funds for innovation

TRANSCRIPT

Angel investors

• angels provide capital and frequently valuable guidance and strategic assistance.

• The ideal angel is someone who is a generation ahead of the entrepreneur in creating value in the industry.

• Angels are sometimes said to invest 'emotional money,' while venture capitalists are said to invest 'logical money'.

To capture angels attention :

• An in-depth understanding of the market in which they're competing.

• A product or service that can be differentiated from the crowd.

• A concept that is very "scalable" (one that can be rapidly expanded).

VENTURE CAPITAL FUND (VCF)

• Venture capitalist or a venture capital company can be defined as a financial institution, which joins the entrepreneurs as a co-promoter, in a project and shares the risks and rewards of an enterprise.

• startup financing sequence starts with the entrepreneurs (inventors) putting their own available funding into a shoestring operation. Next, an angel investor may be convinced to contribute funding. Thereafter comes venture capital.

VC

• expects the enterprise to have a very high growth rate

• provides management and business skills to the enterprise

• expects medium to long-term gains and

• does not expect any collateral to cover the capital provided

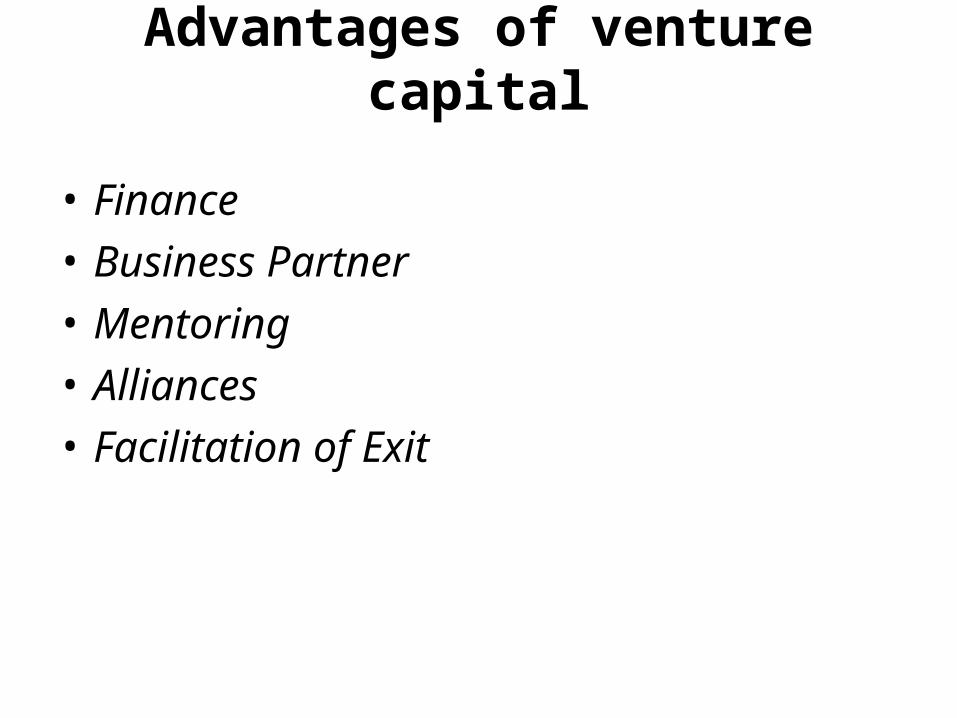

Advantages of venture capital

• Finance

• Business Partner

• Mentoring

• Alliances

• Facilitation of Exit

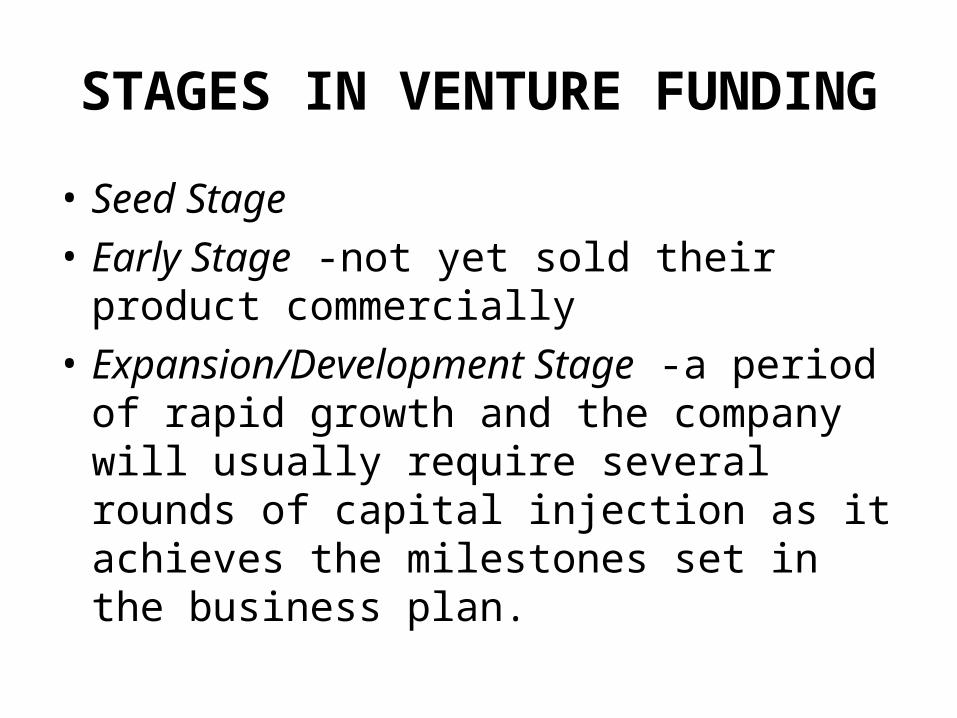

STAGES IN VENTURE FUNDING

• Seed Stage

• Early Stage -not yet sold their product commercially

• Expansion/Development Stage -a period of rapid growth and the company will usually require several rounds of capital injection as it achieves the milestones set in the business plan.

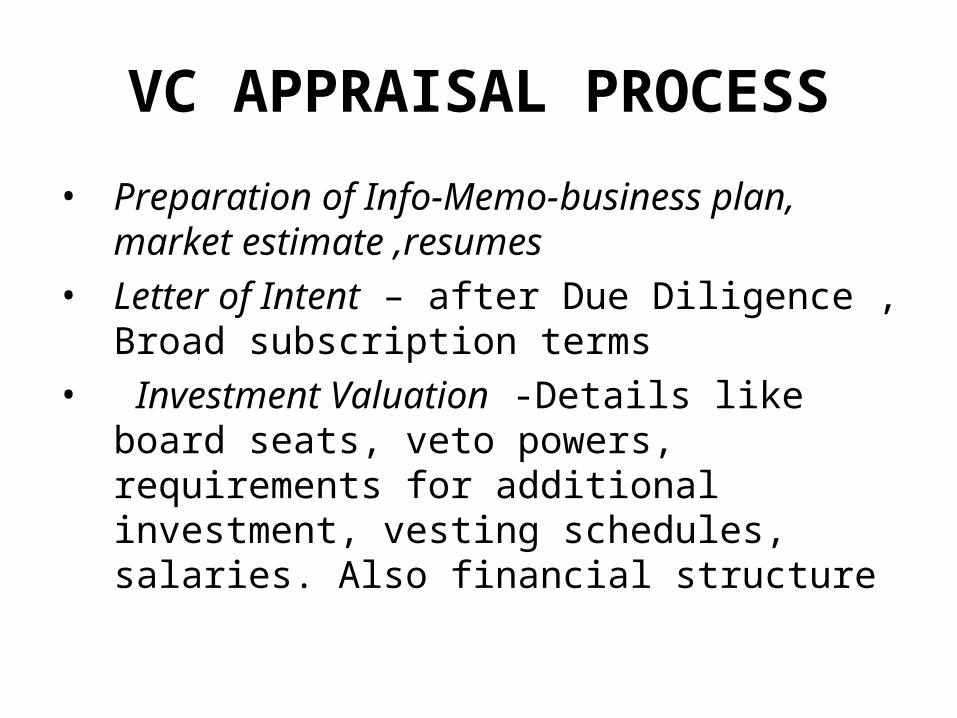

VC APPRAISAL PROCESS

• Preparation of Info-Memo-business plan, market estimate ,resumes

• Letter of Intent – after Due Diligence , Broad subscription terms

• Investment Valuation -Details like board seats, veto powers, requirements for additional investment, vesting schedules, salaries. Also financial structure

