full year 2012 earnings · reserves as of jan. 1, 2012 net flows market forex scope reserves as of...

TRANSCRIPT

Full Year 2012

Earnings

February 21, 2013

Appendices

B2 – AXA FY12 Earnings – February 21, 2013

Table of content

Property & Casualty

Group

Life & Savings

Asset Management

Balance sheet

Business overview

Embedded Value and Cash Flows

B3 – AXA FY12 Earnings – February 21, 2013

FY12 APE by business

Well balanced business mix

G/A Protection

& Health

40%

G/A Savings

17%

Mutual Funds

& other

11%

Unit-Linked

32%

Life & Savings – Scope overview

Global footprint

FY12 APE by channel

Strong proprietary networks

FY12 APE by geography

UK

9%

Asia-Pacific (incl. Japan)

24%

NORCEE

18%

France

22%

MedLA

7%

Total: Euro 6,170 million

Agents & salaried

sales force

47%

Brokers - IFAs

34%

Partnerships

19%

US

20%

Total: Euro 6,170 million

Total: Euro 6,170 million

B4 – AXA FY12 Earnings – February 21, 2013

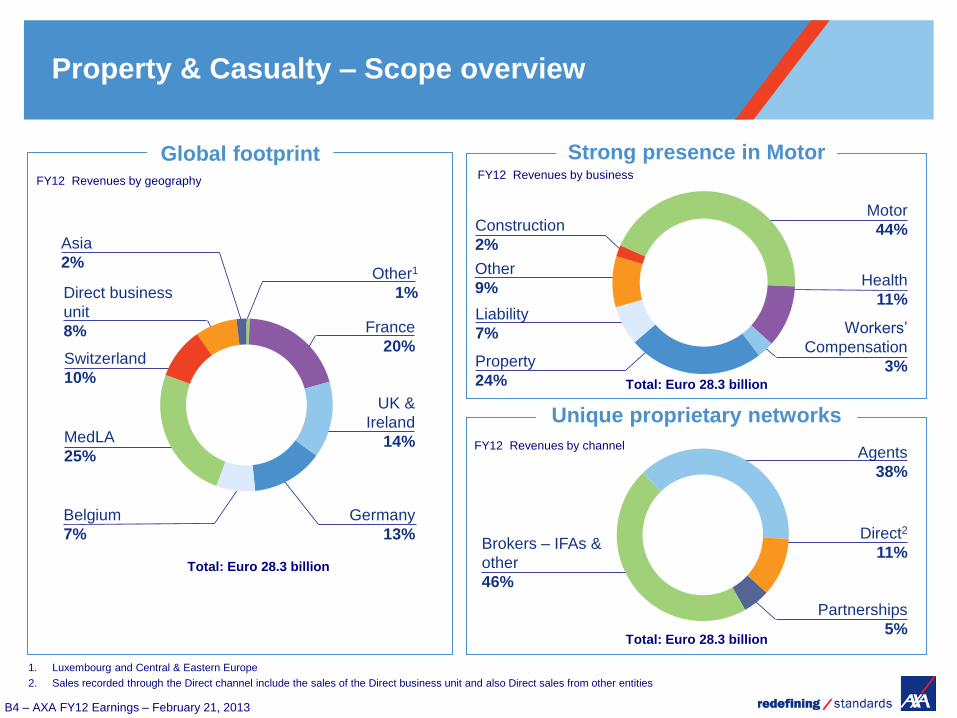

Motor

44%

Health

11%

Property

24%

Construction

2%

Direct2

11% Brokers – IFAs &

other

46%

Agents

38%

Partnerships

5%

Germany

13%

Switzerland

10%

MedLA

25%

France

20%

UK &

Ireland

14%

Belgium

7%

Direct business

unit

8%

Other1

1%

Property & Casualty – Scope overview

FY12 Revenues by channel

Unique proprietary networks

Strong presence in Motor

FY12 Revenues by geography

Total: Euro 28.3 billion

Total: Euro 28.3 billion

Total: Euro 28.3 billion

Asia

2%

FY12 Revenues by business

1. Luxembourg and Central & Eastern Europe

2. Sales recorded through the Direct channel include the sales of the Direct business unit and also Direct sales from other entities

Global footprint

Other

9%

Workers’

Compensation

3%

Liability

7%

B5 – AXA FY12 Earnings – February 21, 2013

Asset Management – Scope overview

Complementary business models

• Multi-expert model: structured by

“Expertise”

• Expertise in fixed income, equities,

quantitative equities

• Focus on alternative investments

(structured finance, private equity,

real estate, funds of hedge funds)

• Structured by “Investment Style”

• Focus on growth equities, value

equities, blend strategies, fixed

income

• New developments in alternative

investments

• Institutional research services

• Separate distribution platforms for third

parties & AXA insurance companies

• Integrated distribution platforms

• Mainly Europe • Mainly the US and Asia

Product

offer

Distribution

Footprint

• Euro 554 billion as at 31/12/2012 AuM • Euro 349 billion as at 31/12/2012

B6 – AXA FY12 Earnings – February 21, 2013

Table of content

Property & Casualty

Group

Life & Savings

Asset Management

Balance sheet

Business overview

Embedded Value and Cash Flows

B7 – AXA FY12 Earnings – February 21, 2013

Revenues

Revenues by segment

Asset Management

In Euro million FY11

International Insurance

Banking & Holdings

FY12

Revenues

Property & Casualty

Life & Savings

Reported

basis Comparable

basis

52,431

55,016

+5%

+3%

27,046

28,315

+5%

+3%

3,269

3,343

+2%

-3%

2,876

2,987

+4%

+3%

485

466

-4%

-3%

86,107

90,126

+5%

+2%

B8 – AXA FY12 Earnings – February 21, 2013

In Euro million

Underlying Earnings

FY113 FY12 Reported

change

Change at

constant

Forex

Life & Savings 2,138 2,635 +23% +19%

United States 235 522 +122% +107%

France 620 706 +14% +14%

NORCEE1 649 594 -8% -10%

UK -6 -17 +173% +158%

Asia-Pacific (incl. Japan) 575 712 +24% +14%

MedLA 102 162 +60% +60%

Other2 -36 -44 +23% +23%

Property & Casualty 1,848 1,895 +3% +1%

NORCEE1 807 945 +17% +16%

France 496 486 -2% -2%

MedLA 353 232 -34% -35%

UK & Ireland 211 154 -27% -29%

Asia 13 23 +79% +66%

Direct -33 54 n.a. n.a.

International Insurance 276 167 -40% -37%

Asset Management 321 382 +19% +14%

AllianceBernstein 106 159 +50% +39%

AXA IM 215 223 +4% +1%

Banking 32 5 -86% -86%

Holdings -843 -833 +1% +1%

Total 3,772 4,251 +13% +9%

Underlying Earnings by region

1. Northern, Central & Eastern Europe: Germany, Belgium, Switzerland, Central and Eastern Europe, Luxembourg and Russia (Property & Casualty only)

2. Other correspond to Architas, Family Protect and AXA Global Distributors

3. Restated for the change in accounting methodology on deferred acquisition costs (DAC) adopted retrospectively as at January 1, 2012

B9 – AXA FY12 Earnings – February 21, 2013

From Underlying Earnings to Net Income

Net realized capital gains/losses

Realized capital gains

In Euro million FY11*

Impairments

Hedging of equity portfolio

FY12

Adjusted Earnings

Underlying Earnings

Net realized capital

gains/(losses)

FY12

Restructuring costs

Net Income

of which impact from other assets

of which impact from equities &

alternative investments (2)

of which impact from interest rates and

credit spreads (1)

In Euro million FY11*

Adjusted Earnings

Change in fair value

(1) More favorable mark-to-market of interest rate derivatives

(2) Notably from private equity

(3) FY11: mainly Euro 902 million exceptional realized gains on the sale of AXA Canada, Euro 798 million from exceptional realized gains on the sale of the 15.6% stake in Taikang Life and Euro 626 million exceptional realized gains on the AXA APH transaction.

(4) FY11: mainly Euro -943m goodwill reduction attributable to US Accumulator Variable Annuity book of business.

Exceptional and discontinued

operations(3)

of which Forex impacts

Key drivers of change in Net income

3,772 4,251

(312) 297

682 815

(840) (283)

(154) (235)

3,460 4,548

3,460 4,548

110 45

(22) 71

32 54

41 61

58 (140)

2,069 (94)

(281) (244)

(1,167) (103)

4,190 4,152

* Restated for the change in accounting methodology on deferred acquisition costs

(DAC) adopted retrospectively as at January 1, 2012

Intangibles amortization and

other(4)

B10 – AXA FY12 Earnings – February 21, 2013

FY12 key sensitivities

Equities

Interest rates

Corporate spreads

• -25%

• +25%

• -100 bps

• +100 bps

• -75 bps

• +75 bps

o/w

Impairments

net of hedges

Net Income

In Euro billion

Net Unrealized

Capital Gains

and Losses

P&L Balance sheet

- 0.2 - 0.2 - 1.4

0.0 - 0.1 + 1.7

+ 0.8 + 8.2

- 0.3 - 7.6

+ 0.2 + 1.6

- 0.2 - 1.6

B11 – AXA FY12 Earnings – February 21, 2013

Table of content

Property & Casualty

Group

Life & Savings

Asset Management

Balance sheet

Business overview

Embedded Value and Cash Flows

B12 – AXA FY12 Earnings – February 21, 2013

Life & Savings

Revenues, new business volumes and profitability

Underlying earnings margin analysis

Underlying earnings margin analysis by product

1

2

3

page B13

page B14

page B20

B13 – AXA FY12 Earnings – February 21, 2013

United States

+8%

L&S Net inflows

Changes are on a comparable basis

In Euro billion

FY12 L&S revenues by region

L&S – Revenues and net inflows 1

MedLA

+1%

France

+1%

Asia Pacific (incl. Japan)

+6%

UK

+20%

NORCEE

-1%

Total: Euro 55.0 billion

Net flows by business

In Euro billion FY11 FY12

G/A Protection & Health +4.3 +4.8

G/A Savings -3.7 -3.9

Unit-Linked +2.4 +2.8

Mutual funds & other +0.2 +0.2

Total +3.3 +3.9

13.7

11.2

0.6 8.7

15.8

4.8

Net flows by country/region

In Euro billion FY11 FY12

France +0.7 +1.1

NORCEE +2.2 +1.5

United States -0.7 -0.2

United Kingdom +0.7 +0.2

Asia Pacific (incl. Japan) +2.2 +3.3

MedLA -1.9 -2.0

Total +3.3 +3.9

of which mature markets +1.5 +2.5

of which high growth markets +1.8 +1.5

B14 – AXA FY12 Earnings – February 21, 2013

L&S – Underlying earnings margin analysis

1. Changes are adjusted for Forex and scope effects related to sale of Bluefin, portfolios transferred to Resolution in November 2011, AXA APH transaction, ICBC-AXA transaction and the change in reporting period in Asia

2. Life & Savings gross written premiums and mutual fund sales. 3. Tax rate increased from 19% in FY11 to 21% in FY12 mainly due to unfavorable country mix, partly offset by higher tax one-offs which amounted to Euro 172 million in FY12 vs. Euro

143 million in FY11

Expenses Gross Margin

In Euro million

Margin on revenues2

Margin on assets

Technical margin

Acquisition expenses

Admin. Expenses

FY12 Comp.

