fiscal austerity socgen oct 2011

TRANSCRIPT

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 1/18

THE NEW WORLD ORDER

CROSS ASSET THEMATIC RESEARCHOctober 2011

Véronique Riches-Flores Phone: +33 (0)1 42 13 84 04

Societe Generale (“SG”) does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that SG mayhave a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making theirinvestment decision. PLEASE SEE APPENDIX AT THE END OF THIS REPORT FOR THE ANALYST(S) CERTIFICATION(S), IMPORTANT DISCLOSURES ANDDISCLAIMERS AND THE STATUS OF NON-US RESEARCH ANALYSTS.

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 2/18

WE ARE ALL GREEKS!

THE REAL-LIFE STRESS TEST OF GREECE – i.e. FAILURE OF AN OECD STATE – IS AN

ELECTROSHOCK FOR THE COMMUNITY OF INDUSTRIALISED NATIONS, THAT WILL BE

FOLLOWED BY MAJOR CHANGES IN THOSE COUNTRIES’ FISCAL POLICIES

NO ONE CAN CLAIM TO BE IMMUNE FROM A GREEK-STYLE SPIRAL, WHY?

» OUR ECONOMIES ARE MATURE - with weak potential GDP, especially post the financial crisis

» WE ARE AGEING - we have no chance to see our future income improving substantially in the

long run ; our savings capacities are shrinking and our health and pensions spending is increasing

225/10/2011

Abstract from our report “After the central banks who will buy our government bonds?” June 09

Already in 2006, S&P was arguing that ageing populations would cause most OECD countries to

