fyp ratio analysis krishak bharat ash

DESCRIPTION

project report on RATIO ANALYSIS kribhcoTRANSCRIPT

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 1/69

1

A PROJECT REPORT

ON

RATIO ANALYSIS

UNDERTAKEN AT

KRISHAK BHARATI CO-OPERATIVE LIMITED

SURAT

MASTER OF BUSINESS ADMINISTRATION (FINANCE)

SUBMITTED IN PARTIAL FULFILLMENT OF

THE REQUIREMENTS FOR AWARD OF

MASTER OF BUSINESS ADMINISTRATION OF

TILAK MAHARASHTRA UNIVERSITY, PUNE.

SUBMITTED BY

HUZAIFA A SOPARIWALA

PRN: 07208013498

OF

PAI INTERNATIONAL CENTER FOR MANAGEMENT

EXECELLENCE

TILAK MAHARASHTRA UNIVERSITY

GULTEKDI, PUNE 411037.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 2/69

2

PREFACE

I have really enjoyed working on this project. In the starting phase,

I found this work difficult, but with ample guidance of all staff members

of the Krishak Bharati Cooperative Limited, Surat. I was able to

complete my work successfully.

It is the responsibility of the Management of an organization to

guide each newly joined individual to remove his anxiety in an

organizational environment and help him in settling down.

In this project I have covered the aspect relating to training

followed by the management of an organization. Under this study I have

put in my best efforts to make this project successful.

While working on this project I got exposure to the training

practice use by the organization.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 3/69

3

ACKNOWLEDGEMENT

Man’s quest for knowledge never ends. Theory and practice are

essential and complementary to each other I am thankful for the

assistance received from various individuals in making this project

successfull. I find no words to express my gratitude towards those who

are constantly involved with us throughout my project in PAI

INTERNATIONAL CENTER FOR MANAGEMENT EXECELLENCE.

I would like to give my special thanks and regards to

“Mr.T.S.Thomas” (General Manager, Surat Who has helped me to carry

out this project as my project in charge under his guidance and blessing

I was able to fulfill the requirements of my university.

I would also like to thanks Mr.A.M.S.Belim, Mr.M.A,Patwa (F&A

Department), for their most precious contribution and their help in my

project. I am very much thankful to other staff members of “Kribhco,

Surat”. Without their help I am not able to finish this project.

I am highly obliged to the management of Pai international

center for management execellence For allocating me a very

interesting and challenging project. I am sincerely thankful to my project

guide Prof. Prashant Gundawar and our Director Prof. R.Ganeshan for

providing the resources for the project. Their guidance and support was aconstant source of inspiration for me.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 4/69

4

EXECUTIVE SUMMARY

This summer project report is prepared at “KRISHAK BHARATI

COOPERATIVE LIMITED.” at Surat on “RATIO ANALYSIS” as a part of

curriculum of the MBA program.

I have selected this topic to measures the financial position of the

company and firm profit ability as well as its credit policy with the help of

ratio analysis. Ratio analysis is a widely used of financial analysis. It is

defined as the systematic use of ratio to interpret the financial

statements so that strengths and weakness of a firm as well as its

historical performance and current financial condition can be

determined.

The main Objectives are: To know the financial condition of the company.

To know the strength and weakness of the company

To know that company has enough asset compare to its liabilities

To study inventory management.

To study company’s ability to earn profit compare to its sales

To analyze the liquidity position of the company.

To study receivable management and company ’s credit policy. To achieve these objectives, I have studied fifteen ratio

analysis which are as below…

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 5/69

5

Ratio analysis :

o

Current Ratioo Quick Ratio

o Inventory Ratio

o Inventory turnover Ratio

o Debtor turnover ratio

o Debtors conversion period

o Current assets turn over ratio

o Cash Ratio

o Debt-equity ratio

o Net-profit ability ratio

o Gross-profit ability ratio

o Return on capital employed

o Inventory conversion period

o Raw material conversion period

o Work in progress conversion period

o Finished good conversion period

Methodology:

Descriptive research design has been used and data are collected

through secondary data collection method.

I have use Microsoft Excel for the data analysis.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 6/69

6

TABLE OF CONTENTS

CHAPTER

NO.

TOPIC PAGE

NO.

1.Industry profile

8

2.Company profile

13

3. Theory of Ratio Analysis

19

4.Literature Review

24

5.

Research Methodology

26

6.Data analysis & inference

30

7.Conclusion & Recommendation

66

8.Suggestions & Limitation

68

9.Bibliography

70

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 7/69

7

INDUSTRY PROFILE

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 8/69

8

IINNTTR R OODDUUCCTTIIOONN OOFF FFEER R TTIILLIIZZEER R IINNDDUUSSTTR R YY

Before introducing organization

KRIBHCO (a Fertilizer producing unit). I feel

necessary to give an overview of the Indian

Fertilizer Industries.

“India lives in villages,” said Mahatma

Gandhi decades ago. It is true even today. Like

every developing economy, the economy of

India is also agro-based. Agriculture accounts for nearly 1/4th of India's GDP and more

importantly, about 2/3rd

of the country's population is dependent on agriculture and allied

activities for their livelihood. As per statistics nearly 175 lakhs MT of fertilizer nutrients

are required every year in this country. The demand of fertilizers was so high that India

had to import almost 30% of its requirement from other countries. Therefore, to achieve

the economic growth, agriculture base of the country must be strengthened. To attain this

objective, agriculture practices have to be improved from their traditional pattern to a

higher technological track involving better irrigation and use of better quality seeds,

fertilizers, insecticides & pesticides. Therefore, chemical fertilizers are key player in this

process and fertilizer industries plays quite a major role in increasing food production in

the country and also helps to modernize the out look of the common farmers and make

them innovative and respective to the new technology change.

India is basically an agricultural country which economy depends largely upon its

agrarian produce. Agricultural sphere contributes about 25% to the country's GDP. As a

result, Indian fertilizer industry has tremendous scope in and outside the country as it is

one of the allied parts of agriculture.

Today, Indian Fertilizer Industry is developing in terms of technology. Indian

manufacturers are adopting advanced manufacturing processes to prepare innovative new

products for Indian agriculture.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 9/69

9

Growth of Fertilizer Industry

One of the most significant achievement of the post Independence period of our Country

has been the ability to achieve self-sufficiency in food grain production. This

achievement is due to the rapid growth and improvement of Fertilizer industry. The

Fertilizer industry is growing at the rate of 4% for the last 10 years and has been

contributing a significant part of G.D.P.

The growth and importance of Fertilizer industry in India can be divided in to three

distinct phases, these are given below.

1. Pro Green Revolution Period:

This period is described in 1952-1953 era where increased growth of food grains took

place however this increased production in food grains took place due to increased

irrigation methods. In this phase the land under agriculture was made more, during this

period about 80% of the country's population was involved in Agriculture either directly

or indirectly. During this period the fertilizer's which were manufactured were Super

Phosphate & Ammonium Sulphate. Irrigation was thought to be heart of Agriculture.

