franklin templeton ira application offer two ways for you to combine your current purchase of class...

TRANSCRIPT

Questions? Please call your financial advisor or Franklin Templeton Retirement Services at (800) 527-2020.page 1 of 4

IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING A NEW ACCOUNT. To help the government fight the funding of terrorism and money launderingactivities, Federal law requires all financial institutions to obtain, verify and record information that identifies each person who opens an account.What this means for you: When you open an account, we will ask for your name, address, date of birth and other information that will allow us to identify you. If you fail to provide all requested information, it may delay or prevent us from opening an account and making your requestedinvestment(s), and if after your account is open we are unable to verify the information you provide, we may close your account.

PLEASE NOTE: You must provide your U.S. Taxpayer Identification Number (TIN); a TIN includes your Social Security number or ITIN.

For assistance, please call your financial advisor or Franklin Templeton Retirement Services at (800) 527-2020.

1 TYPE OF IRA

CHECK ONE:1 � TRADITIONAL IRA � ROLLOVER IRA � ROTH IRA � ROTH CONVERSION IRA

2 ACCOUNT OWNER INFORMATION

First name M.I. Last name Date of birth (mm/dd/yyyy) SSN/TIN

Street address of residence (no P.O. box address) City State ZIP

Mailing address (if different from above) City State ZIP

Primary phone number Alternate phone number

( ) ( ) � U.S. citizen or resident alien � Nonresident alien

3 SALES CHARGE REDUCTIONS

We offer two ways for you to combine your current purchase of Class A fund shares with other existing Franklin Templeton fund share holdings thatmight enable you to qualify for a lower sales charge with your current purchase. You can qualify for a lower sales charge when you reach certain “salescharge breakpoints.” This quantity discount information is available at franklintempleton.com by clicking the “Funds” tab and then choosing“Quantity Discounts.”

3A. CUMULATIVE QUANTITY DISCOUNT FOR CLASS A SHARES

� I am familiar with the cumulative quantity discount provision of the Fund’s prospectus and understand that I can combine the amount of mycurrent purchase of Class A shares with any existing holdings that the prospectus describes as “Cumulative Quantity Discount eligible shares” to determine if I can qualify for a reduced sales charge breakpoint. I also understand that if there are any existing Cumulative Quantity Discounteligible shares that I want combined with my current purchase, I must identify the account(s) in which they are held below or they will not beconsidered in determining if my current purchase qualifies for a reduced sales charge breakpoint.

I have reviewed the prospectus (or referred to the web page noted above) and believe that Cumulative Quantity Discount eligible shares are held inthe following account(s) (identify by account number):

Account number(s)

Fund name(s)

3B. LETTER OF INTENT FOR CLASS A SHARES

� I intend to purchase additional shares issued by one or more Franklin Templeton funds over a 13-month period following my initial purchase inorder to be eligible for a sales charge discount on my purchase of Class A shares. I agree to the terms of the Letter of Intent described in the appli-cable prospectus(es) and grant Franklin Templeton Distributors, Inc., a security interest in the shares to be reserved. Although I am not obligatedto do so, the aggregate amount of Franklin Templeton funds’ shares I intend to purchase over the 13-month period will be in an aggregate amountat least equal to:

� $50,000 (not applicable for all funds) � $100,000 � $250,000 � $500,000 � $1,000,000 or above

Account number(s)

Franklin Templeton IRA Application

1. Please complete a separate application for each type of IRA you wish to establish.

Questions? Please call your financial advisor or Franklin Templeton Retirement Services at (800) 527-2020. page 2 of 4

SIGNATURE GUARANTEE

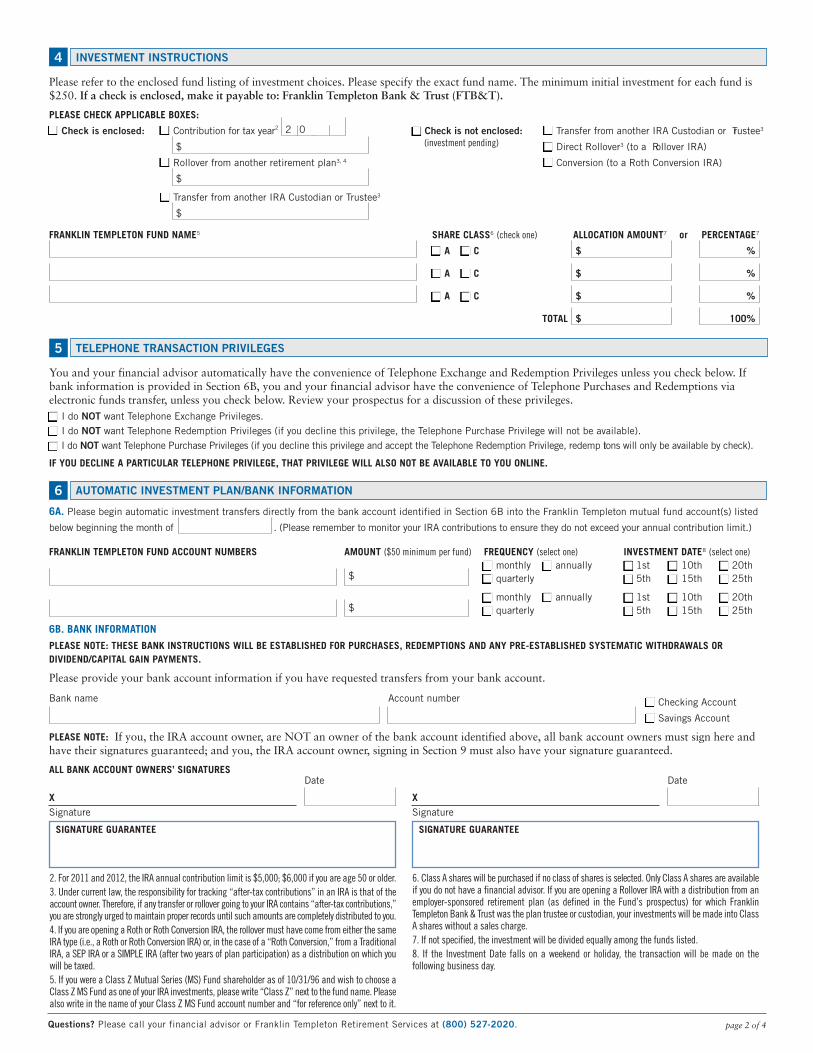

4 INVESTMENT INSTRUCTIONS

Please refer to the enclosed fund listing of investment choices. Please specify the exact fund name. The minimum initial investment for each fund is$250. If a check is enclosed, make it payable to: Franklin Templeton Bank & Trust (FTB&T).

PLEASE CHECK APPLICABLE BOXES:

� Check is enclosed: � Contribution for tax year2 2 0 � Check is not enclosed: � Transfer from another IRA Custodian or Trustee3

$ (investment pending) � Direct Rollover3 (to a Rollover IRA)

� Rollover from another retirement plan3, 4 � Conversion (to a Roth Conversion IRA)

$

� Transfer from another IRA Custodian or Trustee3

$

FRANKLIN TEMPLETON FUND NAME5 SHARE CLASS6 (check one) ALLOCATION AMOUNT7 or PERCENTAGE7

� A � C $ %

� A � C $ %

� A � C $ %

TOTAL $ 100%

5 TELEPHONE TRANSACTION PRIVILEGES

You and your financial advisor automatically have the convenience of Telephone Exchange and Redemption Privileges unless you check below. Ifbank information is provided in Section 6B, you and your financial advisor have the convenience of Telephone Purchases and Redemptions via electronic funds transfer, unless you check below. Review your prospectus for a discussion of these privileges.

� I do NOT want Telephone Exchange Privileges.

� I do NOT want Telephone Redemption Privileges (if you decline this privilege, the Telephone Purchase Privilege will not be available).

� I do NOT want Telephone Purchase Privileges (if you decline this privilege and accept the Telephone Redemption Privilege, redemp tions will only be available by check).

IF YOU DECLINE A PARTICULAR TELEPHONE PRIVILEGE, THAT PRIVILEGE WILL ALSO NOT BE AVAILABLE TO YOU ONLINE.

6 AUTOMATIC INVESTMENT PLAN/BANK INFORMATION

6A. Please begin automatic investment transfers directly from the bank account identified in Section 6B into the Franklin Templeton mutual fund account(s) listed

below beginning the month of . (Please remember to monitor your IRA contributions to ensure they do not exceed your annual contribution limit.)

FRANKLIN TEMPLETON FUND ACCOUNT NUMBERS AMOUNT ($50 minimum per fund) FREQUENCY (select one) INVESTMENT DATE8 (select one)� monthly � annually � 1st � 10th � 20th

$ � quarterly � 5th � 15th � 25th

� monthly � annually � 1st � 10th � 20th$ � quarterly � 5th � 15th � 25th

6B. BANK INFORMATION

PLEASE NOTE: THESE BANK INSTRUCTIONS WILL BE ESTABLISHED FOR PURCHASES, REDEMPTIONS AND ANY PRE-ESTABLISHED SYSTEMATIC WITHDRAWALS OR DIVIDEND/CAPITAL GAIN PAYMENTS.

Please provide your bank account information if you have requested transfers from your bank account.

Bank name Account number � Checking Account

� Savings Account

PLEASE NOTE: If you, the IRA account owner, are NOT an owner of the bank account identified above, all bank account owners must sign here andhave their signatures guaranteed; and you, the IRA account owner, signing in Section 9 must also have your signature guaranteed.