lose their investment grade status by 2040

Australia Canada France Germany Italy Japan S. Korea Spain Sweden UK USA

2005 AAA AAA AAA AAA AA AA A AAA AAA AAA AAA

2020 AA AAA A AAA A Non-IG A AAA AAA AAA BBB

2030 BBB AAA Non-IG A Non-IG Non-IG Non-IG BBB A A Non-IG

2040 Non-IG AAA Non-IG Non-IG Non-IG Non-IG Non-IG Non-IG Non-IG Non-IG Non-IG

Source: S&P 2006, SG Cross Asset Research

S&P 2006 long-term baseline scenario – sovereign debt ratings

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 3/18

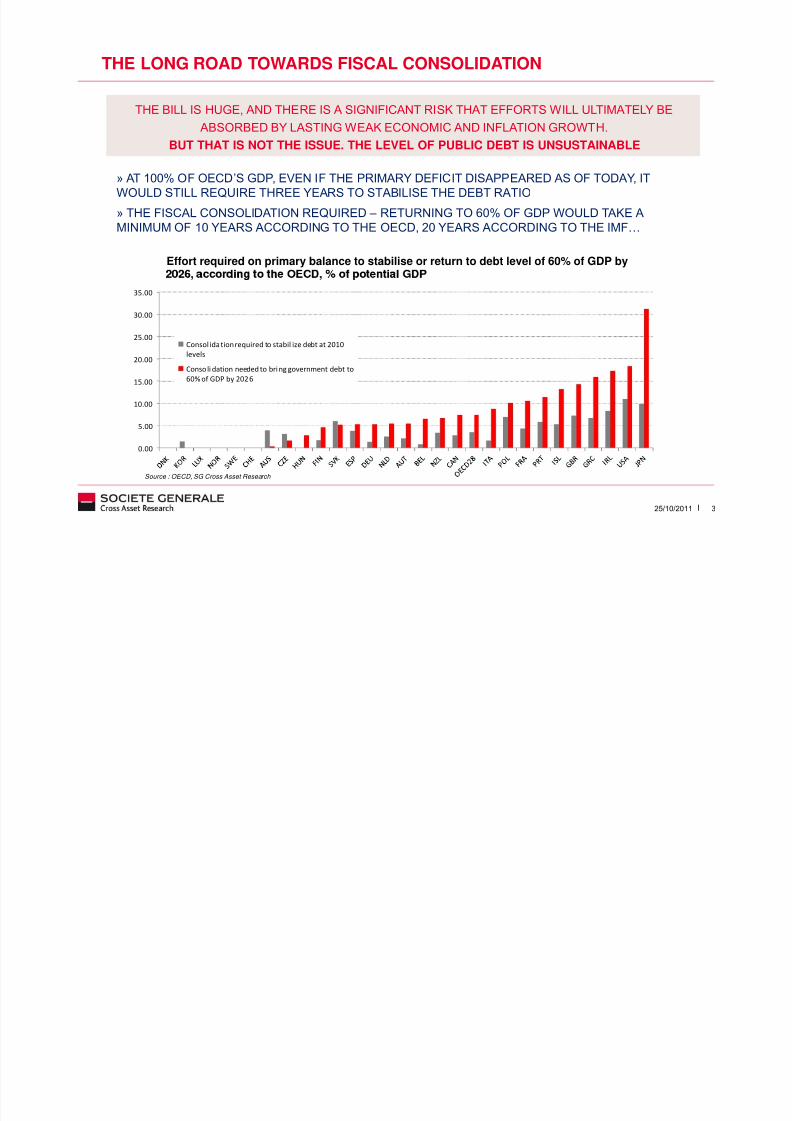

THE LONG ROAD TOWARDS FISCAL CONSOLIDATION

» AT 100% OF OECD’S GDP, EVEN IF THE PRIMARY DEFICIT DISAPPEARED AS OF TODAY, IT

WOULD STILL REQUIRE THREE YEARS TO STABILISE THE DEBT RATIO» THE FISCAL CONSOLIDATION REQUIRED – RETURNING TO 60% OF GDP WOULD TAKE A

MINIMUM OF 10 YEARS ACCORDING TO THE OECD, 20 YEARS ACCORDING TO THE IMF…

Effort required on primary balance to stabilise or return to debt level of 60% of GDP by

THE BILL IS HUGE, AND THERE IS A SIGNIFICANT RISK THAT EFFORTS WILL ULTIMATELY BE

ABSORBED BY LASTING WEAK ECONOMIC AND INFLATION GROWTH.

BUT THAT IS NOT THE ISSUE. THE LEVEL OF PUBLIC DEBT IS UNSUSTAINABLE

325/10/2011

