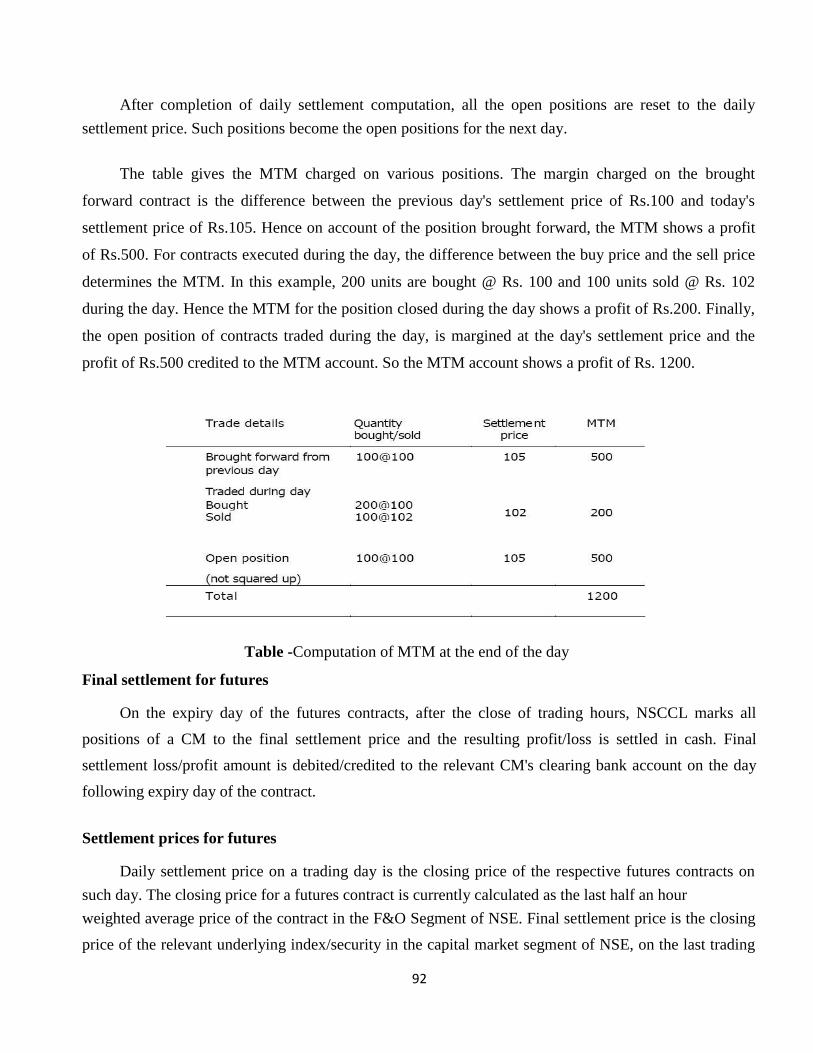

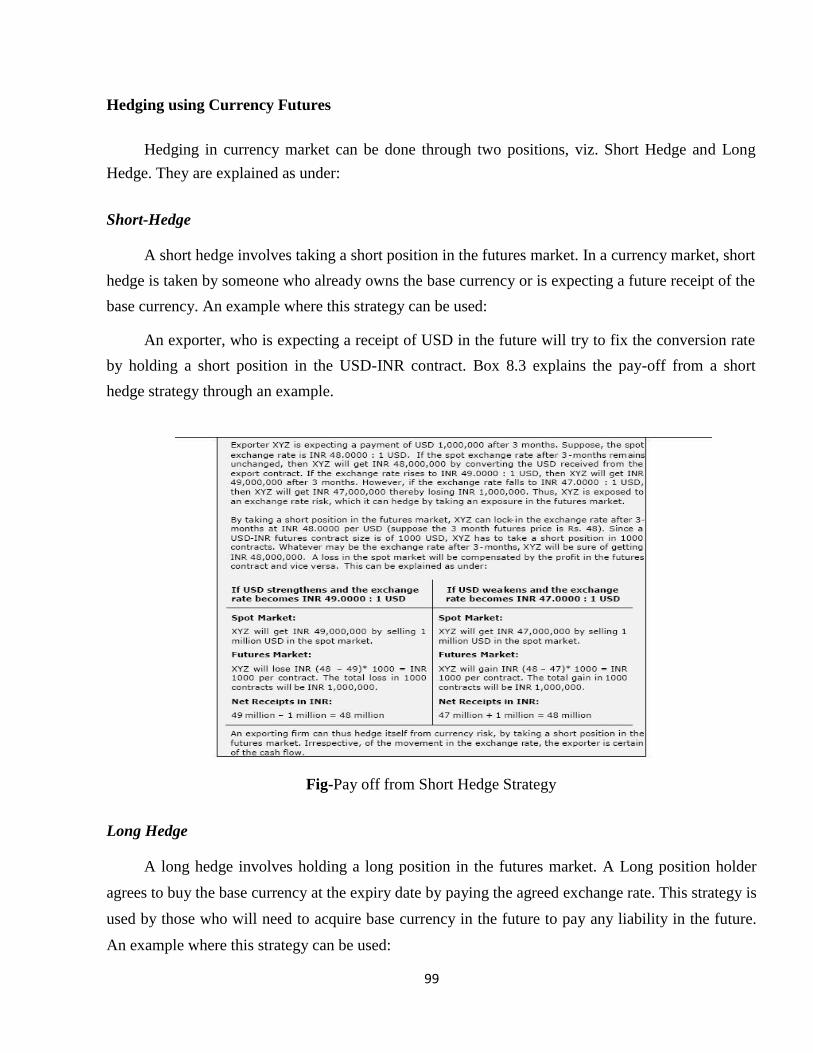

full record

TRANSCRIPT

1

MBABT 516: STOCK AND FOREX TRADING LAB

RECORD

Lab report submitted in partial fulfillment of the requirements for the degree of

MBA: BANKING TECHNOLOGY

Submitted

By

PRAKASH RAJIV. S

Reg No. : 14381044

DEPARTMENT OF BANKING TECHNOLOGY

SCHOOL OF MANAGEMENT

PONDICHERRY UNIVERSITY

PONDICHERRY – 605 014

JANUARY 2016

2

DEPARTMENT OF BANKING TECHNOLOGY

SCHOOL OF MANAGEMENT

PONDICHERRY UNIVERSITY

PONDICHERRY – 605 014

NAME : PRAKASH RAJIV S

REG. NO : 14381044

SUBJECT : Stock and Forex Trading lab

CODE : MBABT-516

Lab in charge Head of the Department

Submitted for the Practical Examination held on………………….

INTERNAL EXAMINER EXTERNAL EXAMINER

ACKNOWLEDGEMENT

3

It gives me an immense pleasure to express my profound gratitude to my beloved guide Dr. S.

Sudalai Muthu,, Associate Professor, Department of Banking Technology, School of Management for his

consistent guidance and constant encouragement in this Lab work. His advice and systematic approach has

given a new dimension to this Lab work.

I express my special thanks to Dr. V. PRASANNA VENKATESAN, Professor and Head of the

Department of Banking Technology, School of Management, Pondicherry University, for his continuous

support, advice and encouragement.

I also express my sincere thanks to Mr. S.GOWTHAM RAJ, Authorized Person, Sharekhan Ltd for

giving us an opportunity to do stock and forex trading practices in their branch.

I am very grateful to my parents and the Almighty. Also I would like to express my heartfelt

gratitude to other Faculty and Friends for their help in making this record work successful.

PRAKASH RAJIV S

TABLE OF CONTENTS

1. OPENING OF PAN AND DP ACCOUNT ............................................................................ 1

2. EVALUATION OF NEW ISSUE APPLICATION FORMS IPO EVALUATION ....................... .9

4

3. IPO RISK FACTORS ........................................................................................................ 12

4. SCREEN BASED TRADING ............................................................................................. 13

5. STUDY OF VARIOUS ORDER TYPES AND ORDER BOOKING ......................................... 18

6. TRADING AND SETTLEMENT ACTIVITIES ..................................................................... 24

7. PREPARATION OF TECHNICAL CHARTS ........................................................................ 27

8. FUNDAMENTAL ANALYSIS OF A COMPANY ................................................................ 38

9. COMPANY SPECIFIC EVENTS AND IDENTIFICATION OF STOCK PRICE REACTION ....... 47

10. STUDY ON INDICES ................................................................................................... 51

11. MARKETING OF MUTUAL FUNDS ............................................................................ 55

12. FUTURES AND OPTIONS ........................................................................................... 64

13. A STUDY ON CLEARING AND SETTLEMENT ACTIVITIES IN FUTURES AND OPTIONS…….. 73

14. STUDY ON CURRENCY DERIVATIVES…………………………………………………...79

15. FOREX TRADING –BASICS……………………………………………………………..89

16. PROBLEMS ON FOREGIN EXCHANGE ARITHMETIC ................................................ .94

17. STUDY ON COMMODITY MARKETS ........................................................................ 103

SHAREKHAN LIMITED

INTRODUCTION

Sharekhan is one of the leading retail broking House of SSKI Group which was running successfully since

1922 in the country. It is the retail broking arm of the Mumbai-based SSKI Group, which has over eight

decades of experience in the stock broking business. Sharekhan offers its customers a wide range of equity

related services including trade execution on BSE, NSE, Derivatives, depository services, online trading,

5

investment advisory, Mutual Fund Advisory etc.

