foreign exchange risk management practices by … · foreign exchange risk management practices by...

TRANSCRIPT

Foreign exchange risk management practices byJordanian nonfinancial firms

Riad Al-Momani*, and Mohammad R. Gharaibeh*Department of Economics, Yarmouk University, Jordan-Irbed.

Fax: 09626 5063042, E-mail: [email protected]

Received (in revised form): 21st June, 2008

Riad Al-Momani is Professor of Economics at the Yarmouk University, Jordan. He graduated from the Utah State

University, USA, in 1985. He has published many papers in national and regional journals. His research interests

include economic development and finance issues, and portfolio management.

Mohammad R. Gharaibeh is a graduate student in Yarmouk University.

Abstract

Foreign exchange risk becomes more and more

important in light of the globalisation and

internationalisation of world markets, and is one of the

most difficult and persistent problems with which the

financial executives must cope. This study concentrates

on the foreign exchange risk management practices of

Jordanian firms, and examines the relationship

between various factors that are presumed to affect the

adopting of foreign exchange risk management

techniques, namely firm size, sector, international

business involvement, and legal structure. The study

focuses on transaction and economic exposures as the

dimensions of foreign exchange risk management

techniques. The results are taken from an empirical

field study of 73 nonfinancial firms listed by Jordan’s

Income and Sales Tax Department as major

taxpayers. The study uses the Kruskal–Wallis one-

way analysis of variances to analyse the data. The

results indicate that the use of foreign exchange risk

management techniques such as financial derivatives is

not a common practice by Jordanian firms. The most

common methods used by firms to counter foreign

exchange risks such as matching, netting, using local

currency, and price policy are internal (natural)

resources. In addition, this study concludes that there

are no relationships between firm size and legal

structure and the management practices toward

transaction exposure. A relationship between a firm’s

sector and international involvement with the

management practices was found in the transaction

exposure dimension. Concerning the economic

exposure dimension, a relationship between all the

characteristics and the managerial techniques is found.

This study recommends proper training programmes for

financial managers in order to enhance their knowledge

about the importance of foreign currency risk and the

different techniques used to manage that risk.

Journal of Derivatives & Hedge Funds (2008) 14,

198–221. doi:10.1057/jdhf.2008.16

Keywords: foreign exchange risk; exchange

rate risk; currency risk; transaction

PREFACE

In an era of globalisation and

internationalisation, the economic environment

198 Journal of Derivatives & Hedge Funds Volume 14 Numbers 3/4 2008

www.palgrave-journals.com/jdhf/

Journal of Derivatives

& Hedge Funds,

Vol. 14 Nos. 3/4, 2008,

pp. 198–221

r 2008 Palgrave

Macmillan

1753-9641

in which most firms operate is highly volatile

and uncertain. This volatility can be reflected in

increased fluctuations in foreign exchange

and interest, and inflation rates; increased

competition, demand levels, etc. In addition, the

extensive use of financial innovations and the

advances in financial instruments to manage this

risk make this issue one of a firm’s priorities.

Foreign currency risk is a crucial factor that

affects most firms, especially those that trade

frequently in international markets. This is so

because if a firm buys a foreign asset, it is

exposed to two types of risk: the first is related to

the value of the asset, while the other is related

to the fluctuations in exchange rates. In other

words, an overseas contract, which is profitable

at the time of the deal, may become unprofitable

if the exchange rates changes. This is an example

of the direct exposure to movements in

exchange rates; however, the exposure can have

an indirect effect through pricing strategy

changes, labour costs, etc. In addition, the

growth in the size of international trade makes

foreign currency risk an important issue for a

whole range of companies.

This study explores the areas of foreign

currency risk management, with a special

emphasis on specific forms of that exposure,

namely transaction and economic exposures.

Translation risk is ignored because of the small

number of multinational firms based in Jordan

exposed to such risk. In addition, the analysis

involves only selected nonfinancial companies as

the sample of the study. Financial companies

were neglected because of the ambiguity

concerning the purpose of their use of hedging

instruments.

Currently, there is a scarcity of research papers

about foreign exchange risk management in

emerging markets. Theoretical studies are

usually supported by findings from developed

countries.1 Therefore, this study will be

distinctive, because it will contribute to the

increase in academic studies on emerging

markets. In addition, it concentrates on Jordan,

one of the Middle Eastern countries, which

makes it one of the first studies in this area.

COMMENTS ON PREVIOUS STUDIES

Previous studies have been conducted regarding

different objectives and visions of the foreign

exchange rate risk. Allayannis et al.2 dealt with

the rationality behind managing such a risk.

Many studied the impact of exchange rate

movements on a firm, such as Karasoy,3 Bradly

and Moles,4 El-Masry,5 and Fang and Miller.6

An investigation of the wide use of exchange

rate risk management techniques was conducted

by Belk and Glaum,7 Batten, et al.,8 and Jonuska

and Samenaite.1 Other studies were conducted

to examine the theory about foreign exchange

risk management and what is done in practice,

such as Brucaite and Yan,9 Dhanani and

Groves,10 and Popov and Stutzmann.11

Most of the literature has been supported.

There are a lot of studies in the developed

countries. However, very few studies were

found to support cases in developing countries.

Such a study is a distinguishing feature because it

is conducted on Jordanian firms as a study case

and Jordan is considered one of the developing

countries in the Middle East.

PROBLEM DEFINITION

As mentioned earlier, there is a scarcity of studies

and papers concerning foreign currency risk

exposure and management in developing

countries. Therefore, to achieve a good start in

this area is to study and identify factors that are

Foreign exchange risk management practices by Jordanian nonfinancial firms 199

presumed to affect the management of foreign

currency risk. This study investigates a problem

that can be defined through the following

questions:

(1) Do Jordanian corporations adopt or

implement foreign exchange risk

management techniques?

(2) What kind of foreign exchange risk

management do Jordanian corporations

mostly use?

(3) Do firm-specific characteristics affect the

level of adoption of foreign exchange risk

management techniques in the Jordanian

environment?

OBJECTIVES OF THE STUDY

The main objective of this study is to investigate

the relationship between foreign currency risk

and international business involvement, legal

structure, firm size, sector, and management

practices in the Jordanian environment.

The impact of firm-specific characteristics on

the managerial practices of Jordanian firms will

also be investigated, by examining the opinions

of financial controllers, treasury managers or

persons involved in foreign exchange

management decisions.

MAIN HYPOTHESIS

In order to conduct this study, the following

hypotheses will be tested:

1H0: There is a significant statistical relationship

between a firm’s international business

involvement level and management practices

and transaction exposure in the Jordanian

environment.

2H0: There is a significant statistical relationship

between a firm’s legal structure and management

practices and transaction exposure risk in the

Jordanian environment.

3H0: There is a significant statistical relationship

between firm size and management practices

and transaction exposure in the Jordanian

environment.

4H0: There is a significant statistical relationship

between a firm’s sector and management

practices and transaction exposure in the

Jordanian environment.

5H0: There is a significant statistical relationship

between a firm’s international business

involvement level and management practices

and economic exposure in the Jordanian

environment.

6H0: There is a significant statistical relationship

between a firm’s legal structure and management

practices and economic exposure risk in the

Jordanian environment.

