fortum’s view of future energy supply...fortum’s view of future energy supply nuclear science...

TRANSCRIPT

Fortum’s View of Future EnergySupplyNuclear Science and Technology Symposium (NST2016), 2-3 Nov 2016Tiina Tuomela, EVP Generation, Fortum

Energy sector is under transformation

2

• In the future– Energy is produced more and

more with unlimited renewableresources

– Production is distributed, andproducers and consumers rolesare partly overlapping

– Importance of flexible powergeneration increasing

– Digitalization brings newopportunities

Forecasted investments in powergeneration globally between 2015-2040(Source: IEA World Energy Outlook, New Policies Scenario)

Nuclear capacity will increase globally

• 59 reactors under constructionglobally, out of which 20 are in China*

• About 40 countries is assessingnuclear new-build while threecountries decided to abandonnuclear**

• Nuclear power generation is expectedto grow also in all IEA scenarios by2040**

3*World Nuclear Association, status in 1 September 2016**IEA World Energy Outlook 2015.

Global power generation capacity retirements andadditions in the IEA New Policies Scenario, 2015-2040**

+148 GW

Also in Europe nuclear remain long a significant part of theenergy system even though RES increases

1. RES-E targets: 2014 realisation 28%, 2020 target 36% and 2030 target about 45% corresponding to 37% total RES target.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

Electricity mix development in EU1

RES (non-hydro) Hydro Fossil Nuclear RES targets

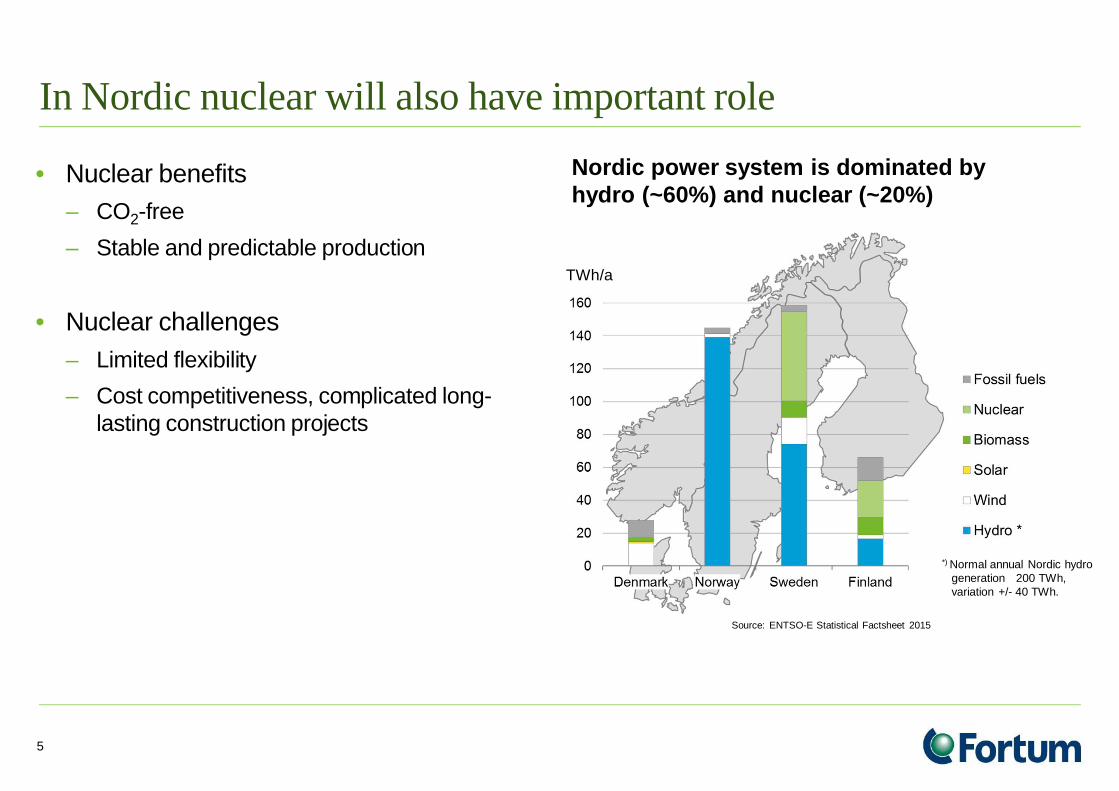

In Nordic nuclear will also have important role

• Nuclear benefits– CO2-free– Stable and predictable production

• Nuclear challenges– Limited flexibility– Cost competitiveness, complicated long-

lasting construction projects

5

Nordic power system is dominated byhydro (~60%) and nuclear (~20%)

*) Normal annual Nordic hydrogeneration 200 TWh,variation +/- 40 TWh.

Source: ENTSO-E Statistical Factsheet 2015

TWh/a

Market outlook and development of renewable energy sourcesforces also nuclear industry to renew

• Need to develop more standardizedplant designs, equipment andcomponents

• Promote development towardsharmonized licensing over differentmarkets and countries

• Utilize more best practices also betweendifferent industries

• Fasten technology development throughR&D, product development and piloting(passive safety systems / simplicity, smallmodular reactors, etc)

6

Nuclearindustry

Technologicaldevelopment

Competitiveness

Acceptability

Regulatoryframework

Nuclear technology outlook – several alternative trends

Economy of scaleComplex projects, large investmentsBeneficial when large amount of powerneeded (e.g. China) → serial deployment

Economy of serial productionManageable projects, stepwise investmentsSimplified, standardized conceptsInternationally harmonized regulatory approach

Short term VVER/AP1000Short/mid term ”CAP1400”Mid term SMR*

Decision to build a new nuclear power plant

Smallreactors(<300 MWe)

Largereactors

*Requires changes to current licensing frameworkand active participation to plant design work

VVER – Russia, AP1000 – USA, CAP1400 – Chinese version of Westinghouse’s AP1000SMR – Small Modular Reactors (several concepts)

Fortum focuses on improving productivity in power generation and findingnew revenue streams by utilizing strong in-house engineering expertise

8

9

Nuclear continues to be important for Fortum

Olkiluoto NPP

Loviisa NPP

Hanhikivi NPP

Forsmark NPP

Oskarshamn NPP

Operating reactorsNew-buildPost-operating phase

Fortum’s nuclear fleet

Fortum hydro assets (total 4,600 MW)

Ownership Capacity(Fortum share)

Production(Fortum share)

Loviisa 100 % 1003 MW 8 TWh

Olkiluoto 26.6% 468 MW 4 TWh

Oskarshamn 43.4% 812 MW 5 TWh

Forsmark 22.2% 727 MW 6 TWh

Total 3 010 MW 23 TWh

• Oskarshamn 2 reactor under post-operating phase andOskarshamn 1 will be closed down June 2017

• Minority owner in two new-build projects:Olkiluoto 3 (25 %) and Hanhikivi (6,6 %)

Many Fortum nuclear products and services are based oninnovative solutions developed for Loviisa NPP

10

• Licensing and design capabilities,e.g. ADLAS concept family

• Plant design

Strong in-house nuclearengineering department

Trust from nuclear operatorexperience

700+ nuclear experts

• Loviisa maintenance concept• APROS• Severe Accident Management• Probabilistic Risk Assessment

• Virtual reality applications• Data analytics• Power upgrades• Automation renewals

• NURES• Nuclear waste management

strategies and plans• Spent fuel management /

Posiva Solutions• Decom services• Solidification plant design

Examples of Fortum’s offerings over nuclear plant lifecycle

NuclearThank you!