ALL BANK ACCOUNT OWNERS’ SIGNATURESDate Date

X XSignature Signature

2. For 2011 and 2012, the IRA annual contribution limit is $5,000; $6,000 if you are age 50 or older.3. Under current law, the responsibility for tracking “after-tax contributions” in an IRA is that of theaccount owner. Therefore, if any transfer or rollover going to your IRA contains “after-tax contributions,”you are strongly urged to maintain proper records until such amounts are completely distributed to you.4. If you are opening a Roth or Roth Conversion IRA, the rollover must have come from either the sameIRA type (i.e., a Roth or Roth Conversion IRA) or, in the case of a “Roth Conversion,” from a TraditionalIRA, a SEP IRA or a SIMPLE IRA (after two years of plan participation) as a distribution on which youwill be taxed.5. If you were a Class Z Mutual Series (MS) Fund shareholder as of 10/31/96 and wish to choose aClass Z MS Fund as one of your IRA investments, please write “Class Z” next to the fund name. Pleasealso write in the name of your Class Z MS Fund account number and “for reference only” next to it.

6. Class A shares will be purchased if no class of shares is selected. Only Class A shares are availableif you do not have a financial advisor. If you are opening a Rollover IRA with a distribution from anemployer-sponsored retirement plan (as defined in the Fund’s prospectus) for which FranklinTempleton Bank & Trust was the plan trustee or custodian, your investments will be made into ClassA shares without a sales charge.7. If not specified, the investment will be divided equally among the funds listed.8. If the Investment Date falls on a weekend or holiday, the transaction will be made on the following business day.

SIGNATURE GUARANTEE

Questions? Please call your financial advisor or Franklin Templeton Retirement Services at (800) 527-2020.page 3 of 4

Franklin Templeton IRA Application (cont’d.)

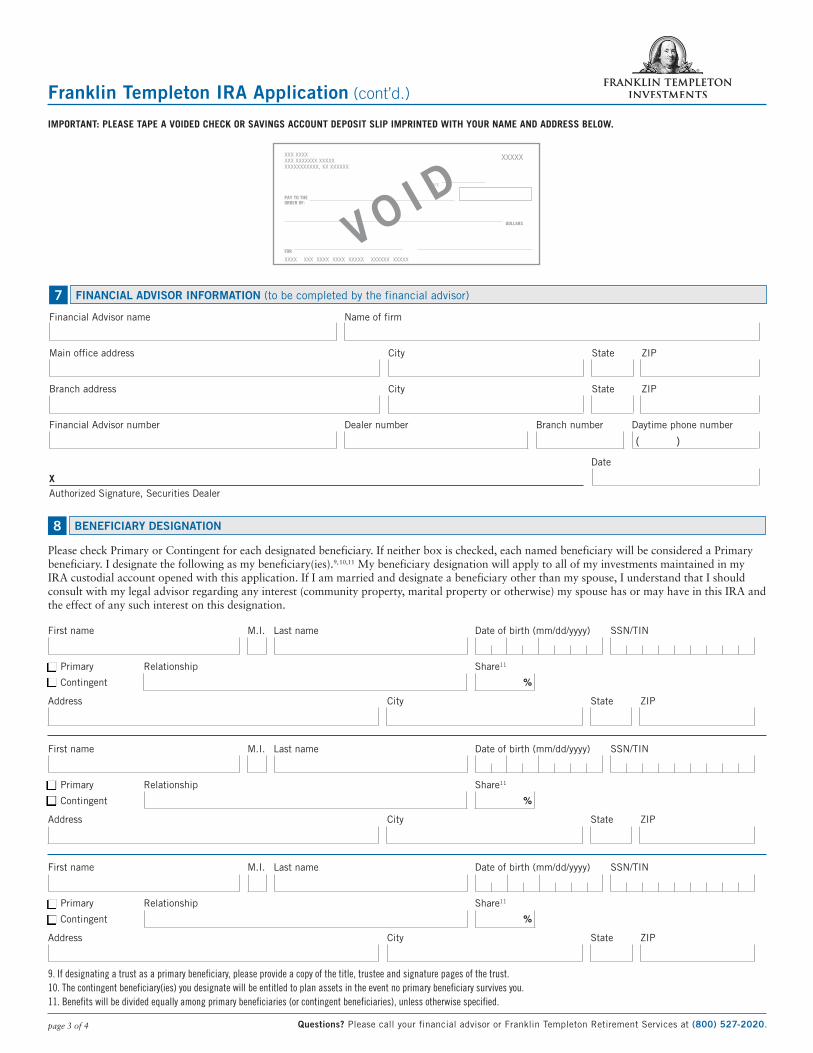

8 BENEFICIARY DESIGNATION

Please check Primary or Contingent for each designated beneficiary. If neither box is checked, each named beneficiary will be considered a Primarybeneficiary. I designate the following as my beneficiary(ies).9,10,11 My beneficiary designation will apply to all of my investments maintained in my IRA custodial account opened with this application. If I am married and designate a beneficiary other than my spouse, I understand that I shouldconsult with my legal advisor regarding any interest (community property, marital property or otherwise) my spouse has or may have in this IRA andthe effect of any such interest on this designation.

First name M.I. Last name Date of birth (mm/dd/yyyy) SSN/TIN

� Primary Relationship Share11

� Contingent %

Address City State ZIP

First name M.I. Last name Date of birth (mm/dd/yyyy) SSN/TIN

� Primary Relationship Share11

� Contingent %

Address City State ZIP

First name M.I. Last name Date of birth (mm/dd/yyyy) SSN/TIN

� Primary Relationship Share11

� Contingent %

Address City State ZIP

9. If designating a trust as a primary beneficiary, please provide a copy of the title, trustee and signature pages of the trust.10. The contingent beneficiary(ies) you designate will be entitled to plan assets in the event no primary beneficiary survives you.11. Benefits will be divided equally among primary beneficiaries (or contingent beneficiaries), unless otherwise specified.

IMPORTANT: PLEASE TAPE A VOIDED CHECK OR SAVINGS ACCOUNT DEPOSIT SLIP IMPRINTED WITH YOUR NAME AND ADDRESS BELOW.

XXX XXXX XXXXXXXX XXXXXXX XXXXXXXXXXXXXXXX, XX XXXXXX

DATE

PAY TO THEORDER OF:

DOLLARS

FOR

XXXX XXX XXXX XXXX XXXXX XXXXXX XXXXX

VOI D

7 FINANCIAL ADVISOR INFORMATION (to be completed by the financial advisor)

Financial Advisor name Name of firm

Main office address City State ZIP

Branch address City State ZIP

Financial Advisor number Dealer number Branch number Daytime phone number

( )

Date

XAuthorized Signature, Securities Dealer

Questions? Please call your financial advisor or Franklin Templeton Retirement Services at (800) 527-2020. page 4 of 4 RIRA APP 12/11

12. The maintenance fee will be $10 if the aggregate balance of all of the participant’s accounts that are linked under the Cumulative Quantity Discount is $50,000 or more at the time the fee isassessed. Please note that the fee is assessed upon an account closing if the account is closed prior to the annual fee assessment, which generally occurs in the first week of December.

Not FDIC Insured | May Lose Value | No Bank Guarantee

BY SIGNING BELOW I CERTIFY AND AGREE THAT:

• The information provided on this application is true, correct andcomplete. You may verify this information with others, includingthird-party credit reporting agencies and databases and U.S. and/orforeign government agencies, and if you are unable to verify myinformation, you are authorized to close my account by redeemingshares at the then applicable net asset value.

• I hereby appoint Franklin Templeton Bank & Trust as Custodian ofmy IRA under the terms of Traditional IRA Custodial AccountAgreement (the “Agreement”). I have received and read theAgreement and the IRA Disclosure Statement.

• I consent to a maintenance fee for the type of IRA custodial accountopened by this application. A $15 maintenance fee will apply to eachaccount with a balance of less than $50,000. The maintenance fee is$10 for accounts with balances of $50,000 and over.12

• I have received and read the prospectus for each fund selected inSection 4 and agree to the terms of each.

• I have full authority and am of legal age (or an emancipated minor)to buy and sell shares.

• The information in Sections 2, 6, 8 and 9 applies to any new fundinto which my shares may be exchanged.

• I consent to the recording of our telephone conversations when I callyou regarding my shares and account.

• If I request transfers to or from my bank account in this appli cationor at any time, including by telephone, electronically or otherwise,you are authorized to make those requested transfers (and to make,if necessary, adjusting transfers if any amounts are transferred inerror). If my bank is not an ACH member bank, you are authorizedto make those transfers by presenting drafts drawn against my bankchecking account that you may sign for me on my behalf. I agree thatFranklin Templeton may make additional attempts to debit/credit the account if the initial attempt fails and if a transfer is denied by mybank for any reason, Franklin Templeton will discontinue thisauthorization. I understand that I can end this authorization at anytime by notifying you in writing or by telephone. If I am an owner of the bank account identified on this application, I certify that mysignature alone is sufficient to authorize debits from my bankaccount.

• You are authorized to provide any information about my account(s)to my dealer or other financial advisor.

• I will review all statements upon receipt at the address of record, and will notify you immediately if there is a discrepancy.

• I understand that my property may be transferred to the appropriatestate if no activity/communication occurs in the account within thetime period specified by my state’s law.

I understand that mutual fund shares are not deposits or obligationsof, or guaranteed or endorsed by, any bank, and are not federallyinsured by the Federal Deposit Insurance Corporation, the FederalReserve Board, or any other agency of the U.S. Gov ernment, and that an investment in mutual fund shares involves risks, including the possible loss of principal.AUTHORIZED SIGNATURE

Date

X

SIGNATURE GUARANTEE: A signature guarantee is required only if you, the IRA account owner, are NOT an owner of the bank account identified in Section 6B.

