formal institutional factors are underestimated in

TRANSCRIPT

0

`

Formal institutional factors are underestimated in

international joint venture performance: An empirical

research in the manufacturing and service sector

Yucheng Huang

S2522195

Supervisor: P.J. (Paulo) Marques Morgado

Co-assessor: M. Astarlioglu

MSc International Business & Management

Master Thesis

Rijkuniversiteit Groningen

Duisenberg Building

Groningen

The Netherlands

Tel: +31 611012008

E-mail: [email protected]

June, 2016

1

ABSTRACT

International joint venture performance is a challenge for businesses and scholars.

Transaction costs theory suggests success of joint ventures depends on the extent to

which transaction costs are lowered with elimination of uncertainties. Contextual

uncertainty in the host country is one factor having influence on the outcome of the

cooperation. Based on an institutional perspective in international business, contextual

variables, in which economic activities are embedded, have impacts on joint venture

performance. While informal institutional factors draw enough attention of scholars

and businesses, if the effects of formal institutional factors are underestimated in the

practice of international joint ventures remains unclear.

In this research, two specific regulatory institutional factors, contract enforcement

and access to infrastructure, are selected to analyze for their impacts on actual

outcomes of international joint ventures to differ from its expected values. Through

the analysis, it is expected to find the actual performance of joint ventures differ from

the expectation of the cooperation. The difference is assumed to be due to the impacts

of formal institutional factor are underestimated. Also, the research is expected to find

positive influences of having a high level of formal institutional factors on the actual

joint venture performance.

This research chooses a sample of 99 international joint venture cases over the

world between 2007 and 2016, within the manufacturing and service sector.

Key words: International joint venture, performance, transaction costs, institutional

factors, contract enforcement, infrastructure

2

TABLE OF CONTENT

ABSTRACT .............................................................................................................................. 1

INTRODUCTION ..................................................................................................................... 4

LITERATURE REVIEW .......................................................................................................... 8

International joint venture and Transaction costs theory ....................................................... 8

International joint venture performance ................................................................................ 9

To eliminate uncertainties - the Control-performance relation ....................................... 10

To eliminate uncertainties - Bargaining .......................................................................... 11

Expectation vs actual IJV performance ........................................................................... 12

Institutional perspective on joint venture performance ....................................................... 13

Normative and cognitive factors on international joint ventures..................................... 14

Regulatory factors on international joint ventures .......................................................... 15

Contract enforcement ...................................................................................................... 16

Infrastructure access ........................................................................................................ 18

Conceptual Model ............................................................................................................... 19

METHODOLOGY .................................................................................................................. 20

Research Design .................................................................................................................. 20

Research strategy and time horizon ................................................................................. 20

Samples and data collection ................................................................................................ 21

Measurement of variables.................................................................................................... 23

Expected performance of IJV .......................................................................................... 23

Actual performance of IJV .............................................................................................. 23

Contract enforcement ...................................................................................................... 23

Access to infrastructure ................................................................................................... 24

Control variables ................................................................................................................. 24

Industry type .................................................................................................................... 24

Data analysis ........................................................................................................................ 25

Analysis ................................................................................................................................... 27

3

Descriptive Analysis ............................................................................................................ 27

Correlations ......................................................................................................................... 28

Multicollinearity .................................................................................................................. 29

Inferential Analysis ............................................................................................................. 30

T-test ................................................................................................................................ 30

Regression ....................................................................................................................... 31

CONCLUSIONS ..................................................................................................................... 33

Managerial Implications ...................................................................................................... 36

Limitations and future research ........................................................................................... 37

REFERENCE .......................................................................................................................... 39

4

INTRODUCTION

International joint venture has become a major business and organizational form

for MNEs (Child, 2002; Hu & Chen, 1996). With more firms internationalizing and

market continues globalizing, international joint venture provides MNEs opportunities

to expand in global market rapidly, create scale of economy, acquire and facilitate

strategic resources, reduce risk, learn new knowledge and skills (Park & Ungson,

1997). However, the performance of international joint venture continues to be a

challenge for players and scholars considering its high instability and consequently a

high rate of dissolution (Park & Ungson, 1997; Pothukuchi, Damanpour, Choi, Chen,

& Park, 2002). The exit rate of international joint venture is around 50 percent, which

is higher than mergers and acquisitions in some industries (Park & Ungson, 1997).

What cause such instability and what influence the implementations of joint

ventures with enhancing the performance? To look into the issue, transaction costs

theory is selected as the theoretical foundation of this research. Uncertainty of the

environment in the host country and the behavior of the alliance partners could

significantly increase transaction costs in the alliance which would negatively affect

the performance (Child & Yan, 2003; Yiu & Makino, 2002). Level of control is an

important predictor of the performance of joint ventures (Child & Yan, 2003). MNEs

often increase their level of control over the cooperation in order to eliminate risks

due to the lack of trust in the partners to avoid opportunism behaviors (Beamish, 1993;

Gulati, 1995).

However, with involving these firm-level factors into considerations, the result

might still be difficult to predict. This is because some other factors can also be

influential for IJV performance. These factors are country-specific and affected by the

local environment. Institutional theory suggests that economic activities are embedded

in, which means deeply influenced by, the social environments (Bae & Salomon, 2010;

5

DiMaggio, P. J & Powell, W.W, 1983). Thus the instability of IJV performance might

be influenced by the risks and uncertainties in the local environment (Beamish, 1993;

Child & Yan, 2003; Granovetter, 1985; Kostova, 1997).

With an institutional perspective in international business, institutions are the

“rules of the game” for MNEs to operate in different countries (North, 1990). The

institution environment has a key impact on the entry mode selection and performance

(Bae & Salomon, 2010; Kogut & Singh, 1988; Kostova, 1997). Institutional theory

distinguishes institutions with three pillars: regulatory (e.g. laws), cognitive (e.g.

habitual actions) and normative (e.g. culture, professions) (Scott, 2005). These

structures and activities have various carriers, such as cultures, structures and routines

(Scott, 2005).

Former studies have emphasized on and have provided empirical proof of the

effects of culture distance or other cognitive/normative factors on IJV performance

(Kogut & Singh, 1988; Oxley, 1999; Park & Ungson, 1997; Pothukuchi et al., 2002).

Oxley asserts long cultural distance would increase costs of joint ventures relative to

contractual alliances (Oxley, 1999). Park & Ungson found difference in cultures adds

misunderstanding and consequently lead to IJV failure (Park & Ungson, 1997). Some

studies, applying the Hofstede cultural dimensions, found the national culture

difference between joint venture parents has a major impact to cause IJV failure and

unsatisfied performance (Pothukuchi et al., 2002). It also has been noticed that

national culture distance increases costs of acquisitions relative to green field or joint

ventures because of the difficulties to integrate foreign management (Kogut & Singh,

1988).

However, comparing with the studies on the informal institutions, less attention

has been paid to analyze how “formal institutional” factors influence the actual

performance of the cooperation. Other than national culture distance, institutional

perspectives in international business suggest that formal factors such as institutional

system, political system, infrastructure, legislations and laws, also influence economic

6

activities (Kostova, 1997; Scott, 1995). These factors are categorized as the regulatory

pillar according to the institution theory (Kostova, 1997; Scott, 1995). In terms of

measuring IJV performance, studies suggest these “unmanageable” exogenous

success factors may create uncertainties and thus influence the actual performance of

IJV to be different from the expected value.

In order to gain more insights into the role that formal or regulatory institutional

factors plays on IJVs performance, this research selects two specific factors, namely

contract enforcement and infrastructure accessibility.

