financial & tax planning for airbnb hosts &...

TRANSCRIPT

Financial & Tax Planning for Airbnb Hosts & Landlords4 Easy Ways to Maximize Your Income and Simplify Your Taxes

A HURDLR QUICK GUIDE

© 2015 Hurdlr, Inc. All Rights Reserved.

2Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

As we’re sure you understand all too well, it’s not uncommon for Airbnb hosts and landlordssuch as yourself to let financial management fall by the wayside. You are constantly respond-ing to the needs of tenants and working on improving your rental or vacation property to be as accommodating as possible. Amongst all of these demands, figuring out how to do your ac-counting or learning your way around cumbersome financial software can seem like a daunting and overwhelming task. Certainly, it takes a lot of time to track expense deductions, and you may not be sure how to do the accounting yourself; the software you’re using may be compli-cated, and you may not have the time or energy to push through the learning curve. And even if you’re just keeping all of your receipts in a folder, or using Microsoft Excel or Google Docs as your primary tool for financial planning (we call that “Spreadsheet Accounting”), all of these take a significant amount of time and effort to maintain and stay organized, even for just a single property.

However, through proper financial planning takes time, it’s a crucial task for Airbnb hosts and landlords alike. Did you know that you could be saving a good deal of money by taking the ap-propriate deductions? But you’re busy – we get that. If you only had more time and energy to focus on your finances, you would.

That’s where Hurdlr comes in. We are here to help ease your number crunching anxieties. We have developed this guide in order to help hosts and landlords like you simplify your account-ing and save money, so when tax time comes around, you will be a little less overwhelmed by it all.

DID YOU KNOW?

Most Airbnb Hosts and Landlords don’t track all of their business expenses and related tax deductions, effectively lowering their profits.

We’ve put together some helpful tips to keep in mind when managing your finances. So let’s get started.

LET’S TALK FINANCES

3Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Always have separate credit card and bank accounts for “Business” and “Personal” finances.

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

Co-mingling your rental property and personal funds can be a recipe for disaster, even though landlords are technically allowed to do so. Whether you’re a landlord or a host, open up a separate checking account where you can deposit your rent proceeds or Airbnb, VRBO and HomeAway payments, pay your mortgage (or rent) from and cover the operating and maintenance expenses you incur on a day-to-day basis. Write yourself a check from your rental account to your personal account when you need money to cover personal expenses, go on vacation, or buy that new TV. By keeping your finances separate, it will be easier to see how well your rental property is doing, organize transaction records, file your taxes, and claim deductions for your rental expenses.

SEPARATE ACCOUNTS

4Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Don’t fall behind on your bookkeeping, or put off your accounting until tax time!

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

Make an effort to update your financial information on a regular basis. You will find it easier to remember the details of each transaction and save time and money when you need to file your tax return. If you’re into using the latest apps and technology, try downloading Hurdlr or Evernote on your smartphone to track your rental expenses. Hurdlr simplifies financial plan-ning for you completely. If you hate entering all of your information into some app, then take heart: with Hurdlr, you barely have to do any data entry at all. Simply sync your credit card and bank accounts with Hurdlr and the app pulls the transaction data for you. It’ll even pull your rental or Airbnb payments for you. Then, you’re set!

BOOKKEEPING

IRS Publication 583 is a great resource for sole proprietors and business owners to find more information on recordkeeping and tracking business expenses.

5Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Get to know your local taxes.

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

It is important to note that these taxes are usually remitted to your city, county or state on a monthly or quarterly basis and are in addition to your regular income taxes.

If you are an Airbnb host, and you live in a jurisdiction that imposes some type of occupancy tax, such as San Francisco, Airbnb typically handles the administration of this tax and deducts it from the payment they submit to you.

Regardless of whether you market your rental through Airbnb, VRBO, HomeAway or inde-pendently, you should visit your locality’s tax and revenue website to find out if you are re-quired to pay additional taxes on your short-term rental (that are not already administered by the rentals marketplace you may be using).

KNOW THE BASICS

DID YOU KNOW?

If you are renting your property on a short-term basis, your city or state may impose occupancy, lodging, use or hotel tax on your rental income.