7H0: There is a significant statistical relationship

between firm size and management practices

and economic exposure in the Jordanian

environment.

8H0: There is a significant statistical relationship

between a firm’s sector and management

practices and economic exposure in the

Jordanian environment.

METHODOLOGY

Because there is no common methodology or

generally accepted design that fits the topic of

this research, the research methodology has been

200 Al-Momani and Gharaibeh

developed in a way that demonstrates the model

of the study, dimensions of the study, hypotheses

and the aspects related to sampling, data and

methods of statistical analysis.

Model of the study

The following chart (Figure 1) shows the firm-

specific characteristics as the independent variables,

which are firm size, industry sector, international

business activities, ownership, and legal structure.

These independent variables will present relations

under two dimensions of dependent variables: the

financial hedging techniques and the operational

hedging techniques.

Variables of the study

The focus of the study is the question of what

determines the method that firms in Jordan use

to manage transaction and economic exposures.

Consequently, the hedging strategies that the

Jordanian firms adopted are designed as

dependent variables.

The dependent variables

(1) Financial hedging techniques. These

techniques are used to hedge transaction

exposure, and they are different from each

other in terms of their sophistication levels.

It starts with using internal hedging

techniques, and then moves to a more

complex hedge by using money market

techniques and currency derivatives.

However, the latter represent a more risky

and expensive instrument to hedge the

transaction exposure.

(2) Operational hedging techniques. These

techniques are used to hedge economic

exposure. They are also different in terms

of risk and cost levels. They start to source

inputs in the same currencies as sales which

can finally be used to conduct major

actions such as altering the currency that

production/operations occur following

movements in foreign exchange rates.

The independent variables

Company-specific characteristics are used to

establish the study of relations to the

management practices concerning foreign

currency risk.

These characteristics are as follows:

(1) Firm size. Total annual sales, equity capital

(capital raised from owners), and market

value of a firm’s assets used as proxies for a

firm size.

(2) International business involvement. This

characteristic is concerned with the degree

of involvement of a firm in the foreign

environment. Three variables are used as

proxies for measuring the degree of foreign

involvement: (1) percentage of foreign

currency sales to total sales (FS/TS),

(2) percentage of foreign currency costs

to total costs (FC/TC), (3) percentage

TransactionExposure

EconomicExposure

FinancialHedging

Techniques

OperationalHedging

Techniques

IndustryGroupings

Firm Size

InternationalInvolvement

LegalStructure

Figure 1: Model of the study

Foreign exchange risk management practices by Jordanian nonfinancial firms 201

of foreign currency debt to total debt

(FD/TD).

(3) Firm’s sector. The financial and operational

hedging techniques across different

industries are examined. The research

covers Jordanian commercial,

manufacturing, and other firms (mining

and processing, agriculture, and building

and construction).

(4) The legal form of the firms. The main legal

forms of Jordanian firms are sole trader,

partnership, closed limited corporations

and public limited corporations.

The main different characteristics of the firms

are presumed to have effects on foreign currency

exposure due to the different structures, markets

and cash flows of the firms.

POPULATION AND SAMPLE OF THE

STUDY

This study was performed by exploring the

impact of selected company-specific

characteristics on the adoption of foreign

currency risk management techniques. To

achieve this goal, a sample of the largest

nonfinancial firms, in terms of annual sales and

annual income, operating in Jordan was used as a

unit of analysis. There were 456 firms. Only 310

firms from different sectors and types met the

criteria of the study.12

The population of the study was sub-grouped

in terms of economic sectors into three strata

(sub-groups), which are manufacturing,

commercial, and other sectors. These sub-

groups are unequal in size: it is preferable to use

proportionate (unequal size) stratified random

sampling to represent the three sub-groups.

This ensures the selection of a representative

sample. Thus, 120 firms were selected: 45

manufacturing firms, 60 commercial firms, and

15 firms from other sectors.

Data collection techniques

Data needed for this study were collected from

two sources: secondary and primary.

Secondary sources

The secondary source represents the related

information that was found in books, articles,

periodicals, working papers, e-papers, and

unpublished studies such as dissertations and

theses, in addition to some related and valuable

websites.

Primary sources

One primary source was a questionnaire

written in Arabic using scales such as itemised

rating scales, which are effective for measuring

anchors as needed. In addition, category

scales were used to identify specific

characteristics of the subject. The questionnaire

consists of three parts, representing general

information on the subjects, a transaction

exposure section, and an economic exposure

section. Finally, a summary of some techniques

for foreign currency risk management is

provided in order to ensure the full

understanding of the question asked.

The questionnaire was distributed to the

respondents, completed by them at their work

locations and returned to the researcher.

They were reminded one to two days before the

due date to return the questionnaire, if they had

not already done so. The respondents targeted

were mainly financial managers and/or

treasurers.

202 Al-Momani and Gharaibeh

Data analysis techniques

To test the hypotheses, the study employed some

known statistical techniques. To measure the

central tendency and dispersion, descriptive

statistics were employed such as frequencies,

ratios, means and standard deviations. The

Kruskal–Wallis one-way analysis of variances

(ANOVA) was used to examine the significance

of statistical differences. This technique

compares the variances between groups with the

variances within groups. In case such significant

statistical differences between groups do exist,

the one-way ANOVA is used when the

dependent variable is on an ordinal scale, and the

independent variables are normally scaled.

Data analysis/major results

This section presents and analyses the data

obtained by the questionnaire. The goodness of

data was examined using the statistical

techniques mentioned above.

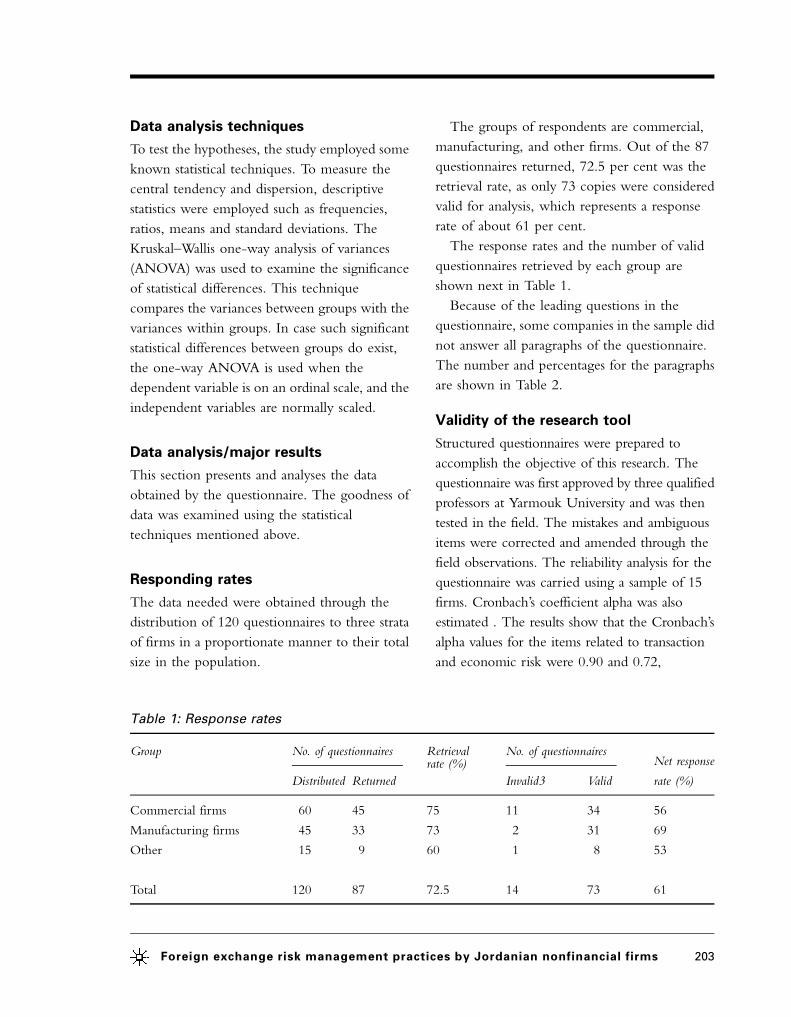

Responding rates

The data needed were obtained through the

distribution of 120 questionnaires to three strata

of firms in a proportionate manner to their total

size in the population.

