full year results 2001 - nestlé global · full year results 2001. 2 28.02.2002/conf.call ... 10.9%...

TRANSCRIPT

Conference call, February 2002Conference call, February 2002

FULL YEAR RESULTS 2001FULL YEAR RESULTS 2001

228.02.2002/Conf.call

This presentation contains forward looking statements which reflect Management’s current views and estimates. The forward looking statements involve certain risks and uncertainties that could cause actual results to differ materially from those contained in the forward looking statements. Potential risks and uncertainties include such factors as general economic conditions, foreign exchange fluctuations, competitive product and pricing pressures and regulatory developments.

328.02.2002/Conf.call

Agenda

Key achievements & figures Income statementCash flowBalance sheetUse of funds

428.02.2002/Conf.call

Agenda

Key achievements & figuresIncome statementCash flowBalance sheetUse of funds

528.02.2002/Conf.call

Key achievements 2001

Strong sales growth+ 4.4% RIG+ 6.4 % organic+ 9.7% comparable structure & constant FX

Profit performanceStable EBIT margin of 11.3% on comparable basis; 10.9% after TTS review and GLOBEExcellent net profit growth of 15.9% EPS rises 15.7%

628.02.2002/Conf.call

Key figures 2000 and 2001

* adjusted for share split . TTS figures are illustrative.

ChangeCHF mio. 2000 % 2001 % %

Sales 81'422 100 84'698 100 4.0 EBITDA 12'516 15.4 12'444 14.7 (0.6)

ex TTS - - - 15.2EBITA 9'600 11.8 9'713 11.5 1.2

ex TTS - - - 11.9Trading profit (EBIT) 9'186 11.3 9'218 10.9 0.4

ex TTS - - - 11.3Net profit 5'763 7.1 6'681 7.9 15.9

ex TTS - - - 8.2Earnings per share (CHF) 14.91* 17.25 15.7

728.02.2002/Conf.call

Agenda

Key achievements & figures Income statementCash flowBalance sheetUse of funds

828.02.2002/Conf.call

Drivers of sales growthJanuary - December 2001 : CHF 84.7 billion

Sales growth at comparable structure and constant exchange rates: + 9.7%

REAL INTERNAL GROWTH (RIG)

Selling price increases and others

Acquisitions minus divestitures

Variation of exchange rates- 4.7%

5.3%

- 1.0%

4.4%

+ 4.0%

TTS 0

928.02.2002/Conf.call

Euro (1) 1.56 1.51 -3.2

U.S. dollar (1) 1.69 1.68 -0.6

£ sterling (1) 2.56 2.43 -5.1

Real (100) 92.40 72.21 -21.9

Yen (100) 1.57 1.39 -11.5

Mex. Peso (100) 17.90 18.09 +1.1

Weighted average exchange rates

Jan. - Dec. Jan. - Dec. Variation CHF per: 2000 2001 (%)

1028.02.2002/Conf.call

Sales and profitability by management responsibilities and geographic area

FoodEurope 26.3 2.75 10.5 26.7 2.78 10.4Americas 25.5 3.50 13.7 26.6 3.53

13.3AOA 15.7 2.67 17.0 15.5 2.60 16.8

Other 13.9 2.02 14.5 15.9 2.15 13.5* Calculation based on non-rounded figures for sales. The % variations are influenced not only by the

evolution of sales volumes, but also by acquisitions and divestitures, exchange rate fluctuations,and changes in selling prices.

