finansdepartementet saksnr. dir. tlf.: 22 93 98 64 var … for stand-alone requirements purposes for...

TRANSCRIPT

rThe Fi ancial Supervisory Authority of Norway

FinansdepartementetFinansmarkedsavdelingenPostboks 8008 Dep0030 OSLO

o J. i=,tt= r:

Saksnr.

Arkivnr.

Saksbehandler: Bjørn AndersenDir. tlf.: 22 93 98 64

Var referanse: 05/5192Deres referanse:

Arkivkode: 501Dato: 05.05.2006

NYE KAPITALDEKNINGSREGLER - OVERSIKT OVER NASJONALE VALG

Det vises til brev av 28. april 2006 vedrørende forslag til forskrift om kapitalkrav mv.

Vedlagt følger en tabellarisk oversikt over hvordan nasjonale valg er foreslått gjennomført.Oversikten bygger på nasjonale valg som er identifisert av og innrapportert til CEBS. Arbeidet iCEBS vedrørende nasjonale valg er ikke avsluttet og det kan ikke utelukkes at nye nasjonalevalg identifiseres i denne prosessen. Kredittilsynet vil i så fall komme tilbake til saken.

Emil Steffensenseksjonssjef

Bjørn Andersenspesialrådgiver

KREDITTILSYNET side 1 av 1

Postadresse: Besøksadresse: Telefon: 22 93 98 00 [email protected] 100 Bryn Østensjøveien 43 Telefaks: 22 63 02 26 www.kredittilsynet.no06110510 0667 Oslo Org. nr.: 840747972

Nasjonale valg og andre valg ved gjennomføring av nye kapitaldekningsregler

Note: in yellow are provØns 'Subject to mutual recognifion' : means that the possibility of a Country sliming its banks to apply the Deaanent of another for their operetiors in the latter may apply

In each yellow row, please specify (i) whether you intend to apply the disrxeØ AND (ii) whether you intend to apply MR when it is provided for.

In green the amendments made when updating the list with the final version of the CRD

so Sal,

I OWN FUNDS Amide 57 (last pare.) 2000/12

OWN FUNDS Article 58 2000/12OWN FUNDS Arb* 59 2000112

OWN FUNDS Anda 60 2000112OWN FUNDS Article 61, 63 1, 64,3 & 2000112

65

OWN FUNDS Article 13.2 93/6

OWN FUNDS Ande 135 93/6

OWN FUNDS Article 14 93A

SCOPE OFAPPLICATION

Ande 69.1 2000112

I SCOPE OFAPPLICATION

Ande 69.2 2000112

11 SCOPE OFAPPLICATION

Ande 70 2000112

1 SCOPE OFAPPLICATION

Ande 72.3 2000112

1 SCOPE OFAPPLICATION

Arlide 73.1 2000/12

I SCOPE OFAPPLICATION

1 COUNTERPARTYRISK INDERIVATIVES ANDOTHEREXPOSURES

Indusion ot,Nedra profits M~ St~ may pem'it the indusion of citerim profits bekre a formal d,,,un hes been taken on the accounts, subject to conditions.

Waiver on certain deductions Shares in anolleresedit institution, firerroa) Institution, insurance or reinsurance undertaking may net be deducted ff held tempore/ly for the purposes of a finaroal assistance operation designed to reorganise and save the entity.

Alternatives to deductions As an attemative to deductions of participations and capital instruments held in otter financial institutions, credit institutions may be allowed to apply, with the necessary changes, any of the methodologies set out in the Annex I to the Conglomerates Directive.

Deductions for stand-alone requirements purposes For the purposes of te cekutation cf their stend alone requirements, institutions may be not required to deduct holdings ard participations in insfitutons inducted in the scope of their Øsolydatbn.

List of own funds The list of awn lunds elements in the Directive is a maximum, both in items and amts. Mertarer States may choose not to adnut certain elements or to apply lower oaitings. They can edd further deductions. Mertoer states may dense to aoxpt otrer elements of own fundsdifferent from these in ande 57, subject to Øditons Finally they can dadda on the possible indusion of cumulative preferential shares and subordinated can capital and on tre indusice of certain dements normally amounted for as assets, when they been a credit (negative'sign

Alternative form of calculation for investment finns not Investment fims that, in view of the services they provide, are allowed to calgdate their own funds as a percentage of the kurover of the previous year (art.21). may be also authorised to apply a definition of own funds other than tret prescribed by directive 2000/12providing certain services and applying Ande 21

Flexibility in thecomposibon of own funds for investment If an insttufion is calculating its own funds in accordance with thealternafive offered in Article 132 of 9316, it can be allowad ksubstitute subordnatedloans byotrerelementsdeeodbed in Ar/ide 57of20001i2, mainly as Tier 2,firms making use of the option in Ande 13 2

Excess of subordinated capitV The Competent Authorities may allow investment firms to hold subordinated capital in exoass of ordinary thresholds, up to certain limits.

Individual waiver for subsidiaries Member states may grant individual Insttutbns which are subsidiaries within a group, subject to the fulfilment of certain conditions, an exemption from individual requirements. The same applies where to parent company is a financial holding company

Individual waiver for parent companies Member states may grant individual institutions which are the parent company within a group, subject to the fulfilment of certain conditions, an exemption from individual requirements.

Solo mnsolidafion Member states may allow, on a case-by-case basis, for the purpose of the calculation of the individual requirements of the parent insfilufion, and subject to certain conditions, the inoØretion of subsidiaries whose material eØØ or liabilities are all to Ihatparent insttuton.

Exemption from Pillar III The Competent Autorifiee may deride to exempt, fully or partially, a credit institution from Pillar III requirements provided such institution is inducted within a group complying with comparable disdosures on a consolidated basis in a third country

Exemption from consolidation Member states may decide that, t certain conditions are met, some subsidiaries need not be inducted in consolidation.

