form 941 and form w2 combined annual wage reporting · combined annual wage reporting ... •...

TRANSCRIPT

8/5/2015

1

Form 941 and Form W‐2Combined Annual Wage Reporting

Kristy Maitre – Tax SpecialistCenter for Agricultural Law and TaxationAugust 7, 2015

When Would Your Client Receive a CAWR Notice?

• If your inaccurately compute payroll tax calculations and withholding, a Combined Annual Wage Report (CAWR) Notice will be issued

The Purpose of the CAWR Program and a bit of History

• To verify that employers paid and reported the correct amount of tax: – Federal Income Tax Withholding (W/H)– Filed all necessary Forms W‐2 with the SSA

• In 1976, a law was passed to simplify employer reporting of wages– The Form W‐2, Wage and Tax Statement, was redesigned to include Social

Security information, and Form W‐3, Transmittal of Income and Tax Statements, was amended to include cumulative totals of each Money Field appearing on the associated Forms W‐2

• This resulted in the creation of the Combined Annual Wage Reporting System (CAWR)– The CAWR Program is worked two years behind the current year to allow

employers time to file Forms W‐2 and/or Forms W‐2c with the Social Security Administration (SSA) and Employment Tax Returns with the IRS

8/5/2015

2

Possible IRS Notices

• Notice CP253 or Letter 99C regarding missing Form(s) W‐2 relate to Missing Form W‐2

• Notice CP251 or Letter 99C relate to the underreporting employment taxes

What is the Internal Revenue Service/Social Security Administration (IRS/SSA) Reconciliation Process?

• The IRS/SSA Reconciliation Process compares the employer's earnings report data processed by SSA with the employer's tax report data processed by IRS

• Earnings report data and tax report data, are submitted to SSA and IRS by employers, their representatives, third parties, and agents

• If wage data processed by SSA is less than the amount reported to IRS, we assume that the processed earnings are incorrect

• SSA sends a notice and questionnaire, asking the employer to explain and resolve the differences

• If they do not receive a response after 45 days, they send the employer a second notice

• If the employer still does not respond, they refer the case to IRS for investigation

SSA Notices

• First Request– SSA‐L‐93‐SM (Notice) and SSA‐95‐SM (Employer Questionnaire ‐ SSA Has No Record of Employer Report)

– SSA‐L‐93‐SM (Notice) and SSA‐97‐SM (Employer Questionnaire ‐ Discrepancy Between IRS and SSA Records)

• Second Request– SSA‐L‐94‐SM (Notice) and SSA‐95‐SM (Employer Questionnaire ‐ SSA Has No Record of Employer Report)

– SSA‐L‐94‐SM (Notice) and SSA‐97‐SM (Employer Questionnaire ‐ Discrepancy Between IRS and SSA Records)

8/5/2015

3

Social Security AdministrationSSA Publication No. 16‐002

• One of two questionnaires is enclosed with this pamphlet: – A “missing report” questionnaire which is sent to employers for whom IRS has received a employment tax return but Social Security has no corresponding wage report; or

– A “discrepancy” questionnaire, which is sent to employers who reported a larger Social Security and/or Medicare wage amount to IRS than they reported to Social Security

First Notice

SSA‐95‐SM

8/5/2015

4

SSA‐95‐SM

SSA‐95‐SM

SSA‐95‐SM

8/5/2015

5

SSA‐95‐SM

Second Notice

SSA‐L‐93‐SM

8/5/2015

6

SSA‐L‐93‐SM

SSA‐L‐93‐SM

SSA‐L‐93‐SM

8/5/2015

7

SSA‐L‐93‐SM

SSA‐L‐93‐SM

Combined Annual Wage Reporting Missing Form W‐2 Inquiries

• The Social Security Administration (SSA) and Internal Revenue Service (IRS) have an agreement to exchange employment tax data

• SSA shares Form W‐2 data with the IRS and the IRS shares Form 941, 943, 944, 945 and Schedule H data with SSA

• The Combined Annual Wage Reporting (CAWR) is a document matching program that compares the Federal Income Tax (FIT) withheld, Medicare wages, Social Security wages, and Social Security Tips reported to the IRS on the Forms 94X and Schedule H against the amounts reported to SSA via Forms W‐3 and the processed totals of the Forms W‐2

8/5/2015

8

RM 01101.009 IRS/SSA CAWR Agreement

• A. Introduction

– Under the authority provided by Section 232 of the Act, IRS and SSA have entered into an interagency agreement that specifies how the Combined Annual Wage Reporting (CAWR) process will work.

