financing & economics of city gas distribution- feedback ventures

TRANSCRIPT

Presentation on

Financing & Economics of City Gas Distribution

Conference on “Distribution of Gas”

Conducted by

India Infrastructure

March 04, 2009

04/03/2009

Energy Division2

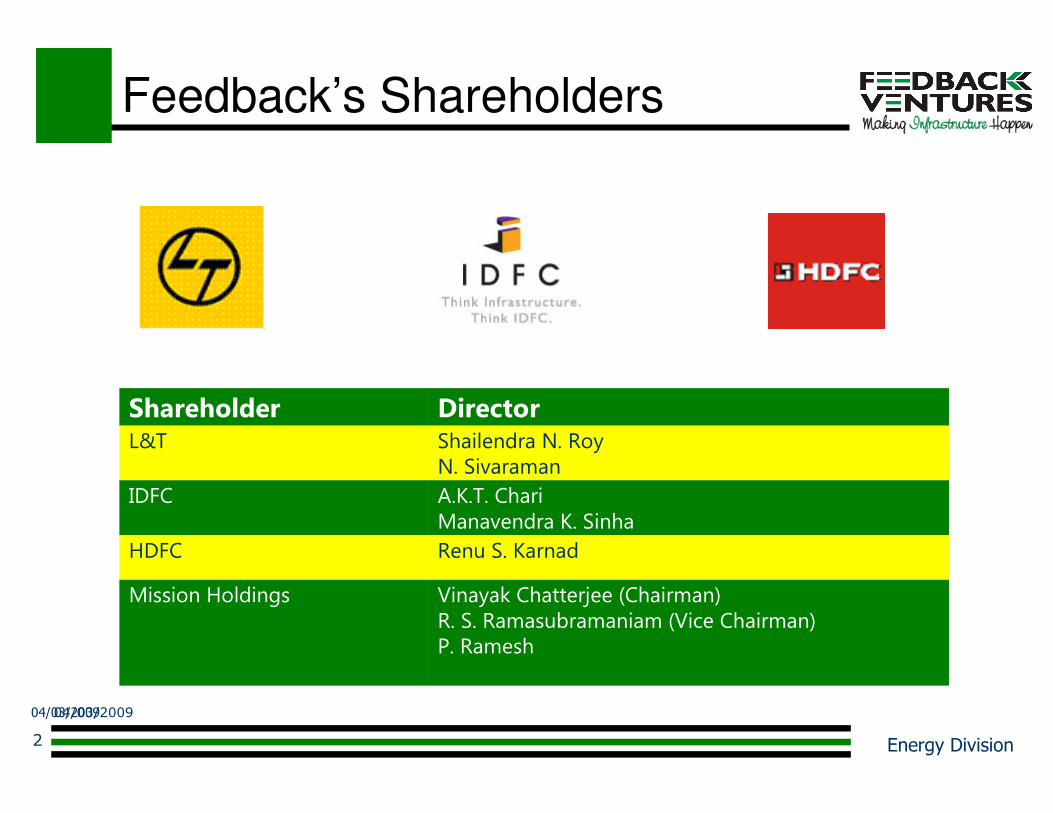

Feedback’s Shareholders

Vinayak Chatterjee (Chairman)R. S. Ramasubramaniam (Vice Chairman)P. Ramesh

Mission Holdings

Shailendra N. Roy N. Sivaraman

L&T

Shareholder Director

IDFC A.K.T. ChariManavendra K. Sinha

HDFC Renu S. Karnad

04/03/2009

04/03/2009

Energy Division3

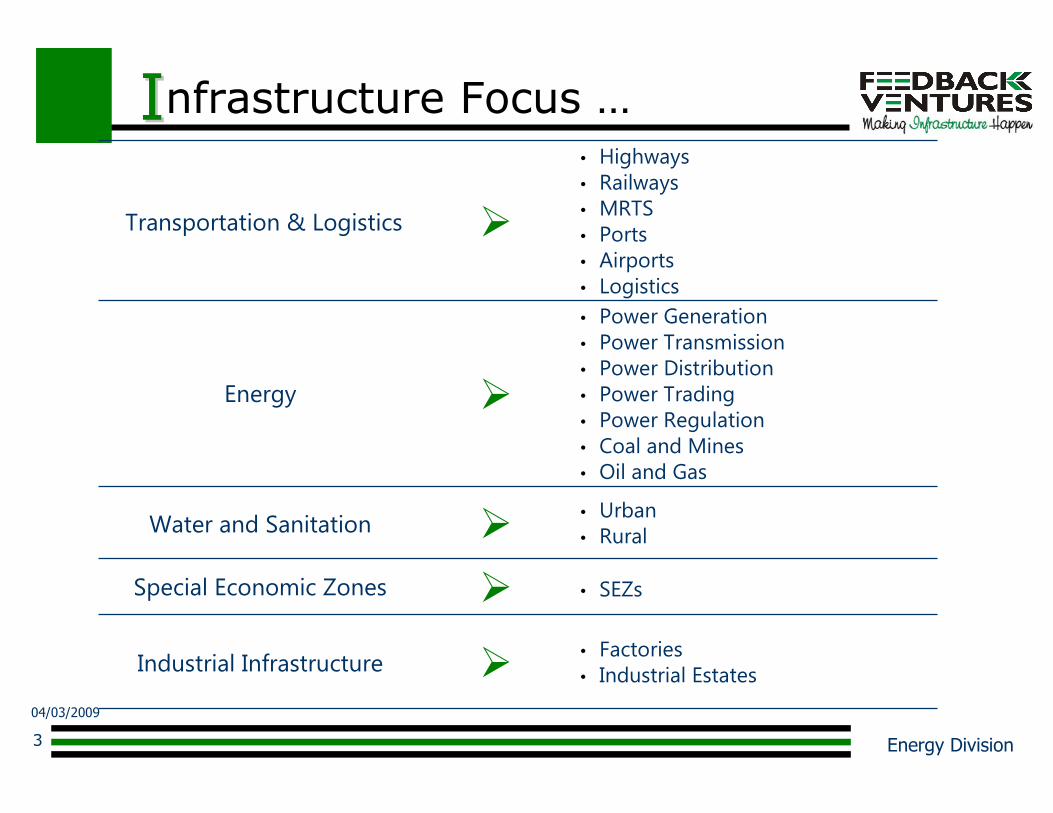

IInfrastructure Focus …

• SEZs�Special Economic Zones

�

�

�

�

• Factories• Industrial Estates

Industrial Infrastructure

• Urban• Rural

Water and Sanitation

• Power Generation• Power Transmission• Power Distribution• Power Trading• Power Regulation• Coal and Mines• Oil and Gas

Energy

• Highways• Railways• MRTS• Ports• Airports• Logistics

Transportation & Logistics

04/03/2009

Energy Division4

… IInfrastructure Focus

• Hospitals

• Primary Healthcare�Healthcare

