gaap accounting for esop sponsors...gaap accounting for esop sponsors brian j. sweeney, cpa redpath...

TRANSCRIPT

.

GAAP Accounting For ESOP Sponsors

Brian J. Sweeney, CPARedpat h and Company, Lt d.St . Paul, Minnesot a 651.407.5856bsweeney@redpat hcpas.com

Cindy J. Dwyer, CPAMayer Hof fman McCann P.C. Kansas Cit y, [email protected]

Jim Myot t , J.D., CPABoulayMinneapolis, Minnesot a952.893.3822jmyot t @boulaygroup.com

Present ed by:

.

• Understand the basic concepts of GAAP ESOP Accounting, especially for leveraged ESOPs

• Provide examples of financial statement impact and journal entries

• Dividends

• Other consideration/advanced issues

• Introduction to accounting for SARs and Warrants

What Do We Want To Accomplish Today?

1

.

For GAAP, the ESOP is treated as an agent of the plan sponsor with a dual purpose:

• Facilitate financing

• Provide an employee benefit

Consequence: Reporting approximates a treasury stock model as if the company redeemed the stock for debt and gradually makes awards to employees as that debt is retired.

Theory

2

.

Non-leveraged ESOP contributions are treated just like profit sharing or 401(k) plans. Cash contributions are expensed at value, share contributions are expensed at the fair value of the shares.

Basic GAAP ESOP Accounting Concepts: Non-leveraged Plans

3

Debit CreditCash $500,000 Contributions $500,000

To Record Cash Contribution

Common Stock/APIC $500,000 Contributions $500,000

To Record Stock Contribution

.

• ESOP loan definitions:

Direct loan – 3rd party lends directly to ESOP

Internal loan – Company lends directly to ESOP

Outside loan – 3rd party lends directly to Company

• Direct loans to the ESOP are reported as debt on company books and a contra equity account – even though the Company is not the borrower

• Internal loan receivable from the ESOP is reported in the equity section of the balance sheets as a contra-equity account, not as a receivable on company books

• Outside loan to the company is recorded as normal debt

Basic GAAP ESOP Accounting Concepts:ESOP Loans

4

.

• Unearned ESOP Shares is a contra-equity account (i.e., debit balance) that is created when the ESOP purchases leveraged shares.

• Very similar to compensating employees with treasury stock.

• CAUTION – Unearned ESOP Shares is NOT the same as the company’s note receivable from the ESOP. Those balances may coincide in the case of a principal-only share release, but will NOT coincide in the case of a principal-and-interest release.

• 718-40-30-3:

“Unearned employee stock ownership plan shares shall be credited as shares are committed to be released based on the cost of the shares to the employee stock ownership plan. Employers shall charge or credit the difference between the fair value of shares committed to be released and the cost of those shares to the employee stock ownership plan to shareholder’s equity in the same manner as gains and losses on sales of treasury stock (generally to additional paid-in capital).”

Basic GAAP ESOP Accounting Concepts:Unearned ESOP Shares

5

.

• Contributions to the ESOP are an element of compensation cost.

• Note – in previous line, cost (not expense) used. These costs are subject to capitalization just like other costs.

• Contributions not used to service ESOP debt are measured at value, similar to accounting for other retirement plans.

• Contributions used to pay interest on ESOP debt are charged to interest expense. In the case of an inside loan, the interest payment by the ESOP to the Company offsets that interest expense.

• Contributions used to pay principal are re-measured as the average fair value of the shares released from contributions, with the balancing adjustment to APIC or retained earnings.

Basic GAAP ESOP Accounting Concepts:Contributions

6

.

• Release and allocation of ESOP shares to participant occurs as the internal loan is paid.

• IRC regulations provide for 2 methods of share release – principal only and principal and interest:

• Principal only – Number of shares released each year is equal to principal paid for the year divided by current and future principal times number of unreleased shares.

• Principal only method is available only if loan amortization is always as much or more as 10-year equal amortization.

