fy 2012 annual report - treasury.gov · audit report oig-13-026 audit of the alcohol and tobacco...

TRANSCRIPT

Audit Report

OIG-13-026

Audit of the Alcohol and Tobacco Tax and Trade Bureau’s

Fiscal Years 2012 and 2011 Financial Statements

December 18, 2012

Office of Inspector General DEPARTMENT OF THE TREASURY

The Alcohol and Tobacco Tax and Trade Bureau (TTB) is committed to making its Web Site accessible to all TTB customers and staff and creates its Web pages in

accordance with the provisions of Section 508 of the Rehabilitation Act.

However, the attachment to our report, TTB's FY 2012 Annual Report, does not conform to the Standards of Section 508 of the Rehabilitation Act.

For a copy of TTB's FY 2012 Annual Report, see TTB's Annual Reports Web page and

for problems with accessibility, please contact TTB at [email protected].

Also see:

About TTB -Accessibility Policy Page

OFFICE OF INSPECTOR GENERAL

D E P AR T M E N T O F T H E T R E AS U R Y WASHINGTON, D.C. 20220

December 18, 2012 MEMORANDUM FOR JOHN J. MANFREDA, ADMINISTRATOR

ALCOHOL AND TOBACCO TAX AND TRADE BUREAU FROM: Michael Fitzgerald

Director, Financial Audits SUBJECT: Audit of the Alcohol and Tobacco Tax and Trade Bureau’s

Fiscal Years 2012 and 2011 Financial Statements

I am pleased to transmit the attached audited Alcohol and Tobacco Tax and Trade Bureau (TTB) financial statements for fiscal years 2012 and 2011. Under a contract monitored by the Office of Inspector General, KPMG LLP, an independent certified public accounting firm, performed an audit of TTB’s financial statements as of September 30, 2012 and 2011 and for the years then ended. The contract required that the audit be performed in accordance with generally accepted government auditing standards; applicable provisions of Office of Management and Budget Bulletin No. 07-04, Audit Requirements for Federal Financial Statements, as amended; and the GAO/PCIE Financial Audit Manual. The following reports, prepared by KPMG LLP, are incorporated in the attachment:

• Independent Auditors’ Report; • Independent Auditors’ Report on Internal Control Over Financial Reporting;

and • Independent Auditors’ Report on Compliance and Other Matters

In its audit, KPMG LLP found:

• the financial statements were fairly presented, in all material respects, in conformity with U.S. generally accepted accounting principles;

• no deficiencies in internal control over financial reporting that are considered material weaknesses; and

• no instances of reportable noncompliance with laws and regulations tested. In connection with the contract, we reviewed KPMG LLP’s reports and related documentation and inquired of its representatives. Our review, as differentiated from an audit performed in accordance with generally accepted government auditing standards, was not intended to enable us to express, and we do not express, an opinion on TTB’s financial statements or conclusions about the

effectiveness of internal control or compliance with laws and regulations. KPMG LLP is responsible for the attached auditors’ reports dated December 14, 2012 and the conclusions expressed in the reports. However, our review disclosed no instances where KPMG LLP did not comply, in all material respects, with generally accepted government auditing standards. Should you have any questions, please contact me at (202) 927-5789, or a member of your staff may contact Catherine Yi, Manager, Financial Audits, at (202) 927-5591. Attachment

a

Alcohol and Tobacco Tax and Trade Bureau

FY 2012 Annual Report

a

Table of Contents

Introduction ............................................................................................................................................. i Message from the Administrator .............................................................................................. iii Vision, Mission, and Values ......................................................................................................... v TTB Strategic Goals and Objectives ...................................................................................... vi TTB Office Locations .................................................................................................................... vii

Part I: Management’s Discussion and Analysis Profile of a Bureau .................................................................................................................................. 1 Performance Summary ...................................................................................................................... 34 Financial Summary .............................................................................................................................. 44

FY 2012 Bureau Budget ..................................................................................................................... 46 Bureau Challenges ............................................................................................................................... 47 Part II: Program Performance Results Performance Overview ...................................................................................................................... 49 Summary of Collect the Revenue Performance ........................................................................ 50 Summary of Protect the Public Performance ............................................................................ 55 Summary of Management and Organizational Excellence Performance ....................... 59

TTB 2012 Annual Report

b

Message from the Chief Financial Officer ........................................................................ 67 Part III: Financial Results, Position, Condition and Auditors’ Reports Budget Highlights by Fund Account ............................................................................................. 69 Linking Budget to Program Spending .......................................................................................... 70 Systems and Controls ......................................................................................................................... 74 Financial Statements, Accompanying Notes and Supplemental Information .............. 78 Independent Auditors’ Reports ............................................................................................................. 79

Financial Statements .................................................................................................................................. 87 Notes to the Financial Statements ........................................................................................................ 93 Required Supplementary Information (Unaudited) .................................................................. 113 Other Accompanying Information (Unaudited) ........................................................................... 115

Part IV: Appendices Principal Officers of TTB ................................................................................................................. 121 TTB Organization Chart ................................................................................................................... 122 Connecting the Treasury and TTB Strategic Plans ............................................................... 123

TTB 2012 Annual Report

i

Introduction Supporting the Nation’s economic recovery and ongoing prosperity is at the core of the work performed by the Alcohol and Tobacco Tax and Trade Bureau (TTB). The Bureau’s role in permitting and regulating the alcohol and tobacco industries ensures a fair marketplace, enhanced trade opportunities, and a level playing field for those engaged in the manufacture and trade of these commodities. As the Nation’s excise tax authority on alcohol and tobacco products, TTB also ensures fair and effective tax administration and enforcement in a globalized marketplace.

As the country continues to recover from the global recession, TTB is focused on supporting the business community it serves by reducing the burden of compliance and addressing the illicit trade that undermines their legitimate operations. In the 10 years since TTB’s inception, the industries that the Bureau regulates have continued to expand, evidenced by the 60 percent growth in the permit applications and registrations that TTB receives. Annual tax revenue from the alcohol, tobacco, firearms, and ammunition industries totals more than $23 billion annually, making TTB the third largest tax collection agency in the Federal government. The revenue that TTB collects on these products goes toward funding national priorities.

Maintaining a responsive and effective organization requires Government agencies to look at their business processes and operations anew. TTB, like the businesses its regulates, must continuously look for ways to effect its mandates more efficiently and effectively, leveraging limited resources in smarter and more innovative ways to ensure that the investments made in its mission show a return. Within its FY 2012 Annual Report, TTB combines program performance and financial data to demonstrate how effectively the Bureau translates its program dollars into quality service, responsible management practices, consumer protection, and increased tax revenue.

Each year, as part of the performance and budget cycle, TTB issues this report to inform its stakeholders of the Bureau’s accomplishments and explain any challenges. The report defines the Bureau’s mission, strategic goals, and major programs, and summarizes its progress in meeting its objectives, as stated in the TTB strategic plan. TTB also presents financial information that depicts how TTB expended its budget according to its major programs, and accounted for tax collections from the alcohol, tobacco, firearms, and ammunition industries.

This report presents this information in four parts:

Part I – Management’s Discussion and Analysis. This section provides an overview of the Bureau including its mission and programs, highlights of program and financial operations, and a summary of TTB’s program performance.

Part II – Program Performance Results. This section provides a discussion of results achieved for each performance measure related to the Collect the Revenue and Protect the Public strategic goals and an overview of the Bureau’s accomplishments under its Management and Organizational Excellence goal.

TTB 2012 Annual Report

ii

Part III – Financial Results, Position, Condition and Auditors’ Reports. In this section, TTB presents audited balance sheets, statements of net cost, changes in net position, budgetary resources, and custodial activity as of and for the years ending September 30, 2012, and September 30, 2011, and the Independent Auditors’ Report on these financial statements. Also included is a report on the Bureau’s internal control over financial reporting and a report on TTB’s compliance with laws and regulations. This report section also includes a discussion of budget activities for each of the Bureau’s seven major programs and supplemental information, such as a history of Federal excise tax collections for the past decade.

Part IV – Appendices. This section includes a listing of TTB principal officers, an organization chart, and strategic plan information that demonstrates the relationship between TTB’s plan and the overall Department of the Treasury’s mission and goals.

TTB 2012 Annual Report

iii

Message from the Administrator Formed by the Homeland Security Act of 2002, TTB has now completed a generation of its existence and, in that time, has distinguished itself as an innovative agency in the Federal government. Effective application of technology and responsive service to our customer and stakeholders were the hallmarks of our first generation as a Bureau. We will build on these foundations in our efforts to create TTB 2.0—a bureau with a leaner, smarter business model that is driven by data, informed by risk, and focused on improving mission results in both its revenue and trade facilitation roles.

As a tax agency, TTB plays an important role in supporting the financial security of the Nation. TTB has transformed its enforcement program in the

past year, refining its approach through advanced risk modeling techniques and by breaking down organizational silos to draw on the complementary skill sets of not only TTB’s auditors and investigators, but also our regulatory and trade specialists, chemists, and data scientists. Through the integration of expertise across the Bureau, TTB has improved its ability to identify illegal activity and efficiently pursue enforcement actions. As part of this approach, in FY 2012, TTB deployed joint forensic audit and investigation teams to detect and pursue fraudulent activity in the alcohol and tobacco trade. Working together with other TTB divisions, these teams pursue major cases with nationwide impact to augment our risk-based enforcement plan, enabling TTB to further focus our limited resources on high-risk areas for revenue loss. The TTB enforcement model produces one of the best returns of any tax collection agency, with the Bureau bringing in $449 for every $1 spent on tax collection. In FY 2012, TTB collections on alcohol, tobacco, and firearms products totaled $23.4 billion.