N

Y

Toa large extent implemented

N

N

N

N

N

N

Institutions may be exempted fromØØidation provided tret the minimum

requirement on a consolidated bases doesnot deviate significantly from the minimum

requirement applying to the financialinsfitufice itself

Andes 22,24&25 9316 Consolidated waiver for investment firms A group of investment finns maybe exempted from consolidated capital requirements, on a mas byr-case basis, provided conditions am mot N

Annex III, Part 3 2000/12 Alternative template for the cwlwlafion of potential futurevalue in ceMin øses

For institutions complying with certain requirements in their trading activities in comorodities, gold and other products, Member States may allow percentages for tr ~bon of potentat future value other tran the general ones

1 COUNTERPARTY Annex III, Part 6, Pam. 2000/12RISK IN 7DERIVATIVES ANDOTHEREXPOSURES

1 COUNTERPARTY Annex III, Pert 6, Pare. 2000/12RISK IN 12DERIVATIVES ANDOTHEREXPOSURES

Higher value of mefident Alpha (multiliker to calculate dis Member Slates may seta value for ceeffident Alpha higher than 1.4exposure value of certain Øtracts)

Internel determination of the value of coeffdent Alpha Member States may allow insttutons to tebusta Alpha internally, sbject to e fl- of 1.2(multiplier k tehoste the exposure value cf cedemcentreds)

Page 7 of 7

Nasjonale valg og andre valg ved gjennomføring av nye kapitaldekningsregler

I STANDARDISEDAPPROACH

Artide80.3&AnnexVI, Part 1, Pare. 24

200.1/12

I STANDARDISEDAPPROACH

Article 80.7 2000112

2 STANDARDISEDAPPROACH

Article 80.70 2000112

21 STANDARDISEDAPPROACH

2rp)O/12

2 STANDARDISED

APPROACHB22 2060/12

2 STANDARDISEDAnnex VI,Pan 1, Para 2GW112APPROACH 6

2 STANDARDISEDAnnex VI, Part 1, Pare. 2000/I2APPROACH 12

2 STANDARDISEDAnnex VI, Pad 1, Para. 2000112APPROACH 15

2 STANDARDISEDAnnex Vi, Pert 1, Pare 2000/12APPROACH 15e

Risk-weghing etposures lo aeditireflstiØ

Exemption of infra-group eØosures from risk-weightedexposures

Treatment of eposures to a counter-party which ismember of the same institutional protection scheme.

N+,tual recog,titla, af ECAIs

MuleS Ørvdon of credit asses marts' sxppire

Reognition0/a thirdØtrys trestrnamtofoentralgovernment and central bank exposures

Recognition of a third munbys treaØnt of regionalgovernments and Inset auØtes

Treatment ofpubliesectorentities as inshlutlons

Treatment of exposures to public sector enuresguaranteed by central governments

Member States may choose between two altematiee metlwtls for risk- weighting exposures to man,, rnssØS: (a) on the basis of the risk-weght of the corresponding central government and (b) on the basis of the credit assessment of the institution ilsett. Alt (a).

If certain conditions are met, The Competent Authorities may assign a 0% risk-weight on eØosurea not forming part ofown funds' of a credit Institution to its parent urrdartekng, 00 subsidiary, a subsidiary of its parent underta king or an undertaking linked by a relationshipwithin the meaning of ArØe 12(1) of Directive 831349/EEC.

N

If certain conditions am met, The Competent Authorities may assign a 0% risk weight on euosures not tomting part of 'own funds' to Ønterpardes which are mendtes of the same institutional protection scheme as the lending institution. N

Ifs Canpefasst At,theity io a rnembersrate has recognised en ECAI as e g/or, The CompetentAuTaitio in Roomer gimber stara may -q- teal ECAI as elgtile without crrryØ 0Ut th u awn -lushes prØ>.

Wfnr r s Cr>npetenl AuV enny in a 5gnber stale hos det-losel a mopon etar eligble ECA' 9 -d i aswsenerentu, CrØeten' AvNadtes 0-t- ri orro he memASr else mey recog,2se tral Tappirvg vimoit tarmnor out II>e s awn dett m marint prowls

When a lard country with spervisory/regoaØ arrangements at least equnnalart to those in the Community, assigns for the exposures to its own central government and central bank denominated and funded in the domserle currency a kurel ritt, weight than the oneapplicable in principle, a member state may allow the risk-weight of such aepbsbms in the same manner.

When a third country with supervisory/regulatory arrangements at least equivalent to those in the Community heats exposures to regional government and local authorities as exposures to its central government, a member state may allow the risk-weight of such exposures inthe same manner.

Y

Y

Exposures to public sector entities may be treated as exposures to credit institutions, wiØut applying the preferential weights applicable to short tens eØosures to institutions. N

The Competent Authorities may, in exceptional cases, treat e>p Su s te public sector entities as exposures to the central goverment in whose jurisdiction they are established where, in their opinion, these is nodifierenca in the risk betwoen such exposures because of the Yd the central government has an unlimitedexistence of an appropriate guarantee from the central goverment labitifies of the contractual obligations of the

PSE. 10 percentage points are added incase of regional governments and la l

suthontes

2 STANDARDISED Annex VI, Pad i, Pam. 2000/12 Recognition of a third country's treatment of public sector When a third country with supervisorytsegulatoryanangements at lesst equivalent to those applied in the Community treats mposures to its public sector entities aseip0res to insttufons, a member state may allow the risk-weight of exposures to such public sector entities inAPPROACH 17 entities the same manner

2 STANDARDISED Annex Vi, Part 1, Pam 2000112 Treatment ofshon term exposures to EU insstWons in A competent authority may allow shat term exposures to mercer states institutions denominated and funded in the national currency a risk weight that is one cetegory lass favourable than the preferential risk weight applicable on exposures to EU central governments.APPROACH 36 their national currency

2 STANDARDISED Annex Vi, Pan 1, Para. 2000112 TreaØnl of short term exposures to men-EU institutions If acompetenteuthonty has recognised the preferential risk weight applied by a third country on exposures to its central government in domesticourrerwy, it may all short teen exposures to that third eouo6y's insfituØS denominated and funded in the nationel cunencyaAPPROACH 36 in their national ounency nok weight that is one category less favourable than the preferential risk weight assigned by the country concerned on the exposures to ila central government.

3 STANDARDISED Annex VI, Pan 1, Pare. 2000/12 Treatment of exposures in the form of minimum reserves Provided that certain Øditions are met, a meØr smte may permit exposures in the form of mkdmum reserves required by the ECB atop the cetsal bank of a member state to be held by a credit insttution, in accordance with to relevant EC8 regulaton on Ø applicationAPPROACH 38a held by an intermediary aed8 institution. of minimum reserves, to be risk weighted as exposures to the central bank of the mamba state concerned.

31 STA11DARDICED Annex l Pan T ram 2137/12 Ep essee ØE:d by mMgages a- reerdexlsol property- )n G,.a trying a Anavur oseurm by morfgsgxi ee e rich n V property for a 3% o: wc§ght, The s e t eenton_Au Ønlies stay wive from me "red aitena me ~nor 1 1 , i , ri,. of th, bomau s nhoold t M motenely d~re~N on the peno5,ance of the undo y,,tq pr yxerty, t

APPROACH 46 Øditonal waerd a aitenen a wet developed and hog eslabtistØ market exists ux the lerrilexs nip sufhaenby low n A rates to te/ty such Dexlmu,l.

STANDARDISED Attec VI Pert 1, Pea. 20DYJ/12 Risk-weighungeØures scarred by Øages on II the defined ehg9,ryenter, a!e ntzf, The CanpcfsrtAutltwjhes nay-,gn e 50"" rri weglta posur,s or nny pan elan exposure fully and Øpletey secured by mortgages on Ø500/øl real estate ,tested within their feebly.

