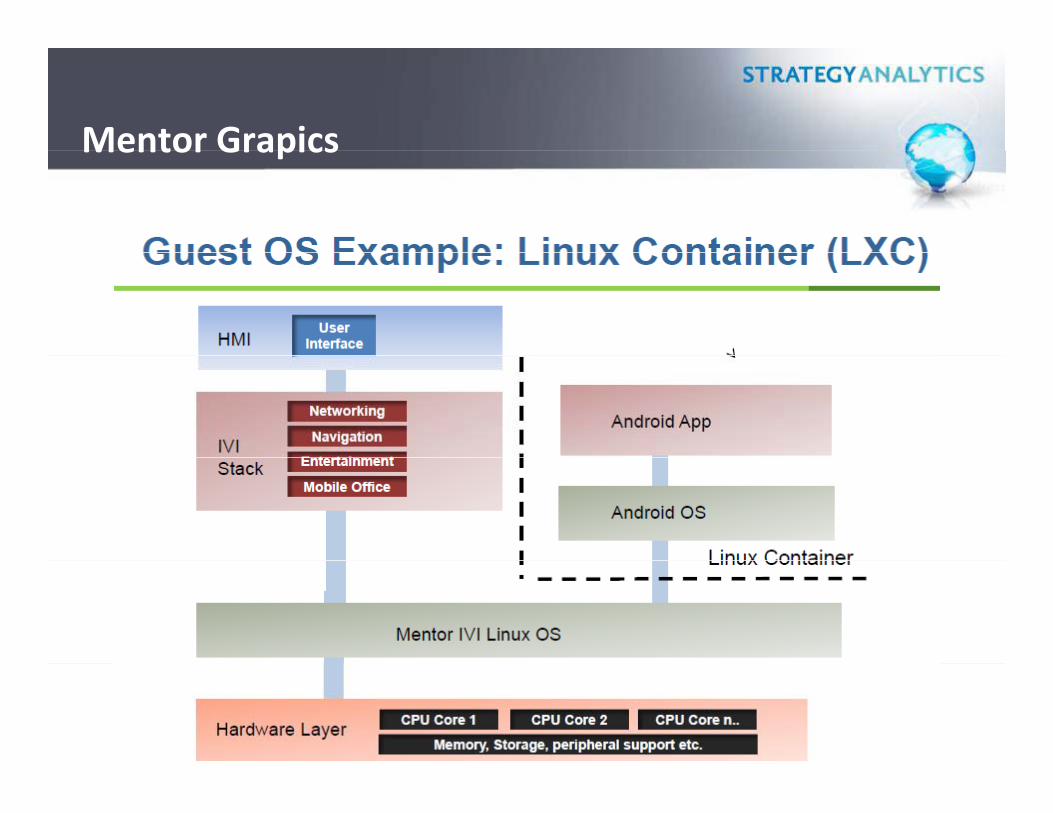

Mentor GrapicsMentor Grapics

Infotainment Services:IP Bandwidth Segmentation

Mid/Low Value – Growing Market Interest

IP Bandwidth SegmentationHigh Value ‐ Growing Market Interest

Weather, Stocks, data, News PAYD – User based Insurance

Location based services

Eco‐DrivingRoad tolling

EV Charging and billing

Basic Traffici l d

Internet radio Workflow Management/Fleet

High Definition Traffic

Remote Diagnostics

Remote Door unlock/Heat

Basic Traffic

Video Download

Music Download

High Bandwidth – High Cost Low Value ‐ Limited market interestStolen vehicle tracking

eCall ‐ Automatic Crash notification

HD Video Download

g gConnectivity Suitability:

Embedded

TetheredSource: Automotive Multimedia & Communications ‐ AMCS

Emergence of Global Wireless PlayersPart IPart I

Telefonica

• OnStar, MasternautA

Vodafone

• VerizonA

American Movil? China Unicom? AT&T?AA

New players:

• Google, Apple, Facebook, Amazon

A role for MVNOs…

Source: Automotive Multimedia & Communications ‐ AMCS

??

Emergence of Global Wireless PlayersPart II

Next steps for carriers – What do OEMs want?

