for more information on these reports and others, visit...

TRANSCRIPT

SmartMarket Report

Produced with support from

Green BuildingRetro� t & RenovationRapidly Expanding Market Opportunities Through Existing Buildings

McGraw-Hill Construction SmartMarket Reports™

Get smart about the latest industry trends.For more information on these reports and others, visit

www.construction.com ⁄market_research

www.construction.com

■ Design and Construction Intelligence

SmartMarket Report

$189Environmental Bene� ts Statement: This report is printed using soy-based inks on New Leaf ReincarnationMatte, made with 100% recycled � ber, 50% post-consumer waste and processed chlorine-free with a cover on New Leaf Primavera Gloss, made with 80% recycled � ber, 40% post-consumer waste, processed chlorine-free. By using this environmentally-friendly paper, McGraw-Hill Construction saved the following resources (calculations provided by new Leaf Paper, based on research conducted by Environmental Defense Fund and other members of the Paper Task Force):

33 fully grown trees

9,291 gallons of water

17 million Btus of energy

1,590 pounds of solid waste

2,914 pounds of greenhouse gases

1335cvr.indd 1 10/16/09 6:27:10 PM

McGraw-Hill Construction

PresidentNorbert W. Young, Jr., FAIA

McGraw-Hill Construction Research & Analytics/Alliances

Vice President, Global Thought Leadership & Business DevelopmentHarvey M. Bernstein, F. ASCE, LEED AP

Senior Director, Research & AnalyticsBurleigh Morton

Director, Green Content & Research CommunicationsMichele A. Russo, LEED AP

Director, Market ResearchJohn DiStefano, MRA, PRC

Director, Industry AlliancesJohn Gudgel

Reproduction or dissemination of any information contained herein is granted only by contract or prior written permission from McGraw-Hill Construction.

Green Building: Retrofit and Renovation SmartMarket Report

Editorial DirectorMichele A. Russo, LEED AP

Editor-in-ChiefDonna Laquidara-Carr, LEED AP

Contributing EditorJulie Miltner, LEED AP

Senior Group Art DirectorFrancesca Messina

Contributing Art DirectorDonald Partyka

Managing Art DirectorTed Keller

Production ManagerAlison Lorenz

Research Project ManagerRichard Goodier, MRA, PRC, LEED AP

ContributorsCatlin O’Shaughnessy, LEED APMonica Andrews

For further information on this SmartMarket Report™ or for any in the series, please contact

McGraw-Hill Construction Research & Analytics 34 Crosby Drive, Suite 201 Bedford, MA 01730

1-800-591-4462 [email protected]

■ Design and Construction Intelligence

SmartMarket Report

About McGraw-Hill ConstructionMcGraw-Hill Construction (MHC), part of The McGraw-Hill Companies, connects people, projects and products across the design and construction industry, serving owners, architects, engineers, general contractors, subcontractors, building product manufacturers, suppliers, dealers, distributors and adjacent markets.

A reliable and trusted source for more than a century, MHC has remained North America’s leading provider of construction project and product information, plans and specifications, indus- try news, market research, and industry trends and forecasts. In recent years, MHC has emerged as an industry leader in the crit-ical areas of sustainability and interoperability as well.

In print, online, and through events, MHC offers a variety of tools, applications, and resources that embed in the workflow of our customers, providing them with the information and intelligence they need to be more productive, successful, and competitive.

Backed by the power of Dodge, Sweets, Architectural Record, Engineering News-Record (ENR), GreenSource and 11 regional publications, McGraw-Hill Construction serves more than one million customers within the $5.6 trillion global construction community. To learn more, visit us at www.construction.com

ResourcesOrganizations, websites and publications that can help you get smarter about green retrofit, renovation and new building

Acknowledgements:

The authors wish to thank our sponsors Autodesk, Siemens and UL Environ-ment, Inc. for helping us bring this information to the market. Specifically, we would like to thank Catherine Palmer and Sarah Hodges; Autodesk; Brad Haeberle and Ari Kobb, Siemens; and Christopher Nelson, Stephen H. Wenc and Julia Farber, UL Environment, Inc.

As always, thanks to the U.S. Green Building Council for their support, in particular Rick Fedrizzi, Rebecca Flora, Doug Gatlin, Tom Dietsche, Anthony Guma, Karol Kaiser, Marc Heisterkamp and Ashley Katz.

A sincere thanks to Chris Ludeman and Raymond Torto from CB Richard Ellis for providing the prospects list for the market research.

Additional thanks to the team at GSA; Kelly Romano and Mary Milmoe, Carrier Corp.; and Chris MacFadden, Turner Construction for their support in the project.

We would also like to thank the many individuals who provided detailed project and performance data on their case study projects as well as Gordon Gill, Adrian Smith and Bob Peck for providing their insights.

Federal GovernmentU.S. Department of EnergyMain website: energy.govOffice of Energy Efficiency and Renewable Energy (EERE): eere.energy.govNational Renewable Energy Laboratory: nrel.gov

U.S. Environmental Protection AgencyMain website: epa.govEnergy Star: energystar.govWaterSense: epa.gov/WaterSense

U.S. General Services Administration: gsa.gov

National Institute of Standards and Technology: nist.gov

American Recovery and Reinvestment Act 2009: recovery.gov

Academia and Nonprofit OrganizationsAlliance to Save Energy: ase.orgAmerican Council for an Energy-Efficient Economy: aceee.orgThe American Institute of Architects (AIA): aia.orgAssociated Builders and Contractors, inc. (ABC): abc.orgAssociated General Contractors of America (AGC): agc.orgBuilding Owners and Managers Association International (BOMA): boma.orgCarnegie Mellon University,

Center for the Building Performance and Diagnostics: arc.cmu.edu/cbpdDatabase for State Incentives for Renewable Energy (DSIRE): dsireusa.orgGreen Building Initiative: thegbi.orgNational Association of Counties (NACo): naco.orgSustainable Buildings Industry Council (SBIC): sbicouncil.orgUniversity of California, Berkeley,

Center for the Built Environment: cbe.berkeley.eduU.S. Conference of Mayors: mayors.orgU.S. Green Building Council: usgbc.org

OtherBuilding Green, LLC: buildinggreen.com

Main Website: construction.com

GreenSource: greensourcemag.com

Research & Analytics: construction.com/market_research

Achitectural Record: archrecord.com

Engineering News-Record: enr.com

Sweets: sweets.com

Green Reports: greensource.construction.com/resources/SmartMarket.asp

usa.siemens.com/industry■■

ulenvironment.com■■

ul.com■■

usgbc.org■■

Green Building Certification Institute: gbci.org■■

autodesk.com■■

autodesk.com/sustainabledesignguide■■

cbre.com■■

1335cvr.indd 2 10/16/09 6:27:11 PM

McGraw-Hill Construction 1 www.construction.com SmartMarket Reports

Harvey M. Bernstein, F.ASCE, LEED AP has been a leader in the engineering and construc-tion industry for over 30 years. He serves as Vice President of Global Thought Leadership and Business Development for MHC, where among other things, he has lead responsibility for MHC’s green building and thought leadership initiatives, including MHC’s first-ever landmark stud-ies on green construction and key market trends in the U.S. and globally. Bernstein was also one of the team members involved in launching MHC’s GreenSource magazine. Previously, Bernstein

served as President and CEO of the Civil Engineering Research Foundation. He has written numerous papers covering inno-vation and sustainability, and currently serves as a member of the Princeton University Civil and Environmental Engineering Advisory Council, the Harvard Joint Center for Housing Studies Policy Advisory Board, and as a visiting Professor with the University of Reading’s School of Construction Management and Engineering in England where he also serves on their Innovative Construction Research Centre Advisory Board. Bernstein has an

M.B.A. from Loyola College, an M.S. in engineering from Princ-eton University and a B.S. in civil engineering from the New Jersey Institute of Technology.

Michele A. Russo, LEED AP, has been working in environ-mental policy and communica-tions for 15 years. She currently serves as MHC’s Director of Green Content & Research Com-munications where she is respon-sible for helping direct the green content across MHC’s portfolio of products and services, includ-ing the management of MHC’s SmartMarket Report series.

Russo is also a contributor to The McGraw-Hill Companies’ corpo-rate initiatives around sustain-ability. Previously, she served as Executive Director of the Clean Beaches Council and Deputy Director of the National Pollution Prevention Roundtable. She has authored several articles around pollution prevention and toxics reduction and is a frequent speaker on green building trends and environmental policy. Russo has a B.S. in Chemical Engineer-ing from Cornell University and a Masters in Public Policy from Harvard University’s Kennedy School of Government.

Only 1.5–2.5% of the U.S. building stock is new each year. Additionally, many of the 4.4 million non-resi-dential buildings that make up this

space are highly inefficient and represent a prime opportunity for green building retrofits.

Therefore, we thought it was critical to investigate the share of the retrofit and renovation market that was green.

What we found is that growth in green ret-rofits is occuring more rapidly than growth in new green buildings. Today, green building comprises 5-9% of retrofit and renova-tion market activity by value—projected to grow to 20-30% in just five years.

Additionally, the trends revealed by the market research and qualitative case studies profiled in this report point to dramatic growth in the longer-term (10-20 years) as owners—both public and private—face mounting pressures to upgrade their build-ings to be green, and as tenants look for ways to improve satisfaction with and the perfor-mance of their building spaces.

Several key results:

86% of commercial building owners expect the ■■

green retrofit market to grow, with half expecting

it to increase 20% or more over just three years.

The downturn is encouraging adoption ■■

of energy- and water-efficient practices in

renovation projects.

70% of owners who have engaged in green retrofit ■■

or renovation activities are planning to continue

to do so for over 15% of future renovation projects;

24% will do so on over 60% of projects.

The fact that such high rates of future activity are reported—coupled with signif-icant government intervention—suggests tremendous market opportunity for industry players offering green building services and products. Not surprisingly, those products and services oriented around energy-efficiency, such as lighting and building controls, have the greatest opportunity.

For the first time, we also profiled over 20 projects (pages 40-64). We felt their inclusion was critical in order to provide qualitative insights to accompany the data. It became clear that though projects are unique in many ways, they all share one thing in common—quantifiable business benefits (demonstrated through energy and water bills and audits). In some cases, further paybacks were measured and reported, such as higher occupancy, rents and tenant satisfaction.

We are very pleased that Autodesk, Siemens and UL Environment, Inc. supported this study to help bring it to the market. We also thank our partners at CB Richard Ellis and the U.S. Green Building Council for helping this study come to light.

As always, we at MHC are committed to continuing to serve as the “voice of the industry,” creating a complete “network” of green building information, resources and expertise through our publications, analytics work, market research and Network database of construction projects and products.

For more information on the methodology, see page 38.

