frontline q4 2012 results presentation

TRANSCRIPT

1

Q4 2012 Results

February 22, 2013

2

MATTERS DISCUSSED IN THIS DOCUMENT MAY CONSTITUTE FORWARD-LOOKING STATEMENTS. THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 PROVIDES SAFE HARBOR PROTECTIONS FOR FORWARD-LOOKING STATEMENTS IN ORDER TO ENCOURAGE COMPANIES TO PROVIDE PROSPECTIVE INFORMATION ABOUT THEIR BUSINESS. FORWARD-LOOKING STATEMENTS INCLUDE STATEMENTS CONCERNING PLANS, OBJECTIVES, GOALS, STRATEGIES, FUTURE EVENTS OR PERFORMANCE, AND UNDERLYING ASSUMPTIONS AND OTHER STATEMENTS, WHICH ARE OTHER THAN STATEMENTS OF HISTORICAL FACTS.

FRONTLINE DESIRES TO TAKE ADVANTAGE OF THE SAFE HARBOR PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 AND IS INCLUDING THIS CAUTIONARY STATEMENT IN CONNECTION WITH THIS SAFE HARBOR LEGISLATION. THE WORDS “BELIEVE,” “ANTICIPATE,” “INTENDS,” “ESTIMATE,” “FORECAST,” “PROJECT,” “PLAN,” “POTENTIAL,” “WILL,” “MAY,” “SHOULD,” “EXPECT” “PENDING” AND SIMILAR EXPRESSIONS IDENTIFY FORWARD-LOOKING STATEMENTS.

THE FORWARD-LOOKING STATEMENTS IN THIS DOCUMENT ARE BASED UPON VARIOUS ASSUMPTIONS, MANY OF WHICH ARE BASED, IN TURN, UPON FURTHER ASSUMPTIONS, INCLUDING WITHOUT LIMITATION, MANAGEMENT'S EXAMINATION OF HISTORICAL OPERATING TRENDS, DATA CONTAINED IN FRONTLINE’S RECORDS AND OTHER DATA AVAILABLE FROM THIRD PARTIES. ALTHOUGH FRONTLINE BELIEVES THAT THESE ASSUMPTIONS WERE REASONABLE WHEN MADE, BECAUSE THESE ASSUMPTIONS ARE INHERENTLY SUBJECT TO SIGNIFICANT UNCERTAINTIES AND CONTINGENCIES WHICH ARE DIFFICULT OR IMPOSSIBLE TO PREDICT AND ARE BEYOND FRONTLINE’S CONTROL, YOU CANNOT BE ASSURED THAT FRONTLINE WILL ACHIEVE OR ACCOMPLISH THESE EXPECTATIONS, BELIEFS OR PROJECTIONS. FRONTLINE UNDERTAKES NO DUTY TO UPDATE ANY FORWARD-LOOKING STATEMENT TO CONFORM THE STATEMENT TO ACTUAL RESULTS OR CHANGES IN EXPECTATIONS.