Change1 In Euro million FY12 Comp.

Change1

Minority interest

Tax3

VBI amortization

+ -

-

2

UE from associates +

4,955 +2% -3,972 +14%

5,065 +5% -2,885 -1%

357 n.a. -179 -27%

86 +99%

Pre-tax underlying earnings +23%

Euro 3,426 million

-713 +30%

-78 n.a.

Underlying earnings +19%

Euro 2,635 million

(vs. Euro -205 million in FY11)

B15 – AXA FY12 Earnings – February 21, 2013

L&S – Margin analysis Details of margin on revenues

1. Life & Savings gross written premiums and mutual fund fees

x

Average margin on L&S revenues1

Life & Savings revenues1

Margin on revenues1

Changes are on a comparable basis

Margin on revenues

2

Detail by product

G/A Protection & Health: 14.7%

G/A Savings: 3.0%

Unit-Linked: 4.2%

Mutual funds & other: 9.3%

-2% business mix

+1% country mix

9.0% 0%

Euro 4,955 million +2%

Euro 55,016 million +3%

B16 – AXA FY12 Earnings – February 21, 2013

Unit-Linked average reserves

In Euro billion

Reserves as of Jan. 1, 2012

Net flows

Market

Forex

Scope

Reserves as of Dec. 31, 2012

L&S – Margin analysis Details of margin on Unit-Linked assets

Unit-Linked management fees

Margin on assets1

Average management fees on Unit-Linked reserves

Unit-Linked management fees

General account investment margin

x

135

+3

+12

-1

0

148

Changes are on a comparable basis

2

+

1. Including other fees (mainly mutual

funds and broker fees) of Euro 302 million

(-1% vs. FY11)

0% business mix

-2% country mix

147 bps -2%

Euro 2,066 million 0%

Euro 5,065 million +5% Euro 140 billion +2%

Euro 2,697 million +10%

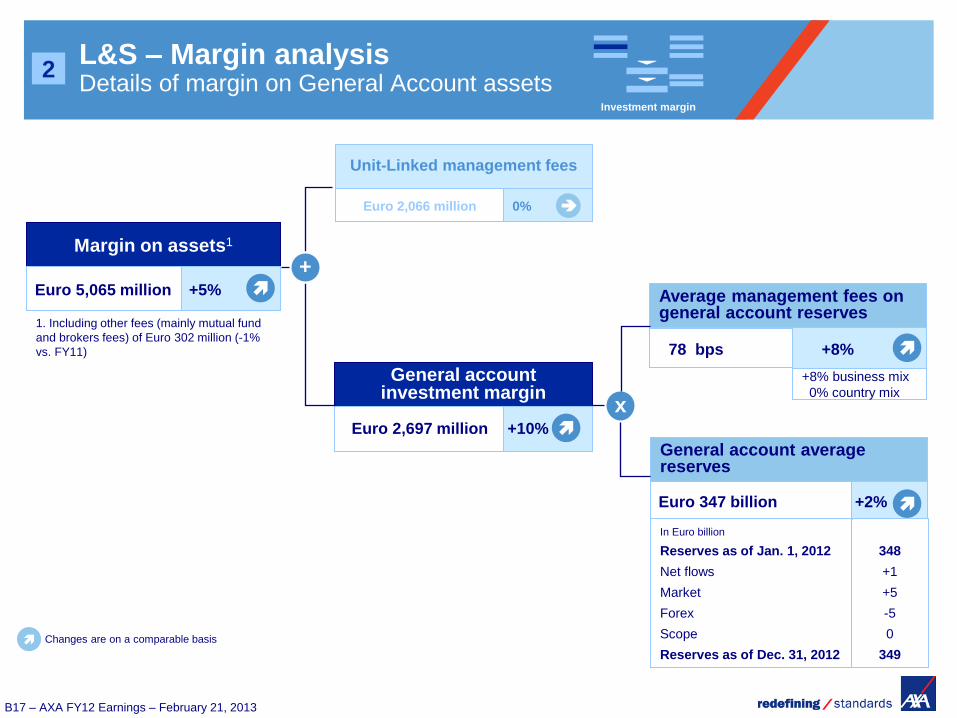

B17 – AXA FY12 Earnings – February 21, 2013

L&S – Margin analysis Details of margin on General Account assets

General account investment margin

Average management fees on general account reserves

General account average reserves

Investment margin

Unit-Linked management fees

Margin on assets1

+

x

In Euro billion

Reserves as of Jan. 1, 2012

Net flows

Market

Forex

Scope

Reserves as of Dec. 31, 2012

348

+1

+5

-5

0

349

2

Changes are on a comparable basis

1. Including other fees (mainly mutual fund

and brokers fees) of Euro 302 million (-1%

vs. FY11)

Euro 2,066 million 0%

Euro 5,065 million +5%

78 bps +8%

Euro 2,697 million +10%

Euro 347 billion +2%

+8% business mix

0% country mix

B18 – AXA FY12 Earnings – February 21, 2013

L&S – Margin analysis Details of technical margin

Technical margin

Technical margin

+

GMxB Variable Annuity margin

Mortality & morbidity margin and other1

In Euro million

Basis

Volatility (equity and interest rates)

Other

Reserve adjustments due to policyholder behavior, management actions including premium suspension and model refinements/assumptions, and refined reserving framework

-51

-249

-342

-401

1. Claims paid, maturities and surrenders

Changes are on a comparable basis

2

(vs. Euro -1,657 million in FY11)

Euro 1,400 million -6%

Euro 357 million n.a.

Euro -1,043 million -41%

(vs. Euro -205 million in FY11)

B19 – AXA FY12 Earnings – February 21, 2013

In Euro million

FY11 FY12

In Euro million FY12 GMxB VA technical margin evolution mainly explained by:

• Euro +0.3 billion driven by lower VA GMxB reserve adjustments,

including premium suspension on old contracts in the US and other

model and assumption refinements, and refined reserving framework

• Euro +0.2 billion improvement in VA GMxB hedging result, mainly in

the US due to decreased volatility and basis losses

Euro -0.4 billion net Underlying

Earnings impact

Gross mortality, morbidity &

surrender margin (pre-tax)

Gross GMxB Variable Annuity

technical margin (pre-tax, pre-DAC)

2 L&S – Margin analysis Focus on gross technical margin

1,4001,452

FY12 FY11

-1,043

-1,657

FY12 mortality, morbidity & surrender margin evolution mainly

explained by:

• Euro +0.1 billion in G/A Protection & Health mainly driven by more

favorable reserve development in France and non repeat of the 2011

Great East Japan earthquake impact

• Euro -0.1 billion in G/A Savings mainly due to the non repeat of 2011

favorable exceptional mortality and disability experience in

Switzerland

• Euro -0.1 billion in Unit-Linked mainly resulting from unfavorable

mortality experience in the US

B20 – AXA FY12 Earnings – February 21, 2013

L&S – FY12 Underlying Earnings by business

G/A Protection & Health

Euro million

Unit-Linked

Pre-tax Underlying Earnings

FY12

G/A Savings

Mutual funds & Other

Tax and minority interest

Underlying Earnings

% change on comp. basis

3

Changes are adjusted for Forex and scope effects related to sale of Bluefin, portfolios transferred to Resolution in November 2011, AXA APH transaction, ICBC-AXA transaction and the change in reporting period in Asia

2,201 2,273 0%

553 692 +25%

-4 504 n.a.

9 -44 n.a.

2,759 3,426 +23%

-621 -791

2,138 2,635 +19%

FY111

1. Restated for the change in accounting methodology on deferred acquisition costs (DAC) adopted retrospectively as at January 1, 2012

B21 – AXA FY12 Earnings – February 21, 2013

G/A Protection

& Health G/A Savings Unit-Linked

Mutual Funds &

Other

Margin on revenues

L&S – FY12 Margin analysis by business

Investment margin

Management fees

Technical margin & Other

Gross margin

Acquisition

Expenses

Pre-tax UE

Admin Exp.

& Other

3

9%

% of GWP

78 bps

of avge G/A reserves

147 bps

of avge UL reserves

Main profit drivers

3,786 360 660

867 1,613 177

0 0 2,066

1,381 -49 -929

6,034 1,924 1,974 444 10,376

-1,373 -625 -820 -159 -2,978

-2,388 -606 -650 -328 -3,972

2,273 692 504 -44 3,426

In Euro million

B22 – AXA FY12 Earnings – February 21, 2013

L&S –Margin analysis by business G/A Protection & Health

Technical result

Protection & Health GWP

Protection & Health

Combined ratio (in %)

In Euro million FY12

x

Net technical result

Net investment margin

Protection & Health

Average reserves

Protection & Health

investment spread

In Euro million FY12

x

Investment margin

+

Comp.

change Comp.

change

3

25,706 +2%

155,885 +2%

94.7% +0.6 pt

56 bps +6 bps

1,406 -8%

867 +14%

Pre-tax underlying earnings 0%

Euro 2,273 million

Changes are adjusted for Forex and scope effects related to sale of Bluefin, portfolios transferred to Resolution in November 2011, AXA APH transaction, ICBC-AXA transaction and the change in reporting period in Asia

B23 – AXA FY12 Earnings – February 21, 2013

L&S – Margin analysis by business G/A Savings

FY12 In Euro million

FY12

x x

+

Technical margin

& Other

FY12

Acquisition costs Administrative

expenses & Other -

G/A Savings

Gross revenues

Margin on

G/A Savings revenues

Margin on revenues

G/A Savings

average reserves

G/A Savings

Investment spread

Investment margin

Comp.

change

Comp.

change

Comp.

change

3

11,950 -12% 190,941 +3%

3.0% +0.5 bp 84 bps +4 bps

360 +4% 1,613 +7%

-49 n.a.