Airbnb’s website is a great resource for additional information on occupancy taxes. Check out this article, as well as this one to get started.

6Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Understand your classifications

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

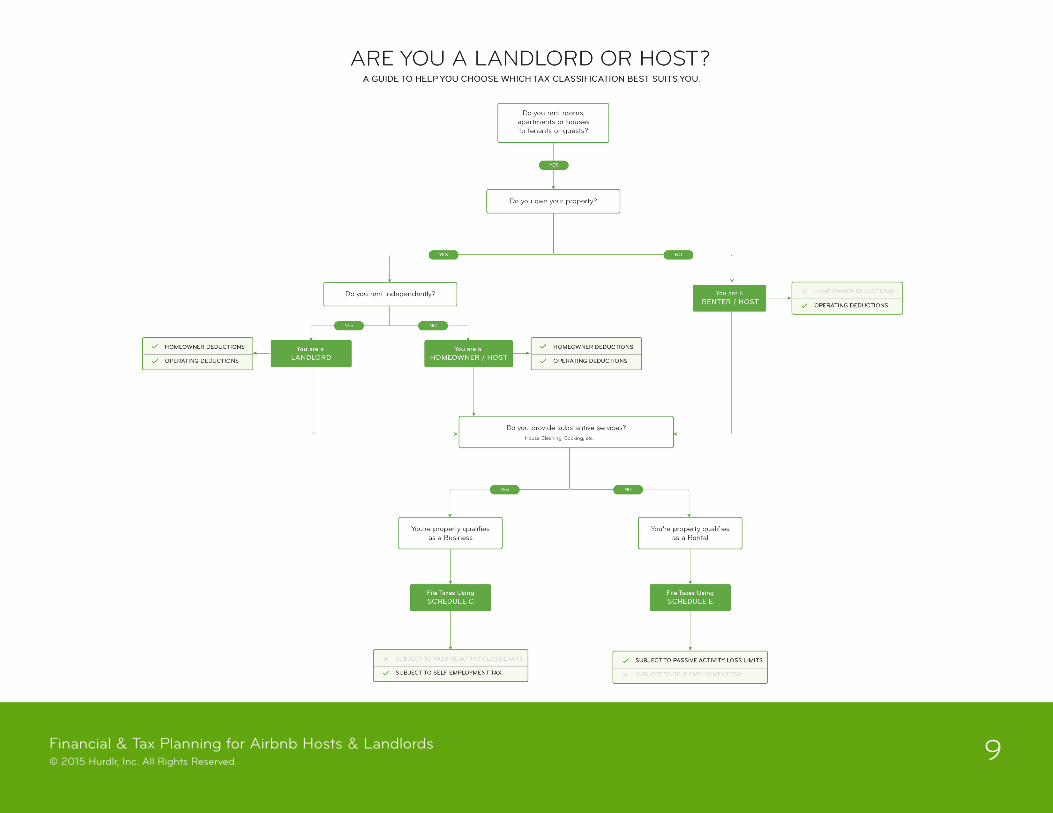

Unfortunately, being a landlord or host isn’t always easy. There are a number of different clas-sifications with which you need to familiarize yourself, so that when tax time rolls around, you’ll feel a little more prepared (and maybe a little less stressed out!).

Host vs. Landlord (Which One Are You?)Depending on what type of rental activity you are engaged in and how you rent your property, you could be considered either a host or a landlord. Here’s the difference:

Hosts typically rent their properties on a short-term basis through rental marketplace plat-forms like Airbnb. At the end of the year, hosts will receive a 1099-K from Airbnb, so they can properly report rental income on their tax return.

Landlords typically rent their properties on a long-term basis independently through web-sites like Craigslist or Zillow, or through a local real estate agent. Unless a landlord is rent-ing to a business, she most likely will not receive any type of 1099 to help her report rental income at the end of the year.

Regardless of whether you are a host receiving a 1099, or a landlord who has independently kept track of rental income throughout the year, it is important to remember that the payments you receive from your guests or tenants will not have any taxes withheld. You should plan on setting aside a portion of your rental income to cover any federal and state income taxes you may be subject to at the end of the year. Apps like Hurdlr can estimate your taxes for you and alert you when payments are due.

