full cycle profitable growth - s3. · pdf filenon-gaap measures: this presentation may contain...

TRANSCRIPT

TSX: BXE NYSE: BXE

Full Cycle Profitable Growth ANALYST UPDATE PRESENTATION SEPTEMBER 14, 2016

Advisories

FORWARD LOOKING STATEMENTS: In the interest of providing Bellatrix’s shareholders and potential investors with information regarding Bellatrix, including management’s assessment of Bellatrix’s future plans and operations, certain statements made by the presenter and contained in these presentation materials (collectively, this “presentation”) are forward looking statements or information within the meaning of applicable securities legislation, collectively referred to herein as “forward looking statements”. The forward-looking statements contained in this presentation speak only as of the date of this presentation and are expressly qualified by this cautionary statement. Forward looking statements in this presentation include, but are not limited to: management's assessment of future plans, operations and strategy, including the Company’s Spirit River play as a low cost natural gas supply source; the Company’s results delivering superior economic returns and industry leading capital efficiencies; ownership and control of strategic infrastructure assets and the sufficiency of the Company’s firm transportation capacity and ability to grow production to 60,000 boe/d; the Company’s cost profile and capital efficiencies supported by material infrastructure assets driving full cycle sustainable profitability; the Company’s ability to create value and upside to commodity price recovery and ability to manage debt and liquidity and further deleverage the Company’s balance sheet; management’s intentions to establish a new long-term revolving credit facility prior to the next scheduled review; the Company’s second half 2016 capital budget, production and operating cost guidance; management’s expectations regarding repayment of remaining balance of the term facility by November 11, 2016; management’s expectations that low cost Spirit River production volumes will continue to comprise a growing portion of total corporate production, management’s expectations that processing facilities and firm transportation capacity will help facilitate growth; management’s expectations regarding drill, complete, equip and tie-in costs for its Spirit River wells; future cost reductions associated with the Alder Flats Plant; management’s expectations regarding the Mannville/Spirit River and Cardium areas; management’s estimates of payouts, the internal rate of return (“IRR”), capital efficiencies, finding and development (“F&D”) costs and expected ultimate recovery of its wells; management’s expectations that the Spirit River is competitive with top tier Marcellus operator F&D costs and efficiencies; the Company’s strategic land position; management’s expectations regarding full cycle F&D costs, cash costs, operating costs, transportation costs, general and administrative expenses and interest and financing costs; management’s expectations regarding its ability to be an industry leader in development of the Spirit River play; management’s expectation that owned and operated infrastructure provides the Company with a strategic advantage and results in improved reliability of operations and sales, reduces operating costs, reduces royalty rates, and provides barriers to competition; management’s expectations regarding utilization of the Alder Flats Plant and the expectation that it will continue to operate at current efficiencies; drilling plans and the timing thereof; commodity price risk management strategies; the Company’s liquidity and compliance with the senior debt / EBITDA financial covenant; the timing of the Company’s next semi-annual borrowing base redetermination; the Company’s unfettered growth potential with its firm processing capacity; the economics of the Company’s resources are highly competitive with those of the Marcellus; management’s expectations that the Company has a large inventory of low risk development opportunities; management’s expectations that well performance will continue to rank among the best in the Spirit River and that the Company will remain a low cost operator and finder; management’s expectation that the Company possesses material leverage to a commodity price recovery; management’s expectation that the Company has unfettered growth potential with frim processing capacity; that the Company’s wells consistently rank among the best in the basin; estimates of commodity prices and exchange rates; drilling inventory and costs and time to develop; management’s expectation that the Company’s differentiated JV strategy provides significant benefits; and management’s expectation that the Cardium will remain a key long-term focus of the Company. Certain statements may constitute financial outlooks under applicable securities laws and were approved by management on September 13, 2016. Forward-looking statements necessarily involve risks, including, without limitation, risks associated with oil and gas exploration, development, exploitation, production, marketing and transportation, loss of markets, volatility of commodity prices, currency fluctuations, imprecision of reserve estimates, environmental risks, competition from other producers, inability to retain drilling rigs and other services, incorrect assessment of the value of acquisitions, failure to realize the anticipated benefits of acquisitions, actual results from wells to be drilled may not be similar to the results from previous wells drilled or the expected type curves, and delays resulting from or inability to obtain required regulatory approvals and ability to access sufficient capital from internal and external sources. Events or circumstances may cause actual results to differ materially from those predicted, as a result of the risk factors set out and other known and unknown risks, uncertainties, and other factors, many of which are beyond the control of Bellatrix. In addition, forward-looking statements or information are based on a number of factors and assumptions which have been used to develop such statements and information but which may prove to be incorrect and which have been used to develop such statements and information in order to provide shareholders with a more complete perspective on Bellatrix's future operations. Such information may prove to be incorrect and readers are cautioned that the information may not be appropriate for other purposes. Although Bellatrix believes that the expectations reflected in such forward-looking statements or information are reasonable, undue reliance should not be placed on forward looking statements because Bellatrix can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the impact of increasing competition; the general stability of the economic and political environment in which Bellatrix operates; the timely receipt of any required regulatory approvals; the ability of Bellatrix to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects which Bellatrix has an interest in to operate the field in a safe, efficient and effective manner; the ability of Bellatrix to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development of exploration; the timing and costs of pipeline, storage and facility construction and expansion and the ability of Bellatrix to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; the regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Bellatrix operates; and the ability of Bellatrix to successfully market its oil and natural gas products. Readers are cautioned that the foregoing list is not exhaustive of all factors and assumptions which have been used. As a consequence, actual results may differ materially from those anticipated in the forward-looking statements. Additional information on these and other factors that could affect Bellatrix's operations and financial results are included in reports on file with Canadian securities regulatory authorities and the U.S. Securities Exchange Commission ("SEC") and may be accessed through the SEDAR website (www.sedar.com), through the SEC website (www.sec.gov), and at Bellatrix's website (www.bellatrixexploration.com). Furthermore, the forward-looking statements contained herein are made as at the date hereof and Bellatrix does not undertake any obligation to update publicly or to revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws. NON-GAAP MEASURES: This presentation may contain certain non-GAAP measures, including the term “cash flow” which is a non-GAAP measure defined as cash from operating activities excluding net change in other assets and liabilities, net change in non-cash working capital and cash tax on sale of assets. This and any other non-GAAP measures used in this presentation are intended to provide shareholders and potential investors with additional information regarding Bellatrix’s liquidity and its ability to generate funds to finance its operations. FD&A COSTS: This presentation includes calculations of FD&A costs for the year ended December 31, 2015. The calculations of FD&A in this presentation include the reserves additions associated with acquisitions and the costs of acquisitions as Bellatrix believes that including the effect of acquisitions provides useful information to investors. BOE PRESENTATION: The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet of natural gas to one barrel of oil equivalent (6 mcf/ 1 bbl) is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value. All boe conversions in this presentation are derived from converting gas to oil in the ratio of six thousand cubic feet of gas to one barrel of oil. INITIAL PRODUCTION RATES: Initial production rates disclosed herein may not be indicative of long-term performance or ultimate recovery. Such rates are not determinative of the future production rates of such wells and do not reflect how the production from such wells will decline thereafter. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for Bellatrix. A pressure transient analysis or well test interpretation has not been carried out in respect of all wells. Accordingly, Bellatrix cautions that the test results should be considered to be preliminary. ESTIMATED ULTIMATE RECOVERY (EUR): In this presentation, estimated ultimate recovery represents the estimated ultimate recovery associated with the type curves presented which are based on the assumptions used by Sproule Associates Limited to estimate Bellatrix's proved plus probable reserves per well as evaluated effective December 31, 2015 based on forecast prices and costs. There is no certainty that such Bellatrix will ultimately recover such volumes from the wells it drills. ANALOGOUS INFORMATION: Certain information in this presentation may constitute "analogous information" as defined in National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities (“NI 51-101”), including, but not limited to, the reservoir data, production rates of industry wells, cumulative production information, and economics information relating to the areas in which Bellatrix has an interest. Such information has been obtained from government sources, regulatory agencies or other industry participants. Management of Bellatrix believes the information is relevant as it helps to define the reservoir characteristics and the reserves and production potential in which Bellatrix holds an interest. Such information has not been prepared in accordance with NI 51-101. Bellatrix is also unable to confirm that the analogous information was prepared by a qualified reserves evaluator or auditor. Such information is not an estimate of the resources attributable to lands held or to be held by Bellatrix and there is no certainty that the reservoir data, resource estimates, production and decline rates and economics information for the lands held by Bellatrix will be similar to the information presented herein. The reader is cautioned that the data relied upon by Bellatrix may be in error and/or may prove not be analogous to the lands be held by Bellatrix. CURRENCY: All dollar amounts in this presentation are Canadian dollars unless otherwise identified. DRILLING LOCATIONS: This presentation discloses drilling locations in three categories: (i) proved locations; (ii) probable locations; and (iii) unbooked locations. Proved locations and probable locations are sometimes collectively referred to as “booked locations”, are derived from Bellatrix’s most recent independent reserves evaluation and account for drilling locations that have associated proved + probable reserves or probable-only reserves, as applicable. Unbooked locations as disclosed herein have been identified by management as an estimation of the Company's multi-year drilling activities using information including evaluation of applicable geologic, seismic, engineering, production, pricing assumptions and reserves information. There is no certainty that Bellatrix will drill all unbooked drilling locations and if drilled there is no certainty that such locations will result in additional oil and gas reserves, resources or production. The drilling locations on which Bellatrix actually drill wells will ultimately depend upon the availability of capital, regulatory approvals, seasonal restrictions, oil and natural gas prices, costs, actual drilling results, additional reservoir information that is obtained and other factors. While the majority of Bellatrix's unbooked locations are extensions or infills of the drilling patterns already recognized by the Company's independent qualified reserves evaluator, other unbooked drilling locations are farther away from existing wells where management may have less information about the characteristics of the reservoir and therefore there may be more uncertainty whether wells will be drilled in such locations and if drilled there may be more uncertainty that such wells will result in additional oil and gas reserves, resources or production. RESERVES INFORMATION: Unless indicated otherwise, reserve estimates and related future net revenue and other reserves information is derived from Bellatrix’s independent reserve report prepared by Sproule Associates Limited as at December 31, 2015 using forecast prices and costs. Land acreage information is as available at December 31, 2015. TYPE CURVE AND CAPITAL EFFICIENCY: In this presentation information relating to the type curve, half cycle economics and capital efficiency for Bellatrix's Spirit River wells have been presented. The type curve set forth herein is based on all Bellatrix operated, Notikewin and Falher B wells drilled between October 2012 and September 2015, and represents the mean (P50) performance curve. Half cycle economics are based on Bellatrix's current expectations of drill, complete, equip and tie-in costs per well (and excluding land, seismic and related costs). Capital efficiency is a measure of expected capital expenditures per well based on half cycle economics divided by average first year production results (IP365) based on the type curve presented. The type curve and capital efficiency numbers have been presented to provide readers with information on the assumptions used for management's budgeting process and future planning. The half cycle economics and capital efficiencies may not be achieved on future wells as a result of a number of factors including the risks identified above under "Forward Looking Statements" and as such are not reliable indicators of future performance. In addition, there is no certainty that future wells will generate results to match historic type curves presented herein. Half cycle economics and capital efficiencies are not terms that have standardized meanings and therefore such calculations may not be comparable with the calculation of similar measures for other entities. FINANCIAL INFORMATION: Unless otherwise stated, financial information is based upon Bellatrix’s 2015 audited consolidated financial statements for the years ended December 31, 2015 and 2014.

2

Agenda

3

TOPIC

Corporate Strategy & Key Themes• Deleveraging Review• Strength & Depth of Asset Portfolio• Repositioned for Growth

Financial Strategy• Risk Management• Capital Structure

Geology• Deep Basin Setting• Spirit River Growth Assets & Cardium optionality

Operations• Drilling & Completions Technical Overview

Engineering• Type Curves & Performance• Reserve Overview

Production• Optimization Initiatives & Decline Attenuation• Strategic Infrastructure & Facilities

Outlook• Budget & Outlook• Capital Allocation Strategy

Concluding Remarks and Q&A

Introduction

Asset Overview Intro

Analyst Update Presentation Themes

4 Long term shareholder value creation

TRANSFORMATIONAL DELEVERAGING ACHIEVED IN 2016

REPOSITIONED FOR GROWTH

TOP TIER ASSETS PROVIDE OPTIONALITY FOR BOTH OIL & NATURAL GAS INVESTMENT

MEANINGFUL EQUITY VALUE PROPOSITION

Experienced & Committed Management Team

5

Mark StephenVP Operations

Steve TothVP Investor Relations

Garrett UlmerVP Engineering

Charles KrausVP General CounselCorporate Secretary

David LaingVP Production

Russell OicleVP Exploration

Tim BlairVP Land

Chris CurryVP Controller

Leanne Gress-BlueVP Finance

Ray SmithPresident & CEO

Ed BrownExecutive VP Finance

& CFO

Brent EshlemanExecutive VP & COO

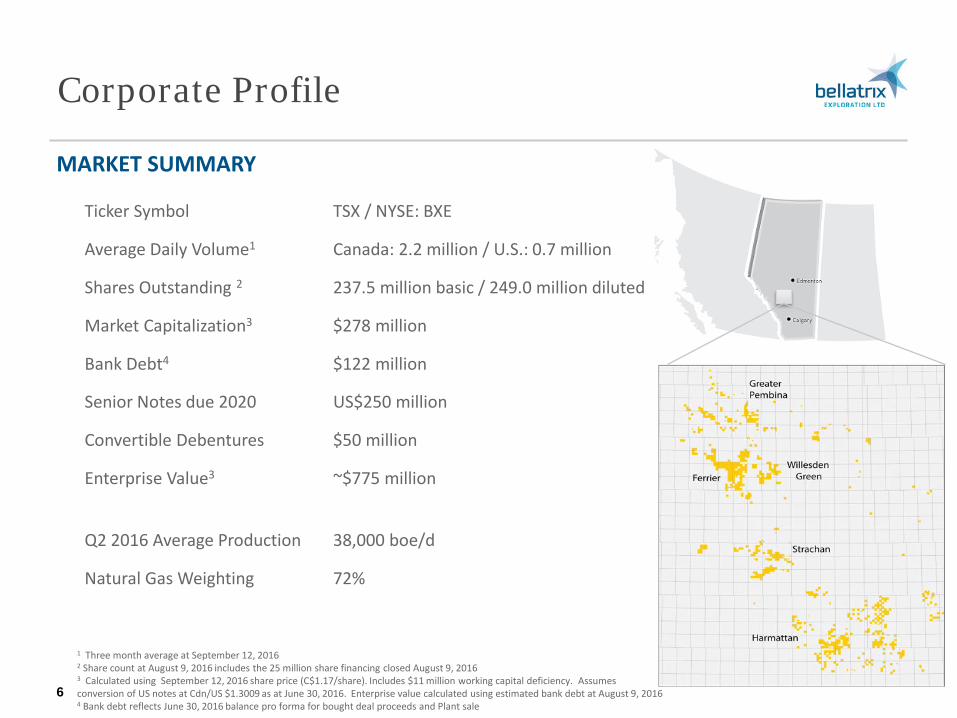

Corporate Profile

MARKET SUMMARY

Ticker Symbol TSX / NYSE: BXE

Average Daily Volume1 Canada: 2.2 million / U.S.: 0.7 million

Shares Outstanding 2 237.5 million basic / 249.0 million diluted

Market Capitalization3 $278 million

Bank Debt4 $122 million

Senior Notes due 2020 US$250 million

Convertible Debentures $50 million

Enterprise Value3 ~$775 million

Q2 2016 Average Production 38,000 boe/d

Natural Gas Weighting 72%

6

1 Three month average at September 12, 2016 2 Share count at August 9, 2016 includes the 25 million share financing closed August 9, 2016 3 Calculated using September 12, 2016 share price (C$1.17/share). Includes $11 million working capital deficiency. Assumes conversion of US notes at Cdn/US $1.3009 as at June 30, 2016. Enterprise value calculated using estimated bank debt at August 9, 2016 4 Bank debt reflects June 30, 2016 balance pro forma for bought deal proceeds and Plant sale

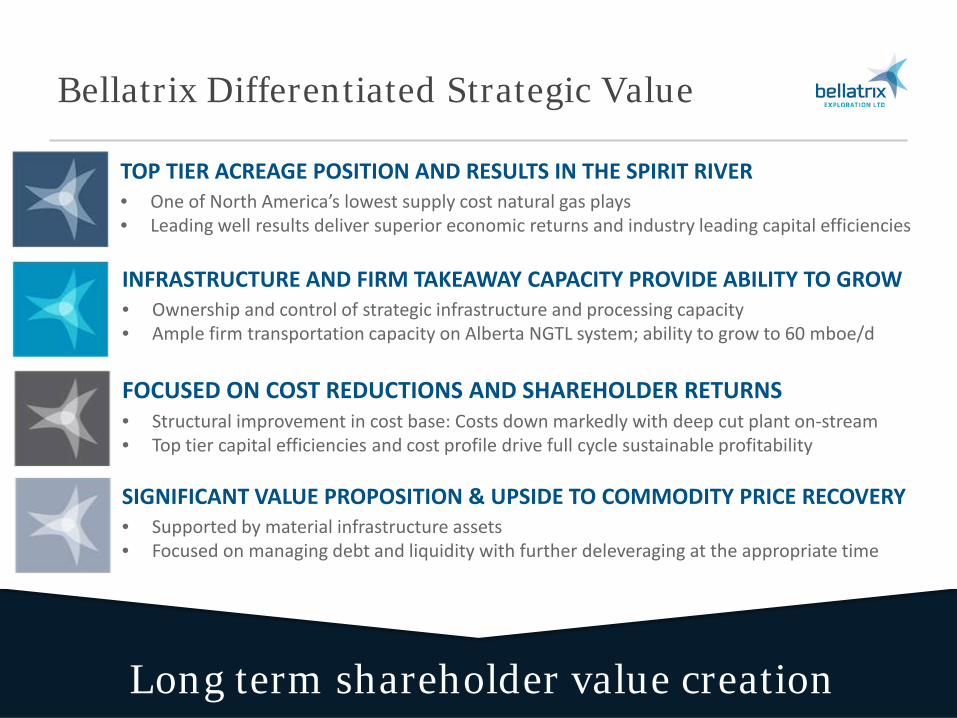

Bellatrix Differentiated Strategic Value

7 Long term shareholder value creation

TOP TIER ACREAGE POSITION AND RESULTS IN THE SPIRIT RIVER • One of North America’s lowest supply cost natural gas plays • Leading well results deliver superior economic returns and industry leading capital efficiencies

SIGNIFICANT VALUE PROPOSITION & UPSIDE TO COMMODITY PRICE RECOVERY • Supported by material infrastructure assets • Focused on managing debt and liquidity with further deleveraging at the appropriate time

INFRASTRUCTURE AND FIRM TAKEAWAY CAPACITY PROVIDE ABILITY TO GROW • Ownership and control of strategic infrastructure and processing capacity • Ample firm transportation capacity on Alberta NGTL system; ability to grow to 60 mboe/d

FOCUSED ON COST REDUCTIONS AND SHAREHOLDER RETURNS • Structural improvement in cost base: Costs down markedly with deep cut plant on-stream • Top tier capital efficiencies and cost profile drive full cycle sustainable profitability

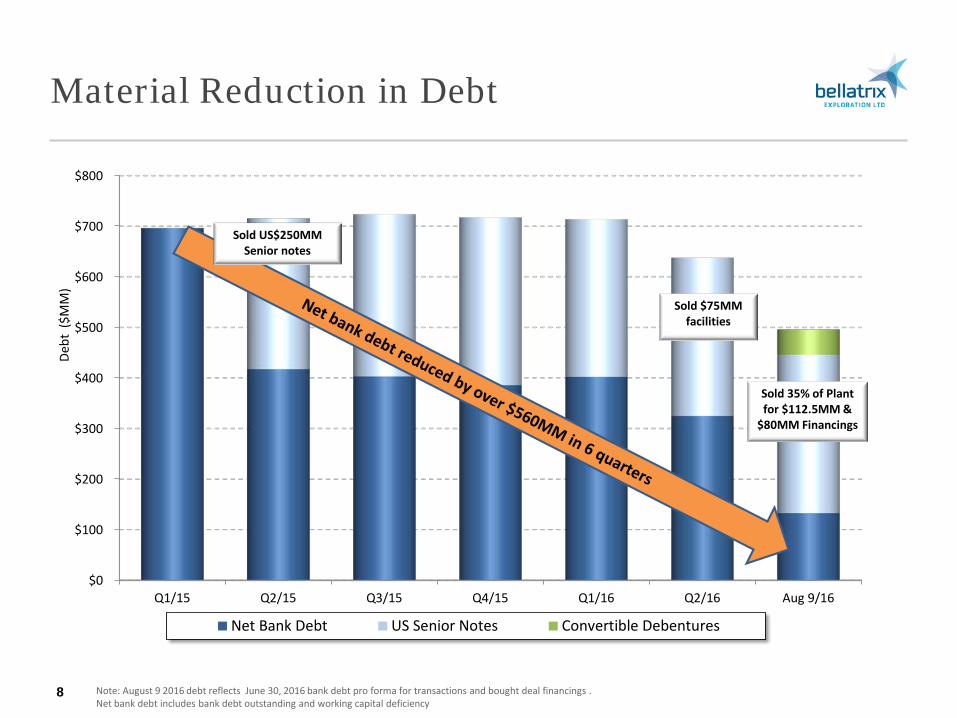

Material Reduction in Debt

8 Note: August 9 2016 debt reflects June 30, 2016 bank debt pro forma for transactions and bought deal financings . Net bank debt includes bank debt outstanding and working capital deficiency

$0

$100

$200

$300

$400

$500

$600

$700

$800

Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Aug 9/16

Debt

($M

M)

Net Bank Debt US Senior Notes Convertible Debentures

Sold $75MM facilities

Sold 35% of Plant for $112.5MM &

$80MM Financings

Sold US$250MM Senior notes

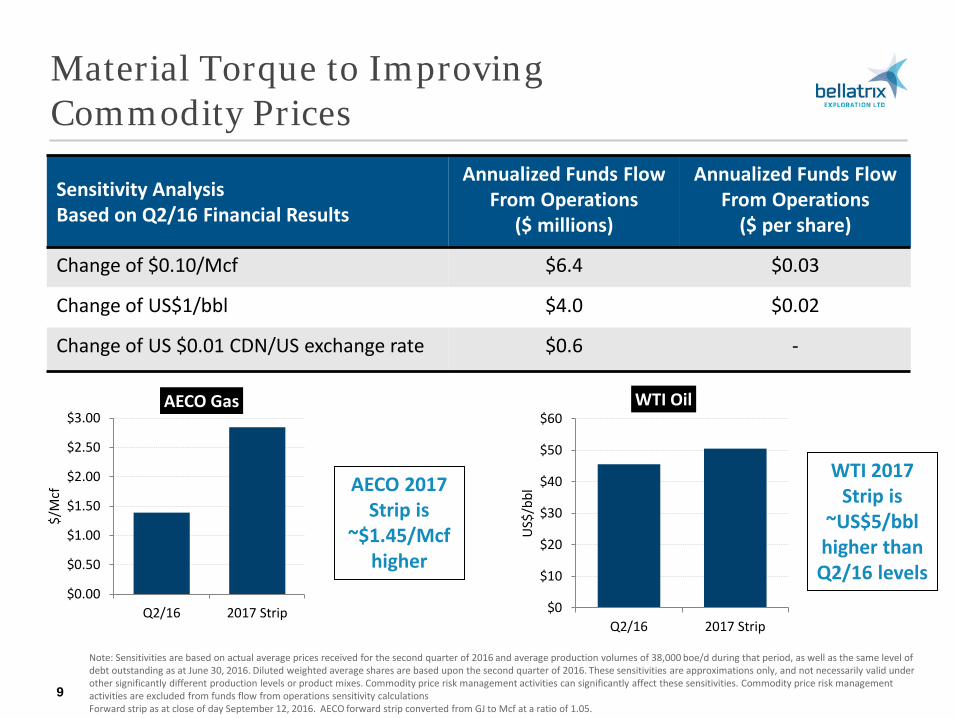

Material Torque to Improving Commodity Prices

9

Note: Sensitivities are based on actual average prices received for the second quarter of 2016 and average production volumes of 38,000 boe/d during that period, as well as the same level of debt outstanding as at June 30, 2016. Diluted weighted average shares are based upon the second quarter of 2016. These sensitivities are approximations only, and not necessarily valid under other significantly different production levels or product mixes. Commodity price risk management activities can significantly affect these sensitivities. Commodity price risk management activities are excluded from funds flow from operations sensitivity calculations Forward strip as at close of day September 12, 2016. AECO forward strip converted from GJ to Mcf at a ratio of 1.05.

