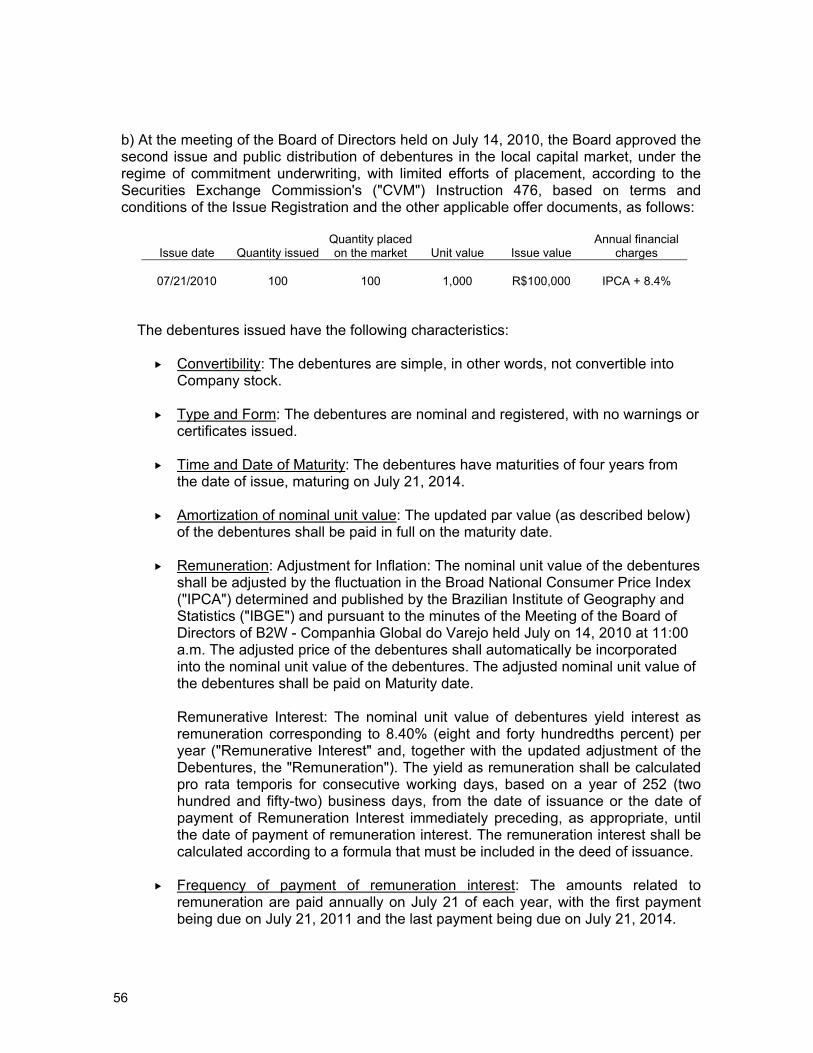

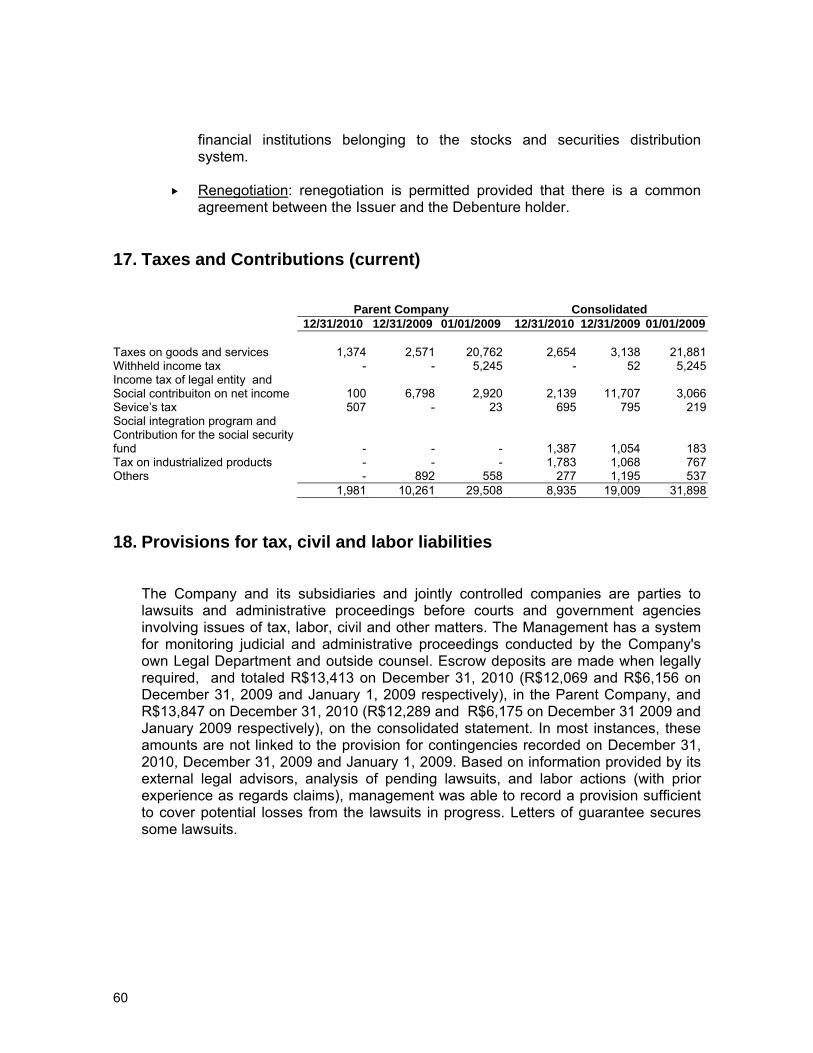

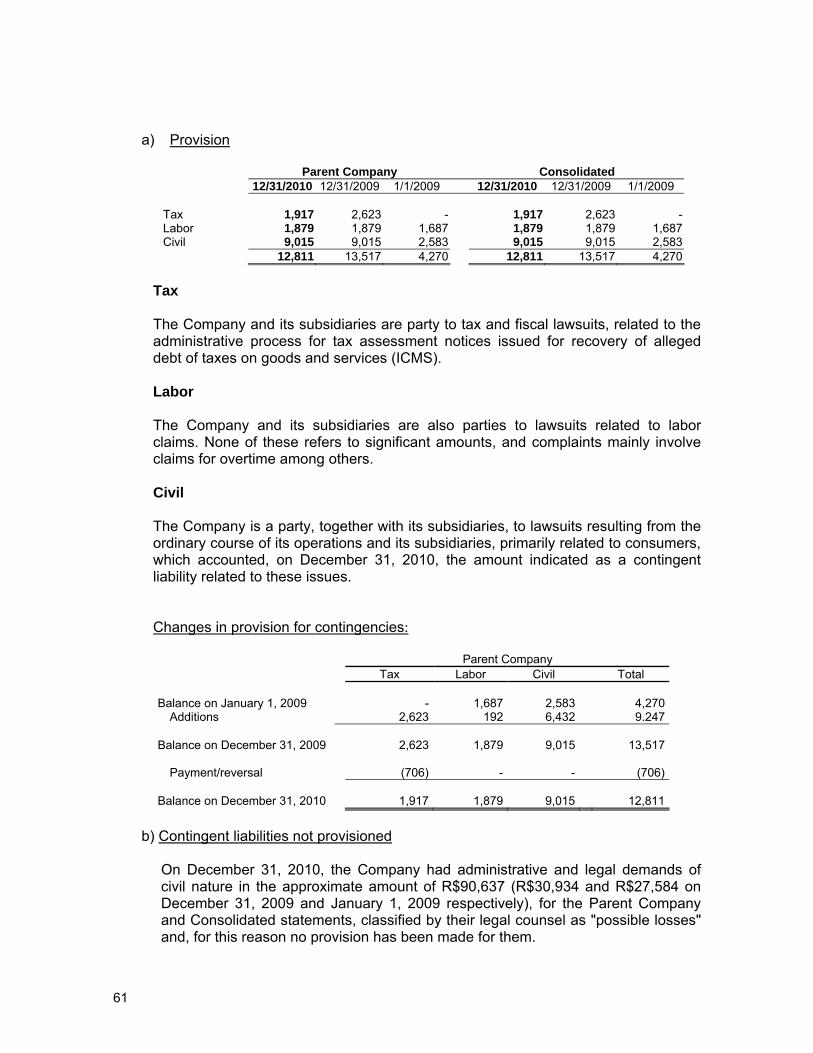

financial statements b2w companhia global do varejo · financial statements b2w companhia global do...

TRANSCRIPT

Financial Statements

B2W Companhia Global do Varejo December 31 2010 and 2009 with Report of the Independent Auditors

B2W COMPANHIA GLOBAL DO VAREJO Financial Statements

December 31 2010 and 2009 Index Report of independent auditors ............................................................................................1 Audited financial statement Balance sheets ....................................................................................................................4 Financial statements............................................................................................................6 Statements of chages in Shareholder’s equity ...................................................................7 Cash flow statements ..........................................................................................................9 Statements of valeu added................................................................................................10 Explanatory notes to the financial statements ...................................................................11

