fundamentals valuation - credit rating agency, … auto ltd.pdf · forging company in india, ......

TRANSCRIPT

FUNDAMENTALS VALUATION

AMTEK AUTO LIMITED

16th

February 2011

ANALYTICAL CONTACT

Ms. Revati Kasture +91-22-6754 3465 [email protected]

BUSINESS DEVELOPMENT CONTACTS

MUMBAI

Mr. P. N. Satheeskumar +91-22-6754 3555 [email protected]

KOLKATA

Mr. Sukanta Nag +91-33- 2283 1800 [email protected]

CHENNAI

Mr. V Pradeep Kumar +91-44-2849 7812 [email protected]

AHMEDABAD

Mr. Mehul Pandya +91-79-40265656 [email protected]

NEW DELHI

Ms. Swati Agrawal +91- 11- 2331 8701 [email protected]

BANGALORE

Mr. G. Sundara Vathanan +91-80-2211 7140 [email protected]

HYDERABAD

Mr. Ashwini Kumar Jani +91-40-40102030 [email protected]

CARE EQUITY RESEARCH OFFERS

Independent Research of equities on fundamentals or valuations or both

IPO Grading

White Label Research

Valuation of companies for Institutional Investors, Asset Managers and Corporates

Sector Write-ups for Offer Documents of securities

AMTEK AUTO LIMITED

1 www.careratings.com

EQUIGRADE

EQUI-GRADE – Analytical Power for Investment Decisions

AMTEK AUTO LTD Auto Ancillaries

Very Good Fundamentals; Considerable Upside Potential CMP : Rs. 118 / CIV : Rs. 178 1

16 February 2011

CARE Equity Research assigns 4/5 on fundamental grade to Amtek Auto

Limited (AAL)

CARE Equity Research assigns fundamental grade of 4/5 to AAL. This

indicates „Very Good Fundamentals‟. AAL is the only Indian company

with integrated component manufacturing facilities across forging,

aluminum casting, machining and sub-assembly of auto and non-auto

components. AAL is the largest machining company and second largest

forging company in India, with diversified product and client mix. It holds

leadership position in some of the critical components like connecting

rods, fly-wheels, ring gears etc. amongst others.

However, it has to cope with the challenges of volatile demand from

cyclical automobile industry and volatile input costs, which currently are on

the rising trend. Foray into railway wagons and defence sector would help

AAL mitigate the risks of volatility in demand to some extent. CARE

Equity Research believes that AAL‟s foreign subsidiaries are a drag on it,

despite the worst being a matter of the past and situation improving for

them. The Amtek Group is the process of restructuring the promoter

holding, with AAL as its flagship company, but the final structure remains

uncertain as of now. There is also imminent dilution of the equity in the

short term on account of the same.

Valuation

CARE Equity Research assigns valuation grade of 5/5 to AAL based on the

current Intrinsic Value (CIV) of Rs. 178 arrived at by using a mix of DCF,

EV/EBITDA and P/E methodologies as against Current Market Price

(CMP) of 118, indicating „Considerable Upside Potential‟ from CMP.

Consolidated Financial Information Snapshot1

(Rs Crore) FY09 FY10 FY11 P FY12 P Operating Income 3,439 3,691 4,796 6,313 EBITDA 700 908 1,132 1,442 Ordinary PAT (After minority interest) 173 240 430 619 Fully Diluted EPS* (Rs.) 10.2 11.8 16.6 23.9 Dividend Per Share (Rs.) 0.5 1.0 2.1 3.1 P/E (times)

10.0 7.1 5.0

EV/EBITDA (times) 6.1 4.9 3.8 1 Year ending 30th June

* Calculated on Current Face Value of Rs. 2/- per share

AMTEK AUTO LIMITED

www.careratings.com 2

EQUIGRADE

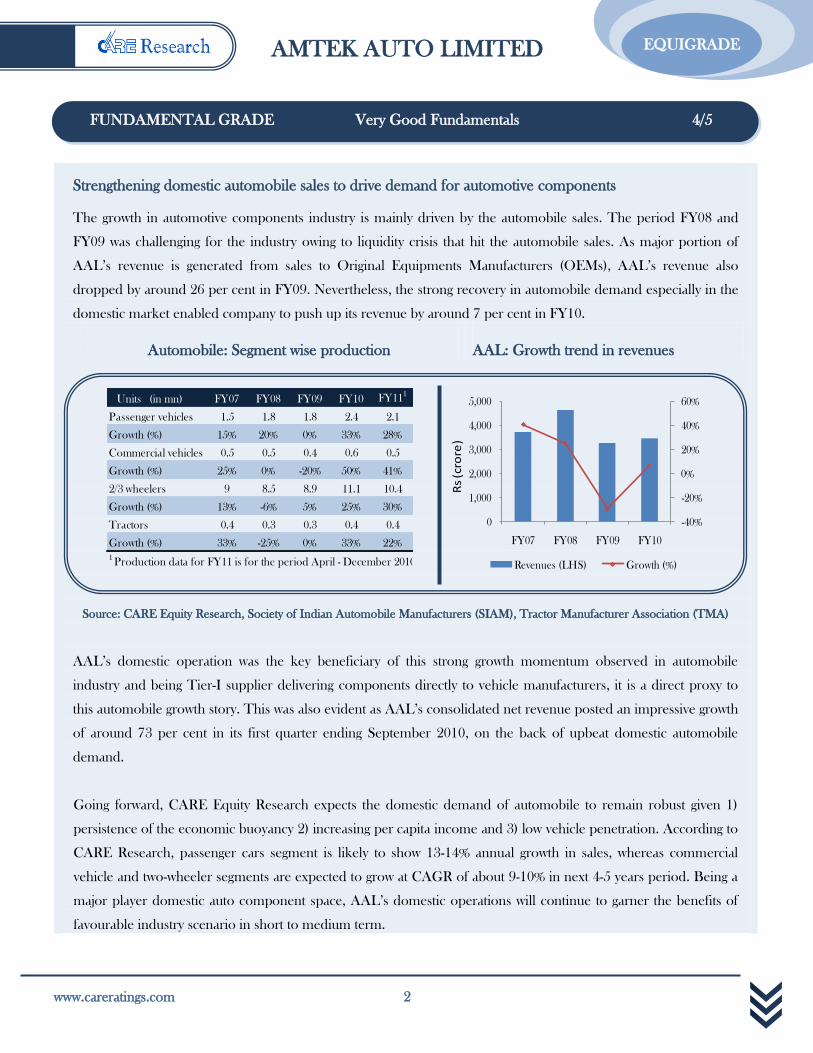

Strengthening domestic automobile sales to drive demand for automotive components

The growth in automotive components industry is mainly driven by the automobile sales. The period FY08 and

FY09 was challenging for the industry owing to liquidity crisis that hit the automobile sales. As major portion of

AAL‟s revenue is generated from sales to Original Equipments Manufacturers (OEMs), AAL‟s revenue also

dropped by around 26 per cent in FY09. Nevertheless, the strong recovery in automobile demand especially in the

domestic market enabled company to push up its revenue by around 7 per cent in FY10.

Automobile: Segment wise production

AAL: Growth trend in revenues

Source: CARE Equity Research, Society of Indian Automobile Manufacturers (SIAM), Tractor Manufacturer Association (TMA)

AAL‟s domestic operation was the key beneficiary of this strong growth momentum observed in automobile

industry and being Tier-I supplier delivering components directly to vehicle manufacturers, it is a direct proxy to

this automobile growth story. This was also evident as AAL‟s consolidated net revenue posted an impressive growth

of around 73 per cent in its first quarter ending September 2010, on the back of upbeat domestic automobile

demand.

Going forward, CARE Equity Research expects the domestic demand of automobile to remain robust given 1)

persistence of the economic buoyancy 2) increasing per capita income and 3) low vehicle penetration. According to

CARE Research, passenger cars segment is likely to show 13-14% annual growth in sales, whereas commercial

vehicle and two-wheeler segments are expected to grow at CAGR of about 9-10% in next 4-5 years period. Being a

major player domestic auto component space, AAL‟s domestic operations will continue to garner the benefits of

favourable industry scenario in short to medium term.

FUNDAMENTAL GRADE Very Good Fundamentals 4/5

Units (in mn) FY07 FY08 FY09 FY10 FY111

Passenger vehicles 1.5 1.8 1.8 2.4 2.1

Growth (%) 15% 20% 0% 33% 28%

Commercial vehicles 0.5 0.5 0.4 0.6 0.5

Growth (%) 25% 0% -20% 50% 41%

2/3 wheelers 9 8.5 8.9 11.1 10.4

Growth (%) 13% -6% 5% 25% 30%

Tractors 0.4 0.3 0.3 0.4 0.4

Growth (%) 33% -25% 0% 33% 22%

1 Production data for FY11 is for the period April - December 2010

-40%

-20%

0%

20%

40%

60%

0

1,000

2,000

3,000

4,000

5,000

FY07 FY08 FY09 FY10

Revenues (LHS) Growth (%)

Rs

(cro

re)

AMTEK AUTO LIMITED

3 www.careratings.com

EQUIGRADE

Presence in all three segments casting, forging and machining enables process integration

AAL‟s presence in all the three segments – Casting, Forging and Machining enables the company to exist in entire

value chain of its product offerings though sophisticated technology is critical for manufacturing AAL‟s products for

engine, transmission, suspension & chassis. Also, the existence in all three segments enables effective cost control

through process integration which is detailed below:

i. The company enjoys diverse product offering components which are high technology , long life, and safety

components that are manufactured through casting and forging process.

ii. Machining involves processing of components manufactured through casting and forging as per the

specification of the buyers. This capability enables AAL to reap benefits through increased realisation

owing to high value addition combined with process integration and less wastages.

