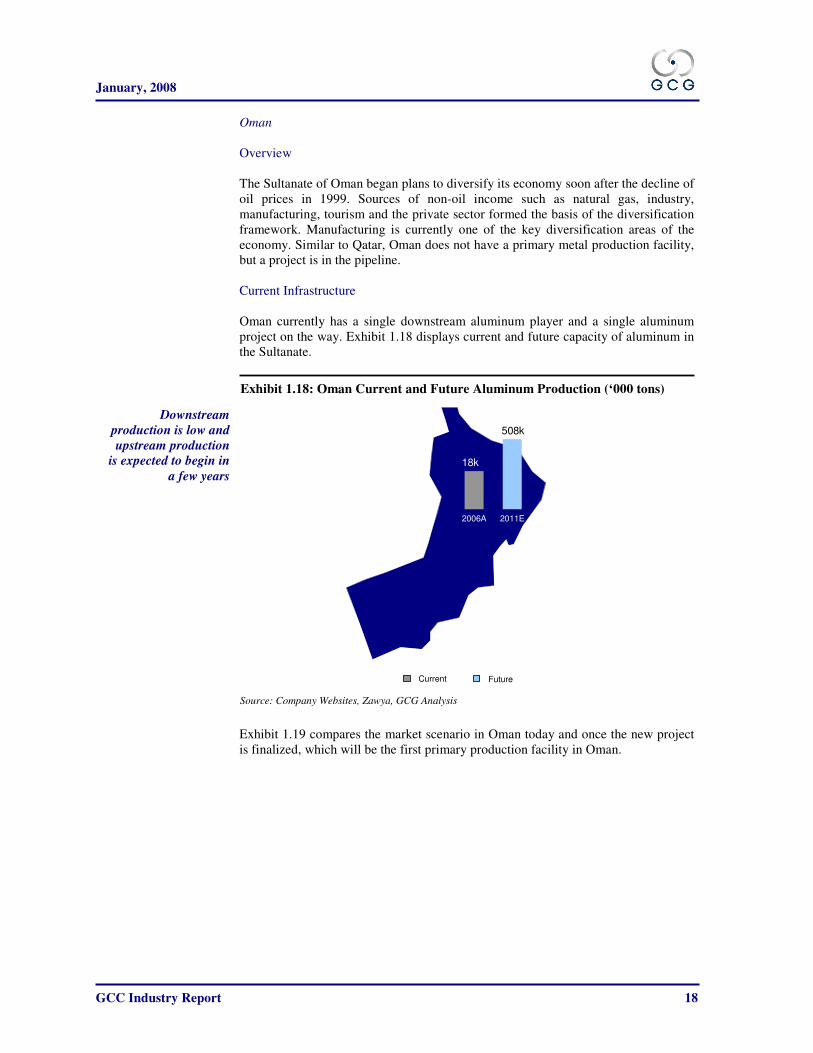

gcc industry report - gulfbase€¦ · this is the abu dhabi oil refining company (takreer). the...

TRANSCRIPT

Manufacturing the Future...

GCG Research

GCC Industry Report

January 2008

Gulf Capital Group (DIFC) Limited

Dubai International Financial Center

Registered Office – Offices 5 & 6, Level 4, Precinct Building 3,

P O Box – 214851, Dubai, UAE

Tel: +971 4 363 5730 Telefax: +971 4 363 5739

Website: www.gulfcapitalgroup.com

Email: [email protected]

GCG is regulated by the Dubai Financial Services Authority

INTRODUCTION...........................................................................................................................1

A building here, a building there .......................................................................................................... 1

Chemicals & Plastics – Being smart about oil ..................................................................................... 1

Market Dynamics................................................................................................................................... 2

Future Projects ...................................................................................................................................... 2

ALUMINUM ...................................................................................................................................3

Production Shift..................................................................................................................................... 4

Aluminum Facts .................................................................................................................................... 5

Aluminum in the GCC........................................................................................................................... 6

Raw Material Procurement............................................................................................................................8

Popularity of Extruded Products ...................................................................................................................8

GCC Aluminum Projects................................................................................................................................9

United Arab Emirates...................................................................................................................................11

Bahrain .........................................................................................................................................................14

Qatar .............................................................................................................................................................16

Oman.............................................................................................................................................................18

Kuwait ...........................................................................................................................................................20

STEEL ...........................................................................................................................................24

The History of Steel ............................................................................................................................. 24

Global Production ............................................................................................................................... 26

Steel in the GCC .................................................................................................................................. 28

Reinforcement Bars- Strong Demand .........................................................................................................29

United Arab Emirates...................................................................................................................................31

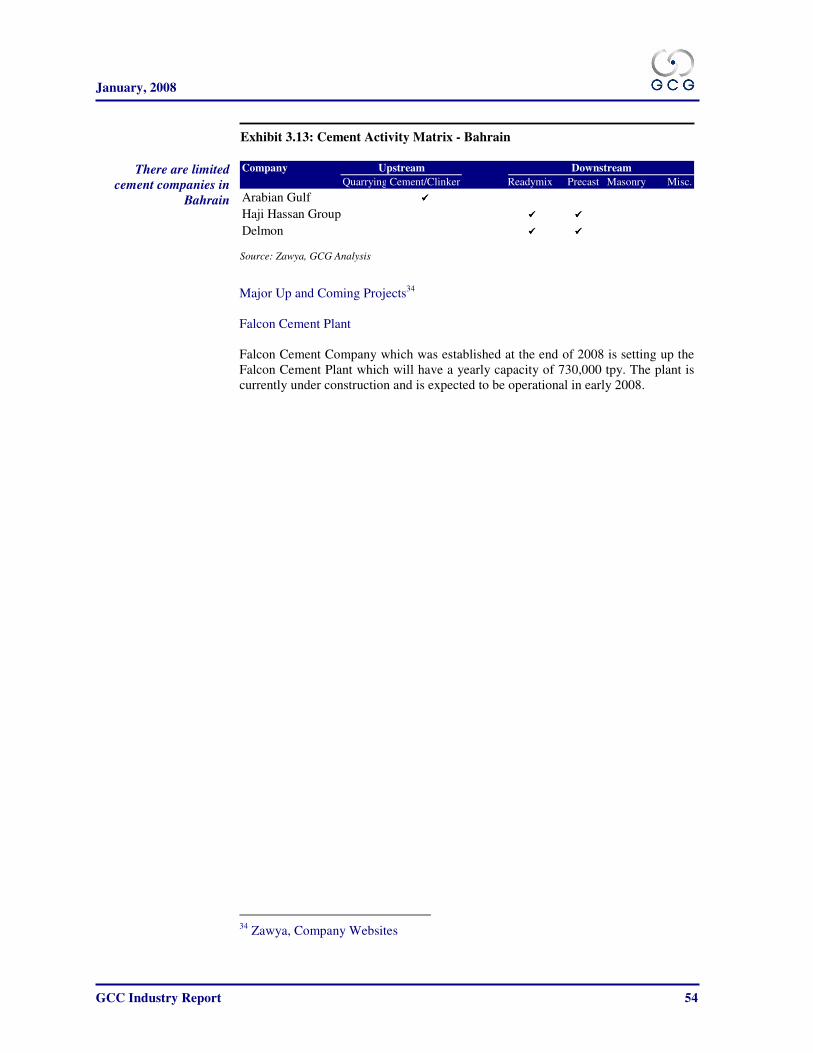

Bahrain .........................................................................................................................................................34

Qatar .............................................................................................................................................................36

Kuwait ...........................................................................................................................................................39

Saudi Arabia .................................................................................................................................................41

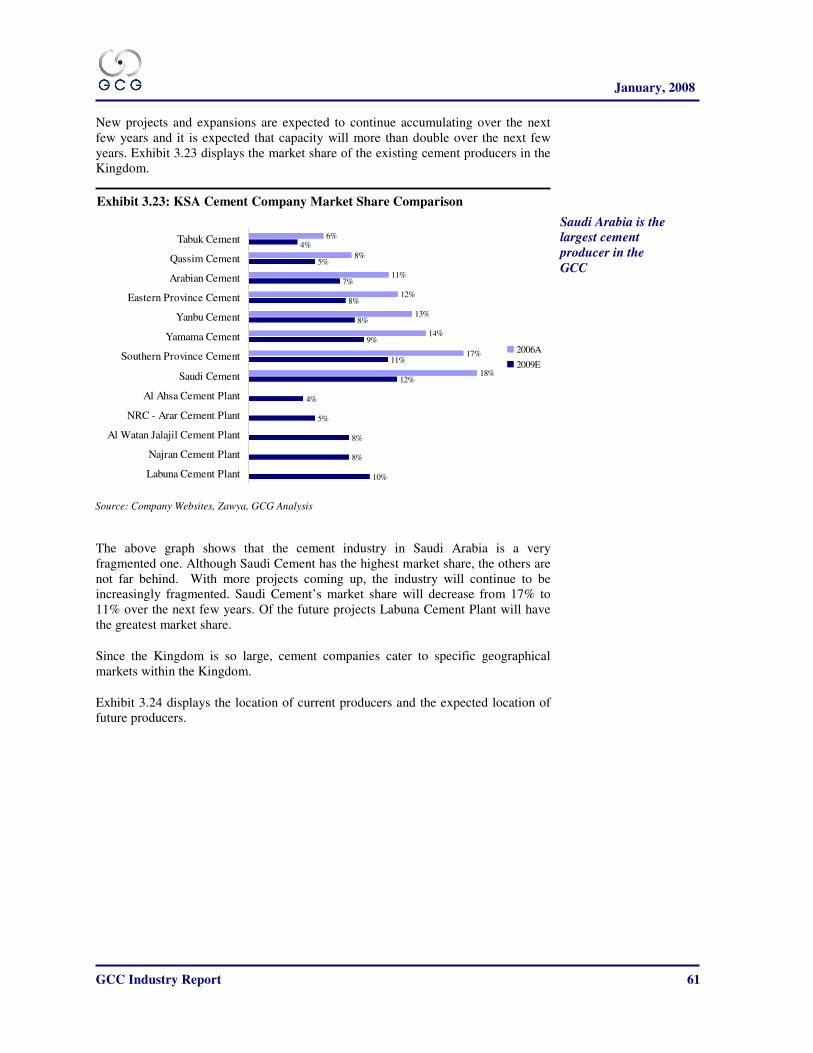

CEMENT.......................................................................................................................................44

Cement Facts ....................................................................................................................................... 44

Global Cement Production.................................................................................................................. 46

Cement in the GCC.............................................................................................................................. 47

GCC Cement Projects...................................................................................................................................47

United Arab Emirates...................................................................................................................................50

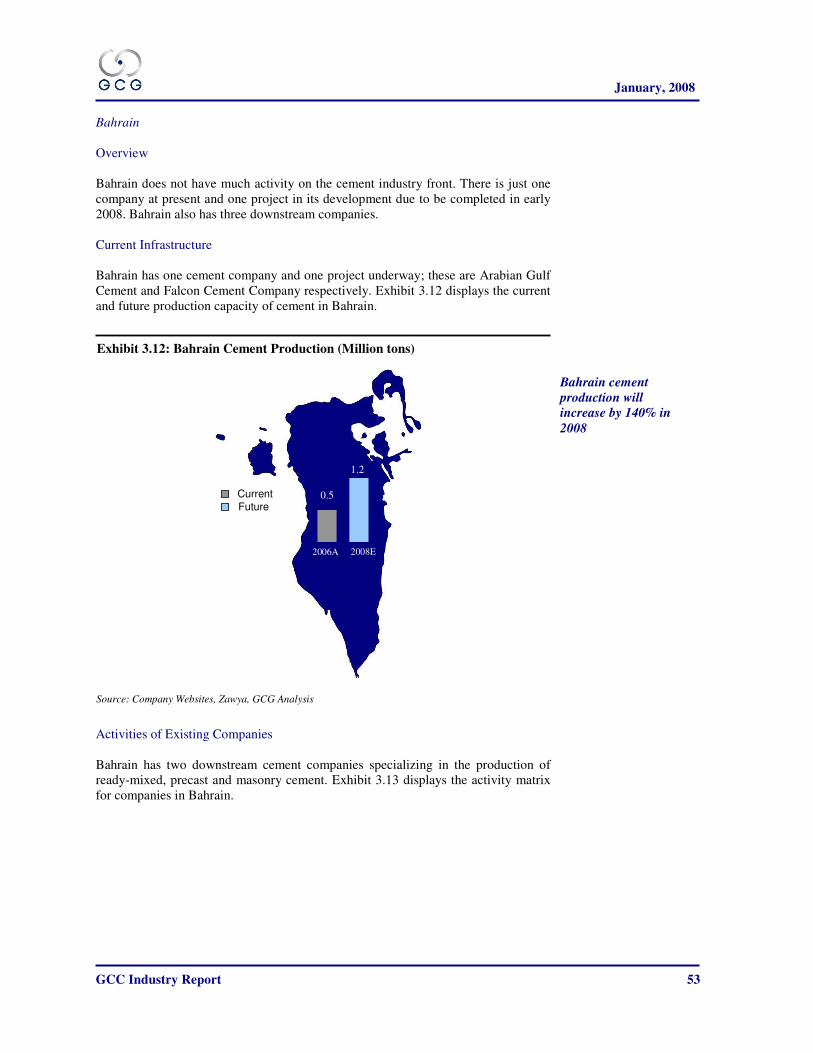

Bahrain .........................................................................................................................................................53

TABLE OF CONTENTS

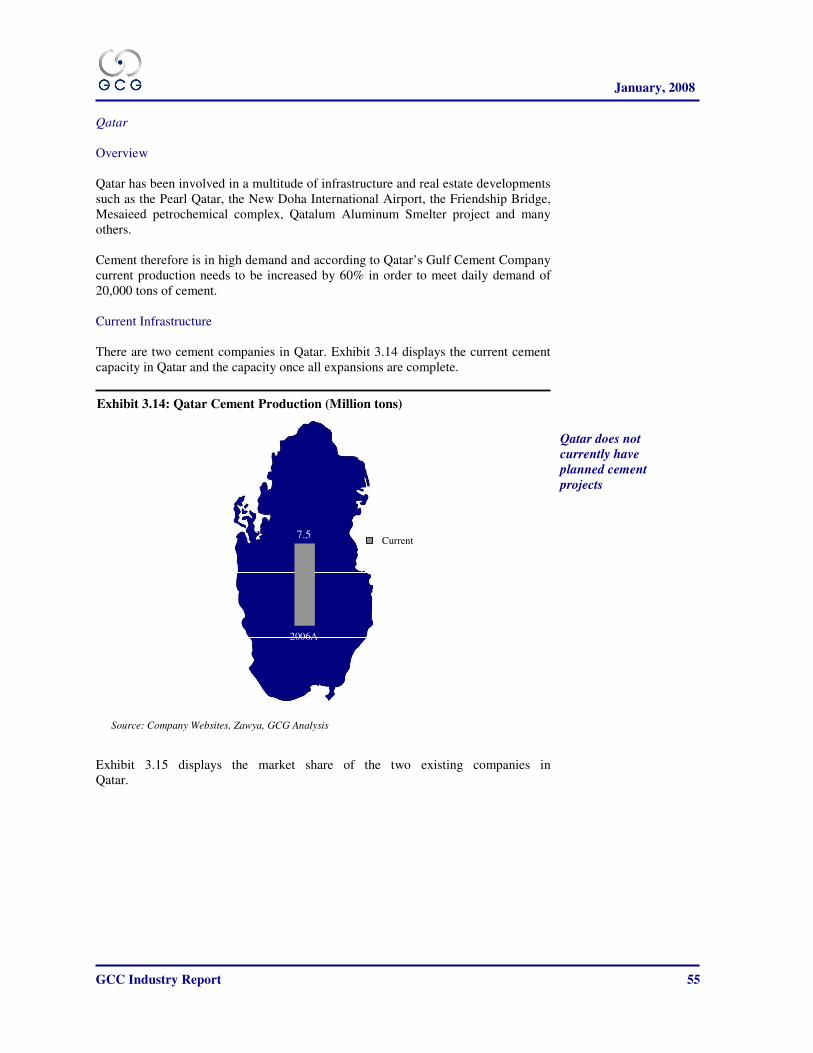

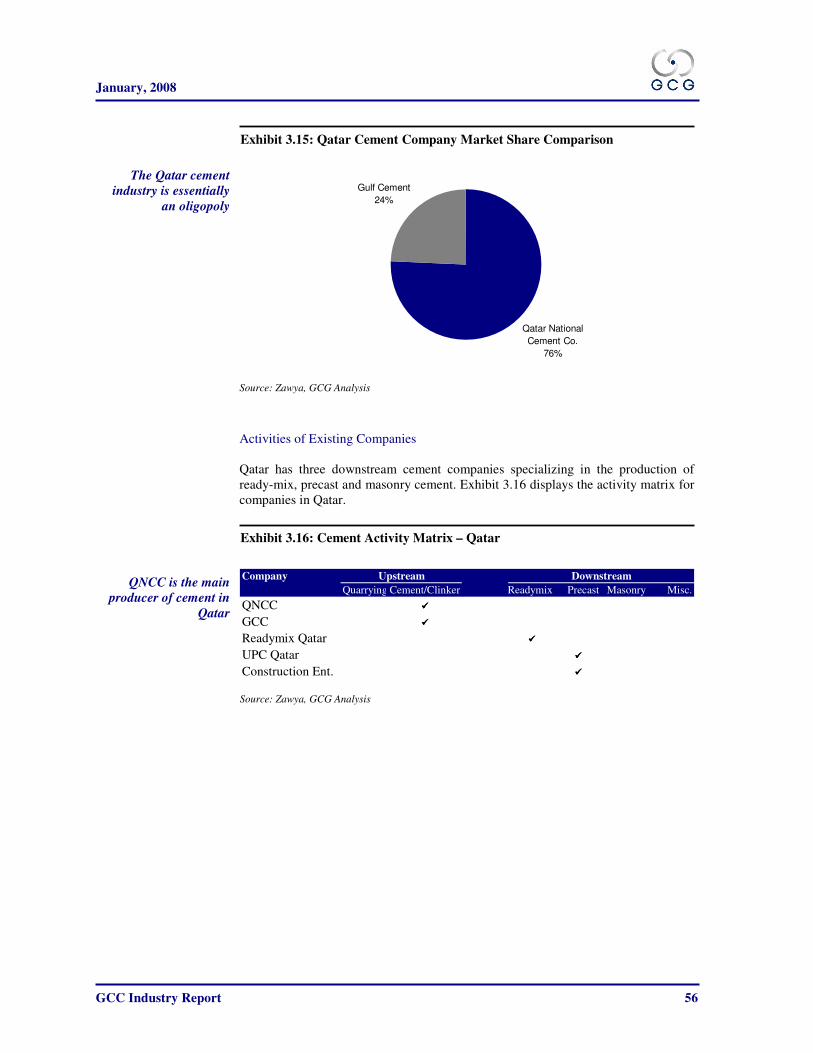

Qatar .............................................................................................................................................................55