• Urban Planning• Urban Infrastructure�Urban Development

• Shopping Malls

• Multiplexes�Retail & Entertainment

�

�

�

• Hotels

• Convention Centres

• Clubs

Hospitality

• IT Parks

• Corporate Offices

• Commercial Buildings

Commercial Infrastructure

• Housing

• TownshipsHousing & Townships

04/03/2009

04/03/2009

Energy Division5

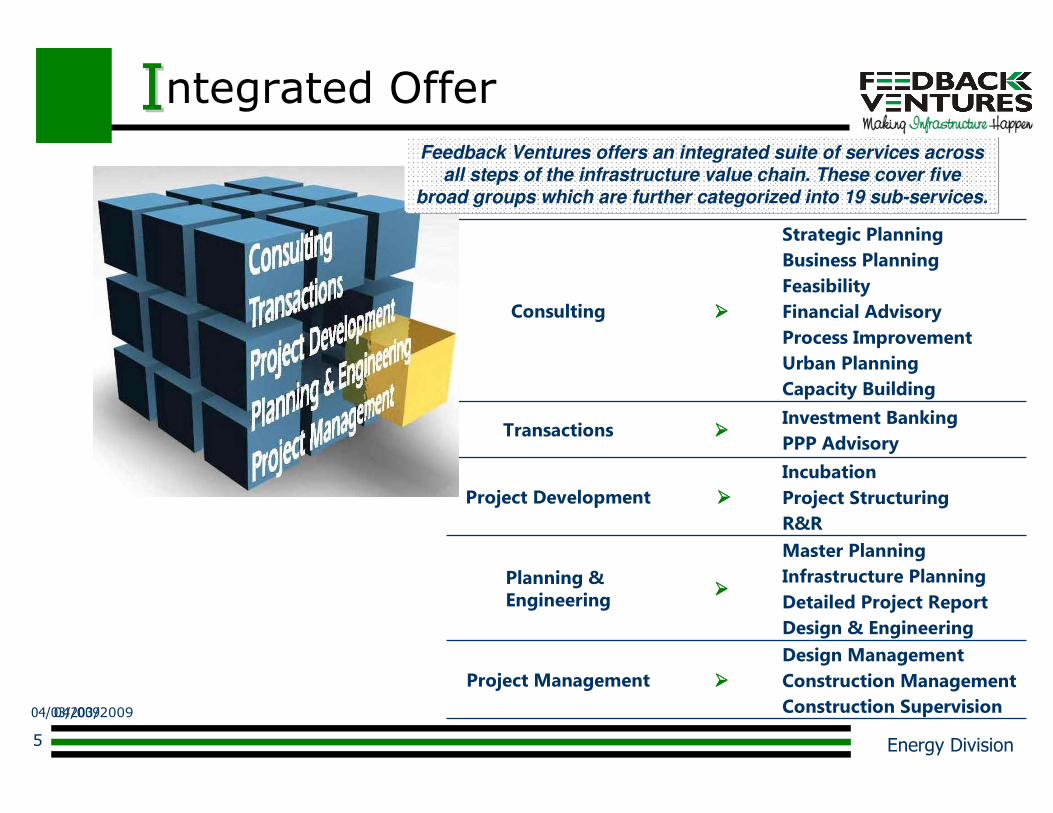

IIntegrated Offer

04/03/2009

Design Management

Construction Management

Construction Supervision

����Project Management

Incubation

Project Structuring

R&R

����Project Development

����

����

����

Master Planning

Infrastructure Planning

Detailed Project Report

Design & Engineering

Planning & Engineering

Investment Banking

PPP AdvisoryTransactions

Strategic Planning

Business Planning

Feasibility

Financial Advisory

Process Improvement

Urban Planning

Capacity Building

Consulting

Feedback Ventures offers an integrated suite of services across

all steps of the infrastructure value chain. These cover five

broad groups which are further categorized into 19 sub-services.