The firm’s online trading and investment site - www.sharekhan.com - was launched on Feb 8, 2000.

The site gives access to superior content and transaction facility to retail customers across the country.

Known for its jargon-free, investor friendly language and high quality research, the site has a registered base

of over two lakh customers. The number of trading members currently stands More than 8 Lacs. While

online trading currently accounts for just over 8 per cent of the daily trading in stocks in India, Sharekhan

alone accounts for 32 per cent of the volumes traded online.

The content-rich and research oriented portal has stood out among its contemporaries because of its

steadfast dedication to offering customers best-of-breed technology and superior market information. The

objective has been to let customers make informed decisions and to simplify the process of investing in

stocks.

On April 17, 2002 Sharekhan launched Speed Trade, a net-based executable application that

emulates the broker terminals along with host of other information relevant to the Day Traders. This was for

the first time that a net-based trading station of this caliber was offered to the traders. In the last six months

Speed Trade has become a de facto standard for the Day Trading community over the net.

On October 01, 2007 Sharekhan again launched his another integrated Software based product Trade

Tiger, a net-based executable application that emulates the broker terminals along with host of other

information relevant to the Day Traders. It has another quality which differs it from other that it has the

combined terminal for EQUITY and COMMODITIES both.

Share khan’s ground network includes over 1005 centers in 410 cities in India, of which 210 are

fully-owned branches. Sharekhan has always believed in investing in technology to build its business. The

company has used some of the best-known names in the IT industry, like Sun Microsystems, Oracle,

Microsoft, Cambridge Technologies, Nexgenix, Vignette, Verisign Financial Technologies India Ltd, Spider

Software Pvt Ltd. to build its trading engine and content. Previously the Morakiya family holds a majority

stake in the company but now a world famous brand CITI GROUP has taken a majority stake in the

6

company. HSBC, Intel & Carlyle are the other investors.

With a legacy of more than 80 years in the stock markets, the SSKI group ventured into institutional

broking and corporate finance 18 years ago. Presently SSKI is one of the leading players in institutional

broking and corporate finance activities. SSKI holds a sizeable portion of the market in each of these

segments. SSKI’s institutional broking arm accounts for 7% of the market for Foreign Institutional portfolio

investment and 5% of all Domestic Institutional portfolio investment in the country. It has 60 institutional

clients spread over India, Far East, UK and US. Foreign Institutional Investors generate about 65% of the

organization’s revenue, with a daily turnover of over US$ 4 million. The Corporate Finance section has a

list of very prestigious clients and has many ‘firsts’ to its credit, in terms of the size of deal, sector tapped

etc. The group has placed over US$ 1 billion in private equity deals. Some of the clients include BPL

Cellular Holding, Gujarat Pipavav, Essar, Hutchison, Planetasia, and Shopper’s Stop.

Sharekhan business

1. Brokering business.

2. White feathering house production.

Vision

To be the best retail broking brand in the retail business of the stock market.

Mission

To educate and empower the individual investor to make better investment decisions through quality

advices and superior services.

Stock exchange Mumbai

Share khan is the retail broking arm of SSKI, an organization with more then eight decade of trust

and credibility in the stock market.

Amongst pioneers of investment research in the Indian market.

In 1984 venture into institutional broking and the corporate finance.

7

Leading domestic player in the Indian institutional business.

Over US$5 billion of private equity deal.

SSKI group companies

SSKI investor services ltd (Sharekhan)

S.S. Kantilal Isharlal securities

SSKI corporate finance.

SHAREKHAN PROFILE

SHAREKHAN RETAIL BROKING

Among the top three (3) branded retail services providers (Rs 856 crs average daily volume.

NO. 2 player in online business

Large network of branded broking outlets in the country servicing around 5, 45, 000 Clients

BENEFITS

Free Depository A/c

Secure Order by Voice Tool Dial-n-Trade.

Automated Portfolio to keep track of the value of your actual purchases.

24x7 Voice Tool access to your trading account.

Personalized Price and Account Alerts delivered instantly to your Cell Phone & E-mail address.

Special Personal Inbox for order and trade confirmations.

On-line Customer Service via Web Chat.

Anytime Ordering.

NSDL Account

Instant Cash Tranferation.

Multiple Bank Option.

8

Enjoy Automated Portfolio.

Buy or sell even single share.

PRODUCTS OF SHAREKHAN

CLASSIC ACCOUNT

This account allows the client to trade through the website www.sharekhan.com and is suitable for the retail

investor who is risk-averse and hence prefers to invest in stocks or who do not trade too frequently.

It allows investor to buy and sell stocks online along with the following features like multiple watch lists,

Integrated Banking, De-mat and Digital contracts, Real-time portfolio tracking with price alerts and Instant

money transfer.

FEATURES

Online trading account for investing in Equity and Derivatives via www.sharekhan.com

Live Terminal and Single terminal for NSE Cash, NSE F&O, BSE & Mutual Funds (online and offline).

Integration of On-line trading, Saving Bank and De-mat Accounts.

Instant cash transfer facility against purchase & sale of shares.

Competative transaction charges.

Instant order and trade confirmation by E-mail.

Streaming Quotes (Cash & Derivatives).

Personlized market watch.

Single screen interface for Cash and derivatives and more.

Provision to enter price trigger and view the same online in market watch.

TRADE TIGER

TRADE TIGER is an internet-based software application which is the combination of EQUITY &

COMMODITIES, that enables you to buy and sell share and well as commodities item instantly. It is ideal

9

for every client of SHAREKHAN LTD.

FEATURES

Integration of EQUITY & COMMODITIES MARKET.

Instant order Execution and Confirmation.

Single screen trading terminal for NSE Cash, NSE F&O & BSE & Commodities.

Technical Studies.

Multiple Charting.

Real-time streaming quotes, tic-by-tic charts.

Market summary (Cost traded scrip, highest value etc.)

Hot keys similar to broker’s terminal.

Alerts and reminders.

Back-up facility to place trades on Direct Phone lines.

Live market debts.

DIAL-N-TRADE

Along with enabling access for your trade online, the CLASSIC and TRADE TIGER ACCOUNT

also gives you our Dial-n-trade services. With this service, all you have to do is dial our dedicated phone

lines which are 1800-22-7500, 3970-7500.

PORTFOLIO MANAGEMENT SERVICES

Sharekhan is also having Portfolio Management Services for Exclusive clients.

1. PROPRIME - Research & Fundamental Analysis.

Ideal for investors looking at steady and superior returns with low to medium risk appetite. This portfolio

10

consists of a blend of quality blue-chip and growth stocks ensuring a balanced portfolio with relatively

medium risk profile. The portfolio will mostly have large capitalization stocks based on sectors & themes

that have medium to long term growth potential.

2. PROTECH - Technical Analysis.

Protech uses the knowledge of technical analysis and the power of derivatives market to identify trading

opportunities in the market. The Protech lines of products are designed around various risk/reward/ volatility

profiles for different kinds of investment needs.

THRIFTY NIFTY: Nifty futures are bought and sold on the basis of an automated trading system

that generates calls to go long/short. The exposure never exceeds value of portfolio i.e. there is no

leveraging; but being short in Nifty allows you to earn even in falling markets and there by generates

linear

BETA PORTFOLIO: Positional trading opportunities are identified in the futures segment based

on technical analysis. Inflection points in the momentum cycles are identified to go long/short on

stock/index futures with 1-2 month time horizon. The idea is to generate the best possible returns in

the medium term irrespective of the direction of the market without really leveraging beyond the

portfolio value. Risk protection is done based on stop losses on daily closing prices.

STAR NIFTY: Trailing Stops Momentum trading techniques are used to spot short term momentum

of 5-10 days in stocks and stocks/index futures. Trailing stop loss method of risk management or

profit protection is used to lower the portfolio volatility and maximize returns. Trading opportunities

are explored both on the long and the short side as the market demands to get the best of both

upwards & downward trends.

3. PROARBITRAGE - Exploit price analysis

- ONLINE IPO'S AND MUTUAL FUNDS ADVISORY IS AVAILABLE.

PROCESS OF ACCOUNT OPPENING

11

LEAD MANAGEMENT SYSTEM (LMS) / REFERENCES

CONTACT

TELEPHONE AND PRESONAL VISIT

APPOINTMENT

DEMONSTRATION

AGREE DISAGREE (CLOSE)

DOCUMANTATION

FILLING THE FORM

SUBMISSION THE FORM

LOGIN OF THE FORM

SENDING THE ACCOUNT OPENING KIT TO THE CUSTOMER FOR TRADING

CHARGE STRUCTURE

1)- PRE PAID OR AMC A/C: -

Advance Amount which will be fully adjsted against your brokerage you paid in One year.

Following Schemes Are Available: - Brokerage will be chagred -

1) - 750/- Scheme:- 0.05 / 0.50 %

2) - 1000/- Scheme 0.045 / 0.45 %

3) – 2,000/- Scheme: - 0.035 / 0.40 %

4) – 6,000/- Scheme: - 0.025 / 0.25 %

5) – 18,000/- Scheme: - 0.020 / 0.20 %

6) – 30,000/- Scheme: - 0.015 / 0.18 %

12

7) – 60,000/- Scheme: - 0.010 / 0.15 %

8) – 1,00,000/- Scheme: - 0.0075 / 0.10 %

Minimum Margine of Rs. 25000/- is Required for Account Opening.