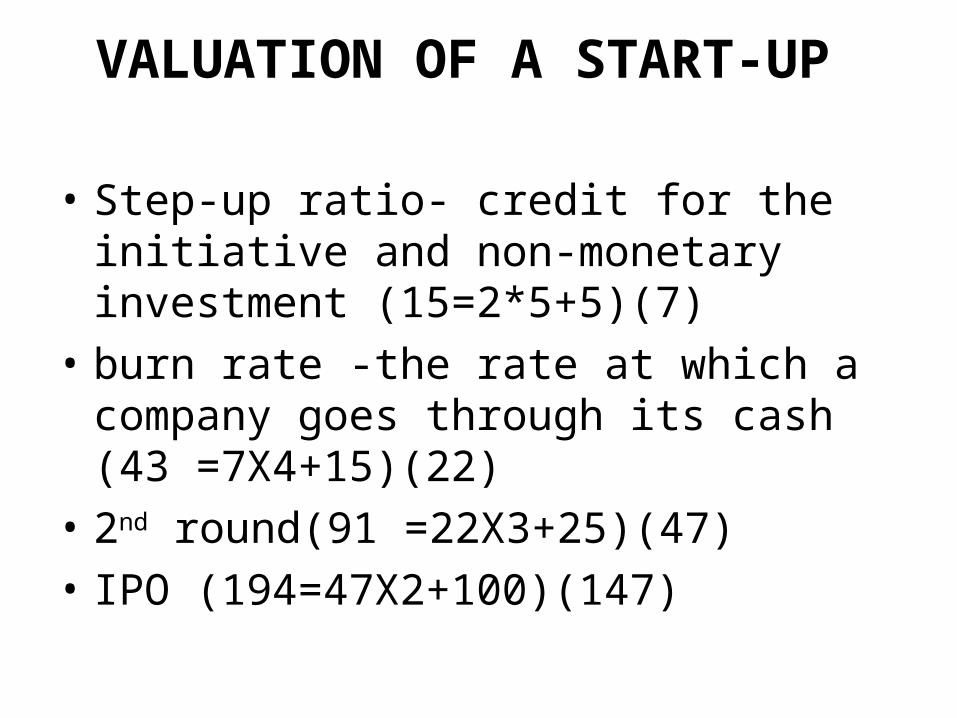

VALUATION OF A START-UP

• Step-up ratio- credit for the initiative and non-monetary investment (15=2*5+5)(7)

• burn rate -the rate at which a company goes through its cash (43 =7X4+15)(22)

• 2nd round(91 =22X3+25)(47)

• IPO (194=47X2+100)(147)