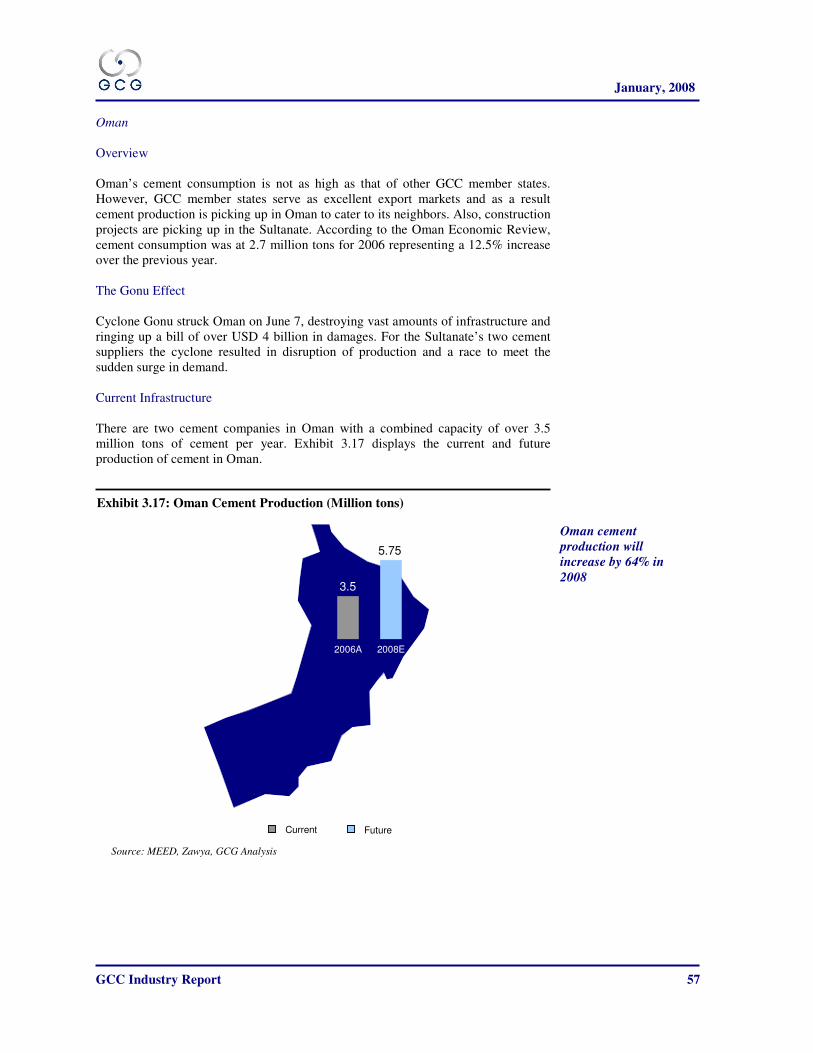

Oman.............................................................................................................................................................57

Kuwait ...........................................................................................................................................................59

Saudi Arabia .................................................................................................................................................60

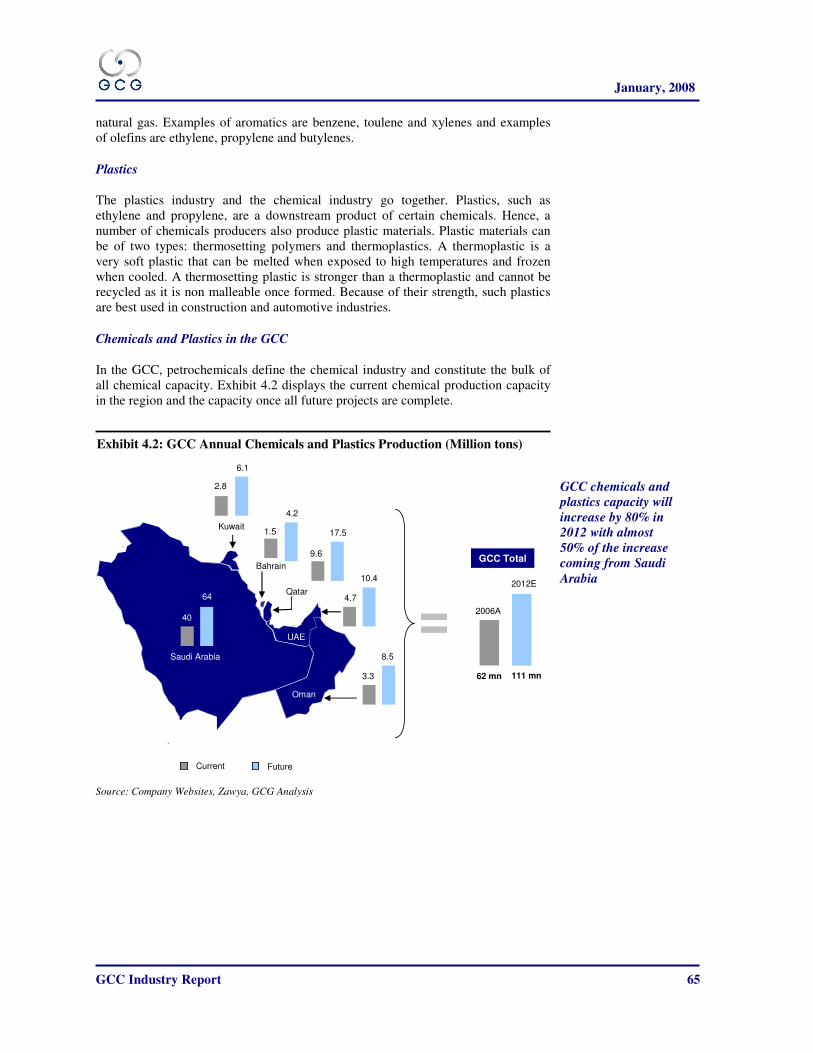

CHEMICALS AND PLASTICS...................................................................................................64

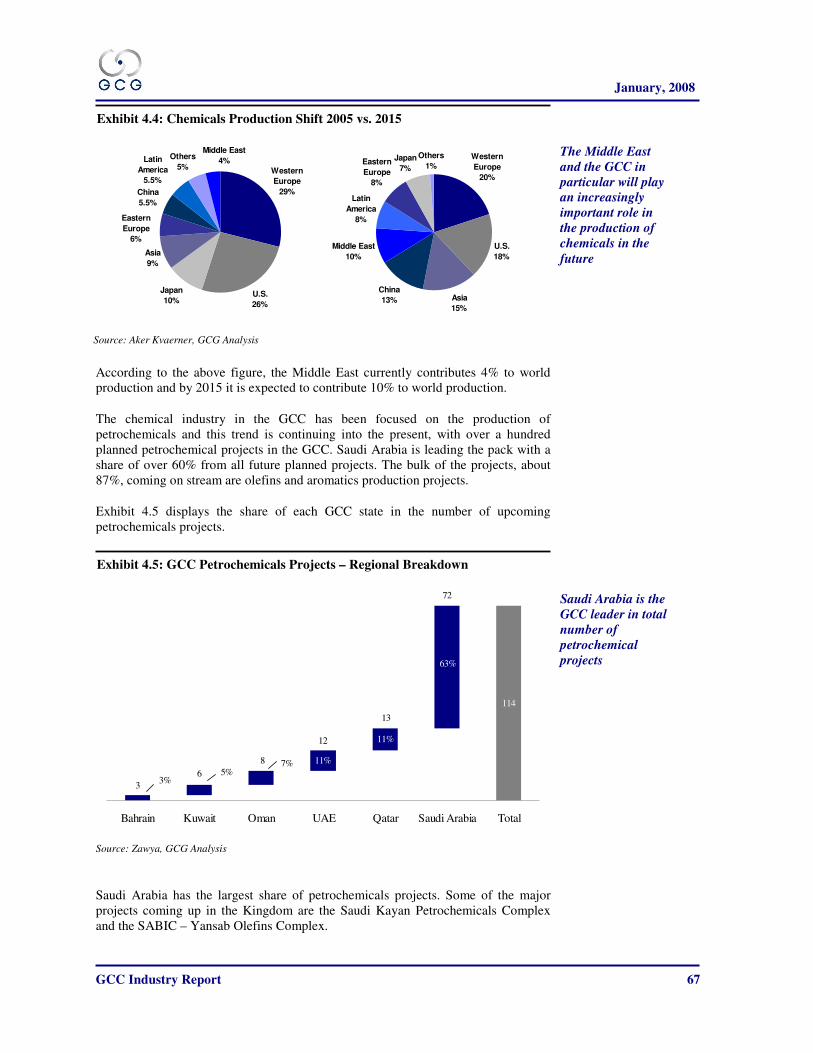

Chemicals and Plastics in the GCC .................................................................................................... 65

United Arab Emirates...................................................................................................................................70

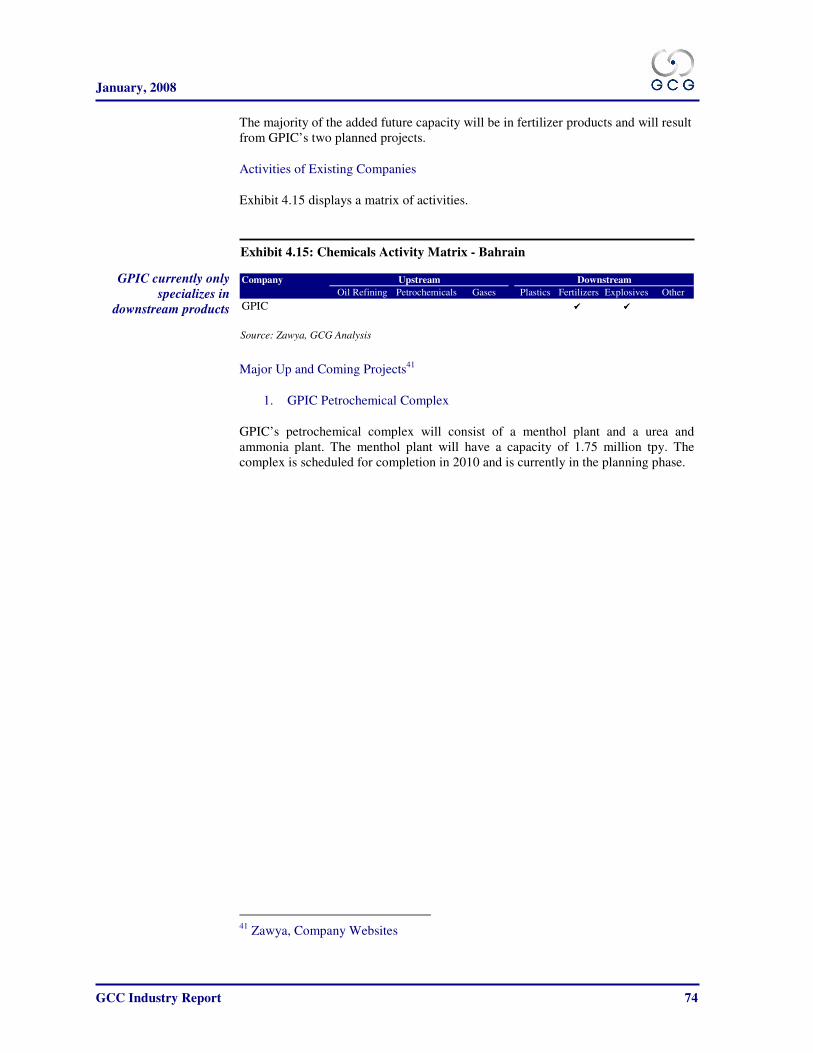

Bahrain .........................................................................................................................................................73

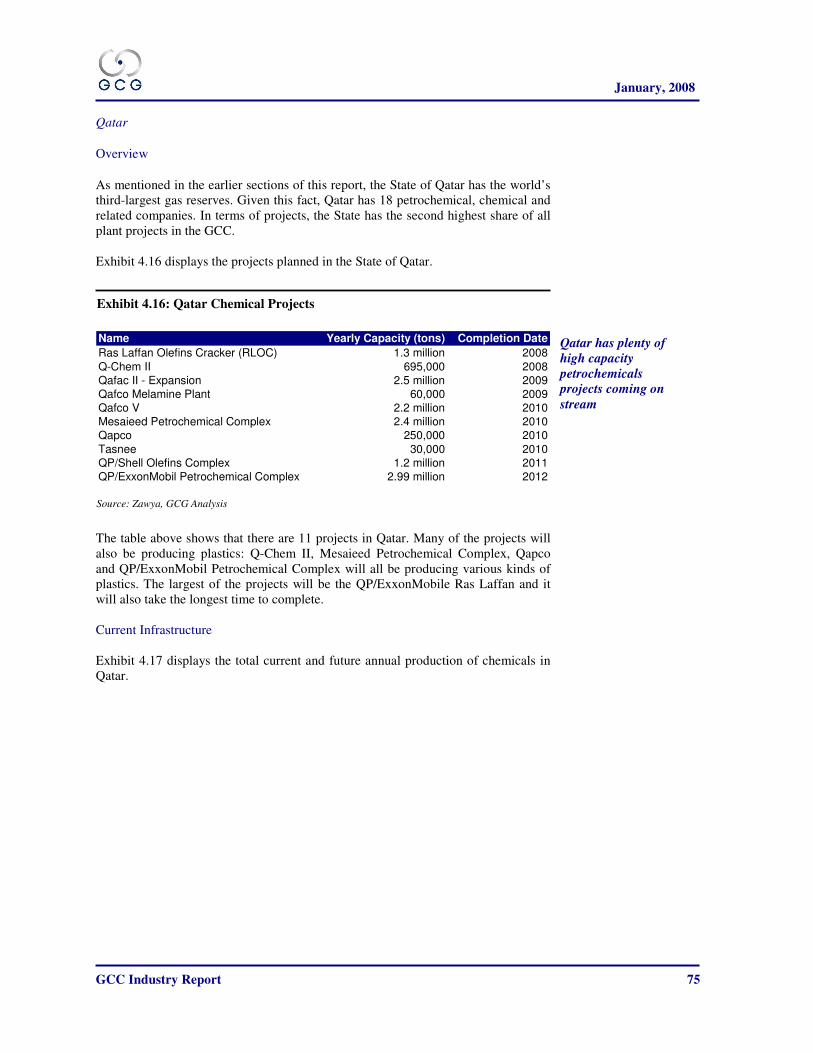

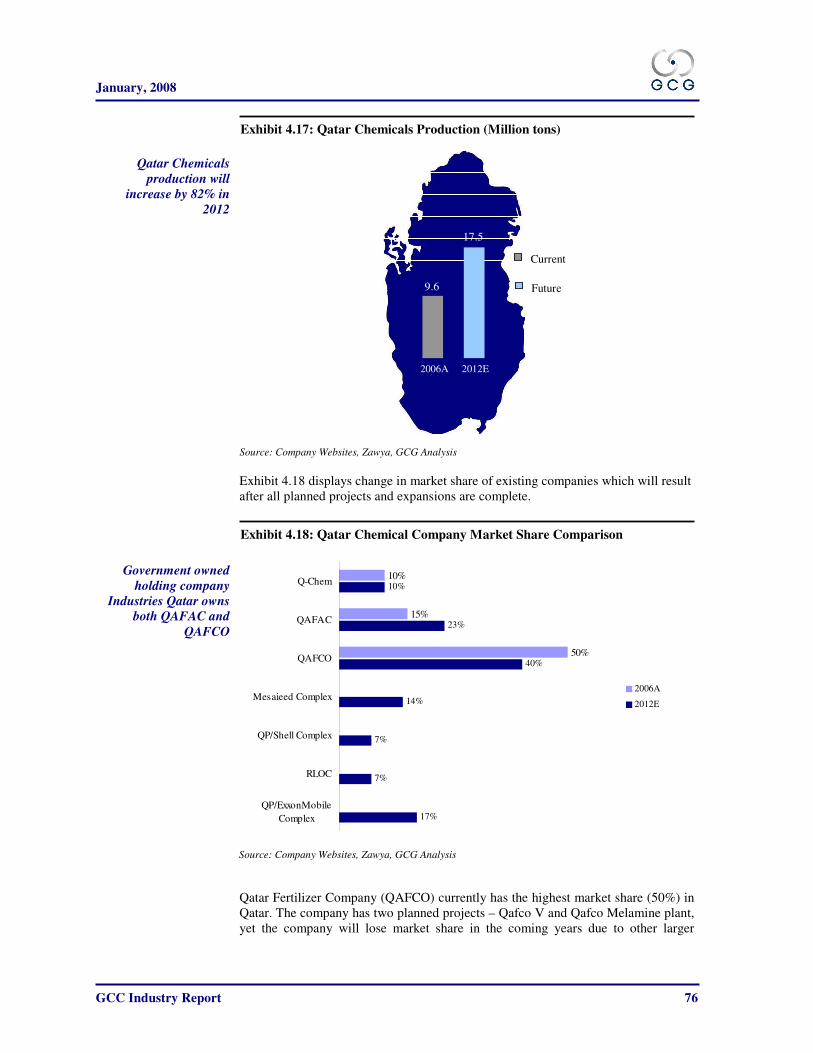

Qatar .............................................................................................................................................................75

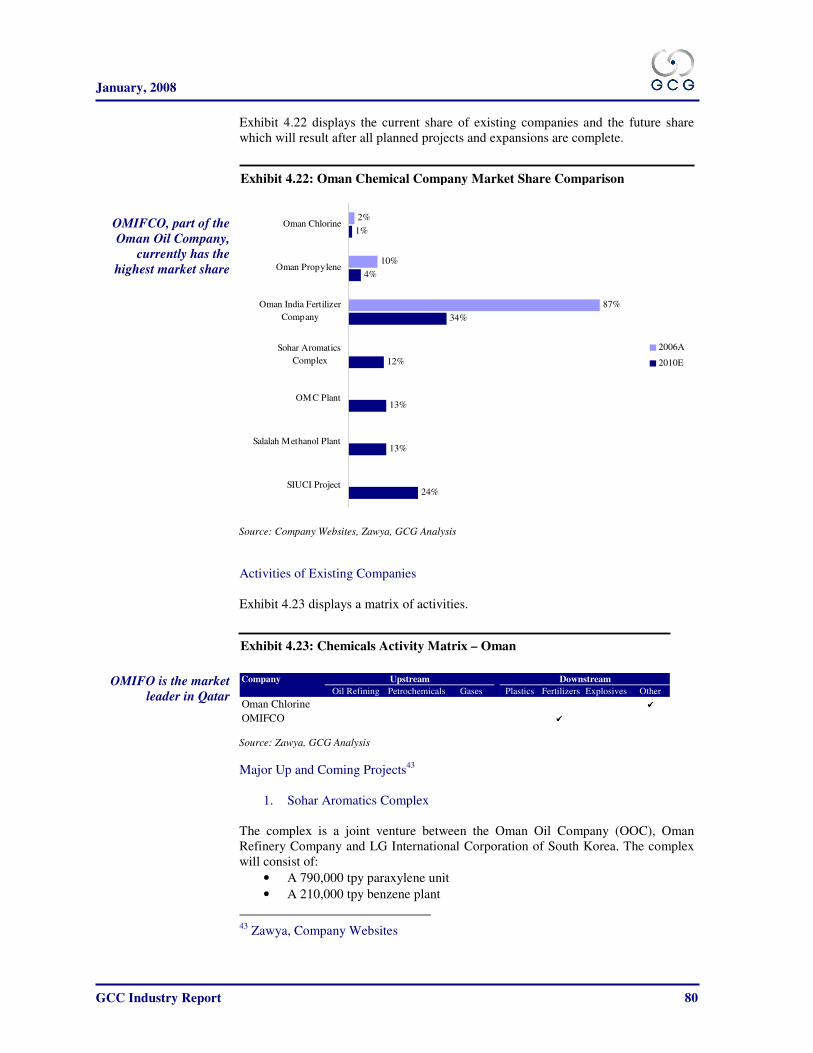

Oman.............................................................................................................................................................79