Introduction

Harvey M. BernsteinF.ASCE, LEED APVice PresidentGlobal Thought Leadership & Business DevelopmentMcGraw-Hill Construction

Michele A. RussoLEED APDirectorGreen Content & Research CommunicationsMcGraw-Hill Construction

SmartMarket ReportG

RE

EN

BU

ILd

ING

RE

TR

oFI

T A

Nd

RE

No

vA

TIo

N

table of

contents

SmartMarket Report

SmartMarket Reports McGraw-Hill Construction 2 www.construction.com

green building retrofit and renovation

4 Executive Summary

7 Data 7 sidebar green retrofit Market opportunity

8 Green Retrofit Market Activity 8 Level of Green Retrofit Activity 9 Future Growth of the Green Retrofit Market

10 Financing the Green Retrofit Market

11 sidebar eSCos and the green retrofit Market

12 Green Retrofit Market Profile 12 Age of Buildings Involved in Green Retrofit 12 Size of a Firm’s Green Retrofit Investment

14 Green Retrofit Business Benefits 14 Measuring Economic Impact 14 Expectation that Energy Cost Savings Will Be Recouped in 10 Years 15 Expected Decrease in Operating Costs 16 Expected Increase in Building Values from Green Retrofit Improvements 16 Expected Increase in ROI 17 Expected Time to Lease Green Retrofitted Space 17 Expected Increase in Overall Occupancy 17 Expected Rent Increase Due to Green Retrofits 18 Tenant Willingness to Pay a Premium for Green Retrofits 18 Importance of Green Retrofitting to Companies Leasing Space

19 sidebar Maximizing business benefits

20 Green Retrofit Market Intelligence 20 Business Motivations for Green Retrofits 21 Environmental and Social Motivations

23 sidebar Achieving Optimal Performance in Green Retrofit & Renovation Projects

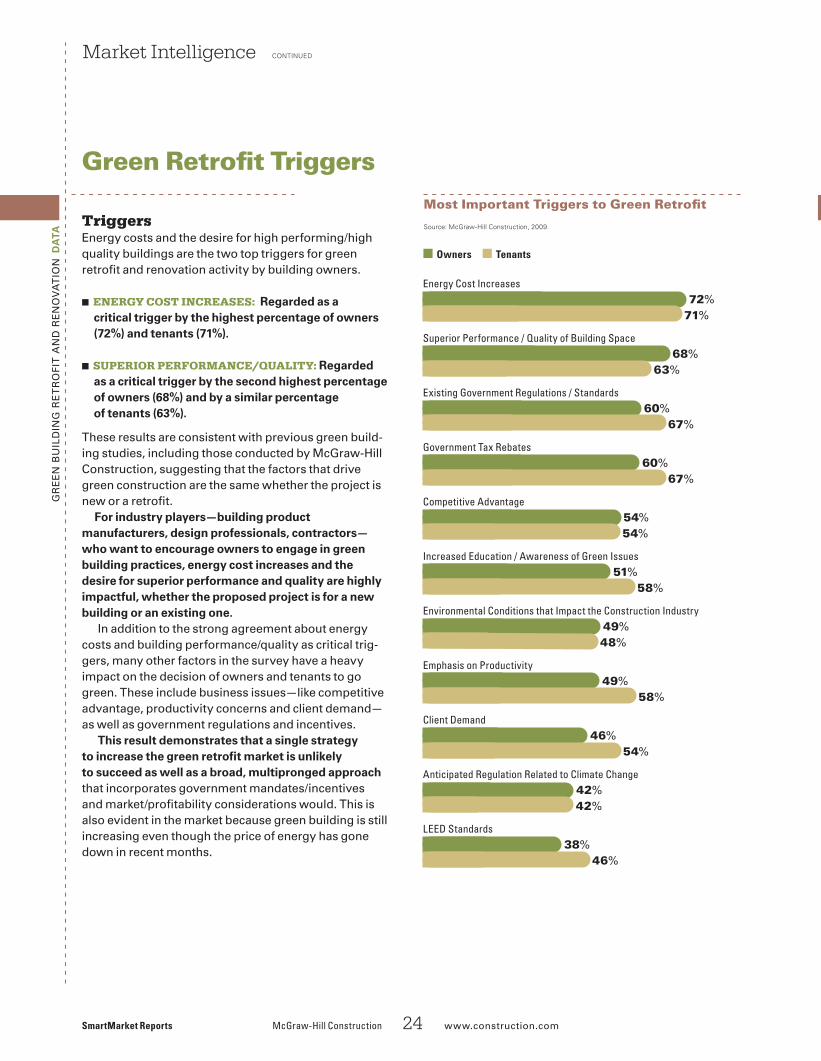

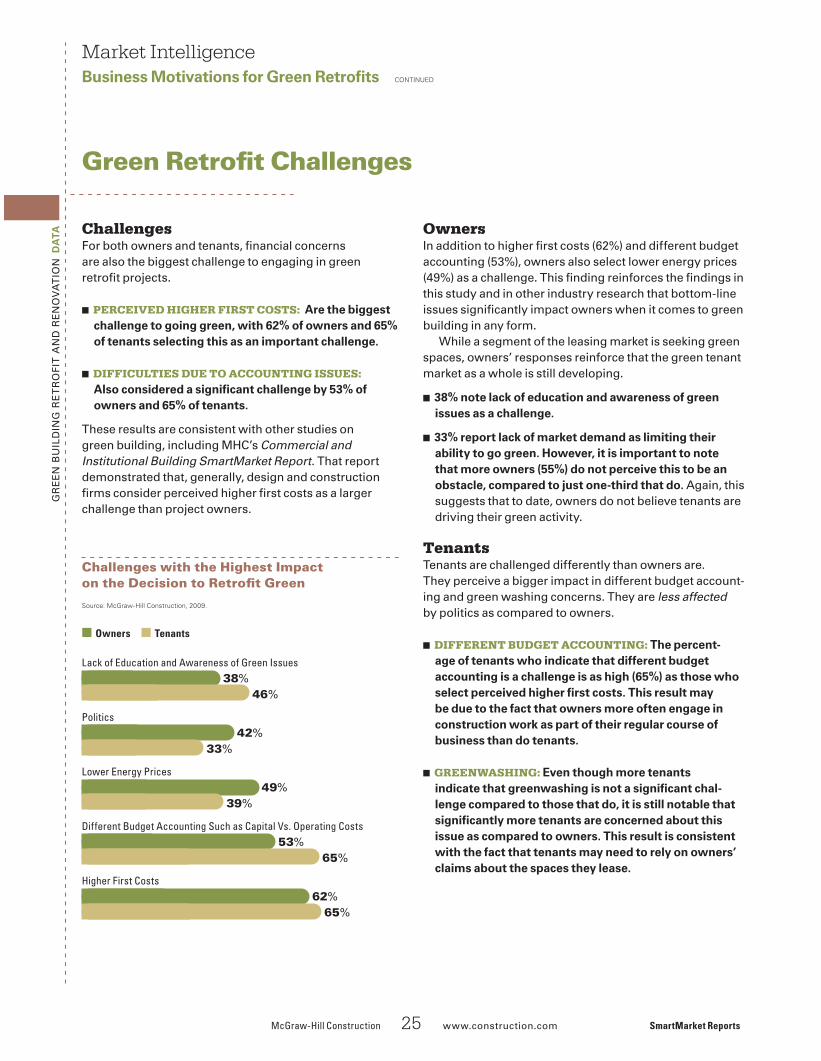

24 Green Retrofit Triggers 25 Green Retrofit Challenges

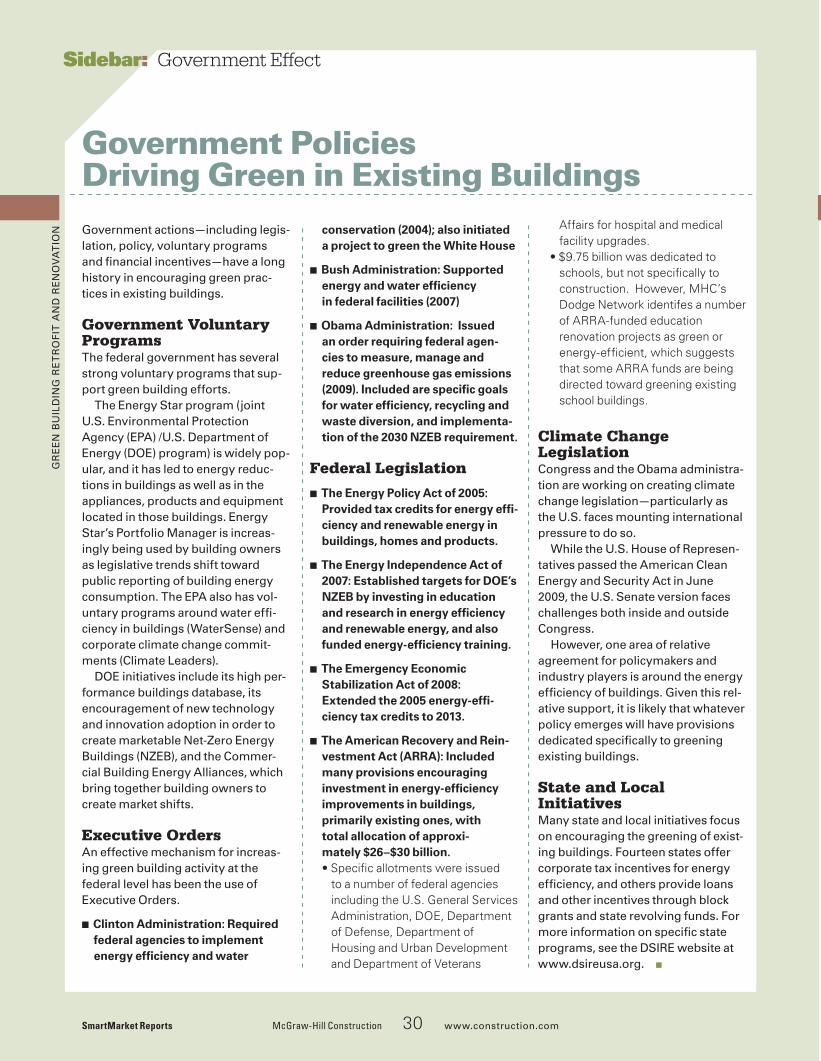

26 Government Effect on Green Retrofit 26 Attitudes about Green and Energy-Efficient Policies 26 Energy Audits 26 Job Creation 26 Stimulus Funding and the Energy-Efficient Market

27 sidebar green Jobs and training 28 Impact of the American Recovery and Reinvestment Act (ARRA) 29 Effectiveness of Government Incentives

30 sidebar government Policies driving green in existing buildings

efficiency

McGraw-Hill Construction 3 www.construction.com SmartMarket Reports

Clockwise from top left:Empire State Building, New York, NY; Armstrong Campus Corporate Headquarters, Lancaster, PA; Founding Farmers Restaurant, Washington, DC

GR

EE

n B

uIL

DIn

G R

ET

RO

FIT

An

D R

En

OV

AT

IOn

Co

nt

en

tS

31 Green Retrofit Practices 31 use of Green Consultants 31 Level of Green Retrofit Activities 32 Types of Green Retrofit Activities 33 Specific Green Retrofit Systems and Product Types

33 Energy-Efficient Mechanical Systems 33 Energy-Efficient Lighting 34 Occupancy Comfort 34 Other Product Systems and Types

35 Green Building Products

36 Performance Ratings and Green Certification

37 sidebar green retrofitting in the global Marketplace

38 Methodology

39 Case Studies 39 Case Study Trends

65 Resources

© E

MP

irE

STa

TE B

uiL

din

g, C

Ou

rTE

Sy

Of

JOn

ES

La

ng

La

Sa

LLE

(fa

r L

Ef

T);

© a

rM

STr

On

g W

Or

Ld in

du

STr

iES

(TO

P);

©

fO

un

din

g f

ar

ME

rS

(nE

ar

LE

fT

)

SmartMarket Reports McGraw-Hill Construction 4 www.construction.com

The results of this latest research, combined with McGraw-Hill Construction proprietary data, demonstrate a growing share for green building in the retrofit and renovation marketplace. Furthermore, market opinion as well as other government and market indicators suggest ongoing, dramatically higher activity in the longer term (10-20 years)—both for retrofit and renovation activity overall as well as for the green share.

Gr

ee

n b

uil

din

G r

eT

ro

FiT

an

d r

en

ov

aT

ion

With 76.9 billion square feet of existing building stock and a number of inefficient buildings, green building has a tremendous long-term opportunity to dramatically reduce U.S. energy consumption and greenhouse gas emissions.

Green Building Retrofit Market Poses Strong Growth Over Next 5 YearsThe growth in green building retrofit projects repre-sents significant opportunity for the industry.

2009Green building retrofit and renovation market ■■

share: 5–9% by value

Market opportunity for major projects (those over ■■

$1 million): $2.1–3.7 billion

2014Green building retrofit and renovation market ■■

share: 20–30% by value

Market opportunity for major projects (those over ■■

$1 million): $10.1–15.1 billion

More broadly, there is significant opportunity in the retrofit market for energy-efficient buildings—one aspect of a green building (see page 8). Currently, this market share is estimated at 66–75% by value and expected to grow to 85–95% in five years (see values in chart at top right).

Owners and Tenants with Green Retrofit Experience Are Likely to Do More Green Retrofit Projectsowners and tenants who have completed green retro-fit and renovation projects are likely to repeat that activity. Furthermore, level of involvment is strong.

70% of owners indicate that over 15% of the retrofit ■■

projects they have done or have planned are green.

24% are greening over 60% of their projects.■■

More tenants fall into the two extremes—One-third ■■

are committed to green retrofits for over 60% of their projects, while 17% are not yet commited.

