fiscal decentralization and intergovernmental fiscal...

TRANSCRIPT

Fiscal Decentralization and Intergovernmental Fiscal

Relations: A Cross-Country Analysis

LUIZ R. DE MELLO JR *

University of Kent, UK

Summary. Ð Fiscal decentralization consists primarily of devolving revenue sources andexpenditure functions to lower tiers of government. By bringing the government closer to thepeople, ®scal decentralization is expected to boost public sector e�ciency, as well as accountabilityand transparency in service delivery and policy-making. Decentralization also entails greatercomplexity in intergovernmental ®scal relations, and coordination failures in ®scal relations arelikely to have a bearing on ®scal positions, nationally and subnationally. Evidence provided in thispaper for a sample of 30 countries suggests that coordination failures in intergovernmental ®scalrelations are likely to result in a de®cit bias in decentralized policy-making, particularly in the caseof developing countries, which may not meet important requirements for successful decentraliza-tion. Ó 2000 Elsevier Science Ltd. All rights reserved.

Key words Ð federalism, policy failures, ®scal policy

1. INTRODUCTION

In recent years, a growing number of coun-tries around the world have embarked onambitious ®scal decentralization programsconsisting, in broad terms, of reassigningexpenditure functions and devolving revenuesources to subnational governments (states/provinces, and/or municipalities/communes).The decentralization of expenditure functionsand revenue sources also calls for decentral-ization in ®scal policy-making. The latterincludes greater autonomy in debt manage-ment, tax administration, and budget execu-tion, so that the task of providing public goodsand services and performing standard publicsector functions can be shared across levels ofgovernment. The key motivation for decen-tralization in a number of countries has beenthe disenchantment of the electorate with theability of the central government to meet ade-quately the increasing demand for public goodsand services (Tanzi, 1999).

The potential bene®ts of devolving ®scalresponsibilities to subnational levels ofgovernment are increased e�ciency in servicedelivery, and reduced information and trans-action costs associated with the provision ofpublic goods and services (World Bank, 1997).Based on the public ®nance principle of subs-idiarity, 1 the performance of the public sectorcan be enhanced by taking account of local

di�erences in culture, environment, endowmentof natural resources, and economic and socialinstitutions. Local preferences and needs arebelieved to be best met by local, rather thannational, governments. Information on theselocal preferences and needs can be extractedmore cheaply and accurately by local govern-ments, which are ``closer'' to the people andhence more identi®ed with local causes. In thisrespect, accountability and transparency ingovernment actions can also be enhanced bybringing expenditure assignments closer torevenue sources. Streamlining public sectoractivities and encouraging the development oflocal democratic traditions are also regarded asimportant goals of ®scal decentralization.Finally, to the extent that ®scal decentralizationpromotes allocative e�ciency, it is expected tohave a bearing on macroeconomic governance.Less severe economy-wide ®scal imbalancesand debt-overhang problems improve macro-economic performance, and scarce publicresources can be channeled away from de®cit®nancing and debt servicing toward fundinggrowth-enhancing, externality-rich spending.

Decentralization is not, however, withoutpitfalls. A key issue in decentralization is the

World Development Vol. 28, No. 2, pp. 365±380, 2000Ó 2000 Elsevier Science Ltd. All rights reserved

Printed in Great Britain0305-750X/00/$ - see front matter

PII: S0305-750X(99)00123-0www.elsevier.com/locate/worlddev

* The author is indebted to two anonymous referees for

comments on a previous version of this paper. The usual

disclaimer applies. Final revision accepted: 15 June 1999.

365

coordination of intergovernmental ®scal rela-tions, which has puzzled theoreticians andpractitioners in recent years (Poterba, 1996).Given the increased complexity in coordinatinggovernment actions when lower levels ofgovernment enjoy greater autonomy in policy-making, the key policy challenge in decentral-ization programs is to design and develop anappropriate system of multilevel public ®nancesin order to provide local public services e�ec-tively and e�ciently while, at the same time,maintaining macroeconomic stability. 2 Thetask consists of managing intergovernmental®scal relations by taking into account, on theone hand, the growing need for local publicgoods and services and, on the other, theimportance of preserving ®scal discipline,nationally and subnationally. When newbudgetary rights and responsibilities areassigned to subnational governments, institu-tional clarity and transparency should bepromoted in the budget-making process, suchthat spending matches revenues at the subna-tional level.

Without special attention to institutionalclarity and transparency, intergovernmental®scal relations may su�er from coordinationfailures. These coordination failures mayinduce subnational governments to spendine�ciently and beyond their means, when®scal policy is designed and implemented in adecentralized fashion. These policy failurestend to manifest themselves as a de®cit bias andhigher costs of borrowing given the riskpremium associated with a higher probabilityof default (Poterba & Rueben, 1997; de Mello,1998). Fiscal decentralization may thereforeaggravate, rather than reduce, ®scal imbal-ances 3 and consequently endanger overallmacroeconomic stability (PrudÕhomme, 1995;Huther & Shah, 1996; Ter-Minassian, 1999),unless subnational governments are committedto ®scal discipline, and the decentralizationpackage includes incentives for prudence indebt and expenditure management. The impo-sition of stringent constraints on subnationalindebtedness and e�ective monitoring ofsubnational ®scal positions are additionalimportant prerequisites for successful ®scaldecentralization, in addition to the availabilityof expertise at the subnational level to managee�ciently an increased volume of resources(Fukasaku & de Mello, 1998).

In short, with regard to the three traditionalMusgravian functions of government, thepitfalls of ®scal decentralization are related

more closely to macroeconomic stability andredistribution, while its bene®ts involve gains inallocative e�ciency (Inman & Rubinfeld, 1997).Against this background, the objective of thispaper is to shed more light on the relationshipbetween ®scal decentralization and budgetbalances from a cross country perspective.Attention is focused on a sample of 30 coun-tries for which internationally comparablepublic ®nance indicators are available in theIMFÕs Government Financial Statistics for asu�ciently long time span over 1970±95 and forat least two levels of government.

The remainder of the paper is organized asfollows. Section 2 provides an overview ofintergovernmental ®scal relations and presentsbasic public ®nance indicators for the sample ofcountries under examination. These indicatorsallow for a deeper analysis of the extent of ®scaldecentralization in di�erent economies, so thata few stylized facts can be highlighted. Section 3describes the most important sources of coor-dination failures examined in the literature.Section 4 provides empirical evidence andsection 5 concludes.

2. INTERGOVERNMENTAL FISCALRELATIONS: AN OVERVIEW

(a) How do public ®nances di�er acrossgovernments levels?

Public ®nances di�er signi®cantly acrossgovernment levels for a number of reasons.First, in terms of revenue mobilization, the taxbases that are e�cient and simple to administerby local governments tend to be few andnarrow (Bird, 1992). Non-tax revenues (usercharges, rents, royalties, fees) tend to be limitedin scope and revenue-generating capacity.Local tax bases are narrow due to the possi-bility of tax exportation, externalities in theprovision of public goods and services, factormobility, and economies of scale. Broad taxbases are best managed by higher levels ofgovernment. As a result, if subnationalgovernments are to be important providers ofpublic goods and services, it is necessary forhigher-level jurisdictions to share part of theirrevenues with subnational governments tobridge the gap between spending and revenuesmobilized locally. 4

Second, with regard to expenditure manage-ment, if budgets are to be balanced, subna-tional spending is constrained by (i) the

WORLD DEVELOPMENT366

revenue-raising capacity of subnationalgovernments which, as suggested above, tendsto be limited, and (ii) vertical and/or horizontalrevenue-sharing. The optimal size of subna-tional governments is hence determined on taxe�ciency grounds, given the breadth of the taxbases that are best managed by these jurisdic-tions, and the willingness of higher-levelgovernments to devolve expenditure functionsto subnational governments, given that ®nanc-ing these expenditures may require extensiverevenue-sharing. An important consequence ofthe above is that the composition of subna-tional revenues plays a crucial role in deter-mining the level of autonomy over expendituremanagement enjoyed by subnational govern-ments. For instance, local revenue mobilizationis boosted when subnational governmentscontrol important tax bases. This gives themmore legitimacy over the use of these resources,and hence leeway to manage them according totheir own preferences and needs.

