florida board of accountancy - cpa resources · if my state of licensure has mobility or if the...

TRANSCRIPT

FLORIDA

BOARD OF

ACCOUNTANCY

2010

UPDATE

David C. Tipton, CPA/CVA Chairman

“I’m from the

government and I’m

here to help…..”

The views and frustrations expressed here today are my own and do not represent the official position of the Florida Board of Accountancy or the

Florida Department of Business & Professional Regulation

Why do we have the BOA

�10th Amendment of Bill of Rights

�Florida Statutes Chapter 455

�Florida Statutes Chapter 473

�Florida Administrative Code Chapter 61

FS Chapter 455 – Business & Professional Regulation

• 455.201 Professions & occupations regulated by department; legislative intent; requirements

– (2) The legislature further believes that such professions shall be regulated only for the preservation of the health, safety, and welfare of the public under the police powers of the state. Such professions shall be regulated when:

FS Chapter 455 – Business & Professional Regulation

• (a) Their unregulated practice can harm or endanger the health, safety, or welfare of the public, and when the potential for such harm is recognizable and clearly outweighs any anticompetitive impact which may result from regulation

• (b) The public is not effectively protected by other means including, but not limited to, other state statutes, local ordinances, or federal legislation

FS Chapter 473 – Public Accountancy

• 473.301 Purpose – The legislature recognizes that there is a public need for independent and objective public accountants and that it is necessary to regulate the practice of public accounting to assure the minimum competence of practitioners and the accuracy of audit statements upon which the public relies and to protect the public from dishonest practitioners and, therefore, deems it necessary in the interest of the public welfare to regulate the practice of public accountancy in this state

Vision & Mission of the FICPA

• Vision– The FICPA is the premier professional

organization representing Florida’s Certified Public Accountants

• Mission– We serve the diverse needs of our members;

enhance their competency and professionalism; support professional standards; promote the value of our members and advocate of behalf of the profession