• Principal and interest – Number of shares released each year is equal to the principal and interest paid for the year divided by the current and future principal and interest times number of unreleased shares at beginning of the year.

• Share release is done as part of ESOP administration – should coordinate with company and outside ESOP administrator (if any) to make sure calculations are consistent between ESOP administration and financial statements.

Basic GAAP ESOP Accounting Concepts:Share Release

7

.Leveraged ESOP: Direct Loan

8

Company

ESOP Trust

Lender(bank or seller)

ESOP Debt - ConceptuallyUnearned ESOP Shares $7MM

Liability ($7MM)

.Leveraged ESOP: Internal Loan

9

ESOP Debt - ConceptuallyCash ($7MM)

Note Receivable $7MM Liability ($7MM)

Unearned ESOP Shares $7MM

ESOP Debt - ReportedCash ($7MM)

Unearned ESOP Shares $7MM

Company

ESOP Trust

Lender(bank or seller)

.Leveraged ESOP: Outside and Internal Loans

10

Step 1 - Corporate DebtCash $7MM

Liability ($7MM)

Step 2 - ESOP Debt - ConceptuallyCash ($7MM)

Note Receivable $7MM Liability ($7MM)

Unearned ESOP Shares $7MM

ESOP Debt - ReportedCash ($7MM)

Unearned ESOP Shares $7MM

Company

ESOP Trust

Lender(bank or seller)

Step 1

Step 2

.

• Direct loan $7,000,000• Annual contribution $500,000• 20 year amortization• Principal-and-interest method

Example – Annual ESOP Transactions: Direct Loan

• Original cost $70.00• Average FMV $40.00• 5,000 shares released• 100,000 ESOP-owned shares

11

Company

ESOP Trust

Lender(Bank or Seller)

Selling Shareholder

Debit CreditCash $500,000 Interest Expense $256,063 ESOP Compensation Cost $243,937

Compensation Cost $43,937 Unearned ESOP Shares $350,000 APIC/Retained Earnings $150,000 ESOP Debt (on Sponsors Books) $243,937

1. Unearned ESOP shares are reduced for 5,000 shares at $70 per share original cost or $350,000. 2. APIC is reduced by difference between cost and average FV per share ($70-40=$30 times 5,000

shares.)3. ESOP compensation cost is 5,000 shares times average FV of $40 or $200,000. ($243,937 cash

contributed, less $43,937 reduction.)

.

• Inside and outside loan $7,000,000• Annual contribution $500,000• Amortization – 20 year loan• Principal-and-interest method

Example – Annual ESOP Transactions: Outside and Indirect Loan

• Or ig inal cost $70• Average FMV $40• 5,000 shares re leased• 100,000 ESOP-owned shares

12

Debit CreditCash - to ESOP $500,000 Compensation Cost $243,937 Interest Expense $256,063

Cash - from ESOP $500,000 Unearned ESOP shares $243,937 Interest Expense $256,063

APIC/Retained Earnings $150,000 Compensation Cost $43,937 Unearned ESOP shares $106,063

Company

ESOP Trust

Lender(Bank or Seller)

Nominal Annual Rate: 3.668%

AMORTIZATION SCHEDULE - Normal AmortizationPrincipal Future Shares Suspense

Date Payment Interest Principal Balance Interest Released SharesLoan 1/1/2011 $ 7,000,000.00 $ 3,000,000.00 100,000

1 12/31/2011 $ 500,000.00 $ 256,063.04 $ 243,936.96 6,756,063.04 2,743,936.96 (5,000) 95,000 2 12/31/2012 500,000.00 247,818.68 252,181.32 6,503,881.72 2,496,118.28 (5,000) 90,000 3 12/31/2013 500,000.00 238,568.43 261,431.57 6,242,450.15 2,257,549.85 (5,000) 85,000 4 12/31/2014 500,000.00 228,978.88 271,021.12 5,971,429.03 2,028,570.97 (5,000) 80,000 5 12/31/2015 500,000.00 219,037.57 280,962.43 5,690,466.60 1,809,533.40 (5,000) 75,000 6 12/31/2016 500,000.00 208,731.61 291,268.39 5,399,198.21 1,600,801.79 (5,000) 70,000 7 12/31/2017 500,000.00 198,047.61 301,952.39 5,097,245.82 1,402,754.18 (5,000) 65,000 8 12/31/2018 500,000.00 186,971.72 313,028.28 4,784,217.54 1,215,782.46 (5,000) 60,000 9 12/31/2019 500,000.00 175,489.55 324,510.45 4,459,707.09 1,040,292.91 (5,000) 55,000