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Consol idation required to stabil ize debt at 2010

levels

Consoli dation needed to bri ng government debt to

60% of GDP by 2026

Source : OECD, SG Cross Asset Research

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 4/18

WHAT’S NEXT?

» OF THE 107 EPISODES OF FISCAL ADJUSTMENTS OBSERVED IN THE PAST 40 YEARS THE MOST

EFFICIENT IN TERMS OF FISCAL RESULTS AND LEAST COSTLY IN TERMS OF GROWTH HAVE

BEEN THE ONES BASED ON SPENDING DRAG RATHER THAN TAX INCREASES

“IDEALLY”, SUCH AN ADJUSTMENT WOULD BE MADE BY EFFORTS TO REDUCE SPENDING

Typolog y and efficiency of fiscal consol idation episodes between 1970 and 2007 in OECD countries

Repartition of the 107 episodes of fiscal

adjustment by d uration

Contribution of expenditure and revenue

items to fiscal adjustment and impact

on growth

Contribution of expenditure and revenue

items to fiscal adjustment and impact

on primary deficit

425/10/2011

0

10

20

30

40

50

60

70

1 2 3 4Duration (years)

Number of episodes by duration

Exp. 86%

Exp. 35%

Revenue

14

Revenue

65%

0%

10%

20%

30%

40%

50%

60%

70%

80%90%

100%

Expansionary

episodes

Contractionary

episodes

Exp.