Quote from Rousseau, Rousseau & McLean Parks (1993) “Contracts are

fundamental to ….. actions of organizations. They imply cooperation and consensus,

but often engender dispute and disagreement”. No matter how well-design the

contracts are, violations of the agreements from one or both sides of the partnership

always occur (Antia & Frazier, 2001). The contract enforcement reflexes as the time,

cost and procedural complexity to resolve a standardized commercial dispute between

two businesses (World Bank Group, 2016a).

Infrastructure is considered as “life supporting services”and has long been under

the monopoly of government in countries like China (Zhang, Gao, Feng, & Sun,

2015). In this research, the access to electricity is chosen to measure the level of

infrastructure in the country where the IJVs takes place. It measures from all

procedures required for a business to obtain a permanent electricity connection and

supply, which include applications and contracts with electricity utilities, all necessary

inspections and clearances from the distribution utility and other agencies, and the

external and final connection works (World Bank Group, 2016b).

Therefore, the research question for this research is: Are formal institutional

factors underestimated in the actual international joint ventures performance?

Most studies look into only one or two developing countries while analyzing the

effects of institutional difference on international joint ventures performance. Most

researches chose China since it is one of the most popular FDI destinations in recent

7

years (Beamish, 1993; Child & Yan, 2003; Hu & Chen, 1996). Instead of looking into

one country, this research selects completed IJV cases over the world in the

manufacturing and service sector, which take place during 2007 to 2016.

Through this research, the effects of regulatory/formal institutional factors on the

actual performance of international joint ventures can be tested. This research focuses

on two specific factors: contract enforcement and infrastructure accessibility. High

level of contract enforcing quality and infrastructure accessibility are expected to

lower transactional costs and uncertainty in the cooperation. This helps MNEs to

create competitive advantages and also ensure the success of international joint

venture.

The research is expected to find that contract enforcement and infrastructure

accessibility are not sufficiently considered in the estimation of IJV performance

before being implemented. The insufficient considerations are reflected as a

difference between the actual and the expected performance. Moreover, the impacts of

the two institutional factors on IJV performance are expected to be considerable. On

that basis, it is also expected to find the influence by these two factors is significantly

positive. In another word, the actual IJV performance will be higher than the expected

value when contract enforcement has a higher quality or when infrastructure is easy to

access in the local context.

This research will have managerial implications as well. Formal institution

factors, such as contract enforcement and infrastructure accessibility, need to draw

more attention of managers. Besides, the formal institutional factors should be more

taken into the considerations when planning for International joint ventures.

8

LITERATURE REVIEW

International joint venture and Transaction costs theory

While competitiveness and competitive advantage have become the keywords

that draw a lot of attention from MNEs with the development of globalized economy,

international joint venture has become a major business and organizational form for

MNEs (Child, 2002; Hu & Chen, 1996). IJV is a separate legal organizational entity

representing the partial holdings of two or more parent firms, in which the

headquarters of at least one parent firm is located outside the country of operations of

the joint venture.” (Shenkar & Zeira, 1987). A common form of IJV is to establish an

entity between an MNE and a local domestic company in the country which the local

partner operates (Shenkar & Zeira, 1987).

The selection of strategic alliance, as a third alternative in governing economic

activities other than hierarchy and market, depends on the magnitude of the

transaction costs involved (Chen & Chen, 2003; Yiu & Makino, 2002). Transaction

costs theory suggests high uncertainty and opportunism are important variables that

make businesses choose joint ventures over contract (Chen & Chen, 2003; Child &

Yan, 2003; Kogut & Singh, 1988; Yiu & Makino, 2002). Pisano suggests that the

more transaction costs in the alliance, the more hierarchical governance would be

chosen (Pisano, 1989).

International joint ventures offer more control mechanisms to eliminate

uncertainty and lower transaction costs (Chen & Chen, 2003; Yiu & Makino, 2002).

There might be unexpected changes in the context, thus increases transaction costs by

monitoring, enforcing and regulating via market mechanism. Similarly, behaviors of

the partners and their performance are difficult to observe and measure by contractual

relations. Transaction costs theory thus suggest, in order to eliminate the uncertainty

and following difficulties to evaluate performance, equity joint ventures are better

solutions, over contracts, for MNEs (Chen & Chen, 2003).

9

Uncertainties can be categorized into two forms: contextual or behavioral

uncertainties (Yiu & Makino, 2002).Contextual uncertainty includes the bounded

rationality of decision makers and it rises from changes of institutional conditions

such as political and economic instability, legal rules, and cultural and social relations

embedded in national environment. For example, study found joint ventures are used

by MNEs to reduce political risks through a share of ownership with local firms

(Hennart, 1988). Although he mentioned that the motive is not obvious enough since

firms can reduce the visibility and still exploit advantages through other entry modes

such as licensing and franchising. But in the meanwhile, study suggests that

considering the appropriate costs and the needs for managing uncertainty, a

governance mode which can provide more hierarchical control than market is

preferred (Gulati & Singh, 1998). Therefore, joint venture is preferred as an efficient

governance mode by MNEs, based on the transaction costs theory.

International joint venture performance

The performance of international joint venture continues to be a challenge for

players and scholars while there is high instability for the activity and a high rate of

dissolution (Park & Ungson, 1997; Pothukuchi et al., 2002). Joint venture

performance is evaluated in different ways and inconsistencies in terms of

measurements occur: 1) the performance is measured from whose perspective (one

partner, both parties, or management); 2) performance indicators (varies from

financial indicators to subjective judgements) (Yan & Gray, 1994). These

inconsistencies make the comparison across studies and generalizations about joint

venture performance problematic (Yan & Gray, 1994). To assist the contraction of this

research, a brief discuss of few measurements and indicators will be given following.

A typology defines two perspectives on IJV performance, which are referred as

goal performance and system performance (Child & Yan, 2003). The goal

performance reflects the extent to which the objectives of both sides of the joint

venture are reached. To be more specific, a goal performance can be seen when both

10

parties in the joint venture reaches their own strategic objectives, such as lower the

transaction costs, access to the strategic resources that is absent but needed, or learn

new knowledge and skills, enter the new market with adapting to the new

environment, or share risks operating in the foreign market. The system performance,

which reflects more directly compared to the goal performance, shows if the venture

performs well as a business unit. It can be seen as if the joint venture partners recover

their financial capital investment. Ideally, an IJV should be able to meet both

performance definitions.

Similarly, some other researches summarize the methods of measuring joint

venture performance as objective (termination, duration, financial gains) and

subjective (goal attainment, satisfaction) types (Beamish, 1993; Park & Ungson,

1997). Furthermore, Beamish found there is a correlation between the subjective and

objective performance in both developed and developing countries (Beamish, 1993).

It suggests that the subjective measures, which reflect as satisfactory towards the

cooperation or the extent to which the goal of IJV was achieved, will have impact on

the objective measures of the performance, and vice versa.

To eliminate uncertainties - the Control-performance relation

Control is a critical concept for performance of joint ventures by overcome

uncertainties (Child, 2002; Geringer & Hebert, 1989; Yan & Gray, 1994). Related to

the issue of eliminating uncertainty, two types of factors are identified by studies that

would determine joint ventures performance: endogenous and exogenous success

factors (Child, 2002). Child sees the endogenous success factors are the manageable

ones for the parents in the alliance. These are the firm level factors concerns such as

legal independence of parent firms creates control problems, cultural differences. To

manage such endogenous factors, theories give solutions to increase the level of

control, by increasing ownership for example, in the alliance, thus lower the

transaction costs (Beamish, 1993; Child & Yan, 2003; Yiu & Makino, 2002).