Snapshot of AAL‟s value chain

Source: CARE Equity Research

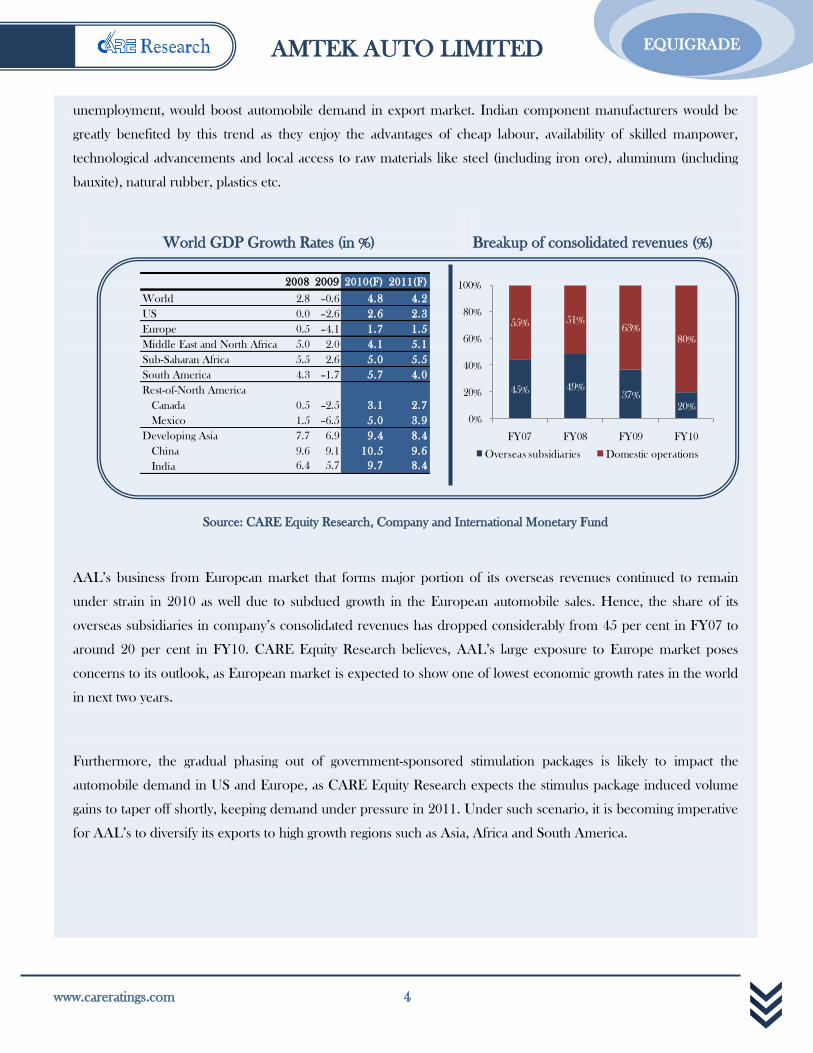

Global economic recovery to boost export potential

AAL‟s revenue mix is geographically diversified into Europe, U.S. and India. Share of direct exports in the total

revenue mix declined substantially from 37% in FY09 to merely 20% in FY10 on the back of difficult market

conditions especially in Europe.

However, going forward, CARE Equity Research believes that worst is over for the global automobile segment. The

global economy is projected to grow at healthy rates of 4.8% in 2010 and 4.2% in 2011, as per International

Monetary Fund (IMF) estimates. This growth, along with rising consumer confidence and easing levels of

Ingots,

BarsRaw materials

Casting Forging

Machining

End-

Users

Hot press &

Cold pressAluminium

OEMs &

Tier I suppliers

Aluminium

AMTEK AUTO LIMITED

www.careratings.com 4

EQUIGRADE

unemployment, would boost automobile demand in export market. Indian component manufacturers would be

greatly benefited by this trend as they enjoy the advantages of cheap labour, availability of skilled manpower,

technological advancements and local access to raw materials like steel (including iron ore), aluminum (including

bauxite), natural rubber, plastics etc.

World GDP Growth Rates (in %)

Breakup of consolidated revenues (%)

Source: CARE Equity Research, Company and International Monetary Fund

AAL‟s business from European market that forms major portion of its overseas revenues continued to remain

under strain in 2010 as well due to subdued growth in the European automobile sales. Hence, the share of its

overseas subsidiaries in company‟s consolidated revenues has dropped considerably from 45 per cent in FY07 to

around 20 per cent in FY10. CARE Equity Research believes, AAL‟s large exposure to Europe market poses

concerns to its outlook, as European market is expected to show one of lowest economic growth rates in the world

in next two years.

Furthermore, the gradual phasing out of government-sponsored stimulation packages is likely to impact the

automobile demand in US and Europe, as CARE Equity Research expects the stimulus package induced volume

gains to taper off shortly, keeping demand under pressure in 2011. Under such scenario, it is becoming imperative

for AAL‟s to diversify its exports to high growth regions such as Asia, Africa and South America.

2008 2009 2010(F) 2011(F)

World 2.8 –0.6 4.8 4.2

US 0.0 –2.6 2.6 2.3

Europe 0.5 –4.1 1.7 1.5

Middle East and North Africa 5.0 2.0 4.1 5.1

Sub-Saharan Africa 5.5 2.6 5.0 5.5

South America 4.3 –1.7 5.7 4.0

Rest-of-North America

Canada 0.5 –2.5 3.1 2.7

Mexico 1.5 –6.5 5.0 3.9

Developing Asia 7.7 6.9 9.4 8.4

China 9.6 9.1 10.5 9.6

India 6.4 5.7 9.7 8.4

45% 49%37%

20%

55% 51%63%

80%

0%

20%

40%

60%

80%

100%

FY07 FY08 FY09 FY10

Overseas subsidiaries Domestic operations

AMTEK AUTO LIMITED

5 www.careratings.com

EQUIGRADE

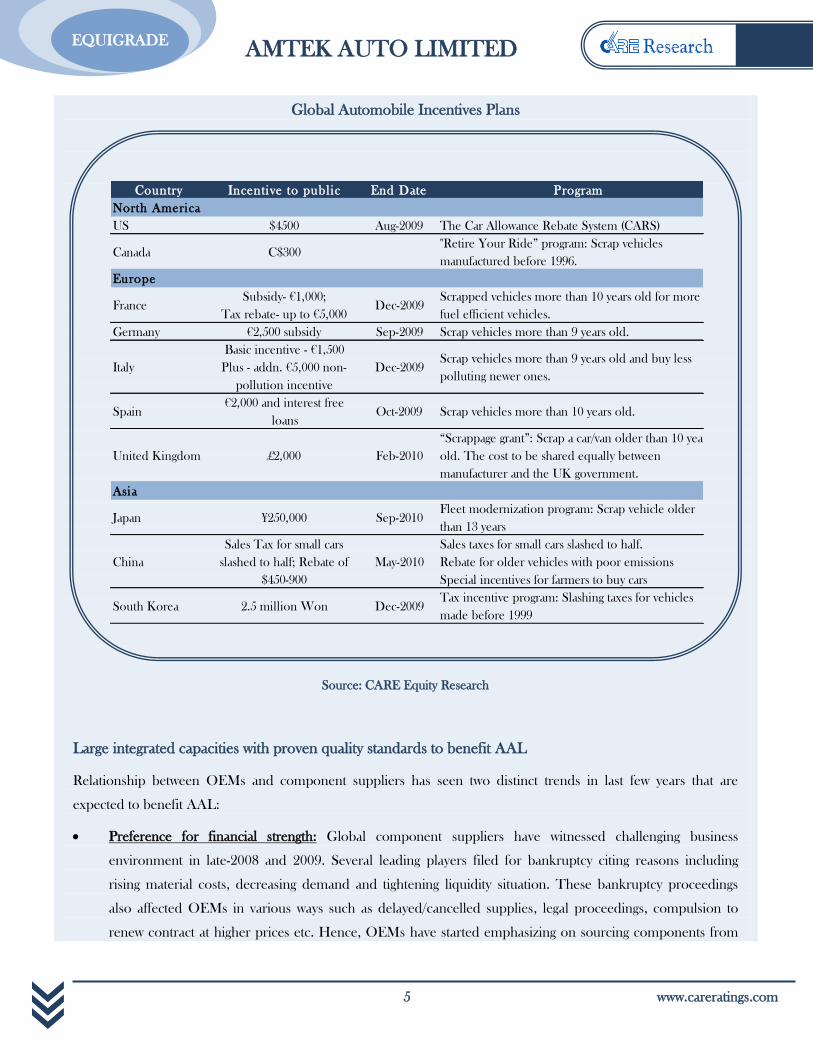

Global Automobile Incentives Plans

Source: CARE Equity Research

Large integrated capacities with proven quality standards to benefit AAL

Relationship between OEMs and component suppliers has seen two distinct trends in last few years that are

expected to benefit AAL:

Preference for financial strength: Global component suppliers have witnessed challenging business

environment in late-2008 and 2009. Several leading players filed for bankruptcy citing reasons including

rising material costs, decreasing demand and tightening liquidity situation. These bankruptcy proceedings

also affected OEMs in various ways such as delayed/cancelled supplies, legal proceedings, compulsion to

renew contract at higher prices etc. Hence, OEMs have started emphasizing on sourcing components from

Country Incentive to public End Date Program

North America

US $4500 Aug-2009 The Car Allowance Rebate System (CARS)

Canada C$300"Retire Your Ride” program: Scrap vehicles

manufactured before 1996.

