ge capital services · oil & gas . $15.2b . aviation . $20.0b ... commercial paper strong...

TRANSCRIPT

GE Capital

Overview / Strategy

“This document contains “forward-looking statements”- that is, statements related to future, not past, events. In this context, forward-looking statements often address our expected future business and financial performance, and often contain words such as “expect,” “anticipate,” “intend,” “plan,” believe,” “seek,” or “will.” Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For us, particular uncertainties that could adversely or positively affect our future results include: the behavior of financial markets, including fluctuations in interest and exchange rates and commodity and equity prices; the commercial and consumer credit environment; the impact of regulation and regulatory and legal actions; strategic actions, including acquisitions and dispositions; future integration of acquired businesses; future financial performance of major industries which we serve, including, without limitation, the air and rail transportation, energy generation, media, real estate and healthcare industries; and numerous other matters of national, regional and global scale, including those of a political, economic, business and competitive nature. These uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements."

2013 third quarter

GE

3

GE’s portfolio

Transportation

$5.6B

$1.0B

Revenue

Operating profit

Power & Water

$28.3B

$5.4B

Energy Management

$7.4B

$0.1B

Oil & Gas

$15.2B

$1.9B

Aviation

$20.0B

$3.7B

Home & Business

$8.0B

$0.3B

Capital

$45.9B

$7.4B

Healthcare

$18.3B

$2.9B

(Total Year 2012 figures)

$147 billion in revenue

52% revenue outside the U.S

$16 billion operating earnings

15% industrial ROTC

$11B industrial CFOA

$7 billion dividends paid

Revenue

Operating profit

4 2013 third quarter

($ in billions)

Infrastructure orders in backlog

3Q’13 orders - $25.7B Largest backlog in history

Equip.

Svcs.

$175 $204 $200 $201 $203 $210 $216 $223 $229 Equipment +32% … book-to-bill 1.2

Service orders +5% with 5/6 segments … PGS +8%, +14% ex. Europe; Aviation commercial spares +9%

Every segment positive

Broad regional growth … U.S. +18%, Europe +17%, growth markets +22% … Russia/CIS +51%, ANZ +36%, SSA +18%, MENAT +17%, China +17%, ASEAN 2x, Canada +10%

Backlog +$6B … Aviation & Transportation

Solid orders performance … very broad based Equipment & services backlog expansion continues

5 2013 third quarter

Investor objectives …

Double-digit Industrial earnings growth

1 Industrial segment profit +11% in 3Q

6/7 segments with strong growth

2 Planning 70 bps. margin expansion

3Q margin expansion +120 bps., YTD +40 bps. … on track for planned 70 bps. in ’13

Returned $3.9B cash to parent YTD, planning up to $6.5B in ’13; solid earnings, ENI $385B

Significant cash from GE Capital

3

Returned $13.9B through dividends and buyback YTD … on track for total year

Expect to return ~$18B to shareowners

5

4 +2-6% Industrial segment organic revenue growth

3Q organic +1% … expect stronger growth in 4Q

6 2013 third quarter

3Q’13 consolidated results

Revenues $35.7 (1)% – Industrial sales 25.3 2 – Capital revenue 10.7 (5)

Operating earnings 3.7 (3) Operating EPS .36 0 Continuing EPS .32 (3) Net EPS .31 (6) CFOA YTD 7.8 (27) – Industrial 3.9 (25) – Industrial (ex. NBCU, pension) 5.9 5

3Q’13 V% Segment

profit

Power & Water $6,498 (10)% $1,289 9%

Oil & Gas 4,315 18 519 11

Energy Mgmt. 1,828 (3 ) 18 (57 )

Aviation 5,364 12 1,091 18

Healthcare 4,304 - 665 7

Transportation 1,406 - 306 15

H&BS 2,098 7 77 28

Industrial 25,813 3 3,965 11

GE Capital 10,670 (5 ) 1,895 13

Total segments $36,483 -% $5,860 12%

Revenues

$ V% $ V%

($ in billions – except EPS)

3Q’13 3Q’12

($ in millions)