Control refers to the process, through the use of power, authority and a wild range

11

of bureaucratic, cultural and informal mechanisms, to influence subunits and members

to behave in ways that lead to the attainment of organizational goals (Geringer &

Hebert, 1989; Yan & Gray, 1994). Insufficient or ineffective control limits managers’

ability to coordinate activities and the efficiency to implement strategies (Geringer &

Hebert, 1989).

To increase the control level, it can be done through both capital and non-capital

investment, which can be shown in both strategic and operational aspects (Child,

2002). Capital control concerns the cash resource and other assets on joint venture

balance sheet (Child, 2002). For example, land, provision of technology, facilities and

brand names. This is seen as equity ownership by studies in alliances. However, it

cannot ensure a high control level (Geringer & Hebert, 1989). In most of the cases,

majority equity ownership means a dominant control, especially in the developed

countries (Beamish, 1993). The non-capital investment includes management, system,

service and training and other factors that cannot be capitalized into assets (Child,

2002). The control is enhanced by the increase of dependence of the venture. This

reflects a high commitment by the parent to the alliance (Child, 2002).

However, researches cannot find consistent results on the relationship between

control and performance (Child, 2002; Geringer & Hebert, 1989). In another word, a

high control level does not ensure a high level of performance. Moreover, it has been

suggested that when foreign firm hold more than 50 percent of the equity, the joint

venture is considered “unstable” (Beamish, 1993). In order to overcome this, the local

partner can limit the instability by contributing more other than only offering local

knowledge (Beamish, 1993). Thus it can be seen that a trade-off of control between

the foreign and local partners would eliminate the uncertainty to some extent but not

ensure the success of the joint venture.

To eliminate uncertainties - Bargaining

To look deeper into the issue of control, the effect of bargaining power and costs

on eliminate uncertainty is found. Bargaining power refers to the one part’s ability and

12

power to change the outcome of the negotiation and to win the accommodations from

the other party (Yan & Gray, 1994). During the process specifying the mutually

acceptance on the conditions and the cooperation, these bargaining will generate

uncertainty and thus bargaining costs (Pearce, 1997). According to Pearce, such

uncertainty might stem from lack of trust, imperfect communication, anticipated

difficulties and verifying post-contract performance, or the JV environment (Pearce,

1997).

Interestingly, while other studies relate bargaining power with accessing and

transferring local knowledge, and efficiency of acquire resources (Inkpen & Beamish,

1997; Yan & Gray, 1994), Pearce asserts that time has more opportunity costs

comparing with bargaining costs. He suggests that the time spending on the

bargaining can save more time to make more important strategic decisions. Therefore,

to have a strong bargaining power in the joint venture would save more time in the

bargaining and that means task of reaching and higher quality of implementation of

decisions (Pearce, 1997). Therefore, a high bargaining power would be important for

the success of joint venture.

Expectation vs actual IJV performance

To have an expectation of IJV performance is one thing while if getting the same

actual performance or even getting an actual performance is another. More than half

the intended joint ventures in China have not even been actually implemented while

signing agreements normally means a very likely implementation in other countries

(Beamish, 1993). As joint ventures are wildly acknowledged as a difficult form to

manage, which cause a high (30% to 70%) of management dissatisfaction and early

terminations, researches did not look into the management process and

implementations (Pearce, 1997). This research suggests this high rate of failure to

implement might because of the uncertain factors in the country.

As mentioned previously, there is another success factor that Child’s study

mentions - the exogenous success factors which is labeled as “unmanageable” for

13

MNEs (Child, 2002). These factors for example, are institutional and economical

context where the joint venture is located (Child, 2002). These unmanageable factors

would increase the uncertainty and risks to allow more opportunism behaviors. New

institutional economics suggests that room for opportunism and uncertainty creates

risks which would lead to an increase of transaction costs (Granovetter, 1985;

Williamson, 2000; Yiu & Makino, 2002). Since economic behaviors are embedded in

the local social, cultural, political environment (DiMaggio, P. J & Powell, W.W, 1983;

Granovetter, 1985), the uncertainty in the context will significantly affect the outcome

the economic activities, for example joint venture in this case.

In the research of the high instability of joint venture in terms of unexpected

terminations, Park and Ungson assert that companies generally would not dissolute

successful joint ventures but only when the cooperation are not financially viable

(Park & Ungson, 1997). They found national cultural distance have a significant

impact on the success rate of the strategic cooperation after it has been implemented

(Park & Ungson, 1997).

Therefore, it should be logical to assume that the institutional factors are having

impacts to international joint venture performance during implementations. These

factors make international joint ventures actual performance differ from the expected

performance. In another word, in the process of implementation of the joint venture,

the presence of these institutional factors, which are difficult to manage, the actual

outcome is deviated from the “ideal” performance that being expected. Thus the null

hypothesis is formulated as:

Ho. The actual performance of international joint ventures is the same as the

expected value prior to the joint venture.

Institutional perspective on joint venture performance

Institutions are the “rules of the game” for MNEs to operate in different countries

(North, 1990). Understand the difference in institutional context between countries is

14

critical for firms to expand their business across national boundaries (Bae & Salomon,

2010). Economic activities are embedded in, which means deeply influenced by, the

social environments (Bae & Salomon, 2010; DiMaggio, P. J & Powell, W.W, 1983). It

is not surprise to find that institutional distance has a key impact in entry mode

selection and performance (Bae & Salomon, 2010; Kogut & Singh, 1988; Kostova,

1997).

It has been observed by studies MNEs often face the “liability of foreignness”

which stem from a lack of knowledge about local culture, regulations. Consequently

the LOF would increase the transaction costs in the operation (Bae & Salomon, 2010).

To overcome the liability of foreignness, firms need to seek legitimacy in order to

survive the social environment through corresponding to regulations and norms,

which means efforts should be done on both formal and informal institutional

distance.

Institutions include 3 pillars, which are regulatory (e.g. laws), cognitive (e.g.

habitual actions) and normative (e.g. culture, professions) structure and activities,

with various carriers, such as cultures, structures, routines (Scott, 2005). Some studies

categorize them into two: the formal and informal institutions.

Normative and cognitive factors on international joint ventures

Plenty previous studies have paid attention to the informal institutions based on a

cultural distance perspective. Oxley asserts it suggests long cultural distance would

increase more costs for joint ventures relative to contractual alliances (Oxley, 1999).

Park et al found difference in cultures adds misunderstanding and failure in

cooperation in terms of IJVs (Park & Ungson, 1997). Some studies, using the

Hofstede cultural dimensions, found the national culture difference between joint

venture parents has a major impact to cause IJV failure and unsatisfactory

performance (Pothukuchi et al., 2002). It also has been suggested that national culture

distance increase costs for acquisitions relative to green field or joint ventures because

of the difficulties to integrate foreign management (Kogut & Singh, 1988).

15

The cultural difference has impacts on the control in the cooperation. A long

geographical and cultural distance would present a particular challenge for manage

the control in the joint venture (Child, 2002). Moreover, since the basic believe and

values are different between countries while they have a long cultural distance, e.g.

Japan and United States, it would have difficulties in the negotiation. The difference

in culture would influence the mutual confidence and trust of mangers and in return

challenge the efficiency of negotiations (Peterson & Shimada, 1978). Therefore it

would have impact on the performance of joint venture by increasing the bargaining

costs.

It is obvious that informal institutions matter for the international joint venture

performance. However, much less attention is paid to the formal institutional factors.