Europe

FranceSubsidy- €1,000;

Tax rebate- up to €5,000 Dec-2009

Scrapped vehicles more than 10 years old for more

fuel efficient vehicles.

Germany €2,500 subsidy Sep-2009 Scrap vehicles more than 9 years old.

Italy

Basic incentive - €1,500

Plus - addn. €5,000 non-

pollution incentive

Dec-2009Scrap vehicles more than 9 years old and buy less

polluting newer ones.

Spain€2,000 and interest free

loansOct-2009 Scrap vehicles more than 10 years old.

United Kingdom £2,000 Feb-2010

“Scrappage grant”: Scrap a car/van older than 10 years

old. The cost to be shared equally between

manufacturer and the UK government.

Asia

Japan ¥250,000 Sep-2010Fleet modernization program: Scrap vehicle older

than 13 years

China

Sales Tax for small cars

slashed to half; Rebate of

$450-900

May-2010

Sales taxes for small cars slashed to half.

Rebate for older vehicles with poor emissions

Special incentives for farmers to buy cars

South Korea 2.5 million Won Dec-2009Tax incentive program: Slashing taxes for vehicles

made before 1999

AMTEK AUTO LIMITED

www.careratings.com 6

EQUIGRADE

financially healthy suppliers that can become reliable long-term partners. CARE Ratings has reaffirmed

„CARE AA‟ (Double A) to long-term bank facilities of AAL in August 2010, which is “considered to offer

high safety for timely servicing of debt obligations”.

Technological collaborations: Stringent emission norms along with rising competition in the market have

compelled OEMs to be more open towards technological collaborations with component suppliers. AAL is

likely to be one of the key beneficiaries of this trend as it is the only Indian company to have integrated

component-manufacturing facilities across forging, casting (Aluminum), machining and sub-assemblies.

Furthermore, in-house design and product development facilities would help AAL in consolidating its

position as stable and low cost partner.

Wide product range and diversified customer base reduces concentration risk …

Amtek group has a wide product range including automotive components such as cylinder blocks/heads,

crankshafts, front axle beams, connecting rods, flywheels, ring gears, knuckles and non-automotive products for

railway components. Furthermore, the company has also diversified its customer base with no customer

contributing more than 15 per cent to its revenue. However, as more than 80 per cent of the consolidated revenues

are generated from the auto component business, company‟s growth is greatly influenced by the volatile demand

from cyclical automobile industry.

…however, increasing focus on non-automotive segment a positive step forward

Non-automotive business contributed about 18 per cent of the group‟s consolidated revenue in FY10. The

company is aiming to increase the share of non-auto segment to 25 per cent of total revenue in next 4 years. CARE

Equity Research views increasing focus on non-automotive segment positively, as it would not only lead to greater

diversification and better returns of its business but also will provide cushion against the cyclical automobile

demand.

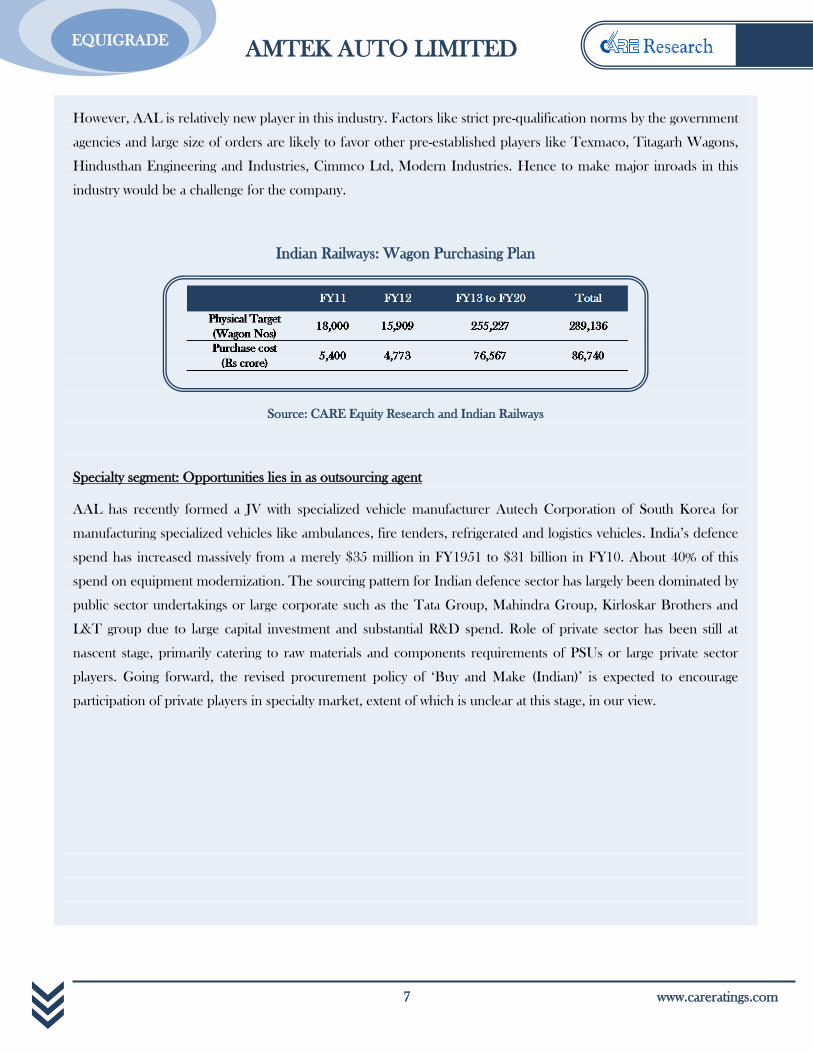

Railway wagon segment: growth opportunity but task uphill

AAL has entered into a joint venture (JV) with American Railcar Industries (USA) to set up a railway wagon

manufacturing facility near Chandigarh. The Government of India (GOI) has rolled out aggressive plans to procure

33,909 wagons till FY12 and around 2,55,227 wagon through FY13-20 period. Hence at a price of Rs 30 lacs per

wagon, the total purchases would aggregates to around Rs10,173 crore till FY12.

AMTEK AUTO LIMITED

7 www.careratings.com

EQUIGRADE

However, AAL is relatively new player in this industry. Factors like strict pre-qualification norms by the government

agencies and large size of orders are likely to favor other pre-established players like Texmaco, Titagarh Wagons,

Hindusthan Engineering and Industries, Cimmco Ltd, Modern Industries. Hence to make major inroads in this

industry would be a challenge for the company.

Indian Railways: Wagon Purchasing Plan

Source: CARE Equity Research and Indian Railways

Specialty segment: Opportunities lies in as outsourcing agent

AAL has recently formed a JV with specialized vehicle manufacturer Autech Corporation of South Korea for

manufacturing specialized vehicles like ambulances, fire tenders, refrigerated and logistics vehicles. India‟s defence

spend has increased massively from a merely $35 million in FY1951 to $31 billion in FY10. About 40% of this

spend on equipment modernization. The sourcing pattern for Indian defence sector has largely been dominated by

public sector undertakings or large corporate such as the Tata Group, Mahindra Group, Kirloskar Brothers and

L&T group due to large capital investment and substantial R&D spend. Role of private sector has been still at

nascent stage, primarily catering to raw materials and components requirements of PSUs or large private sector

players. Going forward, the revised procurement policy of „Buy and Make (Indian)‟ is expected to encourage

participation of private players in specialty market, extent of which is unclear at this stage, in our view.