Enforcing the tax code also requires that TTB address tax evasion and the illicit trade in alcohol and tobacco products. The diversion of these products outside legal commercial channels not only represents potentially billions of dollars in revenue loss but also undermines the lawful business activity of taxpaying industry members and provides a well-established source of funding for criminal enterprises. The clandestine nature of this activity makes it difficult to accurately measure the loss in Federal tax receipts; however, in any case where the intrinsic value of a product is dwarfed by its tax value, there is incentive to evade the tax to gain an illegal profit. The recent tobacco tax rate increase, which tripled the tax on cigarettes, serves to enhance the potential for illegal gains.

Addressing this revenue threat requires a visible enforcement presence. In FY 2012, TTB continued its criminal enforcement program, using a $2 million annual appropriation from Congress to acquire and leverage existing law enforcement resources within the Department of the Treasury to enforce the Bureau’s criminal jurisdiction. Contracting for agent services has ensured that the investment made by Congress in this criminal enforcement initiative was used to maximum effect, minimizing overhead costs and avoiding duplicative infrastructure.

In just 16 months of active investigations, TTB has opened 48 criminal cases that identified nearly $340 million in tax liabilities. We believe these results are artificially low, both because of the limitations placed on our investigations by the short-term spending authority, and because it does not account for the deterrent impact

TTB 2012 Annual Report

iv

of our law enforcement presence. Looking ahead, TTB will continue to rely on the successful relationships we have established with law enforcement partners over the past two years to enforce our criminal jurisdiction in the coming year.

As part of its renewed strategic vision, TTB will continue to focus on improving its business results in two of its core service areas–permit and label applications–by enhancing the electronic filing capabilities for industry and evaluating proposals to streamline TTB’s processing work without compromising our statutory mandates. Applications for permits continue to rise, increasing a staggering 33 percent in FY 2012, and TTB is making strategic investments in e-Gov solutions to avoid degradation to the level of service provided to the businesses applying for a Federal permit. Delays in issuing permits impede the Nation’s economic recovery, as the new businesses that TTB authorizes to operate are predominantly small businesses that contribute to job opportunities locally and to America’s competitiveness globally.

TTB is also pursuing long-term solutions to address the continued growth in alcohol beverage labeling applications, which are well above 150,000 annually. Technology enhancements alone will not entirely address the strain on TTB resources, which is why we are working with industry to assess opportunities to streamline this critical line of business to prevent costly delays in receiving TTB’s approval. Such delays negatively impact businesses, which must have label approval prior to bottling or introducing their products into domestic commerce. This requires that we reshape our label approval program to facilitate the prompt introduction of products into commerce while maintaining our responsibility to ensure that consumers and industry competitors are protected from deceptive or other illegal labels. Part of our approach requires that we update existing regulations so that they are as clear as possible, and TTB plans to initiate rulemaking in this area in FY 2013.

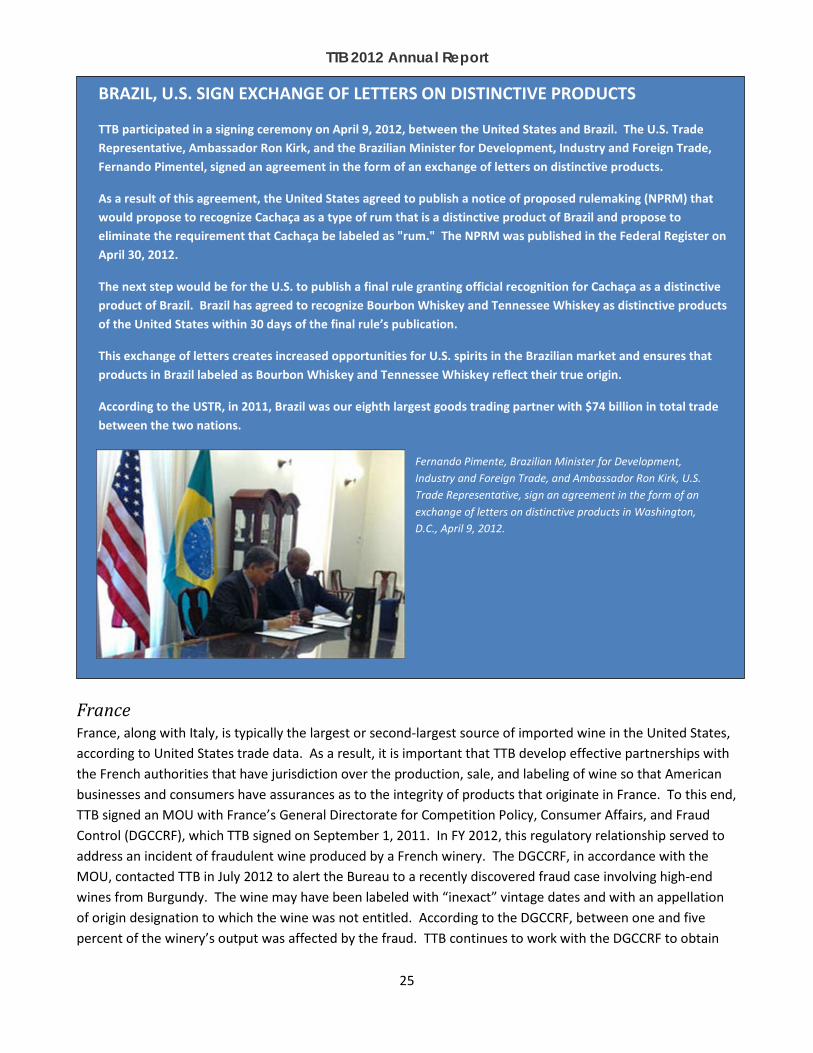

TTB also plays an important role in the facilitation of the global alcohol trade. The trade in alcohol beverages continues to offer significant opportunities for U.S. businesses in overseas markets, with the export value of wine, spirits, and malt beverages totaling close to $3 billion in FY 2011, a 38 percent increase from 2007. TTB expanded our global network of alcohol and tobacco regulators in FY 2012 by signing a memorandum of understanding with Brazil’s National Health Surveillance Agency, a vital ally in addressing the shared challenge of tobacco diversion. TTB continues to engage with regulators from Canada, China, the European Union, France, Italy, Mexico, and the new world wine producers of the World Wine Trade Group—all of which offer important export markets for U.S. producers—through its formal international agreements. These agreements ensure that markets remain open for opportunities for domestic businesses and that illegal activity in international trade is addressed promptly.

As shown in the pages that follow, we have made significant progress over the past year in implementing strategic changes that will improve the Bureau’s efficiency without compromising mission results. The path we are on will help ensure that we are effective in accomplishing our mandates, meeting customer expectations, and ensuring that we maximize the dollars entrusted to us.

The Bureau has validated the accuracy, completeness, and reliability of the performance data contained in this report.

John J. Manfreda Administrator

TTB 2012 Annual Report

v

Vision, Mission, and Values

Vision Our vision is to maintain an organization of people who value each other and who treat each other and their customers with the respect that they deserve. We intend to uphold the laws, for which we are responsible, in a fair, equitable, and appropriate manner, affording all an opportunity to have their opinions heard without prejudice. We intend to carry out our mission without imposing inappropriate or undue burden on those from which TTB collects taxes and those TTB regulates.

Mission Collect the Federal excise taxes on alcohol, tobacco, firearms, and ammunition, and assure compliance with Federal tobacco permitting and alcohol permitting, labeling, and marketing requirements to protect consumers.

Values We value each other and those we serve. This Bureau:

• Upholds the highest standards of excellence and integrity;

• Provides quality service and promotes strong external partnerships;

• Develops a diverse, innovative, and well-trained workforce in order to achieve our goals; and

• Embraces learning and change in order to meet the challenges of the future.

TTB 2012 Annual Report

vi

TTB Strategic Goals and Objectives

Strategic Goal: Collect the Revenue Industry remits the proper Federal tax on alcohol, tobacco, firearms, and ammunition products

Tax Verification and Validation. Assure voluntary compliance in the timely and accurate remittance of tax payments

Civil and Criminal Enforcement. Detect and address excise tax evasion and other criminal violations of the Internal Revenue Code in the industries TTB regulates

Strategic Goal: Protect the Public Alcohol and tobacco industry operators meet permit qualifications, and alcohol beverage products comply with Federal production, labeling, and marketing requirements

Business Integrity. Assure that only qualified persons and business entities operate within the industries TTB regulates

Product Integrity. Assure that alcohol beverage products comply with Federal production, labeling, and advertising requirements

Market Integrity. Assure fair trade practices throughout the alcohol beverage marketplace

Strategic Goal: Management and Organizational Excellence Effectively managed resources and human capital for maximum performance, efficiency, and program results

Human Capital Management. Maintain a qualified, engaged, and satisfied workforce

Technology Solutions. Deliver effective, streamlined, and flexible IT solutions that add value and support program performance

Finance and Performance Results. Facilitate strategic management and financial accountability through the delivery of timely and reliable financial and performance information

TTB 2012 Annual Report

vii

TTB Office Locations

Total TTB Permittees 61,684

TTB Permittees by Industry Type

Alcohol 96.7%

Tobacco 1.5%

Firearms 1.8%

TTB Permittees Not Subject to Tax 48,046

TTB Permittees Subject to Tax 13,643

TTB Permittes Who Filed and Paid Taxes 8,533

Industry at a Glance

Employees 496

Office Locations * 17

Budget Authority $99.9 Million

Revenue Collected $23.4 Billion

Original and Amended Permits Processed 27,363

Certificate of Label Applications Received 152,741

*TTB has some offices co-located in larger cities.

TTB at a Glance

TTB 2012 Annual Report

viii

Page left intentionally blank.

TTB 2012 Annual Report

1

PART I Management’s Discussion and AnalysisProfile of a Bureau The mission of the Alcohol and Tobacco Tax and Trade Bureau (TTB) is to collect the Federal taxes on alcohol, tobacco, firearms, and ammunition products, protect consumers from unsafe or improperly labeled alcohol beverage products, and prevent unfair or unlawful trade of alcohol and tobacco products. TTB’s diverse mission, and its position as a bureau of the Department of the Treasury, means that TTB must strike a balance between its tax and regulatory functions and its role in facilitating fair and robust economic activity in the alcohol and tobacco trades.