2. Green Revolution Period:

During this phase Government stated the programmed aimed at making our country self

sufficient in Food Products. This was the period between the years 1959-1960. This plan

laid the emphasis on production of High Yielding Varieties. To make this plan a success

there was a high need to make soil fertile by providing it with nutrients like Phosphorus,

Nitrogen and Potassium.

During this phase Fertilizer industry tried to play a vital role, became one of the most

important, and inherits part of our economy.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 10/69

10

3. The Post Green Revolution Period:

The world's population along with Indian population has kept on growing at an alarming

rate; the fertilizer companies all over India are trying to expand their scale of operations

in order to increase the production rate. The demand for fertilizers per year is increasing.The current demand of fertilizers in India is 18 million tones.

- According to Fertilizer Association of India.

Fertilizer Industry Scenario in India

In India, First of all in 1906, A Single Super Phosphate (SSP) manufacturing unit was set

up at Ranipat near Chennai (Madras) with annual capacity of 6000 tones per annum.

1. Public Sector

The Fertilizer And Chemicals Travancore Ltd. (FACT)

Hindustan Fertilizer Corporation Ltd. (HFC)

Madras Fertilizer Ltd. (MFL)

Hindustan Copper Ltd. (HCL)

Naively Lignite Corporation Ltd. (NLC)

Pyrites, Phosphates And Chemicals Ltd. (PPCL)

Pradeep Phosphates Ltd. (PPL)

Rashtriya Chemicals And Fertilizers Ltd. (RCFL)

National Fertilizer Ltd. (NFL)

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 11/69

11

2. Co-operative Sector

There are only two fertilizer manufacturing societies in Co-operative sector.

Indian Farmers Fertilizers Co-Operative Ltd. (IFFCO)

Krishak Bharati Co-Operative Ltd. (KRIBHCO)

3. Private Sector

There are 17 companies in private sector, which are producing fertilizer.

Gujarat Narmada Valley Fertilizer Co. Ltd. (GNFC)

Hindustan Lever Ltd. (HLL)

Hari Fertilizer

ICI India Ltd.

Indo Gulf Fertilizers & Chemicals Corporation Ltd.

Mangalore Chemicals & Fertilizers Ltd. (MCFL)

Southern Petro Chemicals Industries Corporations Ltd.

Nagarjuna Fertilizer & Chemical Ltd. (NFCL) Shri Ram Fertilizer & Chemicals Ltd.

Tuticorian Alkali Chemicals & Fertilizer Ltd.

Zuari Agro Chemicals Ltd.

Bindali Agro Chemicals Ltd.

Chambal Fertilizer & Petrochemical Corporations Ltd. (DEPCL)

E.D.I. PASSY (I) LTD.

Gujarat State Fertilizer Company (GSFC

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 12/69

12

COMPANY PROFILE

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 13/69

13

KRISHAK BHARTI CO-OPERATIVE LTD

Introduction:-

Name: - K K K r r r iiissshhhaaak k k BBBhhhaaar r r aaatttiii CCCooo---ooo p p peeer r r aaatttiiivvveee LLLtttddd...

Joint Sector: - Government, IFFCO and NCDC.

Foundation stone laid by smt.Indira Gandhi: - 5th February1982

Trial production of Urea: - 26TH November , 1985

Start of commercial Production: - 1st March 1986

Year of Business: - 25 years

Legal Status: - Multi state co-operative society

No. of Employees: - 2567

Manufacturing and Marketing: - Urea, Ammonia and Bio-fertilizer.

Urea – Ammonia Plant Location: - Distance from Surat, Hazira Guj.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 14/69

14

KRIBHCO Network: -

A. Head office

B. (i) Plant

(ii) Bio fertilizer plant

(iii) Seed processing plant

C. Zonal offices

D. State marketing offices

Fertilizer plant, Noida, Delhi

Surat (Gujarat)

Surat (Gujarat)

Andhra Pradesh, Gujarat, Haryana, U.P.

M.P, Punjab, Rajasthan,

Bhopal, Bangalore, Lucknow and

Chndigarh

Jaipur, Ahmedabad, Chennai,

Mumbai, Banglore, Patna, Lucknow,

Chandigarh, Bhopal, Hyderabad, Guwahati,

Dehurdun, Kolkata.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 15/69

15

OBJECTIVES OF KRIBHCO

MAIN:-

1. To increase the urea installed capacity, maintaining its market share.

2. To ensure optimum utilization of existing plant and machinery, through

proper maintenance.

3. To diversify into other core sector like power, LPG terminal/port,

chemicals etc.

OTHERS:-

1. To enlarge product mix through product development

2. To continue and intensify efforts towards rural development and Co-

operative movements.

MISSION

1. To contribute to agriculture & rural development in the regions.

2. Services to members of cooperatives society by selecting financing.

Managing society desirable and commercial profitable investment

opportunity preferable at multiple locations.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 16/69

16

VISION

We want to be a world class organization that represents the farmer community and

maximizes returns to them through specialization in agricultural inputs and products

and other diversified businesses that maximize stakeholder value.

MILESTONES / RECORDS:-

KRIBHCO has achieved a milestone in handling of OMIFCO urea:

- Total quantity received up to 12.08.2006 - 1001133.890 MT

- Total quantity dispatched up to 08.09.2006 - 1002323.700 MT

First, achieve record capacity utilization in the first year of commercial

production - 93.5% and 97.4% for Ammonia and Urea plants.

First, achieve highest net profit of Rs. 126.80 Crore in the year 1987- 88 by

any fertilizer organization.

First, to achieve 10 and 20 million tones of Urea production milestone within a

short period of 6.4 years and 12.6 years from commencement of production.

First, the country to achieve 10 million tones of Ammonia production milestone

within a period of 10.7 years from commencement of production.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 17/69

17

AWARDS:-

KRIBHCO receives Gold star award of Excellence from Institute of Economic Studies

for its overall excellent performance.

KRIBHCO receives the Rajbhasha Award from Honb'le Minister of Chemical and

Fertilizers for 2002-03, 2003-04, 2004-05.

KRIBHCO was awarded First prize for Production, Promotion, and marketting of

Bio-fertilizers for the year 2004-05 on 1st of December '05 by FAI.

IIIE - ENTERPRISE EXCELLENCE Award for the year 2003-04

KRIBHCO has won INDIRA GANDHI RAJBHASHA PURUSKAR (2nd) for 2003-04.

KRIBHCO -Hazira - Pot Plants exhibition received the 2nd prize in the first National

Horticulture exhibition and flower show for the year 2002.

FAI – Best Video Film Award 1987, 1990, 1991, 1992, 1993, 1994, 1995, 1996 and 1998

FAI Technical Innovation Award: 2001-02 to two KRIBHCO Officers.

SHIELD & CERTIFICATE awarded by Rajbhasha Vibhag, Home Ministry, GOI for

PROMOTION OF HINDI AS AN OFFICIAL LANGUAGE for the year 1993-94.