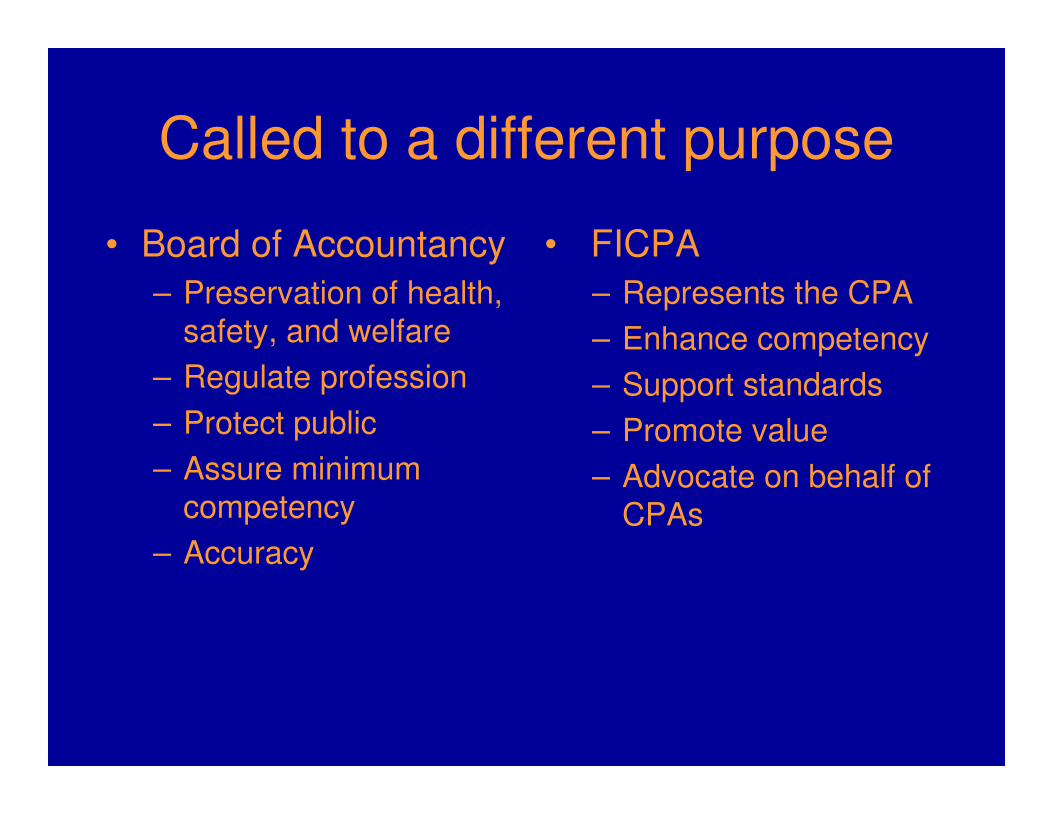

Called to a different purpose

• Board of Accountancy

– Preservation of health, safety, and welfare

– Regulate profession

– Protect public

– Assure minimum competency

– Accuracy

• FICPA

– Represents the CPA

– Enhance competency

– Support standards

– Promote value

– Advocate on behalf of CPAs

Chapter 473.303: The Board of Accountancy

• Consists of nine members

• Appointed by Governor; approved by Senate

• Seven CPA’s & two public members

• One member must be 60 years old

• Term is for 4 years

• Meet approximately every 6 weeks

Current Board Members

• Cynthia Borders-Byrd Ft Lauderdale

• Rick Carroll Tallahassee

• Maria Caldwell Miami

• Bill Durkin Valrico

• Steve Riggs Destin

• Eric Robinson Venice

• Teresa Borcheck Orlando

Issues Impacting the BOA

• Major frauds

• Social changes

• Demographic changes

• Social mobility

• Economic pressures

Major Frauds

• Enron

• Sarbanes-Oxley

• Ethics Course – the Compromise

• Elimination of the Law & Rules Exam

• Signed into law May 27, 2009

• Madoff

• Mandatory peer review

Social changes

• Technology

• Online reporting and renewal

• Computer based CPA exam

– 18 month rolling period

– Defining the date the period starts

– Allowing applicants to sit with 120 hours; still have to have the 150 to be certified

