fintech ecosystem playbook - ey.comfile/ey... · fintech ecosystem playbook 6...

TRANSCRIPT

FinTech ecosystem playbook

1

FinTech ecosystem playbook

FinTech ecosystem playbook

2

Foreword

Inrecentyears,servicesprovidedbyfinancialtechnology(FinTech)start-upshavegainedprominence,andareincreasinglyimpactingconsumers,financialinstitutionsandeconomies.Subsequently,ecosystemshaveemergedaroundtheseFinTechs,consistingofmultipleinterdependentandinterconnectedstakeholders.

AFinTechecosystemismadeupofconsumers,financialinstitutions,FinTechstart-ups,investors,regulatorsandeducationalinstitutions.Thehealthydevelopmentofsuchanecosystemwillresultinmutuallybeneficialcooperationamongstakeholders,andeventually,helpfinancialservicesbedeliveredatlowercost,higherspeedandatbetterqualitytomoreconsumers.Thedevelopmentisparticularlydistinctinemergingmarketswherefinancialservicespresentuniqueopportunitiesandchallenges.

In FinTechecosystemplaybook,theteamsbringyouapanoramicviewofaFinTechecosysteminemergingmarketsinASEAN,LatinAmerica,Central,EasternandSoutheasternEurope&CentralAsia(CESA),theMiddleEast,Africa,andAsia-Pacific.

TheregulatorsandpolicymakersintheseemergingmarketsareactivelyseekingtodevelopattractiveFinTechecosystemsthrougharangeofpoliciesandotherinterventions.Thisreporthighlightssomeleadingpracticesandprovidesasummaryofwhatisgoingonattheregionalandcountrylevel.

Thereportwillnotberankingthehubsastheobjectiveistohelpeachhublearnfromglobalpeersandgrowtheindustryasawhole.SharingtheseleadingpracticesandsuccessstorieswiththeglobalFinTechcommunity,theteambelieveswillhelpusmakeadifference,together.

EYteamsexpressourgratitudetoFinTechassociationsandecosystemenablers,includingFintechGalaxy,FINNOVASIAandFinTechConsortium(FTC).

FinTech ecosystem playbook

3

14

20

26

30

35

40

44

ContentsFast facts

Objective of the study

Pillars of a FinTech ecosystem

Approach and coverage

FinTech hub trends

Cluster analysis

04

05

06

07

08

14

Key cluster takeaways

ASEAN

Latin America

CESA

The Middle East

Africa

Asia-Pacific

14

20

26

30

35

40

44

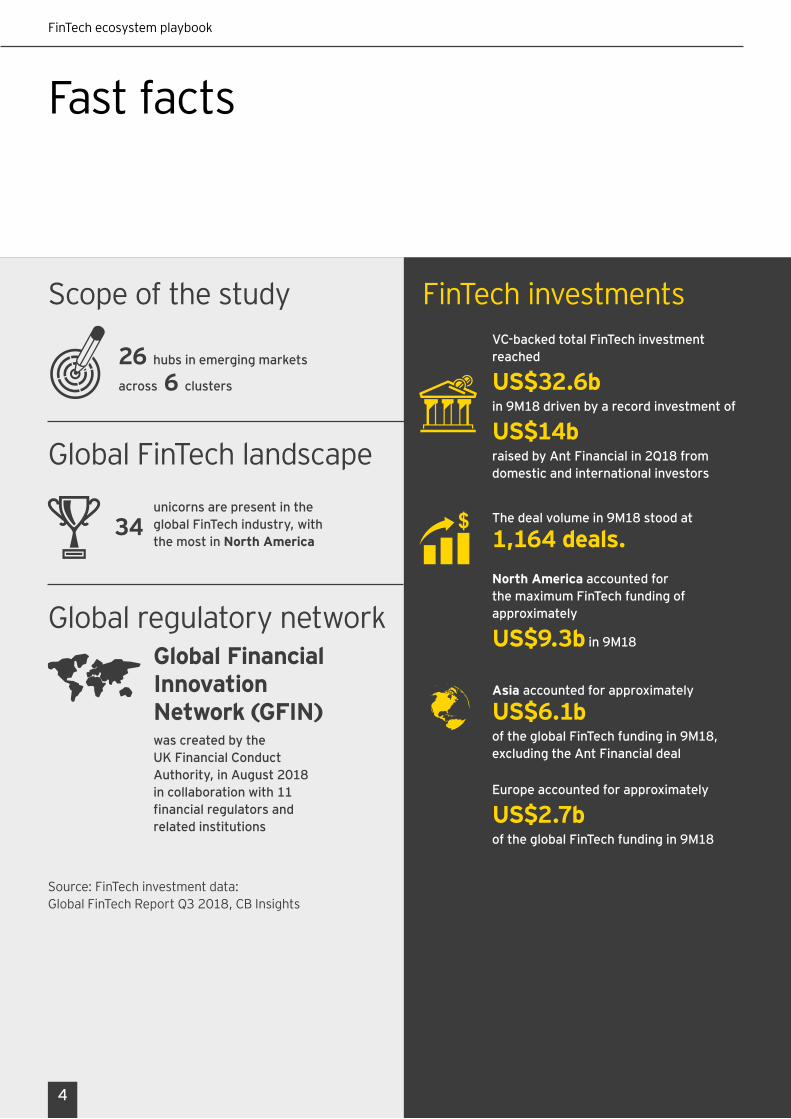

FinTechinvestmentsVC-backed total FinTech investment reached

US$32.6b8b in 9M18 driven by a record investment of

US$14b raised by Ant Financial in 2Q18 from domestic and international investors

$ The deal volume in 9M18 stood at

1,164 deals.North America accounted for the maximum FinTech funding of approximately

US$9.3b in 9M18

Asia accounted for approximately

US$6.1bof the global FinTech funding in 9M18, excluding the Ant Financial deal

Europe accounted for approximately

US$2.7bof the global FinTech funding in 9M18

34

Scopeofthestudy

GlobalFinTechlandscape

Globalregulatorynetwork

unicorns are present in the global FinTech industry, with the most in North America

Global Financial Innovation Network (GFIN)was created by the UK Financial Conduct Authority, in August 2018 in collaboration with 11 financial regulators and related institutions

26 hubs in emerging markets

across 6 clusters

Fastfacts

Source:FinTechinvestmentdata: GlobalFinTechReportQ32018,CBInsights

FinTechecosystemplaybook

4

Objectiveofthestudy

FinTechsareventuresthatleveragetechnologytodevelopnewandaugmentexistingcapabilitiesforthediscovery,distribution,operationsandservicingoffinancialproductsandservices.

AFinTechecosystemcomprises‘tech-savvy’start-upsandscale-ups,regulators,governments,traditionalinstitutions,investors,andtalentinstitutions.EachFinTechecosystemisconstantlyevolving,withplayerscontinuallyinteractinganddeveloping.Regulatorsaretaskedwiththechallengeofevolvingwith

theindustry.Theyneedtoensurethatcompetitionandinnovationarenotstifledwhilemaintainingthesafetyandsoundnessofthefinancialsystem.

The FinTech ecosystem playbook capturesthejourneyof26FinTechhubsintheemergingmarkets—theirexperiencesandlearningsintheprocessofbuildingastrongfinancialservicesecosystem.Theteamshighlightthebestindustrypracticesfromthesemarketssothatparticipantslearnfromeachother

This report will facilitate hubs to think global and act local.

Reviewofhub-levelbestpracticesthatdrivethedevelopmentoflocalFinTechecosystems

Local drivers

OverviewofkeyglobalFinTechtrendsthatareredefiningthefinancialserviceslandscape

Global trends

Studyofsixregionalclusters,assessingtheirmacroeconomicenvironmentandregionalopportunities

Regional opportunities

FinTechecosystemplaybook

5

FinTech ecosystem playbook

6

PillarsofaFinTechecosystem

• Strong:Collaborationwithincumbents;andpresenceofaccelerators,incubators,communityenablersandco-workingspaces(publicorcorporate)

• Scalable:Easeofaccesstolocalandinternationalmarkets

• Sustainable:Governmentandindustrysupportforsustainabledevelopment

Enablingenvironment

• Attract:Accesstointernationaltalent,easeofmobilityandvisapolicies

• Upskill:Developmentoftalentpipeline—universitycourses,researchanddevelopmentinvestment

• Retain:Policiesandinitiativesthatwouldreduce‘braindrain’andprovideconduciveenvironmenttogrowandflourish

Talentavailability

Sustaineddemand• Consumers:Digitalreadinessintermsofmobileandinternetpenetration,

smartphonepenetration,bankingpenetrationandeaseofaccesstofinancialservices

• Corporations:Demandfromenterprises,includingsmall-andmedium-sizedenterprises(SMEs)andinstitutions

• Financialinstitutions:DemandfromfinancialinstitutionsforFinTechofferings

• Riskcapital:Accesstoangelfunding,high-net-worthindividuals(HNIs)andgovernmentfunds;easeofraisingcapitalfromalternativesourcessuchasinitialcoinofferings(ICOs)

• Growthcapital:AccesstoVCandgovernmentfunds,financialinstitutionsandtechcompanies

• Strategiccapital:Fundingfromtraditionalinstitutions,techfirms,corporatesandprivateequity(PE)funds

Accesstocapital

• FinTechlaws:Specificregulationsandpolicies

• Overallregulatoryenvironment:Easeofdoingbusiness,creditavailability,taxationpolicies,visapoliciesandpresenceofregulatorysandboxes

• Competition:Encouragementofcompetitionthroughpolicies

Regulatoryopenness

FinTechecosystemplaybook

Approachandcoverage

Africa ASEAN Latin America CESA Middle East

Nigeria

Kenya

Singapore

Philippines

Malaysia

Brazil

Mexico

Estonia

Russia

UAE

Turkey

Bahrain

HongKongSAR,China

SouthAfrica Indonesia Lithuania China

SouthKorea

India

Vietnam

Cambodia

Thailand CzechRepublic SaudiArabia Japan

Asia-Pacific

Thesixclustersandrespectivehubsarepresentedbelow:

Thefollowingfour-stepapproachisundertakentoanalyzetheFinTechecosystemof26hubs:

7

UAEconstitutestwohubs—DubaiandAbuDhabi

Identifytheoveralldrivers,trendsandopportunitiesateachofthesixregionalclusters

AssesstheFinTechecosystemof26hubsbyleveragingEYextensiveresearchcapabilities,andnetworkofEYfinancialservicesandFinTechprofessionalsacrosstheglobe

Understand themacroeconomicanddigitalfactorsdrivingFinTechdevelopmentatcluster andhublevel

Discussthesuccessstoriesof26hubsbystudyingtheFinTechinitiatives

Advancingtechnologies,rapidlyexpandingeconomiesandchangingcustomerexpectationsaresomeofthefactorsdrivingdemandforFinTechproductsandservicesacrosscountries.Broadly,thedemandforFinTechscanbecategorizedinto:

FinTech hub trends

Demand

• Individuals:Inestablishedhubsthatenjoyhighbankingpenetration,demandislargelydrivenbytech-savvyconsumerslookingforabetterexperienceandawiderrangeofservices.Inemergingmarketswherefinancialinclusionisachallenge,FinTechsarehelpingbridgetheexclusiongap.Rapidurbanization,mobileandinternetpenetration,andeaseofusearedrivingindividualdemandforFinTechservices.AccordingtoWorldBank’sThe Global Findex Report 2017,69%ofadults,i.e.,3.8billionpeople,haveanaccountwithabankoramobilemoneyprovider,whichisanincreasefrom62%in2014andjust51%in2011.Theriseisattributabletotheincreasinguseofmobilephonesandtheinternet.Between2014and2017,thepercentageofuserssendingandreceivingpaymentsdigitallyincreasedfrom67%to76%globally;andfrom57%to70%inthedevelopingworld.

• Corporations and SMEs: SMEspresentanattractiveopportunityforFinTechs.Limited

financialhistory,smallticketloansandhighservicingcostresultedinthissegmentbeingunderservedbytraditionalinstitutions.Thedigitizationofthelendingprocess,includingtheassessmentofcreditrisk,isprovidingSMEswithanalternativewayoffunding.Digitalidentityprojectsinhubs,suchasSingapore,India,ChinaandEstonia,arepresentingnewopportunitiesforFinTechstoservicethisunmetdemandinanefficientmanner.

• Financial institutions: BanksacrosscontinentsarepartneringwithandinvestinginFinTechsacrossthebankvaluechaintodriveefficiencies,offernewproductsandaugmentcustomerexperience,resultinginrisingdemandforbusiness-to-business(B2B)solutions.

• Governments and regulators: RegulatorsareleveragingFinTechs’capabilitiestoimprovetheirprocesses.Forinstance,theMonetaryAuthorityofSingapore(MAS)haspartneredwithFinTechfirmAnquanforblockchain-basedProjectUbin.

Hub subsector specialization

Globally,successfulhubstendtohavediversityintheecosystem,withstart-upsspanningacrossmultiplesubsectorsandgrowthstages.

FinTechecosystemplaybook

8

FinTechecosystemplaybook

9

Atthesametime,someFinTechhubshaveidentifiedsubsectorswheretheyhavecertainadvantages,andhavemanagedtotakeleadershiporarepositioningthemselvestobecomethedominanthubforthosesubsectors.

Someexamplesinclude:

Switzerland for cryptocurrencySwitzerland,whereregulatorsdisplayedaclearandfriendlystanceinfavorofcryptocurrencyfromasearlyas2014,ishometotheCryptoValleyinthecityofZug.

Malaysia for Islamic bankingWithanestimatedMuslimpopulationof61.3%,andanenablingregulatoryenvironment,MalaysiahasmadeconsiderableadvancesintheIslamicbankingsector.

Stockholm for paymentsStockholmhasestablisheditselfasapaymentsgiantbyprovidingaconduciveenvironmentforpaymentFinTechs,andisthehomeofFinTechunicornsKlarnaandiZettle.

Increased access to government-backed funding:

Capital

• ForFinTechentrepreneurs,accesstocapitaloftendependsonanumberoffactorsincludingthestageofproductmaturity,backgroundoffounders,headquarterlocationofthecompanyandtargetcustomersegment.Toeasesomeofthecapitalchallenges,governmentsgloballyaresupportingstart-upsbygivingaccesstoriskandgrowthcapital.Somehubshavededicatedfundsorfund-of-funds(FOF)tosupportFinTechsintheirgrowthphase:

• TheDubaiInternationalFinancialCentre(DIFC)launchedaUS$100mFinTech-focusedfundinNovember2017toacceleratethedevelopmentoftheFinTechsectorbyinvestinginstart-ups,fromincubationtogrowthstage.

• TheGovernmentofIndia(GoI)introducedtheStartupIndiainitiativeinJanuary2016thatincludedaUS$1.5bFOFforstart-ups.

• InJune2018,BahrainDevelopmentBank(BDB)

announcedthatAlWahaFundofFunds,itsVCFOF,tosupportstart-upsinBahrainandacrosstheMiddleEastandNorthAfrica(MENA)region,hadraisedUS$100m.

• In2017,HongKongGovernmentlaunchedtheUS$256mInnovationandTechnologyVentureFundtoinvestinlocaltechnologystart-ups.

• InJune2015,Singapore’sMAScommittedS$225moverafive-yearperiodfortheFinancialSectorTechnologyandInnovationscheme.InDecember2017,itannouncedthelaunchoftheS$27mArtificialIntelligenceandDataAnalytics(AIDA)Grantunderthescheme.

• Policymakersarealsotakinginitiativestoimproveaccesstoprivatecapital:

• InJuly2018,theEstonianGovernment,throughitsEstFundFOF,invested€60mintoVCfundstosupportstart-upsandSMEs.Privateinvestorswilladd€40mto

theseVCfunds.

• Thisyear’sFinTech Investor Summit undertheMAS-sponsored Singapore FinTech Festival 2018hastwocomponents—(a)theFinTechDealDaythatconnectsFinTechswithpotentialinvestorsand(b)Meet ASEAN’sTalentsandChampions(MATCH)thatconnectsstart-upsandenterprisesinASEANacrossallsectorswithpotentialinvestors.The380participatinginvestorswhoenrolledforMATCHhaveindicated intentions to invest uptoatotalofUS$6.2binASEANenterprisesnextyear,andanadditionalUS$6bearmarkedoverthesubsequenttwoyears.Morethan17,000matchesweregeneratedbetweenthe380participatinginvestorsand840enterprise.

FinTech ecosystem playbook

10

Talent

• Themostsought-aftertechnicaltalentincludedatascientists,financialengineers,mobilemarketersandcomputerprogrammers.

• TheBigTechfirmsaregivingstiffcompetitiontoFinTechsandfinancialinstitutionsintheireffortstoattractstrongtechtalent.

• Somecountries,suchastheUK,FranceandtheUAE,are

attemptingtoimporttechnicaltalentfromothercountriesbyofferingspecialvisas.TheUKoffersavisarouteundertheUKRIScience,ResearchandAcademiaschemefornon-EuropeanEconomicArea(EEA)researchersandplanstoofferstart-upvisasforforeigntechentrepreneurs.TheUAEintroduceda10-yearresidencyvisaforinvestorsandspecialists.Meanwhile,countriessuchas

EstoniaandLithuaniahaveStartupVisaprograms.

• NurturingdomestictalentisasustainablesolutiontothetalentunavailabilitychallengefacedbyFinTechsandfinancialinstitutions.HongKongandSingaporearemovingtowardthisdirectionbypartneringwithschoolstotrainstudentstodevelopFinTechknowledgeandcapabilities.