Security deposits are not considered rental revenue unless it is clear you will not be issuing a refund.

KNOW THE BASICS

7Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Understand your classifications

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

Rental vs. Business (Which One is It?)If you provide substantial services in conjunction with your property, you may be required to report your residential rental activity differently. How you classify your rental activity will have implications on what IRS schedules you file, what taxes you are subject to, and how much loss you are able to deduct.

If you rent rooms or apartments and provide basic services, you would normally report your rental income and expenses on Schedule E. You will be required to determine if you are subject to Passive Activity Loss Limitations (to be covered on following pages).

You can include multiple properties on one Schedule E (use columns A, B, C).

If you rent rooms or apartments and provide substantial services (maid service, regular cleaning, cooking, etc.), as a hotel or Bed and Breakfast would, you should report your rent-al income and expenses on Schedule C. You will not be subject to Passive Activity Loss Limitations.

You will be subject to self-employment tax on your rental income.

•

•

KNOW THE BASICS

•

•

8Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Understand your classifications

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

Rental vs. Business (Which One is It?) Cont.

For help understanding whether you’re a host or landlord or whether you should file as a business or rental, check out our flow diagram on the next page.

If you rent rooms or apartments through a partnership, S Corp., C Corp., or other busi-ness type, you will need to report your rental activities differently, such as on form 8825 or schedule 1065, 1120, 1120S, etc. Consult with your tax advisor on what filings will be most appropriate for you if you have an interest in a business that owns rental properties.

Generally, both Schedule E filers and Schedule C filers are subject to 1099 reporting re-quirements if they paid contractors or service providers over $600 during the year. Service providers may include plumbers, carpenters, lawyers, accountants, etc. Refer to IRS publi-cation 1099-Misc for additional details and reporting exceptions.

KNOW THE BASICS

Substantial services exclude providing basic utilities or cleaning of common areas. Refer to IRS publication 334 Real Estate Rents for details of what is considered to be a “sub-

stantial service.”

9Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

10Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Understand your classifications

