foreign investment, technology transfer and foreign capital impact function

TRANSCRIPT

This article was downloaded by: [Akdeniz Universitesi]On: 20 December 2014, At: 10:17Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

International Economic JournalPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/riej20

Foreign Investment, TechnologyTransfer and Foreign Capital ImpactFunctionPan Long Tsai aa National Tsing Hua UniversityPublished online: 28 Jul 2006.

To cite this article: Pan Long Tsai (1989) Foreign Investment, Technology Transfer andForeign Capital Impact Function, International Economic Journal, 3:2, 43-56

To link to this article: http://dx.doi.org/10.1080/10168738900000011

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information(the “Content”) contained in the publications on our platform. However, Taylor& Francis, our agents, and our licensors make no representations or warrantieswhatsoever as to the accuracy, completeness, or suitability for any purpose of theContent. Any opinions and views expressed in this publication are the opinions andviews of the authors, and are not the views of or endorsed by Taylor & Francis. Theaccuracy of the Content should not be relied upon and should be independentlyverified with primary sources of information. Taylor and Francis shall not be liablefor any losses, actions, claims, proceedings, demands, costs, expenses, damages,and other liabilities whatsoever or howsoever caused arising directly or indirectly inconnection with, in relation to or arising out of the use of the Content.

This article may be used for research, teaching, and private study purposes.Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expresslyforbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

INTERNATIONAL ECONOMIC JOURNAL Volume 3, Number 2, Summer 1989

FOREIGN INVESTMENT, TECHNOLOGY TRANSFER AND FOREIGN CAPITAL IMPACT FUNCTION

PAN LONG TSAI*

National Tsing Hua University

This paper analyzes the optimal capital accumulation of a small open economy by incorporating the impact of technology transfer that accompanies foriegn ivestment. Assuming that technology transfer depends on the extent of foreign ownership, it is shown that, whenever there is technology transfer through foreign participation, the optimal rule suggests that a host country maintain some foreign capital in the steady state. The concept of the foreign capital impact function is introduced to capture possible negative effects in addition to the positive effects of foreign investment. The impact of foreign investment is shown to involve an externality, calling for govern- ment intervention for a social optimum. [110]

1. INTRODUCTION

The rapid growth of international capital movement, the desire of developing countries for modernization through foreign participation, as well as the increased activity of multinational enterprises since World War I1 have attracted the atten- tion of scholars, policy-makers, and officials of international agencies all over the world. The concern over the potential economic, political and social consequences of the presence of fo;eign capital has also inspired a spate of studies among economists. One line of investigation, which originates in Mundell (1957) and MacDougall (1960), focuses on the welfare impact of foreign investment on the host country. Related to the concept of immiserizing growth, this subject has been further studied by Minabe (1974), Brecher and Diaz Alejandro (1977), Bhagwati (1979), Brecher and Findlay (1983), Srinivasan (1983), Dei (1985) and Buffie (1985). There are, however, at least two shortcomings in these sutides. First, they slur over the dynamic nature of investment and use static models to draw comparative static implications. Second, most studies neglect the fact that many developing countries regard foreign investment as a vehicle for technology

* This is a revised version of Chapter IV of my Ph. D. dissertation at The Ohio State Universi- ' ty. I deeply appreciate the encouragement of the committee members, Drs. Tetsunori Koizumi,

Robert Driskill, and Marie Thursby. I am also indebted to an anonymous referee for helpful comments. Any remaining errors are my own responsibility.

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

44 PAN LONG TSAI

transfer rather than as a source of capital. While some static works [see Minabe (1974), for example] discuss the problem

of technology transfer, others still get around this crucial dimension of foreign investment activity. Some efforts to incorporate the dynamics of foreign invest- ment have been made in the past two decades. The key contributions include Negishi (1965), Hamada (1966, 1969), Bardhan (1967), Pitchford (1970), Koizumi and Kopecky (1977), Findlay (1978), Ruffin (1979), and Gehrels (1983). Howev- er, only the studies by Koizumi and Kopecky, Findlay, and Gehrels incorporate the phenomenon of technology transfer, though the first two do not study the problem in the context of optimal growth. Gehrels' discussion of optimal policies toward foreign investment and technology transfer, although interesting, fails to examine the process of dynamic evolution of the economy.