Gross margin +1%

Euro 1,924 million

-606 -6%

-625 -11%

Pre-tax underlying earnings +25%

Euro 692 million

(vs. Euro +52 million in FY11)

Changes are adjusted for Forex and scope effects related to sale of Bluefin, portfolios transferred to Resolution in November 2011, AXA APH transaction, ICBC-AXA transaction and the change in reporting period in Asia

B24 – AXA FY12 Earnings – February 21, 2013

Margin on revenues

L&S – Margin analysis by business Unit-Linked

FY12 FY12

x x

+

Technical margin

& Other

FY12

Investment margin

258

o/w GMxB VA margin

Acquisition costs Administrative

expenses & Other -

Unit-Linked

Gross revenues

Average margin on

Unit-Linked revenues

Unit-Linked

Average reserve

Unit-Linked average

Management fees

Unit-Linked

Management fees

Comp.

change

Comp.

change

Comp.

change

In Euro million

3

(vs. Euro -336 million in FY11*)

(vs. Euro -1,504 million in FY11)

* Restated for the change in accounting methodology on deferred acquisition costs (DAC) adopted retrospectively as at January 1, 2012

15,759 +19% 140,102 +2%

4.2% +0.2 pt 147 bps -2%

660 +24% 2,066 0%

-929 n.a.

-1,043 -41%

177 +12%

Gross margin +70%

Euro 1,974 million

-650 n.a.

-820 -6%

Pre-tax underlying earnings n.a.

Euro 504 million

Changes are adjusted for Forex and scope effects related to sale of Bluefin, portfolios transferred to Resolution in November 2011, AXA APH transaction, ICBC-AXA transaction and the change in reporting period in Asia

B25 – AXA FY12 Earnings – February 21, 2013

Focus on US VA GMxB Refined hedging and reserving approach and strengthened policyholder behavior assumptions

1. Long term view of interest rates set at 3% based on post crisis 10-15 year

duration swap market observations and extended duration of the business due to

low lapse rates

2. Underlying earnings impact is net of DAC and tax

Refined hedging and reserving approach

• Market consistent valuation of annuity at point of

annuitization

• IFRS GMxB reserve calculated by discounting future

value of annuity and death benefits at flat 3%1

Change in IFRS reserve remains fully booked through

Underlying Earnings in the same accounting period

Reduces interest rate sensitivity of IFRS

reserve by 25%

Positioned for greater upside in rising

interest rates

Future lapse rates after the surrender charge period have

an interest-sensitive dynamic function and are floored at

1.5% to 2.5%, for deep “in-the-money” policies

Prudent policyholder behavior assumptions

Pro-rata partial withdrawals have an interest-sensitive

dynamic function that reduces pro-rata withdrawals by

30% in low interest rate environment

Expected to reduce the risk of future

significant reserve strengthening

from policyholder behavior

Euro -470 million on

Underlying Earnings2 150bps reduction in lapse floor

Euro -130 million on

Underlying Earnings2

Reduce dynamic pro-rata partial

withdrawals by 70%

Limited downside risk:

B26 – AXA FY12 Earnings – February 21, 2013

Table of content

Property & Casualty

Group

Life & Savings

Asset Management

Balance sheet

Business overview

Embedded Value and Cash Flows

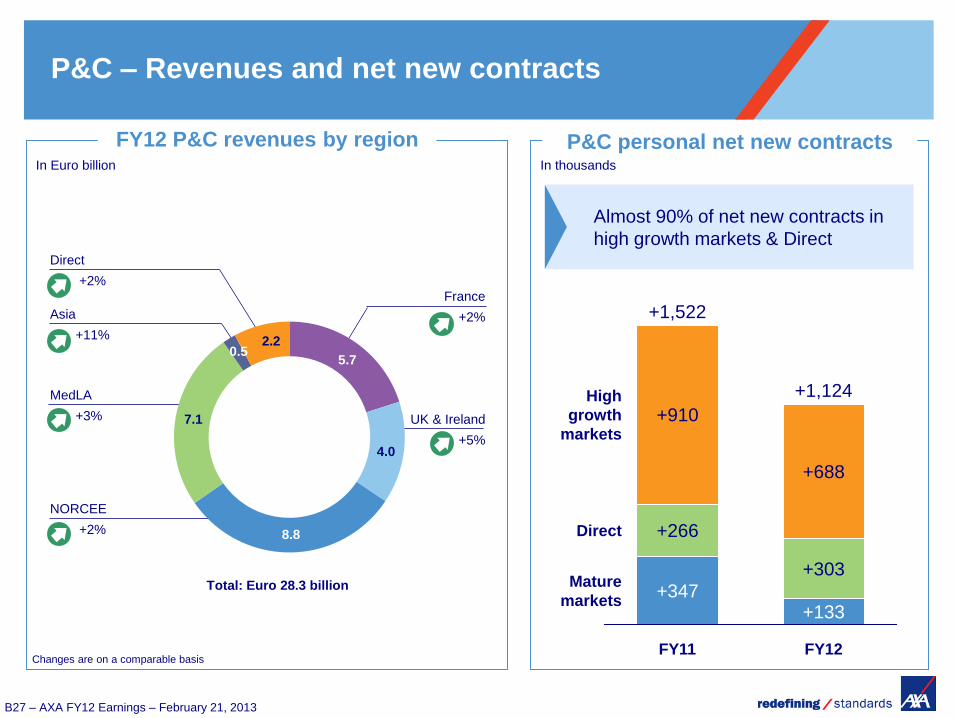

B27 – AXA FY12 Earnings – February 21, 2013

UK & Ireland

+5%

Asia

+11%

France

+2%

NORCEE

+2%

MedLA

+3%

Direct

+2%

P&C personal net new contracts In thousands

Changes are on a comparable basis

In Euro billion

FY12 P&C revenues by region

5.7

7.1

2.2 0.5

8.8

4.0

Almost 90% of net new contracts in

high growth markets & Direct

P&C – Revenues and net new contracts

Total: Euro 28.3 billion +347

+266

+910

Mature

markets

Direct

High

growth

markets

FY12

+1,124

+133

+303

+688

FY11

+1,522

B28 – AXA FY12 Earnings – February 21, 2013

4. Tax rate increased at 31% vs. 28% in FY11, reflecting

higher pre-tax underlying earnings and lower tax one-offs.

Underlying earnings

Euro 1,895 million

Pre-tax underlying earnings

Euro 2,722 million

P&C – Underlying Earnings analysis

Minority interest +11 n.a.

Tax4 -838 +11%

Net technical result

Revenues

Combined ratio1 (in %)

28,315 +3%

97.6% -0.3 pt

In Euro million FY12 Comp.

Change

x

Net technical result2 673 +19%

Net investment income

Average P&C assets

Average asset yield3

55,430 +1%

3.6% -3%

In Euro million FY12 Comp.

Change

x

Net investment income 2,007 -2%

+

-

+2%

+1%

1. Combined ratio calculated based on gross earned premiums

2. Technical result net of expenses

3. Net of interests credited to P&C reserves relating to annuities.

Gross asset yield was 3.9%

UE from associates 43 +10% +

B29 – AXA FY12 Earnings – February 21, 2013

Combined Ratio -0.1 pt

Loss Ratio (%)

-0.2 pt

-0.1 pt change on a comparable basis

-0.2 pt change on a comparable basis

Changes are on a reported basis

Expense Ratio (%)

P&C – Details on Combined Ratio

26.8% 26.3%

Expense

Ratio

Loss

Ratio

FY12

97.6%

26.8%

70.8%

FY11

97.9%

27.0%

70.9% FY12

70.8%

Prior year

reserve

dev.

+0.5 pt

Nat Cat

-0.3 pt

Current

accident

year

-0.3 pt

FY11

70.9%

FY12

26.8%

Adm.

Expenses

-0.2 pt

Acq.

expenses

0.0 pt

FY11

27.0%

B30 – AXA FY12 Earnings – February 21, 2013

P&C – Focus on reserve developments

Prior year reserve development level

(in % of gross earned premiums)

Reserving ratio (Net technical reserves/Net earned premiums)

Note: FY04 to FY09 figures do not exclude Canadian operations

FY10

3.1%

FY08

5.4%

FY07

2.7%

FY06

1.4%

FY05

0.9%

FY04

0.3%

FY12

1.2%

FY09

5.4%

FY11

1.7%

186%

FY09

187% 186%

FY11

187%

FY10 FY12 FY08

187%

FY07

194%

FY06

186%

FY05

193%

FY04

193%

B31 – AXA FY12 Earnings – February 21, 2013

Personal Motor Personal non motor

Total P&C

Total commercial lines incl. Construction & Work. Comp.

P&C – Details on current year loss ratios

1. Other includes opening adjustments, changes in mix, claims handling costs, reinsurance impact excl. Nat Cat, other changes in reserves, Forex and scope

-1.7pts

Nat Cat

-0.2pt

FY11

Current

loss ratio

77.1%

FY12

Current

loss ratio

75.4%

Other

+1.8pts

Frequency &

severity

-1.7pts

Price effect FY12

Current

loss ratio

64.5%

Other

+1.1pts

Frequency &

severity

+1.4pts

Price effect

-2.3pts

Nat Cat

-0.4pt

FY11

Current

loss ratio

64.8%

1 1

Price effect

-2.0pts

Nat Cat

-0.1pt

FY11

Current

loss ratio

74.2%

FY12

Current

loss ratio

74.5%

Other

+1.0pt

Frequency &

severity

+1.5pts

1 FY12

Current

loss ratio

72.0%

Other

+1.1pts

Frequency &

severity

+0.4pt

Price effect

-1.8pts

Nat Cat

-0.3pt

FY11

Current

loss ratio

72.6%

1

B32 – AXA FY12 Earnings – February 21, 2013

Table of content

Property & Casualty

Group

Life & Savings

Asset Management

Balance sheet

Business overview

Embedded Value and Cash Flows

B33 – AXA FY12 Earnings – February 21, 2013

Underlying earnings

Euro 382 million

Expenses Margin

In Euro million

Asset Management fees 2,850 -4%

Distribution revenues 493 +5%

Asset Management

expenses -2,248 -9%1

Distribution expenses -495 +9%

FY12 Comp.

