first nation property taxation report -...

TRANSCRIPT

First Nation

Property Taxation Report

Presentation to the

First Nation Tax Administrators Association

17th Annual National Forum

September 15 – 17, 2010

Enoch Cree Nation, AB

Overview

▶ First Nations Tax Commission

▶ FNTC and FNTAA Relationship

▶ First Nation Property Tax – 2010

• National Statistical Overview

▶ FNTC Performance Report

▶ Property Tax Policy Issues

▶ Year Ahead

First Nations Tax Commission

▶ Established in 2005 by the First Nations Fiscal Statistical

Management Act. 10 Commissioners.

▶ Builds on the work of the Indian Taxation Advisory Board.

▶ Dual regulatory role: review and approve FSMA local revenue laws and advise Minister on s.83 by-laws.

▶ Develops policy, resolves disputes, provides education opportunities (e.g., Tulo Centre of Indigenous Economics).

FNTC Mandate

▶ Protect integrity of First Nation tax system;

▶ Safeguard and enhance First Nation tax jurisdiction;

▶ Assist First Nation property taxation capacity development;

▶ Promote the understanding and use of First Nation property taxation; and

▶ Promote First Nation economic development.

1. Service Agreements

2. Rates Disputes3. Third Party Issues

4. Taxpayer Rep.5. Informal Facilitation

6. Interest Based Negotiations7. Roster of Mediators

8. S.33 review process

9. Maintain informal s.83 complaints process

1. Service Agreements

2. Rates Disputes3. Third Party Issues

4. Taxpayer Rep.5. Informal Facilitation

6. Interest Based Negotiations7. Roster of Mediators

8. S.33 review process

9. Maintain informal s.83 complaints process

1. S. 83 related policies

2. Grants-In-lieu policies3. FSMA related policies

4. FSMA Related Standards5. Debentures

6. Self-Governing First Nations7. Institutional Coordination

8. Law Development

1. S. 83 related policies

2. Grants-In-lieu policies3. FSMA related policies

4. FSMA Related Standards5. Debentures

6. Self-Governing First Nations7. Institutional Coordination

8. Law Development

1. Review Standards

• By-laws• Local Revenue Laws

2. Bylaw Review3. Sample Bylaws

4. Local Revenue Law Review

5. Sample Laws6. Standards Drafting

7. Review process

1. Review Standards

• By-laws• Local Revenue Laws

2. Bylaw Review3. Sample Bylaws

4. Local Revenue Law Review

5. Sample Laws6. Standards Drafting

7. Review process

1. S.83 Training

2. S.83 software3. Admin. Software4. Accredited taxation certificate5. Research

1. S.83 Training

2. S.83 software3. Admin. Software4. Accredited taxation certificate5. Research

1. S. 83 Communications

• Newsletters• Presentations

• Website2. FSMA Communications

• Newsletters

• Presentations• Annual Reports

• Website • OLA Requirements

1. S. 83 Communications

• Newsletters• Presentations

• Website2. FSMA Communications

• Newsletters

• Presentations• Annual Reports

• Website • OLA Requirements

1. Management Committee

2. Organizational Policies3. HR & Staffing

4. Finance & Audit5. IT & Facilities

6. Evaluative Support7. FNTC Meetings

8. Staff & Commissioner Training

9. Gazette10. Admin Support s.83 req

1. Management Committee

2. Organizational Policies3. HR & Staffing

4. Finance & Audit5. IT & Facilities

6. Evaluative Support7. FNTC Meetings

8. Staff & Commissioner Training

9. Gazette10. Admin Support s.83 req

Policy DevelopmentPolicy Development Law, By-law Review and Regulations

Law, By-law Review and Regulations EducationEducation Dispute

Management

Dispute ManagementCommunicationsCommunicationsCorporate

Services & Gazette

CorporateServices & Gazette

First Nations Tax CommissionFirst Nations Tax Commission

Chief Commissioner and 9 Commissioners Chief Commissioner and 9 Commissioners

Chief Executive OfficerChief Executive Officer

Chief Operating Officer Chief Operating Officer

FNTC Relationship with FNTAA

FNTC will maintain a strong FNTAA working relationship with emphasis in 3 areas:

▶ Education and Training

• FNTAA participation through advisory committee

▶ Technical Assistance

• Supporting new tax administrators

▶ FNTC standard and policy development

• FNTAA policy input

First Nations and Selected Provinces and Territories

Local Property Tax Revenues – 2009

$10 $28 $53 $63$293

$519

$962

$1,253$1,591

$3,830

$4,694

$0$500

$1,000$1,500$2,000$2,500$3,000$3,500$4,000$4,500$5,000

Millions

NU YT PE FN NF NB NS MB SK BC AB

First Nations added to the FSMA Schedule

since October 2009

▶ Beaver Lake Cree Nation, AB

▶ Gitsegukla First Nation, BC

▶ Kahkewistahaw First Nation, SK

▶ Brokenhead Ojibway Nation, MB

▶ K’ómoks First Nation, BC

▶ Tseycum First Nation, BC

▶ T’Sou-ke First Nation, BC

Three First Nations are currently waiting to be added.

First Nation Property Tax – 2010

▶ 158 First Nations accessing the FSMA or section 83 of the Indian Act.

• 123 have or developing property tax laws/by-laws

• 58 First Nations on FSMA schedule

• 40 First Nations are collecting tax under the FSMA

• 18 First Nations have repealed and replaced section 83 by-laws with new FSMA laws

• Over $63 million collected each year in property taxes.

• The First Nation property tax system is bigger than that of PEI or any of the three territories

• Over $860M in property taxes collected by First Nations since 1988.