PAPROACH 48 axmrrereinl real allots

3 STANDARDISED Moss Al, Partl, Para 2)170/12 RRk-wMghh'ne expwee severed by shares In [ertish Iltlte dFØ elgbåilv is/Inca ere met The Cwti,eteiet Aumonees nxay essgxa50°rosE/wergttloreØosuras fuly and wmpktey locoed by she cemelgiblc F,nish lwc,sng ømpanes tree ere/of connenisl real estate.

APPROACH 40 housirxq Ønb—

3 STANDARDISED A rsoe VI. Pan', Pars. 2Øl12 Riskyghtirg dig/le prep«iy Ieassrg uattØtiors It the defined ebgåtility er tero a2 met The CaTpetesLAØhexe may .sigi, e 50% risk weghton e>{,osures related to property leasrylg lmnvsst> mrtørnulg comrnoraal real seIeR e Nstod is re , ert—,

APPROACH 50

3 STANDARDISED Annex VI, Pant Para. 20170ri2 Exposures sea,co by mortgages on Ørcnaaal real In quNifying exposures severed by mortgages on commercial res, Dn>perty s'tuatad wtl,in its ternta//era 50",6 nisl:wØhl,eThe CaØe(ehl AuØnM1es may waive tram the ragwred ailerra rho ccvtdniontlen Van r.,k of ile Øarer shoed Irnatenaily Øend nn the

APPROACH AS estate wndiuo;al waiver o[a aiterrcxt pedor5a-tw of Lhe ureertyng property, if a well developed end tong established Øn>e«Ja real estate market esuts in the territory with lass rotes rut exceeding specified limits.

øllaleml.`3 S/ANDARDISED Annex Al, Pan 1. Pare. 2000112 Ris4. weighting pest due eØosuressecured by non eligible A risk weight of 100% may be assigned on pass due ebpuvuies which era WllyØrai by tout nisddtlu 006's" 'al when valueakuvbosps reach l5%oi the Øwure gross u1 me vakee adjustments,UuG,otopemironel spurts exist to ensure the good quality of the

APPROACH 60 0bilateral

3 STANDARDISED Annex Vl, Pad i , Pam. 2000/12 Risk-weighIrg of pest dueeØsures second by Theapplicble risk weight on past due erposuras secured by moØges on residential propery net of value adjustments may be reduced to 50%, if value adjrstrnents are no less than 20% of the expoeureamount gross of the value adjustments.APPROACH 61 mortgages an reødantial properly

STANDARDISED Amex VI, Part 1, Pam. 200WI2 Risk-weighting items belonging to regulatory high risk The Competent Authorities have the discretion to assign a risk weight of 150% on exposures associated with particularly high fiks.APPROACH 63 categories

3 STANDARDISED Annex Vl, Pad 1, Pare. 2000112 Regulatory, high fik categories- kowar fiskweghl due to The risk weight on non past dues>pmures receiving a 150% risk waightmay be reducedto(a) 100% rfvalue adjustments ex'stwhich are as lesslnn 20%ofthe gross exposure and)b)50% /value adjustrnents are no less than 50% of the grosexposure.APPROACH 64 value adjustments

STANDARDISED Annex V/, Pan 1, Pam. 2000112 Loans severed by cemmordalrel estate as Ølaterelfa The Competent Authorities mayreøgniseloansseared by Ømerdal real esthtees eligible øllateal tar awered bonds where the required loan to value ratio of 60%is exceeded upto a maximumlevel of 70%, B certain defined criteria andwnditonsaremet.APPROACH 65e) covered bonds

41 STANDARDISED ne, VI, Pan 1. Pare 2'HUi2 Ehøbk, third -try CIO (CsllemUva InvesUnent If a Cornpelenl Authority le; upprovnl e Iirrd ."ty GIU as xdgibls e Con ØlentAutlxxrity in amtlier nteelt smote may allow the use of thin reeogei/on .,toul serducting ,ts own aevssmenfAPPROACH 75 Undennklags)

4 STANDARDISED Anræx'vl, Parl t, Para. 2000112 Rsk-weghbng inrtitubwis speaaløimg in the eterbank Member Steles may allow a risk weight of10% for exposures a instiluas speoaising in the enter-bank and pubii. debtmarkele in Heir home member states, ifsuchlØtueons are subject to close supervØ and the exposures are adequately ~rød.APPROACH 82 and public debt merket

STANDARDISED Annex Vl, Part 3, Pam 2000/12 Excpe'ors to the non-use ofdarrestic wmswy ratings for The CortpetenlAuthwities rosy albrv tle donxesOc artency rating of an obligor to too used for its foreign artency exposures pravkled sumo exposures aricefØ institiNOns' parØpetion inaloen extended bye Multileterel Developnrent BankAPPROACH 18 foreign-currency exposures

43 STANDARDISED Article 63.2 2000/12 PennissØ to use unsolicited ratingsAPPROACH

In order to use unsolicited ratings, credit institutions most get permission from the competent authorities. To make this possible, that alternative should be incorporated to legislation (implicit discretion)

IRB Artiste 84.2 2000112 Requirements for IRB standards Ø parent and EU When IRB approach is used by an EU parent on firwndal hoding company and its subsidiaries, Member States may allow the minimum requirements to qualify for IRB to be net by parent and subsidiaries considered together,subsidiaries altogether

Article 69.1 Last 20D0/12 Item it Aided to the purposes of mutual sxosrlrtilion only Meenbex states 5øy rscagrtce the sta,ØrdØ cpip~ treatment to equity e>posuree In IRB funks bssrE ueatrnenl hss beet, au0ronsed by -Uler McØer state' re/atw

Y

Y

Y

N (NA for NØegian banks)

(i) N, (li) Y

(i) N, (li) Y

Q A. (,,)Y

(i) N, (b) Y

N

N

Y

N

N

Id

Y

Yes, but orry 8 the methedoØ forassigning the rating satisfies the sane

criteria as fm solidted reings.

Page 2 017

Nasjonale valg og andre valg ved gjennomføring av nye kapitaldekningsregler

Referanse Beskrivelse

IRB Annex VII, Part 1,Pare .5

2000112

IRIS Annex VII, Part 1, 2000112Pare. 11, last sentence

4 IRIS Annex VII, Part 1,Pare. 16

2000/12

IRB 2000112

AnaexYU-paA-2-Para 6d)

2000/12

IRB Annex Vil, Part 2,Pare if & 12

2000112

Annew Vil, Pan li,R.ni

2000/12

5 IRB Annex Vl 1, Pert 2,Pare 14

2000/12

5 IRB Annex Vll, Pert 2,Pare 14 - lastsentence

2000/12

5 IRB Annex VII, Part 2,Par 19 & Annex VIII,Part 1, Para. 26

2000/12

Lower rate for speaaread lending The Competent Authorities may euhaise e credit institution to generaty assign a 50 % fisk weight to SL-Category 1 and 70 % to SL-Category 2 (regardless of maturity) K certain candiuone are met N

5 IRB

Anne Vll Part 4, Prra lVmiiTt12

48.