Part II

Global SIM card: Regional provisioningComprehensive asset managementVehicle diagnosticsVehicle diagnosticsSoftware managementContent managementS i f d hi diService‐focused ownership paradigmVehicle connection restructures OEM, dealer, customer relationships – different regions at different stages of this

l ievolutionNew ownership models will require connections – vehicle sharing etc.

33Source: Automotive Multimedia & Communications ‐ AMCS

??

Status and Outlook for In‐vehicle Smartphone Connectivity SolutionsSmartphone Connectivity Solutions

• Connecting…with the consumer!

Source: Automotive Multimedia & Communications ‐ AMCS

Car to device connectivity:Many optionsoptions…but no winning standard?Many optionsoptions…but no winning standard?

• MirrorLink (Toyota)

• RealVNC (Jaguar)

• Livio Connect (GM)

• Aha Radio (Harman) (Honda, Subaru)

• Choreo (Airbiquity)

• Zypr (Pioneer) (Toyota/Scion)• Zypr (Pioneer) (Toyota/Scion)

• AudiConnect

• BMW ConnectedDriveBMW ConnectedDrive

• MyFord Touch

• Entune/Touch&Go (Toyota)

• MyLink (GM)

• Uconnect (Chrysler)Source: Automotive Multimedia & Communications ‐ AMCS

Car to device connectivity:Many optionsoptions…but no winning standard?Many optionsoptions…but no winning standard?

• Uvo (Kia)

• BlueLink (Hyundai)

• Mbrace (Mercedes)

• Blue&Me (Fiat)

• HondaLink (Honda)

Source: Automotive Multimedia & Communications ‐ AMCS

Two primary approaches have emergedTwo primary approaches have emerged

• MirrorLink – Approved apps, approved HMI framework, vehicle control

• Content proxy – Smartphone as pass‐through for content with customized frameworkcustomized framework

• Both approaches will co‐exist; Both approaches are being pp ; pp gadopted simultaneously to cope with different operating systems and wired and wireless interfaces

• Both approaches may require virtualization

Source: Automotive Multimedia & Communications ‐ AMCS

Device and vehicle connectivity IssuesOEM ‘Cloud’ PerspectiveOEM Cloud Perspective

SYNC, MyFord Touch

MyLink, IntelliLink, CUE

Touch&Go, Entune, EnForm, Bespoke

mBrace 2

BMW Apps

Source: Automotive Multimedia & Communications ‐ AMCS

Device and vehicle connectivity IssuesTier 1 ‘Cloud’ PerspectiveTier 1 Cloud Perspective

Recently announced its Smart Access cloud platform, with its first product Next GATE shown at CTIA 2012. Next GATE is largely underwhelming, the product is not seamlessly integrated and does not represent a compelling orproduct is not seamlessly integrated and does not represent a compelling or fresh take on the market. The product recalls the struggles that Clarion had with its MiND product

Harman has worked with Toyota on many of its connectivity solutions to littleHarman has worked with Toyota on many of its connectivity solutions to little avail. Harman acquired Aha Mobile but these solutions have not been compelling. Harman is working on Dock & Go with RinSpeed, but it appears there are too many solutions and too little direction.

Pioneer first announced its PAIS system, which was later rebranded as ZYPR. ZYPR targets applications across the phone, tablet, car, and TV. While some lauded ZYPR as a potential open alternative to Siri, Pioneer does not have the market size or credibility to move the marketmarket size or credibility to move the market.

Alpine’s approach has been different than other Tier Ones. Alpine has enlisted the help of unlikely new comer Chleon (former Nokia personal) forenlisted the help of unlikely new comer Chleon (former Nokia personal) for help with cloud connectivity. This approach could work, however it further confirms Alpine as reliable hardware manufacturer, a position that Tier One’s are desperate to avoid.

Source: Automotive Multimedia & Communications ‐ AMCS

Nokia MirrorLinkNokia MirrorLinkStrong membership of OEMs, Tier Ones, and CE companies including Daimler GM, Hyundai, Honda, PSA, Toyota, and VW.

Daimler and Toyota have announced future solutions. Systems will be compatible with all Symbian phones from last year and future Nokia Windows phones.

Reduces the number of smartphone protocols an infotainment system has to support, h ll b f l f l dthis is especially beneficial for low‐end systems.

Enables consumers to use applications more safely and lets car markers create apps that can work on multiple smartphones.

CCC support is only luke warm by many members. Many have joined but shown very little commitment. HTC, LG, and Samsung do not appear particularly committed.