Change In Euro million FY12

Comp.

Change

Minority int.& other -139 +19%

Tax2 -189 +23%

+ -

Pre-tax underlying earnings

Euro 710 million

-

+14%

+13%

Investment result 107 -1%1

AM - Underlying Earnings Details of Asset Management margin analysis

1. Changes are restated from deferred compensation benefits variances that have zero net P&L impact with impacts in investment results fully offset in expenses (Euro -14 million impact

in FY11 and Euro +12 million in FY12).

2. Tax rate up from 25% in FY11 to 27% in FY12

B34 – AXA FY12 Earnings – February 21, 2013

AM – Underlying Earnings Details on Asset Management revenues

Average Asset Management fees

on Assets under Management

33 bps -4%

Average Assets under

Management

Euro 870 billion 0%

Asset Management fees

Euro 2,850 million -4%

x

In Euro billion

AUM as of Jan. 1, 2012

Net inflows

o/w AllianceBernstein

o/w AXA IM

Market & other

Forex

Scope

AUM as of Dec. 31, 2012

847

-1

-4

+3

+73

-3

-13

903

o/w performance fees (Euro 137 million, +14%)

o/w research fees (Euro 321 million, -5%)

Changes are on a comparable basis

B35 – AXA FY12 Earnings – February 21, 2013

Table of content

Property & Casualty

Group

Life & Savings

Asset Management

Balance sheet

Business overview

Embedded Value and Cash Flows

B36 – AXA FY12 Earnings – February 21, 2013

Balance sheet

General accounts invested assets

1.1 Government bonds & related

1.2 Corporate bonds

1.3 CDS

1.4 ABS

1.5 Equity

1.6 Real Estate

1.7 Hedge Funds

1.8 Private Equity

1.9 Mortgage loans

Solvency

Net financial debt

1

2

3

Page B37

page B38

page B39

page B42

page B43

page B47

page B49

page B50

page B51

page B52

Page B56

Page B60

B37 – AXA FY12 Earnings – February 21, 2013

General Account invested assets

Fixed income 384 82% 404 82%

o/w govies and related 207 44% 219 45%

o/w Corporate bonds 148 32% 151 31%

o/w Asset backed securities 8 2% 9 2%

o/w Mortgage loans & other 1 22 5% 25 5%

Cash 29 6% 28 6%

Listed equities 14 3% 15 3%

Real Estate 22 5% 23 5%

Alternative Investments2 13 3% 15 3%

Policy loans 6 1% 6 1%

Total Insurance Invested Assets3 467 100% 491 100%

Changes in asset allocation

• Net inflows, investment income and

maturities: invested mainly in corporate

and government bonds

• Mark to market: fixed income assets

benefiting from interest rates decrease and

general spread tightening across most

major European govies

Invested assets (100%) In Euro billion

% % FY12 FY11

1. Mortgage loans & other include residential loans (Euro 12 billion), commercial & agricultural loans (Euro 10 billion) and Agency Pools (Euro 3 billion)

2. Mainly Private Equity and Hedge Funds

3. FY12 invested assets referenced in page 57 of the financial supplement are Euro 677 billion, which include notably Euro 147 billion of Unit-linked contracts and Euro 34

billion related to the banking segment

B38 – AXA FY12 Earnings – February 21, 2013

The Netherlands

2%

Italy

8%

P&C

~11%

L&S

~87%

Other2

~2%

Austria

3% Spain

3%

US

6%

Belgium

13%

France

24%

Breakdown by geography

Total: Euro 219 billion As of Dec 31, 2012

Japan

12%

Germany

12%

Switzerland

7%

Other

~7% Supranational institutions

3%

1. Gross of tax and policyholders’ participation

2. Other includes International Insurance and Holdings segments

Breakdown by segment

Government bonds and related 1.1

Gross1 unrealized capital

gains and losses

10.2

25.3

FY11 FY12

In Euro billion

B39 – AXA FY12 Earnings – February 21, 2013

A

~41%

AAA

~8%

Industrial

7%

Communications

9%

Total: Euro 151 billion

Consumer

cyclical

5%

Consumer non-cyclical

12%

Banks

34%

Other financials

10%

Utilities

9%

Energy

5%

Basic materials

5% Other

2%

Corporate bonds 1.2

Single A range

Other2

~2%

Breakdown by segment

P&C

~14%

L&S

~84%

Gross1 unrealized capital gains and losses

9.2

3.0

FY12 FY11

In Euro billion

BBB

~29%

AA

~11%

Other

~11%

1. Gross of tax and policyholders’ participation

2. Other includes International Insurance and Holdings segments

Breakdown by industry

Technology

2%

As of Dec 31, 2012

B40 – AXA FY12 Earnings – February 21, 2013

Gross market

value

in Euro billion

Senior debt Sub debt

Total Secured

Non

secured

Lower

Tier 2

Upper

Tier 2 Tier 1 Preferred

United States 0.2 7.2 1.9 0.0 0.1 0.0 9.3

France 2.7 3.2 1.1 0.0 0.0 0.0 7.0

Netherlands 2.7 2.6 0.3 0.0 0.1 0.0 5.7

Spain 4.0 0.7 0.2 0.0 0.0 0.0 4.9

UK 0.8 2.8 0.8 0.0 0.2 0.0 4.6

Germany 2.7 0.3 0.9 0.5 0.2 0.0 4.5

Australia 0.8 2.5 0.2 0.0 0.1 0.0 3.7

Italy 1.0 1.3 0.1 0.0 0.0 0.0 2.3

Switzerland 0.6 1.4 0.1 0.0 0.0 0.0 2.2

Sweden 0.4 1.3 0.1 0.0 0.1 0.0 1.9

Norway 0.5 0.5 0.0 0.0 0.0 0.0 1.0

Canada 0.3 0.5 0.0 0.0 0.0 0.0 0.8

Other1 0.7 1.8 0.2 0.1 0.0 0.0 2.9

TOTAL 17.3 25.9 6.0 0.6 0.9 0.0 50.8

1. More than 30 countries

Focus on banking corporate bonds 1.2

As of Dec 31, 2012

B41 – AXA FY12 Earnings – February 21, 2013

Euro billion

As of December 31, 2012 US UK Japan Germany Switzerland France Other1 Total

P NP NP NP P NP P NP P NP P NP P NP

AAA 0 0 0 1 3 1 2 1 3 1 0 0 9 4

AA 1 2 0 3 1 0 2 0 3 1 2 1 9 7

A 3 9 1 7 5 1 6 1 12 5 6 4 32 29

BBB 3 9 1 2 4 1 4 1 9 4 4 2 24 20

Below invest. grade 0 1 0 0 2 0 2 0 2 1 0 1 6 4

Non rated 0 0 0 0 1 0 2 0 1 0 1 2 5 3

Total 7 20 3 14 16 4 17 3 30 13 14 11 84 67

Corporate bonds breakdown by country (including CDS)

P = Participating NP = Non-participating

1. Including Belgium, AXA MPS, Spain, Italy, Asia Pacific (exc. Japan), Other

1.2

B42 – AXA FY12 Earnings – February 21, 2013

• CDS mainly used as alternative to investment grade corporate bonds

• Overlay strategy: synthetically replicate corporate bonds by selling CDS on top of government

bonds to enhance return

• NBT strategy: buy credit derivatives on corporate names to form negative basis trade

Euro million

Overlay strategy

Net notional as of

Dec 31, 2012

NBT strategy

Net notional as of

Dec 31, 2012

Total

Net notional as of

Dec 31, 2012

AAA 161 - 161

AA 828 (35) 793

A 2,765 (348) 2,417

BBB 1,663 (4,097) (2,434)

Below invest. grade 47 (1,105) (1,057)

Non rated (13) (83) (95)

Total 5,451 (5,666) (215)

