fluid fertilizer foundation fresno, california december … · fluid fertilizer foundation fresno,...

TRANSCRIPT

N, P & K

OUTLOOK Fluid Fertilizer Foundation

Fresno, California December 7, 2011

Presenter: Jay Yost, Vice President Fertilizer

0

2

4

6

8

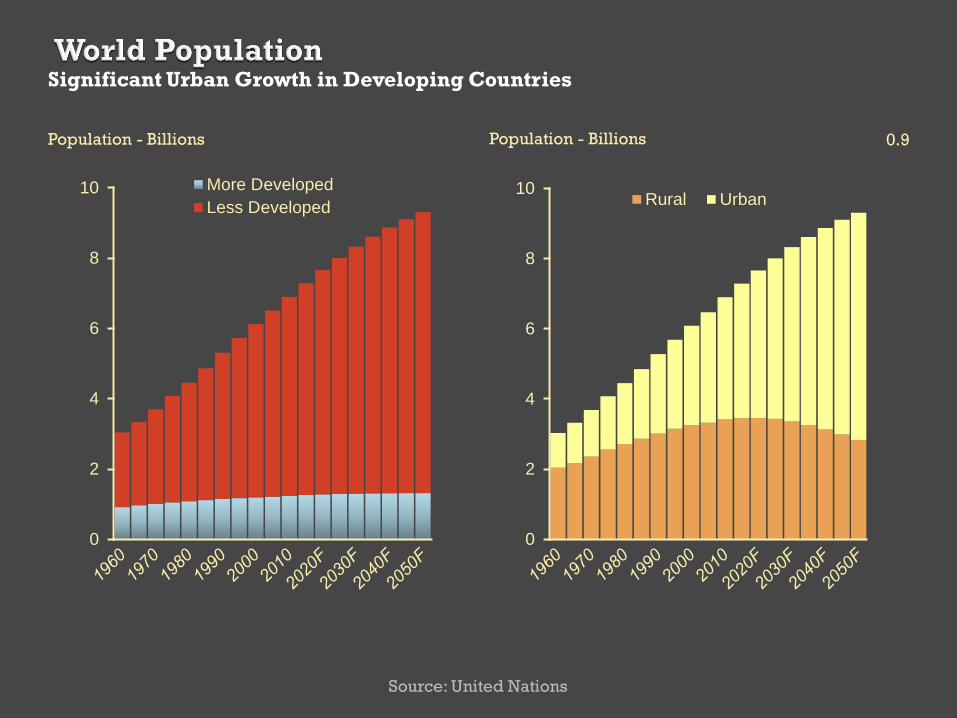

10 More Developed

Less Developed

Source: United Nations

Population - Billions 0.9

Significant Urban Growth in Developing Countries

0

2

4

6

8

10Rural Urban

Population - Billions

1.4

1.5

1.6

1.7

1.8

1.9

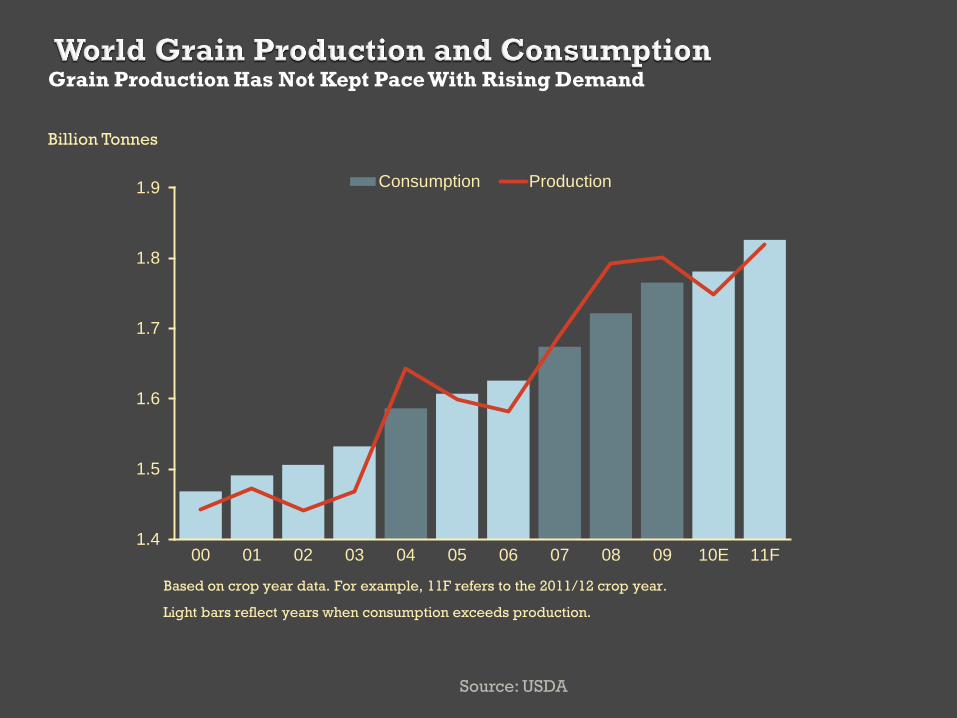

00 01 02 03 04 05 06 07 08 09 10E 11F

Consumption Production

Source: USDA

Billion Tonnes

Grain Production Has Not Kept Pace With Rising Demand

Based on crop year data. For example, 11F refers to the 2011/12 crop year.

Light bars reflect years when consumption exceeds production.

10

15

20

25

30

35

40

86 88 90 92 94 96 98 00 02 04 06 08 10E 12F

Historical 25-Year Average

Source: USDA, PotashCorp

Percent

Grain Inventories Expected to Remain Tight Beyond 2012

Based on crop year data. For example, 11F refers to the 2011/12 crop year.

4% (~ 2X Historical Rate)

6% (~3X Historical Rate)

2% (~ Historical Rate)