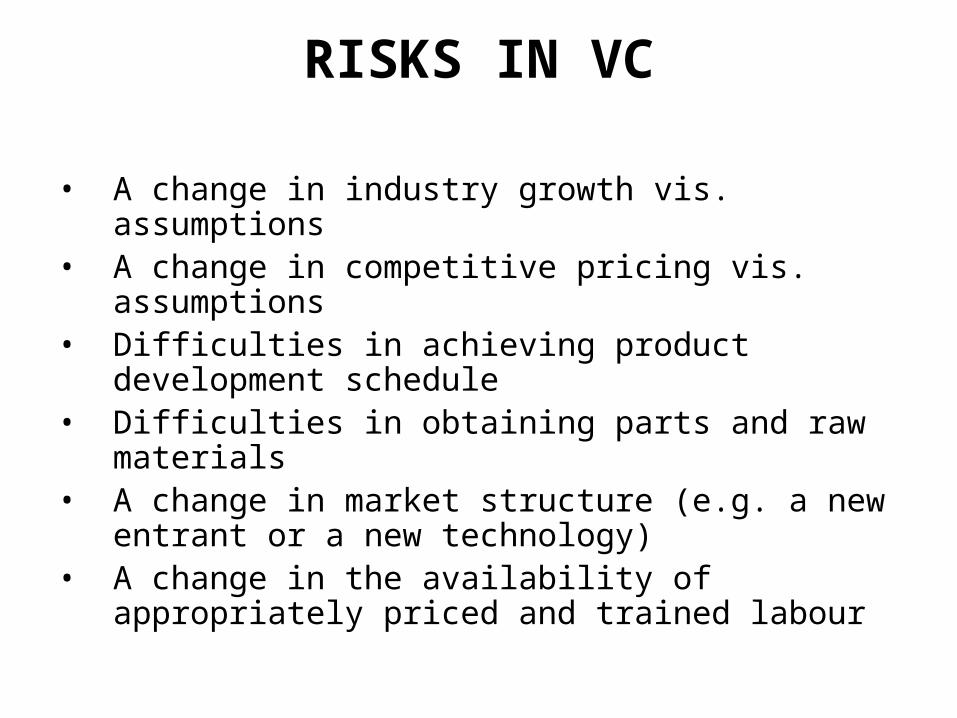

RISKS IN VC

• A change in industry growth vis. assumptions• A change in competitive pricing vis.

assumptions• Difficulties in achieving product development

schedule• Difficulties in obtaining parts and raw materials• A change in market structure (e.g. a new

entrant or a new technology)• A change in the availability of appropriately

priced and trained labour

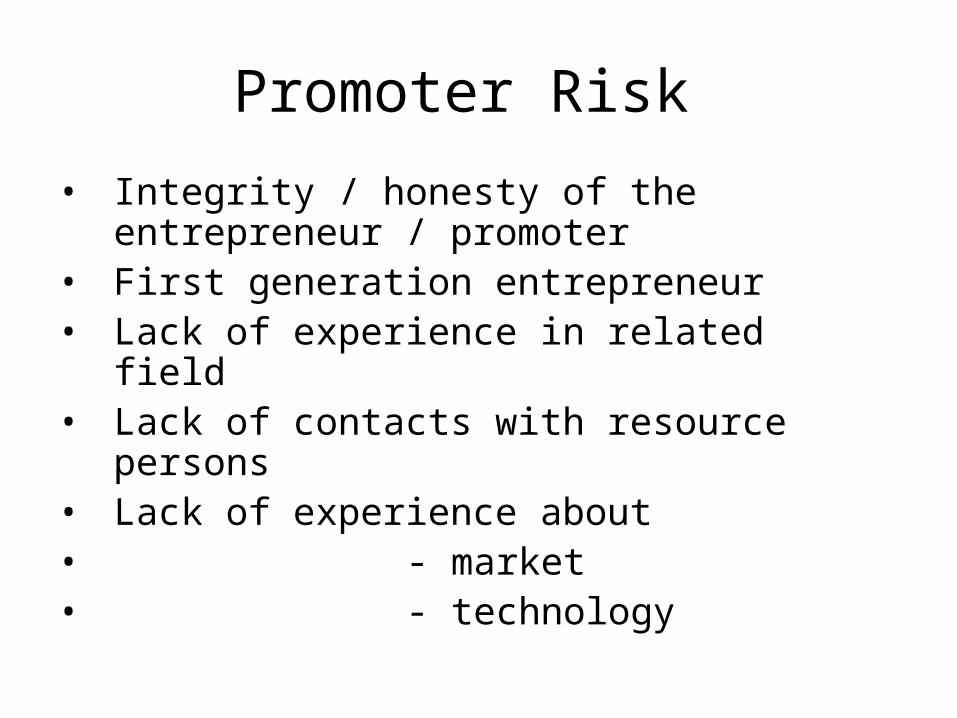

Promoter Risk

• Integrity / honesty of the entrepreneur / promoter

• First generation entrepreneur• Lack of experience in related field• Lack of contacts with resource persons• Lack of experience about• - market• - technology