# 2001 % margin negatively impacted by TTS review

2000 2001 CHF bio. Sales Profit Margin* Sales Profit Margin*#

% %

1128.02.2002/Conf.call

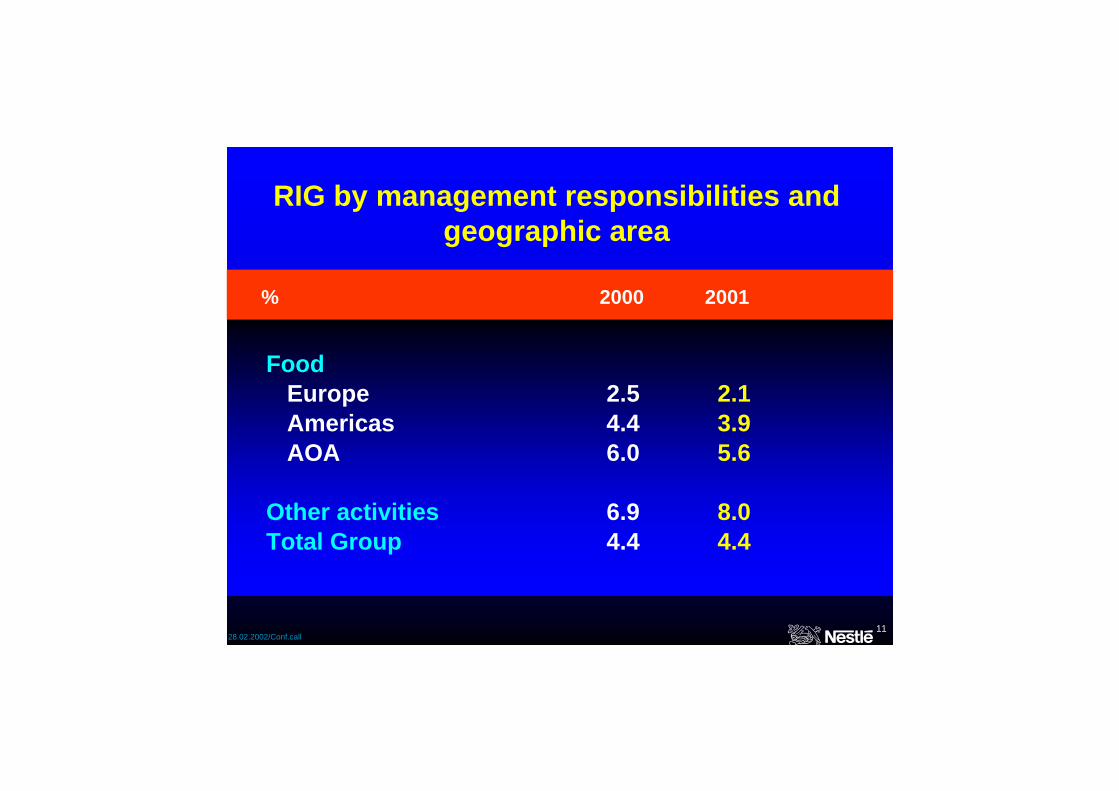

RIG by management responsibilities and geographic area

FoodEurope 2.5 2.1Americas 4.4 3.9AOA 6.0 5.6

Other activities 6.9 8.0Total Group 4.4 4.4

% 2000 2001

1228.02.2002/Conf.call

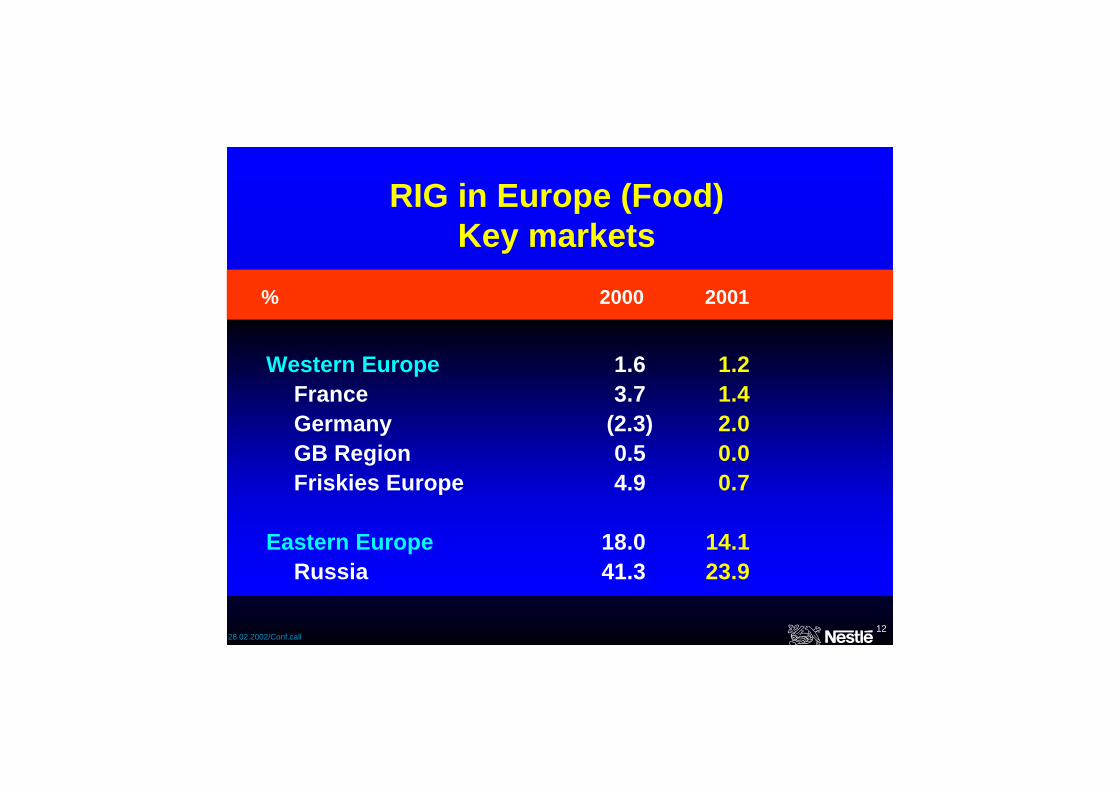

RIG in Europe (Food)Key markets

Western Europe 1.6 1.2France 3.7 1.4Germany (2.3) 2.0GB Region 0.5 0.0Friskies Europe 4.9 0.7