The only operating system MirrorLink has secured is Symbian, which is legacy technology. i f d id l i h h dl l d lNo commitment from Android, Apple, or MSFT is a huge hurdle. Apple and Google

typically do not like having to comply with standards set by others.

OEMs are reluctant to cede “ownership” of the screen to smartphone makers and 3rd

party application makers In the best case a vetting or testing process must be createdparty application makers. In the best case, a vetting or testing process must be created.

Nokia’s HMI focus made it unsuitable for GENIVI participation.

Source: Automotive Multimedia & Communications ‐ AMCS

Device Tethering to WiFiDevice Tethering to WiFiConsumers can enjoy a connected solution without an additional subscription fee from the OEM or TSP.

Smartphones are increasingly fitted with Bluetooth Dial Up Network and Personal Area Network profiles as well as A2DP, HFP, and PBAP.

Tethering is becoming more essential as companies explore the integration of l b d d dapplications beyond navigation and Internet radio.

WiFi hotspots are expensive in the US. Verizon charges an additional $20/month on top of normal data charges for WiFi hotspot capability.

WiFi hotspot technology in Europe varies from country to country and carrier to carrier, though the capability is typically less than in the US.

OEMmay need to work with wireless carriers to create wholesale solutions, that tli th t t th t d t ill b d b th i hi l Thi t k tioutline the extent that data will be consumed by the user in vehicle. This takes time.

?Wireless carriers in both the US and Europe are currently reexamining how tethering fees should be structured. Some argue that they should be an extension of limited data plans where consumer’s bandwidth is either throttled once a certain limit of data is used or? where consumer s bandwidth is either throttled once a certain limit of data is used or where users are charged overage fees are a certain amount of data is used. Wireless carriers are watching the rollout of 4G networks and increasingly looking at the number of connected tablets to create better monetization strategies.

Source: Automotive Multimedia & Communications ‐ AMCS

OEM Connectivity Features: ECU Connectivity (e.g. Ford SYNC)ECU Connectivity (e.g. Ford SYNC)

3 5,0 0 0

4 0 ,0 0 0

Bluet oot h

2 0 ,0 0 0

2 5,0 0 0

3 0 ,0 0 0Wif i

USB

5,0 0 0

10 ,0 0 0

15,0 0 03.5 Mil Jack

Unit Shipment

0

5,0 0 0

2 0 0 9 2 0 10 2 0 11 2 0 12 2 0 13 2 0 14 2 0 15 2 0 16 2 0 17 2 0 18 2 0 19

Tot al

F t T d/O t it 2011 2019

In‐Vehicle Connectivity is a key growth area in Infotainment• Feature Trend/Opportunity: 2011 vs. 2019

– USB 2.0 Shipments +630%: 4.0 Mil to 29.3 Mil units (CAGR 28%)

– Bluetooth Shipments +540%: 4.3 Mil to 27.5 Mil units (CAGR 26%)

Wi Fi Shipments +1700%: 1 4 Mil units to 25 3 Mil units (CAGR 43%)

Infotainment

– Wi‐Fi Shipments +1700%: 1.4 Mil units to 25.3 Mil units (CAGR 43%)

– 3.5 Mil Jack Shipments +500%: 4.3 Mil to 26 Mil units (CAGR 25%)

Source: Automotive Multimedia & Communications ‐ AMCS

Connecting the Car to the InternetConnecting the Car to the Internet

Embedded phone scenario: COB: Connection on Board

Safet and sec rit ACN SVRSafety and security – ACN, SVRComplete control of Content, Application,

Service (CAS) delivery experienceService (CAS) delivery experienceSeamless integration of CAS with voice,

touch, physical interfaces, p yControl of billing and customer relationshipControl of access to vehicle sensor data

43

Potential for proprietary applications and social networks – InkaNet walkie talkie

Connecting the Car to the InternetConnecting the Car to the Internet

COB: The DownsideCOB: The DownsideMonthly or annual subscriptionN t t ’ f d iNot customer’s preferred carrierLimited data planWi l /QOSWireless coverage/QOSLow priority for car purchasing

44

The Consumer ContradictionThe Consumer Contradiction

Customer’s Want a COB ExperienceCustomer s Want a COB Experience from a BYOC Scenario!

