foreign exchange market

TRANSCRIPT

Presentation on

Wasim Yousuf,MIB 3rd Sem.,Bangalore City College.

WHAT IS FOREX?

The FOREX is the world’s biggest financial market.

The FOREX or “FOReign EXchange” is the planets

biggest most liquid financial marketplace hands

down.

“Foreign exchange” refers to money denominated

in the currency of another nation or group of

nations. Any person who exchanges money

denominated in his own nation’s currency for

money denominated in another nation’s currency

acquires foreign exchange.

WHAT IS FOREX? (CONTD.) Foreign exchange can be cash, funds available on credit

cards and debit cards, traveler’s checks, bank deposits, or

other short-term claims. It is still “foreign exchange” if it is a

short-term negotiable financial claim denominated in a

currency other than the U.S. dollar.” – Sam Cross – The

Federal Reserve Bank

The Foreign Exchange is made up of anyone who exchanges

the currency of one country for that of another.

The FOriegn EXchange does not have a centralized

exchange like the stock market in New York or the

commodities markets with centralized exchanges in cities like

New York and Chicago.

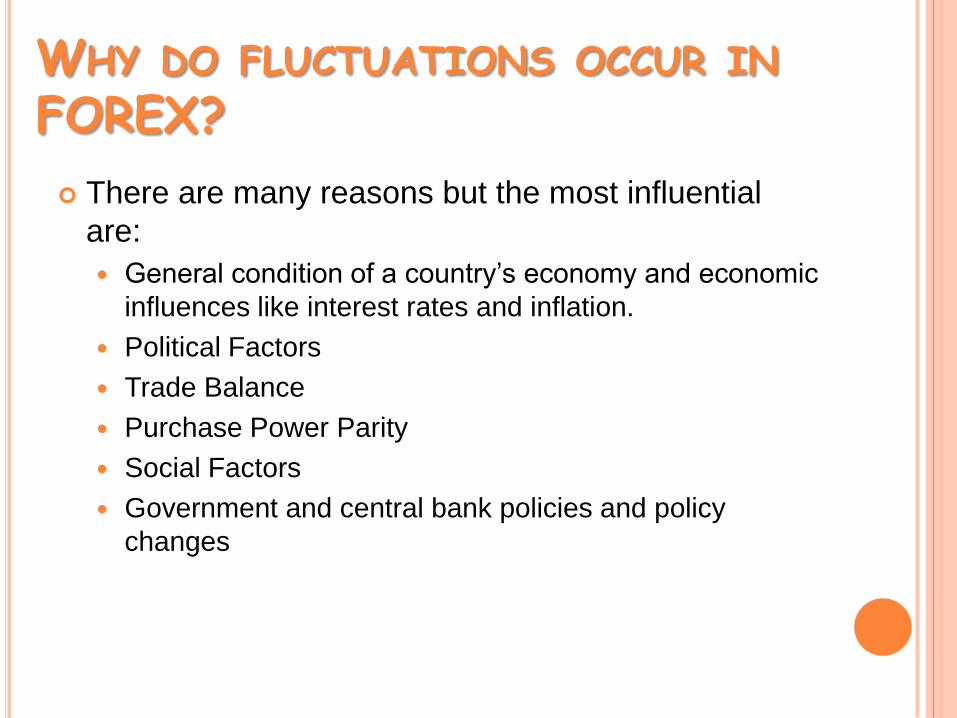

WHY DO FLUCTUATIONS OCCUR IN

FOREX?

There are many reasons but the most influential

are:

General condition of a country’s economy and economic

influences like interest rates and inflation.

Political Factors

Trade Balance

Purchase Power Parity

Social Factors

Government and central bank policies and policy

changes

CURRENCY TRADING VS STOCK

TRADING

Many find trading currency much more attractive

than trading stocks for the following reasons::

Focused Attention –

When you trade stocks, there are literally tens of thousands of companies to

choose from when trying to decide which ones to invest in. That is a lot of

information to assimilate and keep track of. With the Foreign Exchange the

number of choices is dramatically reduced making it much easier to

concentrate on trading. While many countries are traded, there are five main

players in this global arena...

The United States (USD)

The European Union (EURO)

Great Britain (GBP)

Japan (JPY)

Switzerland (CHF)

CURRENCY TRADING VS STOCK TRADING: (CONTD.)