• B. Operating Policy• The following are pertinent extracts from the IRS/SSA interagency agreement on

the CAWR system.– Reconciliation (Article IV): “SSA agrees to: ....Notify employers of missing or discrepant FICA

wage reports identified by SSA based upon comparisons of SSA and IRS records. The employer notices will be sent to employers...prior to any IRS reconciliation activity for the tax year.”

– Employer Education (Article IV): “Both IRS and SSA agree to...Promote better employer reporting practices by participating in joint educational workshops for business employers and magnetic media seminars.”

– Disclosure Safeguards (Article VI): “SSA will provide safeguards prescribed under 26 USC 6013 (p) (4) for all federal tax returns and return information received from taxpayers and IRS. SSA employees and contractors employed by SSA are subject to the provisions of 26 USC 7213 and 7431 regarding unauthorized disclosures.”

– Review Procedures: “Both IRS and SSA agree to: Designate representatives to meet no later than October 1 of each year to review the method and effectiveness of data exchange processes between the two agencies during the preceding 9‐month period and review this agreement for any changes that will improve the processing and/or reconciliation of employer reports.”

RM 01101.009 IRS/SSA CAWR Agreement

• Processing Responsibilities (Appendix, Subsection (a)):– The money fields on the Forms W‐2 that will be electronically and clerically balanced to Forms W‐3 totals by SSA are: Advanced Earned Income Credit (EIC) payments, FICA wages, FICA tips, FICA Tax Withheld, Federal Income Tax Withheld, Allocated Tips, and Wages, Tips, and Other Compensation

– SSA will validate all Forms W‐2 and W‐2P on SSN and name– Tolerances for FICA‐related reconciliation will be less than a quarter of coverage level for that tax year

– SSA will furnish to IRS the reported and processed totals of all Forms W‐2, W‐2P, and W‐3 money fields....

– No changes may be made in SSA's balancing tolerances without prior discussion and consultation with IRS

Several Record Systems are Utilized

• Treasury/IRS 22.061 Individual Return Master File (IRMF)

• Treasury/IRS 24.046 CADE Business Master File (BMF)

• Treasury/IRS 24.047 Audit Under‐reporter Case File

• Treasury/IRS 34.037 IRS Audit Trail and Security Records System

• Treasury/IRS 36.003 General Personnel and Payroll Records

8/5/2015

9

Combined Annual Wage Reporting Missing Form W‐2 Inquiries

• When the Social Security and/or Medicare Wages reported to SSA on Forms W‐2 are lower than the Social Security and/or Medicare Wages reported to IRS on Forms 94X/Schedule H, SSA contacts the employer, issuing Notice SSA‐L‐93‐SM, Employer Questionnaire Discrepancy Between IRS and SSA Records, requesting information to help resolve the discrepancy

• If the initial contact does not fully resolve the discrepancy, SSA follows up with Notice SSA‐L‐94‐SM, Second Request Questionnaire SSA Has No Record of Employer Record

• If, after two contacts, the imbalance is not completely resolved, SSA refers the case(s) to the IRS.

Combined Annual Wage Reporting Missing Form W‐2 Inquiries

• The inventory received from SSA into the CAWR program (known as SSA‐CAWR cases) is reviewed by tax examiners who attempt to reconcile the discrepancy without contact with the employer

• This includes additional research with SSA to determine if Forms W‐2 were filed/corrected in the interim

• The tax examiner review begins in April each year for the third preceding tax year (for example: during 2015 IRS is analyzing tax year 2012 SSA‐CAWR cases)

• If, after the initial case analysis, a discrepancy remains, the tax examiner issues Letter 98C Wage Discrepancy Per SSA: Information /Verification Requested