2012 Production Growth

Rate Scenarios

0

5

10

15

20

25

2001 2003 2005 2007 2009 2011F

Historical 10-Year Average

Billion Bushels Stocks-to-Use - Percent

Source: USDA

Corn Stocks Reduced to Historically Low Levels

8

9

10

11

12

13

14

2001 2003 2005 2007 2009 2011F

Production Consumption

2011F refers to the 2011/12 crop year

2

3

4

5

6

7

8

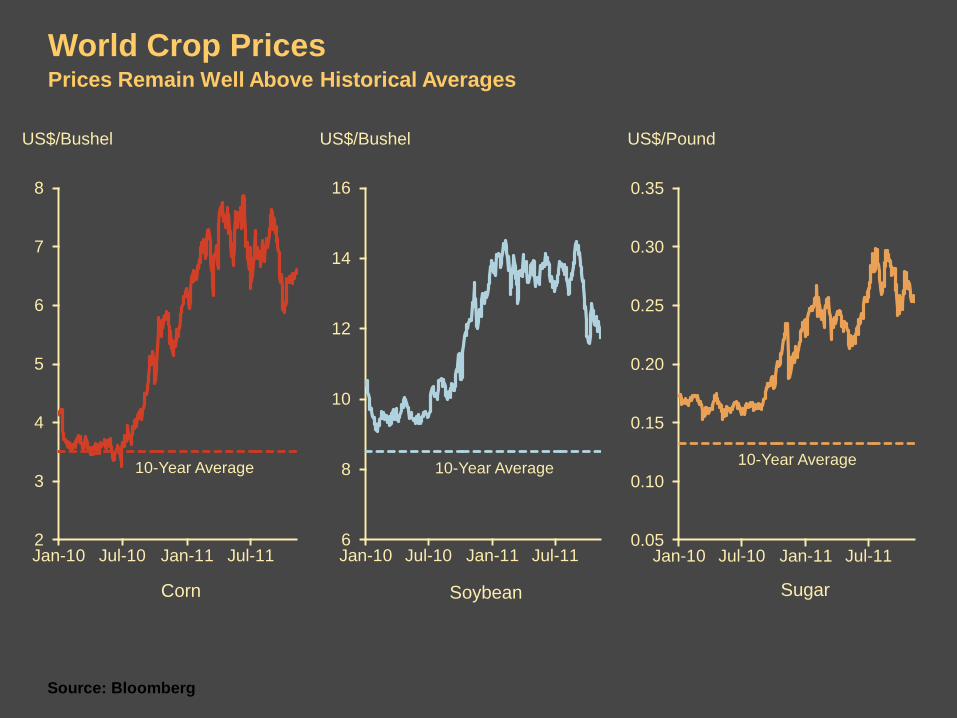

Jan-10 Jul-10 Jan-11 Jul-11

Source: Bloomberg

World Crop Prices Prices Remain Well Above Historical Averages

US$/Bushel US$/Pound

6

8

10

12

14

16

Jan-10 Jul-10 Jan-11 Jul-11

US$/Bushel

10-Year Average

Corn Soybean Sugar

10-Year Average

0.05

0.10

0.15

0.20

0.25

0.30

0.35

Jan-10 Jul-10 Jan-11 Jul-11

10-Year Average

Source: USDA, IPNI, PotashCorp

Percent

Expect Fertilizer Cost Percentage Will Remain Below Historical Levels

Source: USDA

US$ Billions

US Net Cash Farm Income Farm Income Growth Has Accelerated in Recent Years

Record years since 2000

Source: Fertecon, PotashCorp

$US/MMBtu

Natural Gas Prices in Key Producing Regions US Gas Price Increasingly Competitive

W. Europe (Contract)

US Gulf

Ukraine (Port)