The regulatory pillar, while the normative and cognitive pillars representing the

informal institutions, is playing as the only part in the framework speaks to formal

institutions (Bae & Salomon, 2010). It should be logical to assume the formal

institutions are also important for MNEs to consider while form and evaluate

international joint ventures. Thus this report will look into the effects of formal or

regulatory institutional factors.

Regulatory factors on international joint ventures

Institutional theory emphasizes regulatory factors which are often specific to a

country (Huang & Sternquist, 2007). Quote from Scott the regulatory component

“reflects the existing laws and rules in a particular national environment which

promote certain types of behaviors and restrict others.” (Scott, 1995). For example,

legal regulations represent the pressure the MNEs need to face while operating in the

host country (Huang & Sternquist, 2007). According to Bae & Salomon, Regulatory

distance measures the difference in the enactment and enforcement of regulations

(Bae & Salomon, 2010). Moreover, study found that regulatory distance is an

important factor, not only in general, but especially for certain industries such as

16

utilities sector to consider while operating abroad (Bae & Salomon, 2010).

As mentioned previously based on the transaction costs theory, one of the most

important motives of going for international joint venture is to lower transaction costs

to gain competitive advantages. As mentioned by Bae & Salomon, formal rules are

designed to facilitate exchanges reducing transaction costs. These institutions reduce

transaction costs through improving the security of property rights and contract

enforcement (Bae & Salomon, 2010).

Moreover, the rule of law is codified by a country’s governance infrastructure

(Huang & Sternquist, 2007). Thus, the study found that the host country’s level of

infrastructure can effectively reduce uncertainty of operating in the host country and

make it possible to predict what the firm can expect from the local legal system.

Thus it should support the findings from previous researches that formal

institutional factors would significantly influence joint venture performance.

Contract enforcement

“Contracts are fundamental to ….. actions of organizations. They imply

cooperation and consensus, but often engender dispute and disagreement.” (Rousseau

& McLean Parks, 1993). As a matter of fact, contractual alliances can offer a number

of advantages to the cooperation such as flexibility, less institutional relationship

between partners (Chen & Chen, 2003). However, as mentioned previously, control is

an important mechanism that MNEs want to have in order to achieve success. Thus, it

was suggested by Chen that equity joint venture, as more hierarchical governance

mode, is more preferred than contractual alliances by MNEs when transaction costs

are high (Chen & Chen, 2003).

The study suggests that the selection of equity joint venture over contractual

alliance is based on an assumption that contract can be effectively enforced(Chen &

Chen, 2003). A complete contract will reduce transaction costs, contractual hazards,

and operational risks and in turns boost business performance (Gong, Shenkar, Luo, &

NYAW, 2007). The completeness of the contract would gain importance under high

17

uncertainty and nontrivial commitment and thus cost-minimizing transactions would

be possible in the contract-implementation stage (Gong et al., 2007).

However, it has been brought up by studies that every joint-venture contract is

necessarily incomplete and no matter how well-design they are, there are always

violations of the contracts from one or both sides of the partnership (Antia & Frazier,

2001; Henisz, 2000). Furthermore, although it should be equal to all the players in the

context, some individuals create the rules and contracts in their own private interest.

Transaction costs will rise and contractual hazard will happen consequently (Aidis,

Estrin, & Mickiewicz, 2008; Henisz, 2000).

Therefore, as joint venture being selected by MNEs as a governance mode for

strategic alliance, which has more hierarchical control over a pure contractual alliance,

an effective enforcement over the contracts is needed to ensure the performance.

Moreover, while operating joint ventures in some countries, firms rely on trust

other than contract (Child & Yan, 2001). It has been found that companies from

countries with Anglo-Saxon cultures relies more on the contracts while Japanese rely

on trust. But even if there is a huge difference view towards contracts, businesses

from Japan would rely on some formal dispute settling mechanisms to achieve a

mutual goal and ensure the success of the cooperation (Gong et al., 2007).

Considering the literature, it is logical to assume that while the institutional

environment in term of contract enforcement is strong, there should be lower

transaction costs and lower level of uncertainty which would have a positive effect on

the performance. Thus, the hypothesis is formed as

H1: Higher performance of the international joint venture is achieved when

contract enforcement is higher

18

Infrastructure accessibility

Infrastructure is considered to be “life supporting services”and has long been

under the monopoly of government in countries like China (Zhang et al., 2015).

Insufficient access to infrastructure has been a problem for almost all countries; this

problem is exacerbated by the lack of funds available in the public sectors (Zhang et

al., 2015).

Infrastructure may be and may not be physical presences. Joint venture accesses

to the new markets with quick speed and low price by borrowing local infrastructures

(Inkpen & Beamish, 1997). These infrastructures could be sales forces, local plants,

market intelligence, and the marketing presence necessary to understand and serve

local market (Inkpen & Beamish, 1997).

The availability of infrastructure is important for attracting FDI. From a

resource-based view, having more access to the infrastructure means MNEs can reach

more country-specific advantages which allow MNEs to use these CSAs to build

competitive advantages (Buckley, Forsans, & Munjal, 2012). That allows MNEs to

internalize and transfer these CSA and integrate with their own FSAs to build

competitive advantages so enhance the productivity eventually. Studies also assert

that through joint ventures, MNEs can learn from local partners for knowledge and

skills to deal with the regulatory institutions, which are unfavorable for foreign

players, such as institutional infrastructures (Yiu & Makino, 2002). From a transaction

costs theory, study found joint ventures in developing countries such as China and

Brazil would face low level of accessing to infrastructure, comparing with developed

countries. Alliances in such countries would face more uncertainties which lead to an

increase in transaction costs (Child & Yan, 2003).

Moreover, the access to existing infrastructure affects the decision of MNEs if

they need to build their own infrastructure (Bourreau, Doğan, & Lestage, 2014). If

MNEs decide to build their own infrastructure, that would increase the opportunity

costs. A high level of accessibility requires relatively small up-front investment.

19

Based on the theory of transaction costs that minimizing transaction costs can ensure

the performance of a cross-border M&A, a high accessibility to the local

infrastructure might imply a better performance for the M&A practice.

Electricity system is a critical infrastructure for modern society (Krause, Vachon,

& Klassen, 2009). Electricity consumption is positively correlated with GDP thus is

important for the economic development (Jumbe, 2004). Research also shows that

electricity generation, as a typical economic infrastructure, also reflects the political

environmental changes (Henisz, 2002). Krause assert that a well-developed and

advanced electricity system would ensure the capacity of the infrastructure in the

nation (Krause et al., 2009). Thus it is logical to assume a high level of access to

infrastructure in the host country would have positive effect on the actual performance

of the international joint venture. Thus the hypothesis is

H2: Higher performance of the international joint venture is achieved when access

to infrastructure is higher

Conceptual Model

Actual performance

of IJV Expectation of IJV

H1

H2

Contract enforcement

Access to infrastructure

+

+

20

METHODOLOGY

The purpose of the research is look into the impact that two specific formal

institutional factors, namely contract enforcement and infrastructure accessibility,

have on international joint venture performance. The research asks for an appropriate

research design.

Research Design

The research is designed based on a positivism and empiricism assumption on the

phenomena. Positivism believes that true belief is grounded in what can be perceived

and that what can be perceived is based on the reality (Ryan & Scapens, 2002).

Since it is a positivism research, a deductive approach will be suitable to be

applied in this research to test the hypotheses based on the observation of the

phenomena and the data collected.