Attracting talent considered key by FinTechs:

Making the workforce future-ready through FinTech-focused talent initiatives:

• Ascompetitionfortechtalentintensifiesglobally,hubsaredevelopingFinTech-focusedspecializedprogramsandinitiativestodevelopthelocaltalentpool.Someinitiativesbeingtakenbythehubsinclude:

• FinTech-specificcoursesandprogramsincludinggovernment-ledinitiatives:

• SingaporeoffersFinTech-specificcoursesunderitsSkillsFutureprogram.TheNationalTradesUnionCongress,SingaporePolytechnic(SP)andtheSingaporeFinTechAssociation(SFA)havejointlycreatedtheFinTechTalentProgramme.

• TheHongKongGovernmenthaslaunchedtwodedicatedpubliclyfundeddegreesinFinTech,beginningacademicyear2017-18:BachelorofEngineeringProgrammeinFinancialTechnologyatTheChineseUniversityof

HongKongandBachelorofScience(Hons)inFinancialTechnlogyatHongKongPolytechnicUniversity.

• InIndia,BombayStockExchangelaunchedanMBAprograminFinTechinassociationwiththeUniversityofMumbaiin2017.

• AbuDhabiGlobalMarket(ADGM)offersFinTech-specificcoursesthroughtheADGMAcademy.

• FinTechtalentincubatorandacceleratorprograms:

• TheHongKongMonetaryAuthority(HKMA)haspartneredwiththeHongKongAppliedScienceandTechnologyResearchInstitute(ASTRI)fortheFintechCareerAcceleratorScheme(FCAS),whichprovidesinternshipintheFinTechindustrytoundergraduateandpostgraduatestudents.

• SingaporehaslaunchedtheTechSkillsAccelerator(TeSA)FinTechCollectivetostrengthenSingapore’sinfocommandFinTechtalentpool.

• Onlinelearninginitiatives:InOctober2017,theUniversityofHongKong(HKU)launchedAsia’sfirstFinTechMassiveOpenOnlineCourse(MOOC).

FinTech ecosystem playbook

11

Regulations

ToincreasecompetitionandprovideanenablingenvironmentforFinTechfirms,countriesarepushingoutinitiativesinvaryingdegreeswithregardstoOpenBanking.ItallowsFinTechstoleverageonbanks’datatoprovideandextendtheirofferingstobankcustomers.Theteamshavehighlightedafewofthedifferentapproachesundertakenbyregulators:

Facilitation of innovation through Open Banking

Regulatory trends

ChangeisconstantintheFinTechspace,witheachideabeingmorerevolutionarythanthepreviousone.Itisamomentoustaskforregulatorstoprovideregulatoryoversighttoprotectconsumerswhilebeingmindfulofnotinhibitinginnovation.Regulatorshavetakendifferentapproaches,buttheyhavelargelyconvergedintoafewsimilarways:

• Introduction of sandboxes: FinTechswithinasandboxareabletolaunchproductsandserviceswithoutnecessarylicenses.However,thenumberofconsumerswhomtheycanservewouldbelimitedtocontainanypossiblenegativeeffects.Atthesametime,regulatorswouldbeabletohaveconstantconsultationswithcompanieswithinthesandboxtounderstandthesubsector.

• Economic zones:Somecountrieshavecreatedspecialeconomiczoneswhereinnovativefirmscanbesetup.Thesezoneshavevaryingbenefits;buttheunderlyingconceptisthesame—toprovidealocationforthefirmstoinnovateandofferassistancethroughregulationsthatarespecifictothezones.Theseregulationsmayincludelowertaxes,permissiontooperate

withoutnecessarylicenses(orwithspeciallicenses)andfrequentconsultationswithregulators.

• Consultations with industry players:Regulatorshavebeenrunningconsultationswithindustryplayerstolearnwheretheindustryisheadingto,inordertogainanunderstandingoftheindustryandknowhowtheycouldsupporttheindustrywhileprotectingtheconsumers.

• Guiding principles and frameworks rather than rules: AstheFinTechspaceisever-changing,someregulatorshaveimplementedguidingprinciplestomaketheirstanceclear,insteadofcreatingdefiniterulesthatmayinhibitinnovation.

• FinTech laws or licenses: To assistFinTechswithinthelocalenvironmentwithoutchanging

muchofthelocalregulations,somecountrieshaverolledoutFinTech-relatedlawsorlicensesthatallowFinTechstooperatewithouttheneedtogainabankinglicense.

• TheUKpioneeredOpenBanking,launchingtheinitiativeinJanuary2018,thatmandatesnineUKbankstoopenuptheirdataviaasetofsecureapplicationprograminterfaces(APIs).

• Singapore’sMASisencouragingfinancialinstitutionstoadoptOpenAPIasakeyfoundationallayerforinnovationandinteroperability,althoughitis

notmandated.

• InJuly2018,HongKong’sHKMAlaunchedthedraftOpenAPIframework,whichsetouttimelinesforinstitutionstofollow,andmaderecommendationsonspecificprotocolsanddataformats.TheframeworkalsolaidoutexpectationsonhowbanksshoulddeployOpenAPI.

• IntheEU,therevisedPaymentServiceDirective(PSD2)requiresbankstoshareinformationoftheircustomers’accountswiththirdpartieswiththeauthorizationofthecustomers.

FinTech ecosystem playbook

12

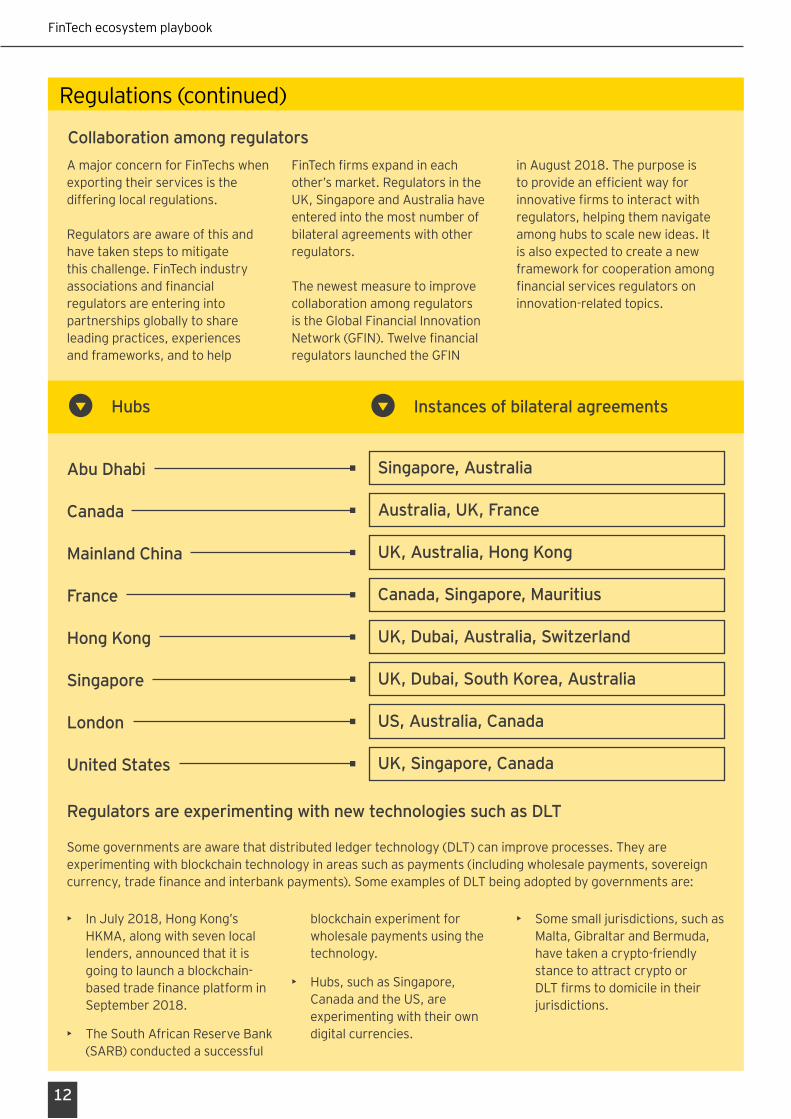

Collaboration among regulators

Regulations(continued)

AmajorconcernforFinTechswhenexportingtheirservicesisthedifferinglocalregulations.

Regulatorsareawareofthisandhavetakenstepstomitigatethischallenge.FinTechindustryassociationsandfinancialregulatorsareenteringintopartnershipsgloballytoshareleadingpractices,experiencesandframeworks,andtohelp

FinTechfirmsexpandineachother’smarket.RegulatorsintheUK,SingaporeandAustraliahaveenteredintothemostnumberofbilateralagreementswithotherregulators.

ThenewestmeasuretoimprovecollaborationamongregulatorsistheGlobalFinancialInnovationNetwork(GFIN).TwelvefinancialregulatorslaunchedtheGFIN

inAugust2018.Thepurposeistoprovideanefficientwayforinnovativefirmstointeractwithregulators,helpingthemnavigateamonghubstoscalenewideas.Itisalsoexpectedtocreateanewframeworkforcooperationamongfinancialservicesregulatorsoninnovation-relatedtopics.

Abu Dhabi Singapore, Australia

Canada Australia, UK, France

Mainland China UK, Australia, Hong Kong

France Canada, Singapore, Mauritius

Hong Kong UK, Dubai, Australia, Switzerland

Singapore UK, Dubai, South Korea, Australia

London US, Australia, Canada

United States UK, Singapore, Canada

Hubs Instances of bilateral agreements

Regulators are experimenting with new technologies such as DLT

Somegovernmentsareawarethatdistributedledgertechnology(DLT)canimproveprocesses.Theyareexperimentingwithblockchaintechnologyinareassuchaspayments(includingwholesalepayments,sovereigncurrency,tradefinanceandinterbankpayments).SomeexamplesofDLTbeingadoptedbygovernmentsare:

• InJuly2018,HongKong’sHKMA,alongwithsevenlocallenders,announcedthatitisgoingtolaunchablockchain-basedtradefinanceplatforminSeptember2018.

• TheSouthAfricanReserveBank(SARB)conductedasuccessful

blockchainexperimentforwholesalepaymentsusingthetechnology.

• Hubs,suchasSingapore,CanadaandtheUS,areexperimentingwiththeirowndigitalcurrencies.

• Somesmalljurisdictions,suchasMalta,GibraltarandBermuda,havetakenacrypto-friendlystance to attract crypto or DLTfirmstodomicileintheirjurisdictions.

FinTech ecosystem playbook

13

Speeding innovation through public accelerator programs

Receiving support from traditional financial institutions

Offering FinTechs global platform through branding and positioning initiatives

Environment

• Incubators,acceleratorprogramsandinnovationslabsorcentersareimportantleverstodrivetheFinTechsectorinaneconomy.Hubsgloballyhaverecognizedthesignificanceoftheseprogramsaimedatdevelopingstart-upsbyprovidingmentoring,funding,training,networking,andmarketingandpublicrelationopportunities:

• Dubai’sDIFChaslauncheditsFinTechHiveacceleratorprogram,whichfocusesonFinTechopportunitiesintheMiddleEast,AfricaandSouthAsia(MEASA)region’sfinancialsector.

• ADGMinAbuDhabihastiedupwithPlugandPlaytolaunchitsacceleratorinOctober2017.

• K-StartupGrandChallengeisagovernment-supportedstart-upacceleratorprograminSouthKorea.

• Singapore’sMASrunsitsglobalacceleratorprogram,Global FinTech Hackcelerator, focusingonstart-upsacrosstheglobe.

• Itisimperativethatgovernment-ledinitiativesaresupportedbyindustryparticipantsinordertoensureathrivingFinTechecosystem.Financialinstitutionsgloballyaresupportingthesectorthroughvariousinitiatives:

• Banksglobally,suchasCiti,

HSBC,Santander,BBVA,UnitedOverseasBankandBankMandiri,havededicatedfundstoinvestinFinTechventures.Ithelpsbankstoachieveatwo-foldobjective:investingtoenjoythebenefitsofrisingFinTechvaluations,andleveraging

theFinTechs’technologicaladvantageinordertoimprovetheirownproductsandprocesses.

• BanksareactivelyengagingwithFinTechsthroughinnovationlabs,hackathonsandacceleratorprograms.

• Severalhubsglobally,throughFinTecheventsandprograms,areprovidingFinTechswithaplatformtoconnect,collaborateandnetworkwithinvestors,techplayers,industryparticipantsandregulators.Theseeventsencompassaseriesofconferences,workshops,awardsandexhibitionsaswellasnetworking,amongotheractivities:

• TheSingapore FinTech Festival (aweek-longevent)isorganizedbyMASinpartnershipwiththeAssociationofBanksinSingaporeandincollaborationwithSingExHoldings.ItincludestheGlobal FinTech Hackcelerator, FinTechconferenceandexhibition,theFinTech Investor Summit and FinTech Awards.

• Hong Kong FinTech Week 2018, hostedbyInvestHongKong

(InvestHK),offersawindowintoHongKong’spositionasAsia’sfinancialhub,andasanentrypointtoPeople’sRepublicofChinaandtheGreaterBayArea.ThethirdannualHong Kong FinTech Week,heldfrom29October2018to2November2018,isthefirstcross-borderFinTechevent,expandingfromHongKongtoShenzhen.

Cluster analysis

Cluster: Key takeaways

ASEAN Fast-growingeconomieswithlargepopulations makeauniqueplayground

Drivers Thekindofdemandandsupplythathavebeendrivingthedevelopmentoftheecosystemsofar

SpotlightNotableplayersandtrendsthathaveemergedinthelocalandregionalecosystem

OpportunityAreasthatpresentsignificantroomforgrowthinthenearfuture

Drivers ASEANistheconnectingbridgebetweenChinaandIndia,makingitaperfectplaceforlargelocalandglobalplayerstocollaborateandcompete.Regulatorsaresupportinginnovation,butatthesametime,arecautiousinordertoensurethatthefinancialsystemispreparedtohandlethestressofaglobalfinancialcrisis.

SpotlightE-commerce,andsocialandmobilityplayersareexpandingintothefinancialservicesfield,leveragingontheirlargeuserbase.

FinTechecosystemplaybook

14

FinTech ecosystem playbook

15

OpportunityTheregionhassomeofthefastest-growingeconomieswiththelargestpopulationbases,andastronghistoricalandculturalheritage.Astheseeconomiescontinuetogrow,therewillbemoredemandforbetterqualityservices.

Drivers SeveralgovernmentsareconsideringFinTechdevelopmentasoneofthepillarstoincreasefinancialinclusion.ThedevelopmentofFinTechhasbeendrivenbystart-upsseekingtoservesegmentspreviouslyinadequatelyaddressedbythefinancialsystem.Financialinclusionwilldrivesustainableeconomicdevelopment.

SpotlightPrivatecorporationsandinternationalinvestorsarebuildingventurestocomplementexistingfinancialservicesproviders.

OpportunityCollaborationintheregionisbecomingmorefrequentandthedevelopmentoftheFinTechindustrywillallowtheexpansioninquantityandqualityofsynergiesamongdifferentactorsintheecosystem.

Latin America Opportunitiesinunderservedmarket

FinTech ecosystem playbook

Drivers Attheturnofthecentury,theseeconomiesopenedup,andsincethenhavebecomeanattractiveinvestmentdestinationduetoconsumerspendinggrowth,competitivewageratesandskilledworkforce.Theregionhasstronginfrastructureandtalentthatarebeingleveragedupon.

SpotlightTheregionisdevelopinghomegrowncompaniesandattractinginternationalcompaniestosetupheadquarterstoservicetheEUmarket.

OpportunityBybeingpartoftheEU,countrieshaveaccesstoalargeunifiedmarket.TheregionisplacedstrategicallybetweenAsia,theMiddleEastandEurope,andcanbeabridgeforcompaniesexpandinggeographicallyintheseareas.

CESA Leveragingstrongtalentbase

The Middle East GovernmentsupportandcapitaldrivingFinTechgrowth

Drivers Capitalhasbeenoneofthekeystrengthsoftheregionduetothepresenceoflargesovereignandprivatefundsthathavealonghistoryofglobalinvestments.SeveralstatesviewFinTechasamajoralleytodiversifytheireconomiesfromnaturalresourcesandhavespecificinitiativestodrivefinancialservices.

16

FinTechecosystemplaybook

FinTech ecosystem playbook

17

Drivers Theregionhasoneofthelargestconcentrationoftheunbankedandunderbankedpopulation,whichprovidesanopportunityforleapfroggingseveralgenerationsoftechnologyandinfrastructuretoprovideacuttingedgesolution.Forexample,theregionhasskippedlandlinesand2Gtogodirectlyto3Gand4G.

SpotlightSeveralwalletsbackedbytelecommunicationcompanieshavebecomeglobalcasestudiesoffinancialinclusion.Mostoftheinnovationisdrivenbytelecomplayers,whichisuniquetotheregion.

OpportunityLargepenetrationofmobilemoneyaccountspresentopportunitiestoFinTechstoexploreexpansioninotherareasincludingalternativelending,cross-bordertransfers,personalfinanceandremittances.CollaborationwithlocalfinancialplayerscanhelpFinTechsnavigatethismarket.

Africa Leapfroginnovations

SpotlightSomeofthehubshaveregulatorytechnology(RegTech)asprimaryfocus.OthershavepositionedthemselvesaslaunchpadstoservicethewholeMiddleEastmarket.

OpportunityTheregionoffersuniqueopportunitytoFinTechproductsandservicesthatarefocusedonIslamicbanking.FinTechscanalsohelpsolvethechallengeoffragmentedaccesstofinancialservicesintheregion.