In the case of reliance on revenue-sharing to®nance subnational spending, which can behorizontal and/or vertical, conditionality onhow sharable funds are spent by subnationalgovernments is likely to reduce their expendi-ture management autonomy. Fiscal decentral-ization may in this case turn out to be littlemore than mere delegation: subnationalgovernments become spending agents of higherlevels of government with limited decision-making autonomy over how public funds arespent. The merit of delegation in expendituremanagement is that it increases transparencyand accountability in service delivery bybringing public sector spending closer totaxpayers. Local preferences and needs may notbe entirely taken into account, however, giventhat conditionality on spending mandatesre¯ects the preferences of the central, ratherthan local, government over particular expen-diture functions. 5

Policy-making autonomy over shared reve-nues allows for local preferences to be takeninto account, when both resources and deci-sion-making mandates are decentralized. Lackof conditionality in revenue-sharing may alsopose additional challenges. First, it may reducethe incentive for subnational governments tomanage shared funds e�ciently, and weakenthe scope for coordination across governmentlevels. 6 Second, when preferences over expen-diture functions do not coincide, the recipientmay use the shared funds to ®nance expendi-tures that reduce the utility of the donor. This is

particularly important at the horizontal level,when several recipients use shared funds to®nance externality-generating expenditures andhave di�erent preferences over those spendingfunctions. Conditional tax-sharing and devo-lution allow for service delivery at lower oper-ational costs while, at the same time, reducingthe risk of free-riding in the case of externality-rich, horizontally-®nanced spending.

Third, despite greater autonomy in budget-making due to ®scal decentralization, subna-tional governments tend to have limited powerin debt issuance and management. These limi-tations may be institutional, given speci®cbudget rules, and/or market-based. Budgetrules may be of several types. 7 For instance, inmany cases, subnational governments may beprohibited from using de®cit ®nancing for longperiods of time, and local legislatures may beconstrained to approve balanced budgets only.Ex post budget imbalances may occur despiteanti-de®cit provisions ex ante, as a result of, forinstance, adverse shocks, wrong forecasts ofrevenues and expenditures, and failure toaccount for contingent liabilities. Should expost budget imbalances occur, subnationalgovernments may be constrained to correctsuch imbalances in a horizon of one or two®scal years (``no carry-over'' constraint). 8 Iflong-term ®nancing is needed, in many coun-tries, subnational governments may be allowedto issue ``golden-rule,'' as opposed to generalobligation, debt. Grants and transfers areadditional instruments used to ®nance invest-ment spending that would otherwise over-whelm the ®scal capacity of subnationalgovernments. In general, the merits of ®scalrules have to be assessed in the light of thetradeo� between short-run budgetary ¯exibilityand long-run ®scal sustainability. Whereasrules tend to impose ®scal discipline at lowerlevels of government, they also limit the abilityof these governments to ®nance public provi-sion at the local level, smooth taxes, and carryout countercyclical demand management(Bohn & Inman, 1996; Inman, 1996).

Subnational government indebtedness mayalso be constrained by market forces. In shal-low capital markets, there may be a shortage ofpotential buyers of subnational debt, and henceno formal market for subnational bonds. Inthis case, the central government itself may bethe main supplier of credit to subnationalgovernments. This seems to be the case in anumber of countries, and subnational bondsare little more than promissory notes signed by

FISCAL DECENTRALIZATION 367

subnational governments and held by thecentral government. When these bonds areactually traded, however, market discipline islikely to ensure ®scal restraint at the local level,despite the smaller size of the subnationalgovernment debt market, relative to that of thecorporate sector or the central government.When subnational debt is traded, market-in-duced discipline is likely to follow from stricter,corporate sector-like accounting standards,transparency in budgeting, independent audit-ing, and timely disclosure of subnational public®nance data. These factors are complementaryin limiting the scope for cosmetic accounting tocircumvent rigid balanced-budget rules. Creditrating agencies are also likely to monitorsubnational governments and contribute to thedissemination of best practices and highaccounting standards, which is likely toimprove governance in the public sector(Capeci, 1994).

(b) Some preliminary evidence: basic public®nance indicators

In what follows, attention is focused on asample of 30 countries for which public ®nancedata, such as government spending and ®scalbalances, are disaggregated between the centralgovernment and subnational governments 9 inthe IMFÕs Government Financial Statistics, for1970±95. 10 Countries with a sizeable discrep-ancy (over ®ve percentage points) in the shareof subnational spending in total public sectorspending are presented in two subsamples.These countries and subsamples are Argentina(1970±85 and 1986±95), Brazil (1970±89 and1990±95), Chile (1970±80 and 1981±95), Thai-land (1970±80 and 1981±95), South Africa(1970±83 and 1984±95), Norway (1970±78 and1979±95), and Spain (1970±89 and 1990±95).

Given the constraints imposed by the data, anumber of public ®nance indicators can beconstructed and a few stylized facts can behighlighted from a crosscountry perspective.

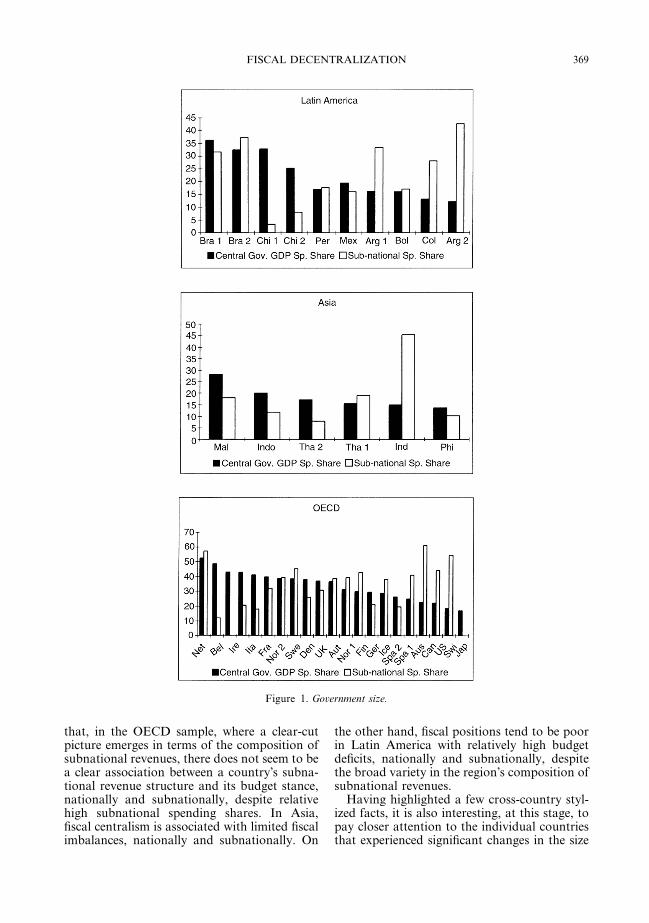

First, the relative importance of di�erentlevels of government in the provision of publicgoods and services is re¯ected in the size ofsubnational governments. Size can be measuredin absolute terms, as in the case of the expen-diture-GDP ratio, or, more interestingly, inrelative terms, as in the case of subnationalspending relative to central governmentspending. As for the absolute size of govern-ment, Figure 1 suggests that governments tendto be smaller in Latin America, and particularly

Asia, than in the OECD sample. It is widelyaccepted that the demand for public goods andservices increases with income such thatgovernment spending tends to be larger inricher countries, ceteris paribus. Centralgovernment spending ratios range from 20% ofGDP in Asia, to 40% in the European countriesof the OECD sample. In terms of relativegovernment sizes, the subnational share of totalgovernment spending is below 5% in Asia, andranges from 10% to 40% in Latin America, andfrom 12% to 60% in the OECD sample.Subnational governments tend to be large incountries where the central government is smallin both OECD and Latin American countries.This is nevertheless not true in Asia, with theexception of India, where countries with smallcentral governments also tend to have verysmall subnational government spending shares.In the OECD area and Latin America, unlikeAsia, a reduction in central governmentspending is achieved chie¯y by delegatingpublic sector functions and spending responsi-bilities to subnational governments, thusincreasing their share in total governmentspending.