135%

Exp. 34%

Revenue

-35%

Revenue

66%

-60

-40

-20

0

20

40

60

80

100

120140

160

Successes Failures

Source: Alesina et Ardagna, 2009, SG Cro ss Asset Research Alesina and Ardagna define fiscal adjustment episodes as the years during which the cyclically adjusted primary balance (public balanceexc. interests) improves by at least 1.5 % of GDP. Authors identified 107 episodes of fiscal adjustmen ts between 1970 and 2007 (91 episodes of stimuli ). Over these 107 periods, 65 lasted only oneyear, 13 lasted two years, 4 lasted three years but one only lasted over four consecutive years (Denmark from 1983 to 1986). An episode of fiscal adjustment is qu alified as “expansionary” if theaverage growth rate of GDP gap with the G7 in the first year of adjustment and the two following years significantly exceeds the same variable in all episodes of fiscal adjustment. They are qualified as“successful” when the cumulative reduction of the debt to GDP ratio three years after the beginning of the fiscal adjustment is greater than 4.5 percentage points.

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 5/18

THE CURRENT SITUATION IS FAR MORE COMPLEX, HOWEVER

Fiscal austerity efforts are more accessible when they

are carried out in isolation (their depressive effects can be

offset by growth in the rest of the world)

60% of the past episodes of adjustment lastedless than one year; none of them dealt with asmany economies as are involved today

The success of a fiscal adjustment is much moreuncertain over the long haul (when it repeatedly affects a

growing number of economic agents and causes a reassessment

of the role of public authorities)

Austerity measures may find differing levels of

acceptance among populationTheir impact on the behaviour of agents is largelyunpredictable and may notably cancel out muchof the effects initially targeted (see Greece)

525/10/2011

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Expenditure RevenueExpen diture versus revenue-based measures in fiscal consolidation plans of 2010

SPENDING CUTS THAT HAVE LARGELY CHARACTERISED BUDGETARY POLICY IN 2010 WILL

BE DIFFICULT TO CONTINUE IN THE LONG TERM

Source : OECD, SG Cross Asset Research

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 6/18

GROWTH CONSTRAINTS

3

4

FittedChange in pub. exp/GDP ratio - OECD

a c t o f

c

80% OF THE CHANGE IN THE RATIO OF PUBLIC SPENDING/GDP HAS RESULTEDFROM THE COMBINATION OF GDP GROWTH AND UNEMPLOYMENT RATE OVER

THE LAST 40 YEARS!

THE CURRENT CONTEXT OF SLOW GROWTH AND A STUBBORNLY HIGH UNEMPLOYMENT RATE

CONSIDERABLY REDUCES THE PROBABILITY OF A SUBSTANTIAL CUT IN PUBLIC SPENDING

625/10/2011

-2

-1

0

1

2

Actual

I m p l i c i t

i m p

S G e c o n

o m i

f o r e c a s t s

-2

0

2

74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 0 1 2 3 4 5 6 7 8 9 10

Residuals

d=1.657+0.096*u-0.53*g

R2=0.789

d = one year change in public

spending/GDP ratio

u = one year change in the unemployment rate

g = one year change in reral GDP growth

Source : SG Cross Asset Research

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 7/18

BEWARE THE SOCIAL/POLITICAL CONSTRAINTS…

THE SOCIAL COST OF THE ONGOING CRISIS WILL LIMIT THE SCOPE OF PUBLIC SPENDING CUTS

Countries with thehighest protection

level will have very

limited room for

manoeuvre to reduce60

70

80

90

OECD average

Average replacement rate of revenue during initial phase of unemployment based on six family types – level

1 of earnings (from 67% to 150% of national average wages)

725/10/2011

Source: From OECD, Tax-Benefit Models, SG Cross Asset Research

their spending.

Those that offer the

least protection may

be faced with the

need to increase

their social action.

40

50

AUS NZL KOR GBR TUR USA POL IRL JPN EST SWE GRC AUT FIN HUN ITA BEL ESP CAN SVK NOR CZE DNK DEU NLD SVN FRA ICE CHE PRT LUX

-20

-10

0

10

20

AUS NZL KOR GBR TUR USA POL IRL JPN EST SWE GRC AUT FIN HUN ITA BEL ESP CAN SVK NOR CZE DNK DEU NLD SVN FRA ICE CHE PRT LUX

Gap to average

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 8/18

PUBLIC INVESTMENT IN THE FIRING LINE

Eventually, public sector investment is likely to bear the

brunt of the spending cuts

Easier to cut or postpone than other forms ofexpenditures, less political/social conflict

BUT A LONG-TERM ECONOMIC COST

A substantial part of public spending (10% of OCDEpublic spending)

Sometimes poor economic efficiency

45.0

Weightof public investmentamong OECD members, 2009

Public investment account for 1/5th of total investmentin OECD countries

Lasting underinvestment in the public sector has alwayscome at a cost in terms of infrastructure efficiency and,in the end, productivity (see UK or German experiences)

825/10/2011

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

.

