future of banking regulations and macro-prudential policies · pdf filefuture of banking...

TRANSCRIPT

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Future of Banking Regulations and

macro-prudential policies

Jon DanıelssonSystemic Risk Centre

London School of Economics

www.systemicrisk.ac.uk

May 8, 2017

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Post crisis regulated developments

• Banks hold much more capital

• Financial institutions are more restricted

• Much more compliance

• Insurance companies and asset managers seen assystemically important (SIFI) and regulated accordingly

• We regulate (or aspire to regulate) much more holistically

• Applying an increasingly similar methodology toeverybody

• Convergence in risk models and business practices

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Why?

• We had a big financial crisis in 2008

• The political leadership (G20) told the financialauthorities

“Do something about finance”

• The authorities have to comply and show action

• Fear of the “unknown unknowns”

• Which is used to justify the regulatory agenda

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The financial authorities might say:

• “Before 2008 the financial sector misbehaved”

• “We admit we were asleep”

• “But now are fully on top of the problem”

• “And are creating rules that promise:”

a. Reducing the frequency and severity of crises

b. Making the economy more resilient and grow more

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

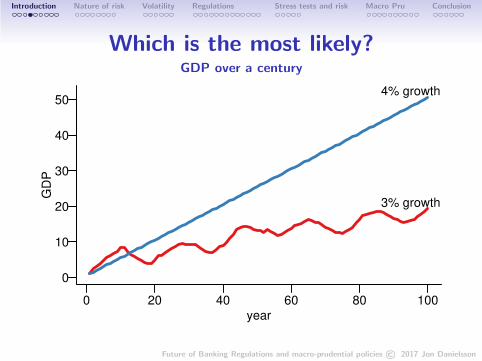

Which is the most likely?GDP over a century

0 20 40 60 80 100

0

10

20

30

40

50

year

GD

P

3% growth

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Which is the most likely?GDP over a century

0 20 40 60 80 100

0

10

20

30

40

50

year

GD

P

4% growth

3% growth

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Which is the most likely?GDP over a century

0 20 40 60 80 100

0

10

20

30

40

50

year

GD

P

4% growth

3% growth

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Which is the most likely?GDP over a century

0 20 40 60 80 100

0

10

20

30

40

50

year

GD

P

4% growth

3% growth

2% growth

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Helicopter view of what is happening with

financial regulations

• Much more emphasis on measuring risk, all the way fromthe most detailed activities up to the entire system

• Use those measurements to control the financial system

• Regulations (what could be called the regulatoryphilosophy) is converging to a Basel style worldview

• All are treated the same: bank, insurance, assetmanagement, pension funds

• The key question is: Is this a positive development?

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Macro and micro prudential regulations

• Macro prudential (MacroPru) — Protect the system

• minimize systemic risk and contain systemic crises

• Micro prudential (MicroPru) — Protect the clients

• Basel II/III is mostly micro

• Current bank stress testing is only micro

• We are now developing macroprudential stress testing(see discussion below)

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

What is systemic risk?FSB-IMF-BIS report to G20 (2009)

• Risk of disruption to financial services that is:

• Caused by an impairment of all or parts of the financialsystem and

• Has the potential to have serious negative consequencesfor the real economy

• Criteria

• Size• Substitutability (the extent to which other components

of the system can provide the same services in the eventof a failure)

• Interconnectedness

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Top down and bottom up

Micro

Retail clients

SMEs

Corporates

Government

Asymmetric abilitiesAbuse

ConductCulture

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Top down and bottom up

Micro

Retail clients

SMEs

Corporates

Government

Asymmetric abilitiesAbuse

ConductCulture

MacroThe economy

Financial system

Government

SIFI

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Top down and bottom up

Institution

Micro

Retail clients

SMEs

Corporates

Government

Asymmetric abilitiesAbuse

ConductCulture

MacroThe economy

Financial system

Government

SIFI

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Top down and bottom up

Institution

Micro

Retail clients

SMEs

Corporates

Government

Asymmetric abilitiesAbuse

ConductCulture

MacroThe economy

Financial system

Government

SIFI

Basel

Processes

Stress test

TLACLTV, DTI, *

Capital

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The five key questions

1. Can we measure risk sufficiently well to control thefinancial system?

2. Does controlling by risk stabilize or destabilize?

3. Should we de-risk?

4. What about the unknown unknowns?

5. Is it desirable to follow a regulatory philosophy thatmakes the financial system more homogeneous?

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

What drives risk?