Research strategy and time horizon

In order to have a better understanding on the effects that institutional factors

have on IJV performance, by testing the hypotheses, a quantitative research will be

applied. To apply a quantitative research means a quantity of data are needed to be

collected to establish a statistically significant result. This research will apply an

archival research strategy which is conducted with existing material. Data will be

collected from existing databases to test the hypotheses to fit with a quantitative

deductive research approach. Since this report applies only a quantitative research,

thus it is a mono-method research.

This research is a cross-sectional research. Completed international joint venture

cases from 2007 till present will be investigated. The Global financial crisis has

affected business and countries worldwide (Dornean, Işan, & Oanea, 2012; Lairson,

2011) The year from 2007 till 2016 is a decade that world economy recovering from

the financial crisis, during which more joint ventures might occur internationally.

21

During this time, more risks and uncertainties might be faced by MNEs and

international joint venture activities. Thus, the impacts of institutional factors on

performance might be more significant. This setting of time horizon will also ensure

more samples can be selected so to test the hypotheses.

Samples and data collection

In total 99 International joint venture cases since 2007 in manufacturing and

service sectors is collected from Zephyr (Table 1). The list of the match between

country and country code can be found in Appendix. Among the 99 cases, most of

them occur in China. The regulatory standards differ regionally in such a big country.

Thus this research distinguishes China into 3 regions: China-Beijing (CN-B),

China-Shanghai (CN-S) and China-other (CN). Similarly, Japan is distinguished into

Japan-Tokyo (JP-T) and Japan-Osaka (JP-O). Russia has two regions: Russia-Moscow

area (RU-M) and other (RU).

Overview of IJV cases

Target

Country Frequency Percent

Cumulative

Percent

Country

code Frequency Percent

Cumulative

Percent

CN-B 17 17.2 17.2 ES 2 2.0 85.9

CN 13 13.1 30.3 GB 2 2.0 87.9

CN-S 11 11.1 41.4 JP 2 2.0 89.9

IT 8 8.1 49.5 SE 2 2.0 91.9

JP-T 7 7.1 56.6 AT 1 1.0 92.9

MY 5 5.1 61.6 GR 1 1.0 93.9

TH 5 5.1 66.7 IN 1 1.0 94.9

FR 3 3.0 69.7 NO 1 1.0 96.0

JP-O 3 3.0 72.7 PH 1 1.0 97.0

KR 3 3.0 75.8 RU 1 1.0 98.0

KY 3 3.0 78.8 RU-M 1 1.0 99.0

TW 3 3.0 81.8 UA 1 1.0 100.0

DE 2 2.0 83.8

The reason of choosing secondary data is it is more time efficient being collected

and analyzed over primary data. To collect primary data from multi-national retailers

Table 1 Overview of IJV cases

22

will be very timely consuming.

Joint ventures taking place around the world are considered. Not only are

developing countries included, but also developed countries. The reason to include all

the countries is that institutional factors are believed to be equally important when it

comes to joint venture performance estimations. No matter it takes place in

developing countries or developed countries, or what motive MNEs have on starting

the alliance practice, the difference in national conditions are significant for MNE

considerations.

Data of institutional factors is collected from the Doing Business Project (DBP)

provided by World Bank. The DBP measures the regulations applied to businesses

through their life cycles. In this research, two specific types of regulatory institutional

factors are selected from the data base. The indexes for “enforcing contracts” and

“access to electricity”, which is the measurement for infrastructure accessibility, are

collected. The DBP project was started in 2002 and the first release was in 2003. The

project updates annually with well-developed methods. In this research, the selected

indicators are from the latest updated data which is based on the research in 2015.

In some countries, since the difference within the country, the DBP gives different

scores for different regions in the country. For example, two sets of data are given for

China, namely Beijing and Shanghai. The two cities are the most important for the

country which have significant influence to the region. The same typology applies to

Japan (Tokyo and Osaka).

By the empirical analysis, hypotheses should be supported by the data and the

research question should be able to be answered eventually. By focusing on a defined

industry, the effect due to other variables which not being included in this research

will be reduced. The result should be able to be generalized into other retailing

industries since no particular fashion-industry-related variables are included in this

research.

23

Measurement of variables

International joint venture cases are collected world wildly, thus it is predictable

they are implemented in region currencies. In order to eliminate the risk that currency

exchange rate causes, all the financial indicators are transferred into US dollars based

on a yearly average exchange rate, which shows at thousands.

Expected performance of IJV

The expected performance of IJV is measured by the pre-deal target revenue. The

pre-deal revenue is the revenue before the deal was announced. For example, in the

AMUNDI SA case, both parties announced the joint venture in July of 2009.

Therefore the pre-deal revenue is for the end of the previous year, 2008. Since the

number is before the joint venture was actually implemented to the field operations, it

is an estimated figure which both parties expected the cooperation hopefully might

achieve in the following year, after considering all the factors they believe would have

impacts on the practice.

Actual performance of IJV

Similarly, the actual performance of IJV cases is measured by revenue, which is

categorized as “Post-deal target financials”. The revenue data is for the first year after

the joint venture being completed. For example, the AMUDI SA case is announced

completion on 31 December 2009, thus the post-deal revenue is on the same date. The

difference in term of the revenue between one-year of implementation of the joint

venture shows how the actual outcome shifting from what it was expected.

Contract enforcement

The level of contract enforcement is measured by the “Enforcing Contract”

indicator from the Doing Business Project by World Bank. This indicator looks into

the efficiency of the judicial system in the host country to solve commercial disputes

by measuring time and costs (World Bank Group, 2016a). In this research, more

specifically, the quality of judicial process is selected as the measurements of the

24

institutional variable contract enforcement.

The index measures if the economy adopts good practice in court system in four

dimensions with 18 points in total. By summing the points, the indicator shows that

the economy that scores higher means a better and more efficient judicial system.

Access to infrastructure

The access to infrastructure variable is measured by the “Getting Electricity”

indicator from the Doing Business Project by World Bank. The indicator looks into

the procedure for a business to obtain permanent electricity connection and supply for

a standardized warehouse (World Bank Group, 2016b). These procedures include

applications and contracts with electricity utilities, necessary inspections and

clearances from the distribution utility and other agencies, and the external and final

connection works (World Bank Group, 2016b).

In this research, the time a business needs to use to get permanent electricity is

applied to measure the level of access to infrastructure. The time is recorded as

calendar days. The median duration that electricity utilities and experts assert that is

necessary in practice, rather than required by law, is captured in the measurement. The

measurement also assumes no time is wasted by the business and each procedure is

being executed without delay. The time that used to gather information by businesses

is taken into considerations. Therefore, it means that the less the days that business

needs in the economy, the better access to infrastructure it can get in the economy.

Control variables

Industry type has been selected as control variable, which is outside of the scope

of this research.

Industry type

Businesses are selected within a limited industry. Key words of “manufacturing”,

“production”, “transform”, “conversion” and “service” are applied in the result filter.

Different industries would have significantly different outcome on the result.

25

According to the typology of economy sectors, there are three economic sectors:

primary sector (e.g. agriculture, fishing, and extraction such as mining), and

secondary sector, which is known as manufacturing sector, and lastly, tertiary sector,

known as service industry (Kaldor, 1976). Among the 3 sectors of world’s economy,

the primary sector is relatively stable comparing with the other two, which is also

defined as the non-industrial sector (Kaldor, 1976). Thus, the industrial sector,

including manufacturing and service sectors, is selected in this research.