Annual Maintanance Charges will NIL for 1st year and Rs. 400/- from 2nd year.

- EXPOSURE : 4 TIMES (ON MARGINE MONEY)

- EXPOSURE : 10 TIMES (ON MAX TRADING)

- ONLINE IPO'S AND MUTUAL FUNDS ADVISORY IS AVAILABLE.

We are having tie-up with Eleven banks for online fund transfering i.e. HDFC, ICICI, IDBI, CITI,

Union Bank of India, Oriental Bank of Commerce, INDUSIND, AXIS, Centurian Bank of Punjab,

Bank of India and Yes Bank. Company Provide 4-6 E-mail to there customers per day.

Online Trade in Share

Sharekhan customers can online trade through there computers, through internet during the market timings.

Online Fund Transfer

We have tie up with Eleven Banks for online fund transferring i.e. HDFC, IDBI, CITI, UBI, OBC,

INDSLANDAND and UTI BANK, Yes bank, Bank of India for Online Money Transfer.

Research based investment advice

Investment and trading services

Trading and seminars

Technology based investment tools

Integrated demat facility

CUSTOMER CAN TRADE IN

o Equities

o Derivatives

o Commodities

13

SWOT ANALYSIS OF SHAREKHAN

(My observation)

STRENGTHS

1. Big client base

2. In-house research house

3. online as well as offline trading

4. Online IPO/ MF services

5. Share shops

6. Transparent

7. User friendly tie ups with 10 banks

8. Excellent order execution speed and reliability

WEAKNESS

1. Lack of awareness among customer

2. Less focus on customer retention

3. Less Exposure

OPPORTUNITIES

1. Diversification

2. Product modification

3. Improve Web based trading

4. Provide competitive brokerage

5. Concentrate on PMS

6. Focus on Institutional investors

7. Concentrate on HNI’s (high net worth investor)

THREATS

1. Aggressive promotional strategies by close competitor like Religare, Angel Broking and India bulls.

2. More and more players are venturing into this domain, which can further reduce the earning of Share

14

Khan.

3. Stock market is very volatile, risk involves is very high.

15

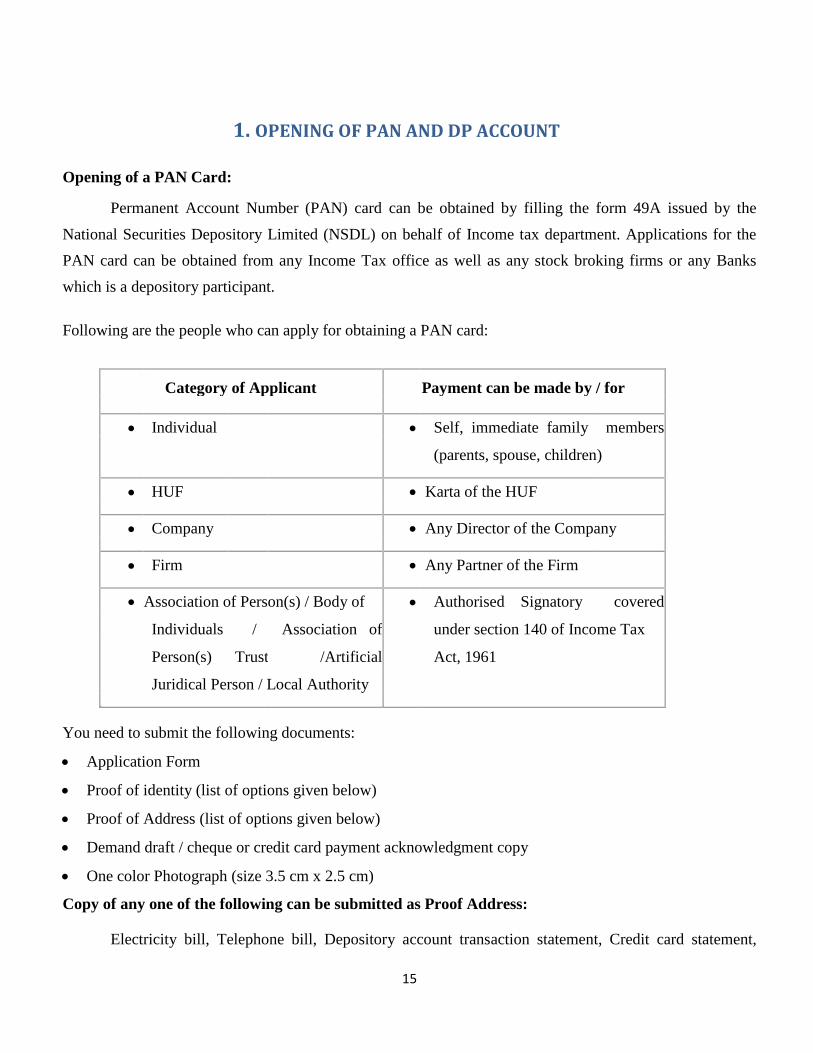

1. OPENING OF PAN AND DP ACCOUNT

Opening of a PAN Card:

Permanent Account Number (PAN) card can be obtained by filling the form 49A issued by the

National Securities Depository Limited (NSDL) on behalf of Income tax department. Applications for the

PAN card can be obtained from any Income Tax office as well as any stock broking firms or any Banks

which is a depository participant.

Following are the people who can apply for obtaining a PAN card:

Category of Applicant Payment can be made by / for

Individual Self, immediate family members

(parents, spouse, children)

HUF Karta of the HUF

Company Any Director of the Company

Firm Any Partner of the Firm

Association of Person(s) / Body of Authorised Signatory covered

Individuals / Association of under section 140 of Income Tax

Person(s) Trust /Artificial Act, 1961

Juridical Person / Local Authority

You need to submit the following documents: Application Form Proof of identity (list of options given below) Proof of Address (list of options given below) Demand draft / cheque or credit card payment acknowledgment copy One color Photograph (size 3.5 cm x 2.5 cm) Copy of any one of the following can be submitted as Proof Address:

Electricity bill, Telephone bill, Depository account transaction statement, Credit card statement,

16

Bank account statement, Ration card, Employer certificate, Passport Voters Identity card,

Property tax assessment order, Driving License, Rent receipt, Certificate of address signed by

Member of Parliament or Member of Legislative Assembly or Municipal Councilor or Gazetted

Officer.

Copy of any one of the following can be submitted as Proof Identity:

School leaving certificate, Matriculation certificate, Degree of a recognized educational

institution, Depository account transaction statement, Credit card, Bank account statement, Water

bill, Ration card, Property tax assessment order, Passport, Voters Identity Card, Driving License,

Certificate of identity signed by Member of Parliament or Member of Legislative Assembly or

Municipal Councilor or Gazetted Officer

OPENING OF BANK ACCOUNT

One can open an account with a deposit as low as Rs.100/- to Rs.300/-(Rs. 250/- for cheque

book facility and Rs.100/- without cheque book facility) depending upon the area and earn interest at

3.5% (w.e.f 01/03/2003) per annum. Computerized branches - Rs.500/- and Specialized hi-tech

branches - Rs.2000/-

The Bank's Savings Bank Rules are laid down in the various circulars issued by Head Office

From time to time. Managers and other Supervising Officials staff must read the instructions here

under in conjunction with the rules with which they must keep themselves fully conversant.

Opening of Accounts:

Accounts may be opened in the names of:-

I. Individuals, singly or jointly with other individuals; II. Minors, or on behalf of minors by their guardians. Special Instructions in this regard are contained in

paragraphs 7 to 14; III. Employees (in their individual names) of Schools and Colleges jointly with the Secretary/ Head

Master/Principal of the School/College, as the case may be for depositing provident fund moneys of the

employees provided there is no Trust Deed/Rules relating to the Provident Fund; IV. Associations, Clubs or similar other non-trading institutions (or purpose of depositing savings, provided

the relevant bylaws, rules etc., are found acceptable and are strictly adhered to;

17

18

V. Societies registered under the Societies Registration Act, 1860 or any other corresponding law in

force in a State or a Union Territory; VI. Companies governed by the Companies Act, 1956 which have been licensed by the Central

Government under Section 25 of the said Act or under the corresponding provision in the Indian

Companies Act, 1913 and permitted not to add lo their names the word limited' or the words

'private limited'. VII. Institutions, which are not liable to pay Income Tax under the Income Tax Act

a. 1961.

b. Savings Bank Account of Hindu Undivided families provided The Hindu undivided family is not

engaged in trading and business activity. Such a Savings Bank account should be preferably

opened in the name of the Karta.

Only in exceptional circumstances will accounts be opened in the names of

companies (other than item VI above), Corporations, Proprietary or Partnership Firms, Trustees,

Liquidators etc., with prior permission of the Controlling Authorities.

An application to open a Savings Bank Account will be taken on Form No. 1725

according to whether the depositor wants an account with or without the facility of withdrawal by

cheque, if the applicant is not well known, he should be required to furnish a written introduction

from some respectable person known to the Bank (. All applications must be approved by the

Manager or Manager (Accounts) / Deputy Manager (Accounts) / Assistant Manager (Accounts).