In this paper, I attempt to take these two missed features of foreign investment into account. In particular, I investigate the optimal capital accumulation of a small open economy by incorporating technology transfer. Assuming that techno- logy transfer depends on the extent of foreign ownership, it is shown that, whenever there is technology transfer through foreign participation, a host coun- try trying to maximize its social welfare over time should in most cases maintain some foreign capital in the long run. Further, to capture the negative effects of foreign investment emphasized by dependency theorists, the concept of the fore- ign capital impact function is introduced. It is shown that the impact of foreign investment can be treated as a kind of externality, calling for government in- tervention for a social optimum.

2. THE MODEL

The problem of optimum capital accumulation and foreign investment is stu- died in the context of a small open economy. The only commodity used for both consumption and accumulation is produced by capital and labor. Foreign capital is paid for by exporting the commodity. The model departs from the standard one by explicitly introducing a neutral technology transfer function to capture one of the most salient features of direct foreign investment.

Let the growth rate of the labor force be ,I. Then, at any moment in time the economy's labor force equals L = LoeAt, where I-,-, is the labor force at the initial point. If lower case letters are used to indicate per capita quantities, then accord- ing to Koizumi and Kopecky (1977), the aggregate production function is

where x is per capita output and k = k, + k f is per capita capital stock used by

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

FOREIGN CAPITAL IMPACT FUNCTION 45

the host country'. The factor kd is the part domestically owned and kf, which belongs to foreigners, is assumed to be non-negative, since the main concern here is the impact of foreign investment on the host country. The sub-production function f(k) is a standard neoclassical production function satisfying the Inada conditions; that is, f'(k) > 0, f ( k ) < 0 for k > 0, and f(0) = f'(m) = 0 and f (w) = f'(0) = m.

The specifications about kf and the technology transfer function need explana- tion. In a physical sense, foreign capital and domestic capital are homogeneous so that they can be added. Nevertheless, foreign investment also brings with it new technical know-how, entrepreneurship, and management skills. Through the "contagion effect" such as discussion and training, these new and presumably superior ideas then permeate throughout the economy, and thus contribute to the improvement of domestic productivity. This process is reflected in the technology transfer function, 4 , which is neutral with respect to the two factors of produc- tion. The host country is assumed always experiencing technology improvement from its contact with foreigners so that +(kf) exceeds unity for any positive kf. Despite this positive effect, however, it is assumed that sufficiently strong dimi- nishing returns apply to such investment. In notations, we have q(0) = 1, 0 < 4 '(kf) < m, + "(kf) < 0 and a 'XI a kZf = 4 "(kf)f(k) + 2 4 ' (kf)f'(k) + +(kf)f"(k) < 0 for kf > 0.

Let us turn to the supply side of foreign capital. Most of the developing countries are relatively small in the international capital market. It is therefore quite reasonable to treat a single developing country as a small country. Howev- er, as pointed out by Hanson (1974) and Eaton and Gersovitz (1981), internation- al investors cannot ignore the risks of national default and expropriation. These risks may be much more serious in the developing countries. The vulnerable economic capacity, the xenophobia inherited from colonial eras, and the highly uneasy political climate in the Third World all contribute to the potential risks of international investment. Thus, with more and more capital at stake, the investors will naturally ask higher and higher rewards to compensate for the risks they assume, which can be captured by an upward sloping supply curve of foreign ~ a ~ t i a l . ~ Symbolically, the supply function of foreign capital, S(kf), is character- ized by S(kf), S'(kf) > 0, S"(kf) > 0 and S'(kf) -. a. The constant kf denotes the maximum amount of per capita foreign capital the host country can obtain.

' All the variables are in real terms and have time subscripts, which are omitted to simplify the notations.