MainlandChinaandHongKong:

Drivers InMainlandChina,confluenceoffactors,includingrelaxedregulations,vastmarketofunaddressedfinancialneedsandthegrowthindigitalpenetration,revolutionizedfinancialservicesandmadeFinTech‘awayoflife’.ProximitytoMainlandChinaandsupportiveregulationsarethekeydriversforFinTechinHongKong.

SpotlightMainlandChinahasindependentfinanceandlifestyle(FinLife)ecosystemsthatstartedoutase-commerceandchatplatformsbeforedevelopingintofull-scalefinancialservicesprovidersgoingontoearnbanklicenses.

OpportunityForChina-basedcompanies,leveringdataandtechtoexpandoutsidecoreareasaswellasinglobalmarketsiskeytogrowth.

India:

Drivers Government-leddigitalinfrastructure,andrapidurbanizationandmobilepenetrationisdrivingthedevelopmentofFinTechsector,particularlyinpayments.

SpotlightIndianFinTechplayersareraisinglargefundingfromforeigninvestorslookingtoexpandoverseas.IndiaisnowhometotwoFinTechunicorns.

Asia RiseofindependentFinLifeecosystemplatformsinGreaterChina;andIndiabringingthebestfromEastandWest.

18

FinTechecosystemplaybook

FinTech ecosystem playbook

19

OpportunityInIndia,globalinvestors,suchasChineseinternetfinanceplayersandAmericane-commerceplayers,havesetupgreenfieldventuresaswellasinvestedsignificantlyinlocalventures,creatinganinterestingstageforaFinTechecosystemtobebuilt.B2Bbusinessmodelsaregainingprominencegiventhebackdropofgovernmentinitiatives.

ASEAN

Keyhighlights

TheInternationalFinancialCorporation,alongwithregionalstakeholders,establishedtheASEANFinancialInnovationNetwork(AFIN)in2017tofacilitatecollaborationamongfinancialinstitutionswiththeprimaryobjectiveoffinancialinclusion.

Theregionhasanestimatedpopulationof646million,withamedianageof28.8years.Ithasa58%internet penetration ratewith390.8millionmobileusers.FinTechinvestmentwasUS$366min2017.

ASEANFintechNetwork(AFN)waslaunchedinNovember2017toenablecollaborationandcooperationonFinTechecosystemsamongsixparticipatingnations.

Malaysia

Thailand

Indonesia

Philippines

Singapore

Cambodia

Vietnam

FinTechecosystemplaybook

20

FinTech ecosystem playbook

21

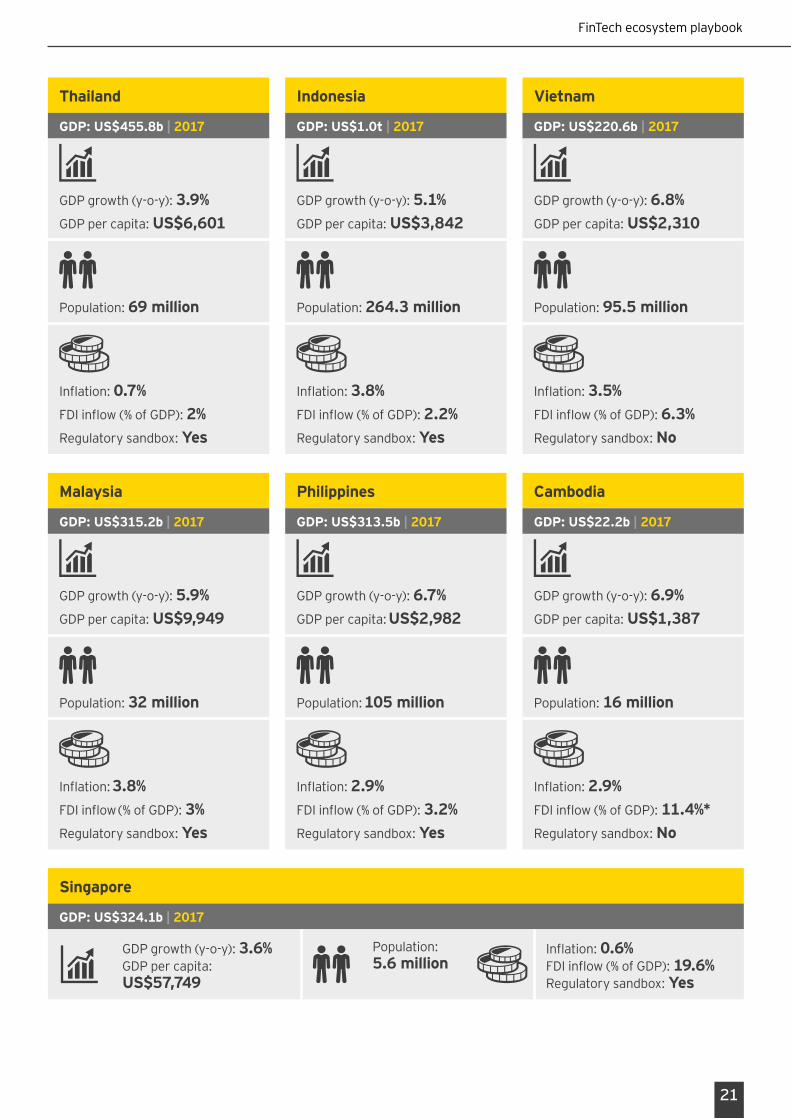

Keyhighlights

Thailand

GDP: US$455.8b | 2017

GDPgrowth(y-o-y):3.9%GDPpercapita:US$6,601

Population:69 million

Inflation:0.7%FDIinflow(%ofGDP):2%Regulatorysandbox:Yes

Indonesia

GDP: US$1.0t | 2017

GDPgrowth(y-o-y):5.1%GDPpercapita:US$3,842

Population:264.3 million

Inflation:3.8%FDIinflow(%ofGDP):2.2%Regulatorysandbox:Yes

Vietnam

GDP: US$220.6b | 2017

GDPgrowth(y-o-y):6.8%GDPpercapita:US$2,310

Population:95.5 million

Inflation:3.5%FDIinflow(%ofGDP):6.3%Regulatorysandbox:No

Philippines

GDP: US$313.5b | 2017

GDPgrowth(y-o-y):6.7%GDPpercapita: US$2,982

Population: 105 million

Inflation:2.9%FDIinflow(%ofGDP):3.2%Regulatorysandbox:Yes

Cambodia

GDP: US$22.2b | 2017

GDPgrowth(y-o-y):6.9%GDPpercapita:US$1,387

Population:16 million

Inflation:2.9%FDIinflow(%ofGDP):11.4%*Regulatorysandbox:No

Malaysia

GDP: US$315.2b | 2017

GDPgrowth(y-o-y):5.9%GDPpercapita:US$9,949

Population:32 million

Inflation: 3.8%FDIinflow (%ofGDP):3%Regulatorysandbox:Yes

Singapore

GDP: US$324.1b | 2017

GDPgrowth(y-o-y):3.6%GDPpercapita:US$57,749

Population:5.6 million

Inflation:0.6%FDIinflow(%ofGDP):19.6%Regulatorysandbox:Yes

FinTech ecosystem playbook

22

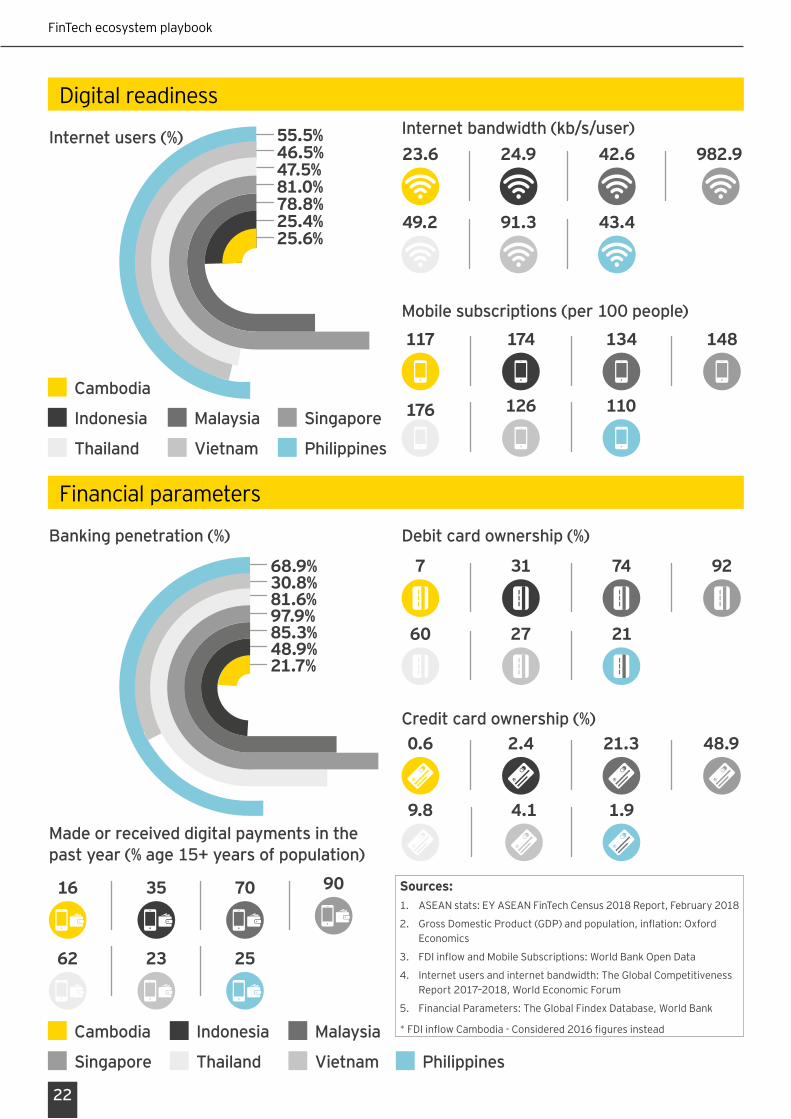

DigitalreadinessInternet bandwidth (kb/s/user)

982.923.6

49.2

24.9

91.3

42.6

43.4

Mobile subscriptions (per 100 people)

110

134

126

174

176

117 148

Cambodia

Indonesia Malaysia Singapore

Thailand Vietnam Philippines

Cambodia Indonesia Malaysia

Singapore Thailand Vietnam Philippines

Financialparameters

Banking penetration (%) Debit card ownership (%)

7 92

60 27

31 74

21

Credit card ownership (%)0.6 2.4 21.3

1.94.19.8

48.9

Made or received digital payments in the past year (% age 15+ years of population)

16 35 70

25

90

62 23

Sources: 1. ASEANstats:EYASEANFinTechCensus2018Report,February2018

2. GrossDomesticProduct(GDP)andpopulation,inflation:OxfordEconomics

3. FDIinflowandMobileSubscriptions:WorldBankOpenData

4. Internetusersandinternetbandwidth:TheGlobalCompetitivenessReport2017–2018,WorldEconomicForum

5. FinancialParameters:TheGlobalFindexDatabase,WorldBank

*FDIinflowCambodia-Considered2016figuresinstead

46.5%55.5%

47.5%81.0%78.8%25.4%25.6%

Internet users (%)

68.9%30.8%81.6%97.9%85.3%48.9%21.7%

FinTech ecosystem playbook

23

Success stories

Singapore• MASsetuptheFinancial

TechnologyandInnovationGroup(FTIG)withinitsorganizationalstructurein2015.TheformationofFTIGisacommitmentbyMAStowardthevisionofasmartfinancialcenter.In2016,MASsetupFinTechOfficetoserveasaone-stopvirtualentityforallFinTechmatters.

• OtherinitiativesoftheSingaporeGovernmentincludetheFinTechRegulatorySandbox,RegTechinitiativesandtheintroductionofblockchainforinterbankpayments.In2015,MASannouncedthatitwouldcommitS$225moverthefollowingfiveyearsforFinTechprojects.MAShasalsoissuedguidanceonICOsandplanstoissueguidelinesfortheuseofartificialintelligence(AI)intheindustry.

• TheannualSingapore FinTech Festivalseestheparticipationofthousandsofstart-upsandinvestors.Over30,000peoplefrom109countriesrepresentingmorethan5,000companiestookpartinthefestivalin2017.

• TheIntellectualPropertyOfficeofSingaporelaunchedtheFinTechFastTrackinitiative,whichprovidesexpeditedpatentapplication-to-grantprocessforFinTechinventions.

• SingaporeFinTechAssociation(SFA)isacross-industryinitiativethathasover300members.

Malaysia• Malaysiawasthefirstcountry

inASEANtointroducearegulatoryframeworkforequitycrowdfunding(ECF)andpeer-to-peer(P2P)financing.BankNegaraMalaysia(BNM)hasestablishedcross-functionalFinancialTechnologyEnablerGroup(FTEG)withinthebank.FTEGisresponsibleforformulatingandenhancingregulatorypoliciestofacilitatetheadoptionoftechnologicalinnovationsintheMalaysianfinancialservicesindustry.BNMalsolaunchedanOpenAPIworkinggroupinSeptember2018.

• MalaysiaaspirestobecomeanIslamicFinTechhub,asevidencedbystrongsupportfromregulators.

• BNMreleasedguidelinesone-KYCin2017.Theguidelinessetoutminimumrequirementsandstandardsthatanapprovedremittanceserviceprovidermustobserveinimplementinge-KYC.

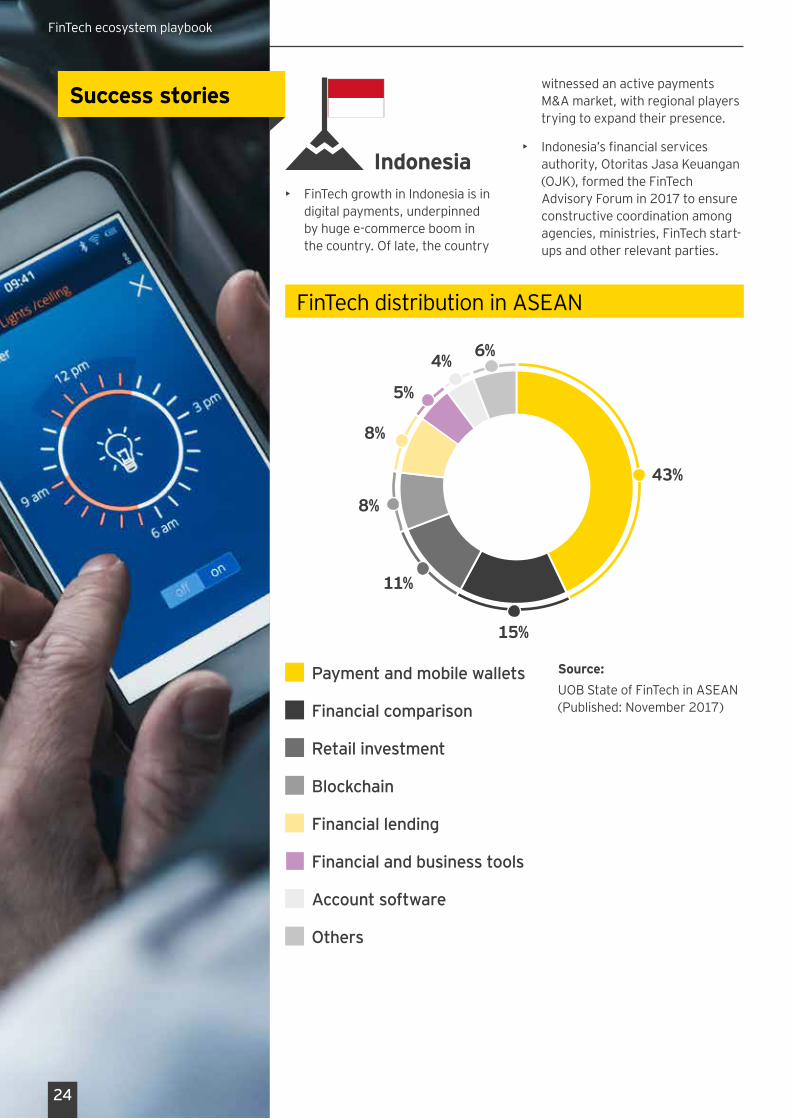

Indonesia• FinTechgrowthinIndonesiaisin

digitalpayments,underpinnedbyhugee-commerceboominthecountry.Oflate,thecountry

witnessedanactivepaymentsM&Amarket,withregionalplayerstryingtoexpandtheirpresence.

• Indonesia’sfinancialservicesauthority,OtoritasJasaKeuangan(OJK),formedtheFinTechAdvisoryForumin2017toensureconstructivecoordinationamongagencies,ministries,FinTechstart-upsandotherrelevantparties.