Market SummaryGreen Retrofit and Renovation Pose Significant Future Market Opportunity for Green Building

■ Owners ■ Tenants

Exploring Whether or Not to Undertake a Green Retrofit (0%)

8%

17%

1–15% of Projects Were/Will Be Green Retrofit22%

25%

16–30% of Projects Were/Will Be Green Retrofit

32%

4%

31–60% of Projects Were/Will Be Green Retrofit

14%

21%

More than 60% of Projects Were/Will Be Green Retrofit

24%

33%

Current Level of Green Retrofit ActivitySource: McGraw-Hill Construction, 2009.

Green Retrofit Market Opportunity (nonresidential buildings), in billions of dollars

GReen BUILDInG

eneRGy effIcIency

GReen BUILDInG

eneRGy effIcIency

Source: McGraw-Hill Construction, 2009

$2.1 $3.7 billion

$27.2 $30.9

$10.1 $15.1 billion

$42.9 $47.9

2014

2009

■ Low ■ High■ ■

5% 9%

66% 75%

20% 30%

85% 95%

Continued

McGraw-Hill Construction 5 www.construction.com SmartMarket Reports

Gr

ee

n b

uil

din

G r

eT

ro

FiT

an

d r

en

ov

aT

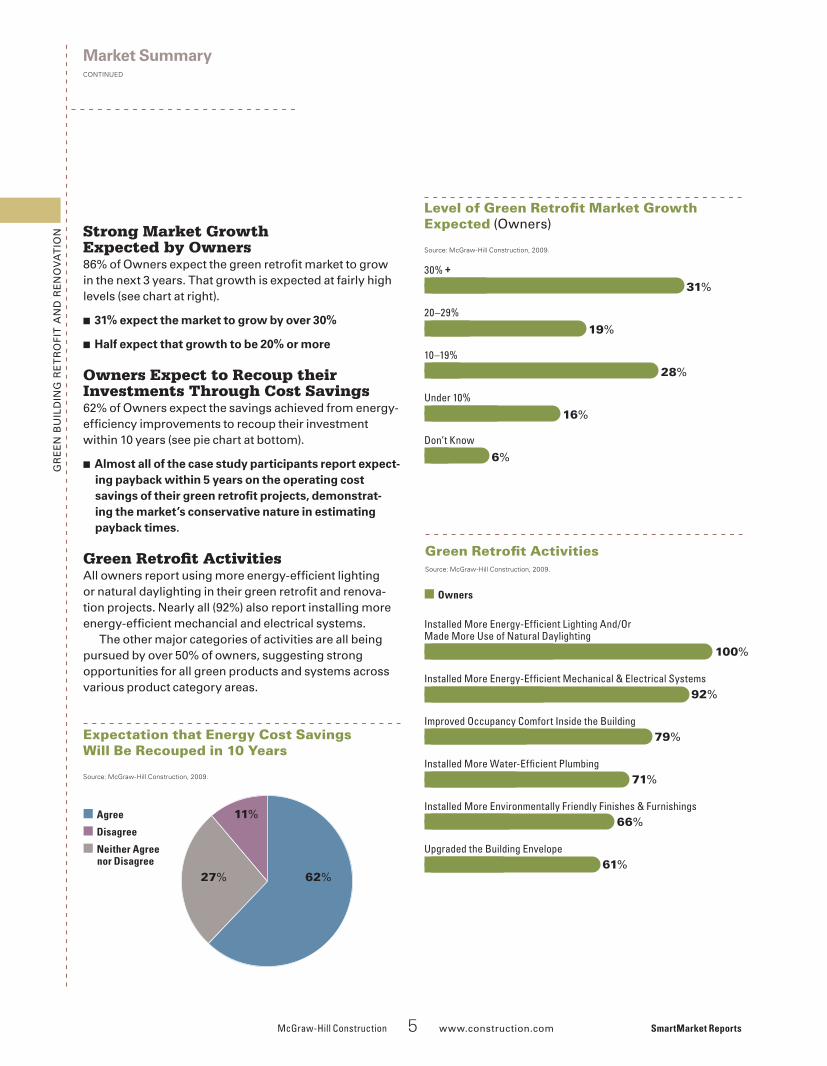

ion Strong Market Growth

Expected by Owners86% of owners expect the green retrofit market to grow in the next 3 years. That growth is expected at fairly high levels (see chart at right).

31% expect the market to grow by over 30%■■

Half expect that growth to be 20% or more■■

Owners Expect to Recoup their Investments Through Cost Savings62% of owners expect the savings achieved from energy-efficiency improvements to recoup their investment within 10 years (see pie chart at bottom).

Almost all of the case study participants report expect-■■

ing payback within 5 years on the operating cost savings of their green retrofit projects, demonstrat-ing the market’s conservative nature in estimating payback times.

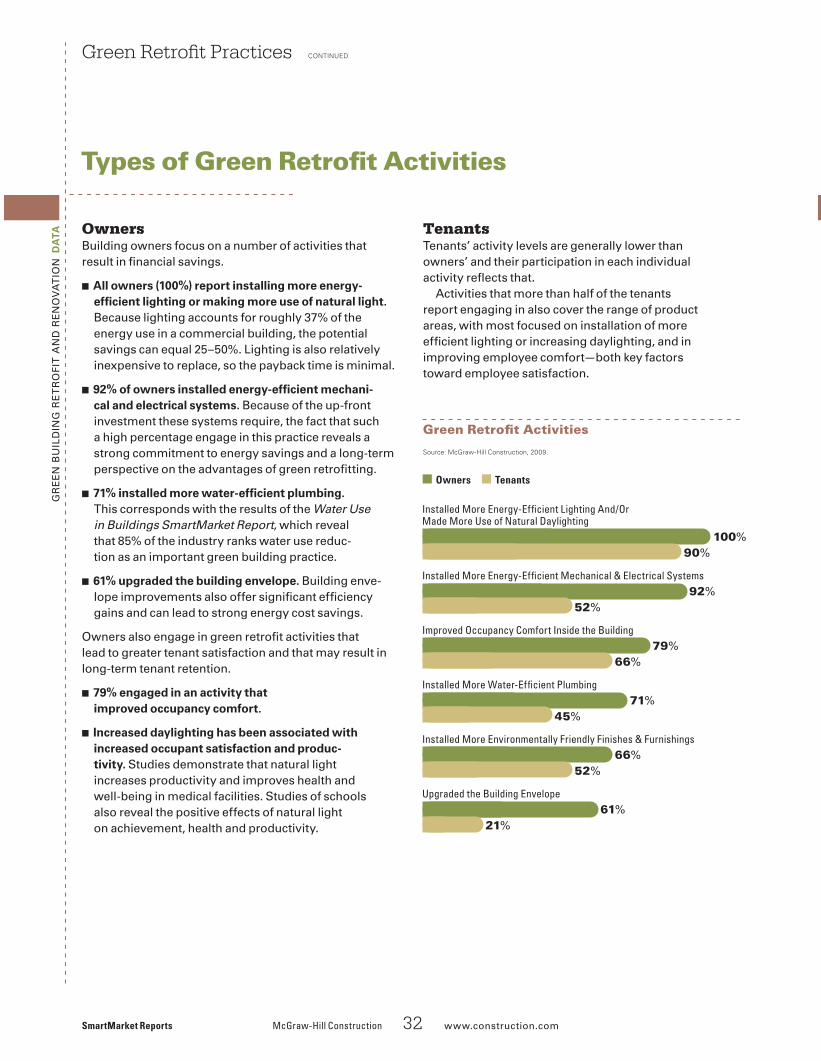

Green Retrofit Activitiesall owners report using more energy-efficient lighting or natural daylighting in their green retrofit and renova-tion projects. nearly all (92%) also report installing more energy-efficient mechancial and electrical systems.

The other major categories of activities are all being pursued by over 50% of owners, suggesting strong opportunities for all green products and systems across various product category areas.

Market SummaryContinued

30% +

31%

20–29%

19%

10–19%

28%

Under 10%

16%

Don’t Know

6%

Level of Green Retrofit Market Growth Expected (owners)

Source: McGraw-Hill Construction, 2009.

Expectation that Energy Cost Savings Will Be Recouped in 10 Years

Source: McGraw-Hill Construction, 2009.

■ Agree

■ Disagree

■ neither Agree nor Disagree

27%

11%

62%

■ Owners

Installed More Energy-Efficient Lighting And/Or Made More Use of Natural Daylighting

100%

Installed More Energy-Efficient Mechanical & Electrical Systems92%

Improved Occupancy Comfort Inside the Building79%

Installed More Water-Efficient Plumbing71%

Installed More Environmentally Friendly Finishes & Furnishings66%

Upgraded the Building Envelope61%

Green Retrofit ActivitiesSource: McGraw-Hill Construction, 2009.

SmartMarket Reports McGraw-Hill Construction 6 www.construction.com

Gr

ee

n b

uil

din

G r

eT

ro

FiT

an

d r

en

ov

aT

ion

MA

rk

et

Su

MM

Ar

y

Focus on Business Benefits and PaybacksFinancial benefits are the primary driver for encouraging owners and tenants to pursue green retrofits.

additionally, owners and tenants recognize that there are financial rewards they can reap from green building retrofit and renovation activities.

as a result, industry players, especially service providers and product manufacturers, need to be able to convey the business benefits of their green products and services. Product manufacturers and contractors should understand leed, since it still plays an important role in the market.

industry players should also foster relationships with owners and owner representatives. in the green retrofit market—especially for the plethora of smaller projects under $1 million—owners are making final decisions, or their consultants are. This is different from the new green building market where architects and designers wield significant influence.

Energy-Efficiency Reigns Supreme, but Other Motives Matterenergy-efficiency improvements offer the broadest opportunity in the current market, and given the specific attention being placed on curbing carbon emissions and reducing energy consumption, energy efficiency will continue to be a requirement for green renovation activity. in fact, we believe it will be embedded into all retrofit activity in coming years.

However, green building retrofits include more than just features that improve energy performance. and those additional advantages are appealing—not only do they yield financial rewards, but they also are accompanied by environmental and social paybacks that can, in certain circumstances, be as powerful as money. This is especially true of owners of education and healthcare buildings.

industry players should not confine themselves to thinking about green in water and energy-saving terms. instead, they should be able to speak to the larger gains green offers.

Measurement MattersThere is a noticeable lack of sufficient measurements of the benefits achieved in green retrofits reported by owners and tenants. Furthermore, as policy continues to focus around public reporting, building owners that don’t have systems in place to effective measure their performance—minimally as it relates to energy and water—will lag in the market and ultimate find it costs them significant money to not have these systems in place.

Major opportunities exist for those who can help owners and tenants capture the data they need to find inefficiencies, establish appropriate benchmarks and set long-term goals.

Current Technologies Can Yield Major Benefitsone theme running through many of the case studies was the big boost available from off-the-shelf technologies. Contractors and building product manufacturers need to be able to effectively convey what can be achieved today for minimal investment.

Once a Firm Conducts a Green Retrofit or Renovation, They Are Likely to Do It Againowners and tenants who have completed green retrofit and renovation proj-ects are likely to repeat that activity. as such, they can be a focal point for green building product manufac-turers and service providers as their receptivity to green expertise is highly likely.

Expand and Promote Your Green Building KnowledgeFirms are embracing com-mitments to sustainability. This trend is supported by the emergence of the new Chief Sustainability officer position at large corpora-tions, expansion of large green building portfolio commitments and increas-ing investment in bringing new and innovative prod-ucts to market that have environmentally, fiscally and socially beneficial properties.

as a result, industry players that have knowl-edge about green building trends—particularly as they relate to existing build-ings will be well-positioned for future personal profes-sional growth. ■

Recommendations

Key Conclusions and Recommendations

There is tremendous opportunity in the existing building market for green building products, processes and services. Through strategic planning, preparation and initiatives, industry players of all types can maximize this expanding retrofit market, and the growing share that is green.

McGraw-Hill Construction 7 www.construction.com SmartMarket Reports

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

Green Retrofit Market OpportunityThe market opportunity for green building has grown dramatically— in both new and existing buildings. By 2014, the green building market share of all retrofit, alterations and renovation activity is expected to be 20%–30% by value.

Existing Buildings Todaythe current u.S. built environment is comprised of 76.9 billion sq. ft.1, including over 4.4 million nonresi-dential buildings2. in comparison, only 1.8% of this was new in 2008.3

today’s building stock also includes some extremely inefficient buildings. as can be seen below, buildings constructed after 1970 consume significantly more energy per square foot as compared to older buildings. given that they comprise 60% of the building stock, there exists strong opportunity for green.

in 2009, the value of the overall major retrofit and alteration market (projects over $1 million) is fore-cast to be $41.2 billion. it is expected to grow to over $50 billion by 20144.