"RAJBHASHA SHIELD" for OUTSTANDING WORK IN OFFICIAL LANGUAGE

for the year 1994-95 by Official Language Implementation Committee, Surat.

'Best House Keeping' Award to KRIBHCO’s Hazira Complex from Baroda

Productivity Council – Awarded 5 times from 1988-89 to 1991-92.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 18/69

18

RATIO ANALYSIS

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 19/69

19

1. RATIO ANALYSIS

Ratio analysis is a widely used of financial analysis. It is defined as the systematic use of

ratio to interpret the financial statements so that strengths and weakness of a firm as well

as its historical performance and current financial condition can be determined. The term

ratio refers to the numerical or quantitative relationship between two items variables.

The alternative, methods of expressing items, which are related to each other , are for

purposes of financial analysis, referred to as ratio analysis. It should be noted that

computing the ratio does not add any information not already inherent in the above

figures of profits and sales. What ratios do is that they reveal the relationship in a more

meaningful way so as to enable us to draw conclusions from them.

The rational of ratio analysis lies in the fact that it makes related information comparable.

A single figure by itself has no meaning but when expressed in terms of a related figure,

it yields significant inferences. For instance, the fact that net profits of a firm amount to

say, Rs. 10 lacks throws no light on its adequacy or otherwise. Figure of net profit has to

be considered in relation to other variables. How does it stand relation to sales? What

does it represent by way of return on total assets used or total capital employed? If

therefore net profits are shown in terms of their relationship with items such as sales,

assets, capital employed equity capital and so on; meaningful conclusions can be drawn

regarding their adequacy.

Ratio is very useful to for grasping the message of the financial statement and

understanding them. It helps to enlarge and understand the financial health and travel of

the business, it past performance makes it possible to forecast about future state of the

business. The ratio use to measure the effectiveness of the employment of resources is

termed as Activity Ratio or Turnover Ratio.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 20/69

20

These ratios are important measures of ratio analysis.

Ratio Formulae Result Interpretation

Stock

Turnover

(in days)

Average

Stock * 365/

Cost of

Goods Sold

= x

days

On average, you turn over the value of your entire

stock every x days. You may need to break this

down into product groups for effective stock

management.

Obsolete stock, slow moving lines will extend

overall stock turnover days. Faster production,

fewer product lines, just in time ordering will

reduce average days.

Receivables

Ratio

(in days)

Debtors *

365/

Sales

= x

days

It takes you on average x days to collect monies

due to you. If you’re official credit terms are 45

day and it takes you 65 days... why?

One or more large or slow debts can drag out the

average days. Effective debtor management will

minimize the days.

Payables

Ratio

(in days)

Creditors *

365/

Cost of Sales

(or

Purchases)

= x

days

On average, you pay your suppliers every x days.

If you negotiate better credit terms this will

increase. If you pay earlier, say, to get a discount

this will decline. If you simply defer paying your

suppliers (without agreement) this will also

increase - but your reputation, the quality of

service and any flexibility provided by your

suppliers may suffer.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 21/69

21

Current

Ratio

Total

Current

Assets/

Total

Current

Liabilities

= x

times

Current Assets are assets that you can readily turn

in to cash or will do so within 12 months in the

course of business. Current Liabilities are amount

you are due to pay within the coming 12 months.

For example, 1.5 times means that you should be

able to lay your hands on $1.50 for every $1.00

you owe. Less than 1 time e.g. 0.75 means that

you could have liquidity problems and be under

pressure to generate sufficient cash to meet

oncoming demands.

Quick Ratio

(Total

Current

Assets -

Inventory)/

Total

Current

Liabilities

= x

times

Similar to the Current Ratio but takes account of

the fact that it may take time to convert inventory

into cash.

Working

Capital

Ratio

(Inventory +

Receivables

- Payables)/

Sales

As %

Sales

A high percentage means that working capital

needs are high relative to your sales.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 22/69

22

Bad debts expressed as a percentage of sales.

Cost of bank loans, lines of credit, invoice discounting etc.

Debtor concentration - degree of dependency on a limited number of customers.

Once ratios have been established for your business, it is important to track them over

time and to compare them with ratios for other comparable businesses or industry sectors.

When planning the development of a business, it is critical that the impact of working

capital be fully assessed when making cash flow forecasts. Our financial planning

software packages - Ex-Plan and Cash flow Plan - can facilitate this task as they provide

for the setting of targets for receivables, payables and inventory.

ADVANTAGES OF RATIO ANALYSIS:

With the help of the ratio you can predict financial position of the company.

After showing the ratio its easy for bank to work with a company

We can compare two firm after seen there ratio

Its help to forecasting and make future plan of the company

With the help of the ratio we can locate the weak spot or problem of the company

Its also help in cost control in the firm

With the help of the ratio employee can know about the company and its helping

in their job.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 23/69

23

LITRERATURE REVIEW

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 24/69

24

Review of previous study

Ratio-analysis is a concept or technique which is as old as accounting

concept. Financial analysis is a scientific tool. It has assumed important role as a

tool for appraising the real worth of an enterprise, its performance during a period

of time and its pit falls. Financial analysis is a vital apparatus for the interpretation

of financial statements. It also helps to find out any cross-sectional and time series

linkages between various ratios.

Unlike in the past when security was considered to be sufficient

consideration for banks and financial institutions to grant loans and advances,

nowadays the entire lending is need-based and the emphasis is on the financial

viability of a proposal and not only on security alone. Further all business

decision contains an element of risk. The risk is more in the case of decisions

relating to credits. Ratio analysis and other quantitative techniques facilitate

assessment of this risk.

Trend ratio involve a comparison of the ratio of a firm over time, that is present

ratio are compared with past ratio for the same firm. The comparison of the profitability

of a firm, say year 1 though 5 is an illustration of a trend ratio. Trend ratio indicate the

direction of change in the performance-improvement, deterioration or constancy-over the

years.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 25/69

25

RESEARCH METHODOLOGY

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 26/69

26

Problem Statement:

How to measure the financial position of the company with the help of ratio

analysis?

Objective of Study:

To know the financial condition of the company.

Interpret the financial statement so that the strength and weakness of a firm

Historical performance and current financial condition can be determined.

To analyze the liquidity position of the company.

Throw light on a long term solvency of a firm.

Research Design:

A research design is the specification of method and procedure for accruing the

information needed. It is overall operational pattern of frame work of project that

stipulates what information is to be collected for source by that procedures

Descriptive Research design is appropriate for this study.

Descriptive study is used to study the situation. This study helps to describe the

situation. A detail descriptive about present and past situation can be found out by

the descriptive study. In this involves the analysis of the situation using the

secondary data.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 27/69

27

Data Collection:

This research study is based on secondary data, means data that are already

available i.e. the data which have been already collected and analyzed by some one else.