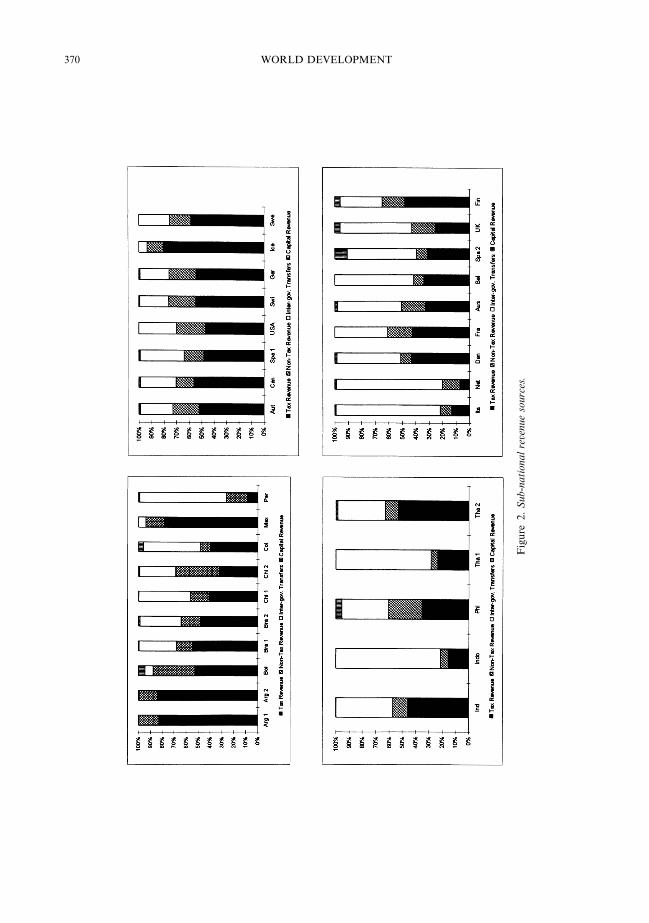

Second, with regard to the composition ofsubnational revenues, Figure 2 suggests that, inAsia, subnational governments rely heavily ontransfers from the center. In the OECD area,there is a clear distinction between the federa-tions (Austria, Canada, Switzerland, Germany,United States), where emphasis is placed onlocal tax revenue mobilization; and the Euro-pean countries (as well as Australia), whereintergovernmental transfers prevail as the mainsource of ®nance of subnational spending. Thepicture is less clear-cut in Latin America. Forinstance, Peru, Bolivia and Mexico di�ersigni®cantly as to how subnational spending is®nanced, despite comparable subnationalspending shares. In the case of Peru, emphasisis placed on intergovernmental transfers andnon-tax revenues, whereas local tax revenuemobilization prevails in Bolivia and Mexico.On the other hand, in Brazil, Chile andColombia, subnational spending shares arehigher and subnational ®nancing is split moreevenly between intergovernmental transfersand local tax revenue mobilization.

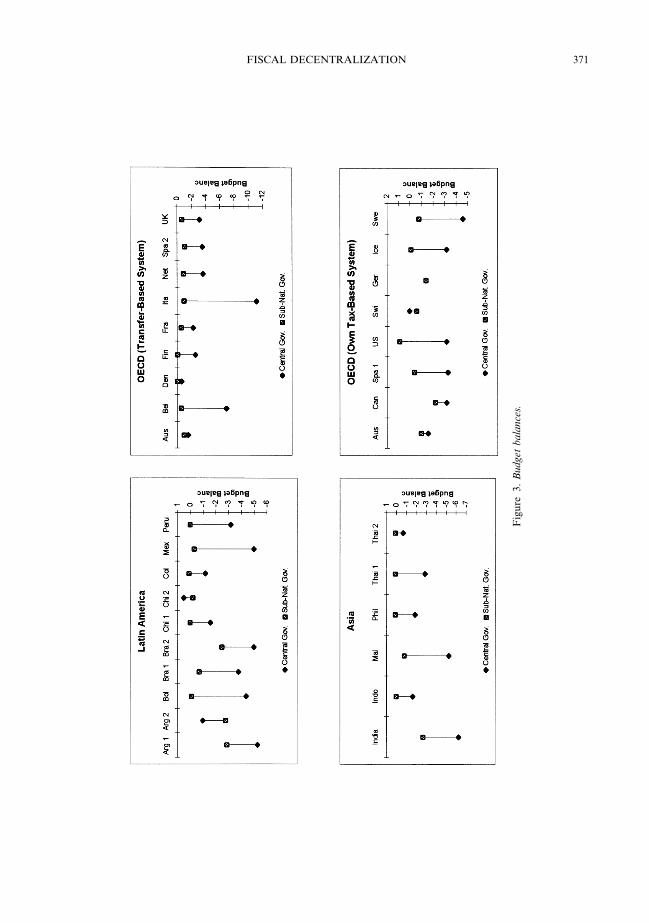

Third, budget de®cits are much smaller at thesubnational, rather than central government,level. This re¯ects the discussion above aboutthe limited autonomy of subnational govern-ments in terms of debt and expendituremanagement. Inspection of Figure 3 reveals

WORLD DEVELOPMENT368

that, in the OECD sample, where a clear-cutpicture emerges in terms of the composition ofsubnational revenues, there does not seem to bea clear association between a countryÕs subna-tional revenue structure and its budget stance,nationally and subnationally, despite relativehigh subnational spending shares. In Asia,®scal centralism is associated with limited ®scalimbalances, nationally and subnationally. On

the other hand, ®scal positions tend to be poorin Latin America with relatively high budgetde®cits, nationally and subnationally, despitethe broad variety in the regionÕs composition ofsubnational revenues.

Having highlighted a few cross-country styl-ized facts, it is also interesting, at this stage, topay closer attention to the individual countriesthat experienced signi®cant changes in the size

Figure 1. Government size.

FISCAL DECENTRALIZATION 369

Fig

ure

2.

Sub-n

ati

onal

reve

nue

sourc

es.

WORLD DEVELOPMENT370

Fig

ure

3.

Budget

bala

nce

s.