Eastern Europe 18.0 14.1Russia 41.3 23.9

% 2000 2001

1328.02.2002/Conf.call

RIG in the Americas (Food)Key markets

United States and Canada 3.5 3.4United States 4.0 3.3Canada (1.1) 4.6Latin America and Caribbean 5.8 4.7Brazil 2.0 5.2Mexico 9.5 2.7

% 2000 2001

1428.02.2002/Conf.call

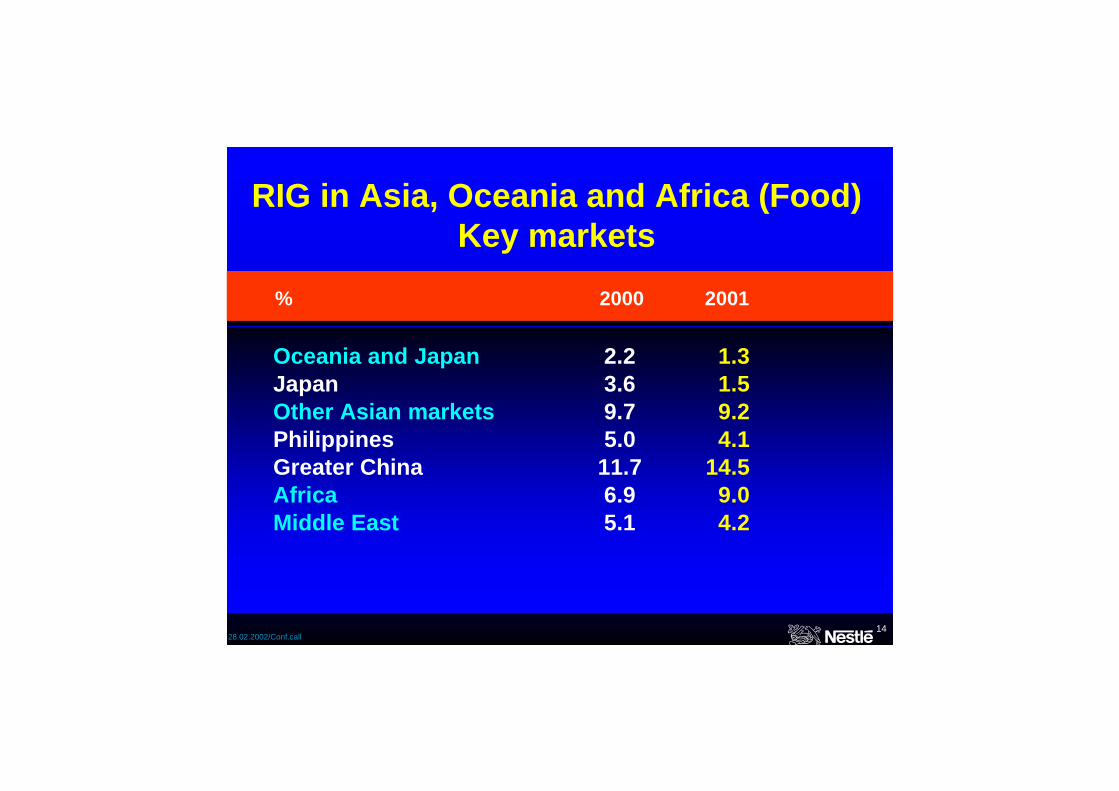

RIG in Asia, Oceania and Africa (Food)Key markets

Oceania and Japan 2.2 1.3Japan 3.6 1.5Other Asian markets 9.7 9.2Philippines 5.0 4.1Greater China 11.7 14.5Africa 6.9 9.0Middle East 5.1 4.2

% 2000 2001

1528.02.2002/Conf.call

RIG in Mineral Water (CHF 8.9 bio.)

United States (Bottled) 10.0 16.3Europe 2.2 2.2Asia 16.2 27.5Total Water (excl. Trinks) 5.4 9.1

Trinks 6.6 (1.3)Total Water (incl. Trinks) 5.7 7.1

% 2000 2001

1628.02.2002/Conf.call

RIG in Alcon and JVs

Alcon (CHF 4.6 bio) 7.1 9.2

Joint Ventures (CHF 1.2 bio) 8.2 8.2Galderma 15.7 6.1CPW 4.7 9.3

% 2000 2001

1728.02.2002/Conf.call

Sales and profitability by product group

Beverages 23.0 4.32 18.7 24.0 4.26 17.7

Milk products, 22.0 2.62 11.9 23.0 2.57 11.2nutrition, ice cream

Prep. dishes... 20.6 1.95 9.4 21.3 2.03 9.5& petcare

Chocolate, 11.0 1.17 10.6 11.2 1.23 11.0confect. & bisc.