The groups of respondents are commercial,

manufacturing, and other firms. Out of the 87

questionnaires returned, 72.5 per cent was the

retrieval rate, as only 73 copies were considered

valid for analysis, which represents a response

rate of about 61 per cent.

The response rates and the number of valid

questionnaires retrieved by each group are

shown next in Table 1.

Because of the leading questions in the

questionnaire, some companies in the sample did

not answer all paragraphs of the questionnaire.

The number and percentages for the paragraphs

are shown in Table 2.

Validity of the research tool

Structured questionnaires were prepared to

accomplish the objective of this research. The

questionnaire was first approved by three qualified

professors at Yarmouk University and was then

tested in the field. The mistakes and ambiguous

items were corrected and amended through the

field observations. The reliability analysis for the

questionnaire was carried using a sample of 15

firms. Cronbach’s coefficient alpha was also

estimated . The results show that the Cronbach’s

alpha values for the items related to transaction

and economic risk were 0.90 and 0.72,

Table 1: Response rates

Group No. of questionnaires Retrieval No. of questionnaires

Distributed Returned

rate (%)

Invalid3 Valid

Net response

rate (%)

Commercial firms 60 45 75 11 34 56

Manufacturing firms 45 33 73 2 31 69

Other 15 9 60 1 8 53

Total 120 87 72.5 14 73 61

Foreign exchange risk management practices by Jordanian nonfinancial firms 203

respectively, while the value for all items was 0.87.

These values of Cronbach’s alpha are acceptable

for studies such as the current one (Table 3).

Hypotheses testing

This section is devoted to testing the previously

mentioned hypotheses of the study. The

hypotheses mainly aim to find significant

relationships between presumed factors (firm-

specific characteristics) and the management

techniques of foreign currency risk.

Firm-specific characteristics are related to

management techniques under two dimensions:

transaction exposure management and economic

exposure management.

Since there are more than two independent

variables (firm-specific characteristics) and the

Table 2: Response rates for each question

Question Frequency Valid %

Sectors of the firm 73 100.0

Firms legal structure 73 100.0

Annual sales of the firms 67 91.8

Firm’s capital 70 95.9

Percentage of foreign sale’s to total sales 70 95.9

Percentage of foreign cost’s to total cost’s 70 95.9

Percentage of foreign debt to total debt 73 100.0

Existence of A/P and A/R 73 100.0

Managing foreign currency risk 42 57.5

Purpose of managing currency risk 28 38.3

Effect of exchange rate variations on the firms activities 64 87.6

Effect of capital size on managing transaction exposure risk 36 49.3

Effect of sales volume on managing transaction exposure risk 39 53.4

Effect of firm’s sector on transaction exposure risk 38 52.0

Percentage of FS/TS sales effect on transaction exposure risk management 39 53.4

Percentage of FC/TC sales effect on transaction exposure risk management 39 53.4

Percentage of FD/TD sales effect on transaction exposure risk management 39 53.4

Legal structure effect on transaction exposure risk management 38 52.0

Effect of capital size on managing economic exposure risk 55 75.3

Effect of sales volume on managing economic exposure risk 52 71.2

Effect of firms sector on managing economic exposure risk 57 78.0

Percentage of FS/TS sales effect on economic exposure risk management 54 73.9

Percentage of FC/TC sales effect on economic exposure risk management 54 73.9

Percentage of FD/TD sales effect on economic exposure risk management 58 79.4

Legal structure effect on economic exposure risk management 57 78.0

204 Al-Momani and Gharaibeh

dependent variables (management techniques for

each dimension) are measured on an interval

scale, ANOVA is appropriate for testing these

hypotheses.

The results of transaction exposure dimension

Transaction exposure is related to the risk that

arises from day-to-day transactions dealt with

foreign currencies that are subject to volatility in

value against the local currency.

In order to obtain results concerning whether

there is a relationship between the firm-specific

characteristics and foreign currency risk

management techniques adopted by Jordanian

firms, different techniques were listed. To show

how often they were used, answers were coded

in such a way that if a technique was always used

by a firm, the code was (5); if it was usually used,

the code was (4); if it was sometimes used, the

code was (3); if it was seldom used, the code was

(2); and finally if the technique was never used,

the code was (1).

(1) The effect of firm size on managing transaction

exposure risk

Firm size is expressed by two variables: capital

and sales volume of a firm. The hypothesis is as

follows:

H01: There is a significant statistical relationship

between firm size and management practices

and transaction exposure in the Jordanian

environment.

The one-way ANOVA results for each

variable are as follows:

(a) The effect of the capital size of a firm on managing

transaction exposure risk

As Table 4 shows, with a significant level of

0.074, there is no significant statistical

relationship between the capital size of a firm

and the techniques used to manage transaction

exposure. This considers 0.05 significance level

or below as the acceptable level for social science

studies.

(b) The effect of the sales volume of a firm on managing

transaction exposure risk

The result of the sales volume character and its

relation to the use of transaction exposure

management techniques (as shown in Table 5)

indicates an insignificant statistical relation. The

significance level for this test is (¼ 0.218>0.05),

which is not acceptable.

Both results assert the rejection of the

hypothesis of the significant statistical

relationship between firm size and the

management of transaction exposure.