Sensitivity Analysis Based on Q2/16 Financial Results

Annualized Funds Flow From Operations

($ millions)

Annualized Funds Flow From Operations

($ per share)

Change of $0.10/Mcf $6.4 $0.03

Change of US$1/bbl $4.0 $0.02

Change of US $0.01 CDN/US exchange rate $0.6 -

WTI 2017 Strip is

~US$5/bbl higher than Q2/16 levels

AECO 2017 Strip is

~$1.45/Mcf higher

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

Q2/16 2017 Strip

$/M

cf

AECO Gas

$0

$10

$20

$30

$40

$50

$60

Q2/16 2017 Strip

US$

/bbl

WTI Oil

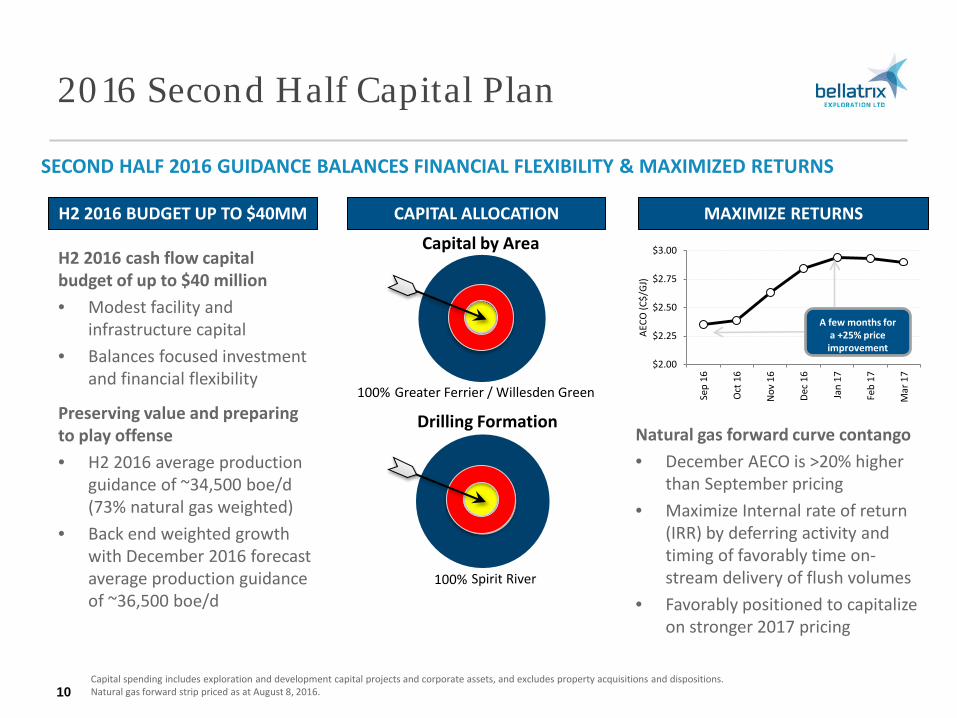

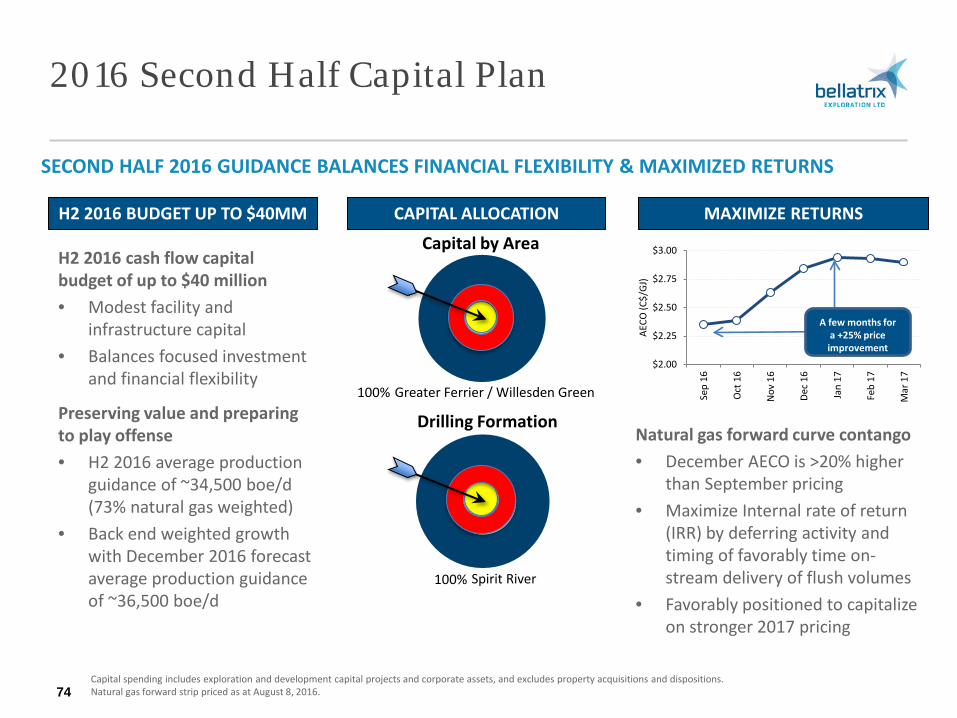

2016 Second Half Capital Plan

Capital spending includes exploration and development capital projects and corporate assets, and excludes property acquisitions and dispositions. Natural gas forward strip priced as at August 8, 2016. 10

SECOND HALF 2016 GUIDANCE BALANCES FINANCIAL FLEXIBILITY & MAXIMIZED RETURNS

H2 2016 BUDGET UP TO $40MM CAPITAL ALLOCATION MAXIMIZE RETURNS

Natural gas forward curve contango • December AECO is >20% higher

than September pricing • Maximize Internal rate of return

(IRR) by deferring activity and timing of favorably time on-stream delivery of flush volumes

• Favorably positioned to capitalize on stronger 2017 pricing

Capital by Area

Greater Ferrier / Willesden Green

Drilling Formation

Spirit River

100%

100%

H2 2016 cash flow capital budget of up to $40 million • Modest facility and

infrastructure capital • Balances focused investment

and financial flexibility

Preserving value and preparing to play offense • H2 2016 average production

guidance of ~34,500 boe/d (73% natural gas weighted)

• Back end weighted growth with December 2016 forecast average production guidance of ~36,500 boe/d

$2.00

$2.25

$2.50

$2.75

$3.00

Sep

16

Oct

16

Nov

16

Dec

16

Jan

17

Feb

17

Mar

17

AECO

(C$/

GJ)

A few months for a +25% price improvement

Financial Summary

Financial Strategy

12 Long term shareholder value creation

PROACTIVELY MAINTAIN AMPLE LIQUIDITY

PRUDENT AND EFFECTIVE RISK MANAGEMENT POLICY

SIMPLE CAPITAL STRUCTURE WITH DIVERSIFIED DEBT MATURITIES

OPPORTUNISTIC STRATEGIC ACQUISITIONS AND CONTINUAL REVIEW AND RATIONALIZATION OF NON-CORE PROPERTIES

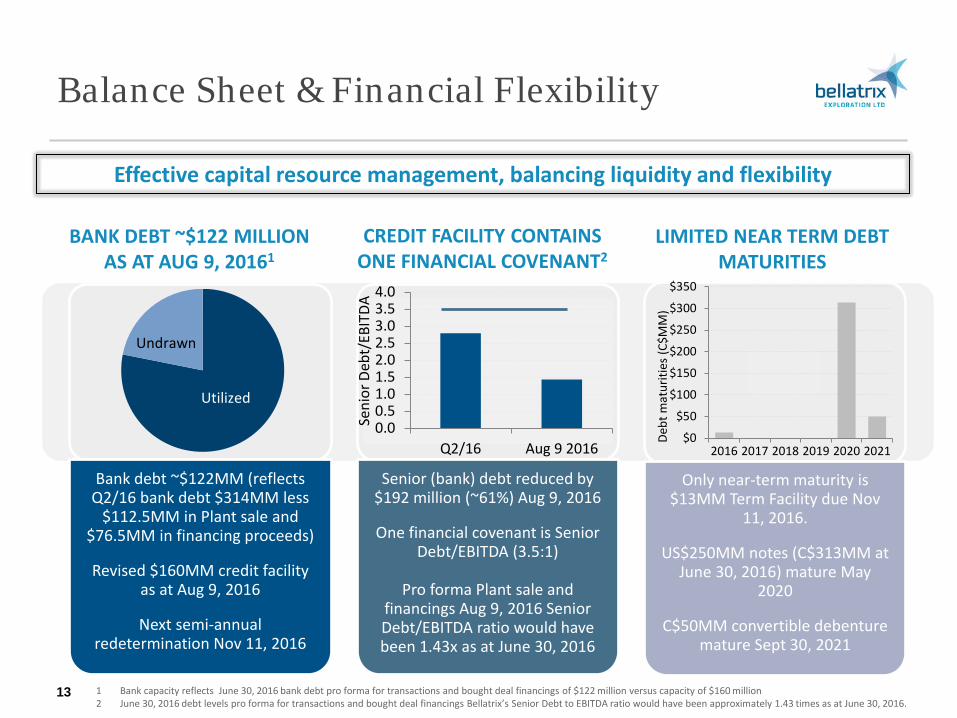

Balance Sheet & Financial Flexibility

13

BANK DEBT ~$122 MILLION AS AT AUG 9, 20161

CREDIT FACILITY CONTAINS ONE FINANCIAL COVENANT2

LIMITED NEAR TERM DEBT MATURITIES

Bank debt ~$122MM (reflects Q2/16 bank debt $314MM less

$112.5MM in Plant sale and $76.5MM in financing proceeds)

Revised $160MM credit facility as at Aug 9, 2016

Next semi-annual redetermination Nov 11, 2016

Senior (bank) debt reduced by $192 million (~61%) Aug 9, 2016

One financial covenant is Senior Debt/EBITDA (3.5:1)

Pro forma Plant sale and

financings Aug 9, 2016 Senior Debt/EBITDA ratio would have been 1.43x as at June 30, 2016

Only near-term maturity is $13MM Term Facility due Nov

11, 2016.

US$250MM notes (C$313MM at June 30, 2016) mature May

2020

C$50MM convertible debenture mature Sept 30, 2021

Effective capital resource management, balancing liquidity and flexibility

1 Bank capacity reflects June 30, 2016 bank debt pro forma for transactions and bought deal financings of $122 million versus capacity of $160 million 2 June 30, 2016 debt levels pro forma for transactions and bought deal financings Bellatrix’s Senior Debt to EBITDA ratio would have been approximately 1.43 times as at June 30, 2016.

Utilized

Undrawn

$0

$50

$100

$150

$200

$250

$300

$350

2016 2017 2018 2019 2020 2021

Debt

mat

uriti

es (C

$MM

)

0.00.51.01.52.02.53.03.54.0

Q2/16 Aug 9 2016

Seni

or D

ebt/

EBIT

DA

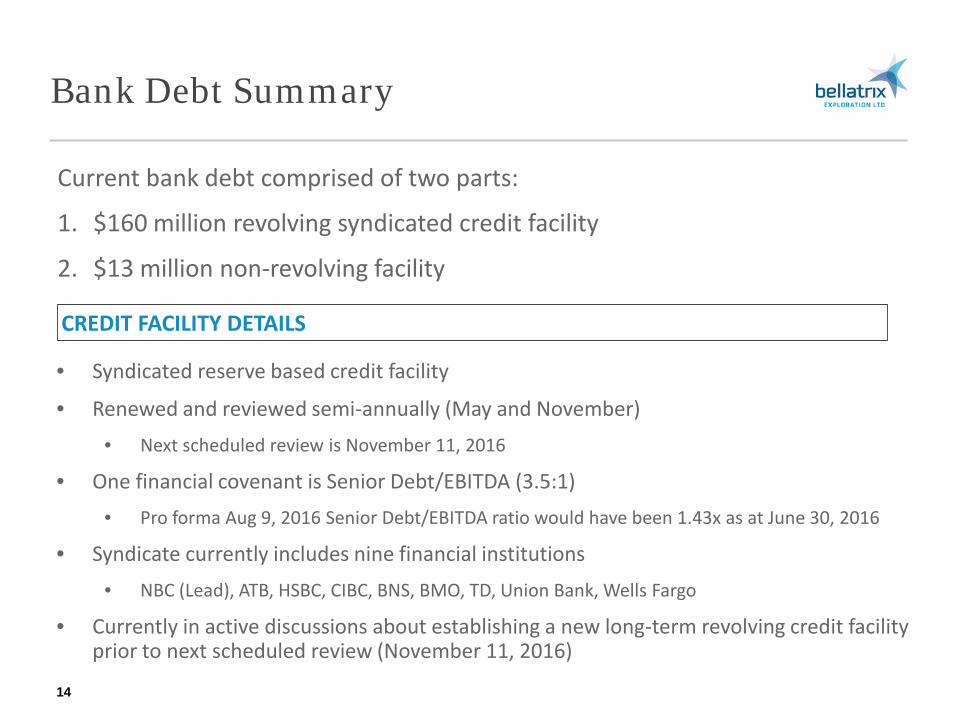

Bank Debt Summary

14

Current bank debt comprised of two parts:

1. $160 million revolving syndicated credit facility

2. $13 million non-revolving facility

• Syndicated reserve based credit facility

• Renewed and reviewed semi-annually (May and November) • Next scheduled review is November 11, 2016

• One financial covenant is Senior Debt/EBITDA (3.5:1) • Pro forma Aug 9, 2016 Senior Debt/EBITDA ratio would have been 1.43x as at June 30, 2016

• Syndicate currently includes nine financial institutions • NBC (Lead), ATB, HSBC, CIBC, BNS, BMO, TD, Union Bank, Wells Fargo

• Currently in active discussions about establishing a new long-term revolving credit facility prior to next scheduled review (November 11, 2016)

CREDIT FACILITY DETAILS

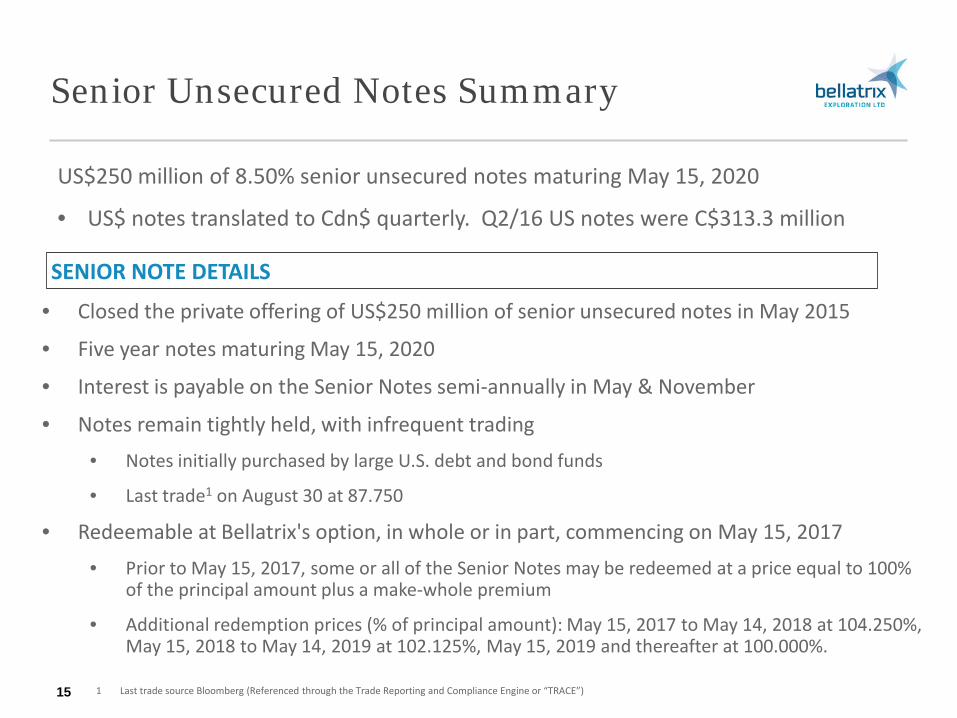

Senior Unsecured Notes Summary

15

US$250 million of 8.50% senior unsecured notes maturing May 15, 2020

• US$ notes translated to Cdn$ quarterly. Q2/16 US notes were C$313.3 million

• Closed the private offering of US$250 million of senior unsecured notes in May 2015

• Five year notes maturing May 15, 2020

• Interest is payable on the Senior Notes semi-annually in May & November

• Notes remain tightly held, with infrequent trading • Notes initially purchased by large U.S. debt and bond funds

• Last trade1 on August 30 at 87.750

• Redeemable at Bellatrix's option, in whole or in part, commencing on May 15, 2017 • Prior to May 15, 2017, some or all of the Senior Notes may be redeemed at a price equal to 100%

of the principal amount plus a make-whole premium

• Additional redemption prices (% of principal amount): May 15, 2017 to May 14, 2018 at 104.250%, May 15, 2018 to May 14, 2019 at 102.125%, May 15, 2019 and thereafter at 100.000%.

SENIOR NOTE DETAILS

1 Last trade source Bloomberg (Referenced through the Trade Reporting and Compliance Engine or “TRACE”)

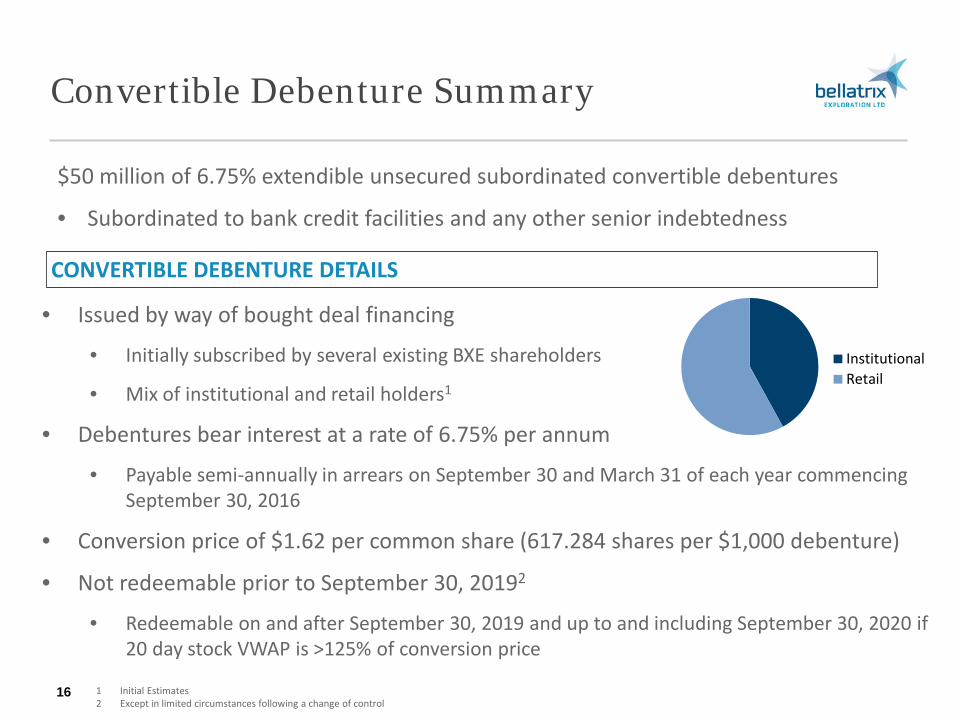

Convertible Debenture Summary

16

$50 million of 6.75% extendible unsecured subordinated convertible debentures

• Subordinated to bank credit facilities and any other senior indebtedness

• Issued by way of bought deal financing

• Initially subscribed by several existing BXE shareholders

• Mix of institutional and retail holders1

• Debentures bear interest at a rate of 6.75% per annum

• Payable semi-annually in arrears on September 30 and March 31 of each year commencing September 30, 2016

• Conversion price of $1.62 per common share (617.284 shares per $1,000 debenture)

• Not redeemable prior to September 30, 20192

• Redeemable on and after September 30, 2019 and up to and including September 30, 2020 if 20 day stock VWAP is >125% of conversion price

CONVERTIBLE DEBENTURE DETAILS

1 Initial Estimates 2 Except in limited circumstances following a change of control

InstitutionalRetail

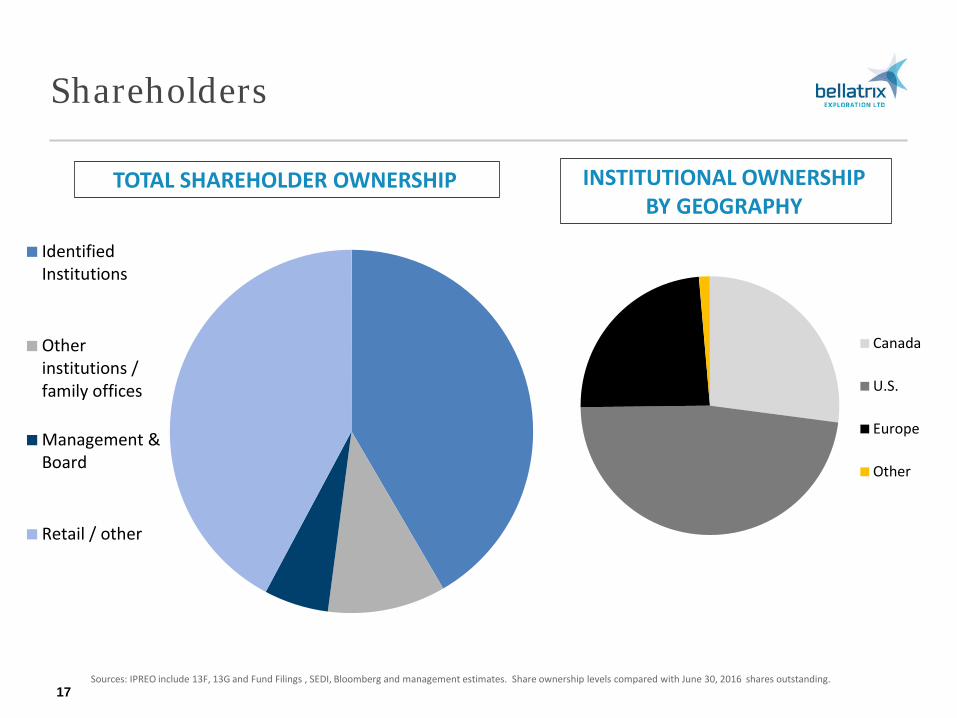

Shareholders

17

IdentifiedInstitutions

Otherinstitutions /family offices

Management &Board

Retail / other

TOTAL SHAREHOLDER OWNERSHIP

Canada

U.S.

Europe

Other

INSTITUTIONAL OWNERSHIP BY GEOGRAPHY

Sources: IPREO include 13F, 13G and Fund Filings , SEDI, Bloomberg and management estimates. Share ownership levels compared with June 30, 2016 shares outstanding.

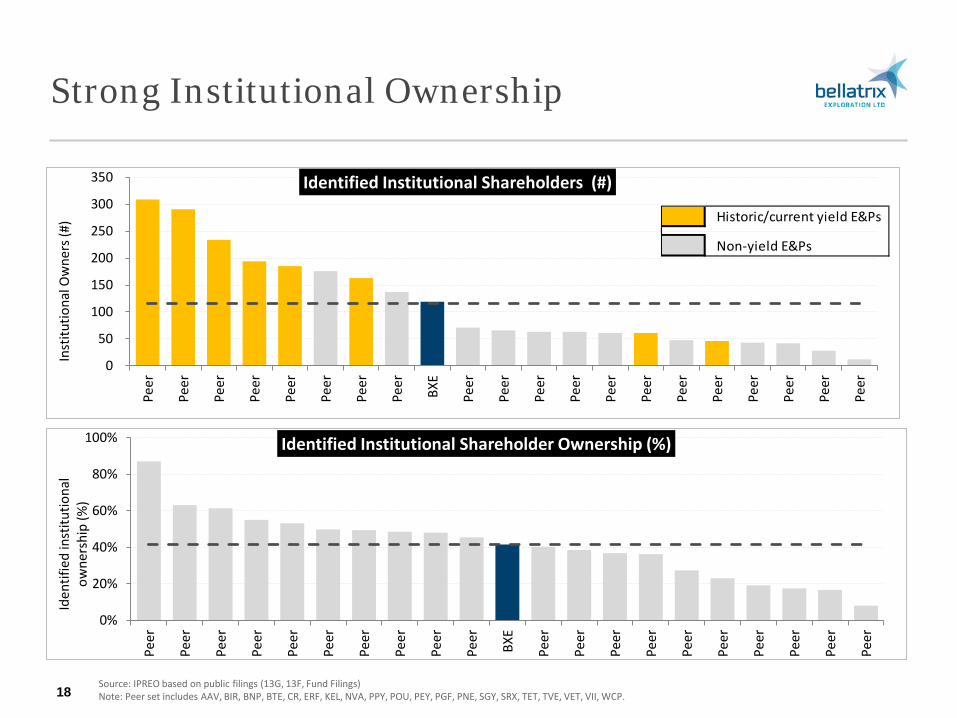

Strong Institutional Ownership

18

0

50

100

150

200

250

300

350

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

BXE

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Inst

itutio

nal O

wne

rs (#

)

Identified Institutional Shareholders (#)

Historic/current yield E&Ps

Non-yield E&Ps

Source: IPREO based on public filings (13G, 13F, Fund Filings) Note: Peer set includes AAV, BIR, BNP, BTE, CR, ERF, KEL, NVA, PPY, POU, PEY, PGF, PNE, SGY, SRX, TET, TVE, VET, VII, WCP.