04/03/2009

Energy Division6

Energy

Sub-sectorsPower Generation

Power Transmission

Power Distribution

Power Trading

Power Regulation

Coal & Mines

Oil & Gas

Services we offer:Consulting

Transactions

Project Development

Planning and Engineering

Project Management

Some of our projects in this sector:Detailed design and project management of sub-stations for NDPL.

Undertaking generation and distribution due diligence for Private Equity firms.

Advisory services to the entire spectrum─from captive power plants to UMPPs.

Implementation of rural-based franchisee system for Uttarakhand Power Corporation.

Assisting leading states on reforms, regulations, process improvement and project based assignments.

Advising most leading developers on their power, coal and gas strategies and projects.

Distribution infrastructure planning for the Government of Maharashtra across 3 zones.

Empanelled by Min. of Power, PFC, USAID as Partner Training Institute under DRUM.

Feedback is supervising the construction of this new bridge over the Ganges at

Kanpur on NH-25.Feedback is working with the Gujarat

State Energy Corporation to develop fuel and procurement strategy.

26,000 MW of new capacity

Investment Opportunities in City Gas Distribution

04/03/2009

Energy Division8

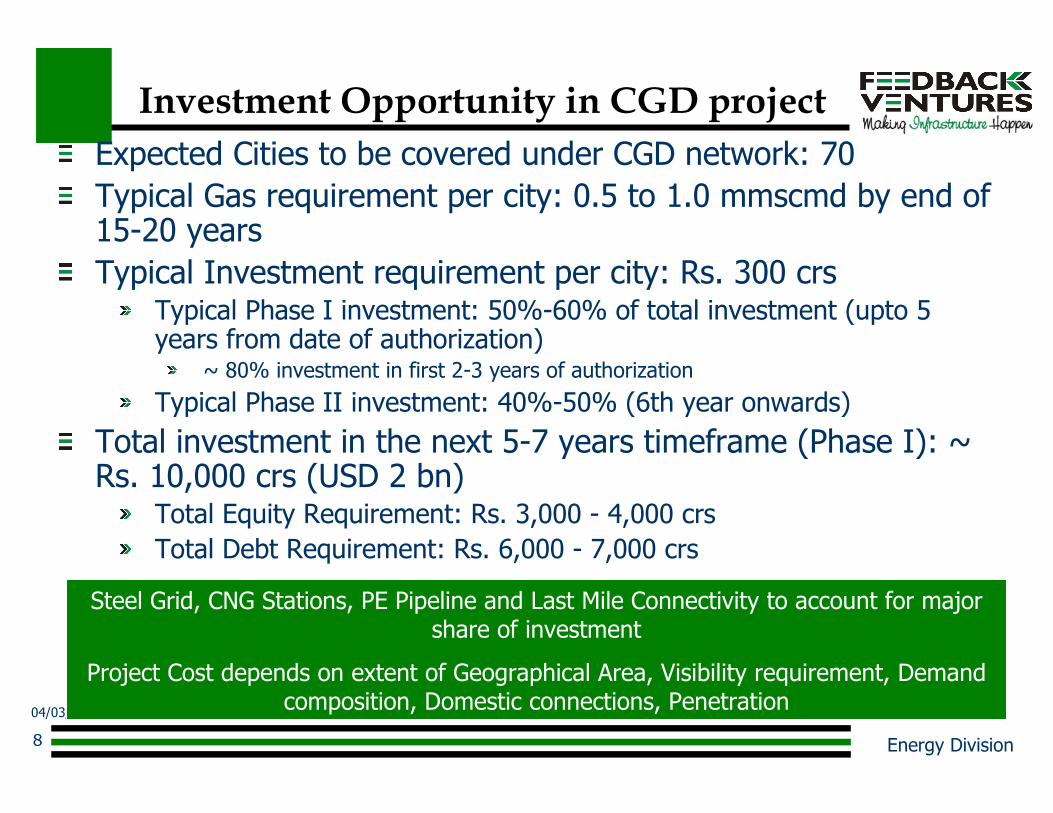

Investment Opportunity in CGD project

Expected Cities to be covered under CGD network: 70

Typical Gas requirement per city: 0.5 to 1.0 mmscmd by end of 15-20 years

Typical Investment requirement per city: Rs. 300 crsTypical Phase I investment: 50%-60% of total investment (upto 5 years from date of authorization)

~ 80% investment in first 2-3 years of authorization

Typical Phase II investment: 40%-50% (6th year onwards)

Total investment in the next 5-7 years timeframe (Phase I): ~ Rs. 10,000 crs (USD 2 bn)

Total Equity Requirement: Rs. 3,000 - 4,000 crs

Total Debt Requirement: Rs. 6,000 - 7,000 crs

Steel Grid, CNG Stations, PE Pipeline and Last Mile Connectivity to account for major share of investment

Project Cost depends on extent of Geographical Area, Visibility requirement, Demand composition, Domestic connections, Penetration