FinTechdistributioninASEAN

15%

43%

6%4%

5%

8%

8%

11%

Payment and mobile wallets

Financial comparison

Retail investment

Blockchain

Financial lending

Financial and business tools

Account software

Others

Source: UOBStateofFinTechinASEAN(Published:November2017)

24

Success stories

FinTechecosystemplaybook

FinTech ecosystem playbook

25

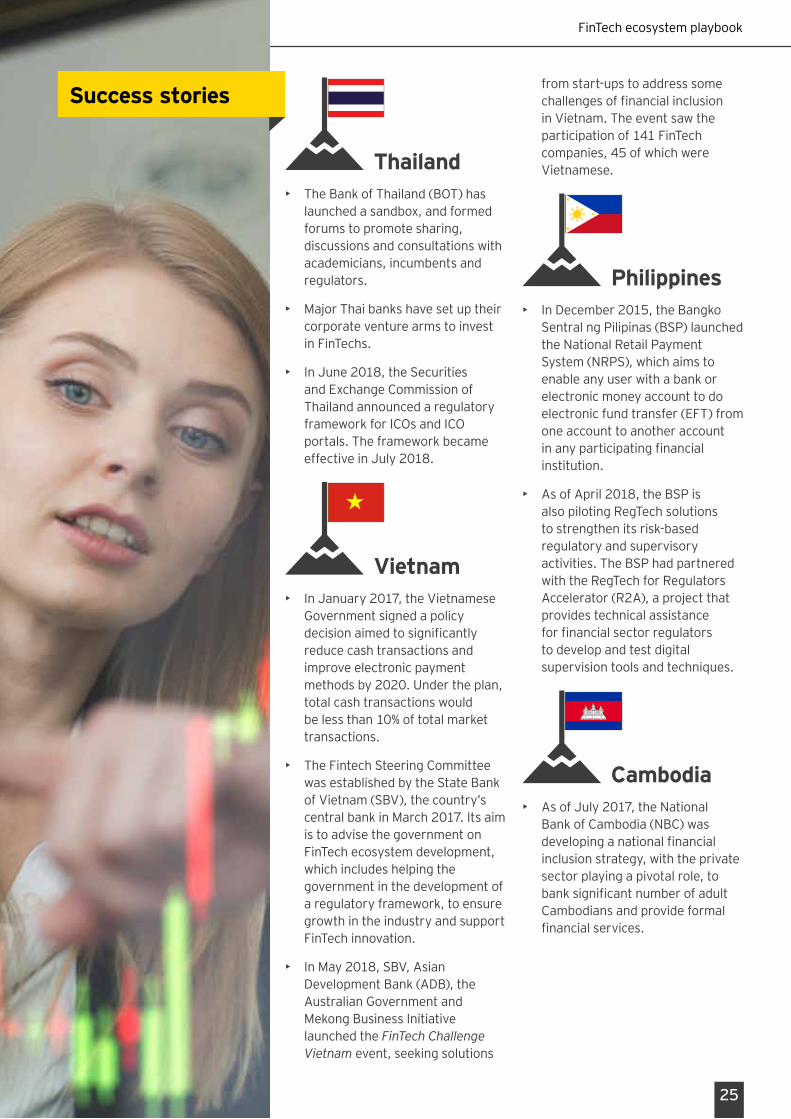

Thailand• TheBankofThailand(BOT)has

launchedasandbox,andformedforumstopromotesharing,discussionsandconsultationswithacademicians,incumbentsandregulators.

• MajorThaibankshavesetuptheircorporateventurearmstoinvestinFinTechs.

• InJune2018,theSecuritiesandExchangeCommissionofThailandannouncedaregulatoryframeworkforICOsandICOportals.TheframeworkbecameeffectiveinJuly2018.

Vietnam• InJanuary2017,theVietnamese

Governmentsignedapolicydecisionaimedtosignificantlyreducecashtransactionsandimproveelectronicpaymentmethodsby2020.Undertheplan,totalcashtransactionswouldbelessthan10%oftotalmarkettransactions.

• TheFintechSteeringCommitteewasestablishedbytheStateBankofVietnam(SBV),thecountry’scentralbankinMarch2017.ItsaimistoadvisethegovernmentonFinTechecosystemdevelopment,whichincludeshelpingthegovernmentinthedevelopmentofaregulatoryframework,toensuregrowthintheindustryandsupportFinTechinnovation.

• InMay2018,SBV,AsianDevelopmentBank(ADB),theAustralianGovernmentandMekongBusinessInitiativelaunchedtheFinTech Challenge Vietnamevent,seekingsolutions

fromstart-upstoaddresssomechallengesoffinancialinclusioninVietnam.Theeventsawtheparticipationof141FinTechcompanies,45ofwhichwereVietnamese.

Philippines• InDecember2015,theBangko

SentralngPilipinas(BSP)launchedtheNationalRetailPaymentSystem(NRPS),whichaimstoenableanyuserwithabankorelectronicmoneyaccounttodoelectronicfundtransfer(EFT)fromoneaccounttoanotheraccountinanyparticipatingfinancialinstitution.

• AsofApril2018,theBSPisalsopilotingRegTechsolutionstostrengthenitsrisk-basedregulatoryandsupervisoryactivities.TheBSPhadpartneredwiththeRegTechforRegulatorsAccelerator(R2A),aprojectthatprovidestechnicalassistanceforfinancialsectorregulatorstodevelopandtestdigitalsupervisiontoolsandtechniques.

Cambodia• AsofJuly2017,theNational

BankofCambodia(NBC)wasdevelopinganationalfinancialinclusionstrategy,withtheprivatesectorplayingapivotalrole,tobanksignificantnumberofadultCambodiansandprovideformalfinancialservices.

Success stories

ASEANFinTechNetwork(AFN)waslaunchedinNovember2017toenablecollaborationandcooperationonFinTechecosystembetweensixparticipatingnations

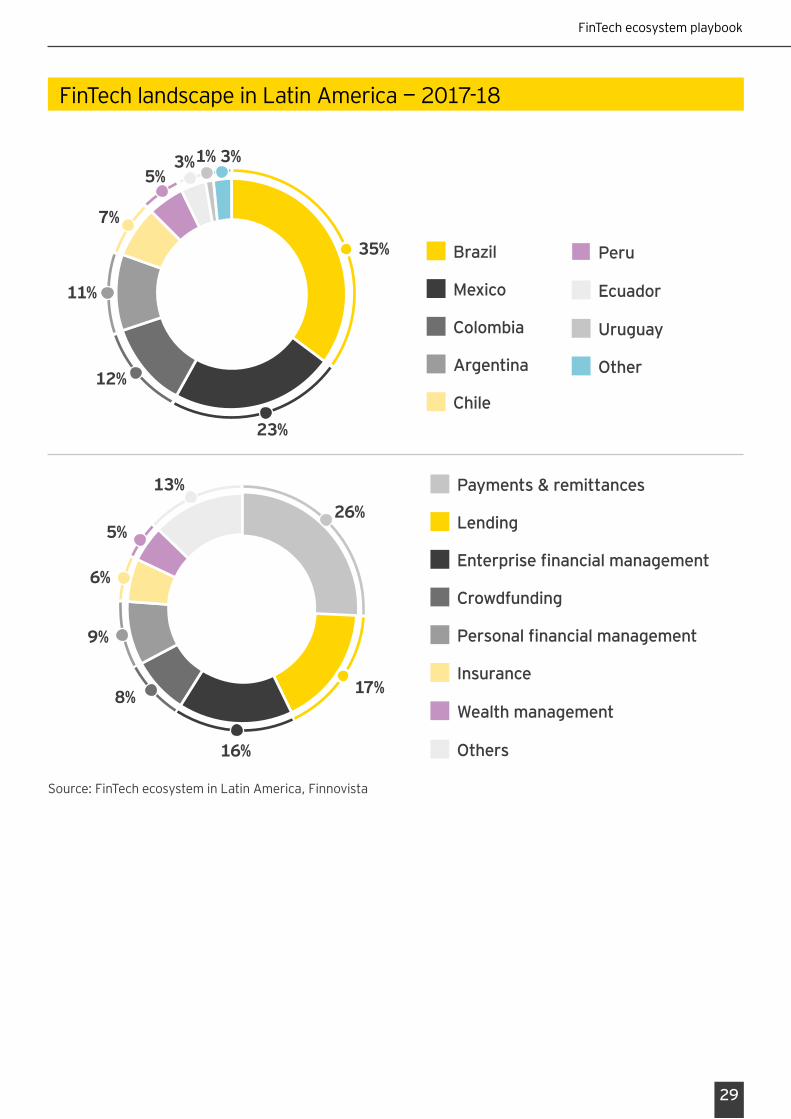

AccordingtoWorldBank’sGlobal Findex Database 2017, themobileinternetpenetrationinLatinAmericaandCaribbeanregionis55%,whichis15%morethanthedevelopingworldaverage.

Theregionhasanestimatedpopulationof553millionwith80%ofpeoplelivinginurbanareas.

Thereareabout1,034FinTechstart-upsinLatinAmerica,ofwhich41%serviceunderservedorexcludedcustomersandtheSMEmarket.

Latin America

Mexico

Brazil

Keyhighlights

26

FinTechecosystemplaybook

FinTech ecosystem playbook

27

Mexico

GDP: US$1.2t | 2017

GDPgrowth(y-o-y):2.3%GDPpercapita:US$8,935

Population:129.4 million

Inflation:6.0%FDIinflow(%ofGDP):2.8%Regulatorysandbox:Yes

Brazil

GDP: US$2.1t | 2017

RealGDPgrowth(y-o-y):1.0%GDPpercapita: US$9,810

Population: 209.5 million

Inflation:3.5%FDIinflow(%ofGDP):3.4%Regulatorysandbox:No

Digitalreadiness

Internet bandwidth (kb/s/user)

66.2 24.9

Mobile subscriptions (per 100 people)

113.0 88.5Brazil

Mexico

Internet users (%)

59.559.7

Keyhighlights

28

Success stories

Financialparameters

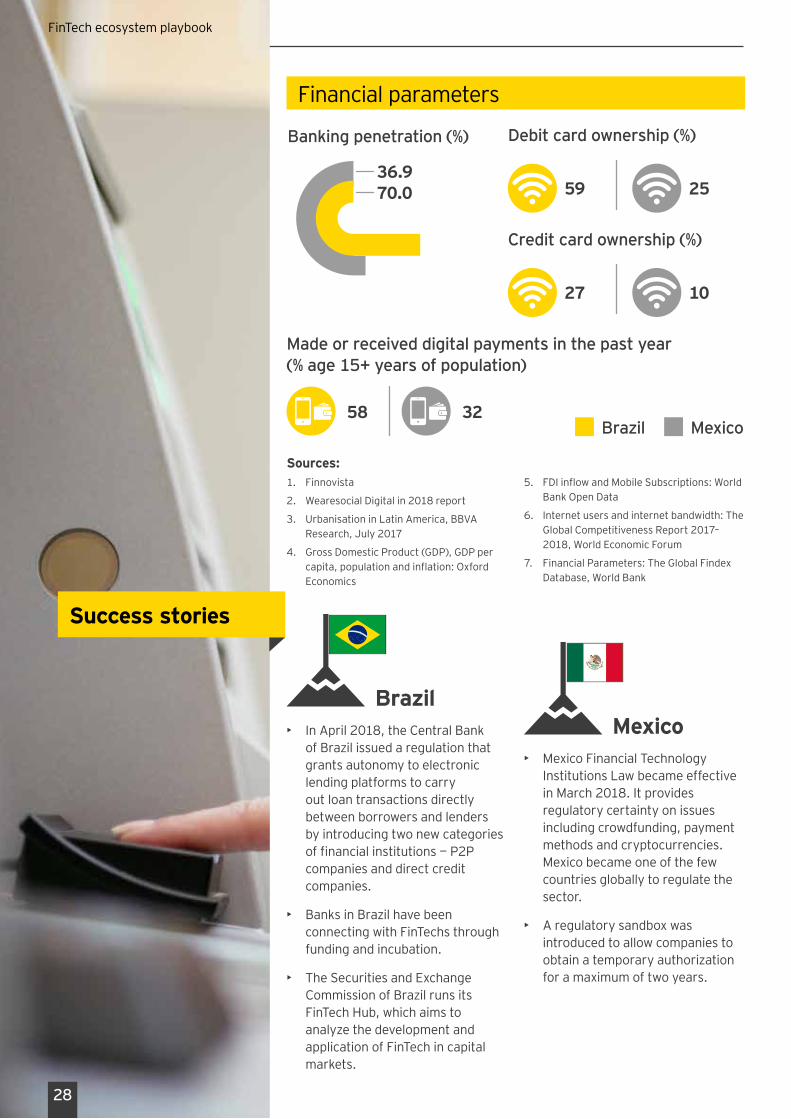

Debit card ownership (%)

59 25

Credit card ownership (%)

27 10

Banking penetration (%)

36.970.0

Made or received digital payments in the past year (% age 15+ years of population)

Sources: 1. Finnovista

2. WearesocialDigitalin2018report

3. UrbanisationinLatinAmerica,BBVAResearch,July2017

4. GrossDomesticProduct(GDP),GDPpercapita,populationandinflation:OxfordEconomics

5. FDIinflowandMobileSubscriptions:WorldBankOpenData

6. Internetusersandinternetbandwidth:TheGlobalCompetitivenessReport2017–2018,WorldEconomicForum

7. FinancialParameters:TheGlobalFindexDatabase,WorldBank

Brazil• InApril2018,theCentralBank

ofBrazilissuedaregulationthatgrantsautonomytoelectroniclendingplatformstocarryoutloantransactionsdirectlybetweenborrowersandlendersbyintroducingtwonewcategoriesoffinancialinstitutions—P2Pcompaniesanddirectcreditcompanies.

• BanksinBrazilhavebeenconnectingwithFinTechsthroughfundingandincubation.

• TheSecuritiesandExchangeCommissionofBrazilrunsitsFinTechHub,whichaimstoanalyzethedevelopmentandapplicationofFinTechincapitalmarkets.

Mexico• MexicoFinancialTechnology

InstitutionsLawbecameeffectiveinMarch2018.Itprovidesregulatorycertaintyonissuesincludingcrowdfunding,paymentmethodsandcryptocurrencies.Mexicobecameoneofthefewcountriesgloballytoregulatethesector.

• Aregulatorysandboxwasintroducedtoallowcompaniestoobtainatemporaryauthorizationforamaximumoftwoyears.

58 32Brazil Mexico

FinTechecosystemplaybook

FinTech ecosystem playbook

29

FinTechlandscapeinLatinAmerica—2017-18

Source:FinTechecosysteminLatinAmerica,Finnovista

Mexico

Brazil

Colombia

Argentina

Chile

Peru

Ecuador

Uruguay

Other

26%

17%

16%

8%

9%

6%

5%

13%

Lending

Payments & remittances

Enterprise financial management

Crowdfunding

Personal financial management

Insurance

Wealth management

Others

35%

3%1%3%5%

7%

12%

23%

11%

Keyhighlights1

ASEANFinTechNetwork(AFN)waslaunchedinNovember2017toenablecollaborationandcooperationonFinTechecosystembetweensixparticipatingnations

Keyhighlights

Theregionhasahighermobilepenetrationrate,withcountrieshavingmobilepenetrationratesabovetheglobalaverageof112%.

Theregionhasanestimatedpopulationof406millionwithnearly74%internetpenetrationratein2017.

EconomiesinCentralandEasternEuropewitnessedabuoyanteconomicgrowthlastyear, driven by a rise inconsumerdemandandinvestment,whicheventuallyloweredtheunemploymentratesintheregion.