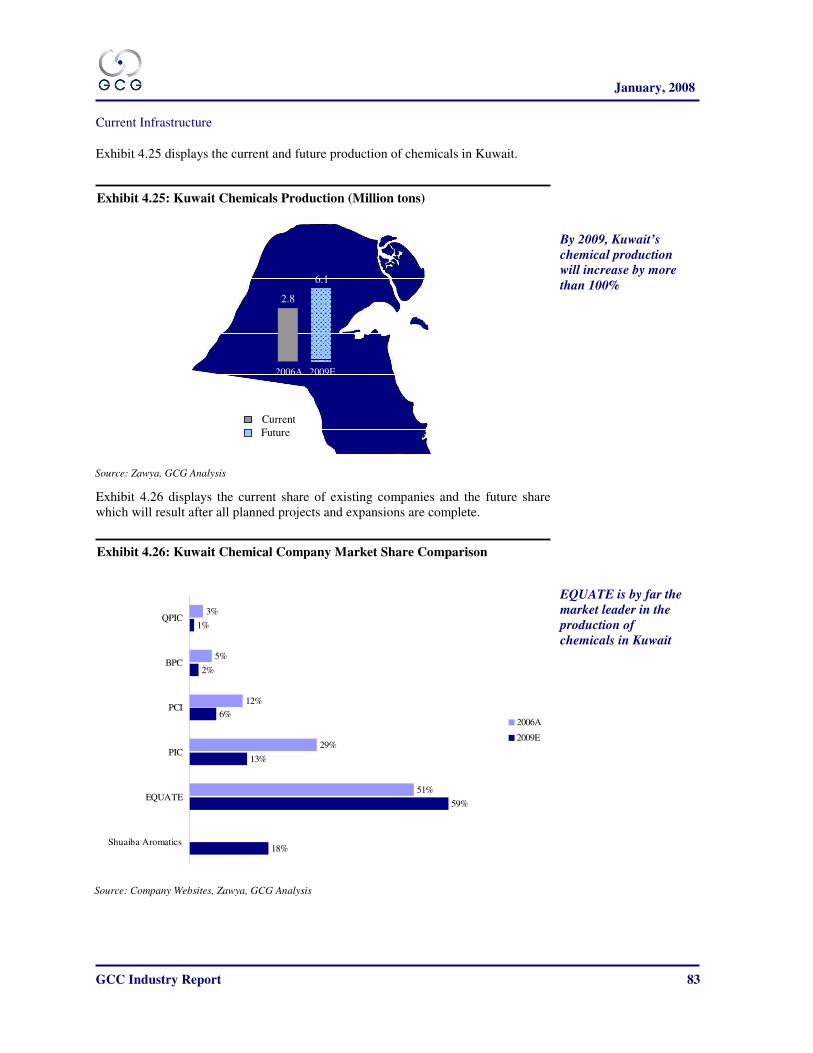

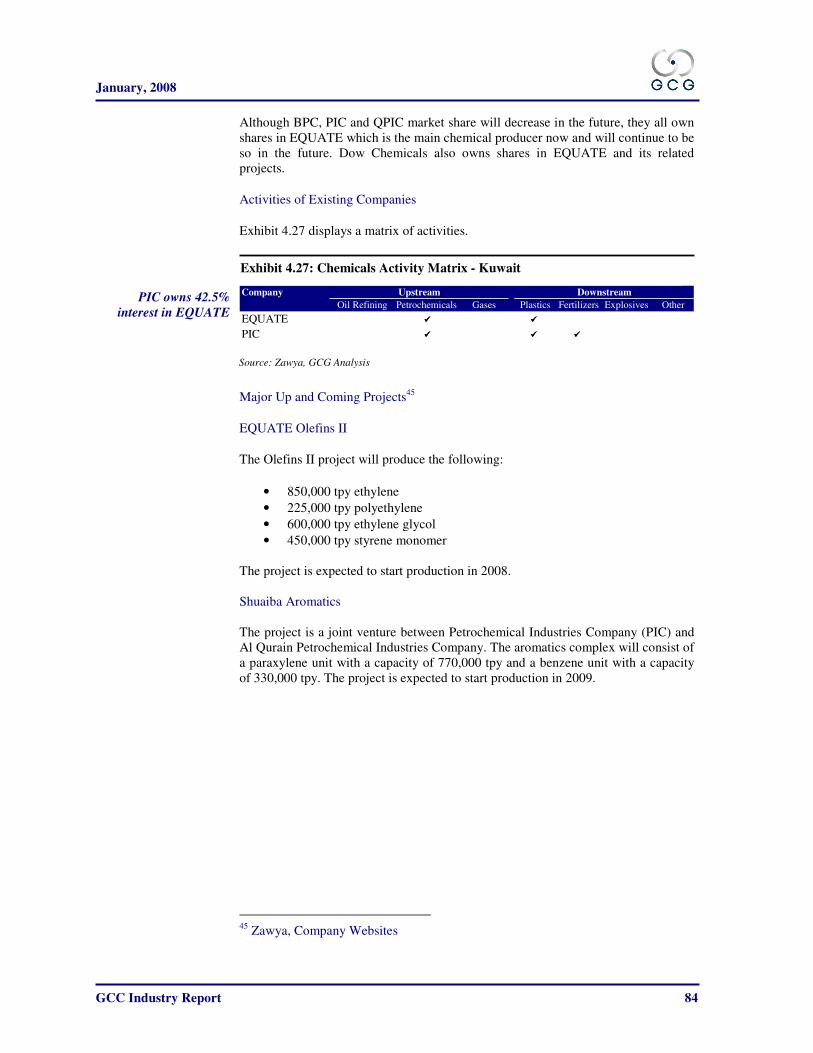

Kuwait ...........................................................................................................................................................82

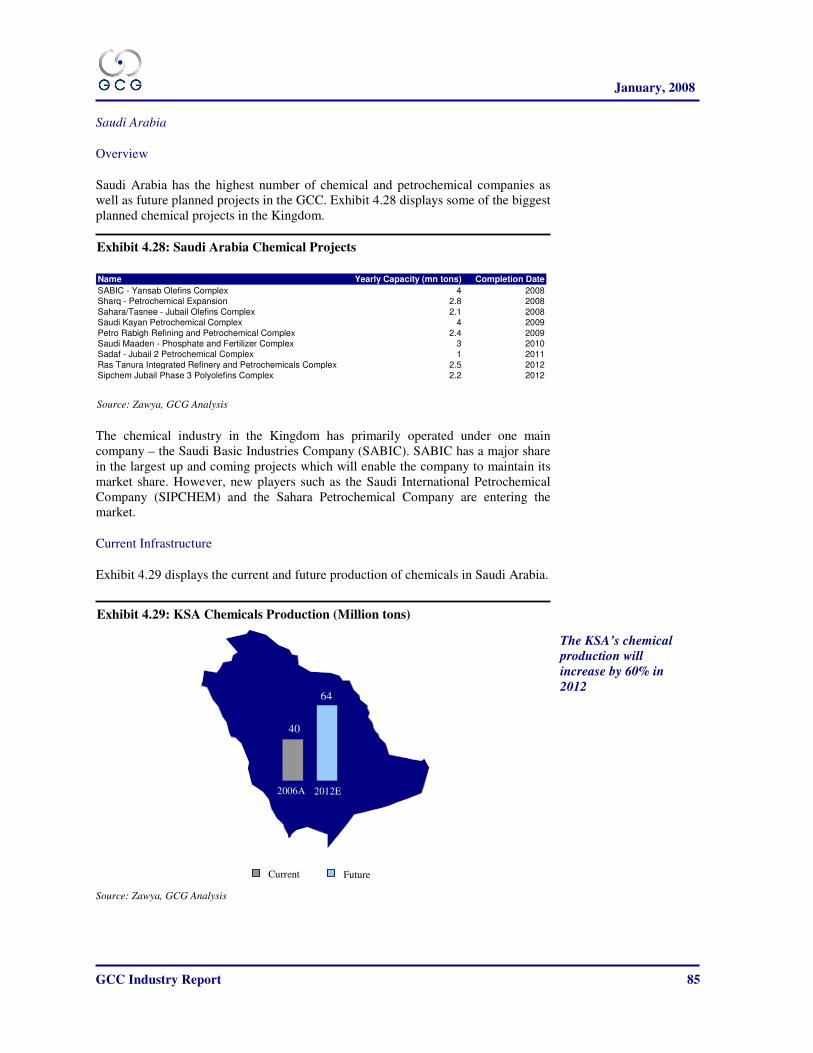

Saudi Arabia .................................................................................................................................................85

APPENDIX A – KEY COMPANY OVERVIEWS.......................................................................88

Aluminum ............................................................................................................................................ 88

Steel ...................................................................................................................................................... 94

Cement ............................................................................................................................................... 110

Chemicals and Plastics...................................................................................................................... 118

January, 2008

GCC Industry Report 1

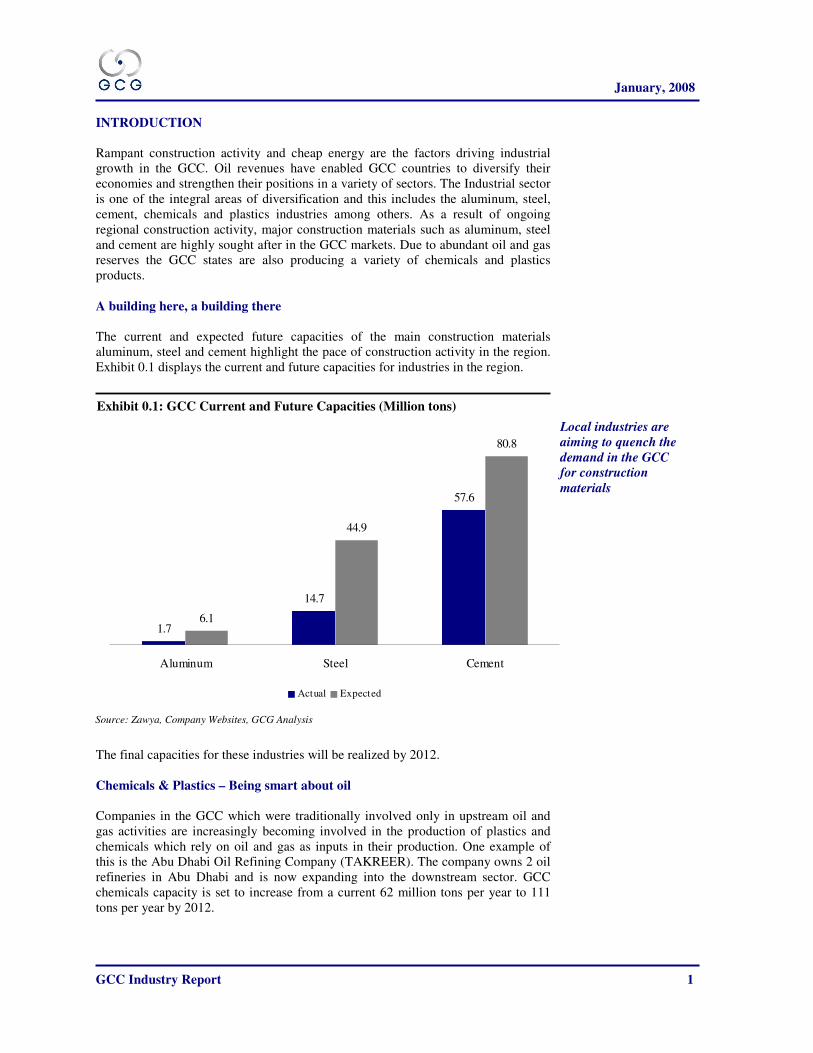

INTRODUCTION

Rampant construction activity and cheap energy are the factors driving industrial

growth in the GCC. Oil revenues have enabled GCC countries to diversify their

economies and strengthen their positions in a variety of sectors. The Industrial sector

is one of the integral areas of diversification and this includes the aluminum, steel,

cement, chemicals and plastics industries among others. As a result of ongoing

regional construction activity, major construction materials such as aluminum, steel

and cement are highly sought after in the GCC markets. Due to abundant oil and gas

reserves the GCC states are also producing a variety of chemicals and plastics

products.

A building here, a building there

The current and expected future capacities of the main construction materials

aluminum, steel and cement highlight the pace of construction activity in the region.

Exhibit 0.1 displays the current and future capacities for industries in the region.

1.7

14.7

57.6

6.1

44.9

80.8

Aluminum Steel Cement

Actual Expected

The final capacities for these industries will be realized by 2012.

Chemicals & Plastics – Being smart about oil

Companies in the GCC which were traditionally involved only in upstream oil and

gas activities are increasingly becoming involved in the production of plastics and

chemicals which rely on oil and gas as inputs in their production. One example of

this is the Abu Dhabi Oil Refining Company (TAKREER). The company owns 2 oil

refineries in Abu Dhabi and is now expanding into the downstream sector. GCC

chemicals capacity is set to increase from a current 62 million tons per year to 111

tons per year by 2012.

Exhibit 0.1: GCC Current and Future Capacities (Million tons)

Source: Zawya, Company Websites, GCG Analysis

Local industries are

aiming to quench the

demand in the GCC

for construction

materials

January, 2008

GCC Industry Report 2

Market Dynamics

Each industry is uniquely positioned and the market supply and demand varies from

industry to industry, from place to place. For example, suppliers can specialize in

either upstream production or downstream activities. The former involving those

processes that lay the foundation for the industry and the latter involving those

processes that result in end-user products. For example, in the aluminum industry,

only two GCC states have primary producing companies while in the cement and

steel industries, markets are highly fragmented with many primary producers.

Future Projects

Suppliers are keeping up with the pace of rising demand in the GCC by planning

projects in virtually all industries. Exhibit 0.2 displays the number of projects

planned for each industry.

42

15

119

Chemicals&Plastics Steel Cement Aluminum

Exhibit 0.2: GCC Future Planned Industrial Projects

Source: Zawya, Company Websites, GCG Analysis

Note: The Chemicals & Plastics bar includes the highest capacity projects in each GCC

country. Total projects are 114.

Industrial projects are

springing up all over

the GCC and

chemicals and plastics

projects exceed the

rest in numbers

January, 2008

GCC Industry Report 3

ALUMINUM

Aluminum has emerged as one of the most important metals to be used in the

twenty-first century. Its attractive characteristics — light, strong, anti-corrosive,

highly conductive, malleable, and recyclable — have made it perfectly suitable for a

remarkable number of applications.

While it is the third most abundant element in the earth’s crust, its use in

manufacturing and construction activities has arrived surprisingly late on the scene.

This is partially due to the sophisticated technological process needed to isolate the

metal from the various oxides in which it is naturally found. Also, iron and steel have

emerged as the building materials of choice since the days of the Industrial

Revolution. Various global advancements have spurred the development and use of

aluminum to date; from the early military build up of the previous century to the

recent emergence of China’s insatiable appetite.

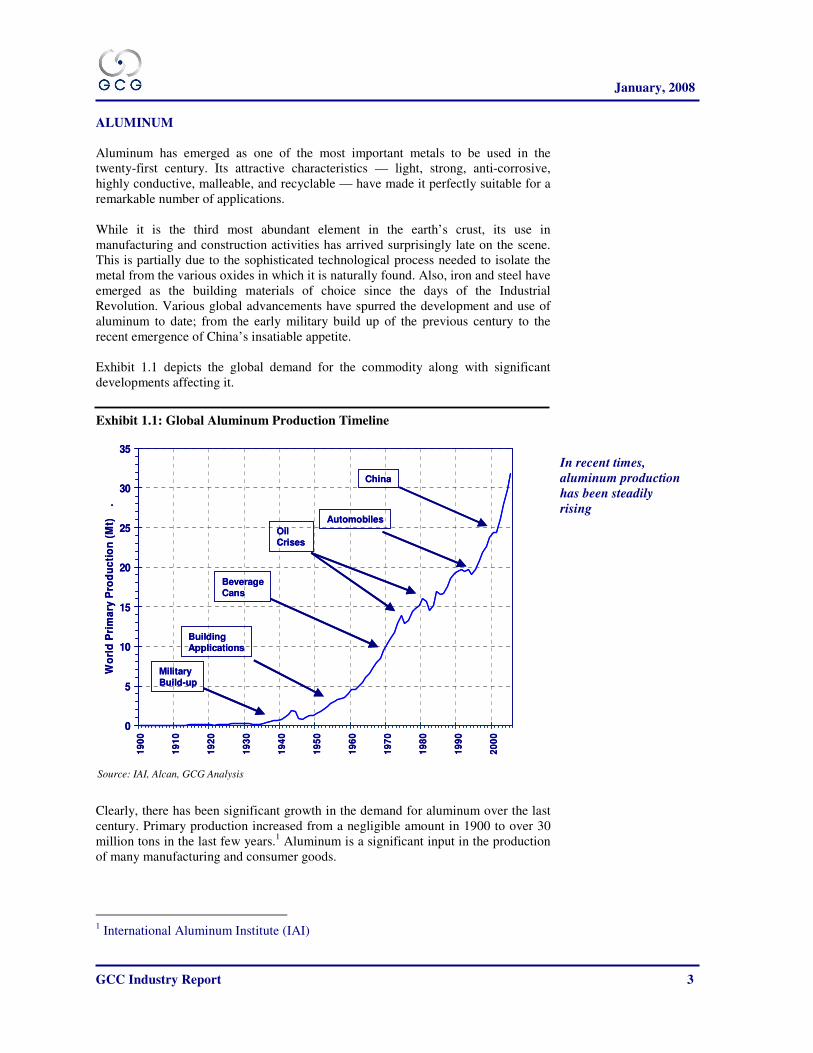

Exhibit 1.1 depicts the global demand for the commodity along with significant

developments affecting it.

Clearly, there has been significant growth in the demand for aluminum over the last

century. Primary production increased from a negligible amount in 1900 to over 30

million tons in the last few years.1 Aluminum is a significant input in the production

of many manufacturing and consumer goods.

1 International Aluminum Institute (IAI)

Exhibit 1.1: Global Aluminum Production Timeline

Source: IAI, Alcan, GCG Analysis

0

5

10

15

20

25

30

35

19

00

19

10

19

20

19

30

19

40

19

50

19

60

19

70

19

80

19

90

20

00

Wo

rld

Pri

ma

ry P

rod

uc

tio

n (

Mt)

.

MilitaryBuild-up

BuildingApplications

BeverageCans

OilCrises

Automobiles

China

0

5

10

15

20

25

30

35

19

00

19

10

19

20

19

30

19

40

19

50

19

60

19

70

19

80

19

90

20

00

Wo

rld

Pri

ma

ry P

rod

uc

tio

n (

Mt)

.

MilitaryBuild-up

BuildingApplications

BeverageCans

OilCrises

Automobiles

China

In recent times,

aluminum production

has been steadily

rising

January, 2008

GCC Industry Report 4

There are few other materials with as many diverse uses as aluminum, and because

of this reason its demand has managed to avoid significant ebbs and flows associated

with underlying business cycle fluctuations. The only sustained slowdown the

aluminum industry experienced was during the 1970’s and 1980’s when the global

energy crises created complications. The 1970’s oil crisis came about when the

Organization of Petroleum Exporting Countries (OPEC) decided to cut back on

exports to certain western countries and also raise the price of oil. As a result, a rise

in inflation and unemployment ensued. The 1980’s energy crisis came about when

political conflicts in Iran caused production there to almost stop, reducing the supply

of oil in the global market and thus raising the price.