10 12/31/2020 500,000.00 163,586.20 336,413.80 4,123,293.29 876,706.71 (5,000) 50,000 11 12/31/2021 500,000.00 151,246.23 348,753.77 3,774,539.52 725,460.48 (5,000) 45,000 12 12/31/2022 500,000.00 138,453.62 361,546.38 3,412,993.14 587,006.86 (5,000) 40,000 13 12/31/2023 500,000.00 125,191.76 374,808.24 3,038,184.90 461,815.10 (5,000) 35,000 14 12/31/2024 500,000.00 111,443.45 388,556.55 2,649,628.35 350,371.65 (5,000) 30,000 15 12/31/2025 500,000.00 97,190.83 402,809.17 2,246,819.18 253,180.82 (5,000) 25,000 16 12/31/2026 500,000.00 82,415.42 417,584.58 1,829,234.60 170,765.40 (5,000) 20,000 17 12/31/2027 500,000.00 67,098.03 432,901.97 1,396,332.63 103,667.37 (5,000) 15,000 18 12/31/2028 500,000.00 51,218.78 448,781.22 947,551.41 52,448.59 (5,000) 10,000 19 12/31/2029 500,000.00 34,757.07 465,242.93 482,308.48 17,691.52 (5,000) 5,000 20 12/31/2030 500,000.00 17,691.52 482,308.48 - (0.00) (5,000) -

Grand Totals $ 10,000,000.00 $ 3,000,000.00 $ 7,000,000.00

Amortization Schedule for Reference

13

.

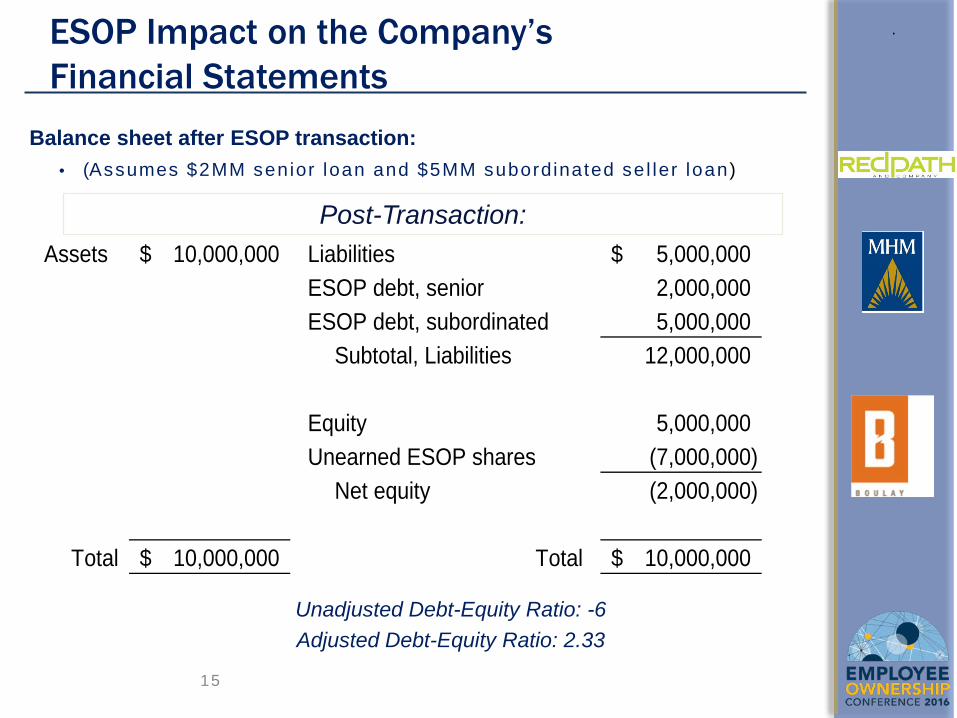

Assets 10,000,000$ Liabilities 5,000,000$

Equity 5,000,000$

Total 10,000,000$ Total 10,000,000$

Pre-Transaction:

Debt-Equity Ratio: 1

ESOP IMPACT ON THE COMPANY’S FINANCIAL STATEMENTS

ESOP Impact on the Company’s Financial Statements

14

.

Assets 10,000,000$ Liabilities 5,000,000$ ESOP debt, senior 2,000,000 ESOP debt, subordinated 5,000,000

Subtotal, Liabilities 12,000,000

Equity 5,000,000 Unearned ESOP shares (7,000,000)

Net equity (2,000,000)

Total 10,000,000$ Total 10,000,000$

Balance sheet after ESOP transaction:• (Assumes $2MM senior loan and $5MM subordinated se l ler loan)

Post-Transaction:

Unadjusted Debt-Equity Ratio: -6Adjusted Debt-Equity Ratio: 2.33

ESOP IMPACT ON THE COMPANY’S FINANCIAL STATEMENTS

15

ESOP Impact on the Company’s Financial Statements

.

So who cares?• Whenever you have additional leverage on the company books current relationships

are impacted:• Current lender• Bonding agent• Customers and vendors• Current shareholders and other stakeholders

• Bankers – new to the transaction – working with a lender that understands what the balance sheet will look like after the transaction is key to closing the loan:• Possible negative equity…….• Ratios……• Loan covenants…….

• Possible alternative? • See FASB ASU 2014-17, Pushdown Accounting

16

ESOP Impact on the Company’s Financial Statements

.

• Upon a change in control, an acquired entity can elect to reflect the acquirer’s purchase on its financial statement by “writing up” the value of its assets, including recognition of intangible such as goodwill.

• Definition of change in control.

• The offsetting credit is to equity, resulting in an increase in net assets, mitigating the negative impact to net assets from a leveraged ESOP transaction.

• Election is irrevocable. Can be applied even if the change-in-control event occurred in a prior reporting period. A different election can be made for each change-in-control event.

• A purchase price allocation is required.

• Any goodwill that is generated would need to be tested for impairment or subject to amortization under ASU 2014-02 for private companies.

• Could be attractive if the pushdown would increase the carrying value of tangible assets.

ASU 2014-17 “Pushdown Accounting”

17

.

Tax Considerations

• A dividend to a C-corporation ESOP is tax deductible as long as the dividend is used to either service the ESOP debt or it is passed through to the participants.

• C-corporation – must be reasonable.

• An S-corporation distribution of earnings/dividend is not deductible.

Plan Consideration

• The employer may use Dividends on ESOP shares that have been allocated to participants for debt service only if the participants are allocated shares of employer stock with a fair value no less than the amount of the dividends used for debt service.

Dividends

18

.

• Dividends on unallocated shares used to pay debt service shall be reported as a reduction of debt or accrued interest payable.

• Dividends on unallocated shares paid to participants or added to participant accounts shall be reported as compensation cost.

• Because the employer can control the use of dividends on unallocated shares, dividends on unallocated shares are not considered “Dividends” for financial reporting purposes.

• Dividends on allocated shares shall be charged to retained earnings.

• Dividends payable may be satisfied by contributing cash to participant accounts or by contributing additional shares.

Dividends

19

.

Case facts:

• A new ESOP is established January 1, 2015.

• The ESOP enters into an internal loan in the amount of $1,000,000.

• The ESOP purchases 100,000 shares of newly issued shares at $10 per share.

• The debt service is funded by cash contributions and dividends.

Dividend Example

20

.