Russia

W. Europe (Spot)

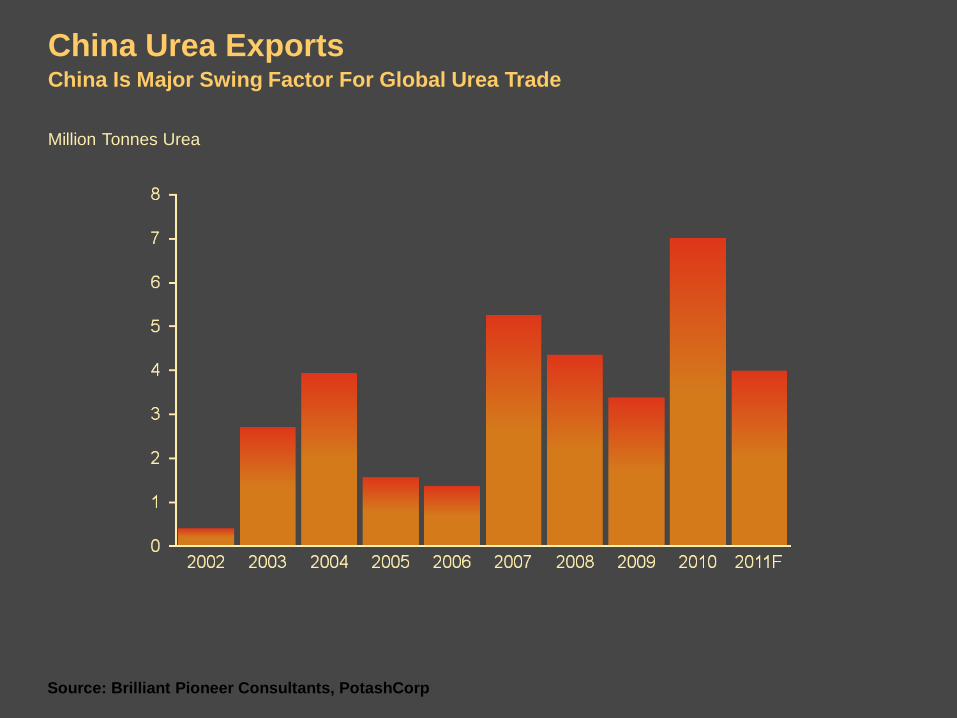

Source: Brilliant Pioneer Consultants, PotashCorp

Million Tonnes Urea

China Urea Exports China Is Major Swing Factor For Global Urea Trade

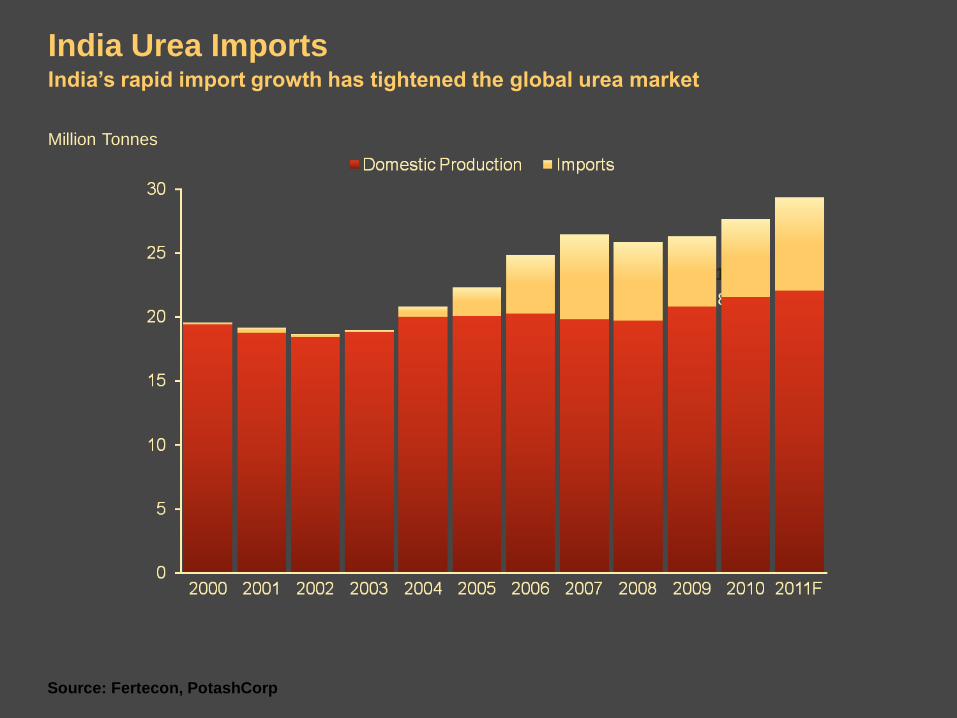

Source: Fertecon, PotashCorp

Million Tonnes

India Urea Imports India’s rapid import growth has tightened the global urea market

21.8

6.1

Source: Fertecon, PotashCorp

Million Tonnes