4

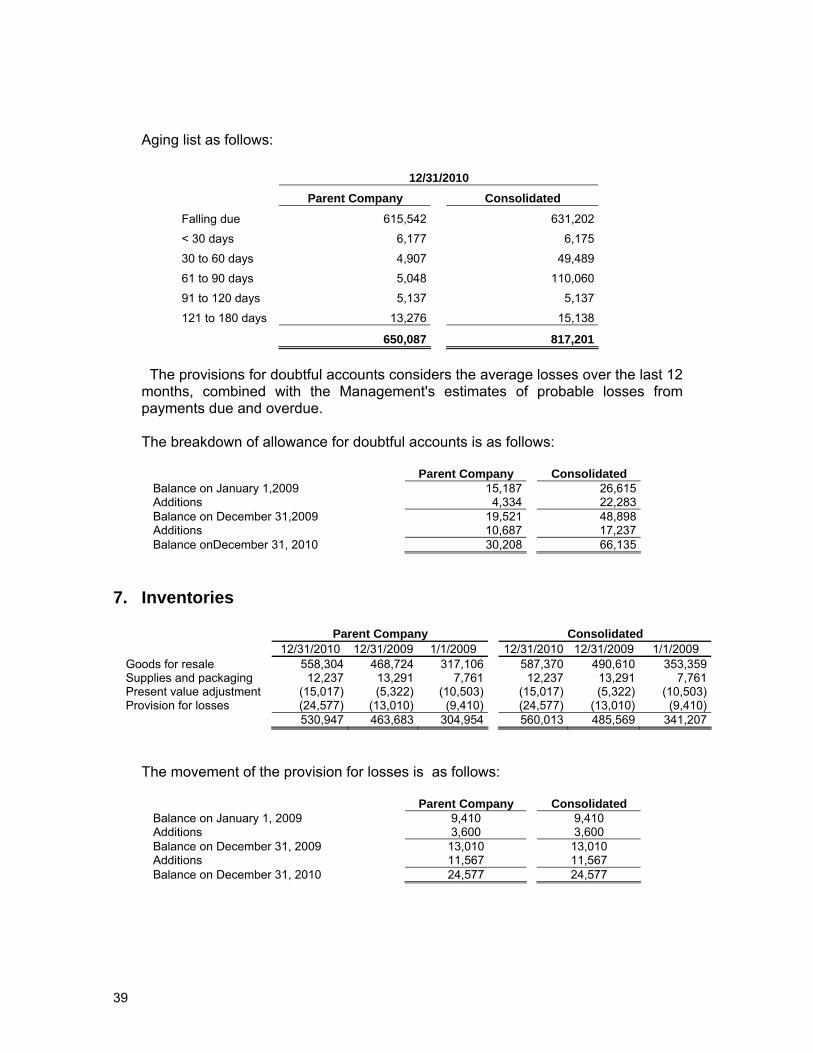

B2W COMPANHIA GLOBAL DO VAREJO Balance Sheets Raised on December 31, 2010 and 2009 (In thousand reais) Parent Company Consolidated Note 12.31.2010 12.31.2009 01.01.2009 12.31.2010 12.31.2009 01.01.2009 Assets Current assets Cash and cash equivalents 7,288 56,974 26,673 15,283 62,047 37,324 Marketable securities 5 776,973 540,010 701,006 790,707 547,832 704,569