• The 98C Letter informs the taxpayer of a discrepancy between information reported on the employment tax returns (i.e.: the Forms 94X or Schedule H) and that reported on Forms W‐2

• The IRS must receive your response within 45 days of the date of the 98C Letter

• If a response is not received within this timeframe the case will be closed, and the employer will be subject to the penalties outlined in the notice

TimeLine

• Mail or furnish correct Forms W‐2 to each employee

• Mail or furnish correct Forms 1099 MISC to each vendor or payee

• File Form 941 for quarter ending 12/31/2013

• File Form 940, if required

• File Form 945, if required

• Don't forget SUTA tax

8/5/2015

10

TimeLine

• Mail Forms W‐2, Copy A, along with Form W‐3 to Social Security Administration

– Forms W‐2 & W‐3 through Social Security Administrations on‐line website

• Mail Forms 1099 MISC, Copy A, along with Form 1096 to Internal Revenue Service

– Forms 1099 & 1096 through IRS FIRE system

Due Dates

• Copy A of Form W‐2 with Form W‐3 by February 29, 2016

• However, if you e‐file , the due date is March 31, 2016

• You may owe a penalty for each Form W‐2 that you file late

Form W‐2

8/5/2015

11

Form W‐3 Transmittal

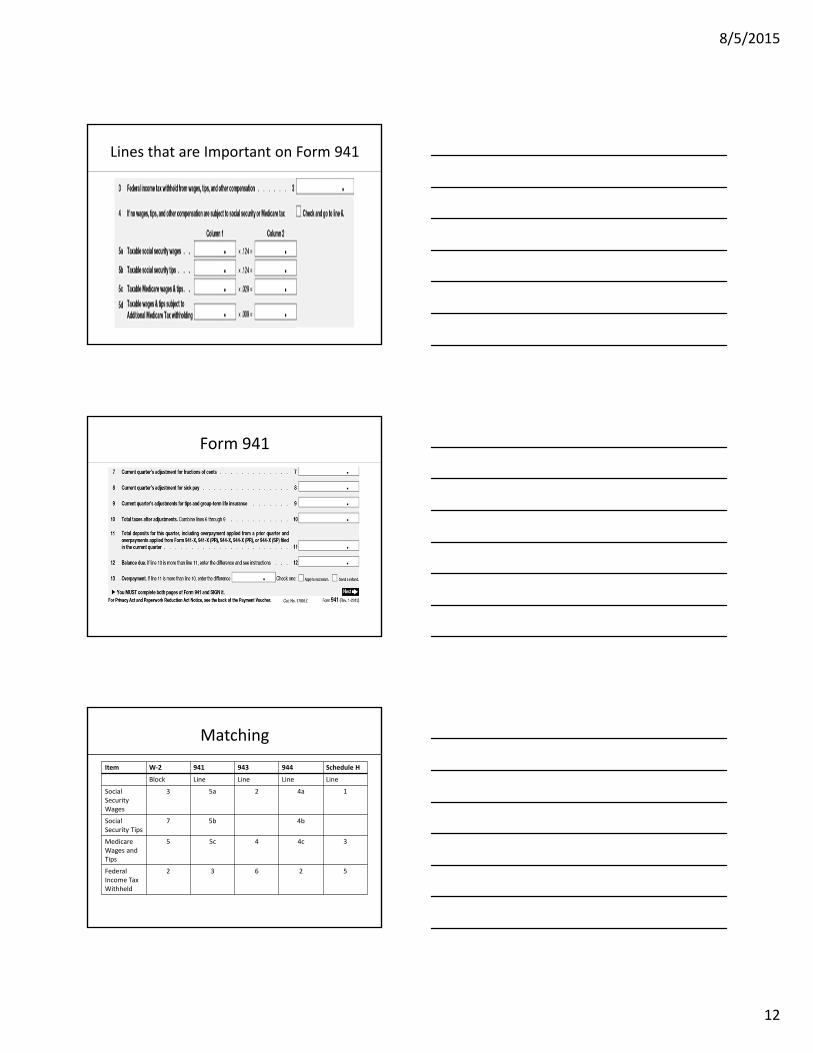

Boxes that are Important on Form W‐3

• Box 2 Federal Income Tax Withholding

• Box 3 Social Security Wages

• Box 7 Social Security Tips

• Box 5 Medicare Wages and Tips

Form 941

8/5/2015

12

Lines that are Important on Form 941

Form 941

Matching

Item W‐2 941 943 944 Schedule H

Block Line Line Line Line

Social Security Wages

3 5a 2 4a 1

Social Security Tips

7 5b 4b

Medicare Wages and Tips

5 5c 4 4c 3

Federal Income Tax Withheld

2 3 6 2 5

8/5/2015

13

How To Prepare Your Response

• If you use the services of an accountant or payroll service provider they will receive a copy from the IRS

• Review your employment tax information and compare it to the issues raised on the CAWR letter.

• If you did not file all the required Form(s) W‐2, submit them to the IRS, by attaching them behind the Letter 98C and response page

• Under IRC 6721(a), Failure to File Correct Information Returns, each original Form W‐2 received in response to CAWR inquiry is subject to a penalty of $50 for tax years 2009 and prior and $100 for tax years 2010 through 2015

• After December 31, 2015, new legislation increases those amounts to $250 per failure to file a return

How To Prepare Your Response

• If you disagree with the issues on the letter, provide your explanation in a signed statement