US Nitrogen Consumption US Nitrogen Demand Expected to Remain Strong in 2011

Ammonia Urea Total Nitrogen Solutions

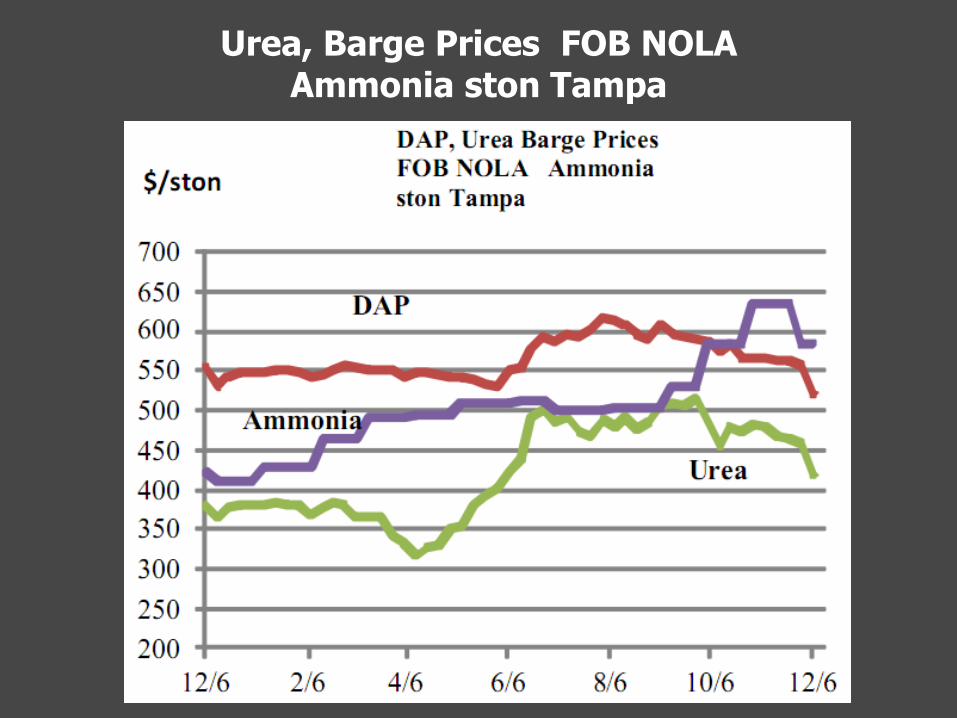

Urea, Barge Prices FOB NOLA Ammonia ston Tampa

Prices have pushed up due to

increased demand and limited supply

• Main Reason is Dramatic Increase in

Crop Commodity Prices

• Fill Large Dealer/Distributor Storage

Gas Costs - $3.75 + producers in

North America are in the drivers seat.

Cost of Gas in Ammonia vs.