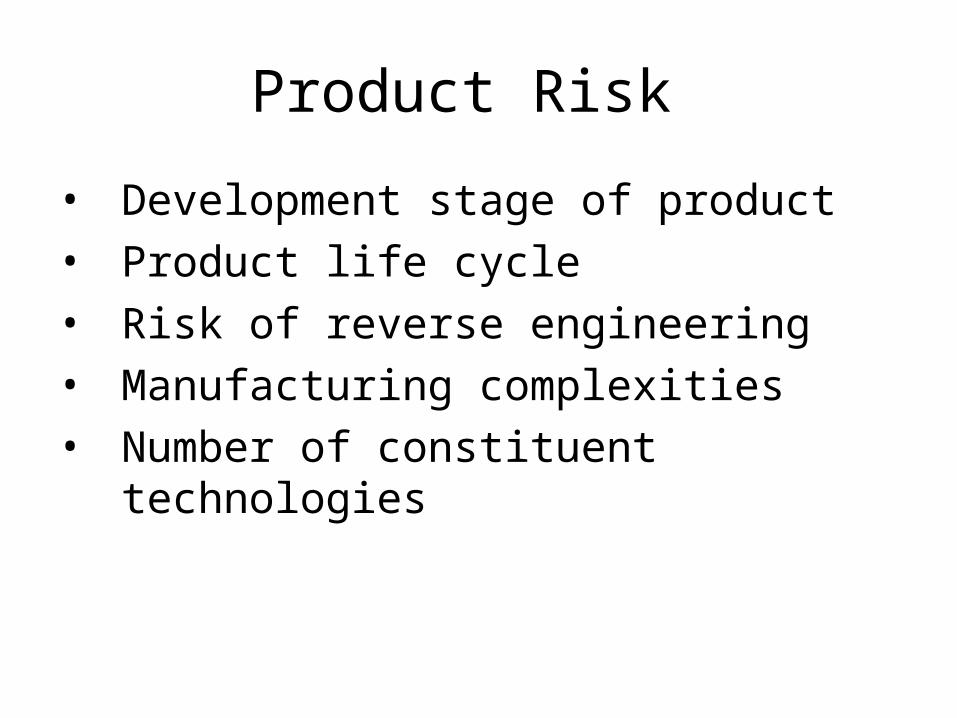

Product Risk

• Development stage of product

• Product life cycle

• Risk of reverse engineering

• Manufacturing complexities

• Number of constituent technologies

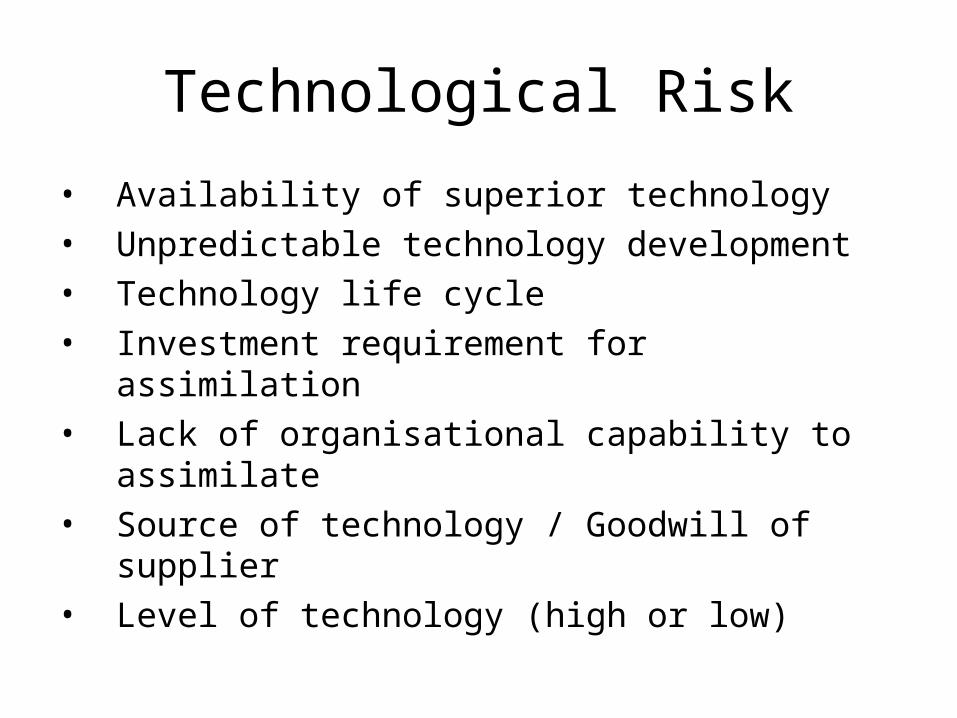

Technological Risk

• Availability of superior technology• Unpredictable technology development• Technology life cycle• Investment requirement