Social Changes

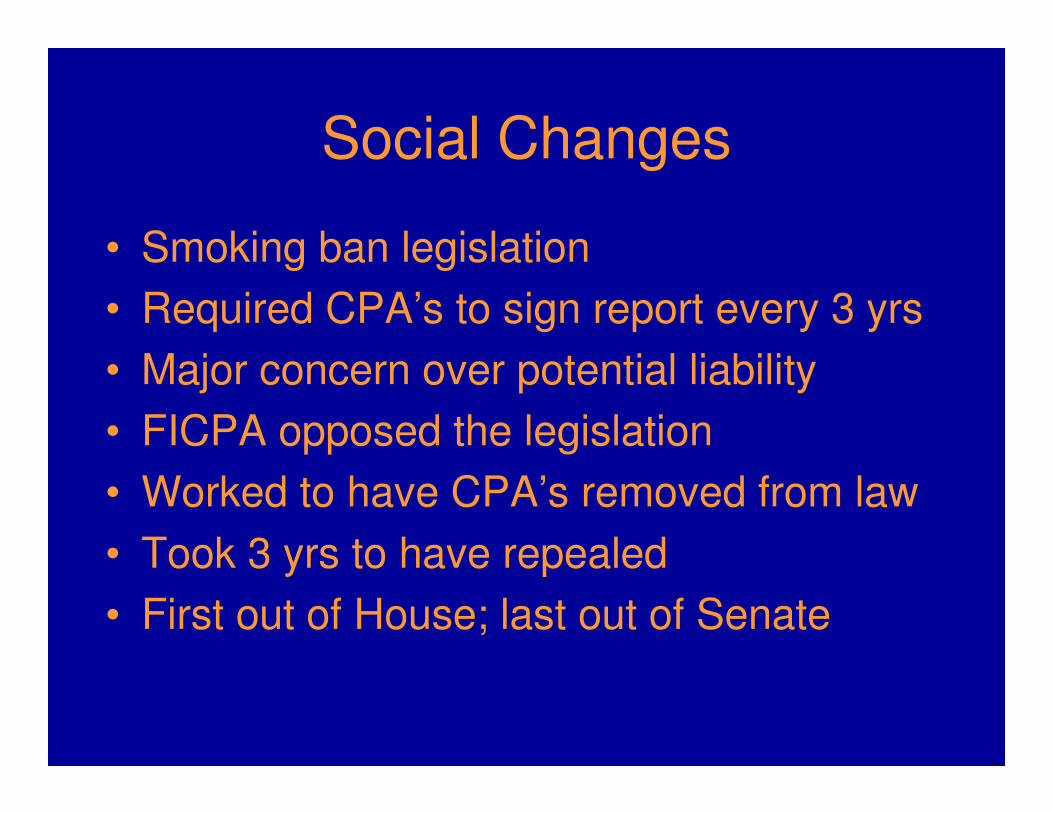

• Smoking ban legislation

• Required CPA’s to sign report every 3 yrs

• Major concern over potential liability

• FICPA opposed the legislation

• Worked to have CPA’s removed from law

• Took 3 yrs to have repealed