Ston Tampa Price

Ammonia: Gas cost in ammonia based on capacity weighted average efficiency for nine Louisiana ammonia

plants x midweek close nearest natural gas future NYM exchange.

Relative Value of N in Fertilizers (Ill., Ia., Mo.)

$/Unit N

PCS to restart Geismar, LA plant –

1,135,000 tons of UAN 32% production

Coffeyville now looking at completing their

UAN 32% expansion at Coffeyville,

Kansas 350,000 – 400,000 additional per

year

Gas curtailment in Trinidad – 30%

• Production - 5,655 Mstpy

• Curtailment – 1,696 Mstpy

Phos Acid / 10-34-0 supply and issue • Limited production in the US

• No opportunities for imports

• Reduced production in the US

• Supplies are impacted in the short run

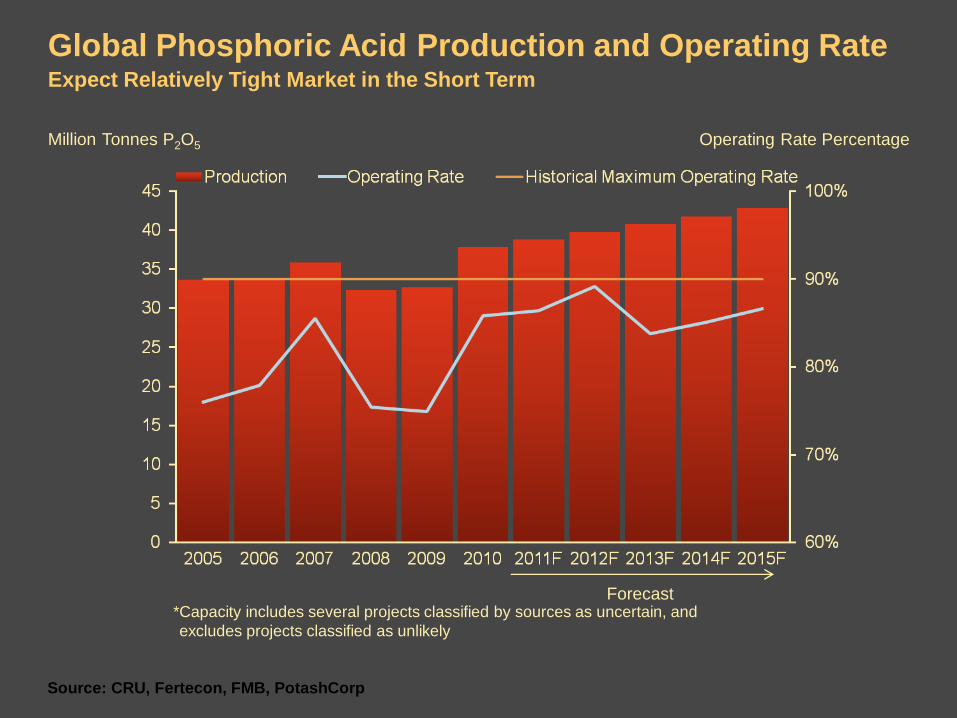

Source: CRU, Fertecon, FMB, PotashCorp

Million Tonnes P2O5 Operating Rate Percentage

Global Phosphoric Acid Production and Operating Rate Expect Relatively Tight Market in the Short Term

*Capacity includes several projects classified by sources as uncertain, and

excludes projects classified as unlikely

Forecast

Million Tonnes DAP

India DAP Supply India’s Demand Expected to Remain Strong in 2011

Source: FAI, Fertecon, PotashCorp

7.8

3.4

Source: Fertecon

Million Tonnes Product

China DAP and MAP Exports Domestic demand expected to limit exports

Source: PotashCorp

Integrated vs Non-Integrated Phosphoric Acid Capacity Approximately 70 percent of Global Phosphoric Acid Producers are Integrated

Integrated

70%

Non-

Integrated

30%

Source: Fertecon, PotashCorp

Integrated vs Non-Integrated Cost of DAP Production Significant Advantage for Integrated Producers

$US/Tonne $US/Tonne

Integrated Non-Integrated

Integrated producers account for approximately 70 percent of production, non-integrated producers account

for about 30 percent of production.

