fourth quarter 2009 financial results - starhill global...

TRANSCRIPT

Fourth Quarter 2009 Financial Results 28 J 201028 January 2010

Agenda

Financial Highlights

P tf li P f U d tPortfolio Performance Update– Singapore– Tokyo– Chengdu

Growth DriversGrowth Drivers

28 Jan 2010 Starhill Global REIT 2

Key highlights

4Q 2009 6%

4Q 2009 income to be distributed of $18.8 million represents a 5.6% increase 4Q 2008

4Q 2009: Income to be distributed up 5.6%

over 4Q 2008

Acquisition of David Jones Building in Perth completed in January 2010

28 Jan 2010 Starhill Global REIT 3

4Q 2009 financial highlights

f 0 9 4Q 2008 ( ) 4%

Period: 1 Oct – 31 Dec 2009 4Q 2009 4Q 2008 % Change

DPU of 0.97 cents exceeded 4Q 2008 (post-rights) by 5.4%

Gross Revenue $34.3 mil $33.8 mil 1.5%

Net Property Income $26.8 mil $26.0 mil 3.2%

Income Available for Distribution $19.1 mil (1) $18.1 mil 5.5%

Income to be Distributed $18.8 mil (1) $17.8 mil 5.6%

DPU (pre-rights) N/A 1.85 cents N/A

DPU (post-rights) 0.97 cents (2) 0.92 cents (3) 5.4%

Note: 1. Approximately $0.3 million of income available for distribution for the fourth quarter ended 31 December 2009 has been retained to satisfy certain legal

reserve requirements in China.

2. The computation of DPU for 4Q 2009 is based on number of units entitled to distributions comprising: (a) number of units in issue as at 31 December2009 of 1,932,418,044 units and (b) estimated units issuable to the Manager as partial satisfaction of management fee (base fee) earned for 4Q 2009 of

28 Jan 2010 Starhill Global REIT 4

2,916,940 units.

3. DPU for 4Q 2008 has been restated to include the 963,724,106 right units.

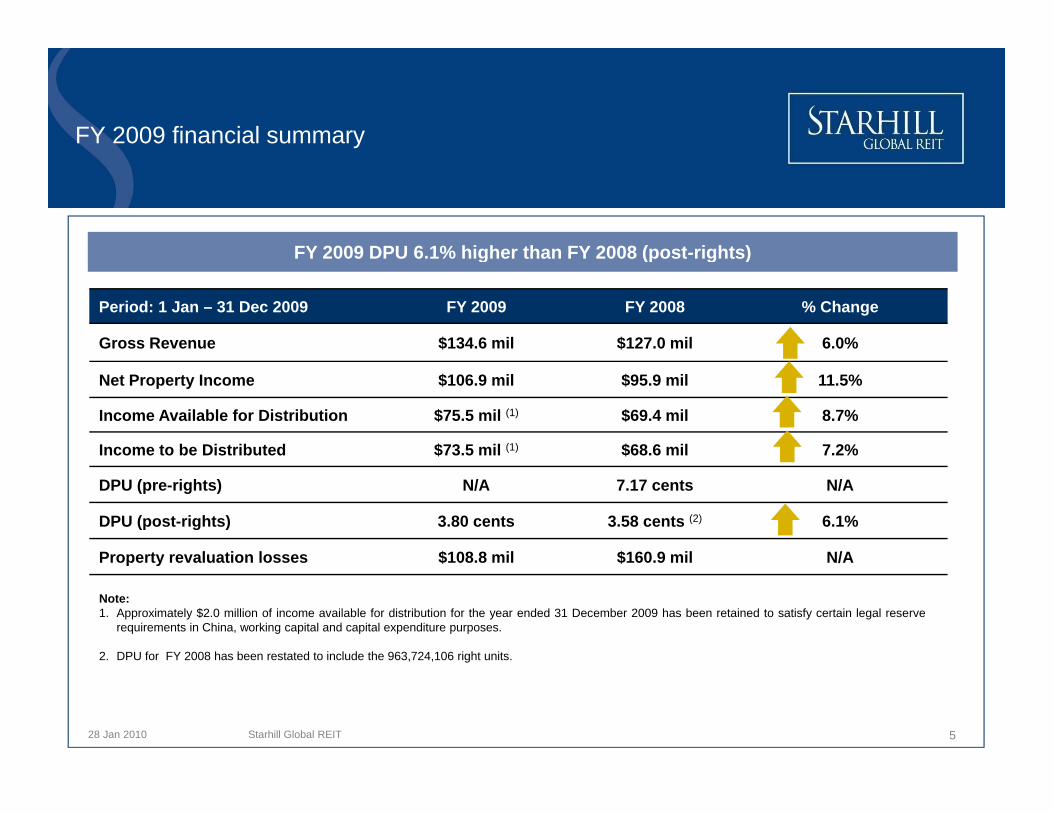

FY 2009 financial summary

FY 2009 DPU 6 1% higher than FY 2008 (post-rights)

Period: 1 Jan – 31 Dec 2009 FY 2009 FY 2008 % Change

Gross Revenue $134.6 mil $127.0 mil 6.0%

FY 2009 DPU 6.1% higher than FY 2008 (post-rights)

Net Property Income $106.9 mil $95.9 mil 11.5%

Income Available for Distribution $75.5 mil (1) $69.4 mil 8.7%

Income to be Distributed $73.5 mil (1) $68.6 mil 7.2%

DPU (pre-rights) N/A 7.17 cents N/A

DPU (post-rights) 3.80 cents 3.58 cents (2) 6.1%

Property revaluation losses $108.8 mil $160.9 mil N/AProperty revaluation losses $108.8 mil $160.9 mil N/A

Note: 1. Approximately $2.0 million of income available for distribution for the year ended 31 December 2009 has been retained to satisfy certain legal reserve

requirements in China, working capital and capital expenditure purposes.

2. DPU for FY 2008 has been restated to include the 963,724,106 right units.

28 Jan 2010 Starhill Global REIT 5

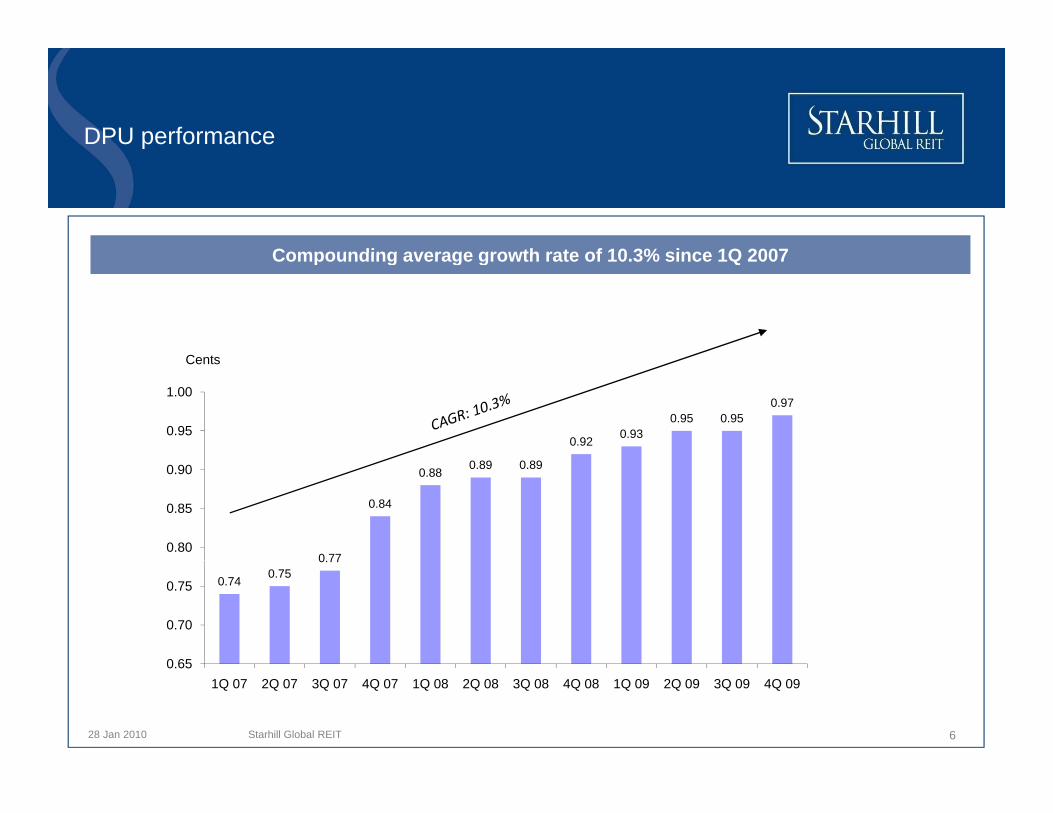

DPU performance

Compounding average growth rate of 10 3% since 1Q 2007

C t

Compounding average growth rate of 10.3% since 1Q 2007

0.92 0.930.95 0.95

0.97

0.95

1.00

Cents

0 77

0.84

0.88 0.89 0.89

0.80

0.85

0.90

0.74 0.750.77

0 65

0.70

0.75

28 Jan 2010

0.651Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08 4Q 08 1Q 09 2Q 09 3Q 09 4Q 09