0%

20%

40%

60%

80%

100%

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

BXE

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Peer

Iden

tifie

d in

stitu

tiona

l ow

ners

hip

(%)

Identified Institutional Shareholder Ownership (%)

Risk Management & Marketing Strategy

19

FINANCIAL RISK MANAGEMENT STRATEGY

A pillar of Bellatrix's strategic planning is a board approved active risk management policy providing reduced commodity price volatility and greater predictability of future revenue and cash flow

Hedging limits form part of the credit facility agreement based on prior quarter average production volumes on a rolling three year basis and are restricted to:

• 70% for forward first year, 60% for second year and 50% for third year for both oil and gas production

PHYSICAL MARKETING STRATEGY

Bellatrix manages its physical marketing exposure through a variety of methods including:

• Crude oil and NGL products are primarily sold at the plant gate which reduces physical and financial exposure to Bellatrix to reach and supply end use markets

• Natural gas volumes are transported on the Nova system to the AECO/NIT market point

• Products sold through ten different physical marketers reduces counterparty risk exposure

• Bellatrix enters into long term agreements for transportation both along the transmission system and through area processing facilities

• Long term fractionation agreements cover 100% of current and forecast NGL volumes

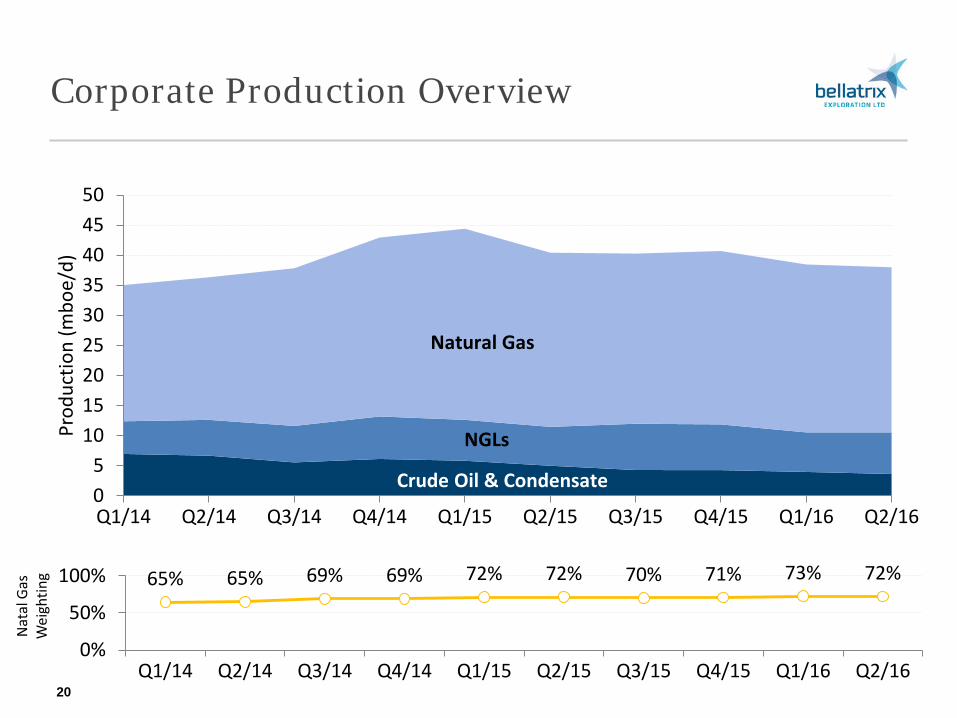

Corporate Production Overview

20

05

101520253035404550

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

Prod

uctio

n (m

boe/

d)

Crude Oil & Condensate

NGLs

Natural Gas

65% 65% 69% 69% 72% 72% 70% 71% 73% 72%

0%

50%

100%

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

Nat

al G

as

Wei

ghtin

g

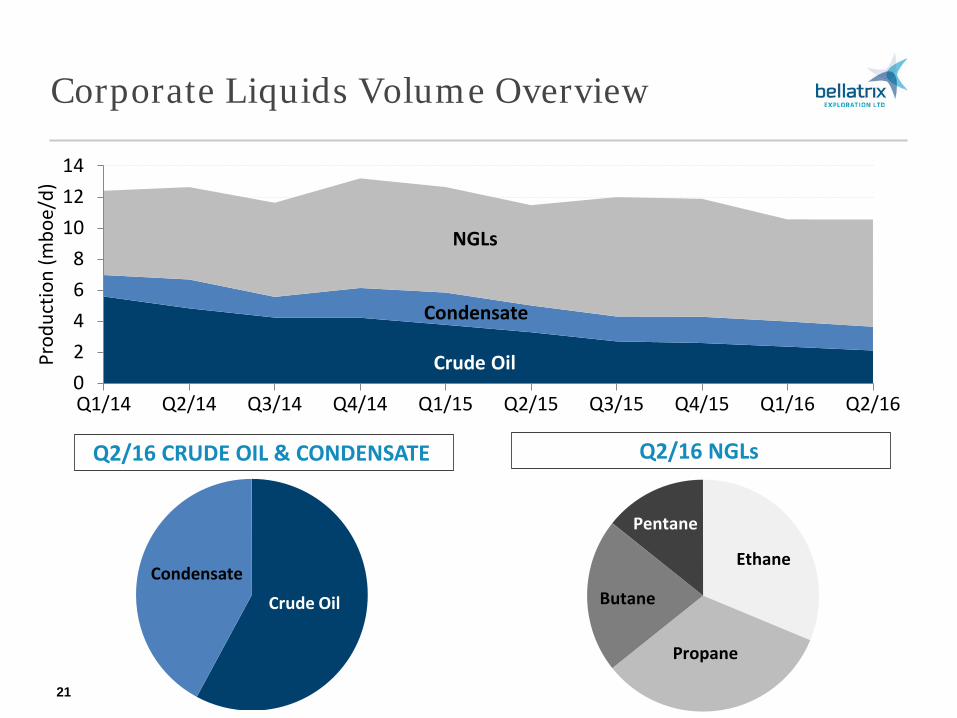

Corporate Liquids Volume Overview

21

02468

101214

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

Prod

uctio

n (m

boe/

d)

Crude Oil

Condensate

NGLs

Q2/16 CRUDE OIL & CONDENSATE Q2/16 NGLs

Crude Oil Condensate

Pentane

Ethane

Propane

Butane

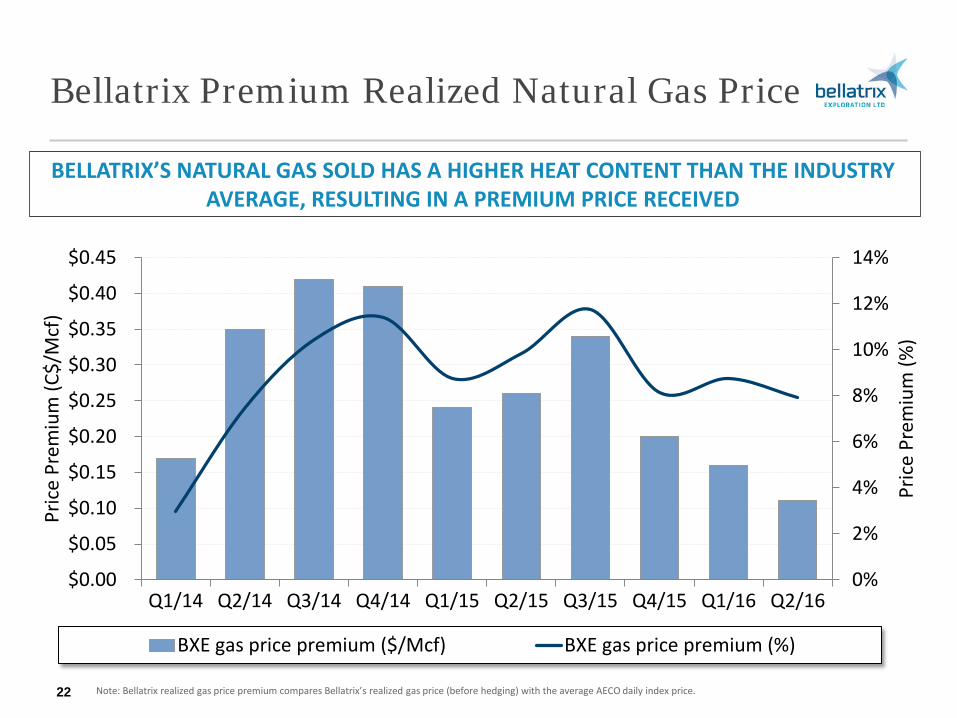

Bellatrix Premium Realized Natural Gas Price

22

BELLATRIX’S NATURAL GAS SOLD HAS A HIGHER HEAT CONTENT THAN THE INDUSTRY AVERAGE, RESULTING IN A PREMIUM PRICE RECEIVED

0%

2%

4%

6%

8%

10%

12%

14%

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

Pric

e Pr

emiu

m (%

)

Pric

e Pr

emiu

m (C

$/M

cf)

BXE gas price premium ($/Mcf) BXE gas price premium (%)

Note: Bellatrix realized gas price premium compares Bellatrix’s realized gas price (before hedging) with the average AECO daily index price.

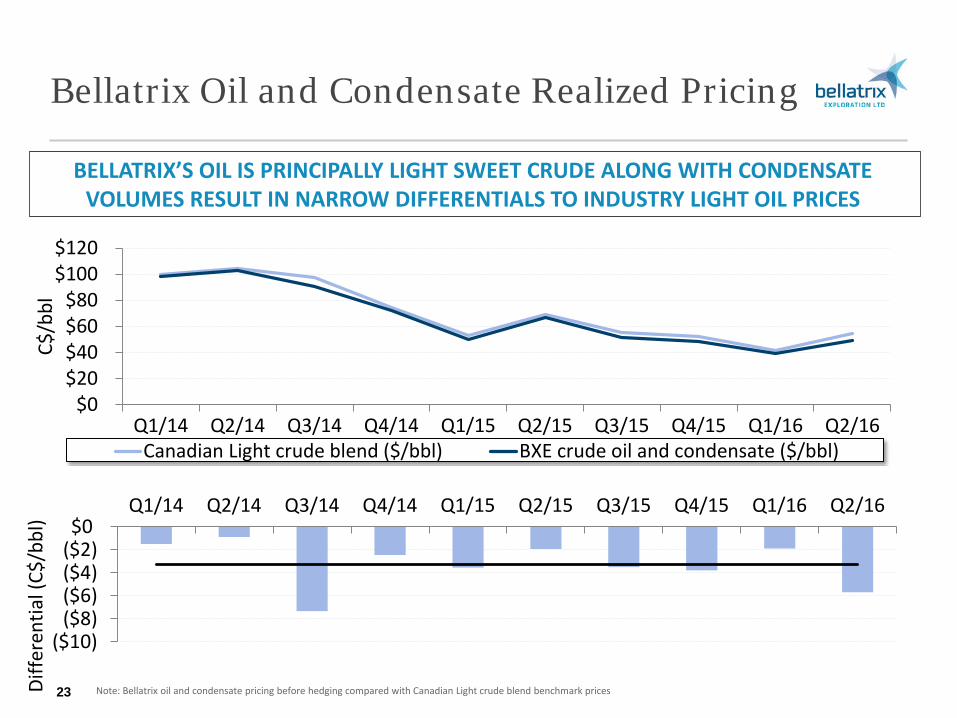

Bellatrix Oil and Condensate Realized Pricing

23

BELLATRIX’S OIL IS PRINCIPALLY LIGHT SWEET CRUDE ALONG WITH CONDENSATE VOLUMES RESULT IN NARROW DIFFERENTIALS TO INDUSTRY LIGHT OIL PRICES

$0$20$40$60$80

$100$120

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

C$/b

bl

Canadian Light crude blend ($/bbl) BXE crude oil and condensate ($/bbl)

($10)($8)($6)($4)($2)$0

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

Diffe

rent

ial (

C$/b

bl)

Note: Bellatrix oil and condensate pricing before hedging compared with Canadian Light crude blend benchmark prices

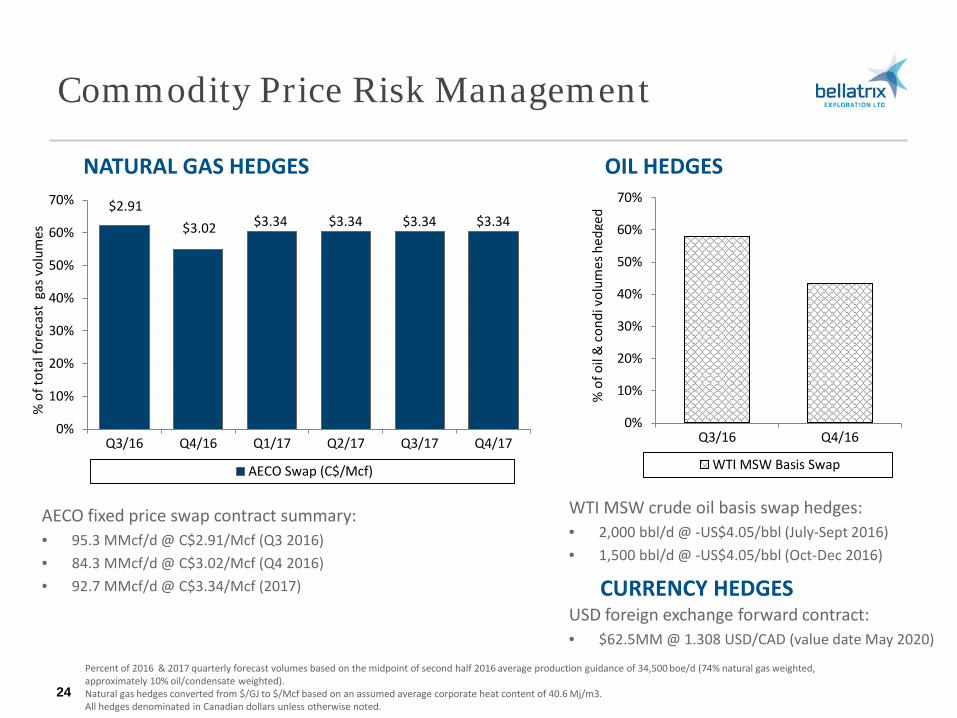

Commodity Price Risk Management

24

AECO fixed price swap contract summary: • 95.3 MMcf/d @ C$2.91/Mcf (Q3 2016) • 84.3 MMcf/d @ C$3.02/Mcf (Q4 2016) • 92.7 MMcf/d @ C$3.34/Mcf (2017)

WTI MSW crude oil basis swap hedges: • 2,000 bbl/d @ -US$4.05/bbl (July-Sept 2016) • 1,500 bbl/d @ -US$4.05/bbl (Oct-Dec 2016)

NATURAL GAS HEDGES OIL HEDGES

Percent of 2016 & 2017 quarterly forecast volumes based on the midpoint of second half 2016 average production guidance of 34,500 boe/d (74% natural gas weighted, approximately 10% oil/condensate weighted). Natural gas hedges converted from $/GJ to $/Mcf based on an assumed average corporate heat content of 40.6 Mj/m3. All hedges denominated in Canadian dollars unless otherwise noted.

CURRENCY HEDGES

USD foreign exchange forward contract: • $62.5MM @ 1.308 USD/CAD (value date May 2020)

$2.91 $3.02 $3.34 $3.34 $3.34 $3.34

0%

10%

20%

30%

40%

50%

60%

70%

Q3/16 Q4/16 Q1/17 Q2/17 Q3/17 Q4/17

% o

f tot

al fo

reca

st g

as v

olum

es

AECO Swap (C$/Mcf)

0%

10%

20%

30%

40%

50%

60%

70%

Q3/16 Q4/16

WTI MSW Basis Swap

% o

f oil

& c

ondi

vol

umes

hed

ged

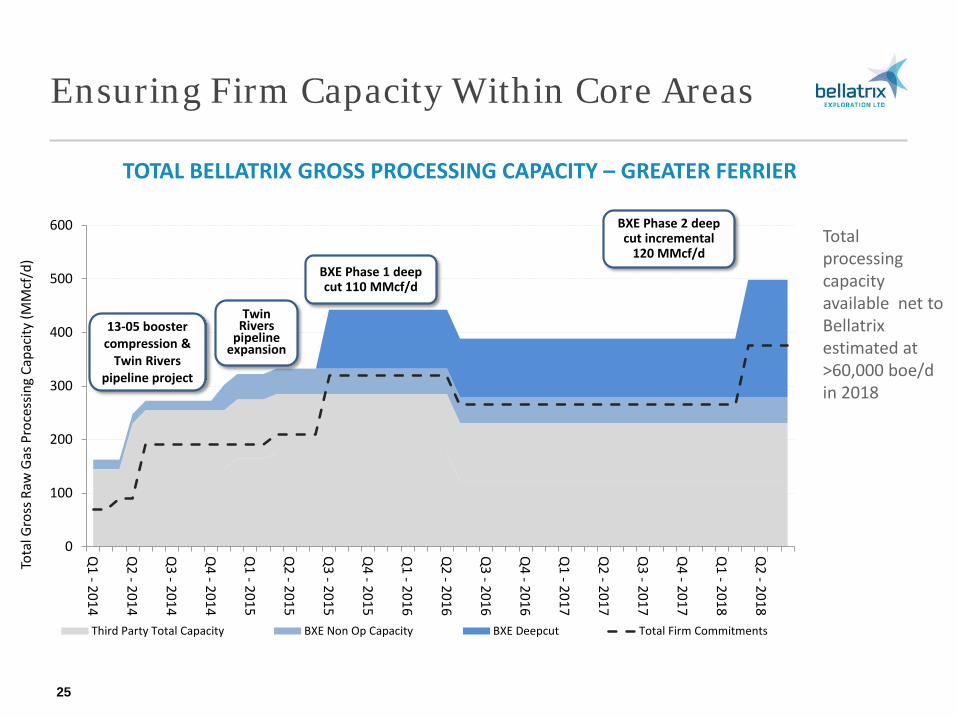

Ensuring Firm Capacity Within Core Areas

TOTAL BELLATRIX GROSS PROCESSING CAPACITY – GREATER FERRIER

25

Total processing capacity available net to Bellatrix estimated at >60,000 boe/d in 2018

0

100

200

300

400

500

600

Q1 - 2014

Q2 - 2014

Q3 - 2014

Q4 - 2014

Q1 - 2015

Q2 - 2015

Q3 - 2015

Q4 - 2015

Q1 - 2016

Q2 - 2016

Q3 - 2016

Q4 - 2016

Q1 - 2017

Q2 - 2017

Q3 - 2017

Q4 - 2017

Q1 - 2018

Q2 - 2018

Tota

l Gro

ss R

aw G

as P

roce

ssin

g Ca

paci

ty (M

Mcf

/d)

Third Party Total Capacity BXE Non Op Capacity BXE Deepcut Total Firm Commitments

13-05 booster compression &

Twin Rivers pipeline project

Twin Rivers

pipeline expansion

BXE Phase 1 deep cut 110 MMcf/d

BXE Phase 2 deep cut incremental

120 MMcf/d

Asset Overview

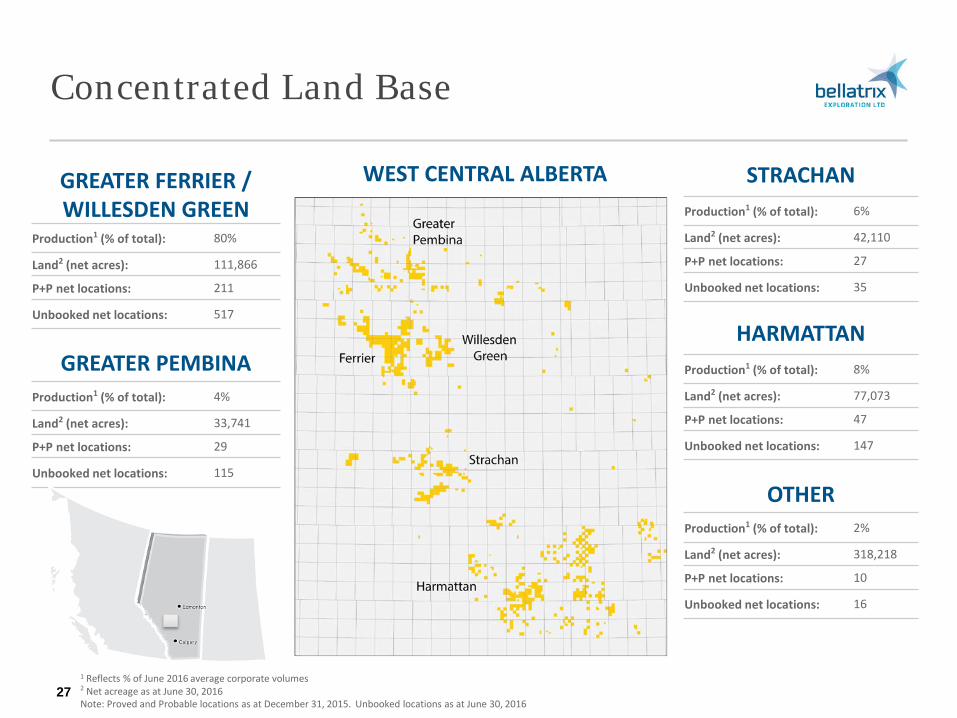

Concentrated Land Base

GREATER FERRIER / WILLESDEN GREEN

Production1 (% of total): 80%

Land2 (net acres): 111,866

P+P net locations: 211

Unbooked net locations: 517

GREATER PEMBINA Production1 (% of total): 4%

Land2 (net acres): 33,741

P+P net locations: 29

Unbooked net locations: 115

STRACHAN Production1 (% of total): 6%

Land2 (net acres): 42,110

P+P net locations: 27

Unbooked net locations: 35

HARMATTAN Production1 (% of total): 8%

Land2 (net acres): 77,073

P+P net locations: 47

Unbooked net locations: 147

OTHER Production1 (% of total): 2%

Land2 (net acres): 318,218

P+P net locations: 10

Unbooked net locations: 16

WEST CENTRAL ALBERTA

27 1 Reflects % of June 2016 average corporate volumes 2 Net acreage as at June 30, 2016 Note: Proved and Probable locations as at December 31, 2015. Unbooked locations as at June 30, 2016

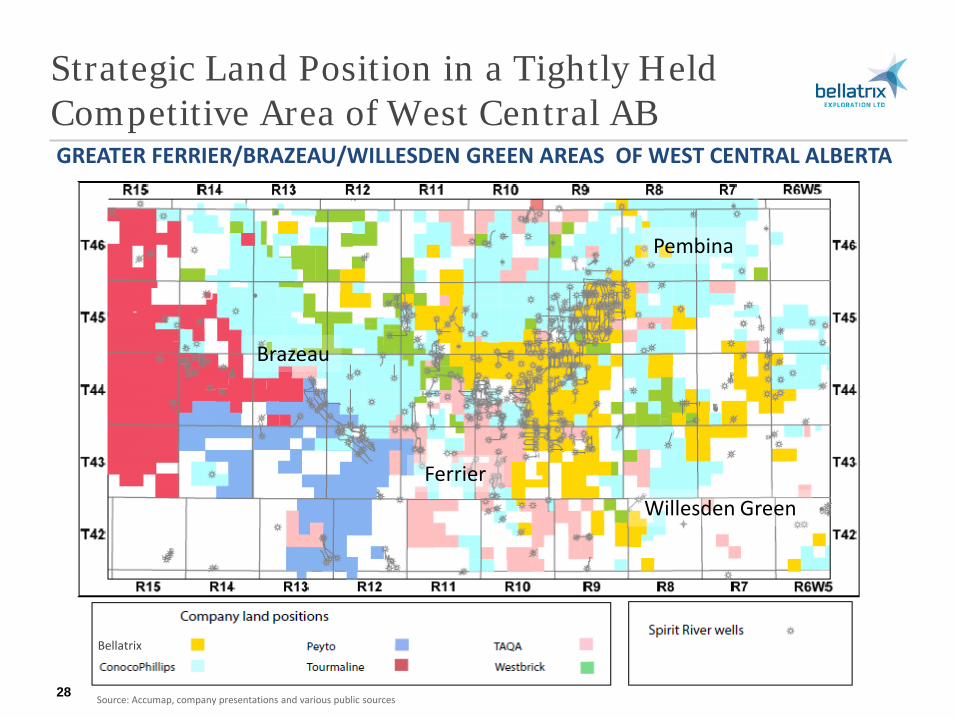

Strategic Land Position in a Tightly Held Competitive Area of West Central AB

28 Source: Accumap, company presentations and various public sources

GREATER FERRIER/BRAZEAU/WILLESDEN GREEN AREAS OF WEST CENTRAL ALBERTA

Brazeau

Ferrier

Pembina

Willesden Green

Bellatrix

Geology Overview

Geology Overview

30 Long term shareholder value creation

FOCUSED ASSET BASE IN AN ESTABLISHED AREA OF THE WESTERN CANADIAN SEDIMENTARY BASIN

MULTI-ZONE PROSPECTIVITY PROVIDES UPSIDE POTENTIAL

ACREAGE CONTAINS FAVORABLE GEOLOGIC CHARACTERISTICS

RIGOROUS & SYSTEMATIC APPROACH TO INVENTORY EVALUATION

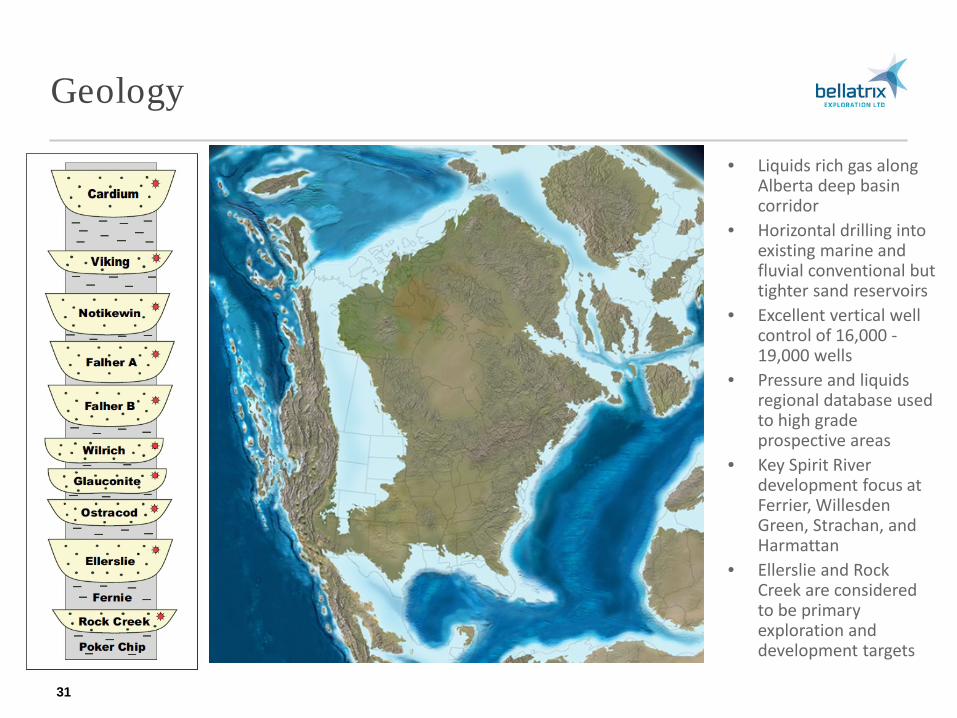

Geology

31

• Liquids rich gas along Alberta deep basin corridor

• Horizontal drilling into existing marine and fluvial conventional but tighter sand reservoirs

• Excellent vertical well control of 16,000 - 19,000 wells

• Pressure and liquids regional database used to high grade prospective areas

• Key Spirit River development focus at Ferrier, Willesden Green, Strachan, and Harmattan

• Ellerslie and Rock Creek are considered to be primary exploration and development targets

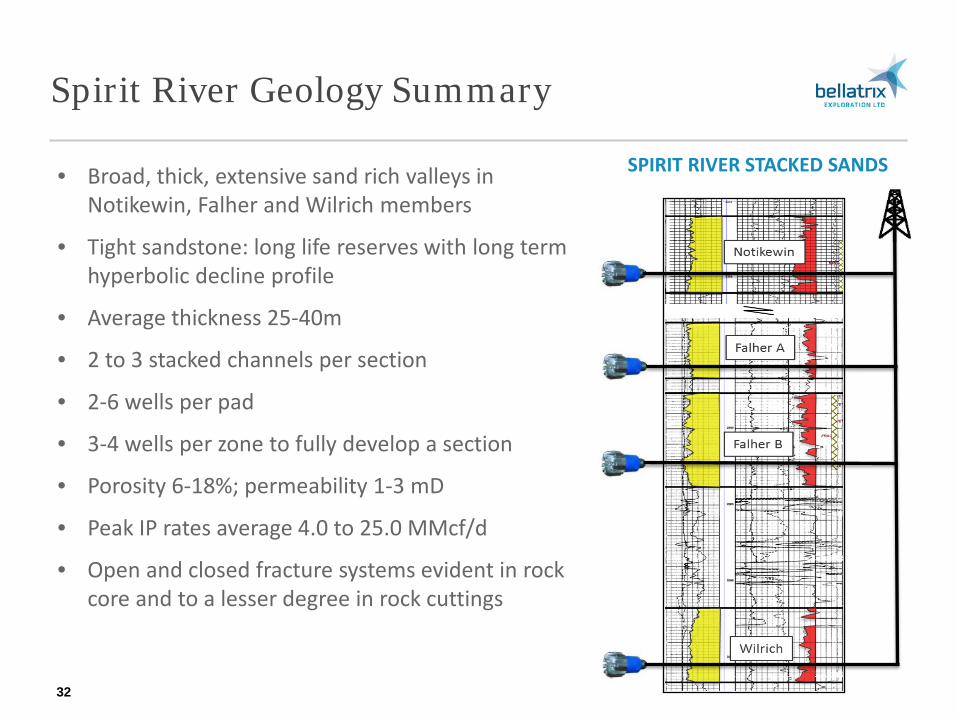

Spirit River Geology Summary

• Broad, thick, extensive sand rich valleys in Notikewin, Falher and Wilrich members