AMTEK AUTO LIMITED

www.careratings.com 8

EQUIGRADE

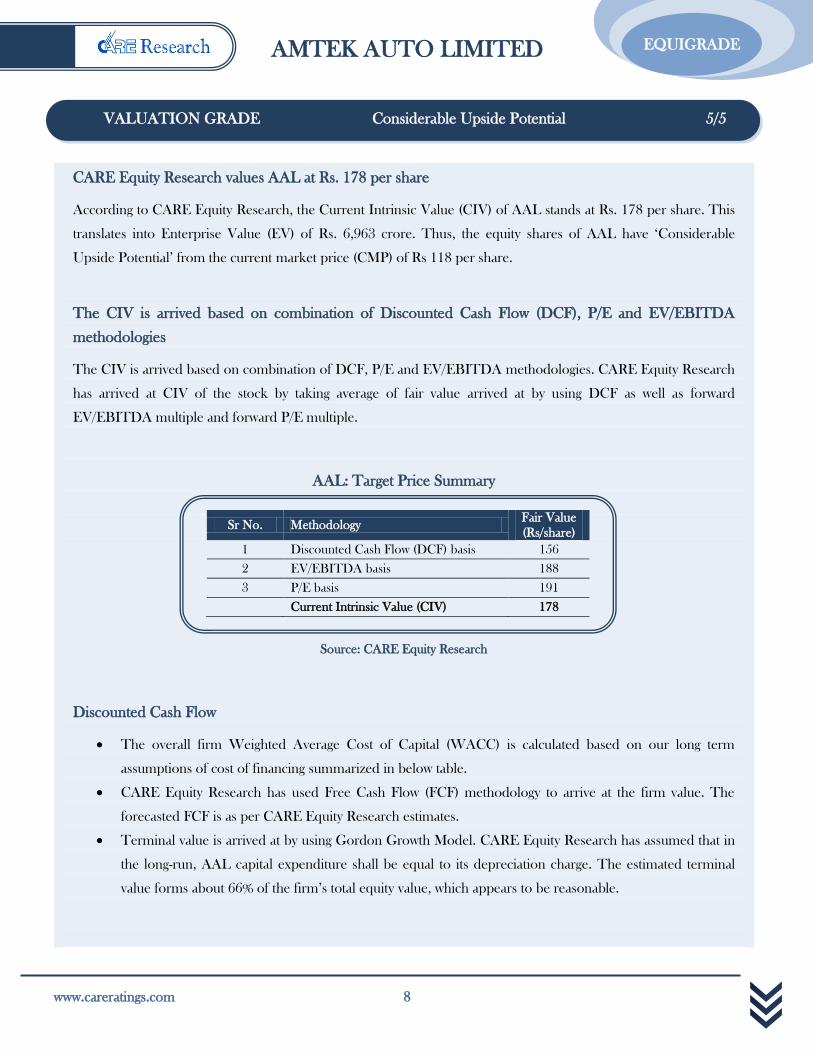

CARE Equity Research values AAL at Rs. 178 per share

According to CARE Equity Research, the Current Intrinsic Value (CIV) of AAL stands at Rs. 178 per share. This

translates into Enterprise Value (EV) of Rs. 6,963 crore. Thus, the equity shares of AAL have „Considerable

Upside Potential‟ from the current market price (CMP) of Rs 118 per share.

The CIV is arrived based on combination of Discounted Cash Flow (DCF), P/E and EV/EBITDA

methodologies

The CIV is arrived based on combination of DCF, P/E and EV/EBITDA methodologies. CARE Equity Research

has arrived at CIV of the stock by taking average of fair value arrived at by using DCF as well as forward

EV/EBITDA multiple and forward P/E multiple.

AAL: Target Price Summary

Source: CARE Equity Research

Discounted Cash Flow

The overall firm Weighted Average Cost of Capital (WACC) is calculated based on our long term

assumptions of cost of financing summarized in below table.

CARE Equity Research has used Free Cash Flow (FCF) methodology to arrive at the firm value. The

forecasted FCF is as per CARE Equity Research estimates.

Terminal value is arrived at by using Gordon Growth Model. CARE Equity Research has assumed that in

the long-run, AAL capital expenditure shall be equal to its depreciation charge. The estimated terminal

value forms about 66% of the firm‟s total equity value, which appears to be reasonable.

VALUATION GRADE Considerable Upside Potential 5/5

Sr No. Methodology Fair Value

(Rs/share)

1 Discounted Cash Flow (DCF) basis 156

2 EV/EBITDA basis 188

3 P/E basis 191

Current Intrinsic Value (CIV) 178

AMTEK AUTO LIMITED

9 www.careratings.com

EQUIGRADE

AAL: Valuation Based on Discounted Cash Flows

Source: CARE Equity Research

AAL: Dilution of equity base

Note: Warrants are proposed to be issued to the promoters at conversion price of Rs. 180 per share

Source: CARE Equity Research

Item Value Basis

Risk Free Rate 8.25% 10 year G-sec yield expected at year end FY11

Equity Risk Premium 6.00%

Beta 1.03

Cost of Equity 14.41%

Cost of Debt 9.00% Long term cost of debt

Tax Rate 33.00% Long term tax rate

D/E Ratio 0.50 Long term target D/E ratio

WACC 11.61%

Terminal growth rate 3.00%

(Rs crore except per share data)

2010-11 2011-12 2012-13 2013-14 2014-15

PAT 430 619 980 1,542 1,823

Depreciation 327 336 345 354 363

Interest (1-T) 156 190 170 135 102

Capex -200 -200 -200 -200 -200

Increase in WC -413 -483 -438 -793 -1,302

Free Cash Flow 299 462 856 1,037 785

Discount Rate 0.95 0.85 0.76 0.68 0.61

PV of FCF 283 391 649 705 478

PV of Terminal Value 4,529

Total Discounted Value of Firm 7,035

Less: Net Debt (FY10) 2,984

Present Value of Equity 4,051

No of Equity Shares (crore) 26

Per Share 156

No. of Shares Crore

Fully Diluted - Sep'10

23.52

Add: Warrants: FY11

0.75

Add: Warrants: FY12

1.65

Total Diluted Equity Base 25.92

AMTEK AUTO LIMITED

www.careratings.com 10

EQUIGRADE

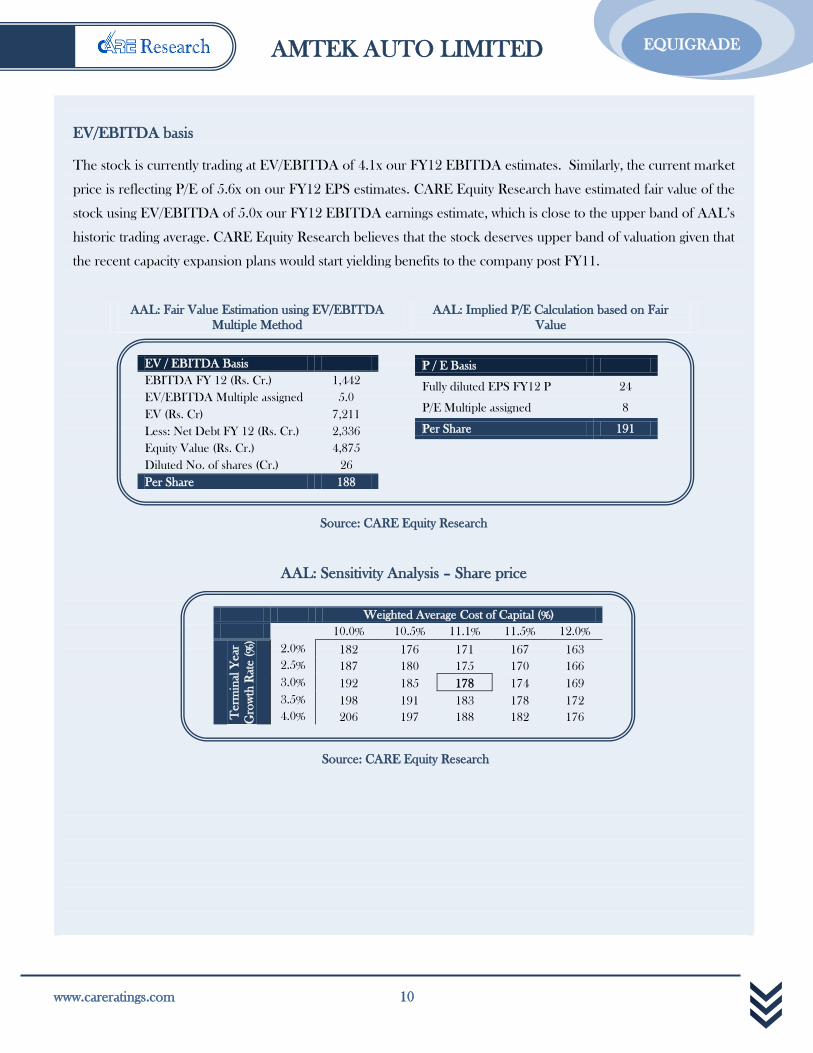

EV/EBITDA basis

The stock is currently trading at EV/EBITDA of 4.1x our FY12 EBITDA estimates. Similarly, the current market

price is reflecting P/E of 5.6x on our FY12 EPS estimates. CARE Equity Research have estimated fair value of the

stock using EV/EBITDA of 5.0x our FY12 EBITDA earnings estimate, which is close to the upper band of AAL‟s

historic trading average. CARE Equity Research believes that the stock deserves upper band of valuation given that

the recent capacity expansion plans would start yielding benefits to the company post FY11.