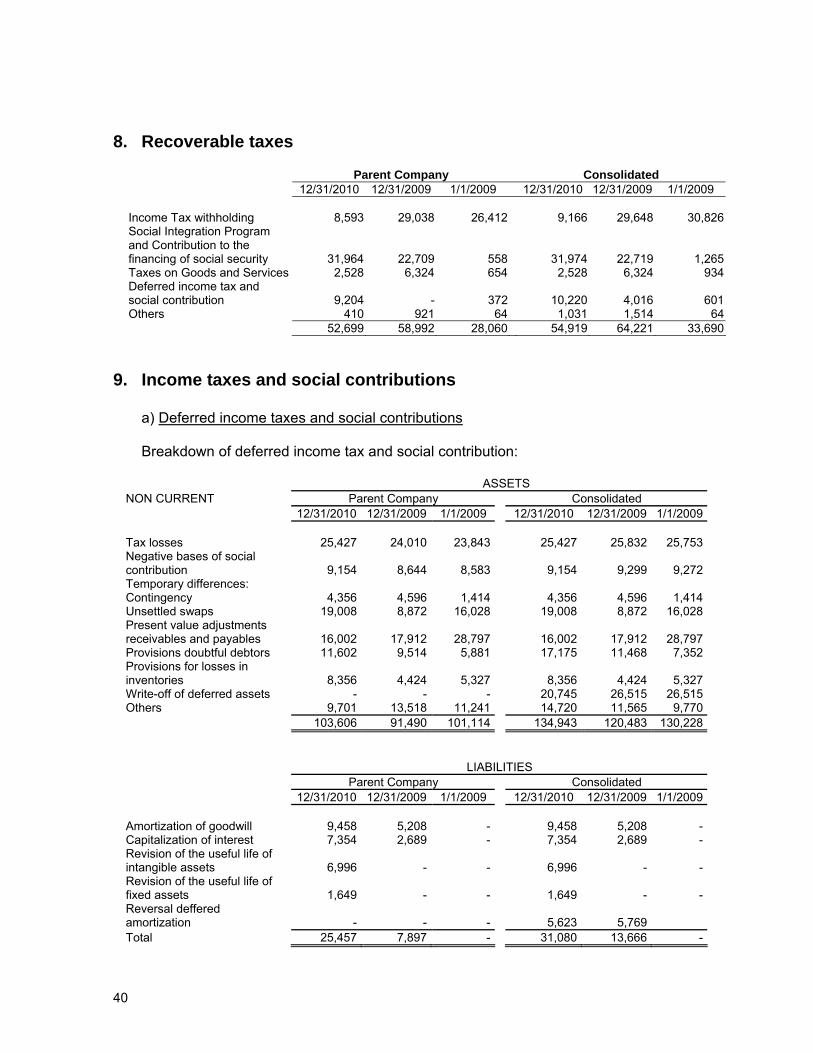

Customers accounts receivables 6 650,087 272,265 346,826 817,201 424,287 554,160 Inventories 7 530,947 463,683 304,954 560,013 485,569 341,207 Recoverable taxes 8 52,699 58,992 28,060 54,919 64,221 33,690 Prepaid expenses 17,813 12,394 25,052 18,783 13,862 25,060 Other accounts receivable 59,984 45,862 63,600 67,391 48,615 68,366

Total current assets 2,095,791 1,450,180 1,496,171 2,324,297 1,646,433 1,764,376 Non current assets Long-term assets

Deferred income and social contribution taxes 9 103,606 91,490 101,114 134,943 120,483 130,228

Escrow deposits 18 13,413 12,069 6,156 13,847 12,289 6,175 Related parties 11 45,614 45,794 31,112 19,361 33,744 22,451 Other accounts receivable - 3,833 4,999 1,051 5,319 6,321

Investments 10 40,772 29,970 22,303 - - - Fixed assets 12 122,471 88,011 75,316 131,949 92,826 76,663 Intangible 13 568,433 381,093 299,227 586,566 392,842 306,388 Deferred charges 14 44,030 60,419 77,350 - - -

Total non current assets 938,339 712,679 617,577 887,717 657,503 548,226 Total assets 3,034,130 2,162,859 2,113,748 3,212,014 2,303,936 2,312,602

5

Parent Company Consolidated Note 12.31.2010 12.31.2009 01.01.2009 12.31.2010 12.31.2009 01.01.2009