• Tight sandstone: long life reserves with long term hyperbolic decline profile

• Average thickness 25-40m

• 2 to 3 stacked channels per section

• 2-6 wells per pad

• 3-4 wells per zone to fully develop a section

• Porosity 6-18%; permeability 1-3 mD

• Peak IP rates average 4.0 to 25.0 MMcf/d

• Open and closed fracture systems evident in rock core and to a lesser degree in rock cuttings

32

SPIRIT RIVER STACKED SANDS

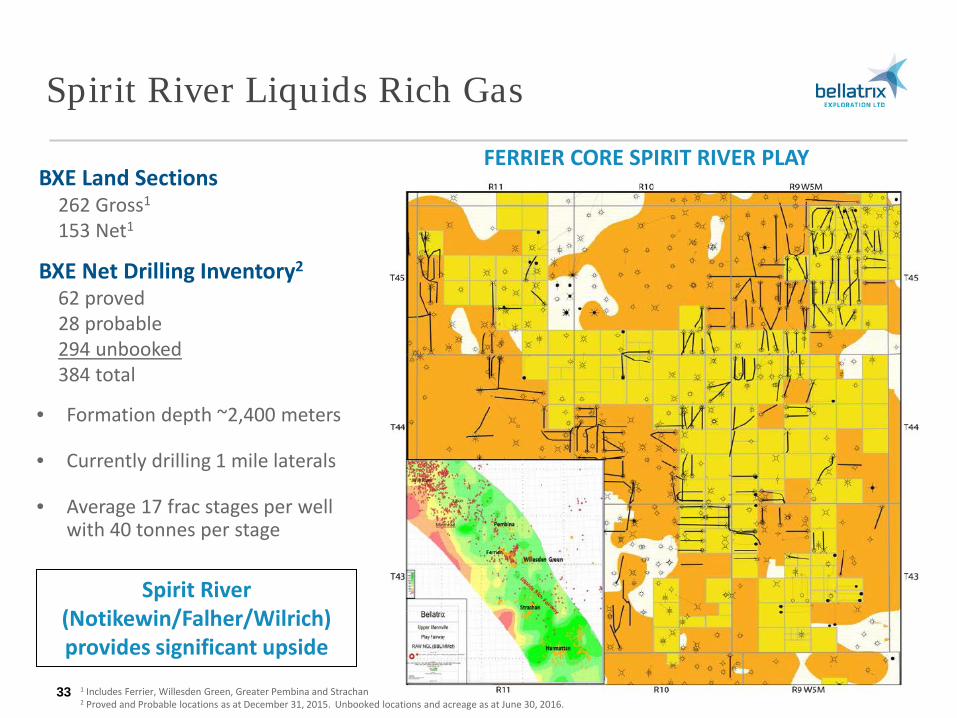

Spirit River Liquids Rich Gas

BXE Land Sections 262 Gross1

153 Net1

BXE Net Drilling Inventory2

62 proved 28 probable 294 unbooked 384 total

Spirit River (Notikewin/Falher/Wilrich) provides significant upside

1 Includes Ferrier, Willesden Green, Greater Pembina and Strachan 2 Proved and Probable locations as at December 31, 2015. Unbooked locations and acreage as at June 30, 2016.

33

FERRIER CORE SPIRIT RIVER PLAY

• Formation depth ~2,400 meters

• Currently drilling 1 mile laterals

• Average 17 frac stages per well with 40 tonnes per stage

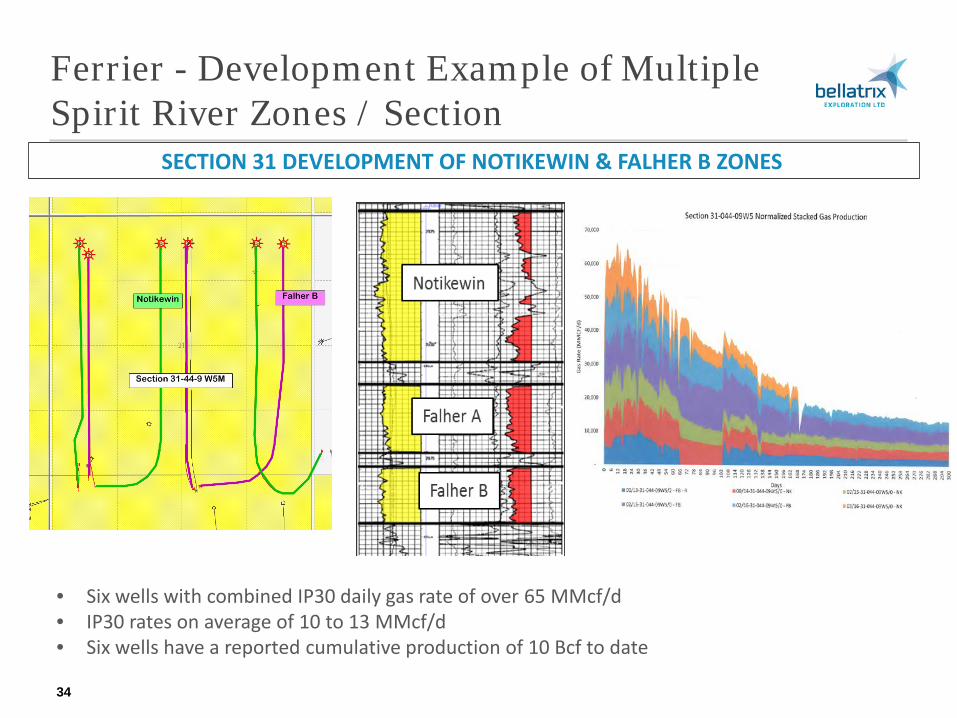

Ferrier - Development Example of Multiple Spirit River Zones / Section

34

• Six wells with combined IP30 daily gas rate of over 65 MMcf/d • IP30 rates on average of 10 to 13 MMcf/d • Six wells have a reported cumulative production of 10 Bcf to date

SECTION 31 DEVELOPMENT OF NOTIKEWIN & FALHER B ZONES

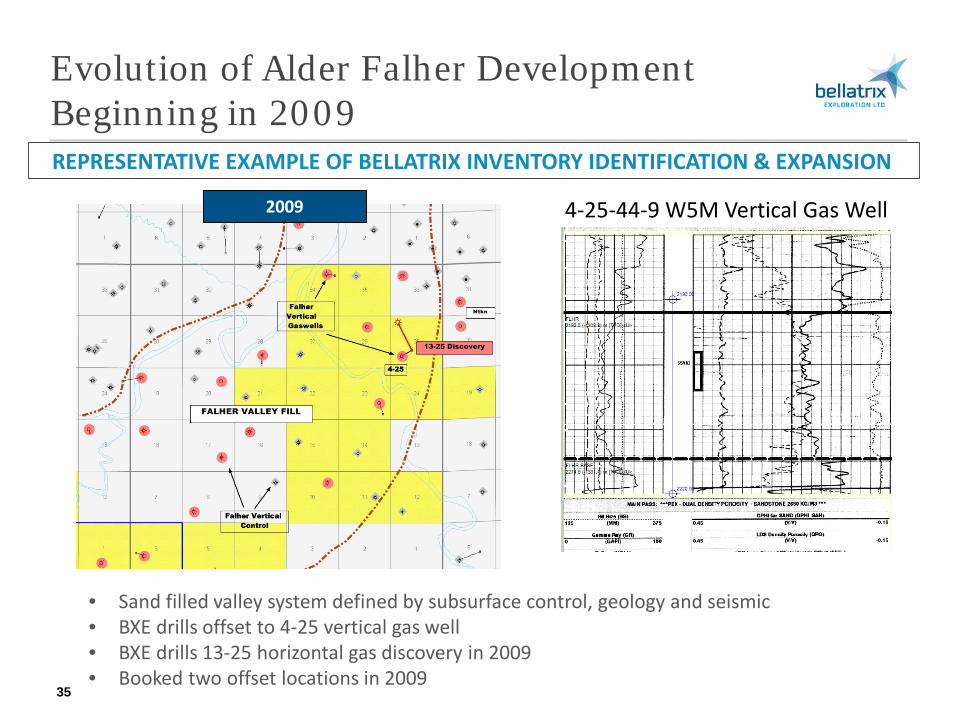

Evolution of Alder Falher Development Beginning in 2009

35

4-25-44-9 W5M Vertical Gas Well

• Sand filled valley system defined by subsurface control, geology and seismic • BXE drills offset to 4-25 vertical gas well • BXE drills 13-25 horizontal gas discovery in 2009 • Booked two offset locations in 2009

REPRESENTATIVE EXAMPLE OF BELLATRIX INVENTORY IDENTIFICATION & EXPANSION

2009

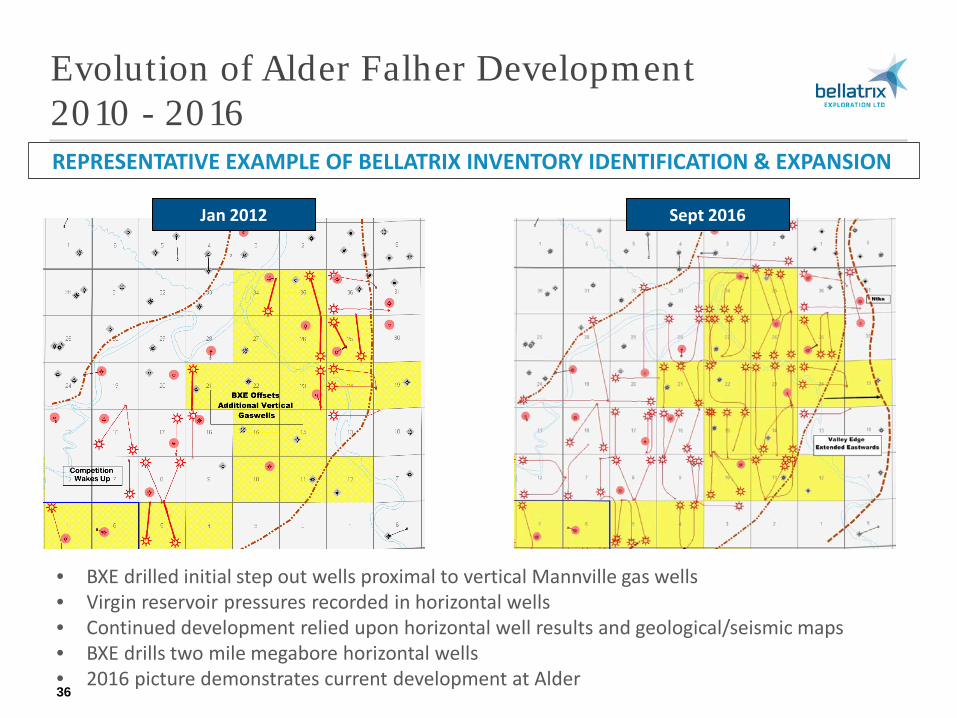

Evolution of Alder Falher Development 2010 - 2016

36

• BXE drilled initial step out wells proximal to vertical Mannville gas wells • Virgin reservoir pressures recorded in horizontal wells • Continued development relied upon horizontal well results and geological/seismic maps • BXE drills two mile megabore horizontal wells • 2016 picture demonstrates current development at Alder

REPRESENTATIVE EXAMPLE OF BELLATRIX INVENTORY IDENTIFICATION & EXPANSION

Jan 2012 Sept 2016

Operations Overview

Operations Overview

38 Long term shareholder value creation

CAPITAL COST SAVINGS INITIATIVES & ACHIEVEMENTS

PLANNING AND OPTIMIZATION

COST SAVINGS SUSTAINABILITY

EFFICIENCY GAINS

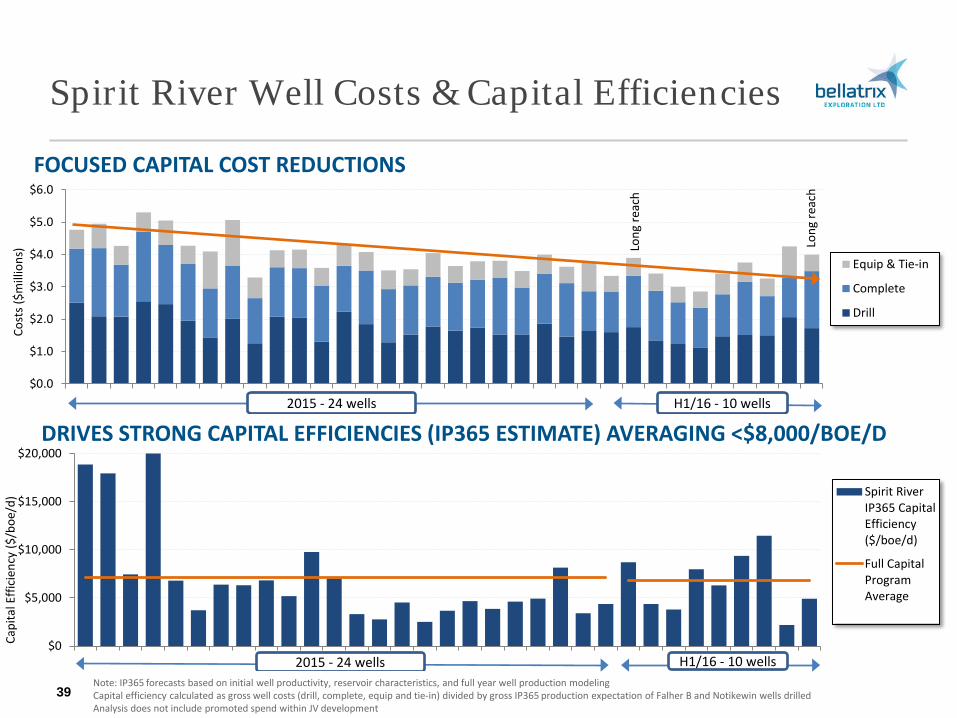

Spirit River Well Costs & Capital Efficiencies

39

FOCUSED CAPITAL COST REDUCTIONS

DRIVES STRONG CAPITAL EFFICIENCIES (IP365 ESTIMATE) AVERAGING <$8,000/BOE/D

Note: IP365 forecasts based on initial well productivity, reservoir characteristics, and full year well production modeling Capital efficiency calculated as gross well costs (drill, complete, equip and tie-in) divided by gross IP365 production expectation of Falher B and Notikewin wells drilled Analysis does not include promoted spend within JV development

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

Cost

s ($m

illio

ns)

Equip & Tie-in

Complete

Drill

2015 - 24 wells H1/16 - 10 wells

Long

reac

h

Long

reac

h

$0

$5,000

$10,000

$15,000

$20,000

Capi

tal E

ffici

ency

($/b

oe/d

) Spirit RiverIP365 CapitalEfficiency($/boe/d)

Full CapitalProgramAverage

2015 - 24 wells H1/16 - 10 wells

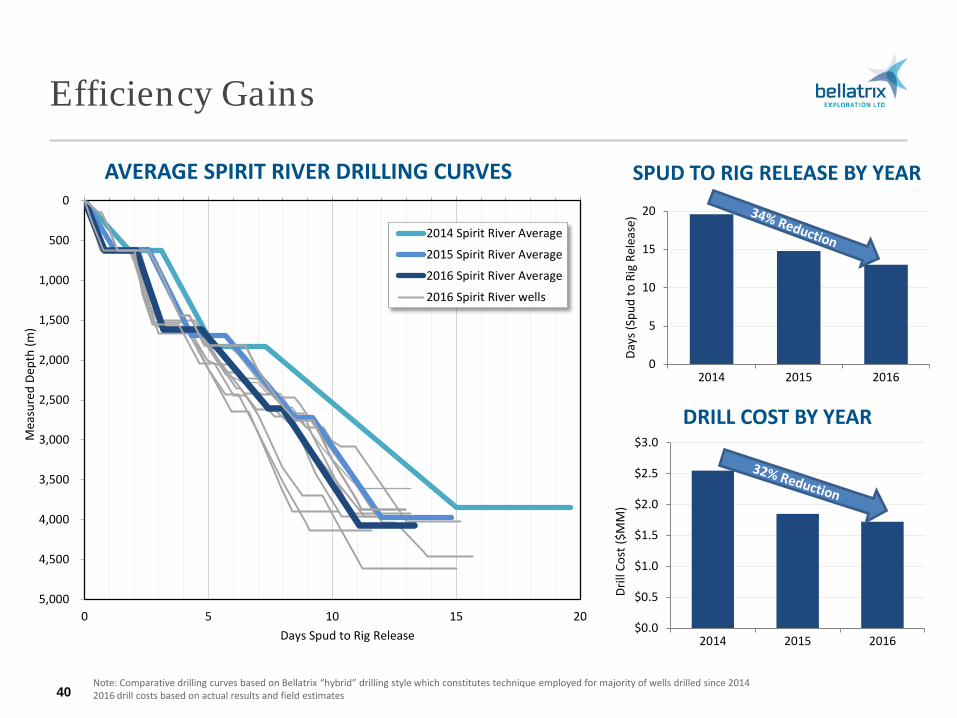

Efficiency Gains

40

AVERAGE SPIRIT RIVER DRILLING CURVES SPUD TO RIG RELEASE BY YEAR

Note: Comparative drilling curves based on Bellatrix “hybrid” drilling style which constitutes technique employed for majority of wells drilled since 2014 2016 drill costs based on actual results and field estimates

0

5

10

15

20

2014 2015 2016

Days

(Spu

d to

Rig

Rel

ease

)

DRILL COST BY YEAR

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

2014 2015 2016Dr

ill C

ost (

$MM

)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,0000 5 10 15 20

Mea

sure

d De

pth

(m)

Days Spud to Rig Release

2014 Spirit River Average

2015 Spirit River Average

2016 Spirit River Average

2016 Spirit River wells

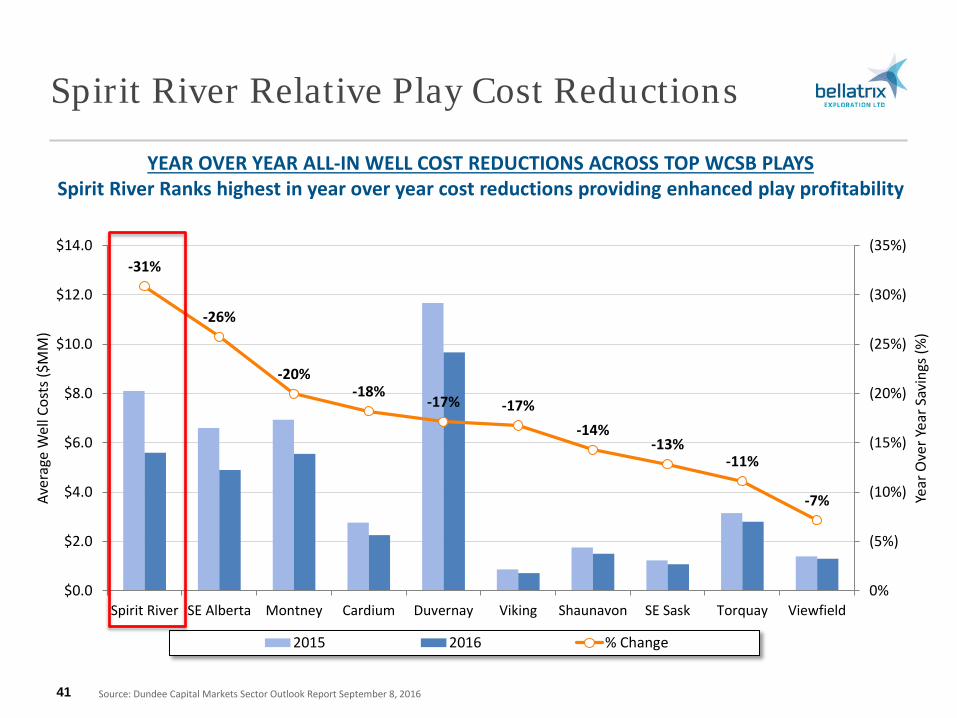

Spirit River Relative Play Cost Reductions

41

-31%

-26%

-20% -18%

-17% -17% -14%

-13% -11%

-7%

(35%)

(30%)

(25%)

(20%)

(15%)

(10%)

(5%)

0%$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

Spirit River SE Alberta Montney Cardium Duvernay Viking Shaunavon SE Sask Torquay Viewfield

Year

Ove

r Yea

r Sav

ings

(%)

Aver

age

Wel

l Cos

ts ($

MM

)

2015 2016 % Change

Source: Dundee Capital Markets Sector Outlook Report September 8, 2016

YEAR OVER YEAR ALL-IN WELL COST REDUCTIONS ACROSS TOP WCSB PLAYS Spirit River Ranks highest in year over year cost reductions providing enhanced play profitability

Capital Cost Reductions

42

• Review and optimize how surface hole is drilled

• Review and optimize bottom hole assembly

• Review and optimize well design

COST REDUCTIONS AND MAINTENANCE OF A LOW COST PROFILE IS ALL ABOUT “REVIEWING & OPTIMIZING”

REVIEW OPTIMIZE REPEAT

• Re-engineered the use of high performance motors

• Reamer run while drilling

• The use of the same equipment and people for improved consistency of results

• Continuous bidding practices ensure best price available

• Working closely with vendors on optimizing operations

• Better communication with respect to concurrent operations reduces downtime, increases field efficiency and optimizes resources

• New bit designs have demonstrated significant improvements

• Three record runs on three different wells

Improvement & Optimization Efforts

43

TANGIBLE BENEFITS ACHIEVED ACROSS MULTIPLE AREAS

TIMING IS A LARGE COMPONENT OF COST & OPTIMIZATION

TESTING AND IMPLEMENTING NEW EQUIPMENT RECORD RUN

RECORD RUN

RECORD RUN

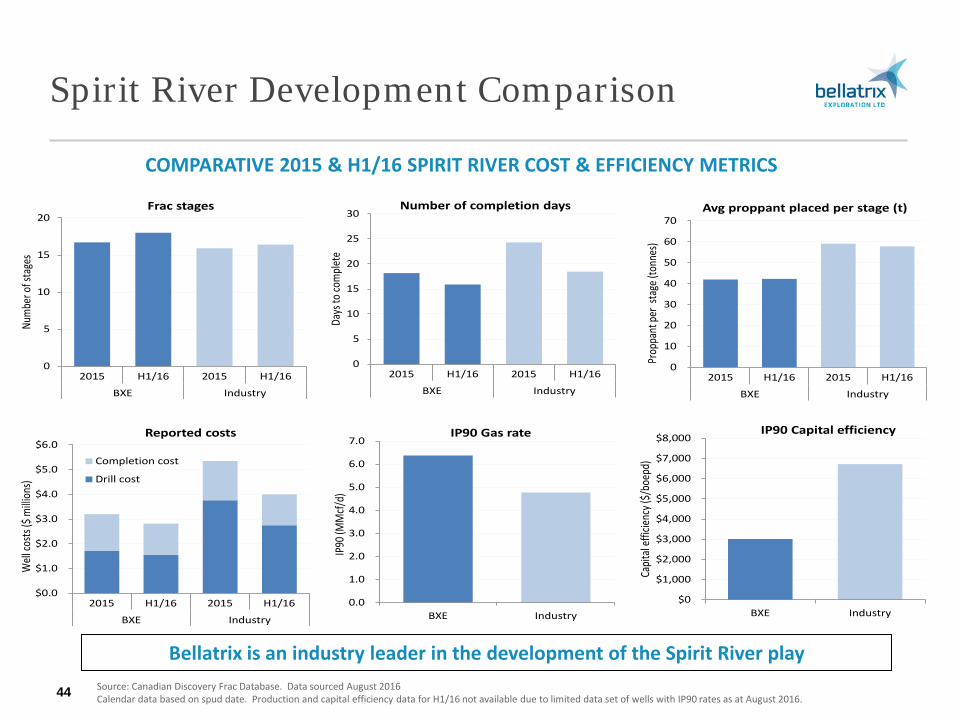

Spirit River Development Comparison

44 Source: Canadian Discovery Frac Database. Data sourced August 2016 Calendar data based on spud date. Production and capital efficiency data for H1/16 not available due to limited data set of wells with IP90 rates as at August 2016.