Pharmaceutical 4.8 1.21 25.3 5.2 1.26 24.4

2000 2001 CHF bio. Sales Profit Margin* Sales Profit Margin *#

% %

* Calculation based on non-rounded figures for sales. The % variations are influenced not only by the evolution of sales volumes, but also by acquisitions and divestitures, exchange rate fluctuations, and changes in selling prices.# 2001 % margin negatively impacted by TTS review

1828.02.2002/Conf.call

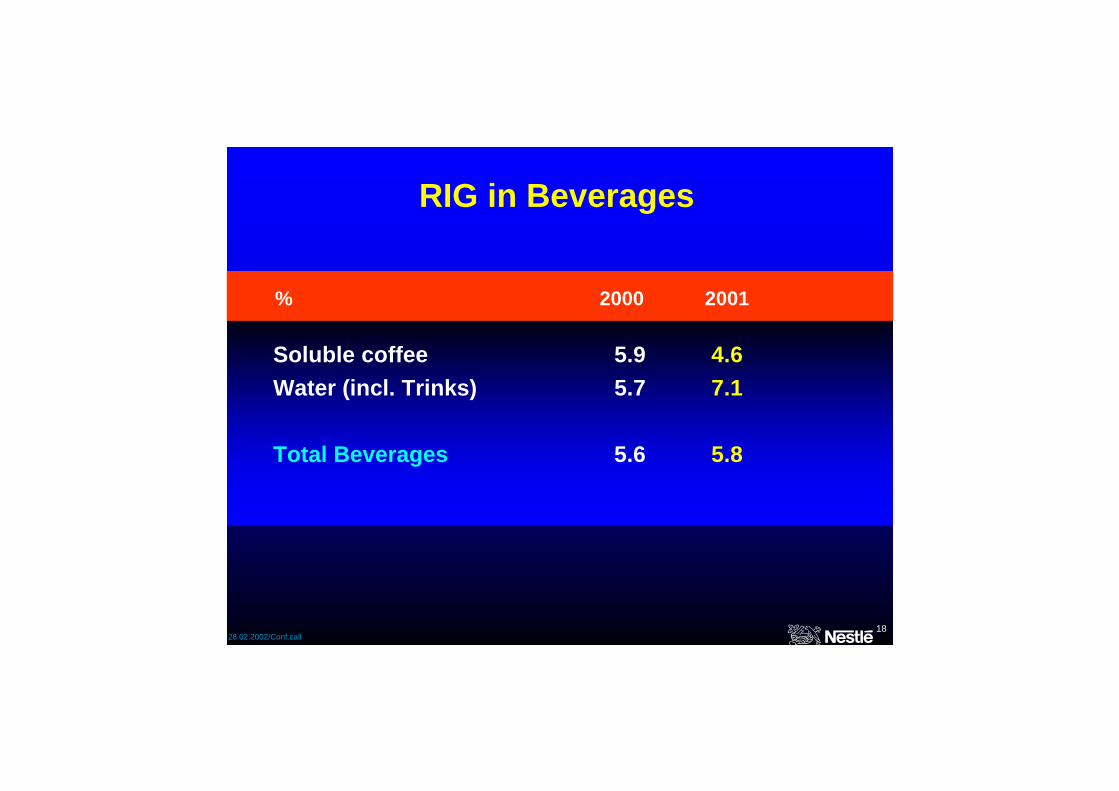

RIG in Beverages

Soluble coffee 5.9 4.6Water (incl. Trinks) 5.7 7.1

Total Beverages 5.6 5.8

% 2000 2001

1928.02.2002/Conf.call

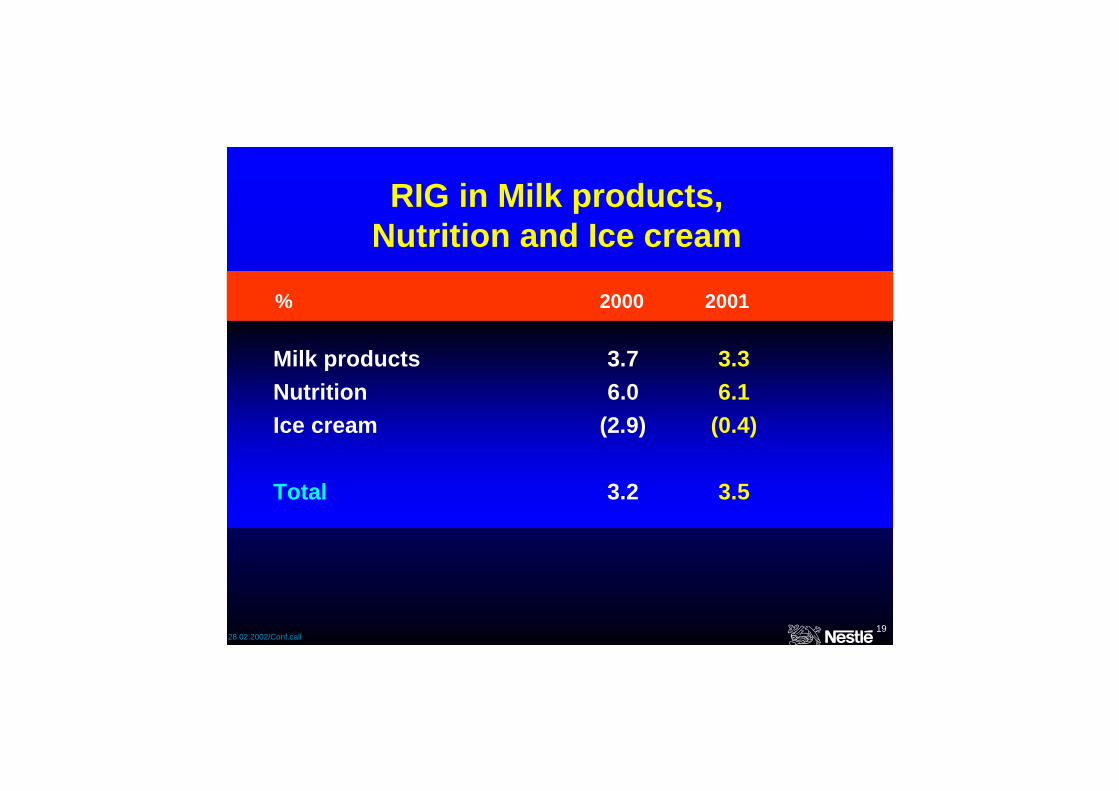

RIG in Milk products,Nutrition and Ice cream

Milk products 3.7 3.3Nutrition 6.0 6.1Ice cream (2.9) (0.4)