• First out of House; last out of Senate

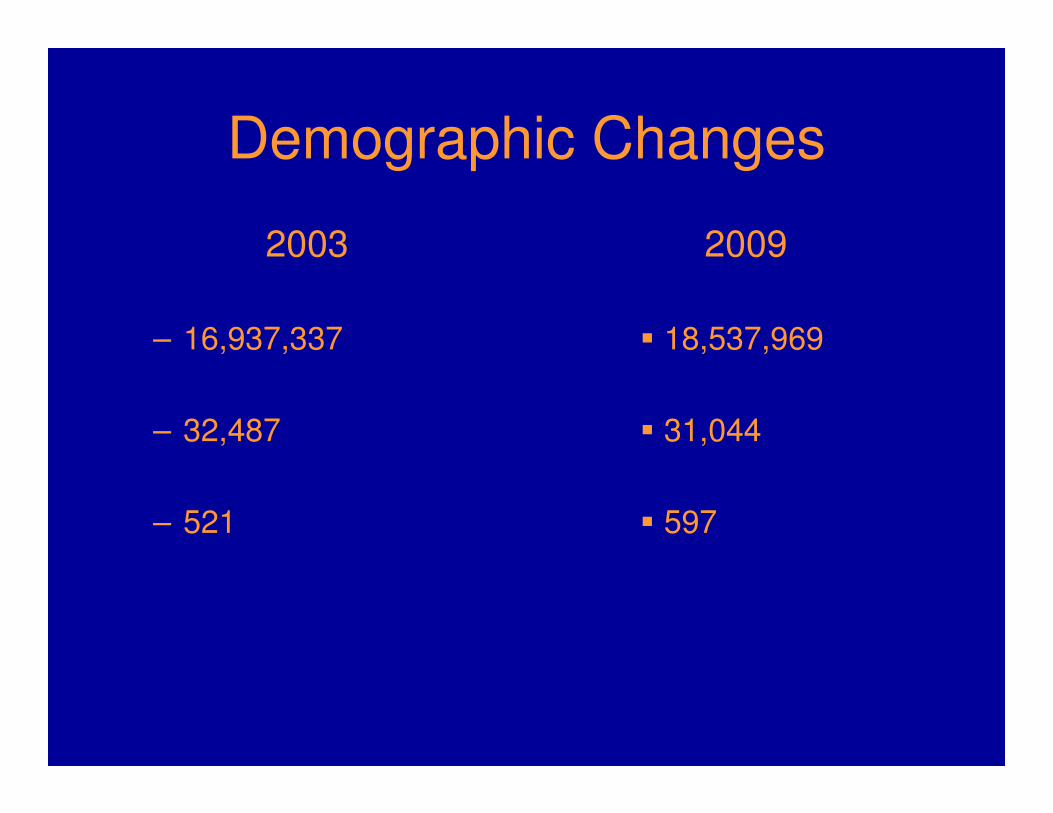

Demographic Changes

2003

– 16,937,337

– 32,487

– 521

2009

� 18,537,969

� 31,044

� 597

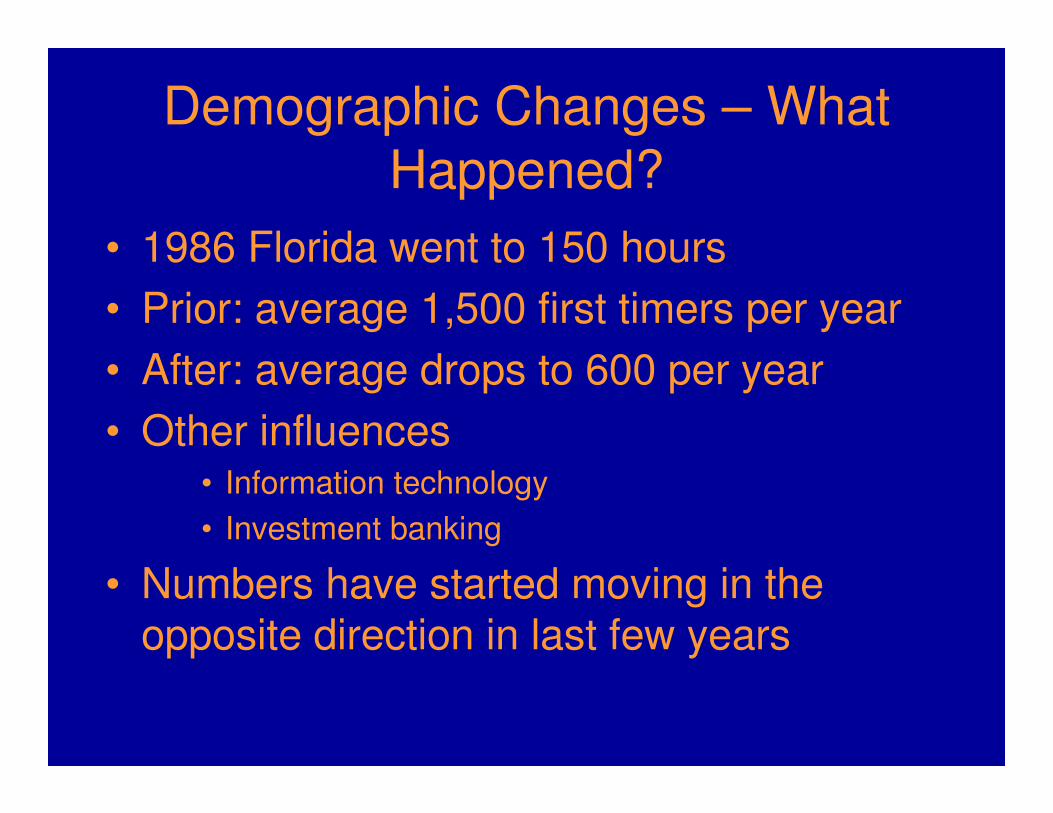

Demographic Changes – What Happened?