Secondary data are used for the study of Ratio analysis of this company. To

collect the data I have refer – Company annual report, annual magazine, last 5 year

balance sheet, and cash flow statements.

Another source of secondary data was in the form of reference books and Literature

Review published by third parties but available to the public. The World Wide Web

(Internet) was also an important source of information related to inventory

management.

Secondary Data Sources

Internal

Sources

External

Sources

Procedure

Manuals

ERP

Reports

Other

Reports

Reference

Books

World

Wide Web

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 28/69

28

Method of Analysis:

Ratio analysis :

o Current Ratio

o Quick Ratio

o Inventory Ratio

o Inventory turnover Ratio

o Debtor turnover ratio

o Current assets turn over ratio

o Cash Ratio

o Debt equity ratio

o Debtor’s conversion period

o Net profit ability ratio

o Gross profit ability ratio

o Return on capital employed

o Inventory conversion period

o Raw material conversion period

o Work in progress conversion period

o Finished goods conversion period

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 29/69

29

DATA ANALYSIS

AND

INTERPRETATION

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 30/69

30

1) Ratio Calculations

{1.1} Current Ratio

Current Ratio =Current Assets

Current Liabilities

Current Assets

For year 04-05 = 171,204.66

05-06 = 142,100.26

06-07 = 157,699.67

07-08 = 185,178.30

Current Liabilities

For year 04-05 = 29,982.54

05-06 = 29,724.31

06-07 = 34,234.82

07-08 = 49,858.31

Current Ratio

For year 04 - 05 =171,204.66

= 5.71 : 129,982.54

05 - 06 =142,100.26

= 4.78 : 129,724.31

06 - 07 =157,699.67

= 4.61: 1

34,234.82

07 - 08 =185,178.30

= 3.71: 149,858.31

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 31/69

31

Interpretation:

The ideal level of current ratio is 2:1.we shown too much higher ratio its good for the

company. Higher the current ratio, the larger is the amount of rupees available per rupees

of current liabilities, the more is the firm’s ability to meet current obliga tion and greater

is safety of fund of short term creditors.

Company’s current ratio is far better than its ideal level. So kribhco may take

some liabilities like bank overdraft, it’s not necessary but if management want. Overall

higher the better for company prestige

5.71

4.78 4.61

3.71

0

1

2

3

4

5

6

2004-05 2005-06 2006-07 2007-08

V a l u e

Year

Current Ratio

Ratio

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 32/69

32

{1.2} Quick Ratio

Quick Ratio =Quick Assets

Current Liabilities- Bank OD

Quick Assets = Current asset – Inventories

For year 04 - 05 = 171,204.66 – 14,670.07 = 156,534.59

05 - 06 = 142,100.26 – 15,289.98 = 126,810.28

06 - 07 = 157,699.67 – 25,090.64 = 132,609.03

07 - 08 = 185,178.30 – 21,404.82 = 163,773.48

Quick Ratio

For year 04 – 05 =156,534.59

= 5.22 : 129,982.54

05 - 06 =126,810.28

= 4.27 : 129,724.31

06 – 07 =132,609.03

= 3.87 : 134,234.82

07 – 08 =

163,773.48

= 3.28 : 149,858.31

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 33/69

33

Interpretation:

Ideal level of this ratio is 1:1.compare to current ratio stock is deducted from current

assets because we can’t convert stock into cash in short period of time. we can predict the

position more accurately compare to current ratio, Higher the ratio higher the company

liquidity position.

We can see that Quick ratio of the year 2008 is 3.28:1 which is lesser then all previous

years indicate company’s bad liquidity position.

5.22

4.273.87

3.28

0

1

2

3

4

5

6

2004-05 2005-06 2006-07 2007-08

V a l u e

Year

Quick Ratio

Ratio

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 34/69

34

{1.3} Debt equity Ratio

Debt equity ratioLong term debt

Share holders equity

Long term debt=total liabilities-current liabilities

For years 04-05= 2095.42

05-06=2204.01

06-07=2312.54

07-08=2603.26

Share holders equity=equity/preference share capital+ discount on share

For year 04 - 05 = 2,691.57 + 5,519.91 / 2 = 4,105.74

05 - 06 = 5,519.91 + 6,376.20/ 2 = 5,948.05

06 - 07 = 6,376.20 + 14,696.98/ 2 = 10,536.59

07 - 08 = 14,696.98 + 11,020.20/ 2 = 12,858.59

Debt equity Ratio

For year 04 – 05 =

2095.42

= 0.514105.74

05 – 06 =2204.01

= 0.375,948.05

06 – 07 =2312.54

= 0.2210,536.59

07 – 08 =2603.26

= 0.2012,858.59

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 35/69

35

Interpretation:

The D/E ratio is an important tool of financial analysis to appraise the financial

structure of a firm. It has important implication from the view point of the creditors,

owners, and the firm itself. The ratio reflect the relative contribution of creditors and

owners of business in its financing. A high ratio shows a large share of financing by

the creditors of the firm, a low ratio implies a small claim of creditors.

We can see that in above ratio that in 2004 ratio is 0.51 it implies that every

rupee of outside liabilities, the firm has two rupees owners capital. in 2005 ratio

decrease to 0.37 after every year its decreasing 0.22 and 0.20 respectively.

0

0.1

0.2

0.3

0.4

0.5

0.6

debt equity ratio

ratio

year

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 36/69

36

{1.4} Inventory Ratio

Inventory Ratio =Inventory

Current Assets

Inventory Ratio

For year 04 - 05 =14,670.07

=0.09:1171,204.66

05 - 06 =15,289.98

=0.11:1142,100.26

06 - 07 =25,090,64

=0.16:1157,699.67

07 - 08 =21,404.82

=0.12:1185,178.30

0.09

0.11

0.16

0.12

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

2004-05 2005-06 2006-07 2007-08

V a l u e

Year

Inventory Ratio

Ratio

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 37/69

37

Interpretation:

This ratio shows a relation between sales and inventory. It shows the no of time an

inventory is converted in to sales over a year. Altogether the inventory turnover ratio

means lesser the stock as compare to sales where as lesser the inventory turnover ratio

means more inventory in stock.

As we can see that in the year 2006-07 ratio is 16 % that is higher than 2004-05 &

2005-06 that is 11 % and 9 % respectively and also 2007-08 is 12 %. That means

investment in inventory is increase over the last 2 years, which gives bad indication and

in 2007-08 is good indication because investment is increase from 2004 to 2006 year.The

position of year shows a downward trend, which means that the enterprise is investing

more in its inventories as compare to its sale. Taking 1998 -99 has shown a 7.63 % of

down fall whereas the investment in inventory for the same year has shown a mere 4.19

% of downfall. This means there is proportionately more fall in sales in inventory. A

similar position follows in the year 1999 - 00 and 2000 - 01. In 1999 -00 the decrease in

sale 11.45 % where the inventory is increase with 23.17 %. In 2000 - 01 the pies is

decrease with 0.85 % and inventory is increase with 39.52 %. This shows that the

enterprise is fail to control the inventory which is not good for enterprise.