Total 3.2 3.5

% 2000 2001

2028.02.2002/Conf.call

RIG in Prepared dishes,Cooking aids and Petcare

Frozen and chilled 6.9 4.2Culinary and others 2.7 4.1Petcare 2.4 0.1

Total 4.0 2.9

% 2000 2001

2128.02.2002/Conf.call

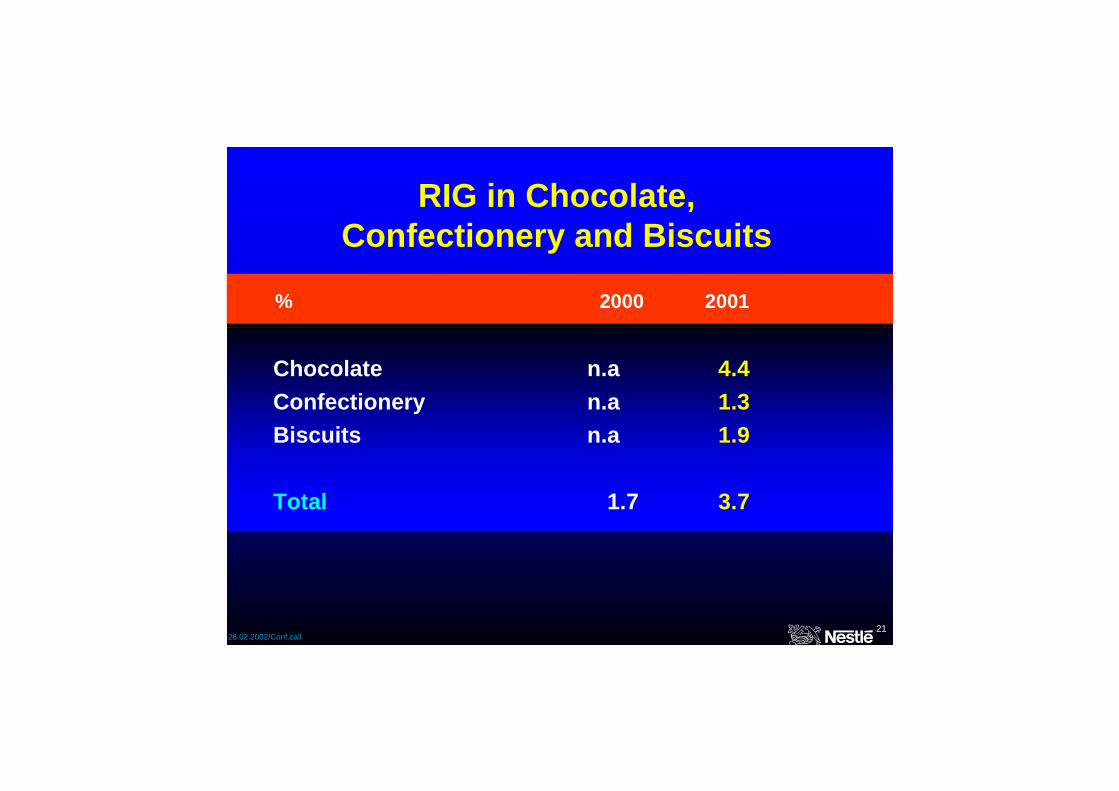

RIG in Chocolate,Confectionery and Biscuits

Chocolate n.a 4.4Confectionery n.a 1.3Biscuits n.a 1.9

Total 1.7 3.7

% 2000 2001

2228.02.2002/Conf.call

RIG in FoodServices

FoodServices 8.7 2.4

% 2000 2001

2328.02.2002/Conf.call

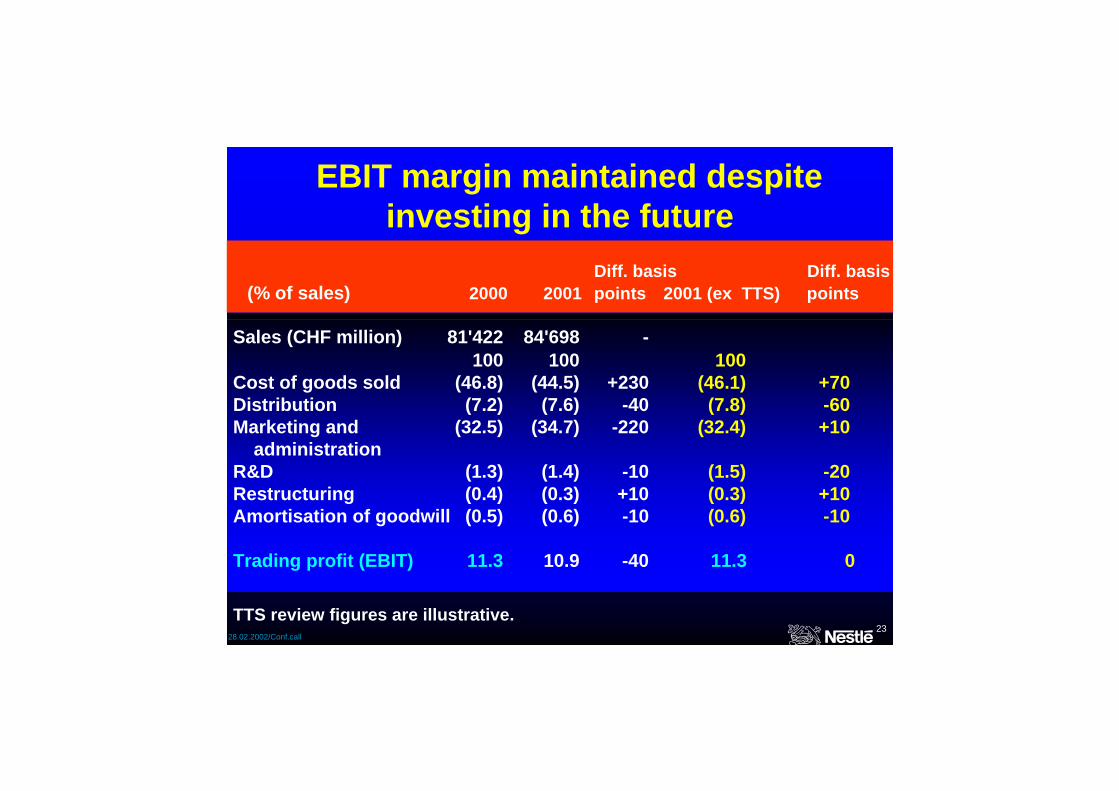

Sales (CHF million) 81'422 84'698 -100 100 100

Cost of goods sold (46.8) (44.5) +230 (46.1) +70Distribution (7.2) (7.6) -40 (7.8) -60Marketing and (32.5) (34.7) -220 (32.4) +10

administrationR&D (1.3) (1.4) -10 (1.5) -20Restructuring (0.4) (0.3) +10 (0.3) +10Amortisation of goodwill (0.5) (0.6) -10 (0.6) -10

Trading profit (EBIT) 11.3 10.9 -40 11.3 0

EBIT margin maintained despite investing in the future

Diff. basis Diff. basis(% of sales) 2000 2001 points 2001 (ex TTS) points

TTS review figures are illustrative.

2428.02.2002/Conf.call

Marketing investment continues -administrative costs fall

ActualCHF bio. % change %of sales

2000 2001 2000 2001

Marketing expenses 19.5 22.7 16.4 23.9 26.8excl. TTS review 19.5 19.9 2.0 23.9 24.2

Administration 7.0 6.7 (4.1) 8.6 7.9

TTS review figures are illustrative. Calculations based on non-rounded figures

2528.02.2002/Conf.call

Net profit - major improvement

Trading profit (EBIT) 11.3 10.9 -40 11.3 0

Net financing cost (0.9) (0.5) +40 (0.5) +40Net non-trading expenses (0.1) (0.1) (0.1)Taxes (3.4) (2.8) +60 (3.0) +40Outside interests (0.3) (0.2) +10 (0.2) +10Associated companies 0.5 0.6 +10 0.7 +20Net profit 7.1 7.9 +80 8.2 +110

Tax as % of pre-tax profit 33.1 27.7 +540

Diff. basis Diff. basis(%of sales) 2000 2001 points 2001 (ex TTS) points

TTS review figures are illustrative. Calculations based on non-rounded figures.