FISCAL DECENTRALIZATION 371

of subnational governments in the period underexamination. In the case of Chile, the degree of®scal autonomy at the subnational level,measured as the share of taxes in total reve-nues, has fallen dramatically since 1981, despitesigni®cant ®scal decentralization in the period,given the increase in the share of subnationalspending (Figure 1). Decentralization did notworsen subnational budget de®cits signi®cantlyin Chile (Figure 3), and an increase in subna-tional spending was ®nanced by higher subna-tional non-tax revenue (fees, sales, ®nes,royalties, etc.), instead of intergovernmentaltransfers and/or local tax revenues. In Brazil,the fall in the average subnational tax revenueshare after 1989 was partly o�set by an increasein intergovernmental transfers, therebydiscouraging local revenue mobilization, giventhe modest increase in the non-tax revenueshare. Turning to Asia, in the case of Thailand,the countryÕs ®scal consolidation e�ort of the1980s involved a signi®cant reduction in thesubnational spending share in favor of thecentral government. This process of ®scalcentralization also led to a drastic change in thecomposition of subnational revenues fromintergovernmental transfers toward local taxesin a policy move in favor of local revenuemobilization. In the OECD sample, SpainÕsdecentralization initiative favored revenue-sharing to ®nance growing subnational spend-ing (Figure 2).

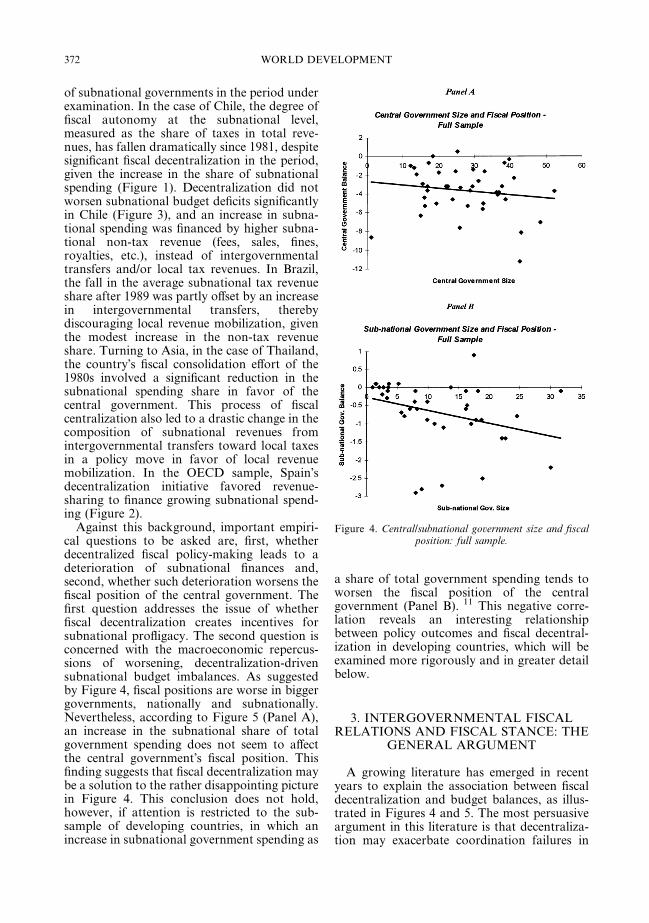

Against this background, important empiri-cal questions to be asked are, ®rst, whetherdecentralized ®scal policy-making leads to adeterioration of subnational ®nances and,second, whether such deterioration worsens the®scal position of the central government. The®rst question addresses the issue of whether®scal decentralization creates incentives forsubnational pro¯igacy. The second question isconcerned with the macroeconomic repercus-sions of worsening, decentralization-drivensubnational budget imbalances. As suggestedby Figure 4, ®scal positions are worse in biggergovernments, nationally and subnationally.Nevertheless, according to Figure 5 (Panel A),an increase in the subnational share of totalgovernment spending does not seem to a�ectthe central governmentÕs ®scal position. This®nding suggests that ®scal decentralization maybe a solution to the rather disappointing picturein Figure 4. This conclusion does not hold,however, if attention is restricted to the sub-sample of developing countries, in which anincrease in subnational government spending as

a share of total government spending tends toworsen the ®scal position of the centralgovernment (Panel B). 11 This negative corre-lation reveals an interesting relationshipbetween policy outcomes and ®scal decentral-ization in developing countries, which will beexamined more rigorously and in greater detailbelow.

3. INTERGOVERNMENTAL FISCALRELATIONS AND FISCAL STANCE: THE

GENERAL ARGUMENT

A growing literature has emerged in recentyears to explain the association between ®scaldecentralization and budget balances, as illus-trated in Figures 4 and 5. The most persuasiveargument in this literature is that decentraliza-tion may exacerbate coordination failures in

Figure 4. Central/subnational government size and ®scalposition: full sample.

WORLD DEVELOPMENT372

intergovernmental ®scal relations, whichdiscourage ®scal discipline, ®rst at the subna-tional level and subsequently at the economy-wide level. The most important sources ofcoordination failures examined in the theoryare agency problems arising from the delega-tion of ®scal powers to subnational govern-ments, and ``common pool'' problemsassociated with funding decentralized govern-ment spending through revenue-sharing.

In a nutshell, agency problems are due to theasymmetry of information on the costs andbene®ts of government spending between thecenter and the subnational governments towhich ®scal powers are delegated. In broadterms, the association between delegation andinformation asymmetry is two-fold. On the onehand, delegation allows the center to providegoods and services according to local marketinformation and, by separating responsibilities,more powerful incentives can be put in place tofoster e�ciency. Because local jurisdictions canidentify community preferences more easily andcheaply, decentralized policy-making tends to

reduce information costs and boost allocativee�ciency (Radner, 1993; Bolton & Dewatrip-ont, 1994; Martimort, 1996). Delegation bringsthe government ``closer'' to the people, therebyincreasing accountability in, and favoringsocietyÕs scrutiny of, public sector actions.Information asymmetries between society andthe government can therefore be reduced bydecentralizing ®scal responsibilities through thedevolution of spending assignments to localgovernments.

On the other hand, by reducing the ``infor-mational distance'' between the governmentand societyÐor the bene®ciaries of the provi-sion of public goods and servicesЮscaldecentralization tends to increase the distancebetween the center and the decentralizedagencies or subnational governments to which®scal responsibilities are devolved or delegated.This loss of control of the center over decen-tralized agencies and/or subnational govern-ments entails an e�ciency loss in delegation,which increases with the distance between bothgovernment levels, and hence renders theacquisition and processing of informationwithin the government more costly (Tirole,1994; Gilbert & Picard, 1996). On the expen-diture side, the central government may beunable to monitor e�ciency in expendituremanagement and service delivery. On therevenue side, when important tax bases aredevolved to subnational governments, agencyproblems arise given that the central govern-ment may be unable to monitor how e�cientlysubnational governments utilize their revenuesources. If the devolution of important taxbases to subnational governments reduces e�-ciency in revenue mobilization across govern-ment levels, and induces underutilization ofsubnational tax bases, central and subnationalbudget positions are likely to deteriorate.Moreover, the transfer of revenue sources tosubnational governments, following the devo-lution of expenditure functions, may deprivethe center of important revenue sources in thesecountries, thus generating imbalances at thecenter (Tanzi, 1995). 12

The essence of ``common pool'' problems 13

is that, as suggested above, local revenuemobilization is limited at the subnational level,and revenue-sharing is an important mecha-nism to correct vertical imbalances in inter-governmental ®scal relations. Revenue-sharingis not, however, without pitfalls. It drives awedge between expenditures and revenuesources in subnational jurisdictions, and hence

Figure 5. Subnational/central government ®scal position.

FISCAL DECENTRALIZATION 373

the costs and bene®ts of public sector provi-sion. As a result, if a large share of subnationalspending is ®nanced through revenue-sharing,subnational governments may face the incen-tive to underutilize their own tax bases at theexpense of national sharable revenues (Inman& Rubinfeld, 1996). In doing so, they minimizethe costs of decentralized provision borne bylocal taxpayers, which can be ®nanced by acommon pool of resources mobilized elsewherein the economy. In this case, the burden ofproviding public goods and services can beshared across government jurisdictions,whereas the bene®ts of public sector spendingcan be internalized and generate a politicalpayo� to local governments. In addition,overspending can be attributed to ``commonpool'' funding because free-riding inducescompetition among subnational governmentsto secure a larger portion of sharable funds inthe form of grants and transfers from thecentral government.