CESA

Czech Republic

Russia

Estonia

Lithuania

30

FinTechecosystemplaybook

FinTech ecosystem playbook

31

Keyhighlights1Keyhighlights

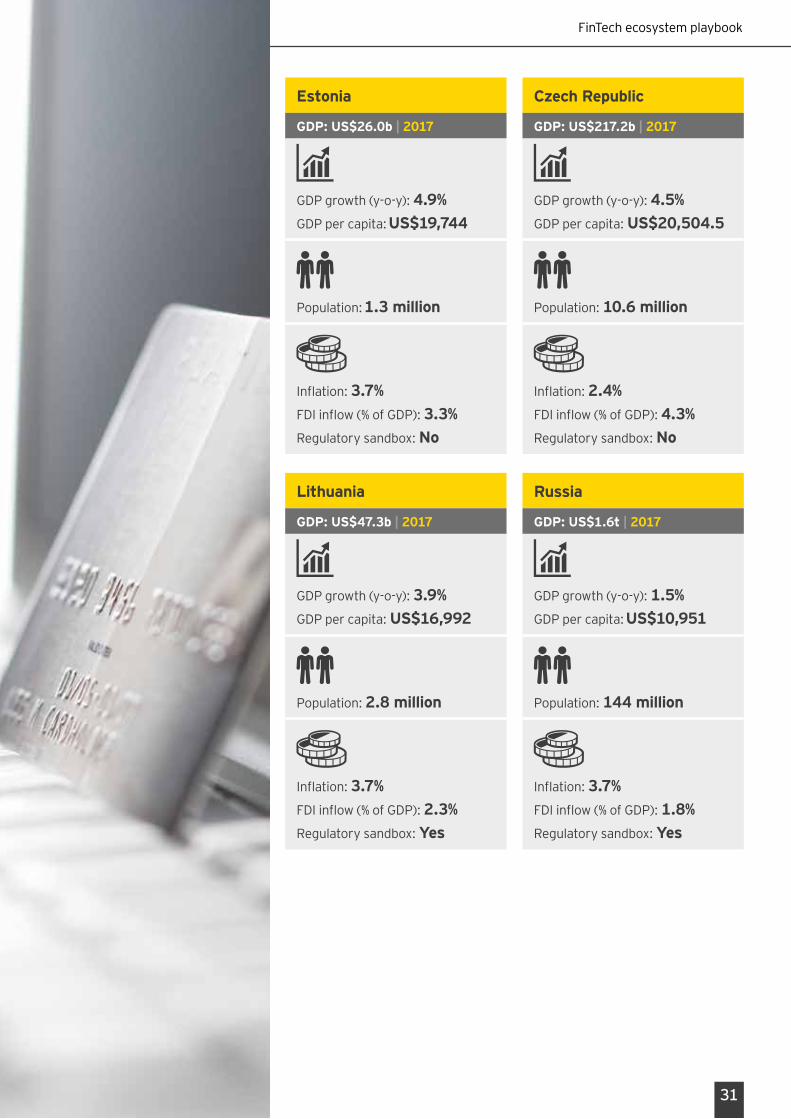

Estonia

GDP: US$26.0b | 2017

GDPgrowth(y-o-y):4.9%GDPpercapita: US$19,744

Population: 1.3 million

Inflation:3.7%FDIinflow(%ofGDP):3.3%Regulatorysandbox:No

Czech Republic

GDP: US$217.2b | 2017

GDPgrowth(y-o-y):4.5%GDPpercapita:US$20,504.5

Population:10.6 million

Inflation:2.4%FDIinflow(%ofGDP):4.3%Regulatorysandbox:No

Lithuania

GDP: US$47.3b | 2017

GDPgrowth(y-o-y):3.9%GDPpercapita:US$16,992

Population:2.8 million

Inflation:3.7%FDIinflow(%ofGDP):2.3%Regulatorysandbox:Yes

Russia

GDP: US$1.6t | 2017

GDPgrowth(y-o-y):1.5%GDPpercapita: US$10,951

Population:144 million

Inflation:3.7%FDIinflow(%ofGDP):1.8%Regulatorysandbox:Yes

FinTech ecosystem playbook

32

Digitalreadiness

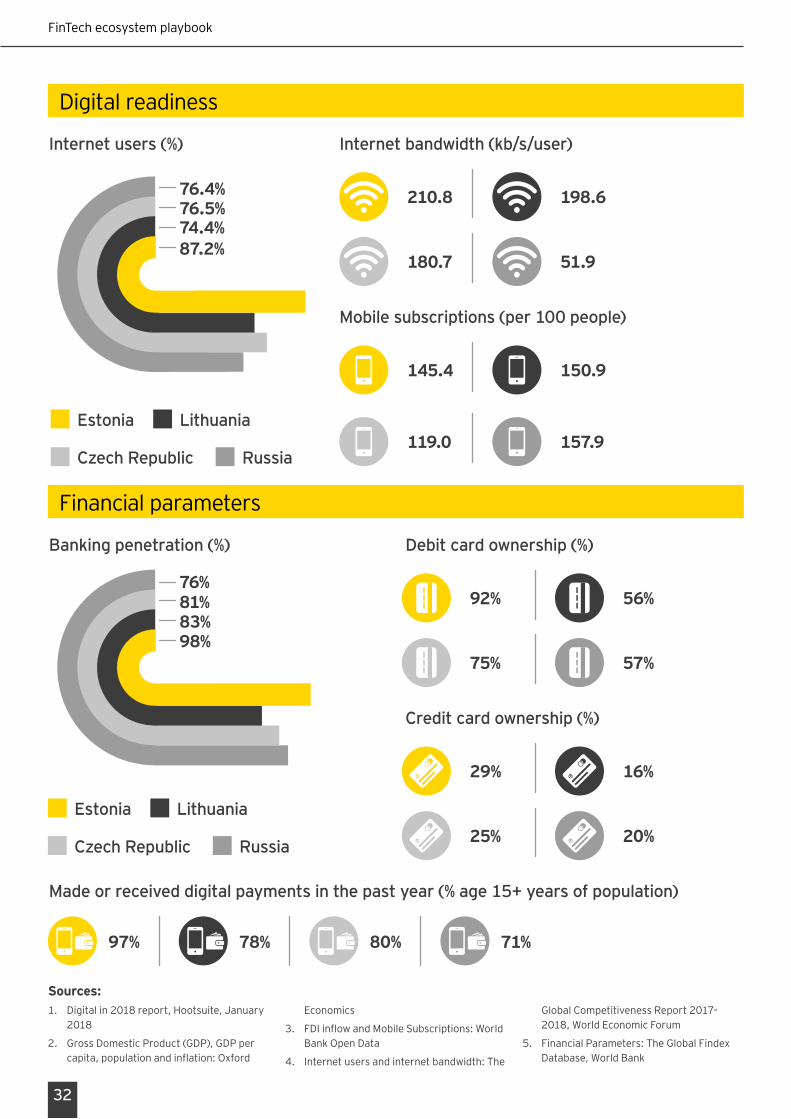

Internet users (%) Internet bandwidth (kb/s/user)

Mobile subscriptions (per 100 people)

180.7

210.8

51.9

198.6

145.4 150.9

119.0 157.9Estonia Lithuania

Czech Republic Russia

76.4%76.5%74.4%87.2%

Financialparameters

Banking penetration (%)

Made or received digital payments in the past year (% age 15+ years of population)

Debit card ownership (%)

92%

75% 57%

56%

Credit card ownership (%)

29% 16%

20%25%

76%81%83%98%

97% 78% 80% 71%

Estonia Lithuania

Czech Republic Russia

Sources: 1. Digitalin2018report,Hootsuite,January

2018

2. GrossDomesticProduct(GDP),GDPpercapita,populationandinflation:Oxford

Economics

3. FDIinflowandMobileSubscriptions:WorldBankOpenData

4. Internetusersandinternetbandwidth:The

GlobalCompetitivenessReport2017–2018,WorldEconomicForum

5. FinancialParameters:TheGlobalFindexDatabase,WorldBank

33

FinTechecosystemplaybook

Estonia• Estoniahasastrongreputation

forbeingadigitaleconomy.Thecountryboastsofmuch-laudede-residencyprogramthatincludesthee-identityprogramande-Estoniastateportal:

• Undertheprogram,theGovernmentissuesadigitalidentitythatallowsentrepreneurstosetupandrunalocationindependentbusiness.Businessescanquicklysetuptheirpresenceinthecountry(in15minutes).

• E-residentscanstartacompanyonline,accessbankingandonlinepaymentserviceproviders(PSPs),managecompanyremotely.

• Estonialaunchedthee-Residencyprogramin2015,anditse-residentshavesincegrowntoapproximately40,000peoplefrom150countriesasofJune2018.

• Estoniahasdevelopedoneofthemostliberaltaxsystemswitha0%corporateincometaxoncompanieswithoutdividends.

• In2015,theEstoniangovernmentestablished‘StartupEstonia’tostrengthentheEstonianstartupecosystem,carryouttrainingprogramsforstartups,educatelocalinvestorswhilstattract

foreigninvestors,andeliminateregulativeissuesandbarriers.

• ThecountryhasaStart-upVisaprogramthatenablesnon-EUresidentstoworkforEstonia’sstart-ups.

Lithuania• Lithuaniapositionsitselfasthe

entrypointforFinTechcompaniestotheEU.ThecountryhastakenmeasurestocreateaconduciveenvironmentforthedevelopmentofitsFinTechindustry.Afastdigitalpaymentore-moneylicense(inabout3to4months),easylicensingforP2PlendingplatformsandcrowdfundinglawsaresomeofthekeyinitiativesbytheGovernment.

• InJuly2018,theBankofLithuaniaintroducedaprocedurethatallowscompaniestoapplyremotelyandonlineforFinTechlicenses.

• Lithuaniaoffersaspecializedbankinglicensethatallowstoestablishabankwitharegisteredcapitalofonly€1m.

• InJanuary2018,theBankofLithuaniaannouncedthatitwillbelaunchingablockchainsandboxplatformfordomesticandforeigncompanies.Theplatform,calledLBChain,willallowFinTechstodevelopandtestoutblockchain-basedsolutions.

Success storiesSuccess stories

• ForFinTechs,specialsupportandadvicesystemsareprovidedfortheirfirstyearofoperations.Non-bankinginstitutionsaregivenaccesstoCENTROlink,thepaymentsystemoperatedbytheCentralBankofLithuania,andthuscanexecutepaymentsintheEU’sSingleEuroPaymentArea.

Czech Republic

• GovernmentagencyCzechICTAlliancesetupthePragueStartupCentrein2016tohelpearly-stagestart-upsconnectwithinvestorsandpartners.Servicesincludeanincubationprogramforuniversitystudentsandearly-stagestart-ups,officesinPraguedowntown,varioustrainingsandworkshopsforstart-ups,andnetworkingevents.

• InJanuary2017,CzechRepublicstartingJanuary1,2017,introducedthelawagainstmoneylaundering.ThelawpreparedbytheMinistryofFinanceoftheCzechRepublicrequiresvirtualcurrencyexchangestodeterminetheidentityofcustomers.

Russia• InApril2016,TheCentral

BankoftheRussianFederationcreatedadedicateddepartment—DepartmentOfFinancialTechnologies,ProjectsandProcessOrganization—tomonitor,analyzeandevaluatethescopeoftheemergingFinTechsector.

• Inearly2018,thecentralbankpublishedadocumentsettingguidelinesforthedevelopmentoffinancialtechnologiesfrom2018to2020.

• InApril2018,thecentralbankintroducedaregulatorysandboxtoserveasaplatformformodelingtheprocessesoftheuseandapplicationofinnovativefinancialservices.

• Thegovernment-fundedInternetInitiativesDevelopmentFund(IIDF)has$100M(6bnRUB)underitsmanagementasofAugust2018.

• From2013toAugust2018,IIDFhadclosed370dealswithvaluesrangingfrom$20kto$5.5M

34

FinTechecosystemplaybook

Keyhighlights

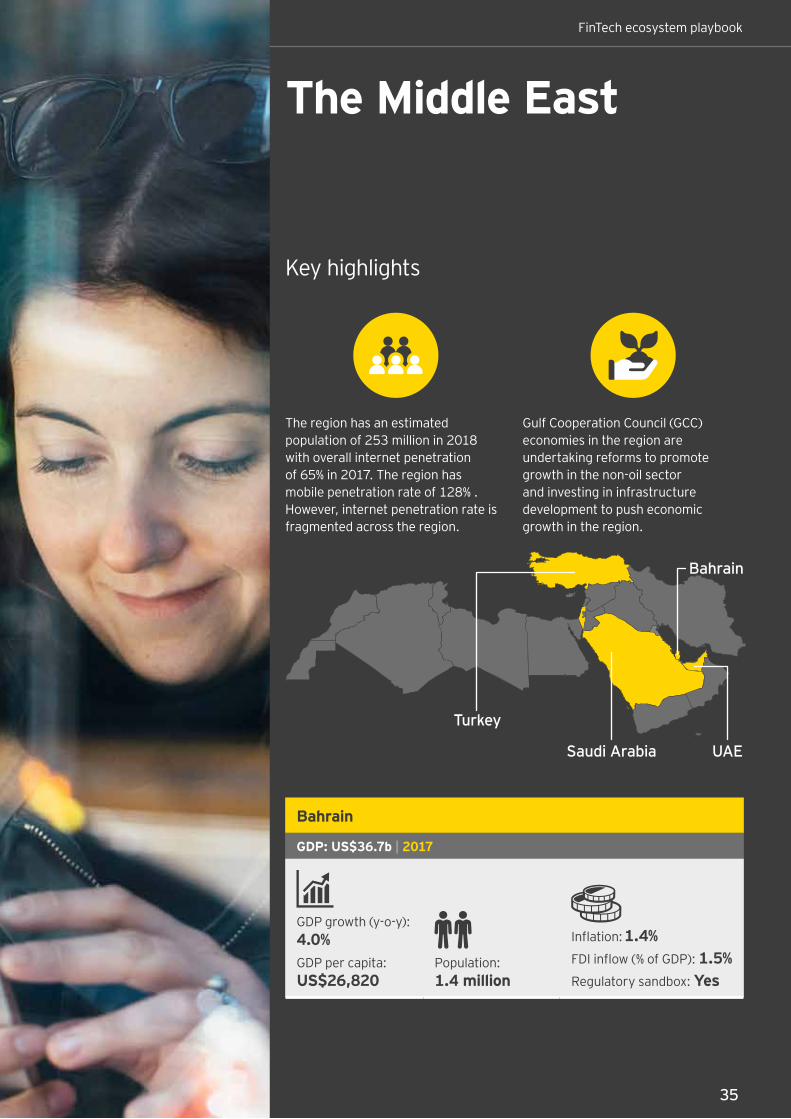

GulfCooperationCouncil(GCC)economiesintheregionareundertakingreformstopromotegrowthinthenon-oilsectorandinvestingininfrastructuredevelopmenttopusheconomicgrowthintheregion.

Theregionhasanestimatedpopulationof253millionin2018withoverallinternetpenetrationof65%in2017.Theregionhasmobilepenetrationrateof128%.However,internetpenetrationrateisfragmentedacrosstheregion.

The Middle East

Bahrain

GDP: US$36.7b | 2017

GDPgrowth(y-o-y):4.0%GDPpercapita:US$26,820

Population: 1.4 million

Inflation: 1.4%FDIinflow(%ofGDP):1.5%Regulatorysandbox:Yes

Bahrain

Saudi Arabia UAE

Turkey

35

FinTechecosystemplaybook

FinTech ecosystem playbook

36

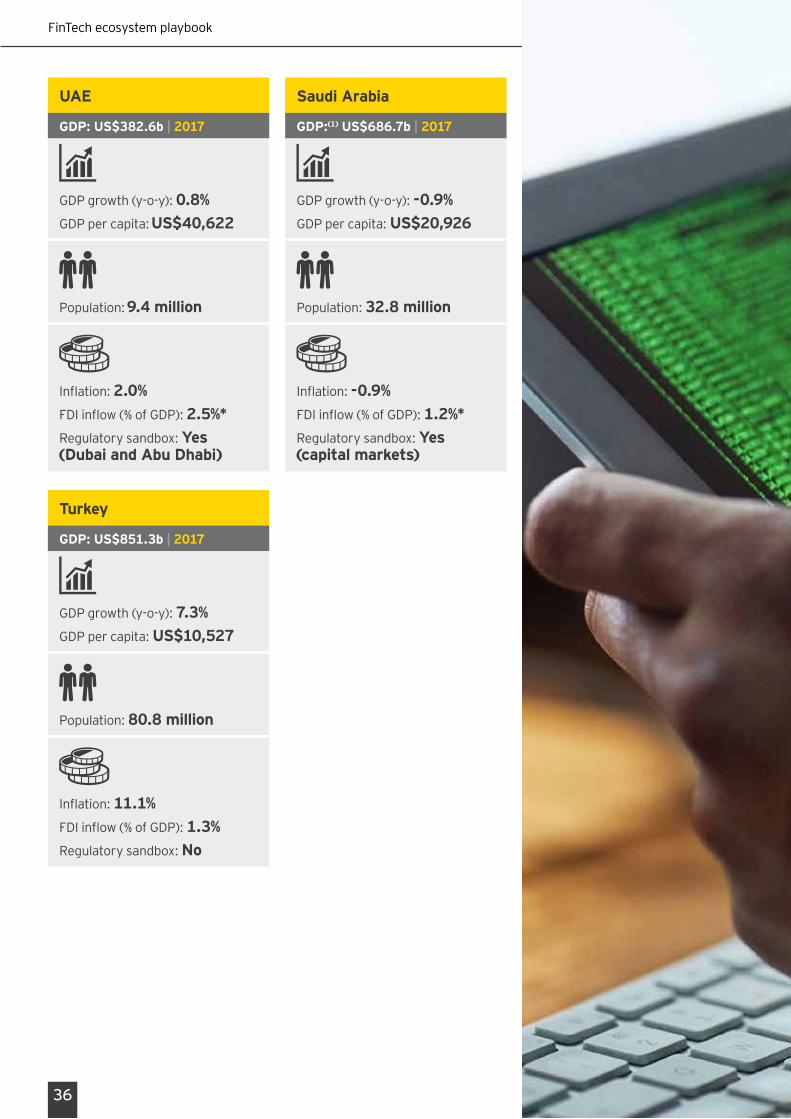

Turkey

GDP: US$851.3b | 2017

GDPgrowth(y-o-y):7.3%GDPpercapita:US$10,527

Population:80.8 million

Inflation:11.1%FDIinflow(%ofGDP):1.3%Regulatorysandbox:No

Saudi Arabia

GDP:(1) US$686.7b | 2017

GDPgrowth(y-o-y):-0.9%GDPpercapita:US$20,926

Population:32.8 million

Inflation:-0.9%FDIinflow(%ofGDP):1.2%*Regulatorysandbox:Yes (capital markets)

UAE

GDP: US$382.6b | 2017

GDPgrowth(y-o-y):0.8%GDPpercapita: US$40,622

Population: 9.4 million

Inflation:2.0%FDIinflow(%ofGDP):2.5%*Regulatorysandbox:Yes (Dubai and Abu Dhabi)

FinTech ecosystem playbook

37

Sources:

1. Digitalin2018report,Hootsuite,January2018

2. GrossDomesticProduct(GDP),GDPpercapita,populationandinflation:OxfordEconomics

3. FDIinflowandMobileSubscriptions:WorldBankOpenData

4. Internetusersandinternetbandwidth:TheGlobal

CompetitivenessReport2017–2018,WorldEconomicForum

5. FinancialParameters:TheGlobalFindexDatabase,WorldBank

Note: * 2017 FDI inflow figures not available. Considered 2016 figures instead.