What are Chinese car consumersWhat are Chinese car consumers saying?y g

45

Consumers in China Need Device ConnectivityConsumers in China Need Device Connectivity

• Smartphone connectivity becoming much more of a must‐have feature than in other regionsother regions– 50% consider access to smartphone

apps a must‐have feature

• CD player interest and usage• CD player interest and usage similar to portable music player– Both usage and interest in portable

music player connectivity similar to CD player

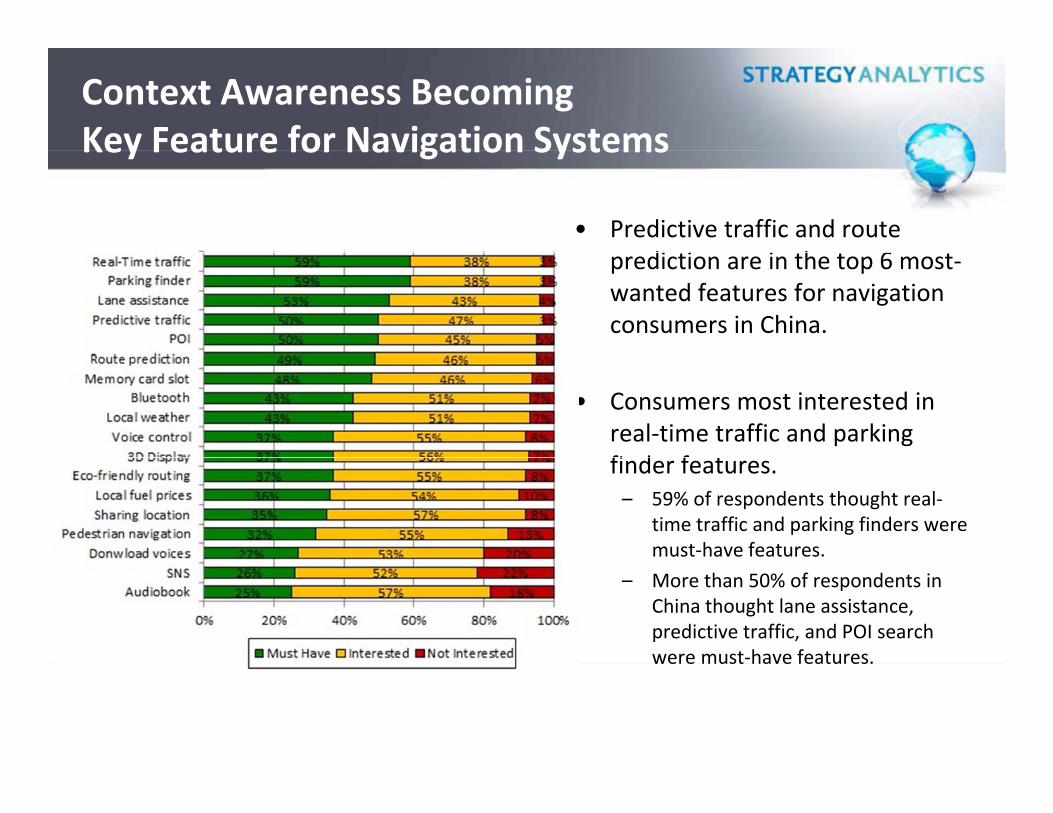

Context Awareness Becoming Key Feature for Navigation SystemsKey Feature for Navigation Systems

• Predictive traffic and route di i i h 6prediction are in the top 6 most‐

wanted features for navigation consumers in China.

• Consumers most interested in real‐time traffic and parking fi d f tfinder features. – 59% of respondents thought real‐

time traffic and parking finders were must‐have features.

– More than 50% of respondents in China thought lane assistance, predictive traffic, and POI search were must‐have features.were must have features.

Interest in Connected Services: ChinaInterest in Connected Services: China

• Consumers in China most interested in local weather

• Social networking features show higher interest, but they are domain specificthey are domain specific– Seeing friends locations and

sharing their locations with friends instead of seeing socialfriends instead of seeing social network feeds

The Car Maker ContradictionThe Car Maker Contradiction

The OEM wants the vehicle dataThe OEM wants the vehicle data for vehicle/customer relationship management.

The OEM justifies embedding j gbased on selling apps, content and

i49

services.