9 AUTHORIZING SIGNATURE

Please mail to WEST COAST EAST COAST

Franklin Templeton Investments Franklin Templeton Investments c/o Retirement Services c/o Retirement ServicesP.O. Box 997153 P.O. Box 33033Sacramento, CA 95899-7153 St. Petersburg, FL 33733-8033

Overnight 3344 Quality Drive 100 Fountain ParkwayRancho Cordova, CA 95670-7313 St. Petersburg, FL 33716-1205

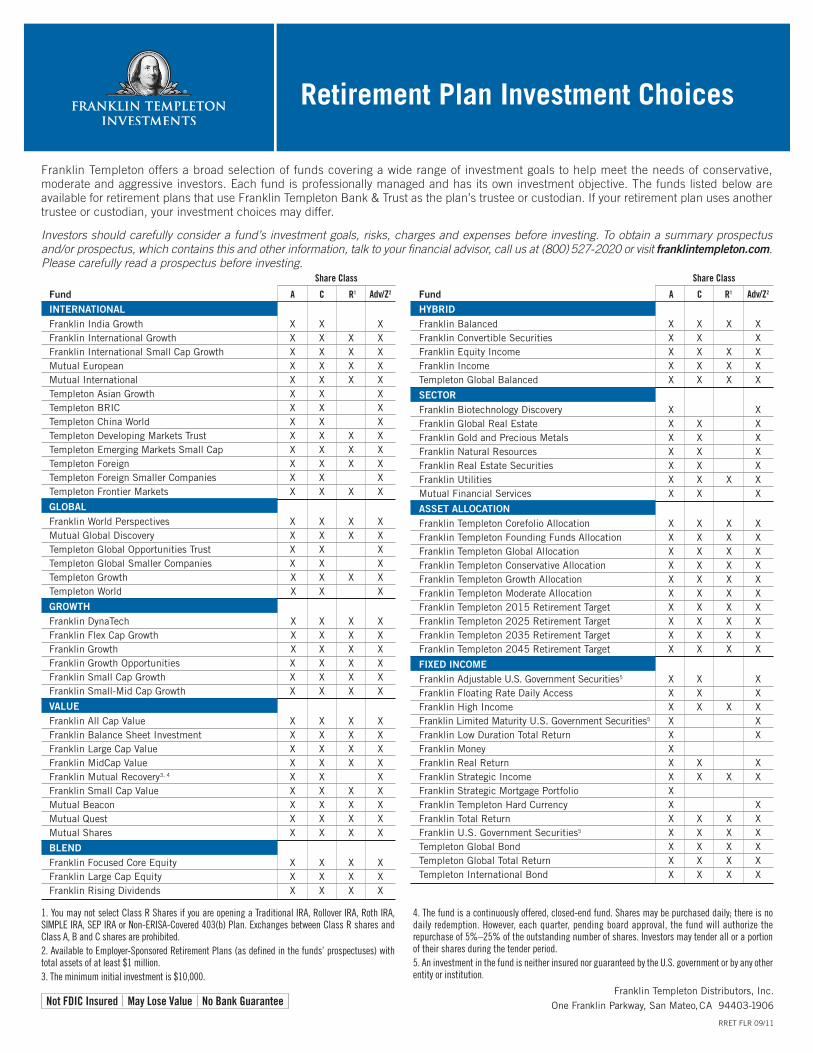

Franklin Templeton offers a broad selection of funds covering a wide range of investment goals to help meet the needs of conservative, moderate and aggressive investors. Each fund is professionally managed and has its own investment objective. The funds listed below are available for retirement plans that use Franklin Templeton Bank & Trust as the plan’s trustee or custodian. If your retirement plan uses anothertrustee or custodian, your investment choices may differ.

Investors should carefully consider a fund’s investment goals, risks, charges and expenses before investing. To obtain a summary prospectusand/or prospectus, which contains this and other information, talk to your financial advisor, call us at (800)527-2020 or visit franklintempleton.com.Please carefully read a prospectus before investing.

Share Class

Fund A C R1 Adv/Z2

INTERNATIONALFranklin India Growth X X XFranklin International Growth X X X XFranklin International Small Cap Growth X X X XMutual European X X X XMutual International X X X XTempleton Asian Growth X X XTempleton BRIC X X XTempleton China World X X XTempleton Developing Markets Trust X X X XTempleton Emerging Markets Small Cap X X X XTempleton Foreign X X X XTempleton Foreign Smaller Companies X X XTempleton Frontier Markets X X X X

GLOBALFranklin World Perspectives X X X XMutual Global Discovery X X X XTempleton Global Opportunities Trust X X XTempleton Global Smaller Companies X X XTempleton Growth X X X XTempleton World X X X

GROWTHFranklin DynaTech X X X XFranklin Flex Cap Growth X X X XFranklin Growth X X X XFranklin Growth Opportunities X X X XFranklin Small Cap Growth X X X XFranklin Small-Mid Cap Growth X X X X

VALUEFranklin All Cap Value X X X XFranklin Balance Sheet Investment X X X XFranklin Large Cap Value X X X XFranklin MidCap Value X X X XFranklin Mutual Recovery3, 4 X X XFranklin Small Cap Value X X X XMutual Beacon X X X XMutual Quest X X X XMutual Shares X X X X

BLENDFranklin Focused Core Equity X X X XFranklin Large Cap Equity X X X XFranklin Rising Dividends X X X X

1. You may not select Class R Shares if you are opening a Traditional IRA, Rollover IRA, Roth IRA, SIMPLE IRA, SEP IRA or Non-ERISA-Covered 403(b) Plan. Exchanges between Class R shares andClass A, B and C shares are prohibited.2. Available to Employer-Sponsored Retirement Plans (as defined in the funds’ prospectuses) withtotal assets of at least $1 million.3. The minimum initial investment is $10,000.

RRET FLR 09/11

4. The fund is a continuously offered, closed-end fund. Shares may be purchased daily; there is nodaily redemption. However, each quarter, pending board approval, the fund will authorize therepurchase of 5%–25% of the outstanding number of shares. Investors may tender all or a portion of their shares during the tender period.5. An investment in the fund is neither insured nor guaranteed by the U.S. government or by any otherentity or institution.

Retirement Plan Investment Choices

Not FDIC Insured | May Lose Value | No Bank GuaranteeFranklin Templeton Distributors, Inc.

One Franklin Parkway, San Mateo,CA 94403-1906

Share Class

Fund A C R1 Adv/Z2

HYBRIDFranklin Balanced X X X XFranklin Convertible Securities X X XFranklin Equity Income X X X XFranklin Income X X X XTempleton Global Balanced X X X X

SECTORFranklin Biotechnology Discovery X XFranklin Global Real Estate X X XFranklin Gold and Precious Metals X X XFranklin Natural Resources X X XFranklin Real Estate Securities X X XFranklin Utilities X X X XMutual Financial Services X X X

ASSET ALLOCATIONFranklin Templeton Corefolio Allocation X X X XFranklin Templeton Founding Funds Allocation X X X XFranklin Templeton Global Allocation X X X XFranklin Templeton Conservative Allocation X X X XFranklin Templeton Growth Allocation X X X XFranklin Templeton Moderate Allocation X X X XFranklin Templeton 2015 Retirement Target X X X XFranklin Templeton 2025 Retirement Target X X X XFranklin Templeton 2035 Retirement Target X X X XFranklin Templeton 2045 Retirement Target X X X X

FIXED INCOMEFranklin Adjustable U.S. Government Securities5 X X XFranklin Floating Rate Daily Access X X XFranklin High Income X X X XFranklin Limited Maturity U.S. Government Securities5 X XFranklin Low Duration Total Return X XFranklin Money XFranklin Real Return X X XFranklin Strategic Income X X X XFranklin Strategic Mortgage Portfolio XFranklin Templeton Hard Currency X XFranklin Total Return X X X XFranklin U.S. Government Securities5 X X X XTempleton Global Bond X X X XTempleton Global Total Return X X X XTempleton International Bond X X X X

• Traditional IRA

• Rollover IRA

• Roth IRA

• SEP IRA

• SIMPLE IRA

Franklin Templeton IRACUSTODIAL AGREEMENTS AND DISCLOSURE STATEMENTS

Not FDIC Insured | May Lose Value | No Bank Guarantee

TABLE OF CONTENTS

Applies to the following products:

Traditional Rollover Roth SEP SARSEP SIMPLEDocuments Page IRA IRA IRA IRA IRA* IRA

Traditional Individual Retirement Custodial Account Agreement . . . . . . . . . . 1

� � � �

Individual Retirement Account Disclosure Statement . . . . . . . . . . . . . . . 4

� � � � �

Roth Individual Retirement Custodial Account Agreement . . . . . . . . . . 6

�

Roth Individual Retirement Account Disclosure Statement . . . . . . . . . 9

�

SIMPLE Individual Retirement Custodial Account Agreement . . . . . . . . . 11 �

* This salary deduction plan was discontinued December 31, 1996 and was effectively replaced by the SIMPLE IRA. However, employers who had already established a SARSEP IRAby that date are able to continue to operate this plan.

Franklin Templeton Traditional Individual Retirement Custodial Account

Under Section 408(a) of the Internal Revenue Code

This Agreement is entered into on the date listednext to the signature(s) on the Application by andbetween the person(s) (each such person beinghereinafter referred to separately as “Depositor”)and the Custodian listed on the Application. TheCustodian’s principal place of business is listed onthe Disclosure Statement provided to the Depositorby the Custodian as required under RegulationsSection 1.408-6.

The Depositor is establishing an Individual RetirementAccount (IRA) [under Section 408(a) of the InternalRevenue Code] to provide for his retirement and forthe support of his beneficiaries after death. TheDepositor has deposited with the Custodian the sumlisted on the Application in cash.