• If the Form(s) W‐2 were previously filed with SSA, please provide proof of timely submission

• If Forms W‐2c or 941‐X will resolve the discrepancy, include them in your reply

• Be sure that any adjustments made do not cause your account to be out of balance

• Mail or FAX your reply by the due date shown on the letter• Under IRC 6721(e), Failure to File Correct Information Returns with

Intentional Disregard, taxpayers that do not respond to CAWR inquiry timely are subject to a penalty based on 10% of the aggregate difference between the employment tax returns filed with the IRS and Forms W‐2 filed with SSA

August Webinars

• August 10 ‐ Fringe Benefits ‐ An overview of fringe benefits that employees enjoy and whether or not they are taxable income or exempt from tax will be discussed. Publication 5137 will be used for this class

8/5/2015

14

August Webinars

• Registration: To register: https://goo.gl/35tM78

• (registration ends at 10 AM CST on the day of the scheduled webinar)

• Cost: $35 per webinar

• Registration fee is non‐refundable

• If you are unable to attend a webinar, we can transfer you to another webinar we are offering

• Please contact us at 515‐294‐5217 for questions

Scoop Dates for Post Filing Season

• September 23, 2015

• October 21, 2015

• November 4, 2015

• November 18, 2015

• December 16, 2015

• December 30, 2015

2015 Farm Tax Schools

• November 9, 2015 to December 15, 2015 • 8 Locations in Iowa• Registration and the Fall Brochure will be out in August

• The program is intended for tax professionals and is designed to provide up‐to‐date training on current tax law and regulations.

• The program stresses practical information to facilitate the filing of individual and small business returns, in addition to farm returns.

8/5/2015

15

2015 Farm Tax Schools‐ Dates and Locations

• Waterloo: Nov 9‐10• Sheldon: Nov. 10‐11• Red Oak: Nov. 11‐12• Ottumwa: Nov. 12‐13• Mason City: Nov. 16‐17• Maquoketa: Nov. 23‐24• Denison: Dec. 7‐8• Ames: Dec. 14‐15 – live as well as attendance via webinar available

CALT Website

http://www.calt.iastate.edu/

Tour of the CALT Website

8/5/2015

16

CALT Staff

Roger A. McEowenCALT Director and is a Leonard Dolezal Professor in Agricultural LawEmail: [email protected]: (515) 294‐4076Fax: (515) 294‐0700

Kristine A. TidgrenStaff AttorneyE‐mail: [email protected]: (515) 294‐6365Fax: (515) 294‐0700

CALT Staff

Kristy S. MaitreTax SpecialistE‐mail: [email protected]: (515) 296‐3810Fax: (515) 294‐0700

Tiffany KayserProgram AdministratorEmail: [email protected]: (515) 294‐5217Fax: (515) 294‐0700