TTB is staffed with approximately 500 employees, most of whom report to either the headquarters office in Washington, D.C., or the National Revenue Center in Cincinnati, Ohio. For its auditors, investigators, and agents to most effectively operate in the field, TTB also has 10 offices in cities across the U.S., as well as Puerto Rico. In recent years, TTB has reduced its physical footprint by converting its auditors and investigators to full-time telework positions; however, the small, strategically located offices that TTB has maintained place the Bureau in close proximity to centers of trade and industry activity, and provide effective launch points for TTB’s investigative teams. Additionally, the Bureau has two laboratory facilities in Walnut Creek, California and Beltsville, Maryland. See Part IV of this report for a chart outlining the TTB organizational structure.

The Bureau was formed in January 2003, under the Homeland Security Act of 2002, but its history began more than 200 years ago as one of the earliest Federal tax collection agencies. Today, TTB operates under the authorities of the Internal Revenue Code of 1986 (IRC)1 and the Federal Alcohol Administration Act (FAA Act),2 including the Alcoholic Beverage Labeling Act of 1988 (ABLA)3 and the Webb-Kenyon Act. 4 These laws put in place strict requirements and controls related to alcohol and tobacco products and place restrictions on who can make, sell, and distribute these commodities.

In essence, TTB administers its jurisdiction according to two core mission areas—“Collect the Revenue” and “Protect the Public”—both of which serve to support the Nation’s economic recovery by ensuring that the Federal government has the cash resources needed to fund the Nation’s priorities and that lawful U.S. businesses are competitive and thriving in the global marketplace.

a137

1 Chapters 51 and 52 of the IRC provide for excise taxation and authorize operations of alcohol and tobacco producers and related industries, and IRC sections 4181 and 4182 provide for excise taxes for firearms and ammunition. 2 The FAA Act provides for regulation of those engaged in the alcohol beverage industry and for protection of consumers through certain requirements regarding the labeling and advertising of alcohol beverages. The FAA Act also includes provisions to preclude unfair trade practices that serve as barriers to competition and trade in the U.S. marketplace. 3 The ABLA mandates that a Government warning statement appear on all alcohol beverages offered for sale or distribution in the United States. 4 The Webb-Kenyon Act prohibits the shipment of alcohol beverages into a State in violation of the receiving State’s laws.

TTB 2012 Annual Report

2

7,200,000

7,300,000

7,400,000

7,500,000

7,600,000

7,700,000

7,800,000

7,900,000

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012

Dol

lars

in T

hous

ands

Alcohol Excise Tax Collections Trend

Alcohol FET Collections

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012

Alcohol Permits Trend

Alcohol Original Permits Issued

Alcohol Industry Snapshot

Tobacco Industry Snapshot

Firearms & Ammunition Industry Snapshot

02,000,0004,000,0006,000,0008,000,000

10,000,00012,000,00014,000,00016,000,00018,000,000

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012

Dol

lars

in T

hous

ands

Tobacco Excise Tax Collections Trend

Tobacco Collections

0

50

100

150

200

250

300

350

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012

Tobacco Permits Trend

Tobacco Original Permits Issued

0

100,000

200,000

300,000

400,000

500,000

600,000

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012

Dol

lars

in T

hous

ands

FAET Collections Trend

Firearms & Ammunition Excise Tax Collections

05

1015202530354045

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012

Firearms & Ammunition Registrations Trend

Firearms & Ammunition Registrations Issued

TTB 2012 Annual Report

3

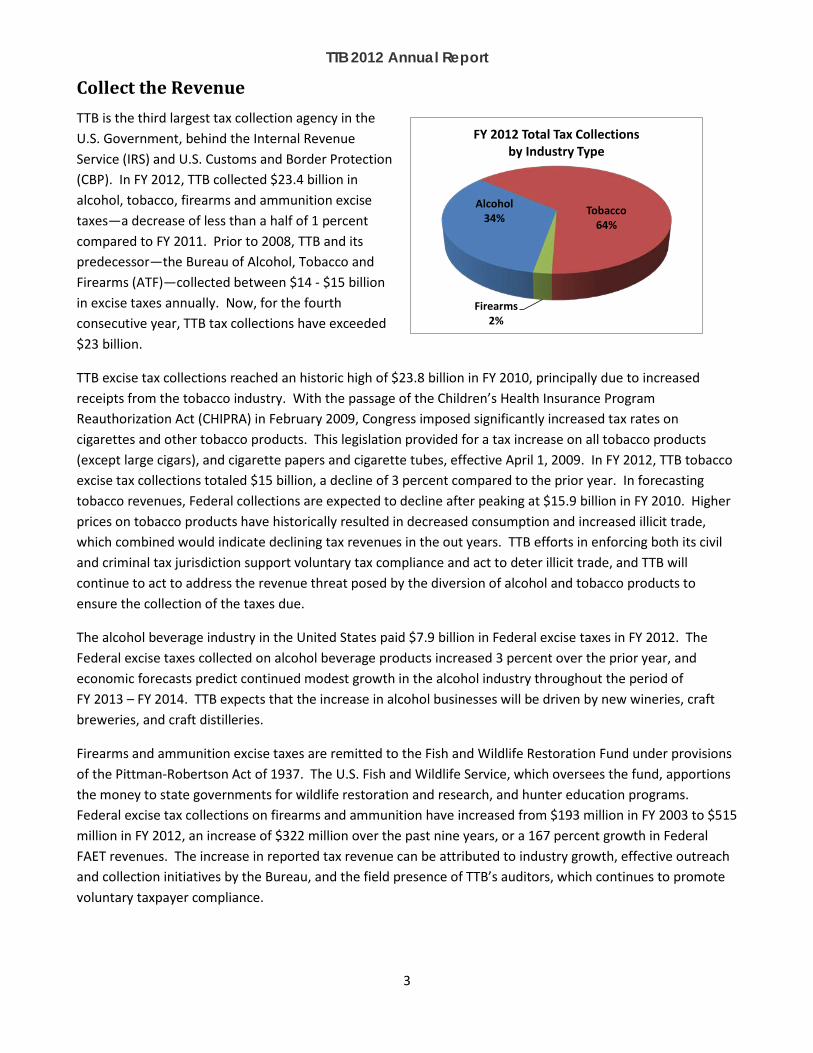

Collect the Revenue TTB is the third largest tax collection agency in the U.S. Government, behind the Internal Revenue Service (IRS) and U.S. Customs and Border Protection (CBP). In FY 2012, TTB collected $23.4 billion in alcohol, tobacco, firearms and ammunition excise taxes—a decrease of less than a half of 1 percent compared to FY 2011. Prior to 2008, TTB and its predecessor—the Bureau of Alcohol, Tobacco and Firearms (ATF)—collected between $14 - $15 billion in excise taxes annually. Now, for the fourth consecutive year, TTB tax collections have exceeded $23 billion.

TTB excise tax collections reached an historic high of $23.8 billion in FY 2010, principally due to increased receipts from the tobacco industry. With the passage of the Children’s Health Insurance Program Reauthorization Act (CHIPRA) in February 2009, Congress imposed significantly increased tax rates on cigarettes and other tobacco products. This legislation provided for a tax increase on all tobacco products (except large cigars), and cigarette papers and cigarette tubes, effective April 1, 2009. In FY 2012, TTB tobacco excise tax collections totaled $15 billion, a decline of 3 percent compared to the prior year. In forecasting tobacco revenues, Federal collections are expected to decline after peaking at $15.9 billion in FY 2010. Higher prices on tobacco products have historically resulted in decreased consumption and increased illicit trade, which combined would indicate declining tax revenues in the out years. TTB efforts in enforcing both its civil and criminal tax jurisdiction support voluntary tax compliance and act to deter illicit trade, and TTB will continue to act to address the revenue threat posed by the diversion of alcohol and tobacco products to ensure the collection of the taxes due.

The alcohol beverage industry in the United States paid $7.9 billion in Federal excise taxes in FY 2012. The Federal excise taxes collected on alcohol beverage products increased 3 percent over the prior year, and economic forecasts predict continued modest growth in the alcohol industry throughout the period of FY 2013 – FY 2014. TTB expects that the increase in alcohol businesses will be driven by new wineries, craft breweries, and craft distilleries.

Firearms and ammunition excise taxes are remitted to the Fish and Wildlife Restoration Fund under provisions of the Pittman-Robertson Act of 1937. The U.S. Fish and Wildlife Service, which oversees the fund, apportions the money to state governments for wildlife restoration and research, and hunter education programs. Federal excise tax collections on firearms and ammunition have increased from $193 million in FY 2003 to $515 million in FY 2012, an increase of $322 million over the past nine years, or a 167 percent growth in Federal FAET revenues. The increase in reported tax revenue can be attributed to industry growth, effective outreach and collection initiatives by the Bureau, and the field presence of TTB’s auditors, which continues to promote voluntary taxpayer compliance.

Alcohol34%

Tobacco64%

Firearms2%

FY 2012 Total Tax Collections by Industry Type

TTB 2012 Annual Report

4

Civil Tax Enforcement

Tax Classification

The tax rate on alcohol and tobacco products is dependent on a variety of factors, including product type (i.e., wine, spirits, or malt beverage) as well as characteristics of the products themselves, such as composition and weight. A critical first step in tax enforcement is the assignment of a tax class to alcohol and tobacco products based on Federal regulatory standards.

For alcohol beverages, classification requires that TTB review the formula of certain products before they enter the market. For example, if an examination of the formula reveals that an imported sake, which is made from fermented rice and is classified and taxed as wine, contains added spirits, then the product is then classified and taxed as a distilled spirits product. This type of formula review, known as a pre-import approval, can have significant tax implications, as wine is subject to a lower tax rate than spirits products.