• 1986 Florida went to 150 hours

• Prior: average 1,500 first timers per year

• After: average drops to 600 per year

• Other influences• Information technology

• Investment banking

• Numbers have started moving in the opposite direction in last few years

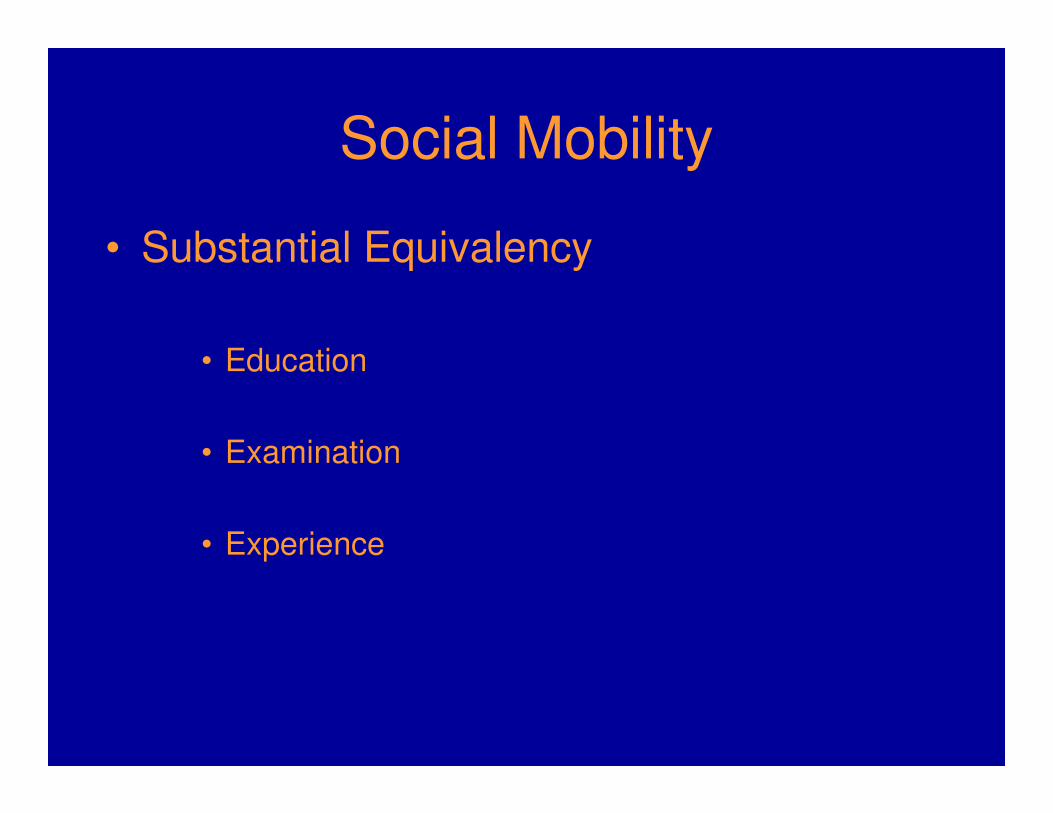

Social Mobility

• Substantial Equivalency

• Education

• Examination

• Experience

Who needs a Florida License?Chapter 473.3101

1) Each sole proprietor, partnership, corporation, limited liability company, or any other firm seeking to engage in the practice of public accounting, as defined in s. 473.302(8)(a), in this state must file an application for licensure with the department and supply the information the board requires. An application must be made upon the affidavit of a sole proprietor, general partner, shareholder, or member who is a certified public accountant.