DAP Barge Prices FOB NOLA $/ston

Production Issues • Mosaic – Permitting Issues in Florida

• Agrifos – 800,000 – Out of Production

• New production coming on around the

world

Saudi Arabia

Morocco

Phos Acid / 10-34-0 supply and

issue • Limited production in the US

• No opportunities for imports

• Reduced production in the US

• Supplies are impacted in the shortrun

Source: Fertecon, PotashCorp

World Potash Production and Demand Major Consuming Markets Are Heavily Dependent on Imports

Production

Demand

North America

Europe

Latin America

FSU

Asia Middle East

Million Tonnes KCl – 2010

16.6

10.2

8.6

2.2

3.9 5.5

5.3

3.3

19.0

22.5

0.5

0.8

Africa

Oceania

0.7

6.7

22%

78%

Domestic Sales

Potash Trade

Source: Fertecon, PotashCorp

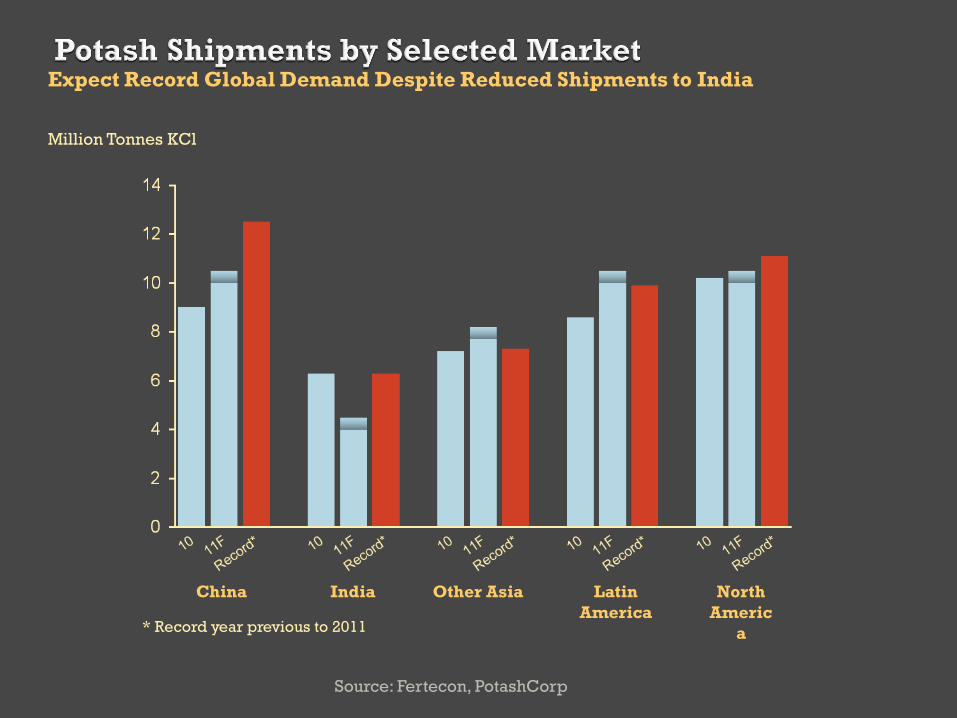

Million Tonnes KCl

Expect Record Global Demand Despite Reduced Shipments to India

China India Other Asia Latin

America

North

Americ

a * Record year previous to 2011

Million Tonnes KCl Million Tonnes KCl

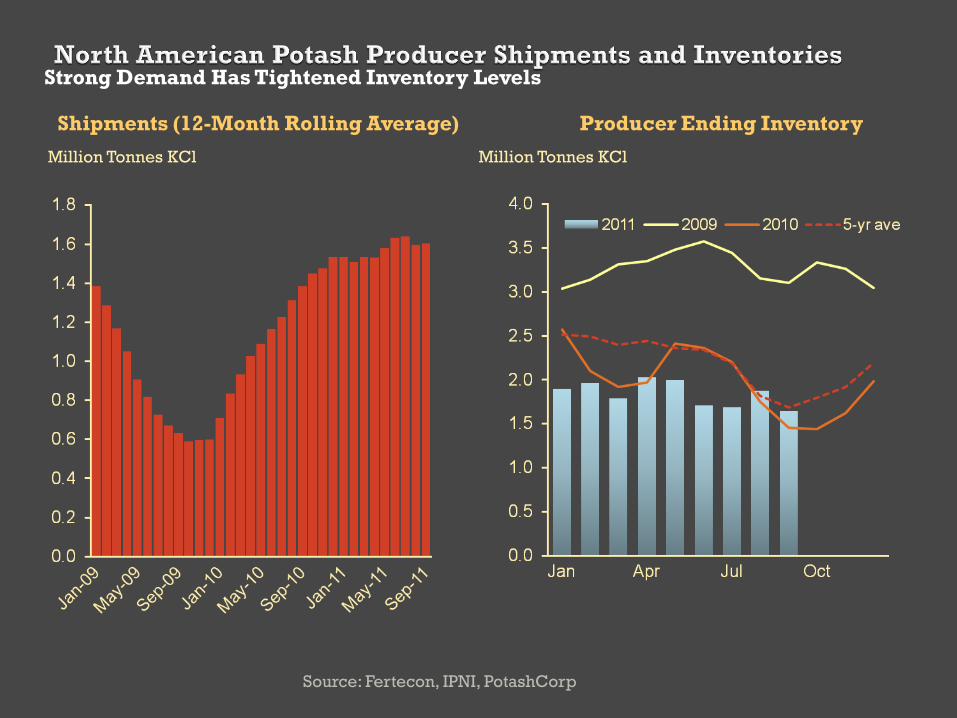

Source: Fertecon, IPNI, PotashCorp

Strong Demand Has Tightened Inventory Levels

Shipments (12-Month Rolling Average) Producer Ending Inventory

Shipments - Million Tonnes KCl

Operating Rate* - Percent

Expect Global Operating Rates to Remain at Historically High Levels

Source: Fertecon, PotashCorp

* Based on percentage of operational capability.

2012 operating rate scenarios based on global shipments of 58 to 60 million tonnes

Source: Fertecon, CRU, IFA, PotashCorp

Million Tonnes KCl – 2011F to 2015F

World Potash Producer Profile Largest Producer by Capacity

PotashCorp

* PotashCorp investments: ICL (14%), APC (28%), SQM (32%) and Sinofert (22%)

Note: PotashCorp based on operational capability (estimated annual achievable production) while competitor

capacity is stated nameplate, which may exceed operational capability.

Source: AMEC, PotashCorp

CDN$ Billions

Estimated Greenfield Potash Capital Costs Greenfield Projects Require Significant Investment