IMPORTANT FACTORS THAT, IN FRONTLINE’S VIEW, COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE DISCUSSED IN THE FORWARD-LOOKING STATEMENTS INCLUDE, WITHOUT LIMITATION: THE STRENGTH OF WORLD ECONOMIES AND CURRENCIES, GENERAL MARKET CONDITIONS, INCLUDING FLUCTUATIONS IN CHARTERHIRE RATES AND VESSEL VALUES, CHANGES IN DEMAND IN THE TANKER MARKET, INCLUDING BUT NOT LIMITED TO CHANGES IN OPEC'S PETROLEUM PRODUCTION LEVELS AND WORLD WIDE OIL CONSUMPTION AND STORAGE, CHANGES IN FRONTLINE’S OPERATING EXPENSES, INCLUDING BUNKER PRICES, DRYDOCKING AND INSURANCE COSTS, THE MARKET FOR FRONTLINE’S VESSELS, AVAILABILITY OF FINANCING AND REFINANCING, ABILITY TO COMPLY WITH COVENANTS IN SUCH FINANCING ARRANGEMENTS, FAILURE OF COUNTERPARTIES TO FULLY PERFORM THEIR CONTRACTS WITH US, CHANGES IN GOVERNMENTAL RULES AND REGULATIONS OR ACTIONS TAKEN BY REGULATORY AUTHORITIES, POTENTIAL LIABILITY FROM PENDING OR FUTURE LITIGATION, GENERAL DOMESTIC AND INTERNATIONAL POLITICAL CONDITIONS, POTENTIAL DISRUPTION OF SHIPPING ROUTES DUE TO ACCIDENTS OR POLITICAL EVENTS, VESSEL BREAKDOWNS, INSTANCES OF OFF-HIRE AND OTHER IMPORTANT FACTORS. FOR A MORE COMPLETE DISCUSSION OF THESE AND OTHER RISKS AND UNCERTAINTIES ASSOCIATED WITH FRONTLINE’S BUSINESS, PLEASE REFER TO FRONTLINE’S FILINGS WITH THE SECURITIES AND EXCHANGE COMMISSION, INCLUDING, BUT NOT LIMITED TO, ITS ANNUAL REPORT ON FORM 20-F.

THIS PRESENTATION IS NOT AN OFFER TO PURCHASE OR SELL, OR A SOLICITATION OF AN OFFER TO PURCHASE OR SELL, ANY SECURITIES OF FRONTLINE.

Forward looking statements

3

Agenda

■ Fourth Quarter 2012 Highlights and Transactions

■ Financial Review

■ Newbuildings

■ Market Update

■ Outlook

■ Q & A

4

Highlights and Transactions

Fourth Quarter 2012

■ The company terminated a number of vessels in the recent period:

■ The OBO carriers Front Climber and Front Driver in October and November

■ The VLCC Ticen Ocean in November, 2012. Recognized a gain of $11.2m

■ The VLCC Titan Aries in January, 2013. Expects to recognize a gain of $7.5m in Q1-13.

■ The Suezmax Front Pride in February, 2013. Recorded an impairment loss of $4.7m in Q4-12.

■ Agreed to an early termination of the TC-out contracts on the OBO carriers Front Viewer and

Front Guider in December.

■ Received compensation for loss of hire of $35m

■ Paid $23.5m in compensation to SFL as the long term charter parties on the vessels were terminated.