An additional type of ``common pool''problem which has an immediate adverseimpact on the central governmentÕs budgetposition is the following. In the case of rigidrevenue-sharing arrangements, in which trans-fers are automatic, every time a centralgovernment raises taxes to improve its own®scal position, subnational governments receivea corresponding revenue bene®t which they arefree to spend. These windfall gains tend toinhibit the potential for reducing the consoli-dated ®scal de®cit by increasing the tax burden.This is also the case of national spendingprograms that are sponsored and fully fundedby the central government, without condition-ality and/or subnational cofunding. 14 Incen-tives to delay adjustment is anotherconsequence of the ``common pool'' problem,since individual jurisdictions have limitedincentives to act alone and strong incentives tofree-ride, if the burden of ®scal retrenchmentcan be shared horizontally across jurisdictionalborders, and vertically across governmentlevels. 15 Free-riding also induces overspendinggiven that each subnational government has anincentive to in¯ate its budget for fear of losingsharable revenues to competing jurisdictions.

Both problemsÐ``common pool'' andagencyÐare intertwined, given that decentral-ization implies delegation of spending functionsto subnational jurisdictions and hence createsvertical imbalances which tend to be correctedvia revenue-sharing. Policy recommendationsto solve one of these problems may well end up

exacerbating the other. Against this back-ground, in providing public goods and services,there seems to be a tradeo� between coordi-nation, which requires some degree of central-ization in policy-making, and the need forinformation on local needs and preferencesover public sector provision and service deliv-ery, which is better handled at the local level(Caillaud, Jullien & Picard, 1996). A strongcase can be made in favor of centralizedprovision and policy-making as far as distrib-utive and macroeconomic stabilization policiesare concerned. In this case, e�ciency gains,which are the main advantages of decentral-ization, may be dwarfed by the challenges ofensuring good macroeconomic governance and®scal discipline in a decentralized governmentstructure. In addition, both types of policy tendto be nationwide in scope, rather than regional,particularly in developing countries, thusrendering the potential gains of decentraliza-tion in terms of allocative e�ciency less prom-ising against the risks involved inmacroeconomic stabilization.

4. INTERGOVERNMENTALCOORDINATION FAILURES AND

FISCAL STANCE: STRONGEREVIDENCE

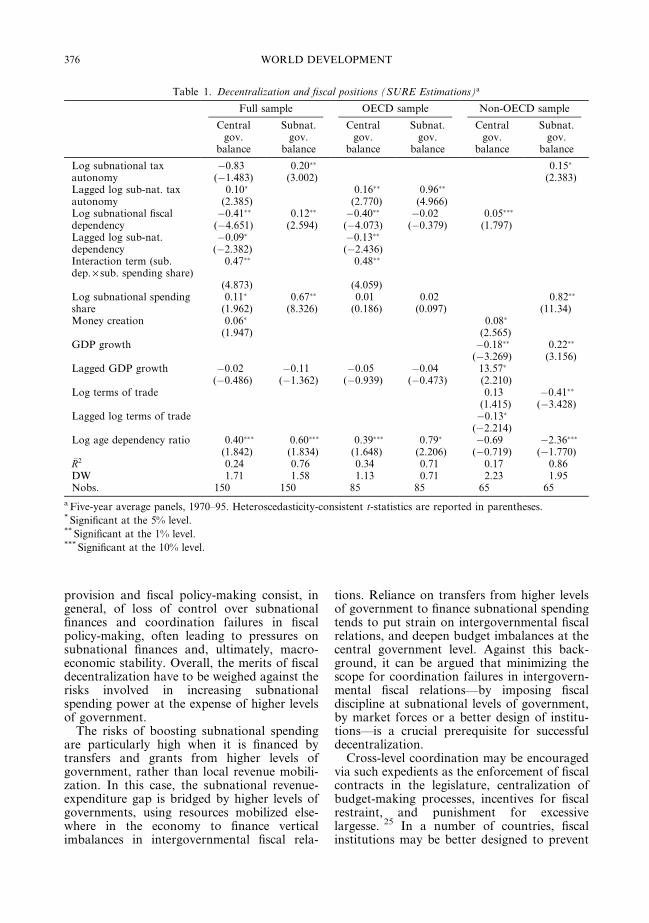

This section reports stronger empirical evi-dence on the relationship between ®scaldecentralization, coordination failures in inter-governmental ®scal relations, and budgetbalances. 16 Because coordination failurescannot be measured directly, their impact on®scal positions can be estimated indirectlywhen proxies for the potential sources ofcoordination failures are available. The budgetbalance, measured as the ratio of the ®scalde®cit to GDP, can be regressed on a set ofvariables of two types: 17 (a) the proxies for thepotential sources of coordination failures inintergovernmental ®scal relations, and (b) anumber of control variables which havebecome standard in the public ®nance literature(e.g., Roubini & Sachs, 1989; Alesina, Cohen &Roubini, 1993; Eichengreen & Bayoumi, 1994).

The proxies for coordination failures usedhere are as follows: (a) the subnationalgovernment size, which measures the extent of®scal decentralization and hence the scope forcoordination failures in intergovernmental®scal relations; (b) the subnational tax auton-omy indicator, which measures the subnational

WORLD DEVELOPMENT374

local revenue mobilization, and is thereforelikely to be a good proxy for moral hazards indecentralized policy-making; and (c) thesubnational dependency on intergovernmentaltransfers, which is a proxy for coordinationfailures due to ``common pool'' problems. Thecontrol variables 18 are as follows: moneycreation, GDP growth, the terms of trade, andthe age dependency ratio. Money creationproxies for the use of monetary, quasi-®scalde®cit-®nancing instruments; GDP growthcontrols for the cyclicality of ®scal policy, sincede®cits tend to fall in periods of expansion andincrease in economic downturns; the terms oftrade variable proxies for alternative sources ofnon-tax revenues; and the age dependency ratioproxies for longer-term, social security-relatedliabilities of the public sector, which are likelyto exacerbate structural imbalances.

The equation is estimated for a panel of 30countries for which the basic ®scal indicatorsshown in Figures 1±3 are available in theIMFÕs Government Finance Statistics. 19 Thevariables in the panel are constructed for ®ve-year averages during 1970±95 to smooth outtransitory ¯uctuations in the data. Given thatthe relationship between decentralization indi-cators and ®scal positions may di�er acrossbroad groups of countries, the equation isestimated for subsamples of 17 OECD and 13non-OECD countries. 20 The distinction bet-ween OECD and non-OECD countries alsore¯ects di�erences in institutional developmentacross countries, as OECD countries tend tohave more mature ®scal institutions than theircounterparts in the non-OECD sample. Theequations are also estimated simultaneouslyfor di�erent levels of government, to accountfor the information in the covariance of theerror terms in each equation.

The results of the estimations are reported inTable 1. The preliminary ®ndings provideprima facie evidence that ®scal stance is likelyto be a�ected by coordination failures due to``common pool'' and agency problems indecentralized policy-making, as hypothesizedabove. 21 An interaction term was included inthe regression to measure the combined impactof subnational ®scal dependency and spendingshares. This is because vertical imbalances tendto increase when subnational governments arelarge relative to the central government interms of their spending assignments. The mostimportant ®ndings are as follows.