COMPARATIVE 2015 & H1/16 SPIRIT RIVER COST & EFFICIENCY METRICS

Bellatrix is an industry leader in the development of the Spirit River play

0

5

10

15

20

2015 H1/16 2015 H1/16

BXE Industry

Num

ber o

f sta

ges

Frac stages

0

5

10

15

20

25

30

2015 H1/16 2015 H1/16

BXE Industry

Days

to co

mple

te

Number of completion days

0

10

20

30

40

50

60

70

2015 H1/16 2015 H1/16

BXE Industry

Prop

pant

per

stage

(ton

nes)

Avg proppant placed per stage (t)

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

2015 H1/16 2015 H1/16

BXE Industry

Well

costs

($ m

illion

s)

Reported costs

Completion cost

Drill cost

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

BXE Industry

IP90

(MM

cf/d)

IP90 Gas rate

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

BXE Industry

Capit

al ef

ficien

cy ($

/boe

pd)

IP90 Capital efficiency

Engineering Overview

Engineering Overview

46 Long term shareholder value creation

SPIRIT RIVER PLAY PROFITABILITY

ENGINEERING VALUE

PLAY PERFORMANCE

DEPTH OF INVENTORY

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

Jan

10Ap

r 10

Jul 1

0O

ct 1

0Ja

n 11

Apr 1

1Ju

l 11

Oct

11

Jan

12Ap

r 12

Jul 1

2O

ct 1

2Ja

n 13

Apr 1

3Ju

l 13

Oct

13

Jan

14Ap

r 14

Jul 1

4O

ct 1

4Ja

n 15

Apr 1

5Ju

l 15

Oct

15

Jan

16Ap

r 16

Aver

age

mon

thly

pro

duct

ion

(boe

/d)

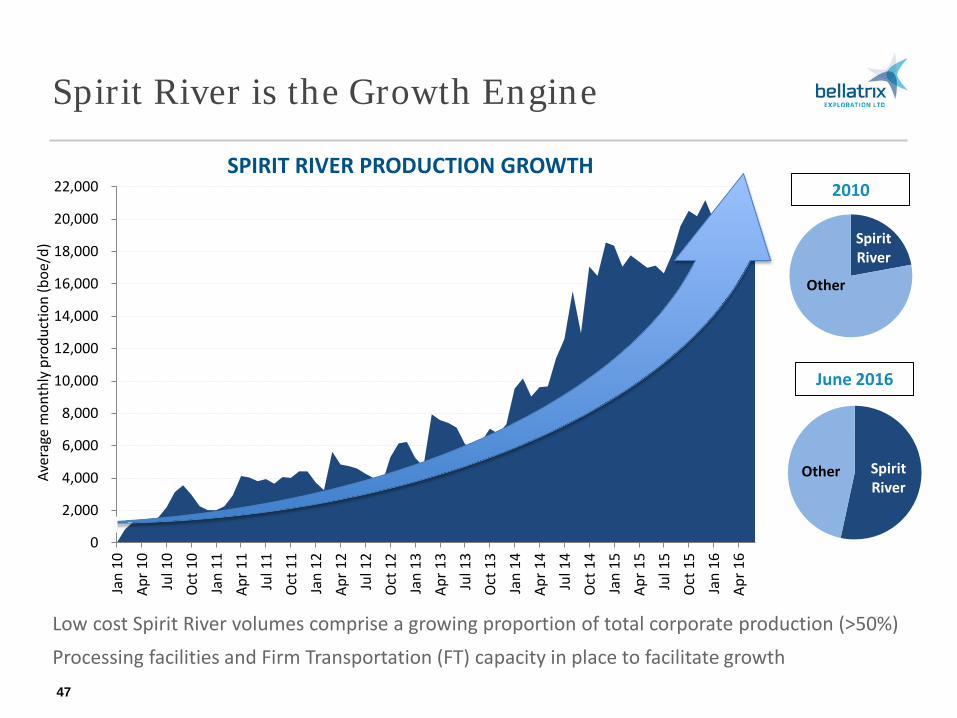

Spirit River is the Growth Engine

47

Low cost Spirit River volumes comprise a growing proportion of total corporate production (>50%) Processing facilities and Firm Transportation (FT) capacity in place to facilitate growth

SPIRIT RIVER PRODUCTION GROWTH 2010

June 2016

Spirit River

Other

Spirit River

Other

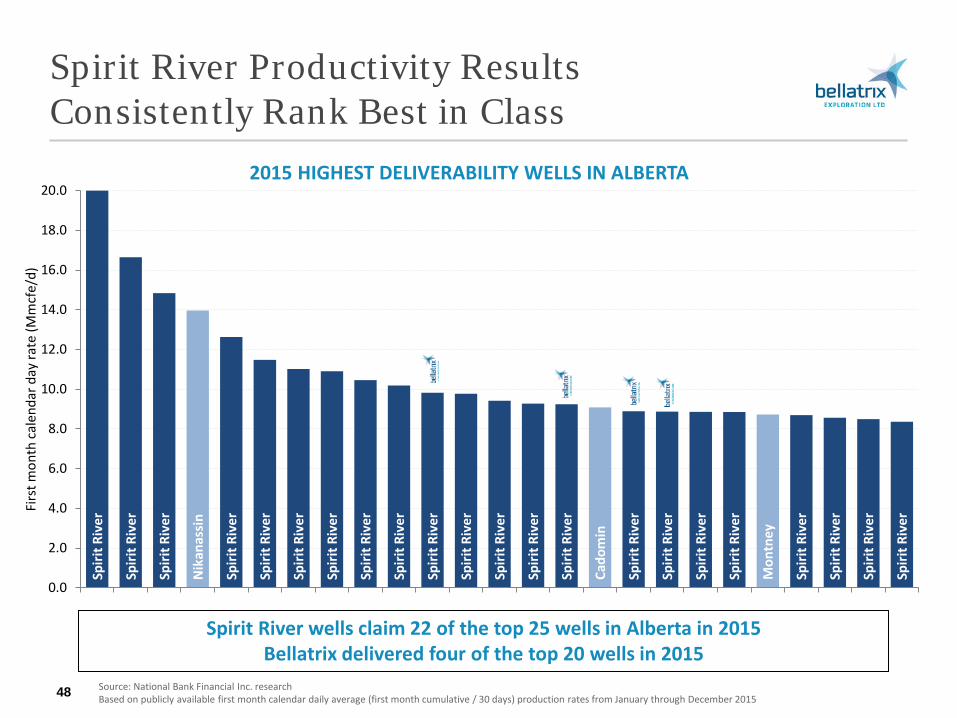

Spirit River Productivity Results Consistently Rank Best in Class

48 Source: National Bank Financial Inc. research Based on publicly available first month calendar daily average (first month cumulative / 30 days) production rates from January through December 2015

2015 HIGHEST DELIVERABILITY WELLS IN ALBERTA

Spirit River wells claim 22 of the top 25 wells in Alberta in 2015 Bellatrix delivered four of the top 20 wells in 2015

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Nik

anas

sin

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Cado

min

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Mon

tney

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

Spiri

t Riv

er

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Firs

t mon

th c

alen

dar d

ay ra

te (M

mcf

e/d)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

Henr

y Hu

b (U

S$/M

Mbt

u)

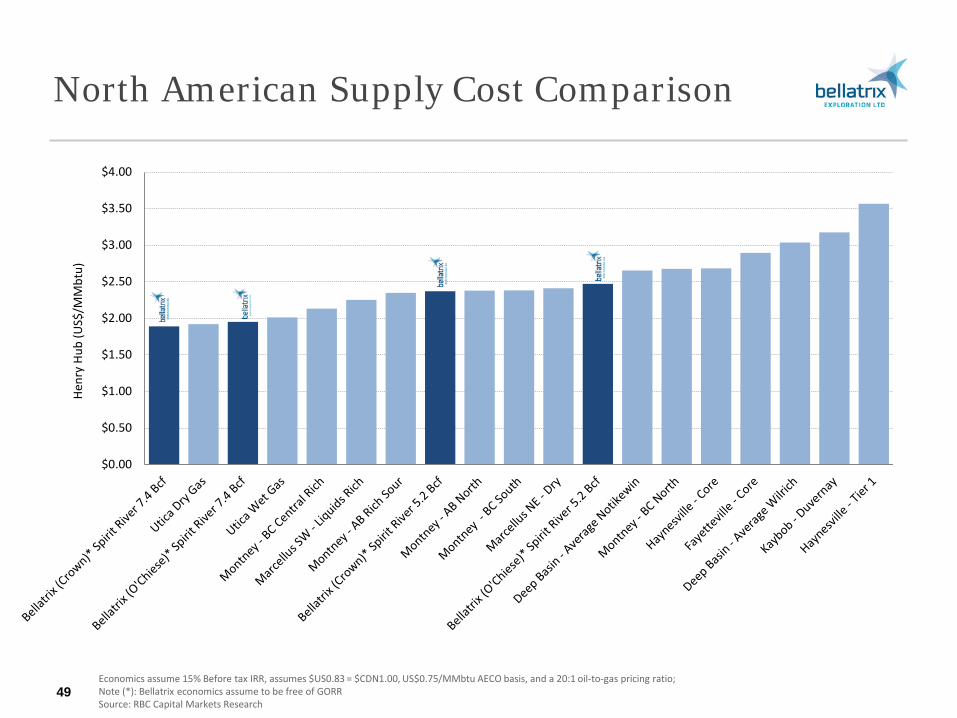

North American Supply Cost Comparison

49 Economics assume 15% Before tax IRR, assumes $US0.83 = $CDN1.00, US$0.75/MMbtu AECO basis, and a 20:1 oil-to-gas pricing ratio; Note (*): Bellatrix economics assume to be free of GORR Source: RBC Capital Markets Research

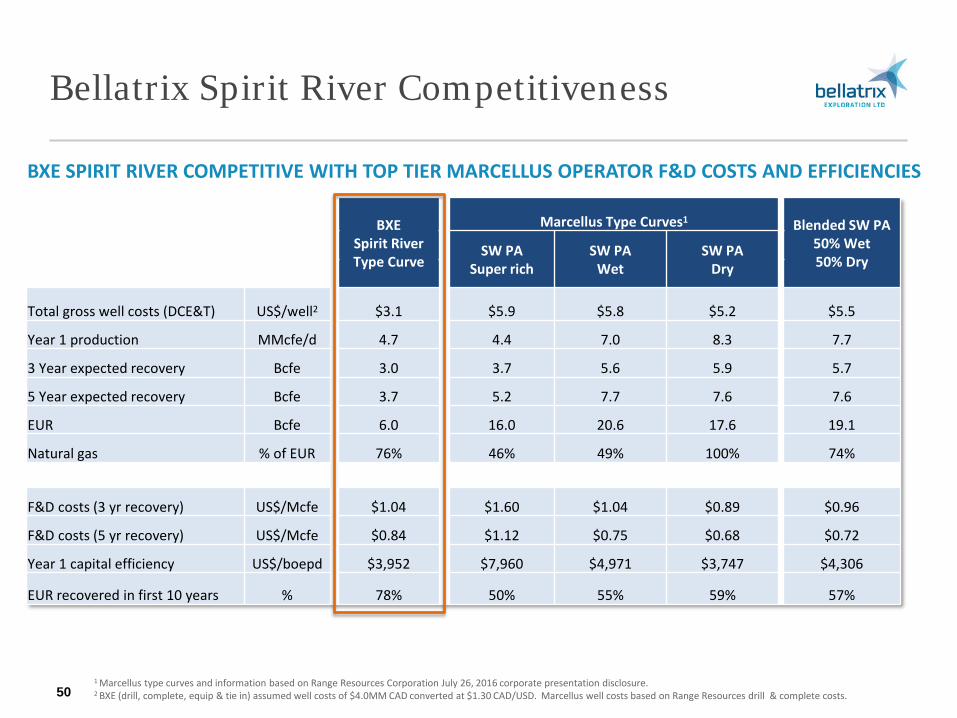

Bellatrix Spirit River Competitiveness

50 1 Marcellus type curves and information based on Range Resources Corporation July 26, 2016 corporate presentation disclosure. 2 BXE (drill, complete, equip & tie in) assumed well costs of $4.0MM CAD converted at $1.30 CAD/USD. Marcellus well costs based on Range Resources drill & complete costs.

BXE SPIRIT RIVER COMPETITIVE WITH TOP TIER MARCELLUS OPERATOR F&D COSTS AND EFFICIENCIES

BXE Spirit River Type Curve

Marcellus Type Curves1 Blended SW PA 50% Wet 50% Dry

SW PA Super rich

SW PA Wet

SW PA Dry

Total gross well costs (DCE&T) US$/well2 $3.1 $5.9 $5.8 $5.2 $5.5

Year 1 production MMcfe/d 4.7 4.4 7.0 8.3 7.7

3 Year expected recovery Bcfe 3.0 3.7 5.6 5.9 5.7

5 Year expected recovery Bcfe 3.7 5.2 7.7 7.6 7.6

EUR Bcfe 6.0 16.0 20.6 17.6 19.1

Natural gas % of EUR 76% 46% 49% 100% 74%

F&D costs (3 yr recovery) US$/Mcfe $1.04 $1.60 $1.04 $0.89 $0.96

F&D costs (5 yr recovery) US$/Mcfe $0.84 $1.12 $0.75 $0.68 $0.72

Year 1 capital efficiency US$/boepd $3,952 $7,960 $4,971 $3,747 $4,306

EUR recovered in first 10 years % 78% 50% 55% 59% 57%

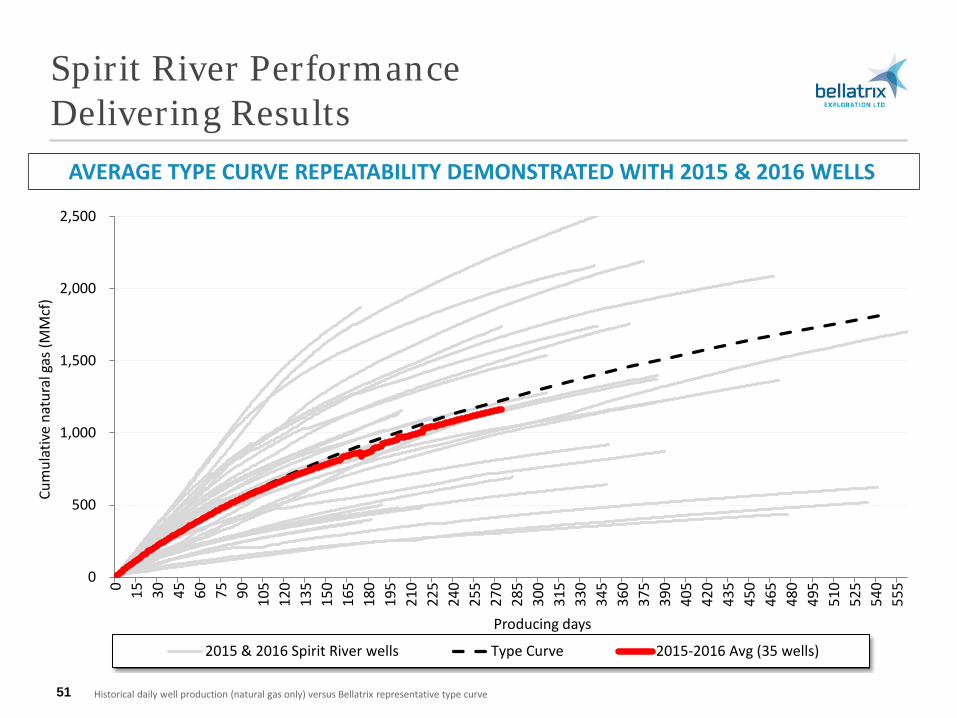

Spirit River Performance Delivering Results

51

0

500

1,000

1,500

2,000

2,500

0 15 30 45 60 75 90 105

120

135

150

165

180

195

210

225

240

255

270

285

300

315

330

345

360

375

390

405

420

435

450

465

480

495

510

525

540

555

Cum

ulat

ive

natu

ral g

as (M

Mcf

)

Producing days

2015 & 2016 Spirit River wells Type Curve 2015-2016 Avg (35 wells)

Historical daily well production (natural gas only) versus Bellatrix representative type curve

AVERAGE TYPE CURVE REPEATABILITY DEMONSTRATED WITH 2015 & 2016 WELLS

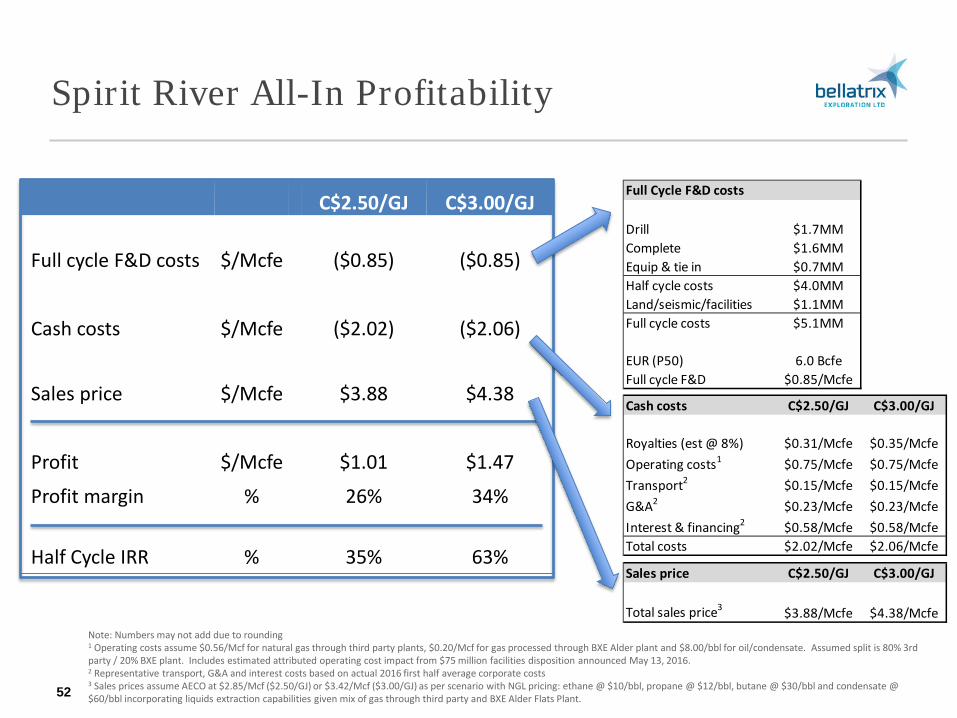

C$2.50/GJ C$3.00/GJ

Full cycle F&D costs $/Mcfe ($0.85) ($0.85)

Cash costs $/Mcfe ($2.02) ($2.06)

Sales price $/Mcfe $3.88 $4.38

Profit $/Mcfe $1.01 $1.47

Profit margin % 26% 34%

Half Cycle IRR % 35% 63%

Spirit River All-In Profitability

52

Note: Numbers may not add due to rounding 1 Operating costs assume $0.56/Mcf for natural gas through third party plants, $0.20/Mcf for gas processed through BXE Alder plant and $8.00/bbl for oil/condensate. Assumed split is 80% 3rd party / 20% BXE plant. Includes estimated attributed operating cost impact from $75 million facilities disposition announced May 13, 2016. 2 Representative transport, G&A and interest costs based on actual 2016 first half average corporate costs 3 Sales prices assume AECO at $2.85/Mcf ($2.50/GJ) or $3.42/Mcf ($3.00/GJ) as per scenario with NGL pricing: ethane @ $10/bbl, propane @ $12/bbl, butane @ $30/bbl and condensate @ $60/bbl incorporating liquids extraction capabilities given mix of gas through third party and BXE Alder Flats Plant.

Full Cycle F&D costs

Drill $1.7MMComplete $1.6MMEquip & tie in $0.7MMHalf cycle costs $4.0MMLand/seismic/facilities $1.1MMFull cycle costs $5.1MM

EUR (P50) 6.0 BcfeFull cycle F&D $0.85/Mcfe

Cash costs C$2.50/GJ C$3.00/GJ

Royalties (est @ 8%) $0.31/Mcfe $0.35/McfeOperating costs1 $0.75/Mcfe $0.75/McfeTransport2 $0.15/Mcfe $0.15/McfeG&A2 $0.23/Mcfe $0.23/McfeInterest & financing2 $0.58/Mcfe $0.58/McfeTotal costs $2.02/Mcfe $2.06/Mcfe

Sales price C$2.50/GJ C$3.00/GJ

Total sales price3 $3.88/Mcfe $4.38/Mcfe

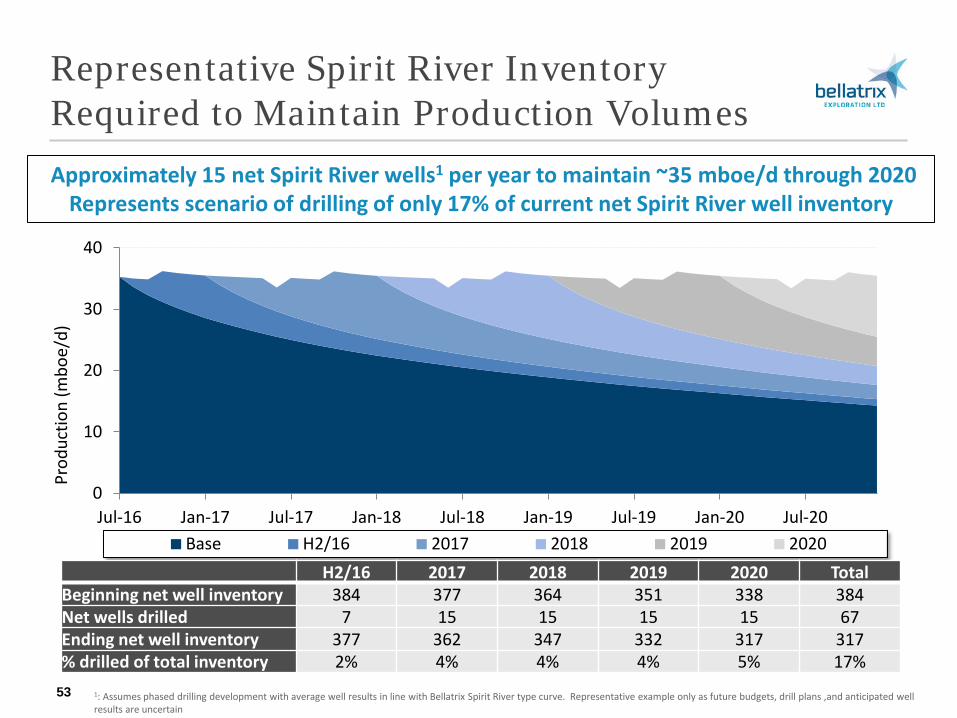

Representative Spirit River Inventory Required to Maintain Production Volumes

53

0

10

20

30

40

Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20 Jul-20

Prod

uctio

n (m

boe/

d)

Base H2/16 2017 2018 2019 2020

Approximately 15 net Spirit River wells1 per year to maintain ~35 mboe/d through 2020 Represents scenario of drilling of only 17% of current net Spirit River well inventory

H2/16 2017 2018 2019 2020 Total Beginning net well inventory 384 377 364 351 338 384 Net wells drilled 7 15 15 15 15 67 Ending net well inventory 377 362 347 332 317 317 % drilled of total inventory 2% 4% 4% 4% 5% 17%

1: Assumes phased drilling development with average well results in line with Bellatrix Spirit River type curve. Representative example only as future budgets, drill plans ,and anticipated well results are uncertain

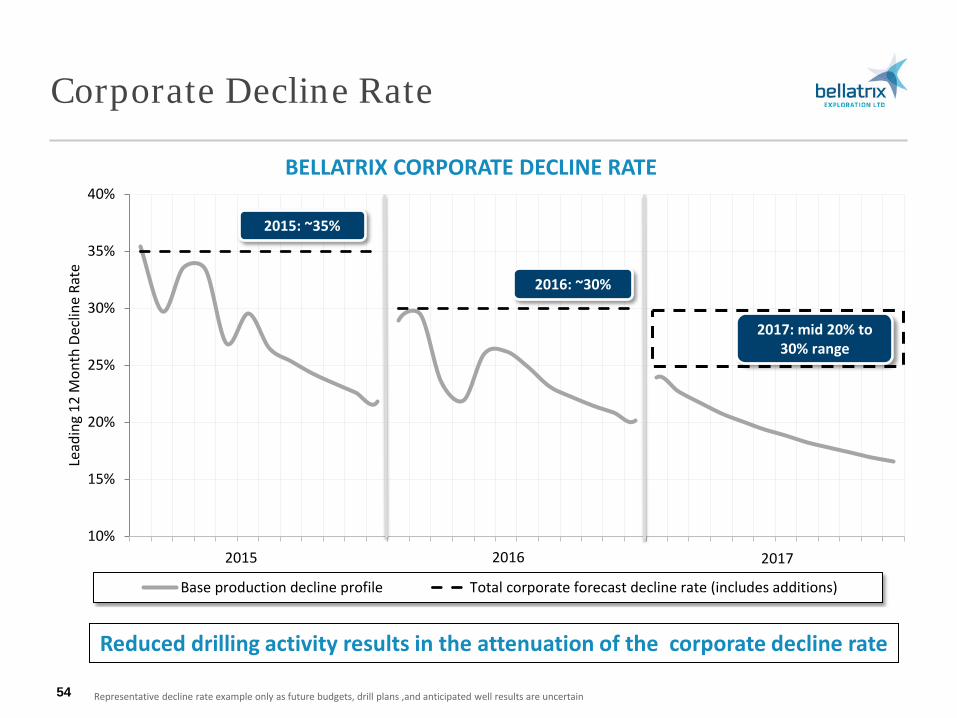

Corporate Decline Rate

54

BELLATRIX CORPORATE DECLINE RATE

Reduced drilling activity results in the attenuation of the corporate decline rate

10%

15%

20%

25%

30%

35%

40%

Lead

ing

12 M

onth

Dec

line

Rate

Base production decline profile Total corporate forecast decline rate (includes additions)

2015: ~35%

2015 2016 2017

2016: ~30%

2017: mid 20% to 30% range

Representative decline rate example only as future budgets, drill plans ,and anticipated well results are uncertain

Production Facilities & Optimization Overview

Production Overview

56 Long term shareholder value creation

STRATEGIC FACILITIES OVERVIEW

BENEFITS OF IN-HOUSE REVIEW & ANALYSIS

FACILITIES INVESTMENT AND IMBEDDED VALUE

OPTIMIZATION EFFORTS & ACHIEVEMENTS

Greater Ferrier Area Infrastructure Overview

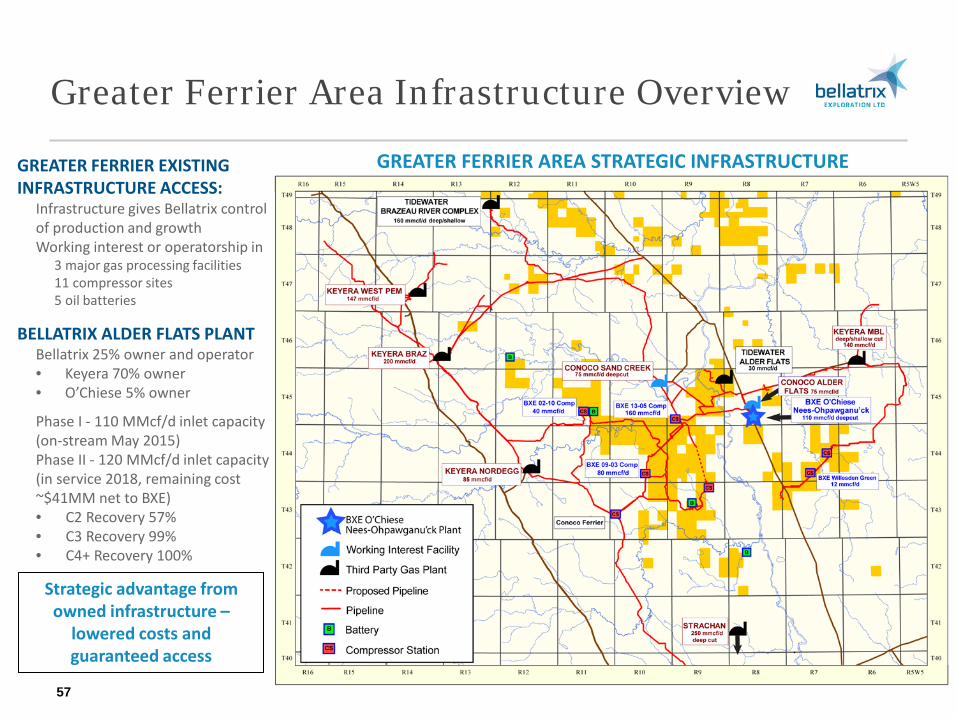

GREATER FERRIER EXISTING INFRASTRUCTURE ACCESS:

Infrastructure gives Bellatrix control of production and growth Working interest or operatorship in

3 major gas processing facilities 11 compressor sites 5 oil batteries

BELLATRIX ALDER FLATS PLANT Bellatrix 25% owner and operator • Keyera 70% owner • O’Chiese 5% owner

Phase I - 110 MMcf/d inlet capacity (on-stream May 2015) Phase II - 120 MMcf/d inlet capacity (in service 2018, remaining cost ~$41MM net to BXE) • C2 Recovery 57% • C3 Recovery 99% • C4+ Recovery 100%

Strategic advantage from owned infrastructure –

lowered costs and guaranteed access

57

GREATER FERRIER AREA STRATEGIC INFRASTRUCTURE

Significant Investment in Strategic Infrastructure

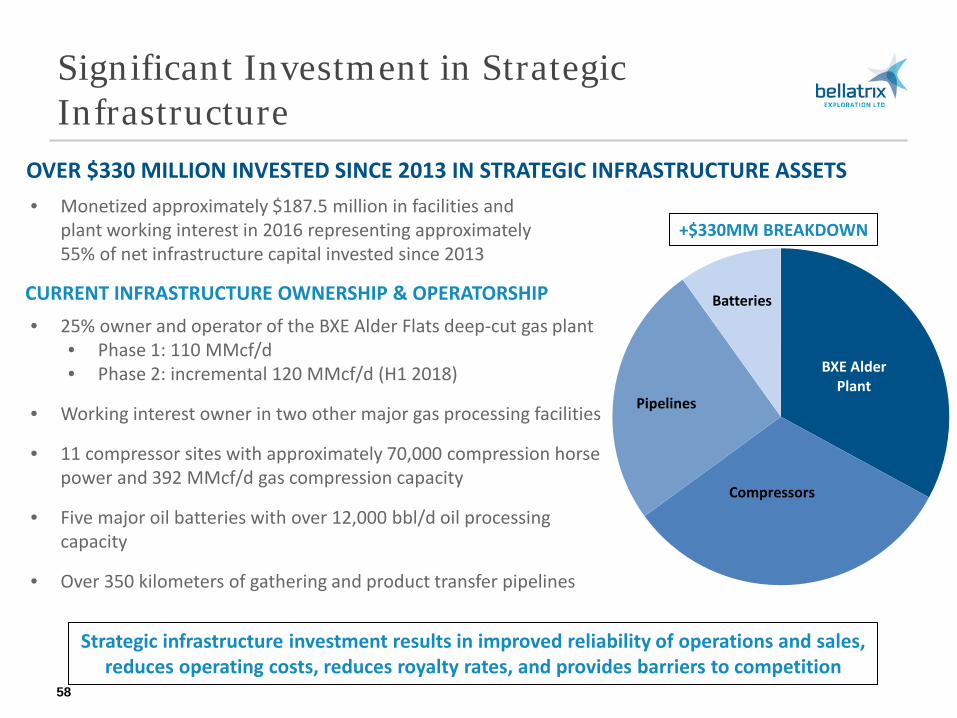

OVER $330 MILLION INVESTED SINCE 2013 IN STRATEGIC INFRASTRUCTURE ASSETS

58

• Monetized approximately $187.5 million in facilities and plant working interest in 2016 representing approximately 55% of net infrastructure capital invested since 2013

+$330MM BREAKDOWN

Strategic infrastructure investment results in improved reliability of operations and sales, reduces operating costs, reduces royalty rates, and provides barriers to competition

BXE Alder Plant

Pipelines

Batteries

Compressors

CURRENT INFRASTRUCTURE OWNERSHIP & OPERATORSHIP

• 25% owner and operator of the BXE Alder Flats deep-cut gas plant • Phase 1: 110 MMcf/d • Phase 2: incremental 120 MMcf/d (H1 2018)

• Working interest owner in two other major gas processing facilities

• 11 compressor sites with approximately 70,000 compression horse power and 392 MMcf/d gas compression capacity

• Five major oil batteries with over 12,000 bbl/d oil processing capacity

• Over 350 kilometers of gathering and product transfer pipelines

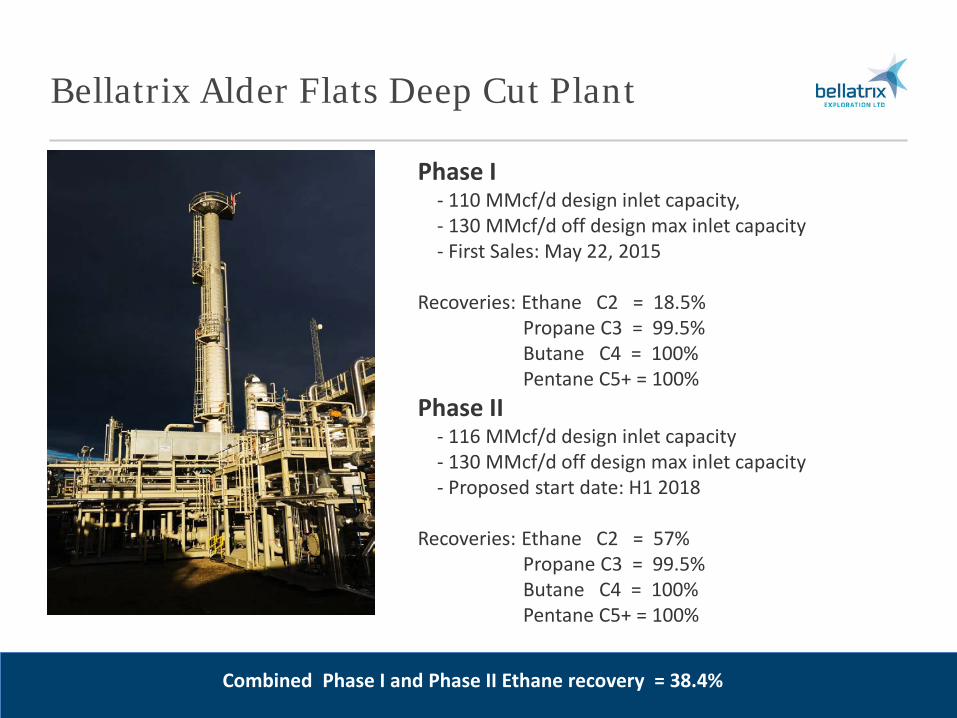

Bellatrix Alder Flats Deep Cut Plant

59

Bellatrix Alder Flats Deep Cut Plant

60

Phase I - 110 MMcf/d design inlet capacity, - 130 MMcf/d off design max inlet capacity - First Sales: May 22, 2015 Recoveries: Ethane C2 = 18.5% Propane C3 = 99.5% Butane C4 = 100% Pentane C5+ = 100% Phase II - 116 MMcf/d design inlet capacity - 130 MMcf/d off design max inlet capacity - Proposed start date: H1 2018 Recoveries: Ethane C2 = 57% Propane C3 = 99.5% Butane C4 = 100% Pentane C5+ = 100%

Combined Phase I and Phase II Ethane recovery = 38.4%

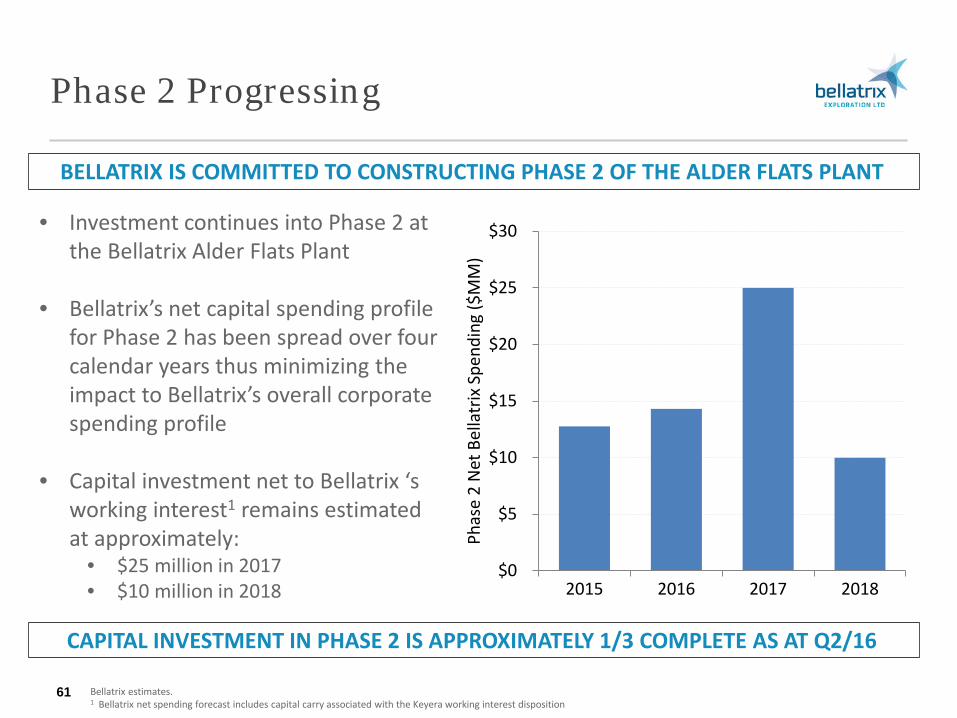

Phase 2 Progressing

61

BELLATRIX IS COMMITTED TO CONSTRUCTING PHASE 2 OF THE ALDER FLATS PLANT

• Investment continues into Phase 2 at the Bellatrix Alder Flats Plant

• Bellatrix’s net capital spending profile for Phase 2 has been spread over four calendar years thus minimizing the impact to Bellatrix’s overall corporate spending profile

• Capital investment net to Bellatrix ‘s working interest1 remains estimated at approximately:

• $25 million in 2017 • $10 million in 2018

$0

$5

$10

$15

$20

$25

$30

2015 2016 2017 2018

Phas

e 2

Net

Bel

latr

ix S

pend

ing

($M

M)

CAPITAL INVESTMENT IN PHASE 2 IS APPROXIMATELY 1/3 COMPLETE AS AT Q2/16

Bellatrix estimates. 1 Bellatrix net spending forecast includes capital carry associated with the Keyera working interest disposition

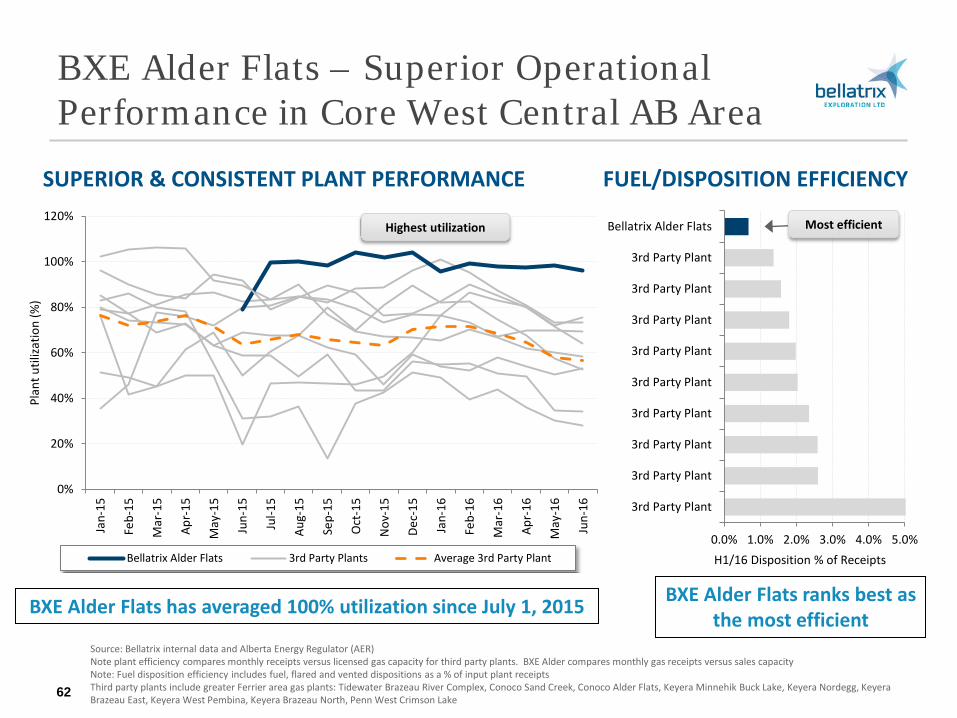

BXE Alder Flats – Superior Operational Performance in Core West Central AB Area

SUPERIOR & CONSISTENT PLANT PERFORMANCE

62

BXE Alder Flats ranks best as the most efficient

FUEL/DISPOSITION EFFICIENCY

Source: Bellatrix internal data and Alberta Energy Regulator (AER) Note plant efficiency compares monthly receipts versus licensed gas capacity for third party plants. BXE Alder compares monthly gas receipts versus sales capacity Note: Fuel disposition efficiency includes fuel, flared and vented dispositions as a % of input plant receipts Third party plants include greater Ferrier area gas plants: Tidewater Brazeau River Complex, Conoco Sand Creek, Conoco Alder Flats, Keyera Minnehik Buck Lake, Keyera Nordegg, Keyera Brazeau East, Keyera West Pembina, Keyera Brazeau North, Penn West Crimson Lake

BXE Alder Flats has averaged 100% utilization since July 1, 2015

0.0% 1.0% 2.0% 3.0% 4.0% 5.0%

3rd Party Plant

3rd Party Plant

3rd Party Plant

3rd Party Plant

3rd Party Plant

3rd Party Plant

3rd Party Plant

3rd Party Plant

3rd Party Plant

Bellatrix Alder Flats

H1/16 Disposition % of Receipts

Most efficient

0%

20%

40%

60%

80%

100%

120%

Jan-

15

Feb-

15

Mar

-15

Apr-

15

May

-15

Jun-

15

Jul-1

5

Aug-

15

Sep-

15

Oct

-15

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-

16

May

-16

Jun-

16

Plan

t util

izatio

n (%

)

Bellatrix Alder Flats 3rd Party Plants Average 3rd Party Plant

Highest utilization

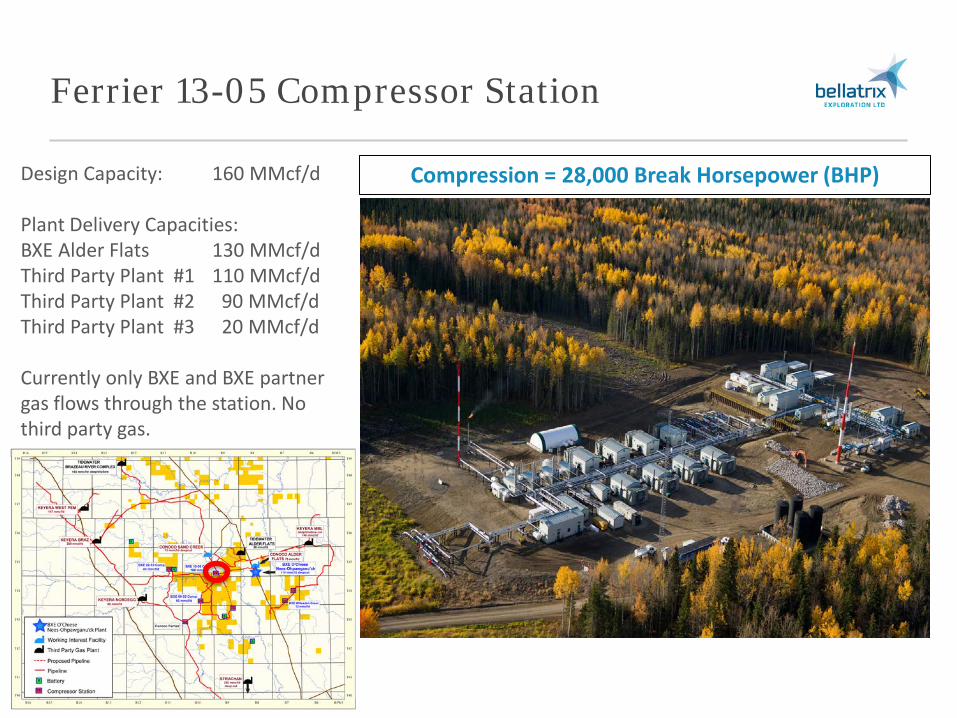

Ferrier 13-05 Compressor Station

63

Design Capacity: 160 MMcf/d Plant Delivery Capacities: BXE Alder Flats 130 MMcf/d Third Party Plant #1 110 MMcf/d Third Party Plant #2 90 MMcf/d Third Party Plant #3 20 MMcf/d Currently only BXE and BXE partner gas flows through the station. No third party gas.

Compression = 28,000 Break Horsepower (BHP)

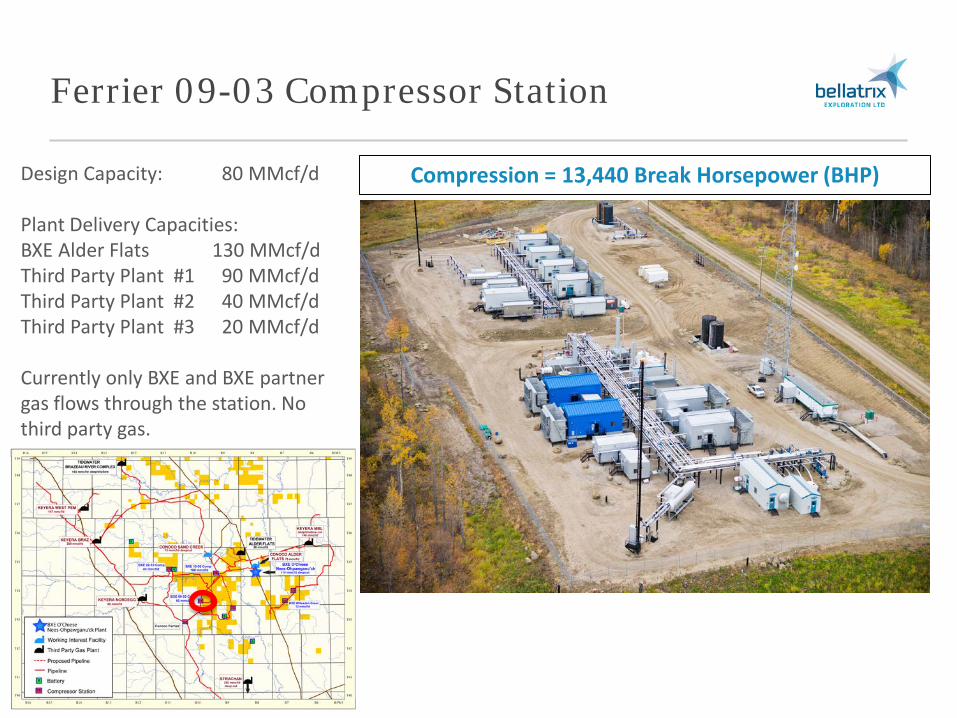

Ferrier 09-03 Compressor Station

64

Design Capacity: 80 MMcf/d Plant Delivery Capacities: BXE Alder Flats 130 MMcf/d Third Party Plant #1 90 MMcf/d Third Party Plant #2 40 MMcf/d Third Party Plant #3 20 MMcf/d Currently only BXE and BXE partner gas flows through the station. No third party gas.

Compression = 13,440 Break Horsepower (BHP)

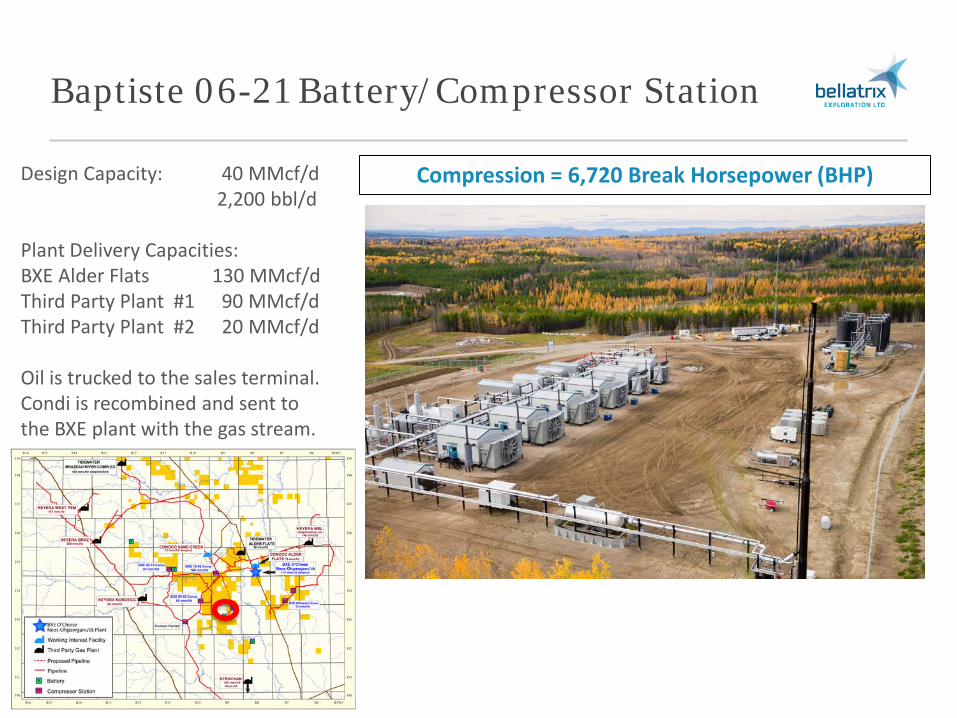

Baptiste 06-21 Battery/Compressor Station

65

Compression = 6,720 Break Horsepower (BHP) Design Capacity: 40 MMcf/d 2,200 bbl/d Plant Delivery Capacities: BXE Alder Flats 130 MMcf/d Third Party Plant #1 90 MMcf/d Third Party Plant #2 20 MMcf/d Oil is trucked to the sales terminal. Condi is recombined and sent to the BXE plant with the gas stream.

Brazeau 02-10 Battery/Compressor Station

66

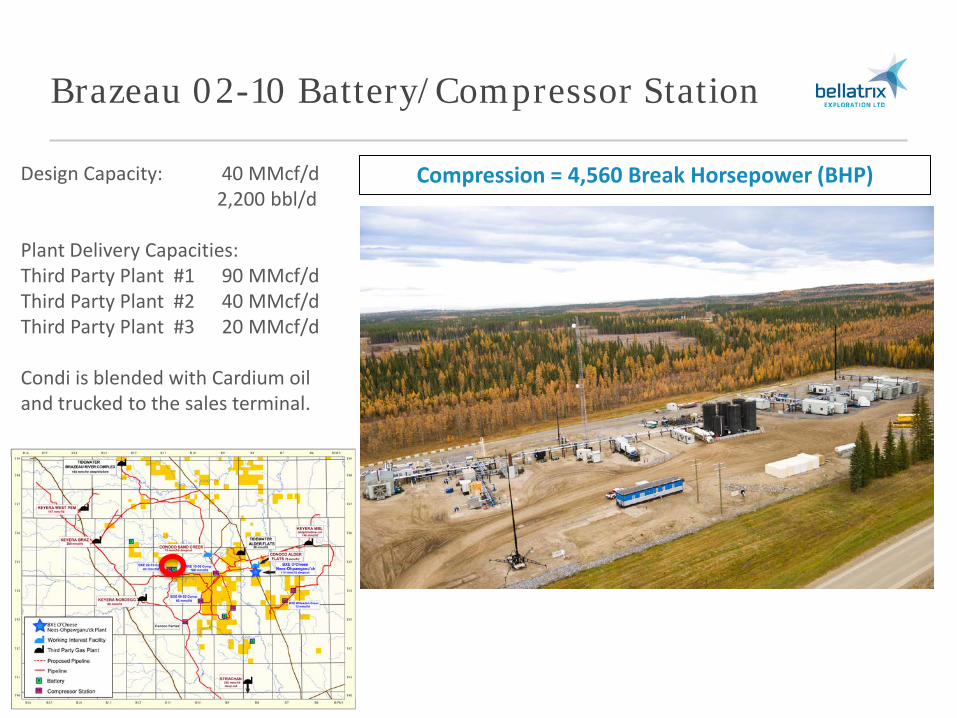

Compression = 4,560 Break Horsepower (BHP) Design Capacity: 40 MMcf/d 2,200 bbl/d Plant Delivery Capacities: Third Party Plant #1 90 MMcf/d Third Party Plant #2 40 MMcf/d Third Party Plant #3 20 MMcf/d Condi is blended with Cardium oil and trucked to the sales terminal.