Corporate bonds: focus on CDS 1.3

Represents

total market

value of

Euro -207 million

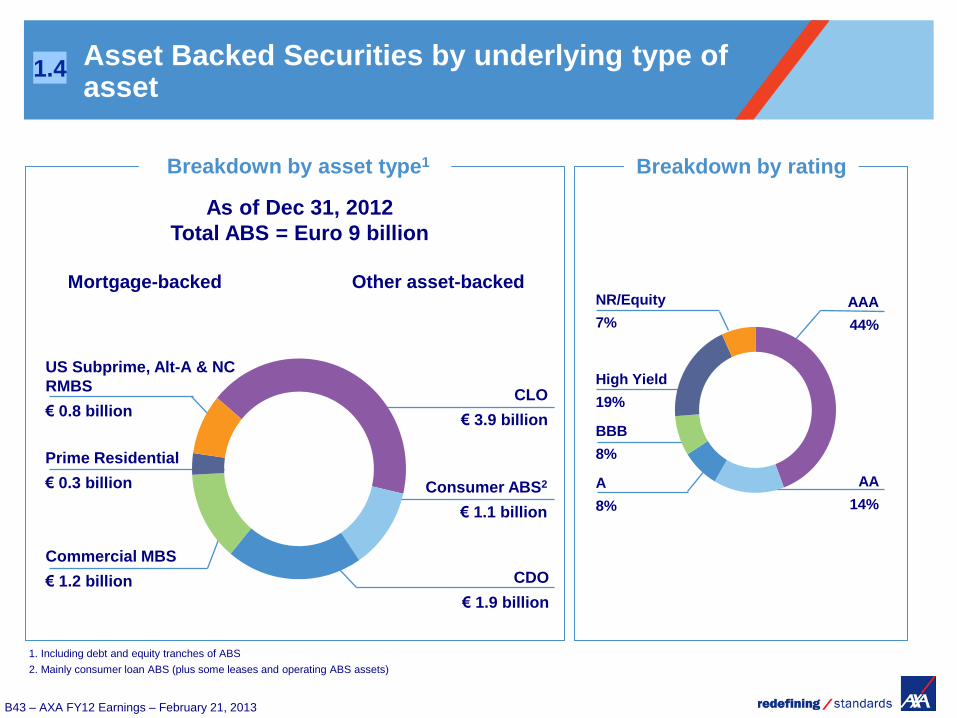

B43 – AXA FY12 Earnings – February 21, 2013

High Yield

19%

BBB

8%

AA

14%

AAA

44%

1. Including debt and equity tranches of ABS

2. Mainly consumer loan ABS (plus some leases and operating ABS assets)

CDO

€ 1.9 billion

Consumer ABS2

€ 1.1 billion

CLO

€ 3.9 billion

Commercial MBS

€ 1.2 billion

US Subprime, Alt-A & NC

RMBS

€ 0.8 billion

Prime Residential

€ 0.3 billion

Mortgage-backed Other asset-backed

As of Dec 31, 2012

Total ABS = Euro 9 billion

Asset Backed Securities by underlying type of asset

Breakdown by asset type1 Breakdown by rating

1.4

A

8%

NR/Equity

7%

B44 – AXA FY12 Earnings – February 21, 2013

Credit risk management: ABS investments

Group ABS Exposure Asset values

In Euro million 31/12/2011 31/12/12 31/12/2011 31/12/12

Mortgage-backed

Prime Residential 494 291 80% 88%

Commercial MBS 1,323 1,210 59% 61%

UK & NC RMBS 108 122 57% 71%

US Subprime 676 673 45% 52%

US Alt-A 36 20 27% 52%

Other asset-backed

Consumer ABS 934 1,096 88% 95%

CLO 3,195 3,928 84% 87%

Investment Grade CDO 1,070 1,588 70% 91%

High-Yield CDO 63 46 48% 55%

Structured Finance CDO 25 42 20% 28%

Other CDO 167 223 43% 79%

Total 8,092 9,239 71% 79%

1.4

Group ABS exposure increased mainly driven by:

• Market effect of Euro 1 billion mainly driven by performance of CMBS and Investment Grade

CDO’s

• Net flows of Euro 0.3 billion, comprised of Euro 2.4 billion of purchases mainly on CLO’s and

Consumer ABS, and Euro 2.1 billion of sales and redemptions

• Minor evolution of scope of Euro -0.1 billion and forex impact of Euro -0.1 billion

B45 – AXA FY12 Earnings – February 21, 2013

Euro million

As of December 31, 2012

(unless indicated)

Prime Residential

MBS Commercial MBS UK & NC RMBS

US Subprime

RMBS US Alt-A RMBS

% of par @ 31/12/09 89% 75% 59% 42% 14%

% of par @ 31/12/10 87% 69% 65% 51% 21%

% of par @ 31/12/11 80% 59% 57% 45% 27%

% of par @ 31/12/12 88% 61% 71% 52% 52%

AAA 165 110 13 3 0

AA 74 53 65 24 0

A 21 229 10 100 2

BBB 14 262 1 48 1

Below invst. Grade 12 555 28 495 17

Equity / Non rated 6 - 5 3 0

Value 291 1,210 122 673 20

Shareholder Exposure 72% 86% 77% 38% 79%

OCI1 57% 84% 43% 92% 82%

P&L 43% 16% 57% 8% 18%

Focus on Mortgage-Backed Securities

1. Fair value changes of assets classified as available for sale are recognized in the OCI component in shareholders’ equity.

1.4

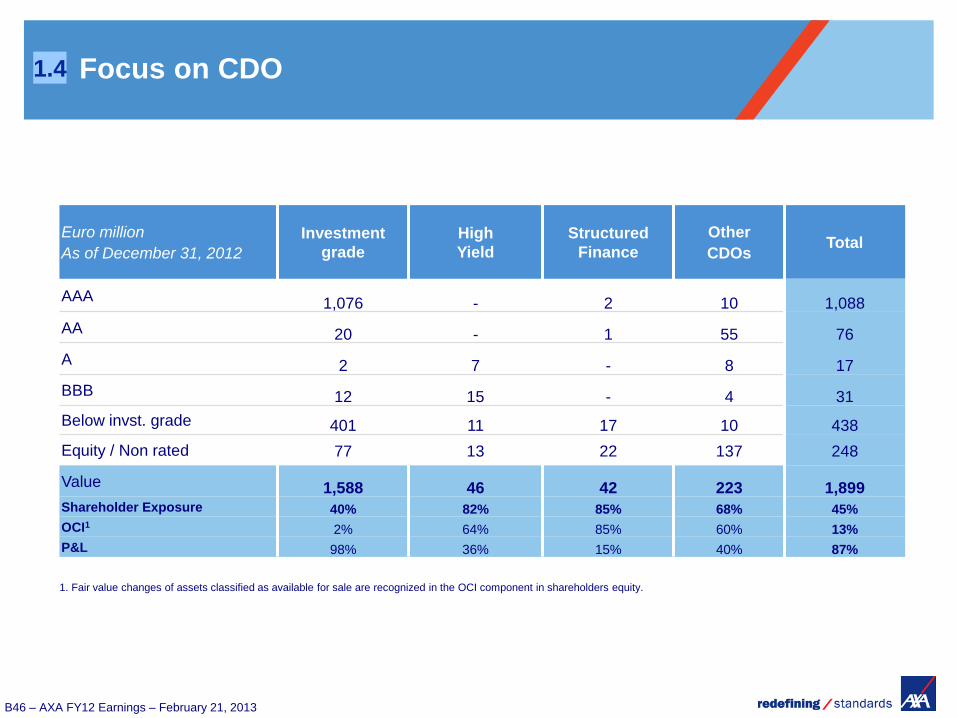

B46 – AXA FY12 Earnings – February 21, 2013

Euro million

As of December 31, 2012

Investment

grade

High

Yield

Structured

Finance

Other

CDOs Total

AAA 1,076 - 2 10 1,088

AA 20 - 1 55 76

A 2 7 - 8 17

BBB 12 15 - 4 31

Below invst. grade 401 11 17 10 438

Equity / Non rated 77 13 22 137 248

Value 1,588 46 42 223 1,899 Shareholder Exposure 40% 82% 85% 68% 45%

OCI1 2% 64% 85% 60% 13%

P&L 98% 36% 15% 40% 87%

Focus on CDO

1. Fair value changes of assets classified as available for sale are recognized in the OCI component in shareholders equity.