Starhill Global REIT 6

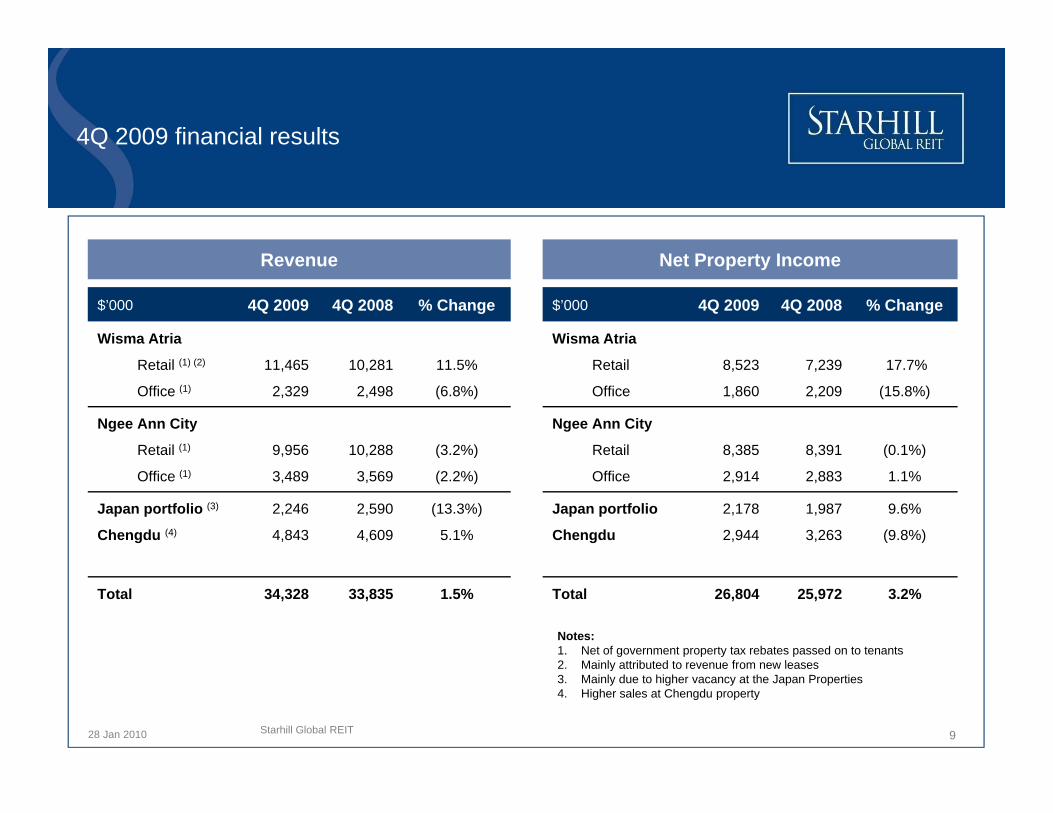

4Q 2009 financial results

$’000 4Q 2009 4Q 2008 % Change$ Q Q % g

Gross Revenue 34,328 33,835 1.5%

Less: Property Expenses (7,524) (7,863) (4.3%)

Net Property Income 26,804 25,972 3.2%

Less: Fair Value Adjustment (1)

Borrowing Costs

Finance income

Management Fees

(93)

(5,895)

302

(2 904)

(106)

(6,278)

5

(2 867)

(12.3%)

(6.1%)

n/m

1 3% Notes: Management Fees

Other Trust Expenses

Tax Expenses (2)

(2,904)

(2,496)

(681)

(2,867)

(812)

(743)

1.3%

207.4%

(8.3%)

Net Income After Tax (3) 15,037 15,171 (0.9%)

1. Being accretion of tenancy deposit stated at amortised cost in accordance with Financial Reporting Standard 39. This financial adjustment has no impact on the DPU

2. Excludes deferred income tax

Add: Non-Tax Deductibles (4) 4,037 2,904 39.0%

Income Available for Distribution 19,074 18,075 5.5%

Income to be Distributed 18,773 17,773 5.6%

DPU ( i ht ) N/A 1 85 t N/A

3. Excludes changes in fair value of unrealised derivative instruments and investment properties

4. Includes management fees payable in units, certain finance costs, depreciation, sinking fund provisions, straight-line rent adjustment, trustee fees and due diligence project costs

28 Jan 2010

DPU (pre-rights) N/A 1.85 cents N/A

DPU (post-rights) 0.97 cents 0.92 cents (5) 5.4%5. DPU for 4Q 2008 has been restated to include the

963,724,106 right units.

Starhill Global REIT 7

FY 2009 financial results

$’000 FY 2009 FY 2008 % Change

Gross Revenue 134,621 127,042 6.0%

Less: Property Expenses (27,672) (31,158) (11.2%)

Net Property Income 106,949 95,884 11.5%

Less: Fair Value Adjustment (1)

Borrowing Costs

Finance income

Management Fees

(666)

(23,690)

431

(10,961)

(28)

(22,146)

87

(11,404)

n/m

7.0%

395.4%

(3.9%)Notes: 1. Being accretion of tenancy deposit stated at

amortised cost in accordance with FinancialOther Trust Expenses

Tax Expenses (2)

(4,907)

(2,297)

(3,421)

(2,196)

43.4%

4.6%

Net Income After Tax (3) 64,859 56,776 14.2%

Add N T D d tibl (4) 10 623 12 651 (16 0%)

amortised cost in accordance with Financial Reporting Standard 39. This financial adjustment has no impact on the DPU

2. Excludes deferred income tax

3. Excludes changes in fair value of unrealised derivative instruments and investment propertiesAdd: Non-Tax Deductibles (4) 10,623 12,651 (16.0%)

Income Available for Distribution 75,482 69,427 8.7%

Income to be Distributed 73,505 68,599 7.2%

derivative instruments and investment properties

4. Includes management fees payable in units, certain finance costs, depreciation, sinking fund provisions, straight-line rent adjustment, trustee fees and due diligence project costs

5. DPU for FY 2008 has been restated to include the

28 Jan 2010

5. DPU for FY 2008 has been restated to include the 963,724,106 right units.

8

DPU (pre-rights) N/A 7.17 cents N/A

DPU (post-rights) 3.80 cents 3.58 cents (5) 6.1%

4Q 2009 financial results

$’000 4Q 2009 4Q 2008 % Change

Wisma Atria

$’000 4Q 2009 4Q 2008 % Change

Wisma Atria

Revenue Net Property Income

Retail (1) (2)

Office (1)

11,465

2,329

10,281

2,498

11.5%

(6.8%)

Ngee Ann City

Retail (1) 9,956 10,288 (3.2%)

Retail

Office

8,523

1,860

7,239

2,209

17.7%

(15.8%)

Ngee Ann City

Retail 8,385 8,391 (0.1%)

Office (1) 3,489 3,569 (2.2%)

Japan portfolio (3)

Chengdu (4)

2,246

4,843

2,590

4,609

(13.3%)

5.1%

Office 2,914 2,883 1.1%

Japan portfolio

Chengdu

2,178

2,944

1,987

3,263

9.6%

(9.8%)

Total 34,328 33,835 1.5% Total 26,804 25,972 3.2%

Notes: 1. Net of government property tax rebates passed on to tenants2 Mainly attributed to revenue from new leases

28 Jan 2010 Macquarie MEAG Prime REIT 9

2. Mainly attributed to revenue from new leases 3. Mainly due to higher vacancy at the Japan Properties 4. Higher sales at Chengdu property

Starhill Global REIT

FY 2009 financial results

$’000 FY 2009 FY 2008 % Change

Wisma Atria

$’000 FY 2009 FY 2008 % Change

Wisma Atria

Revenue Net Property Income

Retail (1) (2)

Office (1) (2)

45,389

10,151

44,238

9,078

2.6%

11.8%

Ngee Ann City

Retail (1) (2) 39,722 37,793 5.1%

Retail

Office

35,515

8,085

31,534

6,957

12.6%

16.2%

Ngee Ann City

Retail 33,990 30,289 12.2%

Office (1) (2) 13,951 12,943 7.8%

Japan portfolio (3)

Chengdu (4)

9,761

15,647

9,157

13,833

6.6%

13.1%

Office 11,331 10,147 11.7%

Japan portfolio

Chengdu

8,479

9,549

7,719

9,238

9.8%

3.4%

Total 134,621 127,042 6.0% Total 106,949 95,884 11.5%

Notes: 1 Net of government property tax rebates passed on to tenants

28 Jan 2010 Macquarie MEAG Prime REIT 10

1. Net of government property tax rebates passed on to tenants2. Renewal of leases at higher market rates and rent reviews3. Mainly due to strengthening of Yen on average4. Higher sales at Chengdu property

Starhill Global REIT

Trading yield

Attractive trading yield compared to other investment instruments

7.33

7

8

Attractive trading yield compared to other investment instruments

5 74%

7.33%

5.74

4

5

6 5.74%

6.88%4.67%

2.66 2.50

1.28

0 451

2

3

1.28%

2.66%

0.45%

2.50%

0.45

-Starhill Global REIT FY2009

yield

Average S-Reit yield

10-Year Spore Govt Bond

CPF Ordinary Acount

5-Year Spore Govt Bond

Bank Fixed Deposit Rate (12

Month)Notes: 1. Based on Starhill Global REIT’s closing price of $0.525 per unit as at 31 Dec 2009 and actual annualised distribution for 4Q 2009

(4)(3)(2)(1) (5)

(3)

28 Jan 2010 11

g p p2. As at 31 Dec 2009 (Source: Bloomberg)3. As at Dec 2009 (Source: Singapore Government Securities website)4. Based on interest paid on Central Provident Fund (CPF) ordinary account in Dec 2009 (Source: CPF website)5. As at 15 Jan 2010 (Source: DBS website)

Starhill Global REIT

Unit price performance

Liquidity statistics

Last 3 months average 3.5 mildaily trading volume (units)

Estimated free float 71.1%

Market cap (31 Dec 09) $1,015 mil1

Source: Bloomberg

28 Jan 2010 Starhill Global REIT 12

Note: 1. By reference to Starhill Global REIT’s closing price of $0.525 as at 31 Dec 2009