2015 2016Average Stock Price $10.75 $10.25Principal paid on loan $163,800 $180,200Interest paid $100,000 $83,600Total Debt Service $263,800 $263,800Shares released – by debt service 20,000 shares 20,000 shares

Dividends paid on common stock .50 cents/share or$50,000 to ESOP

.50 cents/share or$50,000 to ESOP

Employer Contributions paid to plan $213,800 $213,800

Dividend Example

21

.

Dividend Example

22

Entry to record debt payment – 2015Interest Expense $100,000ESOP Loan $163,800

Cash $263,800

Entry to record release of 20,000 shares 2015Compensation expense (20000 X $10.75*) $215,000

Paid-in-Capital $15,000Unearned ESOP plan shares (20,000 x $10) $200,000

Note: None of the dividends are charged to retained earnings in 2015

.

Dividend Example

23

Entry to record debt payment – 2016Interest Expense $83,600ESOP Loan $180,200

Cash $263,800

Entry to record release of 20,000 shares 2016Compensation expense (19,024 X $10.25*) $195,000Retained Earnings (20,000 X 50 cents) $10,000

Paid-in-Capital $5,000Unearned ESOP plan shares (20,000 x $10) $200,000

*Average share price

.

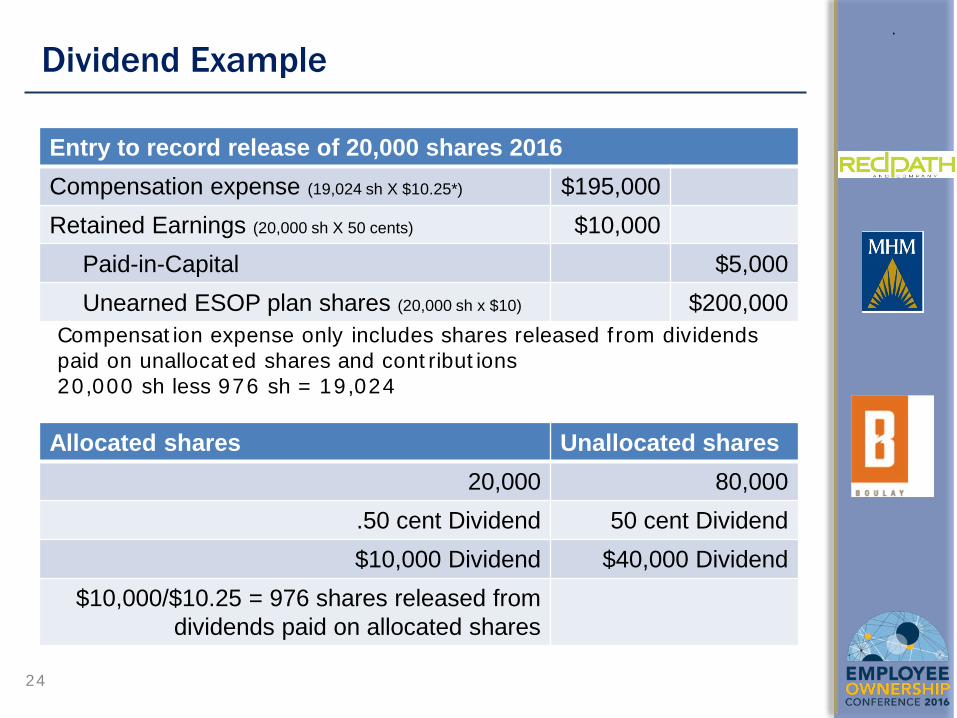

Dividend Example

24

Entry to record release of 20,000 shares 2016Compensation expense (19,024 sh X $10.25*) $195,000Retained Earnings (20,000 sh X 50 cents) $10,000

Paid-in-Capital $5,000Unearned ESOP plan shares (20,000 sh x $10) $200,000

Compensat ion expense only includes shares released f rom dividends paid on unallocat ed shares and cont ribut ions 20,000 sh less 976 sh = 19,024

Allocated shares Unallocated shares20,000 80,000

.50 cent Dividend 50 cent Dividend$10,000 Dividend $40,000 Dividend

$10,000/$10.25 = 976 shares released from dividends paid on allocated shares

.