'This kind of supply curve was used by Hamada (1969), Bardhan (1967), and Pitchford (1970). A vital difference between this model and theirs is that the positive slope of the supply curve here is due to risks, not monopoly power.

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

PAN LONG TSAI

Per capita national income, y, can be expressed as y = x - k,S(kf). Using national income identity and ignoring capital depreciation, we obtain the fun- damental differential equation for this model:

where c is per capita consumption. The objective for the host country is to maximize the discounted sum of the

future utilities. So it can be formulated as an optimal control problem:

Max W = Lrn U ( c ) e " 'dt ic. ktl (3)

subject to (2) and kdo = lido and kf - > 0, where P > 0 is the social rate of discount and lido is the initial value of kd. U(c) is the community utility function, which is also assumed to satisfy the Inada conditions.

3. THE METHOD AND THE RESULTS

Define q as the costate variable associated with domestic capital accumulation. Then the curent value Hamiltonian is

H(c, kf; kd, q) = U(c) + q[$(kf)f(kd + kt) - c - k$(kf) - r\ kd] (4)

By the Pontryagin maximum principle, the conditions for optimization are:

according as kf >, 0

kd = $ (kf)f(k) - c - kfS(kf) - A kd

a H q = p q ---- a kd = - q[Il(kf)f'(k) - ( A + P I ] . (8)

Given these necessary conditions and the fact that the Hamiltonian, H(c, kf; kd, q), is concave in (c, kf, kd),3 the transversality condition sufficient for optimal- ity is

lim e c P t q 2 0, lim eCP'qkd = 0. I-- I--

(9)

Similar to Bardhan (1967), the implications of these equations will be discussed

'The concavity of the Hamiltonian in (k,, k,, c) requires that +(+"ff" - 2fS' - kff'5',) - (+'f')* > 0.

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

FOREIGN CAPITAL IMPACT FUNCTION 47

for three possible types of initial conditions: (1) A + P > S(0); (2) A + p =

S(0); (3) A + P < S(0).

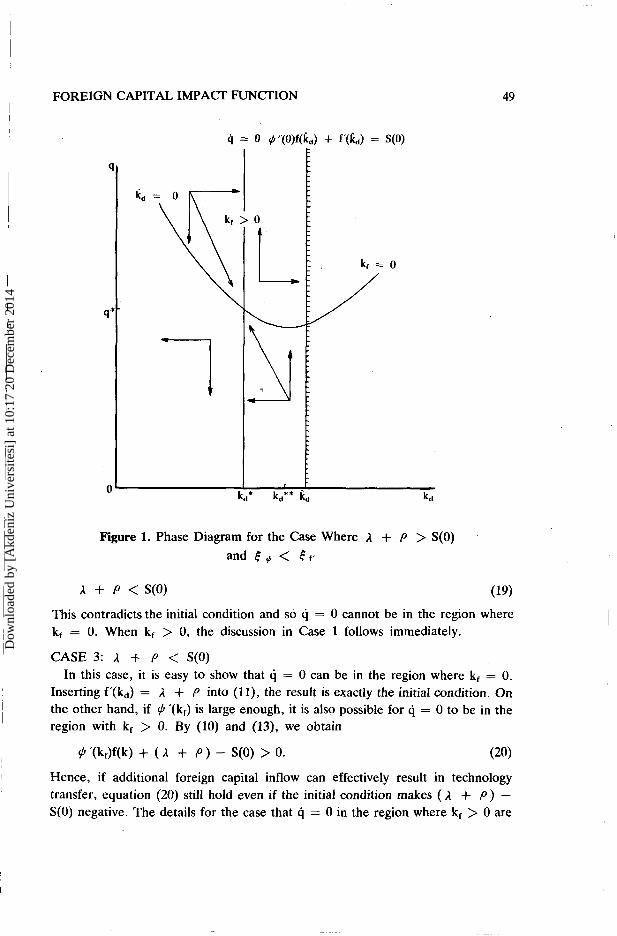

CASE 1: A + P > S(0)

In order to investigate the steady state properties of the solution, it is necessary to characterize the lid = 0 and q = 0 curves. Setting q = 0 in (8) gives us

since q = U'(c) > 0. Under the assumption that g > 1, equation (10) implies that, with technology transfer, the capital intensity in the steady state is higher than that corresponding to the usual golden rule.