Type Variable Description Source

IV Expected IJV performance Pre-deal Target revenue The Zephyr database

DV Actual IJV performance Post-deal Target revenue The Zephyr database

MV Contract enforcement Efficiency of the judicial system in

the host country to solve

commercial disputes by measuring

time and costs

The Doing Business

Project by World Bank

Group

MV Access to infrastructure Getting Electricity- time of getting

electricity

The Doing Business

Project by World Bank

Group

Control variable

CV Industry Type Manufacturing and Service sector Manually: filtered from

the Zephyr database

Data analysis

The following sections explain the statistical tests used to test the hypotheses. The

null hypothesis has the purpose of establishing whether there is a difference between the

expectations and actual outcome of joint venture performance. To test this hypothesis an

independent samples the t-test is performed. The other Hypotheses are aimed to test the

individual effects and the moderating effects. When one or several independent variables

are proposed to affect one dependent variable, regression is the appropriate technique to

use. The formula of a regression analysis is as follows:

Y = β0 + β1 * X1i + β2 * X2i + β3 * X3i +ε

Table 2 Overview of variables

26

Parameter β0 and β1 are the regression coefficients. β1 is the slope, while β0 is

the intercept of a straight line which connects Y to Xi. The slope tells what happens

with the interdependent variables if the dependent variable increases with one unit.

The ε is the error term, which bridges the difference between the actual Xi and the

estimated Xi. To apply to the hypothesis testing in this research, the formula of the

regression is as follows:

Actual outcome performance of IJV = β0+ β1* Expected performance of IJV+

β2* Contract enforcement + β3* Access to infrastructure + β4* (Expectation*

Contract enforcement) + β5* (Expectations * Access to infrastructure) + ε

27

Analysis

Descriptive Analysis

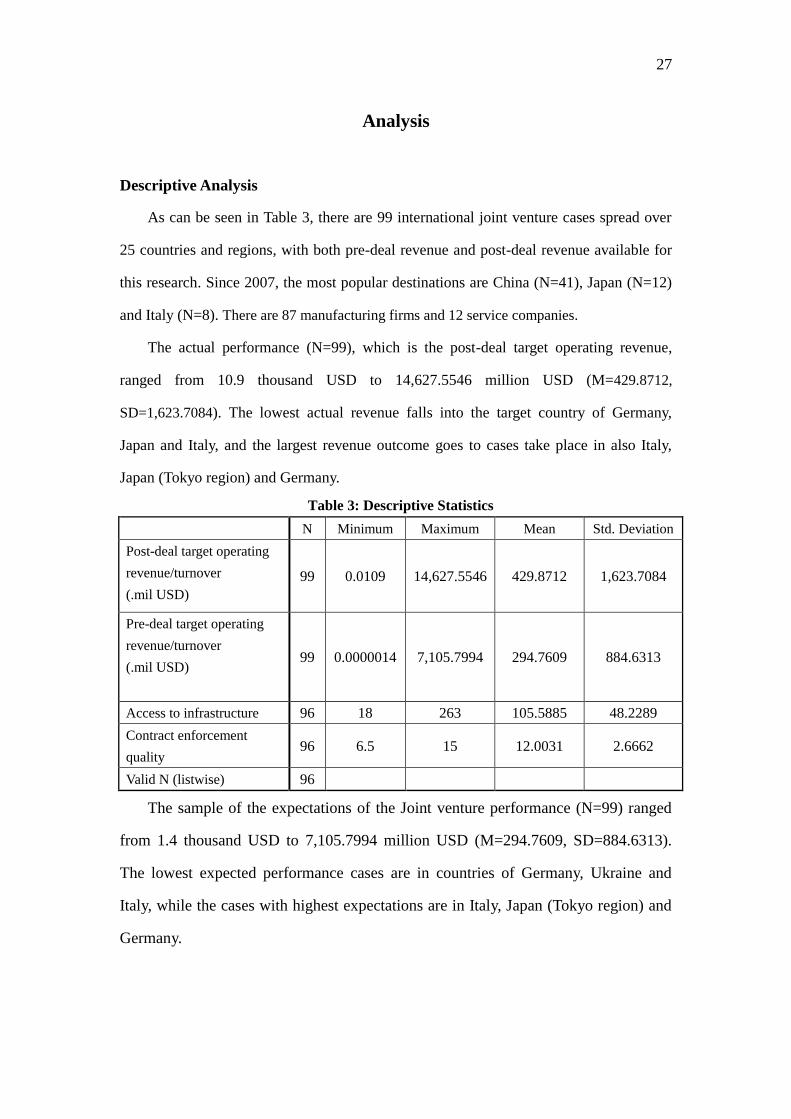

As can be seen in Table 3, there are 99 international joint venture cases spread over

25 countries and regions, with both pre-deal revenue and post-deal revenue available for

this research. Since 2007, the most popular destinations are China (N=41), Japan (N=12)

and Italy (N=8). There are 87 manufacturing firms and 12 service companies.

The actual performance (N=99), which is the post-deal target operating revenue,

ranged from 10.9 thousand USD to 14,627.5546 million USD (M=429.8712,

SD=1,623.7084). The lowest actual revenue falls into the target country of Germany,

Japan and Italy, and the largest revenue outcome goes to cases take place in also Italy,

Japan (Tokyo region) and Germany.

Table 3: Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Post-deal target operating

revenue/turnover

(.mil USD)

99 0.0109 14,627.5546 429.8712 1,623.7084

Pre-deal target operating

revenue/turnover

(.mil USD) 99 0.0000014 7,105.7994 294.7609 884.6313

Access to infrastructure 96 18 263 105.5885 48.2289

Contract enforcement

quality 96 6.5 15 12.0031 2.6662

Valid N (listwise) 96

The sample of the expectations of the Joint venture performance (N=99) ranged

from 1.4 thousand USD to 7,105.7994 million USD (M=294.7609, SD=884.6313).

The lowest expected performance cases are in countries of Germany, Ukraine and

Italy, while the cases with highest expectations are in Italy, Japan (Tokyo region) and

Germany.

28

For two moderating variables, contract enforcement and access to electricity, 3

joint venture cases are missed because of no data is available for a specific country of

Kayman Islands. Therefore, total 96 cases are taken into the analysis in this research.

Access to electricity (N=96) ranged from 18 to 263 days among the 25 countries

and regions which have been selected (M=105.5885, SD=48.2889). The countries

with the least access to electricity are Ukraine (263), Russian Federation in general

(160.5) and Russian Federation-Moscow region (150). The countries with highest

access to electricity are Korea Republic (18), China Taiwan (22) and Austria (23).

Quality of contract enforcement (N=96) ranged from 6.5 to 15 (M=12.0031,

SD=2.6662). The countries with the lowest quality of jurisdiction system are Thailand

(6.5), Philippines (7.5) and India (7.5). The countries with the highest efficiency of

enforcing contracts are United Kingdom (15), China-Shanghai region (14.5) and

China in general (14.1).

These values and variations could also reflect the outcomes of this research. In order

to look into that deeper, the following sections cover the correlation analysis.

Correlations

The relationships between the variables were investigated using the Pearson

correlation coefficient. Table 4 shows the main correlations. The significant

correlations are marked with two (P< 0.01) asterisks. Relevant with H0, there is a

significant correlation (r=0.963, P<0.05) between actual international Joint venture

performance and the expectation performance. There are no significant correlations

between the product terms of expectation performance and actual IJV performance

with contract enforcement (r=.161, P< 0.05) and with access to infrastructure (r=.194,

P<0.05). This indicates that the moderating effect of the two formal institutional

factors as hypothesized in H1 and H2 may not be supported in the subsequential

analyses.

29

Multicollinearity

None of the Pearson’s correlation coefficients of predictors in Table 4 are 0.8 or

higher. This result gives strong indication that there is little multicollinearity. In order to

control for multicollinearity, a VIF test is also conducted.