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

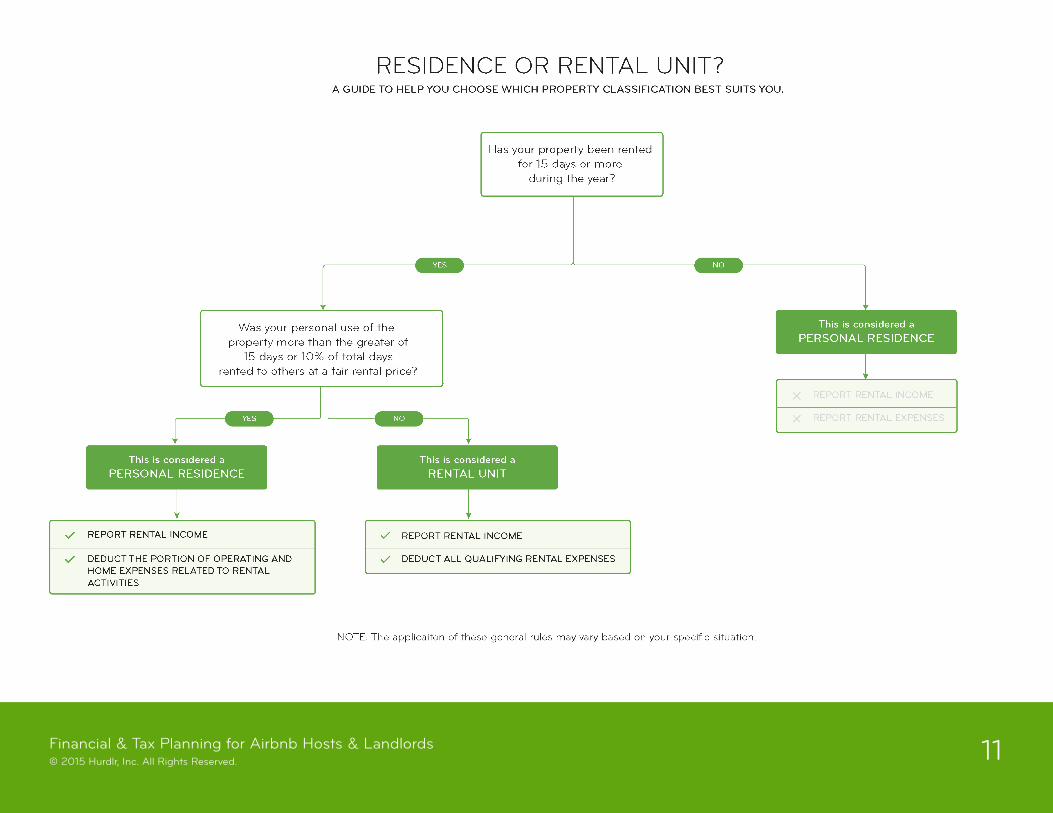

Personal Residence vs. Rental Property (Which One Is It?)

If you rent out your property or a room in your house for fewer than fifteen days during the year, then you do not need to report any rental income or deduct any rental expenses.

Your home or second property would be considered a rental unit if you use it for personal purposes for less than 15 days or 10% of the total days you rent it to others at a fair rental price.

If your property is considered a rental, you can deduct all qualifying expenses related to the rental property (generally subject to passive loss limitations). Your home or second property would be considered a personal residence if you use it for personal purposes for more than the greater of 15 days or 10% of the total days you rent it to others at a fair rental price.

If your property is considered a personal residence, you can deduct the portion of your home expenses directly related to your rental activities (generally subject to passive loss limitations) based on the number of days and how much of your property you rented.

Depending on how many days you use your rental property for personal use, the tax implications are different:

To help you determine which property type to choose see our diagram on the following page.

KNOW THE BASICS

Refer to IRS Topic 415 and Publication 527 for additional information and for the IRS definition of personal use.

•

•

11Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

12Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Understand your classifications

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

Active vs. Passive Involvement (Which One Is It?)

Passive involvement occurs when you own a real estate property, but you are not actively involved in the operation or management of it. Generally, rental property owners who leave substantially all decision making to a management company or real estate agent would be considered passive. Short-term rentals (whether in your personal residence or dedicated rental) are almost always considered to be passive.

Losses from passively managed properties are limited to passive income. In other words, your rental deductions cannot exceed your rental income.

Active involvement occurs when you participate in managing your rental property, including but not limited to making repairs and maintenance decisions, drafting rental terms, ap-proving tenants, etc. Generally, you will need to manage your rental yourself on a long-term basis to be considered active.

Losses from actively managed properties can total $25,000, regardless of how much income or lack there of a property generates.

Active involvement is almost always better than passive involvement.

Passive Activity Loss Limitations will apply to hosts and landlords whose property is deemed to be a rental based on the “Rental or Business” diagram. If you are subject to passive activity loss limitations, your deductions will be limited depending on how involved you are in operating and managing your rental property.

KNOW THE BASICS

If you are subject to passive loss limitations, use Form 8582 to calculate your loss limitation for the year.

•

•

13Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Understand your classifications

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

For the full list of material participation tests, refer to the IRS website. However, if you are a real estate professional, and you can answer yes to any one of the three questions below, you would pass the material participation test:

You work at least 500 hours during the year managing your short-term rental. You work at least 100 hours during the year managing your short-term rental, and nobody works more than you. You do substantially all the work in the activity.

Active vs. passive involvement is a complex topic. Our explanations are only high-level summaries, and actual practice may differ from our explanations – there is just too much to cover. Your tax preparer will be able to clarify the distinctions for you specifically.

KNOW THE BASICS

•

•

•

Exceptions - For a full list of exceptions to the passive loss limitations rules, refer to the IRS website. However, in summary, if you rent your property on a short-term basis (average period of customer use is seven days or less, or the average period of customer use is 30 days or less and significant personal services are provided), your participation will be considered passive regardless of whether you materially participate in managing your property, unless you are a real estate professional (refer to the IRS for the exact definition). If you are a real estate profes-sional, your short-term rentals can qualify for active participation if you materially participate in managing the property.

14Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Deductions, deductions, deductions!

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

DEDUCTIONS

There are a number of deductions available for hosts and landlords, regardless of your proper-ty’s classification or your participation status.