04/03/2009

Energy Division9

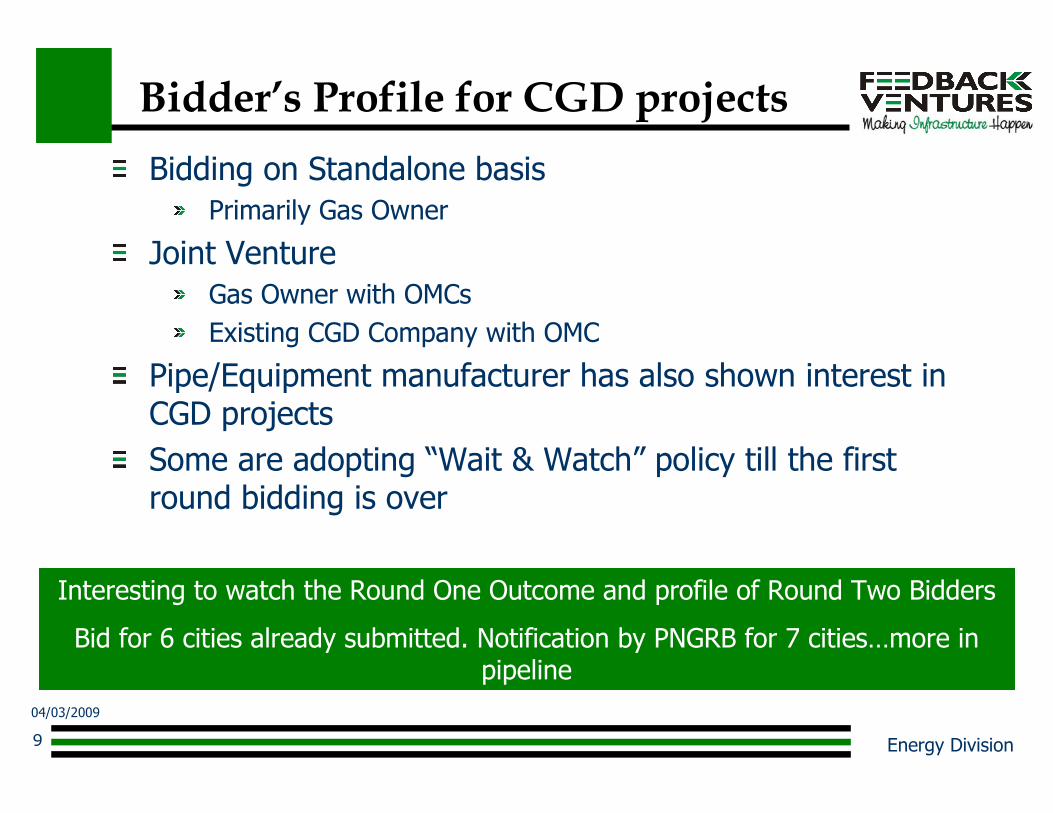

Bidder’s Profile for CGD projects

Bidding on Standalone basis

Primarily Gas Owner

Joint Venture

Gas Owner with OMCs

Existing CGD Company with OMC

Pipe/Equipment manufacturer has also shown interest in CGD projects

Some are adopting “Wait & Watch” policy till the first round bidding is over

Interesting to watch the Round One Outcome and profile of Round Two Bidders

Bid for 6 cities already submitted. Notification by PNGRB for 7 cities…more in pipeline

Economics & Financials Drivers

04/03/2009

Energy Division11

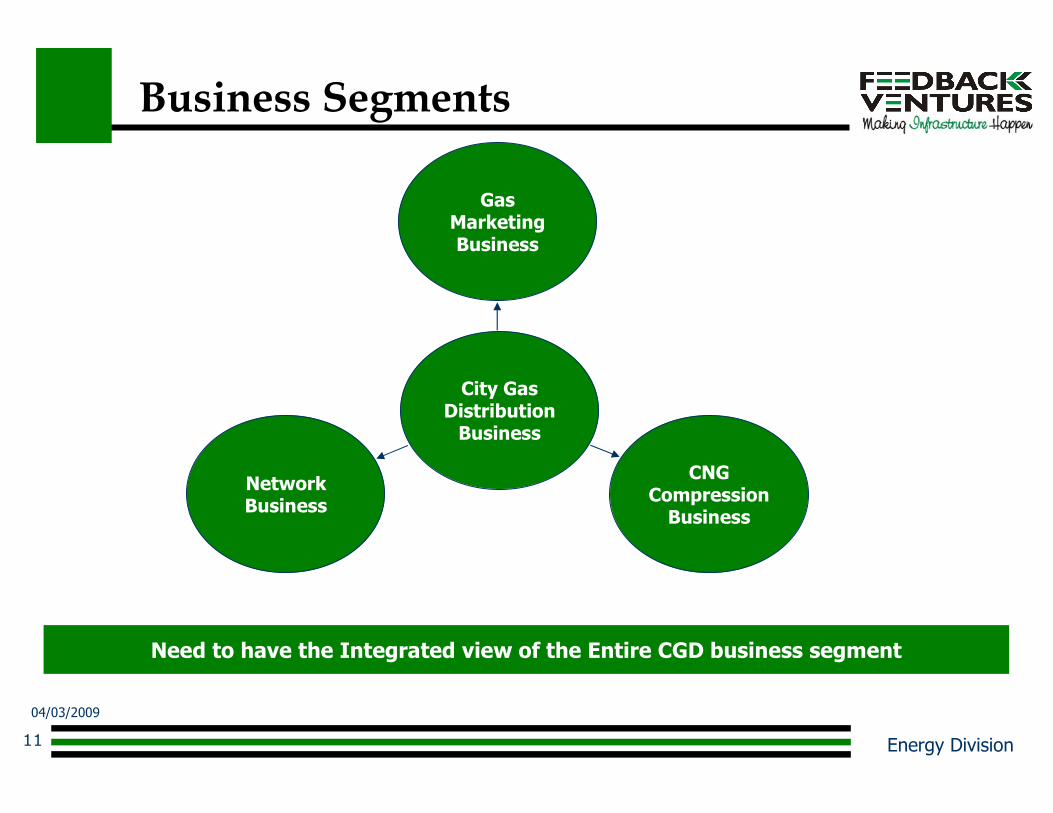

Business Segments

Network Business

CNG Compression

Business

Gas Marketing Business

City Gas Distribution

Business

Need to have the Integrated view of the Entire CGD business segment

04/03/2009

Energy Division12

Economic drivers(1)