Distribution timetable

Distribution Period 1 October to 31 December 2009

Distribution Amount 0.97 cents per unit

Notice of Books Closure Date 28 January 2010

Distribution Timetable

Last Day of Trading on “Cum” Basis 1 February 2010, 5.00 pm

Ex-Date 2 February 2010, 9.00 am

Books Closure Date 4 February 2010, 5.00 pm

Distribution Payment Date 26 February 2010

28 Jan 2010 Starhill Global REIT 13

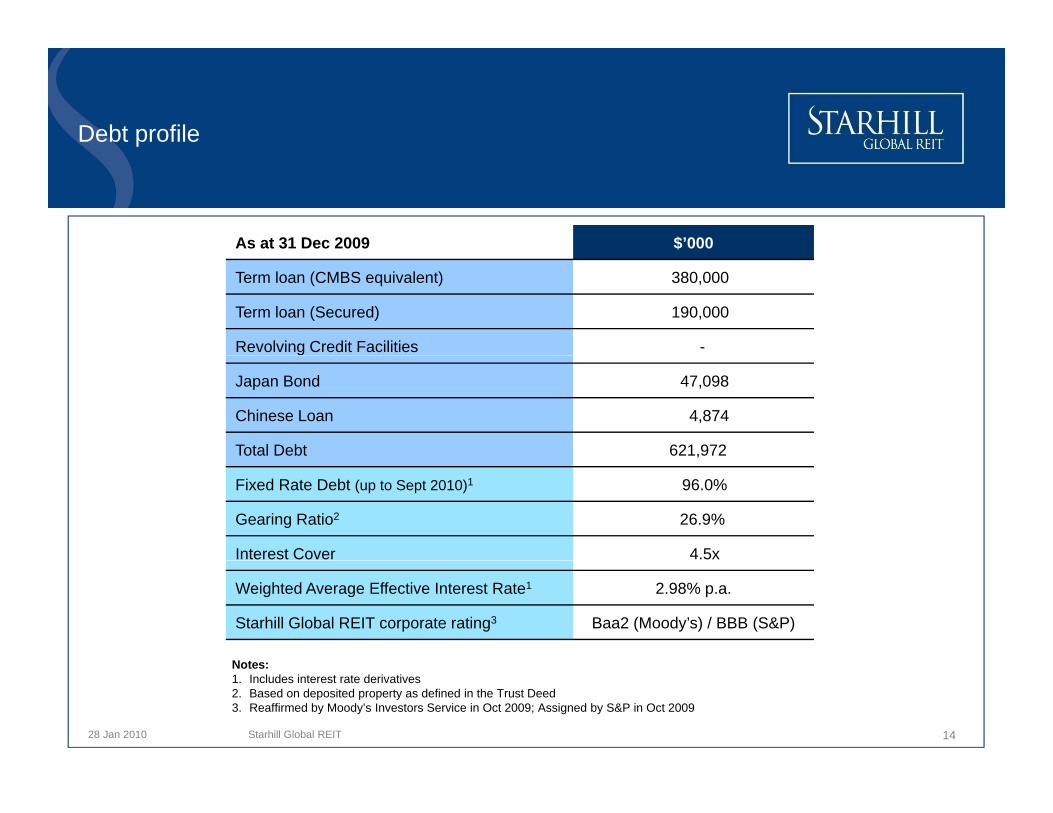

Debt profile

As at 31 Dec 2009 $’000

Term loan (CMBS equivalent) 380,000

Term loan (Secured) 190,000

Revolving Credit Facilities -

Japan Bond 47,098

Chinese Loan 4,874

Total Debt 621,972

Fixed Rate Debt (up to Sept 2010)1 96.0%

Gearing Ratio2 26.9%

Interest Cover 4.5x

Weighted Average Effective Interest Rate1 2.98% p.a.

Starhill Global REIT corporate rating3 Baa2 (Moody’s) / BBB (S&P)

Notes:

28 Jan 2010 Starhill Global REIT 14

Notes:1. Includes interest rate derivatives 2. Based on deposited property as defined in the Trust Deed3. Reaffirmed by Moody’s Investors Service in Oct 2009; Assigned by S&P in Oct 2009

Debt profile

f S 2010Active discussion with relationship banks to refinance debt maturing in September 2010

Weighted average effective interest rate is 2.98% p.a.700

S$ millionDebt maturity profile

96.0% of borrowings is fixed (including derivatives) until September 2010

400

500

600 1

190

$30.0 million secured RCF and $20.9 million unsecured RCF were repaid using the rights issue proceeds in August 2009380

100

200

300

1

‐ ‐ ‐-

100

2010 2011 2012 2013 2014Term loan (CMBS equivalent) RCF (secured)Term loan (secured) RCF (unsecured)J b d Chi l

471

111

28 Jan 2010 Starhill Global REIT 15

Japan bond Chinese loan

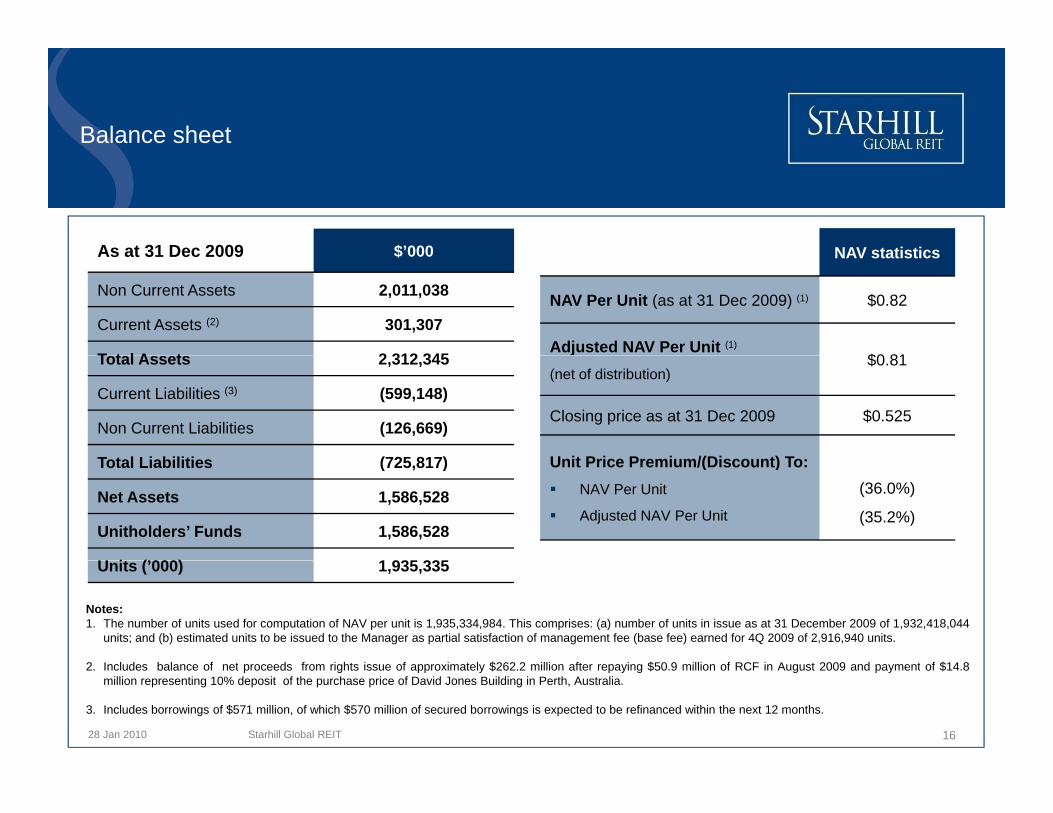

Balance sheet

As at 31 Dec 2009 $’000 NAV statisticsAs at 31 Dec 2009 $ 000

Non Current Assets 2,011,038

Current Assets (2) 301,307

T t l A t 2 312 345

NAV statistics

NAV Per Unit (as at 31 Dec 2009) (1) $0.82

Adjusted NAV Per Unit (1)

$0 81Total Assets 2,312,345

Current Liabilities (3) (599,148)

Non Current Liabilities (126,669)

T t l Li biliti (725 817)

j(net of distribution)

$0.81

Closing price as at 31 Dec 2009 $0.525

U it P i P i /(Di t) TTotal Liabilities (725,817)

Net Assets 1,586,528

Unitholders’ Funds 1,586,528

U it (’000) 1 935 335

Unit Price Premium/(Discount) To:NAV Per Unit

Adjusted NAV Per Unit

(36.0%)

(35.2%)

Units (’000) 1,935,335

Notes:1. The number of units used for computation of NAV per unit is 1,935,334,984. This comprises: (a) number of units in issue as at 31 December 2009 of 1,932,418,044

units; and (b) estimated units to be issued to the Manager as partial satisfaction of management fee (base fee) earned for 4Q 2009 of 2,916,940 units.

2 I l d b l f t d f i ht i f i t l $262 2 illi ft i $50 9 illi f RCF i A t 2009 d t f $14 8

28 Jan 2010 Starhill Global REIT 16

2. Includes balance of net proceeds from rights issue of approximately $262.2 million after repaying $50.9 million of RCF in August 2009 and payment of $14.8million representing 10% deposit of the purchase price of David Jones Building in Perth, Australia.

3. Includes borrowings of $571 million, of which $570 million of secured borrowings is expected to be refinanced within the next 12 months.

Valuation of Investment Properties

1.4% increase in valuation of Starhill Global REIT’s investment properties from June 2009

Description 15-Jun-09 Capex Revaluation FX 31-Dec-09 Change Change

S$'000 S$'000 S$'000 S$'000 S$'000 S$'000 %

Wisma Atria Property 797,510 264 14,056 - 811,830 14,320 1.8%

Ngee Ann City Property 885,885 - 16,515 - 902,400 16,515 1.9%

Renhe Spring Zongbei Property (1) 85,626 - 1,850 (2,935) 84,541 (1,085) -1.3%

Japan Portfolio (2) 185,588 - (7,140) 4,567 183,015 (2,573) -1.4%

Notes:1. Renhe Spring Zongbei Property translated at 31 Dec 2009 at RMB4.86:S$1.00 (15 Jun 2009: RMB4.69: S$1.00)

1,954,609 264 25,281 1,632 1,981,786 27,177 1.4%

28 Jan 2010 17

1. Renhe Spring Zongbei Property translated at 31 Dec 2009 at RMB4.86:S$1.00 (15 Jun 2009: RMB4.69: S$1.00)

2. Japan Portfolio translated at 31 Dec 2009 at JPY65.82:S$1.00 (15 Jun 2009: JPY67.44: S$1.00)

Starhill Global REIT

Agenda

Financial HighlightsFinancial Highlights

Portfolio Performance UpdatePortfolio Performance Update– Singapore– Tokyo– Chengdu

Growth DriversGrowth Drivers

28 Jan 2010 Starhill Global REIT 18

Portfolio summary

Portfolio

y

Di ifi d tf li i i Si J d Chi tDiversified portfolio comprising Singapore, Japan and China assets

Gross Revenue by Property Gross Revenue by CountryGross Revenue by Retail and Office

WA

Renhe Spring

Zongbei Property

14%

Japanese Properties

7%

Gross Revenue by Property(4Q 09)

China14%

Japan7%

Gross Revenue by Country(4Q 09)

Office17%

Gross Revenue by Retail and Office(4Q 09)

40%

NAC39%

14%

S'pore79%

Retail83%

28 Jan 2010 19Starhill Global REIT

Portfolio lease expiry

Portfolio

f 2 16 2 01 ( )Weighted average lease term of 2.16 and 2.01 years (by NLA and gross rent respectively)

Portfolio Lease Expiry (as at 31 Dec 2009)

52.8%

47.0%

40%

50%

60%By NLA By Gross Rent

Office RetailJapan Total

sq ft WA NAC WA NAC

21.5%25.7%25.5%

27.6%

20%

30%2010 23,928 62,054 41,068 2,928 7,501 137,480

2011 19,924 53,387 63,895 17,201 10,084 164,491

Beyond 2011 31 054 14 908 22 931 234 892 34 279 338 064

Notes:1.Portfolio lease expiry profile does not include Renhe Spring Zongbei Property

which operates as a department store with many short term concessionaire

0%

10%

FY2010 FY2011 Beyond 2011

Beyond 2011 31,054 14,908 22,931 234,892 34,279 338,064

Total 74,907 130,350 127,894 255,021 51,864 640,035

28 Jan 2010 20

which operates as a department store with many short-term concessionaire leases running 3-12 months

2.Lease expiry profile based on actual running lease as at 31 Dec 093.Toshin contributes to 35.3% and 29.9% of portfolio lease expiry by NLA and