■ Re-delivered the chartered-in VLCC Gulf Eyadah in December

5

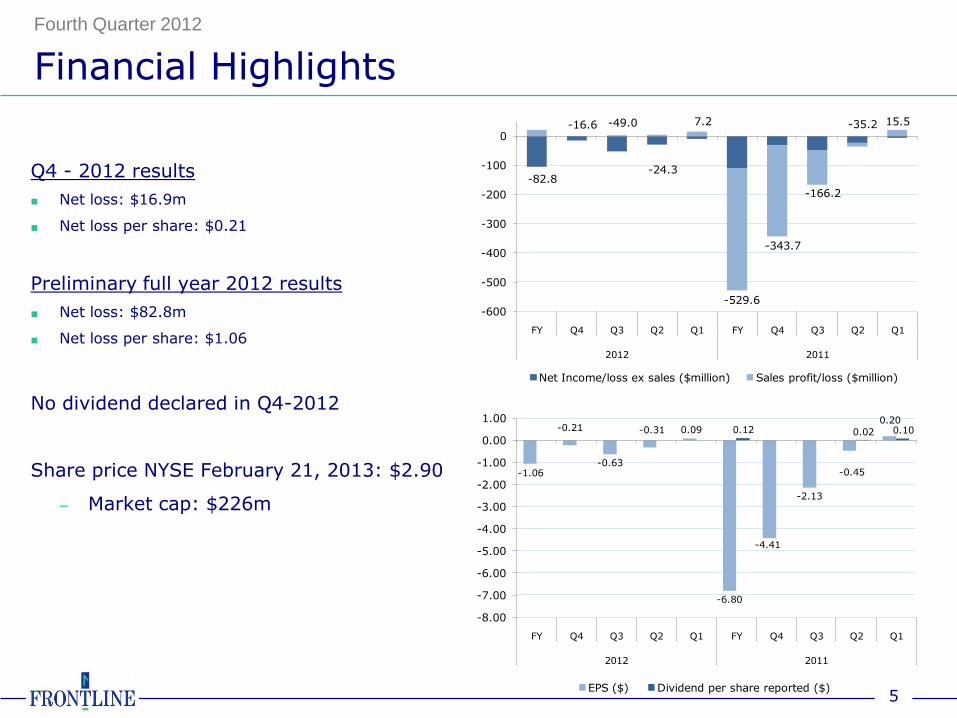

Financial Highlights

Q4 - 2012 results

■ Net loss: $16.9m

■ Net loss per share: $0.21

Preliminary full year 2012 results

■ Net loss: $82.8m

■ Net loss per share: $1.06

No dividend declared in Q4-2012

Share price NYSE February 21, 2013: $2.90

– Market cap: $226m

-82.8

-16.6 -49.0

-24.3

7.2

-529.6

-343.7

-166.2

-35.2 15.5

-600

-500

-400

-300

-200

-100

0

FY Q4 Q3 Q2 Q1 FY Q4 Q3 Q2 Q1

2012 2011

Net Income/loss ex sales ($million) Sales profit/loss ($million)

Fourth Quarter 2012

-1.06

-0.21

-0.63

-0.31 0.09

-6.80

-4.41

-2.13

-0.45

0.200.12 0.02 0.10

-8.00

-7.00

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

1.00

FY Q4 Q3 Q2 Q1 FY Q4 Q3 Q2 Q1

2012 2011

EPS ($) Dividend per share reported ($)

6

Income Statement

Financial Review

2011 2012 CONDENSED CONSOLIDATED INCOME STATEMENTS 2012 2011

Oct-Dec Oct-Dec (in thousands of $) Jan-Dec Jan-Dec

181,981 197,436 Total operating revenues 668,107 810,102

(312,878) (2,560) Gain (loss) on sale of assets and amortization of deferred gains 16,813 (307,894)

67,673 84,607 Voyage expenses and commission 274,132 295,787

(347) - Profit share expense (income) - 482

- 11,981 Contingent rental expense 54,612 -

39,098 29,174 Ship operating expenses 130,685 187,010

14,758 6,362 Charter hire expenses 37,461 65,601

9,397 9,205 Administrative expenses 33,906 35,886

- 18,901 Impairment loss on vessels 32,042 121,443

44,057 27,953 Depreciation 114,845 195,597

174,636 188,183 Total operating expenses 677,683 901,806

(305,533) 6,693 Net operating gain (loss) 7,723 (399,598)

29 40 Interest income 130 3,958

(37,188) (23,149) Interest expense (94,962) (141,497)

(189) (171) Share of results from associated companies (4) (600)

(65) (16) Foreign currency exchange gain (loss) 84 106

(816) (198) Other non-operating items 4,119 9,153

(343,762) (16,801) Net loss before taxes and non controlling interest (83,396) (528,478)

(349) (122) Taxes (379) (532)

445 357 Net loss (income) attributable to non controlling interest 1,021 (591)

(343,666) (16,566) Net loss attributable to Frontline Ltd. (82,754) (529,601)

(4.41) (0.21) Basic loss per share attributable to Frontline Ltd. ($) (1.06) (6.8)

7

Income on time charter basis

Financial Review

$/day FY Q4 Q3 Q2 Q1 FY Q4 Q3 Q2 Q1

VLCC Spot DH 22 400 18 500 13 300 31 500 25 400 20 200 16 800 12 600 23 900 27 400

VLCC w hole fleet 22 200 19 300 12 300 31 000 25 600 22 800 19 100 17 000 26 100 28 600

Suezmax Spot DH 15 200 14 000 10 500 16 200 19 500 12 600 12 400 7 800 14 500 16 000

Orion Suezmax pool 15 500 9 000 11 100 17 400 19 200 13 600 12 000 7 600 16 200 17 700

