fundamentals of excise taxation - tax.gov.kh - warwick ryan_australia.pdf · slide 1 fundamentals...

TRANSCRIPT

Slide 1

Fundamentals ofExcise Taxation

Master ClassAlcohol Products

Mr Warwick RyanTax Counsel,

Distilled Spirits Industry Council of Australia(DSICA)

Seventh Asia Tax ForumExcise Taxation Master Class

20 October 2010, Siem Reap

Slide 2

Presentation outline

• Alcohol taxation definitions• Alcohol taxation structures and the traffic light

system• An ideal alcohol tax system• Asia Pacific region – spirits taxation• The Singapore system• The Indonesian system

– Domestic product reforms– Imported product reforms

• The Australian system – spirits taxation• The Henry Review – alcohol taxation

recommendations

Slide 3

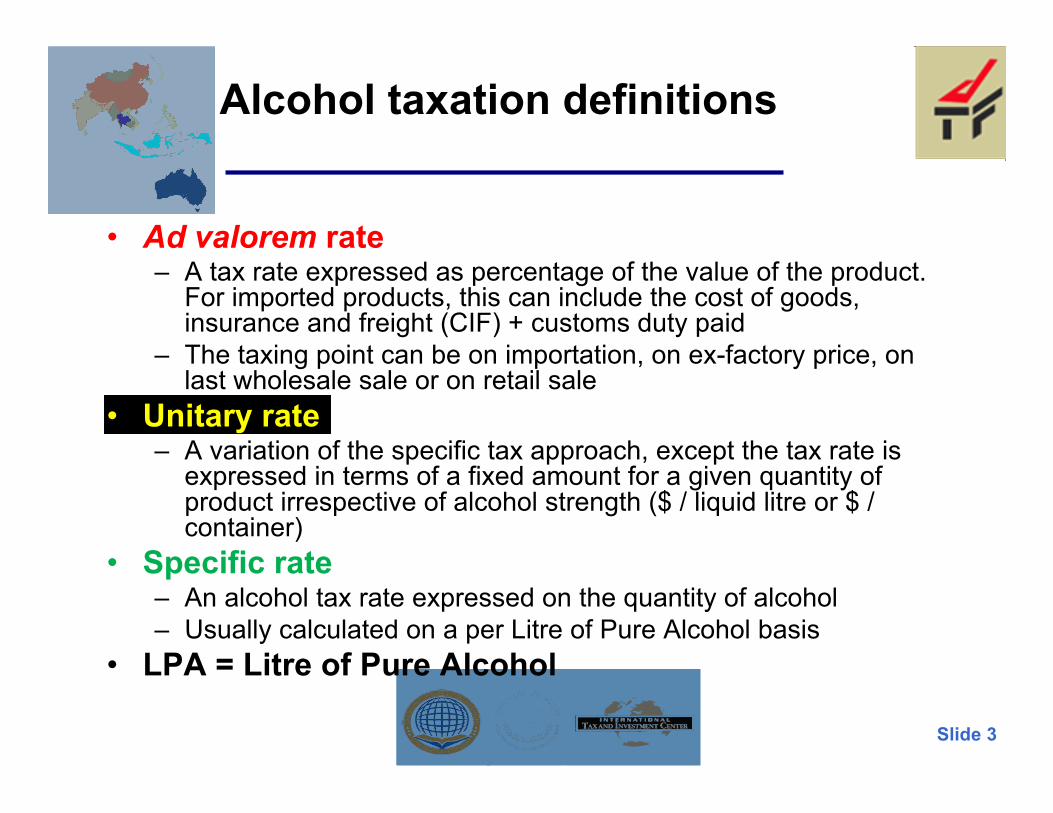

Alcohol taxation definitions

• Ad valorem rate– A tax rate expressed as percentage of the value of the product.

For imported products, this can include the cost of goods,insurance and freight (CIF) + customs duty paid

– The taxing point can be on importation, on ex-factory price, onlast wholesale sale or on retail sale

• Unitary rate– A variation of the specific tax approach, except the tax rate is

expressed in terms of a fixed amount for a given quantity ofproduct irrespective of alcohol strength ($ / liquid litre or $ /container)

• Specific rate– An alcohol tax rate expressed on the quantity of alcohol– Usually calculated on a per Litre of Pure Alcohol basis

• LPA = Litre of Pure Alcohol

Slide 4

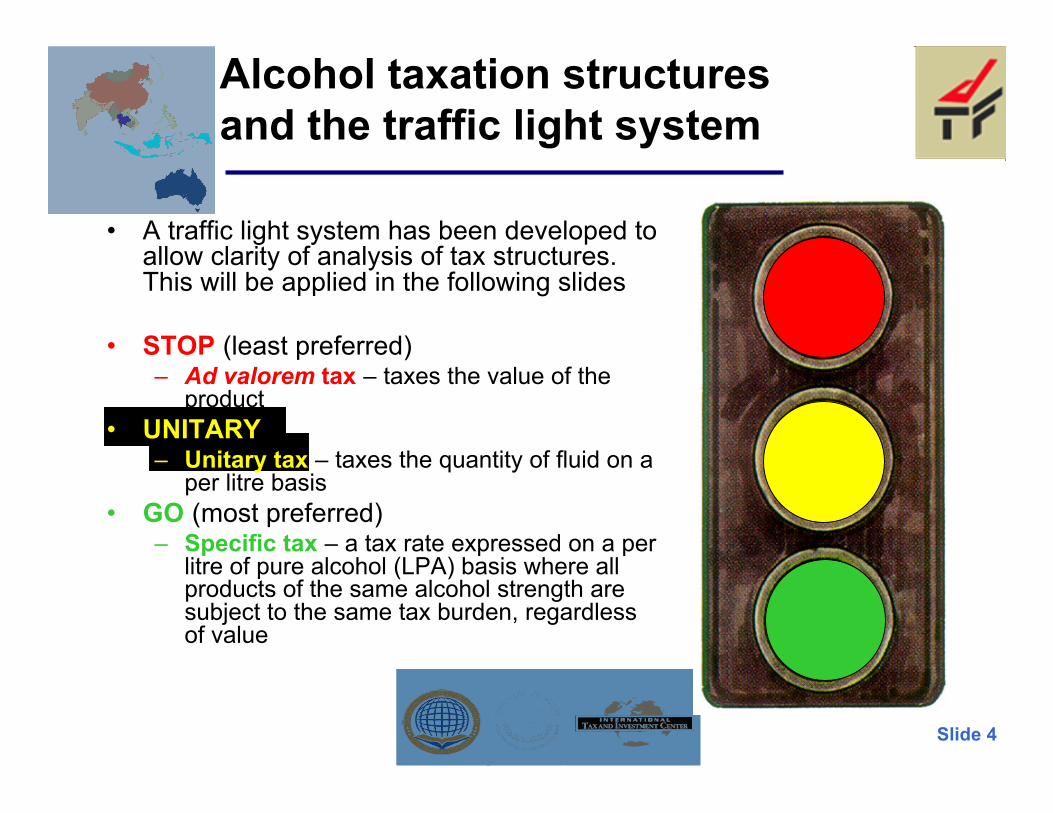

Alcohol taxation structuresand the traffic light system

• A traffic light system has been developed toallow clarity of analysis of tax structures.This will be applied in the following slides