Liabilities and Stockholders’ equity Current liabilities

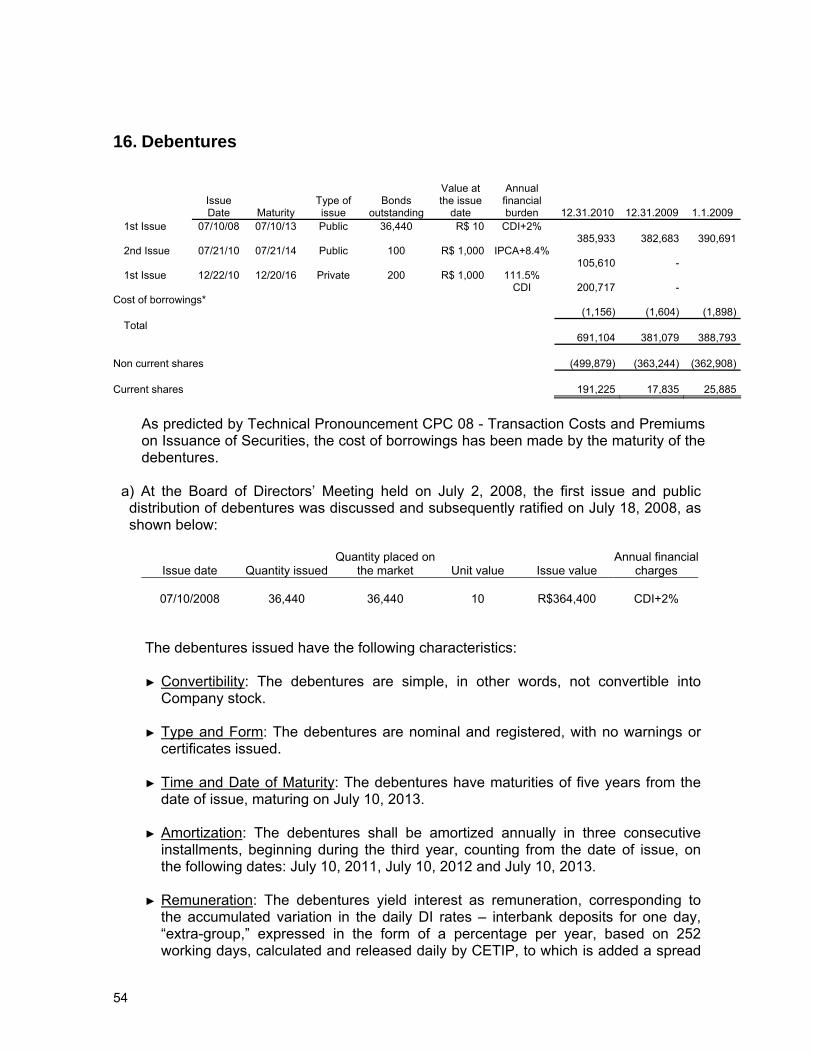

Suppliers 768,436 568,242 575,732 794,052 580,933 583,795 Loans and financing 15 199,929 182,491 592,311 351,888 327,929 808,878 Debentures 16 191,225 17,835 25,885 191,225 17,835 25,885 Wages, provisions and social

contributions 9,229 6,278 6,295 11,520 8,240 8,737 Recoverable taxes 17 1,981 10,261 29,508 8,935 19,009 31,898 Proposed dividends 5,383 11,308 18,012 5,383 11,308 18,012 Other liabilities 25,380 28,952 25,214 37,285 35,694 46,075

Total current liabilities 1,201,563 825,367 1,272,957 1,400,288 1,000,948 1,523,280 Non current liabilities Long term liabilities

Loans and financing 15 1,032,444 710,181 272,774 1,035,337 710,181 272,774 Debentures 16 499,879 363,244 362,908 499,879 363,244 362,908

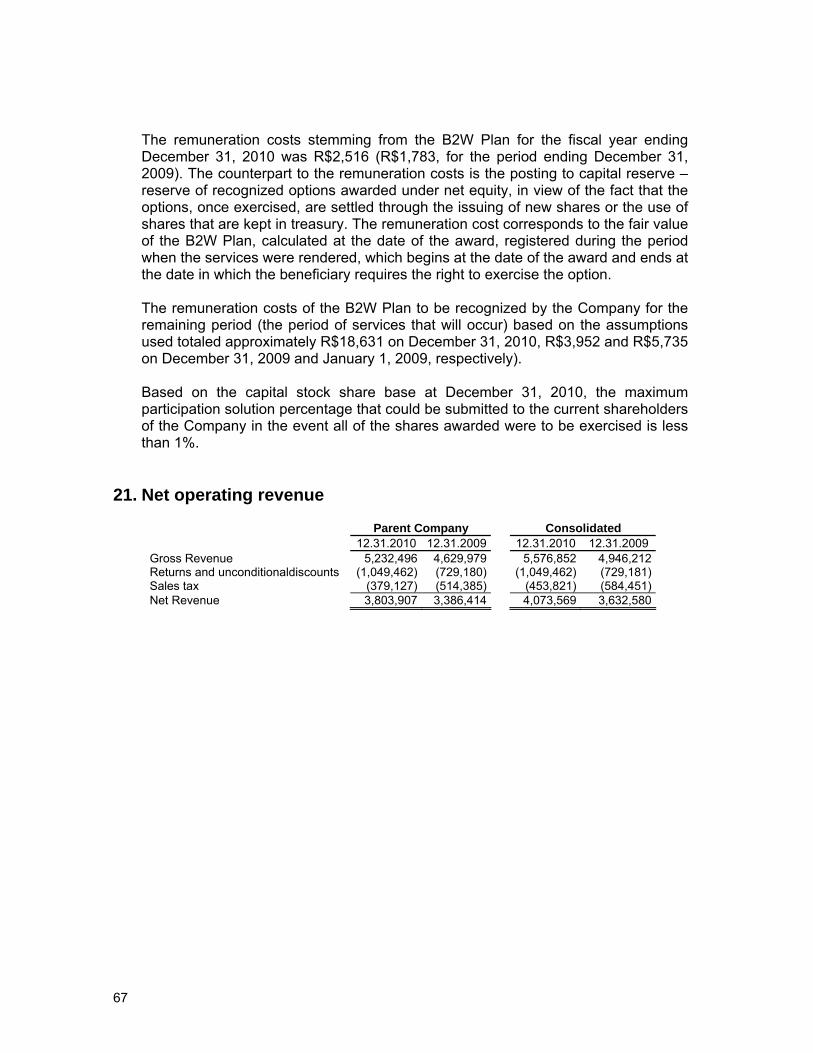

Provision for contingencies 18 12,811 13,517 4,270 12,811 13,517 4,270 Deferred income and social