Here the inventory ratio decreases during the year here the inventory turnover

ratio decrease from 8.86 times to 6.31 times. This is not a good sign for the enterprise.

The number of days the inventory is held is increase. Presently it is about 57 days Where

as it was about its days in 1997 -'98 so we can say that the enterprise is suffering for its

position. The ratio is not -satisfactory.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 38/69

38

{1.5} Current Asset Turnover Ratio

Current Asset Turnover Ratio =Total Sales

Current Asset

Current Assets

For year 04-05 = 171,204.66

05-06 = 142,100.26

06-07 = 157,699.67

07-08 = 185,178.30

Total Sales

For year 04 -05 = 92,421.96

05 - 06 = 125,729.74

06 - 07 = 134,397.10

07 - 08 = 138,488.33

Current Asset Turnover Ratio

For year 04 – 05 =92,421.96

= 0.54 : 1

171,204.66

05 – 06 =125,729.74

= 0.88: 1142,100.26

06 – 07 =134,397.10

= 0.85 : 1157,699.67

07 – 08 =138,488.33

= 0.75 : 1185,178.30

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 39/69

39

Interpretation: This ratio indicates the efficiency with which current asset turn intosales. A higher ratio implies by and large more efficient use of fund. Thus a high turnover

ratio indicates reduced lock-up of fund in current assets. An analysis of this ratio over a

period of time reflects working capital management of a firm.

Current assets turn over ratio is good for the years of 2005-06, 2006-07, 2007-08 that is

0.88:1, 0.85:1 and 0.75:1 respectively. For the year 2004-05 it was decrease because

company’s current assets are higher than its liability.

But we can say that the company’s position is better then the last few years that is 2005-

06 and 2006-07.

0.54

0.88 0.850.75

00.1

0.20.30.40.50.60.70.80.91

2004-05 2005-06 2006-07 2007-08

V a l u e

Year

Current assets Turn over Ratio

Ratio

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 40/69

40

{1.6} Cash Ratio

Cash Ratio =Cash in Hand + Cash at bank + Current investment

Liquid Assets

Cash in Hand + Cash at bank + Current investment

For year 04 - 05 = 124,761.99+14,670.07 = 139,432.06

05 - 06 = 93,558.64 +15,289.98 = 108,848.62

06 - 07 = 80,241.37 +25,090.64 = 105,332.01

07 - 08 = 90,504.27 +21,404.82 = 111,909.09

Liquid Assets = Current Liabilities – Proposed Dividend – Tax on Dividend

For year 04 - 05 = 29,982.54-7,450.02 = 22,532.5205 - 06 = 29,724.31-7,846.69 = 21,877.62

06 - 07 = 34,234.82-7,891.44 = 26,343.38

07 - 08 = 49,858.31-7,920.50 = 41,937.81

Cash Ratio

For year 04 – 05 =139,432.06

= 6.18:122,532.52

05 – 06 =108,848.62

= 4.98:121,877.62

06 – 07 =105,332.01

= 3.99(8):126,343.38

07 – 08 =

111,909.09

=2.67:141,937.81

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 41/69

41

Interpretation:

The cash ratio is perhaps the most stringent measure of liquidity indeed. One can argue

that it is overly stringent lack of immediate can may not matter it. The firm can starch its

payment or borrow many of short notice cash and bank balance and short term

marketable security and liable assets of firm financial analysis looks at cash ratio which is

define.

Management has to maintain a level of cash ratio so that cash is required urgently

they can get it. Too high level of cash loss the opportunity to earn interest on that capital.

We can see that Cash ratio is initially high in the year of 2004-05 that is 6.18.

But its start decreasing from next year. it was 4.98. and next years also decrease. In

current year is 2.67:1 thought its cash and bank balance is high. This level is well and

good for the company.

6.18

4.98

3.99

2.67

0

1

2

3

4

5

6

7

2004-05 2005-06 2006-07 2007-08

V a l u e

Year

Cash Ratio

Ratio

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 42/69

42

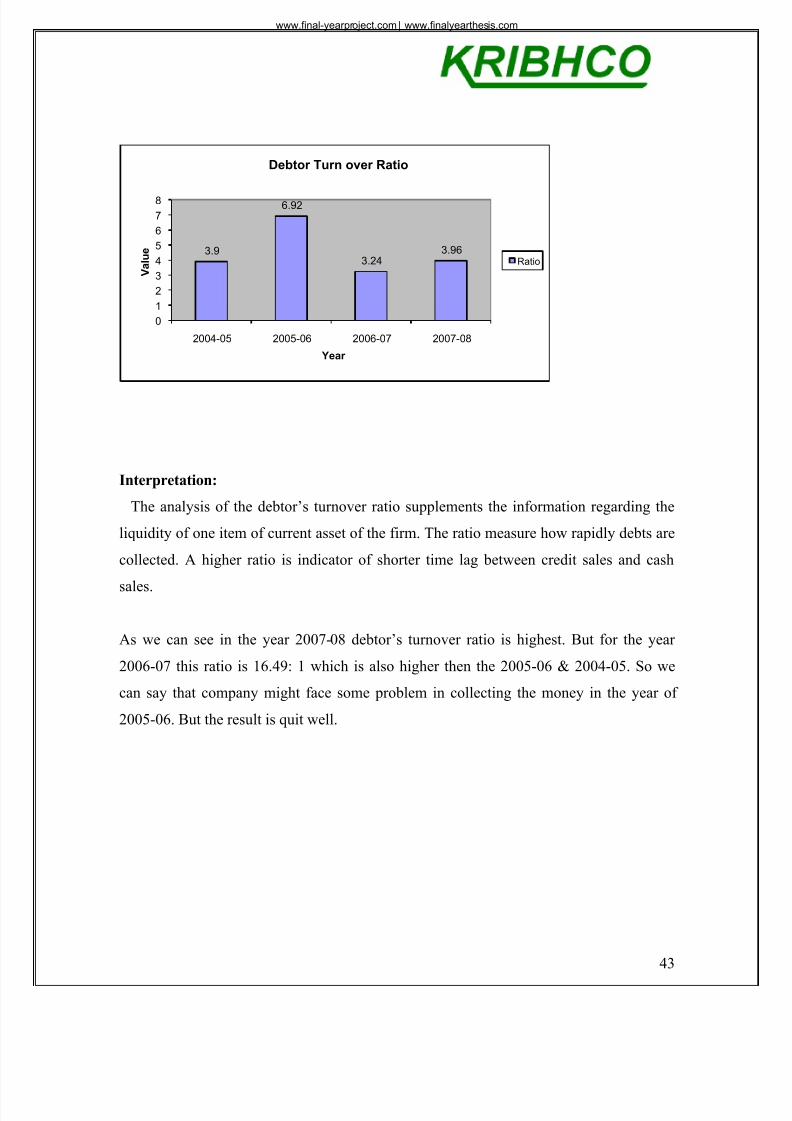

{1.7} Debtor’s Turnover Ratio

Debtor’s Turnover Ratio = Credit Sales

Ave. Debtors

Credit Sales= Credit sale are 75% 0f Total sale.