for assimilation• Lack of organisational capability to assimilate• Source of technology / Goodwill of supplier• Level of technology (high or low)

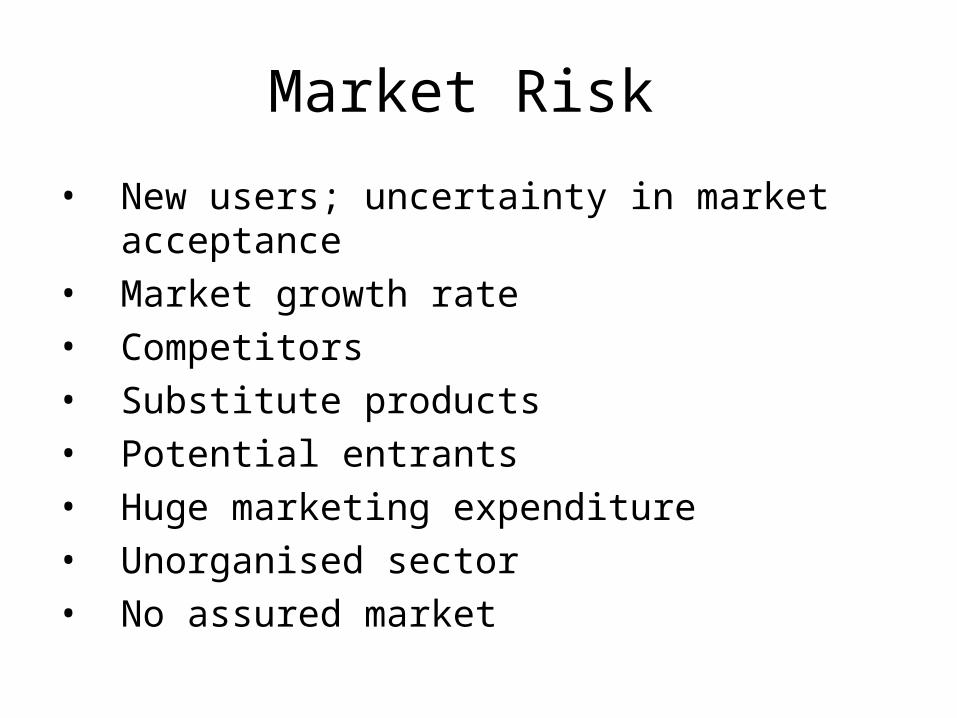

Market Risk

• New users; uncertainty in market acceptance• Market growth rate• Competitors • Substitute products• Potential entrants• Huge marketing expenditure• Unorganised sector• No assured market