Annex VI 1, Part 4, Pare 2000/1256

5 CREDIT RISK Annex Vill, Part 1, 2000/12MITIGATION

CREDIT RISK

Pare 15

Annes Vill, Pert 1, 2000112

MITIGATION

CREDIT RISK

Pate I6

Annet Vlil, Pan 1 3Y_0112

MITIGATION

CREDIT RISK

Pare 17

Annex VIII, Part 1, 2000/12MITIGATION

61 CREDIT RISK

Pare. 20

Annex VIII, Part 1, 2000112MITIGATION

6 CREDIT RISK

Para. 21

Annex VIII, Part 1, 2000112MITIGATION

CREDIT RISK

Para. 28

Annex Vlll, Part 3, 2000112MITIGATION

CREDIT RISK

Para. 12

Annex VIII, Part 2, 2000112MITIGATION

6 CREDIT RISK

Pare. 9. (ii)

Annex Vill, Part 3, 2000112MITIGATION Pare 19

A~ Vill, part 3, 2000/32

6 CREDITRISK

PareA3

Annex Vill, Part 3, 2000112MITIGATION

CREDI1 RISK

Pare. 44

ore11ll Pena, 2Øl12l41TIGATION

6 GREDTRISK

Pare 73

AaoeoVlll,Part3, 2000112MITIGATION

7 CREDIT RISK

Pare 74

Annex Vill, Pad 3, 2000112MITIGATION

71 Seantsaton

Pare. 90

Ar/de973 2000/12

7 SmhnØtion Anide982 2000112

Spedal haheent fa revolving retail errponures seared by The requirement that retail revolving eyosures be unsecured (Annex VI I, Part 1, Pare 11 b)) may be waived by The Competent Authoritea in respect of cdleterelised credit fadlifies Inked to a wage acaunt.a link to a wage =unt

Treaenent of andllery banking services Exposurea to ancillary banking services undertakings (equity) can be treated as noncredit obligation assets.

Possibility to extend the list of unfunded protection For the purposes of the remgnØn of unfunded credit protectlon in PD by inshlufions, The Competent Authorities may extend the list of unfunded credit protection providers further than those inducted in Annex VIII, Part 1, Pare. 26providers fee the purposes of recognition of unfunded (note. this paragraph applies to dilution riskcredit promotion in PD only)

L69fer-seveteå§ende

Alternatives for the celalefion of maturity The Competent Authorities may require all institution in their juris~ to use matunty(M) for eat exposure in accordance with formulae instead of using values by default (0.5 years for repos and 25 for other e>penures), N(not required, not even pennited under

FIRE)

Competent Authortles should net out a series of short-term e>posures for which M is, at least, one day.

Maturity for EU-firms (< EUR 500 mio.) The Competent Authodfies may allow metunty of exposures to European corporates with ønØidated assets of less than EUR 500 million to be set at values by default, even t they apply the formulae option.

Maturity for EU-firms investing primarily in reel estate (< The Competent Authonfias may all= metunty of exposures to European corporates that invest pnmadly in reel estate with oonØidated assets of less than EURi000 million to be set at values by default, even ff they apply the formulae option.EUR 1,000 mil

Posadrility to extend the list of unfunded protection For the purposes of the calculation of dilluton risk, The Competent Authorities may extend the list of unfunded credit protection providers fudher then tase induded in Annex VIII, Pad 1, Para 26providers for Ø purposes of oslevlafon of dilluton fisk

Defiriiboe ofdefn.ot lor rubil and PSE The Competent Authonnes cfeeeh Member state shall set the enact nirtSer of days oast 1.lthl lea] !,t,, SE eØwure beep oxhsiderrxl e default alvhy, between90 nod18Pd,lye The,uebe,snay differ by predun li,-. For expu..uroo Bother !Jen ber Stans. )i)UT.

the number of days employed cannot be hgher than the ones applying ie such Mee ter states I1) Y (but only the other state's er. 1

number - ø90 lave)

Flexibility in data collection The Competent AuØrities may apply less stringence as regards the data needed fa estimator and collected before the implementation of the du ecuve, provided the credit matretten makes appropriate adjustments.

Recognition of shares in Finnish housing companies en The Competent Authorities may authorise their credit institutions to recognise as eligible collateral shares in Finnish hosing companies that are epen3tng in amwdence with the Finnish Housing Cortpany Act of 1991 provided that certain conditions are met.stigble ce atenel

Reerdeetøl real r,tote poØrty axiom For expos ra, :nlal real estate property e,lUutedwithie thyreell-iofChet M6cØ.r Stete, The Competent Author bee nary wave cedere erin a>rditique Ire'Øimameet for ihercedtie)ilutone locaodhply,rdroxditioe (b) in paregeapr l3 which,trim that

the d 4 f tbcrower le rat n,terøly depend !pee the p,erereexe et me uhderlprg prepaM erpøjact but tufter on the underlying dty of the borreuerto Øay Ne debt it n: oøu Øuces.

Gonhmadal raa! estere property wu,,

Amounts receivable as cIneMa collateral

Other plpsical oib(eral

Fern c n n; cal real ,.;rate property situated within Ø territory of tct Menb- State, The .;oeTetent Autwnbes -y werve, If -IS , , -edit,., ere met, the regcae, e,t for !trek 7solotoee to -,,ply .,ti, andlfin (b)in paregeeph 13 whch ,'ales Thal thou ns4 et t, Ø

does hat materially depend upon the Ønotteethm of the underlying property er pe rel, het ra/err ah the underfying rmpeosty of the boeexer to repay ØØt hen other eearms.

The Competent Aufeordes may recognise an eligible collateral amounts receivable linked toe commeroal transector a bertsa000ru xtlo an original maNdly of less than or equal to one year. Eligible receivables de not Include those assodatad with seamfisefiene, sub-pertidpations w credit derivatives w smarts axed by affiliated parØ.

The Competent Autrorities may recognise es eligible collateral phystcel items of a type other than real estate Øistenel, t sefisfied as to the following (a) liquid markets for disposal of the Ølateral do exist in an expeditØS and scwhomicaly etioent manner; and (b) well-established, publicity available market prices for the collateral de edet, the institution must be able to demonstrate that dem is no evidence that the eel R~ it receives when collateral is realised deviates significantly from these market prices.