TTB also conducts marketplace product evaluations to check for proper tax classification. As an example, TTB evaluates samples of products marketed as large cigars to verify that the products are large cigars rather than cigarettes or small cigars, as the tax rates differ markedly between these products. In classifying such a product for tax purposes, TTB evaluates the product’s wrapper, the type of tobacco used in the filler, the product’s packaging and labeling, and its weight to verify that the product meets the statutory criteria for a large cigar.

Shifting Market Trends due to Tax Rates

The recent increase in the Federal excise tax rate on cigarettes and other tobacco products highlights the importance of TTB’s tax classification activities. In reaction to CHIPRA, some manufacturers took advantage of large disparities in the tax rates, shifting their production toward products that carry lower tax burdens by manipulating the character and composition of their products; in some cases, manufacturers and importers intentionally misclassified the identity and classification of their products to evade taxes. These deliberate manipulations, motivated by the desire to avoid taxes and not by market demand, effectively undermine the dual policy objectives of Federal and state governments when they raise excise tax rates: increased revenues and decreased tobacco use.

Since the excise taxes on cigarettes and other tobacco products increased in 2009, TTB has identified and monitored significant market shifts toward lower-taxed tobacco products by manufacturers and price-sensitive consumers. Prior to CHIPRA, TTB faced enforcement challenges due to the disparate tax rates on cigarettes and small cigars, and the ambiguous statutory criteria for these products. The law created parity in the excise tax rates for these two products, thus resolving this long-time tax enforcement challenge. However, CHIPRA created large disparities in tax rates for other tobacco products, thus presenting new challenges for TTB in appropriately classifying and collecting the taxes due on these products.

An important trend is the shift in the volume of small cigars to large cigars. Large cigars are the only tobacco product for which the excise tax is based on the manufacturer or importer’s sale price; all other tobacco products are taxed at a flat rate based either on the number of units or the weight of the product. The ad valorum tax on large cigars can result in significantly lower tax rates on these products, depending on the sale

TTB 2012 Annual Report

5

price of the cigar. As a result, since the tax increase on small cigars, TTB has found that manufacturers and importers are increasing the weight of products that TTB had previously evaluated and determined to be small cigars prior to CHIPRA so that they meet the statutory definition of a large cigar.

A second trend is the stark shift in pipe tobacco and roll-your-own (RYO) tobacco products, which creates another enforcement challenge due to the lack of clear standards to differentiate the two products.5 Prior to CHIPRA, the tax rates on pipe tobacco and RYO tobacco were the same at just under $1.10 per pound. As a result of CHIPRA, the tax on pipe tobacco was increased to just over $2.83 per pound, while the tax on RYO tobacco was increased to $24.78 per pound. This significant tax difference resulted in a dramatic increase in the volume of pipe tobacco reported as removed for sale or distribution by domestic manufacturers, with an equally dramatic decrease in the amount of RYO tobacco reported as removed.

Because of the lack of clear standards in the tax code to differentiate pipe tobacco from RYO tobacco, and the consequent potential for misclassification and erroneous tax payment on these products, TTB has undertaken rulemaking on the types of objective standards that would provide a basis for differentiating between these two products for tax purposes. At the same time, the TTB Tobacco Laboratory has been evaluating proposed methods and standards, and undertaking research to develop methods and standards, in support of this rulemaking. The goal is to set forth objective criteria, based on physical characteristics of the products, that distinguish between pipe tobacco and RYO for tax purposes. TTB intends to publish subsequent rulemaking in this area.

e137

5 Under the IRC, pipe tobacco is any tobacco which, because of its appearance, type, packaging, or labeling, is suitable for use and likely to be offered to, or purchased by, consumers as tobacco to be smoked in a pipe. RYO tobacco is defined as any tobacco which, because of its appearance, type, packaging, or labeling, is suitable for use and likely to be offered to, or purchased by, consumers as tobacco for making cigarettes or cigars, or for use as wrappers of cigars or cigarettes.

EFFECT OF CHIPRA ON TAXABLE REMOVALS OF TOBACCO PRODUCTS

Payment of excise tax is due from tobacco manufacturers at the time the product is removed for sale from the manufacturing premises. Since the enactment of CHIPRA, significant shifts in the tobacco products industry developed, particularly in the markets for small and large cigars and RYO and pipe tobacco. An independent review by the Government Accountability Office (GAO) of shifts in tobacco product removals since the tobacco tax rate increase estimates that Federal revenue losses due to market shifts from RYO to pipe tobacco and from small to large cigars could exceed $1.1 billion for the period April 2009 through September 2011.

0%20%40%60%80%

100%

PRE-CHIPRA POST-CHIPRA4/2009 -

12/2009 (9MONTHS)

(Cumulative)

POST-CHIPRATHROUGH CY

2010 (21MONTHS)

(Cumulative)

POST-CHIPRATHROUGH CY

2011 (33MONTHS)

(Cumulative)

POST-CHIPRATHROUGH7/2012 (40MONTHS)

(Cumulative)

Post CHIPRA Market ShiftPipe vs. RYO Tobacco

Pipe Roll Your Own (RYO)

0%20%40%60%80%

100%

PRE-CHIPRA POST-CHIPRA4/2009 -

12/2009 (9MONTHS)

(Cumulative)

POST-CHIPRATHROUGH CY

2010 (21MONTHS)

(Cumulative)

POST-CHIPRATHROUGH CY

2011 (33MONTHS)

(Cumulative)

POST-CHIPRATHROUGH7/2012 (40MONTHS)

(Cumulative)

Post CHIPRA Market ShiftLarge vs. Small Cigars

Small Cigars Large Cigars

TTB 2012 Annual Report

6

Congress specifically recognized that the differing tax rates applicable to tobacco products can have consequences on both revenue and public health in its passage of the Family Smoking Prevention and Tobacco Control Act (P.L. 111-31), which directed the Government Accountability Office (GAO) to study the cross-border trade of tobacco products. As part of this requirement, GAO reviewed the market shifts in smoking tobacco products since CHIPRA, examined the impact of those market shifts on Federal revenue, and evaluated TTB’s actions to respond. In its FY 2012 report, GAO estimated that Federal revenue losses due to market shifts from RYO to pipe tobacco and from small to large cigars range from about $615 million to $1.1 billion for the period April 2009 through September 2011. GAO recommended that Congress consider equalizing tax rates on RYO and pipe tobacco and, in consultation with the Department of the Treasury, consider options for reducing tax avoidance due to tax differentials between small and large cigars. GAO also recognized that TTB has taken steps to respond to these market shifts, including its efforts to differentiate between RYO and pipe tobacco for tax collection purposes, but acknowledged that TTB has limited options.

Addressing Revenue Threat from Roll-Your-Own Cigarette Machines

The tax differential on certain tobacco products also contributed to the proliferation of cigarette manufacturing machines at retail establishments. Following the enactment of CHIPRA, TTB began receiving reports of retail establishments maintaining commercial cigarette-making machines on their premises for customers to use in the manufacture of cigarettes. TTB also received reports that customers were using pipe tobacco, which is subject to a Federal tax rate much lower than that applicable to RYO, to produce lower cost cigarettes. TTB also was approached by individuals interested in purchasing untaxed processed tobacco and reselling that tobacco to retailers for use in the machines.

TTB issued a ruling in September 2010 that defined retailers that engage in this type of activity as manufacturers of tobacco products. The courts enjoined TTB from taking enforcement action until, in July 2012, Congress enacted the Moving Ahead for Progress in the 21st Century Act (H.R. 4348, also known as "MAP-21"), which definitively addressed the legal status of retailers that provide cigarette-making machines to customers. Under MAP-21, any person who for commercial purposes makes available for consumer use a machine capable of making tobacco products (including cigarettes) is a manufacturer of tobacco products under the IRC and, as such, falls under the jurisdiction of TTB. Such manufacturers are required to apply for a permit from TTB, as well as pay Federal excise taxes and comply with other TTB regulatory requirements. Further, in October 2012, TTB issued public guidance that defines a manufacturer of tobacco products and outlines the statutory and regulatory requirements for manufacturers of tobacco products. In FY 2013, TTB will continue its enforcement efforts in relation to the 1,300 cigarette-making machine operating locations identified to date to ensure compliance with TTB permitting and tax requirements.

Classifying Non-Traditional Tobacco Products

In its tax role, TTB also must determine the tax classification of new forms of tobacco products. Some of these new products are a result of market innovation while others are products that are common in other countries but new to the United States. In FY 2012, TTB evaluated a range of non-traditional products, such as a Middle Eastern tobacco product called “dokha” and products labeled as “tobacco-free” tobacco product alternatives.

An emerging product in the United States, dokha appears to be a Middle Eastern pipe tobacco. This and other non-traditional tobacco products present a tax enforcement challenge, as they may be undeclared as tobacco products upon import or misclassified by the importer in order to evade the higher rate of tax. TTB is working

TTB 2012 Annual Report

7

with its law enforcement partners at U.S. Customs and Border Protection (CBP) to ensure that this new product is recognized and taxpaid upon import.

TTB also is seeing an increasing number of products labeled as “tobacco-free” produced or imported by companies that TTB regulates. One important initial factor for evaluating these products for tax purposes is determining whether the products actually contain tobacco. If the products do not contain tobacco, the tax would not apply. The TTB Tobacco Laboratory tests these unconventional products to confirm the presence of tobacco. States also rely on TTB for these tobacco verification determinations in their tobacco regulatory and tax enforcement efforts.

As a global authority in the technical analysis of tobacco products, TTB’s scientific expertise is sought after by its international law enforcement partners. In FY 2012, the TTB Tobacco Laboratory provided technical assistance to the Royal Canadian Mounted Police (RCMP) in the investigation and subsequent prosecution of a tobacco excise tax case in Canada. Specifically, the RCMP requested that TTB analyze and confirm the presence of tobacco in six hookah-type products that displayed “No Nicotine, No Tobacco” claims on the packages. TTB’s Tobacco Laboratory has been a government leader in the development of methods and protocols to identify chemical markers unique to tobacco leaf, and was identified by law enforcement officials in this case as the only agency that could perform a “tobacco-free” confirmation analysis.