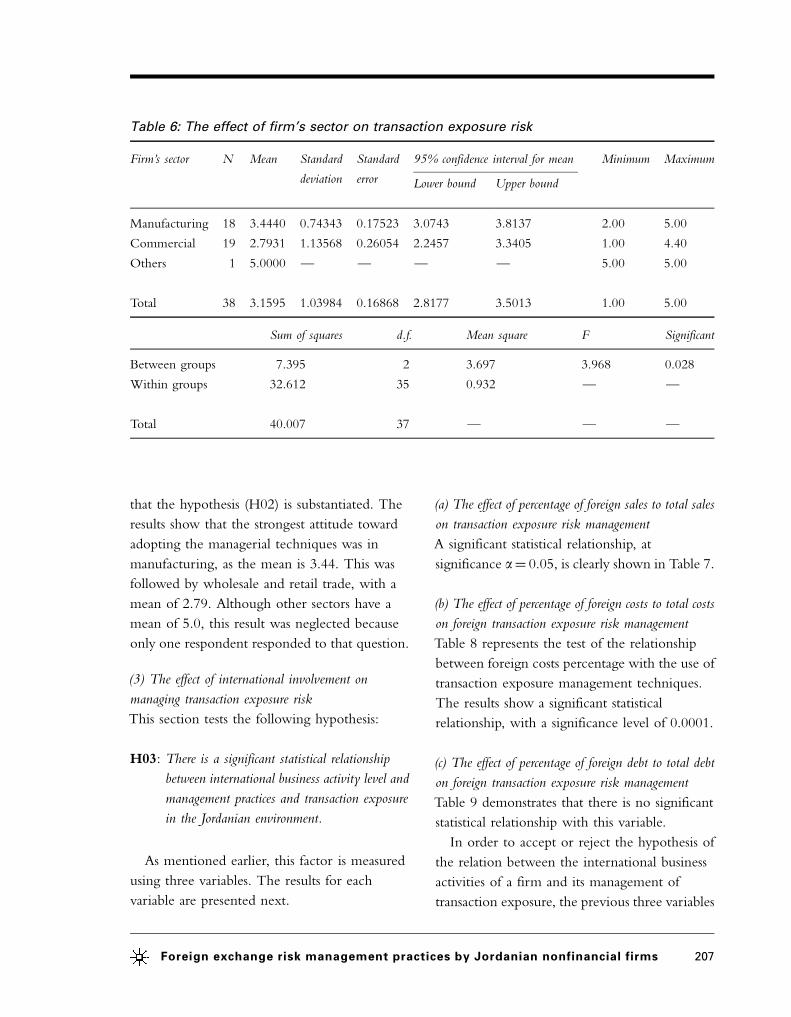

(2) The effect of firm sector on managing transaction

exposure risk

H02: There is a significant statistical relationship

between firm sector and management practices

and transaction exposure in the Jordanian

environment.

Table 6 shows that there is a significant

statistical relationship between the sector of a

firm and the techniques used. The significant

level of 0.028 is lower than 0.05. This implies

Table 3: Cronbach’s coefficient alpha

Dimension No. of

items

Cronbach’s

coefficient alpha

Transaction risk 5 0.90

Economic risk 3 0.72

All items 8 0.87

Foreign exchange risk management practices by Jordanian nonfinancial firms 205

Table 4: The effect of capital size on managing transaction exposure risk

Capital size N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

o1m 13 2.5618 1.25761 0.34880 1.8018 3.3217 1.00 4.33

1–o5m 9 3.3888 0.64716 0.21572 2.8914 3.8863 2.27 4.40

5–o10m 11 3.4977 0.71636 0.21599 3.0165 3.9790 2.40 5.00

10m or more 3 3.6869 1.17689 0.67948 0.7633 6.6104 2.73 5.00

Total 36 3.1483 1.03424 0.17237 2.7983 3.4982 1.00 5.00

Sum of squares d.f. Mean square F Significant

Between groups 7.206 3 2.402 2.543 0.074

Within groups 30.231 32 0.945 — —

Total 37.438 35 — — —

Table 5: The effect of sales volume on managing transaction exposure risk

Sales volume N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

o3m 8 2.3523 1.62872 0.57584 0.9906 3.7139 1.00 5.00

3–6m 15 3.1988 0.70348 0.18164 2.8092 3.5884 2.00 4.40

6–9m 6 3.6015 0.43486 0.17753 3.1452 4.0579 3.00 4.00

9–12m 4 3.5476 0.55737 0.27868 2.6607 4.4345 2.86 4.00

13–15m 2 3.3667 1.36707 0.96667 �8.9160 15.6493 2.40 4.33

15m or more 4 3.4318 1.06374 0.53187 1.7392 5.1245 2.73 5.00

Total 39 3.1554 1.02638 0.16435 2.8227 3.4881 1.00 5.00

Sum of squares d.f. Mean square F Significant

Between groups 7.393 5 1.479 1.495 0.218

Within groups 32.639 33 0.989 — —

Total 40.031 38 — — —

206 Al-Momani and Gharaibeh

that the hypothesis (H02) is substantiated. The

results show that the strongest attitude toward

adopting the managerial techniques was in

manufacturing, as the mean is 3.44. This was

followed by wholesale and retail trade, with a

mean of 2.79. Although other sectors have a

mean of 5.0, this result was neglected because

only one respondent responded to that question.

(3) The effect of international involvement on

managing transaction exposure risk

This section tests the following hypothesis:

H03: There is a significant statistical relationship

between international business activity level and

management practices and transaction exposure

in the Jordanian environment.

As mentioned earlier, this factor is measured

using three variables. The results for each

variable are presented next.

(a) The effect of percentage of foreign sales to total sales

on transaction exposure risk management

A significant statistical relationship, at

significance a¼ 0.05, is clearly shown in Table 7.

(b) The effect of percentage of foreign costs to total costs

on foreign transaction exposure risk management

Table 8 represents the test of the relationship

between foreign costs percentage with the use of

transaction exposure management techniques.

The results show a significant statistical

relationship, with a significance level of 0.0001.

(c) The effect of percentage of foreign debt to total debt

on foreign transaction exposure risk management

Table 9 demonstrates that there is no significant

statistical relationship with this variable.

In order to accept or reject the hypothesis of

the relation between the international business

activities of a firm and its management of

transaction exposure, the previous three variables

Table 6: The effect of firm’s sector on transaction exposure risk

Firm’s sector N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

Manufacturing 18 3.4440 0.74343 0.17523 3.0743 3.8137 2.00 5.00

Commercial 19 2.7931 1.13568 0.26054 2.2457 3.3405 1.00 4.40

Others 1 5.0000 — — — — 5.00 5.00

Total 38 3.1595 1.03984 0.16868 2.8177 3.5013 1.00 5.00

Sum of squares d.f. Mean square F Significant

Between groups 7.395 2 3.697 3.968 0.028

Within groups 32.612 35 0.932 — —

Total 40.007 37 — — —

Foreign exchange risk management practices by Jordanian nonfinancial firms 207

must be considered. The degree of international

involvement of a firm was measured by %FS

(percentage of foreign sales), %FC (percentage of

foreign costs), and %FD (percentage of foreign

debt).

Both %FS and %FC showed a significant

statistical relationship with the use of the

management techniques, but %FD showed no

relation. The sample results of that specific

variable, however, showed that 42.4 per cent of

firms had no debt in foreign currency at all. Also,

83.4 per cent of firms had a %FD of 50 per cent

or less and this weakens the reliability of this

variable. Therefore, the variables %FS and %FC

are more reliable in determining the result of the

test for that hypothesis.

Finally, considering the results of %FS and

%FC and their significance level, H03 is

substantiated.

(4) The effect of legal structure on foreign transaction

exposure risk management

The hypothesis is as follows:

H04: There is a significant statistical relationship

between legal structure and management

practices and transaction exposure risk in the

Jordanian environment.