LIQUIDITY –Because FOREX is literally the biggest "market" on

earth, whether you are entering or exiting, getting your

order filled is almost instantaneous which is not always

the case with stocks.

PROFIT POTENTIAL –You can open a currency trading account for less than

$500 but the profit potential is greater than stocks, with

FOREX you can profit regardless of whether or not the

value of a currency is rising or falling.

CURRENCY TRADING VS STOCK TRADING: (CONTD.)

CONVENIENT –The FOReign EXchange is open for business 24 hours a

day, 5 days a week offering trading opportunities for

even the busiest people.

AMPLE TRADING OPPORTUNITIES –Because the currency process are always fluctuating up

and down, there are plenty of trading opportunities.

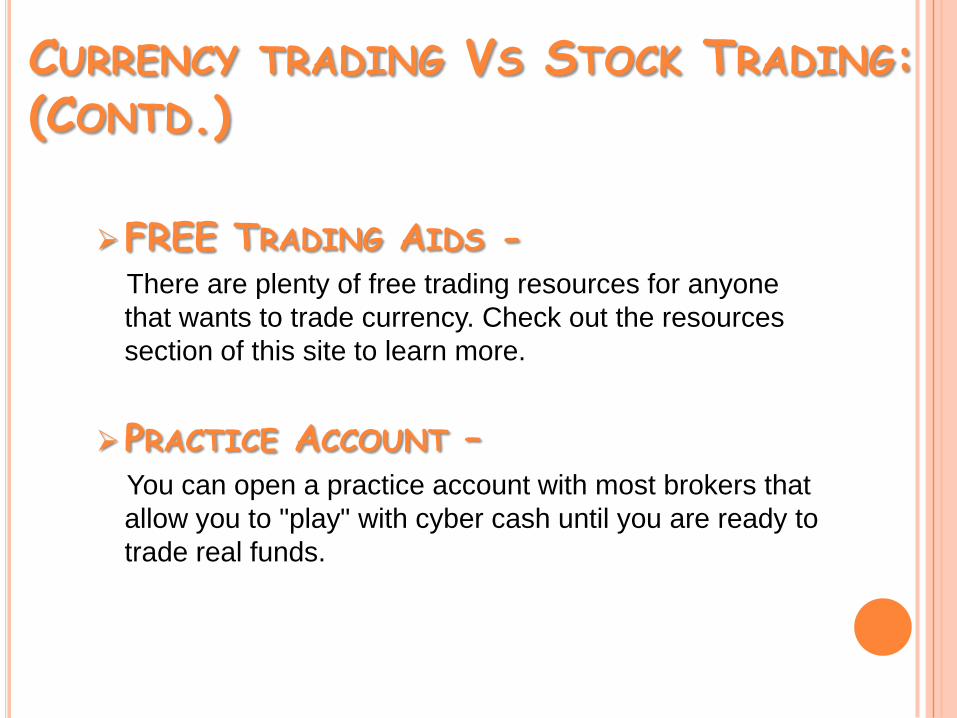

CURRENCY TRADING VS STOCK TRADING: (CONTD.)

FREE TRADING AIDS -There are plenty of free trading resources for anyone

that wants to trade currency. Check out the resources

section of this site to learn more.

PRACTICE ACCOUNT –You can open a practice account with most brokers that

allow you to "play" with cyber cash until you are ready to

trade real funds.

NOMINAL VS. REAL EXCHANGE

RATES

Nominal Exchange Rates are value of one currency

in terms of another.

They do not, however, measure purchasing power,

or Real Exchange Rate.

Example:

Suppose you can exchange $1 for 1818 Italian lira (L).

Though L1818 seems a large number, but in Rome a

hamburger may cost L4500.

In other words, purchasing power of lira is very less as

compared to that of dollar.