The Competent Authoeles may recognise as eligible Ølaterel physicel items of a type other than real estate collateral, if satisfied as to certain oondrØS. N

N

y

y

y

y

N

N

y

y

N

(i) N (ii) V

Permission of internat nssdels apprcet for olalahon of The Competent Autthorties may permit credit institutions meeting certain requirements to use an internat models approet taking into aarount Øelations to celculate the adjusted exposure value for e>posures realting from the applioaton of a master netting agreement. Will be implemented ahem 2007fully adjusted ehposure value (E`)

Mtntmum requirements for the recognition of receivables Credit instirotons must lake all steps necessary to fulfil total requirements in respect of the enforceability of necurity interest. There tihall be afmmewwkwhich allows the lender to have a first priority claim over the collateral subject to .atonal discretion to albs such datms to Nas Ølateral be subject to the daims of preferential creditors provided for in legislative or irnptemenfing provisions.

Perm~ In use empirical Ørelatons within and across The Competent Autrorites may slim credit trenchers to use eØirical ørelatons within risk categories and across risk olistegodes t they are mfl~ that the credit it ethrton's system for measuring correlations is sound and implemented with integrity. Will be implemented after 2007risk categories

eipæuFm)

Own anSmatss of volatility adjushnenls (cetegaies ofsecuny)

Redeeed ICDe for lensing traneande

When debt securities have a credit assessment from a recognised ECAI aquaslant to inveeMænt grade or beter, The Competent Authorities may allow credit instNtons to cebulala a volatility estimate for sat category of searity.

Until 31 December 2012 The Competent Authorities may,subj d to the indcated levels of Ølateraisanon alba wadil ime/tutohn te 00,00 breer levete of LID foe ,error e>Øfres in the torur of Catet'iv0 Reel Estate leasing and of equnmeelleasing At Ø ard el herr

period tue provisio shall be reviewed

Subjeol io certetn requirements Tice Gonpeleni Authonbes oh e Menhbar Slake may auØise credit inslNteeo io apply a 50% risk woigmirhg to the part ot the eposure fury Øleterelised by residential or comneerdal real estate property stuetad within the tem" of theMester Stales,

y

Allernab vv beaiment ire reel es ate Ølateral (50% riskweight)

Sovereign guarantees

Muiunl Re-gnition of ~le ECAIs

Mutthal Reøgnil 'ron of ineppirg of ECAIS aedhl

ØS,nhe1h15

N

The Competent Authorities may apply reduced risk weights to exposures a portions of e>poares guaranteed by the central goverment or central bank, where the guarantee is denominated in fine dørbeste smarty of the borewen and the etposuer is funded in that arena. N

Thee Corhpetethl Authaites can re-garnro on ECAI no elgos d tit was re eegetrml as elgtile by mothor ~ber State wlthaht ennying out theme own evnluano,, proms,

The Competent Authail ee øn accept the de.lererinatron made by anotnr Meralter SVite wh the mappirn of en ECAI credit nsmenrents witØt ca ned out the prep ttemsety

I Seantsaton Annex IA, Part4, Pare 2000112 Treaboentelcerletn retail exposures subject ro early Tha Competent Andras may apply a basunent anil Me lines of para. 21 ro 29 in the yea of saauites subject to an early eØsanon provrswn of certain retail oposures(u-Ømttted, uncondnbonely cerØlleble witØtpriw reouce, early amortsata is triggered by a N30a arnorheffi provision quanfitat ve value in reaped of sossething other than the three months average excess spread) for detannining the conversion figure.

Page 3 of 7

7 ~mist ral Annex IX, Part 4, Pare. 2000112 Appliuolon of U. ornr„,od Supervisory Formula Method51 (lest sentence)

7 OPERATIONALRISK

Article 20.2 93/6 Minimum level of own funds

7 OPERATIONALRISK

Article 20.3 93/6 Minimum foal of own funds

7 OPERATIONALRISK

Article 102.4 & AnnexX, Pert 4, Pare. 1 and

2000/12 Combination of approaches

7 OPERATIONALRISK

Article 1043 2000/12 Alternative Standardised Approach

7 OPERATIONALRISK

Article 105.4 2000/12 Ølifyirg criteria for AMA within the same group

OPERATIONAL Annex X, Pan 2, Pare 2000/12 Alternative Standardised ApproachRISK 7&9

81 QUALIFYINGHOLDINGSOUTSIDE THEFINANCIAL SECTOR

Article 1221 2000112 Spesial treatment for insurance undertakings

B QUALIFYINGHOLDINGSOUTSIDE THEFINANCIAL SECTO

Article 122,2 2000/12 Alternative - deduction

8 TRANSITIONAL 2000112 Transitional roduction of minimum length of observationPROVISIONS periods

8 TRANSITIONAL Article 153, Pare. 1 2000/12 Transitional treatment for certain property leasingPROVISIONS (first sentence) transactions

8 TRANSITIONAL

PROVISIONSArticle 153, Pare 1

(second sentence)2000112 Transitional definition of me secured portion of a loan

Article 154(-1) 2000112Transitional use of a different definition of past due

Article 154.1 2000/12 Trensiaonelty shorter test of use

8 TRANSITIONAL Article 154.1a 2000/12 Transitionally shorter requirement of use forPROVISIONS LGD/conversØ factors estimates

8 TRANSITIONALPROVISIONS

Article 154.3 2000/12 Transitional exemption for certain equity exposures

TRiANSITIOnSAI

PROVISIONS

ArSOn 1544 2000/12 Trensniaal Øfault defniamh for oxporate expos os

6 TRANSITIONALPROVISIONS

Aside 154.5 2000/12 Transltional FD calailaaon(foundamon IRS)

TRANSITIONAL Article 154.6 2OØ12 Trensior dl calculations: at flammetes (retail), LGD endPROVISIONS -smion factors

91 TRANSITIONAL Artide 155 2000/12 Trensitaøl calculations: standardised approach -PROVISIONS operational risk (.edit institutions)

9 TRANSITIONAL Article 45 9316 Transitional caEulations:stendardisedapproach -PROVISIONS operational risk (irwestnent firms)

9 TRANSITIONALPROVISIONS

Annex VII, Part 2,Pare. Bd)

2000/12 Transitional LGD for cowered bonds

Nasjonale valg og andre valg ved gjennomføring av nye kapitaldekningsregler

The Competent AuØilia; may permit credit insatuØS to apply for seceritisetions invoking retail exposures the Supervisory Formula Met 4 using simplifications fa certain risk parameters

The Competent Authorities may allow investment firms with limited licence to provide own funds which are always more then or equal to the higher of the vital requirement for credit and market risk a 25 %of the preceding years fixed overheads

The Competent AuØri/es may allow investrnenls firms which told 730 000 EUR in initial capital, nut which tat within certain categories, to provide own funds which are always more than or equal to the higher of the capital requirement tor.editend market riskar 25 %of C.preceding yea. fixed overheads

The Competent Authoities may allow institutions t.. a ~birøton of approaches

The Competent Authorities may under certain conditions auØse institutions to use a alternative indicator to calculate its coital requirements.

The Competent Authorities may allow the qualifying criteria set out to be met by the parent and its subsidiaries considered together.