Gross Rent respectivelyStarhill Global REIT

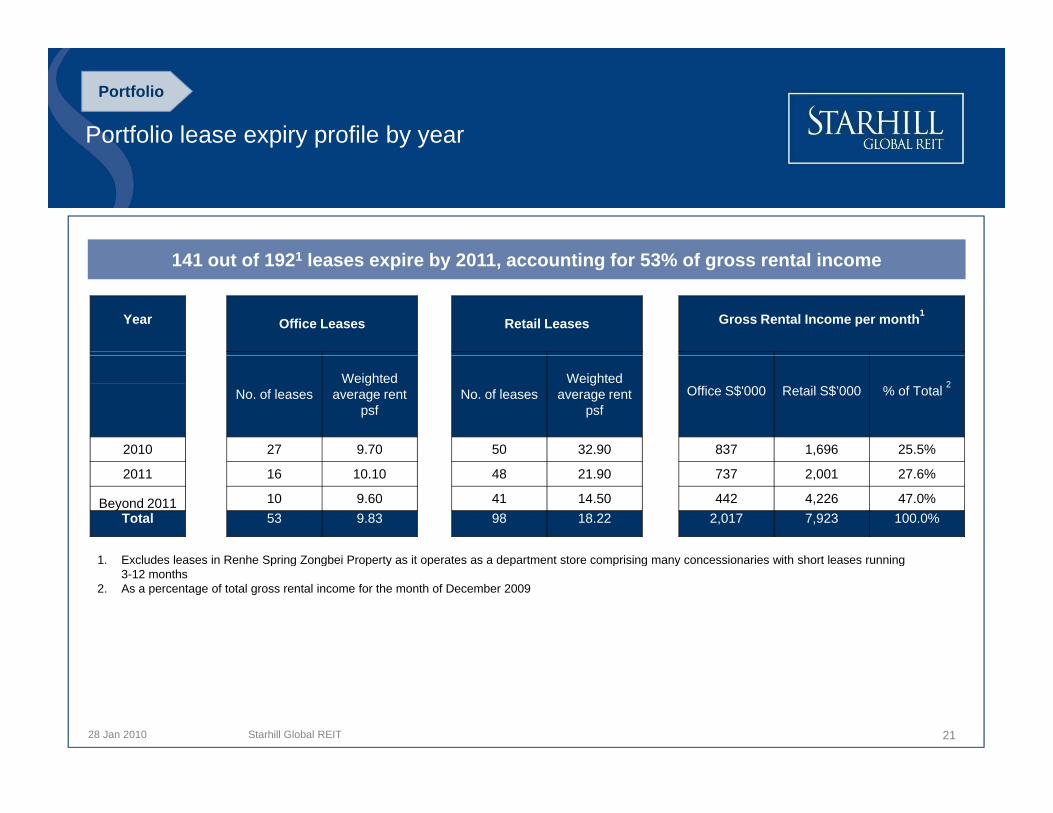

Portfolio lease expiry profile by year

Portfolio

141 f 1921 2011 f 3% f141 out of 1921 leases expire by 2011, accounting for 53% of gross rental income

Year Office Leases Retail Leases Gross Rental Income per month1

No. of leasesWeighted

average rent psf

No. of leasesWeighted

average rent psf

Office S$'000 Retail S$’000 % of Total 2

2010 27 9.70 50 32.90 837 1,696 25.5%

1 Excludes leases in Renhe Spring Zongbei Property as it operates as a department store comprising many concessionaries with short leases running

2011 16 10.10 48 21.90 737 2,001 27.6%

Beyond 2011 10 9.60 41 14.50 442 4,226 47.0%Total 53 9.83 98 18.22 2,017 7,923 100.0%

1. Excludes leases in Renhe Spring Zongbei Property as it operates as a department store comprising many concessionaries with short leases running 3-12 months

2. As a percentage of total gross rental income for the month of December 2009

28 Jan 2010 21Starhill Global REIT

Portfolio top 10 tenants

Portfolio

T 10 t t t ib t d 47% f th tf li t

Tenant Name Property Leased Area (sq ft) Lease Expiry % of Portfolio

Gross Rent 1% of Portfolio Leased Area

Toshin Development Co Ltd NAC 225,969 Jun 2013 29.8% 35.4%

Top 10 tenants contributed 47% of the portfolio gross rent

Wing Tai Retail Pte Ltd WA 7,707

May 2010, May 2010, Jun 2010, Jul 2010, Oct 2010, Nov

2010

2.7% 1.2%

Bread Talk Group WA 58,216 Sep 2011, Sep 2012, Oct 2012 2.4% 9.1%

Nike WA 7,341 Nov 2011 2.2% 1.1%

Feria Tokyo Terzo 14,451 Aug 2013 1.9% 2.3%

FJ Benjamin Lifestyle Pte Ltd WA 9,009 Nov 2011, Sep 2012 1.8% 1.4%

A 2010 S 2011Aspial-Lee Hwa (S) Pte Ltd WA 4,019 Aug 2010, Sep 2011, Oct 2011, Nov 2012 1.7% 0.6%

RSH (Singapore) Pte Ltd WA 4,061 March 2010, Jun 2010, Oct 2010 1.6% 0.6%

Charles & Keith Group WA 2,702 Jun 2010, Jul 2010 1.5% 0.4%

28 Jan 2010

Fashion Retail Pte Ltd WA 3,832 Sep 2011 1.4% 0.6%

22

Note: 1. For the month of December 2009

Starhill Global REIT

Office portfolio lease expiry profile and passing rents

Portfolio

In 4Q 2009, asking office rent was S$10.00 psf pm while leases were committed at between

10.10 10

10

90,000

100,000

Portfolio Office Lease Expiry and Average Gross Passing Rents

S$ psf pmSq ft

pm while leases were committed at between S$7.00 psf pm and S$9.00 psf pm.

9.70

9.60 10

10

10

10

10

40,000

50,000

60,000

70,000

80,000

85,983 73,311 45,962 9

9

10

10

-

10,000

20,000

30,000

2010 2011 Beyond 2011

Expiring office leases (by NLA)Gross passing rents of expiring leases (S$ psf pm)

28 Jan 2010 23

Note: Average monthly gross rent rounded to nearest ten cents

Starhill Global REIT

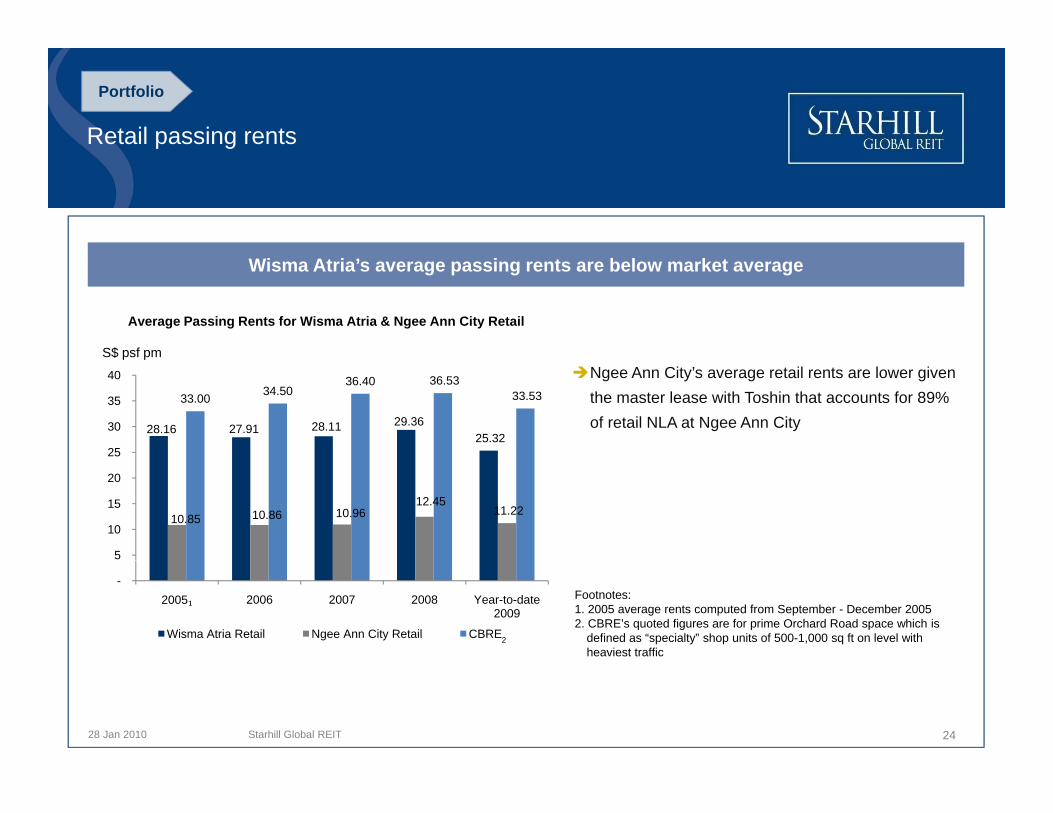

Retail passing rents

Portfolio

Wisma Atria’s average passing rents are below market average

Average Passing Rents for Wisma Atria & Ngee Ann City Retail

S$ psf pmNgee Ann City’s average retail rents are lower given the master lease with Toshin that accounts for 89% of retail NLA at Ngee Ann City28.16 27.91 28.11 29.36

25.32

33.00 34.5036.40 36.53

33.53

25

30

35

40

S$ psf pm

10.85 10.86 10.96 12.45

11.22

5

10

15

20

Footnotes:1. 2005 average rents computed from September - December 20052. CBRE’s quoted figures are for prime Orchard Road space which is

defined as “specialty” shop units of 500-1,000 sq ft on level with heaviest traffic

2

-2005₁ 2006 2007 2008 Year-to-date

2009

Wisma Atria Retail Ngee Ann City Retail CBRE

28 Jan 2010 24Starhill Global REIT

Occupancy costs

Portfolio

Average retail occupancy costsAverage retail occupancy costs

The higher occupancy cost at Wisma Atria is attributed to the higher proportion of fashion tenants given the centre’s positioning as a female

Average retail occupancy costs

Average Occupancy Costs for Wisma Atria & RenheSpring Zongbei

tenants given the centre s positioning as a female-centric mall

Renhe Spring Zongbei Property operates as a hi h d d t t t ith i t ti l l

25%27%

16%14%

20%

30%

high-end department store with international luxury labels such as Prada, Zegna, Hugo Boss, Chopard, Montblanc and Vertu which typically enjoy lower occupancy costs

14%

0%

10%

2008 Year-to-Date 2009

Notes:

1. Year-to-date 2009 occupancy costs for Wisma Atria and Renhe Spring Zongbei Property are for the period of Jan-Dec 2009

Wisma Atria Renhe Spring Zongbei

28 Jan 2010 25Starhill Global REIT

2. Average retail occupancy costs for Ngee Ann City is not available due to master lessee arrangements

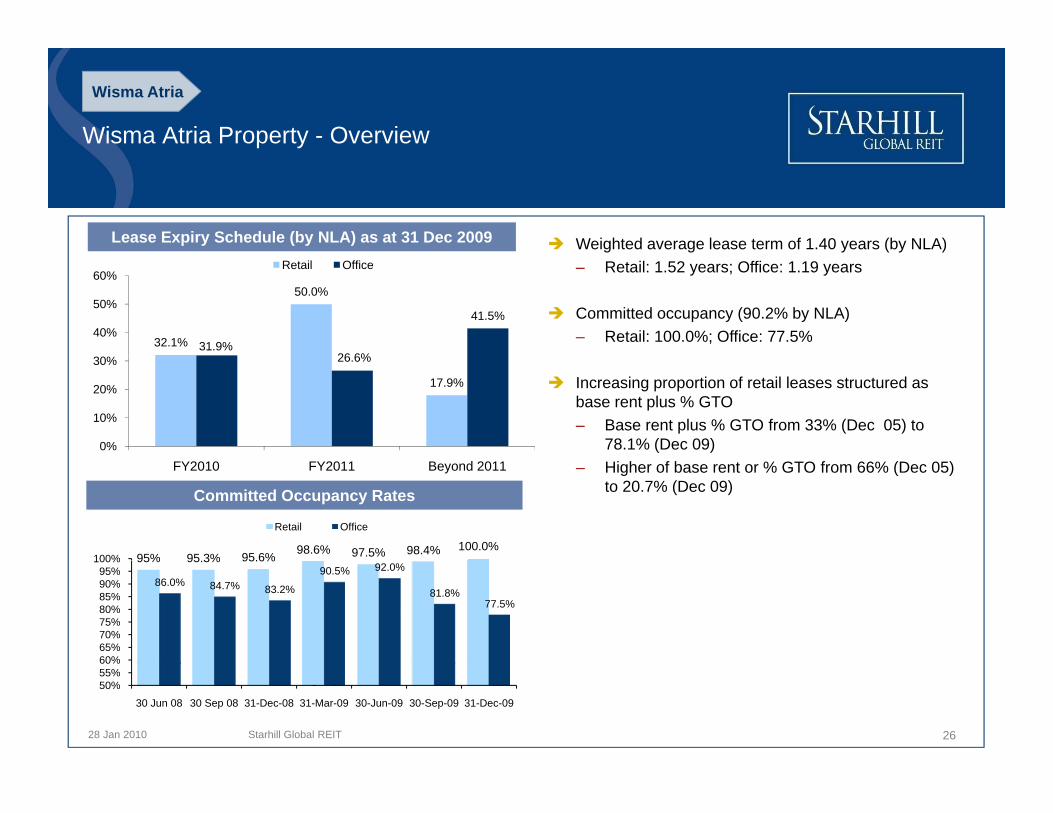

Wisma Atria Property - Overview

Wisma Atria

Lease Expiry Schedule (by NLA) as at 31 Dec 2009 Weighted average lease term of 1.40 years (by NLA)– Retail: 1.52 years; Office: 1.19 years

Committed occupancy (90.2% by NLA) – Retail: 100.0%; Office: 77.5% 32.1%

50.0%

31.9%26 6%

41.5%40%

50%

60%Retail Office

Increasing proportion of retail leases structured as base rent plus % GTO– Base rent plus % GTO from 33% (Dec 05) to

78.1% (Dec 09)

17.9%

26.6%

0%

10%

20%

30%

Committed Occupancy Rates

– Higher of base rent or % GTO from 66% (Dec 05) to 20.7% (Dec 09)

95% 95 3% 95.6% 98.6% 97.5% 98.4% 100.0%100%

Retail Office

FY2010 FY2011 Beyond 2011

95% 95.3% 95.6%

86.0% 84.7% 83.2%

90.5% 92.0%

81.8%77.5%

60%65%70%75%80%85%90%95%

100%

28 Jan 2010 26Starhill Global REIT

50%55%60%

30 Jun 08 30 Sep 08 31-Dec-08 31-Mar-09 30-Jun-09 30-Sep-09 31-Dec-09

Wisma Atria Property - Overview

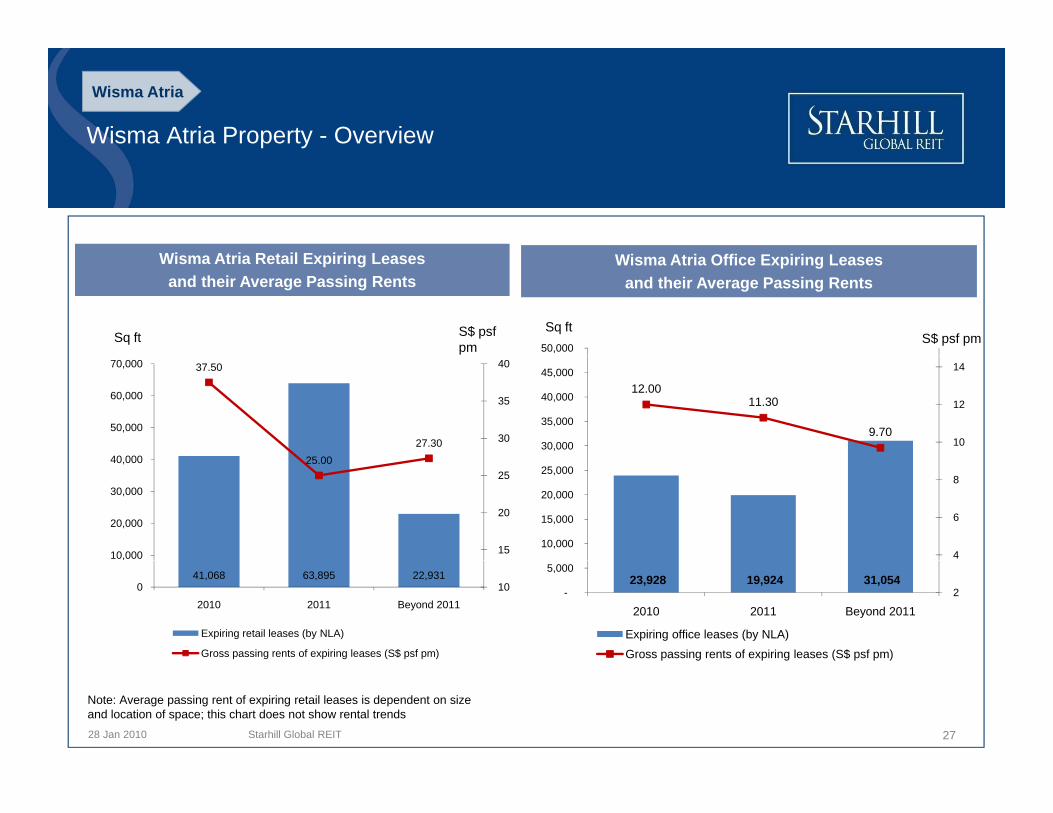

Wisma Atria

Wi At i R t il E i i LWisma Atria Retail Expiring Leases and their Average Passing Rents

Wisma Atria Office Expiring Leases and their Average Passing Rents

50,000 S$ psf pm

Sq ftS$ psf pm

Sq ft

12.0011.30

9.7010

12

14

30,000

35,000

40,000

45,000 37.50

25 0027.30 30

35

40

40 000

50,000

60,000

70,000

4

6

8

10,000

15,000

20,000

25,000 25.00

15

20

25

10,000

20,000

30,000

40,000

23,928 19,924 31,054 2 -

5,000

2010 2011 Beyond 2011

Expiring office leases (by NLA)Gross passing rents of expiring leases (S$ psf pm)

41,068 63,895 22,93110 0

2010 2011 Beyond 2011

Expiring retail leases (by NLA)

Gross passing rents of expiring leases (S$ psf pm)

28 Jan 2010 27Starhill Global REIT

Note: Average passing rent of expiring retail leases is dependent on size and location of space; this chart does not show rental trends

Wisma Atria Property - Diversified tenant base

Wisma Atria

WA Office Trade Mix – by % NLAWA Retail Trade Mix – by % NLA WA Office Trade Mix – by % NLA(as at 31 Dec 2009)

WA Retail Trade Mix – by % NLA(as at 31 Dec 2009)

General Trade

Health & Beauty1.7%

Services1.1%

WA Retail Trade Mix - By % NLA

Real Estate &Government

Jewellery & Watches

5.3%

Investments1.6% Travel/Leisure

0.0%

WA Office Trade Mix - By % NLA

Fashion48.5%

Sh &

Jewellery & Watches

7.1%

General Trade3.4%

Real Estate & Property Services15.1%

Consultancy / Services15.9%

Medical10.2%

Trading7.9%

Government related5.3%

F&B28.7%

Shoes & Accessories

9.6%

Petroleum Related14.4%

Others13.1%

Aerospace11.1%

28 Jan 2010 28

Wisma Atria Property – Traffic and centre sales

Wisma Atria

Shopper traffic surpasses pre-linkway closure levels

3.5

Wisma Atria Traffic Count at Primary Entrances

Million Wisma Atria Property Retail Sales TurnoverS$ Million

2.0

2.5

3.0 Year 2006 Year 2008 Year 2009

18

20

22

24 2007 Sales TurnOver 2008 Sales TurnOver2009 Sales TurnOver

2006 Sales Turnover

2008 S l

0.0

0.5

1.0

1.5

10

12

14

162008 Sales Turnover

2009 Sales Turnover

Overall footfall to Wisma Atria in 4Q 2009 increased 80% compared to the same period in 2008 following the re-opening of the basement linkway to the Orchard MRT station in June 2009 and the opening of ION Orchard on 21 July 2009

10

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

28 Jan 2010 29Starhill Global REIT

of the basement linkway to the Orchard MRT station in June 2009 and the opening of ION Orchard on 21 July 2009

Centre sales in 4Q 2009 declined slightly by 0.8% from 4Q 2008 as Singapore retail sales were slowly picking up as the economy recovered