AAL: Fair Value Estimation using EV/EBITDA

Multiple Method AAL: Implied P/E Calculation based on Fair

Value

Source: CARE Equity Research

AAL: Sensitivity Analysis – Share price

Source: CARE Equity Research

EV / EBITDA Basis

EBITDA FY 12 (Rs. Cr.) 1,442

EV/EBITDA Multiple assigned 5.0

EV (Rs. Cr) 7,211

Less: Net Debt FY 12 (Rs. Cr.) 2,336

Equity Value (Rs. Cr.) 4,875

Diluted No. of shares (Cr.) 26

Per Share 188

P / E Basis

Fully diluted EPS FY12 P 24

P/E Multiple assigned 8

Per Share 191

Weighted Average Cost of Capital (%)

10.0% 10.5% 11.1% 11.5% 12.0%

Term

inal

Year

Gro

wth

Rat

e (

%)

2.0% 182 176 171 167 163

2.5% 187 180 175 170 166

3.0% 192 185 178 174 169

3.5% 198 191 183 178 172

4.0% 206 197 188 182 176

AMTEK AUTO LIMITED

11 www.careratings.com

EQUIGRADE

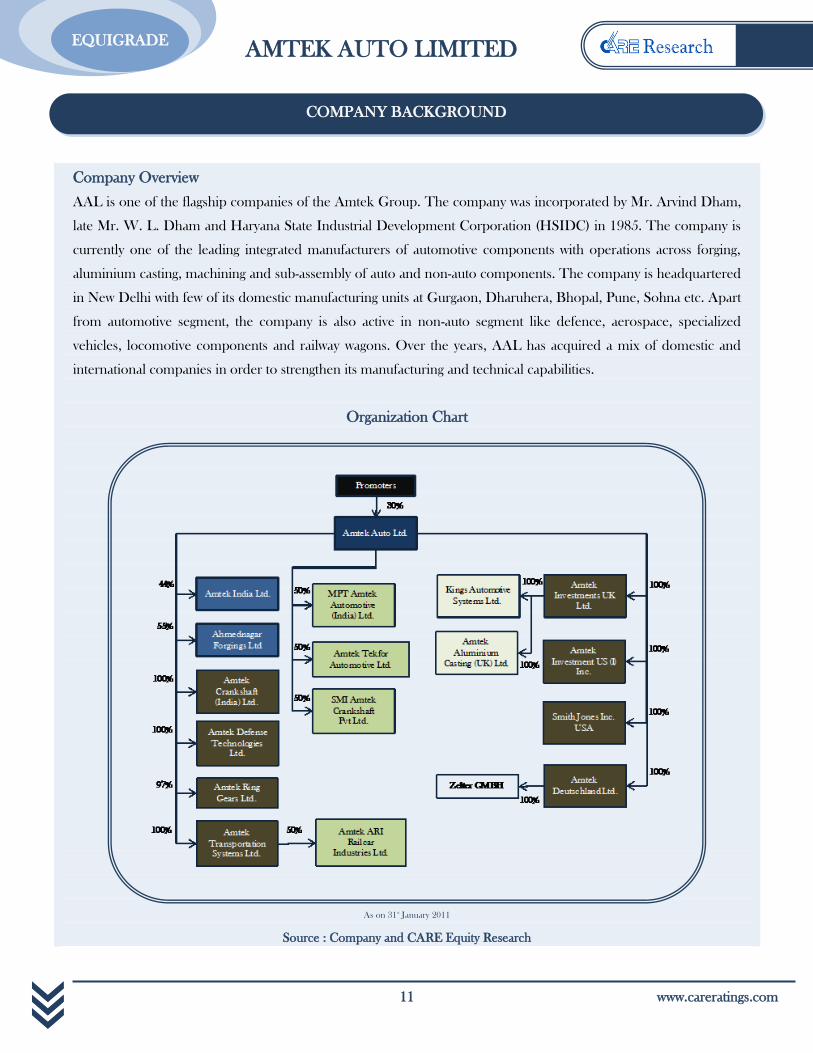

Company Overview

AAL is one of the flagship companies of the Amtek Group. The company was incorporated by Mr. Arvind Dham,

late Mr. W. L. Dham and Haryana State Industrial Development Corporation (HSIDC) in 1985. The company is

currently one of the leading integrated manufacturers of automotive components with operations across forging,

aluminium casting, machining and sub-assembly of auto and non-auto components. The company is headquartered

in New Delhi with few of its domestic manufacturing units at Gurgaon, Dharuhera, Bhopal, Pune, Sohna etc. Apart

from automotive segment, the company is also active in non-auto segment like defence, aerospace, specialized

vehicles, locomotive components and railway wagons. Over the years, AAL has acquired a mix of domestic and

international companies in order to strengthen its manufacturing and technical capabilities.

Organization Chart

As on 31st January 2011

Source : Company and CARE Equity Research

COMPANY BACKGROUND

AMTEK AUTO LIMITED

www.careratings.com 12

EQUIGRADE

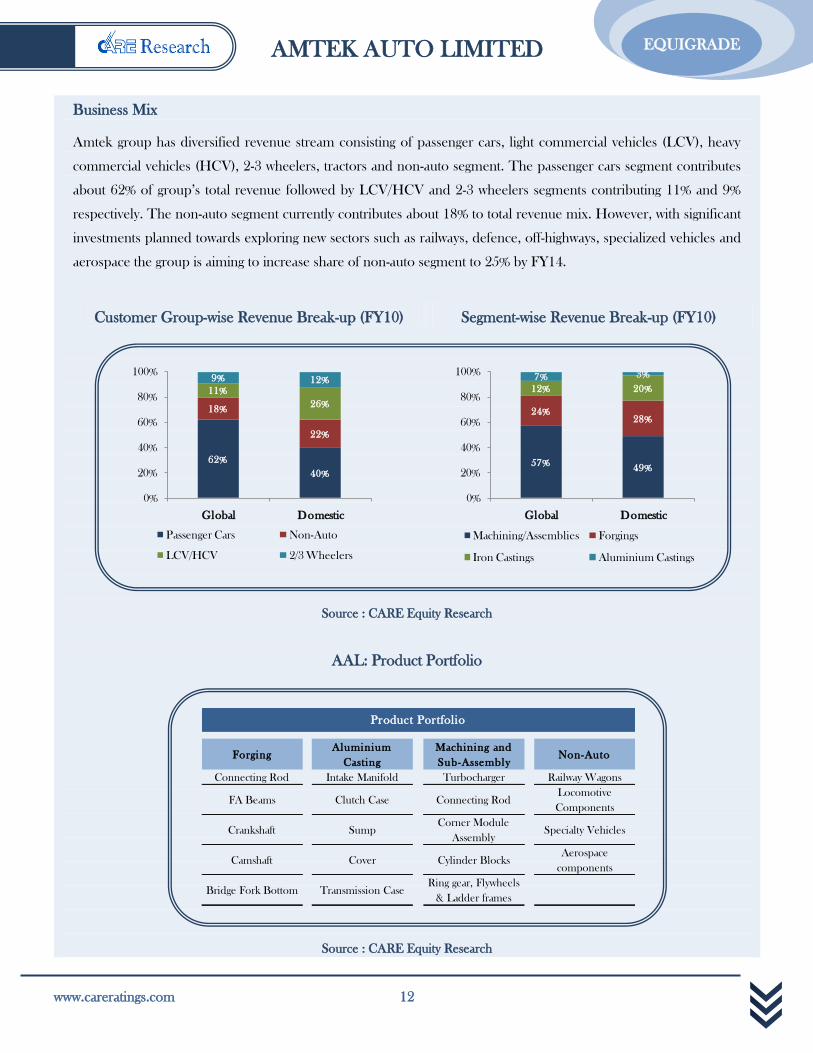

Business Mix

Amtek group has diversified revenue stream consisting of passenger cars, light commercial vehicles (LCV), heavy

commercial vehicles (HCV), 2-3 wheelers, tractors and non-auto segment. The passenger cars segment contributes

about 62% of group‟s total revenue followed by LCV/HCV and 2-3 wheelers segments contributing 11% and 9%

respectively. The non-auto segment currently contributes about 18% to total revenue mix. However, with significant

investments planned towards exploring new sectors such as railways, defence, off-highways, specialized vehicles and

aerospace the group is aiming to increase share of non-auto segment to 25% by FY14.

Customer Group-wise Revenue Break-up (FY10) Segment-wise Revenue Break-up (FY10)