Your accountant or tax software will likely only require summary level information related to your rental revenues and expenses. However, note that you should keep receipts and support-ing documents for all deductions you take, so you have them if you are selected for an audit. See IRS publication 583 for detailed information on recordkeeping and tracking expenses.

Operating Expenses (for Subleasors/Hosts & Homeowners)The following deductions are applicable for everyone engaged in rental activities and are de-ductible to the extent outlined in the prior sections. Please note that this list is only a summa-ry of possible operating expenses.

Utilities

Insurance

Food for Guests

Management Fees

Commissions Paid to Agents

Marketing and Listing Fees

Condo, HOA Fees

Cleaning and Trash Removal

15Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Maintenance and Repairs You can deduct any expenses you incur to make sure that your property is in working order. These expenses can include parts and labor and may include things like plumbing, electrical, HVAC, etc. Maintenance and repairs can be easily confused with improvements. Typically, improvements add value to your property or prolong its useful life, while repairs simply replace something damaged with an item of equal or lesser value and are expensed.

Credit and Background Checks

For Landlords, checking a potential guest’s or tenant’s credit history can be a good way to make sure you are finding the right tenant to occupy your rental. These costs are fully deductible.

Deductions, deductions, deductions!

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

DEDUCTIONS

Operating Expenses (cont.)

•

•

•

Since conducting credit checks are a best practice, here are a few helpful links:

www.Experian.com, www.Equifax.com, www.Transunion.com

16Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Professional Fees Expenses you incur drafting your lease agreement, reviewing vendor contracts, consulting your accountant regarding your rental property, etc. are all deductible.

Business Mileage

Use Hurdlr’s mileage tracker to keep track of miles you drive checking in on your property, buying supplies, meeting tenants, etc.

Deductions, deductions, deductions!

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

DEDUCTIONS

Operating Expenses (cont.)

•

•

Mortgage Interest*

Rent

For Subleasors/Hosts Only (who do not own the property they rent out)

For Homeowner’s Only Unlike the operating deductions mentioned above, there are certain deductions that will only be applicable if you are a host or landlord who owns your property. The following expenses are deductible to the extent outlined in the prior section. Please note that this is only a summary of possible homeowner deductions and that your ability to deduct the expenses below may be limited based on numerous criteria defined by the IRS.

Real Estate Taxes*

17Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Private Mortgage Insurance (PMI)* For homeowners who put down less than 20%, PMI will likely be required to protect your lender in the event you default. While PMI sounds scary the good news is that it is fully deductible.

Depreciation You can deduct the cost of the portion of your property used for rental activities through depreciation. There are a few different ways you can depreciate your property, the main difference being how you spread the depreciation expense out over your rental property’s useful life. Depreciation is a complex topic, so discuss it with your tax preparer, but know that it can generate significant tax savings for you.

You are not eligible to depreciate a property you lease or rent.

Deductions, deductions, deductions!

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

DEDUCTIONS

For Homeowner’s Only (cont.)

*Portion related to rental will be on Schedule E; portion related to personal will be on Schedule A.

•

•

For more information on mortgage interest and PMI deductions, click here.

18Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Deductions, deductions, deductions!

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

DEDUCTIONS

NOTE: The deductions outlined here are only a partial list. The amount you can take for each deduction will depend on how many days you rent your property and how much of your property you rent. Deduction amounts may also be limited by a number of specific IRS rules that may apply to your specific situation.

HOMEOWNER HOST

UTILITIES

INSURANCE

FOOD FOR GUESTS

MANAGEMENT FEES

COMMISSIONS

MARKETING / LISTING FEES

CONDO / HOA FEES

CLEANING AND TRASH REMOVAL

MAINTENANCE AND REPAIRS

CREDIT / BACKGROUND CHECKS

LEGAL / PROFESSIONAL FEES

MORTGAGE INTEREST

REAL ESTATE TAXES

PRIVATE MORTGAGE INSURANCE

DEPRECIATION

UTILITIES

INSURANCE

FOOD FOR GUESTS

MANAGEMENT FEES

COMMISSIONS

MARKETING / LISTING FEES

CONDO / HOA FEES

CLEANING AND TRASH REMOVAL

MAINTENANCE AND REPAIRS

CREDIT / BACKGROUND CHECKS

LEGAL / PROFESSIONAL FEES

MORTGAGE INTEREST

REAL ESTATE TAXES

PRIVATE MORTGAGE INSURANCE

DEPRECIATION

Deductions Summary

19Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Your tax prep checklist.