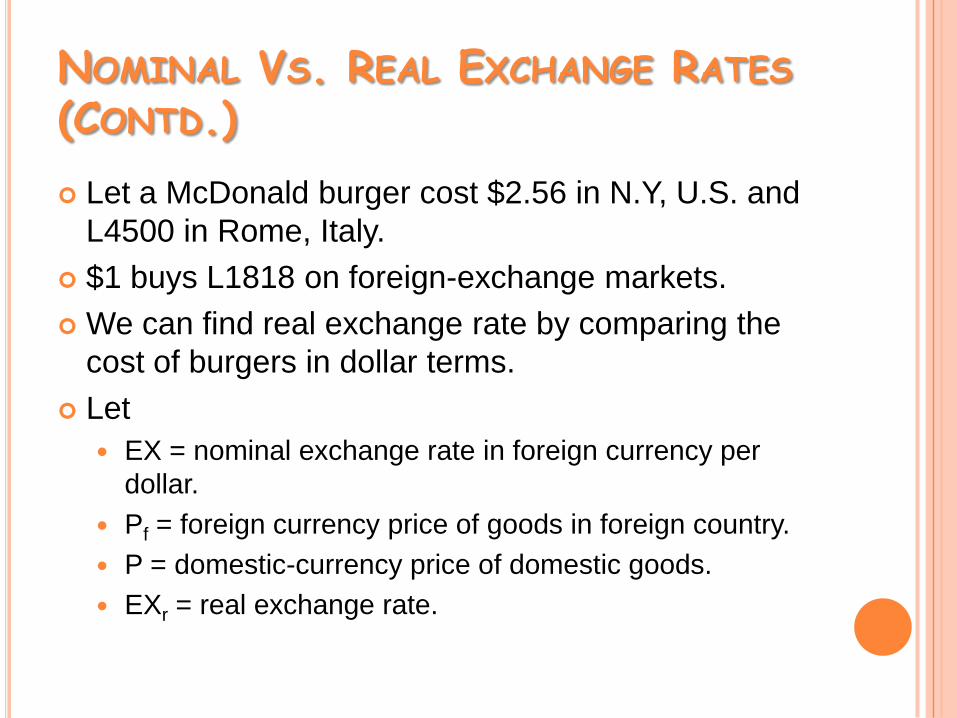

NOMINAL VS. REAL EXCHANGE RATES

(CONTD.)

Let a McDonald burger cost $2.56 in N.Y, U.S. and

L4500 in Rome, Italy.

$1 buys L1818 on foreign-exchange markets.

We can find real exchange rate by comparing the

cost of burgers in dollar terms.

Let

EX = nominal exchange rate in foreign currency per

dollar.

Pf = foreign currency price of goods in foreign country.

P = domestic-currency price of domestic goods.

EXr = real exchange rate.

NOMINAL VS. REAL EXCHANGE RATES

(CONTD.)

EXr = 1.03 Italian

Thus, $2.56 will buy 1 McDonald burger in U.S. but

1.03 McDonald burger in Italy.

NOMINAL VS. REAL EXCHANGE RATES

(CONTD.)

Countries produce many different goods.

Real Exchange Rate computed from price indexes,

which compare price of basket of goods in one

country with price of it in another.

The relationship between nominal and real

exchange rates depends on rates of inflation in two

countries.

We can calculate % change in real exchange rate

as % change in numerator of previous equation

minus the % change in denominator.