For year 04 - 05 = 55,453.18

05 - 06 = 75,443.84

06 - 07 = 80,638.26

07 - 08 = 83,093

Ave. Debtors = (Opening of debtors + Closing of Debtors) / 2

For year 04 - 05 = 20,719.65 + 7,723.20 / 2 = 14,221.43

05 - 06 = 7,723.20 + 14,079.60 / 2 = 10,901.40

06 - 07 = 14,079.60 + 35,736.84 / 2 = 24,908.22

07 - 08 = 35,736.84 + 61,285.98 / 2 = 20,961.41

Debtor’s Turnover Ratio

For year 04 – 05 =55,453.18

= 3.90 : 114,221.43

05 – 06 =75,443.84

= 6.92 : 110,901.40

06 – 07 =80,638.26

= 3.24 : 124,908.22

07 – 08 =83,093

= 3.96: 120,961.41

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 43/69

43

Interpretation:

The analysis of the debtor’s turnover ratio supplements the information regarding the

liquidity of one item of current asset of the firm. The ratio measure how rapidly debts are

collected. A higher ratio is indicator of shorter time lag between credit sales and cash

sales.

As we can see in the year 2007-08 debtor’s turnover ratio is highest. But for the year

2006-07 this ratio is 16.49: 1 which is also higher then the 2005-06 & 2004-05. So we

can say that company might face some problem in collecting the money in the year of

2005-06. But the result is quit well.

3.9

6.92

3.243.96

0

1

2

3

4

5

6

7

8

2004-05 2005-06 2006-07 2007-08

V a l u e

Year

Debtor Turn over Ratio

Ratio

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 44/69

44

(1.8) Debtors conversion Period:

Debtors Conversion Period =Debtors

x 360Credit Sales

Debtors

For year 04 – 05 = 7,723.20

05 – 06 = 15,252.95

06 – 07 = 35,736.84

07 – 08 = 61,285.98

Credit Sales = 60% 0f Total sale

For year 04 – 05 = 55,453.18

05 – 06 = 75,443.84

06 – 07 = 80,638.26

07 – 08 = 83,093

Debtors Conversion Period

For year 04 - 05 = 7723.20 x 360 = 50.14 Days55,453.18

05 - 06 =15252.95

x 360 = 72.78 Days75,443.84

06 - 07 =35736.84

x 360 = 159.54 Days80,638.26

07 – 08 =

61285.98

83,093 x 360 = 265.52 Days

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 45/69

45

Interpretation:

It measures how long it takes to collect amounts from debtors. The actual collection

period can be compared with the stated credit terms of the company. If it is longer than

those terms, then this indicates some insufficiency in the procedures for collection debts.

This ratio indicates the speed with which debtors/accounts receivable are being

collected. The higher the turnover ratio and the shorter the average collection period, the

better is the trade credit management and the better is the liquidity of debtors. On the

other hand, low turnover ratio and long collection period reflect delayed payment by

debtors. In general, therefore, short collection period (high turnover ratio) is preferable.

Here we can see that for the year 2007-08 debtors conversion period is 266

days, which is higher compare to others. But here we can see that for the last three years

company receive the money within their decided well specified period. Here for the year

2004-05 Debtors conversion period is less. But for the year 2005-06 debtor’s conversion

period increase by 23 days and than increase year by year. Company need to control

receivable management.

3044

96

159

0

20

40

60

80100

120

140

160

180

2004-05 2005-06 2006-07 2007-08

D a y s

Years

Debtor's conversion period

Days

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 46/69

46

{1.9} Inventory Turnover Ratio

Inventory Turnover Ratio =Cost of Goods Sold

Ave. Inventory

Cost of Goods Sold = Total Sales – Gross Profit

For year 04 -05 = 92,421.96 – 20,551.76 = 71,870.20

05 - 06 = 125,729.74 – 29,730.20 = 95,999.54

06 - 07 = 134,397.10 – 24,916.88 = 1,09,480.22

07 - 08 = 138,488.33 – 29,492.74 = 1,08,995.59

Ave. Inventories = (Opening stock of inventory + Closing stock of Inventory)/ 2

For year 04 - 05 = 2,691.57 + 5,519.91 / 2 = 4,105.74

05 - 06 = 5,519.91 + 6,376.20/ 2 = 5,948.05

06 - 07 = 6,376.20 + 14,696.98/ 2 = 10,536.59

07 - 08 = 14,696.98 + 11,020.20/ 2 = 12,858.59

Inventory Turnover Ratio

For year 04 – 05 =71,870.20

= 17.50 : 14,105.74

05 – 06 =95,999.54

= 16.14 : 15,948.05

06 – 07 =1,09,480.22

= 10.39 : 110,536.59

07 – 08 =1,08,995.59

= 8.48 : 112,858.59

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 47/69

47

Interpretation:

Inventory stock turnover ratio measure how quickly inventory is sold. It is a test of

efficient inventory management. To judge whether the ratio of a firm is satisfactory or

not, higher ratio shows efficient use of inventory.

As we can see from the graph that in the year 2004-05 ratio is 17.50: 1 which higher then

all the previous years, so we can say that inventory is converted into finished goods

highest in this year which indicate the highest efficient use of the inventory. But in case

of Kribhco the Ratio is decreased year by year.

17.516.14

10.398.48

02468

101214161820

2004-05 2005-06 2006-07 2007-08

V a l u e

Year

Inventory Turn over Ratio

Ratio

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 48/69

48

{1.10} Net profit ability Ratio

Net Profit Ability RatioNet profit

Total sales

Net profit for the year 04-05= 140.59

05-06=192.45

06-07=193.24

07-08=209.24

Sales for the year 04-05=924.22

05-06=1257.30

06-07=1343.97

07-08=1384.88

04-05

140.59

15.21924.22

05-06192.45

15.301257.30

06-07193.24

14.381343.97

07-08209.20

15.101384.88

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 49/69

49

Interpretation:

The net profit margin is indicate of managment’s ability to operate the business

with sufficient success not only to recover from revenues of the period, the cost of

merchandise or services, the expenses of operating the business and the cost of the

borrowed funds, but also to leave a margin of reasonable compensation to the owners for

providing their capital at risk. The ratio of net profit to sales essential expresses the cost

price effectiveness of the operation.

In 2004 company’s profit is 15% and after 4 also they maintain this profit

margin.so company has stable profit margin in this 4 years.