2628.02.2002/Conf.call

Agenda

Key achievements & figures Income statementCash flowBalance sheetUse of funds

2728.02.2002/Conf.call

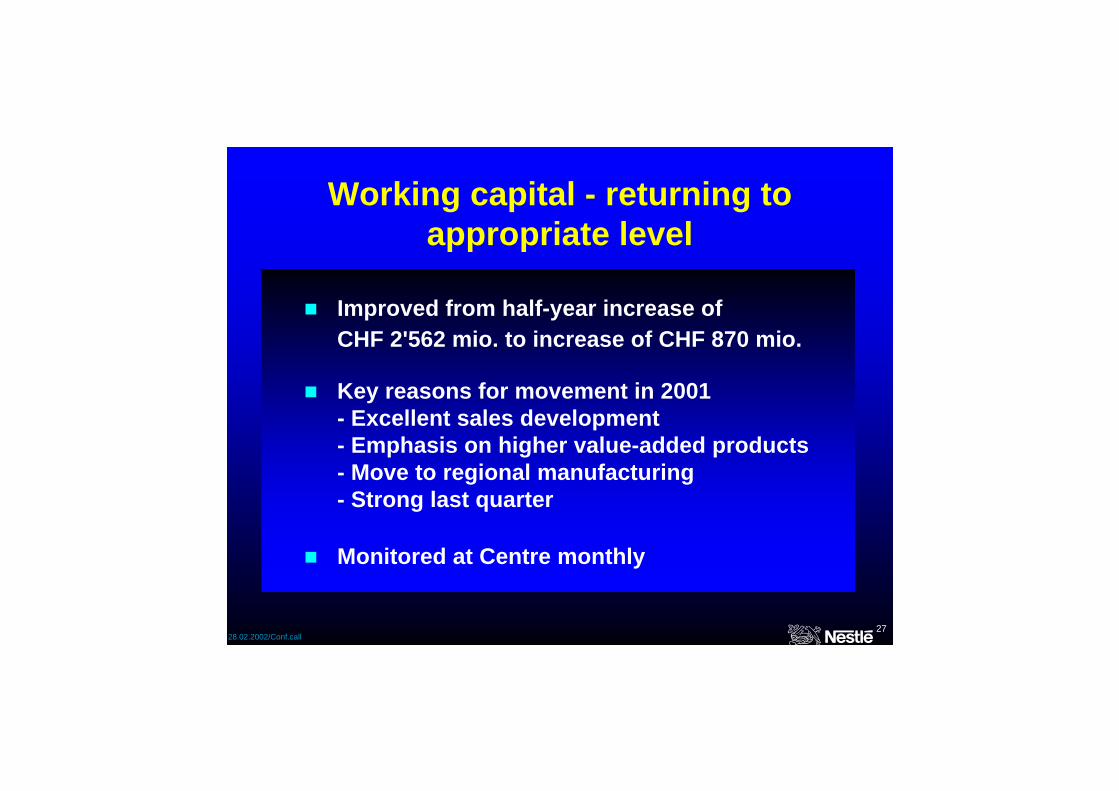

Improved from half-year increase of CHF 2'562 mio. to increase of CHF 870 mio.

Key reasons for movement in 2001- Excellent sales development- Emphasis on higher value-added products- Move to regional manufacturing- Strong last quarter

Monitored at Centre monthly

Working capital - returning to appropriate level

2828.02.2002/Conf.call

Healthy cash flow

9172691 4390 3706

5501 5599 4938

0

2000

4000

6000

8000

10000

1995 1996 1997 1998 1999 2000 2001

Free cash flow Operating Cash Flow (OCF)

CHF mio.

3839

5633

74016372

81878851 8614

2928.02.2002/Conf.call

Agenda

Key achievements & figures Income statementCash flowBalance sheetUse of funds

3028.02.2002/Conf.call

Gross tangible fixed assets 43'519 45'093

Less : accumulated depreciation (24'894) (25'195)

Net tangible fixed assets 18'625 19'898

Tangible fixed assets

CHF mio. 31.12.2000 31.12.2001

3128.02.2002/Conf.call

Return on average allocated assets*

FoodEurope 20.2 21.9Americas 33.6 32.9Asia, Oceania and Africa 38.7 37.7

Other activities 26.6 25.9

* Per Note 1 "Segmental information"