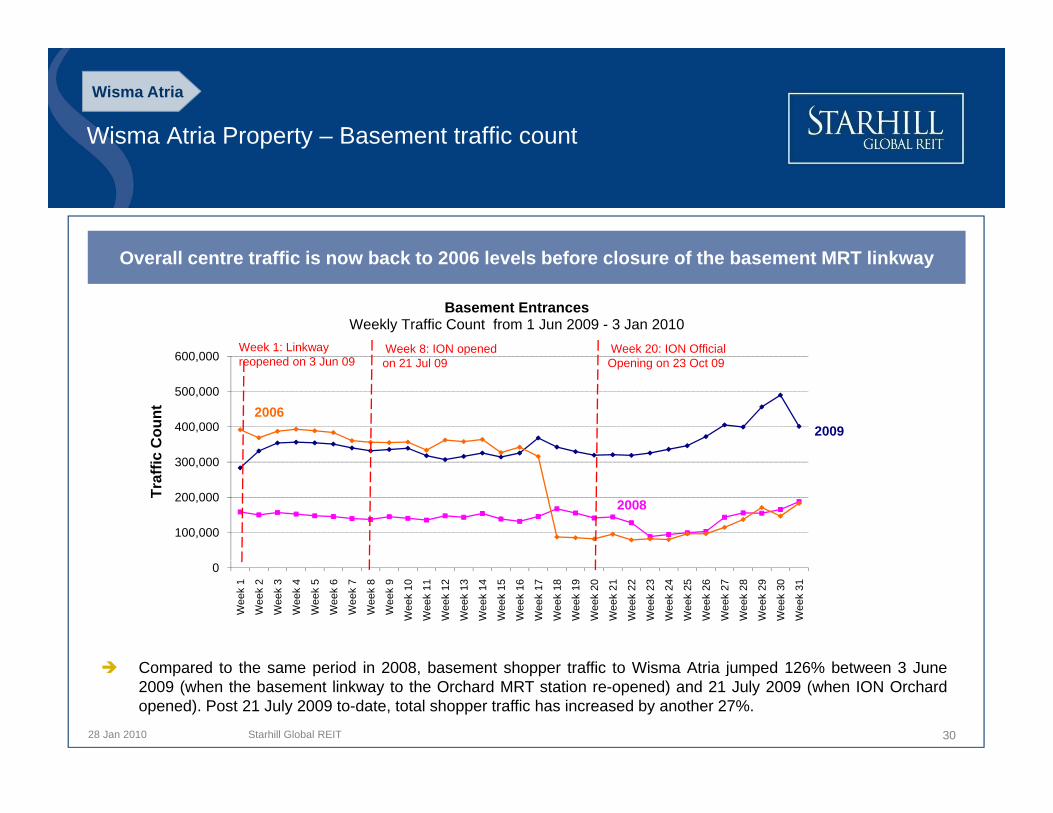

Wisma Atria Property – Basement traffic count

Wisma Atria

O ll t t ffi i b k t 2006 l l b f l f th b t MRT li kOverall centre traffic is now back to 2006 levels before closure of the basement MRT linkway

600 000

Basement EntrancesWeekly Traffic Count from 1 Jun 2009 - 3 Jan 2010

Week 1: Linkway Week 8: ION opened Week 20: ION Official

300 000

400,000

500,000

600,000

c C

ount

20092006

reopened on 3 Jun 09 on 21 Jul 09 Opening on 23 Oct 09

100,000

200,000

300,000

Traf

fic

2008

C d t th i d i 2008 b t h t ffi t Wi At i j d 126% b t 3 J

0

Wee

k 1

Wee

k 2

Wee

k 3

Wee

k 4

Wee

k 5

Wee

k 6

Wee

k 7

Wee

k 8

Wee

k 9

Wee

k 10

Wee

k 11

Wee

k 12

Wee

k 13

Wee

k 14

Wee

k 15

Wee

k 16

Wee

k 17

Wee

k 18

Wee

k 19

Wee

k 20

Wee

k 21

Wee

k 22

Wee

k 23

Wee

k 24

Wee

k 25

Wee

k 26

Wee

k 27

Wee

k 28

Wee

k 29

Wee

k 30

Wee

k 31

28 Jan 2010 30Starhill Global REIT

Compared to the same period in 2008, basement shopper traffic to Wisma Atria jumped 126% between 3 June2009 (when the basement linkway to the Orchard MRT station re-opened) and 21 July 2009 (when ION Orchardopened). Post 21 July 2009 to-date, total shopper traffic has increased by another 27%.

Wisma Atria Property –

Wisma Atria

p yNew lettable area at Basement and Level 1

New lettable retail space arising from removal of escalators in operation since October 2009

Before After

Orchard Rd street level Basement level

More than 1,000 sq ft of net lettable retail space was created arising from the removal of escalators, achieving areturn on investment of more than 60%

28 Jan 2010 31Starhill Global REIT

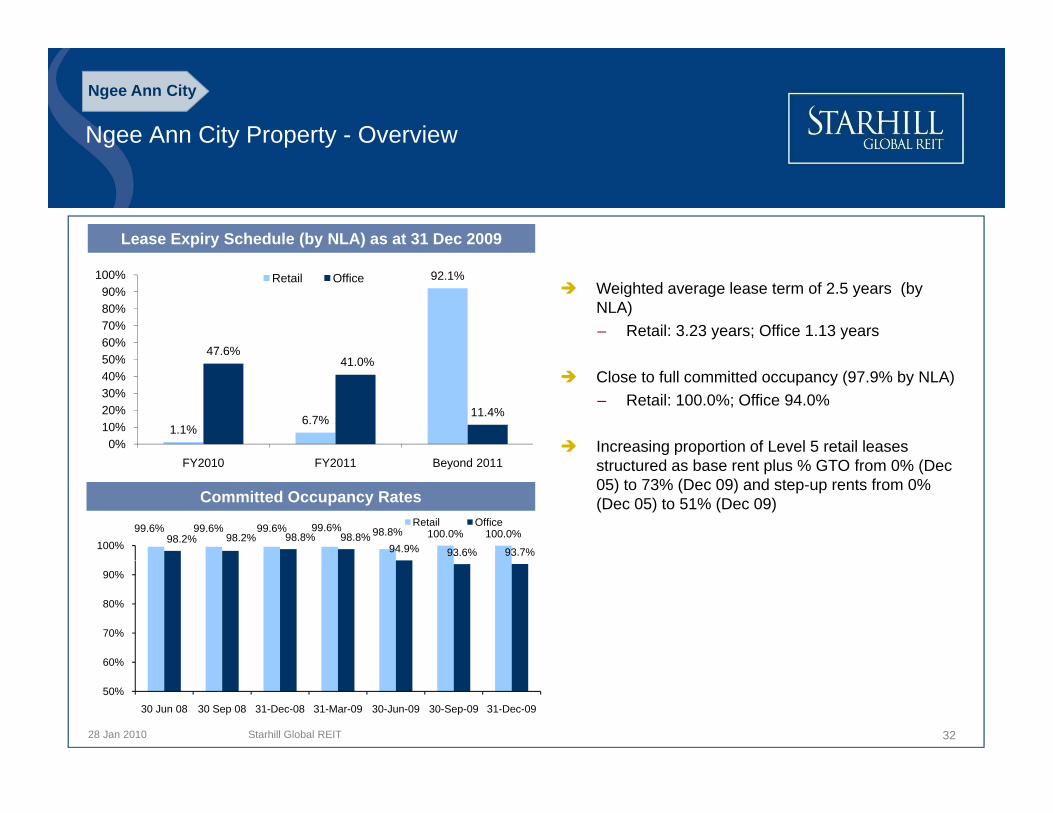

Ngee Ann City Property - Overview

Ngee Ann City

Lease Expiry Schedule (by NLA) as at 31 Dec 2009

Weighted average lease term of 2.5 years (by NLA)– Retail: 3.23 years; Office 1.13 years

92.1%

47.6%50%60%70%80%90%

100% Retail Office

Close to full committed occupancy (97.9% by NLA) – Retail: 100.0%; Office 94.0%

Increasing proportion of Level 5 retail leases 1.1%

6.7%

41.0%

11.4%

0%10%20%30%40%50%

Committed Occupancy Rates

structured as base rent plus % GTO from 0% (Dec 05) to 73% (Dec 09) and step-up rents from 0% (Dec 05) to 51% (Dec 09)

FY2010 FY2011 Beyond 2011

99.6% 99.6% 99.6% 99.6% 98.8% 100.0% 100.0%98.2% 98.2% 98.8% 98.8%94.9% 93.6% 93.7%100%

Retail Office

60%

70%

80%

90%

28 Jan 2010 32Starhill Global REIT

50%

60%

30 Jun 08 30 Sep 08 31-Dec-08 31-Mar-09 30-Jun-09 30-Sep-09 31-Dec-09

Ngee Ann City Property - Overview

Ngee Ann City

Ngee Ann City Retail Expiring Leases Ngee Ann City Office Expiring LeasesNgee Ann City Retail Expiring Leases and their Passing Average Rents

Ngee Ann City Office Expiring Leases and their Passing Average Rents

234 89217 60S$ psfSq ft Sq ft

S$ psf234,892

16.90

17.60

15

16

17

18

150,000

200,000

250,00062,054

8.909.60 9.60

10

12

14

40 000

50,000

60,000

70,000

17,201

13.10

11

12

13

14

50,000

100,000

4

6

8

10,000

20,000

30,000

40,000

2,928

17,201

10

11

0

2010 2011 Beyond 2011

Expiring retail leases (by NLA)

Gross passing rents of expiring leases (S$ psf pm)

53,387 14,908 2 -

,

2010 2011 Beyond 2011

Expiring office leases (by NLA)Gross passing rents of expiring leases (S$ psf pm)

28 Jan 2010 33Starhill Global REIT

Note: Average passing rent of expiring retail leases is dependent on size and location of space; this chart does not show rental trends

p g p g ( p p )

Ngee Ann City - Diversified tenant base

Ngee Ann City

NAC Retail Trade mix by % NLA NAC Office Trade Mix by % NLANAC Retail Trade mix – by % NLA(as at 31 Dec 2009)

NAC Office Trade Mix – by % NLA(as at 31 Dec 2009)

Beauty & Wellness

9 2%

Services1.9% General Trade

0.4%

C lt /Aerospace

Beauty/ Health3.5%

Travel/Leisure2.6% Fashion Retail

2.6%

NAC Office Trade Mix - By % NLA

9.2% Consultancy / Services30.1%

Banking and Financial Services

Real Estate & Property Services

7.4%

Aerospace3.8%

Toshin88.6%

Others19.6%

Jewellery & Watches11.8%

Petroleum Related10.6%

7.9%

28 Jan 2010 34Starhill Global REIT

Japan Properties - Overview

Japan Properties

Weighted average lease term by NLA is 2.47 years

Total Japan portfolio occupancy is 90.4%

1 vacant unit (1,331 sq ft) at Ebisu Fort, 1 vacant unit (934 sq ft ) at Daikanyama and 1 vacant unit (3,254 sq ft) at Holon L

Savills Japan actively sourcing suitable tenants for Ebisu Fort, Holon L and Daikanyama

Committed occupancy rates as at 31 December 09

As at 1 December 2009, Starhill Global ML K.K. and Savills Japan K.K. replaced Future Revolution as master tenant and property manager respectively.