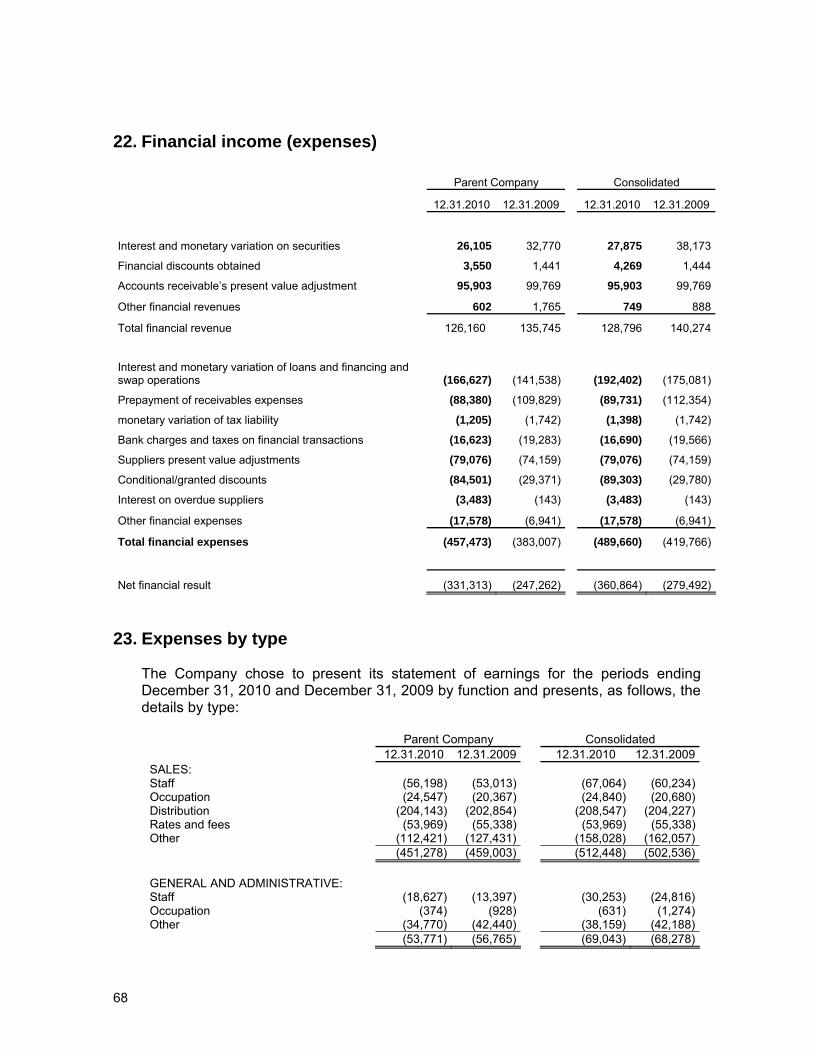

contribution taxes 9 25,457 7,897 - 31,080 13,666 - Other liabilities 6,674 9,509 10,281 6,674 9,508 10,281

Total non curretn liabilities 1,577,265 1,104,348 650,233 1,585,781 1,110,116 650,233 Stockholders’ equity Capital Stock 19 a 182,491 181,566 181,566 182,491 181,566 181,566 Capital reserves 19 d 207,807 205,291 203,508 207,807 205,291 203,508

(-) Treasury shares 19 c (200,000) (200,000) (200,000) (200,000) (200,000) (200,000)Equity adjustment 620 1,250 (861) 620 1,250 (861)Profit reserves 19 d and f g 82,212 64,529 28,228 52,855 24,257 (23,241)(-) Treasury shares 19 c (18,631) (22,701) (21,883) (18,631) (22,701) (21,883)Accumulated profits - 3,209 - - 3,209 - Adittional proposed dividends 803 - - 803 - -

Total stockholders’ equity 255,302 233,144 190,558 225,945 192,872 139,089 Total of liabilities and stockholders’

equity 3,034,130 2,162,859 2,113,748 3,212,014 2,303,936 2,312,602

The explanatory notes are integral part of the financial statements.