CGD Projects

Network backbone

Lengthy gestation period

Significant capital outlays during initial years

Generally Break even in 4-5 years, depending upon the demand, consumer mix and geographical area

Need for

Fiscal incentives

Clarity of law

Stability of regime

Network exclusivity for the authorized CGD player

04/03/2009

Energy Division13

Economic drivers(2)

Transmission pipelines (Cross Country) enjoy a 10 year tax holiday (Section 80 IA) out of first 15 years of Commercial Operation date-Infrastructure status

However, MAT applicable – 11.33% of Book profits during tax holiday

CGD projects not yet included under Infrastructure projects

Infrastructure status important to ease access to External Commercial Borrowings

Development of CGD networks will require imported equipment

Imports liable to Customs duty-Increase Project Cost thus Tariff

Infrastructure status to CGD projects would positively impact the economics

04/03/2009

Energy Division14

Economic drivers(3)

Gas transmission projects eligible for project import status

Scope should also encompass CGD project – Clarity needed

Compression of Natural Gas for supply to CNG Stations is specified to be “manufacture” liable to excise duty

Eligible input credit should be available

Gas allocation

EGoM stipulated earmarking of 5 mmscmd for CGD projects for Domestic and CNG sale

CGD Company may need to procure gas for Industrial and Commercial consumer category from the open market

Whether gas quantity is sufficient

Principle of gas allocation not yet clear

Fiscal incentives are expected to entail earlier recouping of investment as well as increase the profitability

04/03/2009

Energy Division15

Factors impacting Profitability(1)

Sales realization in Rupees and Purchase Price of gas in USD

Financials highly sensitive to Gas input price, Gas Sales Price and demand penetration

Whether 100% pass through of increase in gas price possible

Fluctuation in the alternate fuel price

Fuel Category Unit

Price in

August

2008

Price in

February

2009

Price

Reduction

%

Domestic LPG Rs/ Kg 24 22 7%

Commercial LPG Rs/ Kg 61 41 33%

Furnace Oil Rs/ Ltr 32 16 50%

MS Rs/ Ltr 50 45 10%

Source: Industry

Sharp reduction in Alternate fuel price and Sharp Re. depreciation will substantially impact the CGD economics

Re depreciation

40.26

51.97

0

10

20

30

40

50

60

03.03.2008 03.03.2009

Rs/$

04/03/2009

Energy Division16

Factors impacting Profitability(2)

Regulated price of Domestic LPG as well as Motor Fuel

May require Industry and Commercial sales to Cross subsidize

Possibility of diversion of Domestic LPG Cylinders for commercial use post CGD implementation

Role of Regulatory Agency as well as OMC very critical

Adjacent city having price differential in gas prices due to APM gas supply and non–APM gas supply