• 2008 happened because of decisions made years earlier

• In 2003 all the signs pointed to risk being low

• The authorities and the private sector thought we weresafe

• And so it was perfectly OK to take extra risk

• But

• “Stability is destabilizing” (Minsky)

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The unknown unknowns

• The US stock market goes down by $200 billion in oneday and nobody cares

• Potential subprime losses of less than $200 billion, andOMG, it’s the end of civilization

• The risk we know we prepare for — known unknowns

• The risk we don’t know is the dangerous type

• The unknown unknowns are most damaging

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Risk is endogenousDanielsson–Shin (2002)

• Risk is exogenous or endogenous

exogenous Shocks to the financial system arrive fromoutside the system, like with an asteroid

endogenous Financial risk is created by the interactionof market participants

“The received wisdom is that risk increases in recessions andfalls in booms. In contrast, it may be more helpful to think ofrisk as increasing during upswings, as financial imbalances

build up, and materialising in recessions.”Andrew Crockett, then head of the BIS, 2000

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

• Market participants are guided by a myriad of models andrules, many dictate myopia

• Prices don’t follow random walks in adverse states ofnature

• Because that is when the constraints bind

• Endogenous risk is created by the interaction of humanbeings

• All with their own objectives, abilities, resources, biases

• All large market outcomes are endogenous

Risk models underestimate risk during calm times andoverestimate risk during crisis — they get it wrong in all states

of the world

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

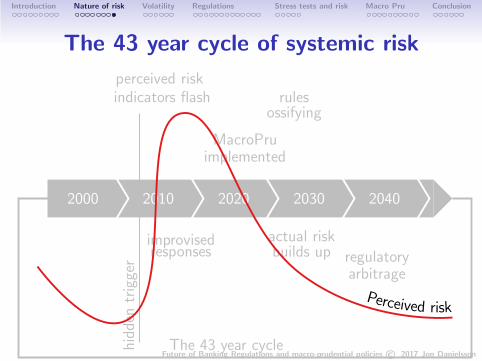

Two faces of risk

• When individuals observe and react — affecting theiroperating environment

• Financial system is not invariant under observation

• We cycle between virtuous and vicious feedbacks

• perceived risk — as reported by risk models• actual risk — hidden but ever present

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Endogenous bubble

1 3 5 7 9 11 13 15 17 19

1

3

5

7

9 PricesPrices

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Endogenous bubble

1 3 5 7 9 11 13 15 17 19

1

3

5

7

9 PricesPrices

Perceived risk

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Endogenous bubble

1 3 5 7 9 11 13 15 17 19

1

3

5

7

9 PricesPrices

Perceived risk

Actual risk

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

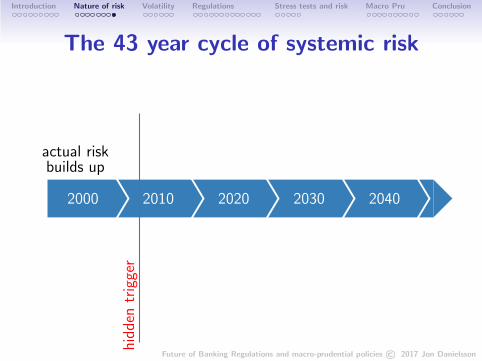

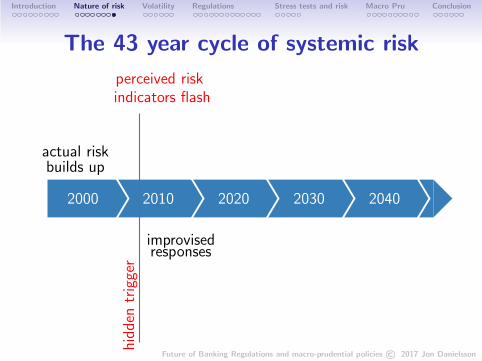

How often do systemic crises happen?