The Depositor and the Custodian make the follow-ing agreement:

ARTICLE I

Except in the case of a rollover contributiondescribed in Section 402(c), 403(a)(4), 403(b)(8),408(d)(3), or 457(e)(16), an employer contribu-tion to a Simplified Employee Pension Plan asdescribed in Section 408(k), or a recharacterizedcontribution described in Section 408A(d)(6), theCustodian will accept only cash contributions up to$3,000 per year for tax years 2003 through 2004.That contribution limit is increased to $4,000 fortax years 2005 through 2007 and $5,000 for2008 and thereafter. For individuals who havereached the age of 50 before the close of the taxyear, the contribution limit is increased to $3,500per year for tax years 2003 through 2004, $4,500for 2005, $5,000 for 2006 and 2007, and$6,000 for 2008 and thereafter. For tax years after2008, the above limits will be increased to reflecta cost-of-living adjustment, if any.

ARTICLE II

The Depositor’s interest in the balance in thecustodial account is nonforfeitable.

ARTICLE III

1. No part of the custodial account funds may beinvested in life insurance contracts, nor may theassets of the custodial account be commingledwith other property except in a common trust fundor common investment fund [within the meaningof Section 408(a)(5)].

2. No part of the custodial account funds may beinvested in collectibles [within the meaning ofSection 408(m)] except as otherwise permitted bySection 408(m)(3), which provides an exception forcertain gold, silver, and platinum coins, coins issuedunder the laws of any state, and certain bullion.

ARTICLE IV

1. Notwithstanding any provision of this agree-ment to the contrary, the distribution of theDepositor’s interest in the custodial account shallbe made in accordance with the following require-ments and shall otherwise comply with Section408(a)(6) and the regulations thereunder, theprovisions of which are herein incorporated byreference.

2. The Depositor’s entire interest in the custodialaccount must be, or begin to be, distributed not later than the Depositor’s required beginningdate, April 1 following the calendar year in whichthe Depositor reaches age 701⁄2. By that date, theDepositor may elect, in a manner acceptable to the Custodian, to have the balance in the custodialaccount distributed in:

(a) A single sum payment or

(b) Payments over a period not longer than the lifeof the Depositor or the joint lives of the Depositorand his or her designated beneficiary.

3. If the Depositor dies before his or her entireinterest is distributed to him or her, the remaininginterest will be distributed as follows:

(a) If the Depositor dies on or after the requiredbeginning date and:

(i) the designated beneficiary is theDepositor’s surviving spouse, the remaininginterest will be distributed over the survivingspouse’s life expectancy as determined eachyear until such spouse’s death, or over theperiod in paragraph (a)(iii) below if longer. Anyinterest remaining after the spouse’s death willbe distributed over such spouse’s remaininglife expectancy as determined in the year of thespouse’s death and reduced by 1 for each sub-sequent year, or, if distributions are beingmade over the period in paragraph (a)(iii)below, over such period.

(ii) the designated beneficiary is not theDepositor’s surviving spouse, the remaininginterest will be distributed over the beneficiary’sremaining life expectancy as determined in theyear following the death of the Depositor andreduced by 1 for each subsequent year, or overthe period in paragraph (a)(iii) below if longer.

(iii) there is no designated beneficiary, theremaining interest will be distributed over theremaining life expectancy of the Depositor asdetermined in the year of the Depositor’s deathand reduced by 1 for each subsequent year.

(b) If the Depositor dies before the required begin-ning date, the remaining interest will be distrib-uted in accordance with (i) below or, if elected orthere is no designated beneficiary, in accordancewith (ii) below:

(i) The remaining interest will be distributed inaccordance with paragraphs (a)(i) and (a)(ii)above [but not over the period in paragraph(a)(iii), even if longer], starting by the end ofthe calendar year following the year of theDepositor’s death. If, however, the designatedbeneficiary is the Depositor’s surviving spouse,

then this distribution is not required to beginbefore the end of the calendar year in whichthe Depositor would have reached age 701⁄2.But, in such case, if the Depositor’s survivingspouse dies before distributions are requiredto begin, then the remaining interest will bedistributed in accordance with (a)(ii) above[but not over the period in paragraph (a)(iii),even if longer], over such spouse’s designatedbeneficiary’s life expectancy, or in accordancewith (ii) below if there is no such designatedbeneficiary.

(ii) The remaining interest will be distributedby the end of the calendar year containing thefifth anniversary of the Depositor’s death.

4. If the Depositor dies before his or her entireinterest is distributed and if the designated benefi-ciary is not the Depositor’s surviving spouse, noadditional contributions may be accepted in theaccount.

5. The minimum amount that must be distributedeach year, beginning with the year containing the Depositor’s required beginning date, is knownas the “required minimum distribution” and isdetermined as follows:

(a) The required minimum distribution underparagraph 2(b) for any year, beginning with theyear the Depositor reaches age 701⁄2, is theDepositor’s account value at the close of businesson December 31 of the preceding year divided by the distribution period in the uniform lifetimetable in Regulations Section 1.401(a)(9)-9.However, if the Depositor’s designated beneficiaryis his or her surviving spouse, the required minimum distribution for a year shall not be morethan the Depositor’s account value at the close of business on December 31 of the preceding yeardivided by the number in the joint life and last sur-vivor table in Regulations Section 1.401(a)(9)-9. The required minimum distribution for a year under this paragraph (a) is determined using theDepositor’s (or, if applicable, the Depositor andspouse’s) attained age (or ages) in the year.

(b) The required minimum distribution underparagraphs 3(a) and 3(b)(i) for a year, beginningwith the year following the year of the Depositor’sdeath [or the year the Depositor would have reachedage 701⁄2, if applicable, under paragraph 3(b)(i)]is the account value at the close of business onDecember 31 of the preceding year divided by the life expectancy [in the single life table inRegulations Section 1.401(a)(9)-9] of the individualspecified in such paragraphs 3(a) and 3(b)(i).

(c) The required minimum distribution for the yearthe Depositor reaches age 701⁄2 can be made aslate as April 1 of the following year. The requiredminimum distribution for any other year must bemade by the end of such year.

6. The owner of two or more Traditional IRAs maysatisfy the minimum distribution requirementsdescribed above by taking from one Traditional IRAthe amount required to satisfy the requirement foranother in accordance with the regulations underSection 408(a)(6).

1

� NEW AGREEMENT � AMENDMENT

Form

5305-A(Rev. March 2002)Department of the Treasury Internal Revenue Service

DO NOT FILE WITH INTERNAL REVENUE SERVICE

x

2

Traditional Individual Retirement Custodial Account Agreement

ARTICLE V

1. The Depositor agrees to provide the Custodianwith all information necessary to prepare anyreports required by Section 408(i) and RegulationsSections 1.408-5 and 1.408-6.

2. The Custodian agrees to submit to the InternalRevenue Service (IRS) and Depositor the reportsprescribed by the IRS.

ARTICLE VI

Notwithstanding any other articles which may beadded or incorporated, the provisions of Articles Ithrough III and this sentence will be controlling.Any additional articles inconsistent with Section408(a) and the related regulations will be invalid.

ARTICLE VII

This agreement will be amended as necessary to comply with the provisions of the Code and the related regulations. Other amendments may be made with the consent of the persons whose signatures appear below.

ARTICLE VIII

1. The Custodian shall invest each custodialaccount contribution as directed by the Depositor.The amount of each contribution to be invested inFranklin Templeton Funds shall be applied to thepurchase of full and fractional shares issued by theFranklin Templeton Fund(s) selected by Depositor.

For purposes of this IRA custodial accountAgreement only, the terms “Franklin TempletonFund” or “Fund” shall mean either an investmentcompany or series of an investment company (a “mutual fund”) whose shares are distributed by Franklin Templeton Distributors, Inc. or aclosed-end mutual fund or real estate investmenttrust (REIT) which is advised by an affiliate ofFranklin Templeton Distributors, Inc.

2. The Depositor has the sole authority and discre-tion to select and direct the investments in thiscustodial account and accepts full and soleresponsibility for any investment selection that is made. Notwithstanding any other provisions ofthis Article, the Custodian reserves the right torefuse to follow any investment direction which theCustodian determines would violate Section 408.A designation by the Depositor of an investment asa rollover contribution shall be deemed irrevocable,and such investment shall be deemed to meet theeligible rollover requirements of the Code.

3. All dividends and capital gains distributionsreceived on shares of a Franklin Templeton Fundheld in the custodial account shall be reinvestedin additional shares of the same Fund unless theDepositor (or Beneficiary, if applicable) affirmativelyelects otherwise.

4. The Custodian shall forward to the Depositor(or Beneficiary, if applicable) any notices, prospec-tuses, financial statements, proxies and proxysoliciting materials relating to shares issued by a mutual fund whose shares are distributed by anaffiliate of Custodian (each a “Franklin TempletonFund”) and held in this custodial account(“Account”). Each such mailing shall be effective

if sent by mail to the Depositor (or Beneficiary, if applicable) at his or her last address on recordwith the Custodian. By establishing this Account,the Depositor directs the Custodian to vote FranklinTempleton Fund shares held in the Account forwhich no voting instructions are timely received in the same proportion as shares timely voted bysuch Fund’s other shareholders.

5. Any income taxes or other taxes of any kind thatmay be levied or assessed upon the custodialaccount, any administrative expenses incurred bythe Custodian in the performance of its duties,including fees for legal services rendered to theCustodian, and the maintenance fees to theCustodian as set forth in paragraph 6 of this Article,shall be paid from assets of the custodial accountin such manner as the Custodian may determine.

6. The Custodian shall charge a custodial accountmaintenance fee, in the amount specified in theApplication, on a per beneficial account ownerbasis. This maintenance fee shall be collected fromthe IRA custodial account (a) in December of eachyear; and (b) at the time this account is closed or atthe time of any redemption request that wouldcause the value of assets in this account to fallbelow the amount of the maintenance fee (at whichtime this account will be closed). The beneficialaccount owner may elect to pay this fee separatelyby check only if payment is received before the feeis scheduled to be deducted from the custodialaccount. The Custodian shall have the right tochange this maintenance fee, from time to time,upon thirty (30) days prior written notice to thebeneficial account owner.