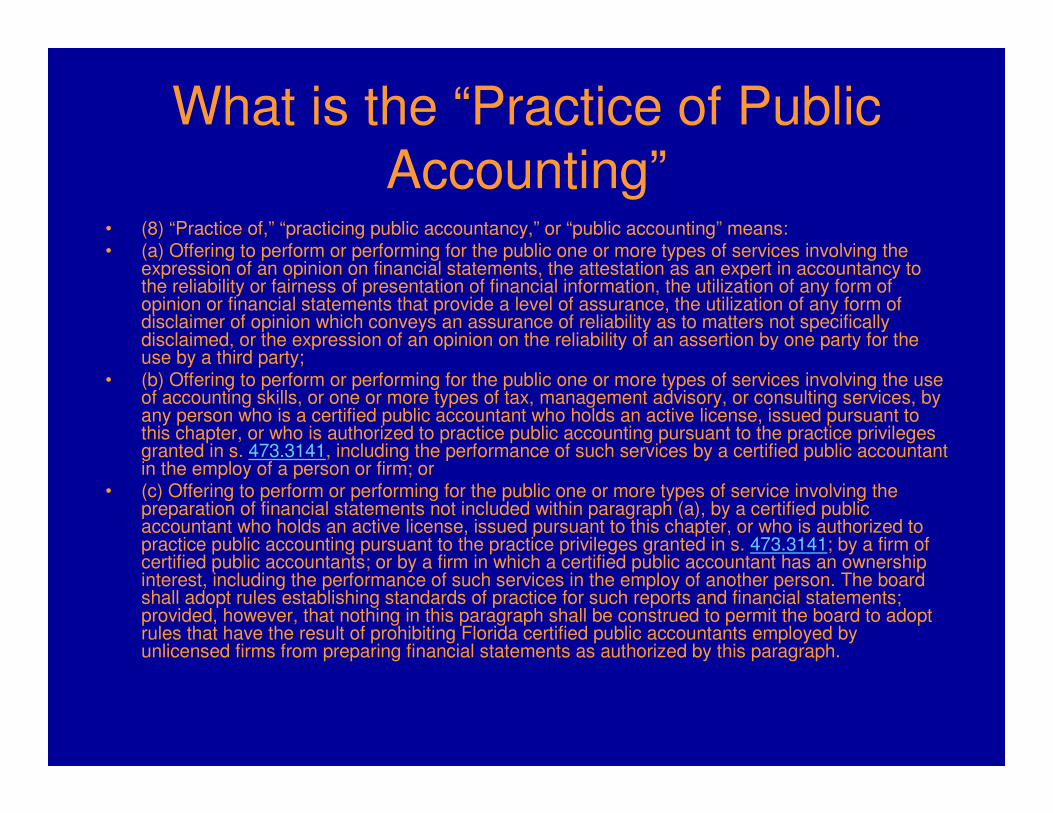

What is the “Practice of Public Accounting”

• (8) “Practice of,” “practicing public accountancy,” or “public accounting” means:• (a) Offering to perform or performing for the public one or more types of services involving the

expression of an opinion on financial statements, the attestation as an expert in accountancy to the reliability or fairness of presentation of financial information, the utilization of any form of opinion or financial statements that provide a level of assurance, the utilization of any form of disclaimer of opinion which conveys an assurance of reliability as to matters not specifically disclaimed, or the expression of an opinion on the reliability of an assertion by one party for the use by a third party;

• (b) Offering to perform or performing for the public one or more types of services involving the use of accounting skills, or one or more types of tax, management advisory, or consulting services, by any person who is a certified public accountant who holds an active license, issued pursuant to this chapter, or who is authorized to practice public accounting pursuant to the practice privileges granted in s. 473.3141, including the performance of such services by a certified public accountant in the employ of a person or firm; or

• (c) Offering to perform or performing for the public one or more types of service involving the preparation of financial statements not included within paragraph (a), by a certified public accountant who holds an active license, issued pursuant to this chapter, or who is authorized to practice public accounting pursuant to the practice privileges granted in s. 473.3141; by a firm of certified public accountants; or by a firm in which a certified public accountant has an ownership interest, including the performance of such services in the employ of another person. The board shall adopt rules establishing standards of practice for such reports and financial statements; provided, however, that nothing in this paragraph shall be construed to permit the board to adopt rules that have the result of prohibiting Florida certified public accountants employed by unlicensed firms from preparing financial statements as authorized by this paragraph.

Mobility Licensure• 3. If my state of licensure has Mobility or if the Florida Board of

Accountancy determines that I meet the Mobility criteria set forth in section 5 of the Uniform Accountancy Act, are there any circumstance that would still require me to get a license? Yes – see below:

• Any individual or firm with an office in Florida which uses the title “CPA,”“CPA firm,” or any other title, designation, abbreviations, or device tending to indicate that the firm practices public accounting in Florida, would be required to meet the licensure requirements of a Florida CPA as set forth in s. 473. 308, s. 473. 309 and s. 473. 3101.

• Any firm that does not have an office in Florida but performs one or more types of services involving the expression of an opinion (compilations, reviews, and audits) on financial statements, the attestation as an expert in accountancy to the reliability or fairness of presentation of financial information, the utilization of any form of opinion or financial statements that provide a level of assurance, the utilization of any form of disclaimer or opinion which conveys an assurance of reliability as to matters not specifically disclaimed, or the expression of an opinion on the reliability of an assertion by one party for the use by a third party for a client having its home office in Florida must obtain a Florida firm license.