Tax rate 10% 14% – GE (ex. GECC) 20 21 – GECC 0 5

Segment profit +12% … broad strength

GE Capital

8

GE Capital ‘12 revenue: $46B ‘12 assets: $537B ($418B Ending Net Investment) –a) ‘12 profit: $7.4B –b)

a) ENI is shown ex-cash b) Continuing operations attributable to company

GE Capital Aviation Services

Commercial aircraft leasing &

financing

$49B

Consumer

Consumer & retail financing

$139B

Real Estate

Debt & equity financing for commercial real estate

$46B

Energy Financial Services

Financing for energy & water

industries

$19B

Middle market lending &

leasing

Commercial Lending &

Leasing

$181B

$1.2B $3.2B $0.8B $0.4B $2.4B

Assets

Net income

9

GE Capital businesses Business

Commercial Lending & Leasing

3Q’13 assets • Entered in the 60’s • ~100% secured loans and leases • Support mid-market customers

• Entered in the 70’s • Secured loans against diversified properties • Own/operate high quality properties

• Entered in the 30’s • Store cards and sales finance for retailers • Broad spread of risk

• Entered in the 60’s • GE domain • Broad product set with full life cycle management

• Entered in the 80’s • GE domain • Essential assets; secure cash flows

Domain + expertise

Businesses we know…deep domain… decades of performance

Real Estate $40 - Debt - Equity

Consumer $136 - U.S. PLCC - Global

Aviation Services $47

Energy Financial Services $18

($ in billions)

$170

10 2013 third quarter

GE Capital: next phase

Aviation financing

Energy financing

Global mid-market

financing

CRE debt

Retail finance Int’l. banks

Global mortg. CRE equity Misc. other

Non-core

Value- maximizing

Core

~$59

~$350

ENI today

$300-350

ENI target Year-end 2014

Portfolio actions ‒ Run-off non-core ‒ Staged exits of value maximizing ‒ Grow core

Maintain attractive ROI

Less CP & long-term unsecured bonds

Maintain strong Basel 3 capital ratios

Great enterprise risk management

Strategic imperatives

($ in billions)

~$326

1

2

3

4

5

Continuing to execute on a clear & consistent strategy

11 2013 third quarter

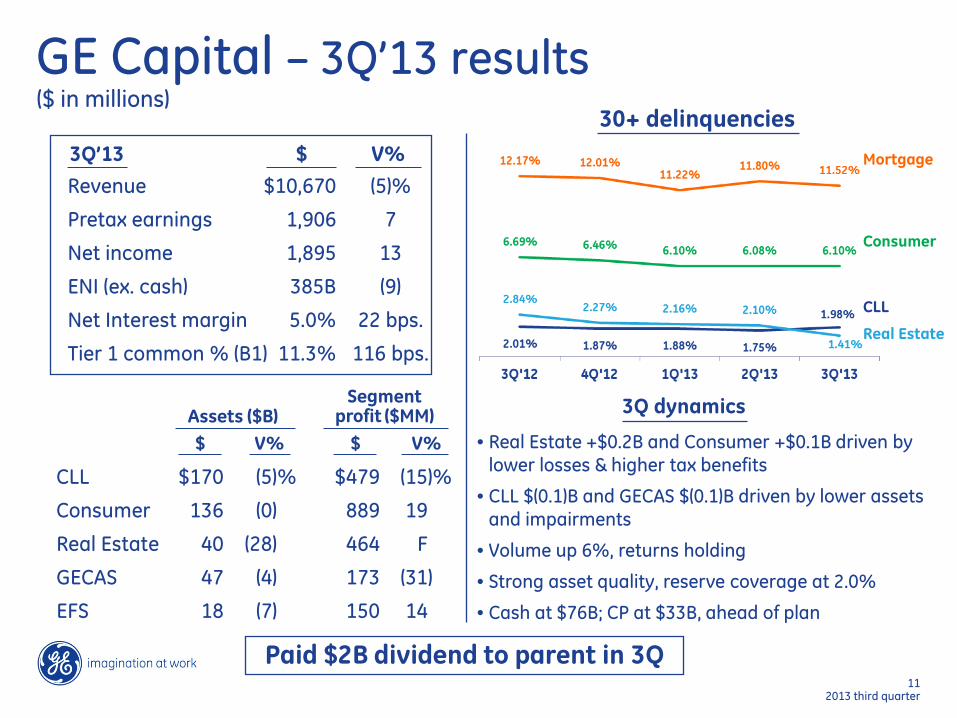

GE Capital – 3Q’13 results

Revenue $10,670 (5)%

Pretax earnings 1,906 7

Net income 1,895 13

ENI (ex. cash) 385B (9)

Net Interest margin 5.0% 22 bps.