Table 7: Percentage of foreign sales to total sales effect on transaction exposure currency risk

management

Percentage of

FS/TS

N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

0 5 2.8667 0.81989 0.36667 1.8486 3.8847 2.50 4.33

10 5 1.4909 1.09771 0.49091 0.1279 2.8539 1.00 3.45

20 4 3.8333 0.33333 0.16667 3.3029 4.3637 3.33 4.00

30 5 3.3891 — 0.43407 2.1839 4.5943 2.40 5.00

40 7 3.4208 0.87233 0.32971 2.6140 4.2275 2.00 4.40

50 5 3.8273 0.82597 0.36939 2.8017 4.8529 2.73 5.00

60 2 3.2667 0.09428 0.06667 2.4196 4.1137 3.20 3.33

70 2 3.4167 0.11785 0.08333 2.3578 4.4755 3.33 3.50

80 2 3.4545 0.89995 0.63636 �4.6312 11.5403 2.82 4.09

100 2 2.8182 0.77139 0.54545 �4.1125 9.7488 2.27 3.36

Total 39 3.1554 1.02638 0.16435 2.8227 3.4881 1.00 5.00

Sum of squares d.f. Mean square F Significant

Between groups 19.699 9 2.189 3.122 0.009

Within groups 20.333 29 0.701 — —

Total 40.031 38 — — —

208 Al-Momani and Gharaibeh

The results show that there is no significant

statistical relationship between the legal structure

of a firm and its management of transaction

exposure. Therefore, H04 is rejected. As shown

in Table 10, the test resulted in a significant level

of 0.443.

The results of economic exposure dimension

Economic exposure is related to the risk that is

generated from dealing with foreign currencies

in the long run.

This section tests the hypotheses concerning

the relationship between a firm’s specific

characteristics and the use of risk management

techniques concerning economic exposure.

Like transaction exposure, economic exposure

management techniques were coded depending

on how often these techniques were used by

firms. If a technique was always used by the

respondent, the code was (5); if it was usually

used, the code was (4); if it was sometimes used,

the code was (3); if it was seldom used, the code

was (2); and if the technique was never used, the

code was (1). ANOVA was used to test the

hypotheses.

Results depending on each character are

presented next.

Table 8: Percentage of foreign costs to total costs effect on transaction exposure risk

management

Percentage of

FC/TC

N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

0 1 1.0909 — — — — 1.09 1.09

10 4 1.0000 0.00000 0.00000 1.0000 1.0000 1.00 1.00

30 2 3.9091 1.54278 1.09091 �9.9522 17.7704 2.82 5.00

40 1 2.0000 — — — — 2.00 2.00

50 2 3.1000 0.14142 0.10000 1.8294 4.3706 3.00 3.20

60 3 3.2121 0.61881 0.35727 1.6749 4.7493 2.73 3.91

70 8 3.6940 0.42059 0.14870 3.3423 4.0456 3.33 4.33

80 12 3.4128 0.86226 0.24891 2.8650 3.9607 2.50 5.00

90 5 3.3073 0.61100 0.27325 2.5486 4.0659 2.40 4.09

100 1 2.2727 — — — — 2.27 2.27

Total 39 3.1554 1.02638 0.16435 2.8227 3.4881 1.00 5.00

Sum of squares d.f. Mean square F Significant

Between groups 25.955 9 2.884 5.942 0.000

Within groups 14.076 29 0.485 — —

Total 40.031 38 — — —

Foreign exchange risk management practices by Jordanian nonfinancial firms 209

(1)

Firm size

The hypothesis was as follows:

H05: There is a significant statistical relationship

between firm size and management practices

and economic exposure in the Jordanian

environment.

The variables used to measure this character were

sales volume and capital size. The one-way

ANOVA results for each variable are presented next.

(a) The effect of the capital size of a firm on managing

economic exposure risk

Table 11 shows a significant statistical

relationship between the capital size of a firm

and the techniques used to manage economic

exposure, with a significance level of 0.0001.

(b) The effect of the sales volume of a firm on managing

economic exposure risk

The result of the test shows a significant

statistical relationship concerning this variable.

The significance level is 0.001 for this test, as

shown in Table 12.

Both capital and sales tests show significant

statistical relationships with the degree of using

the management techniques to handle economic

exposure. Thus, H06 is substantiated concerning

the relationship between firm size and its

management of economic exposure.

Table 9: Percentage of foreign debt to total debt effect on transaction exposure risk