As a % of total investment

As a % of total publ ic expenditure

Source: OECD, SG Cross Asset Research

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 9/18

HIGHER TAX AND MORE PROGRESSIVITY AHEAD

250000

300000

350000

400000USA

1981

1981 at 2010 prices

2010

Income level, nat.cur.

0

10000

20000

30000

40000

50000

60000

70000

80000

0 10 20 30 40 50 60

France1981

1981 at 2010 prices

2010

Marginal tax rate, %

Income level, nat.cur.

Greece

925/10/2011

0

50000

100000

150000

200000

0 20 40 60 80

Marginal tax rate, %

0

20000

40000

60000

80000

100000

120000

0 10 20 30 40 50 60 70

1981

1981 at 2010 prices

2010

Income level, nat. cur.

Marginal tax rate, %Source: OECD, SG Cross Asset Research

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 10/18

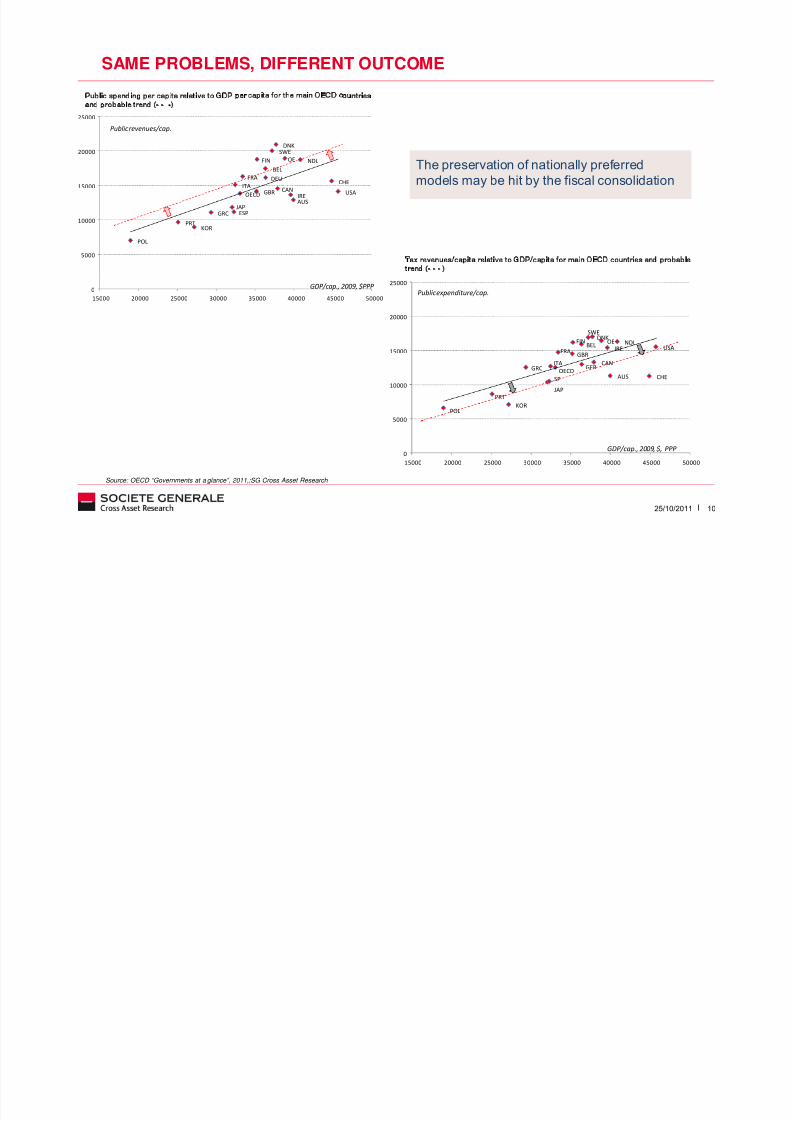

SAME PROBLEMS, DIFFERENT OUTCOME

The preservation of nationally preferred

models may be hit by the fiscal consolidation

AUS

OE

BEL

CAN

DNK

FIN

FRA DEU

GRC

IRE

ITA

JAP

KOR

NDL

OECD

POL

PRT

ESP

SWE

CHE

GBR USA

5000

10000

15000

20000

25000

Public revenues/cap.

Public spending per capita relative to GDP per capita for the main OECD countriesand probable trend (- - -)

Tax revenues/capita relative to GDP/capita for main OECD countries and probabletrend (- - - )

1025/10/2011

0

15000 20000 25000 30000 35000 40000 45000 50000

GDP/cap., 2009, $PPP

AUS

OEBEL

CAN

DNKFIN

FRA

GERGRC

IRE

ITA

JAP

KOR

NDL

OECD

POL

PRT

SP

SWE

CHE

GBRUSA

0

5000

10000

15000

20000

25000

15000 20000 25000 30000 35000 40000 45000 50000

GDP/cap., 2009, $, PPP

Public expenditure/cap.

Source: OECD “Governments at a glance”, 2011,;SG Cross Asset Research

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 11/18

INCREASING INCOME TAX OR REDUCING EXPENDITURE?

To bring its fiscalsituation in line withthe OECD average,

the US would

actually have toincreasegovernment

revenues by 33% (or$4,700/cap.) and to

increase ublic

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0 Restriction needed to bring gvt revenue/cap. within OECD average, % change from 2009

Restriction

0.0

12.5

25.0

Restriction needed to bring gvt expenditure/cap. within OECD average, % change from 2009

Restriction

1125/10/2011

expenditure by 10%(or $1,280/cap.)

France would haveto decrease both its

revenues andexpenditure by PPP

$ 2,300- 2,100/cap.