However, because the renovation market also includes thousands of small projects not captured in this value, the full renovation market is likely 1.5 to 2 times higher.

Green Building Retrofitstoday, we project the green share (see page 8 for definition) of the retro-fit and renovation market to be 5–9% by value—equating to a $2–4 billion marketplace for major projects.

by 2014, that share is expected to increase to 20–30%—a $10–15 billion market for major retrofit projects.

More broadly, we expect an over-whelming amount of the retrofit market to pose an opportunity for energy efficiency since the nature of a retrofit or renovation project is to

create a higher performing building. today, that market is expected to be 66-75% of retrofit activity, growing to comprise 85–95% by 2014.

dramatic increases in green retrofit activity is expected over the longer-term (10–15 years) after major legislative and competitive drivers force building owners to engage in retrofit projects (most notably to address climate change). this will significantly increase both the base of all retrofit activity as well as the green share, which by then, is expected to have reached its tipping point.

the sectors with the largest green retrofit opportunity are education and office (~50% of all retrofit activity), with the biggest growth in retail. ■

Sidebar: Market Activity

1 McGraw-Hill Construction Building Stock Database (2009, data through end of 2008); 2 U. S. Department of Energy, Energy Information Administration, 2006; 3 McGraw-Hill Construction Building Stock Database (2009, data through end of 2008); 4 Construction Market Forecasting Service, McGraw-Hill Construction as of October 2009

Energy Use in Buildings by Age (thousand btu/sq. ft.)Source: U.S. Department of Energy, Energy Information Administration, 2006.

Before 1920

72.651920–1945

94.921946 –1959

101.781960–1969

122.751970–1979

163.521980–1989

186.331990–1999

166.822000–2003

166.82

nuMber of buildingS

318,000

499,000

541,000

571,000

700,000

668,000

809,000

298,000

Green Retrofit Market Opportunity (nonresidential buildings), in billions of dollars

GReen BUILDInG

eneRGy effIcIency

GReen BUILDInG

eneRGy effIcIency

Source: McGraw-Hill Construction, 2009

$2.1 $3.7 billion

$27.2 $30.9

$10.1 $15.1 billion

$42.9 $47.9

2014

2009

■ Low ■ High■ ■

5% 9%

66% 75%

20% 30%

85% 95%

SmartMarket Reports McGraw-Hill Construction 8 www.construction.com

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta The greatest opportunity for green design and construction activity lies not in constructing new green buildings, but in engaging in the retrofit and renovation of the existing build-ing stock. recent legislation has focused on increasing energy

efficiency in existing buildings (see page 30), but a true green retro-fit addresses more than energy performance. in fact, green approaches to retrofit and renovation projects lead to a multitude of benefits: lower energy use, reduced greenhouse gas emissions, water savings and better indoor environmental quality.

this study focuses on the attitudes and behaviors of commercial building owners and tenants who had already committed to doing green retrofits before many of the major incentives—from the american recovery and reinvestment act to potential incentives from climate legislation—were known or available. therefore, the results reveal what drives the private sector to embrace green retrofits, what benefits they expect to receive and where they think this market is going in the future.

Note About the Data The sample of build-ing owners who have done or will do a green retrofit interviewed in this survey is statisti-cally valid. However, the sample size of ten-ants who qualified was smaller. Findings and con-clusions about build-ing owner opinions are considered quan-titative, while inter-pretations of tenant behavior are qualita-tive in nature.

For full methodology, see page 38.

Owners who engage in green retrofit and renovation* activity tend to do so for multiple projects—70% of owners who have done or are planning to do a green retrofit project state that 16% or more of their projects are green retrofits. furthermore, nearly a quarter of owners (24%) engaging in retrofit activity report that more than 60% of those projects are green.

this finding suggests that building owners undertake green retrofit and renovation projects in a holistic fashion, rather than just doing one or two showcase green projects.

on the other hand, tenants appear to fall at either the high or low end in terms of level of green retrofit activity.

33% highly dedicated to making the majority (more than ■■

60%) of retrofit projects green

17% not yet committed■■

* a “green” project is one that employs multiple practices, prod-ucts and processes covering a minimum of three out of five aspects of green building—energy, water or resource efficiency, improved indoor environmental quality or responsible site management.

■ Owners ■ Tenants

Exploring Whether or Not to Undertake a Green Retrofit (0%)

8%

17%

1–15% of Projects Were/Will Be Green Retrofit22%

25%

16–30% of Projects Were/Will Be Green Retrofit

32%

4%

31–60% of Projects Were/Will Be Green Retrofit

14%

21%

More than 60% of Projects Were/Will Be Green Retrofit

24%

33%

Current Level of Green Retrofit Activity

Source: McGraw-Hill Construction, 2009.

IntroductionData:

Level of Green Retrofit Activity

Market Activity

McGraw-Hill Construction 9 www.construction.com SmartMarket Reports

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta Eighty-six percent of building owners expect the U.S. commercial green retrofit market to grow. out of the remaining 14%, no building owners expect the market to decline—all believe it will at least remain stable.

once again, this finding confirms the expected growth of the green building market reported in The Green Outlook, Commercial & Institutional Green Building SmartMarket Report and other industry studies. additionally, it demonstrates that this growth applies not only to new construction, but also to retrofits and renovations of existing buildings.

those building owners who expect growth in the green retrofit market anticipate strong levels of growth: 50% expect an increase of 20% or more.

as a group, building owners—especially those with a portfolio of buildings—are more likely to have active

construction projects on a regular basis than tenants, making their expected growth levels noteworthy.

the overwhelming agreement that the green retrofit market is increasing, coupled with its high rate of expected growth, is particularly notable in the midst of the current economic downturn. Strong growth in green retrofit and renovation activity is predicted by the majority of building owners despite the many downward pressures on overall construction due to today’s economy.

these results provide a clear signal to the industry—particularly product manufacturers—that green will play an important role in the future design and construction of renovations and retrofits of existing buildings. accordingly, the industry should include these considerations in their business planning.

COntInUED

Sizing the Commercial Green Retrofit MarketA qualitative indicator of the level of adoption of commercial green retrofit projects is the incidence of building owners and tenants who qualified to be part of the study out of the overall population contacted. That incidence was 10%, which does cor-respond to the overall market size project-sion across all build-ings types on page 7.

50% +

16%

40–49%

6%

30–39%

9%

20–29%

19%

10–19%

28%

Under 10%

16%

Don’t Know

6%

Market will…

grow

86%remain stable

14%

Future Growth of the Green Retrofit Market

U.S. Commercial Green Retrofit Market(owner projections for the next 3 years)

Source: McGraw-Hill Construction, 2009.

Level of Green Retrofit Market Growth Expected (owners)

Source: McGraw-Hill Construction, 2009.

SmartMarket Reports McGraw-Hill Construction 10 www.construction.com

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

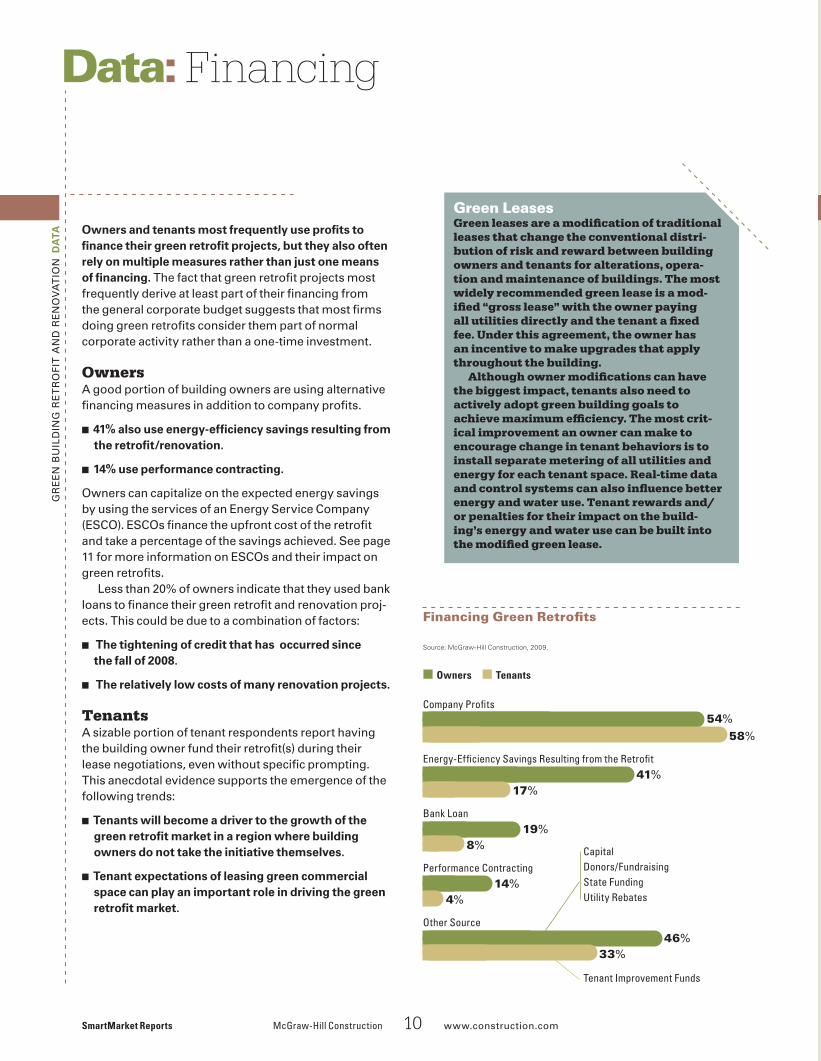

ta Owners and tenants most frequently use profits to finance their green retrofit projects, but they also often rely on multiple measures rather than just one means of financing. the fact that green retrofit projects most frequently derive at least part of their financing from the general corporate budget suggests that most firms doing green retrofits consider them part of normal corporate activity rather than a one-time investment.

Ownersa good portion of building owners are using alternative financing measures in addition to company profits.

41% also use energy-efficiency savings resulting from ■■

the retrofit/renovation.

14% use performance contracting.■■

owners can capitalize on the expected energy savings by using the services of an energy Service Company (eSCo). eSCos finance the upfront cost of the retrofit and take a percentage of the savings achieved. See page 11 for more information on eSCos and their impact on green retrofits.

less than 20% of owners indicate that they used bank loans to finance their green retrofit and renovation proj-ects. this could be due to a combination of factors:

the tightening of credit that has occurred since ■■

the fall of 2008.

the relatively low costs of many renovation projects.■■

Tenantsa sizable portion of tenant respondents report having the building owner fund their retrofit(s) during their lease negotiations, even without specific prompting. this anecdotal evidence supports the emergence of the following trends:

tenants will become a driver to the growth of the ■■

green retrofit market in a region where building owners do not take the initiative themselves.

tenant expectations of leasing green commercial ■■

space can play an important role in driving the green retrofit market.

FinancingData:

Financing Green Retrofits

Source: McGraw-Hill Construction, 2009.

■ Owners ■ Tenants

Company Profits

54%

58%

Energy-Efficiency Savings Resulting from the Retrofit41%

17%

Bank Loan

19%

8%

Performance Contracting

14%

4%

Other Source

46%

33%

CapitalDonors/FundraisingState FundingUtility Rebates

Tenant Improvement Funds

Green LeasesGreen leases are a modification of traditional leases that change the conventional distri-bution of risk and reward between building owners and tenants for alterations, opera-tion and maintenance of buildings. The most widely recommended green lease is a mod-ified “gross lease” with the owner paying all utilities directly and the tenant a fixed fee. Under this agreement, the owner has an incentive to make upgrades that apply throughout the building.

Although owner modifications can have the biggest impact, tenants also need to actively adopt green building goals to achieve maximum efficiency. The most crit-ical improvement an owner can make to encourage change in tenant behaviors is to install separate metering of all utilities and energy for each tenant space. Real-time data and control systems can also influence better energy and water use. Tenant rewards and/or penalties for their impact on the build-ing’s energy and water use can be built into the modified green lease.