Production Shift

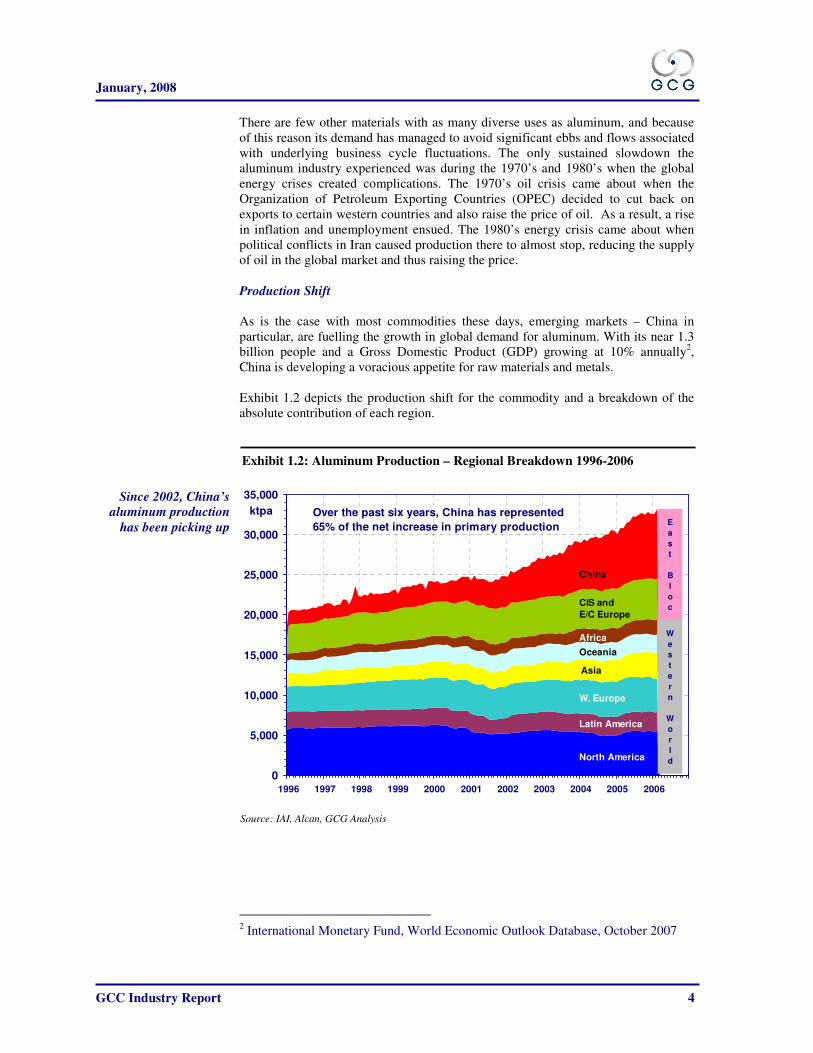

As is the case with most commodities these days, emerging markets – China in

particular, are fuelling the growth in global demand for aluminum. With its near 1.3

billion people and a Gross Domestic Product (GDP) growing at 10% annually2,

China is developing a voracious appetite for raw materials and metals.

Exhibit 1.2 depicts the production shift for the commodity and a breakdown of the

absolute contribution of each region.

2 International Monetary Fund, World Economic Outlook Database, October 2007

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Over the past six years, China has represented

65% of the net increase in primary production

North America

Latin America

W. Europe

Asia

Oceania

Africa

CIS and

E/C Europe

China

W

e

s

t

e

r

n

W

o

r

l

d

E

a

s

t

B

l

o

c

ktpa

Exhibit 1.2: Aluminum Production – Regional Breakdown 1996-2006

Source: IAI, Alcan, GCG Analysis

Since 2002, China’s

aluminum production

has been picking up

January, 2008

GCC Industry Report 5

Increased production in China has been the story over the last decade; Chinese

production is responsible for over half of the increase in global production since

1996. Generally speaking, a trend of production shifting from the West to the East

has emerged. In fact, not only has Eastern production increased but Western

production has simultaneously decreased. The net result underscores the production

redistribution trend.

Aluminum Facts

Aluminum can be produced via scrap metal (recycled aluminum) or via primary

production using bauxite. Regardless of the process used, molten aluminum is cast

into ingots which are then used in the production of extruded and rolled products.

Extruded products are used in the making of prefabricated buildings, window and

door frame systems, curtain walling and a variety of facades. Rolled products include

foil, sheet and plate which are used packaging, transportation, electrical and

household applications.

Exhibit 1.3 displays the value chain for aluminum.

Exhibit 1.3: Aluminum Products Value Chain

Source: The Aluminum Association, European Aluminum Association, GCG Analysis

Primary Aluminum

Slabs, Billets

Extruded Products Rolled Products

Fabricated Products

Powder and Paste

Aluminum products

are used in every

industry imaginable

January, 2008

GCC Industry Report 6

Aluminum in the GCC

While most of the GCC countries are currently planning major aluminum projects,

only the United Arab Emirates and Bahrain are presently producing primary

aluminum. The two primary aluminum smelting companies in the region are United

Arab Emirates’ DUBAL and Bahrain’s ALBA and together they are presently

producing over 1.7 million tons3 of aluminum representing the entire region’s

primary aluminum production. However, a number of projects on the horizon will

change the landscape of the industry into a much more fragmented one than it

currently is.

Exhibit 1.4 displays the current aluminum capacity in the region and the capacity

once all future projects are complete.

Similar to the trend occurring in China, aluminum production is shifting to GCC

countries. There are two primary reasons why the GCC, in particular, is an attractive

environment for aluminum production facilities, namely:

1) Comparative Advantage – Energy: The GCC region has substantial oil and

gas reserves. Given that aluminum smelting is an energy intensive process

(one quarter to one third of production cost)4, the region has a natural

advantage that has begun to be profitably exploited by both local and

international players.

3 Company Websites

4 The Aluminium Association, 2004

Exhibit 1.4: GCC Annual Aluminum Production (Million tons)

Source: Company Websites, Zawya, GCG Analysis

Oman, Qatar and

KSA member states

are all planning a

smelting complex

1.7

2006A

6.1

2012E

UAE

Oman

Saudi Arabia

Bahrain

Qatar

1.2

0.86

3

0.87

0.18

0.51

1.5

GCC Total

Current Future

0.12

Kuwait

January, 2008

GCC Industry Report 7

Exhibit 1.5 displays a breakdown of aluminum smelting costs.

Raw Materials

50%

Energy

30%

Other

20%

2) Proximity to Key Markets: The petrodollar influx of the last few years has

fuelled substantial economic and infrastructure development. The resulting

increase in domestic demand, coupled with the region’s proximity to

Europe and the Subcontinent, which serve as key export markets,

has proven to create juicy opportunities for smelter operations in this

region.

Exhibit 1.6 displays the key global markets in proximity to the GCC.

Exhibit 1.6: Key Markets in Proximity to the GCC

Source: GCG Analysis

GCC

Africa

India

China

Europe

Russia

SE Asia

Exhibit 1.5: Aluminum Production Costs – Global Average

Source: Industry Sources, GCG Analysis

The GCC has a

significant cost

advantage when it

comes to one of the

primary cost

components – energy.

The GCC has a prime

location in relation to

lucrative export

markets

January, 2008

GCC Industry Report 8

Raw Material Procurement

Since aluminum is extremely reactive, it is not found in its original form but as one

of a selection of around 250 minerals. Hence, one challenge that exists for upstream

aluminum producers in the GCC is the limited access to the chief raw material and

principle ore involved in the production of aluminum – bauxite. To this end, GCC

states have forged alliances and developed units abroad to maintain a sufficient

supply of the raw material.

Popularity of Extruded Products

Aluminum is highly suited to the extrusion process due to its malleability

characteristics at high temperatures and thus it can be cast, rolled or extruded into an

infinite variety of shapes. The term ‘extrusion’ is used interchangeably to refer to

both the end-products and the process by which the products are created. The

construction industry has a high requirement for aluminum extrusions or customized

aluminum profiles. Given the fact that construction is a rampant activity in the GCC,

companies have sprung up to quench the demand in the region for extruded

aluminum products.

January, 2008

GCC Industry Report 9

GCC Aluminum Projects

Given the advantages of establishing smelting operations in the GCC it is

understandable that each of the member states that do not currently have smelting

operations, except Kuwait, has begun planning for its respective aluminum industry.

Exhibit 1.7 displays the total number of projects in the GCC. The graph shows the

total number of projects for each country and the share of each country in the total

project pie.

9

1

2

3

4

Qatar Oman Saudi Arabia UAE Total

33%

11%

11%

44%

The previous graph shows that several projects are underway in the GCC region,

with Saudi Arabia, Qatar and Oman establishing aluminum production operations for

the first time. Exhibit 1.8 displays the current scenario of aluminum projects in the

GCC with greater detail.

Name Yearly Capacity (tons) Completion Date Country

DIC Aluminum Glass Factory N/A 2007 UAE

Sohar Aluminum Company Smelter 330,000 2008 Oman

Emirates Aluminum Smelter (EMAL) 1.4 million 2010 UAE

Nova Aluminum Processing Plant 135,000 2010 UAE

Jizan Aluminum Complex 700,000 2010 KSA

Al Ahsa - Jubail Aluminum Chip Manufacturing 45,000 2010 KSA

Qatalum Aluminum Smelter 585,000 2010 Qatar

Ruwais Aluminum Smelter 550,000 2011 UAE

Garmco Aluminum Rolling Mill 160,000 2011 Oman

Maaden Integrated Aluminum Complex 720,000 2012 KSA

In addition to having the most number of planned projects, the UAE and Saudi

Arabia also have the highest number of downstream aluminum companies.

Exhibit 1.9 displays the total number of companies in each country and the share of

each country in the total pie.

Exhibit 1.8: GCC Aluminum Project Details

Source: Zawya, GCG Analysis

Exhibit 1.7: GCC Aluminum Smelter Projects – Regional Breakdown

Source: Zawya, GCG Analysis

The UAE and Saudi

Arabia are planning

the maximum number

of smelting projects

The UAE, KSA and

Qatar are planning

projects with the

highest capacities in

the GCC

January, 2008

GCC Industry Report 10

41

13

5

7

11

14

Oman Qatar Kuwait Bahrain UAE Saudi

Arabia

Total

7%

2%12%

17%

27%

34%

Exhibit 1.9: GCC Aluminum Smelting and Non-Smelting Companies

Source: Zawya, GCG Analysis

All GCC states have

downstream

companies with UAE

and Bahrain having

primary production

capabilities

January, 2008

GCC Industry Report 11

United Arab Emirates

Overview

Aluminum is one of the oldest and most important non-petroleum industries in the

United Arab Emirates. The sector has spearheaded the country’s drive to diversify its

economy away from the oil and gas sector and to gain a foothold in this highly

important industry. The availability of raw materials and major resources used in the

production is qualifying the country to be dominant in the GCC aluminum industry.

Current Infrastructure

The UAE currently has eleven companies specializing in upstream and downstream

aluminum related activities5. Among these DUBAL is the only primary production

facility in the UAE. Exhibit 1.10 displays the total current and future annual

production of aluminum in the UAE.

Although Dubai has a number of downstream companies, there are only two players

in the market with significant production levels.

Exhibit 1.11 displays the current share of existing companies and the future share

which will result after all planned projects are operational.

5 Zawya, GCG Analysis

Exhibit 1.10: UAE Aluminum Metal and Related Production (Million tons)

Source: DUBAL, Zawya, GCG Analysis

Projects coming on

stream will represent

almost a 250%

increase in capacity to

the aluminum

industry in the UAE

.86

3

Current Future

2006A 2011E

January, 2008

GCC Industry Report 12

7%

93%

52%

18%

23%

3%

4%

2006A 2011E

Gulf Extrusions Dubal Noval Ruwais Mubadala (EMAL)

The above graph highlights the change in market share of the existing two players

which will result once existing players complete capacity expansions and once new

players enter the market. For example, after three new players enter the market,

DUBAL’s market share will decrease from a current 93% to an estimated 52% in 5

years.

Activities of Existing Companies

As mentioned earlier, DUBAL is the only upstream (i.e. production of aluminum

metal) company in the UAE and the other companies are involved in various

downstream (i.e. production of end-products) activities. Exhibit 1.12 displays a

matrix of activities.

Company Upstream

Primary Prod. Extrusions Façade Syst. Bev. Cans Alum. & Glass Misc.

DUBAL ����

Gulf Extrusions ����

Alumco ���� ����

Alico ����

Alutec

Al Fahya (AFAF) ����

Bin Hussain ����

Hamarain and Partners

Rigidal ����

Sunrise Metal Coating ����

Thomas Bennett Gulf ����

Fabricated Metal Products

Exhibit 1.12: Aluminum Activity Matrix - UAE

Source: Zawya, GCG Analysis

Exhibit 1.11: UAE Aluminum Company Market Share Comparison

Source: Company Websites, Zawya, GCG Analysis

Aluminum companies

in the UAE produce a

variety of downstream

products

The UAE aluminum

industry landscape

will change quite

significantly as new

players come on board

January, 2008

GCC Industry Report 13

Major Up and Coming Projects6

The country’s capital, Abu Dhabi, has made a grand entrance into the aluminum

production scene over the past few years. Projects on the drawing board call for the

Emirate to become one of the largest aluminum producers in the world over the next

decade. Some of the major projects are:

1. Emirates Aluminum (EMAL)

In early 2007, Mubadala investment company and Dubai Aluminum came together

to create Emirates Aluminum (EMAL). The AED 33 billion project will have an

initial capacity of 700,000 tpy by 2010 and gradually increase its capacity to 1.4

million tpy in the years that follow. DUBAL’s technological expertise will play a

critical role in this project.

2. Ruwais Aluminum Smelter

During late 2006, General Holding Corporation and Rio Tinto Aluminum formed the

Abu Dhabi Aluminum Company (ADALCO) under which the Ruwais Aluminum

Smelter Project was launched. The project, valued at approximately AED 70 billion,

will have an initial capacity of 550,000 tpy which will be increased to 2 million tpy

over several phases. The first phase of the project is expected to be completed in

2011.

Upon completion of these two mega projects, the UAE will become the GCC’s top

aluminum producer with a total capacity of over 3 million tons.

6 Zawya, Company Websites

January, 2008

GCC Industry Report 14

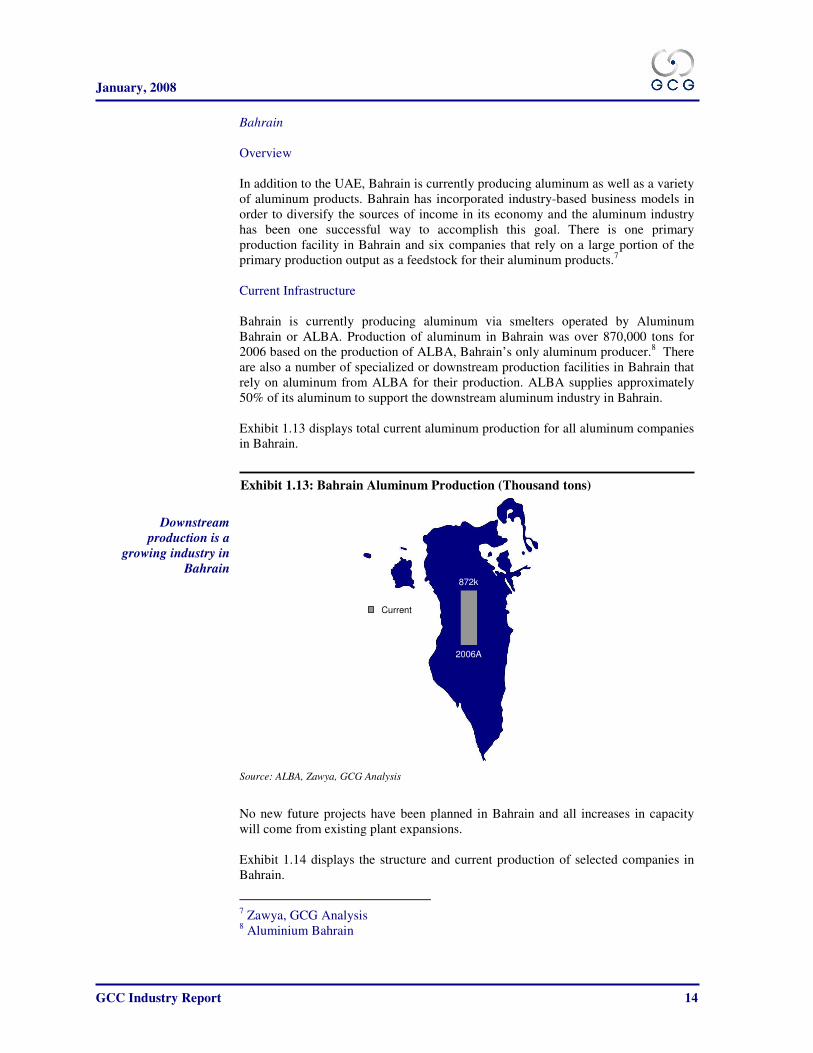

Bahrain

Overview

In addition to the UAE, Bahrain is currently producing aluminum as well as a variety

of aluminum products. Bahrain has incorporated industry-based business models in

order to diversify the sources of income in its economy and the aluminum industry

has been one successful way to accomplish this goal. There is one primary

production facility in Bahrain and six companies that rely on a large portion of the

primary production output as a feedstock for their aluminum products.7

Current Infrastructure

Bahrain is currently producing aluminum via smelters operated by Aluminum

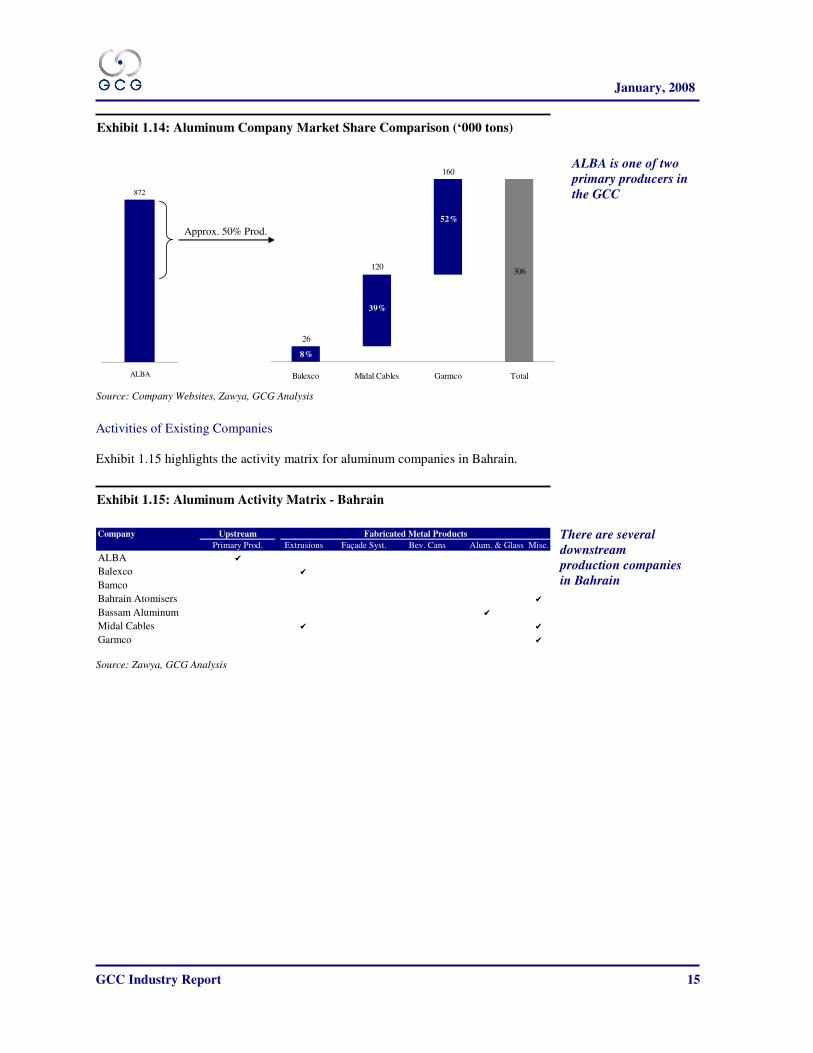

Bahrain or ALBA. Production of aluminum in Bahrain was over 870,000 tons for

2006 based on the production of ALBA, Bahrain’s only aluminum producer.8 There

are also a number of specialized or downstream production facilities in Bahrain that

rely on aluminum from ALBA for their production. ALBA supplies approximately

50% of its aluminum to support the downstream aluminum industry in Bahrain.