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

Overall restriction per capita, % change from 2009

Restriction

-50.0

-37.5

-25.0

-12.5

Source: OECD, SG Cross Asset Research

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 12/18

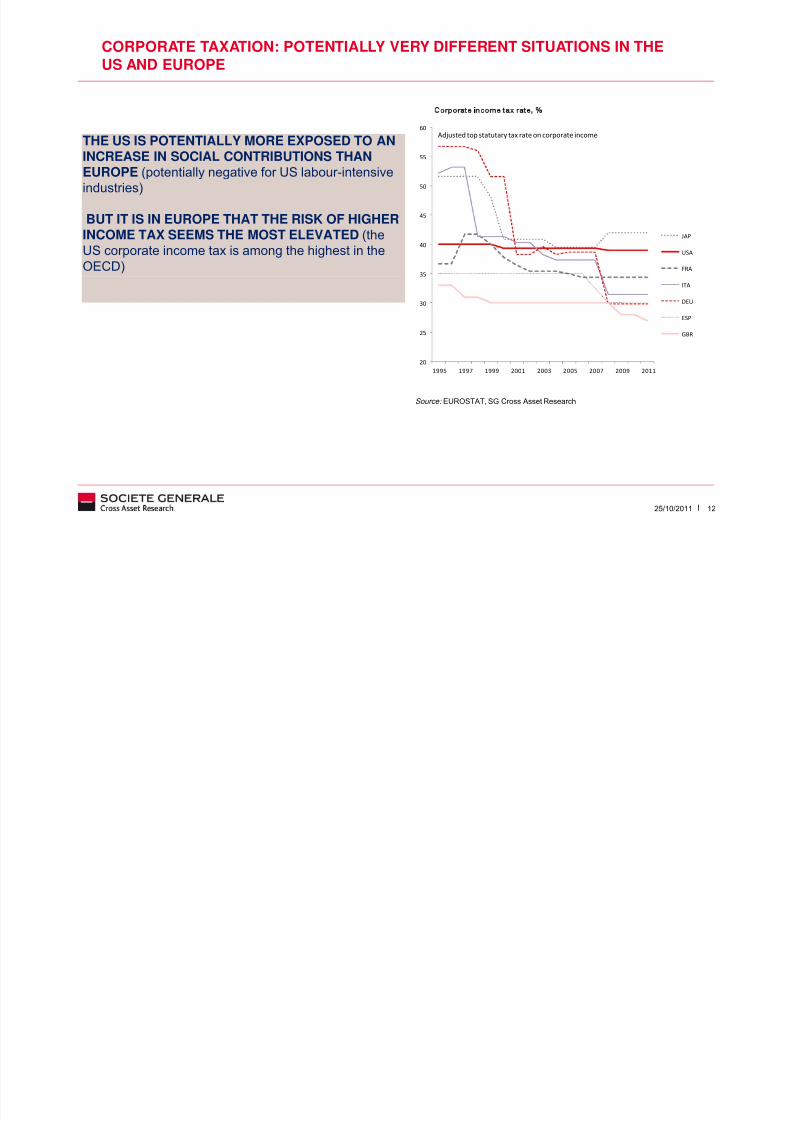

CORPORATE TAXATION: POTENTIALLY VERY DIFFERENT SITUATIONS IN THEUS AND EUROPE

35

40

45

50

55

60

JAP

USA

FRA

Adjusted top statutary tax rate on corporate income

Corporate income tax rate, %

THE US IS POTENTIALLY MORE EXPOSED TO ANINCREASE IN SOCIAL CONTRIBUTIONS THANEUROPE (potentially negative for US labour-intensive

industries)

BUT IT IS IN EUROPE THAT THE RISK OF HIGHERINCOME TAX SEEMS THE MOST ELEVATED (the

US corporate income tax is among the highest in the

OECD)

1225/10/2011

20

25

30

1995 1997 1999 2001 2003 2005 2007 2009 2011

ITA

DEU

ESP

GBR

Source: EUROSTAT, SG Cross Asset Research

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 13/18

CROWDING-OUT EFFECTS

DRAIN ON REVENUES/weaker economic growthHigher risk premium

UNSTABLE TAX AND REGULATORY ENVIRONMENT

/negative for investmentStructural decline in P/E

CONSUMER TAXATION Negative on consumption outlook

1325/10/2011

CORPORATE TAXATIONNegative on investment and corporateperformance

WHICH ARE THE MOST EXPOSED SECTORS?