In the year ahead, TTB will continue to share its scientific and regulatory expertise with other state, Federal, and international agencies to review new and emerging non-traditional tobacco products in the United States market and ensure that they are properly classified and taxpaid. In this vein, TTB also will continue to serve in its leadership role in the North American Tobacco Regulatory Laboratory Network technical forum, organized by TTB chemists and held for the first time in April 2012 at the TTB National Laboratory Center in Beltsville, Maryland. Forty scientists and regulators representing 11 Federal agencies from the United States, Canada, and Mexico participated in the forum to discuss tobacco science in the context of tobacco regulation. The forum establishes a network of laboratories to exchange information on technical regulatory matters, collaborate on testing protocols, develop analytical methods, and build a partnership to proactively address emerging issues on tobacco.

Tax Verification

In effecting its revenue mission, TTB uses a coordinated enforcement approach to verify that industry members remit the excise taxes due on the alcohol, tobacco, firearms, and ammunition products sold to U.S. consumers. The Bureau’s auditors, investigators, agents, chemists, and tax and regulatory specialists work

John Shifflet, Chemist in TTB’s Tobacco Laboratory, speaking to producers and industry representatives during a tour of TTB’s Tobacco Laboratory in Beltsville, Maryland. Scientists and regulators representing Federal agencies from the United States, Canada, and Mexico participated in the tour.

TTB 2012 Annual Report

8

jointly to verify and validate that industry members pay the proper amount of tax on these strictly regulated commodities. The strategic risk-based approach used to deploy limited staff resources enables TTB to leverage its field presence to cover a wide universe of taxpayers.

In FY 2012, TTB continued to address revenue risk areas through enhanced risk modeling and increased automation of its investigative targeting models. This included expansion of TTB’s use and analysis of its internal and external data for enforcement actions, resulting in the identification of industry members and others that could be involved in diversion and tax fraud.

Enforcing Importer Compliance

Due to the known revenue risk in the import and export trade in tobacco products, and as the Federal permitting authority for tobacco importers, TTB developed a tobacco importer risk model to identify the highest risk tobacco importers operating with a Federal permit. In FY 2012, TTB integrated its tobacco importer risk model into its data analytics platform and implemented upgrades that allow for more real-time targeting of tobacco importers for audit or investigation.

Further, in FY 2012, TTB developed a pilot risk model for alcohol importers. The alcohol importer risk model combines import data from CBP with tax and permitting data from TTB databases to identify potential non-permitted alcohol imports and other anomalies. This model will be used to identify audit candidates in FY 2013 and, based on those results, TTB will evaluate and enhance the accuracy of its model. TTB also intends to explore options to more efficiently update and add external data into its risk models.

In just two years, the Bureau’s audits of these businesses resulted in the identification of more than $10 million in additional excise tax liability associated with imported alcohol and tobacco products. TTB has referred these cases to CBP, the agency responsible for collecting the Federal excise tax on imported products. In 2009, CHIPRA extended the statute of limitations to three years for the collection of taxes on imported alcohol and tobacco products. TTB is partnering with CBP’s Office of Regulatory Audits (ORA) to ensure that the taxes due on these imported products are collected. During FY 2012, TTB and CBP’s ORA agreed to pilot a joint audit of a tobacco importer. Under the pilot audit, TTB and CBP are working together to identify and collect any outstanding tax liabilities identified during the audit. Developing effective relationships with its enforcement partners is critical to TTB’s long-term strategy and, following this pilot enforcement initiative, TTB will assess additional opportunities to work with CBP ORA to ensure alcohol and tobacco importer compliance.

Addressing the Revenue Risk from Tobacco Processors

As required by CHIPRA, tobacco processors now report to TTB on the removal, transfer, or sale of processed tobacco. As processed tobacco is untaxed, the diversion of this product outside the lawful distribution chain for use in the illegal manufacture of tobacco products poses a significant revenue risk. In FY 2011, TTB initiated a pilot project to address the identified revenue threat posed by processed tobacco sold to non-permitted manufacturers who did not report or file Federal excise taxes.

There are 30 domestic tobacco processors and approximately 180 importers of processed tobacco who distribute roughly 1.1 billion pounds of processed tobacco to a myriad of brokers, manufacturers, and other tobacco processors. The TTB risk model developed for the pilot project indicated that many of these businesses warranted a joint investigation/audit to determine compliance with TTB laws and regulations. In its

TTB 2012 Annual Report

9

first year, this enforcement initiative identified approximately $9 million in additional Federal excise tax due on illegally manufactured tobacco products.

In FY 2012, TTB expanded this enforcement initiative to a nationwide program. TTB conducted field examinations of these manufacturers and importers of processed tobacco, and then conducted subsequent audits and forward traces of suspicious processed tobacco removals outside of the permitted system. As of the close of FY 2012, TTB identified approximately $182.2 million in potential tax liabilities. In the year ahead, TTB plans to increase the number of audits and investigations of manufacturers and importers of processed tobacco, and will explore methods of refining its targeting model to incorporate transactional sales data from domestic tobacco processors.

Enforcing the Floor Stocks Tax

In FY 2012, TTB continued to address the significant revenue exposure that remains from the floor stocks tax (FST) levied on tobacco products under CHIPRA. An FST is a one-time excise tax placed on a commodity undergoing a tax increase, and was imposed on all tobacco products held for sale as of April 1, 2009. The FST is equal to the difference between the new tax rate and the previous rate. As TTB has no regulatory authority over tobacco wholesalers and retailers, the enactment of the FST has presented an ongoing enforcement challenge for TTB as it added approximately 400,000 new taxpayers to TTB’s enforcement responsibility. TTB has used a variety of techniques to enforce the FST and ensure collection of the revenue due.

Since its enactment, TTB has continued its FST enforcement efforts based, in part, on findings that many wholesalers and retailers failed to report or underreported their tobacco inventory and associated tax payments. In three years, TTB has completed FST field examinations for many of the largest taxpayers, with findings of more than $15 million and collections of more than $7 million, as well as resulting criminal investigations. However, the number of FST non-filers is so great that existing enforcement resources cannot conduct on-site examinations of the entire population of high-risk taxpayers.

In FY 2012, TTB enhanced its FST non-filer program to pursue tax liabilities at companies where TTB’s targeting analysis indicates that FST liabilities still exist, but where it is not cost effective or practical to conduct an on-site examination. The National Revenue Center uses the results of TTB’s targeting analysis to initiate a “substitute-for-return” process to issue assessments on the estimated tax liabilities en masse. The IRC allows TTB to create a tax return for a taxpayer where no return has been filed, or where the return that was filed is considered false. In FY 2012, this approach resulted in TTB compliance actions against 188 taxpayers that had failed to file FST, with potential FST liabilities of $22.5 million, plus interest and penalties. In total, the FST non-filer program has resulted in TTB collections in excess of $1.28 million in FY 2012. In FY 2013, TTB will continue collection actions and seek resolution of outstanding FST liabilities identified through the non-filer project.

Additionally, in FY 2012, TTB met with legal representatives for five Native American companies that received non-compliance notifications from TTB, resulting in a settlement with one company for $1 million. TTB continues to work with the remaining four companies to collect inventory and sales records to support the FST amount due.

TTB 2012 Annual Report

10

Criminal Enforcement

TTB is the Federal agency responsible for detecting and addressing Federal excise tax evasion in relation to alcohol and tobacco products. Under its criminal authority, TTB is charged with identifying any gaps in tax payment from entities and individuals manufacturing or selling alcohol and tobacco products outside of the lawful distribution system. By developing leads from TTB’s internal data collected through its regulatory mission, government databases, referrals from other Federal and state agencies, and other external sources, TTB is able to identify trends and schemes used to facilitate or engage in tax fraud and diversion.

Although tax losses from diversion are difficult to estimate due to the clandestine nature of the activity, a 2010 Department of the Treasury study of Federal revenue losses from cigarette diversion estimates that tax receipts were diminished by as much as $1.5 billion annually for the years 2005 to 2007 due to smuggling and other criminal diversion activity.6 At the current tax rate, assuming all other factors remain constant, potential Federal revenue losses from cigarette diversion could be $5 billion annually. In its 2009 review of Federal tobacco tax enforcement efforts, the Department of Justice Office of the Inspector General cited Federal and state government estimates of $5 billion in annual revenue losses resulting from the diversion of tobacco products. 7

The stakes surrounding diversion enforcement were raised in 2009, however, when Congress roughly tripled the Federal excise tax on tobacco products and, thus, multiplied the potential illegal profits to be gained from tobacco diversion. Since the Federal tax increase, 19 states and the District of Columbia have also raised taxes on cigarettes, further increasing the diversion profit incentive. Historical data establishes that tax increases result in increased profit potential from diversion and, as a result, increased tax evasion. The relationship between tax rates and diversion was specifically recognized in an August 2010 report by the Framework Convention on Tobacco Control8 when it stated that high tax increases provide financial incentives for diversion of tobacco products from lawful commercial channels, particularly when enforcement and tax laws are weak, penalties are small, and the prosecution process is long.

In recent years, the increased profit motive for cigarette trafficking has resulted in a proliferation of tobacco diversion schemes. A March 2011 Government Accountability Office Report found that there are a wide range of schemes used to evade tobacco excise taxes and fees and described the scope of current diversion activity, which extends to high and low tax states alike, as well as Native lands and other countries.9 However, the j137

6 “Department of the Treasury Report to Congress on Federal Tobacco Receipts Lost Due To Illicit Trade and Recommendations for Increased Enforcement,” U.S. Department of the Treasury, Feb. 2010. 7 “The Bureau of Alcohol, Tobacco, Firearms and Explosives’ Efforts to Prevent Diversion of Tobacco,” U.S. Department of Justice, Office of the Inspector General, Report No. I-2009-005, Sept. 2009.