After the accounts have been opened, the forms will be signed by the Manager or Manager

(Accounts) / Deputy Manager (Accounts) / Assistant Manager (Accounts) and will be numbered

with the account numbers and filed in serial order.

The application to open such an account is to be taken on Form No.1725 signed by the minor.

The minor should declare his/her date of birth, which may be accepted as prima facie in order and

no supporting evidence, need be called for. Introductory reference may be taken from the father or

mother where he/she is already known to the Bank or the Head Master/Principal of the educational

institution where the minor is studying. Upon the minor attaining majority, all that will need to be

done will be to note this fact in the account opening forms, specimen signature card and ledger

sheet for completion of record.

19

When an account is opened in the names of two or more persons, who are not minors,

all of them must sign the application and the account will be operated in accordance with their

instructions on the back of the form, unless the instructions are rescinded by any one of them in

terms of the Savings Bank Rules. Under the same rules, the balance is repayable to the survivor or

survivors without reference to the representatives of the deceased person or persons.

Branches may open Savings Bank accounts in the names of two persons payable to

'Former or Survivor' or 'Later or Survivor' on similar lines on which Term Deposit Accounts are

opened.

Accounts will be opened segment wise in the Savings Bank ledger(s), each account being

allotted a serial number which will be entered in the pass book . The passbook should be handed over to

the depositor after the amount of the initial deposit has been credited to the account and entered in the

passbook under the initial of the supervising official.

An alphabetical index of accounts must be accurately maintained and kept upto date as

accounts are carried over to new folios or into new ledgers. Specimen Signatures

Specimen Signatures will be obtained on specimen signature cards at the time of opening their

accounts and must be individually attested by the Manager or Manager (Accounts)/Deputy Manager

(Accounts)/Assistant Manager (Accounts). The same precautions must be taken to record as are observed

in the case of specimen signatures on constituent accounts (vide paragraph 149 and 150 of Chapter 3).

Specimen Signatures in Kannada or other Indian languages may be accepted.

Minimum Balance in Savings Bank account:-

The minimum balance to be maintained in the Savings Bank account with cheque book and

without cheque book is furnished in relation to the population category.

OPENING OF DP ACCOUNT

In order to avail of depository facilities, an investor has to open a beneficiary account with a

depository participant of his choice. This is similar to opening a bank account to use the banking

services.

20

Just as one can hold funds in a bank account and transfer funds across accounts without actually

handling cash; one can hold securities in a depository account and transfer securities across depository

accounts without actually handling share certificates. The account holder is called 'beneficial owner' in a

depository system and the account is known as 'beneficiary account'.

Features of Beneficiary Account No minimum balance is required to be retained in a beneficiary account.

An investor can close a beneficiary account with one DP and open an account with another DP.

To dematerialized existing physical holdings, the beneficiary account must be opened in the same

ownership pattern in which the securities are held in the physical form e.g., if one certificate is in

individual name and another certificate is jointly held by X & Y, two different accounts should be

opened. However, in case of joint holders, securities can be dematerialized in the same account even

though share certificates are in different sequence of names e.g., shares held in joint names of X & Y

can also be dematerialized in an account opened in the names of Y & X as well by submitting an

additional form (Transposition Form) along with Demat Request Form to the DP.However, shares

held jointly by X & Y cannot be dematerialized in an account opened in the name of only X or only

Y or any combination of a joint account with three names i.e., X, Y and Z.

Procedure

Investor will choose a DP for the purposes of opening beneficiary account. The choice of the

investor may be based on convenience, comfort, services offered, cost or any other reason.

The investor will obtain the relevant account opening form from the chosen DP.

For the purpose of verification, investor has to submit the following documents along with the

prescribed account opening form. In case investor wants to open account jointly with other

person(s), following should be submitted for all the account holders:

PROOF OF IDENTITY (POI) (COPY OF ANY ONE PROOF): Passport

Voter ID Card

PAN card with photograph

21

PROOF OF ADDRESS (POA) (COPY OF ANY ONE PROOF):

Ration card Voted ID card Electricity Bill

Passport-Size Photograph

Copy of Pan Card

Original documents must be taken to the DP for verification. DP will carry out "in-person

verification" of account holder(s) at the time of opening the account.

Account opening form requires the applicants to give the following details:

Name(s) of account holder(s) -The investor should ensure that the name is identical to that which

appears on the certificate(s) to be dematerialised. In case of joint holdings, account may be opened in

any one combination, irrespective of the sequence in which names are appearing on share certificates.

Investors are advised to open their account in their fully expanded name, i.e., to spell to the first

name as well as the middle name. This would obviate any doubts about the veracity of the

information.

Mailing and communication addresses - The veracity of the applicant's address is determined

through the documents submitted for verification like ration card, passport, voter ID, PAN card,

driving license, bank passbook, etc. For NRI accounts, proof is required for both addresses - that of

the account holder as well as the constituted attorney. For corporate accounts, a copy of

Memorandum of Association, Articles of Association, Board resolution permitting opening of

account, the registered address of the company have to be furnished.

Details of guardian in case account holder is a minor -Only a guardian can open a depository

account for a minor. The guardian is required to sign the application form, and details of his name

and address need to be given in addition to the details of the minor.

Foreign Address and RBI approval details for NRI, FII or OCB accounts -For foreign-based

applicants like NRIs, Flls, OCBs, etc., the applicant must furnish original or attested copies of the

power of attorney and the approval letter from RBI permitting them to invest, as the case may be. If

the account holder is an FII or an OCB, SEBI registration details along with attested copy of

22

registration certificate issued by SEBI and authorisation letter is required.

Details of bank account -Details of bank account of the account holder, including the nine digit code

number of the bank and branch appearing on the MICR cheques issued by the bank have to be filled

in the application form. Companies use this information for printing them on dividend/interest

warrants etc.

Nomination declaration -A beneficial owner can make a nomination of his account in favour of any

person by filing the nomination form with his DP. Such nomination is considered to be conclusive

evidence of the account holder'(s) disposition in respect of all the securities in the account for which

the nomination is made. Standing Instruction - a facility of standing instruction is provided to the investors for receiving

securities to the credit of their accounts without giving a separate receipt instruction.

The Demat account cannot be operated on "either or survivor" basis like the bank account. In

case of the joint account for the beneficial owners, all the joint holders have to sign the account

opening form.

The investor will submit to his DP the duly filled in account opening form & DP-client

agreement along with the documents. The DP will verify whether the account opening form has been

duly filled in or not. He will also verify the submitted documents. For corporate investors, the DP

will also verify whether the board resolution for the authorised signatories has been enclosed. The DP

will ensure that client's signature is recorded on the form which will serve as specimen for

authorizations in future.

If the application form and documents are in order, the DP will accept them and give an

acknowledgement slip duly signed and stamped to the client. The DP will execute the agreement and

give a copy of it to the client.

After completion of all documentation, the DP will enter the client details as mentioned in the

account opening form in the DPM (software provided by NSDL to the DP) screen provided for the

purpose. After entering client details in the system, a client account number will be generated by the

DPM. The DP will enter this in the account opening form.

23

On successful opening of the account, the DP will give:

Client Id - an eight digit number to be used along with DP Id for any future transactions.

Delivery Instruction slip book.

A copy of the report listing the client details captured in the DPM database to the client. The

report will be generated by the DPM. Precautions:

Corporate investors to enclose Memorandum of Association/Trust deed/Board resolution for

the authorised signatories along with the account opening form.

Details with respect to the bank account details of an investor must be indicated in the space

provided for the same in the account opening form.

If an investor is interested in availing the facility of standing instructions for credits to his

account, then such instructions may be given to the DP. Otherwise, he will need to give a

receipt instruction to his DP for receiving credits to his account.

24

2. EVALUATION OF NEW ISSUE APPLICATION FORMS IPO EVALUATION

Introduction

Public issues can be classified into Initial Public Offerings and Further Public Offerings.

In a public offering, the issuer makes an offer for new investors to enter its shareholding family. The

issuer company makes detailed disclosures as per the DIP guidelines in its offer document and offers

it for subscription. Initial Public Offering (IPO) is when an unlisted company makes either a fresh

issue of securities or an offer for sale of its existing securities or both for the first time to the public.

This paves way for listing and trading of the issuer’s securities.

IPO is new shares Offered to the public in the Primary Market .The first time the company is

traded on the stock exchange. A prospectus is issued to read about its risk before investing. IPO is a

company's first sale of stock to the public. Securities offered in an IPO are often, but not always,

those of young, small companies seeking outside equity capital and a public market for their stock.

Investors purchasing stock in IPOs generally must be prepared to accept very large risks for the

possibility of large gains. Sometimes, just before the IPO is launched, Existing share Holders get

very liberal bonus issues as a reward for their faith in risking money when the project was new

How to apply to a Public issue?

When a company floats a public issue or IPO, it prints forms for application to be filled by

the investors. Public issues are open for a few days only. As per law, any public issue should be kept

open for a minimum of 3days and a maximum of 21 days. For issues, which are underwritten by

financial institutions, the offer should be kept open for a minimum of 3 days and a maximum of 21

days.

For issues, which are underwritten by all India financial institutions, the offer should be kept

open for a maximum of 10 days. Generally, issues are kept open for only 3 to 4 days. The duly

complete application from, accompanied by cash, cheque, DD or stock invest should be deposited

before the closing date as per the instruction on the form. IPO's by investment companies (closed end

funds) usually contain underwriting fees which represent a load to buyers.