If kf = 0, then, from (6), it must be the case that

f'(kd) - S(0) < - '(O)f(kd) < 0. (11)

But, from (10) and the initial condition, it follows that (when kf = 0)

Since (11) and (12) cannot hold at the same time the curve q = 0 cannot be in the region where kf = 0.

If kf > 0, then (6) implies that

which means that the marginal social benefit and marginal social cost of foreign capital should be equalized for optimality. Moreover, equation (13) can be rewrit- ten as

Comparing (13) and (14), we find that private profits will be negative at social optimum. This implies that foreign investment will fall short of optimal quantity if all the foreign investment activities are left to private decisions.

From equations ( 9 , (6) and (7) it can be shown that, when kf > 0, the slope of the k, = 0 curve is

dq - . = - a I;,/ a k,

dk, I k.=O = U"(C)( 4 (kf)f'(k) - A ).

a$ , laq

The sign of dq/dRd I kd=, depends on the relative magnitude of +(kf)f'(k) and A. However, from (8), we know that +'(kf)f(k) = A + P when cj = 0. So (15) is negative at the intersection of the kd = 0 and q = 0 curves, where we have the stationary solution q = q* and k, = k,*. For kd < kz, +(kf)f'(k) - A > P ,

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

48 PAN LONG TSAI

hence dq/dkd I I;,=" < 0. For kd > kd* there exists a kd** such that dq/dkd I = 0 at kd = kd** and dq/dkd 1 kdZo > 0 when kd > kd** Linearizing equations (7) and (8) around the steady state solution (kd*, q*), the characteristic roots can be solved as

, ak, J a k , a k d a q

% + ( = 1 2 + 4 - - hl, h2 = a q akd

where all the partial derivatives are evaluated at (kd*, q*). Since ( a kd/ a q)( aq 1 a k,) > 0, the characteristic roots are both real and opposite in their signs.4 The steady state solution is, therefore, a saddle point.

It can be concluded that on the optimum growth path domestically owned capital, kd, will increase (decrease) steadily if kdo < dd*(kdo > kd*). The solu- tions for the control variables, (c*, kf*), can be obtained by (5) and (13). Howev- er, unless further assumptions concerning the technology transfer function are made, it is not clear whether kf will increase or decrease during its convergence to the steady state solution, kf*. From (13), we get

The sign of (17) depends on the elasticity of the technology transfer function and that of the marginal productivity curve of capital for the sub-production function, I.e.,

More precisely, there are two opposite forces generated by the inward investment on the aggregate production function. One is the improvement of technology, and the other is the decrease in the marginal productivity of capital. Their relative strength determine whether the host country should encourage more foreign in- vestment in its path towards the steady state. Figure 1 and Figure 2 are phase diagrams for c p < E r - and E + > f-, respectively.The arrows show the possible stable branches.

CASE 2: ,I + P = S(0) When k, = 0, q = 0 implies f'(kd) = ,I + P , which, combined with (11),

gives us

Evaluating at (k*,, q*), we have 3 kdl a q = -1N"(c* ) > 0 and 3cjl.3 k, = -q* *(k*,)f"(k*) > 0.

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

1 FOREIGN CAPITAL IMPACT FUNCTION

I

I

I il = 0 !h3(0)f($) + f'(b) = S(0)

Figure 1. Phase Diagram for the Case Where A + P > S(0) and -$+, < Ct-

A + P < S(0) (19)

This contradicts the initial condition and so q = 0 cannot be in the region where k, = 0. When k, > 0, the discussion in Case 1 follows immediately.

CASE 3: A + P < S(0) In this case, it is easy to show that q = 0 can be in the region where kf = 0.