• STOP (least preferred)– Ad valorem tax – taxes the value of the

product• UNITARY

– Unitary tax – taxes the quantity of fluid on aper litre basis

• GO (most preferred)– Specific tax – a tax rate expressed on a per

litre of pure alcohol (LPA) basis where allproducts of the same alcohol strength aresubject to the same tax burden, regardlessof value

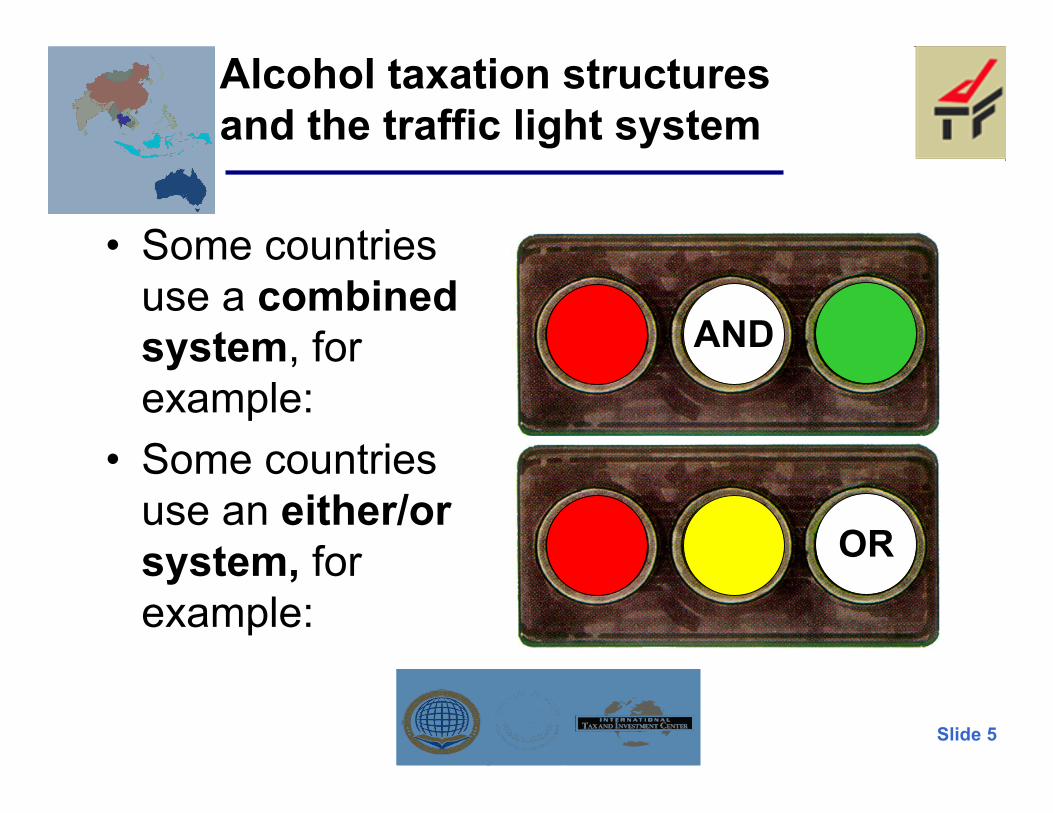

Slide 5

Alcohol taxation structuresand the traffic light system

• Some countriesuse a combinedsystem, forexample:

• Some countriesuse an either/orsystem, forexample:

AND

OR

Slide 6

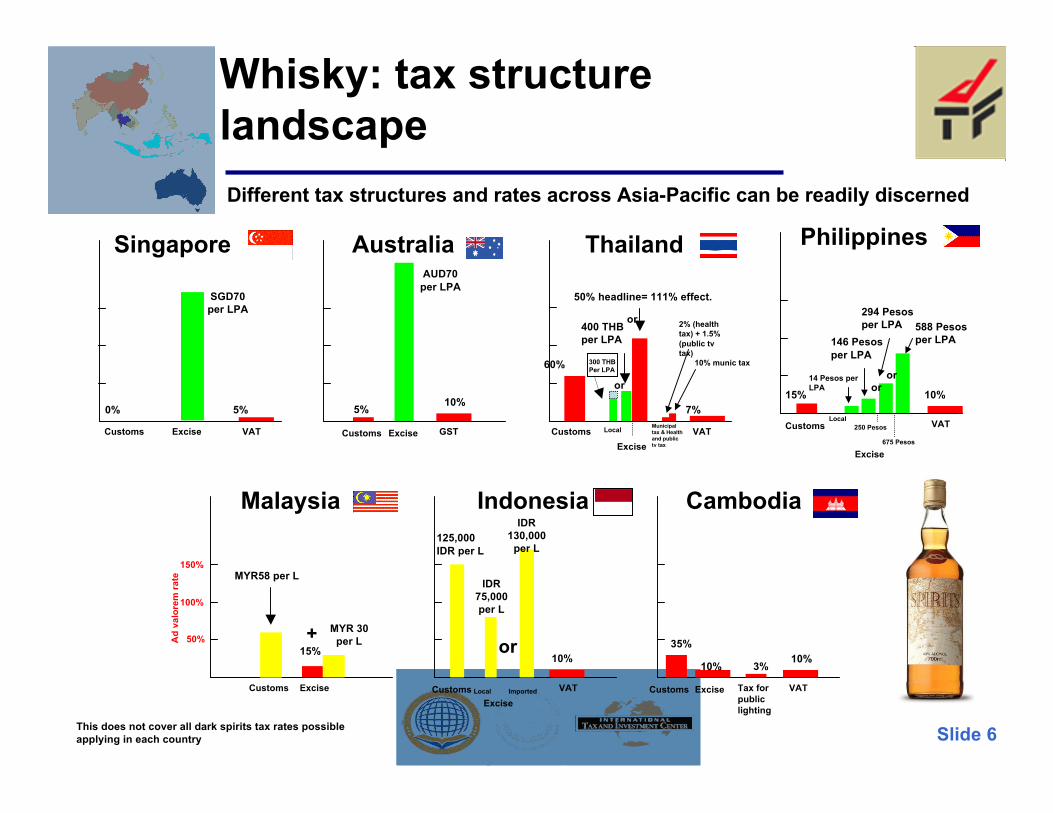

Malaysia

50%

100%

150%

Excise

MYR58 per L

Indonesia

ExciseCustoms

125,000IDR per L

Local Imported

IDR75,000per L

or

VAT

10%

Ad

valo

rem

rate

Customs

MYR 30per L+

IDR130,000

per L

15%

Different tax structures and rates across Asia-Pacific can be readily discerned

Thailand

ExciseCustoms

Municipaltax & Healthand publictv tax

VAT

60%

50% headline= 111% effect.