Enabling Regulation/ Legislation on Clean Fuel use by the State Government

Need for Enabling Regulation and check on diversion of Domestic LPG

04/03/2009

Energy Division17

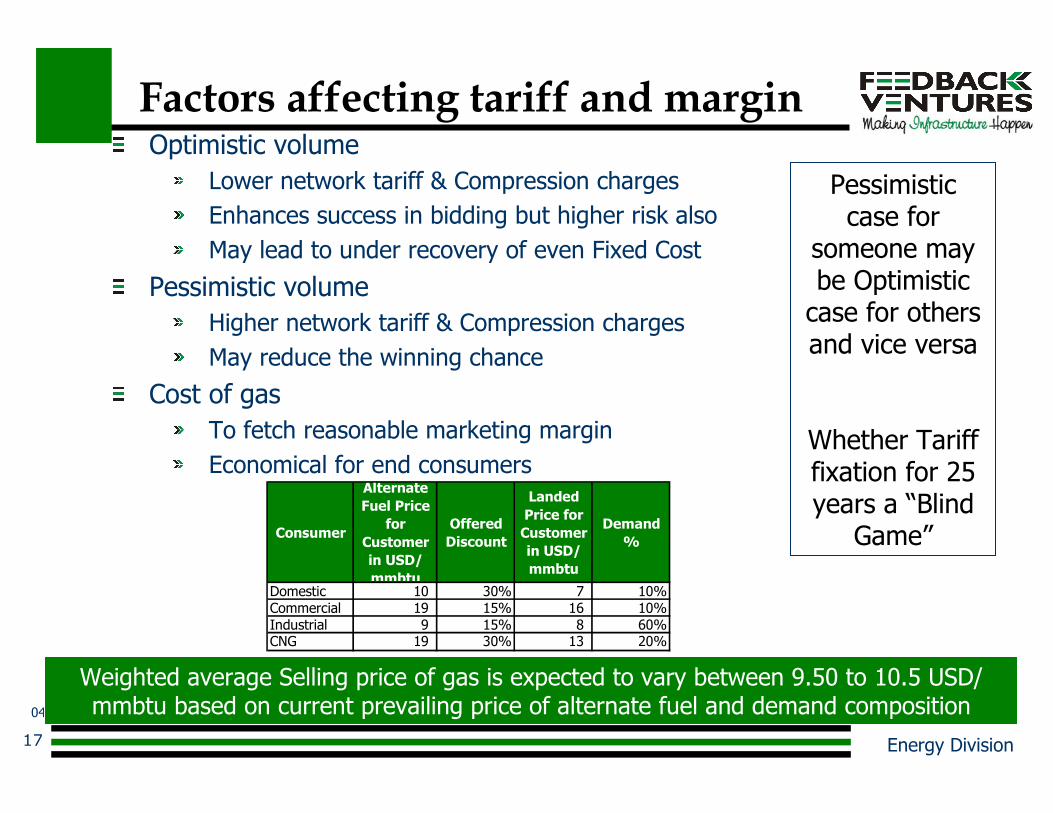

Factors affecting tariff and marginOptimistic volume

Lower network tariff & Compression charges

Enhances success in bidding but higher risk also

May lead to under recovery of even Fixed Cost

Pessimistic volume

Higher network tariff & Compression charges

May reduce the winning chance

Cost of gas

To fetch reasonable marketing margin

Economical for end consumers

Consumer

Alternate

Fuel Price

for

Customer

in USD/

mmbtu

Offered

Discount

Landed

Price for

Customer

in USD/

mmbtu

Demand

%

Domestic 10 30% 7 10%Commercial 19 15% 16 10%Industrial 9 15% 8 60%CNG 19 30% 13 20%

Weighted average Selling price of gas is expected to vary between 9.50 to 10.5 USD/ mmbtu based on current prevailing price of alternate fuel and demand composition

Pessimistic case for

someone may be Optimistic case for others and vice versa

Whether Tariff fixation for 25 years a “Blind

Game”

04/03/2009

Energy Division18

Possible development post authorization period

CNG: Low Competition as additional operating cost in Daughter – Booster Station

Domestic: Very low competition as Low volume and low profitability

Industrial/ CommercialProspect of high volume and high profitability

Sufficient incentive for 3rd Party to focus on such segment

Potential loss of large industrial consumers could also negatively accentuate load swings in the network making operations difficult

Territory having large industrial load are susceptible to more risk

Whether the “Open access” in the CGD business post exclusivity would have the same fete as happened in the Power Sector

Probability of Consolidation, Mergers & Acquisitions

CGD Project Financing

04/03/2009

Energy Division20

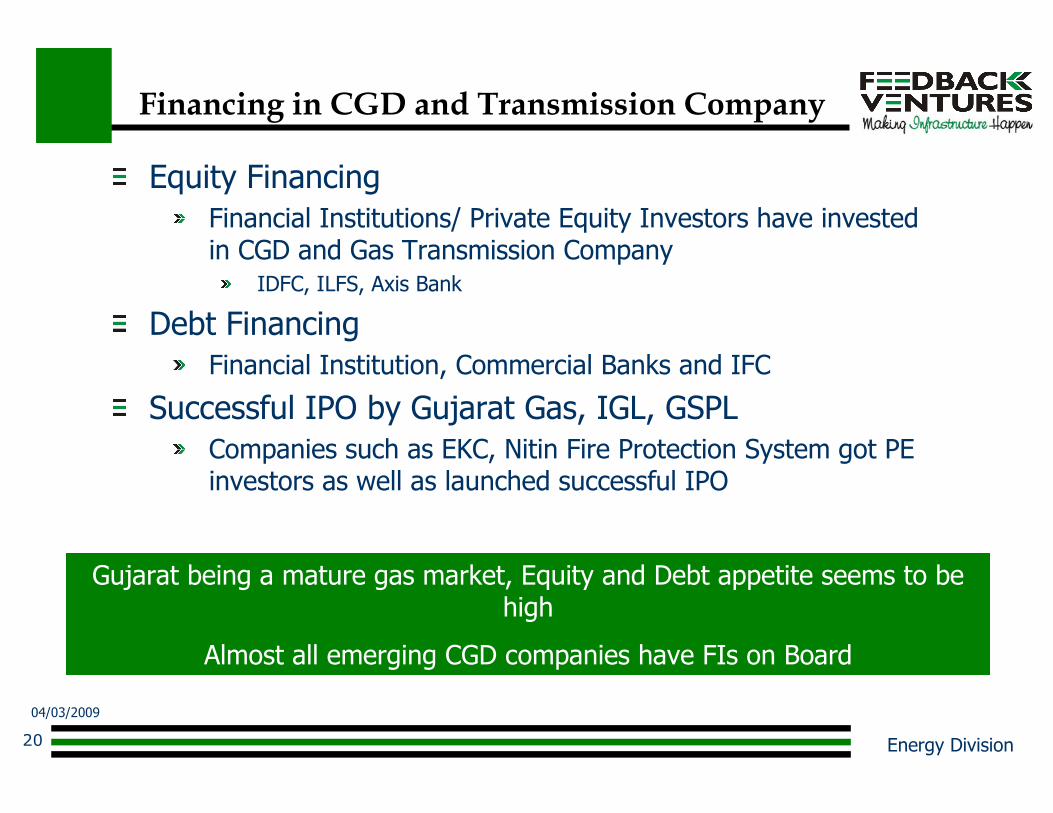

Financing in CGD and Transmission Company

Equity Financing

Financial Institutions/ Private Equity Investors have invested in CGD and Gas Transmission Company