management

Percentage of

FD/TD

N Mean Standard

deviation

Standard

error

95 per cent confidence interval for mean Minimum Maximum

Lower bound Upper bound

0 12 2.5455 1.32130 0.38143 1.7060 3.3851 1.00 4.40

10 1 4.3333 — — — — 4.33 4.33

20 6 3.3681 0.37120 0.15154 2.9785 3.7576 3.00 4.00

30 3 3.3394 0.60311 0.34821 1.8412 4.8376 2.82 4.00

40 8 3.7397 0.74113 0.26203 3.1201 4.3593 2.73 5.00

50 4 2.5000 0.00000 0.00000 2.5000 2.5000 2.50 2.50

60 1 3.3636 — — — — 3.36 3.36

70 2 4.0909 1.28565 0.90909 �7.4602 15.6420 3.18 5.00

80 2 3.2455 1.19565 0.84545 �7.4971 13.9880 2.40 4.09

Total 39 3.1554 1.02638 0.16435 2.8227 3.4881 1.00 5.00

Sum of squares d.f. Mean square F Significant

Between groups 12.483 8 1.560 1.699 0.140

Within groups 27.548 30 0.918 — —

Total 40.031 38 — — —

210 Al-Momani and Gharaibeh

Table 10: Legal structure effect on transaction exposure risk management

Legal structure N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

Public shareholding 12 3.4868 0.77937 0.22499 2.9916 3.9820 2.00 5.00

Private shareholding 3 2.7697 0.39263 0.22669 1.7943 3.7450 2.40 3.18

Partnership 3 3.6263 0.40693 0.23494 2.6154 4.6371 3.33 4.09

Limited liability 15 2.9539 1.38090 0.35655 2.1892 3.7186 1.00 5.00

Private company 5 2.7000 0.44721 0.20000 2.1447 3.2553 2.50 3.50

Total 38 3.1273 1.02487 0.16626 2.7905 3.4642 1.00 5.00

Sum of squares d.f. Mean square F Significant

Between groups 4.046 4 1.011 0.959 0.443

Within groups 34.818 33 1.055 — —

Total 38.863 37 — — —

Table 11: The effect of capital size on managing economic exposure risk

Capital size N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

o1m 20 4.4826 0.59637 0.13335 4.2035 4.7617 3.00 5.00

1–o5m 16 3.5336 0.76772 0.19193 3.1245 3.9427 1.33 4.57

5–o10m 14 3.4653 0.53724 0.14358 3.1551 3.7755 3.00 4.71

10m or more 5 3.0333 0.46248 0.20683 2.4591 3.6076 2.50 3.67

Total 55 3.8158 0.80685 0.10880 3.5977 4.0340 1.33 5.00

Sum of squares d.f. Mean square F Significant

Between groups 14.948 3 4.983 12.576 0.000

Within groups 20.206 51 0.396 — —

Total 35.154 54 — — —

Foreign exchange risk management practices by Jordanian nonfinancial firms 211

Table 13: The effect of firm’s sector on economic exposure risk

Firm’s sector N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

Manufacturing 26 3.3736 0.76520 0.15007 3.0646 3.6827 1.33 4.83

Wholesale and

retail trade

29 4.1319 0.76916 0.14283 3.8393 4.4244 2.50 5.00

Others 2 3.0833 0.35355 0.25000 �0.0932 6.2599 2.83 3.33

Total 57 3.7492 0.84651 0.11212 3.5246 3.9738 1.33 5.00

Sum of squares d.f. Mean square F Significant

Between groups 8.801 2 4.400 7.585 0.001

Within groups 31.328 54 0.580 — —

Total 40.129 56 — — —

Table 12: The effect of sales volume on managing economic exposure risk

Sales volume N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

o3m 16 4.3905 0.88562 0.22141 3.9186 4.8624 1.33 4.86

3–o6m 17 3.4529 0.57337 0.13906 3.1581 3.7477 2.00 4.17

6–o9m 9 3.1296 0.41481 0.13827 2.8108 3.4485 2.50 4.00

9–o12m 4 3.3917 0.23154 0.11577 3.0232 3.7601 3.20 3.67

13–o15m 2 3.4286 0.60609 0.42857 �2.0169 8.8741 3.00 3.86

15m or more 4 3.2500 0.44096 0.22048 2.5483 3.9517 2.83 3.83

Total 52 3.6642 0.79678 0.11049 3.4424 3.8860 1.33 4.86

Sum of squares d.f. Mean square F Significant

Between groups 12.865 5 2.573 6.065 0.000

Within groups 19.513 46 0.424 — —

Total 32.378 51 — — —

212 Al-Momani and Gharaibeh

(2) The effect of firm sector on managing economic

exposure risk

H06: There is a significant statistical relationship

between industry groupings and management

practices and economic exposure in the

Jordanian environment.

Table 13 shows that there is a significant

statistical relationship between sector of a firm

and its management of economic exposure. The

significant level of 0.001 asserts this relationship

and H06 is substantiated.

The results show that the strongest attitude

toward adopting the managerial techniques was

for wholesale and retail trade, as the mean is

4.13. This is followed by manufacturing, with a

mean of 3.37.

(3) The effect of international involvement on

managing economic exposure

In this section, we tested the following

hypothesis:

H07: There is a significant statistical relationship

between international business activity level and

Table 14: Percentage of foreign sales to total sales effect on economic exposure currency risk

management

Percentage of

FS/TS

N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

10 2 3.0000 0.00000 0.00000 3.0000 3.0000 3.00 3.00

20 3 3.0000 0.60093 0.34694 1.5072 4.4928 2.50 3.67

30 3 3.0556 1.49381 0.86245 �0.6553 6.7664 1.33 4.00

40 9 3.4630 0.51301 0.17100 3.0686 3.8573 2.83 4.33

50 8 3.4000 0.89389 0.31604 2.6527 4.1473 2.00 4.83

60 2 3.2500 0.35355 0.25000 0.0734 6.4266 3.00 3.50

70 6 3.5167 0.49610 0.20253 2.9960 4.0373 3.00 4.33

80 7 4.1327 0.91884 0.34729 3.2829 4.9824 3.00 4.86

100 6 3.7857 0.58902 0.24046 3.1676 4.4038 3.00 4.71

Total 54 3.6612 0.79521 0.10821 3.4441 3.8783 1.33 4.86

Sum of squares d.f. Mean square F Significant

Between groups 11.808 9 1.312 2.659 0.015

Within groups 21.708 44 0.493 — —

Total 33.515 53 — — —

Foreign exchange risk management practices by Jordanian nonfinancial firms 213

management practices and economic exposure in

the Jordanian environment.

As mentioned earlier, this characteristic is

measured using three variables. The results for

each variable are presented next.

(a) The effect of percentage of foreign sales to total sales

on economic exposure risk management

With significance value equalling 0.015, the

percentage of foreign sales to total sales has a

significant statistical relationship with the use of

management techniques. This is clearly shown in

Table 14.

(b) The effect of percentage of foreign costs to total costs

on economic exposure risk management

In addition, with significance value equalling

0.001, the percentage of the foreign costs to the

total costs has a significant relationship with the

use of management techniques. This is shown in

Table 15.

(c) The effect of percentage of foreign debt to total debt

on economic exposure risk management

Finally, the test of the relation between the

percentage of foreign debt to total debt and the

managerial actions toward economic exposure

reveal a significant statistical relationship. The

Table 15: Percentage of foreign costs to total costs effect on economic exposure risk

management

Percentage of

FC/TC

N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

0 1 1.3333 — — — — 1.33 1.33

10 2 3.0833 1.53206 1.08333 �10.6817 16.8484 2.00 4.17

30 5 3.7095 0.81726 0.36549 2.6948 4.7243 2.83 4.71

40 10 3.9000 0.87206 0.27577 3.2762 4.5238 2.50 4.67

50 6 3.7119 0.78975 0.32241 2.8831 4.5407 2.50 4.57

60 3 3.3889 0.50918 0.29397 2.1240 4.6537 2.83 3.83

70 13 3.4916 0.41186 0.11423 3.2427 3.7405 3.00 4.33

80 9 3.3963 0.34859 0.11620 3.1283 3.6642 3.00 4.00

90 4 4.8571 0.00000 0.00000 4.8571 4.8571 4.86 4.86

100 1 4.8333 — — — — 4.83 4.83

Total 54 3.6612 0.79521 0.10821 3.4441 3.8783 1.33 4.86

Sum of squares d.f. Mean square F Significant

Between groups 15.007 9 1.667 3.964 0.001

Within groups 18.508 44 0.421 — —

Total 33.515 53 — — —

214 Al-Momani and Gharaibeh

significance figure is 0.008, which is

demonstrated in Table 16.

The results of the previous three tests assert

the acceptance of the relation between the

degree of international involvement of a firm

and its management of the economic exposure.

Therefore, H07 is substantiated. In addition, an

indication of a stronger attitude toward using the

managerial techniques moving to higher levels of

foreign sales, costs, and debts is seen by

reviewing the means.

(4) The effect of legal structure on foreign economic

exposure risk management

The hypothesis is as follows:

H08: There is a significant statistical relationship

between legal structure and management

practices and economic exposure risk in the

Jordanian environment.

The test was performed to ascertain whether

there is a relationship between the legal structure

of a firm (as a character) and the management

techniques used in handling economic exposure

risk. The results show a significant statistical

relationship under a significance level of 0.001.

Therefore, H08 is also accepted, as shown in

Table 17.

The results show that the strongest attitude

toward adopting the managerial techniques was

Table 16: Percentage of foreign debt to total debt effect on economic exposure risk

management

Percentage of

FD/TD

N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

0 4 3.0000 0.00000 0.00000 3.0000 3.0000 3.00 3.00

10 2 3.0000 0.00000 0.00000 3.0000 3.0000 3.00 3.00

20 3 3.5079 0.45008 0.25985 2.3899 4.6260 3.00 3.86

30 8 3.5000 0.59040 0.20874 3.0064 3.9936 2.83 4.83

60 2 3.0833 0.35355 0.25000 �0.0932 6.2599 2.83 3.33

70 9 3.3444 0.47697 0.15899 2.9778 3.7111 2.50 4.00

80 2 4.2738 0.62293 0.44048 �1.3230 9.8706 3.83 4.71

90 5 4.6667 0.00000 0.00000 4.6667 4.6667 4.67 4.67

Total 58 3.7535 0.83970 0.11026 3.5327 3.9743 1.33 5.00

Sum of squares d.f. Mean square F Significant

Between groups 13.170 8 1.646 2.985 0.008

Within groups 27.020 49 0.551 — —

Total 40.190 57 — — —

Foreign exchange risk management practices by Jordanian nonfinancial firms 215

for partnerships, as the mean is 4.54. This is

followed by limited liabilities firms, with a mean

of 3.97 and private and public shareholdings

firms, with means of 3.60 and 3.19, respectively.