7. “Beneficiary” shall mean the person or persons(including a trust or estate) designated as such bythe Depositor or, following the death of the Depositor,designated as such by a Beneficiary (each personmaking such beneficiary designations is referred to as a “Designator”). Such designation shall be(a) in writing on a form provided by the Custodianfor such purpose, or in such other written formatacceptable to the Custodian, (b) signed by eachDesignator and (c) received by the Custodian priorto the Designator’s death. The Custodian may relyupon the last written designation received at the Custodian’s office which shall revoke all priordesignations and such designation shall apply toall custodial account assets, including each FundAccount opened and maintained in this custodialaccount. Unless indicated otherwise on the applicationor designation form, if any primary or contingentbeneficiary dies before the Designator, the interestattributable to such beneficiary and to his heirs shallterminate completely and the percentage share ofany remaining beneficiary(ies) shall be increasedon a pro rata basis. If none of the Designator’s primarybeneficiaries survive him, the interest in his IRAshall pass to his contingent beneficiary(ies), if named.If no designated beneficiary survives the Designatoror if no ascertainable beneficiary is designated, theDesignator’s Beneficiary shall be his spouse or, if hehas no surviving spouse, his estate. A Beneficiary(other than a minor or otherwise under a legal disability,as addressed in Section 8 of this Article) with a presentinterest shall have sole authority and investmentdiscretion with respect to the portion of the custodialaccount to which he is entitled and accept full and soleresponsibility for any investment selection that is made.

The Depositor should ensure that Beneficiary contactinformation on file with the Custodian remainscurrent and accurate. If, upon notification of the

death of the Depositor, the Custodian is unable to find the Beneficiary, the Custodian may engagean outside search company to attempt to find theBeneficiary. Upon locating the Beneficiary, the searchcompany may charge the Beneficiary a percentage(agreed upon by both parties) of the value of thecustodial account as a fee in exchange for itslocation services to establish contact between theBeneficiary and the Custodian. The Beneficiaryshall remain responsible for all taxes connectedwith distributions (including any portion thereofauthorized as payment to the search company)from the custodial account.

8. If upon the death of the Depositor (orBeneficiary) the custodial account is payable to aperson known by the Custodian to be a minor orotherwise under a legal disability, the Custodianmay, in its absolute discretion, make all, or anypart of the distribution to (a) a parent of suchperson, (b) the guardian, conservator, or other legalrepresentative, wherever appointed, of such person,(c) a custodial account established under a UniformGifts to Minors, Uniform Transfers to Minors Act,or similar act, (d) any person having control orcustody of such person, or (e) to such person directly.

9. The Custodian will keep records of all receipts,investments, disbursements, and other transactionsfor this custodial account and for each FundAccount. As soon as is practicable after the closeof each calendar year, and whenever required bythe Code, the Custodian shall deliver to theDepositor (or Beneficiary, if applicable) a writtenreport(s) reflecting all activity in the custodialaccount during the prior calendar year and the fairmarket value of the custodial account. Upon theexpiration of sixty (60) days after the Custodianhas furnished such written report(s) to theDepositor (or Beneficiary), the Custodian shall bereleased and discharged from all liability andaccountability with respect to any such acts ortransactions except those to which the Depositor(or Beneficiary) has filed written objections withthe Custodian within the sixty (60) day period afterthe calendar year.

10. The Depositor shall have sole responsibilityfor determining whether any contribution, conver-sion, or distribution shall be permitted, including(but not limited to) the determination of the allow-able amount and tax effect of any such transac-tion to or from the custodial account. TheDepositor shall also be responsible for reporting onhis personal tax return, whenever required by theInternal Revenue Service, any transaction made toor from the custodial account.

11. The Custodian shall have the right to amendthis Agreement in any manner it deems necessaryor advisable in order to qualify (or maintain qualifi-cations of) this Agreement under the applicableprovisions of the Code or to maintain proper anddesirable operation of this custodial account. Anysuch amendment shall be effected by delivery tothe Depositor (or Beneficiary, if applicable) of arestatement of this Agreement including any suchamendment. The Depositor (or Beneficiary) shallbe deemed to consent to any such amendment(s)if he fails to object thereto by written noticereceived by the Custodian within fifteen (15)calendar days from the date of the Custodian’smailing to the Depositor (or Beneficiary) a copy of such amendment(s) or restatement.

Questions? Please call your financial advisor or Franklin Templeton Retirement Services at (800) 527-2020.

12. The Depositor shall have the right to terminatethis custodial account or to remove the Custodianupon thirty (30) days prior written notice to theCustodian, which notice shall include instructionsregarding the final distribution or transfer of allcustodial account assets. If the Depositor fails toprovide such distribution or transfer instructions,the Custodian may terminate this custodial accountby distributing all custodial account assets (lessamounts required to satisfy unpaid fees, costs,expenses and obligations) directly to the Depositor.

13. The Custodian shall have the right to resignas custodian under this Agreement upon thirty(30) days prior written notice to the Depositor (orBeneficiary, if applicable). Unless the Depositor(or Beneficiary) provides written instructions to thecontrary, the Custodian shall have the right toappoint and transfer the custodial account assets(less amounts required to satisfy unpaid fees,costs, expenses, and obligations), together withcopies of relevant books and records, to a successorcustodian. A successor custodian shall satisfy therequirements of Section 408(a)(2). The Custodianis not liable for the acts or omissions of anysuccessor custodian.

14. The Custodian is authorized to perform allacts necessary to carry out the terms of thisAgreement and to hire an agent to perform certainof its duties hereunder, which agent may be theTransfer Agent for the Fund (if such transfer agentis other than the Custodian).

15. Distribution requests that are received by the Custodian in good order will be made to theDepositor, his beneficiary (if appropriate), or asuccessor custodian, normally within five (5) business days. To be in good order, distributionrequests must meet the IRA distribution require-ments of the Custodian. The Custodian reservesthe right to change these requirements at anytime without prior notice to the Depositor (orBeneficiary, if applicable).

16. The Custodian may transfer custodial accountassets to a successor custodian named by theDepositor (or Beneficiary, if applicable) in relianceon, and without any duty of investigation, receiptof a letter of acceptance signed by an individualclaiming to be an authorized officer or principalof the successor custodian. The Depositor (orBeneficiary) shall be responsible for satisfying theminimum distribution rule in Section 408(a)(6),if applicable, prior to such transfer. Furthermore,if a Beneficiary is requesting the transfer, suchBeneficiary shall be solely responsible for ensuringthat the transfer is made to an IRA registered in the Depositor’s name in order to maintain thetax-deferred status of the IRA.

17. The Custodian does not assume any responsi-bility to make any distributions unless and until theDepositor (or Beneficiary, if applicable) specifies ina manner acceptable to the Custodian. Furthermore,the Custodian shall not be responsible to makeminimum distributions other than upon theDepositor’s or Beneficiary’s, as applicable, expressedwritten instructions as herein provided.

18. The terms and conditions of this Agreementshall be applicable without regard to the commu-nity property laws of any state.

19. This Agreement shall be construed under thelaws of the State of California.

20. IN WITNESS WHEREOF, the acceptance ofthis Agreement by the Depositor is indicated by theDepositor’s signature in the Custodian’sApplication, and the Custodian, to evidenceacceptance of this Agreement, has signed theAgreement as written below.

Authorized SignatureFranklin Templeton Bank & Trust, F.S.B., Custodian:

XMichael Mee, President

GENERAL INSTRUCTIONSSection references are to the Internal RevenueCode unless otherwise noted.

PURPOSE OF FORM Form 5305-A is a modelaccount agreement that meets the requirements ofSection 408(a) and has been pre-approved by theIRS. A Traditional Individual Retirement Account(Traditional IRA) is established after the form isfully executed by both the individual (Depositor)and the Custodian and must be completed no laterthan the due date of the individual’s income taxreturn for the tax year (excluding extensions). Thisaccount must be created in the United States forthe exclusive benefit of the Depositor or his or herbeneficiaries.

Do not file Form 5305-A with the IRS. Instead,keep it for your records. For more information onIRAs, obtain IRS Publication 590, IndividualRetirement Arrangements (IRAs).

DEFINITIONS

CUSTODIAN The Custodian must be a bank orsavings and loan association, as defined in Section408(n), or any person who has the approval of theIRS to act as custodian.

DEPOSITOR The Depositor is the person whoestablishes the custodial account.

IDENTIFYING NUMBER The Depositor’s SocialSecurity number will serve as the identificationnumber of his or her IRA. An employer identifica-tion number (EIN) is required only for an IRA forwhich a return is filed to report unrelated businesstaxable income. An EIN is required for a commonfund created for IRAs.

TRADITIONAL IRA FOR NONWORKING SPOUSEForm 5305-A may be used to establish the IRAcustodial account for a nonworking spouse.Contributions to an IRA custodial account for a nonworking spouse must be made to a sepa-rate IRA custodial account established by thenonworking spouse.

SPECIFIC INSTRUCTIONS

ARTICLE IV Distributions made under this Articlemay be made in a single sum, periodic payments,or a combination of both. The distribution optionshould be reviewed in the year the Depositorreaches age 701⁄2 to insure that the requirements of Section 408(a)(6) have been met.