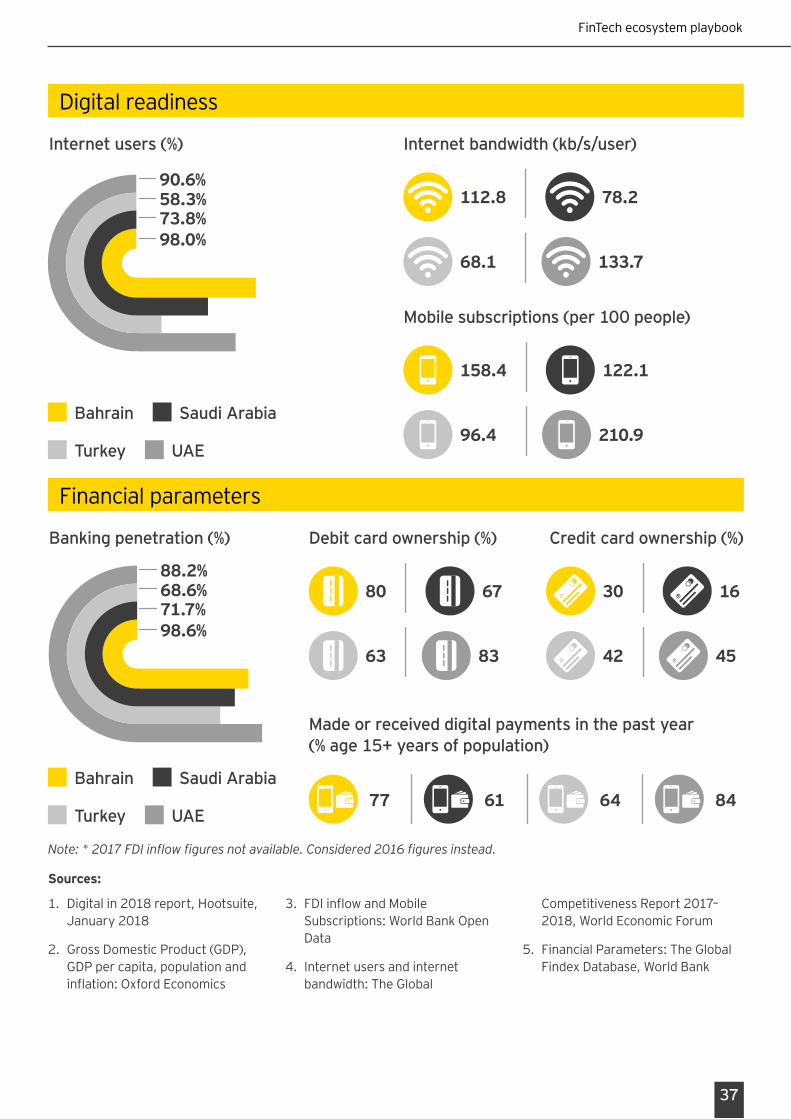

Financialparameters

Bahrain Saudi Arabia

Turkey UAE

Banking penetration (%) Debit card ownership (%)

80

63 83

67

Credit card ownership (%)

30 16

4542

Made or received digital payments in the past year (% age 15+ years of population)

77 61 64 84

88.2%68.6%71.7%98.6%

Digitalreadiness

Internet users (%)

Bahrain Saudi Arabia

Turkey UAE

90.6%58.3%73.8%98.0%

Mobile subscriptions (per 100 people)

158.4 122.1

210.996.4

Internet bandwidth (kb/s/user)

68.1 133.7

112.8 78.2

United Arab Emirates

Dubai• Establishedin2004,DIFCisa

majorfinancialhubintheMEASAregion.Ithasanindependentregulatorandjudicialsystem,andaglobalfinancialexchange.Thefinancialdistricthas2,003activeregisteredcompaniesoperatingwithacombinedworkforceof22,768.

• DIFCestablishedFinTechHive,anacceleratorthataimstobringfinancialandtechnologyfirmstogether.ItofferslicensingsolutionsforFinTechsandsupportiveregulationthroughitsInnovationTestingLicence.Italsooffersdedicatedcommerciallicense,specificallydevelopedforFinTech,RegTechandInsurTechfirmstooperatewithinthecenter.

• DIFClaunchedaUS$100mFinTech-focusedfundtoacceleratethedevelopmentinfinancialtechnologybyinvestinginstart-ups,fromincubationtogrowthstage.

• ItlaunchedTheAcademy,anexecutiveeducationcenter,in2017.Formedinpartnershipwithleadingbusinessschools,TheAcademyprovidesaccesstofinancialservicescourses.

• InAugust2017,theDubaiFinancialServicesAuthority(DFSA),launcheditsregulatory

frameworkforloan-andinvestment-basedcrowdfundingplatforms.

AbuDhabi• ADGMwasfoundedin2013.

Itcomprisesthreeindependentauthorities:ADGMCourts,theFinancialServicesRegulatoryAuthorityandtheRegistrationAuthority.

• ADGMhasintroducedseveralinitiativesandprogramstosupportthecountry’sFinTechecosystem.IthasaregulatorysandboxprogramandispartofGFIN.

• InOctober2017,ADGMlaunchedtheFinTechInnovationCentre,aco-workingspaceforFinTechs,andenteredintopartnershipwithPlugandPlay,aglobalacceleratorprogramtosupportfinancialinnovation.

• InSeptember2018,ADGMlaunchedaregulatoryframeworkforprivatefinancingplatformsthatenableenterprisestoseekfinancingfromprivateandinstitutionalinvestorstolaunchandgrowtheirbusinesses.

• FinTech-specificcourseswerelaunchedbyADGMAcademyinMay2018.Theacademyispartneringwitheducationalinstitutionsforarangeofprogramsonbankingandfinance,personalandprofessionaldevelopment,entrepreneurship,andnationaldevelopment.

Success storiesSuccess stories

38

FinTechecosystemplaybook

FinTech ecosystem playbook

39

Bahrain• BahrainFinTechBaywaslaunched

inNovember2017withthecollaborationofBahrainEconomicDevelopmentBoard(EDB)andFTC.

• InBahrain,FinTechdevelopmentisinspiringIslamicfinanceinstitutionstoadoptdigital.InDecember2017,AlBarakaBankingGroup,KuwaitFinanceHouseandBahrainDevelopmentBank(BDB)launchedthefirstglobalIslamicFinTechconsortium,ALGOBahrain.Theconsortium,whichaimstoincreasetheadoptioninFinTechinIslamicbanking,planstolaunch15bankingplatformsby2022.

• TheCentralBankofBahrainhasadedicatedFinTech&InnovationUnitthataimstocreateasupportiveregulatoryenvironmenttoencourageinvestmentinFinTech.DevelopmentsincludeadedicatedlicensecategoryforconventionalandShari’a-compliantcrowdfundingandaregulatorysandbox.

• InJune2018,BDB’sAlWahaFundofFundscloseditsUS$100mfundraisinground.Thefundwillsupportstart-upsinBahrainandacrossMENAregion.

Saudi Arabia• AspartofSaudiVision2030,the

SaudiArabiaGovernmenthaslaunchedtheFinancialSectorDevelopmentprogram.Undertheprogram,theSaudiArabianMonetaryAuthority(SAMA)shall

establishacentralpaymentunittoregulatethepaymentsindustry.Italsoplanstodevelopfinancialservicespaymentlawsandregulationstogetherwithcreatingnewlicensesforinnovativenonbankingplayers.Additionally,SAMAhaslaidoutframeworkforcybersecuritycompliance.InMay2018,SAMAlaunchedtheFintechSaudiinitiativetosupporttheFinTechdevelopment.

• CapitalMarketAuthority(CMA)laidouttheregulatoryframeworkfortheinnovationofFinTechincapitalmarketwithinSaudiArabia.FinTechsalsorequireapermitthatwouldenablethemtofirsttesttheirofferingsintheFinTechLab.InJuly2018,CMAapprovedthefirsttwolicensesforFinTechs.

Turkey• InJuly2018,theTurkish

GovernmentsetupFinTechTaskForcewiththeaimtoimprovetheFinTechecosysteminthecountryConsistingofexecutivesfromtheCentralBankoftheRepublicofTurkey,theBankingRegulationandSupervisionAgency,theUndersecretariatofTreasury,theCapitalMarketsBoardTurkey,andtheSavingsDepositInsuranceFund,thetaskforceissettinganationalvisionandgoal,determiningastrategyandaroadmapfortheindustry.

• InDecember2017,TurkeyamendeditsCapitalMarketsActtomakecrowdfundingthatoffersareturnoninvestment(e.g.,throughshares)availableinthecountry.

• TheInterbankCardCenter,BKM,hasalsobeenplayinganactiveroleinsupportingFinTechinTurkey.In2016,BKMintroducedTurkey’sPaymentMethod(Troy),anelectroniccardpayment

system,inlinewithitsvisionofcreatingacashlesssocietyby2023.

Keyhighlights

AccordingtotheWorldBank,insub-SaharanAfrica,21%oftheadultpopulationhaveamobilemoneyaccount,whichisthehighestinanyregionintheworld.WhilemobilemoneyhasbeencenteredinEastAfrica,ithasexpandedtoWestAfricaandbeyond.

Theregionhasanestimatedpopulationofaboutabillionin2018with34%internetpenetrationrateand82%mobilepenetrationrate.

GlobalFinTechhubplaybook2018

South Africa

KenyaNigeria

Africa

40

FinTechecosystemplaybook

FinTech ecosystem playbook

41

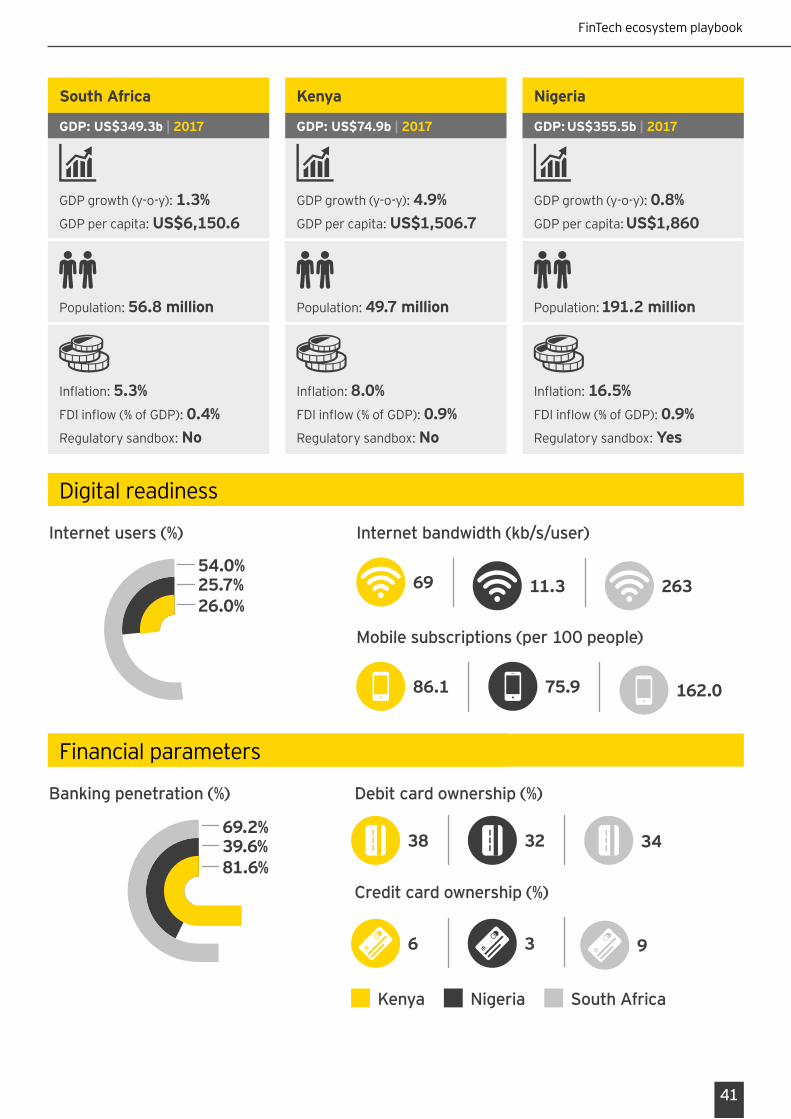

Keyhighlights

South Africa

GDP: US$349.3b | 2017

GDPgrowth(y-o-y):1.3%GDPpercapita:US$6,150.6

Population:56.8 million

Inflation:5.3%FDIinflow(%ofGDP):0.4%Regulatorysandbox:No

Kenya

GDP: US$74.9b | 2017

GDPgrowth(y-o-y):4.9%GDPpercapita:US$1,506.7

Population:49.7 million

Inflation:8.0%FDIinflow(%ofGDP):0.9%Regulatorysandbox:No

Nigeria

GDP: US$355.5b | 2017

GDPgrowth(y-o-y):0.8%GDPpercapita: US$1,860

Population: 191.2 million

Inflation:16.5%FDIinflow(%ofGDP):0.9%Regulatorysandbox:Yes

Digitalreadiness

Internet users (%)

Mobile subscriptions (per 100 people)

86.1 75.9 162.0

Internet bandwidth (kb/s/user)

69 11.3 26354.0%25.7%26.0%

Kenya Nigeria South Africa

Financialparame

Debit card ownership (%)

38 3432

Credit card ownership (%)

6 3 9

Banking penetration (%)

69.2%39.6%81.6%

Financialparameters

Sources:

1. Digitalin2018report,Hootsuite,January2018

2. GrossDomesticProduct(GDP),GDPpercapita,populationandinflation:OxfordEconomics

3. FDIinflowandMobileSubscriptions:WorldBankOpenData

4. Internetusersandinternetbandwidth:TheGlobalCompetitivenessReport2017–2018,WorldEconomicForum

5. FinancialParameters:TheGlobalFindexDatabase,WorldBank

Made or received digital payments in the past year (% age 15+ years of population)

79 30 60

Kenya Nigeria South Africa

Nigeria• ThePaymentsSystemVision2020

oftheCentralBankofNigeria(CBN)identifieswaystoincreasetheresilienceofthepaymentssysteminfrastructure.Thesectorisusinginnovations,suchasUnstructuredSupplementaryServiceDataservice(USSD),forpayments.

• InMarch2018,CBN,alongwithNigeriaInter-BankSettlementSystem,introducedaregulatorysandboxwiththeaimtofacilitatedigitalinnovationbyFinTechcompanies.

Kenya• M-Pesaisakeydriverbehind

successofmobilebankinginKenya,whichhashelpedalleviatefinancialexclusion.AccordingtotheGlobalFindexDatabase2017,73%ofadultsinKenyahaveamobilemoneyaccount.

• TheCentralBankofKenya(CBK)isthefinancialregulatorybodyinthecountryandisreceptiveoftheFinTechinnovations,whichisevidentfromthemeasuresithastaken.In2007,theCBKtookthepivotalstepofallowingmobileoperator,Safaricom,tolaunchM-Pesawhentherewasnoregulatoryframeworksetup.

South Africa• InFebruary2018,SARB

establishedaFinTechprogramthataimstostrategicallyassesstheemergenceofFinTechandconsideritsregulatoryimplications.Ithasthreeprimaryobjectives:evaluatingprivatecryptocurrencies,investigatinginnovationfacilitators(sandboxes,incubatorsandaccelerators)andlaunchingaDLTexperiment(ProjectKhoka).

• InJune2018,SARBreleasedareportontheProjectKhoka,aPoCdesignedtosimulateareal-worldtrialofaDLT-basedwholesalepaymentsystem.

Success storiesSuccess stories

42

FinTechecosystemplaybook

FinTech ecosystem playbook

43

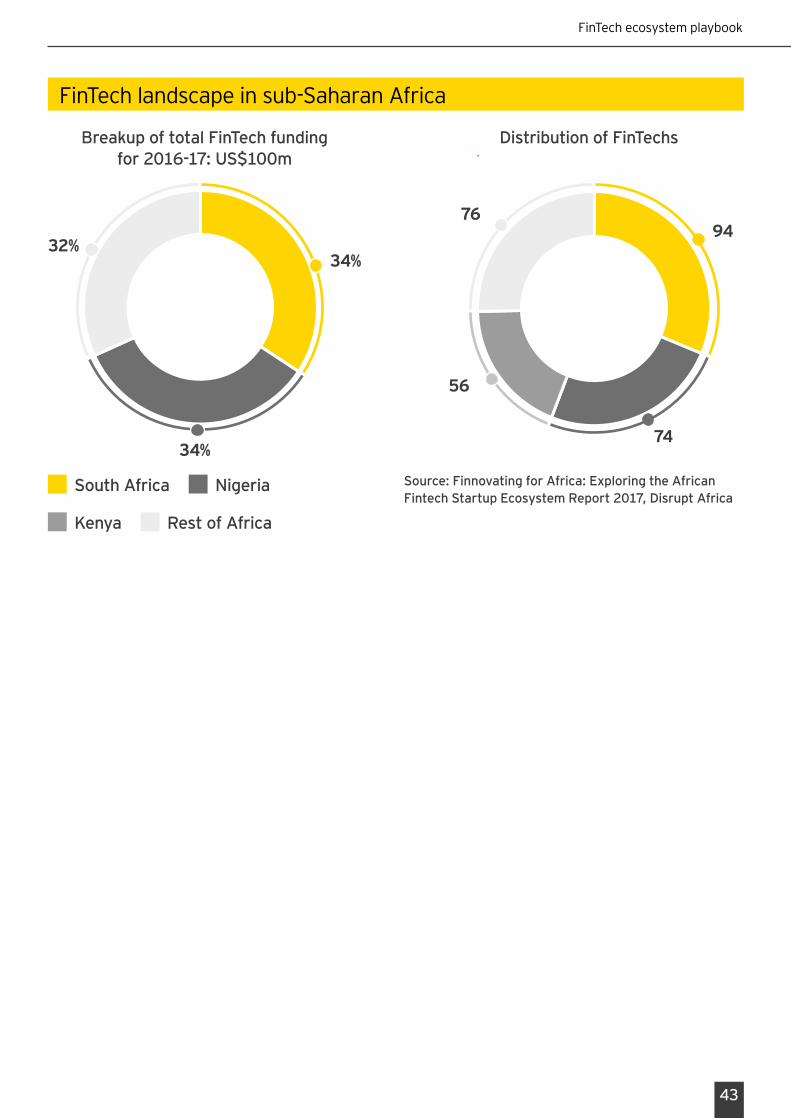

FinTechlandscapeinsub-SaharanAfrica

Breakup of total FinTech funding for 2016-17: US$100m

Distribution of FinTechs

34%

34%

32%94

74

56

76

Source: Finnovating for Africa: Exploring the African Fintech Startup Ecosystem Report 2017, Disrupt Africa

South Africa Nigeria

Kenya Rest of Africa

South Korea

GDP: US$1.5t | 2017

GDPgrowth(y-o-y):3.1%GDPpercapita:US$30,008

Population: 51.0 million

Inflation: 1.9%FDIinflow(%ofGDP):1.1%Regulatorysandbox:Yes

Mostofthehubsareencouragingdigitalpaymentinitiativesandworkingtowardfinancialinclusion.