8 World Health Organization Framework Convention on Tobacco Control, “Price and Tax Policies,” FCTC/COP/4/11, Aug. 15, 2010, p. 8, para. 33. The FCTC is the international treaty organization established to address the health and revenue effects of tobacco use and the illicit trade of tobacco products.

9 “Illicit Tobacco: Various Schemes are Used to Evade Taxes and Fees,” U.S. Government Accountability Office, GAO-11-313, March 2011.

TTB 2012 Annual Report

11

diversion of products to evade Federal excise tax is not limited to tobacco. Though TTB has no similar estimates of revenue losses from the diversion of alcohol, criminal case work in FY 2012 indicates that fraud in the alcohol beverage trade poses both a public safety risk and a serious revenue threat.

Implementing the TTB Criminal Enforcement Program

Until FY 2011, addressing criminal activity in the alcohol and tobacco industries required that TTB coordinate with other law enforcement agencies to exercise the Bureau’s criminal jurisdiction. Without dedicated special agents to address the evasion of alcohol and tobacco excise taxes, TTB’s criminal case referrals were subject to the availability of other law enforcement agencies, which have their own resource limitations and mission priorities.

Recognizing the Bureau’s lack of resources to hire special agents and its inability to enforce its criminal jurisdiction without agents, Congress authorized TTB funding in 2010 and 2012 to establish a criminal enforcement program to address tobacco smuggling and other diversion activity. With this funding, TTB entered into an agreement with IRS Criminal Investigation (IRS CI) to obtain criminal investigative services, effectively allowing TTB to leverage the existing law enforcement resources within the Treasury Department to enforce its criminal jurisdiction. This arrangement allowed TTB to engage in operations quickly and bypass certain operational costs, both of which were critical considerations given the short-term nature of the funding.

The complexity of diversion cases requires leveraging all of TTB’s enforcement resources to identify, investigate, and successfully prosecute offenders. Recognizing the expertise required to develop these cases effectively, in FY 2012, TTB provided advanced fraud and diversion training to its auditors and investigators and expanded its team-based enforcement approach for major criminal cases with potential nationwide impact. National Response Teams, or NRT, are comprised of auditors, investigators, and intelligence analysts that work collaboratively on cases when TTB suspects that fraud and diversion are present. A total of eight NRT cases were carried out in FY 2012, resulting in successful civil examinations, criminal case referrals, and the identification of more than $75 million in potential excise tax liabilities. TTB will continue its use of NRT in FY 2013 to enhance its criminal enforcement program.

Achieving Criminal Enforcement Results

In its two years of operations, the criminal enforcement program at TTB has produced significant results. Using a small contingent of agents supported by a robust team of forensic auditors, investigators, and intelligence analysts, TTB has opened a total of 48 cases, 27 of which were opened in FY 2012. The total estimated tax liability associated with these 48 cases is nearly $340 million. As of the close of FY 2012, TTB had referred 43 of these cases to an Assistant United States Attorney (AUSA), all of which were accepted for investigation. This unprecedented acceptance rate for criminal referrals demonstrates both the merit and the magnitude of these cases. The success of these investigations reflects the synergy that results from combining experienced civil fraud auditors and investigators who are knowledgeable about the industry with skilled agents to develop criminal cases.

The types of investigations initiated in the two years of TTB’s criminal enforcement program are representative of the extensive tax fraud and criminal activity in the illicit alcohol and tobacco trade. The schemes employed to evade excise tax payment include:

TTB 2012 Annual Report

12

• Manufacturing of tobacco products without payment of Federal excise tax • Cigarette distributors evading tobacco FST • Cigarette distributors selling “exported” cigarettes in the U.S. without payment of Federal excise tax • Cigarettes smuggled into the U.S. without payment of Federal excise tax • Failure to pay Federal excise tax on distilled spirits • Importation of misclassified distilled spirits to evade Federal excise tax • Operating without a permit/wholesaling violations • Importing alcohol without a permit • False wine labeling and sales of counterfeit wine

Significantly, though criminal cases are often multi-year endeavors, TTB has resolved several cases in its two year of operations. Notably, in FY 2012, three subjects indicted for illegal trafficking of cigarettes, tax evasion, and other related crimes pleaded guilty. This case involved a TTB permittee operating in Florida who evaded approximately $37.5 million in excise tax liabilities through off book manufacturing and sales of cigarettes. The primary defendant in this case was sentenced on October 18, 2012, in United States District Court to 60 months of incarceration and three years of supervised release. He was also ordered to pay $9.4 million in restitution and was ordered to forfeit $19.6 million. Two additional defendants were also sentenced to 30 months and 24 months of incarceration, respectively, and ordered to pay restitution of over $9.4 million for Federal excise taxes, Department of Agriculture tobacco buy-out assessments, and escrow deposits due to states for the tobacco litigation settlement fund.

Of the criminal cases currently under investigation, six subjects entered plea negotiations in FY 2012. These subjects are expected to enter guilty pleas in early FY 2013.

Coordinating with Law Enforcement Partners

In FY 2012, TTB met with AUSAs from the Eastern, Northern, and Western Districts of New York to establish a working relationship for matters of mutual interest in tax enforcement. In these exchanges, both parties exchanged information regarding the current tobacco environment in New York as well as the practical considerations involved with tobacco enforcement on Native lands. Enforcement of Federal excise tax laws on Native American reservations involves the application of Federal revenue laws to activities that occur on tribal lands, which raises issues regarding claims of tribal sovereignty in some cases. These matters are extremely sensitive and have presented difficult enforcement issues based upon existing law establishing that Federal excise tax laws apply on Native American lands.

During the meetings, TTB briefed the AUSAs on ongoing tax enforcement initiatives to ensure that TTB’s efforts will not impede any ongoing criminal investigations. The Northern District AUSA also coordinated a meeting between TTB and an Indian Tribal Nation. This meeting led to an ongoing relationship with the Nation that will assist in our efforts to resolve potential Federal tax matters in FY 2013.

Unlicensed cigarette manufacturing on Native lands continues to be an enforcement problem and, in FY 2013, TTB will continue to work proactively with tribal leaders, Federal law enforcement partners, and the AUSAs to bring all of the illegal operations into compliance or terminate their operations.

TTB 2012 Annual Report

13

Protect the Public

TTB’s public protection mission has broad meaning and is inclusive of activities that directly impact American consumers, such as testing the safety of alcohol beverage products and verifying that label claims are truthful, accurate, and not misleading, as well as work that directly impacts the U.S. economy by facilitating lawful trade and fair competition within the alcohol and tobacco trade. TTB’s role in regulating the trade of alcohol and tobacco products ensures consumer confidence in the integrity of the products manufactured in the U.S. and ensures that businesses are operating on a level playing field—key outcomes that promote job growth and a strong economy.

TTB’s work in this mission area aligns under three main programs: 1) Permits and Business Assurance; 2) Trade Facilitation; and 3) Advertising, Labeling, and Product Safety. Taken together, these programs ensure the integrity of the businesses that produce and distribute alcohol and tobacco products, the integrity of the alcohol beverage products, and the integrity of the market in which these businesses operate.

Business Integrity TTB facilitates growth in the U.S. economy by ensuring that only qualified applicants enter business as an alcohol producer, wholesaler or importer, or as a tobacco products manufacturer, importer or exporter. The FAA Act includes provisions to require a permit for those who engage in the business as a producer, importer, or wholesaler of alcohol beverages. The IRC includes similar permitting requirements for tobacco manufacturers, importers, and export warehouses, as well as some alcohol industry members.