Source : CARE Equity Research

AAL: Product Portfolio

Source : CARE Equity Research

62%

40%

18%

22%

11%

26%

9% 12%

0%

20%

40%

60%

80%

100%

Global Domestic

Passenger Cars Non-Auto

LCV/HCV 2/3 Wheelers

57%49%

24%28%

12% 20%

7% 3%

0%

20%

40%

60%

80%

100%

Global Domestic

Machining/Assemblies Forgings

Iron Castings Aluminium Castings

ForgingAluminium

Casting

Machining and

Sub-AssemblyNon-Auto

Connecting Rod Intake Manifold Turbocharger Railway Wagons

FA Beams Clutch Case Connecting RodLocomotive

Components

Crankshaft SumpCorner Module

AssemblySpecialty Vehicles

Camshaft Cover Cylinder BlocksAerospace

components

Bridge Fork Bottom Transmission CaseRing gear, Flywheels

& Ladder frames

Product Portfolio

AMTEK AUTO LIMITED

13 www.careratings.com

EQUIGRADE

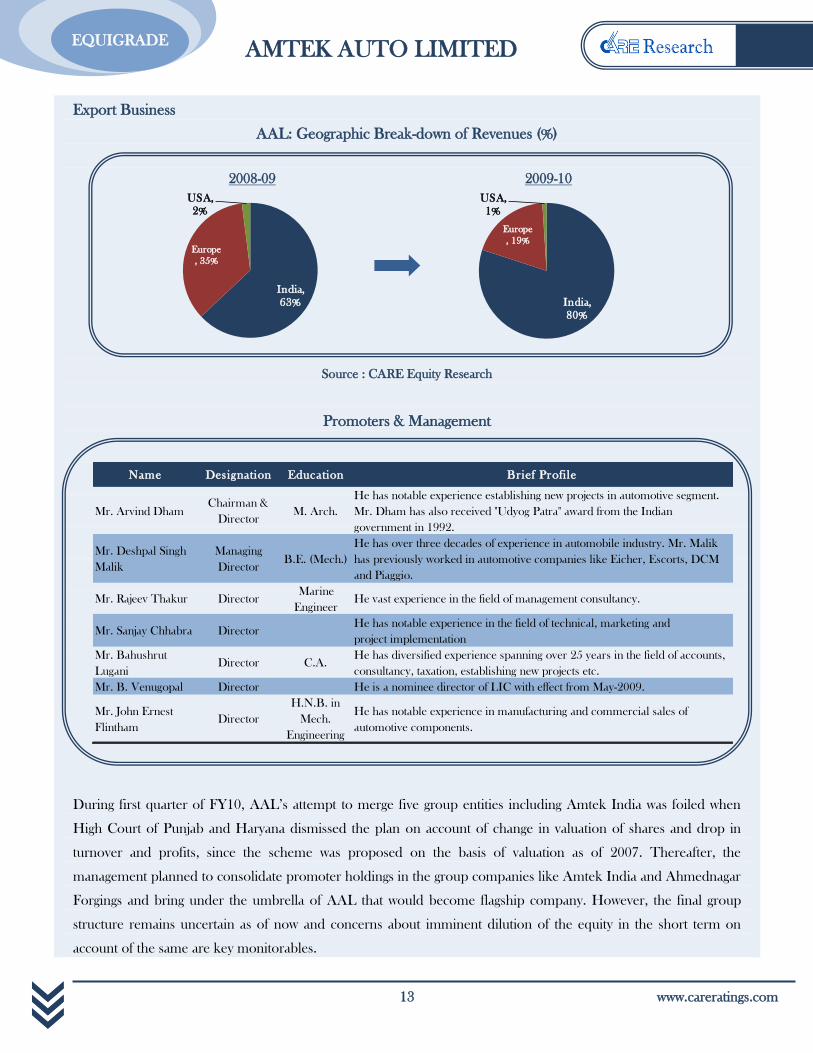

Export Business

AAL: Geographic Break-down of Revenues (%)

Source : CARE Equity Research

Promoters & Management

During first quarter of FY10, AAL‟s attempt to merge five group entities including Amtek India was foiled when

High Court of Punjab and Haryana dismissed the plan on account of change in valuation of shares and drop in

turnover and profits, since the scheme was proposed on the basis of valuation as of 2007. Thereafter, the

management planned to consolidate promoter holdings in the group companies like Amtek India and Ahmednagar

Forgings and bring under the umbrella of AAL that would become flagship company. However, the final group

structure remains uncertain as of now and concerns about imminent dilution of the equity in the short term on

account of the same are key monitorables.

2008-09 2009-10

India,

63%

Europe

, 35%

USA,

2%

India,

80%

Europe

, 19%

USA,

1%

Name Designation Education Brief Profile

Mr. Arvind DhamChairman &

DirectorM. Arch.

He has notable experience establishing new projects in automotive segment.

Mr. Dham has also received "Udyog Patra" award from the Indian

government in 1992.

Mr. Deshpal Singh

Malik

Managing

DirectorB.E. (Mech.)

He has over three decades of experience in automobile industry. Mr. Malik

has previously worked in automotive companies like Eicher, Escorts, DCM

and Piaggio.

Mr. Rajeev Thakur DirectorMarine

EngineerHe vast experience in the field of management consultancy.

Mr. Sanjay Chhabra DirectorHe has notable experience in the field of technical, marketing and

project implementation

Mr. Bahushrut

LuganiDirector C.A.

He has diversified experience spanning over 25 years in the field of accounts,

consultancy, taxation, establishing new projects etc.

Mr. B. Venugopal Director He is a nominee director of LIC with effect from May-2009.

Mr. John Ernest

FlinthamDirector

H.N.B. in

Mech.

Engineering

He has notable experience in manufacturing and commercial sales of

automotive components.

AMTEK AUTO LIMITED

www.careratings.com 14

EQUIGRADE

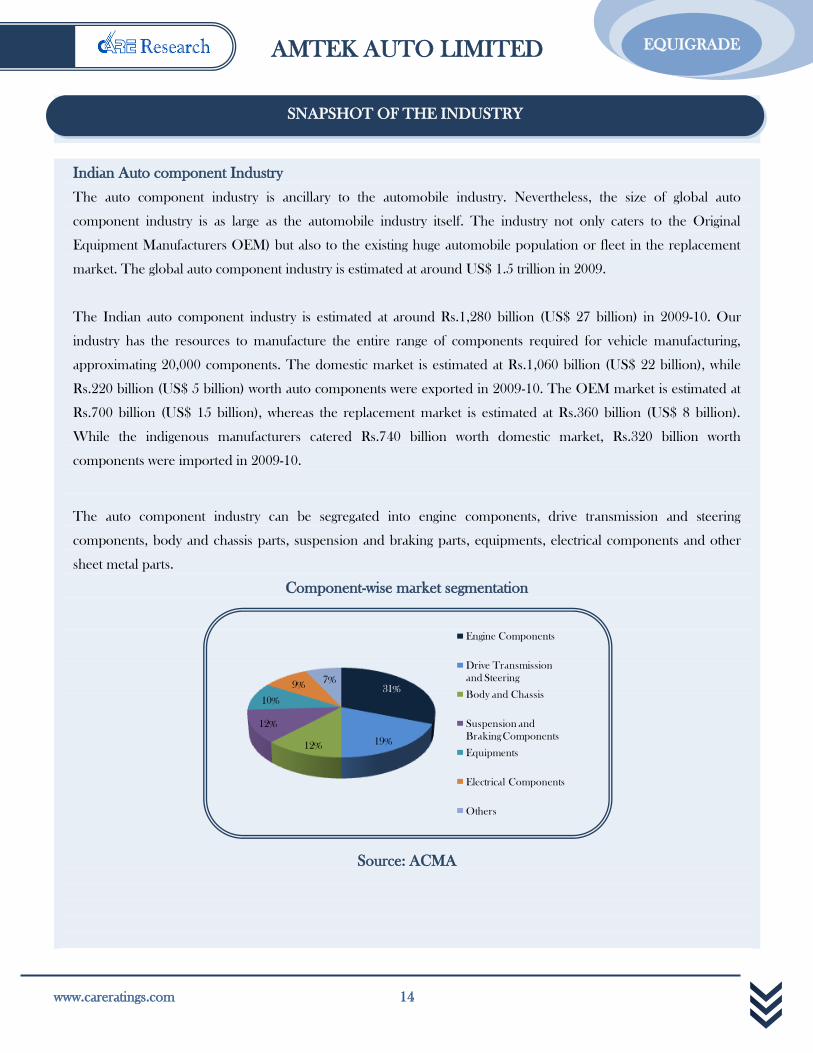

Indian Auto component Industry

The auto component industry is ancillary to the automobile industry. Nevertheless, the size of global auto

component industry is as large as the automobile industry itself. The industry not only caters to the Original

Equipment Manufacturers OEM) but also to the existing huge automobile population or fleet in the replacement

market. The global auto component industry is estimated at around US$ 1.5 trillion in 2009.

The Indian auto component industry is estimated at around Rs.1,280 billion (US$ 27 billion) in 2009-10. Our

industry has the resources to manufacture the entire range of components required for vehicle manufacturing,

approximating 20,000 components. The domestic market is estimated at Rs.1,060 billion (US$ 22 billion), while

Rs.220 billion (US$ 5 billion) worth auto components were exported in 2009-10. The OEM market is estimated at

Rs.700 billion (US$ 15 billion), whereas the replacement market is estimated at Rs.360 billion (US$ 8 billion).

While the indigenous manufacturers catered Rs.740 billion worth domestic market, Rs.320 billion worth

components were imported in 2009-10.

The auto component industry can be segregated into engine components, drive transmission and steering

components, body and chassis parts, suspension and braking parts, equipments, electrical components and other

sheet metal parts.

Component-wise market segmentation

Source: ACMA

SNAPSHOT OF THE INDUSTRY

31%

19%12%

12%

10%

9%7%

Engine Components

Drive Transmission

and Steering

Body and Chassis

Suspension and

Braking Components

Equipments

Electrical Components

Others

AMTEK AUTO LIMITED

15 www.careratings.com

EQUIGRADE

Domestic market offers huge potential

India is one of the fastest growing automobile market in the world. Rise in the income levels and easy liquidity

scenario is enabling healthy growth in automobile sales in last one decade. The auto component industry has also

been able to reap the benefit of this rise. CARE Research foresees strong economic scenario would continue to

push automobile demand northwards resulting in healthy growth in auto component industry as well. During the

next five years (FY10-FY15) the domestic auto component industry is expected to grow at a Compounded Annual

Growth Rate (CAGR) of 20-21 per cent from Rs.1,060 billion in 2009-10 to Rs.2,700 billion in 2014-15. Original

Equipment Manufacturer (OEM) segment would drive the growth, with healthy automobile production foreseen

going forward. The replacement demand too would remain healthy on account of persistent and significant addition

to the existing automobile fleet.