OBO 33 600 35 100 33 700 28 100 37 800 36 700 41 600 38 200 31 300 36 300

2012 2011

8

Ship operating expenses/Off-hire

Financial Review

Tentative drydock schedule/no. of vessels

– Q1-2013: 3 VLCCs

10 400

9 700

11 800

11 100

9 000

9 900

9 2009 300

10 80010 200

6 000

7 000

8 000

9 000

10 000

11 000

12 000

13 000

FY Q4 Q3 Q2 Q1 FY Q4 Q3 Q2 Q1

2012 2011

Total fleet opex ($/day)

10

1

45

9

1

3 32

0

2

4

6

8

10

12

FY Q4 Q3 Q2 Q1 FY Q4 Q3 Q2 Q1

2012 2011

Number of vessels drydocked

368

42

144 141

41

677

86

159211 221

0

100

200

300

400

500

600

700

800

FY Q4 Q3 Q2 Q1 FY Q4 Q3 Q2 Q1

2012 2011

Off hire (days)

9

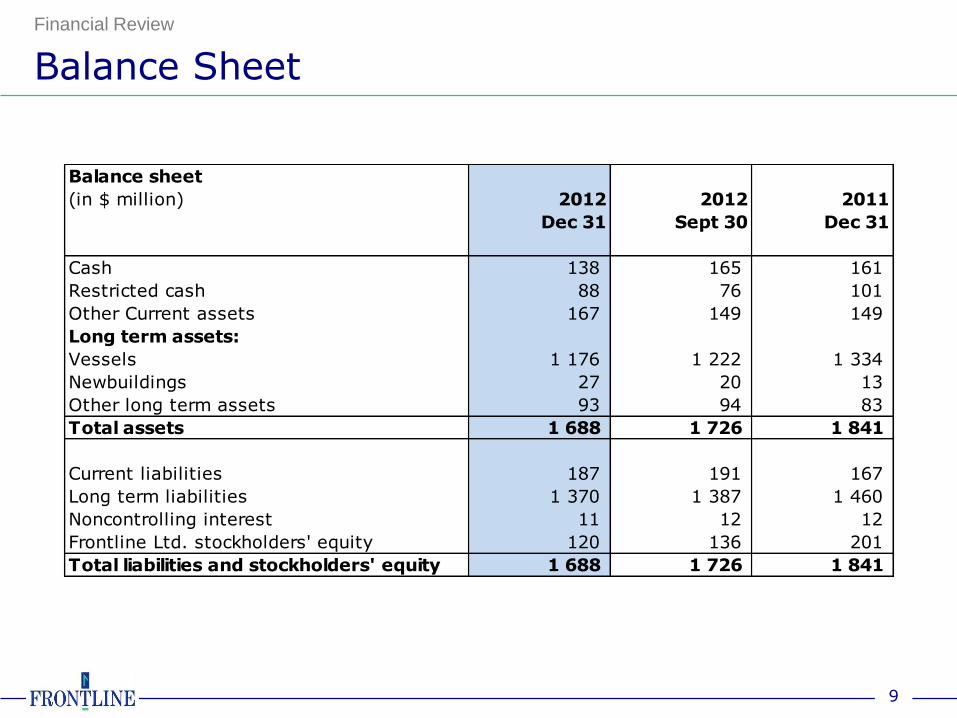

Balance Sheet

Financial Review

Balance sheet

(in $ million) 2012 2012 2011

Dec 31 Sept 30 Dec 31

Cash 138 165 161

Restricted cash 88 76 101

Other Current assets 167 149 149

Long term assets:

Vessels 1 176 1 222 1 334

Newbuildings 27 20 13

Other long term assets 93 94 83

Total assets 1 688 1 726 1 841

Current liabilities 187 191 167

Long term liabilities 1 370 1 387 1 460

Noncontrolling interest 11 12 12

Frontline Ltd. stockholders' equity 120 136 201

Total liabilities and stockholders' equity 1 688 1 726 1 841

10

Cash Cost Breakeven

Comments to B/E rates:

– Included in cash B/E rates are: BB hire, opex , interest and admin. expenses

– B/E rates exclude vessels on short term TC-in, vessels on BB-out, capex. and ITCL vessels