400 THBper LPA

7%

or

10% munic tax

2% (healthtax) + 1.5%(public tvtax)

Local

300 THBPer LPA

or

Philippines

Excise

Customs

15%

146 Pesosper LPA

250 Pesos

294 Pesosper LPA 588 Pesos

per LPA

or

VAT

10%

or

675 Pesos

14 Pesos perLPA

Local

Australia

ExciseCustoms

5%

AUD70per LPA

GST

10%

Singapore

Excise

SGD70per LPA

VAT

5%

Customs

0%

This does not cover all dark spirits tax rates possibleapplying in each country

Cambodia

Excise VAT

10%10% 3%

Tax forpubliclighting

35%

Customs

Whisky: tax structurelandscape

Slide 7

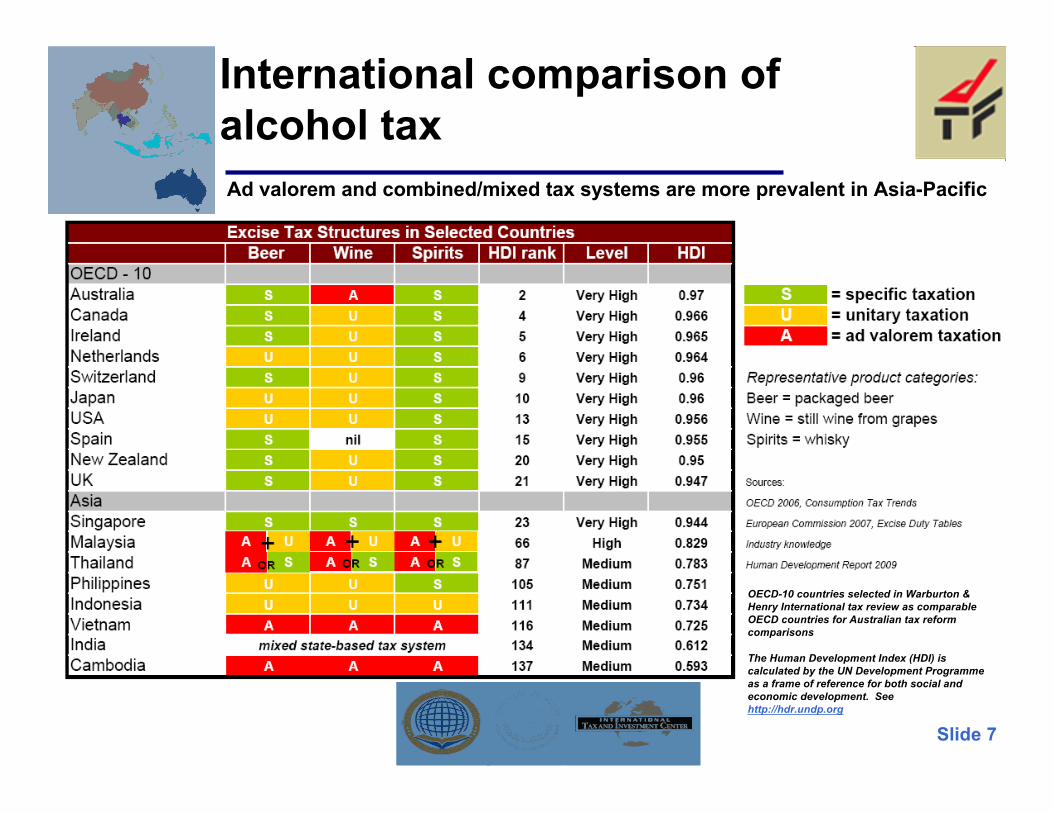

Ad valorem and combined/mixed tax systems are more prevalent in Asia-Pacific

OECD-10 countries selected in Warburton &Henry International tax review as comparableOECD countries for Australian tax reformcomparisons

The Human Development Index (HDI) iscalculated by the UN Development Programmeas a frame of reference for both social andeconomic development. Seehttp://hdr.undp.org

International comparison ofalcohol tax

Slide 8

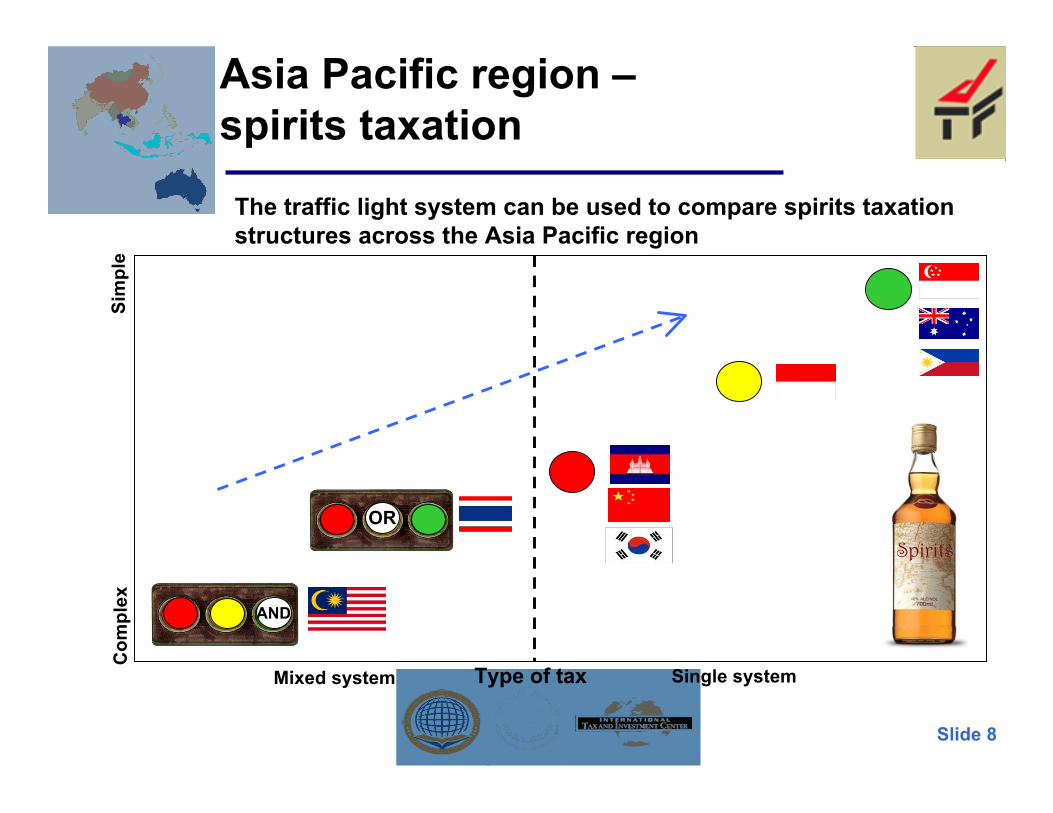

Asia Pacific region –spirits taxation

Sim

ple

Mixed system Single systemType of tax

Com

plex

AND

Spirits

The traffic light system can be used to compare spirits taxationstructures across the Asia Pacific region