Asset Optimization

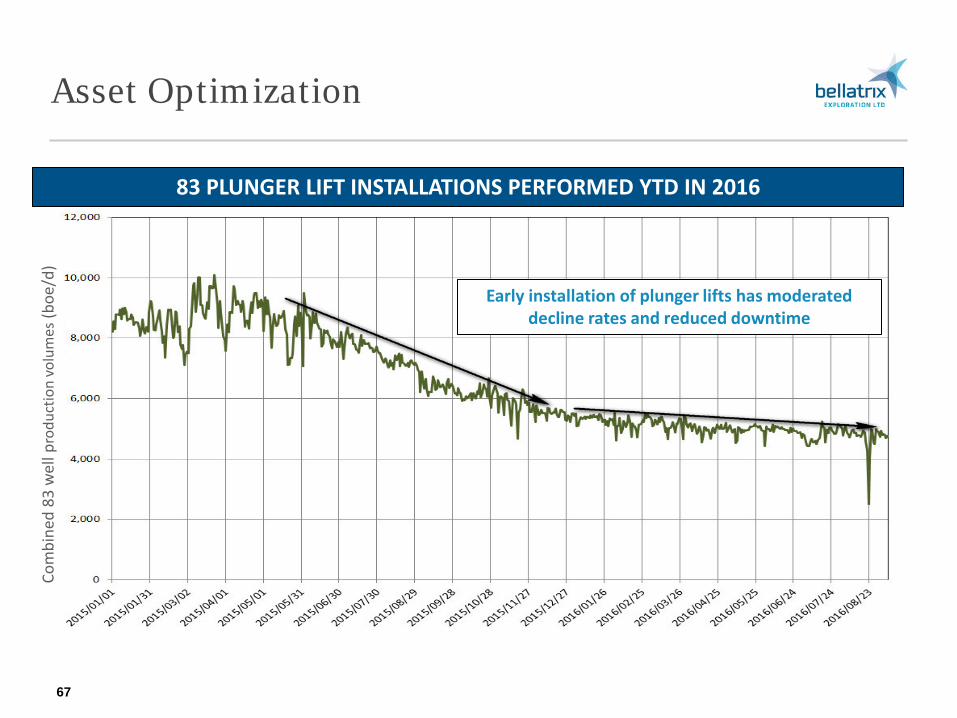

67

Early installation of plunger lifts has moderated decline rates and reduced downtime

83 PLUNGER LIFT INSTALLATIONS PERFORMED YTD IN 2016

Com

bine

d 83

wel

l pro

duct

ion

volu

mes

(boe

/d)

POC Installations and Optimization

68

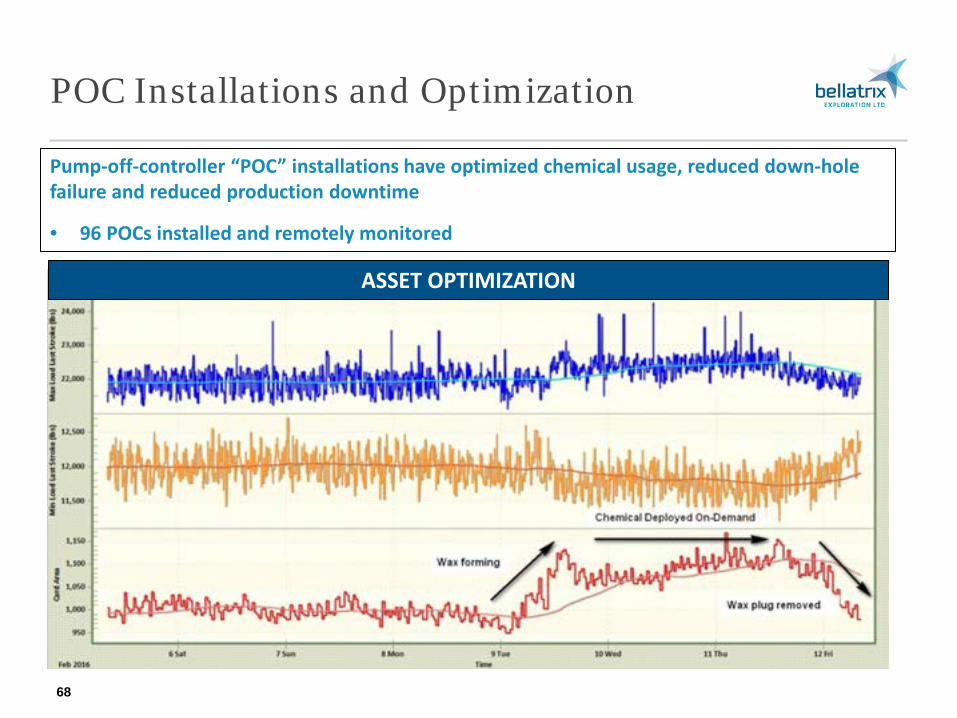

ASSET OPTIMIZATION

Pump-off-controller “POC” installations have optimized chemical usage, reduced down-hole failure and reduced production downtime

• 96 POCs installed and remotely monitored

Pipeline Pressure Optimization and Analysis

69

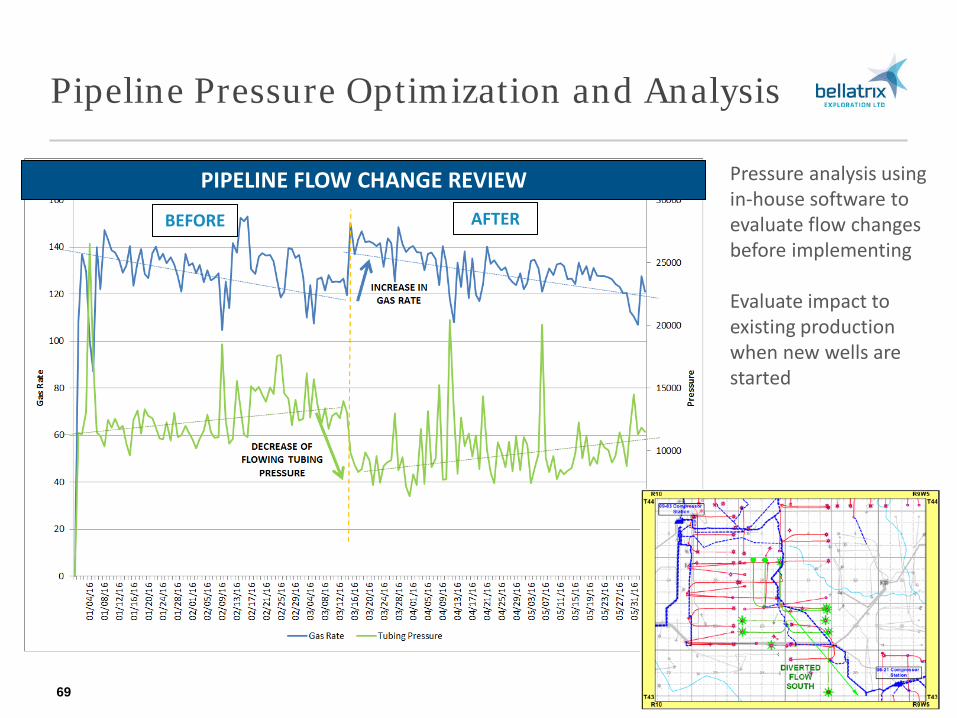

PIPELINE FLOW CHANGE REVIEW

BEFORE AFTER

Pressure analysis using in-house software to evaluate flow changes before implementing Evaluate impact to existing production when new wells are started

Historical Performance & Outlook

Analyst Update Presentation Themes

71 Long term shareholder value creation

TRANSFORMATIONAL DELEVERAGING ACHIEVED IN 2016

REPOSITIONED FOR GROWTH

TOP TIER ASSETS PROVIDE OPTIONALITY FOR BOTH OIL & NATURAL GAS INVESTMENT

MEANINGFUL EQUITY VALUE PROPOSITION

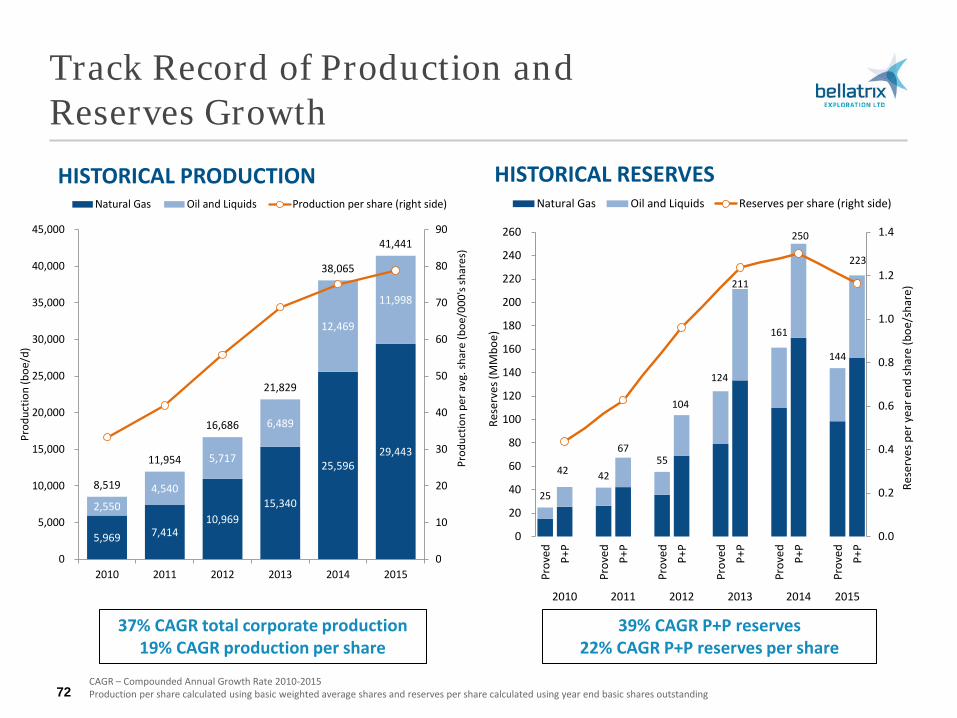

25

42 42

6755

104

124

211

161

250

144

223

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

0

20

40

60

80

100

120

140

160

180

200

220

240

260

Prov

ed P+P

Prov

ed P+P

Prov

ed P+P

Prov

ed P+P

Prov

ed P+P

Prov

ed P+P

2010 2011 2012 2013 2014 2015

Rese

rves

per

yea

r end

shar

e (b

oe/s

hare

)

Rese

rves

(MM

boe)

Natural Gas Oil and Liquids Reserves per share (right side)

Track Record of Production and Reserves Growth

HISTORICAL PRODUCTION HISTORICAL RESERVES

CAGR – Compounded Annual Growth Rate 2010-2015 Production per share calculated using basic weighted average shares and reserves per share calculated using year end basic shares outstanding 72

37% CAGR total corporate production 19% CAGR production per share

39% CAGR P+P reserves 22% CAGR P+P reserves per share

5,969 7,41410,969

15,340

25,59629,443

2,5504,540

5,717

6,489

12,469

11,998

8,519

11,954

16,686

21,829

38,065

41,441

0

10

20

30

40

50

60

70

80

90

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2010 2011 2012 2013 2014 2015

Prod

uctio

n pe

r avg

. sha

re (b

oe/0

00's

shar

es)

Prod

uctio

n (b

oe/d

)

Natural Gas Oil and Liquids Production per share (right side)

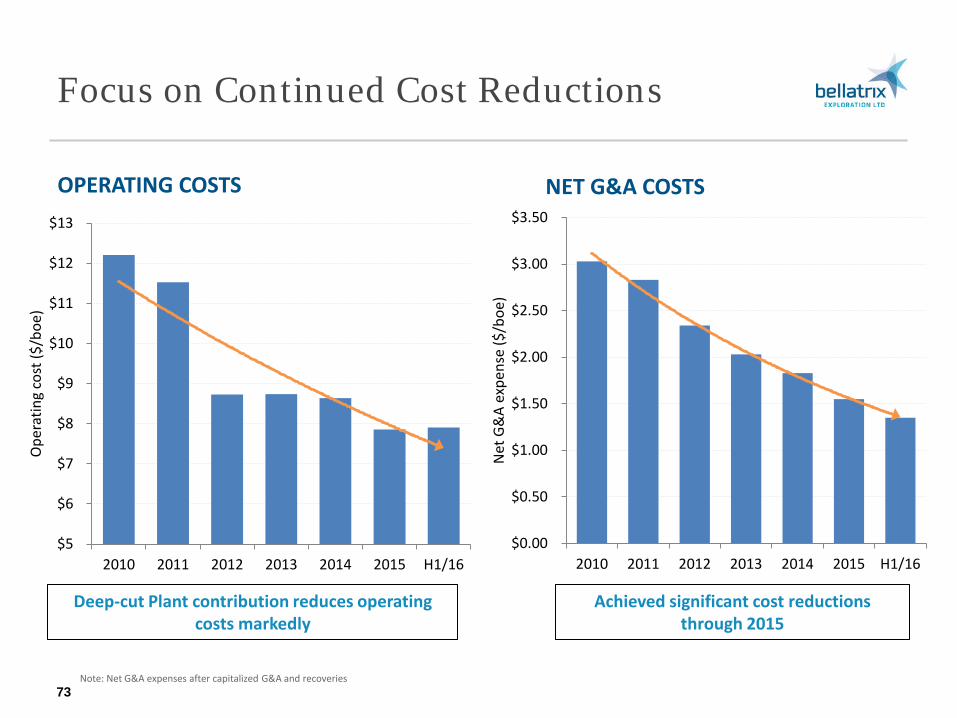

OPERATING COSTS NET G&A COSTS

Deep-cut Plant contribution reduces operating costs markedly

Achieved significant cost reductions through 2015

Note: Net G&A expenses after capitalized G&A and recoveries

73

Focus on Continued Cost Reductions

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

2010 2011 2012 2013 2014 2015 H1/16

Net

G&

A ex

pens

e ($

/boe

)

$5

$6

$7

$8

$9

$10

$11

$12

$13

2010 2011 2012 2013 2014 2015 H1/16

Ope

ratin

g co

st ($

/boe

)

2016 Second Half Capital Plan

Capital spending includes exploration and development capital projects and corporate assets, and excludes property acquisitions and dispositions. Natural gas forward strip priced as at August 8, 2016. 74

SECOND HALF 2016 GUIDANCE BALANCES FINANCIAL FLEXIBILITY & MAXIMIZED RETURNS

H2 2016 BUDGET UP TO $40MM CAPITAL ALLOCATION MAXIMIZE RETURNS

Natural gas forward curve contango • December AECO is >20% higher

than September pricing • Maximize Internal rate of return

(IRR) by deferring activity and timing of favorably time on-stream delivery of flush volumes

• Favorably positioned to capitalize on stronger 2017 pricing

Capital by Area

Greater Ferrier / Willesden Green

Drilling Formation

Spirit River

100%

100%

H2 2016 cash flow capital budget of up to $40 million • Modest facility and

infrastructure capital • Balances focused investment

and financial flexibility

Preserving value and preparing to play offense • H2 2016 average production

guidance of ~34,500 boe/d (73% natural gas weighted)

• Back end weighted growth with December 2016 forecast average production guidance of ~36,500 boe/d

$2.00

$2.25

$2.50

$2.75

$3.00

Sep

16

Oct

16

Nov

16

Dec

16

Jan

17

Feb

17

Mar

17

AECO

(C$/

GJ)

A few months for a +25% price improvement

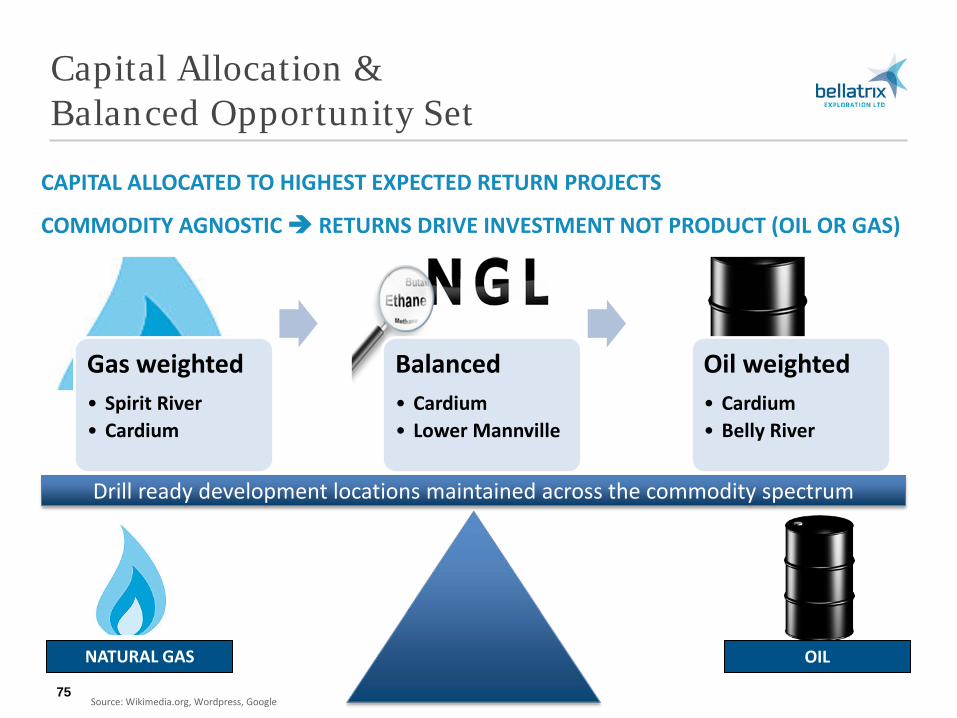

Capital Allocation & Balanced Opportunity Set

75

Drill ready development locations maintained across the commodity spectrum

CAPITAL ALLOCATED TO HIGHEST EXPECTED RETURN PROJECTS

COMMODITY AGNOSTIC RETURNS DRIVE INVESTMENT NOT PRODUCT (OIL OR GAS)

OIL NATURAL GAS

Source: Wikimedia.org, Wordpress, Google

Gas weighted • Spirit River • Cardium

Balanced • Cardium • Lower Mannville

Oil weighted • Cardium • Belly River

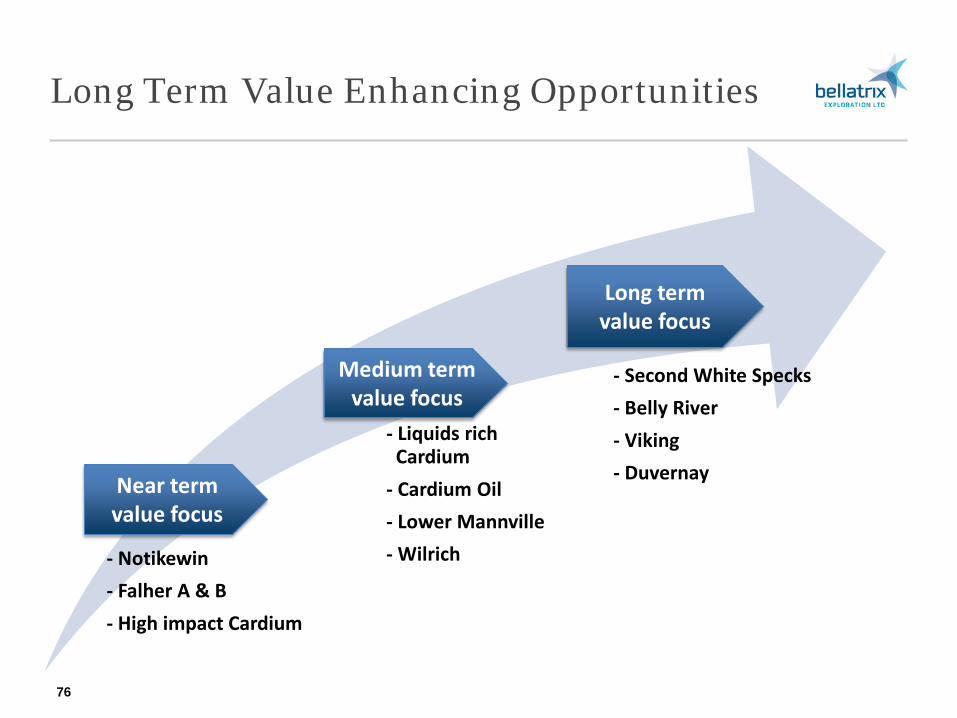

Long Term Value Enhancing Opportunities

76

- Notikewin - Falher A & B - High impact Cardium

- Liquids rich Cardium

- Cardium Oil - Lower Mannville - Wilrich

- Second White Specks - Belly River - Viking - Duvernay Near term

value focus

Medium term value focus

Long term value focus

Corporate Responsibility

77

Bellatrix is dedicated to achieving industry leading economic results in an environmentally responsible, compliant, and safe manner

Safety We are committed to operating in a safe, compliant and environmentally responsible manner.

Teamwork Together we collaborate and innovate.

Accountability We are ethical and trustworthy in our relationships with all stakeholders.

Results We are focused on creating value for our shareholders and stakeholders by delivering results.

Our core Company values are rooted in Safety, Teamwork, Accountability, and Results

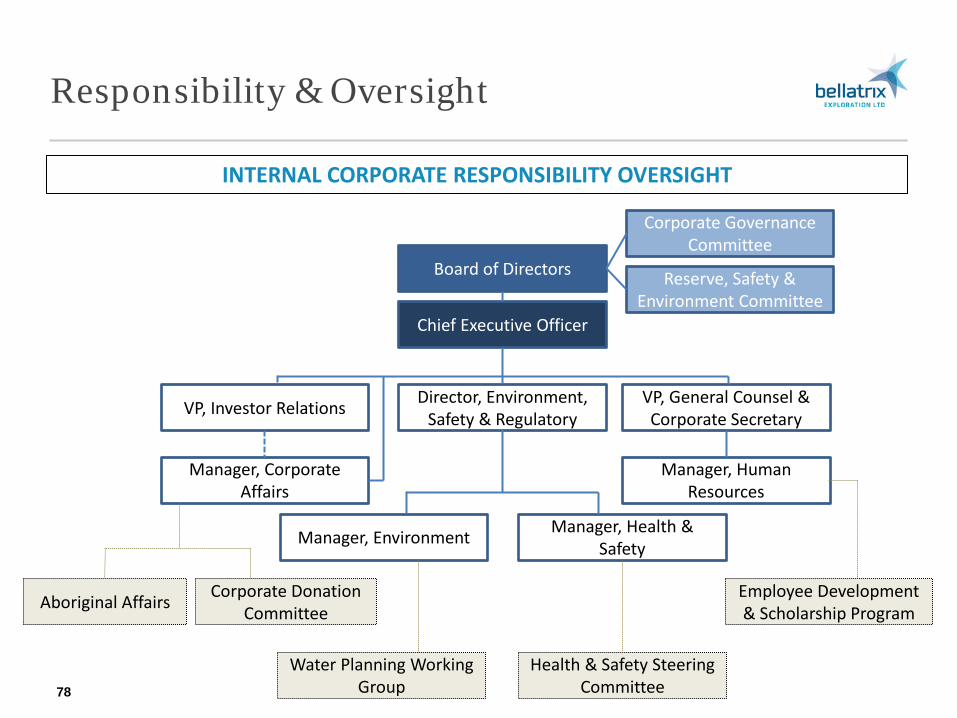

Responsibility & Oversight

78

INTERNAL CORPORATE RESPONSIBILITY OVERSIGHT

Board of Directors Reserve, Safety & Environment Committee

Chief Executive Officer

Director, Environment, Safety & Regulatory

Manager, Corporate Affairs

VP, Investor Relations VP, General Counsel & Corporate Secretary

Manager, Human Resources

Manager, Environment Manager, Health & Safety

Water Planning Working Group

Health & Safety Steering Committee

Corporate Donation Committee

Employee Development & Scholarship Program Aboriginal Affairs

Corporate Governance Committee

Stakeholder Engagement

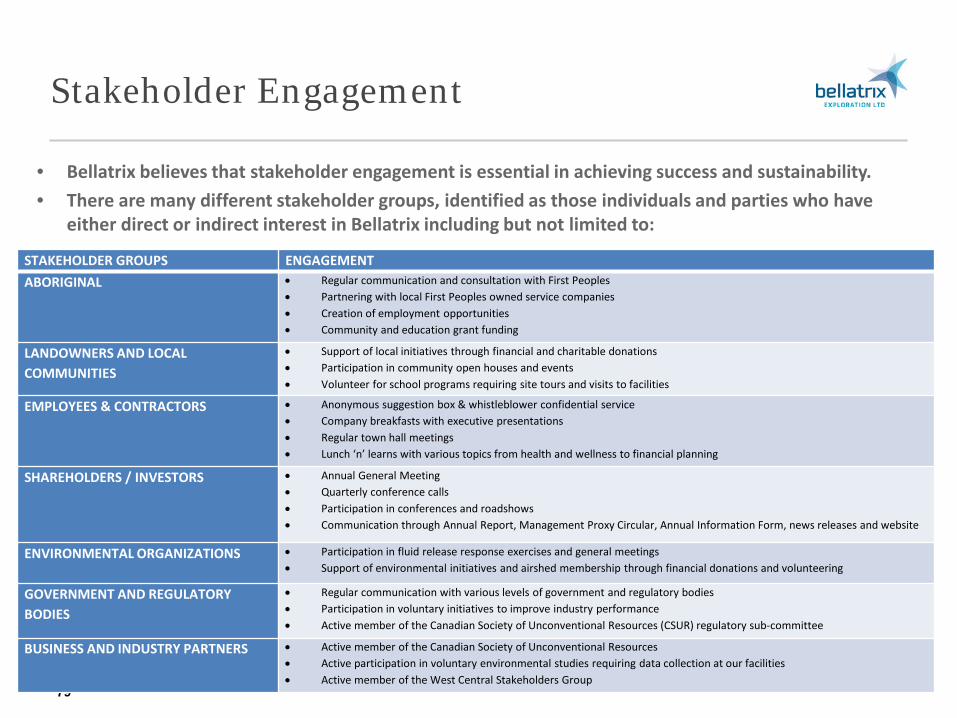

79

• Bellatrix believes that stakeholder engagement is essential in achieving success and sustainability. • There are many different stakeholder groups, identified as those individuals and parties who have

either direct or indirect interest in Bellatrix including but not limited to:

STAKEHOLDER GROUPS ENGAGEMENT ABORIGINAL • Regular communication and consultation with First Peoples

• Partnering with local First Peoples owned service companies • Creation of employment opportunities • Community and education grant funding

LANDOWNERS AND LOCAL COMMUNITIES

• Support of local initiatives through financial and charitable donations • Participation in community open houses and events • Volunteer for school programs requiring site tours and visits to facilities

EMPLOYEES & CONTRACTORS • Anonymous suggestion box & whistleblower confidential service • Company breakfasts with executive presentations • Regular town hall meetings • Lunch ‘n’ learns with various topics from health and wellness to financial planning

SHAREHOLDERS / INVESTORS • Annual General Meeting • Quarterly conference calls • Participation in conferences and roadshows • Communication through Annual Report, Management Proxy Circular, Annual Information Form, news releases and website

ENVIRONMENTAL ORGANIZATIONS • Participation in fluid release response exercises and general meetings • Support of environmental initiatives and airshed membership through financial donations and volunteering

GOVERNMENT AND REGULATORY BODIES

• Regular communication with various levels of government and regulatory bodies • Participation in voluntary initiatives to improve industry performance • Active member of the Canadian Society of Unconventional Resources (CSUR) regulatory sub-committee

BUSINESS AND INDUSTRY PARTNERS • Active member of the Canadian Society of Unconventional Resources • Active participation in voluntary environmental studies requiring data collection at our facilities • Active member of the West Central Stakeholders Group

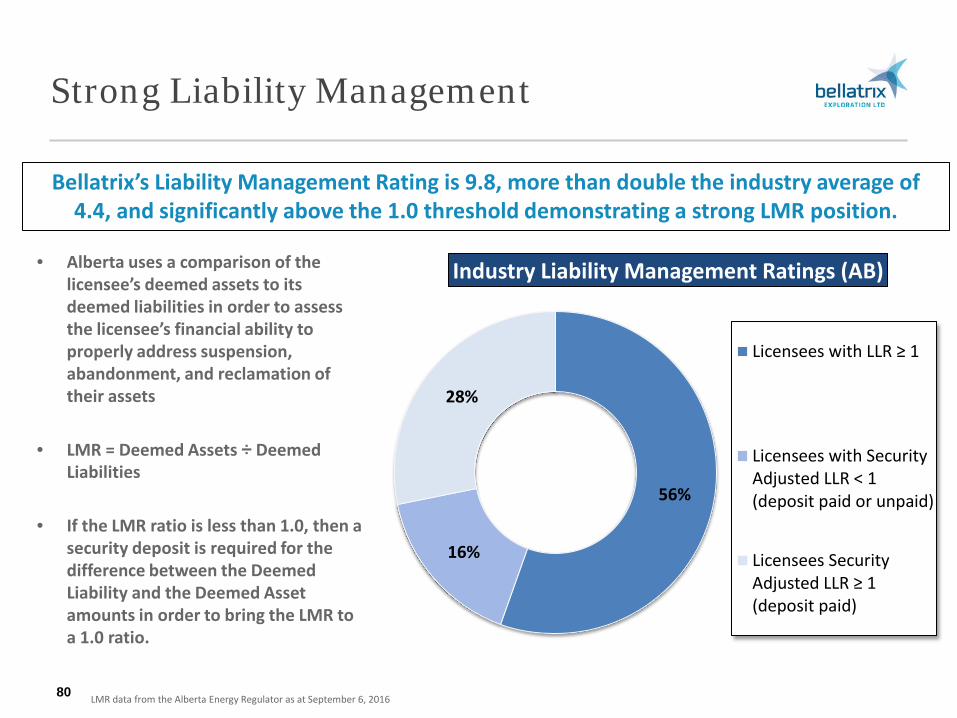

Strong Liability Management

80

• Alberta uses a comparison of the licensee’s deemed assets to its deemed liabilities in order to assess the licensee’s financial ability to properly address suspension, abandonment, and reclamation of their assets

• LMR = Deemed Assets ÷ Deemed Liabilities

• If the LMR ratio is less than 1.0, then a security deposit is required for the difference between the Deemed Liability and the Deemed Asset amounts in order to bring the LMR to a 1.0 ratio.