Inserting f'(kd) = 1 + P into ( l l ) , the result is exactly the initial condition. On the other hand, if + '(kf) is large enough, it is also possible for q = 0 to be in the region with kf > 0. By (10) and (13), we obtain

Hence, if additional foreign capital inflow can effectively result in technology transfer, equation (20) still hold even if the initial condition makes ( A + P ) - S(0) negative. The details for the case that q = 0 in the region where kf > 0 are

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

PAN LONG TSAI

Figure 2. Phase Diagram for the Case Where ,I + P > S(0) and € + > € f -

the same as those in Case 1. Let us trun to the case with q = 0 in the region where kf = 0.

Under this situation (7) and (8) reduce to (21) and (22)

kd = f(kd) - C - A kd Q1)

q = -q[f'(kd) - ( A + P ) ] . (22)

The slope of the curve kd = 0 is

dq dk, 1 &=" = U"(o)(f'(k,) - A ).

As kd increases, dq/dkd I starts with a negative value, becomes zero at a point kd**, and then turns positive as kd exceeds kd**. but its value will be negative at q = 0. This is depicted in Figure 3. By a linearizing process similar to that shown in Case 1, it is also true that the steady state solution is a saddle

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

FOREIGN CAPITAL IMPACT FUNCTION

Figure 3. Phase Diagram for the Case Where A + P < S(0) and kf* = 0

point.

4. FOREIGN CAPITAL IMPACT FUNCTION

Up to this point, we have concentrated on the merits of foreign investment. Specifically, we have interpreted the function +(kf) as a technology transfer function, with the properties + (kf) 2 1 and +'(kf) > 0. However, one should not overlook all the criticisms surrounding the activities of foreign investment. We will therefore reexamine the model developed in Sections 2 and 3 to see how the conclusions change when undesirable impacts of foreign investment are taken into account. For that purpose, the function + (kf) is renamed as the foreign capital impact function, with the properties: 11, (0) = 1, + (k,) > 0, + "(k,) < 0 and

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

PAN LONG TSAI

a2x/a k2f < 0 for kf > 0.' Thus, one major difference between the technology transfer function and the

foreign capital impact function is that the value of the latter is not necessarily greater than one because of possible immiserizing impacts such as inappropriate technology, psychological strain and cultural distortion^.^ The other difference is that the function + does not always have a positive slope as before, which means that additional foreign capital inflow may have either a positive or negative con- tribution to the host country. The positive effect may come from foreign inves- tors' becoming more familiar with and therefore more capable of adapting to local situations, or from the people in the host country, with more contact with foreign cultures, adjusting themselves better to the new international environ- ment. On the other hand, it is quite possible that the presence of more and more foreign capital becomes damaging to the host country. Forexample, foreign enter- prises may just displace the indigenous production, inhibit the formation of the local entrepreneurial class, and thus spoil the host country's effort at industrializa- tion.

It is now clear that the model subsumes some of the recent literature in the dynamic models of foreign investment. For instance, Hamada (1969) and Pitch- ford (1970) can be considered as special cases of our model with + = 1. Koizumi and Kopecky (1977) focus on the positive aspect of the foreign capital impact function, namely, + > 1 and +' > 0, As will be discussed below, Bardhan (1967) can be interpreted as a special case of ours, i.e., $b < 1 and +' < 0. This last result is particularly interesting. As indicated in note 6, it is better to disting- uish between the detrimental effects of foregin investment from different sources, and treat them separately. The similarity between Bardhan's results and ours implies that this model is general enough to give us all the fundamental results regardless of the sources of the impacts.

By similar procedures as in Section 3, we can obtain the results presented in Table 1. It is clear that the key factor determining whether a country should maintain foreign capital in the steady state is the marginal contribution of foreign

' The most devastating consequence of the new assumptions is that they may invalidate the concavity property of the Hamiltomian. It is clear from note 3 that the condition may fail when + is close to zero. While this is mathematically possible, it is not economically meaningful since +(k,)f(k) is also close to zefo in that case. Thus, we assume that the concavity property of H holds in the following discussion.