6

B2W COMPANHIA GLOBAL DO VAREJO Financial Statements Years ended on December 31, 2010 and 2009 (In thousands of reais except where otherwise mentioned) Parent Company Consolidated Note 12.31.2010 12.31.2009 12.31.2010 12.31.2009 Net revenue from sales and/or services 21 3,803,907 3,386,414 4,073,569 3,632,580 Cost of goods and/or services sold (2,811,748) (2,427,298) (2,937,529) (2,570,035) Gross profit 992,159 959,116 1,136,040 1,062,545 Operating income (expenses)

Selling expenses 23 (451,278) (459,003) (512,448) (502,536)Depreciation/amortization (66,819) (63,817) (55,767) (48,528)General and administrative expenses 23 (53,771) (56,765) (69,043) (68,278)Equity pick up 10 10,802 6,667 - -

Management fees (7,215) (3,810) (7,565) (4,460) Other operating income (expenses) (63,982) (63,071) (80,453) (63,062) Result before financial result 359,896 319,317 410,764 375,681 Financial Result Financial revenue 22 126,160 135,745 128,796 140,274 Financial expenses 22 (457,473) (383,007) (489,660) (419,766) Income before income and social contribution

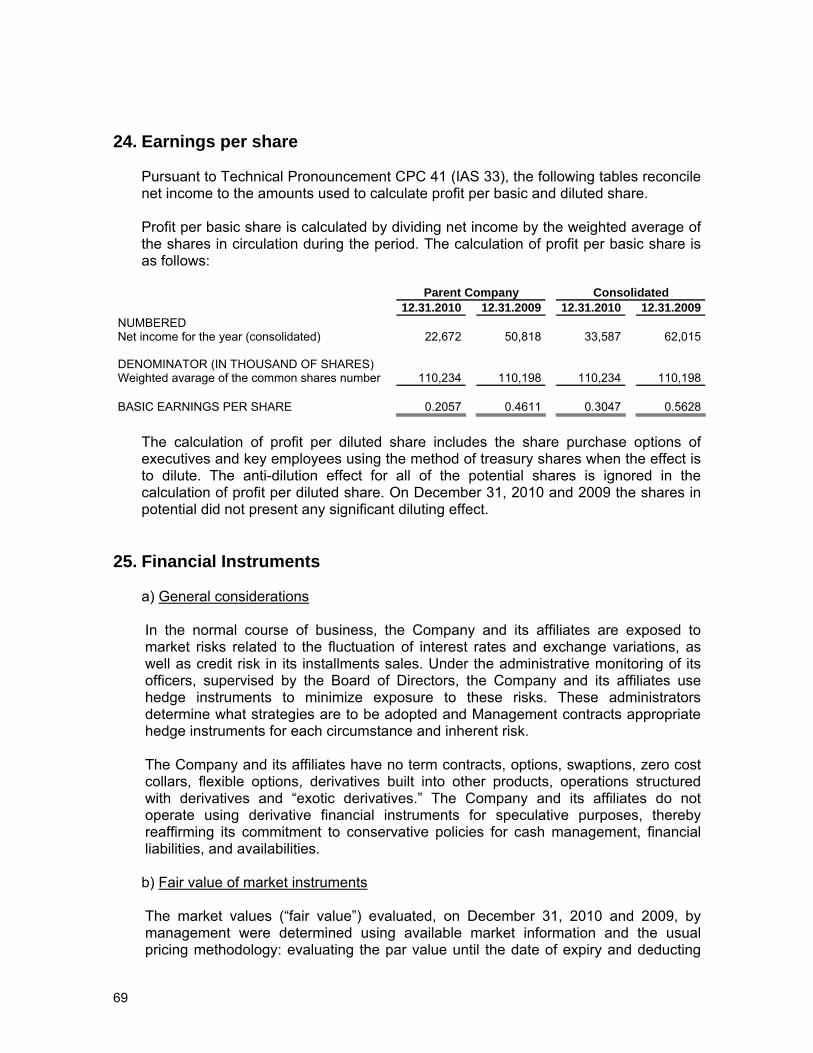

taxes 28,583 72,055 49,900 96,189 Income tax and social contribution taxes (5,911) (21,237) (16,313) (34,174) Current 9 c - (10,361) (12,470) (17,482) Deferred 9 c (5,911) (10,876) (3,843) (16,692) Net income of the period 22,672 50,818 33,587 62,015 Earnings per share of the capital stock at the end

of the period, excluding treasury shares - R$ 0.2057 0.4611 0.3047 0.5628

The explanatory notes are integral part of the financial statements.

7

B2W COMPANHIA GLOBAL DO VAREJO Statements of changes in Shareholders’ equity For the years ended on December 31, 2010 and 2009 – Parent Company On December 31, 2010 and 2009 (In thousands of reais)

Profi reserves Additional

Capital stockCapital

reserves Treasury shares

Equity adjustment Legal reserve

Expansion reserves

Treasury shares

Accumulated profit

dividends proposal Total

Balance in December 31, 2008 181,566 203,508 (200,000) (861) 6,118 39,143 (21,883) - - 207,591

Adjustment to the CPC's/IFRS suitability - - - - - (17,033) - - - (17,033) Balance in December 31, 2008 (adjusted) 181,566 203,508 (200,000) (861) 6,118 22,110 (21,883) - - 190,558