Form 5305-A (Rev. March 2002)

3

12/10

Individual Retirement Account Disclosure Statement

The following information is provided to you inaccordance with the requirements of the InternalRevenue Code (the “Code”) and should be reviewedin conjunction with both the Custodial Agreementand the Application for your Individual RetirementAccount (“IRA”). Your IRA is a tax-deferred custodialaccount, created for your exclusive benefit, andamounts held in it are generally not taxed untildistributed. Your interest in your IRA is at all timesnonforfeitable.

RIGHT TO REVOKE

You may revoke this custodial account at any timewithin seven (7) calendar days after it is establishedby mailing or delivering a written request [includingyour name, Social Security number, and thename(s) of your investment option(s)] for revocationto the Custodian, Franklin Templeton Bank & Trust,F.S.B., at: One Franklin Parkway, San Mateo, CA94403-1906 [Phone: (800) 527-2020].

IRA CONTRIBUTIONS

You are eligible to make regular contributions intoan IRA for a calendar year (in which you are underage 701⁄2) if you have received compensationduring that year from the performance of personalservices. [Please see Table A (below) for contribu-tion limits.] Compensation includes such items assalaries, bonuses, commissions, and, in the caseof a self-employed individual, net earnings fromself-employment. All taxable alimony and separatemaintenance payments received by an individualunder a divorce decree or a separate maintenanceagreement are also treated as compensation.

TABLE A: Traditional IRA Contribution LimitsTax Year If Under Age 50 If Age 50 or Over

2010 $5,000 $6,000

2011 $5,000 $6,000

The different types of IRAs and each respectivecontribution limit are set forth as follows:

TRADITIONAL IRA You may make a TraditionalIRA contribution up to the Traditional IRA contri-bution limit or 100% of your compensation,whichever is less, for each tax year.

SPOUSAL IRA If you file a joint federal tax returnand your spouse earns less than the Traditional IRAcontribution limit, you may set up two custodialaccounts—one IRA for yourself and one for yourspouse (“Spousal IRA”). You can contribute thelesser of (1) the Traditional IRA contribution limitfor each spouse or (2) 100% of your combinedcompensation between the two IRAs, so long asno more than the Traditional IRA contribution limitis contributed to either IRA. If you have reachedage 701⁄2, but your spouse is still under that age, youmay still be able to contribute up to the TraditionalIRA contribution limit (or 100% of your combinedcompensation, if less) to your spouse’s IRA.

ROLLOVER IRA If you retire or change jobs, youmay be eligible for a distribution from youremployer’s retirement plan. To avoid mandatorywithholding of 20% of your distribution, and topreserve the tax-deferred status of the distribution,you can roll it over directly to a Rollover IRA. If youchoose to have the distribution paid directly to you,20% withholding will apply. You may still reinvestup to 100% of the total amount of your distribu-tion, which is eligible for rollover treatment, byreplacing the 20% that was withheld for federaltaxes with other assets you may own. You generallyhave 60 days of receipt of your distribution to roll itover. The amount invested in a Rollover IRA will notbe included in your taxable income for the year inwhich you received the plan distribution. Rolloverscan also be made from distributions from anotherIRA, and may be made from each IRA only onceduring any 12-month period.

SEP IRA Your employer may establish a separateIRA for use as part of a Simplified EmployeePension Plan (“SEP”) arrangement. Your employermay contribute to your SEP IRA up to a maximum25% of your compensation or $49,000 for 2010and 2011, whichever is less. In addition to theSEP contributions made on your behalf by youremployer, you may contribute to a Traditional IRA,although the amount you are able to deduct maybe limited (see “Deductibility of IRA Contributions”below for further information).

SIMPLE IRA SIMPLE stands for “savings incentivematch plan for employees” and is a plan that allowsyou to contribute on your own behalf through salaryreduction contributions. You may defer up to$11,500 annually for 2010 and 2011, and youremployer will either match the first 3% that youdefer, or will contribute 2% of each eligibleemployee’s compensation. In two of every five years,your employer may elect to match less than the first3% you defer, but cannot match less that 1%.[Please see Table B (below) for contribution limits.]All SIMPLE contributions are made to your IRA, andare subject to the rules which govern IRA distributions(see IRA Distributions), except that distributionstaken within two years of participating in a SIMPLEare subject to a 25% penalty tax, unless an exceptionapplies. Only employers who have 100 eligibleemployees or fewer and do not maintain other retire-ment plans may sponsor a SIMPLE.

TABLE B: SIMPLE IRA Contribution LimitsTax Year If Under Age 50 If Age 50 or Over

2010 $11,500 $14,000

2011 $11,500 $14,000

SARSEP IRA Your employer may allow you tocontribute on your own behalf to the SEP Planthrough a salary reduction SEP (“SARSEP”)arrangement. This will enable you to reduce yourannual compensation up to a maximum of 25%of your compensation (adjusted for deferrals) or

$16,500 for 2010 and 2011, whichever is less.[Please see Table C (below) for contribution limits.]If your employer maintains both a SARSEP and aregular SEP, the annual combined contribution limitis still 25% of your compensation (adjusted fordeferrals) or $49,000 for 2010 and 2011,whichever is less. Only employers with 25 or fewereligible employees may establish a SARSEParrangement, and at least 50% of those eligiblemust participate. No new SARSEP plans may be established after December 31, 1996. Existing SARSEP plans may be maintained withthe previously mentioned conditions and employeeshired after December 31, 1996 may still partici-pate in previously existing SARSEPs.

TABLE C: SARSEP IRA Contribution LimitsTax Year If Under Age 50 If Age 50 or Over

2010 $16,500 $22,000

2011 $16,500 $22,000

EXCESS CONTRIBUTIONS

Contributions which exceed the allowable maximumlimits per year are considered excess contributions.A nondeductible penalty tax of 6% of the excessamount contributed will be incurred for each yearin which the excess remains in your IRA. If youmake a contribution [or your employer makes aSEP (including SARSEP) contribution on yourbehalf] which is not eligible to be deducted for a tax year, the 6% penalty may be avoided bywithdrawing the excess contribution and its earningsby your tax filing deadline, including extensions,for that year. Although the excess contributionwithdrawn is not taxable, the earnings will beincluded as income for the tax year the excesswas made and may be subject to a 10% prematurepenalty tax if you are under age 591⁄2.

After your tax filing deadline, only IRA contributionsin excess of the “lesser of 100% of compensationor the Traditional IRA contribution limit” may bewithdrawn. Provided that the total IRA contributionyou made for the year did not exceed theTraditional IRA contribution limit, the amount of any excess contribution withdrawn will not beconsidered a premature distribution nor (except in the case of a salary reduction contribution) be taxed as ordinary income.

TIME OF CONTRIBUTION

Contributions to your IRA may be made any timeup to and including the due date for filing yourtax return for the year (not including extensions).Employer contributions to a SEP IRA may bemade up by the employer’s tax filing deadlineincluding extensions.

Questions? Please call your financial advisor or Franklin Templeton Retirement Services at (800) 527-2020.4

Form 5305-A (Rev. March 2002)

DEDUCTIBILITY OF IRA CONTRIBUTIONSThe deductibility of your IRA contributions willdepend upon whether you are an “active partici-pant.” An “active participant” is one who is, atany time during the year, covered by a “retirementplan” of an employer or union under whichemployer or employee contributions are made, or one is eligible to earn retirement credits,regardless of vested status. For these purposes,“retirement plans” includes profit sharing plans,government plans (other than a 457 plan), taxsheltered annuity arrangements or 403(b) custo-dial accounts, SEP IRAs, 401(k), SIMPLE, anddefined benefit plans. Active participation in a retirement plan for a given year is generallyindicated on one’s Form W-2.

If you are single and not an active participant (asdefined above), your IRA contributions are fullydeductible (up to 100% of your compensation orthe Traditional IRA contribution limit, whichever isless). You are also entitled to the same if you aremarried and neither you nor your spouse is anactive participant.

If your combined Adjusted Gross Income (“AGI”)is in excess of $169,000 in 2011 ($167,000 in2010), your spouse’s active participation in aretirement plan automatically makes you an activeparticipant for purposes of determining deductibil-ity of your IRA contribution. Also, if your combinedAGI is between 169,000 and 179,000 in 2011($167,000 and $177,000 in 2010), and you arenot an active participant, you can make a partiallydeductible IRA contribution. If your combined AGIis less than $169,000 in 2011 ($167,000 in2010), your spouse’s active participation in a retirement plan will have no effect on whetheryou are considered an active participant. If youand your spouse file separate tax returns (and youlive apart for the entire year), your spouse’s activeparticipation in a retirement plan will not affectthe deductibility of your IRA contribution.

If you are an active participant, you must look atyour Adjusted Gross Income (“AGI”) for the year(if you filed a joint tax return with your spouse, useyour combined AGI) to determine your deductibleIRA contribution. Your tax return will show you howto calculate your AGI for this purpose. If you are ator below a certain AGI level, called the ThresholdLevel, you are treated as if you were not an activeparticipant and can deduct your entire IRA contri-bution (up to 100% of your compensation or theTraditional IRA contribution limit, whichever is less).

If you are single, your Threshold Level is $56,000in 2010 and 2011. The Threshold Level, if youare married and file a joint tax return, is $90,000for 2011 ($89,000 for 2010), and if you are marriedbut file a separate tax return, the threshold levelis $0 for 2010 and 2011.

If your AGI is less than $10,000 above your ThresholdLevel, you are still entitled to a partial IRA deduction.To determine this amount, subtract your AGI from$66,000 for 2010 or 2011 if you are single, or$110,000 for 2011 ($109,000 for 2010) if youare married, filing jointly. Multiply the result by .20.This is your deductible amount. If your deductibleamount is not a multiple of $10, round up to thenext highest $10. If your deductible amount isbetween $1 and $199, you are still entitled todeduct $200. If all or any part of your IRA contribu-tion is nondeductible, you must indicate this amounton your tax return by completing IRS Form 8606.