• Ask the IMF–WB systemic crises database (only OECD)

• Every 43 years (17 for UK)

• Best indication of the target probability for policymakers

• However, most indicators focus on much more frequentevents

• Typically every month to every five months

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The 43 year cycle of systemic risk

2000 2010 2020 2030 2040

actual riskbuilds up

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The 43 year cycle of systemic risk

2000 2010 2020 2030 2040

actual riskbuilds up

hidden

trigger

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The 43 year cycle of systemic risk

2000 2010 2020 2030 2040

actual riskbuilds up

hidden

trigger

perceived riskindicators flash

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

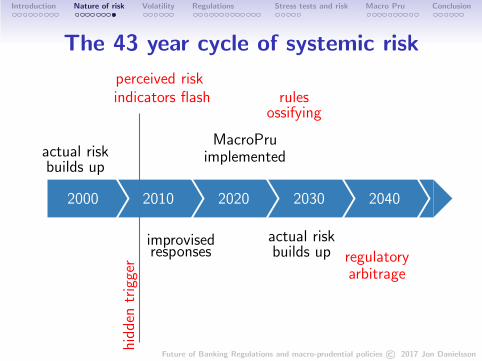

The 43 year cycle of systemic risk

2000 2010 2020 2030 2040

actual riskbuilds up

hidden

trigger

perceived riskindicators flash

improvisedresponses

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The 43 year cycle of systemic risk

2000 2010 2020 2030 2040

actual riskbuilds up

hidden

trigger

perceived riskindicators flash

improvisedresponses

MacroPruimplemented

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The 43 year cycle of systemic risk

2000 2010 2020 2030 2040

actual riskbuilds up

hidden

trigger

perceived riskindicators flash

improvisedresponses

MacroPruimplemented

actual riskbuilds up

rulesossifying

regulatoryarbitrage

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The 43 year cycle of systemic risk

2000 2010 2020 2030 2040

actual riskbuilds up

hidden

trigger

perceived riskindicators flash

improvisedresponses

MacroPruimplemented

actual riskbuilds up

rulesossifying

regulatoryarbitrage

The 43 year cycle

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The 43 year cycle of systemic risk

2000 2010 2020 2030 2040

hidden

trigger

perceived riskindicators flash

improvisedresponses

MacroPruimplemented

actual riskbuilds up

rulesossifying

regulatoryarbitrage

The 43 year cycle

Perceived risk

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The 43 year cycle of systemic risk

2000 2010 2020 2030 2040

hidden

trigger

perceived riskindicators flash

improvisedresponses

MacroPruimplemented

actual riskbuilds up

rulesossifying

regulatoryarbitrage

The 43 year cycle

Perceived risk

Actualrisk

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

“Learning from History:Volatility and Financial Crises”

(2017)with Marcela Valenzuela (University of Chile)

Ilknur Zer (Federal Reserve)

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

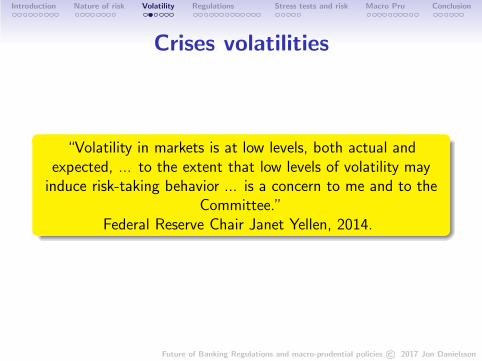

Crises volatilities

“Volatility in markets is at low levels, both actual andexpected, ... to the extent that low levels of volatility mayinduce risk-taking behavior ... is a concern to me and to the

Committee.”Federal Reserve Chair Janet Yellen, 2014.

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

What drives risk?

• 2008 happened because of decisions made years earlier

• In 2003 all the signs pointed to risk being low

• The authorities and the private sector thought we weresafe

• And so it was perfectly OK to take extra risk

• But

• “Stability is destabilizing” (Minsky)

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

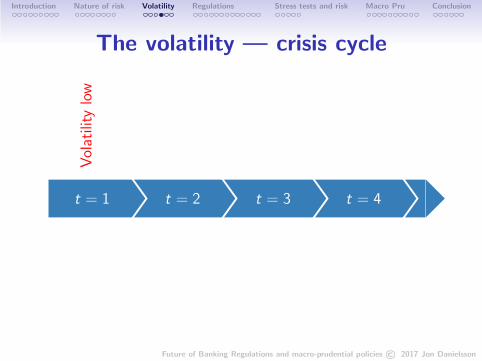

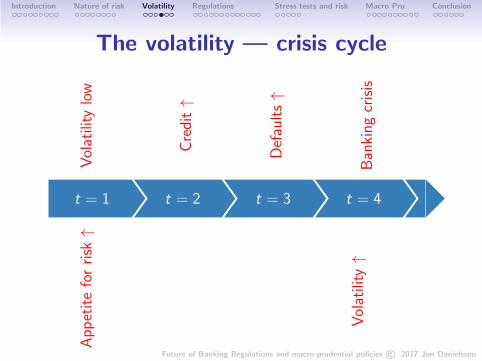

The volatility — crisis cycle

t = 1 t = 2 t = 3 t = 4

Volatility

low

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The volatility — crisis cycle