This is a highly simplified assumption. Ideally, it would be better to separate the detrimental effects of foreign investment in the production aspect from those in the political, social and psychological aspects. Our specification captures well the production aspect of foreign invest- ment. However, the other aspects may be more naturally captured by a community utility function in the form of the disutility of foreign investment, as was done in Bardhan (1967).

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

FOREIGN CAPITAL IMPACT FUNCTION

Table 1. Steady State Properties of the Host Economy in the Presence of Foreign Capital Impact Function

Cl:k,* > 0 a : k f * > 0

> 0 C3:kfa > 0 PP < 0 swab ? (Koizumi and Kopecky)

C1:kr* > 0 C2:kf* > 0 C3:kf* - > 0 PP? akdak,, ?

C1:kf* > 0 C1:kf* > 0 C1:kf* > 0 a : ? a : ? a : ?

= 0 C3:kfa = 0 C3:kf* = 0 C3:kf* = 0 PP < 0 PP = 0 PP > 0 a k t / a b < 0 akdakd < 0 akdak, , < 0

(Hamada and Pitchford)

Cl:k,* > 0 - Cl:k,* > 0 - C2:kf* = 0 C2:kf* = 0

< 0 C3:kfa = 0 C3:kf* = 0 PP? PP > 0 akdakd < o a k t / a b < o

(Bardhan)

Notations: C1: the initial condition 1 + P > S(O);C2: the initial condition 1 + p = S(0); C3: the initial condition 1 + P < S(0); kf*: per capita foreign capital in the steady state; PP: private profit at the social optimum.

investment, i.e., +'. As long as the foreign capital impact function has positive slope, the steady state properties discussed in the preceding section hold. Never- theless, whenever +' < 0, the positive value of k*, can hold only under the initial condition ,I + P > S(0). Although the steady state properties with + ' < 0 and k*f > 0 are basically the same as those in Case 1, Section 3, there are

crucial differences. First, depending on the value of + and 9' the sign of (14) may be positive or negative. Therefore, the private decision-making may deviate from the opimal policy in either direction. In the special case with P < 1 and 9 ' < 0, equation (14) is positive and thus private decision tends to over-attract foreign investment because of failing to recognize the implicit social costs, a result similar to that obtained by Bardhan (1967). Second, when 4 ' < 0, the value of a kda kd is always negative, implying that kf and kd are substituted and foreign capital inflow will always replace domestic capital.

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

5. CONCLUDING REMARKS

PAN LONG TSAI

The problem of foreign investment was studied in the context of a one-sector optimal growth model. The possibility of technology transfer through foreign investment have been incorporated to reflect a salient feature of direct foreign investment. In the last section, the technology transfer function was re- interpreted as the foreign capital impact function to capture possible negative effects of foreign investment. The main results are:

(1) The key element determining whether a country should maintain foreign capital in the long run is the marginal impact of foreign investment. Unless the sum of the social discount rate and the growth rate of the labor force is well below the interest rate S(0) and/or the technology transfer is not large enough, the optimal policy for the host country always involve a positive amount of foreign capital. This conclusion is directly in opposition to the conclusions obtained by Bardhan (1%7), Pitchford (1970), and Hamada (1969) where the only time for the host country to have foreign capital in the steady state is when A + P > S(0). However, our result coincides with theirs if the marginal impact of foreign investment if negative, though we might have k*f = 0 if A + P is not sufficiently greater than S(0) and/or +' is sufficiently small.

(2) The time profile of the control variable kf is also determined by the sign of +'. If it is negative, kf increases (decreases) steadily as kd approaches its steady state value from ho > k', ( h o < k*d). This is the same as that reported by Bardhan (1967) and Pitchford (1970). When 9' > 0 the time profile of kf need not be a monotonic function of kd. It depends on the elasticity of the technology transfer function and that of the margainal productivity curve of capital associated with the sub-production function, f(k).