IRA DISTRIBUTIONSDistributions from your IRA are taxed at ordinaryincome tax rates. However, if you have made non-deductible contributions to your IRA, a portion ofeach distribution you receive will be considered a partial return of those contributions and will not be taxed. Use IRS Form 8606 to compute the nontaxable portion of your IRA distribution.Distributions from your IRA do not qualify for capital gains treatment, nor do they qualify for the 10-year forward averaging tax treatment that isavailable to certain qualified plan distributions.When you are ready to take a distribution, pleasecontact Franklin Templeton Bank & Trust to obtain current information regarding distributionprocedures and any forms you may require.

PREMATURE DISTRIBUTIONS A distributionyou receive prior to reaching age 591⁄2 is subjectto a 10% federal tax penalty, in addition to ordinary income tax. There is no 10% tax penaltyfor distributions made because of: (i) death,permanent disability, distributions “rolled over”within 60 days of receipt or timely removal of anexcess contribution, (ii) distributions in the formof substantially equal periodic payments (not lessfrequently than annually) over your life expectancy(or the joint life expectancies of you and yourbeneficiary) made in accordance with Section 72(t)of the Code, (iii) deductible medical expenses, (iv) medical insurance payments for recipients of unemployment compensation for at least 12consecutive weeks, (v) higher education expensesfor you, your spouse, your child or grandchild, (vi) expenses related to the purchase of your firstprincipal residence in two years ($10,000 lifetimecap), or (vii) a direct payment to the government tosatisfy a federal tax levy.

MINIMUM DISTRIBUTION REQUIREMENTSYou must begin distributions from your IRA byApril 1 following the calendar year you reach age701⁄2. The assets in your IRA at that time may bedistributed in a single payment, or in substantiallyequal monthly, quarterly, or annual payments overa uniform distribution period that is determined byusing a single table and your actual age attained inthe distribution year regardless of whether or notyou have named a beneficiary. An exceptionapplies if your spouse is your sole beneficiary forthe entire year and is more than 10 years youngerthan you are. In that case, your distributions mustbe made over a period not longer than the joint lifeexpectancy of you and your spouse. (The IRSprovides a Uniform Lifetime Table, available inPublication 590, for this purpose.) Subsequentdistributions must be made by December 31 ofeach calendar year, starting with the calendar yearcontaining your required beginning date.

ON TRANSFERS AND ROLLOVERS Should youtransfer or roll over assets in your custodial accountto another custodian or trustee, the minimum distri-bution rules, if applicable, for such amounts mustbe met prior to the transfer or rollover.

AT DEATH Should you die after minimum distribu-tions have begun, the remaining balance of thecustodial account must generally be distributed toyour beneficiary over a period that does not exceedhis life expectancy. Generally, if you die beforedistributions have commenced, the entire fundmust be distributed within 5 years after yourdeath. However, the five-year rule does not apply

if distributions begin by December 31 of the yearafter your death and are made to your beneficiaryover his life expectancy. If your spouse is yourbeneficiary, distributions are not required until thetime you would have attained age 701⁄2.

INHERITED IRAS If your beneficiary is yoursurviving spouse, he may elect to treat your entireinterest in the IRA as his own IRA, subject to theTraditional IRA distribution requirements.

UNDER-DISTRIBUTION PENALTY If you reachage 701⁄2 and the amount distributed to you or yourbeneficiary in any year is less than the amountrequired to be distributed, you or your beneficiarywill be subject to a federal excise tax equal to 50%of any such deficiency.

FEDERAL ESTATE AND GIFT TAXESAmounts payable to your spouse as beneficiary of your IRA may qualify for the estate tax maritaldeduction. An election under an IRA to have adistribution payable to your beneficiary on yourdeath will not be treated as a gift subject to federalgift tax as long as you are able to change yourbeneficiary.

PROHIBITED TRANSACTIONS AND LOANSIf you or your beneficiary engage in a “prohibitedtransaction” as described in the Code, whichincludes borrowing from your IRA or pledging yourIRA as security for a loan, your IRA will lose its taxexemption. In that event, you will be taxed on thefull market value of the assets in the custodialaccount on the first day of the year in which theprohibited transaction occurred, and you will alsobe subject to a 10% penalty tax if you are underage 591⁄2 and not permanently disabled.

FILING WITH THE IRSContributions to your IRA must be reported on yourtax return (Form 1040 or 1040A, and Form 8606for nondeductible IRA contributions) for thetaxable year contributed. You (or your beneficiary)must also file Form 5329 if you (or your benefici-ary) are subject to any of the federal penalty taxesdue to excess contributions, premature distribu-tions, excess distributions, or under-distributions.

IRS APPROVALThe form of your Individual Retirement Accounthas been approved by the Internal RevenueService. The approval is a determination only asto the form and does not represent a determinationof the merits of the custodial account. Furtherinformation concerning IRAs can be obtained fromany district office of the Internal Revenue Service.In particular, please obtain a copy of IRS Publication590, Individual Retirement Arrangements (IRAs).

The significant changes to retirement planscontained in EGTRRA pertain only to federal tax law. To determine whether your state hasadopted conforming laws, you should consult withyour tax or financial advisor.

5

Questions? Please call your financial advisor or Franklin Templeton Retirement Services at (800) 527-2020.6

This Agreement is entered into on the date listednext to the signature(s) on the Application by andbetween the person(s) (each such person beinghereinafter referred to separately as “Depositor”)and the Custodian listed on the Application. TheCustodian’s principal place of business is listed onthe Disclosure Statement provided to the Depositorby the Custodian as required under RegulationsSection 1.408-6.

The Depositor is establishing a Roth IndividualRetirement Account (Roth IRA) under Section 408Ato provide for his retirement and for the support ofhis beneficiaries after death. The Depositor hasdeposited with the Custodian the sum listed on theApplication in cash.

The Depositor and the Custodian make the follow-ing agreement:

ARTICLE I

1. Except in the case of a rollover contributiondescribed in Section 408A(e), a recharacterizedcontribution described in Section 408A(d)(6), oran IRA Conversion Contribution, the Custodian will accept only cash contributions up to $3,000per year for tax years 2003 through 2004. Thatcontribution limit is increased to $4,000 for taxyears 2005 through 2007 and $5,000 for 2008and thereafter. For individuals who have reachedthe age of 50 before the close of the tax year, thecontribution limit is increased to $3,500 per yearfor tax years 2003 through 2004, $4,500 for2005, $5,000 for 2006 and 2007, and $6,000for 2008 and thereafter. For tax years after 2008,the above limits will be increased to reflect a cost-of-living adjustment, if any.

ARTICLE II

1. The annual contribution limit described inArticle I is gradually reduced to $0 for higherincome levels. For a single Depositor, the annualcontribution is phased out between adjusted grossincome (AGI) of $95,000 and $110,000; for amarried Depositor filing jointly, between AGI of$150,000 and $160,000; and for a marriedDepositor filing separately, between AGI of $0 and$10,000.1 In the case of a conversion, theCustodian will not accept IRA ConversionContributions in a tax year if the Depositor’s AGIfor the tax year the funds were distributed from theother IRA exceeds $100,000 or if the Depositor ismarried and files a separate return. Adjusted grossincome is defined in Section 408A(c)(3) and doesnot include IRA Conversion Contributions.2

2. In the case of a joint return, the AGI limits inthe preceding paragraph apply to the combinedAGI of the Depositor and his or her spouse.

ARTICLE III

The Depositor’s interest in the balance in thecustodial account is nonforfeitable.

ARTICLE IV

1. No part of the custodial account funds may beinvested in life insurance contracts, nor may theassets of the custodial account be commingledwith other property except in a common trust fundor common investment fund [within the meaningof Section 408(a)(5)].

2. No part of the custodial account funds may beinvested in collectibles [within the meaning ofSection 408(m)] except as otherwise permitted bySection 408(m)(3), which provides an exception forcertain gold, silver, and platinum coins, coins issuedunder the laws of any state, and certain bullion.

ARTICLE V

1. If the Depositor dies before his or her entireinterest is distributed to him or her and theDepositor’s surviving spouse is not the designatedbeneficiary, the remaining interest will be distrib-uted in accordance with (a) below or, if elected orthere is no designated beneficiary, in accordancewith (b) below:

(a) The remaining interest will be distributed,starting by the end of the calendar year followingthe year of the Depositor’s death, over the desig-nated beneficiary’s remaining life expectancy as determined in the year following the death ofthe Depositor. (b) The remaining interest will be distributed bythe end of the calendar year containing the fifthanniversary of the Depositor’s death.

2. The minimum amount that must be distributedeach year under paragraph 1(a) above is theaccount value at the close of business onDecember 31 of the preceding year divided by the life expectancy [in the single life table inRegulations Section 1.401(a)(9)-9] of the desig-nated beneficiary using the attained age of the beneficiary in the year following the year of the Depositor’s death and subtracting 1 from the divisor for each subsequent year.

3. If the Depositor’s surviving spouse is the desig-nated beneficiary, such spouse will then be treatedas the Depositor.

ARTICLE VI

1. The Depositor agrees to provide the Custodianwith all information necessary to prepare any reportsrequired by Sections 408(i) and 408A(d)(3)(E),Regulations Sections 1.408-5 and 1.408-6, orother guidance published by the Internal RevenueService (IRS).

2. The Custodian agrees to submit to the IRS andDepositor the reports prescribed by the IRS.

ARTICLE VII

Notwithstanding any other articles, which may beadded or incorporated, the provisions of Articles Ithrough IV and this sentence will be controlling.Any additional articles that are not consistent withSection 408A, the related regulations, and otherpublished guidance will be invalid.

ARTICLE VIIIThis agreement will be amended as necessary tocomply with the provisions of the Code, the relatedregulations, and other published guidance. Otheramendments may be made with the consent of thepersons whose signatures appear below.