* Based on 2mmt per-year conventional mine in Saskatchewan; costs could vary depending on conventional vs. solution mine,

depth of ore body, geographic location, and other factors.

** Dependent on geographic location, access and distance to port. Includes railcars, utility systems, port facilities, etc.

*** Based on publicly reported cost of recent purchases.

$0.0B-$1.0B

$0.6M-$1.2B

$4.7B-$6.3B

$4.1B

Source: AMEC, PotashCorp

Capital Cost per Tonne – (CDN$)

Saskatchewan Brownfield and Greenfield Costs

* New Brunswick cost per tonne based on new 2MMT mine (net addition totals 1.2MMT).

** Based on 2MMT conventional greenfield mine constructed in Saskatchewan.

PotashCorp project costs exclude infrastructure.

Brownfield Expansion Advantage

Potash Price FOB St. Louis

$/ston

Fall Supply Issues • Producers are tying in new production causing

outages at existing mines

Producers moving prices up because

they can

Time will tell if higher prices have an

appreciable affect on demand

Corn, Wheat, Soybean Prices Thurs. Close CBOT $/ Bu.

Watch commodity prices – if

commodity prices fall fertilizer will

follow

Falling commodity prices will cause

buyers to be cautious and producers

to be concerned

Move from a demand driven market to

a supply driven market

Questions?

UAN Price FOB St. Louis

$/Unit N

Million Tonnes

Source: IFA, FAO, USDA, PotashCorp

Corn Is the Largest Potash Consumer

Grain and Oilseed

Production

Potash Use by Crop

All Other Crops

Cor

n

Soybeans

Wheat

Cotton

Fruits &

Vegetables

2010E refers to the 2010/11 crop

year

Million Tonnes

Source: IFA, FAO, USDA, PotashCorp

Significant Growth in Production of Fruits and Vegetables

Major Crop Production

All Other Crops

Sugar Crops

Wheat

Rice Fruits &

Vegetables

Potash Use by Crop

Million Tonnes

Source: IFA, FAO, USDA, PotashCorp

Rice and Wheat Account for Nearly Half of Potash Consumption

Potash Use by Crop Major Crop Production

All Other

Crop

s

Fruits &

Vegetables

Sugar Crops

Wheat

Rice