NOMINAL VS. REAL EXCHANGE RATES

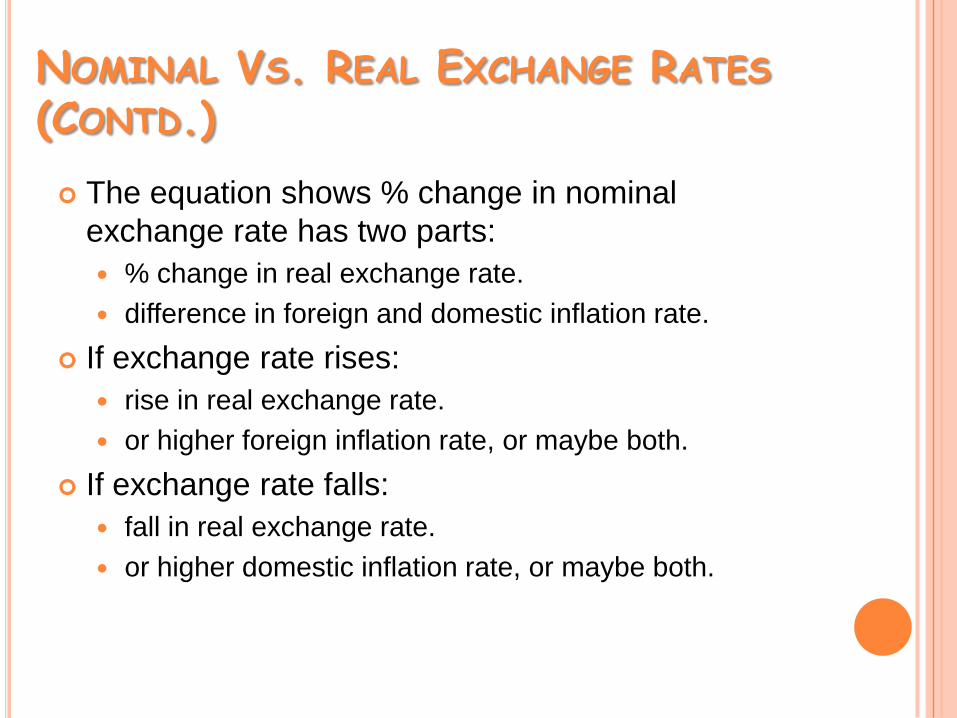

(CONTD.)

The equation shows % change in nominal

exchange rate has two parts:

% change in real exchange rate.

difference in foreign and domestic inflation rate.

If exchange rate rises:

rise in real exchange rate.

or higher foreign inflation rate, or maybe both.

If exchange rate falls:

fall in real exchange rate.

or higher domestic inflation rate, or maybe both.

NOMINAL VS. REAL EXCHANGE RATES

(CONTD.)

Suppose Peynolds and Barker are companies in

two countries whose currencies are crown and

royal.

Peynolds makes ball pens sold at 2 crown each.

Barker makes high-quality ink pens sold at 10

royals each.

Real exchange rate between Peynolds and Barker

pens is 10 ball pens per ink pen.

What is the nominal Exchange rate?

FOREIGN EXCHANGE MARKETS

From perspective of individual consumers orinvestors, exchange rates can be used to convertone currency into another.

International currencies are traded in foreign-exchange-markets around the world.

Market forces determine the exchange rate thatprevails for consumers and investors.

Exchange rates affect the cost of acquiring foreignfinancial assets or foreign goods and services.

Major participants are importers and exporters,banks, investment portfolio managers, and centralbanks.

FOREIGN EXCHANGE MARKETS

(CONTD.)

The worldwide volume of foreign exchange trading

is enormous, and it has ballooned in recent years.

New technologies, such as Internet links, are used

among the major foreign exchange trading centres

(London, New York, Tokyo, Frankfurt, and

Singapore).

The integration of financial centres implies that

there can be no significant arbitrage.

The process of buying a currency cheap and selling it

dear.

FOREIGN EXCHANGE MARKETS

(CONTD.)

Two types of transactions take place in foreignexchange markets.

1) Spot Market Transactions:

Currencies or bank deposits are exchangedimmediately (two day settlement period).

Spot rate is the price quote at which you can buyimmediately.

2) Forward Transactions:

Currencies or bank deposits are exchanged at a setdate in the future.

Investors sign a contract for a given quantity ofcurrency and exchange rate.

At future date, actual exchange takes place at rateknown as forward rate.

DETERMINING LONG RUN EXCHANGE

RATES

We will look at four key factors that account for

long-run trends in the supply of and demand for

currencies in the foreign exchange markets:

o Price level differences.

o Productivity differences.

o Preference for domestic or foreign goods.

o Trade barriers

DETERMINING LONG RUN

EXCHANGE RATES: PRICE LEVEL

DIFFERENCES

When price levels rise in U.K. relative to price levels in U.S., then U.K. goods or financial assets become more costly as compared to similar U.S. goods or financial assets.

In such case where U.K. experiences higher inflation rate, pound is less useful as store of value than dollar.

All else being equal, relative increase in price levels lead to depreciation of domestic currency.

Example:

In late 1970’s excess growth of U.K.’s price levels over U.S. price levels lead pound to depreciate against dollar.

DETERMINING LONG RUN

EXCHANGE RATES: PRODUCTIVITY

DIFFERENCES

Productivity growth measures the increase in output level of a country for a given input level.

Higher productivity leads to cheaper production of domestic goods than foreign goods.

Hence domestic goods can be supplied at lower prices than foreign goods, leading to higher demand.

This higher demand for domestic goods leads to higher demand for domestic currency.

Thus higher productivity leads to appreciation of domestic currency.