1.4

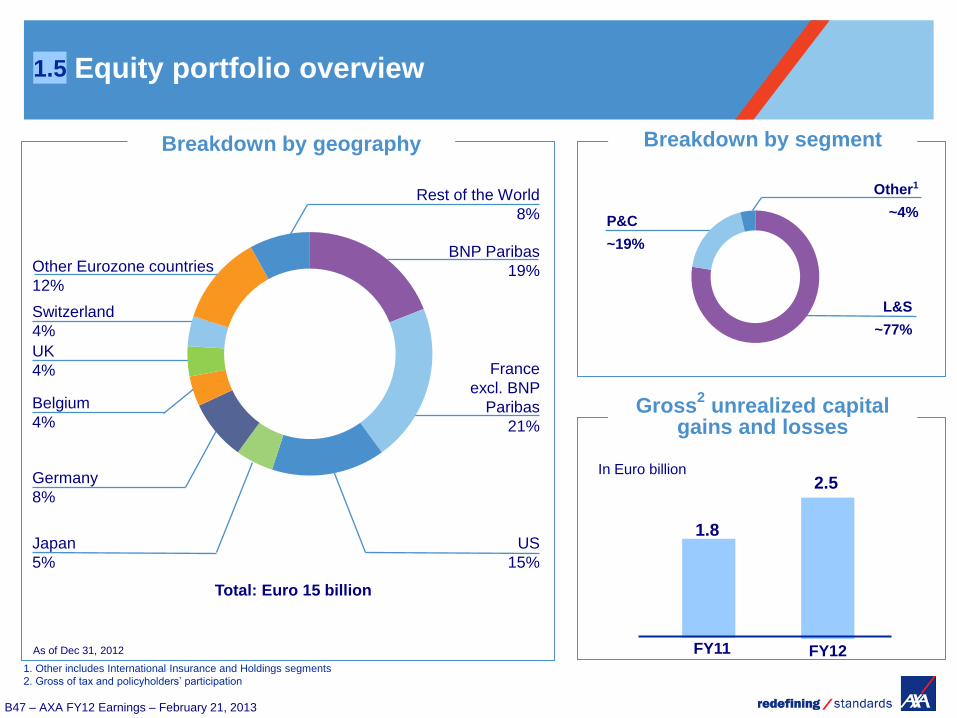

B47 – AXA FY12 Earnings – February 21, 2013

Belgium

4%

Germany

8%

Switzerland

4%

Japan

5%

UK

4%

P&C

~19%

L&S

~77%

Other1

~4%

France

excl. BNP

Paribas

21%

Breakdown by geography

Total: Euro 15 billion

US

15%

Rest of the World

8%

Breakdown by segment

Equity portfolio overview

Gross2 unrealized capital

gains and losses

1.8

FY12 FY11

In Euro billion

1. Other includes International Insurance and Holdings segments

2. Gross of tax and policyholders’ participation

BNP Paribas

19%

1.5

2.5

As of Dec 31, 2012

Other Eurozone countries

12%

B48 – AXA FY12 Earnings – February 21, 2013

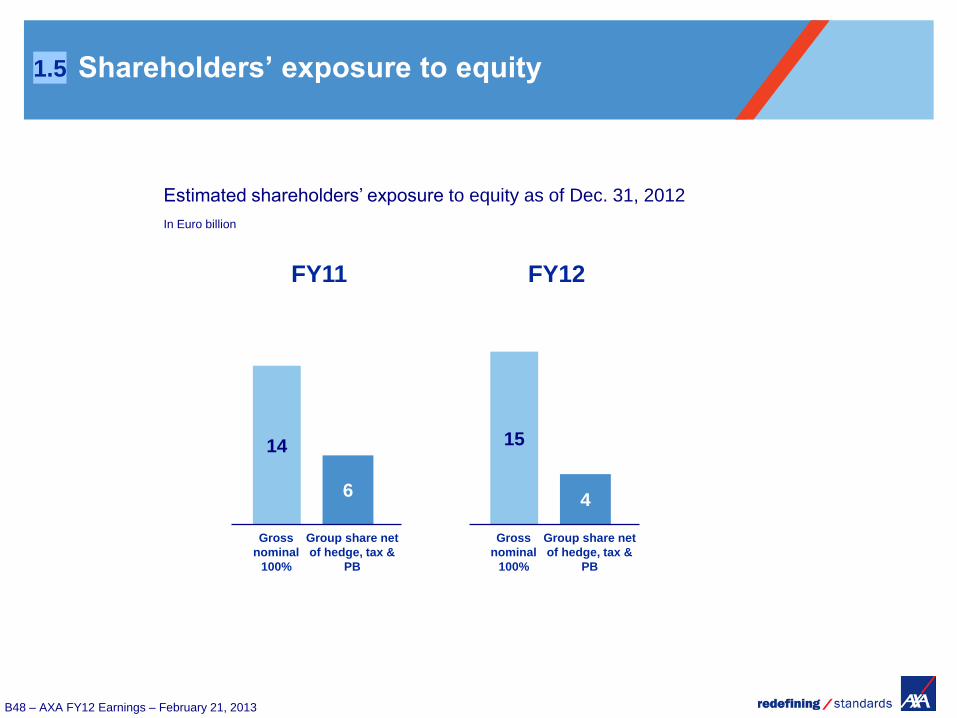

Estimated shareholders’ exposure to equity as of Dec. 31, 2012

In Euro billion

Shareholders’ exposure to equity

15

1.5

4

Gross

nominal

100%

Group share net

of hedge, tax &

PB

FY12

14

6

Gross

nominal

100%

Group share net

of hedge, tax &

PB

FY11

B49 – AXA FY12 Earnings – February 21, 2013

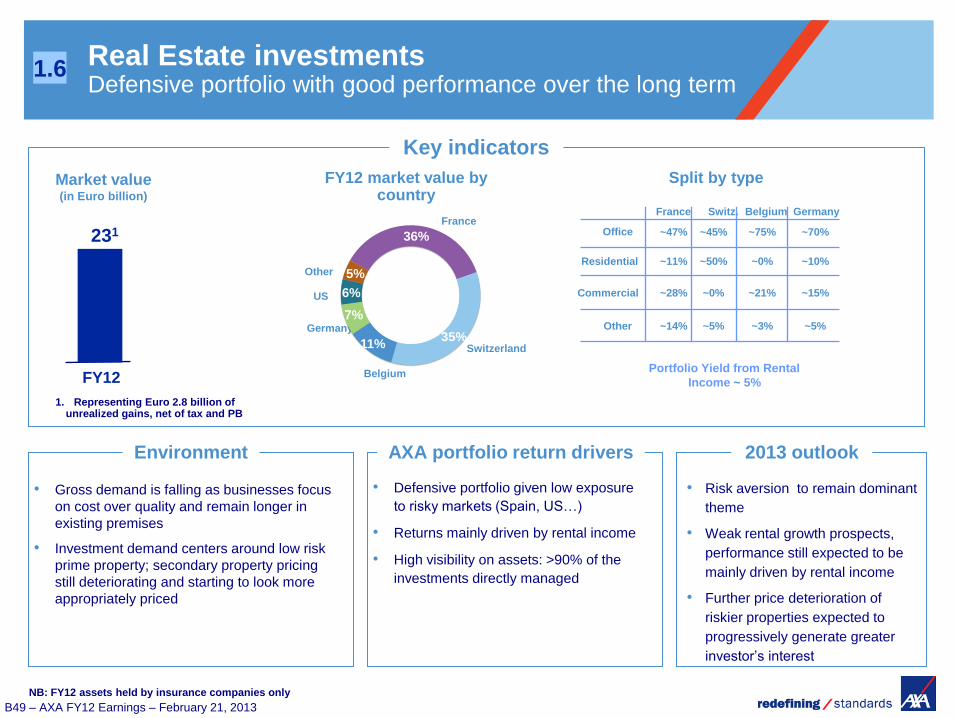

Real Estate investments Defensive portfolio with good performance over the long term

1.6

Key indicators

Market value (in Euro billion)

FY12

231

FY12 market value by country

2013 outlook

• Risk aversion to remain dominant

theme

• Weak rental growth prospects,

performance still expected to be

mainly driven by rental income

• Further price deterioration of

riskier properties expected to

progressively generate greater

investor’s interest

• Gross demand is falling as businesses focus

on cost over quality and remain longer in

existing premises

• Investment demand centers around low risk

prime property; secondary property pricing

still deteriorating and starting to look more

appropriately priced

Environment AXA portfolio return drivers

• Defensive portfolio given low exposure

to risky markets (Spain, US…)

• Returns mainly driven by rental income

• High visibility on assets: >90% of the

investments directly managed

Switzerland

France

US

Germany

Belgium

Other

Office

Residential

France Switz. Belgium Germany

~47%

~11%

~45%

~50%

~75%

~0%

~70%

~10%

1. Representing Euro 2.8 billion of unrealized gains, net of tax and PB

Split by type

Commercial

Other

~28%

~14%

~0%

~5%

~21%

~3%

~15%

~5%

Portfolio Yield from Rental

Income ~ 5%

NB: FY12 assets held by insurance companies only

36%

35%11%

7%

6%

5%

B50 – AXA FY12 Earnings – February 21, 2013

Hedge Fund investments Diversified portfolio of hedge funds

1.7

FY12

4

Exposure and concentration risk

• Mostly management of diversified funds of hedge funds

• Top 10 fund managers represent ~40% of portfolio market value

• Comprised of 10 strategic categories, with the largest strategy representing ~20% of

the portfolio

• Liquid portfolios

Market value (in Euro billion)

Key indicators

Industry Environment 2013 Outlook

Positive growth and new all-time high in AUM

Most new money directed to large well-established managers

New inflows mainly originating from US institutions, while EU and Asian inflows remain weak

Positive performance in 2012, after a challenging start in the first half

Diversified Funds strategy (~87% of book): focus on low volatility and uncorrelated returns

2012 performance in-line with benchmark1, but experienced lower volatility due to market neutral positioning

Well balanced 2012 strategy contribution driven by Fixed Income Arbitrage, quantitative equity market neutral and credit funds.

Tail Equity Diversifier strategy (~13% of book): focus on tail hedge strategy, sharp downturn protection

2012 Performance down ~14% , as product expected to decline when markets rallied in Q1 and second half of 2012

AXA portfolio performance

Improved macro environment given substantial monetary policy support, improving US housing market, less risk of EU zone break-up and stronger growth figures from China

Focus on quantitative equity market neutral & trading oriented credit funds to generate uncorrelated positive returns

2013 might become a more favourable environment for global macro funds due to the improved, more stable market environment

(1) Benchmark: HFRI FOF Conservative EUR Index – up approx. 3% in 2H12

B51 – AXA FY12 Earnings – February 21, 2013

8%

70%

14%

9%

55%34%

4%7%

Private Equity investments Diversified portfolio built over the long run

1.8

• Valuations slightly

increased in FY12

• Private equity saw

strong performance in

FY12, with US market

volumes back to pre-

crisis level

Breakdown by geography

Europe

US

Asia

Breakdown by expertise

Other

Buyout

Venture Mezzanine

Infrastructure

Market value (in Euro billion)

Environment

FY12

• Gold award for “Best French Mid and

Upper Mid-Market LBO Fund”– Private

Equity Exchange Awards

• “Best French LBO team” – Magazine

des Affaires

• “Deal of the year – Transport”

Infrastructure Journal, PFI Awards

• “French LBO Mid-Cap Team of the

Year” – Capital Finance Awards

• “French Lender of the Year, 1st in 200-

500m Euro Enterprise Value, 1st in

Mezzanine Debt Category” – Private

Equity Magazine

8

2012 Awards

• Diversified portfolio: counter-cyclical fields of

expertise (Infrastructure and Mezzanine) and exposure to quality buy-outs

• 46% Direct: high quality portfolio • 54% Funds of Funds: very active monitoring

• In FY12, valuations and distributions increased across all expertise

• Direct portfolio (no default / repayment issues) • Funds of Funds portfolio (underlying companies

continue deleveraging) • Exit of portfolio investments realized at high

multiples

• Active private equity activity

(both investments and

disposals) in both Direct and

Funds of Funds

• AXA Private Equity still a

buyer with no pressure to

sell assets.

• Targets: anti-cyclical

companies, resilient to crisis,

portfolio of funds

Key indicators

NB: Assets held by insurance companies only

Outlook AXA portfolio return drivers

B52 – AXA FY12 Earnings – February 21, 2013

27%

22%

37%

7%7%

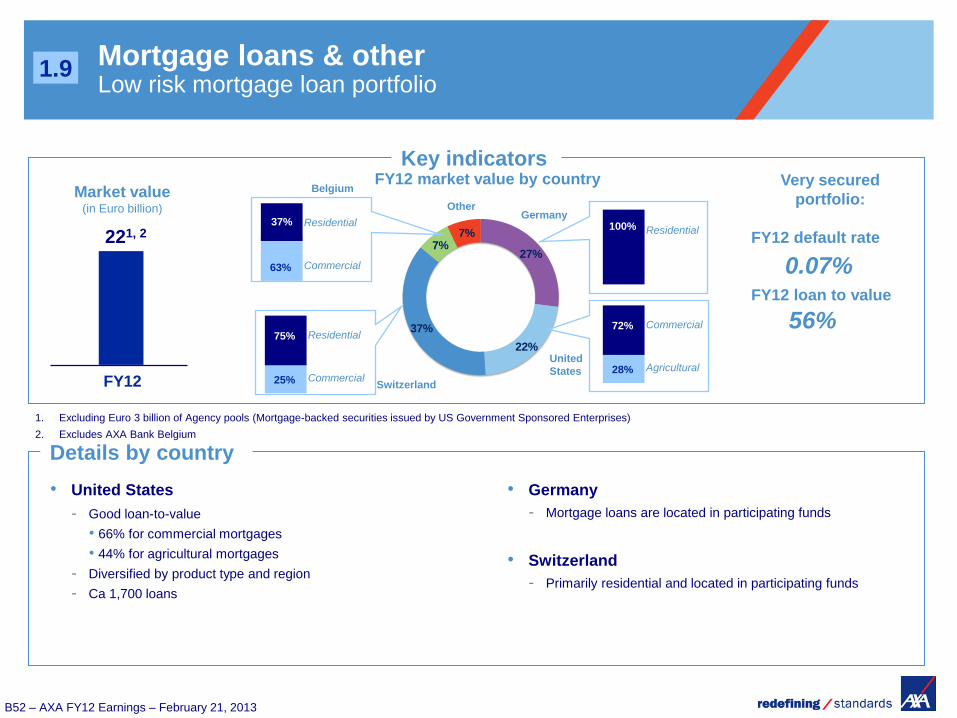

Mortgage loans & other Low risk mortgage loan portfolio

Key indicators

Details by country

• United States

- Good loan-to-value

• 66% for commercial mortgages

• 44% for agricultural mortgages

- Diversified by product type and region

- Ca 1,700 loans

FY12

221, 2

Very secured

portfolio:

FY12 default rate

FY12 loan to value

Agricultural

Commercial 72%

28%

Residential 100%

United

States

Switzerland

Germany Other

• Germany

- Mortgage loans are located in participating funds

• Switzerland

- Primarily residential and located in participating funds

0.07%

56%

Market value (in Euro billion)

FY12 market value by country

1. Excluding Euro 3 billion of Agency pools (Mortgage-backed securities issued by US Government Sponsored Enterprises)

2. Excludes AXA Bank Belgium

1.9

Commercial

Residential 75%

25%

Belgium

Commercial

Residential 37%

63%

B53 – AXA FY12 Earnings – February 21, 2013

1.2 6.8

1.5

0.9

5.2

3.1

FY11*

2.8

FY12

11.2

Focus on net unrealized capital gains

Balance sheet net unrealized

capital gains1

Off balance sheet net

unrealized capital gains In Euro billion In Euro billion

2.0

France Germany Belgium Switzerland Japan US Eurozone

peripheral

countries

0.0

0.7

1.7

0.2

1.0 0.6

Other

(mainly

Netherlands and

Austria)

0.5

Net unrealized capital gains on Government bonds by issuer

Corporate bonds

Equities

Government bonds

3.2

FY11* FY12

3.5

Real Estate and loans2

* Restated for the change in accounting methodology on deferred acquisition costs (DAC) adopted retrospectively as at January 1, 2012

1. Excluding Forex, minority interests and other

2. Excluding net unrealized gains on bank loans. Total off-balance sheet net unrealized gains, including net unrealized gains on bank loans, amounted to €4.6bn in FY12 vs. €4.3bn

in FY11

B54 – AXA FY12 Earnings – February 21, 2013

Focus on exposure to Eurozone peripheral countries government bonds

Exposure by issuer

De-risking actions in 1H12 benefited from tightening of sovereign spreads

Reinvestment in Italy and Ireland in 2H12 in short to mid-term maturities

AFS OCI

in Euro billion

Gross book value

Dec. 31, 2011

Gross book value

June 30, 2012

Gross book value

December 31, 2012

Gross market value

December 31, 2012

Italy 16.1 14.7 16.4 16.7

Spain 8.5 7.7 7.6 7.3

Ireland 1.1 1.0 2.7 2.8

Portugal 2.0 0.9 0.9 0.7

Greece 0.3 0 0 0

TOTAL 28.1 24.4 27.6 27.5

Or Euro 13.0 billion

with AXA MPS JV at

Group share

B55 – AXA FY12 Earnings – February 21, 2013

3.0% 4.3%

Asset & Liability Management Life & Savings investment spreads for main entities

Belgium

AXA MPS

L&S average

guaranteed rate

Reinvestment yield on

L&S fixed income assets

• G/A reserves: Euro 26 billion

• Significant reduction in guaranteed rate

during 2H12, after 1H12 exceptional

sales campaign

• G/A reserves: Euro 13 billion

• G/A deemphasized, focus on Unit-

Linked and Protection businesses

Yield on total L&S

asset base

0.9%

4.3%

0.0%

3.2%

3.4% 4.1%

1.7%

3.0%

FY12

1.6%1 2.4%

FY12

FY12

2.1% 3.4%

1.4%

3.5%

FY12

210bps

Germany

• G/A reserves: Euro 55 billion

• Asset portfolio well diversified with long

investment horizon (8 to 9 years) and

with limited reinvestments in Bunds

FY12 FY12

130bps 70bps

FY12

France

• G/A reserves: Euro 95 billion

• G/A Savings new business sales with

long term guarantees stopped in 1998

FY12

320bps 340bps

New business Inforce

Switzerland (Group Life)

• G/A reserves: Euro 36 billion

• Protection components making products

very profitable

FY12

FY12

70bps 40bps

2.2% 2.6%

1.5% 2.2%

130bps

80bps 130bps

1. Reflects current guaranteed rate in 2013

B56 – AXA FY12 Earnings – February 21, 2013

Solvency I

Solvency I ratio at 233%

In Euro billion

Solvency I

Sensitivities

Ratio as of December 31, 2012 233%

Interest rate +100bps 176%

Interest rate -100bps 292%

Equity markets -25% 226%

Equity markets +25% 245%

Corporate spreads +75 bps 221%

On fixed income assets, the combination of sensitivity impacts from interest

rates increase and widening corporate spreads is capped at -79 pts of solvency

2

FY12

233%

FX & other URGL Underlying

Earnings

FY11

188%

127%

171%

FY08

182%

FY10 FY09

+18 pts

+40 pts

-13 pts

Of which +32 pts on fixed income assets

2132

Requirement

Surplus

44

FY11

24

FY12

24

56

B57 – AXA FY12 Earnings – February 21, 2013

Solvency I reconciliation to shareholders’ equity

- 26

+ 2

56

Available financial resources(1)

In Euro billion

56

+ 4

- 2

+ 10

(1): AXA is not a financial conglomerate but its solvency margin is nevertheless reduced by the amount of its equity interests in credit institutions, investment companies or financial

institutions if the Group holds more than 20% in the mentioned entities. These stakes are deducted in “Other” for a total €-4.0 billion

(2): All subordinated debt (including undated already booked in shareholders’ equity) is admitted up to 50% of requirements

(3): And loans

(4): Notably includes gross up of tax and policyholder participation of net unrealized gains on investments minus net consolidated book value in financial services (see (1)) and Zillmer

adjustment)

+ 8

+ 4

2

Available capital

SH equity 100%

Intangibles

Admitted sub debt (2)

Locally admitted assets

Real estate(3)

Dividend to be paid

Other(4)

Pension benefit

B58 – AXA FY12 Earnings – February 21, 2013

FY12 operating return

FY11 dividend payment

Market impact net of liquidity

premium**

Model changes

Increase in capital requirements from

business evolution, forex & other

FY11

206%

Economic solvency ratio*

FY12

183%

Economic solvency rollforward

+26 pts

-7 pts

-2 pts

+10 pts

-4 pts

Refinement in the economic parameters

modeling, notably improvement in yield

curve modeling in line with Solvency 2

framework

+6 pts

+6 pts

of which

*with US equivalence

** as defined in QIS5

Improvement of inflation risk modeling

Improvement in credit modeling

-2 pts

2

B59 – AXA FY12 Earnings – February 21, 2013

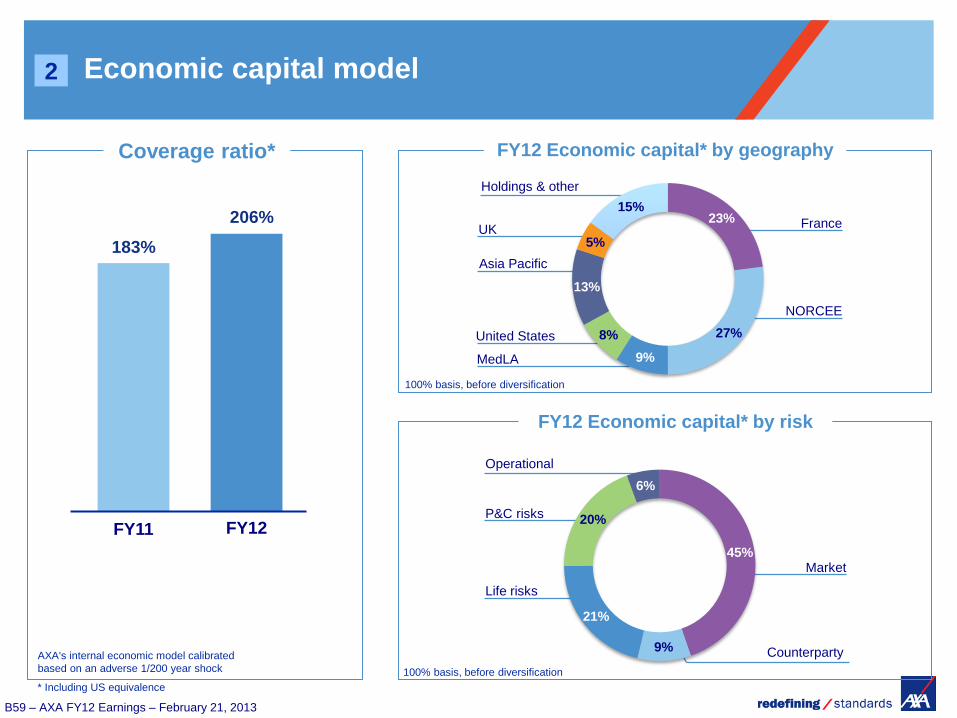

Economic capital model

Coverage ratio*

183%

FY11

206%

FY12

United States

UK France

NORCEE

MedLA

FY12 Economic capital* by geography

Holdings & other

FY12 Economic capital* by risk

100% basis, before diversification

Asia Pacific

2

100% basis, before diversification

AXA's internal economic model calibrated

based on an adverse 1/200 year shock

P&C risks

Market

Counterparty

Operational

Life risks

43%

29%

6%

23%

27%

9%

8%

13%

5%

15%

45%

9%

21%

20%

6%

* Including US equivalence

B60 – AXA FY12 Earnings – February 21, 2013

Net financial debt Long-term maturities

TSS = undated deeply subordinated notes

TSDI = undated subordinated notes

Senior debt

Subordinated debt

In Euro billion

3

In Euro billion

Economic maturity breakdown

Total net debt In Euro billion

Contractual maturity breakdown

Undated subordinated debt

Senior debt

Subordinated debt*

Cash

1.0 0.8 1.0 0.2 0.3

2.1

0.2 3.2

0.9 0.4

0.2 1.3

4.4

1.0 0.8

2012 2013 2014 2015 2016-2020 2021-2025 2026-2040 Undated

1.0 0.8 1.0 0.2 0.3

2.1 0.2 1.9

2.2

0.4

1.6

6.2

2012 2013 2014 2015 2016-2020 2021-2025 2026-2040 Undated

• Undrawn credit lines Euro 12 billion

• Cash & cash equivalent Euro 30 billion

* Including Euro -0.1 billion of reversal of mark-to-market on interest rates derivatives vs. Euro -0.3 billion in FY11