McGraw-Hill Construction 11 www.construction.com SmartMarket Reports

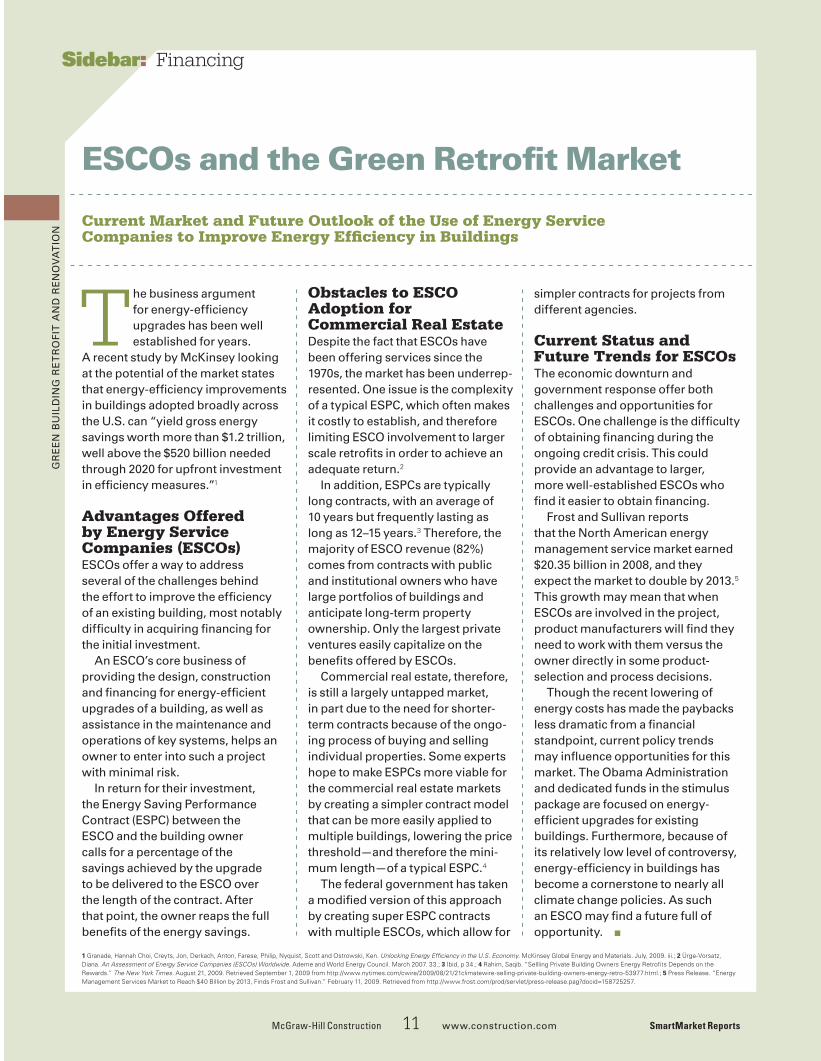

ESCOs and the Green Retrofit Market

Current Market and Future Outlook of the Use of Energy Service Companies to Improve Energy Efficiency in Buildings

The business argument for energy-efficiency upgrades has been well established for years.

a recent study by McKinsey looking at the potential of the market states that energy-efficiency improvements in buildings adopted broadly across the u.S. can “yield gross energy savings worth more than $1.2 trillion, well above the $520 billion needed through 2020 for upfront investment in efficiency measures.”1

Advantages Offered by Energy Service Companies (ESCOs)eSCos offer a way to address several of the challenges behind the effort to improve the efficiency of an existing building, most notably difficulty in acquiring financing for the initial investment.

an eSCo’s core business of providing the design, construction and financing for energy-efficient upgrades of a building, as well as assistance in the maintenance and operations of key systems, helps an owner to enter into such a project with minimal risk.

in return for their investment, the energy Saving Performance Contract (eSPC) between the eSCo and the building owner calls for a percentage of the savings achieved by the upgrade to be delivered to the eSCo over the length of the contract. after that point, the owner reaps the full benefits of the energy savings.

Obstacles to ESCO Adoption for Commercial Real Estatedespite the fact that eSCos have been offering services since the 1970s, the market has been underrep-resented. one issue is the complexity of a typical eSPC, which often makes it costly to establish, and therefore limiting eSCo involvement to larger scale retrofits in order to achieve an adequate return.2

in addition, eSPCs are typically long contracts, with an average of 10 years but frequently lasting as long as 12–15 years.3 therefore, the majority of eSCo revenue (82%) comes from contracts with public and institutional owners who have large portfolios of buildings and anticipate long-term property ownership. only the largest private ventures easily capitalize on the benefits offered by eSCos.

Commercial real estate, therefore, is still a largely untapped market, in part due to the need for shorter- term contracts because of the ongo-ing process of buying and selling individual properties. Some experts hope to make eSPCs more viable for the commercial real estate markets by creating a simpler contract model that can be more easily applied to multiple buildings, lowering the price threshold—and therefore the mini-mum length—of a typical eSPC.4

the federal government has taken a modified version of this approach by creating super eSPC contracts with multiple eSCos, which allow for

simpler contracts for projects from different agencies.

Current Status and Future Trends for ESCOsthe economic downturn and government response offer both challenges and opportunities for eSCos. one challenge is the difficulty of obtaining financing during the ongoing credit crisis. this could provide an advantage to larger, more well-established eSCos who find it easier to obtain financing.

frost and Sullivan reports that the north american energy management service market earned $20.35 billion in 2008, and they expect the market to double by 2013.5

this growth may mean that when eSCos are involved in the project, product manufacturers will find they need to work with them versus the owner directly in some product-selection and process decisions.

though the recent lowering of energy costs has made the paybacks less dramatic from a financial standpoint, current policy trends may influence opportunities for this market. the obama administration and dedicated funds in the stimulus package are focused on energy-efficient upgrades for existing buildings. furthermore, because of its relatively low level of controversy, energy-efficiency in buildings has become a cornerstone to nearly all climate change policies. as such an eSCo may find a future full of opportunity. ■

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

Sidebar: Financing

1 Granade, Hannah Choi, Creyts, Jon, Derkach, Anton, Farese, Philip, nyquist, Scott and Ostrowski, Ken. Unlocking Energy Efficiency in the U.S. Economy. McKinsey Global Energy and Materials. July, 2009. iii.; 2 Ürge-Vorsatz, Diana. An Assessment of Energy Service Companies (ESCOs) Worldwide. Ademe and World Energy Council. March 2007. 33.; 3 Ibid, p 34.; 4 Rahim, Saqib. “Sellling Private Building Owners Energy Retrofits Depends on the Rewards.” The New York Times. August 21, 2009. Retrieved September 1, 2009 from http://www.nytimes.com/cwire/2009/08/21/21climatewire-selling-private-building-owners-energy-retro-53977.html.; 5 Press Release. “Energy Management Services Market to Reach $40 Billion by 2013, Finds Frost and Sullivan.” February 11, 2009. Retrieved from http://www.frost.com/prod/servlet/press-release.pag?docid=158725257.

SmartMarket Reports McGraw-Hill Construction 12 www.construction.com

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta

8%

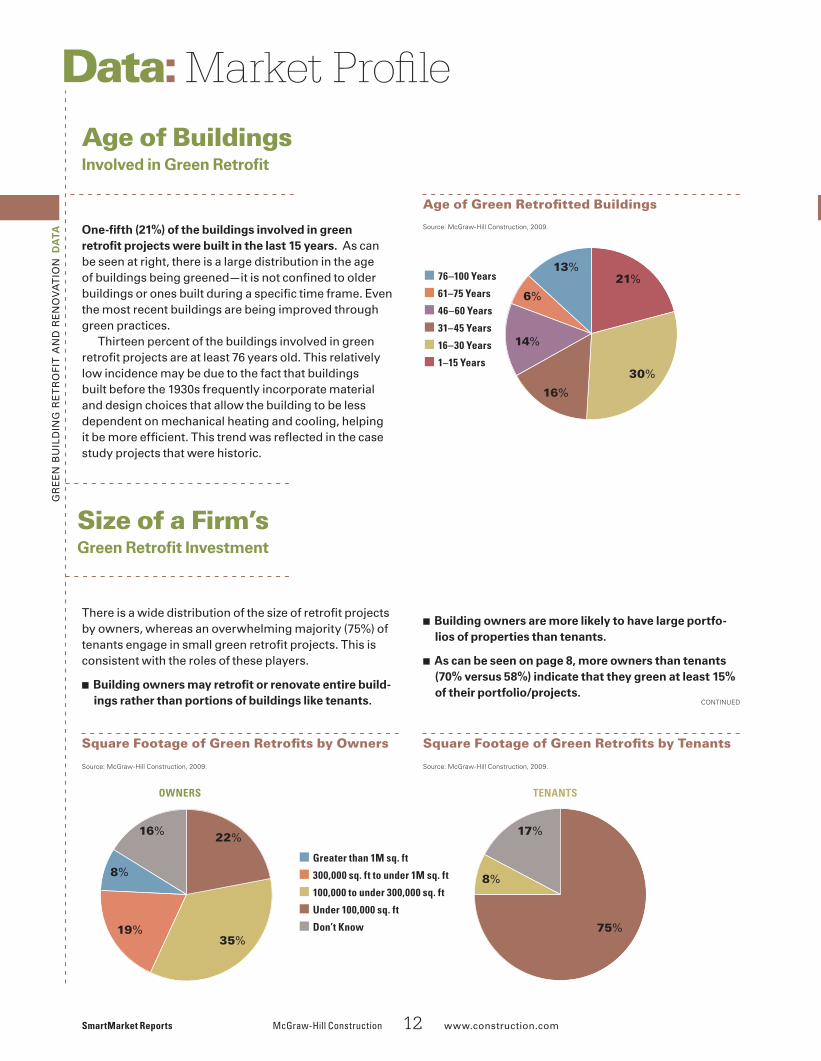

One-fifth (21%) of the buildings involved in green retrofit projects were built in the last 15 years. as can be seen at right, there is a large distribution in the age of buildings being greened—it is not confined to older buildings or ones built during a specific time frame. even the most recent buildings are being improved through green practices.

thirteen percent of the buildings involved in green retrofit projects are at least 76 years old. this relatively low incidence may be due to the fact that buildings built before the 1930s frequently incorporate material and design choices that allow the building to be less dependent on mechanical heating and cooling, helping it be more efficient. this trend was reflected in the case study projects that were historic.

Market ProfileData: Age of Buildings Involved in Green Retrofit

there is a wide distribution of the size of retrofit projects by owners, whereas an overwhelming majority (75%) of tenants engage in small green retrofit projects. this is consistent with the roles of these players.

Building owners may retrofit or renovate entire build-■■

ings rather than portions of buildings like tenants.

Age of Green Retrofitted Buildings

Source: McGraw-Hill Construction, 2009.

■ 76–100 years

■ 61–75 years

■ 46–60 years

■ 31–45 years

■ 16–30 years

■ 1–15 years30%

21%

16%

14%

13%

6%

■ Greater than 1M sq. ft

■ 300,000 sq. ft to under 1M sq. ft

■ 100,000 to under 300,000 sq. ft

■ Under 100,000 sq. ft

■ Don’t Know35%

22%

19%

16%

8%

17%

75%

Building owners are more likely to have large portfo-■■

lios of properties than tenants.

as can be seen on page 8, more owners than tenants ■■

(70% versus 58%) indicate that they green at least 15% of their portfolio/projects.

Size of a Firm’s Green Retrofit Investment

Square Footage of Green Retrofits by Owners

Source: McGraw-Hill Construction, 2009.

Square Footage of Green Retrofits by Tenants

OWneRS TenanTS

COntInUED

Source: McGraw-Hill Construction, 2009.