Estimated Cash cost breakeven rates

for the remainder of 2013 ($/day)

VLCC 24,200

Suezmax 18,800

Financial Review

11

Newbuilding Overview

■ Total newbuilding program as of December 31, 2012:

– Two Suezmax tankers

– Remaining installments to be paid approx. $87.9m

Newbuilding

12

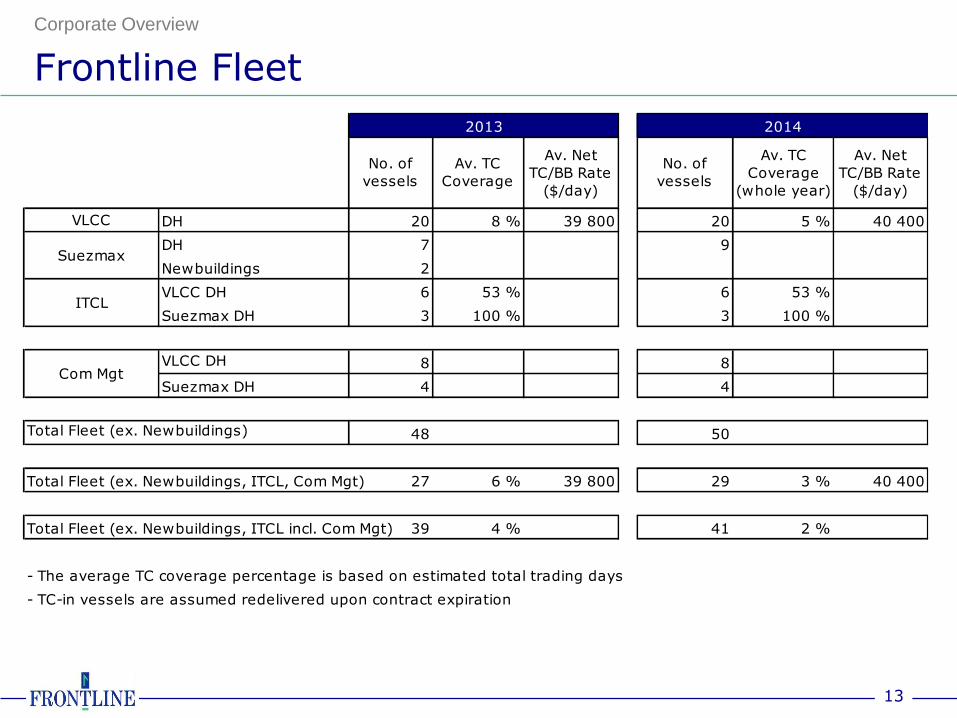

Frontline Fleet

Incl. vessels on commercial management & ITCL, excl. newbuildings

Total: 48 As per 21 February DH: Double Hull

Corporate Overview

VLCC DH 34

Suezmax DH 14

13

Frontline Fleet

Corporate Overview

DH 20 8 % 39 800 20 5 % 40 400

DH 7 9

Newbuildings 2

VLCC DH 6 53 % 6 53 %

Suezmax DH 3 100 % 3 100 %

VLCC DH 8 8

Suezmax DH 4 4

Total Fleet (ex. Newbuildings) 48 50

Total Fleet (ex. Newbuildings, ITCL, Com Mgt) 27 6 % 39 800 29 3 % 40 400

Total Fleet (ex. Newbuildings, ITCL incl. Com Mgt) 39 4 % 41 2 %

- The average TC coverage percentage is based on estimated total trading days

- TC-in vessels are assumed redelivered upon contract expiration

2014

No. of

vessels

Av. TC

Coverage

Av. Net

TC/BB Rate

($/day)

No. of

vessels

Av. TC

Coverage

(whole year)

Av. Net

TC/BB Rate

($/day)

VLCC

ITCL

2013

Com Mgt

Suezmax

14

Earnings & Market Factors

Q4 – Average Market earnings / Marex

■ VLCC (TD3) : $9,000/day (current: $5/day)

■ Suezmax (TD5) : $11,500/day (current: 10,750/day)

The Market:

■ IEA estimates world oil demand in the fourth quarter averaged 91 mb/d in the fourth quarter, an increase of 0.8 mb/d compared to Q3. Parts of this increase might be “borrowed” demand from Q1 because of Chinese refinery startups.