Exhibit 1.13 displays total current aluminum production for all aluminum companies

in Bahrain.

No new future projects have been planned in Bahrain and all increases in capacity

will come from existing plant expansions.

Exhibit 1.14 displays the structure and current production of selected companies in

Bahrain.

7 Zawya, GCG Analysis

8 Aluminium Bahrain

Exhibit 1.13: Bahrain Aluminum Production (Thousand tons)

Source: ALBA, Zawya, GCG Analysis

Downstream

production is a

growing industry in

Bahrain 872k

2006A

Current

January, 2008

GCC Industry Report 15

s

Activities of Existing Companies

Exhibit 1.15 highlights the activity matrix for aluminum companies in Bahrain.

Company Upstream

Primary Prod. Extrusions Façade Syst. Bev. Cans Alum. & Glass Misc.

ALBA ����

Balexco ����

Bamco

Bahrain Atomisers ����

Bassam Aluminum ����

Midal Cables ���� ����

Garmco ����

Fabricated Metal Products

Exhibit 1.14: Aluminum Company Market Share Comparison (‘000 tons)

Source: Company Websites, Zawya, GCG Analysis

Exhibit 1.15: Aluminum Activity Matrix - Bahrain

Source: Zawya, GCG Analysis

ALBA is one of two

primary producers in

the GCC

There are several

downstream

production companies

in Bahrain

872

ALBA

306

26

120

160

8%

39%

52%

Balexco Midal Cables Garmco Total

Approx. 50% Prod.

January, 2008

GCC Industry Report 16

Qatar

Overview

Qatar has the world’s third-largest gas reserves9. It therefore comes as no surprise

that the State has encouraged and invested heavily in utilizing its natural resources to

establish a healthy manufacturing and industrial sector. Qatar has three downstream

aluminum companies and although Qatar does not currently have aluminum

producing capabilities, an exciting project is underway, namely, Qatalum.

Current Infrastructure

Qatar has three companies specializing in downstream production activities. These

are Aluglass, Alutec and Ishaq and Sons Co.10

These are all small companies that do

not have significant production numbers.

Exhibit 1.16 displays expected future aluminum production in Qatar.

The future production number represents the production which will be available once

Qatar’s major aluminum project, Qatalum, begins production.

9 Ministry of Economy and Commerce, State of Qatar

10 Zawya, GCG Analysis

Exhibit 1.16: Qatar Future Aluminum Production (Million tons)

Source: Company Websites, Zawya, GCG Analysis

2010E

1.2

Qatar has

one major aluminum

project in the pipeline

January, 2008

GCC Industry Report 17

Activities of Existing Companies

Exhibit 1.17 highlights the activity matrix for the three companies in Qatar.

Company Upstream

Primary Production Extrusions Façade Systems Beverage Cans Aluminum and Glass Misc.

Aluglass ���� ����

ALU-TEC ����

Ishaq and Sons Co. ����

Fabricated Metal Products

Major Up and Coming Projects11

1. Qatalum

In 2006 it was announced that government owned oil and gas company Qatar

Petroleum (QP), and Hydro, a Norwegian aluminum and renewable energy company,

initiated a new aluminum smelter project called Qatalum. The former company will

provide the energy component and the latter company will provide the technology

and expertise for producing extrusion ingles –the plants’ main product. The cost of

the project is estimated to be USD 4.8 billion and will include an aluminum smelter

and a 1350 megawatt power plant. The final capacity of the smelter will be 1.2

million tpy by 2010 and the first phase capacity will be 585,000 tpy. Construction of

the smelter is already underway.

Industrial Cities

Mesaieed Industrial City (MIC) and Ras Laffan Industrial City are the two main

industrial cities in the State of Qatar. The other two are Doha Industrial Estate and

Dukhan Petroleum City. MIC was set up to provide the services and infrastructure

for all present and future industries in Qatar. The Qatalum project will be established

in this industrial base. The Ras Laffan Industrial City is the State’s most recent

industrial city and the port at Ras Laffan is the world's largest Liquefied Natural Gas

(LNG) exporting facility.

11

Zawya, Company Websites

Exhibit 1.17: Aluminum Activity Matrix - Qatar

Source: Zawya, GCG Analysis

The aluminum

industry is quite small

in Qatar

January, 2008

GCC Industry Report 18

Oman

Overview

The Sultanate of Oman began plans to diversify its economy soon after the decline of

oil prices in 1999. Sources of non-oil income such as natural gas, industry,

manufacturing, tourism and the private sector formed the basis of the diversification

framework. Manufacturing is currently one of the key diversification areas of the

economy. Similar to Qatar, Oman does not have a primary metal production facility,

but a project is in the pipeline.

Current Infrastructure

Oman currently has a single downstream aluminum player and a single aluminum

project on the way. Exhibit 1.18 displays current and future capacity of aluminum in

the Sultanate.

Exhibit 1.19 compares the market scenario in Oman today and once the new project

is finalized, which will be the first primary production facility in Oman.

Exhibit 1.18: Oman Current and Future Aluminum Production (‘000 tons)

Source: Company Websites, Zawya, GCG Analysis

18k

508k

Current Future

2011E2006A

Downstream

production is low and

upstream production

is expected to begin in

a few years

January, 2008

GCC Industry Report 19

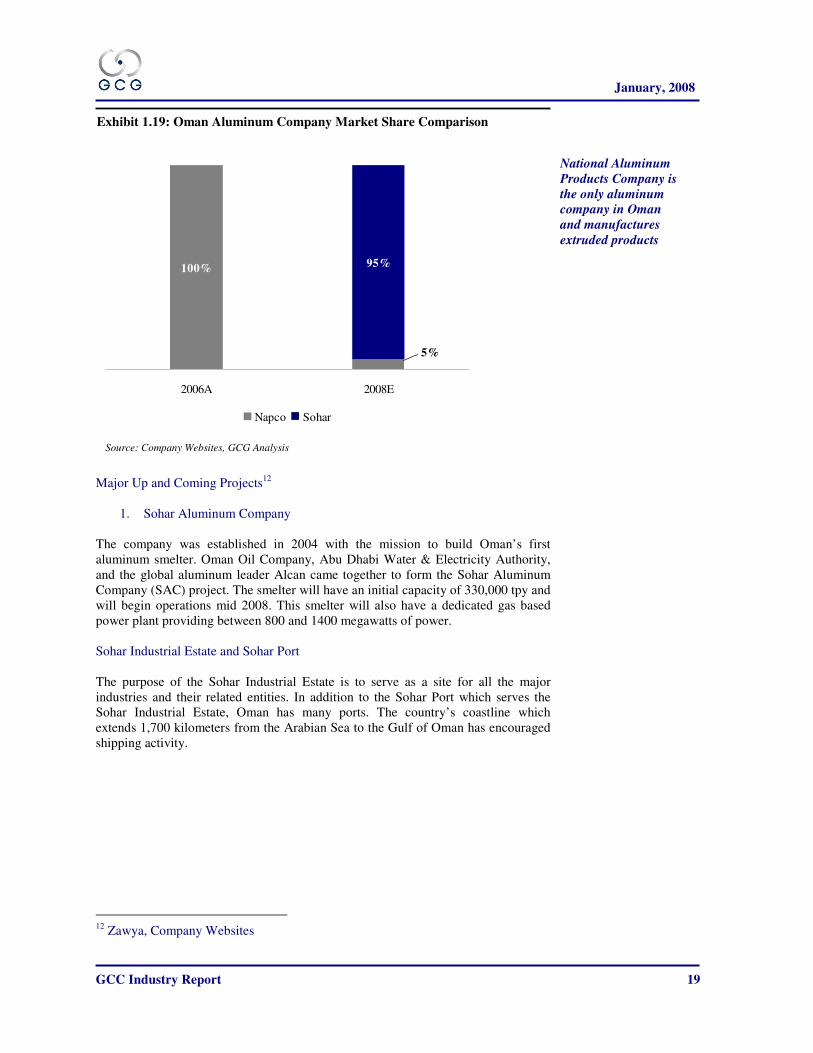

95%

5%

100%

2006A 2008E

Napco Sohar

Major Up and Coming Projects12

1. Sohar Aluminum Company

The company was established in 2004 with the mission to build Oman’s first

aluminum smelter. Oman Oil Company, Abu Dhabi Water & Electricity Authority,

and the global aluminum leader Alcan came together to form the Sohar Aluminum

Company (SAC) project. The smelter will have an initial capacity of 330,000 tpy and

will begin operations mid 2008. This smelter will also have a dedicated gas based

power plant providing between 800 and 1400 megawatts of power.

Sohar Industrial Estate and Sohar Port

The purpose of the Sohar Industrial Estate is to serve as a site for all the major

industries and their related entities. In addition to the Sohar Port which serves the

Sohar Industrial Estate, Oman has many ports. The country’s coastline which

extends 1,700 kilometers from the Arabian Sea to the Gulf of Oman has encouraged

shipping activity.

12

Zawya, Company Websites

Exhibit 1.19: Oman Aluminum Company Market Share Comparison

Source: Company Websites, GCG Analysis

National Aluminum

Products Company is

the only aluminum

company in Oman

and manufactures

extruded products

January, 2008

GCC Industry Report 20

Kuwait

Overview

According to the Public Authority for Industry (PAI), the industrial sector is one of

the most important sources of national income and the main pillar of the economy of

the State of Kuwait. With regards to the aluminum industry, the State of Kuwait has

five small to mid-size downstream aluminum businesses.

Current Infrastructure

Kuwait has five downstream aluminum companies.13

Exhibit 1.20 displays the

current downstream production in Kuwait.

Currently there are no planned projects in Kuwait.

Activities of Existing Companies

Exhibit 1.21 displays the activity matrix for the companies in Kuwait.

Company Upstream

Primary Prod. Extrusions Façade Syst. Bev. Cans Alum. & Glass Misc.

Kalexco ���� ����

Al Hadi Aluminum ����

Aluminum Industries Co. ���� ����

Arabian Light Metals ���� ����

Kuwait Aluminum Co. ���� ����

Fabricated Metal Products

13

Zawya, GCG Analysis

Exhibit 1.21: Aluminum Activity Matrix - Kuwait

Source: Company Websites, Zawya, GCG Analysis

Exhibit 1.20: Kuwait Aluminum Production (Thousand tons)

Source: Zawya, GCG Analysis

Production quantities

of downstream

aluminum products

are not significant

Most companies are

involved in the

distribution of

aluminum products

rather than primary

production

2006A

Current

12

January, 2008

GCC Industry Report 21

Saudi Arabia

Overview

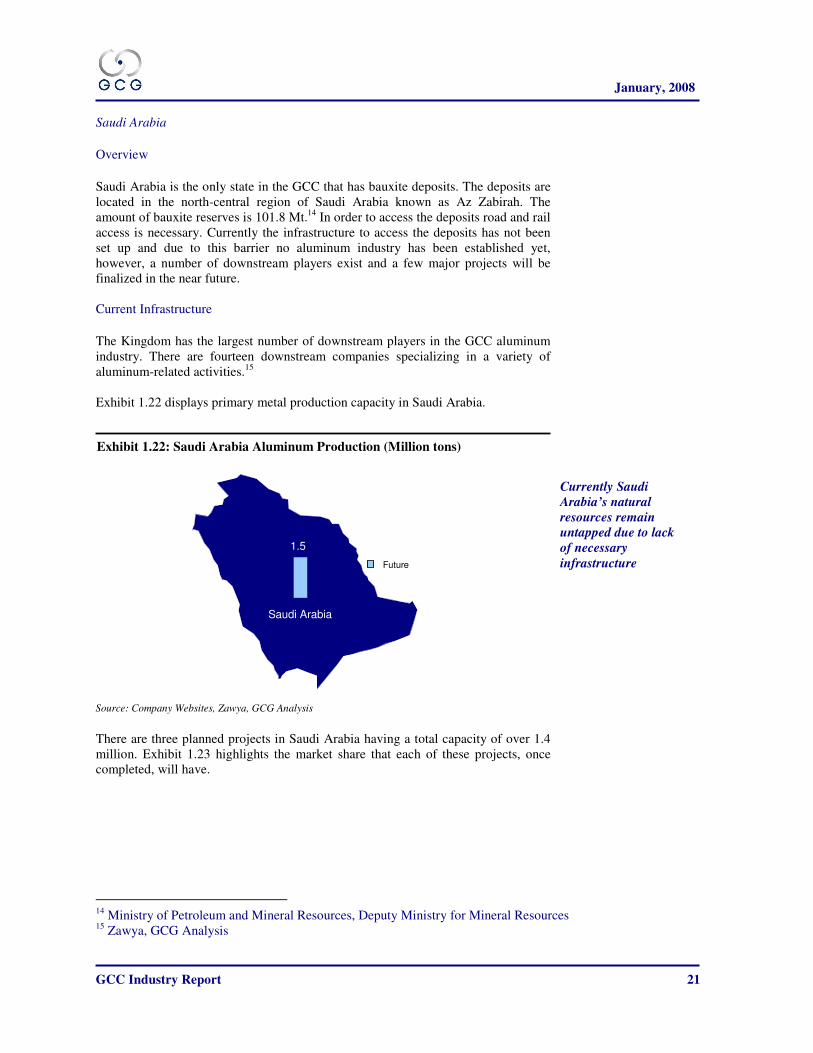

Saudi Arabia is the only state in the GCC that has bauxite deposits. The deposits are

located in the north-central region of Saudi Arabia known as Az Zabirah. The

amount of bauxite reserves is 101.8 Mt.14

In order to access the deposits road and rail

access is necessary. Currently the infrastructure to access the deposits has not been

set up and due to this barrier no aluminum industry has been established yet,

however, a number of downstream players exist and a few major projects will be

finalized in the near future.

Current Infrastructure

The Kingdom has the largest number of downstream players in the GCC aluminum

industry. There are fourteen downstream companies specializing in a variety of

aluminum-related activities.15

Exhibit 1.22 displays primary metal production capacity in Saudi Arabia.

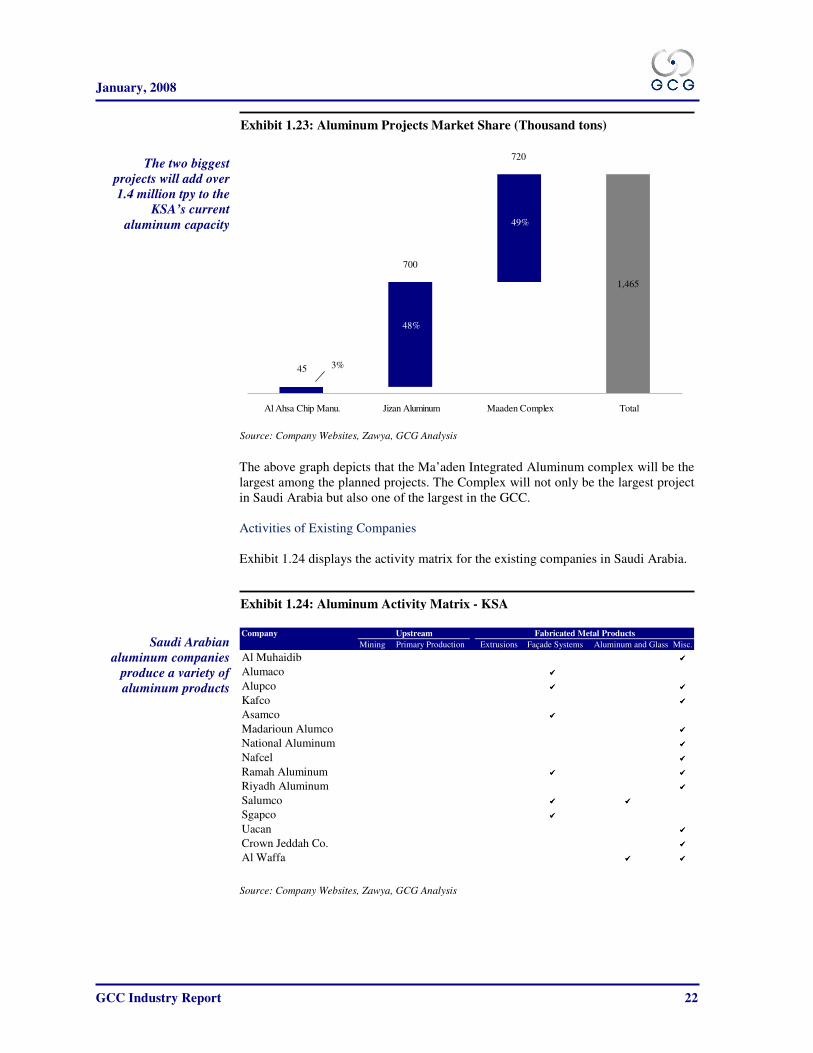

There are three planned projects in Saudi Arabia having a total capacity of over 1.4

million. Exhibit 1.23 highlights the market share that each of these projects, once

completed, will have.

14

Ministry of Petroleum and Mineral Resources, Deputy Ministry for Mineral Resources 15

Zawya, GCG Analysis

Exhibit 1.22: Saudi Arabia Aluminum Production (Million tons)

Source: Company Websites, Zawya, GCG Analysis

Currently Saudi

Arabia’s natural

resources remain

untapped due to lack

of necessary

infrastructure

Saudi Arabia

1.5

Future

January, 2008

GCC Industry Report 22

1,465

720

700

45

49%

48%

3%

Al Ahsa Chip Manu. Jizan Aluminum Maaden Complex Total

The above graph depicts that the Ma’aden Integrated Aluminum complex will be the

largest among the planned projects. The Complex will not only be the largest project

in Saudi Arabia but also one of the largest in the GCC.

Activities of Existing Companies

Exhibit 1.24 displays the activity matrix for the existing companies in Saudi Arabia.

Company

Mining Primary Production Extrusions Façade Systems Aluminum and Glass Misc.

Al Muhaidib ����

Alumaco ����

Alupco ���� ����

Kafco ����

Asamco ����

Madarioun Alumco ����

National Aluminum ����

Nafcel ����

Ramah Aluminum ���� ����

Riyadh Aluminum ����

Salumco ���� ����

Sgapco ����

Uacan ����

Crown Jeddah Co. ����

Al Waffa ���� ����

Fabricated Metal ProductsUpstream

Exhibit 1.24: Aluminum Activity Matrix - KSA

Exhibit 1.23: Aluminum Projects Market Share (Thousand tons)

Source: Company Websites, Zawya, GCG Analysis

The two biggest

projects will add over

1.4 million tpy to the

KSA’s current

aluminum capacity

Saudi Arabian

aluminum companies

produce a variety of

aluminum products

Source: Company Websites, Zawya, GCG Analysis

January, 2008

GCC Industry Report 23

Major Up and Coming Projects16

1. Ma’aden Az Zabira Aluminum Project

In order to capitalize the region’s significant bauxite reserves a bauxite mine,

alumina refinery and aluminum smelter are all being built via a USD 7 billion project

undertaken by the Saudi Arabian Mining Company also known as Ma’aden. Rail

and road access linking the mine to the refinery/smelter complex will be provided by

the Ministry of Finance. The smelter will have a capacity of 720,000 tpy and

Canada’s Alcan will be providing the refinery and smelter technology. A power and

desalination complex and a port will also be built. The project is scheduled to begin

operations in 2011.

2. Jazan Aluminum Smelter

Two thirds of the Jazan Economic City is a dedicated industrial zone. One of the

projects taking place will be the construction of an aluminum complex consisting of

a smelter with a capacity of 700,000 tpy and an integrated alumina refinery. The

project is scheduled to complete in 2010 and has an estimated cost of USD 4 billion.