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta

McGraw-Hill Construction 13 www.construction.com SmartMarket Reports

Market ProfileSize of a Firm’s Green Retrofit Investment COntInUED

■ $10M or more

■ $5M to under $10M

■ $1M to under $5M

■ $500K to under $1M

■ $100K to under $500K

■ $50K to under $100K

■ Don’t Know/Refused

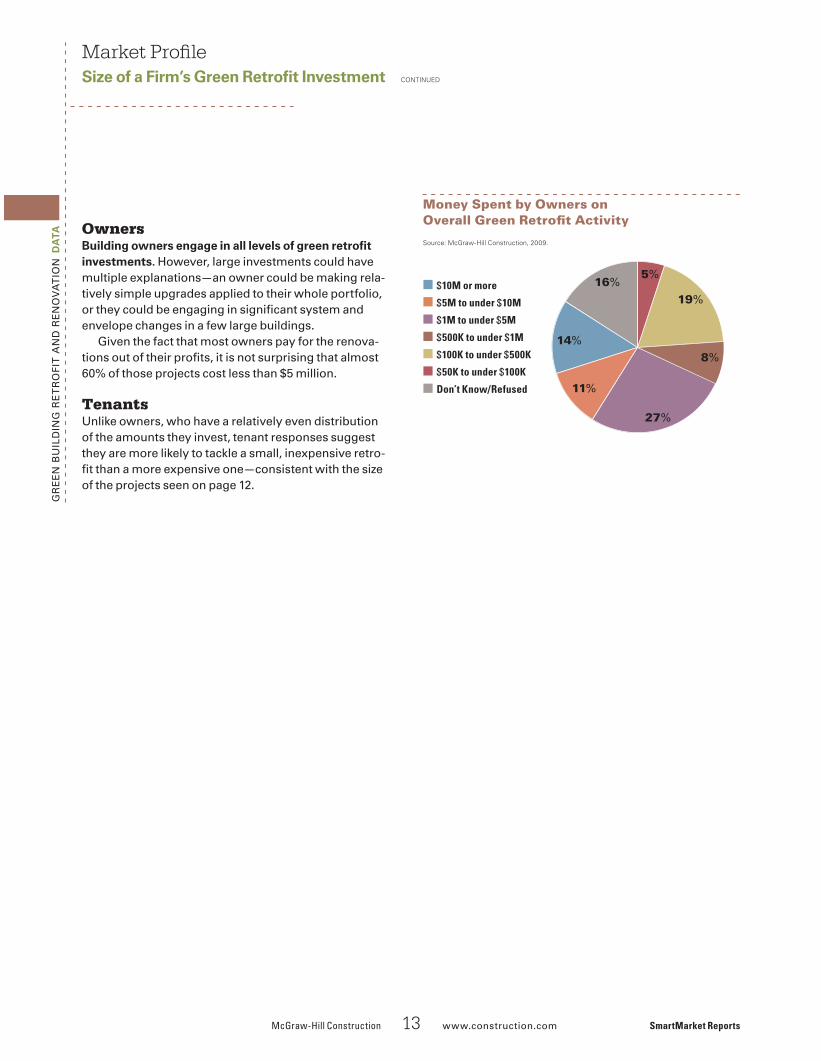

Money Spent by Owners on Overall Green Retrofit Activity

Source: McGraw-Hill Construction, 2009.

19%16%

11%

8%

5%

14%

27%

OwnersBuilding owners engage in all levels of green retrofit investments. However, large investments could have multiple explanations—an owner could be making rela-tively simple upgrades applied to their whole portfolio, or they could be engaging in significant system and envelope changes in a few large buildings.

given the fact that most owners pay for the renova-tions out of their profits, it is not surprising that almost 60% of those projects cost less than $5 million.

Tenantsunlike owners, who have a relatively even distribution of the amounts they invest, tenant responses suggest they are more likely to tackle a small, inexpensive retro-fit than a more expensive one—consistent with the size of the projects seen on page 12.

SmartMarket Reports McGraw-Hill Construction 14 www.construction.com

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta

capital expenses versus budgets to cover operating costs. in fact, over 50% of those surveyed identify this as a challenge to doing a green retrofit project (see page 25).

another issue may be that building owners are engaging in retrofit and renovation projects to improve tenant satisfaction, which is difficult to measure. further-more, because benefits may pass directly to tenants in some instances, those owners may choose not to measure the impacts.

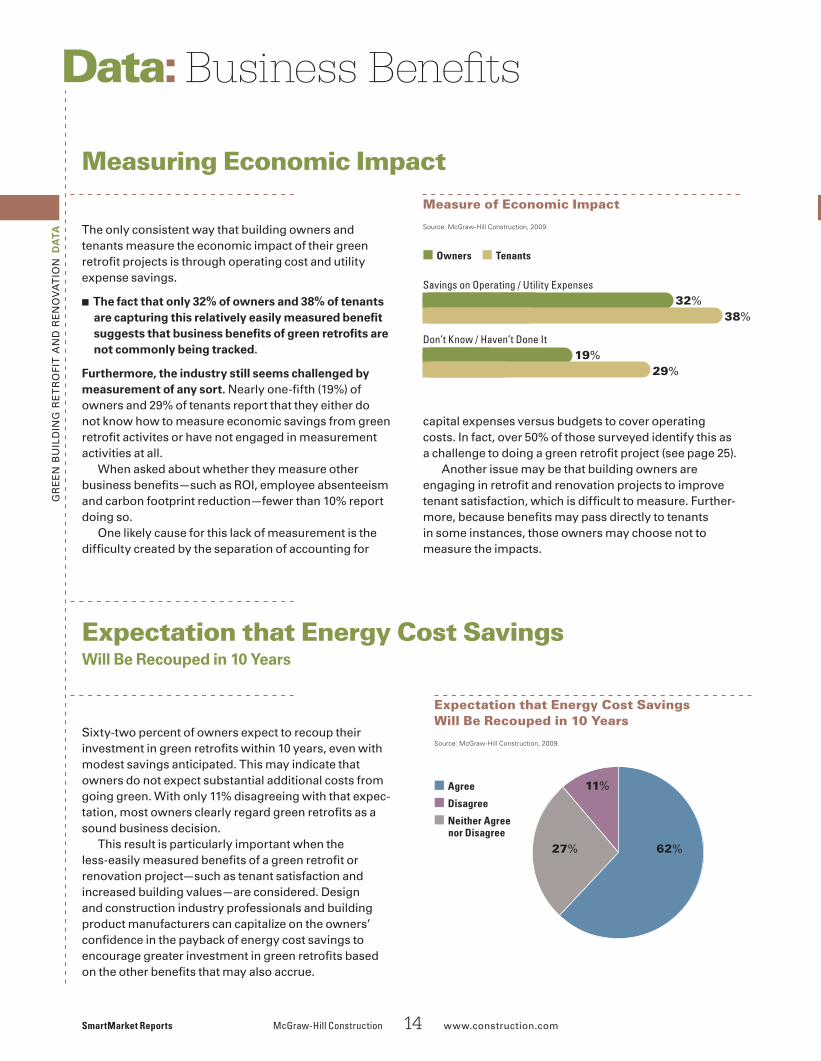

the only consistent way that building owners and tenants measure the economic impact of their green retrofit projects is through operating cost and utility expense savings.

the fact that only 32% of owners and 38% of tenants ■■

are capturing this relatively easily measured benefit suggests that business benefits of green retrofits are not commonly being tracked.

Furthermore, the industry still seems challenged by measurement of any sort. nearly one-fifth (19%) of owners and 29% of tenants report that they either do not know how to measure economic savings from green retrofit activites or have not engaged in measurement activities at all.

When asked about whether they measure other business benefits—such as roi, employee absenteeism and carbon footprint reduction—fewer than 10% report doing so.

one likely cause for this lack of measurement is the difficulty created by the separation of accounting for

Measuring Economic Impact

Business BenefitsData:

Measure of Economic Impact

Source: McGraw-Hill Construction, 2009.

■ Owners ■ Tenants

Savings on Operating / Utility Expenses32%

38%

Don’t Know / Haven’t Done It

19%

29%

Expectation that Energy Cost Savings Will Be Recouped in 10 Years

Sixty-two percent of owners expect to recoup their investment in green retrofits within 10 years, even with modest savings anticipated. this may indicate that owners do not expect substantial additional costs from going green. With only 11% disagreeing with that expec-tation, most owners clearly regard green retrofits as a sound business decision.

this result is particularly important when the less-easily measured benefits of a green retrofit or renovation project—such as tenant satisfaction and increased building values—are considered. design and construction industry professionals and building product manufacturers can capitalize on the owners’ confidence in the payback of energy cost savings to encourage greater investment in green retrofits based on the other benefits that may also accrue.

Expectation that Energy Cost Savings Will Be Recouped in 10 Years

Source: McGraw-Hill Construction, 2009.

■ agree

■ Disagree

■ neither agree nor Disagree

27%

11%

62%

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta

McGraw-Hill Construction 15 www.construction.com SmartMarket Reports

Business BenefitsExpected decrease in Operating Costs COntInUED

Expected Decrease in Operating Costs

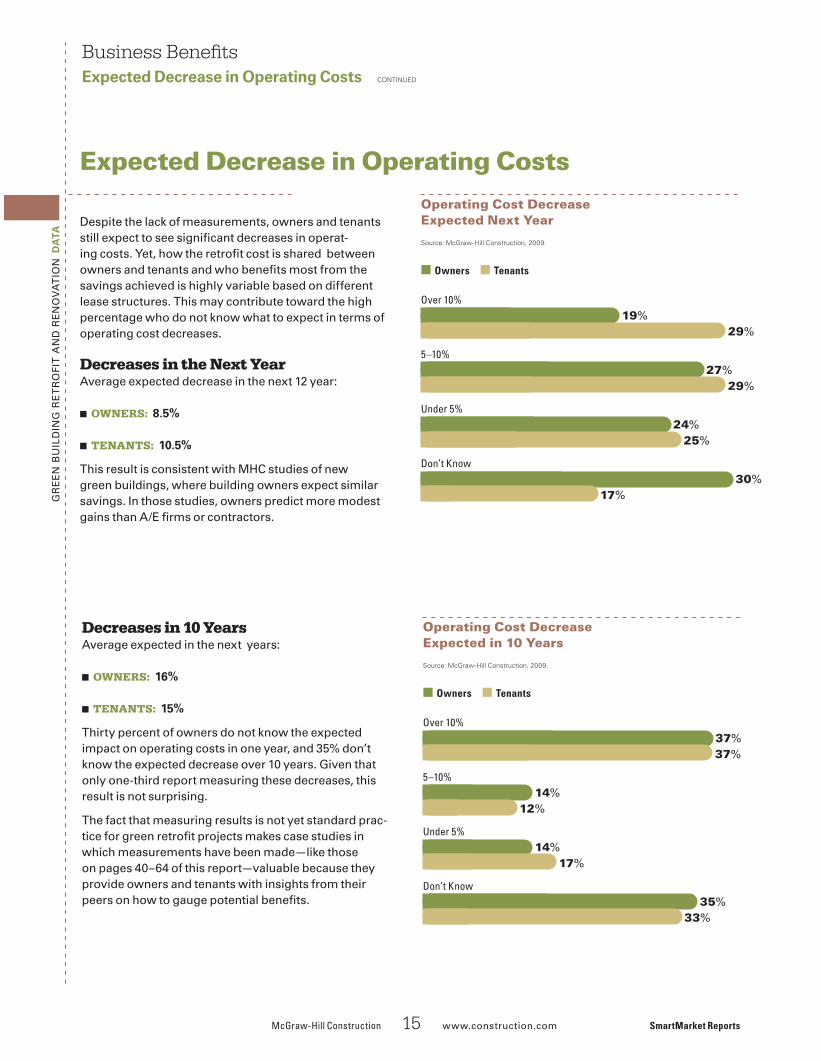

despite the lack of measurements, owners and tenants still expect to see significant decreases in operat-ing costs. Yet, how the retrofit cost is shared between owners and tenants and who benefits most from the savings achieved is highly variable based on different lease structures. this may contribute toward the high percentage who do not know what to expect in terms of operating cost decreases.

Decreases in the Next Yearaverage expected decrease in the next 12 year:

OwNeRs: ■■ 8.5%

TeNANTs: ■■ 10.5%

this result is consistent with MHC studies of new green buildings, where building owners expect similar savings. in those studies, owners predict more modest gains than a/e firms or contractors.

Operating Cost Decrease Expected Next Year

Source: McGraw-Hill Construction, 2009.

■ Owners ■ Tenants

Over 10%19%

29%

5–10%27%

29%

Under 5%24%

25%

Don’t Know

30%

17%

Decreases in 10 Yearsaverage expected in the next years:

OwNeRs:■■ 16%

TeNANTs: ■■ 15%

thirty percent of owners do not know the expected impact on operating costs in one year, and 35% don’t know the expected decrease over 10 years. given that only one-third report measuring these decreases, this result is not surprising.

the fact that measuring results is not yet standard prac-tice for green retrofit projects makes case studies in which measurements have been made—like those on pages 40–64 of this report—valuable because they provide owners and tenants with insights from their peers on how to gauge potential benefits.