Before applying for any IPO, analyse the following factors:

1. Who are the Promoters? What is their credibility and track record?

25

2. What is the company manufacturing or providing services - Product, its potential 3. Does the Company have any Technology tie-up? if yes , What is the reputation of the collaborators 4. What has been the past performance of the Company offering the IPO? 5. What is the Project cost, what are the means of financing and profitability projections? 6. What are all the Risk factors involved? 7. Who has appraised the Project? In India Projects apprised by IDBI and ICICI have more credibility

than small Merchant Bankers

How to make payments for IPO?

The payment terms of any IPO or Public issue is fixed by the company keeping in view its

fund requirements and the statutory regulations. In general, companies stipulate that either the entire

money should be paid along with the application or 50 percent of the entire amount be paid along

with the application and rest on allotment. However, if the funds requirements are staggered, the

company may ask for the money in calls, that is, the company demands for the money after allotment

as and when the cash flow demands. As per the statutory requirements, for public issue large than Rs.

250 crore, the money is to be collected as under:

25 per cent on application 25 per cent on allotment 50 per cent in two or more calls

Understanding IPO Grading

IPO grading is a unique concept involving an independent agency that is free from bias and

with the available tools for assessing the investment attractiveness of an equity security. IPO grading

is a service aimed at facilitating the assessment of equity issues offered to the public, says SEBI. IPO

grading can act as an additional decision-making tool for them.

The idea is that IPO grading will help the investor better appreciate the meaning of the

disclosures in the issue documents, collapsing all of the above information into a single digit. Thus,

IPO grading could be seen as an added investment guidance tool seeking to hide the ignorance of the

above factors and still help the investors make an informed decision. Grading of IPOs in terms of

their fundamental quality will enable investors steer clear of unsound offers. IPO grading in general

26

would be a relative assessment of the fundamentals of the equity security by credit rating agencies

registered with SEBI.

But IPO grading is totally unheard of anywhere else and is a First-From-India initiative. The

grading, to be done by the SEBI-registered credit rating agencies, would be applicable to all IPOs for

which offer documents are filed after April 30, SEBI said in a circular. SEBI does not play any role

in the assessment made by the grading agency.

The grading is intended to be an independent and unbiased opinion of that agency. The

company needs to first contact one of the grading agencies and mandate it for the grading exercise.

Though this process will ideally require 2-3 weeks for completion, it may be a good idea for

companies to initiate the grading process about 6-8 weeks before the targeted IPO date to provide

sufficient time for any contingencies. IPO grading is a service aimed at facilitating the assessment of

equity issues offered to the public, says SEBI.

“IPO grading is the grade assigned by a Credit Rating Agency registered with SEBI, to the initial

public offering (IPO) of equity shares or any other security which may be converted into or

exchanged with equity shares at a later date”

3. IPO RISK FACTORS

RISK FACTORS

An investment in Equity Shares involves a high degree of risk. The risks and uncertainties

described in this section are not the only risks that the company currently faces. Additional risks and

uncertainties not presently known to us or that we currently believe to be immaterial may also have

27

an adverse effect on this business, results of operations and financial condition. If any of the

following risks, or other risks that are not currently known or are now deemed immaterial, actually

occur, adani business, results of operations and financial condition could suffer, the price of this

Equity Shares could decline, and investor may lose all or part of the investor investment.

The financial and other related implications of risks concerned, wherever quantifiable, have

been disclosed in the risk factors mentioned below. However, there are risk factors where the effect

is not quantifiable and hence has not been disclosed in such risk factors.

The numbering of the risk factors has been done to facilitate the ease of reading and

reference, and does not in any manner indicate the importance of one risk factor over another. In

making an investment decision, prospective investors must rely on their own examination of the

Company and the terms of the Issue, including the merits and risks involved.

Unless otherwise stated, the financial information of the Company used in this section is

derived from our audited consolidated financial statements under Indian GAAP, as restated.

4. SCREEN BASED TRADING-NEAT, BOLT AND ODIN

NSE ARCHITECTURE – NEAT

NSE has deployed NIBIS (NSE's Internet Based Information System) for real-time

dissemination of trading information over the Internet and NEAT a client-server-based application to

help its operations.

NEAT (National Exchange for Automated Trading) stores all trading information in an in-

memory database at the server end to achieve minimum response time and maximum system

availability for users. The trading server software runs on a fault-tolerant STRATUS mainframe and

the client software runs on Windows PCs.The telecommunications network uses the X.25 protocol

and is the backbone of the automated trading system. Each trading member trades on the NSE with

28

other members through a PC located in the trading member's office.

The trading members on the Wholesale Debt Market segment are linked to the central

computer at the NSE through dedicated 64 Kbps leased lines and VSAT terminals. These leased lines

are multiplexed using dedicated 2 MB optical-fiber links. The WDM participants connect to the

trading system through dial-up links.

The exchange uses RISC-based UNIX servers from Digital and HP for back office

processing. Applications like Oracle 7 and SQL/Oracle Forms 4.5 front ends are used for the

exchange functions.

BSE ARCHITECTURE – BOLT

BSE has deployed an Online Trading system (BOLT) on March 14, 1995. It works on a

Tandem S74016 platform running on 16 CPUs. The Tandem Himalaya S74016 machines act as the

backend to more than 8000 Trader Workstations networked on Ethernet, VSAT and Managed Leased

Data Network (MLDN). The systems claim to handle up to two million trades a day.

BOLT has a two-tier architecture. The trader workstations are connected directly to the

backend server which acts as a communication server and a Central Trading Engine (CTE). Other

services like information dissemination, index computation, and position monitoring are also

provided by the system. A transaction monitoring facility in the Tandem architecture helps keep data

integrity through non-stop SQL.

29

With the help of MTNL, BSE has setup a MLDN Network comprising 300 2 Mbps lines

and 1500 64 Kbps lines which connect all regional stock exchanges and offices in Mumbai.

Access to market related information through the trader workstations is essential for the market

participants to act on real-time basis and take instantaneous decisions. BOLT has been interfaced

with various information vendors like Bloomberg, Bridge, and Reuters. Market information is fed

to news agencies in real time. The exchange plans to enhance the capabilities further to have an

integrated two-way information flow.

'BSE On-Line Trading System’ (BOLT) has been awarded the globally recognized

the

Information Security Management System standard BS7799-2:2002.

ODIN - OPEN DEALER INTEGRATED NETWORK

ODIN™ - the Multi-Exchange, Multi-Currency Front Office trading and risk management

system - makes trading on multiple markets easier through the use of a single application. It

incorporates appealing features and works on advanced technology which facilitates higher

accessibility, ensuring speedy performance and advanced risk management.

ODIN™ Trader Work Station (TWS) is the trading front-end for the brokers. The broker

can view an integrated Market Watch allowing him to view and trade on more than one market on

the same screen.

Features

Sophisticated trading front-end with Microsoft Excel compatibility

Offers alerts and basket trading features

Allows multiple portfolio creation, customizable preferences like font, layout, color, columns,

etc.

Offers real time integrated order and trade book.

Provides integrated view of mark-to-market profits & losses, net positions and exposures

Advanced trading strategies tool for capturing finest profit making opportunities

ODIN™ ADMINISTRATOR Defines organization structure by setting up groups, branches, dealers and clients Creates multiple administrators for role segregation as well as permit ease of monitoring

30

Defines various limits with alerts for each type of user and the end clients Defines risk views, risk scenarios and real-time update on risk at organization level and at each user

level Features panic withdrawal to cancel or close out all/selected outstanding orders in one click

ODIN™ Connect

ODIN™ Connect acts as a bridge between a client application, which could be an OMS

or a direct trading workstation, and a Stock Exchange’s Central Trading Engine. It provides a

higher level of abstraction over the exchange message structures to offer a uniform interface for a

client application to communicate with the Stock Exchange.

ODINTM

– DIET

Overview

ODIN™ Diet is a high-end, integrated trading application for active retail traders. It

works on an advanced technology algorithm. This facilitates higher accessibility and availability,

ensuring any where any time trading and delivers speedy performance on very low bandwidth

requirement. As the name suggest ODIN™ Diet works on the principle of high optimization of

the hardware and network requirements at the end-trader level.

ODIN™ Diet is a new generation, easy to access client level trading application. It

provides streaming quotes on a real-time basis and an ability to transmit buy/sell order requests

directly to the exchange. Existing ODIN™ users can provide this ‘direct trading facility' to their

clients without investing much on hardware or network. ODIN™ Diet application can easily

interface with the existing ODIN™ Server Setup.

ODIN™ Diet is capable of functioning on heterogeneous network platforms and ensures

high performance & scalability whereby facilitating anywhere any time trading environment. It is

user-friendly in the sense that the size of the application is shrink-wrapped to ease the distribution

and availability of the trading front-end.

Features

The self-installing kit of ODIN™ Diet is easy to deploy. It can be put on the Broker’s website to

allow client/s to download, install and trade anytime from any computer. For optimum utilization

of bandwidth ODIN™ Diet provides real-time streaming information for scrips set-up in the portfolio

thus optimizing the bandwidth utilization.

31

Integrated Market Watch provides a view with real-time streaming information from the

exchange Central Trading Engine for all the markets i.e.Equities, Derivatives and Commodities.

Ability to configure column profile makes it easier to view and navigate across columns.