100% 100% 100% 100%88% 93%

70%80%90%

100%

33%

10%20%30%40%50%60%

28 Jan 2010 35Starhill Global REIT

0%

Holon L Harajyuku Secondo

Roppongi Terzo

Roppongi Primo

Naka-meguro Daikan-yama Ebisu Fort

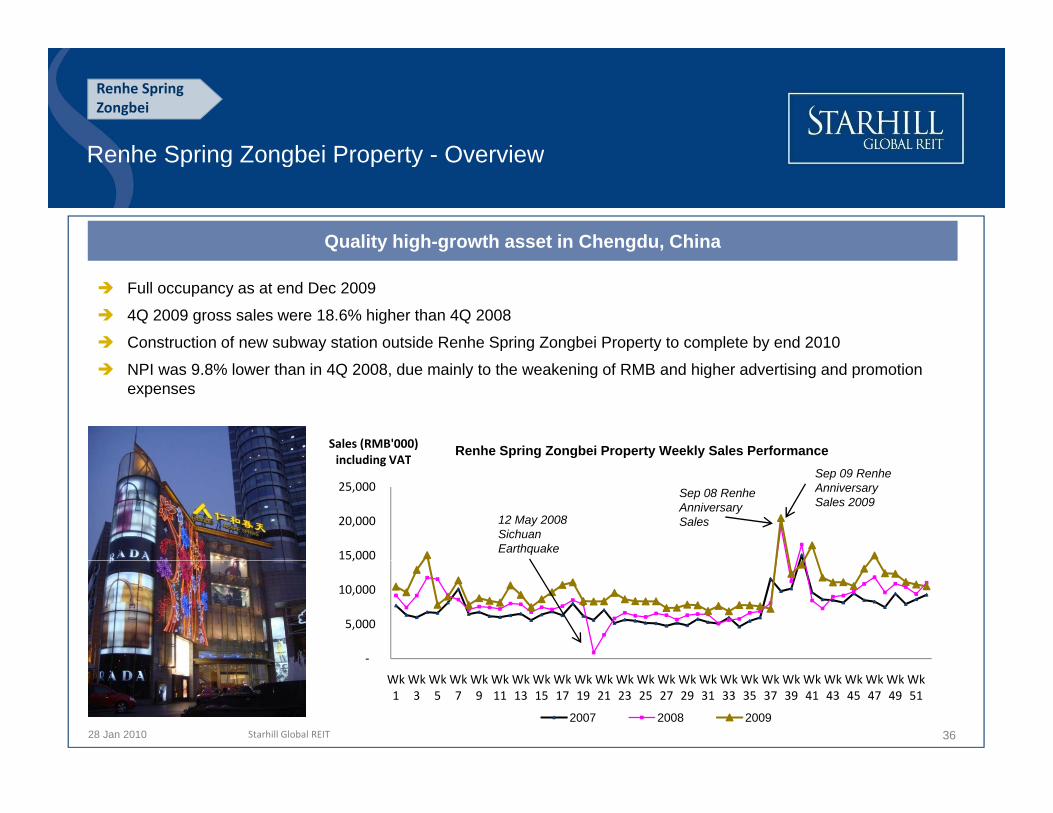

Renhe Spring Zongbei Property Overview

Renhe Spring Zongbei

Quality high-growth asset in Chengdu, China

Renhe Spring Zongbei Property - Overview

Full occupancy as at end Dec 2009

4Q 2009 gross sales were 18.6% higher than 4Q 2008

Construction of new subway station outside Renhe Spring Zongbei Property to complete by end 2010

NPI was 9.8% lower than in 4Q 2008, due mainly to the weakening of RMB and higher advertising and promotion expenses

Sales (RMB'000)including VAT

Renhe Spring Zongbei Property Weekly Sales Performance

15,000

20,000

25,000

including VATSep 09 Renhe Anniversary Sales 2009

12 May 2008Sichuan Earthquake

Sep 08 Renhe Anniversary Sales

‐

5,000

10,000

,

28 Jan 2010 Starhill Global REIT

Wk 1

Wk 3

Wk 5

Wk 7

Wk 9

Wk 11

Wk 13

Wk 15

Wk 17

Wk 19

Wk 21

Wk 23

Wk 25

Wk 27

Wk 29

Wk 31

Wk 33

Wk 35

Wk 37

Wk 39

Wk 41

Wk 43

Wk 45

Wk 47

Wk 49

Wk 51

2007 2008 200936

Agenda

Financial Highlights

Portfolio Performance Update– Singapore– Tokyo

Growth Drivers & Contributors

28 Jan 2010 37Starhill Global REIT

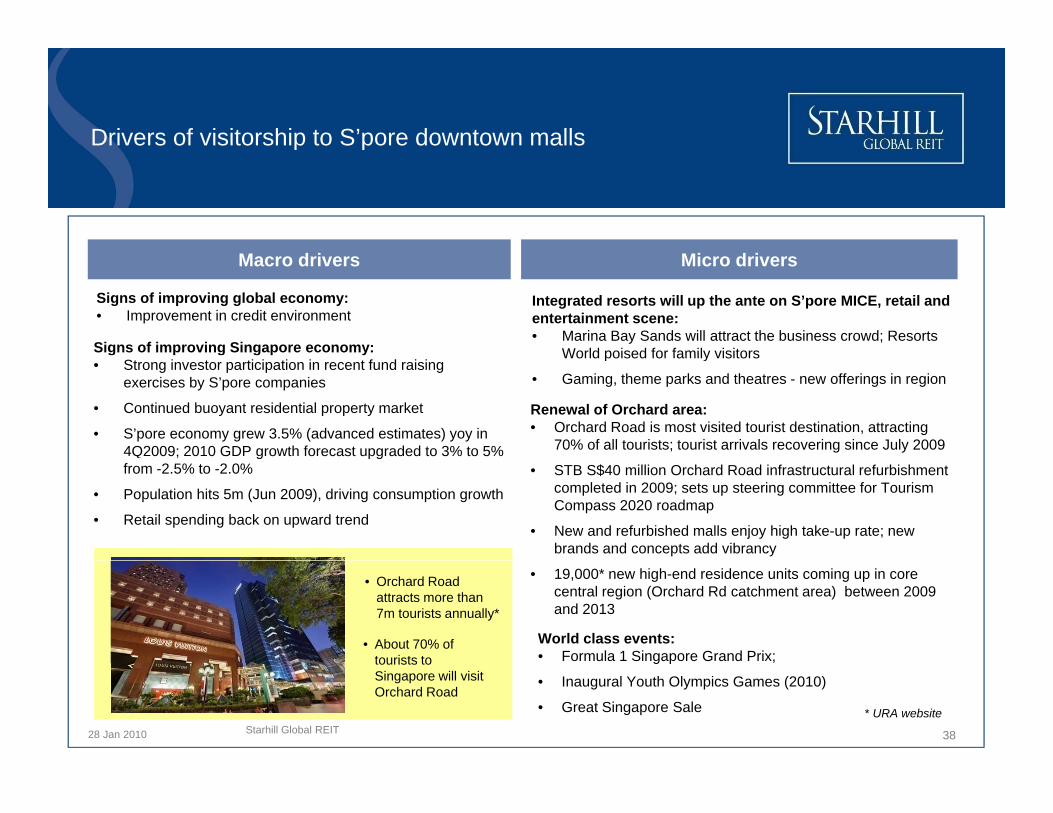

Drivers of visitorship to S’pore downtown malls

Integrated resorts will up the ante on S’pore MICE, retail and entertainment scene:• Marina Bay Sands will attract the business crowd; Resorts

World poised for family visitors

Macro drivers Micro drivers

Signs of improving global economy:• Improvement in credit environment

Signs of improving Singapore economy: World poised for family visitors

• Gaming, theme parks and theatres - new offerings in region

Renewal of Orchard area: • Orchard Road is most visited tourist destination, attracting

70% of all tourists; tourist arrivals recovering since July 2009

• Strong investor participation in recent fund raising exercises by S’pore companies

• Continued buoyant residential property market

• S’pore economy grew 3.5% (advanced estimates) yoy in 4Q2009; 2010 GDP growth forecast upgraded to 3% to 5%

• STB S$40 million Orchard Road infrastructural refurbishment completed in 2009; sets up steering committee for Tourism Compass 2020 roadmap

• New and refurbished malls enjoy high take-up rate; new brands and concepts add vibrancy

; g pgfrom -2.5% to -2.0%

• Population hits 5m (Jun 2009), driving consumption growth

• Retail spending back on upward trend

World class events: • Formula 1 Singapore Grand Prix;

• 19,000* new high-end residence units coming up in core central region (Orchard Rd catchment area) between 2009 and 2013

• About 70% of tourists to

• Orchard Road attracts more than 7m tourists annually*

28 Jan 2010 Starhill Global REIT

g p

• Inaugural Youth Olympics Games (2010)