The Car Maker Contradiction IIThe Car Maker Contradiction II

The OEM knows the customer wants to use his or her connected d i d d t t tdevice and does not want to pay for additional subscription.for additional subscription.

h l hBut the OEM also wants the vehicle data – which is harder to

50

vehicle data which is harder to achieve via smartphone.

Winning Connectivity StrategiesWinning Connectivity Strategies

1. OEMs are increasingly providing hybrid1. OEMs are increasingly providing hybrid connectivity – embedded + smartphone2. The onset of Wi‐Fi Direct is enhancing the2. The onset of Wi Fi Direct is enhancing the value of smartphone connections for a wider range of applicationsrange of applications3. Embedded modems enhanced by open APIs allow for aftersales application enhancementsallow for aftersales application enhancements

Ultimate Goal: Maximum flexibility51

Ultimate Goal: Maximum flexibility

Roger’s Rules of Vehicle Connectivity ‐ #1Roger s Rules of Vehicle Connectivity #1

A system with embedded modemA system with embedded modem must first and foremost provide for automatic crash notification plus vehicle diagnostics/prognostics.g /p g

52

Roger’s Rules of Vehicle Connectivity ‐ #2Roger s Rules of Vehicle Connectivity #2

Call centers should be focused onCall centers should be focused on customer/vehicle relationship management – (not destination download!))

53

Roger’s Rules of Vehicle Connectivity ‐ #3Roger s Rules of Vehicle Connectivity #3

Data intensive applications such asData intensive applications such as Wi‐Fi hotspot and mobile video should be enabled via customer’s phone and data plan.p

54

Roger’s Rules of Vehicle Connectivity ‐ #4Roger s Rules of Vehicle Connectivity #4

App stores should be left to Apple andApp stores should be left to Apple and Google. OEMs can offer a few car‐specific apps (remote start, vehicle location, status, conditioning) but the , , g)on‐board store is a distraction.

55

Roger’s Rules of Vehicle Connectivity ‐ #5Roger s Rules of Vehicle Connectivity #5

Smartphone integrations requireSmartphone integrations require dedicated drive‐safe in‐vehicle HMI –not screen replication – ie. Apple video out.

56

Roger’s Rules of Vehicle Connectivity ‐ #6Roger s Rules of Vehicle Connectivity #6

Siri and Google voice solutions are notSiri and Google voice solutions are not likely to be competitive with true automotive grade solutions from Nuance, AT&T, Iflytek, Xiaoi, etc. , , y , ,

57

Revisiting an Old Friend – InkaNet Gen 4?Revisiting an Old Friend InkaNet Gen 4?

58

InkaNet: An Exception to the RulesInkaNet: An Exception to the Rules

InkaNet remains the most advanced telematics and i f t i t d li l tf i th ldinfotainment delivery platform in the world:

Android basedInnovative social networking – walkie talkieInnovative social networking walkie talkieApp storeInnovative data management – concierge viag g

customer’s phone, SD card updatesMultiple source music access

’l l /d kNat’l language recognition/dictation – iVokaInternet search – in‐dash video

59

InkaNet User EvaluationInkaNet User Evaluation

60

Problems with InkaNetProblems with InkaNet

Not on the CAN bus – no vehicle data, no probe h t f t ffi d t CRMenhancement of traffic data, no CRM

Offers apps‐in‐dashboard experience – WRONG! –Offers apps in dashboard experience WRONG! should use existing apps via phone

No one is paying! – Advertising strategy of the creator makes it challenging to charge for service –f d f ff “ b b ” h hafraid of scaring off “subscribers” OnStar has the same problem in China.

61

What about LTE?What about LTE?

IP‐based traffic dataSt i di t tStreaming audio contentHybrid (on‐board/off‐board) voice recognitionWideband (HD) voice – for enhanced recognitionWideband (HD) voice for enhanced recognitionLow latency for safety applications

62

BMW ConnectedDrive personified in funny commercials [videos].wmv

Connecting the Car to the InternetConnecting the Car to the Internet

The Two Most Important Reasons to Connect Cars:

To sell more cars!

To increase aftersales revenue and profit

To save lives

64

Thank you!Thank you!

Roger C. Lanctotg

Associate Director

Global Automotive Practice

Strategy Analytics

+1 (617) 614‐0714

Twitter: @rogermud