Market Snap Shot provides the Best Buy / Sell price, Volume in Quantity and Value, day’s

Open, High, Low and Close prices for every individual scrips/contracts.

Best Five Orders Real-Time Market Information of securities & contracts, displaying the

market depth. Portfolio Portfolio is a selected set of scrips/ contracts logically grouped, as per the

requirements of the user. The portfolio can then be applied to views such as the Market Watch or the

Ticker. The user can create multiple portfolios and switch from one portfolio to another anytime.

The user can create a dynamic portfolio in Futures and options. This feature allows the user to

create a portfolio for Futures or Options based on Available/Current month, with strike prices based

on In/Out/At the Money. Thus on every expiry date/month the user is not required to create a new

portfolio for new maturities being introduced.

Order entry screen with minimum required inputs from user for quick creation and execution

of orders. Order and Trade confirmations are transmitted to the trader workstation in real-time,

thereby eliminating the need to query the server for order and trade information. Using the

comprehensive filters, the user can customize the order / trade book. The Order status is displayed in

the order book

e.g. pending at the exchange, executed, cancelled, pending administrator approval, amongst others.

Pending orders in the order book can be modified or cancelled.

Integrated Net Position and Exposures

A view to track the clients net-position either contract or security-wise. Further this provides

an aggregate view of exposures and maintains not only daily position but also expiry. Multi scrip

graphing facility, graph for comparison in F&O with the underlying. Intraday charting with pan,

zoom facility for scrips and index. Charting options with trend lines, mounts, cross, dots. Time

coordinates on graph with values.

32

The data window displays the data on which the graph is plotted.. Intraday data plotted on the

graph can be viewed in the data window.. The data can be viewed either on value or on volume. Data

can also be saved to file for future records.

The tick watch window displays the tick-by-tick movement in any scrip. This enables the user

to make more informed buy/sell decision based on the information. Data can be saved to file. The

facility of filter watch allows the user to set filters/alerts. The filters can be set for Volume, Price,

Quantity, Change in price % as and when any scrip satisfies the criteria it will appear in the filter

Benefits

Helps in leveraging business expertise for growth Trading facility available at marginal cost Common screen for multiple exchange segment User definable fully customizable views at all levels

Single interface for Multi Tier Risk Management across Multi-Exchange segments with user defined

periodicity Online integration with the bank & depository to monitor and control clients Provides safety against uncertain volatility of market Real time streaming quote of multi exchanges/segments Stability / Robustness Scalability Business Expansion Risk Management Performance

33

5. STUDY OF VARIOUS ORDER TYPES AND ORDER BOOKING

ORDER TYPES

An Order is an instruction to a broker/dealer to buy, sell, deliver, or receive financial

instruments or commodities which commits the issuer of the "order" to the terms specified.

Indication, inquiry, bid wanted, offer wanted.

Basically, two types of share transaction exist- buy orders and sell orders. Technically sell

orders can be further classified as either selling long or selling short. Various types of orders that you

can put through to exchanges are as follows:

Buy Orders

Buy orders, obviously are used when the investor anticipates a rise in prices. When he deems

the time appropriate for the share purchase, the investor enters a buy order.

Sell Orders

A brokerage order is to sell a specified amount of a security.

Sell – Long Orders

When the investor determines that a stock he already owns (i.e. long position) is going to

experience a decline in price, he may decide to dispose of it. Here also, other determinations must be

made to accompany sell order.

Sell-Short Orders

Short selling, or "going short," is a special and quite speculative variety of selling. Basically it

involves selling shares of a stock that are not owned in the anticipation of a price decline. The short

seller sells a stock in the first leg of transaction, which is neutralized by eventual purchase of sold

position at a lower market price. The short seller makes profit/loss by the difference between the sale

price and the purchased price. However, short selling can be very dangerous since every rise in price

of stock would add to losses of the short-seller, the stock may never reach the lower price (the price

of short sell) for a long time and booking losses would be the only solution for short-seller. Sell-short

transaction, by its very nature leads to unlimited losses till the transaction is neutralized. In the case

of a buy into a stock at least the investor acquires stake in the company whose performance may

eventually get reflected in the share price and provide exit to the buyer. Sell-short transactions are

34

hence executed by experienced participants who follow markets and company performances on a

daily basis.

Price Limit Orders: Market Order:

Investors, who want to buy or sell the share regardless of price on that day. They are executed

as fast as possible at the best prevailing price on the exchange. It means that your order quantity will

be executed the moment it reaches the exchange provided the required quantity is available. This

order type is accepted by both the exchanges i.e. BSE and NSE. The obvious advantage of a market

order is the speed with which it is executed. The disadvantage is that the investor does not know the

exact execution price until after the execution. This advantage is potentially most troublesome when

dealing in either very inactive or very volatile securities.

Limit orders

Limit type orders refer to a buy or sell order with a limit price. Limit orders overcome the

disadvantage of the market order-namely, not knowing in advance the price at which the transaction

will take place. It means that if the order gets executed, them it will within the limit specified or at a

better rate than that. This order type is accepted by both the exchanges i.e. BSE and NSE.

When using a limit order, the investor specifies in advance the limit price at which he wants

the transaction to be carried out. It is always understood that the price limitation includes an "or

better" instruction. In the case of a limit order to buy, the investor specifies the maximum price he

will pay for the share; the order can be carried out only at the limit price or lower. In the case of a

limit order to sell, the investor specifies the minimum price he will accept for the share; the order can

be carried out only at the limit price or higher Use of Market and limit orders:

To safe guard against extreme volatility in the markets, you can put a limit on what price you

would want your order to execute. Generally, limit orders are placed "away from the market." This

means that the limit price is somewhat removed from the prevailing price (generally, above the

prevailing price in the case of a limit order to sell, and below the prevailing price in the case of a

limit order to buy). Obviously, the investor operating in this manner believes that his limit price will

35

be reached and executed in a reasonable period of time. Therein, however, lies the chief disadvantage

of a limit order-i.e. it may never be executed at all. If the limit price is set very close to the prevailing

price, there is little advantage over the market order. Moreover, if the limit is considerably removed

from the market, the price may never reach the limit – even because of a fractional difference. Also

because limit orders are filled on a first come first basis, it is possible that so many of them are in

ahead of the investor’s limit at a given price that his order will never be executed. Thus, selecting a

proper limit price is a delicate maneuver.

On the other hand a market order is filled at the best possible price as soon as an investor

places the order and it will not be even possible to cancel the order. However, a limit order may be

cancelled or modified at any time prior to execution.

Time limit of Orders: Day Orders or End of Day Orders

A day order is one that remains active only for the normal trading time on that day. Unless

otherwise requested by the investor, all orders are treated as day orders only. Market orders are

almost day orders because they do not specify a particular price. One key rationale for the day order

is that market conditions might change overnight, and thus a seemingly good investment decision one

day might seem considerably less desirable the following day.

Good Till Cancel Order

A Good Till Cancelled (GTC) order remains in the system until they are executed or

cancelled. These types of orders are used in conjunction with limit orders. However, the system

cancels this order if it is not traded within a number of days, which is parameterized by the

Exchange. In the case of BSE and NSE, such order expires at the end of settlement in which it was

placed.

When using a GTC order, the investor is implying that he understands the market mechanics,

and therefore feels sufficiently confident that, given enough time, the order will be executed at the

limit price.

Good Till Date Order

A Good Till Days/Date (GTD) order allows you to specify the number of days/date till which

the order should stay in the system if not executed. The days counted are inclusive of the day/date on

which the order is placed and inclusive of holidays. Such orders are automatically cancelled at the

36

end of settlement in case strike-price is not reached during the tenure of settlement in which the order

was placed. The investor would then have to refresh the order with his broker, in the subsequent new

settlement.

Immediate or Cancel Order

An Immediate or Cancel (IOC) order allows the user to buy or sell a security as soon as the

order is released into the system, failing which the order is cancelled from the system. Partial match

is possible for the order and the unmatched portion of the order is cancelled immediately. NSE uses

the same terminology while BSE calls it Hit BUY/SELL.

SPECIAL TYPES OF ORDERS: Stop Loss Order:

A stop loss order allows investor to place an order, which gets activated only when the last

traded price of the share is reached or crosses a predefined threshold price also called as trigger price.

It means that if investor feels that any particular share will be worth buy or sell only after it crosses

some threshold rate then this type of order gets activated. Several possible dangers are inherent when

using this type of order. First, if the stop is placed too close to the market, the investor might have his

position closed out because of a minor price fluctuation, even though his idea will prove correct in

the long run. On the order hand, if the stop is too far away from the market, the stop order serves no

purpose. Further classification of this type of orders can be defined depending upon the price limit of

orders, i.e. the price on which the order should execute, as explained under:

Stop Loss Market Orders

A stop order is a special type of limit order but with very important differences in intent and

application. A stop market order to sell is treated as a market order when the stop price or a price

below is "touched" (reached); a stop market order to buy is treated as a market order when the stop

price or a price above it is reached. Thus, stop market order to sell is set at a price below the current

market price, and a stop order to buy is set at a price above the current market price.

The possible inherent danger associated with this type of order is that because they become

market orders after the proper price level has been reached, the actual transaction could take place

37

some distance away from the price the investor had in mind when he placed the order. The reason

may be prior queuing up of other orders or order quantity not available.