First Nations Taxing Across Canada

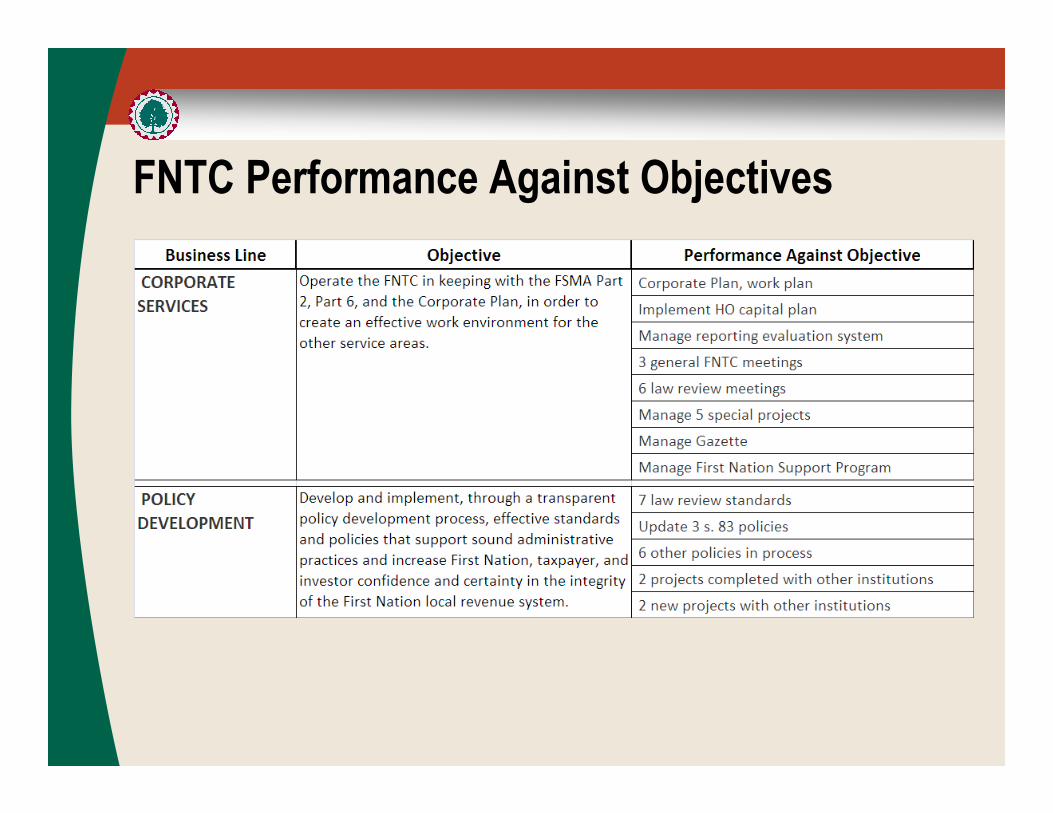

FNTC Performance Against Objectives

FNTC Performance Against Objectives

FNTC Performance Against Objectives

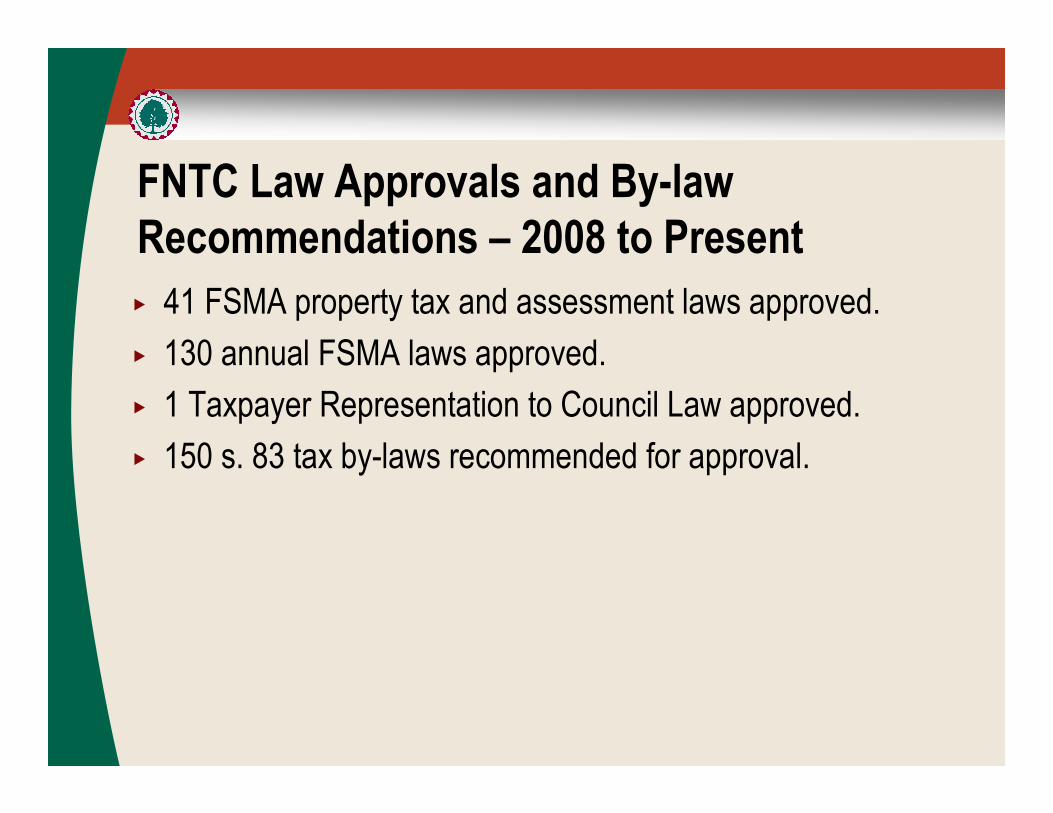

FNTC Law Approvals and By-law

Recommendations – 2008 to Present

▶ 41 FSMA property tax and assessment laws approved.

▶ 130 annual FSMA laws approved.

▶ 1 Taxpayer Representation to Council Law approved.

▶ 150 s. 83 tax by-laws recommended for approval.