16

Zawya, Company Websites

January, 2008

GCC Industry Report 24

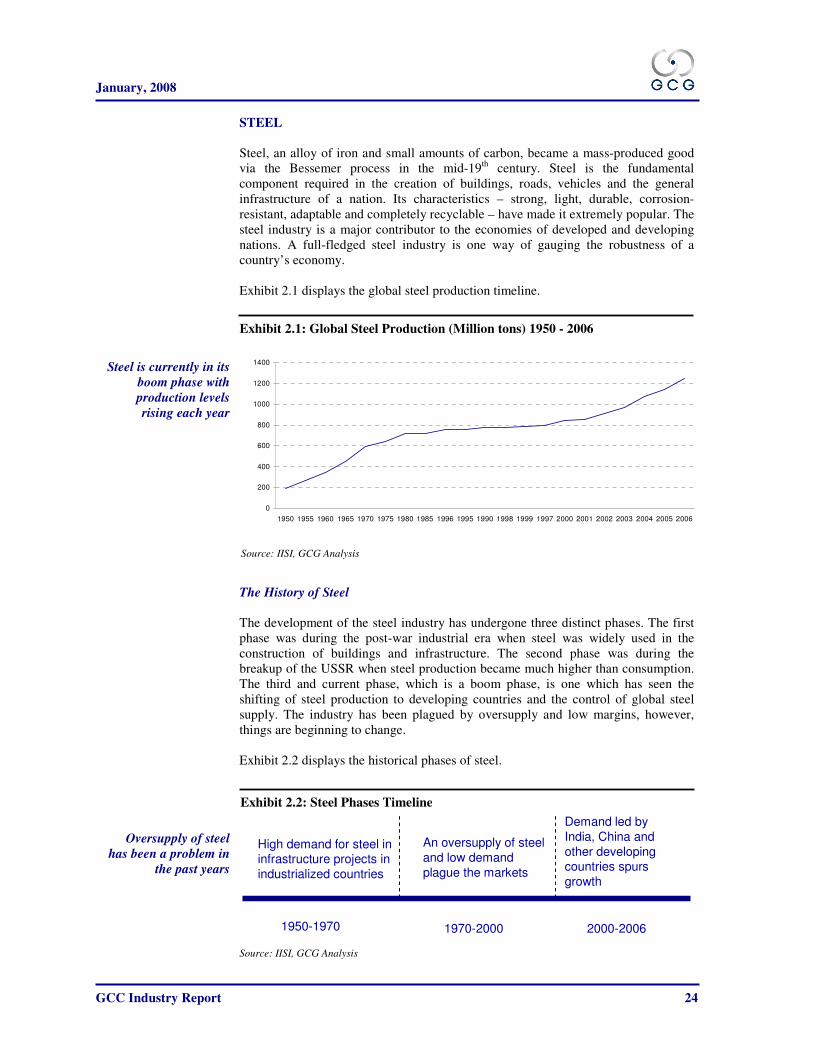

STEEL

Steel, an alloy of iron and small amounts of carbon, became a mass-produced good

via the Bessemer process in the mid-19th

century. Steel is the fundamental

component required in the creation of buildings, roads, vehicles and the general

infrastructure of a nation. Its characteristics – strong, light, durable, corrosion-

resistant, adaptable and completely recyclable – have made it extremely popular. The

steel industry is a major contributor to the economies of developed and developing

nations. A full-fledged steel industry is one way of gauging the robustness of a

country’s economy.

Exhibit 2.1 displays the global steel production timeline.

0

200

400

600

800

1000

1200

1400

1950 1955 1960 1965 1970 1975 1980 1985 1996 1995 1990 1998 1999 1997 2000 2001 2002 2003 2004 2005 2006

The History of Steel

The development of the steel industry has undergone three distinct phases. The first

phase was during the post-war industrial era when steel was widely used in the

construction of buildings and infrastructure. The second phase was during the

breakup of the USSR when steel production became much higher than consumption.

The third and current phase, which is a boom phase, is one which has seen the

shifting of steel production to developing countries and the control of global steel

supply. The industry has been plagued by oversupply and low margins, however,

things are beginning to change.

Exhibit 2.2 displays the historical phases of steel.

Exhibit 2.1: Global Steel Production (Million tons) 1950 - 2006

Source: IISI, GCG Analysis

Exhibit 2.2: Steel Phases Timeline

Source: IISI, GCG Analysis

Steel is currently in its

boom phase with

production levels

rising each year

1950-1970 1970-2000 2000-2006

High demand for steel in infrastructure projects in

industrialized countries

An oversupply of steel

and low demand

plague the markets

Demand led by

India, China and

other developing countries spurs

growth

Oversupply of steel

has been a problem in

the past years

January, 2008

GCC Industry Report 25

Steel Facts

Steel was first produced via the Bessemer process in the 1850’s. Iron ore is the main

raw material used in the making of steel and 98% of all mined iron ore is used for

this purpose.17

Major producers of iron ore include Australia and the BRIC countries

- Brazil, Russia, India and China. One interesting fact about steel is that it is highly

recyclable. The use of steel scrap in making steel is highly prevalent due to its lower

cost and the fact that steel retains its characteristics during the recycling process.

Steel products include long, flat, semi-finished, finished, hot rolled, cold-rolled etc.

Exhibit 2.3 classifies various kinds of steel products in terms their place along the

value chain.

Steel can be produced using scrap (recycled steel) in an electric arc furnace, using

iron ore, coke (a derivative of coal) and limestone in a blast furnace via the basic

oxygen steelmaking process or using iron ore in the direct reduction process (DRI)

using natural gas.

An ingot is the absolute first shape that molten metal takes on. After this, ingots can

be molded into blooms, billets and slabs. These are collectively referred to as semi

finished shapes or semi finished products. Blooms and billets are used in the

production of long products and slabs are used in the production of flat products.

Long products are bars, rods and steel sections. Flat products are plates, strip or hot-

rolled (HR) coils which are much thinner than plates. Specialty products include

coated steel products and wire.

17

Mineral Information Institute (MII)

Exhibit 2.3: Steel Products Value Chain

Source: Industry Websites, GCG Analysis

Long and flat

products have an

almost infinite

number of uses

Ingots

Semi-Finished Products

Long Products Flat Products Specialty Products

January, 2008

GCC Industry Report 26

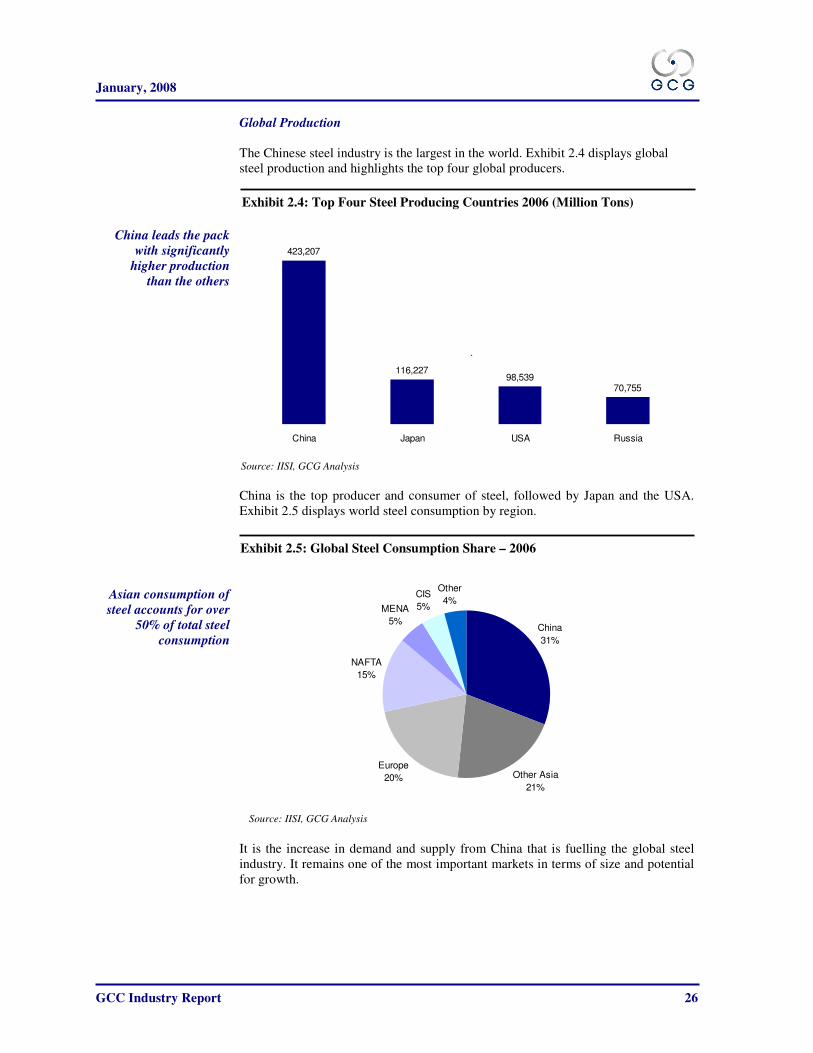

Global Production

The Chinese steel industry is the largest in the world. Exhibit 2.4 displays global

steel production and highlights the top four global producers.

423,207

116,22798,539

70,755

China Japan USA Russia

`

China is the top producer and consumer of steel, followed by Japan and the USA.

Exhibit 2.5 displays world steel consumption by region.

China

31%

Other Asia

21%

Europe

20%

NAFTA

15%

MENA

5%

CIS

5%

Other

4%

It is the increase in demand and supply from China that is fuelling the global steel

industry. It remains one of the most important markets in terms of size and potential

for growth.

Exhibit 2.5: Global Steel Consumption Share – 2006

Source: IISI, GCG Analysis

Exhibit 2.4: Top Four Steel Producing Countries 2006 (Million Tons)

Source: IISI, GCG Analysis

China leads the pack

with significantly

higher production

than the others

Asian consumption of

steel accounts for over

50% of total steel

consumption

January, 2008

GCC Industry Report 27

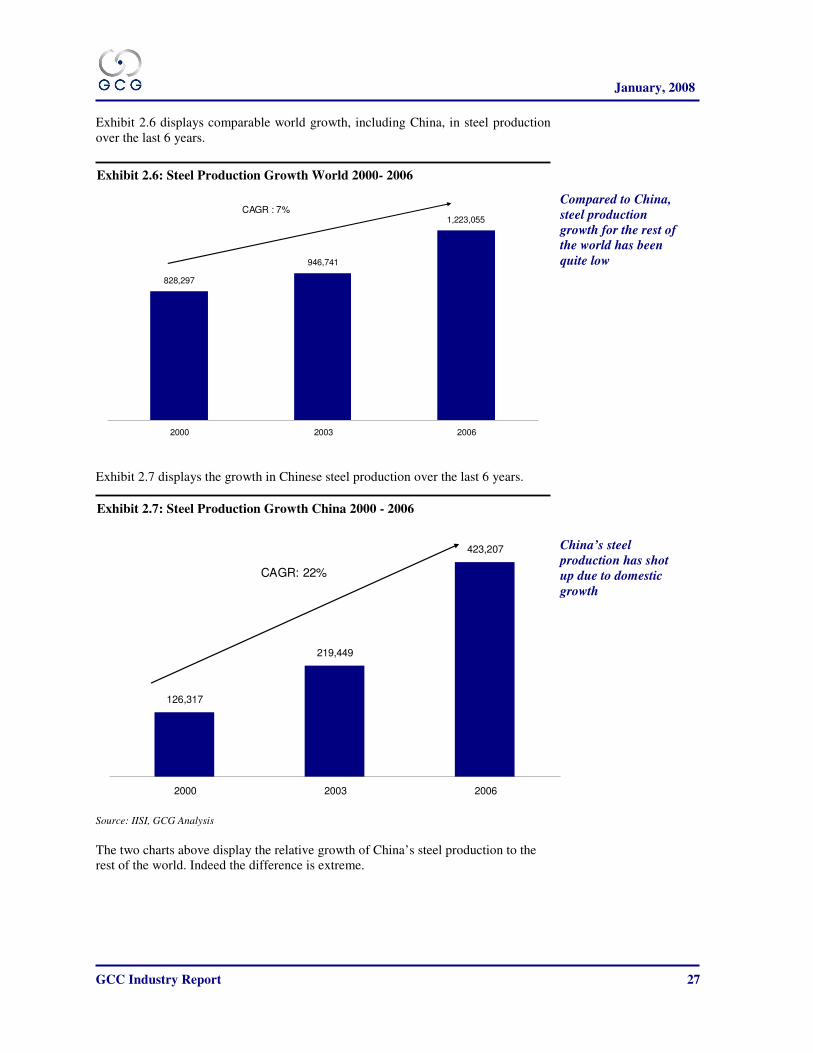

Exhibit 2.6 displays comparable world growth, including China, in steel production

over the last 6 years.

828,297

946,741

1,223,055

2000 2003 2006

CAGR : 7%

Exhibit 2.7 displays the growth in Chinese steel production over the last 6 years.

The two charts above display the relative growth of China’s steel production to the

rest of the world. Indeed the difference is extreme.

Exhibit 2.7: Steel Production Growth China 2000 - 2006

Source: IISI, GCG Analysis

Source: IISI, GCG Analysis

Exhibit 2.6: Steel Production Growth World 2000- 2006

126,317

219,449

423,207

2000 2003 2006

CAGR: 22%

China’s steel

production has shot

up due to domestic

growth

Compared to China,

steel production

growth for the rest of

the world has been

quite low

January, 2008

GCC Industry Report 28

Steel in the GCC

The steel industry is well developed in the GCC and is much more fragmented than,

for example, the aluminum industry, with many players taking a chunk of the overall

production pie. As we will see, all the GCC states have invested in local steel

industries. Considering the current economic boom, infrastructure projects and

construction activity are the main drivers of the demand for manufacturing in the

GCC and steel is the construction material of choice. GCC member states consume

378 kg of steel per person. The corresponding rate at the world level is only 182 kg.18

Currently, demand outstrips supply in the GCC and steel prices have already risen by

25% this year.

Exhibit 2.8 displays the steel imports of GCC countries over three years. It is clear

from the graph that steel imports have gone up and local production is not meeting

demand.

0

1

2

3

4

5

6

UAE KSA Kuwait Qatar Oman Bahrain

2003 2004 2005

Some strategic advantages that GCC states have relative to the rest of the world are:

1) Comparative Advantage – Energy and Natural Gas: Similar to aluminum

smelting, steel processing is an energy intensive process and readily

available low-cost energy resources are plentiful in the GCC. Due to the

availability of natural gas, GCC states can produce steel via the direct

reduction (DRI) process which does not require a heavy capital investment.

2) Labor Advantage – Due to the availability of low-cost labor construction is

literally out of control in the GCC. Steel is extensively used in the

18

Gulf Organization for Industrial Consulting (GOIC), Gulf Industrial Bulletin, Volume

6, Issue 73, August 2006

Exhibit 2.8: GCC Steel Imports (Million tons)

Source: ISSB, GCG Analysis

Steel imports for all

GCC states, except

Kuwait, have been

rising, with the UAE

importing the highest

quantities

January, 2008

GCC Industry Report 29

construction industry and given that a large number of projects are currently

taking place, the demand for steel is definitely here to stay.

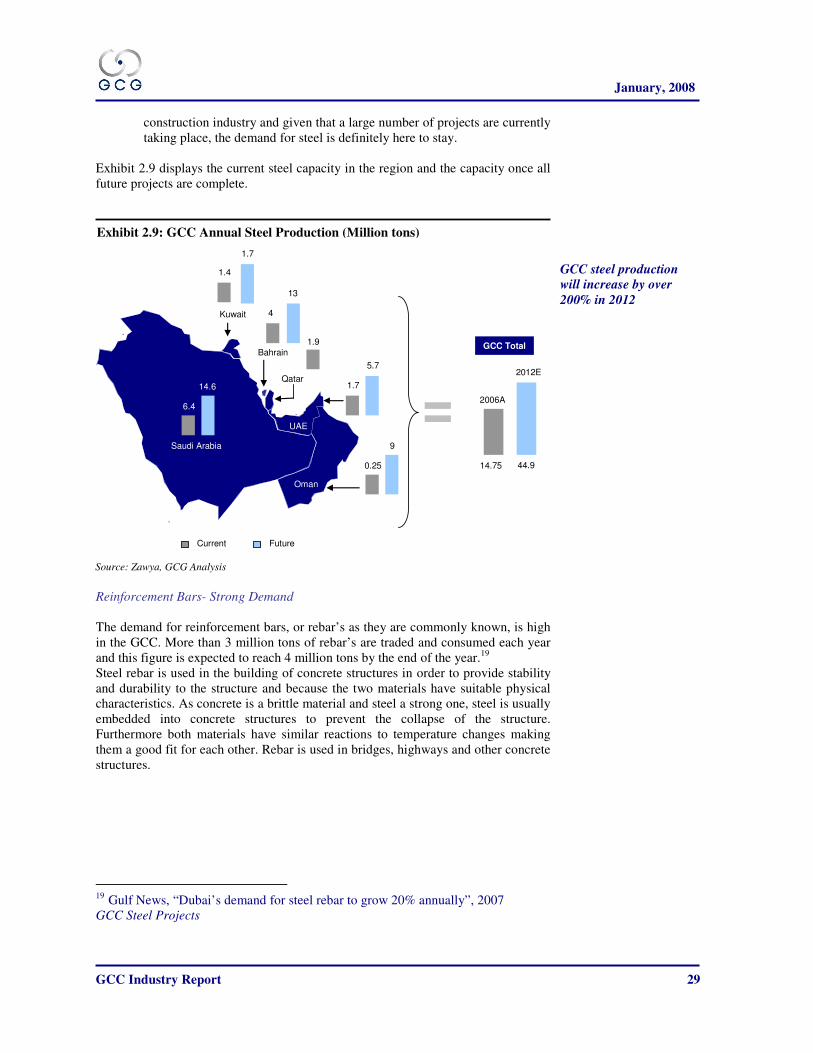

Exhibit 2.9 displays the current steel capacity in the region and the capacity once all

future projects are complete.

Reinforcement Bars- Strong Demand

The demand for reinforcement bars, or rebar’s as they are commonly known, is high

in the GCC. More than 3 million tons of rebar’s are traded and consumed each year

and this figure is expected to reach 4 million tons by the end of the year.19

Steel rebar is used in the building of concrete structures in order to provide stability

and durability to the structure and because the two materials have suitable physical

characteristics. As concrete is a brittle material and steel a strong one, steel is usually

embedded into concrete structures to prevent the collapse of the structure.

Furthermore both materials have similar reactions to temperature changes making

them a good fit for each other. Rebar is used in bridges, highways and other concrete

structures.