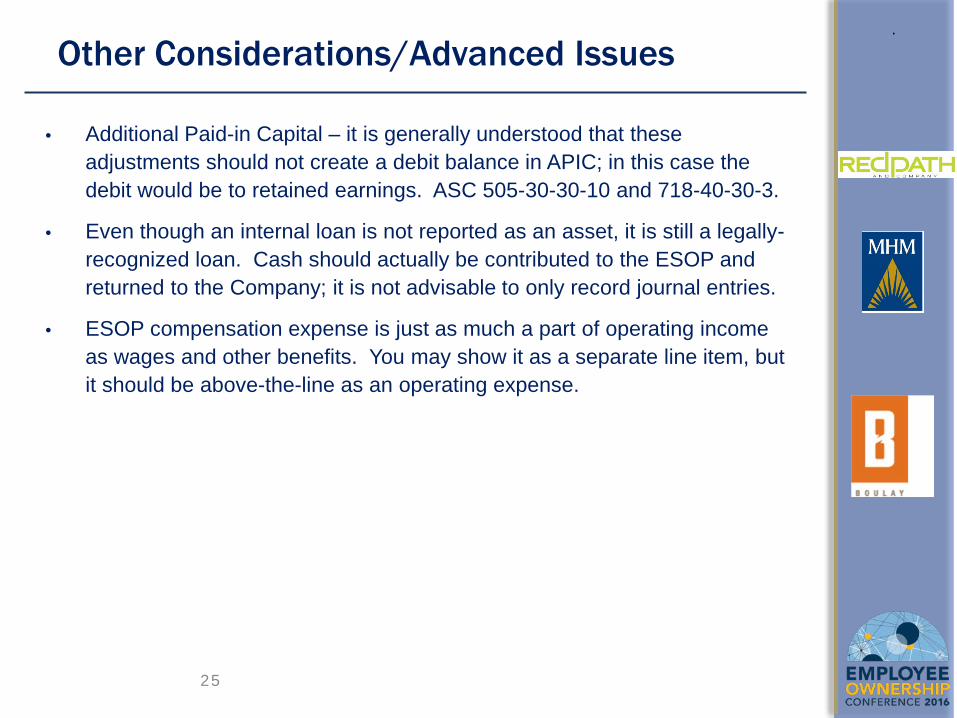

• Additional Paid-in Capital – it is generally understood that these adjustments should not create a debit balance in APIC; in this case the debit would be to retained earnings. ASC 505-30-30-10 and 718-40-30-3.

• Even though an internal loan is not reported as an asset, it is still a legally-recognized loan. Cash should actually be contributed to the ESOP and returned to the Company; it is not advisable to only record journal entries.

• ESOP compensation expense is just as much a part of operating income as wages and other benefits. You may show it as a separate line item, but it should be above-the-line as an operating expense.

Other Considerations/Advanced Issues

25

.

• In general, remember that dividends on the same class of stock are paid pro-rata. If the non-ESOP shareholder receives a dividend, the ESOP must as well.

• The ESOP’s dividend on suspense shares must be allocated to participants. The dividend cannot be held in suspense.

• What if dividends on allocated shares are used to pay interest on the acquisition loan to the Company? DR Retained Earnings, not Interest Expense. When the return funds are received by the company do we still credit interest expense? Yes. What if that creates negative interest expense? Then it becomes interest income.

ON MISTAKESOther Considerations/Advanced Issues

26

.Other Considerations/Advanced Issues

• Plan and tax accounting for ESOPs are substantially the same - different from GAAP.• ESOP Compensation Expense – Contributions are contributions, period. No

adjustment for FMV of shares released. No distinction between contributions earmarked for principal payments or interest payments. Should be reported on line 23 of the 1120 or line 17 of the 1120S. • Novel concept – total on that line should match the total employer contribution on

the Form(s) 5500!• Dividends – Dividends are dividends, period. Doesn’t matter if they are attributable to

allocated shares or unallocated/suspense shares. • If you’re a C Corporation, you might be able to deduct certain dividends under

404(k). Can be line 23 or line 26 (I prefer 26).• Interest – Contributions (or dividends on suspense shares)

used by the ESOP to pay interest are still either contributionsor dividends.• Interest paid by the ESOP to the Company is simply

interest income.