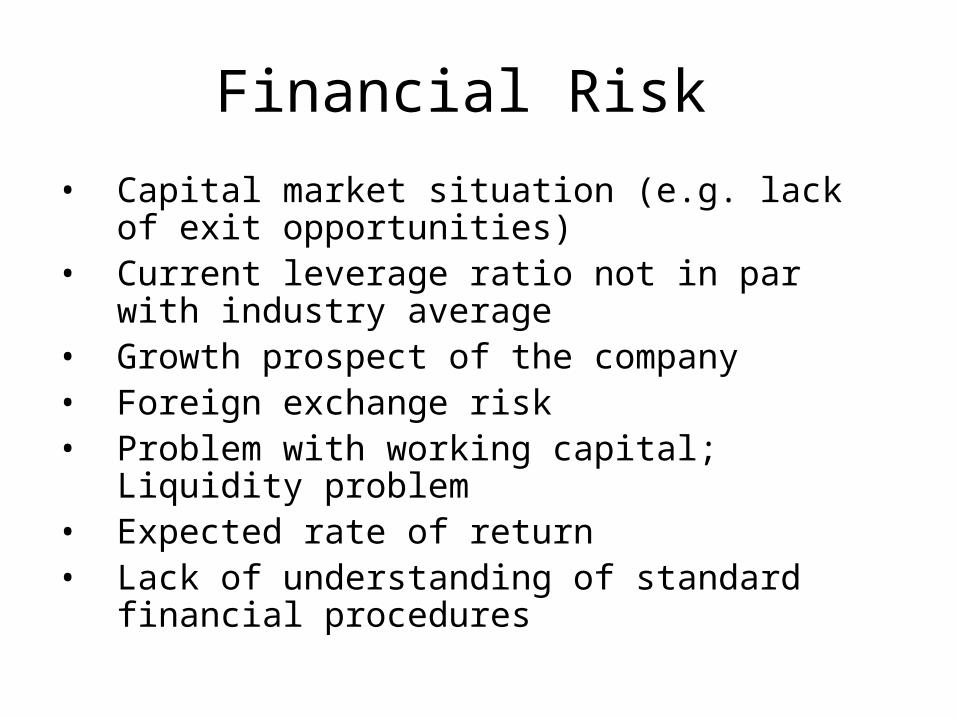

Financial Risk

• Capital market situation (e.g. lack of exit opportunities)

• Current leverage ratio not in par with industry average

• Growth prospect of the company• Foreign exchange risk• Problem with working capital; Liquidity problem• Expected rate of return• Lack of understanding of standard financial