Variance inflation factors (VIF) were controlled for. VIF scores above 5 (Rogerson,

2001) is strong evidence of multicollinearity. In order to eliminate issue of

multicollinearity, centered variable are used. As shown in Table 5, no VIF are higher than

5 thus multicollinearity is no longer an issue for this research after using the centered

variables.

Table 5: Test for Multicollinearity

Variable VIF 1/VIF

Expectations IJV performance 1.024 0.98

Contract Enforcement (CE) 1.160 0.86

Access to Infrastructure (AI) 1.172 0.85

Expectations * CE_centered 1.329 0.75

Expectations * AI_centered 1.340 0.75

Mean VIF 1.205

Table 4: Correlations

1 2 3 4 5 6

1. Actual IJV performance 1

2. Expectation of IJV performance .963**

1

3. Contract enforcement .013 .005 1

4. Access to Infrastructure -.006 -.034 .363**

1

5. Expectation* Contract Enforcement-

Centered .161 .048 -.118 -.024 1

6. Expectation *Access to Infrastructure-

Centered .194 .147 .026 -.063 .483

** 1

**. Correlation is significant at the 0.01 level (2-tailed).

30

Inferential Analysis

The null was tested by means of a T-test. To test Hypotheses 1, 2, a multiple

regression was used. In this regression, model 1 to 4 tested the direct relationships, whilst

model 5, 6 and 7 tested the moderation effects.

Table 6: Setup of multiple regression

Variables/Model 1 2 3 4 5 6 7

Expected IJV performance x

x x x x

Contract enforcement

x

x x

x

Access to Infrastructure

x x

x x

Expectations * Contract Enforcement

x

x

Expectations * Access to Infrastructure x x

T-test

To test the null hypothesis, the mean for actual IJV performance was compared to the

expected IJV performance through a one-sample T-test. The results of this T-test are

shown in Tables 7 and 8. As shown in Table 6, the actual IJV performance measured in

post-deal target revenue (M= 429.87, SD= 1623.71, mil USD) is higher than what was

expected (M= 294.76, SD= 884.63, mil USD). By comparing the mean of actual IJV

performance to the expectation, the difference was not significant t(98)= 0.828, p>0.05;

which also shows from the low effect size of r= .052. This means the actual performance

of IJV is not significantly different from what it was expected to work out.

Table 7: One Sample Statistics; Expected Vs Actual IJV performance

N Mean Std. Deviation

Expected IJV performance 99 294.76 884.63

Actual IJV performance 99 429.87 1623.71

Table 8: One-sample T-test: Expected Vs Actual IJV performance

T-test for Equality of Means

t df sig.(2-tailed)

Mean

Difference

95% confidence Interval of the

Difference

Lower Upper

Actual IJV

performance .828 98 .41 135.1103 -188.7327 458.9532

N=99; Independent variable is Expected IJV performance, M= 294.7609

31

Regression

Table 8 below provides a summary of the OLS multiple regression results. The

first model excludes other variables, while only testing the effect on the independent

variable- expected IJV performance. The overall model is significant as indicated by

the significant F-value. The model has a rather large R2

with .928.

The model 2 and model 3 test the direct effects that moderating variables might

have on the dependent variable. In model 3, it has been observed access to

infrastructure has significant Beta-coefficient on the dependent variable. However, the

insignificant F-values and very small R2 in both models suggest that the moderating

variables, namely contract enforcement and access to infrastructure, have no

significant direct influences on the actual performance of international joint ventures.

The 2 moderating variables are tested alongside the predictor variable in Model 4,

without taking the interaction effects into account. However, the Beta-coefficients for

the two moderators were not significant even though the F-value for the model is

significant and the R2

gives a high explanatory power.

The Hypothesis 1 and 2 predicted positive effects on the actual IJV performance

deviated from what is expected. The effects are tested in Model 5 to 7. Firstly, each

moderator is involved individually (Contract enforcement in Model 5, Access to

infrastructure in Model 6). The interactions for both moderators in Model 5 and 6 are

significant. However, the Beta-coefficients are insignificant with significant F-values

and high adjusted R2. It cannot conclude that contract enforcement has significant

influence on the relationship between the expected and actual IJV performance in

model 5 and neither can access to infrastructure in model 6.

All 2 moderating variables are involved in the Model 7 with their interacting

effects are also taken into consideration. The F-value is significant and adjusted R2

shows that 93.8% of the effects can be explained. However, the coefficients for

contract enforcement and access to infrastructure are not statistically significant.

Therefore, Hypothesis 1 and 2 are not supported.

32

Table 8: Regression Results

Standardized coefficients

Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7

1.Expected IJV performance 1.768***

1.770***

1.757***

1.755***

1.759***

(.050)

(.051) (.046) (.051) (.047)

2.Contract enforcement

8.014

-1.238 13.422

7.954

(63.763)

(18.527) (15.740)

(17.031)

3.Access to Infrastructure

-.207* -.928

1.013 .832

(3.525) (1.025)

(.936) (.937)

4.Expectations * Contract Enforcement

.110***

.110***

(.024)

(.027)

5.Expectations * Access to Infrastructure

.003**

-8.779E-5

(.002) (.002)

Constant -91.202* 435.786** 435.786** -91.670* -89.368** -82.724

* -90.092**

(46.541) (169.117) (169.128) (48.272) (43.703) (47.451) (44.223)

N (observed number) 96 96 96 96 96 96 96

F-value 1242.984***

.016 .003 396.869***

490.912***

415.673***

290.875***

R2 .928 .000168 .000037 .928 .941 .931 .942

Adj. R2 .927 -.010 -.011 .926 .939 .929 .938

R2 change .928 .000168 .000037 .928 .941 .931 .942

*P<.1; **P< .05; ***P<.01

33

CONCLUSIONS

Findings

Through testing a sample of 96 IJV cases (99 collected) in the manufacturing and

service sectors, this research created a linkage between formal institutional factors and

the implementation of international joint ventures. The effects of formal institutional

factors on the actual performance which might differ from the expectations were

tested based on the transaction costs view. Two specific formal institutional factors

were selected: contract enforcement and infrastructure accessibility.

To test if formal institutional variables have impacts on the implementations, IJVs

with both pre-deal revenue and post-deal revenue available were taken. Analyzing the

relationships, proxies for the two regulatory institutional factors were selected from

the Doing Business Project by World Bank. Hypotheses were made of which one was

aimed at comparing the expectation performance and actual performance, one

predicted the positive impact of contract enforcement on the actual performance, and

another one was to test the possible positive influence of a high access to

infrastructure.

The null hypothesis (H0) assumed the actual after-implantation performance of

IJVs to be exactly the same as the expected value prior to the joint venture. The T-test

showed a non-significant result so cannot reject the null hypothesis. Although it was

found that the expected performance has a strong relationship with the actual

performance. The result in fact means the actual IJV performance is not significantly

different from their expectation values for the sample cases selected.

Theories suggested the instability of joint venture performance is due to the

uncertainty raised by the unmanageable factors (Child, 2002). These uncertainties and

consequential opportunism behavior and high transaction costs occur in the context

would influence the performance of economic practice which is embedded in the

34

environment (Granovetter, 1985; Williamson, 2000; Yiu & Makino, 2002). One

possible reason of which the null hypothesis cannot be rejected in this research might

be related to a more extended view on the MNEs’ choice on governance mode.