First, the subnational tax autonomy wasfound to worsen ®scal positions at the subna-

tional level in the full sample and in the non-OECD sample, and at both levels of govern-ment in the OECD sample. This is suggestive ofcoordination failures due to moral hazards indecentralized policy-making. Second, evidenceof coordination failures due to subnational®scal dependency was found in the non-OECDsample, in which reliance on intergovernmentaltransfers was found to worsen ®scal positionsat the central government level. The conversewas nevertheless found in the full sample and inthe OECD sample. In the OECD sample, thedependency of subnational governments onintergovernmental transfers tends to improve®scal positions, as long as subnational spendingis not too large relative to that of the centralgovernment. In this case, in the OECD sample,vertical imbalances, rather than measuring thescope for ``common pool'' problems, mayprovide evidence of the ability of centralgovernments to constrain subnational pro¯i-gacy by limiting their spending assignments tothe availability of ®nancing through intergov-ernmental transfers. Subnational ®scal posi-tions may therefore improve. 22 Stricter controlof the center over subnational ®nances andstringency of subnational balanced budgetrequirements 23 may also limit the scope for``common pool'' problems in the OECDcountries.

Finally, as for the control variables, in thenon-OECD sample, money creation and theterms of trade were found to worsen ®scalpositions. In both the OECD and the fullsamples, ®scal positions were found to worsendue to the social security liabilities associatedwith high age dependency ratios. Dealing withthese long-term liabilities is the most importantchallenge facing policy-makers in rapidly agingsocieties. Finally, as expected, an improvementin the terms of trade tends to improve ®scalpositions in the non-OECD sample. 24

5. CONCLUDING REMARKS

Fiscal decentralization has been an integralpart of overall public sector reform in a numberof countries, both developed and developing,and consists primarily of re-assigning expendi-ture functions and revenue sources to lowertiers of government. Among the merits of ®scaldecentralization, policy-makers have stressede�ciency gains, reduction in operational costs,and improved public sector performance inservice delivery. The pitfalls of decentralized

FISCAL DECENTRALIZATION 375

provision and ®scal policy-making consist, ingeneral, of loss of control over subnational®nances and coordination failures in ®scalpolicy-making, often leading to pressures onsubnational ®nances and, ultimately, macro-economic stability. Overall, the merits of ®scaldecentralization have to be weighed against therisks involved in increasing subnationalspending power at the expense of higher levelsof government.

The risks of boosting subnational spendingare particularly high when it is ®nanced bytransfers and grants from higher levels ofgovernment, rather than local revenue mobili-zation. In this case, the subnational revenue-expenditure gap is bridged by higher levels ofgovernments, using resources mobilized else-where in the economy to ®nance verticalimbalances in intergovernmental ®scal rela-

tions. Reliance on transfers from higher levelsof government to ®nance subnational spendingtends to put strain on intergovernmental ®scalrelations, and deepen budget imbalances at thecentral government level. Against this back-ground, it can be argued that minimizing thescope for coordination failures in intergovern-mental ®scal relationsÐby imposing ®scaldiscipline at subnational levels of government,by market forces or a better design of institu-tionsÐis a crucial prerequisite for successfuldecentralization.

Cross-level coordination may be encouragedvia such expedients as the enforcement of ®scalcontracts in the legislature, centralization ofbudget-making processes, incentives for ®scalrestraint, and punishment for excessivelargesse. 25 In a number of countries, ®scalinstitutions may be better designed to prevent

Table 1. Decentralization and ®scal positions (SURE Estimations)a

Full sample OECD sample Non-OECD sample

Centralgov.

balance

Subnat.gov.

balance

Centralgov.

balance

Subnat.gov.

balance

Centralgov.

balance

Subnat.gov.

balance

Log subnational tax ÿ0.83 0.20�� 0.15�

autonomy (ÿ1.483) (3.002) (2.383)Lagged log sub-nat. tax 0.10� 0.16�� 0.96��

autonomy (2.385) (2.770) (4.966)Log subnational ®scal ÿ0.41�� 0.12�� ÿ0.40�� ÿ0.02 0.05���

dependency (ÿ4.651) (2.594) (ÿ4.073) (ÿ0.379) (1.797)Lagged log sub-nat. ÿ0.09� ÿ0.13��

dependency (ÿ2.382) (ÿ2.436)Interaction term (sub.dep. ´ sub. spending share)

0.47�� 0.48��

(4.873) (4.059)Log subnational spending 0.11� 0.67�� 0.01 0.02 0.82��

share (1.962) (8.326) (0.186) (0.097) (11.34)Money creation 0.06� 0.08�

(1.947) (2.565)GDP growth ÿ0.18�� 0.22��

(ÿ3.269) (3.156)Lagged GDP growth ÿ0.02 ÿ0.11 ÿ0.05 ÿ0.04 13.57�

(ÿ0.486) (ÿ1.362) (ÿ0.939) (ÿ0.473) (2.210)Log terms of trade 0.13 ÿ0.41��

(1.415) (ÿ3.428)Lagged log terms of trade ÿ0.13�

(ÿ2.214)Log age dependency ratio 0.40��� 0.60��� 0.39��� 0.79� ÿ0.69 ÿ2.36���

(1.842) (1.834) (1.648) (2.206) (ÿ0.719) (ÿ1.770)�R2 0.24 0.76 0.34 0.71 0.17 0.86DW 1.71 1.58 1.13 0.71 2.23 1.95Nobs. 150 150 85 85 65 65

a Five-year average panels, 1970±95. Heteroscedasticity-consistent t-statistics are reported in parentheses.* Signi®cant at the 5% level.** Signi®cant at the 1% level.*** Signi®cant at the 10% level.

WORLD DEVELOPMENT376

vertical imbalances in intergovernmental rela-tions from worsening ®scal positions, nation-ally and subnationally. The OECD experienceis a case in point. These countries have hadhigher subnational spending shares for a muchlonger span of time than most developingcountries examined here, without signi®cant®scal imbalances at the center. More stringentcontrol of subnational ®nances is believed tohave prevented the deterioration of nationaland subnational ®scal positions and keptintergovernmental coordination failures incheck.

In other cases, local revenue mobilizationmay not have been encouraged and importantvertical imbalances have given rise to ``commonpool'' problems, which tend to worsen ®scalpositions at the central government level. Infact, a number of developing countries haverecently gone a long way in ®scal decentral-

ization, by raising subnational spending ratiossubstantially, devolving revenue sources andexpenditure functions to subnational jurisdic-tions, and granting signi®cant autonomy inpolicy-making at the subnational level. Thedevolution of tax bases to subnational govern-ments, however, may have reduced the e�-ciency of tax instruments and created moralhazards in decentralized policy-making. Thetransfer of spending assignments to subnationalgovernments may not have been matched by aproportional reduction in the spending share ofthe center in these countries. Finally, when®scal decentralization is carried out in a hasteas in the case of many developing countries,subnational ®scal imbalances may also beattributed to insu�cient expertise building inlocal and state governments to handle largerresources and to deal e�ectively with expendi-ture management.

NOTES

1. See, for instance, Olson (1969), Oates (1972, 1977),

and Wildasin (1988).

2. See, for example, Wildasin (1996) and Fukasaku

and de Mello (1998), for a concise overview of problems

of ®scal decentralization and macroeconomic gover-

nance.

3. See Boadway, Roberts and Shah (1994) and Tanzi

(1995), for further details.

4. Revenue-sharing is also advocated for equalization

purposes, given that di�erent subnational jurisdictions

have di�erent revenue mobilization capacities.

5. See de Mello (1999b) and Fukasaku and de Mello

(1998), for further details.

6. This is particularly true in the case of revenue-

sharing formulas involving broad-base taxes to ®ll the

gap between local revenues and expenditures. Block

grants, on the other hand, tend to encourage more

e�cient use of transferred funds.