19 Gulf News, “Dubai’s demand for steel rebar to grow 20% annually”, 2007

GCC Steel Projects

Exhibit 2.9: GCC Annual Steel Production (Million tons)

Source: Zawya, GCG Analysis

GCC steel production

will increase by over

200% in 2012

14.75

2006A

44.9

2012E

UAE

Oman

Saudi Arabia

Bahrain

Qatar

1.9

1.7

5.7

4

0.25

9

6.4

14.6

GCC Total

Current Future

13

1.4

Kuwait

1.7

January, 2008

GCC Industry Report 30

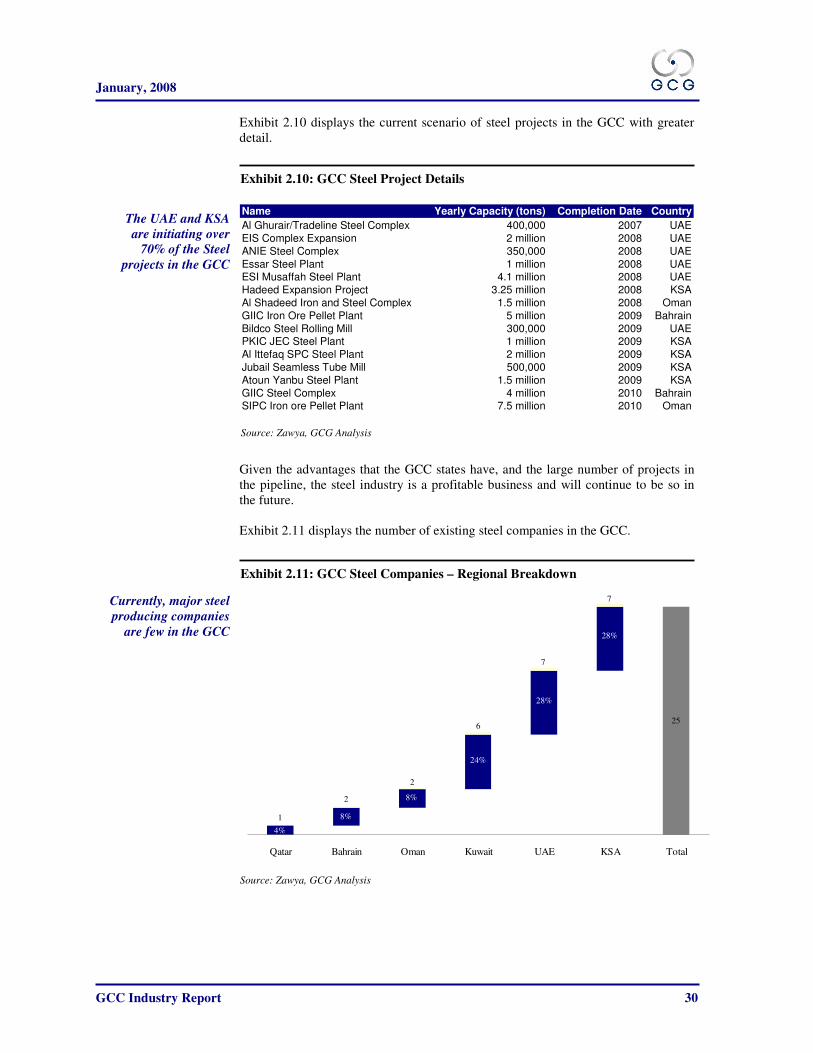

Exhibit 2.10 displays the current scenario of steel projects in the GCC with greater

detail.

Name Yearly Capacity (tons) Completion Date Country

Al Ghurair/Tradeline Steel Complex 400,000 2007 UAE

EIS Complex Expansion 2 million 2008 UAE

ANIE Steel Complex 350,000 2008 UAE

Essar Steel Plant 1 million 2008 UAEESI Musaffah Steel Plant 4.1 million 2008 UAE

Hadeed Expansion Project 3.25 million 2008 KSA

Al Shadeed Iron and Steel Complex 1.5 million 2008 Oman

GIIC Iron Ore Pellet Plant 5 million 2009 Bahrain

Bildco Steel Rolling Mill 300,000 2009 UAEPKIC JEC Steel Plant 1 million 2009 KSA

Al Ittefaq SPC Steel Plant 2 million 2009 KSA

Jubail Seamless Tube Mill 500,000 2009 KSA

Atoun Yanbu Steel Plant 1.5 million 2009 KSA

GIIC Steel Complex 4 million 2010 BahrainSIPC Iron ore Pellet Plant 7.5 million 2010 Oman

Given the advantages that the GCC states have, and the large number of projects in

the pipeline, the steel industry is a profitable business and will continue to be so in

the future.

Exhibit 2.11 displays the number of existing steel companies in the GCC.

25

1

2

2

6

7

7

4%

8%

8%

24%

28%

28%

Qatar Bahrain Oman Kuwait UAE KSA Total

Exhibit 2.10: GCC Steel Project Details

Source: Zawya, GCG Analysis

The UAE and KSA

are initiating over

70% of the Steel

projects in the GCC

Exhibit 2.11: GCC Steel Companies – Regional Breakdown

Currently, major steel

producing companies

are few in the GCC

Source: Zawya, GCG Analysis

January, 2008

GCC Industry Report 31

United Arab Emirates

Overview

In 2005, the UAE was the fourth largest net importer of steel in the world after the

United States, Thailand and Iran, importing 5.4 million metric tons of steel.20

There

are a multitude of infrastructure projects developing in UAE. The construction of the

tallest building in the world, various residential complexes and the Dubai Metro are

all examples of major projects that involve the use of steel on a massive scale. The

steel demand is expected to grow from over 5 million tons currently to 10 million

tons by 2010.21

Current Infrastructure

The UAE has 4 major steel companies and a number of smaller ones. Exhibit 2.12

displays the current and future capacity of steel in the UAE.

20

International Iron and Steel Institute, Major Importers and Exporters of Steel, 2005 21 Gulf News, “Demand for steel in UAE set to double in three years”, December

2007

Exhibit 2.12: UAE Steel Production (Million tons)

Source: Company Websites, Zawya, GCG Analysis

UAE Steel production

will increase by 235%

in 2009

2006A 2009E

1.7

5.7

Current Future

January, 2008

GCC Industry Report 32

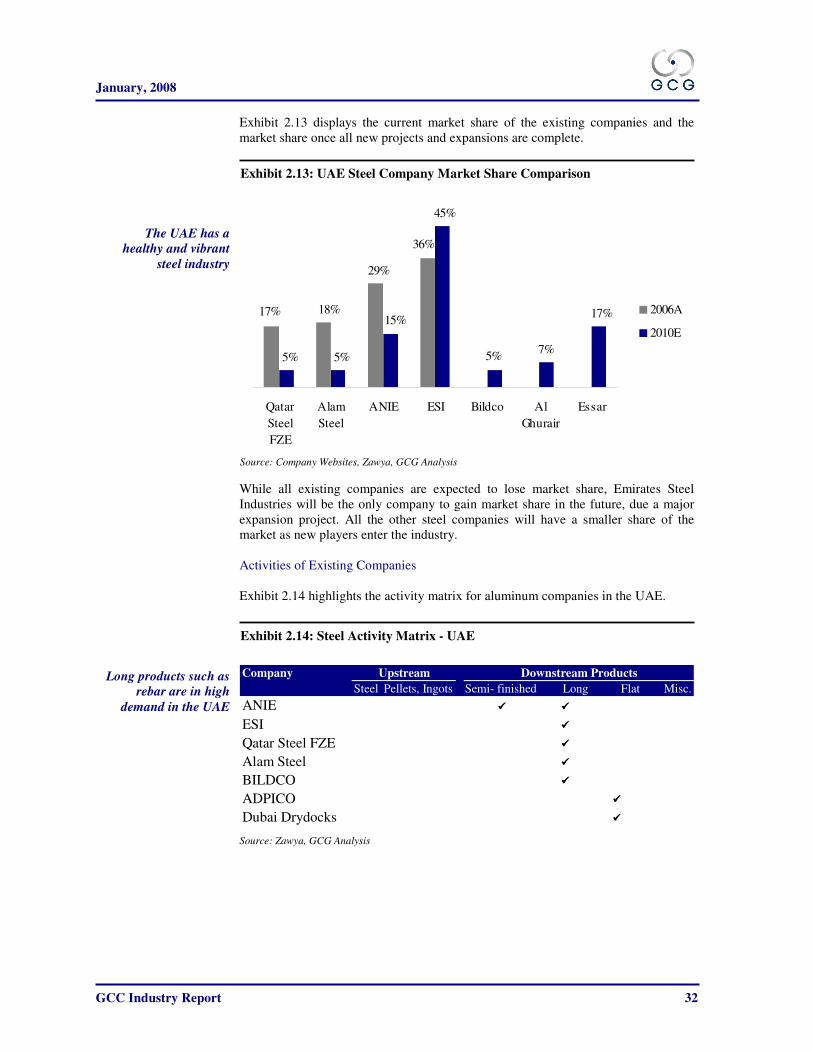

Exhibit 2.13 displays the current market share of the existing companies and the

market share once all new projects and expansions are complete.

7%

36%

29%

18%17% 17%

5%5% 5%

15%

45%

Qatar

Steel

FZE

Alam

Steel

ANIE ESI Bildco Al

Ghurair

Essar

2006A

2010E

While all existing companies are expected to lose market share, Emirates Steel

Industries will be the only company to gain market share in the future, due a major

expansion project. All the other steel companies will have a smaller share of the

market as new players enter the industry.

Activities of Existing Companies

Exhibit 2.14 highlights the activity matrix for aluminum companies in the UAE.

Company

Steel Pellets, Ingots Semi- finished Long Flat Misc.

ANIE ���� ����

ESI ����

Qatar Steel FZE ����

Alam Steel ����

BILDCO ����

ADPICO ����

Dubai Drydocks ����

Upstream Downstream Products

Exhibit 2.13: UAE Steel Company Market Share Comparison

Exhibit 2.14: Steel Activity Matrix - UAE

Source: Zawya, GCG Analysis

The UAE has a

healthy and vibrant

steel industry

Long products such as

rebar are in high

demand in the UAE

Source: Company Websites, Zawya, GCG Analysis

January, 2008

GCC Industry Report 33

Major Up and Coming Projects22

1. Emirates Integrated Steel (EIS) Complex Expansion

The project is owned by the General Holding Corporation under the name of

Emirates Iron Industries Company (EIIC) and will be an addition to the Emirates

Steel Industries’ current productions. A capacity of 2 million tpy of wire rod and

rebar will be reached via the addition of 2 new rolling mills, a direct reduction plant

and a steel melt shop.

2. ANIE Musaffah Steel Complex

ANIE is planning the construction of a Direct Reduction Iron (DRI) sponge iron

plant with a capacity of 250,000 tpy and a steel billet manufacturing facility with a

capacity of 350,000 tpy. The cost of the project is USD 300 million and it is

expected to be complete by 2008.

22

Zawya, Company Websites

January, 2008

GCC Industry Report 34

Bahrain

Overview

The Bahrain steel industry is in its developing stage. There is one main company that

is heading all future projects.

Current Infrastructure

Exhibit 2.15 displays the current and future capacity of steel in Bahrain.

The Gulf Industrial Investment Company (GIIC) is the only company that produces

steel and is the only company planning projects in the market. Hence all steel

production market shares will belong to GIIC.

Activities of Existing Companies

Exhibit 2.16 highlights the activity matrix for aluminum companies in Bahrain.

Company

Steel Pellets, Ingots Semi- finished Long Flat Misc.

BRC Weldmesh ����

GIIC ����

Upstream Downstream Products

Exhibit 2.15: Bahrain Steel Production (Million tons)

Source: Company Websites, Zawya, GCG Analysis

Exhibit 2.16: Steel Activity Matrix - Bahrain

Source: Zawya, GCG Analysis

Steel production in

Bahrain will increase

by 225% in 2010

Bahrain has a limited

number of steel

companies

13

2006A

4Current

Future

2010A

January, 2008

GCC Industry Report 35

Major Up and Coming Projects23

GIIC Projects

The GIIC Iron Ore Pellet Plant and Steel Complex are the second and third largest

projects by capacity in the GCC, respectively. The former facility will increase iron

ore pellet production capacity to 11 million and is expected to be completed by late

2009. The latter facility will include a Direct Reduction Iron (DRI) plant with a

capacity of 1.6 million tpy, a steel melt shop with a capacity of 1.2 million tpy and a

rolling mill with a capacity of 1.1 million tpy. The expected year of completion is

2010 and the total cost of the two projects is over USD 925 million.

23

Zawya, Company Websites

January, 2008

GCC Industry Report 36

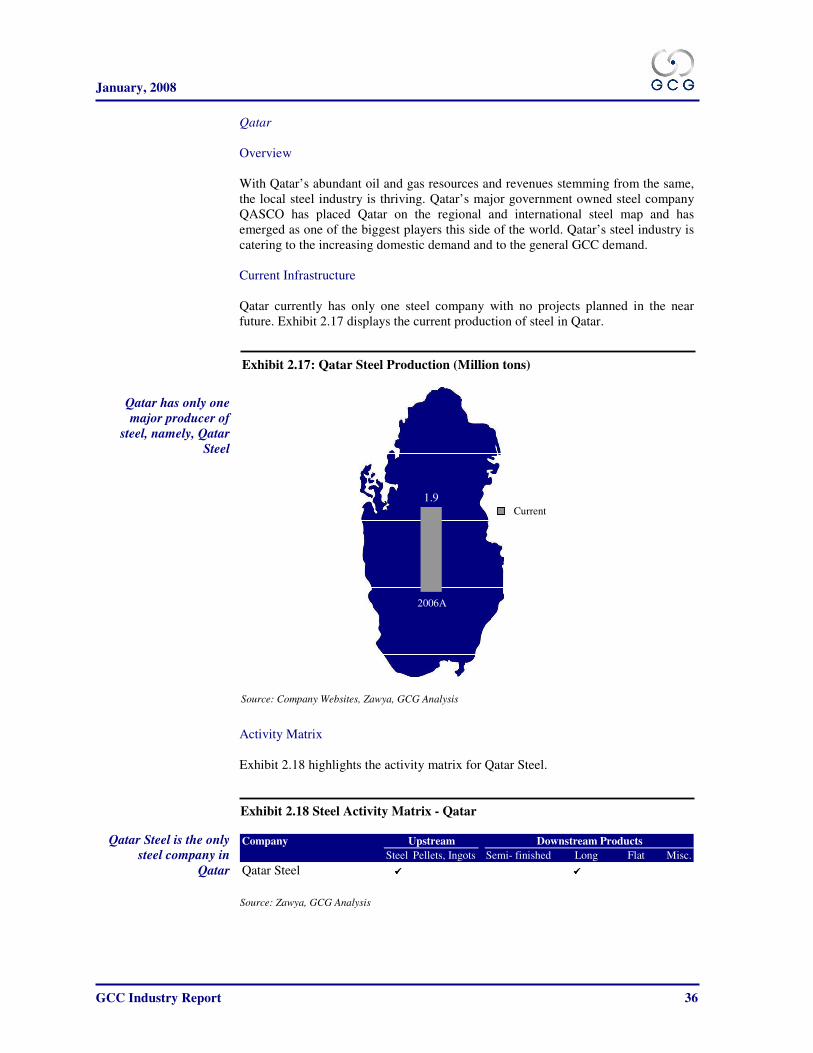

Qatar

Overview

With Qatar’s abundant oil and gas resources and revenues stemming from the same,

the local steel industry is thriving. Qatar’s major government owned steel company

QASCO has placed Qatar on the regional and international steel map and has

emerged as one of the biggest players this side of the world. Qatar’s steel industry is

catering to the increasing domestic demand and to the general GCC demand.

Current Infrastructure

Qatar currently has only one steel company with no projects planned in the near

future. Exhibit 2.17 displays the current production of steel in Qatar.

Activity Matrix

Exhibit 2.18 highlights the activity matrix for Qatar Steel.

Company

Steel Pellets, Ingots Semi- finished Long Flat Misc.

Qatar Steel ���� ����

Upstream Downstream Products

Exhibit 2.17: Qatar Steel Production (Million tons)

Source: Company Websites, Zawya, GCG Analysis

Qatar has only one

major producer of

steel, namely, Qatar

Steel

2006A

1.9Current

Exhibit 2.18 Steel Activity Matrix - Qatar

Source: Zawya, GCG Analysis

Qatar Steel is the only

steel company in

Qatar

January, 2008

GCC Industry Report 37

Oman

Overview

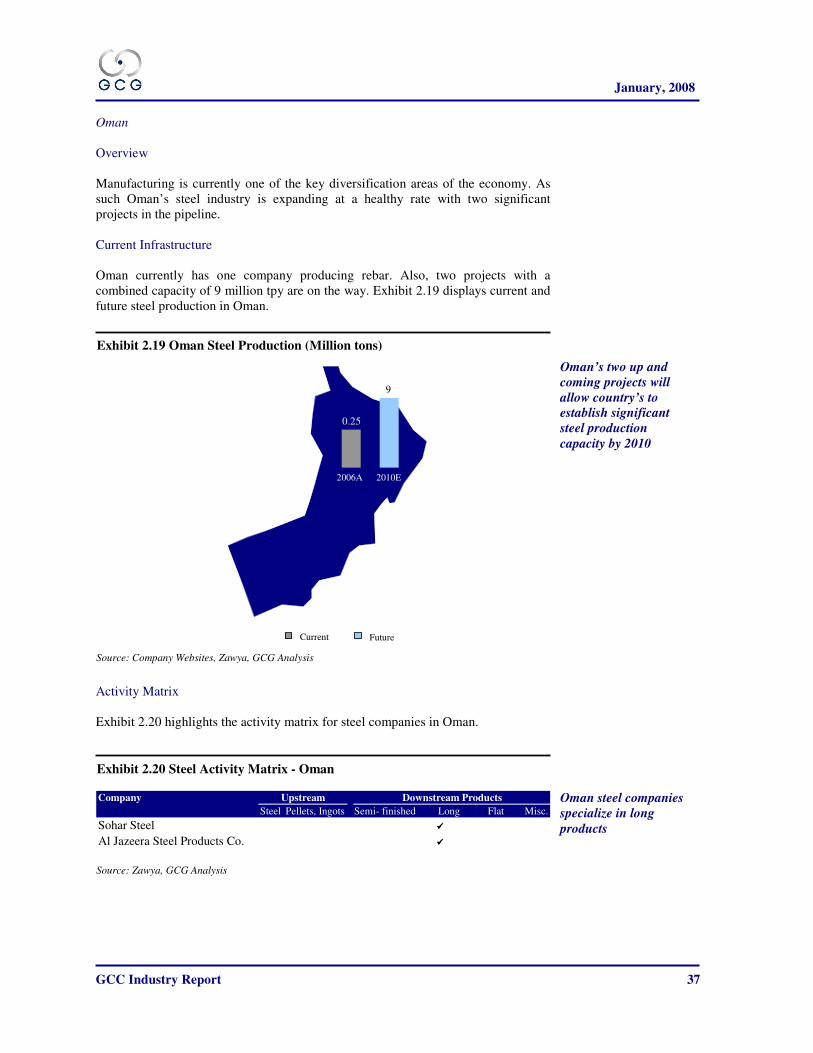

Manufacturing is currently one of the key diversification areas of the economy. As

such Oman’s steel industry is expanding at a healthy rate with two significant

projects in the pipeline.

Current Infrastructure

Oman currently has one company producing rebar. Also, two projects with a

combined capacity of 9 million tpy are on the way. Exhibit 2.19 displays current and

future steel production in Oman.

Activity Matrix

Exhibit 2.20 highlights the activity matrix for steel companies in Oman.

Company

Steel Pellets, Ingots Semi- finished Long Flat Misc.

Sohar Steel ����

Al Jazeera Steel Products Co. ����

Upstream Downstream Products

Exhibit 2.19 Oman Steel Production (Million tons)

Source: Company Websites, Zawya, GCG Analysis

Oman’s two up and

coming projects will

allow country’s to

establish significant

steel production

capacity by 2010

0.25

9

Current Future

2010E2006A

Exhibit 2.20 Steel Activity Matrix - Oman

Source: Zawya, GCG Analysis

Oman steel companies

specialize in long

products

January, 2008

GCC Industry Report 38

Major Up and Coming Projects24

1. Sohar Industrial Port Company (SIPC) Iron ore Pellet Plant

The SIPC steel project is the largest both by contract value and by capacity size and

will be located in the Sohar Industrial City. An iron ore palletizing plant with a

capacity of 7.5 million tpy will be built. Companhia Vale do Rio Doce (CVRD), the

world’s second largest mining company and the world leader in iron ore and pellets

production and commercialization conducted the feasibility study for this project and

will provide all the iron ore for the plants operations. SIPC is a 50:50 partnership

between the Government of Oman and the Rotterdam Municipal Port Management

of Netherlands.