27

.Other Considerations/Advanced Issues

Committed to be Released Shares – after-end of year loan payments that produce shares allocated to participants for the prior year.

• Contribution must be allocated and deductible for prior year.

• Fair value of shares allocated are included in compensation expense.

• Committed to be released shares are listed separately in ESOP footnote.

• If principal and interest method of share release is used, interest after end of year cannot be included since it did not exist as of year-end.

28

.

Committed to be Released Example• Same assumptions as slides 8-13 example except loan and

annual payments are on 1/31 and always for the prior year.• Year 1 – 4787 shares released and fair value included in

compensation expense; listed as committed to be released shares in ESOP footnote (calculation includes 11/12 of 1st

interest payment made plus all of 1st principal payment).• Year 2 – 5007 shares released and fair value included in

compensation expense (calculation includes 1/12 of 1st interest payment, 11/12 of 2nd interest payment plus all of 2nd principal payment); ESOP footnote shows 4787 allocated shares, 5007 committed to be released shares and 90,206 unallocated shares.

Other Considerations/Advanced Issues

29

.

Administrative Loans• A no-interest loan from the company to the ESOP to pay expenses,

including distributions (PTE 80-26).• Normally paid off with contributions, ideally before end of current year.• If not paid off by year-end, no clear guidance on how to account for it on

company financial statement.• May need to treat the same as other loans used for stock purchases –

i.e. establish contra-equity account for loan amount.• Shown as “Advance to ESOP” contra-equity account in one case.

Other Considerations/Advanced Issues

30

.

• Repurchase liability is not on the financial statements, but is there a contingency to be disclosed under FASB ASC 440-10-50-4?

• Additional disclosures – shares allocated, released, committed to be released and unallocated. FV of shares for each period reported.

• Existence of put option.

• Any floor price protection.

Other Considerations/Advanced Issues

31

.

Warrants in ESOP Transaction

What is a warrant? • A security that allows the holder to purchase the underlying stock of the issuing

Company at a fixed price and for a specified period.

Why are warrants prevalent in ESOP transactions? • Most transactions include some seller financing (direct or outside loan).

• Subordinated outside seller loans are frequently accompanied by detachable stock purchase warrants in order to provide a market-level return to the lender/seller.

• Provides a market rate of return for seller financed subordinated debt - which in turn reduces the cash needs to service the related debt.

• Access to capital from traditional sources may be limited - warrants are a way to help finance a transaction.

• Possible tax advantages for the seller - capital gain rates paid on appreciation of the warrants.

32

.Accounting for Warrants

• Allocate the proceeds to the debt instrument (loan) and the warrant based on their relative fair values using an option pricing model.

• Amortize the loan based on the fair value of the loan - this will in effect increase interest expense.

• Adjust the fair value of the warrant at the end of each reporting period through earnings.

Note: Put options in connection with warrants are common in ESOP transactions. GAAP says if there is a put, then the warrant is a liability. If not, the warrant is treated as equity.

33

.

1. Subordinated seller note entered into for face value of $17,000,000 for redemption of stock.

2. Cash interest on note of 4%.

3. Detachable warrant provided that allows the holder to purchase 33,000 shares ofcommon stock at $150 per share.

4. Put included in warrant agreement - allows holder to settle in cash

5. At issuance date the fair value of the warrant is deemed to be $650,000. The fair value of the seller note is deemed to be $16,350,000.

6. Annual note payments of $2,095,946.

Warrant Example

34

Entries related to the stock redemption

Stock/APIC/Retained earnings $17,000,000 Note payable $17,000,000

To record the stock redemption

Note payable $650,000 Warrant liability $650,000

To record the warrant and note at FVThe result of the above 2 entries is to state the note to FV at $16,350,000 and the warrants on the books at FV of $650,000.