7. See Bohn and Inman (1996) and Lowry and Alt

(1997), for further details.

8. The literature suggests that ``no carry-over'' rules

with constitutionally-embedded ex post end-of-period

balanced budget provisions tend to constrain de®cits

and induce adjustments via expenditure cuts, rather than

tax increases.

9. For a small number of countries, disaggregated data

are available for local and middle-tier governments.

Despite the di�erences between municipal and state

budgets and autonomy in ®scal policy-making, these

subnational levels of governments were taken together

to ensure comparability with the other countries in the

sample, for which the level of disaggregation of public

®nance statistics is lower.

10. In fact, the IMF Government Financial Statistics is

the most widely used internationally comparable data

source on subnational ®nances. Although coverage is

not universal, cross-country comparability is assured. In

the sample of countries under examination here, no

distinction is made between proper federations and those

decentralized States in which subnational governments

are responsible for substantial spending and revenue

mobilization.

11. The negative relationship prevails even if the

outliers are removed from the sample.

12. This is the case of, for instance, VAT in Brazil,

which was devolved to middle-tier governments in the

late 1980s (Afonso, 1996; McLure, 1997, de Mello,

1999a).

FISCAL DECENTRALIZATION 377

13. See Weingast, Shepsle and Johnsen (1981), for

further details on the social choice aspects of ``common

pool'' problems.

14. Matching grants tend to encourage more e�cient

use of transferred resources.

15. See Alesina and Drazen (1991), for further details.

16. This section draws heavily on de Mello (1999b).

17. A summary of data sources and variable descrip-

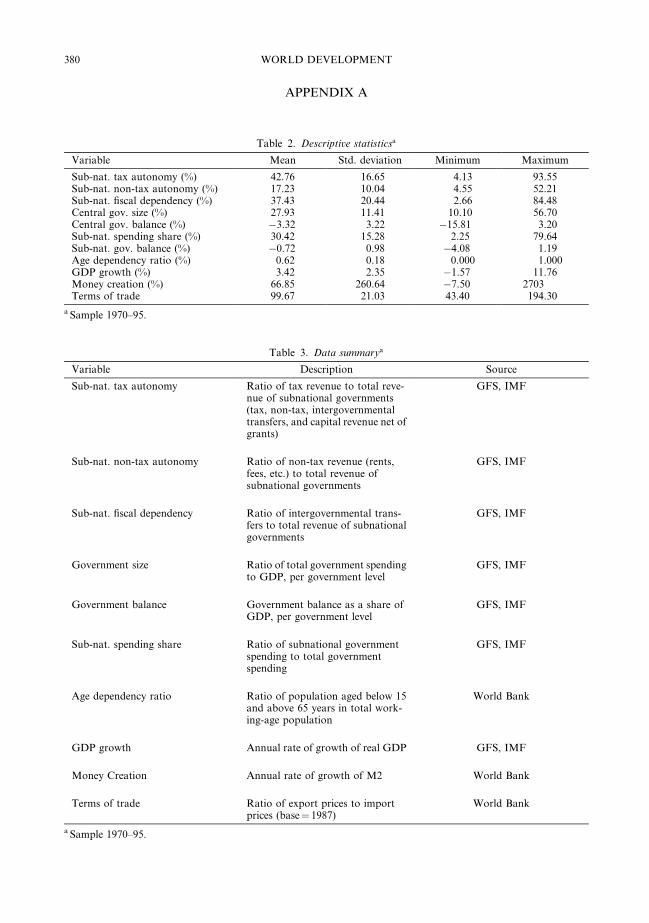

tions is provided in Table 3, appendix. Descriptive

statistics are reported in Table 2, appendix.

18. Additional variables that are expected to a�ect

®scal positions are related to electoral systems and

budgetary institutions. These political economy vari-

ables do not normally survive if other, more powerful

regressors, such as the ®scal decentralization indicators

considered here, are included in the estimating equation.

For further details, see Roubini and Sachs (1989),

Roubini (1991), Grilli Masciandaro and Tabellini

(1991), Alesina, cohen and Roubini (1993), Borrelli

and Royed (1995) and von Hagen and Harden (1995).

For the speci®c case of Latin America, see Alesina et al.

(1996).

19. The countries in the panel are: seven Latin Amer-

ican countries (Argentina, Bolivia, Brazil, Chile, Colom-

bia, Mexico, Peru), 17 OECD countries (Australia,

Austria, Belgium, Canada, Denmark, Finland, France,

Germany, Iceland, Italy, Netherlands, Norway, Spain,

Sweden, Switzerland, UK, and USA), ®ve Asian coun-

tries (India, Indonesia, Malaysia, Philippines, Thailand),

and one African country (South Africa).

20. Given that Mexico has not been an OECD member

country during most of the sample period under

examination here, and in the face of the countryÕssocioeconomic indicators, it is included in the non-

OECD sample.

21. The non-tax autonomy indicator was also exper-

imented with but failed to be statistically signi®cant at

classical con®dence intervals. Non-tax revenues tend to

be volatile, given that they comprise natural resource

rents, and are therefore likely to worsen ®scal posi-

tions.

22. Australia has an interesting ®scal arrangement:

although it is a federation, subnational governments

have limited taxing powers. Taxes are collected by the

center and subsequently transferred to subnational

jurisdictions for equalization purposes. However, high

dependency ratios have not been translated into sizeable

subnational ®scal imbalances, which suggests limited

``common pool'' problems in intergovernmental ®scal

relations.

23. See Eichengreen and Bayoumi (1994) for further

details based on evidence for the US.

24. The stock of public debt was also experimented

with as an additional control variable but found to be

collinear with other controls, particularly the age

dependency ratio.

25. See von Hagen and Harden (1996), for further

details. For a review of the political economy aspects of

budget enforcement, delegation and ®scal contracts, see

Hallerberg and von Hagen (1998).

REFERENCES

Afonso, J. R. R. (1996). Descentralizacß~ao ®scal, efeitosmacroeconomicos e funcß~ao de estabilizacß~ao: o caso(peculiar) do Brasil. Paper presented at the VIIRegional Seminar of Fiscal Policy, ECLAC, Santi-ago, Chile.

Alesina, A., & Drazen, A. (1991). Why are stabilizationsdelayed?. American Economic Review, 81.

Alesina, A., Cohen, G. D., & Roubini, N. (1993).Electoral business cycle in industrial democracies.European Journal of Political Economy, 9, 1±23.

Alesina, A., Hausmann, R., Hommes, R., & Stein, E.(1996). Budget institutions and ®scal performance inLatin America. NBER Working Paper No. 5586,NBER, Cambridge, MA.

Bird, R. (1992). Tax policy and economic development.Baltimore, MD: Johns Hopkins University Press.

Boadway, R., Roberts, S., & Shah, A. (1994). Thereform of ®scal systems in developing and emergingmarket economies: a federalism perspective. PolicyResearch Working Paper No. 1259, World Bank,Washington, DC.

Bohn, H., & Inman, R. P. (1996). Balanced budget rulesand public de®cits: evidence from the United StatesNBER Working Paper No. 5533, NBER, Cam-bridge, MA.

Bolton, P., & Dewatripont, M. (1994). The ®rm as acommunication network. Quarterly Journal ofEconomics, 109, 809±840.

Borrelli, S. A., & Royed, T. J. (1995). Governmentstrength and budget de®cits in advanced democra-cies. European Journal of Political Research, 28, 225±260.

WORLD DEVELOPMENT378

Caillaud, B., Jullien, B., & Picard, P. (1996). Hierarchi-cal organization and incentives. European EconomicReview, 40, 687±695.

Capeci, J. (1994). Local ®scal policies default risk andmunicipal borrowing costs. Journal of PublicEconomics, 53, 73±89.