Tier 1 common % (B1) 11.3% 116 bps.

CLL $170 (5)% $479 (15)%

Consumer 136 (0) 889 19

Real Estate 40 (28) 464 F

GECAS 47 (4) 173 (31)

EFS 18 (7) 150 14

$ V% 3Q’13

Segment profit ($MM)

$ V% $ V% Assets ($B) 3Q dynamics

• Real Estate +$0.2B and Consumer +$0.1B driven by lower losses & higher tax benefits

• CLL $(0.1)B and GECAS $(0.1)B driven by lower assets and impairments

• Volume up 6%, returns holding

• Strong asset quality, reserve coverage at 2.0%

• Cash at $76B; CP at $33B, ahead of plan

Paid $2B dividend to parent in 3Q

30+ delinquencies

Real Estate

Consumer

Mortgage

CLL

($ in millions)

Funding

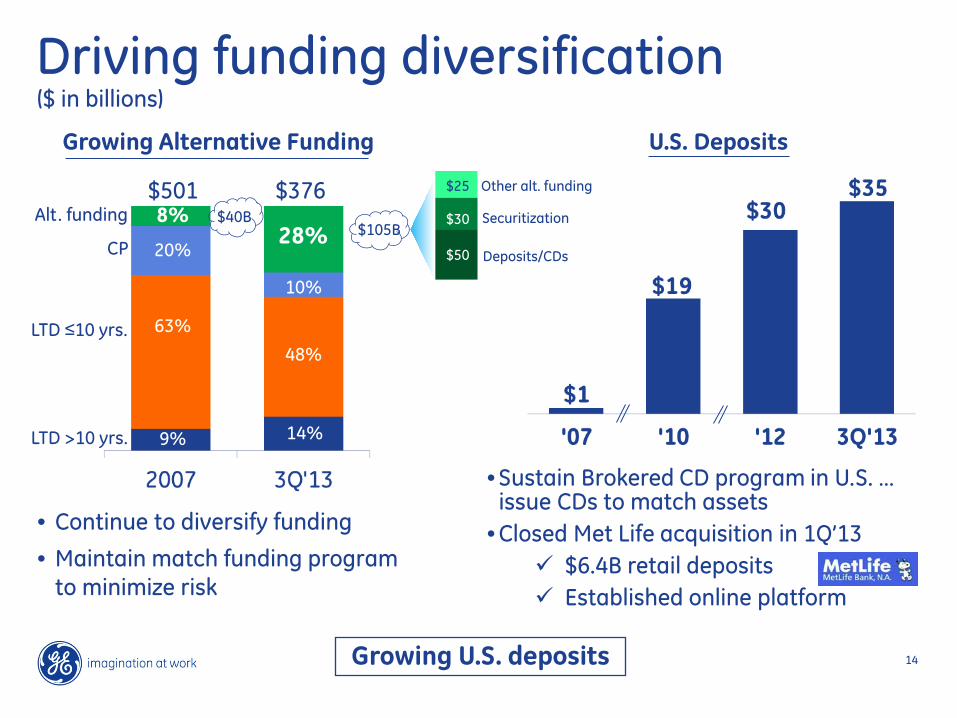

13 2013 third quarter

GE Capital funding ($ in billions)

Debt composition–a)

Comm’l paper

LT debt - TLGP

LT debt non-guaranteed

Alternative funding/other

(a- Continuing operations (b- Includes ~$(2.8)B YTD FX impact and ~$(4.9)B YTD FAS 133

Deposits/CDs

$397 $376-b)

Non-recourse Securitization

$420

Bank lines $48 $48 $48 CP coverage 100%+ 100%+ 100%+ Cash & equiv. $78 $62 $76 LT debt <1yr. $61 $44 $38

Funding strategy

Centralized Treasury operation

‒ No speculative trading … not a profit center

Matched funding policy

Diversification of funding

Rigorous liquidity management

− Cash $76B at 100%+ coverage of next 12 months LT debt maturities

− Bank lines $48B at 100%+ coverage of commercial paper

Strong implicit and explicit GE parent support … Income Maintenance Agreement

14

$105B

Growing U.S. deposits

Growing Alternative Funding

($ in billions)

• Continue to diversify funding

• Maintain match funding program to minimize risk

Alt. funding

CP

LTD ≤10 yrs.