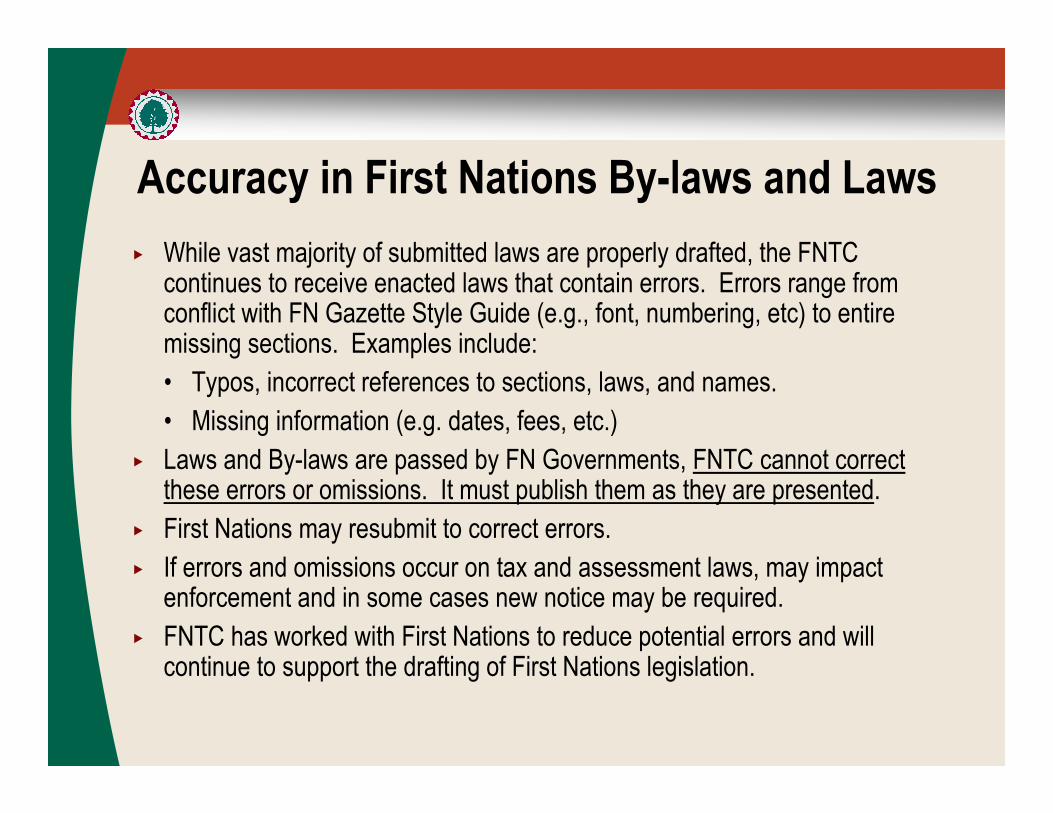

Accuracy in First Nations By-laws and Laws

▶ While vast majority of submitted laws are properly drafted, the FNTC continues to receive enacted laws that contain errors. Errors range from conflict with FN Gazette Style Guide (e.g., font, numbering, etc) to entire missing sections. Examples include:

• Typos, incorrect references to sections, laws, and names.

• Missing information (e.g. dates, fees, etc.)

▶ Laws and By-laws are passed by FN Governments, FNTC cannot correct these errors or omissions. It must publish them as they are presented.

▶ First Nations may resubmit to correct errors.

▶ If errors and omissions occur on tax and assessment laws, may impact enforcement and in some cases new notice may be required.

▶ FNTC has worked with First Nations to reduce potential errors and will continue to support the drafting of First Nations legislation.

FNTC Sample Laws

▶ Property and Assessment laws for:

• BC, AB, SK, MB,ON, NS, NB, PQ (2010)

▶ Taxpayer Representation to Council Law

▶ DCC’s

▶ Taxation for the Provision of Services

▶ Borrowing Laws

▶ Delegation of Authority Law and Business Activity Tax (BAT) Law to be completed in 2011.