t = 1 t = 2 t = 3 t = 4

Volatility

low

Appetiteforrisk

↑

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The volatility — crisis cycle

t = 1 t = 2 t = 3 t = 4

Volatility

low

Appetiteforrisk

↑

Credit↑

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The volatility — crisis cycle

t = 1 t = 2 t = 3 t = 4

Volatility

low

Appetiteforrisk

↑

Credit↑

Defaults↑

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

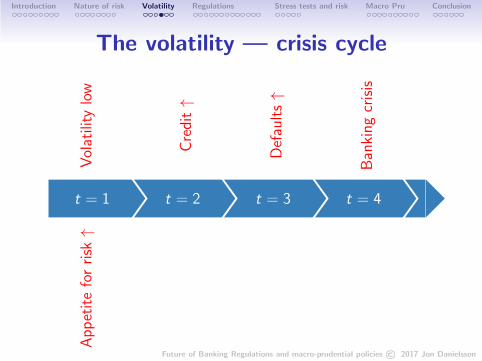

The volatility — crisis cycle

t = 1 t = 2 t = 3 t = 4

Volatility

low

Appetiteforrisk

↑

Credit↑

Defaults↑

Bankingcrisis

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The volatility — crisis cycle

t = 1 t = 2 t = 3 t = 4

Volatility

low

Appetiteforrisk

↑

Credit↑

Defaults↑

Bankingcrisis

Volatility

↑

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Empirical approach

• We construct a comprehensive database on historicalvolatilities from primary sources (1800 to 2010, 60countries

• Realized volatility

• Decomposed with HP filter into low and high volatilities(deviations from trend)

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

• Strong and significant support for volatility cycle

• Low volatility increases the probability of banking crisesyears in future

• Low volatility significantly increases risk-taking(credit-to-GDP)

• High volatility correlated with crisis but not causal

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Overview

• Recognition that we did not regulate well before 2007

• Initial reaction was to take before 2007 regulations andmake them more strict

• Increased understanding that this is not sufficient orcorrect

• Searching for better solutions

• But considerable regulatory fatigue — resistance tochanges

• Basel IV unlikely to happen for many years

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Non–bank drivers

• G20 called for policies to prevent “Too Big To Fail” in2010

• G20 in 2011 asked the FSB and IOSCO to preparemethodologies to identify systemically important NBNIs

• FSB list of global systemically important insurers in 2015

• Grappling with asset managers (next slide)

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Asset managers

• Maybe largest managers, like BlackRock, Vanguard,Allianz, Asmundi

• Limits on fund leverage?

• Limits on liquidity mismatches?

• Minimum capital?

• More disclosure?

• More scrutiny?

• Stress tests?

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Harmonization I — Regulatory philosophy

• All parts of the financial system to be brought under theregulatory umbrella

• asset managers, insurance companies, non-bank banks

• Best understood is banking

• So apply banking vulnerability analysis to the rest

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Internal management of risk

• Some banks use the same methodology for managing riskacross the board

• annual report, regulatory capital, trading floor, riskcapital allocations

• Others use different models and methodologies acrossoperations

• multiple models and stress tests for risk-taking

• Dependent on institution sophistication and size, andsupervisor preference

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Harmonization II — Models

• If we regulate by models, the regulators must believethere is one true model

• Therefore, banks should not report different risk readingsfor the same portfolio

• However, forcing model harmonization across banks ispro–cyclical

• So is forcing the same models to be used for everythinginternally

• Forcing the same models on non-banks is even worse

• And pro–cyclicality negatively affects economic growthand increases financial instability

• The rationale is to reduce cyclicality but it can easilyachieve the opposite

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The SIFI paradox

• Most would argue that SIFIs are not good for clients norsystem (micro and macro undesirable)

• Still they are growing and new are being formed

a. Useful in resolving failed institutions (Lloyds, MS, etc. )b. Governments like national champions (DB, HSBC, Citi,

etc.)