AMTEK AUTO LIMITED

www.careratings.com 16

EQUIGRADE

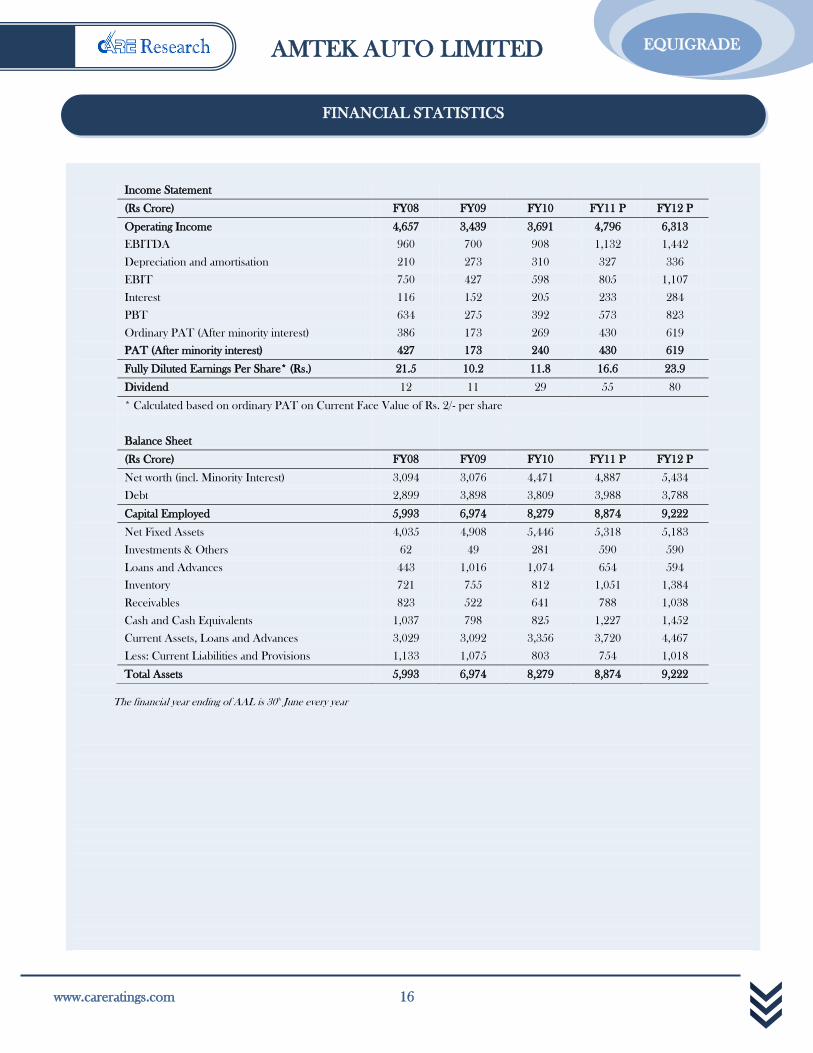

Income Statement

(Rs Crore) FY08 FY09 FY10 FY11 P FY12 P

Operating Income 4,657 3,439 3,691 4,796 6,313

EBITDA 960 700 908 1,132 1,442

Depreciation and amortisation 210 273 310 327 336

EBIT 750 427 598 805 1,107

Interest 116 152 205 233 284

PBT 634 275 392 573 823

Ordinary PAT (After minority interest) 386 173 269 430 619

PAT (After minority interest) 427 173 240 430 619

Fully Diluted Earnings Per Share* (Rs.) 21.5 10.2 11.8 16.6 23.9

Dividend 12 11 29 55 80

* Calculated based on ordinary PAT on Current Face Value of Rs. 2/- per share

Balance Sheet

(Rs Crore) FY08 FY09 FY10 FY11 P FY12 P

Net worth (incl. Minority Interest) 3,094 3,076 4,471 4,887 5,434

Debt 2,899 3,898 3,809 3,988 3,788

Capital Employed 5,993 6,974 8,279 8,874 9,222

Net Fixed Assets 4,035 4,908 5,446 5,318 5,183

Investments & Others 62 49 281 590 590

Loans and Advances 443 1,016 1,074 654 594

Inventory 721 755 812 1,051 1,384

Receivables 823 522 641 788 1,038

Cash and Cash Equivalents 1,037 798 825 1,227 1,452

Current Assets, Loans and Advances 3,029 3,092 3,356 3,720 4,467

Less: Current Liabilities and Provisions 1,133 1,075 803 754 1,018

Total Assets 5,993 6,974 8,279 8,874 9,222

The financial year ending of AAL is 30th June every year

FINANCIAL STATISTICS

AMTEK AUTO LIMITED

17 www.careratings.com

EQUIGRADE

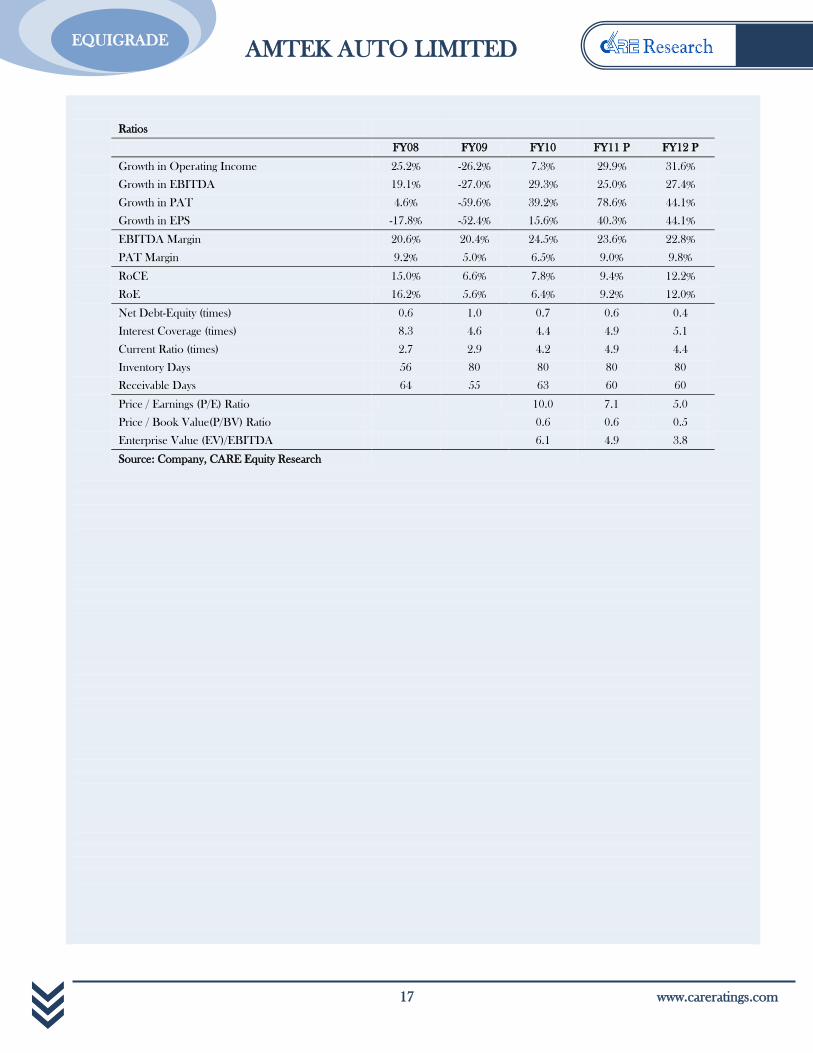

Ratios

FY08 FY09 FY10 FY11 P FY12 P

Growth in Operating Income 25.2% -26.2% 7.3% 29.9% 31.6%

Growth in EBITDA 19.1% -27.0% 29.3% 25.0% 27.4%

Growth in PAT 4.6% -59.6% 39.2% 78.6% 44.1%

Growth in EPS -17.8% -52.4% 15.6% 40.3% 44.1%

EBITDA Margin 20.6% 20.4% 24.5% 23.6% 22.8%

PAT Margin 9.2% 5.0% 6.5% 9.0% 9.8%

RoCE 15.0% 6.6% 7.8% 9.4% 12.2%

RoE 16.2% 5.6% 6.4% 9.2% 12.0%

Net Debt-Equity (times) 0.6 1.0 0.7 0.6 0.4

Interest Coverage (times) 8.3 4.6 4.4 4.9 5.1

Current Ratio (times) 2.7 2.9 4.2 4.9 4.4

Inventory Days 56 80 80 80 80

Receivable Days 64 55 63 60 60

Price / Earnings (P/E) Ratio 10.0 7.1 5.0

Price / Book Value(P/BV) Ratio

0.6 0.6 0.5

Enterprise Value (EV)/EBITDA 6.1 4.9 3.8

Source: Company, CARE Equity Research

AMTEK AUTO LIMITED

www.careratings.com 18

EQUIGRADE

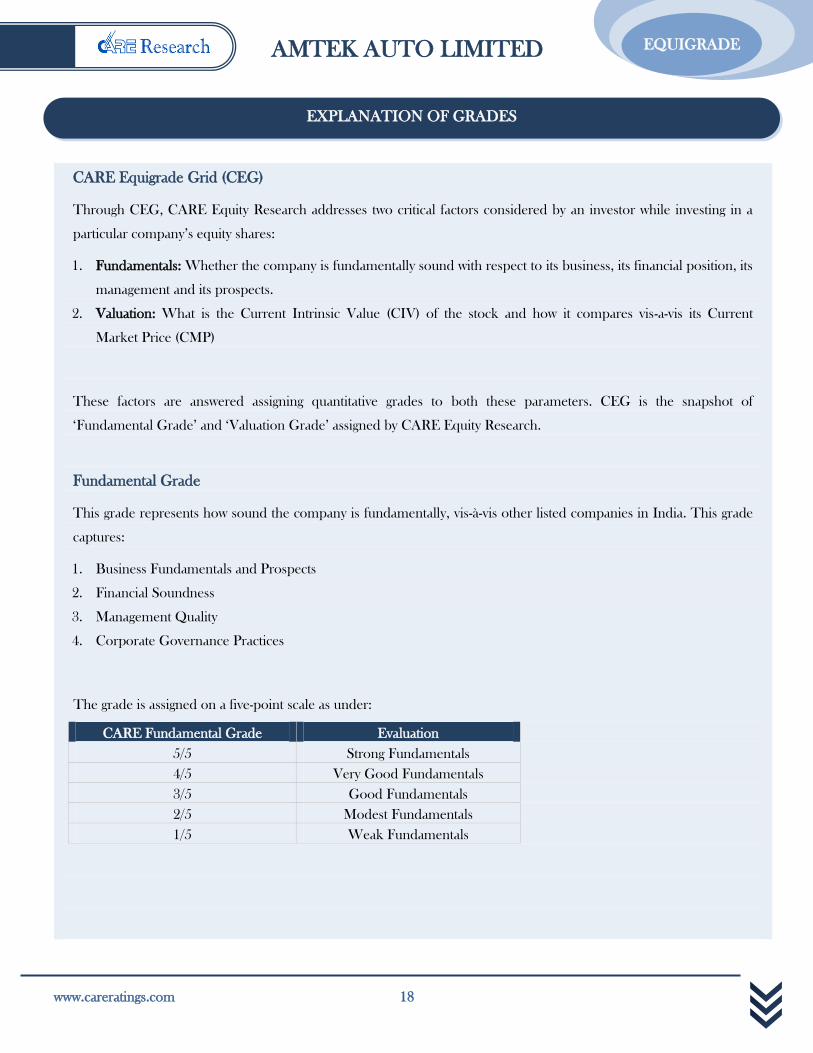

CARE Equigrade Grid (CEG)

Through CEG, CARE Equity Research addresses two critical factors considered by an investor while investing in a

particular company‟s equity shares:

1. Fundamentals: Whether the company is fundamentally sound with respect to its business, its financial position, its

management and its prospects.

2. Valuation: What is the Current Intrinsic Value (CIV) of the stock and how it compares vis-a-vis its Current

Market Price (CMP)

These factors are answered assigning quantitative grades to both these parameters. CEG is the snapshot of

„Fundamental Grade‟ and „Valuation Grade‟ assigned by CARE Equity Research.

Fundamental Grade

This grade represents how sound the company is fundamentally, vis-à-vis other listed companies in India. This grade

captures:

1. Business Fundamentals and Prospects

2. Financial Soundness

3. Management Quality

4. Corporate Governance Practices

The grade is assigned on a five-point scale as under:

CARE Fundamental Grade Evaluation

5/5 Strong Fundamentals

4/5 Very Good Fundamentals

3/5 Good Fundamentals

2/5 Modest Fundamentals

1/5 Weak Fundamentals

EXPLANATION OF GRADES

AMTEK AUTO LIMITED

19 www.careratings.com

EQUIGRADE

Valuation Grade

This grade represents the potential value in the company‟s equity share for the investor over a 1 year period. The

Current Intrinsic Value (CIV) or the price arrived by CARE Equity Research on fundamental basis is compared with

the current market price (CMP) of the stock and the grade is assigned based on the gap between CIV and CMP of the

stock.

The grade is assigned on a five-point scale as under:

CARE Valuation Grade Evaluation

5/5 Considerable Upside Potential

(>25% from CMP)

4/5 Moderate Upside Potential

(10-25% from CMP)

3/5 Fairly Priced

(+/- 10% from CMP)

2/5 Moderate Downside Potential

(Negative 10-25 from CMP)

1/5 Considerable Downside Potential

(<25% from CMP)

Grading determination is a matter of experienced and holistic judgment, based on relevant quantitative and qualitative factors of

the company in relation to other listed companies.

DISCLOSURES

Each member of the team involved in the preparation of this grading report, hereby affirms that there exists no conflict of interest

that can bias the grading recommendation of the company.

This report has been sponsored by the company.