OR

Slide 9

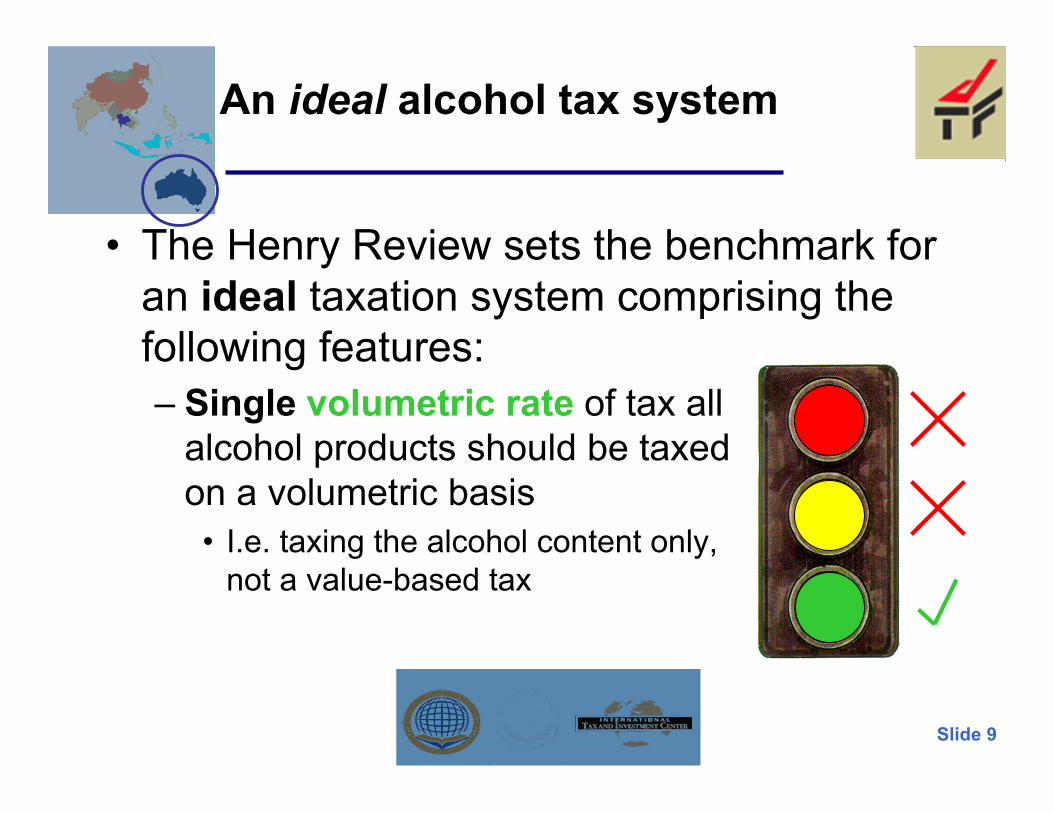

An ideal alcohol tax system

• The Henry Review sets the benchmark foran ideal taxation system comprising thefollowing features:– Single volumetric rate of tax all

alcohol products should be taxedon a volumetric basis

• I.e. taxing the alcohol content only,not a value-based tax

Slide 10

An ideal alcohol tax system (2)

– The single rate shouldapply to all products

• One taxation system shouldapply to all alcoholbeverages and avoiddiscrimination on the basis ofingredients, method ofmanufacture and country oforigin

Local Import

Slide 11

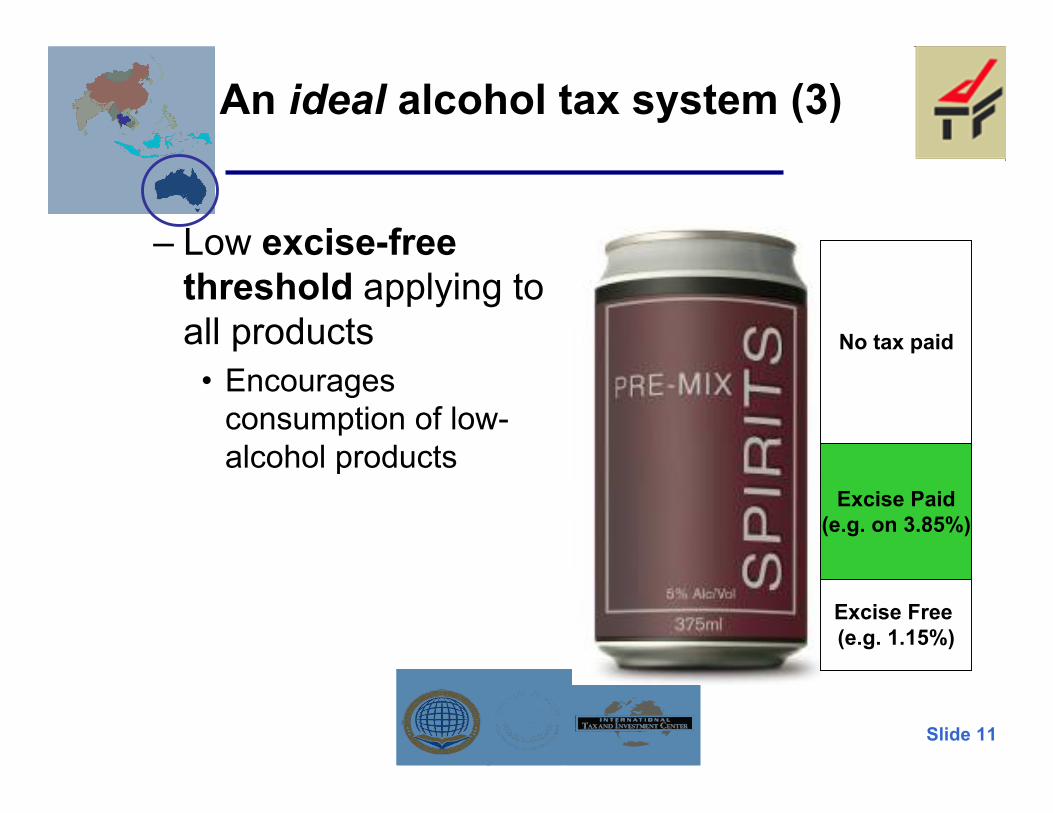

An ideal alcohol tax system (3)

– Low excise-freethreshold applying toall products

• Encouragesconsumption of low-alcohol products

Excise Free (e.g. 1.15%)

Excise Paid(e.g. on 3.85%)