(3) Depending on the values of + and + ', marginal private profit may deviate from marginal social benefit in either direction. This implies that perfect competi- tion in general cannot achieve a socially optimal solution. Some intervening poli- cy to attract or deter foreign investment is needed by the host country to offset this difference. In fact, the influx of foreign capital may be thought of as creating technological as well as psychic externalities which are captured explicitly by the foreign capital impact function. Thus the standard answer to an externality prob- lem, government intervention, is readily obtained.

Finally, we raise an important issue which deserves further investigation. Sup- pose that productivity is raised by the cumulative a m ~ u n t of foreign capital in- stead of the current amount. Will the conclusions of this study be affected by such "irreversibility" of foreign impact? This question, together with empirical supports of an appropriate foreign capital impact function, needs to be carefully investigated if we want to understand more about impact of foreign investment on

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

FOREIGN CAPITAL IMPAm FUNCTION

the host country.

REFERENCES

Bardhan, P.K., "Optimum Foreign Borrowing," in: K.Shell, ed., Essays on the Theory of Optimal Economic Growth, Cambrdge: MIT Press, 1967, 117-128.

Bhagwati, J.N., "International Factor Movements and National Advantage," Indian Economic Review, October 1979, 73-100.

Brecher, R.A. and Diaz Alejandro, C.F., "Tariffs, Foreign Capital, and Immiserizing Growth," Journal of International Economics, November, 1977, 317-322.

Brecher, R,A. and Findlay, R., "Tariffs, Foreign Capital and National Advantage," Journal of International Economics, May 1983, 277-288.

Buffie, E., "Quantitative Restrictions and the Welfare Effects of Capital Inflows," Journal of International Economics, August 1985, 291-303.

Dci, F., "Volunatary Export Restraints and Foreign Investment," Journal of Interna- tional Economics, August 1985, 305-312.

Baton, J. and Gersovitz, M. "Debt with Potential Repudiation: Theoretical and Empirical Analysis," Review of Economic Studies, April 1981, 289-309.

Findlay, R. "Relative Bachwardness, Direct Foreign Investment, and the Transfer of Technology; a Simple Dynamic Model," Quarterly Journal of Economics, February 1978, 1-16.

Gehrels, F., 'Foreign Investment and Technology Transfer: Optimal Policies," Welt- wirtschaftliches Archiv, 119, No.4, 1983, 663-685.

Hamada, K., "Economic Growth and Long-term International Capital Movements," Yale Economic Essays, Spring 1966, 49-96.

, "Optimal Capital Accumulation by an Economy Facing an Interna- tional Capital Market," Journal of Political Economy, July/August 1969, 684-697.

Hanson, J., "Optimal International Borrowing and Lending," American Economic Review, September 1974, 616-630.

Koizumi, T. and Kopecky, K. J., "Economic Growth, Capital Movements, and Inter- national Transfer of Technical Knowledge," Journal of International Economics, February 1977.

MacDougall, G.D.A., "The Benefits and Costs of Private Investment from Abroad: a Theoretical Approach," Economic Record, March 1960, 13-35.

Minabe, N., "Capital and Technology Movements and Economic Welfare," American Economic Review, December 1974, 1088-1 100.

Mundell, R.A. "International Trade and Factor Mobility," American Economic Re- view, June 1957, 321-335.

Negishi, T., "Foreign Investment and the Long-Run National Advantage," Economic Record, December 1965, 628-632.

Pitchford. J.D., "Foreign Investment and the National Advantage in a Dynamic Con- text." in: I.A. MacDougall and R.H. Snape, e d ~ . , Studies in International Econom- ics, Amsterdam: North-Holland Publishing Company 1970, 193-206.

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014

56 PAN LONG TSAI

Ruffin, R.J., "Growth and the Long-Run Theory of International Capital Move- ments," American Economic re vie.^, December 1979, 832-842.

Tsai, P.L., Investment from Abroad and Nation1 Welfare, Unpublished Ph.D. Dis- sertation, The Ohio State University, 1985.

Dow

nloa

ded

by [

Akd

eniz

Uni

vers

itesi

] at

10:

17 2

0 D

ecem

ber

2014