■ High OPEC output through the first part of the quarter and Chinese import with higher tonnage miles supported freight rates

■ Global refinery throughputs averaged 75.9 mb/d in Q4 with growth in activity concentrated in China, India and Russia. Favorable refinery margins and cold snap in Asia supporting throughputs.

■ 11 VLCC newbuilding and 14 Suezmax were delivered during the quarter

■ 6 VLCC and 8 Suezmax were removed during the quarter

Market Update

Source: MAREX, IEA. Graphs: Clarksons

0

20 000

40 000

60 000

80 000

100 000

Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

$ / d

ay

VLCC

Q4 2011 2012 Ave 2008 - 2012

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

100 000

Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

$ / d

ay

SUEZMAX

Q4 2011 2012 Ave 2008 - 2012

15

VLCC Fleet

Market Update

Source: Fearnleys January 2013

Delivery Schedule

Fleet

Current fleet & Orderbook

Current Fleet 622 Orderbook 81

DH Fleet 605 Delivered 2012 49

SH (DS, DB, SS) Fleet 17 Estimated deliveries 2013 50

16

Suezmax Fleet

Market Update

Source: Fearnleys January 2013

Delivery Schedule

Fleet

Current fleet & Orderbook

Current Fleet 468 Orderbook 72

DH Fleet 463 Delivered 2012 47

SH (DS, DB, SS) Fleet 5 Estimated deliveries 2013 37

1

7 8 8 8 11 20

15 22

17 23 24 27 25 26 25

14

46 38 35

47

55

5 12

-12 -13 -9 -10 -6 -6

-26 -20

-29

-15 -15 -15

-4 -6

-17 -18

-4 -12

-6

-17 -9

-25

-22

-19

-16

-13

-10

-7

-4

-1

2

5

8

11

14

17

20

23

-80

0

80

1988

1990

1993

1995

2000

2005

2009

2010

2011

2012

2013

2014

2015

% # of vsls

FRO Assumptions on Phase Out / Deletions Suezmax Deletions

Orderbook Suezmax DH

17

Rates

TC MARKET

Source: Clarksons

Market Update

NEWBUILDING

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

Fe

b-0

6

Jun

-06

Oct-

06

Fe

b-0

7

Jun

-07

Oct-

07

Fe

b-0

8

Jun

-08

Oct-

08

Fe

b-0

9

Jun

-09

Oct-

09

Fe

b-1

0

Jun

-10

Oct-

10

Fe

b-1

1

Jun

-11

Oct-

11

Fe

b-1

2

Jun

-12

Oct-

12

Fe

b-1

3

$ / D

AY

3Y TC VLCC 3Y TC SUEZMAX

50

60

70

80

90

100

110

120

130

140

150

160

170

180

20

06-0

2

20

06-0

6

20

06-1

0

20

07-0

2

20

07-0

6

20

07-1

0

20

08-0

2

20

08-0

6

20

08-1

0

20

09-0

2

20

09-0

6

20

09-1

0

20

10-0

2

20

10-0

6

20

10-1

0

20

11-0

2

20

11-0

6

20

11-1

0

20

12-0

2

20

12-0

6

20

12-1

0

20

13-0

2

M U

SD

VLCC NB SMAX NB

18

Outlook General

■ Market at rock bottom

■ Increased technical issues on ships observed in market

– less maintenance of ships

■ Last year with big newbuilding program

■ Increased tonnage demand but not enough to offset newbuilding program

■ Some more interest in scrapping

Market Update

Frontline

■ Reducing fleet:

- Continue to redeliver older and non core chartered in tonnage

■ Outperformed our peers on VLCC’s and Suezmax earnings

■ Frontline will continue to remain cautious and focus its resources on the present activities until a clearer sign of recovery can be seen in the tanker market

19

Questions?