• Great Singapore Sale

tourists to Singapore will visit Orchard Road

* URA website

38

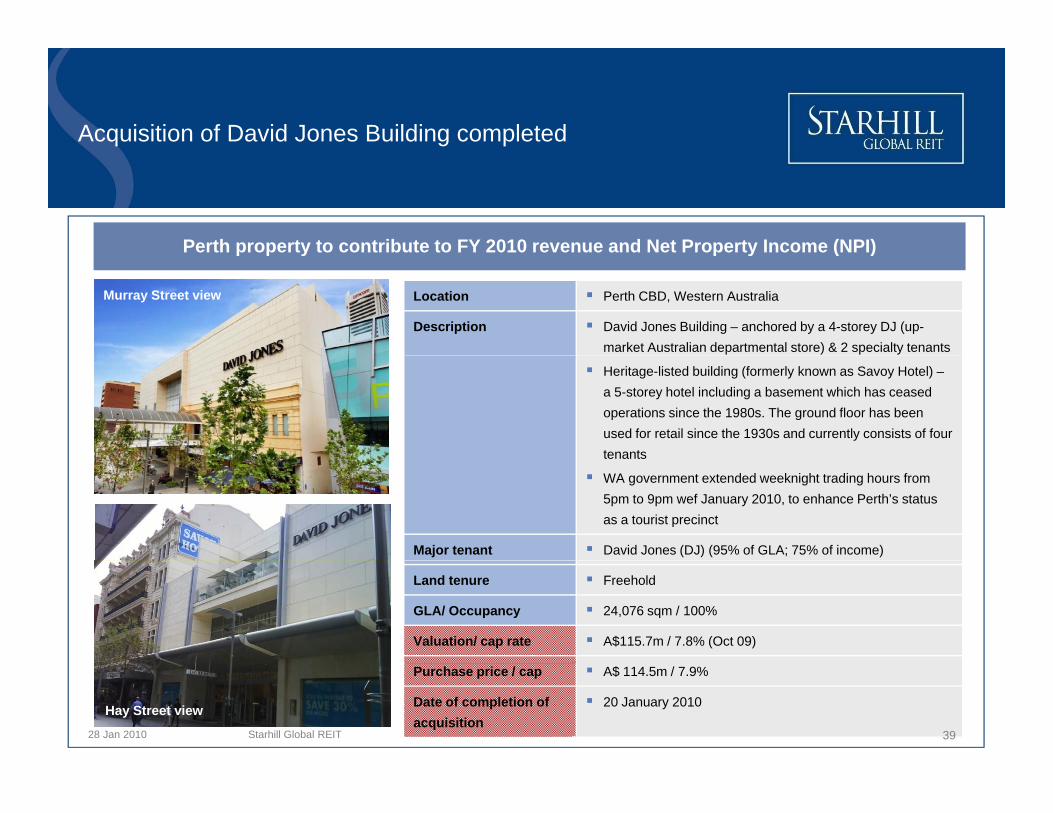

Acquisition of David Jones Building completed

Perth property to contribute to FY 2010 revenue and Net Property Income (NPI)

Location Perth CBD, Western Australia

Description David Jones Building – anchored by a 4-storey DJ (up-market Australian departmental store) & 2 specialty tenants

Murray Street view

p p y p y ( )

Heritage-listed building (formerly known as Savoy Hotel) –a 5-storey hotel including a basement which has ceased operations since the 1980s. The ground floor has been used for retail since the 1930s and currently consists of four tenantstenants

WA government extended weeknight trading hours from 5pm to 9pm wef January 2010, to enhance Perth’s status as a tourist precinct

Major tenant David Jones (DJ) (95% of GLA; 75% of income)

Land tenure Freehold

GLA/ Occupancy 24,076 sqm / 100%

Valuation/ cap rate A$115.7m / 7.8% (Oct 09)

28 Jan 2010

Purchase price / cap A$ 114.5m / 7.9%

Date of completion of acquisition

20 January 2010

39Starhill Global REIT

Hay Street view

Proposed acquisition of Malaysia properties

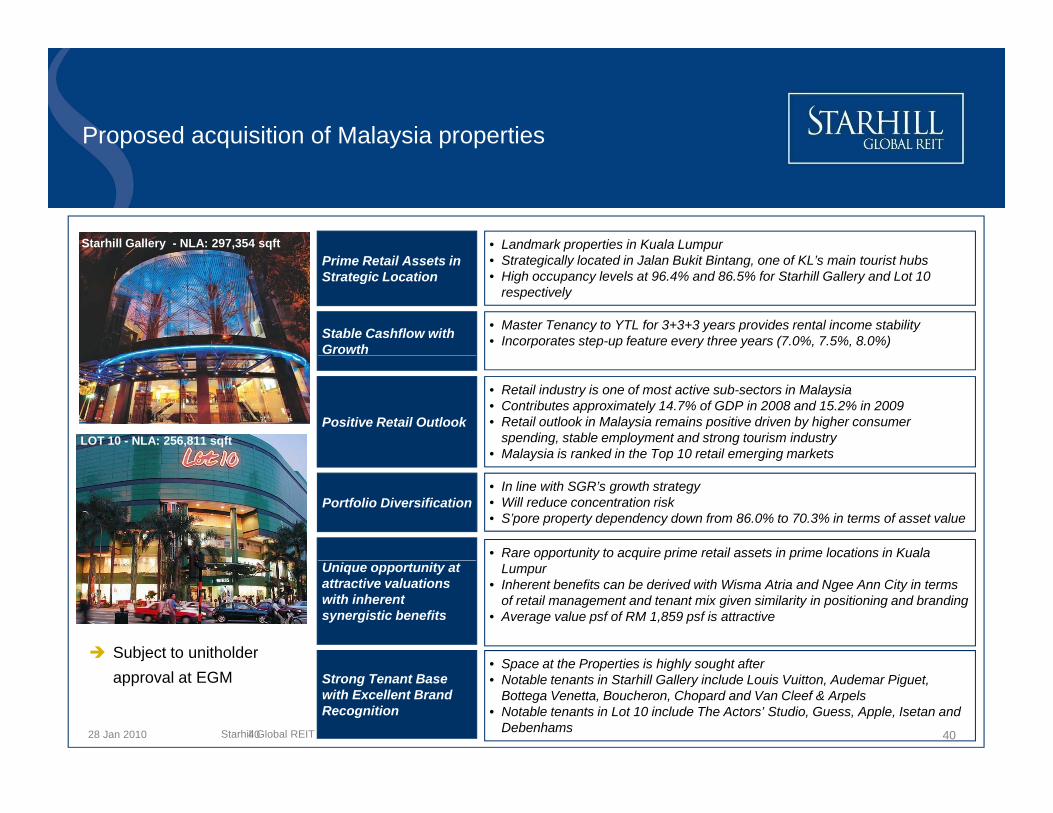

• Landmark properties in Kuala LumpurStarhill Gallery - NLA: 297,354 sqft

Stable Cashflow with Growth

• Master Tenancy to YTL for 3+3+3 years provides rental income stability• Incorporates step-up feature every three years (7.0%, 7.5%, 8.0%)

• Strategically located in Jalan Bukit Bintang, one of KL’s main tourist hubs• High occupancy levels at 96.4% and 86.5% for Starhill Gallery and Lot 10

respectively

Prime Retail Assets in Strategic Location

Positive Retail Outlook

• Retail industry is one of most active sub-sectors in Malaysia• Contributes approximately 14.7% of GDP in 2008 and 15.2% in 2009• Retail outlook in Malaysia remains positive driven by higher consumer

spending, stable employment and strong tourism industry• Malaysia is ranked in the Top 10 retail emerging markets

LOT 10 - NLA: 256,811 sqft

Portfolio Diversification• In line with SGR’s growth strategy• Will reduce concentration risk• S’pore property dependency down from 86.0% to 70.3% in terms of asset value

Malaysia is ranked in the Top 10 retail emerging markets

• Rare opportunity to acquire prime retail assets in prime locations in Kuala

• Space at the Properties is highly sought after

Unique opportunity at attractive valuations with inherent synergistic benefits

Lumpur• Inherent benefits can be derived with Wisma Atria and Ngee Ann City in terms

of retail management and tenant mix given similarity in positioning and branding• Average value psf of RM 1,859 psf is attractive

Subject to unitholder

28 Jan 2010

• Space at the Properties is highly sought after• Notable tenants in Starhill Gallery include Louis Vuitton, Audemar Piguet,

Bottega Venetta, Boucheron, Chopard and Van Cleef & Arpels• Notable tenants in Lot 10 include The Actors’ Studio, Guess, Apple, Isetan and

Debenhams

Strong Tenant Base with Excellent Brand Recognition

40Starhill Global REIT

approval at EGM

40

Estimated geographical revenue contribution post transactions

C t t ti i k ill b d d t i itiCountry concentration risks will be reduced post acquisitions

Gross Revenue by Country(4Q 09)

Estimated Gross Revenue by Country(post Australian acquisition)

China14%

Japan7% Australia

9%

Japan6%

China13%

Singapore79%

Singapore72%

28 Jan 2010 41Starhill Global REIT 41

References used in this presentation

1Q, 2Q, 3Q, 4Q means the periods between 1 January to 31 March; 1 April to 30 June; 1 July to 30 September; and 1 October to 31 December respectively

CMBS means Commercial Mortgage Backed Securities

DPU means distribution per unit

FY means financial year for the period from 1 January to 31 December

GTO means gross turnover

IPO means initial public offering (Starhill Global REIT was listed on the SGX-ST on 20 September 2005)

NLA means net lettable area

NPI means net property income

pm means per month

psf means per square foot

WA and NAC mean the Wisma Atria Property (74.23% of the total share value of Wisma Atria) and the Ngee Ann City Property (27.23% of the total share value of Ngee Ann City respectively).

All values are expressed in Singapore currency unless otherwise stated

28 Jan 2010 42Starhill Global REIT

Disclaimer

This presentation has been prepared by YTL Pacific Star REIT Management Limited (the “Manager”), solely in its capacity as Manager of Starhill Global Real Estate Investment Trust (“Starhill Global REIT”). A press release has been made by the Manager and posted on SGXNET on 28 October 2009 (the “Announcements”). This presentation is qualified in its entirety by, and should be read in conjunction with the Announcement posted on SGXNET. Terms not defined in this document adopt the same meanings in the Announcements.

The information contained in this presentation has been compiled from sources believed to be reliable. Whilst every effort has been made to ensure the accuracy of this presentation, no warranty is given or implied. This presentation has been prepared without taking into account the personal objectives, financial situation or needs of any particular party. It is for information only and does not contain investment advice or constitute an invitation or offer to acquire, purchase or subscribe for Starhill Global REIT units (“Units”). Potential investors should consult their own financial and/or other professional advisers.

This document may contain forward-looking statements that involve risks and uncertainties. Actual future performance, outcomes and results may differ materially from those expressed in forward-looking statements as a result of a number of risks, uncertainties and assumptions.

Representative examples of these factors include (without limitation) general industry and economic conditions, interest rate trends, cost of capital and capital availability, competition from similar developments, shifts in expected levels of property rental income, changes in operating expenses (including employee wages, benefits and training costs), property expenses and governmental and public policy changes. Investors are cautioned not to place undue reliance on these forward-looking statements, which are based on the Manager’s view of future events.

The past performance of Starhill Global REIT is not necessarily indicative of the future performance of Starhill Global REIT. The value of Units and the income derived from them may fall as well as rise. The Units are not obligations of deposits in, or guaranteed by, the Manager or any of its affiliates. An investment in Units is subject to investment risks, including the possible loss of the principal amount invested. Investors have no right to request that the Manager redeem their Units while the Units are listed. It is intended that unitholders of Starhill Global REIT may only deal in their Units through trading on the SGX-ST. Listing of the Units on the SGX-ST does not guarantee a liquid market for the Units.

28 Jan 2010 43Starhill Global REIT

28 Jan 2010Investor, Analyst and Media Contact: Ms Mok Lai Siong Tel : +65 6835 8633 Email : [email protected]