Contract is the default choice for MNEs with little control and low level of transaction

costs (Chen & Chen, 2003). While MNEs are trying to enter a foreign country, they

need to face uncertainties stem from lack of the local knowledge. Thus businesses

often choose market mechanisms to enter the new market at the beginning with low

risk of failure and exit costs. After getting familiar with the local market, they might

increase the control and equity investment into the cooperation and choose a

governance mode like joint ventures with more commitment. However, once the

partner thinks the cooperation is facing too much uncertainties and risks, the

cooperation would be terminated without being actually implemented. This can be an

explanation for the fact observed by other researches the termination rate of joint

ventures are so high (Beamish, 1993; Pearce, 1997). The other joint ventures which

are actually implemented have considered most of the factors that could create the

uncertainties and risks. If they can be implemented, the results would to the most

extent match the expectations.

The Hypothesis 1 and 2 predicted positive influences of contract enforcement

and access to infrastructure on the actual performance of international joint ventures.

The multiple-regression test results cannot support the hypotheses. The insignificant

findings mean the quality of contract enforcement and the level of infrastructure

accessing do not significantly influence the implementation of joint ventures differing

form the expected values.

In the test for contract enforcement (H1), the coefficient showed that the

relationship is positive, meaning higher contract enforcing quality tend to have a

positive influence on joint venture performance. Although this is in line with the

findings of Gong et al (2007), the result was not significant and therefore cannot be

proven statistically. The first explanation for the insignificant result might because an

35

assumption the hypothesis was built on that there are always violations of the

contracts and IJV contracts are necessarily incomplete (Antia & Frazier, 2001; Henisz,

2000). While contract disputes not happen frequently in the cases chosen for this

research, the effects of the quality of contract enforcement might be not significant to

be observed. Secondly, among the 99 cases which were selected for this research,

most cases were from China (41) and Japan (12). It was suggested by theories that

trust can also play an important role in alliances besides contract enforcement (Child

& Yan, 2001). To be more specific, Japanese firms rely on trust than contracts to

manage cooperation (Child & Yan, 2001). Therefore, another explanation for the

finding might be that partners in international joint ventures might rely more on

informal dispute settle mechanism than the formal ones, for example contracts

enforcement, to ensure the success of the cooperation. Thirdly, since the actual and

expected performance were not significantly different, it is possible that the impacts

of the quality of contract enforcement in the local market had been taken into

estimation of the cooperation sufficiently before the implementations.

In the test for infrastructure accessibility (H2), the coefficients suggested a

positive correlation that higher level of access to the electricity tends to have higher

actual IJV performance. However, the effect was not statistically significant.

Therefore, it cannot be concluded that the level of access to infrastructure can

significantly differs the actual performance from the expectations. The non-significant

effect can be explained by that the research was built on the assumption that the

access to electricity is steady in the host country after the implementation of the joint

venture. In another word, some unexpected changes happen to the infrastructure

accessibility in the host country might still be influential to the actual outcome of the

joint ventures which are under implementations. Secondly, another explanation could

because of the typology of infrastructure. The expectation of joint venture

performance might be significantly determined by the level of physical infrastructure.

Thus if the cooperation can easily get electricity had been considered sufficiently as

36

one of the priority infrastructure conditions in the host country before a joint venture

being implemented. In fact, theories categorized local knowledge and market

intelligence as non-physical infrastructures (Inkpen & Beamish, 1997). The

non-physical infrastructures might also matter and should be more involved in the

estimation of joint venture performance.

To summarize the findings by the empirical tests, by testing the 96 IJV cases

since 2007 in the manufacturing and service sectors, it was found the actual

performance is not significantly different from the expected values before

implementations. Besides, the regulatory (formal) institutional factors that were

selected in this research cannot find statically significant proofs to support their

effects on the actual IJV performance. This result gave a possible explanation that that

other formal variables might matter more than contract enforcement and electricity

accessibility. It could also because that the selected two factors had been sufficiently

involved in the considerations of the estimations of IJV performance.

Managerial Implications

This research has few implications for managers even though the actual

performance is proved to be not significant different from the expected value. Since

there is a high correlation between the expected value and the actual performance, it

suggests that managers need to be careful when making the plan before the

implementations of international joint ventures. They should include as many factors

into considerations as they would be influential to the actual performance of the

cooperation. By doing so, an accurate estimation can maximize the chance of reaching

a successful outcome with an efficient implementation.

Once the implementation was launched, managers can worry less for the contract

enforcement and electricity accessibility in the host country, if the institutional

conditions remain steady. However, this should be built on a premise that these two

factors had been sufficiently included in the planning before the real operations.

Moreover, managers can also build more mutual trust between partners to settle

37

disputes, instead of always using formal mechanisms like contract enforcement.

However, the extent to which rely on trust rather than contracts should also depend on

the national culture in the host country. Therefore, while looking into formal

institutions, the effects of informal (normative, cognitive) institutions also need to be

enough considered by MNEs.

Since the institutional factors are the “unmanageable” factors for MNEs to

operate in an unfamiliar context, it might overdraw attention in the operations while

ignoring the “manageable” ones. Therefore, MNEs cannot ignore the

control-performance relationship in the implementation of the alliance. To be more

specific, managers need to maintain a reliable level in terms of capital and non-capital

investment to create a strong connection with the partners in the alliance so to keep

the stability of the joint venture. Moreover, a strong bargaining power is also needed

for MNEs to keep in order maintaining the control over the alliance.

Limitations and future research

This research has limitations and leaves areas for the future researches to explore.

They will be specified in the following section.

Firstly, the field of measuring international joint venture performance is so large

that various studies and scholars have found proofs of the impacts of vast variables

based on different theories. It should be more ideal to include all of the variables, both

objective and subjective measurements (Beamish, 1993; Park & Ungson, 1997).

However, it was not feasible to include all the variables mentioned by the previous

studies. Future research could construct a more comprehensive approach by

integrating all these theories and variables.

Another limitation for this research is the data use. Since only secondary data

from existing databases were included in this research, the number of sample was

limited. Consequently, it was difficult to control other variables that could make the

research more specific. The relatively small sample size limited the chance to look

deeper into the impacts that regulatory institutional factors have on the joint venture

38

performance. Moreover the limitation on the sample size leaded to a flawed sample

structure. About half of the sample was from a similar cultural/regulatory region. That

might lead to a biased result of the research. The future research could try to gather

more primary data so to have a better structured sample set, therefore might have a

smaller variance.

The future research should also look deeper into the impacts of regulatory factors

in implementation of international joint ventures. It had been found in this research

the level of access to infrastructure might not be influential significantly after the

operation starts. However, as stated in the conclusions, an unexpected change in the

infrastructure access in the host country can be also included in the measurement of

this variable so to get a deeper view. Besides, other than physical infrastructures,

non-physical infrastructures such as access to local insights could be considered

having impacts.

Future research can look into the impact of trust between joint venture partners,

rather than only considering formal dispute settle mechanism of contract enforcement.

Thus, the future research can include both informal institutions such as national

culture differences with the consideration of the regulatory factors to gain a more

comprehensive view on the effects that institutional factors have on actual

international joint venture performances.

39

REFERENCE

Aidis, R., Estrin, S., & Mickiewicz, T. 2008. Institutions and entrepreneurship

development in russia: A comparative perspective. Journal of Business Venturing,

23(6): 656-672.

Antia, K. D., & Frazier, G. L. 2001. The severity of contract enforcement in interfirm

channel relationships. Journal of Marketing, 65(4): 67-81.

Bae, J., & Salomon, R. M. 2010. Institutional distance in international business

research. Advances in international management: The past, present and future of

international business and management, 23.

Beamish, P. W. 1993. The characteristics of joint ventures in the people's republic of

china. Journal of International Marketing, 1(2): 29-48.