No tax paid

Slide 12

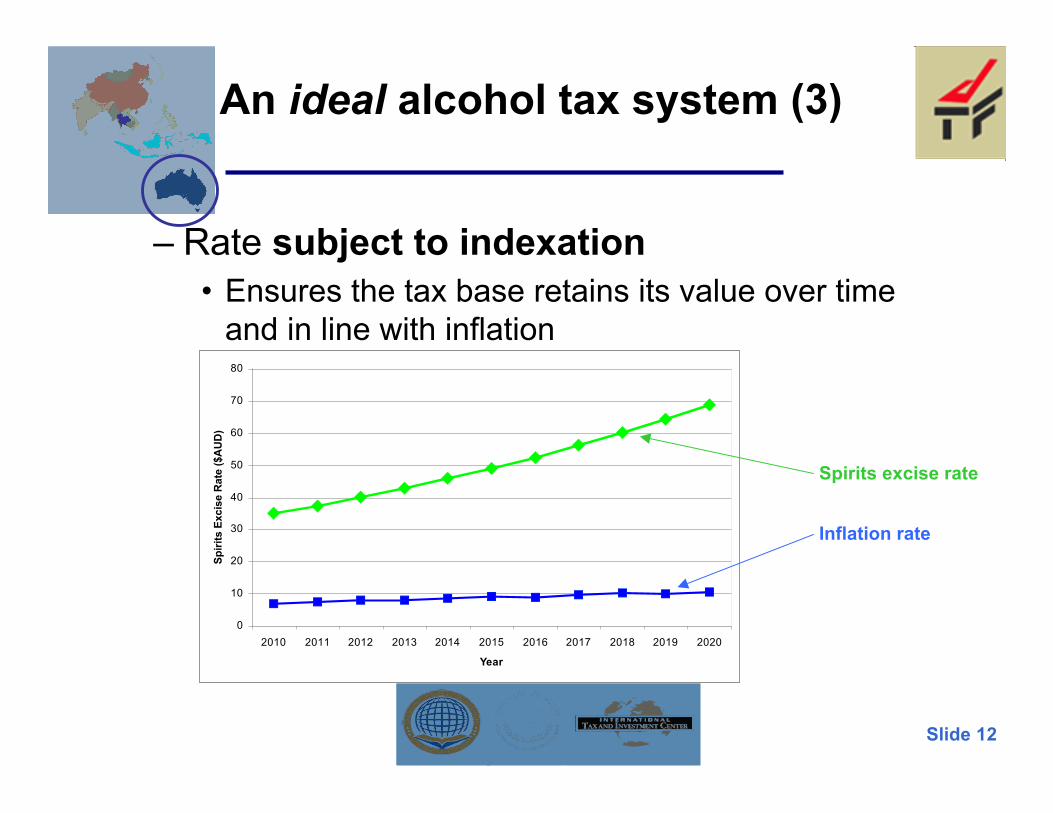

An ideal alcohol tax system (3)

– Rate subject to indexation• Ensures the tax base retains its value over time

and in line with inflation

0

10

20

30

40

50

60

70

80

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Year

Sp

irit

s E

xcis

e R

ate

($A

UD

)

Spirits excise rate

Inflation rate

Slide 13

An ideal alcohol tax system (4)

– Rate of taxation based on the net marginalspillover costs (i.e. externalities) of alcoholconsumption

• This is a long-term target to be discussed atanother time

Slide 14

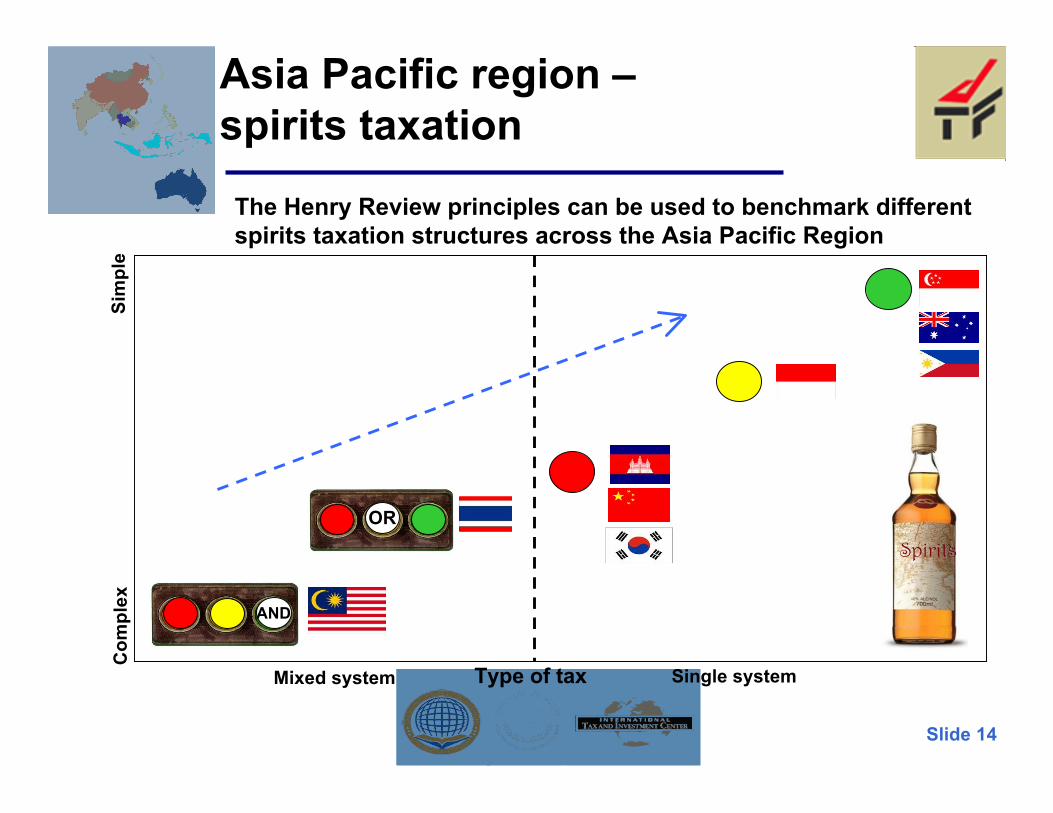

Asia Pacific region –spirits taxation

Sim

ple

Mixed system Single systemType of tax

Com

plex

AND

Spirits

The Henry Review principles can be used to benchmark differentspirits taxation structures across the Asia Pacific Region

OR

Slide 15

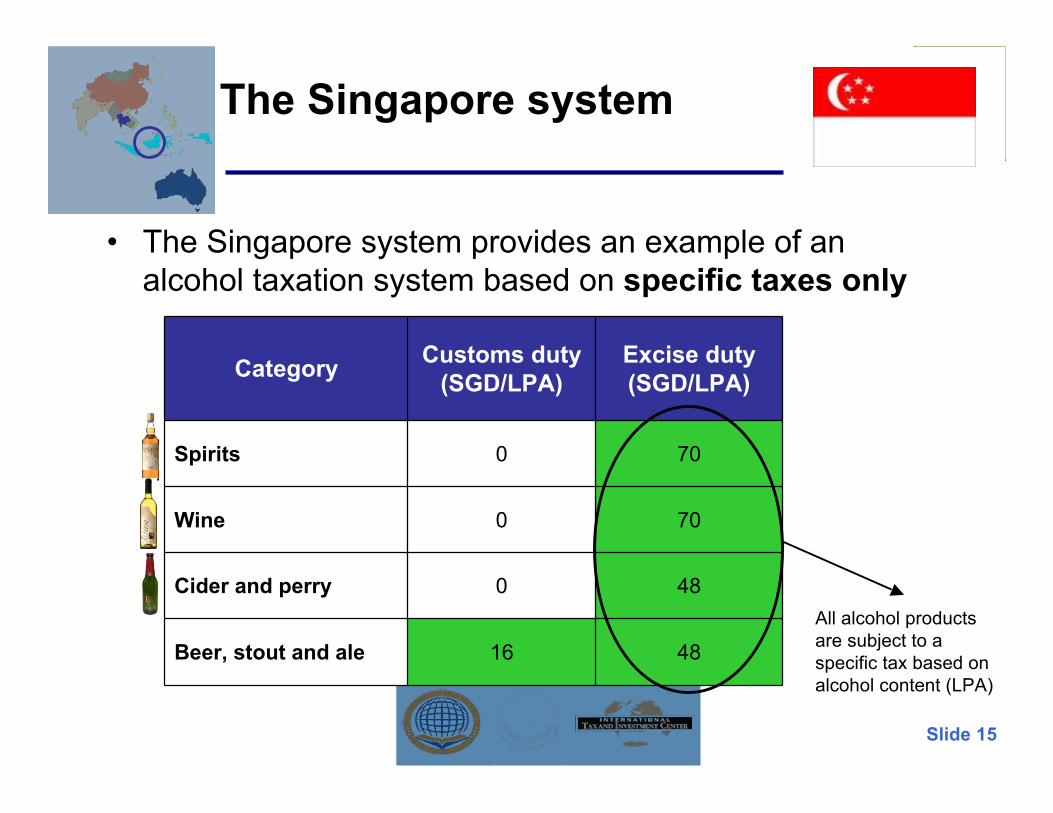

The Singapore system

• The Singapore system provides an example of analcohol taxation system based on specific taxes only