Stop Loss Limit Orders

The stop limit order is a device to overcome the uncertainties connected with a stop market

order – namely that of not knowing what the execution price will be after the order becomes a market

order. The stop limit order gives the investor the advantage of specifying the limit price: the

maximum price on which the buy order should filled or minimum price on which the sell order

should filled. Therefore, a stop limit order to buy is activated as soon as the stop price or higher is

reached, and then an attempt is made to buy at the limit price or lower. Conversely, a stop limit order

to sell is activated as soon as the stop price or lower is reached, and then an attempt is made to sell at

the limit price or higher. The obvious danger is that the order may not be executed in a volatile

market because the difference between execution limit and stop price may be too low. However, if

things work out as planned, the stop limit order to sell will be very effective.

Disclosed Quantity (DQ) order

The system provides a facility for entering orders with quantity conditions: DQ order allows

you to disclose only a part of the order quantity to the market.

Price Bands

Also known as circuit filters or circuit breakers, price bands set the upper and lower limit

within which a stock can fluctuate on any given day. A price band for the day is a function of

previous trading day’s closing. Currently the both BSE and NSE have fixed price bands for different

securities within which they can move within a day. Pursuant to a SEBI directive effective from July

03, 2000 the Exchanges decided that the price bands in respect of all the securities shall be relaxed by

8% after the security has touched the initial price band of 8%. However, for securities traded at or

above Rs.10 and below Rs.20 will have daily price band of +/-25% without any settlement / weekly

price band and for securities traded below Rs.10/- will have daily price band of +/- 50% without any

other settlement price band. The utility of price bands is that they are supposed to prevent extreme

price movements, thus reducing the scope of price manipulation. In a way price bands do slow things

down and make it that much harder for operators wanting to quickly manipulate prices in huge leaps.

When there is general euphoria or panic in the market that seems fundamentally unwarranted, price

38

bands give wary investors the benefit of a cooling period. Operators with access to large funds,

shares and time at their disposal, however can manipulate the price bands to their advantage by

blocking exit/entry of other investors from a particular counter by placing huge orders.

Example

For example when a stock touches the lower circuit in a sharp downtrend, ordinary buyers

would wait for the next trading session believing that the stock will be available at a still lower price. As a result, investors wanting to sell the stock won’t find buyers at the lower circuit price but would

have to offload at a much lower price due to the volume-led manipulation executed by operator. The

operator would thus be able to batter the stock down by a large gap created by his own sell order.

39

6. TRADING AND SETTLEMENT ACTIVITIES Introduction

The trading on stock exchanges in India used to take place through open outcry without use

of information technology for immediate matching or recording of trades. This was time consuming

and inefficient. This imposed limits on trading volumes and efficiency. In order to provide

efficiency, liquidity and transparency, NSE introduced a nation-wide on-line fully automated screen

based trading system (SBTS) where a member can punch into the computer quantities of securities

and the prices at which he likes to transact and the transaction is executed as soon as it finds a

matching sale or buy order from a counter party. SBTS electronically matches orders on a strict

price/time priority and hence cuts down on time, cost and risk of error, as well as on fraud resulting

in improved operational efficiency.

It allows faster incorporation of price sensitive information into prevailing prices, thus

increasing the informational efficiency of markets. It enables market participants, irrespective of their

geographical locations, to trade with one another simultaneously, improving the depth and liquidity

of the market. It provides full anonymity by accepting orders, big or small, from members without

revealing their identity, thus providing equal access to everybody. It also provides a perfect audit

trail, which helps to resolve disputes by logging in the trade execution process in entirety. This

sucked liquidity from other exchanges and in the very first year of its operation, NSE became the

leading stock exchange in the country, impacting the fortunes of other exchanges and forcing them to

adopt SBTS also. Today India can boast that almost 100% trading take place through electronic order

matching.

Technology was used to carry the trading platform from the trading hall of stock exchanges to

the premises of brokers. NSE carried the trading platform further to the PCs at the residence of

investors through the Internet and to handheld devices through WAP for convenience of mobile

investors. This made a huge difference in terms of equal access to investors in a geographically vast

country like India.

The trading network is depicted in Figure 1.1. NSE has main computer which is connected

through Very Small Aperture Terminal (VSAT) installed at its office. The main computer runs on a

fault tolerant STRATUS mainframe computer at the Exchange. Brokers have terminals (identified as

40

the PCs in the Figure 1.1) installed at their premises which are connected through VSATs/leased

lines/modems.

An investor informs a broker to place an order on his behalf. The broker enters the order

through his PC, which runs under Windows NT and sends signal to the Satellite via VSAT/leased

line/modem. The signal is directed to mainframe computer at NSE via VSAT at NSE's office. A

message relating to the order activity is broadcast to the respective member. The order confirmation

message is immediately displayed on the PC of the broker. This order matches with the existing

passive order(s), otherwise it waits for the active orders to enter the system. On order matching, a

message is broadcast to the respective member.

The trading system operates on a strict price time priority. All orders received on the system

are sorted with the best priced order getting the first priority for matching i.e., the best buy orders

match with the best sell order. Similar priced orders are sorted on time priority basis, i.e. the one that

came in early gets priority over the later one. Orders are matched automatically by the computer

keeping the system transparent, objective and fair. Where an order does not find a match, it remains

in the system and is displayed to the Whole market, till a fresh order comes in or the earlier order is

cancelled or modified.

The trading system provides tremendous flexibility to the users in terms of kinds of orders

that can be placed on the system. Several time - related (immediate or cancel), price-related (buy/sell

41

limit and stop loss orders) or volume related (Disclosed Quantity) conditions can be easily built into

an order. The trading system also provides complete market information on-line. The market screens

at any point of time provide complete information on total order depth in a security, the five best

buys and sells available in the market, the quantity traded during the day in that security, the high and

the low, the last traded price, etc. Investors can also know the fate of the orders almost as soon as

they are placed with the trading members. Thus the NEAT system provides an Open Electronic

Consolidated Limit Order Book (OECLOB).

Limit orders are orders to buy or sell shares at a stated quantity and stated price. If the price

quantity conditions do not match, the limit order will not be executed. The term ‘limit order book’

refers to the fact that only limit orders are stored in the book and all market orders are crossed against

the limit orders sitting in the book. Since the order book is visible to all market participants, it is

termed as an ‘Open Book’.

42

7. PREPARATION OF TECHNICAL CHARTS

TECHNICAL ANALYSIS

Fundamental and technical analyses are the 2 basic techniques used to analyze securities in

the stock market. Technical analysis is a mathematical approach to predict stock price movements

based on historical price and volume data. Usually stock charts are combined with the analytical data

to interpret technical indicators in a graphical format.

Technical analysis does not consider company fundamentals such as earnings, PE (Price to

Earnings Ratio), EBITDA, cash, debt, dividends, insider transactions, take-over’s, bankruptcy’s,

etc.Many professional securities traders recommend that aspiring traders use both fundamental and

technical analysis.

Interpreting stock charts Bar Chart

A method of displaying the open, high, low and close prices for a financial instrument for a

specific period.

Bar charts use single, vertical bars to illustrate a stock's price range and opening/closing

prices for a designated time period. The bars may illustrate daily, weekly, or monthly periods. For

example on a weekly chart, each bar represents one week and on a daily chart, each bar represents

one day.

The top of the bar indicates the stock's highest price of the period. The bottom of the bar

represents the stock's lowest price for that period. The small perpendicular bar on the left designates

the stock's opening price. The one on the right shows the stock's closing price.

Candle stick chart

A charting method used to display open, high, low and close prices for a security,

Candlesticks were invented by a 17th century Japanese rice broker, Munehisa Homma, who was one

of the first Japanese traders to use price history to predict future prices. His trading theories and

principles evolved into the candlestick charting techniques used today.

43

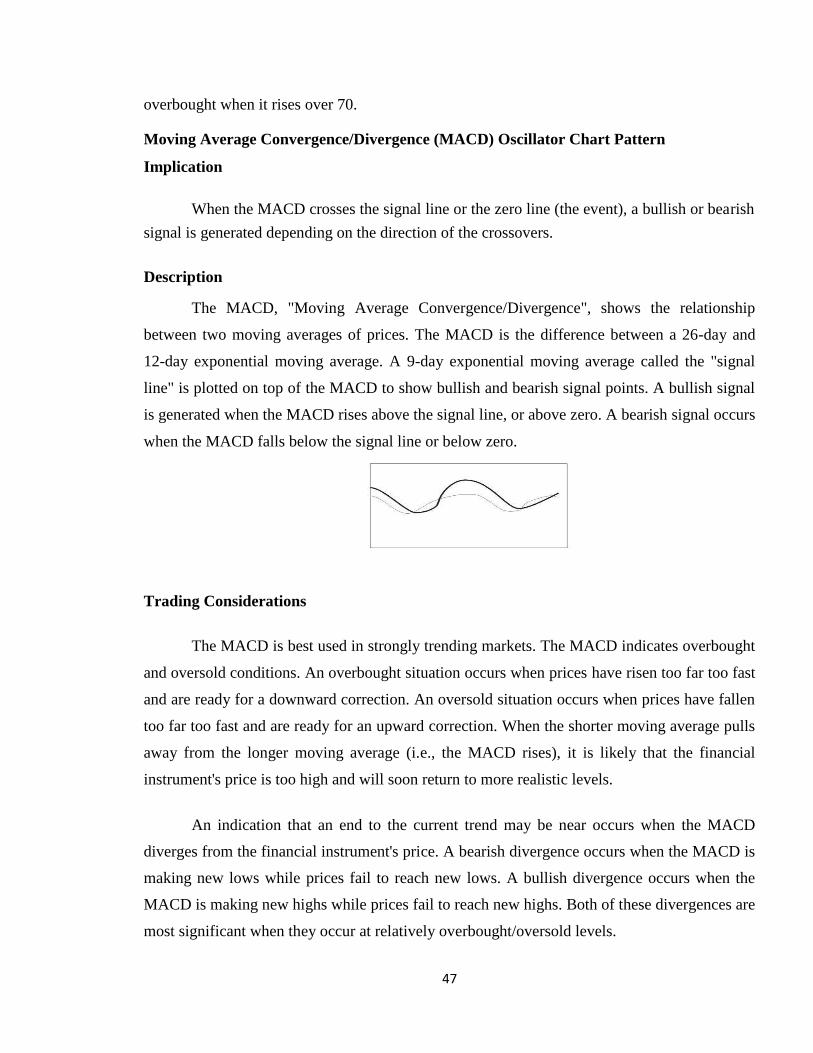

A candlestick uses the top and bottom of its bar to indicate high and low prices of the time