• Regulations have fixed and variable cost, both are growing

• The fixed cost gives competitive advantage to the largest

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Healthy financial systems are heterogenous

• Encourage different models to be used internally andacross industry

• Have different regulations for different parts of theindustry

• Regulate banks differently from insurance companies andthose differently from asset managers

• When some sell we want others to buy

• Encourage new forms of intermediation

• Encourage new entrants• Shadow banking Parallel banking and fintec is good• Just make sure to not regulate them with banking

regulators

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Do we like where we are going?

• Policy makers know that homogeneity is pro—cyclical

• But “We have to do our job, what else can we do?”

• And march towards uniformity

• The same government agency could regulates banks,asset managers, insurance and parallel banks

• Using very similar regulatory methodology

• Because that is easier

• But we will not say that instead say

• “more consistent, simpler, fairer, cheaper, more reliable,less subjective,...”

• Pity it won’t work

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Regulations and risk controls

• Any control process, internal and regulatory, can onlytarget known risk

• We are really good in managing the risk that doesn’tmatter

• It is much easier to control the known knowns

• Because we can easily measure it

• We ignore the risk we should care about

• Because it is much harder to model and plug into acontrol process

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Risk is multifaceted

• Some aspects of risk are good, others bad

• Some risk can be measured, other not

• Different people and financial institutions care about verydifferent aspects of risk

• The trader, the CEO, the stockholder, the pension saver,the house buyer, the regulator, the risk manager all seerisk very differently

• Trying to distill risk into a single set of numbers (likeVaR) is not helpful

• And can easily be destabilizing

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

De-risking

Fact A lot of risk was being taken before 2008, oftenin obscure and hidden ways

Fact The crisis of 2008 revealed the scale of thisrisk-taking and the severity of the consequences

The usual conclusion We therefore need to reduce theamount of risk in the financial system

Question Is that true?

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Does de-risking make us better off?

• No

• The only way the economy will grow is if we take riskydecisions

• With risk comes failure

• If we de-risk, we de-grow

• Losses and failures and some crises

• Are a sign of healthy well-functioning economy

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Risk models and stress tests

• Widespread recognition of limitations of risk models

• The common solution is stress tests (both internal andexternal)

• Run a portfolio or a financial institution on a historical ormade-up scenario

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Regulators bank tests

• US — CCAR (Comprehensive Capital Analysis & Review)

• macroeconomic scenarios from Fed• market

• EU — EBA,

• macroeconomic• market shocks (e.g. included credit risk market risk and

counterparty credit risk, op risk• static balance sheet

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Pros and cons

• Pros

a. recognition of some risks not picked up by modelsb. evaluation of risk engines and processes

• Cons

a. often impossible to identify likelihood of scenariosb. an infinite number of potential scenariosc. paralysis by analysis

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Issues

• Test the resiliency of each individual institution to anexogenous shock

• A useful complement to risk models

• Misses out on systemwide interactions

• For that, macroprudential stress tests (next slide)

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Macroprudential stress tests

• Interaction of all sectors of the financial system

• banks, asset managers, insurance companies, sovereignwealth funds, parallel banks

• each with their own cyclicality

• Jointly model how they interact

• Capturing feedback loops (like bubbles and fire sales)

• Ultimately may inform capital determination and othermacroprudential rules

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

MacroPru objectives

a. Prevent excessive risk accumulating

b. Contain financial crises when they happen

c. Ensure the financial system contributes to growth

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Effective MacroPru authorities needVoxEU.org (2016) Jon Danielsson and Robert Macrae

a. Estimates of systemic risk (and its impact on the realeconomy)

• from the early signs of a build-up of stress to• the post-crisis economic and financial resolution

b. Tools to implement effective policy remedies

c. Legitimacy, a reputation for impartiality, and politicalsupport

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Central banks and monetary policy

• The powers given to central banks are extraordinary for ademocratic society

• Justified by the importance of politicians notmanipulating monetary policy for short-term gains

• But it is relatively straightforward

a. One measurement (inflation)b. Two tools (price and quantity of money)

• Clear objective, target and tools

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

By contrast

• Micropru is complex and ill-defined

• Indicators are imprecise and conflicting

• Surgical tools are ineffective

• Powerful tools too blunt

• Identifies clear winners and losers (lobbying and politics)

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Major financial stress events

• Very few stress events arise purely from excessive risk

• Most are strongly influenced by politics

a. Warsb. Venezuelac. Transition between political systemsd. Populism and anti-globalism

• The macropru event is only a consequence of somethingbigger

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The dilemma of political risk

• Can a nonpolitical entity legitimately implementmacroprudential policies that affect democraticoutcomes?