0

2

4

6

8

10

12

14

16

18

net profit

ratio ratio

ratio ratio

ratio year

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 50/69

50

{1.11} Gross profit ability Ratio

Gross Profit Ability RatioGross profit

Total sales

Gross profit for the year 04-05= 272.14

05-06=231.53

06-07=280.20

07-08=185.83

Sales for the year 04-05=924.22

05-06=1257.30

06-07=1343.97

07-08=1384.88

04-05272.14

29%924.22

05-06231.53

18%1257.30

06-07280.20

21%1343.97

07-08185.83

13%1384.88

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 51/69

51

Interpretation:

Gross profit is the result of the relationship between prices, sales volume and

costs. A change in the gross margin can be brought about by changes in any of these

factors. The gross margin represent the limit beyond which fall in sales prices are

outside the tolerance limit.

In this company in 2004-05 gross profit margin is 29%,its good for the

every company, but after one year its was fallen down to 18%. In 2007-08 margin

was very low compare to previous year.

0

5

10

15

20

25

30

35

1 2 3 4 5 6

Series3

Series2

Series1

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 52/69

52

(1.12)Return on capital employed

Return on capital employednet profit

Share capital

Net profit for the year 04-05= 140.59

05-06=192.45

06-07=193.24

07-08=209.20

Share capital=equity/ preference share capital+ discount on share

For the year 04-05= 2691.57+5519.91/2=4105.74

05-06=5519.91+6376.20/2=5948.05

06-07=6376.20+14698.98/2=10536.59

07-08=14696.98+11020.20/2=12858.59

04-05140.59

3.44105.74

05-06192.45

3.25948.05

06-07193.24

1.8

10536.59

07-08209.20

1.612858.59

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 53/69

53

Interpretation:

Here the profit related to the total capital employed. The term capital employed

refers to long term funds supplied by the creditors and owners of the firm. It can be

computed in two ways. First, It is equal to non-current liabilities plus owners of the firm.

The Higher the ratio, the more efficient is the use of capital employed.

in 2004-05 ratio of capital employed is 3.4% its better than other year. In

2007-08 ratio was decrease to 1.6%. its was half compare to 2004-05.

0

0.5

1

1.5

2

2.5

3

3.5

4

capital employed

ratio

year

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 54/69

54

(1.14) Inventory Conversion Period

Inventory Conversion Period =Ave. Inventory

x 360Cost of Good Sold

Ave. Inventories = (Opening stock of inventory + Closing stock of Inventory) / 2

For year 04 - 05 = (2691.57 + 5519.91 ) / 2 = 4105.74

05 – 06 = (5519.91 + 6376.20 ) / 2 = 5948.05

06 – 07 = (6376.20 + 14696.98 ) / 2 = 10536.59

07 – 08 = (14696.98 + 11020.20 ) / 2 = 12858.59

Cost of Sales = Total Sales – Gross Profit

For year 04 – 05 = 92421.96 – 20551.76 = 71870.20

05 – 06 = 125729.74 – 29730.20 = 95999.54

06 – 07 = 134397.10 – 24916.88 = 109480.22

07 – 08 = 138488.33 – 29492.74 = 108995.59

Inventory Conversion Period

For year 04 - 05 =4105.74

x 360 = 42.47 Days71870.20

05 - 06 =5948.05

x 360 = 34.65 Days95999.54

06 - 07 =10536.59

x 360 = 22.30 Days109480.22

07 - 08 =12858.59

x 360 = 20.57 Days108995.59

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 55/69

55

Interpretation:

Inventory conversion period means, time taken to convert raw material in to finished

goods to goods sold. It indicates how effectively and efficiently an inventory is

controlled. Lesser the inventory conversion period more efficient and effective use of

inventory.

Here we can see that for the year 2004-05 inventory conversion periods is 21 days which

is less then the rest of year. As we can see from the graph for the year 2007-08 inventory

conversion period is 42 days which is highest among the collected data. But as year

passing it increases. And we can find that it was maximum for the year 2007-08. So we

can say that they are able to substantially increase the inventory holding period from 21

days to 42 days. It may happen because the average inventory holding period has been

increase and also the cost of goods sold decrease.

0

5

10

15

2025

30

35

40

45

Year 2004-05 2005-06 2006-07 2007-08

Inventory Conversion period

Series1

Series2

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 56/69

56

(1.14) Raw material conversion period

Raw Material Conversion Period = Raw material Inventory ÷Raw Material consumption

360

Raw Material Inventories

For year 04 - 05 = 5,519.91

05 - 06 = 6,376.20

06 - 07 = 14,696.98

07 - 08 = 11,020.20

Raw Material Consumption

For year 04 - 05 = 39,150.61

05 - 06 = 47,231.80

06 - 07 = 47,310.96

07 - 08 = 65,404.97

Raw Material Conversion Period

For year 04 - 05 = 5,519.91 ÷39,150.61

= 50.75 Days360

05 - 06 = 6,376.20 ÷47,231.80

= 48.60 Days360

06 - 07 = 14,696.98 ÷

47,310.96

= 80.98 Days360

07 - 08 = 11,020.20 ÷65,404.97

= 60.65 Days360

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 57/69

57

Interpretation:

Raw material conversion period indicate the smoothness of the production or we can say

that how much time taken by the production to convert raw material in to finished good.

Smaller the raw material conversion period higher the efficiency of production.

In this case we can say that for the year of 2004-05 and 2005-06 raw material conversion

periods are 51 days and 49 days respectively which is lower then the others years. Lowest

conversion period is recorded for the year of 2004-05 because in this year raw material

inventories is less and raw material consumption is highest. But as we can see that in the

year 2006-07 & 2007-08 raw material inventories increase dramatically compare to

previous year and consumption per day was reduced so here raw material conversion

period is increase but we can control this by holding the inventories lower and increase

the raw material consumption per day.

Raw Material Conversion Period

50.75 48.6

111.83

60.65

0

20

40

60

80

100

120

2004- 05 2005-06 2006- 07 2007-08

Year

D a y s

Days

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 58/69

58

(1.15) work in process conversion period

Work in Process Conversion Period =Work in process

Inventory÷

Cost of Production

360

Work in Process Inventories

For year 04 - 05 = 36.96

05 - 06 = 40.94

06 - 07 = 46.13

07 - 08 = 61.77

Cost of Production

For year 04 - 05 = 61,732.20

05 - 06 = 1,03,463.13

06 - 07 = 1,28,279.30

07 - 08 = 1,48,885.75

Work in Process Conversion Period

For year 04 - 05 = 36.96 ÷61,732.20

= 0.22 Days360

05 - 06 = 40.94 ÷1,03,463.13

= 0.14 Days360

06 - 07 = 46.13 ÷ 1,28,279.30 = 0.13 Days

360

07 - 08 = 61.77 ÷1,48,885.75

= 0.15 Days360

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 59/69

59

Interpretation:

It indicates the work-in-process inventory (can say semi-finished good) converted in to

finished goods. Its also contain the production cost holding by it.

Here we can say that for the year 2004-05 due to high work in process inventory. Work in

process conversion period is low even though the cost of production is too high compare

to others. For next years it was decreased by day to day because, work in process

inventory is high compare to all previous year. Work in process conversion period can becontrolled by keeping work in process inventory low.