Theregionhasanestimatedpopulationofabout3.6billionin2018.Asia-Pacifichasabout2billioninternetusers,whichisabout51%ofthetotalworldinternetusers.Theregionhasa48%internetpenetrationrate,and102%mobilepenetrationrate.

Keyhighlights

Asia-Pacific

44

Hong Kong

India

Japan

South KoreaChina

FinTechecosystemplaybook

FinTech ecosystem playbook

45

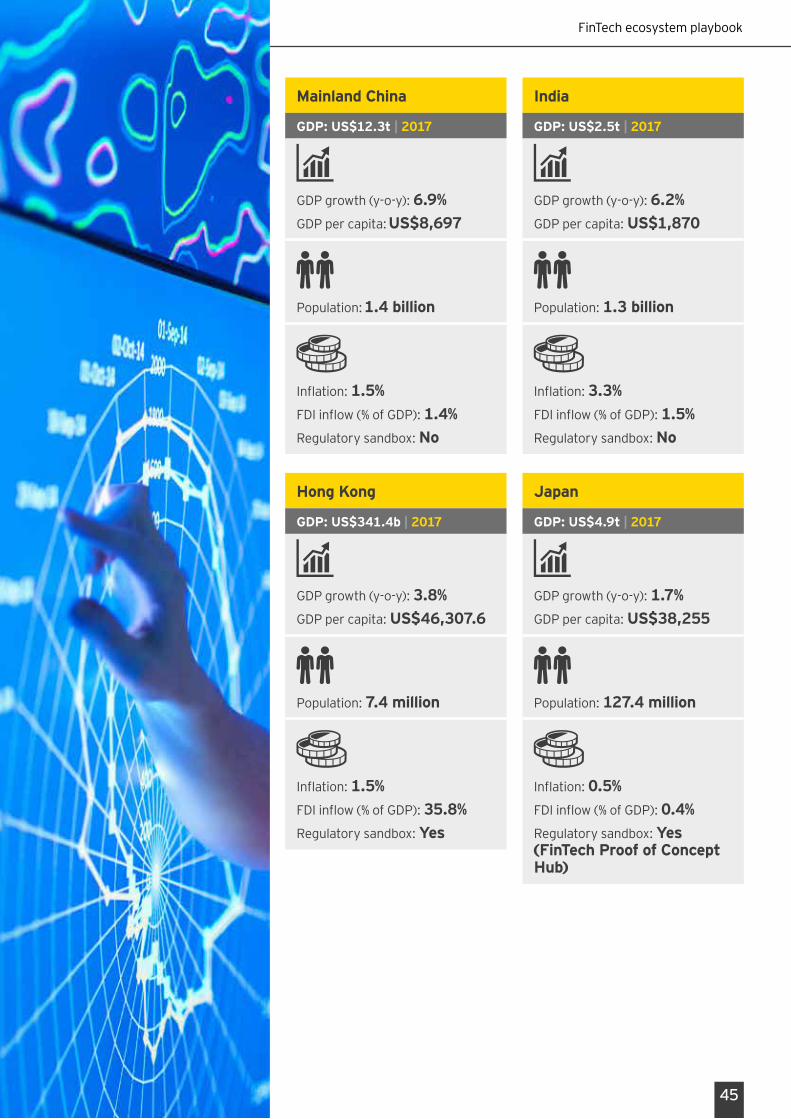

Hong Kong

GDP: US$341.4b | 2017

GDPgrowth(y-o-y):3.8%GDPpercapita:US$46,307.6

Population:7.4 million

Inflation:1.5%FDIinflow(%ofGDP):35.8%Regulatorysandbox:Yes

Japan

GDP: US$4.9t | 2017

GDPgrowth(y-o-y):1.7%GDPpercapita:US$38,255

Population:127.4 million

Inflation:0.5%FDIinflow(%ofGDP):0.4%Regulatorysandbox:Yes (FinTech Proof of Concept Hub)

India

GDP: US$2.5t | 2017

GDPgrowth(y-o-y):6.2%GDPpercapita:US$1,870

Population:1.3 billion

Inflation:3.3%FDIinflow(%ofGDP):1.5%Regulatorysandbox:No

Mainland China

GDP: US$12.3t | 2017

GDPgrowth(y-o-y):6.9%GDPpercapita: US$8,697

Population: 1.4 billion

Inflation:1.5%FDIinflow(%ofGDP):1.4%Regulatorysandbox:No

FinTech ecosystem playbook

46

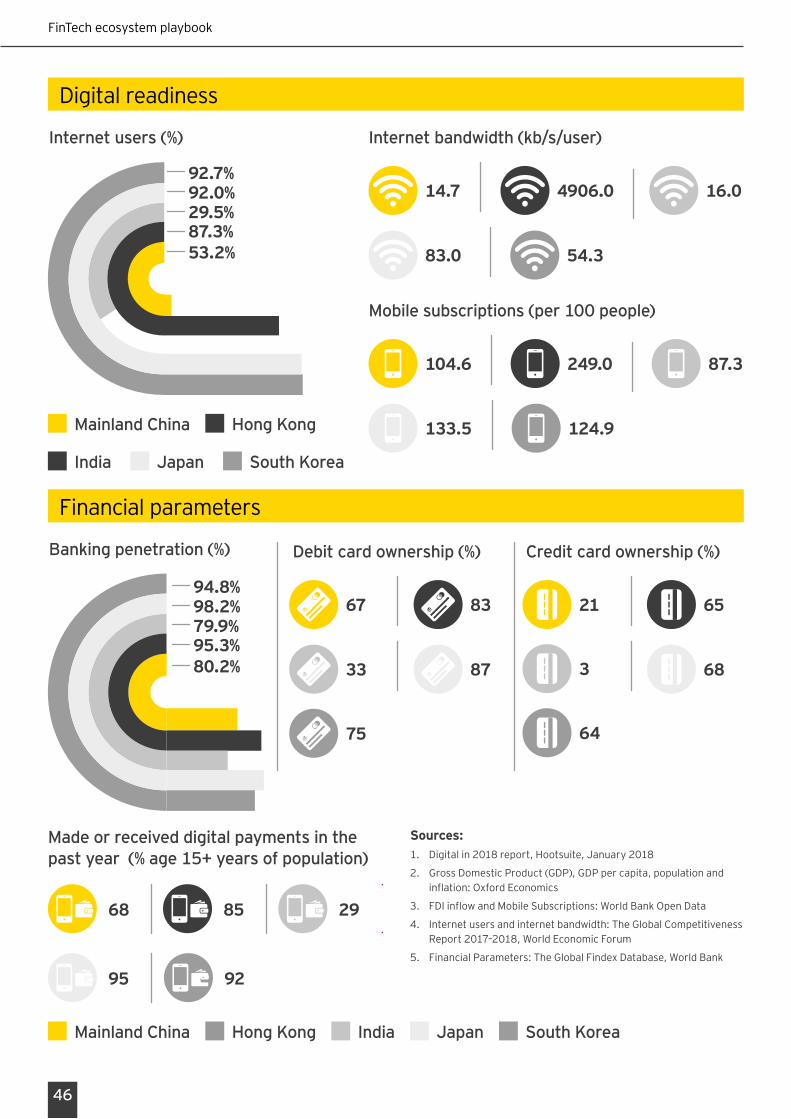

Digitalreadiness

Internet users (%) Internet bandwidth (kb/s/user)

Mobile subscriptions (per 100 people)

83.0 54.3

14.7 4906.0 16.0

104.6 249.0 87.3

124.9133.5

India Japan South Korea

Mainland China Hong Kong

92.7%92.0%29.5%87.3%53.2%

Financialparameters

Banking penetration (%) Credit card ownership (%)

21

3 68

64

65

Debit card ownership (%)

67 83

75

8733

Sources: 1. Digitalin2018report,Hootsuite,January2018

2. GrossDomesticProduct(GDP),GDPpercapita,populationandinflation:OxfordEconomics

3. FDIinflowandMobileSubscriptions:WorldBankOpenData

4. Internetusersandinternetbandwidth:TheGlobalCompetitivenessReport2017–2018,WorldEconomicForum

5. FinancialParameters:TheGlobalFindexDatabase,WorldBank

Made or received digital payments in the past year (% age 15+ years of population)

95 92

68 85 29

94.8%98.2%79.9%95.3%80.2%

Hong Kong India Japan South KoreaMainland China

FinTech ecosystem playbook

47

Hong Kong• HongKonghastakenanumberof

stepstostrengthenFinTechsector.InMarch2016,HKMAestablishedtheFinTechFacilitationOffice(FFO)tosupportthedevelopmentoftheecosystem.

• TheHKMAhaslaunchedsevensmartbankinginitiatives,whichincludethefollowing:

• FasterPaymentSystem(FPS):LaunchedinSeptember2018,thenewsystemoperatesonaround-the-clockbasis,andconnectsbanksandstored-valuefacility(SVF)operatorsonthesameplatform.

• OpenAPI:InJuly2018,OpenAPIFrameworkfortheHongKong’sbankingsectorwasreleased.

• EnhancedFintechSupervisorySandbox(FSS)2.0:AsoftheendofJuly2018,33newtechnologyproductshavebeentestedintheFSS.Separately,bankshavecollaboratedwithtechfirmsin18trialcases.

• Virtualbanking:InSeptember2017,theHKMAannounceditsintentiontoencouragevirtualbankinginHongKong.

• Closercross-bordercollaboration:ThelatestinitiativesincludethedevelopmentofaDLTplatformtodigitalizebanks’tradefinanceprocessesinHongKongwithpotentialconnectivitywithSingapore’stradeplatform.

• Researchandtalentdevelopment:HKMAhascollaboratedwiththeHongKongAppliedScienceandTechnologyResearchInstitute,ScienceParkandCyberportinanumberofresearchandeducationinitiatives.

• BankingMadeEasyInitiative—Aimistominimizeregulatoryfrictionsincustomers’digitalexperience,includingremoteonboarding,onlinefinanceandonlinewealthmanagement

• TheHongKonggovernment’s2018budgethaspledgedHK$500mtothedevelopmentoffinancialservicesoverthenextfiveyears,includingFinTech.

• In2017,theGovernmentlaunchedUS$256m(HK$2b)InnovationandTechnologyVentureFundtocoinvestwithprivateVCinlocaltech-basedstart-ups.

• WithspecificfocustoexpandFinTech-basedtalentinHongKong,HKMApartneredwithASTRItolaunchFCAS,providinginternshiptoundergraduatesandpostgraduatestudentsintheFinTechindustry.HKMAalsorunsatalentacceleratorprogram.

Success storiesSuccess stories

FinTech ecosystem playbook

48

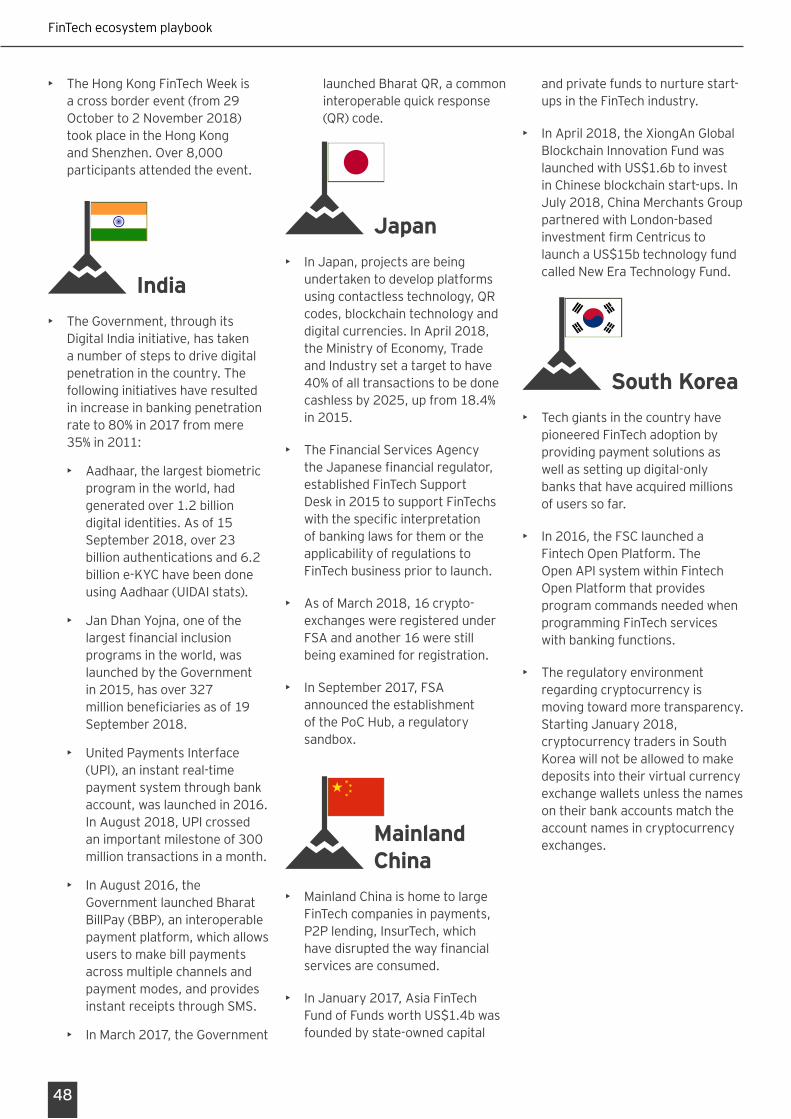

• TheHongKongFinTechWeekisacrossborderevent(from29Octoberto2November2018)tookplaceintheHongKongandShenzhen.Over8,000participantsattendedtheevent.

India• TheGovernment,throughits

DigitalIndiainitiative,hastakenanumberofstepstodrivedigitalpenetrationinthecountry.Thefollowinginitiativeshaveresultedinincreaseinbankingpenetrationrateto80%in2017frommere35%in2011:

• Aadhaar,thelargestbiometricprogramintheworld,hadgeneratedover1.2billiondigitalidentities.Asof15September2018,over23billionauthenticationsand6.2billione-KYChavebeendoneusingAadhaar(UIDAIstats).

• JanDhanYojna,oneofthelargestfinancialinclusionprogramsintheworld,waslaunchedbytheGovernmentin2015,hasover327millionbeneficiariesasof19September2018.

• UnitedPaymentsInterface(UPI),aninstantreal-timepaymentsystemthroughbankaccount,waslaunchedin2016.InAugust2018,UPIcrossedanimportantmilestoneof300milliontransactionsinamonth.

• InAugust2016,theGovernmentlaunchedBharatBillPay(BBP),aninteroperablepaymentplatform,whichallowsuserstomakebillpaymentsacrossmultiplechannelsandpaymentmodes,andprovidesinstantreceiptsthroughSMS.

• InMarch2017,theGovernment

launchedBharatQR,acommoninteroperablequickresponse(QR)code.

Japan• InJapan,projectsarebeing

undertakentodevelopplatformsusingcontactlesstechnology,QRcodes,blockchaintechnologyanddigitalcurrencies.InApril2018,theMinistryofEconomy,TradeandIndustrysetatargettohave40%ofalltransactionstobedonecashlessby2025,upfrom18.4%in2015.

• TheFinancialServicesAgencytheJapanesefinancialregulator,establishedFinTechSupportDeskin2015tosupportFinTechswiththespecificinterpretationofbankinglawsforthemortheapplicabilityofregulationstoFinTechbusinesspriortolaunch.

• AsofMarch2018,16crypto-exchangeswereregisteredunderFSAandanother16werestillbeingexaminedforregistration.

• InSeptember2017,FSAannouncedtheestablishmentofthePoCHub,aregulatorysandbox.

Mainland China

• MainlandChinaishometolargeFinTechcompaniesinpayments,P2Plending,InsurTech,whichhavedisruptedthewayfinancialservicesareconsumed.

• InJanuary2017,AsiaFinTechFundofFundsworthUS$1.4bwasfoundedbystate-ownedcapital

andprivatefundstonurturestart-upsintheFinTechindustry.

• InApril2018,theXiongAnGlobalBlockchainInnovationFundwaslaunchedwithUS$1.6btoinvestinChineseblockchainstart-ups.InJuly2018,ChinaMerchantsGrouppartneredwithLondon-basedinvestmentfirmCentricustolaunchaUS$15btechnologyfundcalledNewEraTechnologyFund.

South Korea• Techgiantsinthecountryhave

pioneeredFinTechadoptionbyprovidingpaymentsolutionsaswellassettingupdigital-onlybanksthathaveacquiredmillionsofuserssofar.

• In2016,theFSClaunchedaFintechOpenPlatform.TheOpenAPIsystemwithinFintechOpenPlatformthatprovidesprogramcommandsneededwhenprogrammingFinTechserviceswithbankingfunctions.