Entries to record loan payment and warrant liability in year 1. Assume warrant liability is $775,000 at reporting date.

Entries to record loan payment and warrant liability in year 2. Assume warrant liability is $700,000 at reporting date.

Note payable $1,375,531 Interest expense $720,415 Cash $2,095,946

To record seller note paymentWarrant expense/interest expense $75,000 Warrant liability $75,000

To record change in FV of warrants

Note payable $1,312,644 Interest expense $783,302 Cash $2,095,946

To record seller note paymentWarrant expense/interest expense $125,000 Warrant liability $125,000

To record change in FV of warrants

.

Amortization schedule - face value of notePayment Interest Principal Balance

17,000,000

1 2,095,946 680,000 1,415,946 15,584,054

2 2,095,946 623,362 1,472,584 14,111,470

3 2,095,946 564,459 1,531,487 12,579,983

4 2,095,946 503,199 1,592,747 10,987,236

5 2,095,946 439,489 1,656,457 9,330,779

6 2,095,946 373,231 1,722,715 7,608,065

7 2,095,946 304,323 1,791,623 5,816,441

8 2,095,946 232,658 1,863,288 3,953,153

9 2,095,946 158,126 1,937,820 2,015,333

10 2,095,946 80,613 2,015,333 (0)

Warrant Amortization Schedule

35

Amortization schedule - fair value of note Payment Interest Principal Balance

16,350,000

1 2,095,946 783,302 1,312,644 15,037,356

2 2,095,946 720,415 1,375,531 13,661,825

3 2,095,946 654,516 1,441,430 12,220,395

4 2,095,946 585,459 1,510,487 10,709,909

5 2,095,946 513,094 1,582,852 9,127,057

6 2,095,946 437,263 1,658,684 7,468,373

7 2,095,946 357,798 1,738,148 5,730,225

8 2,095,946 274,526 1,821,420 3,908,805

9 2,095,946 187,265 1,908,682 2,000,123

10 2,095,946 95,823 2,000,123 (0)

.

SARs In ESOP Transactions

What are stock appreciation rights (SARs)?

• Non-qualified deferred compensation tool

• Entitles employees to receive cash, stock or a combination of both in an amount equal to the excess of the fair value of a stated number of shares of the employer’s stock over the reference value

Why ESOPs Utilize SARs

• Deigned to provide long-term incentive in the form of deferred compensation to key employees

36

.

Accounting for SARs

• Recognize compensation cost and a related liability ratably over the requisite service period (vesting period)

• Compensation cost is equal to the fair value of the SAR

• Recognize change in fair value or intrinsic value at the end of each reporting period through earnings - compensation cost

• Public Companies required to measure SARs at fair value

• Non-public entities may elect to use the intrinsic value method to value the SARs

• Intrinsic value - simply the fair value of the stock less the reference value

37

.

1. SAR plan instituted for certain employees

2. Award of SAR's are at the discretion of theBOD

3. At award date 1,000 SARs were issued to employees with a reference value of $3.00 per SAR unit

4. Assume the following fair values for a SAR unit and a share of stock:

SAR Example

38

SAR unit common stockYear fair value fair value

1 4.00 3.50

2 6.00 5.00

3 10.00 9.00

4 15.00 18.00

5. At the date of the issuance of the SAR unit the fair value of a SAR unit was $4.00 per.

6. Vesting in the SARs occur over a 3 year period.

.

SAR Example

39

Fair Value Method Intrinsic Value Method

Year 1 entry

Expense 1,333.33 166.67

SAR Liability 1,333.33 166.67

Year 2 entry

Expense 2,666.67 1,166.67

SAR Liability 2,666.67 1,166.67

Year 3 entry

Expense 6,000.00 4,666.67

SAR Liability 6,000.00 4,666.67

Year 4 entry

Expense 5,000.00 9,000.00

SAR Liability 5,000.00 9,000.00