Usage levels of different managerial

techniques by Jordanian firms

Other results describe the usage levels of each

foreign currency risk management technique in

each dimension, that is, transaction and

economic exposures. Tables 18 and 19 show the

means and standard deviations for each

technique.

Techniques to deal with transaction exposure

were classified in terms of sophistication level

into three groups. The highest sophisticated level

in terms of cost and risk is that of derivatives,

which are forward, future, options, and swap

contracts. The low value of mean of the various

hedging techniques suggests a low usage level of

these techniques by firms. Forward contracts had

the highest mean relative to this group, with

3.32.

The second group, which has a relatively

moderate risk and cost hedging level, is short-

term borrowing and deposit. A stronger attitude

toward using these techniques is indicated by the

higher means in the table, with 3.40 for the

short-term deposits and 3.57 for short-term

borrowing.

Finally, the last group of techniques, in which

the management hedges the cost and risk

internally, without involving a third party, is

considered the least sophisticated. The technique

with the highest level of usage is the pricing

policy, with a mean of 4.61, followed by the

domestic currency, with 4.50. The technique

Table 17: Legal structure effect on economic exposure risk management

Legal structure N Mean Standard

deviation

Standard

error

95% confidence interval for mean Minimum Maximum

Lower bound Upper bound

Public shareholding 16 3.1979 0.53451 0.13363 2.9131 3.4827 2.00 4.17

Private shareholding 6 3.6000 0.58310 0.23805 2.9881 4.2119 2.83 4.33

Partnership 7 4.5476 0.71824 0.27147 3.8834 5.2119 3.50 5.00

Limited liability 27 3.9730 0.84504 0.16263 3.6387 4.3073 1.33 4.86

Private company 1 2.5000 — — — — 2.50 2.50

Total 57 3.7609 0.84527 0.11196 3.5366 3.9852 1.33 5.00

Sum of squares d.f. Mean square F Significant

Between groups 12.364 4 3.091 5.814 0.001

Within groups 27.647 52 0.532 — —

Total 40.011 56 — — —

216 Al-Momani and Gharaibeh

with the least usage in that group is netting, with

a mean of 3.50.

Generally, the results show that the higher the

sophistication level of the technique in terms

of risk and cost, the lower the level of usage.

Table 19 shows the usage level of techniques to

deal with economic exposure. The technique

with the highest usage level, with a mean of

4.71, is altering the currency, in which the

production cost occurs, following movements in

Table 18: Level of using the following hedging instrument to manage foreign exchange risk

(transaction exposure)

Hedging instrument Mean N Standard deviation

Forward contracts 3.32 34 1.28

Future contracts 3.25 25 1.10

Option contracts 3.17 18 1.35

Swap contracts 3.00 17 0.98

Short-term borrowing 3.57 23 1.04

Short-term deposits 3.40 23 1.40

Pricing policy 4.61 31 0.77

Using domestic currency 4.50 25 1.00

Netting 3.50 23 1.10

Leading and lagging 3.61 17 1.08

Matching 4.11 24 1.05

Other methods 4.35 4 1.22

Table 19: Level of using the following hedging instrument to manage foreign exchange risk

(economic exposure)

Hedging technique Mean Standard

deviation

Sourcing inputs in the same currencies as sales are made 3.27 1.25712

Altering the currency from which inputs are sourced, following

movement in foreign exchange rates

3.45 1.24025

Altering the currency in which production occur, following

movements in foreign exchange rates

4.71 0.75020

Foreign currency denominated debt 3.75 1.21873

Diversifying sales in many different currencies 3.72 1.11496

Long-term derivatives 3.32 1.09515

Foreign exchange risk management practices by Jordanian nonfinancial firms 217

foreign exchange rates. Foreign currency

denominated debt and diversifying sales in many

different currencies, with means of 3.75 and

3.72, respectively. Altering the currency from

which inputs are sourced following movement

in foreign exchange rates had a mean of 3.45.

Finally, the use of long-term derivatives and the

technique of sourcing inputs in the same

currencies as those in which sales are made had

the lowest means, with 3.32 and 3.27,

respectively.

Reasons behind not using the managerial

techniques by Jordanian firms

Firms were asked about the reasons behind not

using the different techniques mentioned in the

questionnaire.

The results for the transaction dimension

are presented in Table 20. It is clear that the

majority of the respondents (33.4 per cent)

consider complexity and lack of experience

to be two of the problems that stand against

adopting some of the techniques. 35.6 per cent

Table 20: The reasons behind not using one or more of the managing techniques (transaction

exposure)

Reason Frequency Valid %

Too complex and there is no trained staff to deal with this

kind of risk

15 33.4

Not allowed 5 11.1

Instruments are not available 6 13.3

Not logical to manage foreign exchange risk 3 6.6

Other reasons 16 35.6

Total 45 100.0

Table 21: The reasons behind not using one or more of the managing technique (economic

exposure)

Reason Frequency Valid %

Instruments are not available 8 14.5

Too complex and there is no trained staff to deal with this risk 4 7.3

Not allowed 7 12.7

Not logical to manage foreign exchange risk 3 5.5

The pegged JD to the US dollar gave the firm a stable position 33 60.0

Total 55 100.0

218 Al-Momani and Gharaibeh

of respondents stated other reasons for not

using the techniques: the majority answered

that their transactions have a certain stability

due to the Jordanian dinar being pegged to the

US dollar. Others added that as they gain from

the volatility of currency they accept a certain

level of loss, otherwise the firm limits that

loss through reflecting the differences to the

prices. 11.1 per cent of the respondents said

they do not use the techniques simply because

they do not have the authority to do so,

while 13.3 per cent believe that those

instruments do not exist or are not available.

In this section, the implied instruments

are the derivatives because the other instruments

are natural and do not need a second party in

order to use them. Finally, 6.6 per cent of

respondents said they do not believe in the

rationality behind managing transaction

exposure.

The same questions were asked again but they

this time were concerned with the reasons

behind not using the different techniques to

manage economic exposure. The results are as

shown in Table 21.

The pegging of the Jordanian dinar to

the US dollar gives stability to firms toward

the movement of the currencies. The majority

of respondents therefore believe there is no need

to act to this exposure.

In addition, the results show that 14.5 per cent

of respondents believe that the instruments are

not available in the Jordanian environment. 7.3

per cent believe that using these techniques is

overly complex and that staff lack the experience

to use them. On the other hand, 12.7 per cent of

respondents do not use the techniques because

they do not have the authority to do so. Finally,

5.5 per cent do not believe in the relevance of

managing foreign currency risk.