IDFC, ILFS, Axis Bank

Debt Financing

Financial Institution, Commercial Banks and IFC

Successful IPO by Gujarat Gas, IGL, GSPL

Companies such as EKC, Nitin Fire Protection System got PE investors as well as launched successful IPO

Gujarat being a mature gas market, Equity and Debt appetite seems to be high

Almost all emerging CGD companies have FIs on Board

04/03/2009

Energy Division21

Financing parameters of matured CGD Companies

GGCL

Initial focus on industrial demand; currently increasing its presence in transport and domestic sector

Peak leverage : 1.3 (CY 1999) and Current leverage : ~ 0

IGL

Initial focus on high margin transport sector backed by regulatory support for conversion; Currently also focussing on domestic and industrial sector

Peak leverage : 0.4 (FY 2002) and Current leverage : ~ 0

MGL

Currently focused on building both transport and industry volumes

Current leverage ~ 0

Minimal additional Capex, typically being funded by Internal Accruals

04/03/2009

Energy Division22

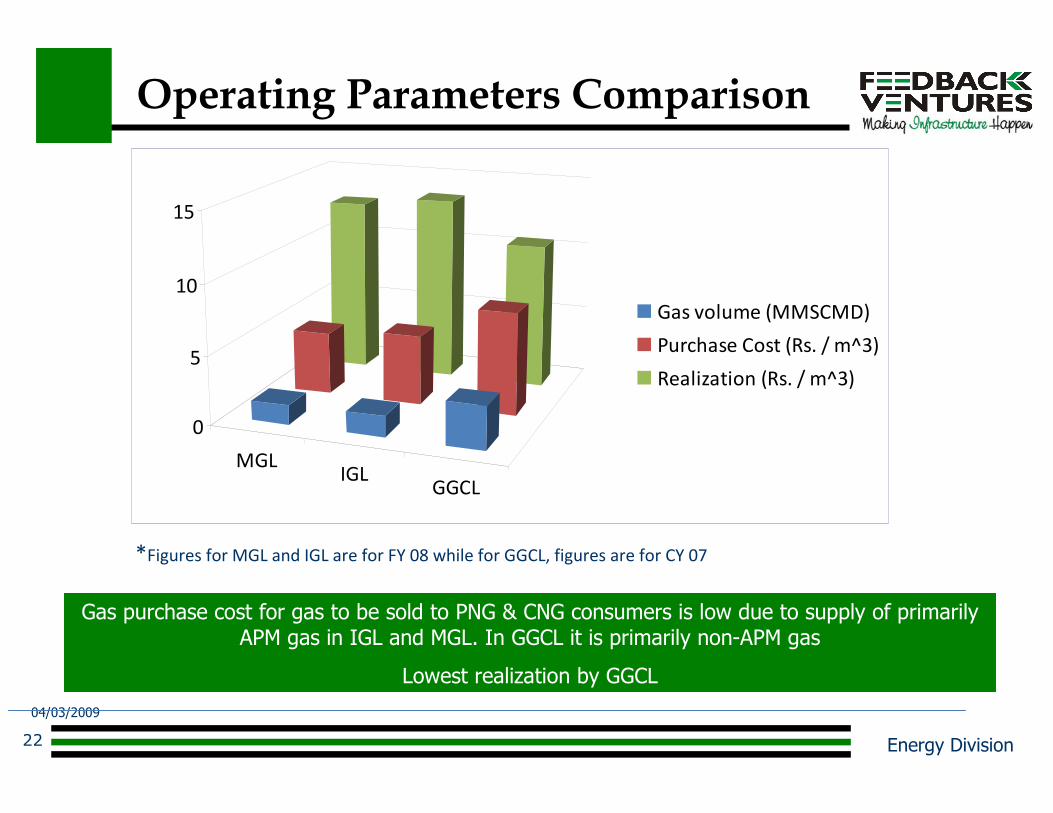

Operating Parameters Comparison

Gas purchase cost for gas to be sold to PNG & CNG consumers is low due to supply of primarily APM gas in IGL and MGL. In GGCL it is primarily non-APM gas

Lowest realization by GGCL

*Figures for MGL and IGL are for FY 08 while for GGCL, figures are for CY 07

MGLIGL

GGCL

0

5

10

15

Gas volume (MMSCMD)

Purchase Cost (Rs. / m^3)

Realization (Rs. / m^3)