Operating Cost Decrease Expected in 10 Years

Source: McGraw-Hill Construction, 2009.

■ Owners ■ Tenants

Over 10%37%

37%

5–10%14%

12%

Under 5%14%

17%

Don’t Know

35%

33%

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta

SmartMarket Reports McGraw-Hill Construction 16 www.construction.com

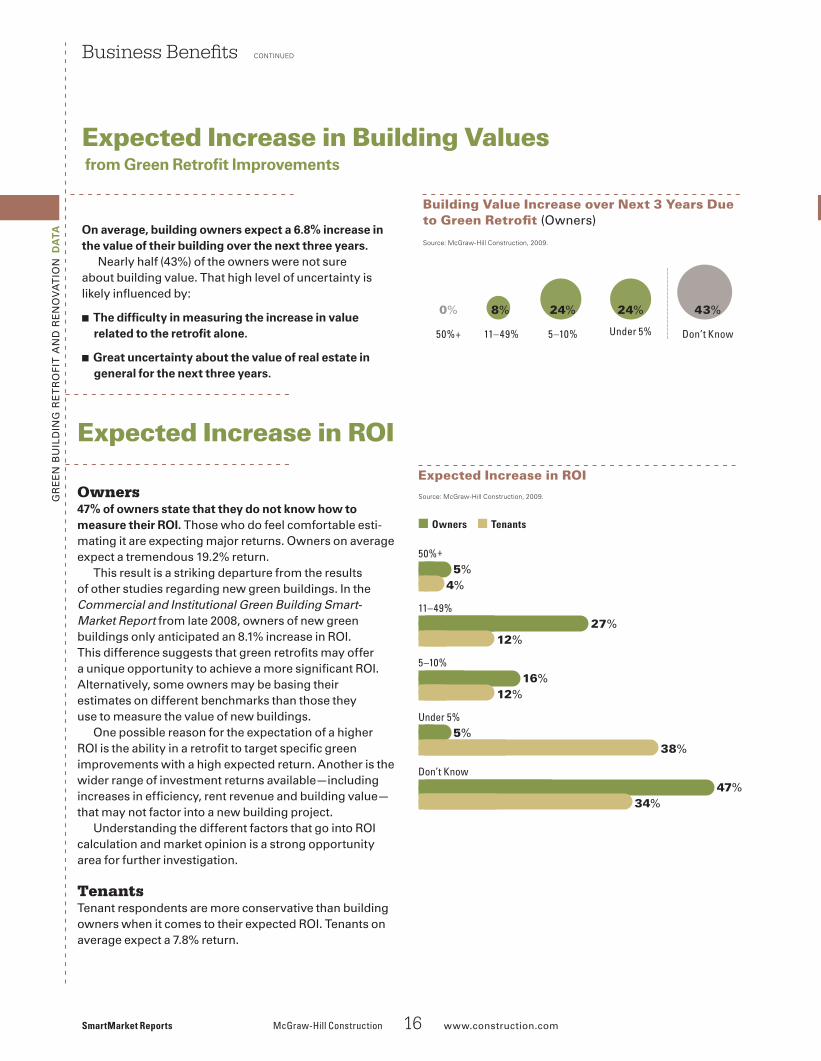

On average, building owners expect a 6.8% increase in the value of their building over the next three years.

nearly half (43%) of the owners were not sure about building value. that high level of uncertainty is likely influenced by:

the difficulty in measuring the increase in value ■■

related to the retrofit alone.

Great uncertainty about the value of real estate in ■■

general for the next three years.

0% 8% 24% 24% 43%

50%+ 11–49% 5–10% Under 5% Don’t Know

Expected Increase in Building Values from Green Retrofit Improvements

Business Benefits COntInUED

Building Value Increase over Next 3 Years Due to Green Retrofit (owners)

Source: McGraw-Hill Construction, 2009.

Expected Increase in ROI

Owners47% of owners state that they do not know how to measure their ROI. those who do feel comfortable esti-mating it are expecting major returns. owners on average expect a tremendous 19.2% return.

this result is a striking departure from the results of other studies regarding new green buildings. in the Commercial and Institutional Green Building Smart-Market Report from late 2008, owners of new green buildings only anticipated an 8.1% increase in roi. this difference suggests that green retrofits may offer a unique opportunity to achieve a more significant roi. alternatively, some owners may be basing their estimates on different benchmarks than those they use to measure the value of new buildings.

one possible reason for the expectation of a higher roi is the ability in a retrofit to target specific green improvements with a high expected return. another is the wider range of investment returns available—including increases in efficiency, rent revenue and building value—that may not factor into a new building project.

understanding the different factors that go into roi calculation and market opinion is a strong opportunity area for further investigation.

Tenantstenant respondents are more conservative than building owners when it comes to their expected roi. tenants on average expect a 7.8% return.

Source: McGraw-Hill Construction, 2009.

Expected Increase in ROI

■ Owners ■ Tenants

50%+

5%

4%

11–49%27%

12%

5–10%16%

12%

Under 5%5%

38%

Don’t Know

47%

34%

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta

McGraw-Hill Construction 17 www.construction.com SmartMarket Reports

there are still mixed opinions about the impact of green retrofit projects on the expected time to lease a space.

27% of owners expect them to lease more quickly.■■

35% expect them to lease at the same rate.■■

33% don’t know what to expect.■■

as green retrofitted spaces become more common, a clearer pattern may emerge about how they compare in leasing rate with traditional spaces.

27% 35% 5% 33%

More At About the Less Don’t Know Quickly Same Rate Quickly

Expected Time to Lease Green Retrofitted Space

Business Benefits COntInUED

Expected Time to Lease Green Retrofitted Space (owners)

Source: McGraw-Hill Construction, 2009.

3% 11% 5% 41% 40%

50%+ 11–49% 5–10% Under 5% Don’t Know

16% 8% 11% 41% 24%

50%+ 11–49% 5–10% Under 5% Don’t Know

Most owners (60%) expect to be able to charge an increased rent due to the green retrofits, though their esti-mates of those increases are conservative, with a median expected increase of 1%. there are a few outliers with significantly higher estimates of rent increases, which suggests that some commercial owners are seeing a will-ingness to pay in the market. lack of certainty about the real estate market and the nascency of green building also likely contribute to the high percentage of owners who do not know what level of rent increase to expect.

Expected Rent Increase due to Green Retrofits

Expected Increase in Overall Occupancy

the median increase in occupancy expected by respon-dents is 2.5%. However, the mean is skewed by a few respondents expecting large increases, which could be due to the conversion of previously unoccupied space or to shifting a property from Class C to Class a.

three-quarters of the building owners surveyed expect to see occupancy increase due to their green retrofit and renovation activity.

Source: McGraw-Hill Construction, 2009.

Increase in Overall Occupancy Due to Green Retrofit over Next Year (owners)

Source: McGraw-Hill Construction, 2009.

Overall Rent Increase Due to Green Retrofit over the Next 3 Years (owners)

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta

SmartMarket Reports McGraw-Hill Construction 18 www.construction.com

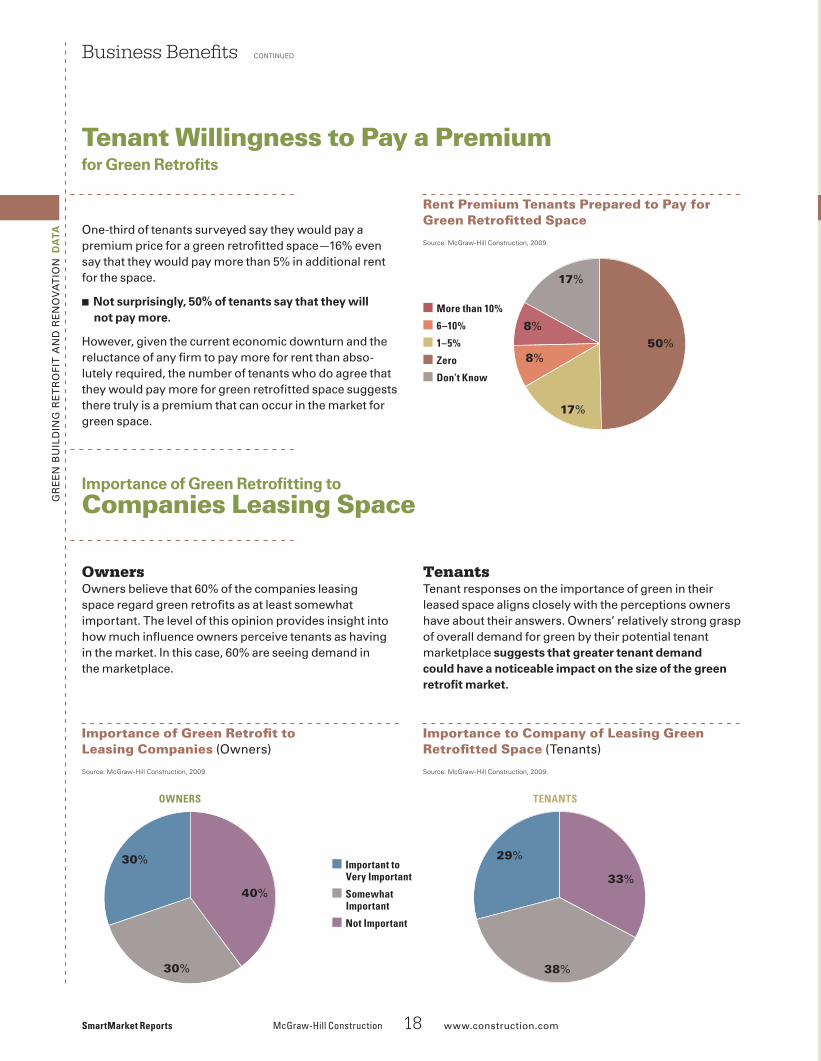

one-third of tenants surveyed say they would pay a premium price for a green retrofitted space—16% even say that they would pay more than 5% in additional rent for the space.

Not surprisingly, 50% of tenants say that they will ■■

not pay more.

However, given the current economic downturn and the reluctance of any firm to pay more for rent than abso-lutely required, the number of tenants who do agree that they would pay more for green retrofitted space suggests there truly is a premium that can occur in the market for green space.

Tenant Willingness to Pay a Premium for Green Retrofits

Business Benefits COntInUED

Rent Premium Tenants Prepared to Pay for Green Retrofitted Space

Source: McGraw-Hill Construction, 2009.

■ More than 10%

■ 6–10%

■ 1–5%

■ Zero

■ Don’t Know

50%

17%

8%

8%

17%

Ownersowners believe that 60% of the companies leasing space regard green retrofits as at least somewhat important. the level of this opinion provides insight into how much influence owners perceive tenants as having in the market. in this case, 60% are seeing demand in the marketplace.

Tenants tenant responses on the importance of green in their leased space aligns closely with the perceptions owners have about their answers. owners’ relatively strong grasp of overall demand for green by their potential tenant marketplace suggests that greater tenant demand could have a noticeable impact on the size of the green retrofit market.

Importance of Green Retrofitting to

Companies Leasing Space

OWneRS TenanTS

33%

29%

38%30%

30%

40%

■ Important to Very Important

■ Somewhat Important

■ not Important

Importance of Green Retrofit to Leasing Companies (owners)

Source: McGraw-Hill Construction, 2009.

Importance to Company of Leasing Green Retrofitted Space (tenants)

Source: McGraw-Hill Construction, 2009.

McGraw-Hill Construction 19 www.construction.com SmartMarket Reports

as owners seek operational cost savings, increased building values and faster returns on investment, they are approaching green retrofit and renovation activity by greening their building portfolios versus a single-building approach.

Advantages to a Portfolio Approachin just one building, research has shown cost savings from energy-efficiency upgrades alone (not including water or other efficient practices) are saving firms money. When firms green their buildings from a broader portfolio viewpoint, their savings multiply dramatically—particularly crucial in a down economy.