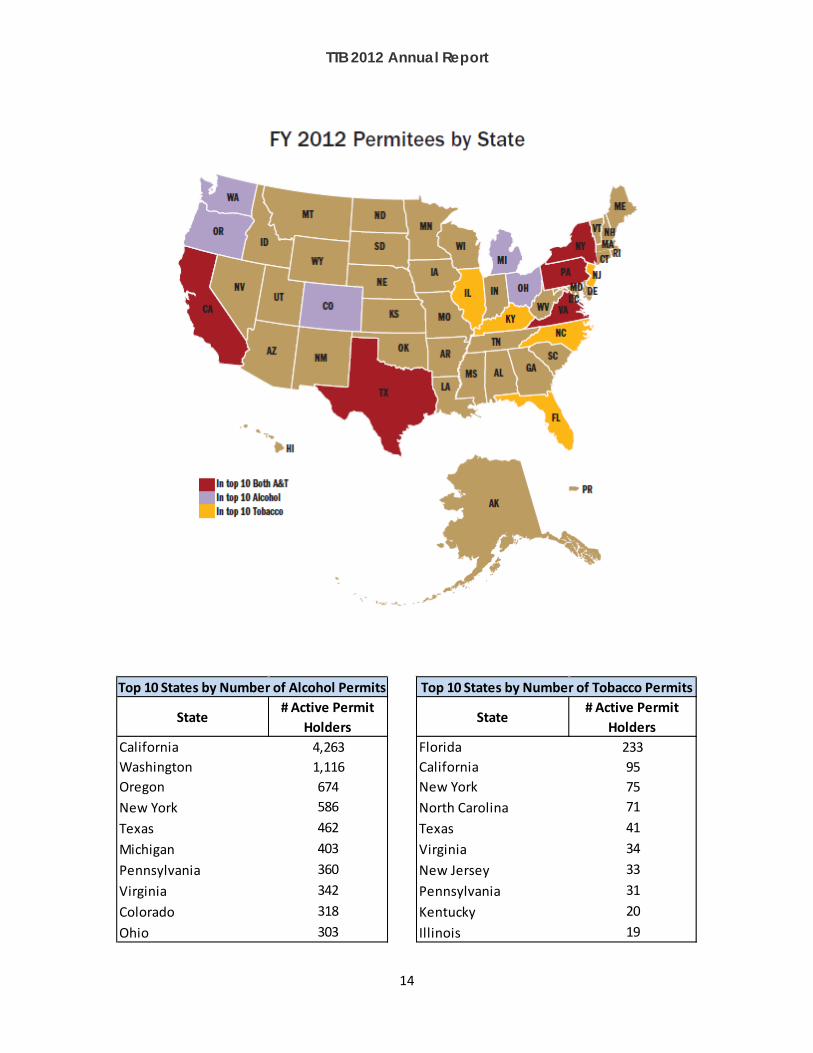

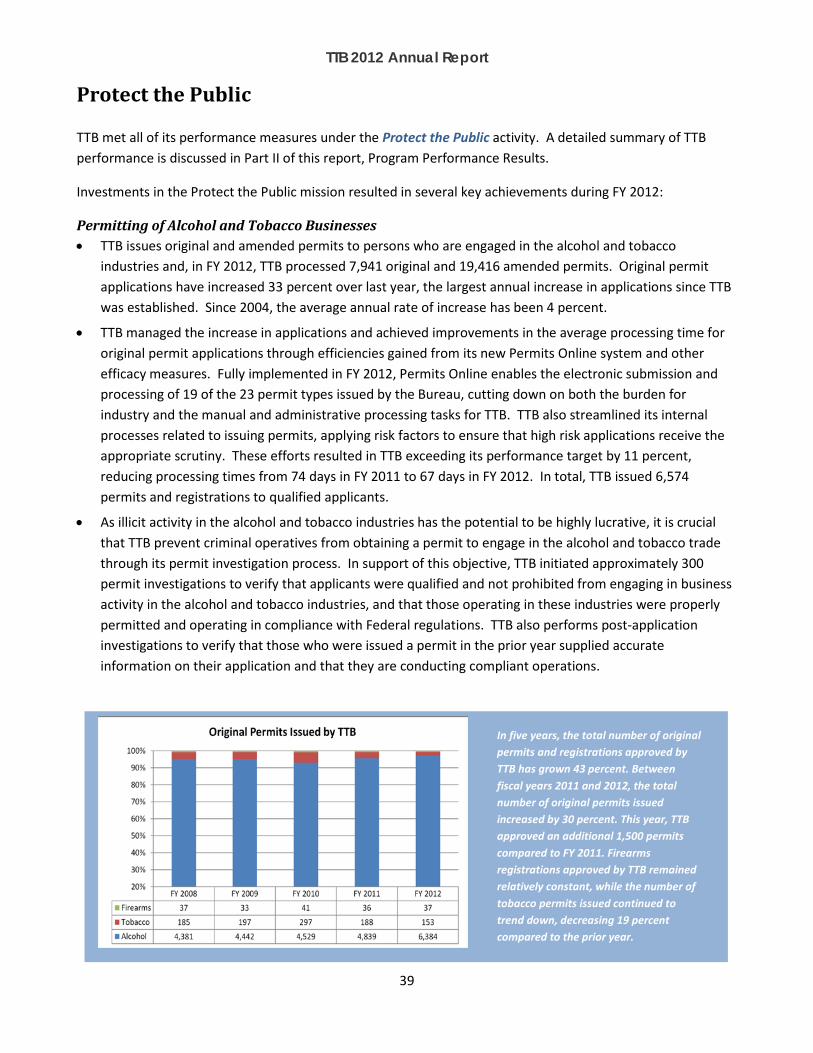

The number of applicants filing for an original permit or registration with TTB has grown 50 percent between FY 2008 and FY 2012. Today, the Bureau regulates nearly 61,700 industry members, an increase of 32 percent over the 46,700 permit holders in FY 2008.

Under its FAA Act authority, TTB conducts a multi-tiered background evaluation prior to issuing a permit to ensure that only qualified persons obtain a permit to operate within the regulated industries. Through this process, and other activities under its Permits and Business Assurance Program, TTB prevents prohibited persons from commencing operations and potentially diverting products from legitimate commercial channels in order to fund illicit activity. Given the substantial tax revenue associated with the commodities TTB regulates, the incentive to operate under color of law for illegal purpose and illegal profit is substantial and, therefore, an important area of the Bureau’s focus.

In order to make the most effective use of limited resources, TTB applies risk criteria to its review of permit applications and refers the highest risk applications to its investigators for a field inspection. TTB investigators also perform field investigations on a random sample of applicants who received a permit to verify that the business’ operations comply with Federal law. If TTB determines that a business is violating the conditions of its Federal permit, TTB may suspend or revoke its permit.

TTB 2012 Annual Report

14

State# Active Permit

HoldersCalifornia 4,263Washington 1,116Oregon 674New York 586Texas 462Michigan 403Pennsylvania 360Virginia 342Colorado 318Ohio 303

Top 10 States by Number of Alcohol Permits

State# Active Permit

HoldersFlorida 233California 95New York 75North Carolina 71Texas 41Virginia 34New Jersey 33Pennsylvania 31Kentucky 20Illinois 19

Top 10 States by Number of Tobacco Permits

TTB 2012 Annual Report

15

Efficiency in permit processing is equally critical to support improved economic opportunities for U.S. businesses. Prompt turnaround time for permit application processing enables those who are qualified to hold a Federal permit to begin their operations sooner, facilitating U.S. economic growth in a fair marketplace.

Improving Service in Permit Processing

TTB processes applications for more than 20 types of permits or registra-tions for the alcohol, tobacco, firearms, and ammunition industries. New or existing alcohol and tobacco industry members must be approved by TTB in order to commence a new regulated industry operation or to update critical permit information, such as a change in location for an existing business. The new businesses permitted by TTB are predominantly small businesses, which contribute to local job opportunities as well as America’s competitiveness in the global market.

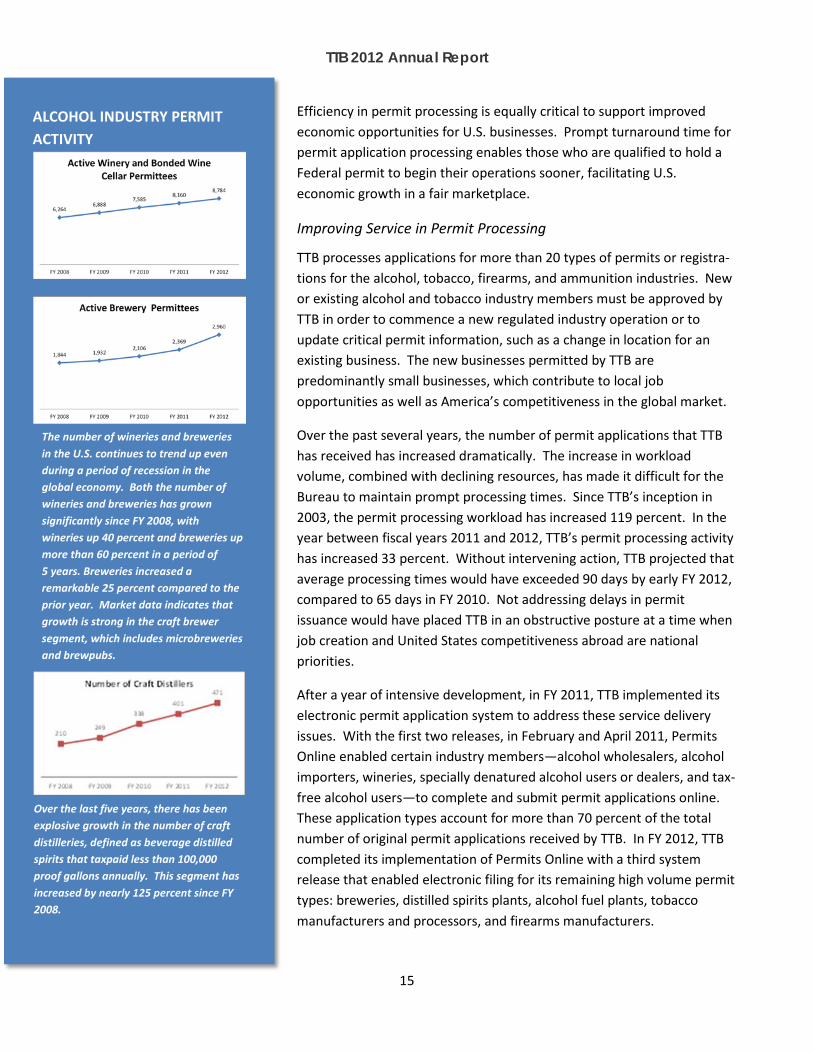

Over the past several years, the number of permit applications that TTB has received has increased dramatically. The increase in workload volume, combined with declining resources, has made it difficult for the Bureau to maintain prompt processing times. Since TTB’s inception in 2003, the permit processing workload has increased 119 percent. In the year between fiscal years 2011 and 2012, TTB’s permit processing activity has increased 33 percent. Without intervening action, TTB projected that average processing times would have exceeded 90 days by early FY 2012, compared to 65 days in FY 2010. Not addressing delays in permit issuance would have placed TTB in an obstructive posture at a time when job creation and United States competitiveness abroad are national priorities.

After a year of intensive development, in FY 2011, TTB implemented its electronic permit application system to address these service delivery issues. With the first two releases, in February and April 2011, Permits Online enabled certain industry members—alcohol wholesalers, alcohol importers, wineries, specially denatured alcohol users or dealers, and tax-free alcohol users—to complete and submit permit applications online. These application types account for more than 70 percent of the total number of original permit applications received by TTB. In FY 2012, TTB completed its implementation of Permits Online with a third system release that enabled electronic filing for its remaining high volume permit types: breweries, distilled spirits plants, alcohol fuel plants, tobacco manufacturers and processors, and firearms manufacturers.