Example:

In late 1970’s and early 1980’s U.S. productivity level was higher than U.K. leading to appreciation of dollar against pound.

DETERMINING LONG RUN EXCHANGE RATES: PREFERENCE FOR DOMESTIC OR FOREIGN GOODS.

If U.S. consumers prefer British-made goods, they

will demand more pounds to buy these goods.

It will put upward pressure on pound and depreciate

the dollar.

Example:

In mid 1980’s U.S. consumers in second half of decade

They preferred U.K. goods leading to depreciation of

dollar.

DETERMINING LONG RUN EXCHANGE RATES: TRADE BARRIERS

Countries do not always allow goods to be traded

freely with no market intervention.

Example of trade barriers are quotas and tariffs.

They increase demand for domestic currency,

leading to higher exchange rates in the long run for

the country imposing these barriers.

Example:

Suppose U.S. imposes tariff on U.K. leather goods, this

will lead to higher price of the U.K. leather goods than

U.S. made leather goods.

There will be higher demand for domestic U.S. made

leather goods leading to higher dollar demand.

LAW OF ONE PRICE AND THE PURCHASING

POWER PARITY THEORY

The Law Of One Price states that identical goodsshould be sold at identical prices.

Profit opportunities should ensure that its price issame.

Lets start with an example:

Suppose a yard of cloth produced by manufacturers inU.S. sells for $10

Same type of cloth produced by British manufacturers inU.K. sells for 5 pounds.

Law of one price says that exchange rate should be 5pound per 10 dollar or 0.5 pound/dollar.

Lets consider two cases if starting exchange rate is notwhat is supposed to be.

LAW OF ONE PRICE AND THE PURCHASING

POWER PARITY THEORY

If current exchange rate is 0.25 pound /dollar.

Then U.S. cloth will be cheaper as compared to the

U.K. cloth.

Consumers would demand dollars for purchasing

U.S. cloth.

This will lead to appreciation of dollar till exchange

rate reaches 0.50 pound/dollar.

LAW OF ONE PRICE AND THE PURCHASING

POWER PARITY THEORY

If current exchange rate is 0.75 pound /dollar.

Then U.K. cloth will be cheaper as compared to the

U.S. cloth.

Consumers would demand dollars for purchasing

U.K. cloth.

This will lead to depreciation of dollar till exchange

rate reaches 0.50 pound/dollar.

LAW OF ONE PRICE AND THE PURCHASING

POWER PARITY THEORY

When we extend law of one price from one good tobasket of goods, it becomes Purchasing PowerParity theory of exchange rate determination.

The Purchasing Power Parity (PPP) theory is basedon the assumption that real exchange rates arefixed.

Thus it means that differences in the inflation rate inthe two countries causes changes in nominalexchange rate between two countries.

It states that whenever a country’s price level isexpected to fall relative to other country’s pricelevel, it’s currency should appreciate relative toother country’s currency.

LAW OF ONE PRICE AND THE PURCHASING

POWER PARITY THEORY

Movements in exchange rates not completely

consistent with PPP theory:

For differentiated products, law of one price does not

hold, e.g. Kodak and Sony camera.

Not all goods and services (e.g. haircut, sandwich) are

internationally traded.

Significant differences in prices of non-traded goods and

services are not completely reflected in exchange rates.

The assumption of constant real exchange rate is not

reasonable. There may be shifts in preferences for

domestic or foreign goods and trade barriers.

EXPECTED RETURNS ON DOMESTIC AND

FOREIGN ASSETS

Suppose you want to invest $1000 for one year.

You have choice between U.S. Treasury bill or aJapanese government bond.

U.S. instrument pays you interest and principal indollars with nominal interest rate of 5% per year.

Japanese instrument pays you interest andprincipal in yen and carries nominal interest rate of5% per year.

You should invest in one which will give you higherreturn.

To compare the returns you should compare theirreturns in dollar terms.

EXPECTED RETURNS ON DOMESTIC AND FOREIGN

ASSETS

you invest in U.S. Treasury bill, you will receive an

interest return of $50, so your investment will be

worth $1050 after one year.

If you want to calculate the expected return from

the Japanese bond you must convert it into yen and

then a year from now you must convert the interest

and principal from yen into dollars.

Then you can compare it with the return from U.S.

Treasury bill.