Current Property Tax Policy Issues

Evaluation of Annual Laws/By-laws –

Process and Policy

• Survey of Tax Administrators – Fall 2010

• Rate setting indicators, sub-rate setting

• Expenditures on Land Acquisition

• FNTC Technical Support Procedures

Major Industrial Property Taxation - BC

Sustainability Model Report

▶ Catalyst Paper challenges industrial tax rates and loses, currently appealing.

▶ Sponsors report which calls for a closer relationship between taxes paid and services consumed.

▶ In March 2010, BC establishes Steering Committee with Industry, Province, UBCM, and municipal representation. Will make recommendations to the province in Fall 2010.

▶ FNTC will ensure that the FN interests are represented.

Linear Property Assessment in Alberta

(MOU)

▶ First Nations in Alberta annually require linear property assessment data consistent with practices in Alberta to support property taxation.

▶ The Linear Property Assessment Unit (LPAU) of the Assessment Services Branch (ASB) annual receives the well and pipeline datafrom the Energy Resources Conservation Board (ERCB) and processes the information to prepare the calculation of the annual linear property assessment.

▶ Currently this information is being provided to First Nations on a discretionary basis, a formal approach is required to ensure that the service will continue without interruption.

Linear Property Assessment in Alberta

(MOU)

▶ Municipal Government Act (MGA) precludes the Designated Linear Assessor (DLA) from preparing linear property assessment on property in Indian reserves as per section 298(1)(t).

▶ FNTC and Mr. Al Fenton are working to develop a Memorandum of Agreement with Alberta that will help ensure First Nations will receive reliable annual linear property assessment data on a timely basis.

▶ Once the MOA is completed, First Nations will annually provide a letter of authorization to the Linear Property Assessment Unit to name their appointed agent (assessor) who will receive the data on their behalf. Without this annual letter of authorization the information will not be provided.

First Nation Taxation Grant Programs

• First Nations can establish granting programs to off-set taxes.

• Should further social or economic community objectives.

• Grants can be for eligible profit and non-profit taxpayers.

• Granting programs are

� transparent (criteria are set out in taxation law/by-law and amounts given shown in annual expenditure law/by-law)

�flexible (determined each year by Council)

First Nation Taxation Grant Programs

Granting programs must:

•have clear objectives designed for a community purpose or goal;

•have clear and transparent eligibility criteria;

•ensure that recipients are current year taxpayers;

•ensure that the grant amount does not exceed the taxes payable by the recipient in that year;

•limit grant purposes to the payment of property taxes; and

•ensure all grants are included as grant expenditures in the annual expenditure law/by-law.

First Nation Taxation Grant Programs

Enabling Granting Programs will require amendment to the FNTC Taxation Law Standards and FNTC Tax By-law Policy to:

•clarify that First Nations can establish granting programs to off-set taxes;

•ensure First Nations can design granting programs to reflect their community objectives; and

•ensure granting programs meet the policy requirements.

The Commission welcomes your input on these proposed changes to its standards and policy.

Section 33 FNTC Reviews

▶ Section 33 reviews are triggered when taxpayers, members, or the FNTC have a belief that the FN has not complied with the FSMA, or that its law has been improperly or unfairly applied.

▶ Regulations largely govern section 33 proceedings.

▶ FNTC is developing procedures for greater clarity, transparency and consistency.

The Year Ahead

• National Meeting of First Nations Tax Authorities

October 19, 2010.

• Working to assist First Nations in expanding revenue options (DCC’s, Taxation for the provisions of services).

• Sample laws for Quebec First Nations.

• BAT and Delegation of Authority Laws and Standards.

• Consulting with FNTAA and FN tax administrators on improving the annual laws/by-laws policy and procedures.

• Continue to work with the Institutions and communities to support First Nations borrowing.

Thank You

www.fntc.ca

(250) 828-9857 (Head Office)

(613) 789-5000 (NCR Office)