FY12

13.0

5.1

3.3

6.9

7.8

FY11

13.4

4.5

3.3

6.8

7.8

B61 – AXA FY12 Earnings – February 21, 2013

Table of content

Property & Casualty

Group

Life & Savings

Asset Management

Balance sheet

Business overview

Embedded Value and Cash Flows

B62 – AXA FY12 Earnings – February 21, 2013

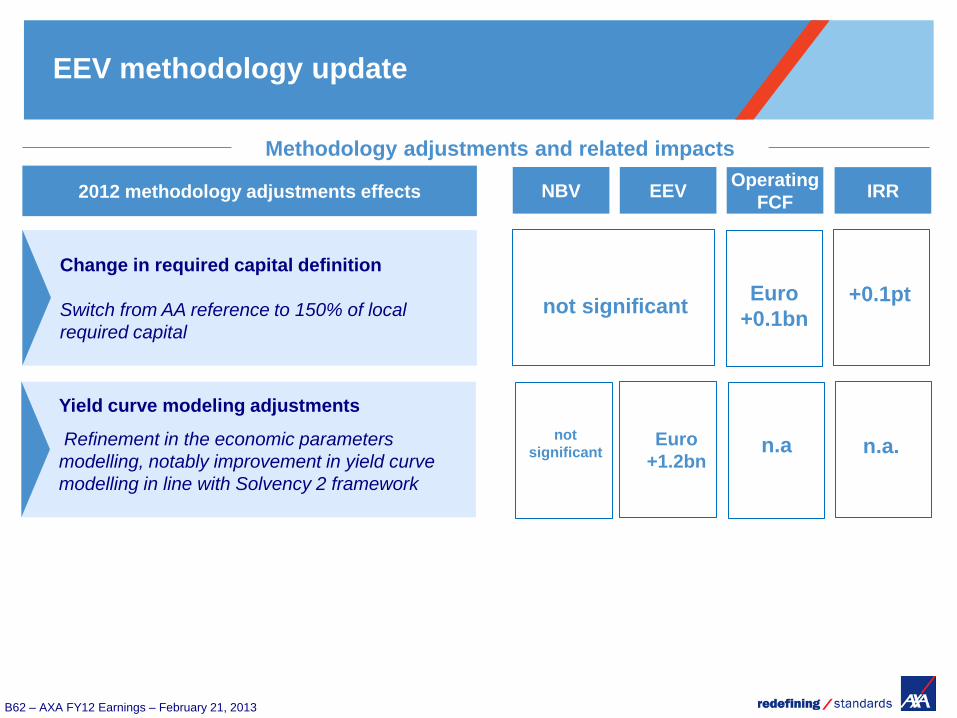

Change in required capital definition

Switch from AA reference to 150% of local

required capital

Yield curve modeling adjustments

Refinement in the economic parameters

modelling, notably improvement in yield curve

modelling in line with Solvency 2 framework

NBV

Methodology adjustments and related impacts

EEV 2012 methodology adjustments effects

EEV methodology update

Operating

FCF IRR

Euro

+1.2bn

Euro

+0.1bn +0.1pt

n.a n.a.

not significant

not

significant

B63 – AXA FY12 Earnings – February 21, 2013

L&S

EV = VIF + ANAV

Required

capital

(included in ANAV)

Opening (FY11) 38.2 17.1 21.1 16.0

Modeling adj., FX

& scope 0.2 1.7 (1.5) (0.6)

Existing business

contribution 3.7 (0.1) 3.8 (0.5)

New business

value 1.9 3.2 (1.3) 0.9

Operational

variances* (0.9) (0.2) (0.7) (0.1)

Economic

variances 1.6 0.9 0.7 0.0

Capital flows and

other (0.5) (0.0) (0.4) (0.0)

Closing (FY12) 44.2 22.6 21.6 15.6

In Euro billion

Life & Savings Embedded Value

2.2

FY12

1.8

FY11**

Life & Savings operating Free Cash Flows

2012 Life & Savings Free Cash Flow

breakdown

-1.3

In-force

capital

release

+0.5

Expected

exiting

business

contribution

3.8

2012 L&S

operating

Free Cash

Flow

2.2

New

business

required

capital

-0.9

New business

strain

*Operational variances include actuarial and tax assumptions, expense and modeling of

participating and adjustable credited rates business

** Not restated for the change in required capital methodology

B64 – AXA FY12 Earnings – February 21, 2013

L&S Embedded Value key sensitivities

Key sensitivities

Impact on L&S

NBV

Impact on L&S

EEV

Euro

million %

Euro

million %

Sensitivity to equity markets

10% increase

+75

+4%

+1,211

+3%

10% decrease -89 -5% -1,271 -3%

Sensitivity to interest rates

Upward 100bps parallel shift

+88

+5%

+2,360

+5%

Downward 100bps parallel shift -237 -12% -5,107 -12%

Sensitivity to volatility

25% increase in volatility on equity markets

-42

-2%

-614

-1%

25% increase in volatility on bonds -99 -5% -981 -2%

B65 – AXA FY12 Earnings – February 21, 2013

L&S – IRR and new business investments

US

Euro million

France

APE

UK

NB IRR1

Japan

New business investments2

MedLA

NORCEE

Total

o/w Germany

o/w Switzerland

o/w Belgium

FY11

APE NB IRR1 New business investments2

FY12

1. New Business Internal Rate of Return

2. New business strain + New business required capital

3. Hong Kong, South-East Asia, India & China

Asia excl. Japan3

1,378 8.9% (595)

1,244 13.2% (288)

535 4.3% (196)

598 11.8% (330)

1,139 10.4% (406)

454 9.5% (130)

374 13.3% (97)

175 8.9% (87)

402 14.4% (118)

871 32.1% (245)

6,170 12.5% (2,177)

1,340 8.7% (592)

1,018 10.7% (291)

535 7.7% (146)

463 11.7% (242)

1,289 8.8% (559)

506 8.3% (236)

397 9.4% (94)

173 7.9% (87)

432 10.6% (182)

656 34.7% (170)

5,733 11.5% (2,182)

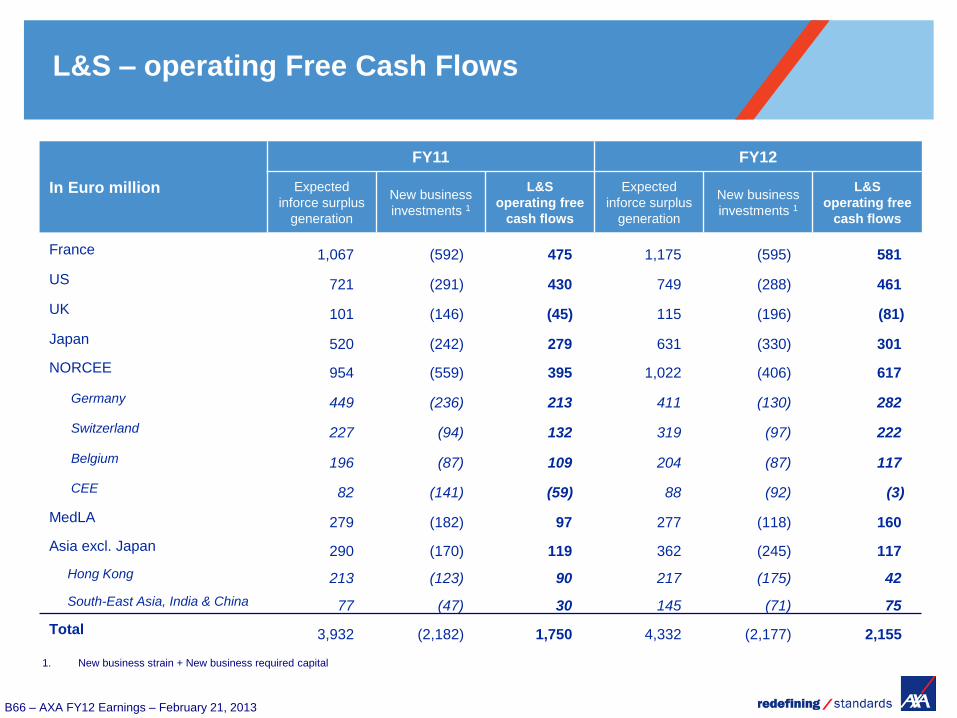

B66 – AXA FY12 Earnings – February 21, 2013

L&S – operating Free Cash Flows

In Euro million

FY11 FY12

Expected

inforce surplus

generation

New business

investments 1

L&S

operating free

cash flows

Expected

inforce surplus

generation

New business

investments 1

L&S

operating free

cash flows

France 1,067 (592) 475 1,175 (595) 581

US 721 (291) 430 749 (288) 461

UK 101 (146) (45) 115 (196) (81)

Japan 520 (242) 279 631 (330) 301

NORCEE 954 (559) 395 1,022 (406) 617

Germany 449 (236) 213 411 (130) 282

Switzerland 227 (94) 132 319 (97) 222

Belgium 196 (87) 109 204 (87) 117

CEE 82 (141) (59) 88 (92) (3)

MedLA 279 (182) 97 277 (118) 160

Asia excl. Japan 290 (170) 119 362 (245) 117

Hong Kong 213 (123) 90 217 (175) 42

South-East Asia, India & China 77 (47) 30 145 (71) 75

Total 3,932 (2,182) 1,750 4,332 (2,177) 2,155

1. New business strain + New business required capital

B67 – AXA FY12 Earnings – February 21, 2013

Life & Savings Free Cash Flows emergence from inforce and new business

Expected undiscounted cash

flows from 2012 inforce

Expected undiscounted cash

flows from 2012 New Business

Euro billion Euro billion

Euro 20 billion undiscounted free cash flows expected to be released from 2012 inforce over 5 years

On top of this, expected free cash flow generation from inforce should be boosted by:

• Actions to improve value of the existing book

• Actions to release more capital from the existing book

Years Years

New business

investments

20

15

10

5

0

31-35 26-30 21-25 16-20 11-15 6-10 1-5

2,0

1,5

1,0

0,5

0,0

-0,5

-1,0

-1,5

-2,0

-2,5 -2.2

2012 1-5 6-10 11-15 16-20 21-25 26-30 31-35