04/03/2009

Energy Division23

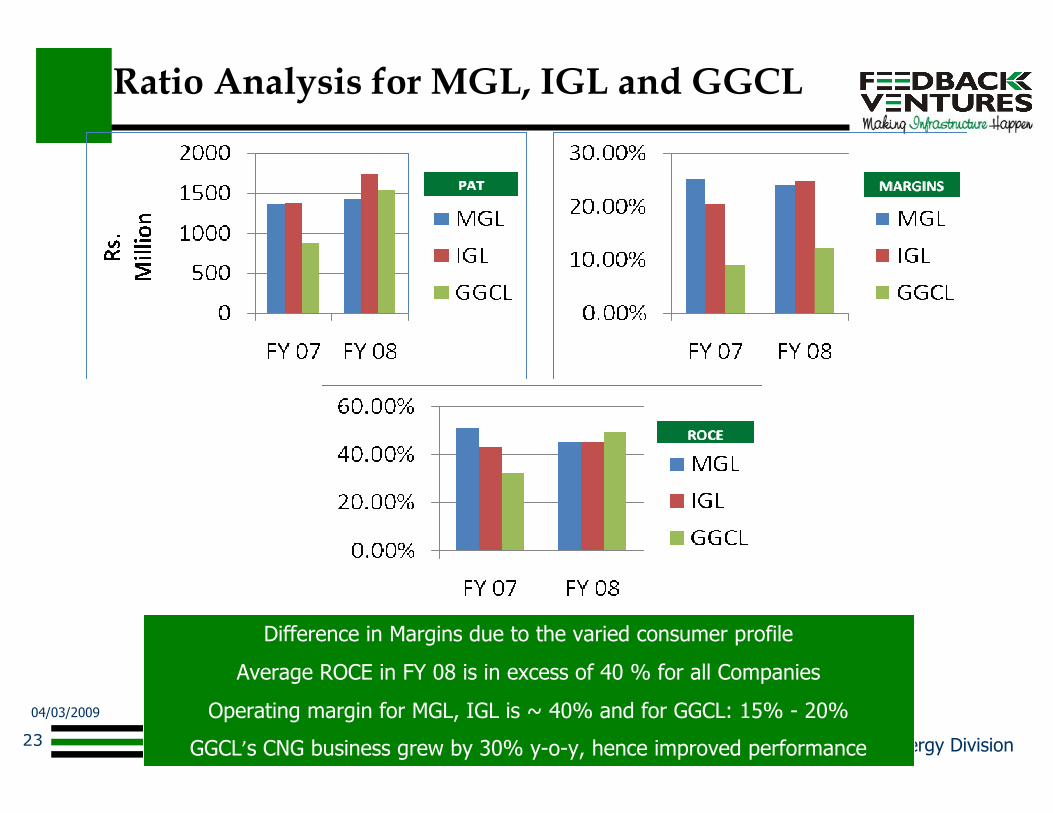

Ratio Analysis for MGL, IGL and GGCL

Difference in Margins due to the varied consumer profile

Average ROCE in FY 08 is in excess of 40 % for all Companies

Operating margin for MGL, IGL is ~ 40% and for GGCL: 15% - 20%

GGCL’s CNG business grew by 30% y-o-y, hence improved performance

04/03/2009

Energy Division24

Case Study- MNGL

Financial Closure is expected shortly

Equity Structure

GAIL (India) Limited : 22.5%

BPCL : 22.5%

Govt. of Maharashtra : 5%

IDFC PE : 20%, IL & FS : 20%, AXIS Bank : 10%

Total Project Cost : ~ Rs. 470 crs

Debt : Equity Ratio: 2.33:1

Expenditure made till February 2009: ~ Rs. 45 crs

Substantial stake holding by FIs shows their strong appetite for CGD projects

04/03/2009

Energy Division25

Case Study: Other Projects

FIs have generally been comfortable with the CGD Projects

Typical Peak Debt : Equity ratio is 2:1 to 2.33:1, Reduces overtime

Possibility of higher leveraging also exist

Gas cost is expected to constitute ~ 85-90% of the total expenditure

Company Leading

JV

Partner

With GAIL

Financial

Closure

Peak

Debt

Equity

Ratio

AGL HPCL GAIL:

22.50%

HPCL:

22.50%

Govt.: 5% Public/Fl:

50%

Under

process NA

BGL HPCL GAIL: 25% HPCL: 25% - Public/FI:

50%

Under

process

NA

CUGL BPCL GAIL:

22.50%

BPCL: 10% Govt.: 5% Public/FI:

50%

Accomplis

hed 2.3:1

GGL IOCL GAIL: 25% IOCL: 25% FI: 40% Individual:

10%

Under

process 2.0:1

MNGL BPCL GAIL:

22.50%

BPCL:

22.50%

Govt.: 5% Public/FI:

50%

Under

process 2.0:1

Present Equity structure

Source: IndiaInfrastructure

04/03/2009

Energy Division26

Typical Source of Funding

Equity

CGD Promoters

FIs

Strategic divestment

Private Equity Investors

Multilateral Funding Agencies (IFC, ADB)

IPO

Debt

FIs

Commercial Banks

Multilateral Funding Agencies

CGD Company not having gas supply security may divest stake to Gas owners (E&P Companies) post authorization

04/03/2009

Energy Division27

Typical Checklist for Financiers(1)

Authorization

Gas security and Purchase price

Business model

Ability to cross the Stress test specially with respect to gas purchase price, sales price and demand

Threshold Debt Service Coverage Ratio

Adequate Integrated Business IRR as well as Network and Compression Business IRR

Preparedness for demand penetration

Reasonable forecast on expansion of City/ New Industrial Zones

Lender’s due diligence is expected to be tighter for Non-Gas owners in the prevailing Regulatory domain

04/03/2009

Energy Division28

Typical Checklist for Financiers(2)

Adequate Capex capturing and Operating Cost estimate

Capability of the Project management/execution team

Relationship with the Local Government

Relationship with Vendors/ Suppliers

Status of RoU/RoW permission

Preparedness level for undertaking Retail business

How the market develops for the incumbent CGD player post authorization period

Interest rate expected to be ~ 12% with Door to Door Loan tenor of 6-9 years with 1 year moratorium

After Long Wait…Finally Bid Submission is Over

Over to

Authorization!

Financial Closure!!

Project Implementation!!!

Thanks…

India’s Leading Integrated Infrastructure Services Company

www.feedbackventures.com

Presenter

Rakesh Jain

Feedback Ventures, 3rd Floor

Central Plaza, Rajbhawan Road, Hyderabad

Tel: +91 40 23415085