Category Customs duty(SGD/LPA)

Excise duty(SGD/LPA)

Spirits 0 70

Wine 0 70

Cider and perry 0 48

Beer, stout and ale 16 48All alcohol productsare subject to aspecific tax based onalcohol content (LPA)

Slide 16

The Indonesian system

• Recent Indonesian reforms simplified thealcohol taxation system– On 1 April 2010 the Indonesian Government

reduced the number of excise rates fromfive to three, creating greater simplicity andminimising administrative burdens

– This tiered banding system provides a bestpractice example of a transition method thatcan be used as a step towards theintroduction of a single specific rate

Slide 17

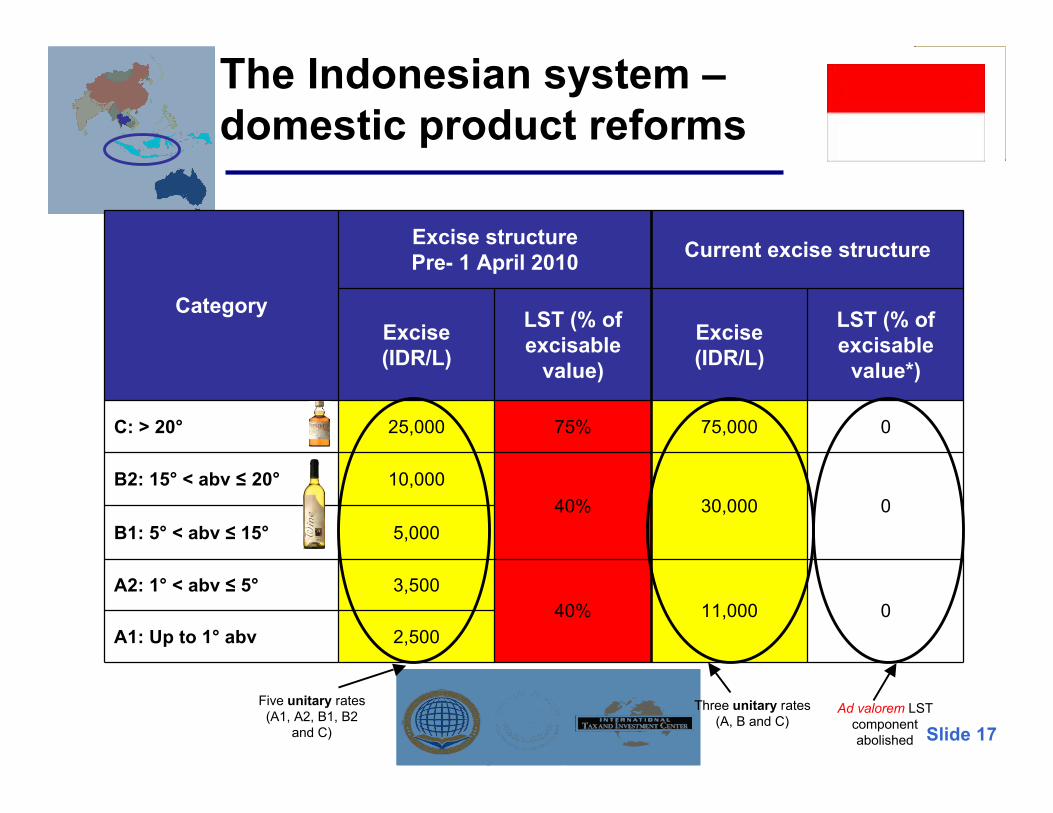

The Indonesian system –domestic product reforms

Five unitary rates(A1, A2, B1, B2

and C)

Three unitary rates(A, B and C)

Category

Excise structurePre- 1 April 2010 Current excise structure

Excise(IDR/L)

LST (% ofexcisable

value)

Excise(IDR/L)

LST (% ofexcisable

value*)

C: > 20° 25,000 75% 75,000 0

B2: 15° < abv ≤ 20° 10,00040% 30,000 0

B1: 5° < abv ≤ 15° 5,000

A2: 1° < abv ≤ 5° 3,50040% 11,000 0

A1: Up to 1° abv 2,500

Ad valorem LSTcomponentabolished

Slide 18

The Indonesian system –imported product reforms

Category

Excise structurePre- 1 April 2010 Current excise structure

Excise(IDR/L)

LST (% ofexcisable

value)

Excise(IDR/L)

LST (% ofexcisable

value*)

C: > 20° 50,000 75% 130,000 0

B2: 15° < abv ≤ 20° 30,00040% 40,000 0

B1: 5° < abv ≤ 15° 20,000

A2: 1° < abv ≤ 5° 5,00040% 11,000 0

A1: Up to 1° abv 2,500

Five unitary rates(A1, A2, B1, B2

and C)

Three unitary rates(A, B and C)