The Competent Authorities may authorise institution to calculate its dritel requirement using an alternative standerdined approach.

Member states may exempt insurance sector undertakings from the general limits established for qualifying holdings

Member states may dede not to apply limits on qualifying holdings, provided excess is deducted from own funds

Member Sues may tranan500ely allow a reduction of the minimum length of the observation periods required for own estimations of PD, LGD and CCF, subject to an absolute minimum of 2 years.

The Competent Authailhes may, until December 31, 2012 allow leasing exposures on offices or commercial premises in their territory and subject to certain conditions, to be rated 50%

1 he Competent Aurhonaes may, until December 31, 2010 allow, for the purpose of deicing the secured portion of a loan, recognise eligible collateral other than the one meeting the requirements

Until December 31, 2011, the Competent Auhtaiaes may set the number of days past due up to 180 days it local conditions make it appropriate (for the purposes of application of the standardised approach). The specific number may differ across product lines

Institutions applying for the use of IRS before 2010 may bereft from a test of use shorter Øn 3 years but above I, unfit December, 31 2009

For trace inn/lotions applying fa the use of their own LGD/conversion factors estimates, the thres-year period of experience in use required by Article 84.4 maybe reduced to two until December 31, 2008

The Competent Authorities may, until December 31, 2017, exempt from IRIS certain equity exposures held on December 31, 2007.

Until DØnber 31, 2011, i he Competent Authøities may sot to ofini- of defnut at arty number of days prist due helonen 90 and 180. For e>posurem skuated in omen Member star,me numer of days will not be inferior to dl one in ht Member state

Forn inqrlwhhanlalxm of IRS, or frum Detente, 31, 2007 ar the latest, .edit Iriltulons maybe allowed iu uØ en hisbhical 501100 of dala 0000111/6 c Golly 2 years instead of 5), then increase up to five urfil December 31, 2010, at the latest (increase ot 1 year per year)-

Historoal series maybe allowed to Øer initially (from IRB implementation or December 31, 2007) only 2 years, ten increasing I year per year urral December, 31, 2010

Unfit December 31, 2012, the 'trading and sales" business One may be applied a 15 %factc, tit represents at least a 50 % of the total relevant indisØ.

Unfit December 31, 2012, the'hading and sales' business line may be applied a 15 % laces, tit represents at least a 50 % of the total relevant indicates.

Unfit December 31, 2010, covered bonds maybe assigned an LGD of 11.5 %

Page 4 of 7

Y

Y

N

Y

N

Y

N

Y

N

Y

N

N

N

Y

Y

N

(i) 90,

pq v (but .,to ma ormar states exactnumber - ur 90 days)

y

Y

N

N

Y

Nasjonale valg og andre valg ved gjennomføring av nye kapitaldekningsregler

9 TRANSITIONAL Article 456 93Rd

PROVISIONS

TRANSITIONAL Article 45c 93/6PROVISIONS

TRADING BOOK Article 18.3 9316

9 TRADING BOOK Article 19.2 9316

TRADING BOOK Article 26 93/6

TRADING BOOK Article 33.3 93/6

I TRADING BOOK Annex I, Pam. 4, 2nd 93/6sub-paragraph

101 TRADING BOOK Annex I, Pam. 4, 3rd 93/6subgamgreph

10 TRADING BOOK Annex I, Pam. 5, 2nd 93/66sub-paragraph

10 TRADING BOOK Annex I, Pam. 5, 3rd 9316subparagraph

I TRADING BOOK Annex I, Pam. 5, 3rd 93/6sub-paragraph

1 TRADING BOOK Annex I, Pam. 14 93/6

I TRADING BOOK Annex I, Pam 26 9316

-P am, ritr 93/6

10 TRADING BOOK Annex I, Para. 35, First 93/6sentence

10 TRADING BOOK Annex I, Para 35 c) 9316

11 TRADING BOOK Annex III, Pam. 21, 93/6Last sentence

111 TRADING BOOK Annex III, Pam. 31 9316

11 TRADING BOOK Annex IV, Pam. 7 93/611 TRADING BOOK Annex IV, Pare. 8 93/6

11 TRADING BOOK Annex IV, Pam 10 93/6

11 TRADING BOOK Annex IV, Para, 10, 93/6Last three sub-paragraphs

11 TRADING BOOK Annex IV, Pam. 14 93/6

Alternative tranalional operational risk requirement Until December 31, 2011, The Competent Aul ro u nay choose not to apply requirements for operational risk as set out in Article 75(d) 2000/12 to low size investment firms. An atemative treatment applies instead

Trensitioral applicability of recognized spedfo nsk models Until December 31, 2009, or any other data spedfied by The Competent Aumotibes on a msebycese basis, it may be provided that for institutions that have received specific 4ks model recognidon prior to Jan 1, 2007 previous requirements (as in the old directive) apply

Application of the banking book roles to Wing book, t not The Competent Authorities may allow institutions to epppty banking book rules to their trading book exposures, provided the trading book activities does not exceed certain limb,material

Specific rØ requirement for covered bonds Member States may seta reduced specific risk requirement for covered bonds, with reductions similar to tse applied in the banking book under the standardised approach.

Offseffing trading positions For the purposes of calculation of consolidated capital requirements, The Competent Authorities may authorise the offsetting of trading (trading book, commodities Bc) positions even when they are booked in different insttufions within the group, subject to certain conditions.

Alternative requirements for valuation in absence of readily The Competent Authorities, in the absence of readily available market prices, may choose not to apply daily mark to market edn, instead, require institutions to apply alternative methods subject to their approvalavailable market prices

Capital requirement for an exchange-traded future Subject to certain conditions, The ConpelentAuthori/es may allow that the capital requirement for an exchange-traded future contract be equal to the margin required by the exchange.

Capital requirement for OTC dervative cleared by a Subject to certain conditions, The Competent Authorities may allow that the capital requirement for an OTC derivative deemed by a clearing house to be equal to the margin required by the clearing house.clearing house

PresØfian ofspedhc methodologies for the caØafion of The CompelentAutudtes may preembe that delta be calculated foØing methodologies specified by tam.den

Capital requirement for exchange-traded written options Subject to certain conditions, The Competent AuØnties may allow that the capital requirement to an exchange-traded written option, or an OTC option cleared by a clearing house to be equal to the margins required by the exchange or the clearing house, respectivelyand OTC options cleared by a clearing house

Capital requirement for exchange-traded bought options Subject to certain cendifions, The Competent Authorities may allow that the capital requirement for an exchange-traded bought option, or an OTC bought option cleared by a deadrg house to be equal to the requirement for the underlying instrument.

and OTC bought options cased by a deeming house

Spec risk charge fora nor-qualifying issuer The Competent Authorities may require that instruments issued by non qualifying issuer ere applied a spedfø risk capital charge higher than 8 % or 12 %and/or disallow offsetting for the purposes of general market risk between such instruments and any other instrument.