DISLCLAIMER

This report is prepared by CARE Research, a division of Credit Analysis & REsearch Limited [CARE]. CARE Research has taken

utmost care to ensure accuracy and objectivity while developing this report based on information available in public domain or from

sources considered reliable. However, neither the accuracy nor completeness of information contained in this report is guaranteed.

CARE Research operates independently of ratings division and this report does not contain any confidential information obtained by

ratings division, which they may have obtained in the regular course of operations. Opinions expressed herein are our current

opinions as on the date of this report. Nothing in this report can be construed as either investment or any other advice or any

solicitation, whatsoever. The subscriber / user assumes the entire risk of any use made of this report or data herein. CARE specifically

states that it or any of its divisions or employees have no financial liabilities whatsoever to the subscribers / users of this report. This

report is for personal information only of the authorised recipient in India only. This report or part of it should not be reproduced or

redistributed or communicated directly or indirectly in any form to any other person, especially outside India or published or copied

for any purpose.

Published by Credit Analysis & REsearch Ltd., 4th Floor Godrej Coliseum, Off Eastern Express Highway, Somaiya

Hospital Road, Sion East, Mumbai – 400 022.

CARE Research is not responsible for any errors or omissions in analysis/inferences/views or for results obtained from the use of

information contained in this report and especially states that CARE (including all divisions) has no financial liability whatsoever to the

user of this product. This report is for the information of the intended recipients only and no part of this report may be published or

reproduced in any form or manner without prior written permission of CARE Research.

AMTEK AUTO LIMITED

www.careratings.com 20

EQUIGRADE

Credit Analysis & REsearch Ltd. (CARE) is a full service rating company that offers a wide range of rating and grading services

across sectors. CARE has an unparallel depth of expertise. CARE Ratings methodologies are in line with the best international

practices.

CARE Research

CARE Research is an independent research division of CARE Ratings, a full service rating company. CARE Research is

involved in preparing detailed industry research reports with 5 year demand and 2 year profitability outlook on the industry

besides providing comprehensive trend analysis and the current state of the industry. CARE Research also offers research that

is customised to client requirements. CARE Research currently offers reports on more than 21 industries that include Cement,

Steel, Aluminium, Construction, Shipping, Ship-building, Commercial Vehicles, Two-Wheelers, Tyres, Auto Components,

Pipes, Natural Gas, Retail, Sugar, etc. CARE Research now offers independent research of equities through its product

„EQUIGRADE‟.

CREDIT ANALYSIS & RESEARCH LTD

HEAD OFFICE |Mr. P. N. Satheeskumar | Cell: +91-9820416004 | Tel: +91-22-6754 3555 | E-mail:

4th Floor, Godrej Coliseum, Somaiya Hospital Road, Off Eastern Express Highway, Sion (East), Mumbai - 400 022 |

Tel: +91-022- 6754 3456 | E-mail: [email protected] | Fax: +91-022- 6754 3457

KOLKATA | Mr. Sukanta Nag | Cell: +91-98311 70075 | Tel: +91-33- 2283 1800/ 1803, 2280 8472 |

E- mail: [email protected] | 3rd Flr., Prasad Chambers (Shagun Mall Bldg), 10A, Shakespeare Sarani, Kolkata -700 071

CHENNAI | Mr. V Pradeep Kumar | Cell: +91 9840754521 | Tel: +91-44-2849 7812/2849 0811 | Fax: +91-44-2849 0876 |

Email: [email protected] | Unit No. O-509/C, Spencer Plaza, 5th Floor, No. 769, Anna Salai, Chennai - 600 002

AHMEDABAD | Mr. Mehul Pandya | Cell: +91-98242 56265 | Tel: +91-79-40265656 | Fax: +91-79-40265657 |

E-mail:[email protected] | 32, Titanium, Prahaladnagar Corporate Road, Satellite, Ahmedabad - 380 015.

NEW DELHI | Ms. Swati Agrawal | Cell: +91-98117 45677 | Tel: +91- 11- 2331 8701/ 2371 6199 |

E-mail: [email protected] | 710 Surya Kiran,19 K.G. Road, New Delhi - 110 001.

BANGALORE | Mr. G. Sundara Vathanan | Cell: +91 98860 24430 | Tel:+91-80-2211 7140 |

E-mail: [email protected] | Unit No. 8, I floor, Commander's Place, No. 6, Raja Ram Mohan Roy Road,

(Opp. P F Office), Richmond Circle, Bangalore - 560 025.

HYDERABAD | Mr. Ashwini Kumar Jani | Cell: +91-91766 47599 | Tel: +91-40-40102030 |

E-mail: [email protected] | 401, Ashoka Scintilla | 3-6-520, Himayat Nagar | Hyderabad - 500 029

ABOUT CARE