Economic Pressure

• State wide consolidation

• Help spending our money

• From positive to negative to positive

• Reduction of cost of oversight

• Increasing fees and penalties

• Monitor impact of mobility

• Statement of estimated Regulatory Costs

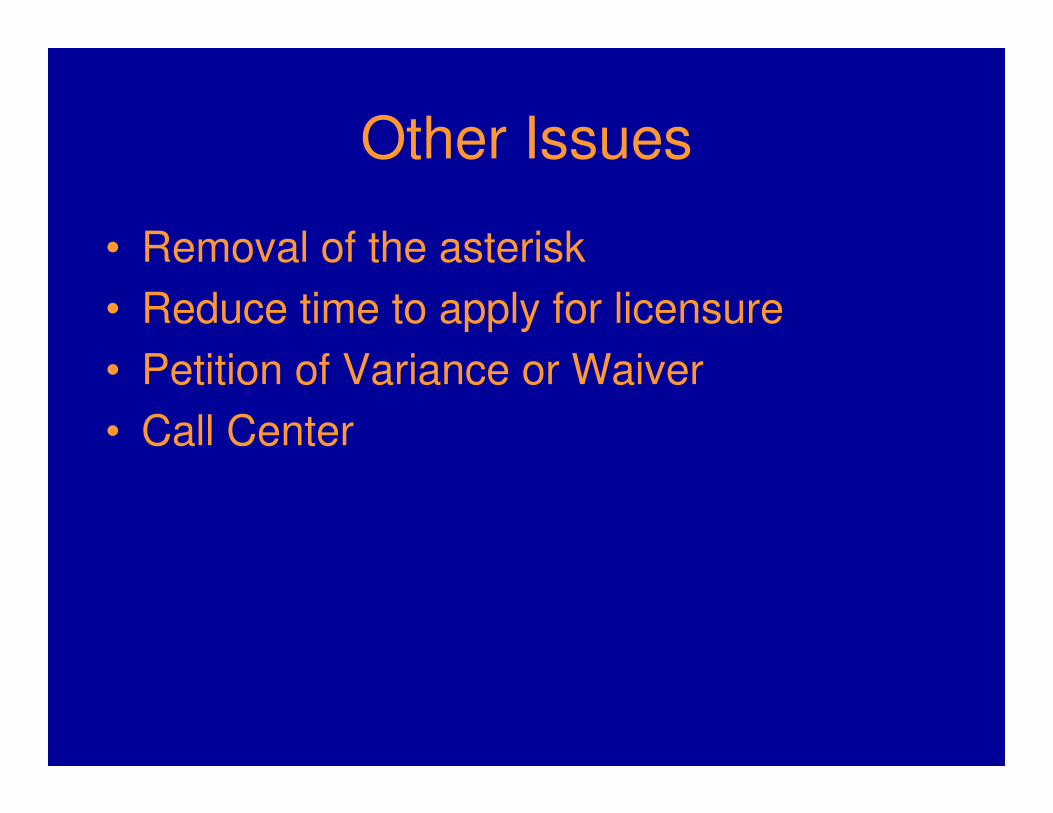

Other Issues

• Removal of the asterisk

• Reduce time to apply for licensure

• Petition of Variance or Waiver

• Call Center

Staying out of Trouble(Risk assessment for your practice)

• Complaints filed against a Florida CPA» From the XXXX’s

» Regulatory authorities

» Competitors

» Blamers

Staying out of Trouble(Risk assessment for your practice)