EXPECTED RETURNS ON DOMESTIC AND FOREIGN

ASSETS

Suppose current nominal exchange rate is 100

yen/dollar.

You expect the exchange rate will rise by 5% in the

next year, thus the expected future nominal

exchange rate EXe will be 100*1.05 = 105

yen/dollar.

Now when you convert $1000 into yen you have an

investment of 100000 yen.

After receiving and interest rate of 5%, your

investment is worth 105000 yen after a year.

At that time expected exchange rate EXe is 105

yen/dollar.

EXPECTED RETURNS ON DOMESTIC AND FOREIGN

ASSETS

Thus the expected value of your investment in

dollar terms will be 105000 yen/105 = $1000. !!!

Hence even though Japanese bond pays you the

same stated interest rate as the U.S. Treasury bill,

but it carries a lower expected return: $0 instead of

$50.

EXPECTED RETURNS ON DOMESTIC AND FOREIGN

ASSETS

$1• Investment

i• Earns Interest i

(1 + i)• Yielding total $(1 + i)

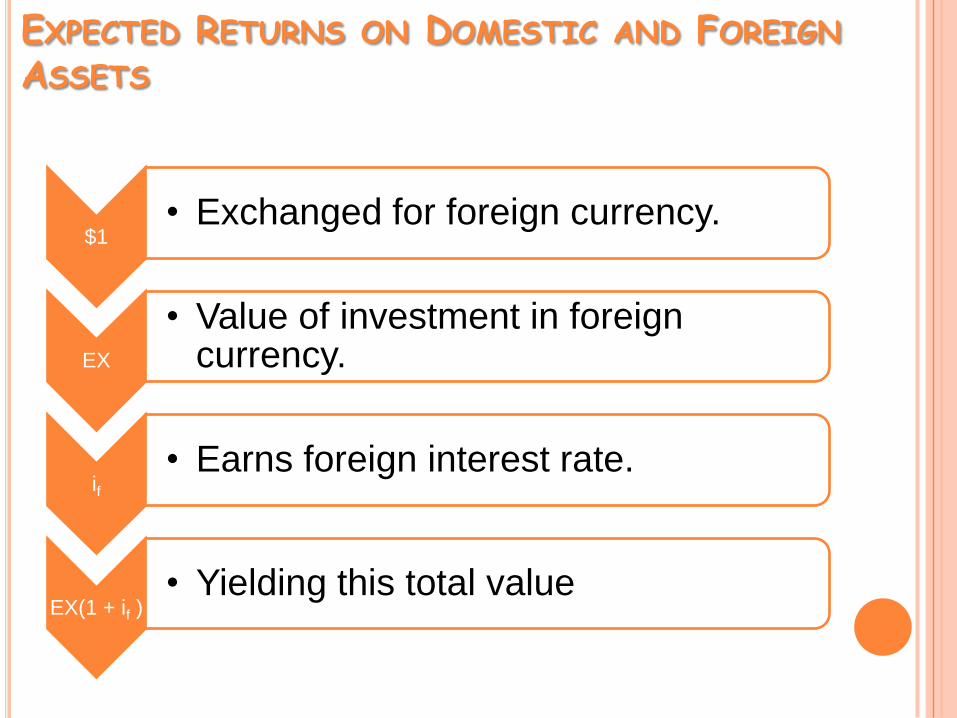

EXPECTED RETURNS ON DOMESTIC AND FOREIGN

ASSETS

$1• Exchanged for foreign currency.

EX

• Value of investment in foreign currency.

if• Earns foreign interest rate.

EX(1 + if )• Yielding this total value

EXPECTED RETURNS ON DOMESTIC AND FOREIGN

ASSETS

EX(1 + if )• Value of investment.

EX(1 + if)/EXe

• Convert to domestic currency.

1 + if -∆EXe/EX

• Yielding approximately

INTEREST RATE PARITY

Nominal Interest Rate Parity Condition:

When domestic and foreign assets have identical risks,

liquidity and information characteristics, their nominal

returns (measured in same currency) must be identical.

Thus any difference between the nominal interest rates

on U.S. assets and Japanese assets reflect currency

appreciation and depreciation.

This condition states:

i = if - ∆EXe/EX

When domestic interest rate is higher than the

foreign interest rate, the domestic currency

depreciates.

THANK YOU!

WASIM YOUSUF