frame indicated. The bar is referred to as a "real body" and connects the opening and closing prices.

The real body shows the opening and closing prices with a clear, or a dark, rectangle. When the

rectangle or real body is clear, it means that the stock closed above its opening price. When the real

body is dark, it means that the stock closed below its opening price. The bar that extends above and

below the real body is called the upper shadow and lower shadow respectively.

Another major component of stock charts is the volume data. This data is usually shown in

bar graph format below the price chart

Line Chart The most basic of the four charts is the line chart because it represents only the closing prices over a

set period of time. The line is formed by connecting the closing prices over the time frame. Line

charts do not provide visual information of the trading range for the individual points such as the

high, low and opening prices. However, the closing price is often considered to be the most

important price in stock data compared to the high and low for the day and this is why it is the only

value used in line charts.

44

Head & Shoulders chart

The Head and Shoulders bottom is a popular pattern with investors. This pattern marks a

reversal of a downward trend in a financial instrument's price.

Volume is absolutely crucial to a Head and Shoulders Bottom. An investor will be looking for

increasing volumes at the point of breakout. This increased volume definitively marks the end of the

pattern and the reversal of a downward trend in the price of a stock.

A perfect example of the Head and Shoulders Bottom has three sharp low points created by

three successive reactions in the price of the financial instrument. It is essential that this pattern form

following a major downtrend in the financial instrument's price.

The first point - the left shoulder - occurs as the price of the financial instrument in a falling

market hits a new low and then rises in a minor recovery. The second point - the head happens when

prices fall from the high of the left shoulder to an even lower level and then rise again. The third

point - the right shoulder - occurs when prices fall again but don't hit the low of the head. Prices then

rise again once they have hit the low of the right shoulder. The lows of the shoulders are definitely

higher than that of the head and, in a classic formation, are often roughly equal to one another.

The neckline is a key element of this pattern. The neckline is formed by drawing a line

connecting the two high price points of the formation. The first high point occurs at the end of the

left shoulder and beginning of the downtrend to the head. The second marks the end of the head and

the beginning of the downturn to the right shoulder. The neckline usually points down in a Head and

Shoulders Bottom, but on rare occasions can slope up.

The pattern is complete when the resistance marked by the neckline is "broken". This occurs

when the price of the stock, rising from the low point of the right shoulder moves up through the

neckline. Many technical analysts only consider the neckline "broken" if the stock closes above the

neckline.

45

The volume sequence should progress beginning with relatively heavy volume as prices

descend to form the low point of the left shoulder. Once again, volume spikes as the stock hits

a new low to form the point of the head. It is possible that volume at the head may be slightly

lower than at the left shoulder. When the right shoulder is forming, however, volume should be

markedly lighter as the price of the stock once again moves lower.

It is most important to watch volume at the point where the neckline is broken. For a

true reversal, experts agree that heavy volume is essential. Technical indicators

Technical indicators are mathematical parameters that are constructed by intelligent

design with the intent to be used as tools to predict stock prices. The indicators are constructed

using stock price and volume data. View or create technical indicators at our example technical

indicators page. One signal market technicians look for is a divergence between certain

indicators and the price action of a stock. A positive divergence (classic buy signal) exists

when the price action of a stock is going down while the indicator is simultaneously becoming

more bullish. A negative divergence is the opposite of a positive divergence.

There are hundreds of well known technical indicators. Well known technical indicators

such as RSI (Relative Strength Index), Stochastics, Moving Average Cross-overs, MACD were

all contructed by humans. AiStockCharts.com goes far beyond relying on humans to construct

new intelligent technical indicators. Every day the AI (Artifical Intelligence) programs run at

AiStockCharts.com to find new and historically profitable technical indicators. Only the

strongest daily top stock picks are automatically entered into the AI StockCharts trading log as

open positions. Unlike other trading systems that set arbitrary entry and exit points,

AistockCharts.com sets exit prices including stop losses that are calculated based on the history

of the individual stock. Subscribers can lookup the historical performance of all technical

indicators. Some traders may be surprised to find some well known technical indicators have

worked well while others have not.

Hypothetical performance results have many inherent limitations, some of which are

described below. No representation is being made that any account will or is likely to achieve

profits or losses similar to those shown. In fact, there are frequently sharp differences between

hypothetical performance results and the actual results subsequently achieved by any particular

46

trading system. One of the limitations of hypothetical performance results is that they are

generally prepared with the

benefit of hindsight. In addition, hypothetical trading does not involve financial risk, and no

hypothetical trading record can completely account for the impact of financial risk in actual

trading. For example, the ability to withstand losses or to adhere to a particular trading program

in spite of trading losses are material points which can also adversely affect actual trading

results. There are numerous other factors related to the markets in general or to the

implementation of any specific trading program which cannot be fully accounted for in the

preparation of hypothetical performance results and all of which can adversely affect actual

trading results. The risk of loss in trading stocks can be substantial.

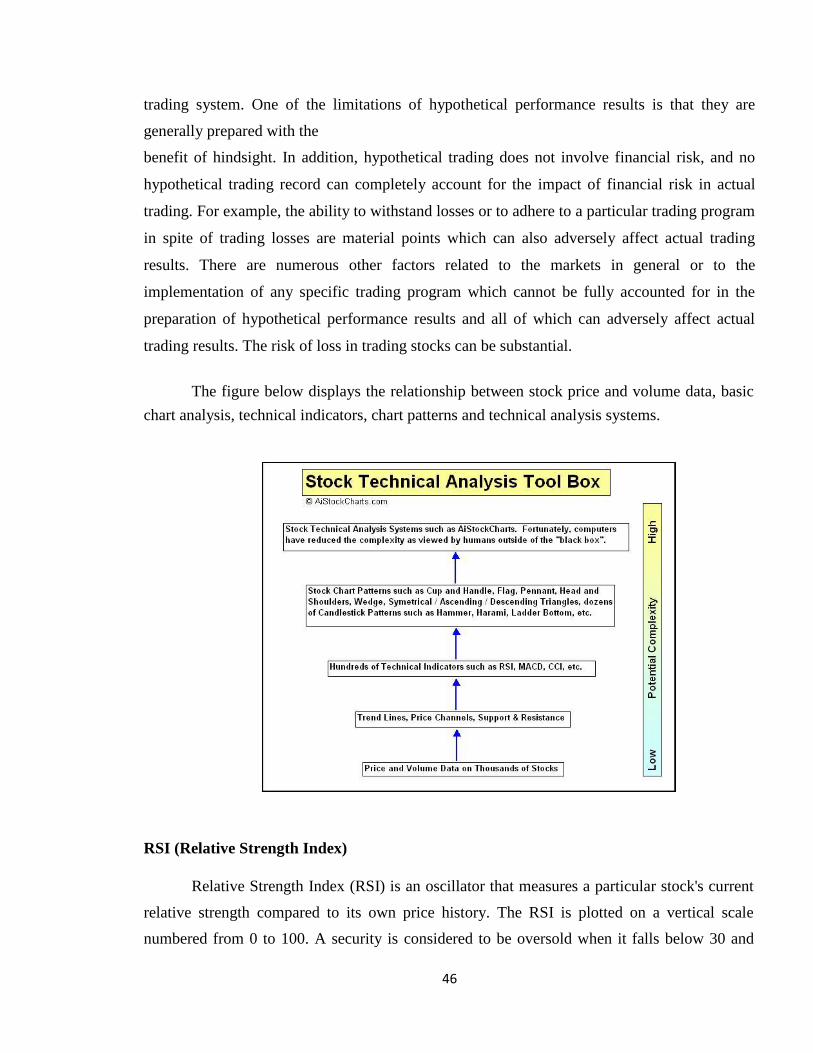

The figure below displays the relationship between stock price and volume data, basic

chart analysis, technical indicators, chart patterns and technical analysis systems.

RSI (Relative Strength Index)

Relative Strength Index (RSI) is an oscillator that measures a particular stock's current

relative strength compared to its own price history. The RSI is plotted on a vertical scale