procedures

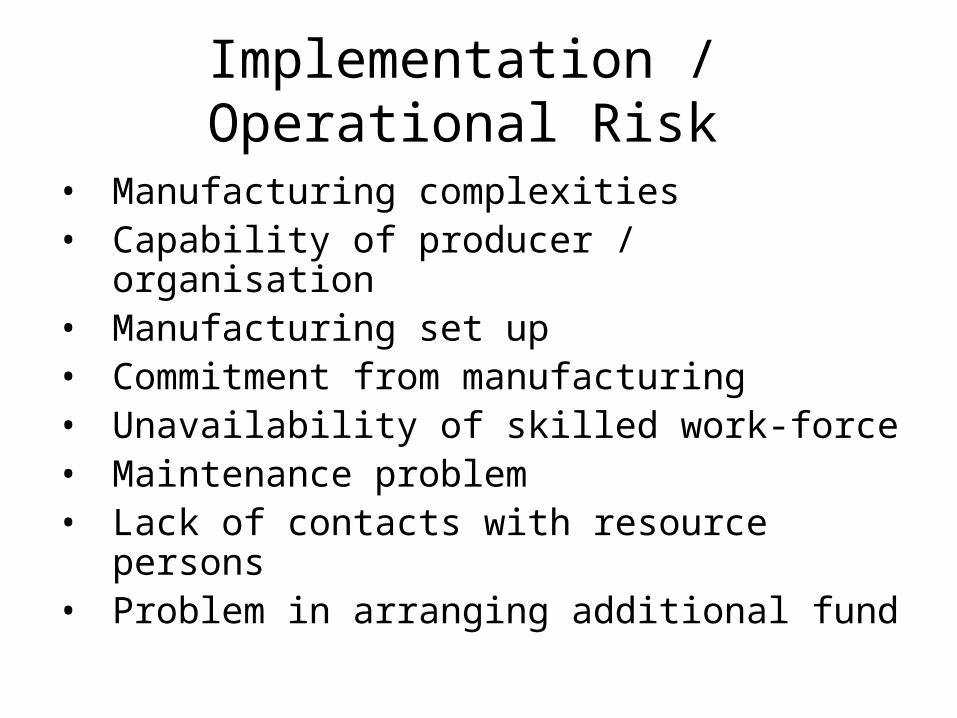

Implementation / Operational Risk

• Manufacturing complexities• Capability of producer / organisation• Manufacturing set up• Commitment from manufacturing• Unavailability of skilled work-force• Maintenance problem• Lack of contacts with resource persons• Problem in arranging additional fund

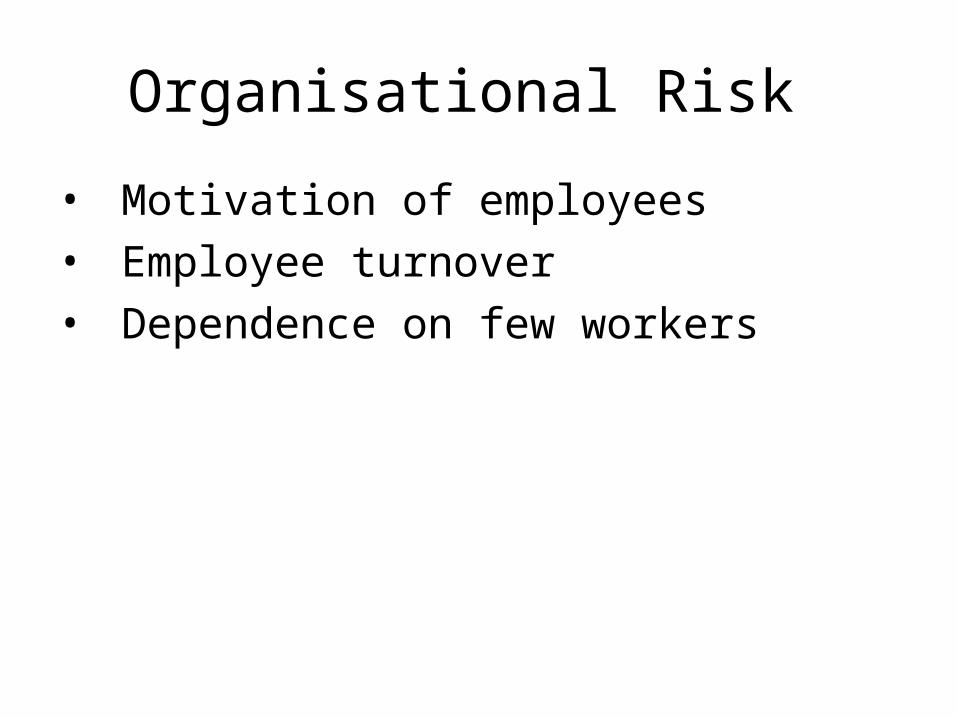

Organisational Risk

• Motivation of employees

• Employee turnover

• Dependence on few workers

Strategy Risk

• Loosing competitiveness

• Unrelated diversification

Environmental Risk

• Changes in Government policy

• Lack of understanding about regulations

• Pollution / hazard

• Availability of raw material

• Legal barriers - piracy / patent etc.

HOW TO IMPRESS A VENTURE CAPITALIST

VC Fundamentals-• The venture capital firm get paid first. Whether by

means of a liquidity event or the liquidation of the company in the event of failure, the VC firm will get paid first.

• Participation in the upside of the venture. The VC will benefit from the appreciation in value of the venture over and above the original investment.

• Control over critical events. VC will want to have decision rights in matters that vitally affect the business, such as the decision to do an IPO.

• Creation of a path to liquidity. There must be a way for the VC to cash out of the venture.

Other factors

• Winning Team

• Financials -Hockey Stick Appoach

requires an investment of 20 L over a 3 year period. VC expects a return of 5 times . PAT-30L.P/E-10

VC share= 20X5/ 30X10= 100/300= 33.3 %