CONCLUSIONS

Motivated by the fact that foreign currency risk

becomes more and more important in the light

of the globalisation and internationalisation, this

study was conducted in order to gain insight into

the management of foreign currency risk by

Jordanian firms. In addition, it examined the

impact of firm-specific characteristics and their

relationship with the managerial techniques used

to face that risk with respect to two dimensions:

transaction and economic exposures. The

specific factors of a firm included size, sector,

legal structure, and international involvement.

The results of the questionnaire give an idea

about Jordan’s economic environment in terms

of comprehension, exposure, and management

of foreign currency risk.

Evidence from the analysis shows that 66

per cent of the firms do manage their foreign

currency risk. The majority of the firms rely,

however, on natural hedging techniques, and the

use of more sophisticated techniques such as

financial derivatives is not common practice by

Jordanian firms.

The lack of knowledge in managers and other

staff members in management is one of the

major obstacles for the use of the techniques.

Some firms do not believe in the relevance of

their exposure to foreign currency risk. Others

believe that financial derivatives are not available

in the Jordanian market. Financial derivatives do,

however, exist in some major Jordanian banks.

The great majority of firms considered the

pegged Jordanian dinar to the US dollar one of the

reasons that gave their foreign transactions a certain

level of stability, since both currencies move in the

same direction with approximately the same

proportion. Dealing with other currencies that are

subject to volatility in their exchange rates respect

Foreign exchange risk management practices by Jordanian nonfinancial firms 219

to the Jordanian dinar as the euro needs substantial

effort to manage.

Concerning the firm-specific characteristics

and their hypothesised relationship to the

management of transaction exposure dimension,

this study shows that there is no relationship

between a firm size and the management

practices toward transaction exposure. The same

result was shown for a firm’s legal structure.

The relationship between a firm’s different

sectors and the hedging techniques used was

significant, and the highest attitude was in the

manufacturing sector. The study also found that

a firm’s international involvement and

management practices positively correlated.

On the other hand, the results concerning

the firm-specific characteristics and their

relationship to the managerial techniques used

toward economic exposure were as follows:

Firm size negatively correlated to the

management practices. This result could be

attributed to the fact that larger firms have less

flexibility to act toward economic exposure. The

operational hedging techniques are expensive

and risky because they involve a large amount of

resources. Shifting the industry from one

currency to another is one example for

techniques that need to adopt major resources.

In addition, larger firms may be engaged in

long-term contracts that take into consideration

the foreign currency volatility risk.

The evidence also found a correlation

between a firm’s sector and its management

practices: commercial firms had the strongest

attitude toward managing economic exposure.

Moreover, a relationship between the legal

structure of a firm and its management to

economic exposure was found to be significant.

Partnerships seemed to have a higher adoption

rate of the managerial techniques than other

types of entities. This can be attributed to the

fact that the owners of a firm have more motive

and authority to make decisions involving

business than managers in other legal structures.

A firm’s degree of international involvement

and its management practices positively

correlated.

RECOMMENDATIONS

Based on the results of the study, some

recommendations are stated as follows:

(1) Proper training programmes should be

conducted for financial managers in order

to enhance their knowledge about the

importance of foreign currency risk and

the different techniques used to manage

that risk.

(2) Many of the Jordanian firms attributed the

absence of the hedging techniques in their

firms to the exchange rate policy of the

CBJ (Central Bank of Jordan). This policy

gives firms a stable position toward the

JD/$US exchange rate changes. Jordanian

firms must, however, be conscious of the

fact that the JD may be floated against the

US dollar in the future. In this case, the

magnitude of the foreign currency

exposure will be very high and will need

effective foreign currency risk management

practices.

(3) Banks and other financial firms should play

a vital role in handling of risk management

issues. Financial derivatives should be

offered and promoted more. In addition,

consulting services should be provided to

manage such risk.

(4) Specialised financial firms that offer a wide

range of financial instruments to hedge

220 Al-Momani and Gharaibeh

foreign currency risk and that also provide

well-experienced staff familiar with

Jordan’s economic environment should be

established. Furthermore, the experiences

of such specialised firms in developed

countries must be benefited from.

References and Notes

1 Jonuska, M. and Samenaite, I. (2003) ‘Foreign

Exchange Risk Management in Lithuanian Economy:

The Use of Currency Derivatives’, Published Master

Thesis, Stockholm School of Economics in Riga,

Available online.

2 Allayannis, G., Brown, G. and Klapper, L. (2001)

‘Exchange Rate Risk Management Evidence from East

Asia’, Policy Research Working Paper, No. 2606,

The World Bank, Available online: http://

www-wds.worldbank.org/external/default/

WDSContentServer/IW3P/IB/2001/06/15/

000094946_01060604005427/Rendered/PDF/

multi0page.pdf.

3 Karasoy, A. (1995) ‘Management of Exchange Rate

Risk in Turkish Banking Sector: A Model and Tests’,

Discussion Paper, No. 9602, Central Bank of the

Republic of Turkey, Available online: http://

www.tcmb.gov.tr/research/discus/9602eng.pdf.

4 Bradley, K. and Moles, P. (2001) ‘The Effects of

Exchange Rate Movements on Non-financial UK

Firms’, International Business Review, Vol. 10,

pp. 51–69.

5 El-Masry, A. (2003) ‘The Exchange Rate Exposure of

UK Non-financial Companies: Industry Level Analysis’,

Journal of Managerial Finance, Vol. 32, No. 2, pp. 115–136.

6 Fang, W. and Miller, S. (2004) ‘Exchange Rate

Depreciation and Exports: The Case of Singapore’,

Working Paper, No. 2004-45, University of

Connecticut, Available online: http://www.

econ.uconn.edu/working/2004-45.pdf.

7 Belk, P.A and Glaum, M. (1990) ‘The Management of

Foreign Exchange Risk in UK Multinationals: An

Empirical Investigation’, Accounting and Business

Research, Vol. 21, No. 81, pp. 3–13.

8 Batten, J., Mellor, R. and Wan, V. (1993) ‘Foreign

Exchange Risk Management Practices and Products

Used by Australian Firms’, Journal of International

Business Studies, Vol. 25, pp. 557–573.

9 Brucaite, V. and Yan, S. (2000) ‘Financial Risk

Management — Case Studies with SKF and Elof

Hansson’, Published Master Thesis, Goteborg

University, Available online: http://www.

handels.gu.se/epc/archive/00001538/01/

Brucaite_200014.pdf.

10 Dhanani, A. and Groves, R. (2001) ‘The Management

of Strategic Exchange Risk: Evidence from Corporate

Practices’, Accounting and Business Research, Vol. 31,

No. 4, pp. 275–290.

11 Popov, V. and Stutzmann, Y. (2003) ‘How is

Foreign Exchange Risk Managed? An Empirical

Study to Two Swiss Companies’, Published Master

Thesis, University of Lausanne, Available online:

http://www.hec.unil.ch/cms_mbf/master_thesis/

0314.pdf.

12 Company statistics. Main Economic Sectors, Jordan

Companies Control Department, Available online:

www.ccd.gov.jo.

Foreign exchange risk management practices by Jordanian nonfinancial firms 221