But in case of Kribhco the Work-in-process conversion periods are not a single day r say

it is minor because in Kribhco the duration in convert Semi finished goods to finished

goods is very less

Work in Process Conversion Period

0.22

0.14 0.13 0.15

0

0.05

0.1

0.15

0.2

0.25

2004- 05 2005- 06 2006- 07 2007- 08

Year

D a y s

Days

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 60/69

60

(1.16 )finished good conversion period

Finished Goods Conversion Period = Finished Goods Inventory ÷Cost of Goods Sold

360

Finished Goods Inventories

For year 04 - 05 = 5,548.10

05 - 06 = 6,399.69

06 - 07 = 14,650.85

07 - 08 = 10,958.76

Cost of Goods Sold

For year 04 - 05 = 58,870.52

05 - 06 = 1,02,611.14

06 - 07 = 1,02,028.14

07 - 08 = 1,52,577.84

Finished Goods Conversion Period

For year 04 - 05 = 5,548.10 ÷58,870.52

=33.93 Days360

05 - 06 = 6,399.69 ÷1,02,611.14

=22.45 Days360

06 - 07 = 14,650.85 ÷1,02,028.14

=43.94 Days360

07 - 08 = 10,958.76 ÷1,52,577.84

=25.85 Days360

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 61/69

61

Inventory Conversion =

Raw material Conversion period

+ Work in progress conversion period

+ Finish goods conversion period

For year 04 - 05 = 50.75 + 0.22 + 33.93 = 84.90 Days

05 - 06 = 48.60 + 0.14 + 22.45 = 71.19 Days

06 – 07 = 80.83 + 0.13 + 43.94 = 124.90 Days

07 - 08 = 60.65 + 0.15 + 25.85 = 86.65 Days

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 62/69

62

Debtors Conversion Period

For year 04 - 05 =7,723.20

x 360 =50.14 Days55,453.18

05 - 06 =15,252.84

x 360 = 72.78 Days75,443.84

06 - 07 =35,736.84

x 360 =159.54 Days80,638.26

07 - 08 = 61,285.98 x 360 =265.52 Days83,093

Gross Operating Cycle Period = Inventory Conversion Period +

Debtors’ conversion period

For year 04 - 05 = 351.65 + 50.14 = 106.4 Days

05 - 06 = 283.90 + 72.78 = 74.95 Days

06 - 07 = 144.19 + 159.54 = 57.22 Days

07 - 08 = 134.90 + 265.52 = 74.30 Days

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 63/69

63

Conclusion

And

Recommendations

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 64/69

64

Conclusion

From the study of ratio analysis, I have found that it is a very difficult task to

maintain ideal ratios in such a big organization. There are various factorsaffecting while managing ratio analysis like credit policy, inventory management

system , production cycle etc. But it is very important to manage it every

situation.

Fertilizer is a product whose price is highly controlled by Government. of India

Where by it may not be easily possible to increase the sales. Because the product

is sold as per Government of India allocated area. But efforts can surely be made

to reduce the cost factors. It is suggested that cost may highly be control through

effective budgeting and continuous analysis there off.

IFFCO playing a big role in deciding price factors, so kribhco can’t set its own

price and sale to directly to farmers

Kribhco’s current ratio is far more better than its ideal ratio, so in the future if

kribhco can borrow some money from the market, if It’s necessary.

Kribhco’s net profit is almost 15% every year its very good for the company

who’s main objective is to not earn a profit

In Kribhco all financial year have the double current assets compare to current

liabilities & all years satisfy sound financial condition requirement & more

liquidity of company indicate safe and sound position.

Inventory conversion period has continuously decreased from the year 2004-05 to

2007-08.

KRIBHCO have fix inventory management system.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 65/69

65

Liquidity position of a company can be ensured by the current ratio, it can be said

that if the ratio is 2: 1 then the company’s liquidity position is sound. In the year

2004-05 only the company liquidity position is good.

KRIBHCO strongly follows the credit policy but Receivable period is more

Compare to Creditor’s period.

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 66/69

66

Suggestions:

If KRIBHCO can directly contact to the farmers and sell them

without interfere of government or IFFCO. So it can increase its

profit margin

In case of KRIBHCO they need to change their credit policy, because in this case

we can see that the average creditor’s credit period is 30 days in raw materials and

10 days in case of spares. Where as debtor’s credit period (Bills receivable) is for

45 days. Here debtor’s credit period is more then creditor’s credit period which

need to be modified.

It is possible because KRIBHCO is the only company in SAARC countries who

are producing Urea and also have biggest Ammonia plant all over India. So we

can say they have the monopoly in urea and also they are the market leader in

case of Ammonia. So either they can increase the period of creditor’s credit

period or decease the debtor’s credit period, they can shorten collection period.

KRIBHCO have the 60:40 ratio of credit to cash sales which also can be modified

by taking advance payment from the customer and it can be used to maintain

liquidity for daily cash need raw material conversion period.

Net operating cycle period was increase which need to be maintain as low as

possible by reduce raw material conversion period, debtor’s conversion period ,

finish good conversion period ect. It helps to keep down the Net operating cycle

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 67/69

67

.

Limitations of Study:

During the study of this project some limitation I have found which are as below,

This research is based on the secondary data and during the study of working

capital there are so many data required from various department which was not

disclosed by the respective department, for example budget of the current

financial year.

Some approx data provided from the various departments for the calculation

purpose, e.g. Carrying cost, Ordering cost ECT, inter firm comparision which

were not calculated by the respective departments.

Available information for the study of ratio analysis is limited,

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 68/69

68

BIBLIOGRAPHY

Books

1) I.M.PANDEY- 2000,FINANCIAL MANAGEMENT, EIGHT EDITION

VIKASH PUBLISING HOUSE PRIVATE LTD.

2) R.S.N.PILLAI & BAGHAVATHI, – DEC. 2005, MANAGEMENT

ACCOUNTING THIRD EDITION S.CHAND PUBLICATION.

3) DONALD R. COOPER & PAMELA S. SCHINDLER ,BUSINESS

RESEARCH METHODS EIGHT EDITION , TATA Mc. GRAW-HILL

EDITION.

4) M Y KHAN, P K JAIN 2008,FINANCIAL MANAGEMENT FIFTH

EDITION-,TATA MCGRAW-HILL PUBLISHING COMPANY LIMITED.

Reports

Company Annual Report from 2004-05 to 2007-08.

Inventory statues report maintain by stores

Purchase Order records

Cash flow statements.

Websites

www.kribhco.net

www.kribhcoindia.com

www.kribhco.org.

WWW.KRIBHCOSURAT .COM

WWW.WIKIPEDIA.COM

www.final-yearproject.com | www.finalyearthesis.com

7/18/2019 FYP Ratio Analysis Krishak Bharat ASH

http://slidepdf.com/reader/full/fyp-ratio-analysis-krishak-bharat-ash-56d51c337daec 69/69

www.final-yearproject.com | www.finalyearthesis.com