% 2000 2001

3228.02.2002/Conf.call

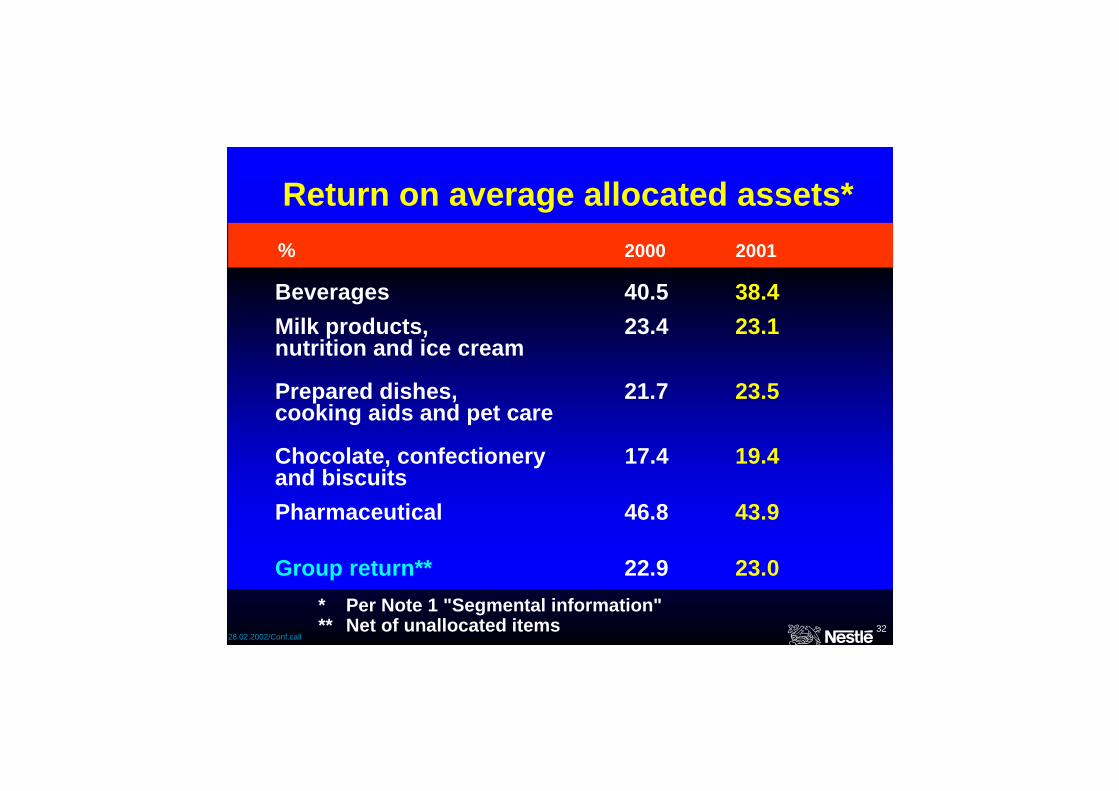

Return on average allocated assets*

* Per Note 1 "Segmental information"** Net of unallocated items

Beverages 40.5 38.4Milk products, 23.4 23.1nutrition and ice cream

Prepared dishes, 21.7 23.5cooking aids and pet care

Chocolate, confectionery 17.4 19.4and biscuitsPharmaceutical 46.8 43.9

Group return** 22.9 23.0

% 2000 2001

3328.02.2002/Conf.call

Agenda

Key achievements & figures Income statementCash flowBalance sheetUse of funds

3428.02.2002/Conf.call

AcquisitionsRalston Purina US Petcare 5.0 bio.Ice Cream Partners US Ice cream 1.1 bio.Water Eur, AOA,AMS Retail & Home 400 mio.

and officeDivestitures

Minag Germany Water 250 mio.David & Sons US Confectionery 160 mio.

Major acquisitions and divestments in 2001

Annual salesCompany Country Business (CHF)

3528.02.2002/Conf.call

The Ralston Purina transaction

Has added net debt of USD 10.3 bio. (CHF 17.3 bio. at 1.68 CHF vs. USD)

Favourable impact on WACC

3628.02.2002/Conf.call

Capital expenditure supports growth

25382815

3191 3093 3029 3056 30543261

2806

33053611

3061

4.34.15.5 5.6 5.9 5.4 5.3 5.4 5.0 4.7 4.3 3.8

0

500

1000

1500

2000

2500

3000

3500

4000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 20010

5

10

15

CHF mio. % of sales

3728.02.2002/Conf.call

Net indebtedness* up"AAA" maintained

* Total financial liabilities minus liquid assets.Liquid assets do not include the carrying value of treasury shares(CHF 2.8 bio. at year-end 2001)

CHF billion

H1 H2 H1 H2 H1 H2 H1 H21998 1999 2000 2001

6.03.0

6.69.5

6.2 5.2

19.4

9.1

0

4

8

12

16

20

24

3828.02.2002/Conf.call

Capital gain on partial IPO of Alcon (no material impact on taxes expected)

Realignment of the Group's Petcare assets to realise announced synergies, including US Distribution Network

Rationalisation of asset base triggered by increased globalisation and regionalisation of our businesses and implementation of Globe

Treatment of goodwill amortisation currently under review by IAS

Non recurring events anticipated for 2002