U. of dumt instead ot tfa standard system for The Competent Auhtaities may, eimer b general or on an individual basis, allow institutions to use a system for calculating the general irsk for traded debt instruments which reflects duration instead cf the system set nut in the directive.calotlation cf the general duk of traded debt positions

Reduced specific risk requirement for certain equity The Competent Aumodties may allow certain equity portfole to be assigned a specific risk requirement of 2 % instead of 4 %portfolios

Altemativemaximum weight of an indiidualposition in an The Competent Authorities may authorise that individual positions represent a maximum of 10% of the total equity porfolio(instead of5% as in the Directive), provided that the sum of such positions do not exceed 50%insttufion's equity portfolio

Discretional use of net present value for delemummg the The ConpetentAutødges have the discretion to dim institutions to use net present value when determining their open positions in currencies or goldopen position in currencies or gold

Lower capital requirements for closely correlated The Competent Authori/es may ablow institutions to provide lower coital requirements for podtions in dosety correlated concedes, as defined in the Directive.curreadea

Definition of'poeitøns in to same ømmadiy The Competent Authorities may regard, in some cocas, different but closely linked commodities as the same, for the purposes of calculating the position in a Ømodity.Capital requirement for exchange-traded commodities Subject to certain conditions, The Competent Augadties may allow met the capital requirement for an exchange-traded commodity, or an OTC commodity derivative cleared by a dcering house to be equal to the margins required by the exchange or the clearing house,OTC commodity derivatives cleared by a clearing larvae respectively.

PresØtion of speck methodologies for the osculation of The Competent Aumonbes may prescribe that delta for commodity derivatives be calculated following methodologies specified by themdeb for derivatives on commodities

Capital requirement to exchange-traded options and OTC Subject to certain øndibons, The Competent Authorities may allow that the capital requirement for an exchange-traded written option, or an OTC option dented by a denting house to be equal to the margins required by the exchange or the clearing house, respectively. Alsooptions cleared by a clearing house OTC bought options may be assinged the same requirement as the underlying ovnnØily

Offcetfing posifions in the same Ømodity The Competent Authorities may allow positions in the same commodity ar in Ømodities regarded as t e name- to be offset prim to ossignement lo the appropriate maturity band.

N

N

Y

N

N

Y

N

N

Y

Y

N

N

Y

N

Y

N

Y

N

Y

Page 5 of 7

Nasjonale valg og andre valg ved gjennomføring av nye kapitaldekningsregler

Oni,å Referanse

Subjet to approval clause

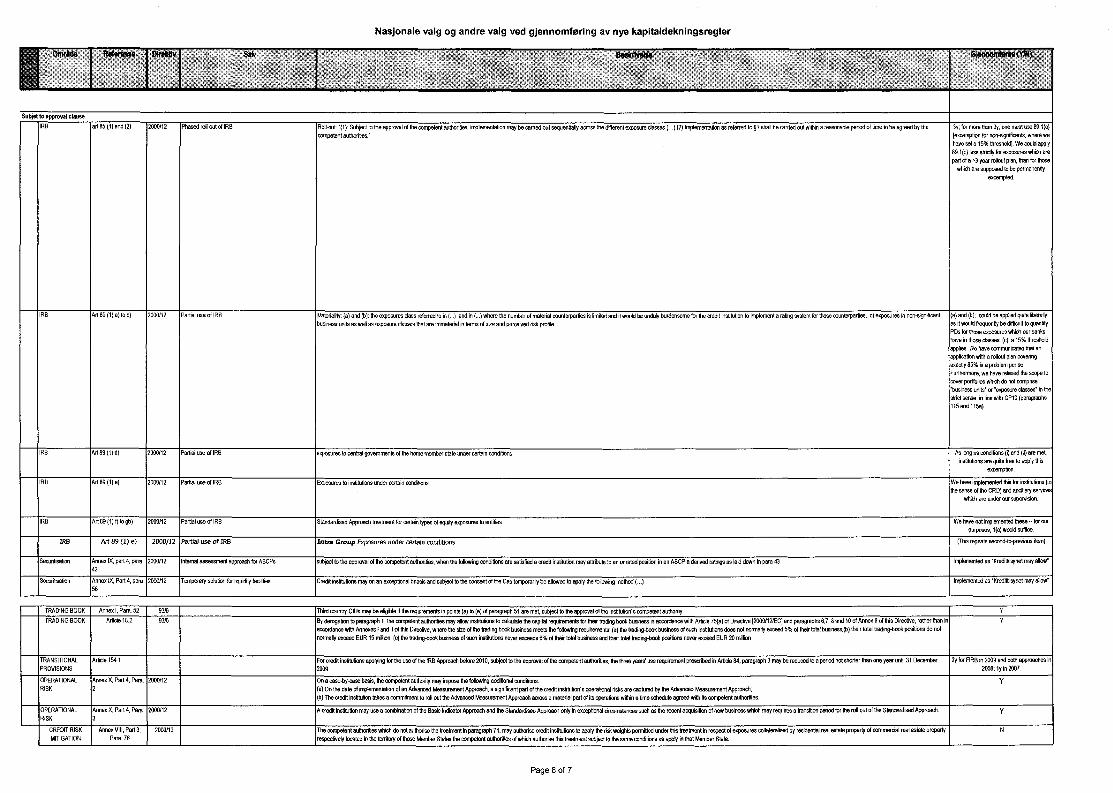

IRB ad 85(1) and (2) 2000/12 Phased roll out of IRB

Sak

IRB Art 89(1) a) to c) 2000/12 Partiel use of IRB

IRB Art 89 (1) d) 2000/12 Partial use of IRB

IRB Art 89 (1) e) 2000/12 Partial use of IRB

IRA Art 89(1)t)to gt) 2000/12 Partial useoflRB

IRB Art 89 (1) e) 2000112 Partial use of IRB

SecudtisationAnnexlX, part4, pare 2000/12 Inlemal assessnlerrt approach for ABCPs42

Securiftsalon Annex IX, Pert 4, para 2000112 Temporary solution for liquidity facilities56

TRADING BOOK

TRADING BOOK

TRANSITIONALPROVISIONS

OPERATIONAL

Annex I, Pare 52 93/6

Article 18.2 93/6

Article 154.1

Annex X, Part4, Pam. 201X/12RISK 2

OPERATIONAL Annex X, Part 4, Pare. 2000112RISK 3

Roll-out. )t): Subject to the approval of the competent authorities, implementation may be carried out sequentially, across the different exposure classes (...)(2) Implementation as referred to§1 shall be corned out Within a reasonable pencil of time to be agreed by thecompetent authordes."