Corporations tend to operate a range of buildings that vary in size, usage and energy loads. Case study research conducted by iCf international, a global environmental consulting firm, has shown that evaluating resource consumption trends from an entire portfolio perspective allows owners to assess potential savings and achieve maximum results.1

identifying the most energy-intensive buildings in a portfolio is not necessarily intuitive, as it depends significantly on tenant behavior and operations. Plotting buildings by size and energy usage can help compan-ies target outliers and implement effective portfolio-wide green retrofits. Some of the companies that have experienced success with

green portfolio upgrades include retail grocery company food lion, who achieved 28% annual cost savings through low-cost and no- cost operational upgrades and Starbucks, with $1.5 million saved per year through lighting upgrades and the implementation of a store energy checklist.2

Commitments to Greening Existing Portfoliosthe u.S. green building Coun-cil’s volume Certification program enables companies to achieve leed certification across multiple build-ings. Many large companies—market leaders that can drive future activity at significant levels—have engaged in the program. Some of these firms include commercial real estate ser-vices companies like transwest-ern, Cb richard ellis and Cushman & Wakefield as well as other large commercial building owners, such as Citi, Wachovia, office depot and Kohl’s. uSgbC reports that to date, the pilot program covers 1,700 build-ings and approximately 135 million square feet of building space. Many of these same firms are active part-ners in government voluntary pro-grams—such as energy Star or u.S. department of energy’s Commercial building energy alliances.

according to doug gatlin, vice president, market development for uSgbC, one of the major advantages of volume certification is that it “pro-vides companies with the tools to

integrate leed into new and exist-ing building projects as a standard feature of design, construction and operations [which will]…help stream-line the certification process and…move closer towards the ultimate goal of market transformation.

Role of Operations & MaintenanceWhile commitment to improving buildings through green retrofit and renovation projects is important, simple changes in operations and upgrades in maintenance procedures can maximize energy and water performance. new policies such as green cleaning and environmen-tal procurement programs can lead to healthier workplaces and cata-lyze larger market shifts (similar to the effect the federal government’s policy on recycled content paper had on increasing availability and decreasing costs of this paper in the larger marketplace). it also allows firms that cannot afford renovation activity across their portfolios to reap benefits that will ultimately help improve the environment. as gatlin says, “by improving performance of existing buildings, owners and operators will expe-rience substantial cost savings stemming from a number of sources, including reduced maintenance/repair expenditures, resource consumption through improved efficiency and increased occupant productivity due to high indoor environmental quality.” ■

A Portfolio-Approach to Greening Existing Buildings and Focus on Sustainable Operations and Maintenance Maximizes Benefits of Green Retrofit and Renovation Project

Maximizing Business Benefits

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

Sidebar: Business Benefits

1, 2 Anderson, Don. “Green Operations: An Overlooked Opportunity in Existing Guildings,” Presentation made at the 2009 China Green Building and Energy Efficiency Conference, August 19, 2009.

SmartMarket Reports McGraw-Hill Construction 20 www.construction.com

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta these results highlight the influence of the down economy:

LiFecYcLe cOsTs: ■■ Some owners reap the financial benefits directly because they have set up fixed utility rates in leases. Others will pass benefits along to tenants but can still market their properties based on reduced energy costs, potentially allowing for higher rents and faster turnaround when leasing.

ROi: ■■ In an economic downturn, cost savings are particularly critical to achieving a higher return on investment.

TeNANT sATisFAcTiON: ■■ tenant satisfaction may carry particular weight given the current economic downturn. Even in a strong leasing market, keeping tenants is more cost-effective than seeking new ones, so it is not surprising that tenant satisfaction is selected by a significant percentage of owners as an important driver for engaging in green retrofit and renovation activities. as vacancy rates continue to grow in the office sector in the second quarter of 2009, retaining existing tenants becomes even more critical.

the high level (60%) of owners who expect improved tenant satisfaction also speaks to trends documented in the The Green Home Consumer SmartMarket Report and The Green Home Builder SmartMarket Report. MHC research demonstrates that green building practices are associated with higher quality buildings, which could account for the strong connection indicated by building owners between tenant satisfaction and green practices.

While tenant satisfaction and direct financial payback are clearly the primary drivers for building owners to engage in green retrofit projects, many owners also indicate that attracting new tenants to their spaces is an important driver for engaging in green efforts. Most of the other factors measured—such as improved rental speed (44%) and the competitive advantage offered by a green building (39%)—provide insight into owner estimation of tenant demand for green. the level of response for these factors suggests that tenant demand can function as a driver for the green retrofit market, but that the majority of owners do not perceive a strong demand to date.

tenants and owners agree that lowering operating/ lifecycle building costs is the prime motivation for engaging in a green retrofit project. this result is con-sistent with other studies conducted by Mcgraw-Hill Construction on the green building market, in particu-lar the Commercial and Institutional Green Building SmartMarket Report, in which the same percentage of respondents (76%) report lifecycle costs an important business motivator for new green building.

Ownersdirect financial benefits of the retrofit itself, not the expected desirability of the space to tenants, are the biggest business motivates for building owners to engage in a green retrofit project.

76% cite lowering building lifecycle costs.■■

64% cite higher ROI.■■

60% cite improved tenant satisfaction.■■

Market IntelligenceData: Business Motivations for Green Retrofits

Green Retrofit Business Motivation (owners)

Source: McGraw-Hill Construction, 2009.

Lowering Building Lifecycle Costs

76%

Higher ROI

64%

Improved Tenant Satisfaction

60%

Improved Rental Speed

44%

Higher Building / Asset Values

43%

Anticipate an Increase in Demand For Green Commercial Buildings

41%

Competitive Advantage Offered by Green Building

39%

Higher Lease Rates / Higher Rents

35%COntInUED

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta

McGraw-Hill Construction 21 www.construction.com SmartMarket Reports

Market IntelligenceBusiness Motivations for Green Retrofits COntInUED

Tenantsthe greatest business motivation for tenants is lowering operating costs, followed by improved employee satisfaction.

Productivity gains were noted by almost half (48%) as another important business motive behind green retrofits. in commercial ventures, workers’ salaries are the largest corporate expense. according to the building owner and Managers association and the electric Power research institute, office workers’ salaries are 83.4% of total annual commercial expenditures.

While productivity gains offer the largest potential for monetary paybacks, most types of work output are not easily measured. therefore, these gains are infrequently tracked, especially with new green build-ings. one study from australia on productivity in a green law office revealed a 39% reduction in average sick leave days, a 44% reduction in the monthly average cost of sick leave and a 7% increase in lawyers’ billing rates.

as the green retrofit market increases, more exact understanding of the impact of green building on employee productivity may be gained. Case studies on pages 40–64 offer some insight into these soft benefits.

Lowering Space’s Yearly Operating Costs

96%

Improved Employee Satisfaction

71%

Improved Productivity / Reduced Sick Days Among Employees

48%

Competitive Advantage by Offering a Green Building

38%

Green Retrofit Business Motivation (tenants)

Source: McGraw-Hill Construction, 2009.

the most important environmental motives are the same for both building owners and tenants.

Eighty-nine percent of owners and nearly all (96%) ■■

tenants cite reduced energy use as the most impor-tant environmental motivation. energy use is easily quantifiable, so reductions can be equated to financial savings without difficulty.

Most owners (87%) and tenants (79%) cite improved ■■

indoor environment/air quality as also important.

the high rate of response for these two factors is consistent with similar findings about environmental motivations behind new green buildings in the Commer-cial and Institutional Green Building SmartMarket Report.

Environmental and Social Motivations

■ Owners ■ Tenants

Reduce Energy Use

89%

96%

Improve Indoor Environment / Air Quality

87%

79%

Reduce Water Use

81%

63%

Lower Carbon Footprint

60%

54%

Usage of Rapidly Renewable Materials / Recycled Material / Green Certified Materials

49%

58%

Achieve LEED Certification

47%

29%

Encourage Sustainable Busines Practices 0%

75%

Environmental Motivations for Green Retrofit Projects

Source: McGraw-Hill Construction, 2009.

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

da

ta

SmartMarket Reports McGraw-Hill Construction 22 www.construction.com

the case study data support these findings. for example, two of the three of u.S. general Services administra-tion (gSa) profiled green retrofit projects (see page 44) were in part motivated by the gSa’s interest in improving indoor air quality for their tenants.

Nearly 80% of owners and tenants most often cite improved health and well-being of building occupants/employees as their top social motivator for going green in retrofit and renovation projects. this finding corre-sponds to the high level of concern about improved indoor environment/air quality as an environmental motivator.

OwnersEconomic concerns are the primary motivation for owners. as shown on page 21, 81% of owners cite reduced water use as an important environmental motivation, making it the third most common environ-mental motivation for owners (behind reduced energy use and improved indoor environment). aside from its environmental benefit, water conservation also provides a direct economic benefit for the owner.

Social motivations for building owners are inspired by a macro-level view of their building in relation to their immediate vicinity and the larger economy:

73% are motivated to support a more sustainable ■■

economy.

57% want to redevelop existing buildings to ■■

improve the overall quality of the built environment in their cities.

the value of real estate is tied to client perception of the building and its environs. among firms who have already committed to green retrofits, therefore, it it consistent that they want to see growth in the overall and perceived value of sustainability.

as early adopters of green retrofit and renovation projects, these owners also frequently cite activities that have a less direct economic benefit but offer marketing potential:

60% aspire to lower their carbon footprint.■■

49% are motivated to use renewable/recycled/ ■■

certified materials.

TenantsWhile the smaller number of respondents makes specific conclusions difficult, there is a clear tendency that tenants are influenced by public perception of their company and the green movement in general.

sOciAL: ■■ 71% want to be seen as being on board with the environment as a cause.

eNviRONmeNTAL:■■ 75% want to encourage sustain-able business practices.

Market IntelligenceEnvironmental and Social Motivations COntInUED

■ Owners ■ Tenants

Greater Health and Well-Being of Building Occupants / Employees

78%

79%

Supports a More Sustainable Economy

73%

71%

Lead Redevelopment of Existing Buildings to Improve Overall Quality of City Environs

57%

38%

Seen as Being on Board With an Important Environmental Cause0%

71%

Social Motivations for Green Retrofit Projects

Source: McGraw-Hill Construction, 2009.

McGraw-Hill Construction 23 www.construction.com SmartMarket Reports

gr

ee

n b

uil

din

g r

et

ro

fit

an

d r

en

ov

at

ion

A s can be seen throughout the market research con-tained in this report, there is a significant portion of

the industry unable to evaluate the full impact of their retrofit and reno-vation project(s). on page 14, a fifth of owners either don’t know how to measure economic impact or they haven’t done it.

achieving the optimal perfor-mance of a project, however, requires good upfront planning, ongoing monitoring and appropriate end-use reporting to demonstrate returns.

However, with the wide array of methods, finding appropriate bench-marks, measures and reporting is complicated. as various indus-try players (including government, nonprofit organizations and trade associations) have pointed out for years, if measures are not evaluated based on appropriate benchmarks and comparable projects, it can make the eventual reported results misleading and not optimal for the ultimate goal of conducting those measures—improving the building performance and yielding financial, environmental and social benefits.

Designing for Performancethe design phase of a project is an ideal time to address different aspects of a green retrofit project, such as selection of products, sys-tems and processes.

integrated project delivery that involves all players in the project has been consistently reported by indus-try leaders and successful green project teams as key to efficient, cost-

effective solutions leading to better quality and higher performing build-ings. in fact, many of the case studies profiled in this report involved teams that engaged with each other from the earliest stages of the project.

virtual tools, such as building information Modeling (biM), facilitate the exchange of information among project team members leading to a better and more-efficient work process. furthermore, simulation models can help estimate a project’s eventual energy performance. the industry is making these connections between biM and green building. in Mcgraw-Hill Construction’s The Business Value of BIM SmartMarket Report released in September 2009, 73% of the entire industry (owners, contractors, architect and engineers) expect use of biM to increase on leed projects—46% believe it will see a high increase.

Setting Effective Bench-marks and Measuresthere are a number of ways that owners are creating benchmarks for the performance of their build-ings, but there is wide variation in how they actually go about that mea-surement. Some forms of measur-ing energy use, tracking utility bills (before versus after or comparable to similar space by building type, size and location), conducting engineer-ing audits and analysis and creating simulations with computer modeling tools (as mentioned above).

finding the right measures is important both for making the internal business case as well as for justifying future projects.

Reporting and Transparencythere are several pressures under-way encouraging—or even requir-ing—public reporting of building performance data, most notably around energy and water use.

one motivator has been the growing trend in legislative policies requiring public reporting of a building’s energy use. though mandates around specific reduction goals hve not been set to date, this trend suggests that policy is moving in that direction. it also indicates that the energy Star program, its Portfolio Manager and doe’s High Performance buildings database will become more widely used and influential in the future.