Ad valorem LSTcomponentabolished

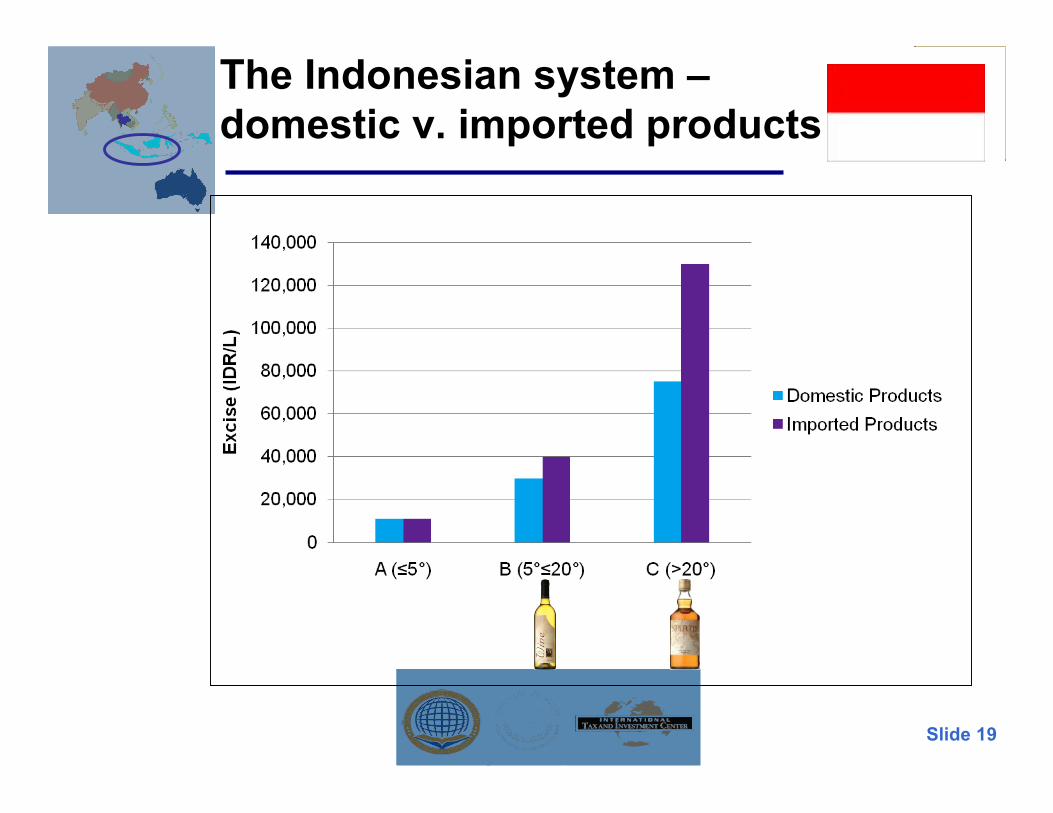

Slide 19

The Indonesian system –domestic v. imported products

Slide 20

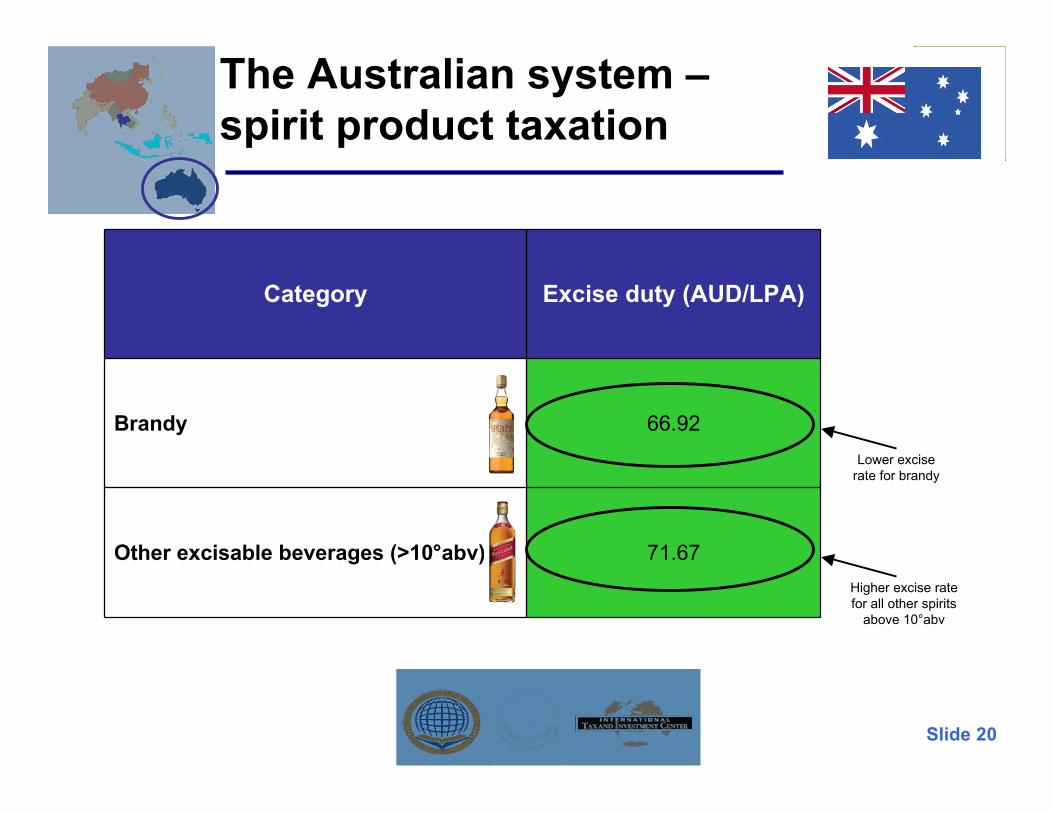

The Australian system –spirit product taxation

Category Excise duty (AUD/LPA)

Brandy 66.92

Other excisable beverages (>10°abv) 71.67

Lower exciserate for brandy

Higher excise ratefor all other spirits

above 10°abv

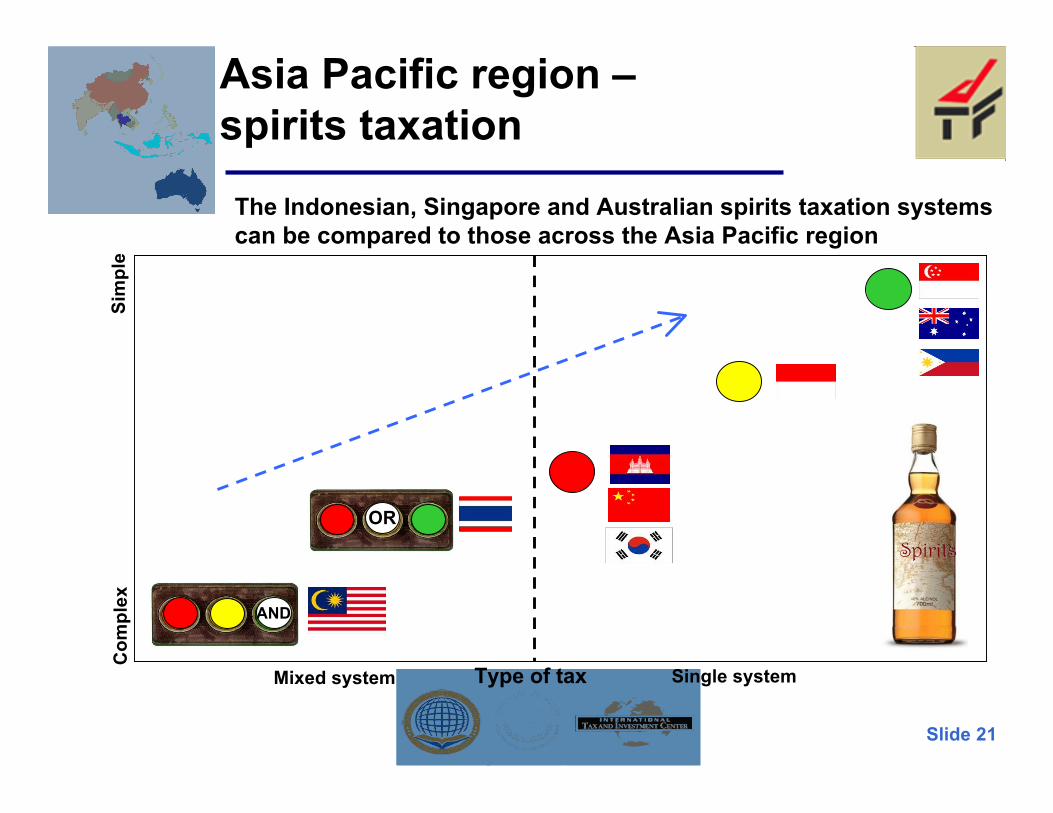

Slide 21

Asia Pacific region –spirits taxation

Sim

ple

Mixed system Single systemType of tax

Com

plex

AND

Spirits

The Indonesian, Singapore and Australian spirits taxation systemscan be compared to those across the Asia Pacific region