LTD >10 yrs.

8%

20%

63%

9%

U.S. Deposits

• Sustain Brokered CD program in U.S. … issue CDs to match assets

• Closed Met Life acquisition in 1Q’13 $6.4B retail deposits Established online platform

$501 Other alt. funding

Securitization

Deposits/CDs

$25

$30

$50 28%

10%

48%

14%

$376 $40B

Driving funding diversification

15

2007 2008 3Q'13 2013Target

Future

Commercial paper

Significantly reduced footprint … lowest CP balance in 21 years

Global Outstanding ($B)

• Credit ratings … A-1+/P-1

• Issue in four currency markets

• Direct placement to end investors by experienced teams in U.S., Europe

• Committed undrawn credit lines $48B from ~50 institutions globally

17%

83%

GECC U.S. Market share down from 5.1% in ‘07

to ~2.8% at 3Q’13

$72

$101

Highlights

Int’l

U.S. $33 $33

$20-30

16 2013 third quarter

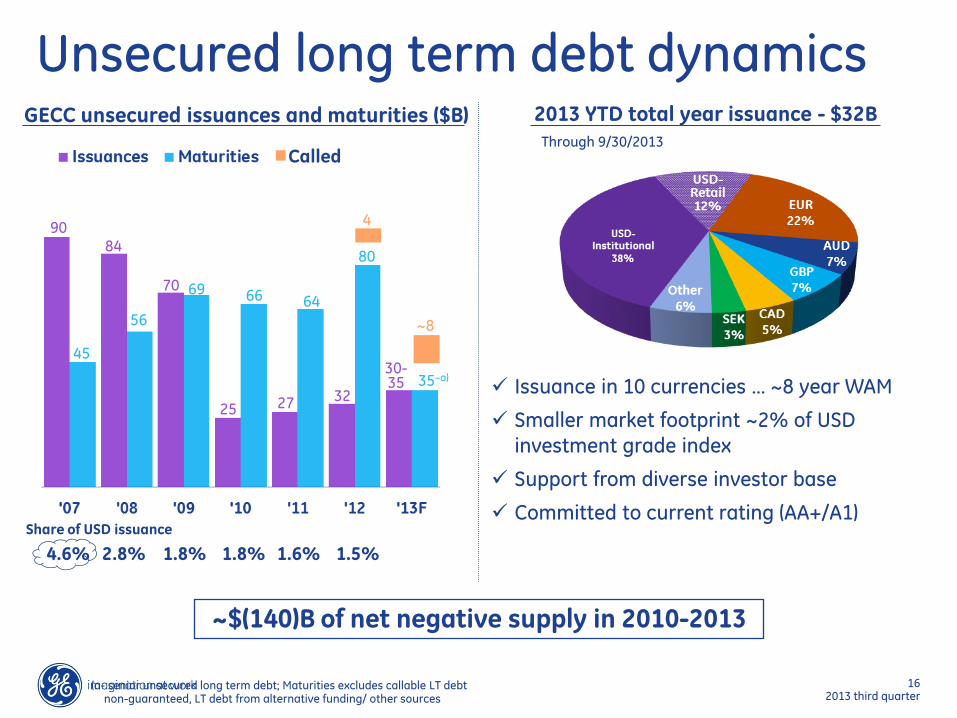

Unsecured long term debt dynamics GECC unsecured issuances and maturities ($B)

90 84

70

25 27

45

56

69 66 64

32

80

35–a) Issuance in 10 currencies … ~8 year WAM

Smaller market footprint ~2% of USD investment grade index

Support from diverse investor base

Committed to current rating (AA+/A1)

(a- senior unsecured long term debt; Maturities excludes callable LT debt non-guaranteed, LT debt from alternative funding/ other sources