• Theregulatoryenvironmentregardingcryptocurrencyismovingtowardmoretransparency.StartingJanuary2018,cryptocurrencytradersinSouthKoreawillnotbeallowedtomakedepositsintotheirvirtualcurrencyexchangewalletsunlessthenamesontheirbankaccountsmatchtheaccountnamesincryptocurrencyexchanges.

49

FinTechecosystemplaybook

Appendix

ASEAN• Singapore

• “MASsetsupnewFinTech;InnovationGroup,”Monetary Authority of Singapore website, http://www.mas.gov.sg/news-and-publications/media-releases/2015/mas-sets-up-new-fintech-and-innovation-group.aspx,accessedon15October2018.

• “Singapore’sFinTechJourney—WhereWeAre,WhatIsNext”-SpeechbyMrRaviMenon,ManagingDirector,MonetaryAuthorityofSingapore,atSingaporeFinTechFestival-FinTechConferenceon16November2016,”Monetary Authority of Singapore website, accessedon15October2018.

• “SingaporeFintech:TopInfluencers,”finews.asia,23July2018.

• “FinTechFastTrack(FTFT),”Singapore FinTech Association website,https://singaporefintech.org/fintech-fast-track/,accessedon15October2018.

• “Home,”Singapore FinTech Association website,https://singaporefintech.org/,accessedon15October2018.

• Malaysia

• “ListofRegisteredMarketOperators”,Securities Commission Malaysia website, https://www.sc.com.my/digital/list_rmo/,accessedon18September2018

• “EquityCrowdfunding”,Securities Commission Malaysia website,https://www.sc.com.my/digital/equity-crowdfunding/,accessedon18September2018

• “ImplementationGuidanceone-KYCbyMSBIndustry”,BankNegaraMalaysia,http://www.bnm.gov.my,accessedon18September2018

• Indonesia

• “OJKSETSUPFINTECHADVISORYFORUM”,OJK website,https://www.ojk.go.id/en/berita-dan-kegiatan/siaran-pers/Documents/Pages/Press-Release-OJK-Sets-Up-Fintech-Advisory-Forum,accessedon18September2018

• Thailand

• “SECreleasescryptodetails”,Bangkok Post website,https://www.bangkokpost.com/business/news/1481525/sec-releases-crypto-details,accessedon18September2018

• “ThestateofICOregulationinThailand”,Bangkok Post website,https://www.bangkokpost.com/business/news/1510938/the-state-of-ico-regulation-in-Thailand,accessedon18September2018

• Vietnam

• “Non-cashpaymentperformancegainedsignificantimprovement,”State Bank of Vietnam website,https://www.sbv.gov.vn/webcenter/portal/

en/home/sbv/news,accessed5January2017.

• “SBVestablishesSteeringCommitteeonFintech”,State Bank of Vietnam website, https://www.sbv.gov.vn/webcenter/portal/en/home/sbv/news/news,accessedon18September2018

• First-everFintechChallengeVietnamlaunched,”VietnamEconomicTimes,http://vneconomictimes.com/article/business/first-ever-fintech-challenge-vietnam-launched,accessed5January2017.

• Philippines

• “BSPandIndustryLaunchestheNationalRetailPaymentSystem”,Bangko Sentral ng Pilipinas website,http://www.bsp.gov.ph/publications/media.asp?id=3948,accessedon18September2018

• “ThriveNotJustSurvive”,Bangko Sentral ng Pilipinas website,http://www.bsp.gov.ph/publications/speeches.asp?id=606,accessedon18September2018

• Cambodia

• “Fintechcouldbe‘gamechanger’,”ThePhnomPenhPost,28July2017

Latin America• Brazil

• “Brazil’sCentralBankauthorizespeer-to-peerlendingP2plending”,Reuters, https://www.reuters.com/

FinTech ecosystem playbook

50

article/brazil-credit-fintechs/brazils-central-bank-authorizes-peer-to-peer-lending-idUSL1N1S32Y6,accessedon18September2018

• CVMcreatesaFinTechHub,CVM,http://www.cvm.gov.br/noticias/arquivos/2016/20160613-1-1.html,accessedon18September2018

• Mexico

• “MexicoPassesNewFintechLawasSectorSurges,”Mexico Business Blog website,bdp-americas.com/blog/2018/04/18/mexico-passes-new-fintech-law-as-sector-surges/,accessedon27September2018.

CESA• Estonia:

• “e-residency,”e-Estonia website,https://e-estonia.com/solutions/e-identity/e-residency/,accessedon15October2018

• “e-identity,”e-Estonia website, https://e-estonia.com/category/e-identity/,accessedon15October2018

• “e-governance,”e-Estonia website,https://e-estonia.com/solutions/e-governance/state-e-services-portal/,accessedon15October2018

• “ESTONIA:“ITTAKES15MINUTESTOSETUPACOMPANYONTHEINTERNET”,”L’Atelier BNP Paribas website, https://atelier.bnpparibas/en/smart-city/article/estonia-it-takes-15-minutes-set-company-internet,accessedon15October2018

• “e-Estonia:Whatisallthefussabout?,”ZDNet website,

https://www.zdnet.com/article/e-estonia-what-is-all-the-fuss-about/,accessedon15October2018

• “About,”StartupEstoniawebsite,https://startupestonia.ee/about,accessedon27September2018

• Lithuania:

• “KeySectors—FinTech,”Go Vilnius website,http://www.govilnius.lt/business/key-business-sectors-vilnius/fintech/,accessedon15October2018

• “BankofLithuaniaintroducesremoteFintechlicensing”,Invest Lithuania website, https://investlithuania.com/news/lithuania-introduces-remote-fintech-licensing-making-the-prime-destination-for-fintech-even-better/,accessedon15October2018.

• “TheBankofLithuaniatolaunchblockchainsandboxplatform-service”Invest Lithuania website,https://investlithuania.com/news/the-bank-of-lithuania-to-launch-blockchain-sandbox-platform-service/,accessed27September2018.

• Czech Republic:

• “Home,”Prague Startup Centre website,http://en.praguestartupcentre.cz/,accessedon15October2018.

• “CZECHREPUBLIC:MajorNewImmigrationLawIncludesNewEUIntra-CompanyTransferCard,”Newland Chase website,https//newlandchase.com/immigration-insights/latest-news/czech-republic-major-new-immigration-law-includes-new-eu-intra-company-transfer-card/,accessedon15October2018.

• “CzechRepublicIntroducesLawRegulating(Restricting)Bitcoin,”CNN, 31 January 2017.

• Russia:

• “Russia’sc-banklaunchesregulatorysandbox”,Finance feeds website,https://financefeeds.com/russias-c-bank-launches-regulatory-sandbox/,accessedon20September2018

• “RussianCentralBankSetsGuidelinesforFintechDevelopment,AimsatCompetitionandAccessibility—IBS Intelligence,” IBS Intelligence website,accessedon27September2018.

• “Home,”IIDF website,https://www.iidf.ru/,accessedon27September2018

The Middle East• UAE

• Dubai:

• “Home”,Dubai International Financial Center website, https://www.difc.ae/,accessedon30August2018

• “Home,”FinTech Hive website,https://fintechhive.difc.ae/,accessedon15October2018.

• “DFSAlaunchesCrowdfundingFramework,”Dubai Financial Services Authority website,https://www.dfsa.ae/MediaRelease/News/DFSA-launches-Crowdfunding-Framework,accessedon27September2018.

• Abu Dhabi:

• “Home”,Abu Dhabi Global Market website,https://www.adgm.com/,accessed

51

on20September2018.

• “Home,”ADGM Academy website,https://www.adgmacademy.com/,accessedon27September2018

• “Home,”Emirates Digital Wallet website,http://www.edw.ae/,accessedon15October2018.

• Bahrain

• “Home”,Bahrain FinTech Bay website,https://www.bahrainfintechbay.com/,accessedon10September2018.

• “BahrainlaunchesanewResearchandDevelopmentFinTechfirm!,”Startup Bahrain website,http://startupbahrain.com/newsfeatures/bahrain-launches-new-research-development-fintech-firm/,accessedon15October2018.

• “WorldsFirstFintechConsortiumofIslamicBanksAnnouncedByBahrain,”Albaraka website,https://www.albaraka.com/default.asp?action=article&id=644,accessedon15October2018.

• “BDBcloses$100mVCfund,”Arab News,http://www.arabnews.com/node/1328086/corporate-news,26June2018.

• Saudi Arabia:

• “Home”,Capital Market Authority website,https://cma.org.sa/en/Pages/default.aspx,accessedon27September2018.

• “Home”,Saudi Arabian Monetary Authority website, http://www.sama.gov.sa/en-US/Pages/default.aspx,accessedon27September2018.

• “FinancialSectorDevelopmentProgram”,Saudi Vision 2030 website,http://vision2030.gov.sa/en/FSDP,accessed15October2018.

• Turkey:

• “Home”,FinTech Istanbul website,http://fintech.istanbul/en/,accessedon15October2018.

• “TurkeyLaunchesitsFirstFintechTaskForce,”The FinTech Times,23July2018.

• “EUROPE:TheNewAgeOfTurkey’sPayments,”PYMNTS website,https://www.pymnts.com/news/payment-methods/2015/the-new-age-of-turkeys-payments/,accessedon15October2018.

Africa• South Africa:

• “Mediastatement,”South African Reserve Bank (SARB), 13February2018

• “TheSouthAfricanReserveBankreleasestheProjectKhokhareport,”South African Reserve Bank (SARB),20June2018.

• Nigeria:

• “PaymentsSystemVision2020,”Central Bank of Nigeria, September2013.

• “FinancialInclusionNewsletter,”Central Bank of Nigeria,March2018.

• Kenya:

• “TheRiseofMobileMobileandMobileSavingsinKenya,”World Bank Group,2011.

• “Home,”Central Bank of Kenya website,https://www.centralbank.go.ke/,accessed

on15October2018.

• “News&Publications,”Capital Markets Authority website, accessedon15October2018.

Asia-Pacific• Hong Kong

• “ANewEraofSmartBanking”,HKMA website,https://www.hkma.gov.hk/eng/key-information/press-releases/2017/20170929-3.shtml,accessedon15September2018

• “Aboutus,”Hong Kong Monetary Authority website, https://ffo.hkma.gov.hk/about,accessedon15October2018

• “HongKongPushesFintechInnovation,”FinTechnews.hk, published7March2018

• “InnovationandTechnologyVentureFundopensforapplicationbyventurecapitalfunds,”GovHK website, https://www.info.gov.hk/gia/general/201709/15/P2017091400760.htm,accessedon15October2018

• “HKMAlaunchesFintechCareerAcceleratorScheme2.0withitsstrategicpartners,”Hong Kong Monetary Authority website, https://www.hkma.gov.hk/eng/key-information/press-releases/2018/20180131-8.shtml,accessedon15October2018

• “EventsPage,“FinTechHK website,http://www.hongkong-fintech.hk/en/events/,accessedon15September2018

• India

• “AadhaarDashboard”,Aadhaar website,https://uidai.gov.in/aadhaar_dashboard/,accessedon15September2018

FinTechecosystemplaybook

FinTech ecosystem playbook

52

• “JanDhanYojna”,Pradhan Mantri Jan Dhan Yojana website,https://www.pmjdy.gov.in/account,accessedon20September2018

• “Home,”United Payments Interface website,http://cashlessindia.gov.in/upi.html,accessedon15September2018

• “AboutUs,”Bharat BillPay website,https://www.bharatbillpay.com/aboutus.php,accessedon15October2018

• “BharatQRCode,”Ministry of electronics & Information Technology website,http://meity.gov.in/bharat-qr-code,accessedon15October2018

• Japan:

• “BanksRushtoTurnJapanCashlessbeforeLegalChangeAttractsTechGiants.”The Japan Times website, www.japantimes.co.jp/news/2018/04/05/business/banks-rush-turn-japan-cashless-legal-change-attracts-tech-giants/#.Wwz1zkiFOUk,accessedon27September2018.

• “IndustryministryreporturgesJapantoshedcustomofcashdependence”,The Japan Times website,https://www.japantimes.co.jp/news/2018/04/11/business/industry-ministry-report-urges-japan-shed-custom-cash-dependence/#.W6yn5mgzaM8,accessedon27September2018

• FinTechSupportDesk,Financial Services Agency,https://www.fsa.go.jp/news/27/sonota/20151214-2.html,accessedon27September2018

• “EstablishmentofFinTechProofofConceptHub”,Financial

Services Agency,https://www.fsa.go.jp/en/newsletter/weekly2017/262.html,accessedon27September2018

• Mainland China

• “Chinalaunchesmega$1.44bAsiaFinTechM&AFundofFunds”,Deal Street Asia Website,https://www.dealstreetasia.com/stories/china-launches-1-44-bn-asia-fintech-fund-of-funds-for-asian-fintech-mas-61848/,accessedon15September2018

• “HangzhouSetsUp$1.6BGovernment-backedBlockchainFundToInvestInStart-ups”,China Money Network,https://www.chinamoneynetwork.com/2018/04/10/hangzhou-sets-up-1-6b-government-backed-blockchain-fund-to-invest-in-start-ups,accessedon15September2018

• South Korea

• “Asia:Regulatingdigital-onlybanksinSouthKorea”,Rfi Group website,https://www.rfigroup.com/global-retail-banker/news/asia-regulating-digital-only-banks-south-korea,accessedon16October2018

• “KoreaFinancialAuthorityStrengthenTiesWithSingaporeasFintechsEyeGlobalExpansion,”Fintech News website,http://fintechnews.sg/3300/fintech/korea-financial-authority-strengthen-ties-singapore-fintechs-eye-global-expansion/,accessedin27September2018.

• “S.Koreaopensspecialfintechplatform,”Yonhap News Agency website,http://english.yonhapnews.co.kr/news/2016/08/30/0200000000AEN20160830006000320.html,accessedon27September

2018.

• “SouthKoreatoBanCryptocurrencyTradersfromUsingAnonymousBank...”Reuters website,ThomsonReuters,23Jan.2018,www.reuters.com/article/us-southkorea-bitcoin/south-korea-to-ban-cryptocurrency-traders-from-using-anonymous-bank-accounts-idUSKBN1FC069,accessedon27September2018.

53

Contacts

Jan BellensEYGlobalBanking&CapitalMarketsDeputySector[email protected]

Imran Gulamhuseinwala EYGlobalFinTech[email protected]

Charlie AlexanderEYGlobalTransactionAdvisoryServicesLeader—BankingCapitalMarkets[email protected]

Varun MittalEYGlobalEmergingMarketsFinTech[email protected]

Globalcontacts

Matt HatchEYAmericasFinTechandFinancialServicesGrowthMarkets[email protected]

Spyros Zachariadis EYCentral,Eastern,SouthernEurope[email protected]

Rana SanyouraEYMiddleEast&NorthAfricaFinTech[email protected]

Rachael LowProgramLeader,EYAsia-PacificFinancialServicesBrand,Marketing&[email protected]

James LloydEYAsia-PacificFinTech&Payments[email protected]

Rocio Velazco-RotemLatinAmericaFinTech[email protected]

Mahesh Makhija DigitalandEmergingTechnologyLeader,[email protected]

Ankita SrivastavaFinTechAnalyst,EY[email protected]

Regionalcontacts

FinTechecosystemplaybook

FinTech ecosystem playbook

54

Notes:

FinTech ecosystem playbook

55

Notes:

EY |Assurance|Tax|Transactions|Advisory

About EYEYisagloballeaderinassurance,tax,transactionandadvisoryservices. Theinsightsandqualityserviceswedeliverhelpbuildtrustandconfidenceinthecapitalmarketsandineconomiestheworldover.Wedevelopoutstandingleaderswhoteamtodeliveronourpromisestoallofourstakeholders.Insodoing,weplayacriticalroleinbuildingabetterworkingworldforourpeople,forourclients,andforourcommunities.

EYreferstotheglobalorganisation,andmayrefertooneormore,ofthememberfirmsofErnst&YoungGlobalLimited,eachofwhichisaseparatelegalentity.Ernst&YoungGlobalLimited,aUKcompanylimitedbyguarantee,doesnotprovideservicestoclients.Formoreinformationaboutourorganisation,pleasevisitey.com.

TheviewsofthirdpartiessetoutinthispublicationarenotnecessarilytheviewsoftheglobalEYorganisationoritsmemberfirms.Moreover,theyshouldbeseeninthecontextofthetimetheyweremade.

EY is a leader in serving the financial services industry

Weunderstandtheimportanceofaskinggreatquestions.It’showyouinnovate,transformandachieveabetterworkingworld.Onethatbenefitsourclients,ourpeopleandourcommunities.Financefuelsourlives.Noothersectorcantouchsomanypeopleorshapesomanyfutures.That’swhygloballyweemploy26,000peoplewhofocusonfinancialservicesandnothingelse.Ourconnectedfinancialservicesteamsarededicatedtoprovidingassurance,tax,transactionandadvisoryservicestothebankingandcapitalmarkets,insurance,andwealthandassetmanagementsectors.It’sourglobalconnectivityandlocalknowledgethatensureswedelivertheinsightsandqualityservicestohelpbuildtrustandconfidenceinthecapitalmarketsandineconomiestheworldover.Byconnectingpeoplewiththerightmixofknowledgeandinsight,weareabletoaskgreatquestions.Thebetterthequestion.Thebettertheanswer.Thebettertheworldworks.

©2018EYGMLimited.AllRightsReserved.

EYGno.04870-185Gbl

EDNone

InlinewithEY’scommitmenttominimiseitsimpactontheenvironment,thisdocument hasbeenprintedonpaperwithahighrecycledcontent.