ALCOHOL INDUSTRY PERMIT ACTIVITY

The number of wineries and breweries in the U.S. continues to trend up even during a period of recession in the global economy. Both the number of wineries and breweries has grown significantly since FY 2008, with wineries up 40 percent and breweries up more than 60 percent in a period of 5 years. Breweries increased a remarkable 25 percent compared to the prior year. Market data indicates that growth is strong in the craft brewer segment, which includes microbreweries and brewpubs.

Over the last five years, there has been explosive growth in the number of craft distilleries, defined as beverage distilled spirits that taxpaid less than 100,000 proof gallons annually. This segment has increased by nearly 125 percent since FY 2008.

TTB 2012 Annual Report

16

Significant system features include online self-registration, self-monitoring of an application’s status, and electronically guided assistance through the application process. The built-in prompts and self-help instructions at each step of the application process also ensure that the applications that reach TTB specialists are completed correctly and contain all the required documentation. In FY 2012, TTB added numerous system enhancements to improve both internal processing efficiencies and the ease of use for its customers, including pre-population of certain required fields and streamlined fields for permit amendments.

The impact of Permits Online has been substantial. At year end, the overall adoption rate for Permits Online was 62 percent. This level of electronic filing helped TTB to reduce the average processing time for original applications to 67 days, which represents processing times 7 days faster than the FY 2011 average. The average processing time for all approved permit applications filed in Permits Online was just under 57 days. This improvement is notable given the influx of permit applications in FY 2012 and the decrease in the number of employees processing them.

Going forward, TTB will continue to promote the use of Permits Online and implement enhancements that improve its functionality. Enhancements planned for FY 2013 include the uploading of historical permit information from TTB’s legacy permit system to Permits Online, which will allow existing industry members to use Permits Online for filing amendments to their approved permit. As TTB receives more than 18,000 amendments annually, this upgrade will result in efficiencies for both TTB and its regulated industry members. TTB also is working on an initiative that will make available to industry members who obtain their permits through Permits Online an encrypted electronic copy of their application data, which may be provided to state liquor authorities when applying for the equivalent state licenses. If states adopt this program, the application process will be streamlined for applicants as they will only be required to enter certain information once that is needed by both TTB and the states in the permitting process.

Importing Tobacco Products without a Permit

In support of the Bureau’s business integrity objectives, TTB monitors compliance with Federal permit requirements among tobacco product importers through a variety of data analysis and investigative techniques.

In FY 2012, through this data analysis, TTB intelligence analysts identified that 13 percent of active tobacco importers in FY 2012 had illegally imported products. TTB responded by issuing cease and desist letters to these importers. These efforts to identify and address compliance violations have proven effective, as all of the importer entities notified by TTB have subsequently complied with their legal obligations or ceased operations, and the overall rate of non-compliance with Federal permit requirements has declined since TTB began tracking this information.

The rate of non-permitted tobacco importers that have declared entries of tobacco products to U.S. Customs has declined since the Bureau initiated this enforcement strategy in FY 2008. During this period, the level of illegal importers has dropped from 22 percent to 13 percent in FY 2012. As tobacco products are often smuggled into the U.S. through undeclared importations, however, TTB must continue to supplement these data mining efforts and to monitor importer activity through audits, investigations, and other intelligence efforts to detect undeclared importations and address the substantial potential tax losses that they represent.

TTB 2012 Annual Report

17

Market Integrity

TTB is charged with assuring that the alcohol marketplace is free from practices that would stifle competition and act as a barrier to trade. Under its Trade Facilitation program, TTB meets this mandate through a variety of activities, ranging from investigations of industry trade practices to engaging foreign counterpart agencies to keep the channels of commerce open and operating in compliance with U.S. and international laws.

TTB’s work in this area has direct influence on the Nation’s economic recovery. Industry trade association reports10 state that the alcohol beverage industry contributes directly or indirectly to the U.S. economy by providing nearly 4 million jobs and roughly $400 - $500 billion in economic activity. Overseas demand for the products TTB regulates remains strong, with U.S. exports of all alcohol beverages totaling nearly $3 billion in 2011. The majority of these exports are spirits and wine products.

Promoting Fair Competition in the U.S. Marketplace

As part of its Trade Facilitation Program, TTB has reinvigorated its FAA Act trade practices program to investigate acts that violate Federal law relating to alcohol beverage marketing practices. The FAA Act provisions that TTB enforces require TTB to ensure fair competition in the alcohol beverage trade by not only verifying that persons who engage in the trade are qualified to do so within the meaning of the statute but also by ensuring the trade practices among industry competitors comply with the law. Regulated trade practices entail restrictions involving exclusive

q137

10 “The Impact of Wine, Grapes and Grape Products on the American Economy 2007,” MKF Research LLC; “The National Trade Association Representing Producers and Marketers of American’s Favorite Brands of Distilled Spirits,” Distilled Spirits Council of the United States; “Beer Industry Contributes Nearly $200 Billion to U.S. Economy,” Beer Institute and National Beer Wholesalers Association. Economic Impact study conducted by John Dunham & Associates, New York City, using data compiled in 2008.

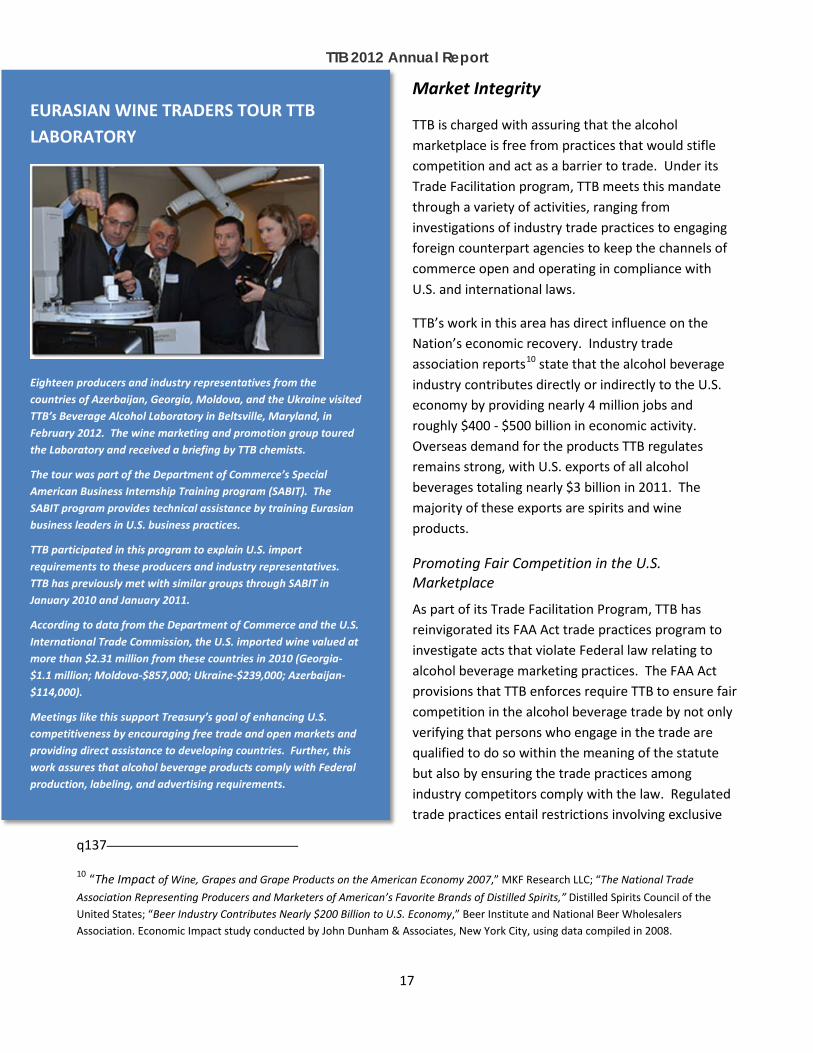

EURASIAN WINE TRADERS TOUR TTB LABORATORY

Eighteen producers and industry representatives from the countries of Azerbaijan, Georgia, Moldova, and the Ukraine visited TTB’s Beverage Alcohol Laboratory in Beltsville, Maryland, in February 2012. The wine marketing and promotion group toured the Laboratory and received a briefing by TTB chemists.

The tour was part of the Department of Commerce’s Special American Business Internship Training program (SABIT). The SABIT program provides technical assistance by training Eurasian business leaders in U.S. business practices.

TTB participated in this program to explain U.S. import requirements to these producers and industry representatives. TTB has previously met with similar groups through SABIT in January 2010 and January 2011.

According to data from the Department of Commerce and the U.S. International Trade Commission, the U.S. imported wine valued at more than $2.31 million from these countries in 2010 (Georgia-$1.1 million; Moldova-$857,000; Ukraine-$239,000; Azerbaijan-$114,000).

Meetings like this support Treasury’s goal of enhancing U.S. competitiveness by encouraging free trade and open markets and providing direct assistance to developing countries. Further, this work assures that alcohol beverage products comply with Federal production, labeling, and advertising requirements.

TTB 2012 Annual Report

18

outlets, tied-house arrangements, commercial bribery, and consignment sales. Unlawful trade practices threaten fair competition because such practices undermine equal access to the marketplace, precluding healthy small business activity, and limit consumer choices by allowing influential producers to unlawfully interfere with the supply chain.

In FY 2012, TTB issued two industry circulars providing guidance to industry members on trade practice prohibitions. TTB issued Industry Circular 2012-01, Guidance Regarding Industry Members’ Participation in Retail Programs, to inform all industry members and other interested parties of the Bureau’s position regarding participation in retail promotional programs. In this circular, TTB provided guidance on the promotional activities it considers permissible between alcohol beverage suppliers and retailers. This circular was issued following the 2011 settlement of a series of trade practice investigations. As a result of these investigations, the Bureau alleged that certain suppliers violated the tied-house “slotting fee” provisions of the FAA Act by offering inducements to a large casino chain in order to receive preferred shelf and warehouse space. These TTB investigations resulted in offers in compromises from six companies totaling approximately $1.9 million, and marked the largest set of offers in compromise ever accepted by TTB for trade practice violations.