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

Now that we’ve instructed you on the main points to keep in mind when tending to your fi-nances, we have also prepared a general checklist that you can use at tax time to be sure you are thinking of the right rental-related information to input into your tax software or provide to your tax preparer.

Calculate the number of days each month that you used your property for personal use and for rental use. This will determine the tax treatment of your rental and help you calculate your deductions.

Add up your total operating costs (utilities, insurance, food for guests, etc.) you incurred each month during the year so you can calculate your deductions. If you took our advice on keeping information in real time, this should already be done!

If you own your home, add up your total “homeowner” costs (mortgage interest, real estate tax-es, etc.) you incurred each month during the year so you can calculate your rental deductions. If available, use supporting documents like the 1098 you received from your mortgage lender to make this step a breeze.

Tally your assets. To the extent not detailed on your balance sheet, compile a list of the im-provements you made to your rental property during the year, and make sure to include the price of improvements and dates put in use.

Gather your property information (address, type). Make sure you have the information about your property that you will need if you are required to complete Schedule E, including the physical address of each property you rent and the property type (single family residence, multi-family residence, short-term rental, etc.) of each rental.

BONUS

20Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

Your tax prep checklist.

SEPARATE ACCOUNTS

BOOKKEEPING

KNOW THE BASICS

DEDUCTIONS

BONUS

For a complete checklist of what you will need to complete your individual tax return, refer to your local CPA, H&R Block or tax software for guidance.

Renting is a complex topic. Our explanations are only high-level summaries, and actual practice may differ from our explanations – there is just too much to cover. Your tax preparer will be able to clarify the distinctions for you specifically.

BONUS

Hold on to that 1099 from Airbnb (or VRBO, HomeAway); you’ll need it so you know how much income to report on your Schedule C or Schedule E.

Export key statements. If you use accounting software to track your rental revenues and ex-penses, export your profit and loss statement and trial balance to excel or directly into your tax software. This information will also be used to populate your Schedule C or Schedule E. With an app like Hurdlr, a few taps on your smart-phone will generate these.

Get Hurdlr. Wouldn’t it be great if there was an app that simplified this for you? There is - it’s called Hurdlr, and it allows you to easily track and manage your finances from anywhere, any-time on your phone.

21Financial & Tax Planning for Airbnb Hosts & Landlords© 2015 Hurdlr, Inc. All Rights Reserved.

We hope that we’ve provided you with some helpful tips that will allow you to maximize your profits and streamline your ac-counting. By abiding by these tips and utilizing our checklist, you will find that your financial and tax planning will be infinitely more simple - and infinitely less stressful! If you have any questions about how Hurdlr can help ease your numbercrunching

anxieties, email us at [email protected]

To learn more about how Hurdlr can help hosts and landlords like you, visit our website: www.hurdlr.com/airbnb

Matt Briefer, CPA is Hurdlr’s Accountant-in-Residence (AIR) and shares Hurdlr’s passion for serving fellow entrepreneurs. Matt holds a Master of Ac-countancy from the George Washington University and previously worked at PricewaterhouseCoopers.

Hurdlr is a mobile-first app for busy entrepreneurs to seamlessly manage their business expenses, finances and tax planning in seconds, from their smartphones. Hurdlr for Airbnb Hosts and Landlords also helps you track your rental specific expenses and income from tenants and Airbnb

(VRBO, HomeAway, etc.) so you have a clear financial picture of your true income and can plan for your future.

“We designed and built Hurdlr with the entrepreneur in mind. We believe accounting should only take seconds...not days, hours or even minutes. It should help you grow your income, not increase your expenses.”

Disclaimer:The information contained in this article is provided for informational purposes only and should not be construed as financial or tax advice. It is not

intended to be a substitute for obtaining accounting or other financial advice from an appropriate financial advisor or for the purpose of avoiding U.S. Federal, state or local tax payments and penalties.

-Raj Bhaskar, Founder & CEO, Hurdlr

About The Author

About Hurdlr