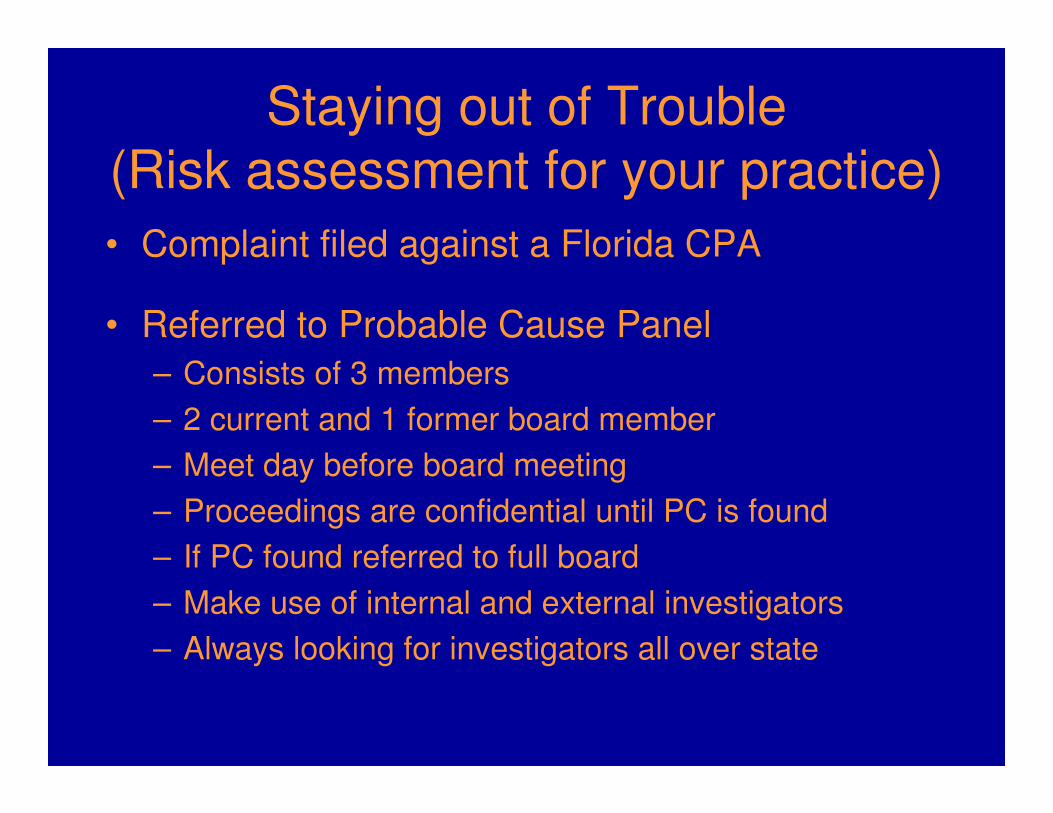

• Complaint filed against a Florida CPA

• Referred to Probable Cause Panel

– Consists of 3 members

– 2 current and 1 former board member

– Meet day before board meeting

– Proceedings are confidential until PC is found

– If PC found referred to full board

– Make use of internal and external investigators

– Always looking for investigators all over state

Staying out of Trouble(Risk assessment for your practice)

• Options for the Probable Cause Panel• Close case with no action

• Letter of Guidance

• Finding of Probable Cause

• Options for Board• Reprimand to Revocation

• Fines up to $5,000 per violation

• Penalties set forth in the Rules Ch 61

• COST$

Staying out of Trouble(Risk assessment for your practice)

Let’s make a deal

Staying out of Trouble(Risk assessment for your practice)

Maybe they’ll just go away

Staying out of Trouble(Risk assessment for your practice)

Hide and seek

Staying out of Trouble(Risk assessment for your practice)

Playing for both sides

Staying out of Trouble(Risk assessment for your practice)

One hit wonders

Staying out of Trouble(Risk assessment for your practice)

No good deed goes unpunished

Staying out of Trouble(Risk assessment for your practice)

You gotta pay to play

Staying out of Trouble(Risk assessment for your practice)

What’s yours is mine

Staying out of Trouble(Risk assessment for your practice)

Play nicely - especially with the IRS

Staying out of Trouble(Risk assessment for your practice)

Too close for comfort

Staying out of Trouble(Risk assessment for your practice)

If you play with fire …….

Issues to Watch

• Check the box reporting

• Reporting convictions under Chapter 455

• Mandatory peer review

• Appointment of new members to the board

Grounds for Discipline

• FS Chapter 455.227(1)(t)

– “Failing to report in writing to the board or,…to the department within 30 days after the licensee is convicted or found guilty of, or entered a plea of nolo contendere or guilty to, regardless of adjudication, a crime in any jurisdiction.”

Florida Board of Accountancy

• Web Site

– http://www.myfloridalicense.com/dbpr/cpa/index.html

• Division Home

• Check Status

• Minority Scholarships

• Statutes & Rules

• Forms

• FAQ’s