2. Shadeed Iron and Steel Complex

The project will consist of a 1 million tpy steel melt shop and a 500,000 tpy Direct

Reduction Iron (DRI) plant. The Shadeed Iron & Steel Limited company, a part of

Al Ghaith Holding was established in 2006. The USD 870 million steel project is

still in the process of being set up and will begin primary metal production in 2008.

Annual production will be 1.1 million tpy of steel billets and 400,000 tpy of hot

briquette iron (HBI) which is a feed material in steelmaking. The complex will be

located in the Sohar Industrial City.

24

Zawya, Company Websites

January, 2008

GCC Industry Report 39

Kuwait

Overview

Kuwait has a number of steel products companies but primary production facilities

have not yet been established in the State.

Current Infrastructure

Kuwait has around ten companies supplying steel products in Kuwait but no

upstream producers of steel.25

Exhibit 2.21 displays the current production of downstream steel products in Kuwait.

Exhibit 2.22 displays the current market share of the existing companies.

25

Zawya, GCG Analysis

Exhibit 2.21: Kuwait Steel Production (Million tons)

Source: Company Websites, Zawya, GCG Analysis

Kuwait steel

production will

increase by over 20%

in 2008

1.66

2006A

1.4

Current

Future

2008E

January, 2008

GCC Industry Report 40

120

150

500

600

1370

11%

36%

44%

9%

KPIOS Kuwait Reinf. Steel Al Oula United Steel Total

Activities of Existing Companies

Exhibit 2.23 highlights the activity matrix for steel companies in Kuwait.

Company

Steel Pellets, Ingots Semi- finished Long Flat Misc.

United Steel ����

Al Oula ����

Kuwait Reinforced Steel ����

KPIOS ����

Qudaibi Steel ����

Hayakel ���� ����

Upstream Downstream Products

Exhibit 2.23: Steel Activity Matrix – Kuwait

Source: Company Websites, Zawya, GCG Analysis

Exhibit 2.22: Kuwait Steel Company Market Share Comparison

Source: Company Websites, Zawya, GCG Analysis

United Steel is the

only manufacturer of

reinforcement bars in

Kuwait

In relation to other

industries Kuwait has

a fairly competitive

steel industry

January, 2008

GCC Industry Report 41

Saudi Arabia

Overview

In 2005, Saudi Arabia was the twelfth largest net importer of steel in the world.26

The Kingdom has the most players in the steel industry compared to the other GCC

states and thus contributes significantly to domestic requirements. In the Kingdom,

iron and steel factories are entitled to benefit from the Public Investment Fund which

finances projects from these industries and further helps growth of the steel industry.

Current Infrastructure

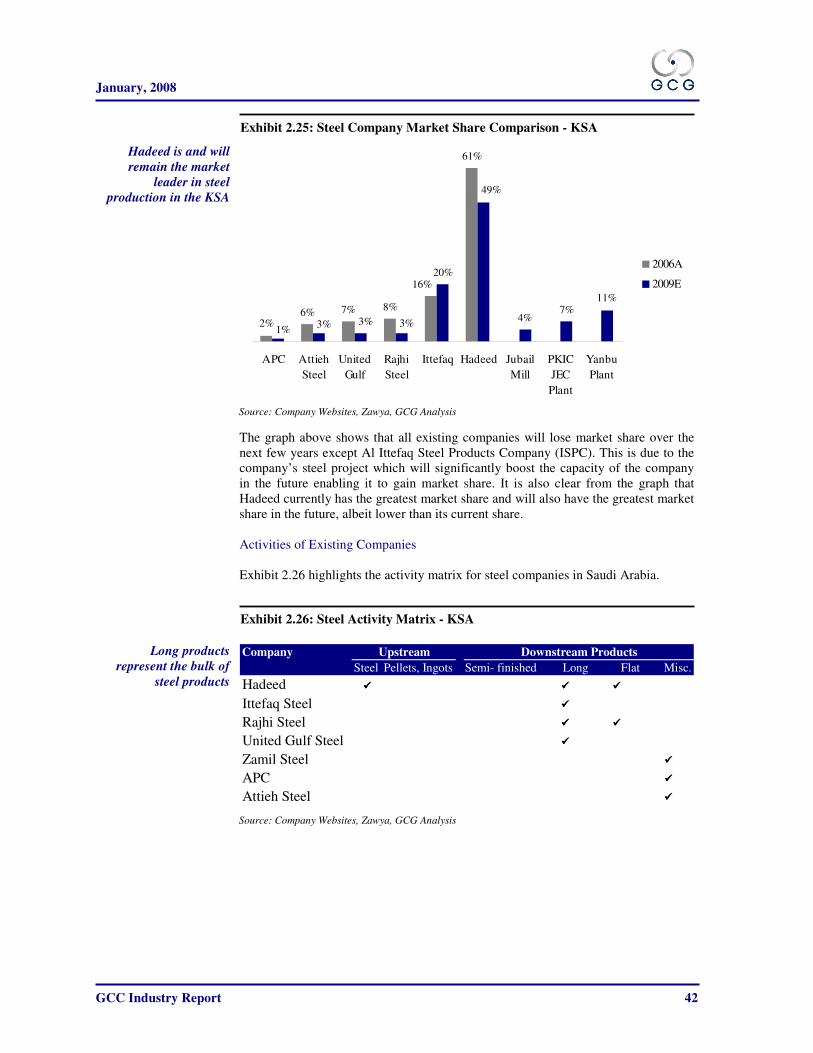

Saudi Arabia has seven major steel companies specializing in a variety of products.

Exhibit 2.24 displays the current and future production of steel in the Kingdom.

Exhibit 2.25 displays the current market share of the existing companies and the

market share once all new projects and expansions are complete.

26

International Iron and Steel Institute, Major Importers and Exporters of Steel, 2005

Exhibit 2.24: Saudi Arabia Steel Production (Million tons)

Source: Company Websites, Zawya, GCG Analysis

Steel production in

the KSA will increase

by almost 130% in

2009

6.4

14.6

2006A 2009E

Current Future

January, 2008

GCC Industry Report 42

11%

61%

16%

8%7%6%2%

7%4%

49%

20%

3%3%3%1%

APC Attieh

Steel

United

Gulf

Rajhi

Steel

Ittefaq Hadeed Jubail

Mill

PKIC

JEC

Plant

Yanbu

Plant

2006A

2009E

The graph above shows that all existing companies will lose market share over the

next few years except Al Ittefaq Steel Products Company (ISPC). This is due to the

company’s steel project which will significantly boost the capacity of the company

in the future enabling it to gain market share. It is also clear from the graph that

Hadeed currently has the greatest market share and will also have the greatest market

share in the future, albeit lower than its current share.

Activities of Existing Companies

Exhibit 2.26 highlights the activity matrix for steel companies in Saudi Arabia.

Company

Steel Pellets, Ingots Semi- finished Long Flat Misc.

Hadeed ���� ���� ����

Ittefaq Steel ����

Rajhi Steel ���� ����

United Gulf Steel ����

Zamil Steel ����

APC ����

Attieh Steel ����

Upstream Downstream Products

Exhibit 2.25: Steel Company Market Share Comparison - KSA

Source: Company Websites, Zawya, GCG Analysis

Exhibit 2.26: Steel Activity Matrix - KSA

Source: Company Websites, Zawya, GCG Analysis

Hadeed is and will

remain the market

leader in steel

production in the KSA

Long products

represent the bulk of

steel products

January, 2008

GCC Industry Report 43

Major Up and Coming Projects27

1. Al Ittefaq Steel Products Company – Dammam Steel Plant

ISPC-Dammam is planning to build a flat steel products plant in the Dammam

Second Industrial City. The plant costs USD 400 million and will have a capacity of

2 million tpy. The plant is expected to be completed by late 2009.

2. Hadeed Expansion Project

Hadeed is building a 1.75 million tpy DRI plant and increasing its flat products

capacity to 2 million and its long products capacity to 3 million. Total capacity

inreaase will be 3.25 and actual increase in steel production will be 1.22 million tpy.

The cost of the expansion is USD 383 million and is to be completed by early 2008.

27

Zawya, Company Websites

January, 2008

GCC Industry Report 44

CEMENT

Cement, a super-fine gray or white powder, is comprised of four elements – calcium,

silicon, aluminum and iron. Portland cement is the most common type of cement and

was invented by Joseph Aspdin in 1824. It is named after the Isle of Portland, where

the limestone used in its production was quarried. Raw materials involved in the

production of cement can be all or any of the following - limestone, marl, shale, iron

ore, clay, and fly ash. However, the most common ingredients are limestone, clay

and sand. The raw materials are crushed and proportioned in order to produce

cement with specific properties before the production process begins.

Cement production is an energy intensive process with fuel representing 35% of

variable costs.28

A lot of heat is required in the production of cement as temperatures

go as high as 3400 F (one-third of the sun’s surface temperature) in the kiln. The kiln

is the largest moving piece of industrial equipment and the main piece of equipment

used in the production of cement. It is in the kiln that clinker is formed. When raw

materials are heated to extremely high temperatures a chemical reaction takes place

causing the calcium and silicon oxides to fuse into calcium silicates – cement’s key

component. The resulting mass is known as clinker and is gray in color. Once clinker

is cooled, combined with gypsum and made into a powder form it can be called

cement.29

Cement Facts

Clinker is powdered to make cement. The types of cement produced are used to

make concrete with specific properties. The word cement literally means a substance

to make objects adhere to each other. Portland cement is one type of cement; others

include blended and expansive cements. All kinds of cement are hydraulic cements

which means that they harden when mixed with water. Cement is the primary

constituent of concrete. Concrete is a rock-like mass which has a variety of

construction applications - highways, streets, parking lots, parking garages, bridges,

high-rise buildings, dams, homes, floors, sidewalks, driveways, and numerous other

applications.

Exhibit 3.2 displays the physical make-up of concrete.

28

British Cement Association (BCA) 29

Portland Cement Association (PCA)

Exhibit 3.1: The Four Components of Cement

Source: Portland Cement Association, GCG Analysis

20

CaSilvery White

Alkaline Earth Metal

14

SiBlue Grey

Semi Metallic

Element

13

AlSilvery White

Metal

26

FeGrey Metallic Element

Cement plants are

usually located near

limestone quarries

where raw materials

are abundant

January, 2008

GCC Industry Report 45

Aggregate

67%

Water

16%

Cement

11%

Air

6%

Concrete is formed when paste (cement and water) and aggregate (sand and gravel)

are combined. The water content controls many of the characteristics of the resulting

concrete and low water content results in high quality concrete. The most common

type of concrete usage is ready-mixed concrete.

Exhibit 3.3 displays the value chain of cement.

Exhibit 3.2: The Four Components of Concrete

Exhibit 3.3: Cement Products Value Chain

Source: Industry Websites, GCG Analysis

Source: PCA, GCG Analysis

Aggregate containing

sand and gravel forms

the largest component

of concrete

Ready-mix concrete is

handled in trucks with

revolving drums

Cement

Concrete

Precast Ready-mix Masonry

Clinker

January, 2008

GCC Industry Report 46

Global Cement Production

China and India are the world leaders in cement production. Exhibit 3.4 displays

cement production on a global level.

1100

155101

68

China India US Japan

The above graph depicts that China has over 40% share of the world’s cement

production. China is also the world’s top consumer of cement. Chinese cement

consumption accounts for more than 46% of world consumption and 75% of

expected growth in world cement consumption during 2007. According to the report

emerging and developing countries such as those of the GCC are generating the rest

of the global growth.30

30

Portland Cement Association, The Monitor, Flash Report, March 2007

Exhibit 3.4: World Cement Production 2006 in Thousand Metric tons

Source: USGS Mineral Commodity Summaries, GCG Analysis

China is the world

leader in cement

production

January, 2008

GCC Industry Report 47

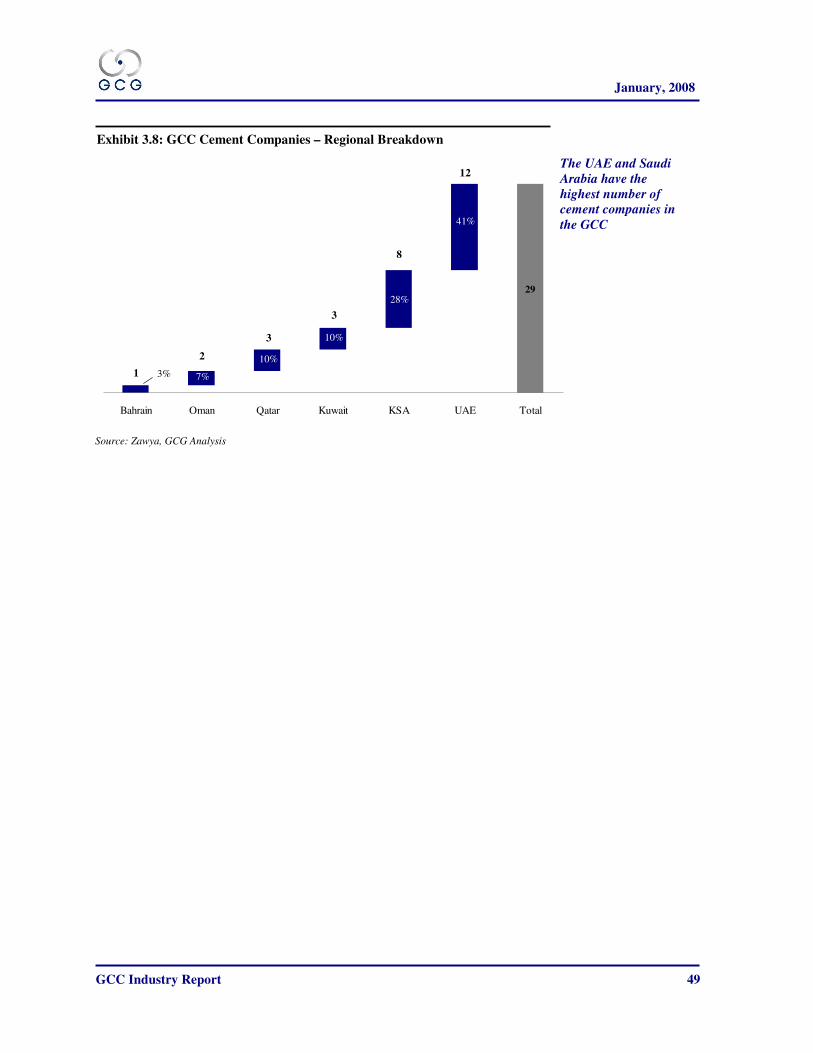

Cement in the GCC

The construction sector and the cement industry go hand in hand. Construction

activity in all the GCC states is rampant and demand for cement has shot through the

roof in the recent years as have cement prices. The Kingdom of Saudi Arabia and the

UAE are leading the way for the GCC cement industry. Prices have been rising over

the past few years because of the high demand as well as rising fuel and raw material

costs. Coal is being increasingly sought after as a fuel and raw material input.

Capacity expansions are happening region wide and questions of oversupply in the

near future are being addressed. Exhibit 3.5 shows the current and anticipated future

production of cement in the GCC.

GCC Cement Projects

Exhibit 3.6 displays the current scenario of cement projects in the GCC with greater

detail. Most of the capacity increases are arising from the United Arab Emirates and

Saudi Arabia. As mentioned earlier, this is primarily because of the scope of

construction activity and infrastructure developments happening in these regions.

Exhibit 3.5: GCC Annual Cement Production (Million tons)

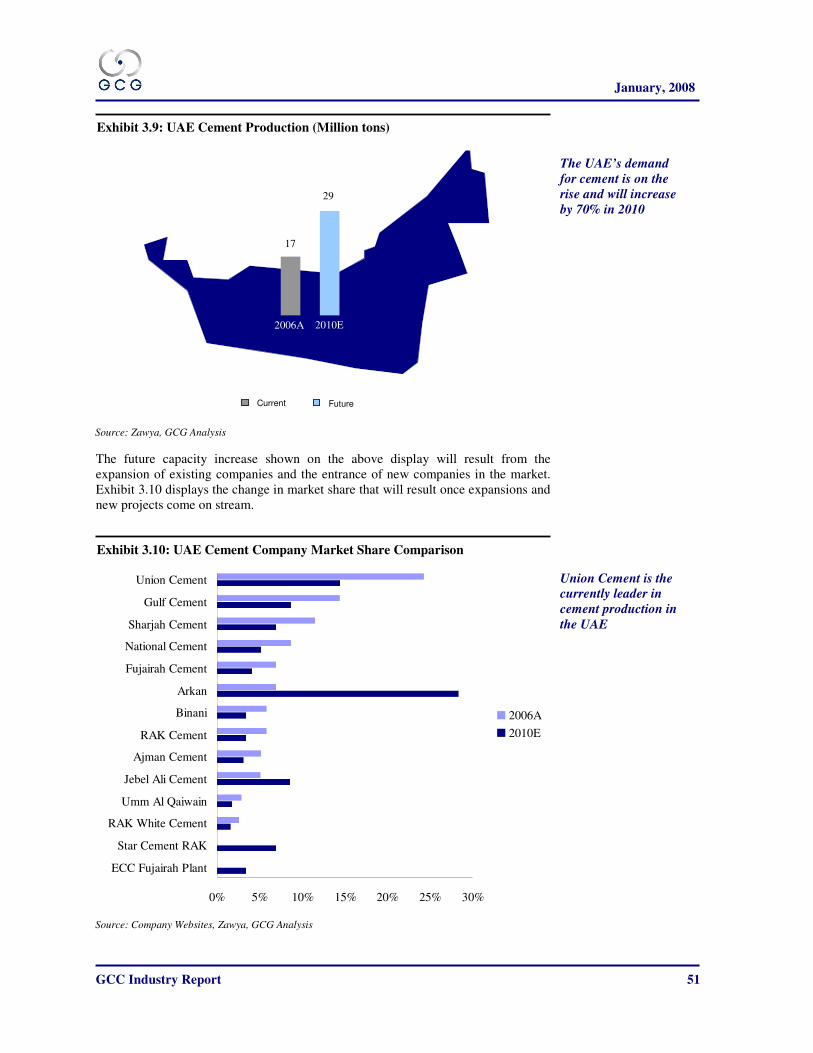

Source: Company Websites, Zawya, GCG Analysis

Annual cement

production in the

GCC will increase by

40% in 2012

2006A

2012E

UAE

Oman

Saudi Arabia

Bahrain

Qatar

7.5

17

29

0.5

3.5

5.75

27

42

GCC Total

Current Future

1.2

Kuwait

2.1

2.9

57.6 80.8

January, 2008

GCC Industry Report 48

11

1

5

5

9%

45%

45%

Bahrain UAE KSA Total

Exhibit 3.7 displays the projects with greater detail.

Name Yearly Capacity (tons) Completion Date Country

Emirates Cement Company Fujairah Plant 1.1 million 2007 UAE

Falcon Cement Plant 730,000 2008 Bahrain

Star Cement Ras Al Khaimah Plant 2 million 2008 UAE

Arkan Building Materials Fujairah Plant 3.1 million 2008 UAE

Najran Cement Plant 3.3 million 2008 KSA

NRC - Arar Cement Plant 2.2 million 2008 KSA

Al Watan Jalajil Cement Plant 3.3 million 2009 KSA

ACC Labuna Cement Plant 4 million 2009 KSA

Al Ahsa Cement Plant 1.8 million 2009 KSA