OR

Slide 22

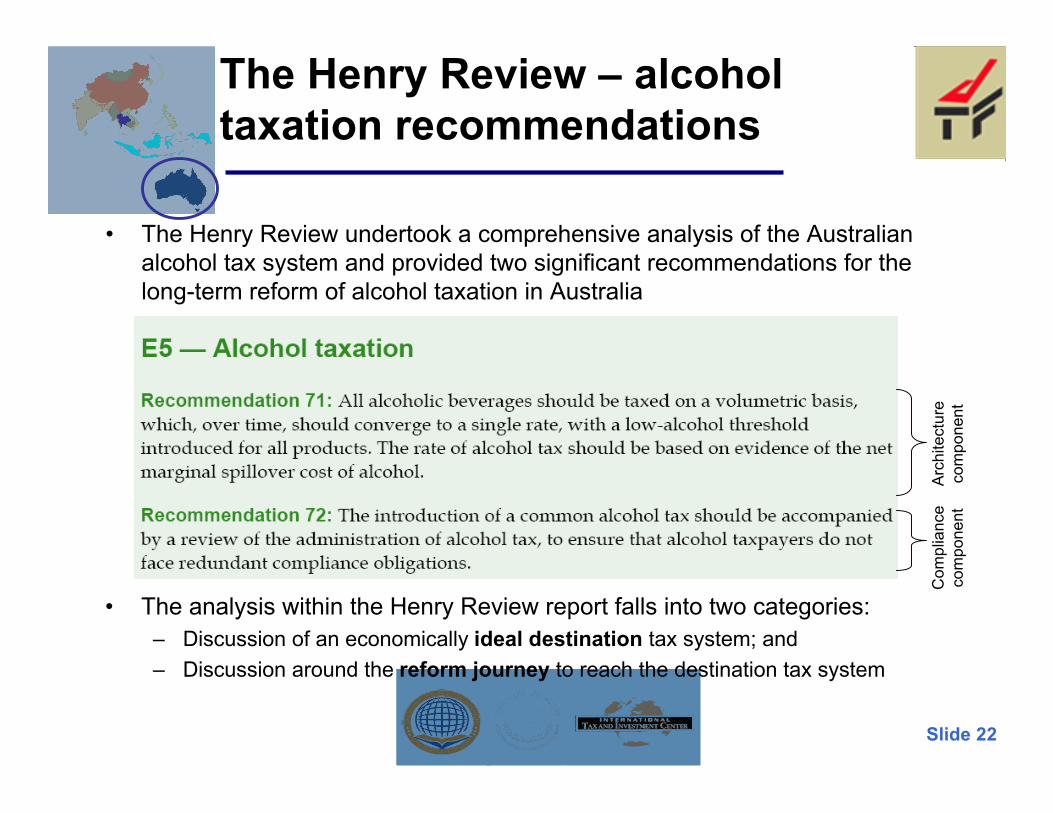

The Henry Review – alcoholtaxation recommendations

• The Henry Review undertook a comprehensive analysis of the Australianalcohol tax system and provided two significant recommendations for thelong-term reform of alcohol taxation in Australia

Arc

hite

ctur

eco

mpo

nent

Com

plia

nce

com

pone

nt

• The analysis within the Henry Review report falls into two categories:– Discussion of an economically ideal destination tax system; and– Discussion around the reform journey to reach the destination tax system

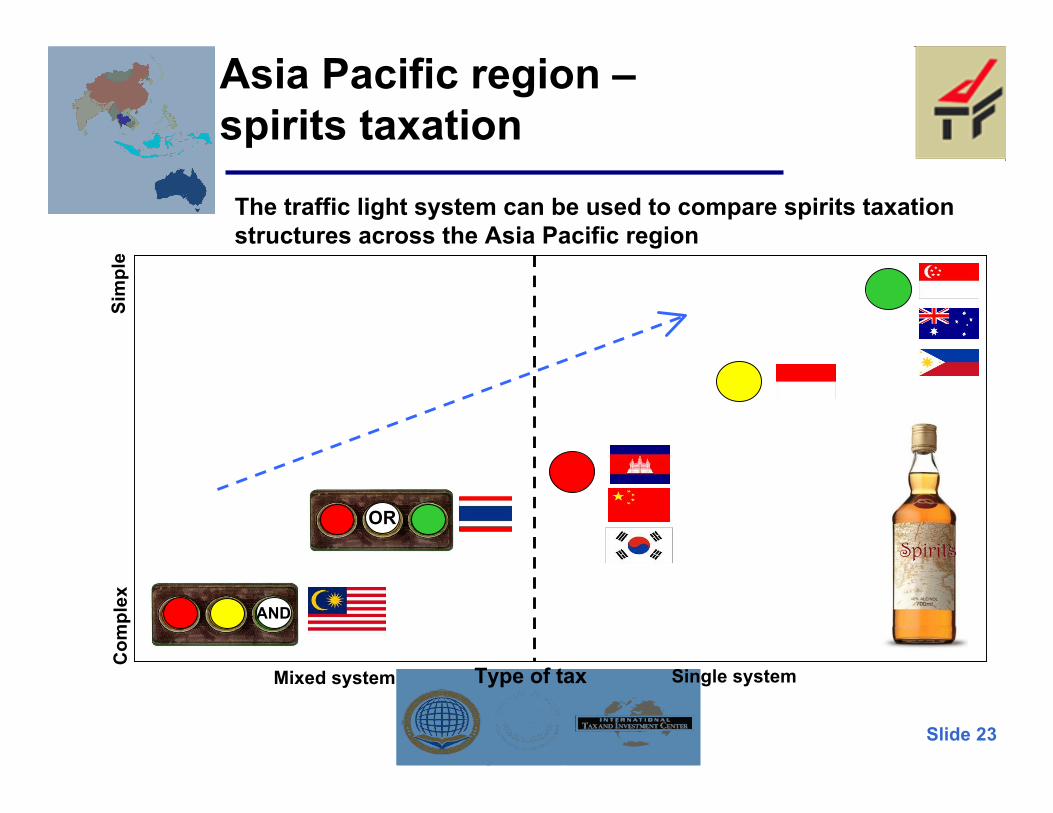

Slide 23

Asia Pacific region –spirits taxation

Sim

ple

Mixed system Single systemType of tax

Com

plex

AND

Spirits

The traffic light system can be used to compare spirits taxationstructures across the Asia Pacific region

OR

Slide 24

Thank you

Presenter Details

Mr Warwick Ryan

Tax Counsel,Distilled Spirits Industry Council of Australia

(DSICA)

+61 2 6248 1124