Share of USD issuance

4.6% 2.8% 1.8% 1.8% 1.6% 1.5%

~$(140)B of net negative supply in 2010-2013

2013 YTD total year issuance - $32B

30-35

Through 9/30/2013 Called

4

~8

17 2013 third quarter

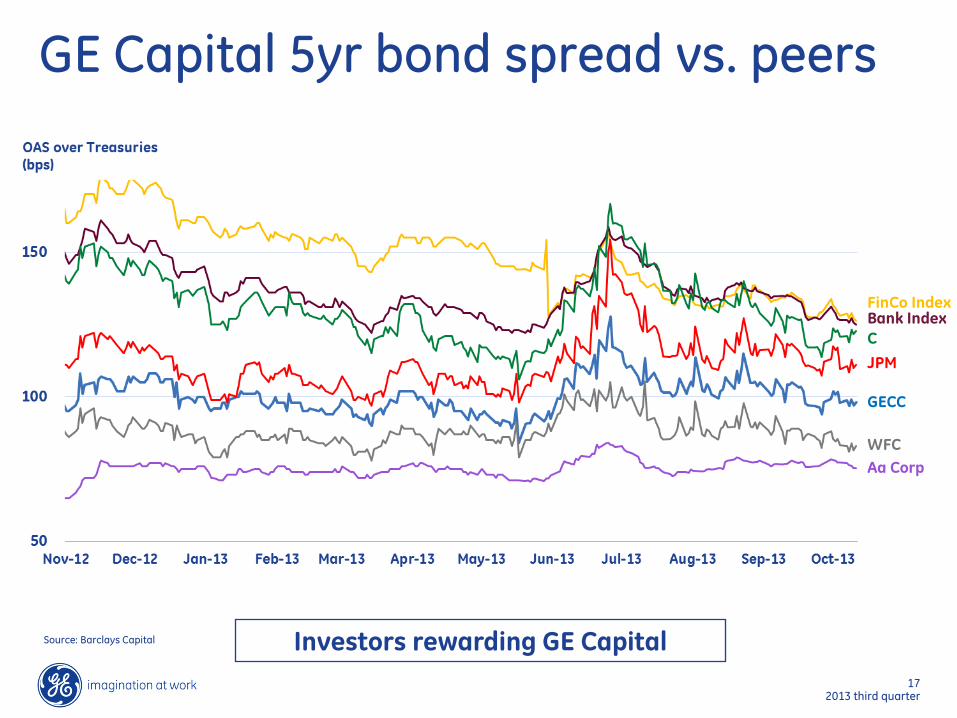

WFC

GECC

Bank Index

JPM

FinCo Index

C

Aa Corp

GE Capital 5yr bond spread vs. peers

Source: Barclays Capital Investors rewarding GE Capital

18 2013 third quarter

Support • GE support to ensure GECC 1.1x fixed-charge

coverage ratio (strengthened Income Maintenance Agreement in 2009)

• History of capital infusion or dividend reductions when necessary

GE Capital structure

100% AA+/Aa3

General Electric Capital Corporation

Primary GE Issuer/Guarantor

General Electric Company

Owns all of GE’s financing

assets

AA+/A1 100%

Commitment to local markets • GECC unconditional guarantee • Highly rated parent • Proceeds used primarily to fund local

assets • Access to deeper investor base

GE Capital UK Funding

GE Capital Australia Funding

GE Capital European Funding

GE Capital Canada Funding

GE Japan Funding KK

GE Capital New Zealand Funding

GE Capital Mexico Funding

19 2013 third quarter

GE credit ratings

General Electric Company P-1 Aa3 A-1+ AA+

General Electric Capital Corporation P-1 A1 A-1+ AA+

• GE Capital Australia Funding* P-1 A1 A-1+ AA+

• GE Capital Canada Funding* P-1 A1 A-1+ AA+

• GE Capital European Funding* P-1 A1 A-1+ AA+

• GE Japan Funding KK* P-1 A1 A-1+ AA+

• GE Capital Mexico Funding* P-1 A1 A-1+ AA+

• GE Capital UK Funding* P-1 A1 A-1+ AA+

* Guaranteed by General Electric Capital Corporation

Moody’s Rating

Short Term Long Term

S&P Rating

Short Term Long Term

20

$7.4

Net income –a)

+

’12 ’13E

ENI ($B) -b)

b) - Ending net investment ex. cash and equivalents

Summary

Smaller and safer franchise … expect to grow earnings in 2013 on a smaller balance-sheet

Our businesses are strong and well positioned competitively

Capital levels are in excess of expected targets

We have strong liquidity and funding … continuing to diversify funding sources

Regulatory policies continue to evolve − Designated nonbank SIFI

Key messages

Strong and valuable franchise

($ in billions)

a) - Earnings from continuing operations attributable to GECC

‘11

$6.6