Bellatrix’s Liability Management Rating is 9.8, more than double the industry average of 4.4, and significantly above the 1.0 threshold demonstrating a strong LMR position.

LMR data from the Alberta Energy Regulator as at September 6, 2016

56%

16%

28%

Industry Liability Management Ratings (AB)

Licensees with LLR ≥ 1

Licensees with SecurityAdjusted LLR < 1(deposit paid or unpaid)

Licensees Security Adjusted LLR ≥ 1 (deposit paid)

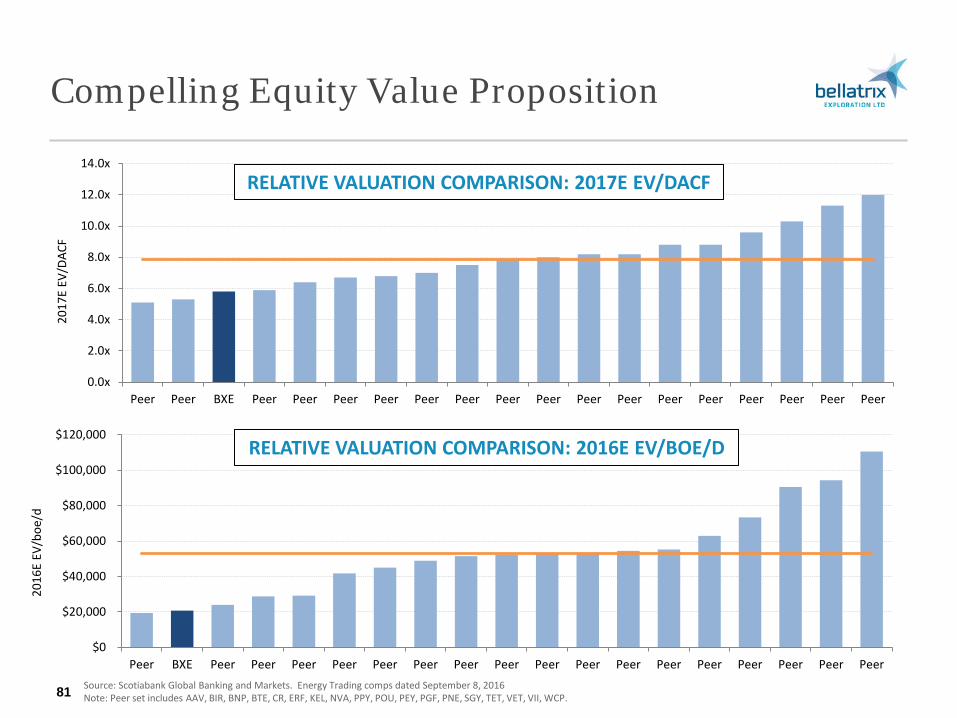

Compelling Equity Value Proposition

81

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

Peer Peer BXE Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer

2017

E EV

/DAC

F

RELATIVE VALUATION COMPARISON: 2017E EV/DACF

Source: Scotiabank Global Banking and Markets. Energy Trading comps dated September 8, 2016 Note: Peer set includes AAV, BIR, BNP, BTE, CR, ERF, KEL, NVA, PPY, POU, PEY, PGF, PNE, SGY, TET, VET, VII, WCP.

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Peer BXE Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer

2016

E EV

/boe

/d

RELATIVE VALUATION COMPARISON: 2016E EV/BOE/D

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

Peer Peer Peer BXE Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer

EV/$

boe

(2P)

0%

50%

100%

150%

200%

250%

300%

350%

400%

Peer BXE Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer

P/N

AV (2

P)

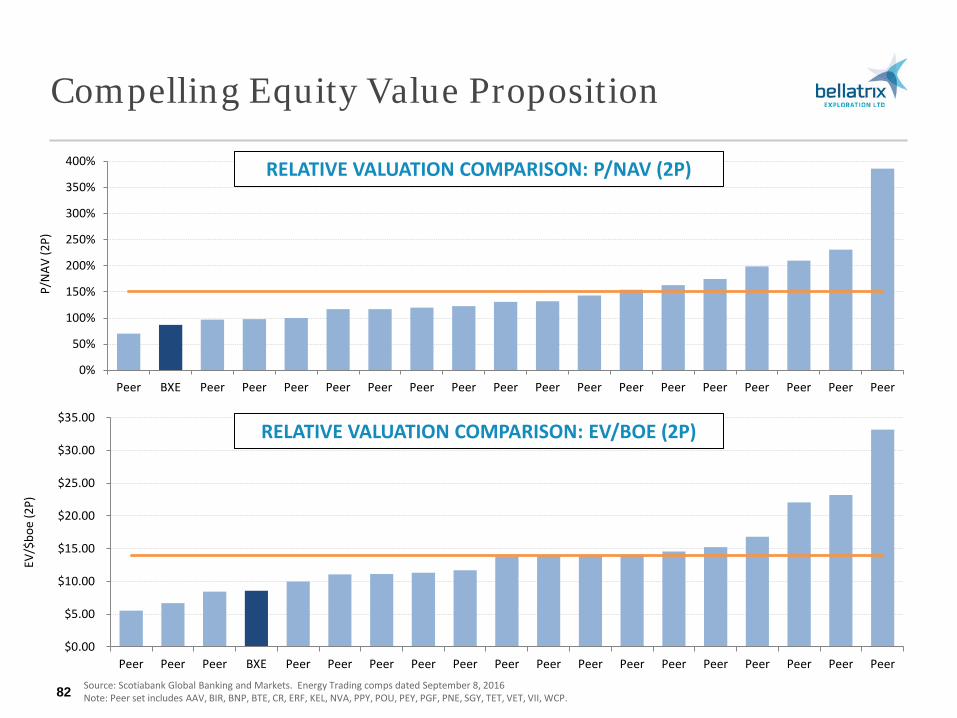

Compelling Equity Value Proposition

82 Source: Scotiabank Global Banking and Markets. Energy Trading comps dated September 8, 2016 Note: Peer set includes AAV, BIR, BNP, BTE, CR, ERF, KEL, NVA, PPY, POU, PEY, PGF, PNE, SGY, TET, VET, VII, WCP.

RELATIVE VALUATION COMPARISON: P/NAV (2P)

RELATIVE VALUATION COMPARISON: EV/BOE (2P)

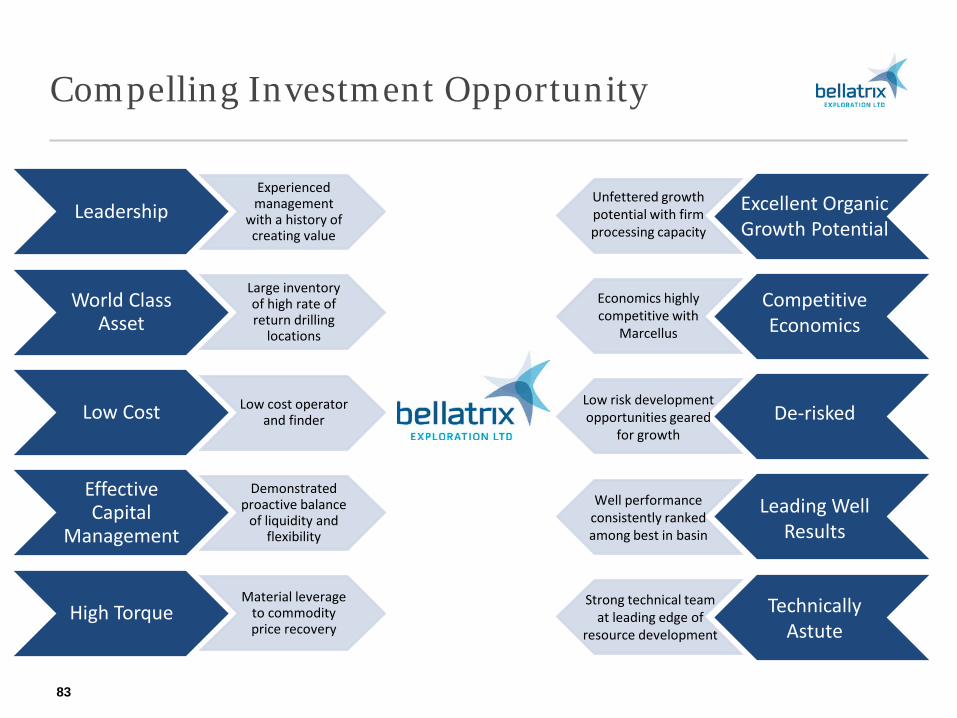

Compelling Investment Opportunity

83

Leadership Experienced management

with a history of creating value

World Class Asset

Large inventory of high rate of return drilling

locations

Low Cost Low cost operator and finder

Effective Capital

Management

Demonstrated proactive balance

of liquidity and flexibility

High Torque Material leverage

to commodity price recovery

Excellent Organic Growth Potential

Competitive Economics

De-risked

Leading Well Results

Technically Astute

Unfettered growth potential with firm processing capacity

Economics highly competitive with

Marcellus

Low risk development opportunities geared

for growth

Well performance consistently ranked among best in basin

Strong technical team at leading edge of

resource development

Supplemental Information

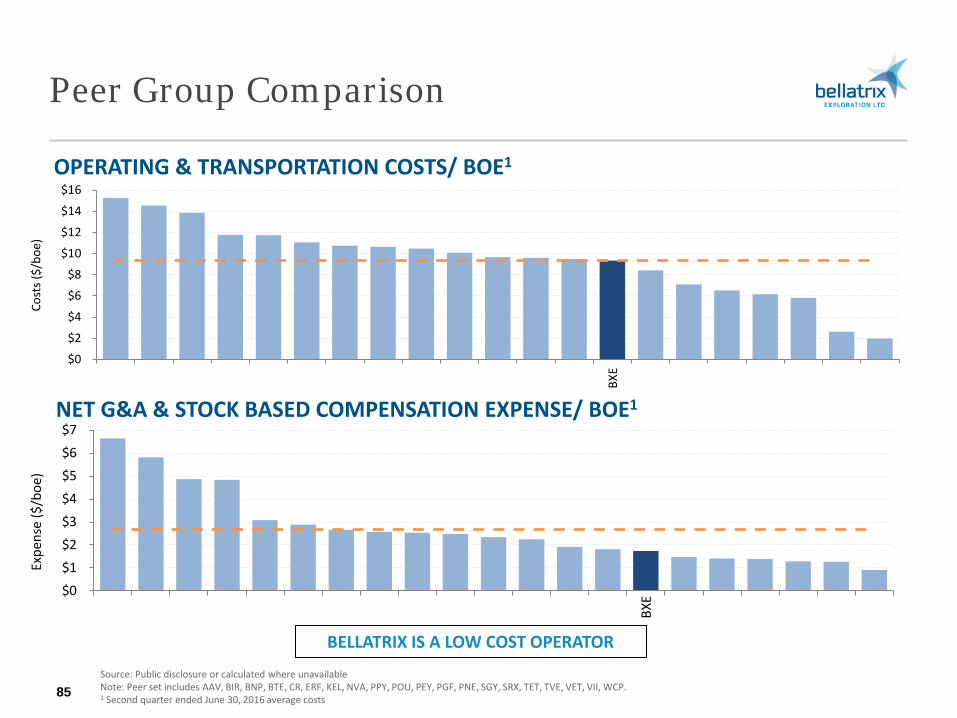

Peer Group Comparison

OPERATING & TRANSPORTATION COSTS/ BOE1

NET G&A & STOCK BASED COMPENSATION EXPENSE/ BOE1

Source: Public disclosure or calculated where unavailable Note: Peer set includes AAV, BIR, BNP, BTE, CR, ERF, KEL, NVA, PPY, POU, PEY, PGF, PNE, SGY, SRX, TET, TVE, VET, VII, WCP. 1 Second quarter ended June 30, 2016 average costs 85

BELLATRIX IS A LOW COST OPERATOR

$0

$2

$4

$6

$8

$10

$12

$14

$16

BXE

Cost

s ($/

boe)

$0$1$2$3$4$5$6$7

BXE

Expe

nse

($/b

oe)

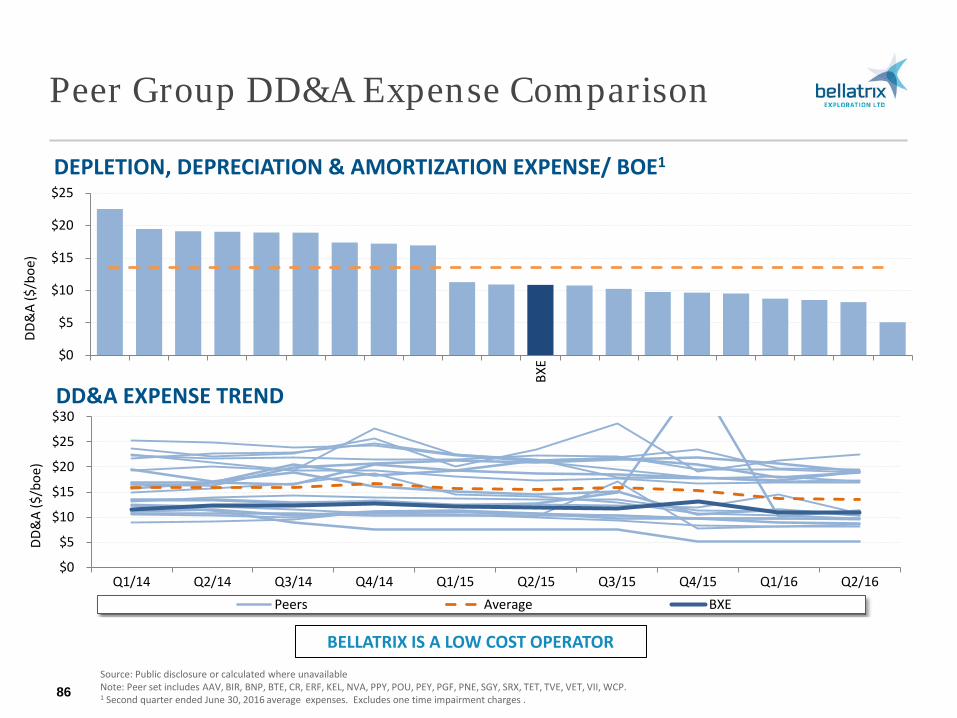

Peer Group DD&A Expense Comparison

DEPLETION, DEPRECIATION & AMORTIZATION EXPENSE/ BOE1

DD&A EXPENSE TREND

Source: Public disclosure or calculated where unavailable Note: Peer set includes AAV, BIR, BNP, BTE, CR, ERF, KEL, NVA, PPY, POU, PEY, PGF, PNE, SGY, SRX, TET, TVE, VET, VII, WCP. 1 Second quarter ended June 30, 2016 average expenses. Excludes one time impairment charges . 86

BELLATRIX IS A LOW COST OPERATOR

$0

$5

$10

$15

$20

$25

BXE

DD&

A ($

/boe

)

$0

$5

$10

$15

$20

$25

$30

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

DD&

A ($

/boe

)

Peers Average BXE

Joint Ventures

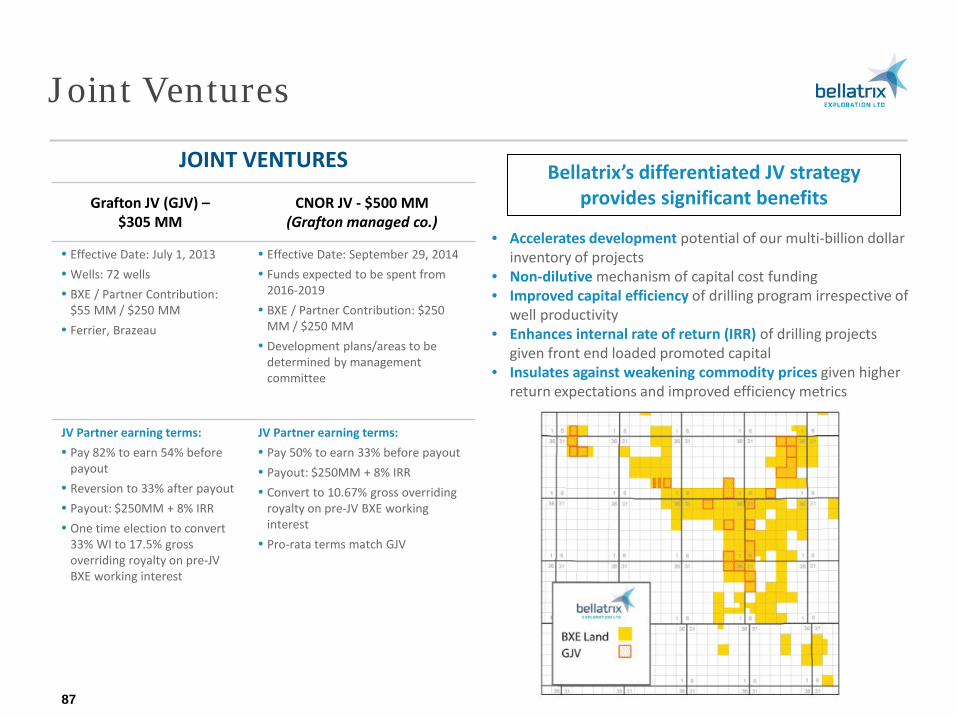

JOINT VENTURES

Grafton JV (GJV) – $305 MM

CNOR JV - $500 MM (Grafton managed co.)

• Effective Date: July 1, 2013 • Wells: 72 wells • BXE / Partner Contribution:

$55 MM / $250 MM • Ferrier, Brazeau

• Effective Date: September 29, 2014 • Funds expected to be spent from

2016-2019 • BXE / Partner Contribution: $250

MM / $250 MM • Development plans/areas to be

determined by management committee

JV Partner earning terms: • Pay 82% to earn 54% before

payout • Reversion to 33% after payout • Payout: $250MM + 8% IRR • One time election to convert

33% WI to 17.5% gross overriding royalty on pre-JV BXE working interest

JV Partner earning terms: • Pay 50% to earn 33% before payout • Payout: $250MM + 8% IRR • Convert to 10.67% gross overriding

royalty on pre-JV BXE working interest

• Pro-rata terms match GJV

87

• Accelerates development potential of our multi-billion dollar inventory of projects

• Non-dilutive mechanism of capital cost funding • Improved capital efficiency of drilling program irrespective of

well productivity • Enhances internal rate of return (IRR) of drilling projects

given front end loaded promoted capital • Insulates against weakening commodity prices given higher

return expectations and improved efficiency metrics

Bellatrix’s differentiated JV strategy provides significant benefits

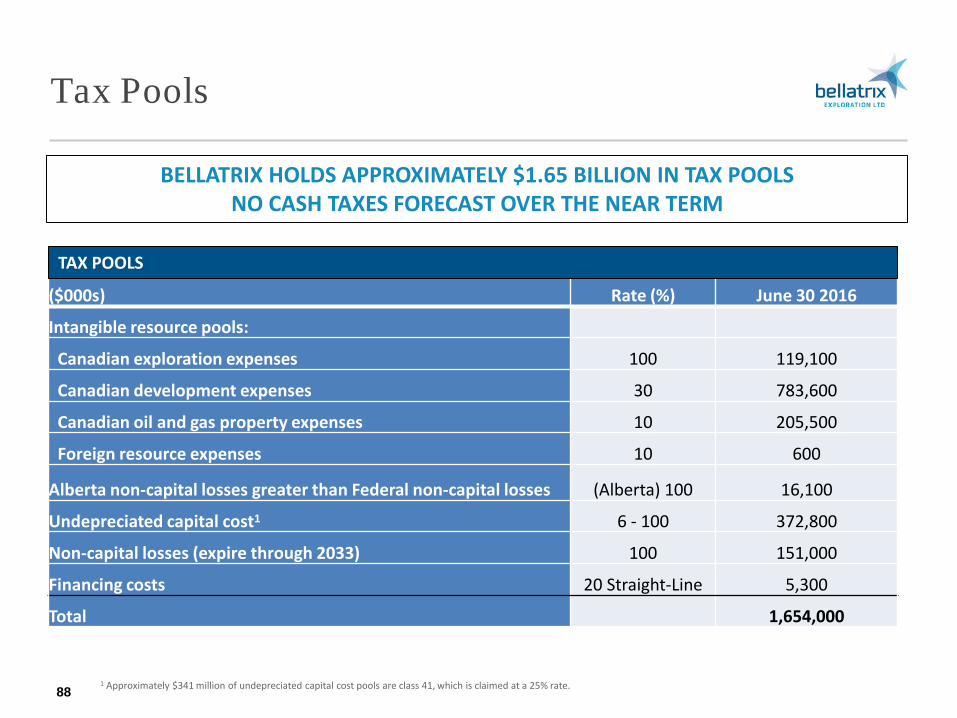

Tax Pools

88

BELLATRIX HOLDS APPROXIMATELY $1.65 BILLION IN TAX POOLS NO CASH TAXES FORECAST OVER THE NEAR TERM

($000s) Rate (%) June 30 2016

Intangible resource pools:

Canadian exploration expenses 100 119,100

Canadian development expenses 30 783,600

Canadian oil and gas property expenses 10 205,500

Foreign resource expenses 10 600

Alberta non-capital losses greater than Federal non-capital losses (Alberta) 100 16,100

Undepreciated capital cost1 6 - 100 372,800

Non-capital losses (expire through 2033) 100 151,000

Financing costs 20 Straight-Line 5,300

Total 1,654,000

TAX POOLS

1 Approximately $341 million of undepreciated capital cost pools are class 41, which is claimed at a 25% rate.

Additional Long Term Opportunities

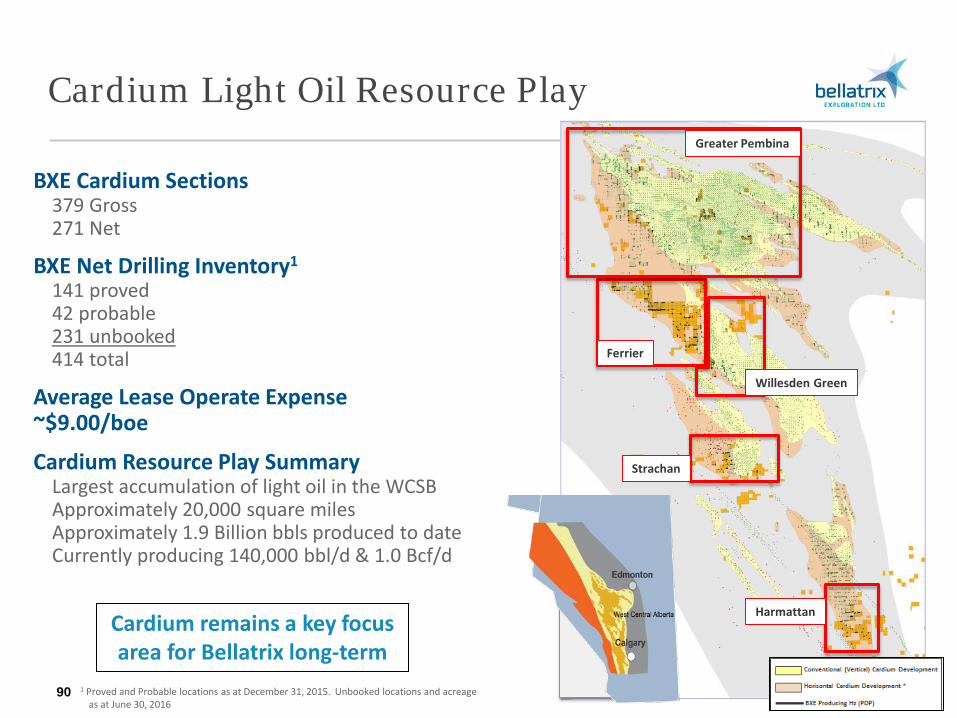

Cardium Light Oil Resource Play