• Recall Bank of England and Brexit

• Does the mandate given by the political leadership to theregulator extend to the behavior of the politicalleadership?

• If the macropru authorities are not able to incorporatepolitical risk in their analytic frameworks, how effectivecan they be?

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

MacroPru directions

• Most are passive, focusing on crisis resolution and fixedrules that hold through the financial cycle

• Ambitious macroprudential policies aim to lean againstthe wind in a discretionary manner

• Discretion to deviate from rules• Tighten capital and liquidity requirements during

upswings and relax the same rules during and after acrisis

• Cut through the amplifying feedback loops

• Discretionary macropru policies aim to be countercyclical

• If successful, of considerable benefit to the wider economy

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

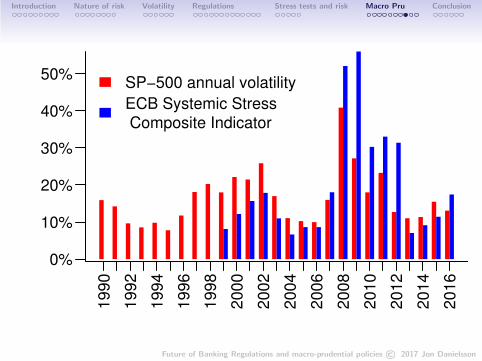

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

SP−500 annual volatility

ECB Systemic Stress

Composite Indicator

0%

10%

20%

30%

40%

50%

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

The potential for procyclical macropruVoxEU.org (2016) Jon Danielsson, Robert Macrae, Dimitri Tsomocos, Jean-Pierre Zigrand

• Minsky argument;

• Homogenization of the financial system;

• Most current indicators of systemic risk, only identifyperceived risk;

• Danger of reacting with some time lag to the postulatedindicators that are themselves measured with a time lag;

• When macropru policy is known to the market, banks willschedule risk-taking around indicators, stress tests andexpected policy reaction;

• The authorities should be willing to reduce aggregaterisk-taking and leverage during booms and increase it intimes of stress.

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

All of these objections call for a procyclical

policy response

• “Banks are failing because they already extended toomuch credit”

• “Surely bank capital needs injections rather than allowingthe banks capital to absorb losses”

• “Helping the City to increase lending now leads to evenbigger moral hazard”

• “Macropru is discredited because it was supposed to haveprevented this credit event in the first place, why shouldit do better this time?”

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Can models beat the FT?

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Can models beat the FT?

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Towards useful risk models

• Understanding model risk is a precondition for risk modelsbeing useful

• Good scientific practice suggests that risk modeloutcomes should come with confidence bounds

• Focus on the unknown unknowns

• Risk of unknown unknowns usually not to be found inmarket data

• But they can be bound

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Risk models are

most useful for controlling traders

less useful in internal risk capital allocation

• e.g. invest in European equities or JPG

often useless for micro–prudential regulations

• Traders read things like Basel III as manualfor where to take risk

dangerous when used for macro–prudential policy

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Policies intended to protect us from the

financial system could easily increase

instability

• MacroPru can be pro–cyclical

• Basel can be pro–cyclical

• Shrinking the known risks encourages the unknown onesto grow

• Monoculture destabilizes the financial system

• Excessive regulation suppresses growth

• Excessive regulation increases the rewards for regulatoryarbitrage and sows the seeds of the next crisis

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Next crisis

• There will be another crisis

• And that is not necessarily a bad thing

• Crises are also a healthy consequence of good risk taking

• Unlikely to be found in 2008 or where the authorities arelooking now

• To speculate

Future of Banking Regulations and macro-prudential policies © 2017 Jon Danielsson

Introduction Nature of risk Volatility Regulations Stress tests and risk Macro Pru Conclusion

Next crisis

• Fixed income

• Suppose inflation hits target levels

• With interest to follow

• And considering duration of some sovereign and corporatedebt

• And rapidly growing EM corporate USD bond issues

• The trigger may be

• Italy