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 14/18

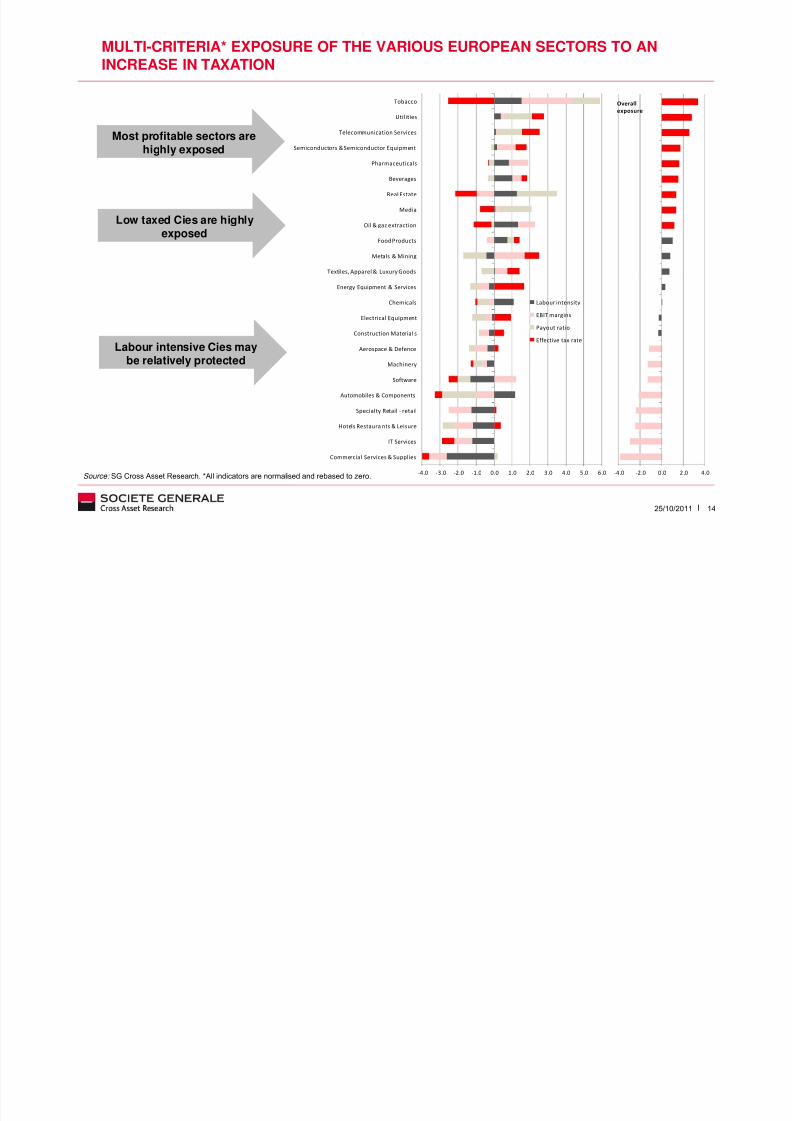

MULTI-CRITERIA* EXPOSURE OF THE VARIOUS EUROPEAN SECTORS TO ANINCREASE IN TAXATION

Textiles, Apparel & Luxury Goods

Metals & Mining

Food Products

Oil & gaz extraction

Media

Real Estate

Beverages

Pharmaceuticals

Semiconductors & Semiconductor Equipment

Telecommunication Services

Utilities

Tobacco Overall

exposure

Most profitable sectors arehighly exposed

Low taxed Cies are highlyexposed

1425/10/2011

-4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0 3.0 4.0 5.0 6.0

Commercial Services & Supplies

IT Services

Hotels Restaura nts & Leisure

Specialty Retail - retail

Automobiles & Components

Software

Machinery

Aerospace & Defence

Construction Material s

Electrical Equipment

Chemicals

Energy Equipment & Services

Labour intensity

EBIT margins

Payout ratio

Effective tax rate

-4.0 -2.0 0.0 2.0 4.0Source: SG Cross Asset Research. *All indicators are normalised and rebased to zero.

Labour intensive Cies maybe relatively protected

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 15/18

THE EUROPEAN FISCAL HIT LIST

Exposure of the various sectors to tougher fiscal conditions for companies in Europe

The most exposed sectors Neutral sectors The most protected sectors

Tobacco Agrifood Commercial services

Utilities Metals & Mining Hotels, restaurants & leisure

Telecoms Textiles, apparel & Luxury goods Specialised distribution

1525/10/2011

Semiconductors Energy equipment & Services Automobile & Equipment makers

Pharmaceuticals Chemicals Software & IT services

Real estate Electrical equipment Machinery

Media Construction & Materials Aerospace & Defence

Beverages

Oil & Gas

Source: SG Cross Asset Research

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 16/18

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 17/18

8/3/2019 Fiscal Austerity SocGen Oct 2011

http://slidepdf.com/reader/full/fiscal-austerity-socgen-oct-2011 18/18

SG LEADER IN GLOBAL CROSS ASSET RESEARCH

Macro & Strategy

#1 Global Strategy#1 Multi Asset Research

#2 Global Economics

#2 Pan-Euro Economics

Fixed Income

#1 Overall Trade Ideas

#1 Credit Research Team

#1 Overall Credit Strategy

#1 in Sovereigns

#1 in 4 sector teams

20112011

1825/10/2011

Commodities

#3 Research in Power and Gas

#4 Research in Oil

#4 Research in Base Metals

#5 Research in Precious Metals

Equity

#1 Equity Quant

#1 Index Analysis

10 sector teams in the Top 10

2011