ARTICLE IX1. The Custodian shall invest each custodialaccount contribution as directed by the Depositor.The amount of each contribution to be invested inFranklin Templeton Funds shall be applied to thepurchase of full and fractional shares issued by theFranklin Templeton Fund(s) selected by Depositor.

For purposes of this Agreement only, the terms“Franklin Templeton Fund” or “Fund” shall meaneither an investment company or series of aninvestment company (a “mutual fund”) whoseshares are distributed by Franklin TempletonDistributors, Inc. or a closed-end mutual fund orreal estate investment trust (REIT) which isadvised by an affiliate of Franklin TempletonDistributors, Inc.

2. The Depositor has the sole authority and discre-tion to select and direct the investments in thiscustodial account and accepts full and soleresponsibility for any investment selection that ismade. Notwithstanding any other provisions of thisArticle, the Custodian reserves the right to refuseto follow any investment direction which theCustodian determines would violate Section 408A.A designation by the Depositor of an investment asa rollover contribution shall be deemed irrevocable,and such investment shall be deemed to meet theeligible rollover requirements of the Code.

3. All dividends and capital gains distributionsreceived on shares of a Franklin Templeton Fundheld in the custodial account shall be reinvestedin additional shares of the same Fund unless the Depositor (or Beneficiary, if applicable) affir-matively elects otherwise.

4. The Custodian shall forward to the Depositor (or Beneficiary, if applicable) any notices, prospec-tuses, financial statements, proxies and proxysoliciting materials relating to shares issued by a mutual fund whose shares are distributed by

Franklin Templeton Roth Individual Retirement Custodial Account

Under Section 408A of the Internal Revenue Code

� NEW AGREEMENT � AMENDMENT

Form

5305-RA(Rev. March 2002)Department of the Treasury Internal Revenue Service

x

DO NOT FILE WITH INTERNAL REVENUE SERVICE

1. Revised limits for 2010 and 2011: For a single Depositor, the annual contribution is phased out between adjusted gross income (AGI) of $105,000 and $120,000 in 2010 or $107,000 and $122,000 in 2011;for a married Depositor filing jointly, between AGI of $167,000 and $177,000 in 2010 or $169,000 and $179,000 in 2011; and for a married Depositor filing separately, between AGI of $0 and $10,000 in2010 or 2011.2. Starting 2010, the $100,000 AGI limit on Roth IRA Conversions Contributions does not apply.

an affiliate of Custodian (each a “Franklin TempletonFund”) and held in this custodial account(“Account”). Each such mailing shall be effectiveif sent by mail to the Depositor (or Beneficiary, ifapplicable) at his or her last address on recordwith the Custodian. By establishing this Account,the Depositor directs the Custodian to voteFranklin Templeton Fund shares held in theAccount for which no voting instructions are timelyreceived in the same proportion as shares timelyvoted by such Fund’s other shareholders.

5. Any income taxes or other taxes of any kind thatmay be levied or assessed upon the custodialaccount, any administrative expenses incurred bythe Custodian in the performance of its duties,including fees for legal services rendered to theCustodian, and the maintenance fees to theCustodian as set forth in paragraph 6 of this Article,shall be paid from assets of the custodial accountin such manner as the Custodian may determine.

6. The Custodian shall charge a custodial mainte-nance fee, as specified on the Application, perbeneficial owner. The Custodian shall deduct themaintenance fee from any Fund Account during orimmediately preceding each calendar year, at thetime of the initial investment, or at the time theDepositor (or Beneficiary, if applicable) redeemsan amount from the custodial account whichcauses the custodial account balance to be lessthan the maintenance fee. The Depositor (orBeneficiary) may pay this fee separately by checkonly if payment is received before the fee is sched-uled to be deducted from the custodial account.The Custodian shall have the right to change itsmaintenance fee upon thirty (30) days prior writtennotice to the Depositor (or Beneficiary, if applicable).

7. “Beneficiary” shall mean the person or persons(including a trust or estate) designated as such by the Depositor or, following the death of theDepositor, designated as such by a Beneficiary(each person making such beneficiary designationis referred to as a “Designator”). Such designationshall be (a) in writing on a form provided by theCustodian for such purpose, or in such other writtenformat acceptable to the Custodian, (b) signed byeach Designator and (c) received by the Custodianprior to the Designator’s death. The Custodian mayrely upon the last written designation received atthe Custodian’s office which shall revoke all priordesignations and such designation shall apply toall custodial account assets, including each FundAccount opened and maintained in this custodialaccount. Unless indicated otherwise on the appli-cation or designation form, if any primary orcontingent beneficiary dies before the Designator,the interest attributable to such beneficiary andto his heirs shall terminate completely and thepercentage share of any remaining beneficiary(ies)shall be increased on a pro rata basis. If none ofthe Designator’s primary beneficiaries survive him,the interest in his IRA shall pass to his contingentbeneficiary(ies), if named. If no designated benefi-ciary survives the Designator or if no ascertainablebeneficiary is designated, the Designator’s Beneficiaryshall be his spouse or, if he has no surviving spouse,his estate. A Beneficiary (other than a minor orotherwise under a legal disability, as addressed inSection 8 of this Article) with a present interestshall have sole authority and investment discretionwith respect to the portion of the custodial accountto which he is entitled and accept full and soleresponsibility for any investment selection that is made.

The Depositor should ensure that Beneficiary contactinformation on file with the Custodian remains currentand accurate. If, upon notification of the death ofthe Depositor, the Custodian is unable to find theBeneficiary, the Custodian may engage an outsidesearch company to attempt to find the Beneficiary.Upon locating the Beneficiary, the search companymay charge the Beneficiary a percentage (agreedupon by both parties) of the value of the custodialaccount as a fee in exchange for its location servicesto establish contact between the Beneficiary and the Custodian. The Beneficiary shall remainresponsible for all taxes connected with distributions(including any portion thereof authorized as paymentto the search company) from the custodial account.

8. If upon the death of the Depositor (orBeneficiary) the custodial account is payable to a person known by the Custodian to be a minor or otherwise under a legal disability, the Custodianmay, in its absolute discretion, make all, or anypart of the distribution to (a) a parent of suchperson, (b) the guardian, conservator, or other legal representative, wherever appointed, of suchperson, (c) a custodial account established under a Uniform Gifts to Minors, Uniform Transfers toMinors Act, or similar act, (d) any person havingcontrol or custody of such person, or (e) to suchperson directly.

9. The Custodian will keep records of all receipts,investments, disbursements, and other transac-tions for this custodial account and for each FundAccount. As soon as is practicable after the closeof each calendar year, and whenever required bythe Code, the Custodian shall deliver to theDepositor (or Beneficiary, if applicable) a writtenreport(s) reflecting all activity in the custodialaccount during the prior calendar year and the fairmarket value of the custodial account. Upon theexpiration of sixty (60) days after the Custodianhas furnished such written report(s) to theDepositor (or Beneficiary), the Custodian shall bereleased and discharged from all liability andaccountability with respect to any such acts ortransactions except those to which the Depositor(or Beneficiary) has filed written objections withthe Custodian within the sixty (60) day period afterthe calendar year.

10. The Depositor shall have sole responsibilityfor determining whether any contribution, conver-sion, or distribution shall be permitted, including(but not limited to) the determination of the allow-able amount and tax effect of any such transac-tion to or from the custodial account. TheDepositor shall also be responsible for reporting onhis personal tax return, whenever required by theInternal Revenue Service, any transaction made toor from the custodial account.

11. The Custodian shall have the right to amendthis Agreement in any manner it deems necessaryor advisable in order to qualify (or maintain qualifi-cations of) this Agreement under the applicableprovisions of the Code or to maintain proper anddesirable operation of this custodial account. Anysuch amendment shall be effected by delivery tothe Depositor (or Beneficiary, if applicable) of arestatement of this Agreement including any suchamendment. The Depositor (or Beneficiary) shallbe deemed to consent to any such amendment(s)if he fails to object thereto by written noticereceived by the Custodian within fifteen (15)calendar days from the date of the Custodian’smailing to the Depositor (or Beneficiary) a copy of such amendment(s) or restatement.

12. The Depositor shall have the right to termi-nate this custodial account or to remove theCustodian upon thirty (30) days prior writtennotice to the Custodian, which notice shall includeinstructions regarding the final distribution ortransfer of all custodial account assets. If theDepositor fails to provide such distribution ortransfer instructions, the Custodian may terminatethis custodial account by distributing all custodialaccount assets (less amounts required to satisfyunpaid fees, costs, expenses and obligations)directly to the Depositor.

13. The Custodian shall have the right to resign ascustodian under this Agreement upon thirty (30)days prior written notice to the Depositor (orBeneficiary, if applicable). Unless the Depositor(or Beneficiary) provides written instructions to thecontrary, the Custodian shall have the right toappoint and transfer the custodial account assets(less amounts required to satisfy unpaid fees,costs, expenses, and obligations), together withcopies of relevant books and records, to a succes-sor custodian. A successor custodian shall satisfythe requirements of Section 408(a)(2). TheCustodian is not liable for the acts or omissions of any successor custodian.

14. The Custodian is authorized to perform allacts necessary to carry out the terms of thisAgreement and to hire an agent to perform certainof its duties hereunder, which agent may be theTransfer Agent for the Fund (if such transfer agentis other than the Custodian).

15. Distribution requests that are received by theCustodian in good order will be made to theDepositor, his beneficiary (if appropriate), or asuccessor custodian, normally within five (5) business days. To be in good order, distributionrequests must meet the Roth IRA distributionrequirements of the Custodian. The Custodianreserves the right to change these requirementsat any time without prior notice to the Depositor(or Beneficiary, if applicable).