Eichengreen, B., & Bayoumi, T. (1994). The politicaleconomy of ®scal restrictions: implications forEurope and the United States. European EconomicReview, 38, 783±791.

Fukasaku, K., & de Mello, L. R. Jr. (1998). Fiscaldecentralization and macroeconomic stability: theexperience of large developing and transition econ-omies. In K. Fukasaku & R. Hausmann, Democracy,decentralization and de®cits in Latin America. Paris:OECD.

Gilbert, G., & Picard, P. (1996). Incentives and theoptimal size of local territories. European EconomicReview, 40.

Grilli, V., Masciandaro, D., & Tabellini, G. (1991). Insti-tutions and policies. Economic Policy, 6, 341±391.

von Hagen, J., & Harden, I. (1995). Budget processesand commitment to ®scal discipline. EuropeanEconomic Review, 39, 771±779.

von Hagen, J., & Harden, I. (1996). National budgetprocesses and ®scal performance. IMF WorkingPaper, IMF, Washington, DC.

Hallerberg, M., & vonHagen, J. (1998). Electoral insti-tutions and the budget process. In K. Fukasaku & R.Hausmann, Democracy decentralization and de®citsin Latin America. OECD, Paris.

Huther, J., & Shah, A. (1996). A simple measure of goodgovernance and its application to the debate on theappropriate level of ®scal decentralization. WorldBank, Washington, DC.

Inman, R. P. (1996). Do balanced budget rules work: USexperience and possible lessons for the EMU, NBERWorking Paper No. 5838, NBER, Cambridge, MA.

Inman, R. P., & Rubinfeld, D. L. (1996). Designing taxpolicy in federalist economies: an overview. Journalof Public Economics, 60, 307±334.

Inman, R. P., & Rubinfeld, D. L. (1997). Rethinkingfederalism. Journal of Economic Perspectives, 11, 43±64.

Lowry, R. C., & Alt, J. E. (1997). A visible hand? Bondmarkets, political parties, balanced budget laws, andstate government debt. Harvard University, Depart-ment of Government, Cambridge, MA.

Martimort, D. (1996). The multiprincipal nature ofgovernment. European Economic Review, 40, 673±685.

McLure, C. E., Jr. (1997). Topics in the theory ofrevenue assignment. In M. I. Blejer, & T. Termin-assian, Macroeconomic dimensions of public ®nance:essays in Honor of Vito Tanzi. London: Routledge.

de Mello, Jr, L. R. (1998). Fiscal decentralization and thecost of borrowing: the case of local governments.University of Kent, UK.

de Mello, Jr, L. R. (1999a). Fiscal federalism andmacroeconomic stability. in Brazil: Background andperspectives. In L. R. de Mello Jr., & K. Fukasaku,Fiscal decentralization, intergovernmental ®scal rela-

tions and macroeconomic governance. OECD Devel-opment Center, Paris.

de Mello, Jr, L. R. (1999b). Intergovernmental ®scalrelations: co-ordination failures and ®scal outcomes.Public Budgeting and Finance, 19 (1), 3±25.

Oates, W. (1972). Fiscal federalism. New York: HarcourtBrace Janovich.

Oates, W. (1977). The political economy of ®scal feder-alism. D.C. Heath, Lexington, MA.

Olson, M. J. (1969). The principle of ®scal equivalence:the division of responsibilities among di�erent levelsof government. American Economic Review, 59, 479±487.

Poterba, J. (1996). Budget institutions and ®scal policyin the US States. American Economic Review, 86,395±400.

Poterba, J., & Rueben, K. S. (1997). State ®scalinstitutions and the US municipal bond market.NBER Working Paper No. 6237, NBER, Cam-bridge, MA.

PrudÕhomme, R. (1995). On the dangers of decentral-ization. World Bank Research Observer, August,201±210.

Radner, R. (1993). The organization of decentralizedinformation processing. Econometrica, 61, 1109±1146.

Roubini, N., & Sachs, J. (1989). Political and economicdeterminants of budget de®cits in the industrialdemocracies. European Economic Review, 33, 903±938.

Roubini, N. (1991). Economic and political determi-nants of budget de®cits in developing countries.Journal of International Money and Finance, 10, S49±S72.

Tanzi, V. (1995). Fiscal federalism and decentralisation:A review of some e�ciency and macroeconomicaspects. In Annual Bank Conference on DevelopmentEconomics. The World Bank, Washington, DC.

Tanzi, V. (1999) The Changing role of the state in theeconomy: A historical perspective. In L. R. de MelloJr., & K. Fukasaku, Fiscal decentralization, intergov-ernmental ®scal relations and macroeconomic gover-nance. OECD Development Center, Paris.

Ter-Minassian, T. (1999) Decentralization and macro-economic management. In L. R. de Mello Jr., & K.Fukasaku, Fiscal decentralization, intergovernmental®scal relations and macroeconomic governance.OECD Development Center, Paris.

Tirole, J. (1994). The internal organization of govern-ment. Oxford Economic Papers, 46, 1±29.

Weingast, B., Shepsle, K., & Johnsen, C. (1981). Thepolitical economy of bene®ts and costs: A neo-classical approach to distributive politics. Journal ofPolitical Economy, 89, 642±664.

Wildasin, D. (1988). Nash equilibria in models of ®scalcompetition. Journal of Public Economics, 35.

Wildasin, D. (1996). Introduction: Fiscal aspects ofevolving federations. International Tax and PublicFinance, 3, 121±135.

World Bank (1997). The world development report. NewYork: Oxford University Press.

FISCAL DECENTRALIZATION 379

APPENDIX A

Table 3. Data summarya

Variable Description Source

Sub-nat. tax autonomy Ratio of tax revenue to total reve-nue of subnational governments(tax, non-tax, intergovernmentaltransfers, and capital revenue net ofgrants)

GFS, IMF

Sub-nat. non-tax autonomy Ratio of non-tax revenue (rents,fees, etc.) to total revenue ofsubnational governments

GFS, IMF

Sub-nat. ®scal dependency Ratio of intergovernmental trans-fers to total revenue of subnationalgovernments

GFS, IMF

Government size Ratio of total government spendingto GDP, per government level

GFS, IMF

Government balance Government balance as a share ofGDP, per government level

GFS, IMF

Sub-nat. spending share Ratio of subnational governmentspending to total governmentspending

GFS, IMF

Age dependency ratio Ratio of population aged below 15and above 65 years in total work-ing-age population

World Bank

GDP growth Annual rate of growth of real GDP GFS, IMF

Money Creation Annual rate of growth of M2 World Bank

Terms of trade Ratio of export prices to importprices (base� 1987)

World Bank

a Sample 1970±95.

Table 2. Descriptive statisticsa

Variable Mean Std. deviation Minimum Maximum

Sub-nat. tax autonomy (%) 42.76 16.65 4.13 93.55Sub-nat. non-tax autonomy (%) 17.23 10.04 4.55 52.21Sub-nat. ®scal dependency (%) 37.43 20.44 2.66 84.48Central gov. size (%) 27.93 11.41 10.10 56.70Central gov. balance (%) ÿ3.32 3.22 ÿ15.81 3.20Sub-nat. spending share (%) 30.42 15.28 2.25 79.64Sub-nat. gov. balance (%) ÿ0.72 0.98 ÿ4.08 1.19Age dependency ratio (%) 0.62 0.18 0.000 1.000GDP growth (%) 3.42 2.35 ÿ1.57 11.76Money creation (%) 66.85 260.64 ÿ7.50 2703Terms of trade 99.67 21.03 43.40 194.30

a Sample 1970±95.

WORLD DEVELOPMENT380