Materiality: (a) and (b): the exposures dass referred to in(.) and in(.,.) where the number of material counterpanes is limited and it would be unduly burdensome for the credit institution to implement a roing system for thone ccunterparties, c) expØres in non-significantbusiness units as well as exposure classes That are immaterial in terms of size and perceived risk profile

exposures to central governments of the home member state under certain ØdiIons

Exposures to institutions under certain conditions

Standardised Approach treatment for certain types of equity exposures to entities

Intra Group Exposures under certain conditions

subject to the approval of the competent auØriles, when the following condØns are satisfied a credit institution may attribute to an urinated position in an ABCP a derived ratings as laid down in pare 43

Credit institutions may on an exceptional brass and subject to the consent of the Cas temporarily be allowed to apply the following method (..)

Third county CIUs may be eligite if the requirements in points (a) to (e) of paragraph 51 are met, subject to the approval of the instituØ's competent authority.

By derogation to paragraph 1, the competent authorities may allow institutions to calculate the capital requirements for their bading book business in accordance with Article 75(a) of Directive [2000/I2/EC] and paragraphs 6,7, 8 and 10 of Annex II of this Directve, rather than inaccordance with Annexes I and I I of this Diredwe, where the size of the trading book business meets the following requirements (a) the tadingbook business of such instotons does not normally exceed 5% of treir total business;(b) their total tradingbook positions do notnamely exceed EUR 15 million; (c) the "ding-hook tilsi- cf seoh instiNtons never exceeds 6% of their total business and thea tote) trading-bØ posteons never exceed EUR 20 million

For credit insllugØ applying for the use of the IRB Approach before 2010, subject to the approval of the competent authorities, the three years' use requirement prescribed in Artois 84, paragraph 3 may be reduced to a period not shorter than one year until 31 December2009.

On a caseby- ase basis, the competent authority may impose the following additional conditions:(a) On the date of implementation of an Advanced Measurement Approach, a significant part of the credit institution's operational risks are captured by the Advanced Measurement Approach;By The credit institution takes a commitment to roll out the Advanced Measurernent Approach across a material part of its operators within a time schedule agreed with its competent authorities.

A credit inaoWtiah may use a combination of the Basic Indicator Approach and the Standardised Approach only in exceptional circumstances such as the recent acquisition of new business which may requires a transtion period for the roll out of the Standardised Approach.

3y; for more than 3y, one must use 89.1(c)[excemption for n-sgnificents, where weheve seta 15% threshold). We could apply89,1(c) less strictly for exposures which arepart of a >3 year rollout plen, than for those

which are supposed to be permanentlyexcenpted.

(a) and (b): could be applied quite liberally,as it would frequently be difficult to quantityPDs for those exposures which our bankshave in those dasser (c): a 15% thresholdapplies We have communicated that anapplication with a rollout plen coveringexactly 85% is a problem perse.Furthermore, we have relaxed the scope tocover portfolios which do not comprise'business units' or 'exposure classes" in thestrid sense, in line with CP10 (paragraphs115 and 115a)

As long as conditions (i) and (ii) are met,institutions are quite free to apply this

excerption.

We have implemented this for institutions (inthe sense of the CRD) and ancillary sere

which are under our spervision.

We have not implemented these - for ourpurposes, 1(c) would suffice.

(This repeats seoo,d-"redous item)

Implemented as 'Kredittilsynef may allow'

Implemented as 'Kredittilsynet may allow'

Y

Y

29 for FIRB in 2009 and both approaches in2008; ty in 2007.

Y

Y

CREDIT RISK Annex VIII, Part 3, 2000112 The corspetent autoriller which do not autrorise the treatment in paragraph 74, may autorise credit institutions to apply the risk weights permitted undo this treatment in respect of exposures collaleralised by residential real estate property of dommerdal real estate property NMITIGATION Pam. 76 respectively bøtad in the terop of tose Member States the competent aul horites of which aularise this treatment subject to the same conditions as apply in that Member State.

Page 6 of 7

Nasjonale valg og andre valg ved gjennomføring av nye kapitaldekningsregler

CREDIT RISK Annex VIII, Part 3, 2000/12MITIGATION

IRB

Pam. 60

Artide 87.4 2000/12

STANDARDISEDAnnex VI, Part 1, Pare. 2000112APPROACH 73

STANDARDISEDAnnex VI, Part 1, Para. 2000/12APPROACH 52

TRADING BOOK Annex VII, part CA,para. 3

93/6

COUNTERPARTYAnnex III, part 5,para. 2000112RISK 19

COUNTERPARTYRISK

Annex Ili, part 7,Winne of

2000112

Where a oxryetent authority permits the treatment set out in paragraph 59 to be applied in the rase of repurchase transactions or securities lending or borrowing transactions in secunees issued by its domestic govamment, then other competent autlhonaes may choose toallow credit institutions incorporated in their jurisdiction to adapt the same approach to the same transactions

Y

Approaches to determine risk weights forequiy eØosures NotwiØtending paragraph 3, tre calculation of risk-weighted exposure amounts for credit risk for all agrosures belonging to the erosu re dess referred to in point(e)of Artide86(1) shall be calculated in ~danne with Annex Vil, part I, paragraphs 15 to 24 subject to SRWA and PD/LGD Approachapproval of competent aul rorbas. Conhpe(ent authorities shall any aihw a credit institution to use tre approedh set out in Annex Vil, part 1, paragraphs 23 and 24, il the credit institution meets the minimum requirements Annex VII, part 4, paragraphs 114 to 122. implemented, but not VaR. Combination

possible.

Where competent authorities consider that a position in a CIU is associated with particularly high risks they shall require that that position is assigned a risk weight of 150%. Y

The 50% risk weight shall apply to the part of the loan that does not exceed a limit calculated according to either of the following conditions: a)50% of the market value of thepnpery in question, b)55% of the market value of the property or 60% of the mortgage lending value, Nwhichever is lower, in those Member Stales that have hid down rigorous criteria for the assessment of the mortgage lending value in statutory or regulatory provisions.

Indusion of holdings in the trading book Conpetentauthorities may slim institutions to treat positions that are holdings as set out in Directive(20001121EC) Article 57(I),(m)and)n) in the trading book es equity or dept instruments as appropriate where an institution demonstrates that it is an active market maker in NIn- positions.

standardised method: transactions with anon-linear risk For transactions with a non-linear risk profile or for payment legs and transactions with debt instruments se underlying for which the credit institution cannot determine the delta or the modified dureton,respectively, with an instrument model that the conpetent authority has Institutions must use mark to market methodprofile approved for the purposes of determining the minimum capital requirements for market risk, Ø competent authority shall determine the size of the risk positions and the applicable CCRf s conservatively. Alternatively, competent authorities may require the use of the method

set out in Part 3 (CEM).

net gross ratio anti-togross ratio»: at the discretion of the competent authorities either (i) separate calculation ..; (ii) aggregate mkuleflon N - only separate calculation

Page 7of7