Repurshase of shares - - - - - - (818) - - (818) Stock option plan - 1,783 - - - - - - - 1,783 Equity adjustment – Financial applications - - - 2,111 - - - - - 2,111 Net income of the period - - - - - - - 50,818 - 50,818 Allocation of net income Legal reserves - - - - 2,380 - - (2,380) - - Mandatory dividends (R$ 102.62 per

thousand chares, excluding treasury shares) - - - - - - - (11,308) - (11,308)

Destination of expansion reserve - - - - - 33,921 - (33,921) - - Balance in December 31, 2009 181,566 205,291 (200,000) 1,250 8,498 56,031 (22,701) 3,209 - 233,144

Destination of accumulated profits Additional dividends proposal - - - - - - - (803) 803 - Destination of expansion reserve - - - - - 2,406 - (2,406) - - Capital increase 925 - - - - - - - - 925 Stock option plan - 2,516 - - - - - - - 2,516 Sale of treasury shares - - - - - (2,012) 4,070 - - 2,058 Equity valuation adjustment – Financial

applications - - - (630) - - - - - (630) Net income of the period - - - - - - - 22,672 - 22,672 Allocation of net income - - - - - - - - - - Legal reserves - - - - 1,134 - - (1,134) - - Mandatory dividends (R$ 163.43 per

thousand chares, excluding treasury shares) - - - - - - - (5,383) - (5,383)

Destination of expansion reserve - - - - - 16,155 - (16,155) - - Balance in December 31, 2010 182,491 207,807 (200,000) 620 9,632 72,580 (18,631) - 803 255,302

The explanatory notes are integral part of the financial statements.

8

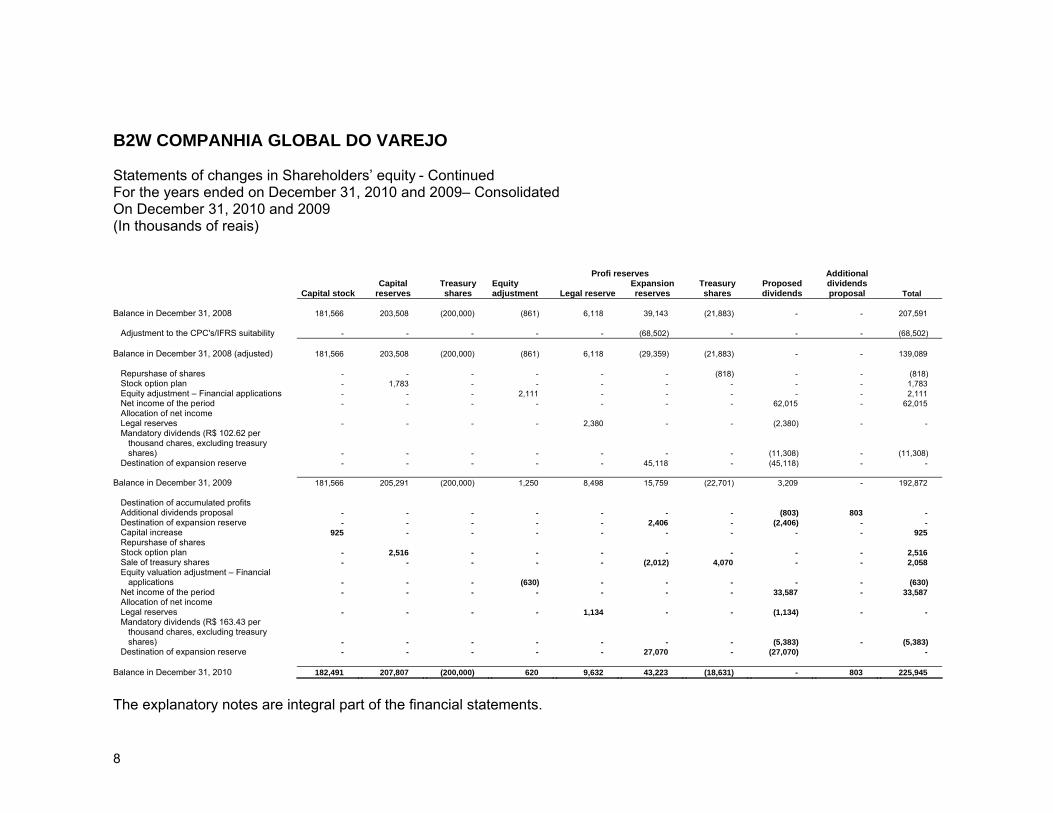

B2W COMPANHIA GLOBAL DO VAREJO Statements of changes in Shareholders’ equity - Continued For the years ended on December 31, 2010 and 2009– Consolidated On December 31, 2010 and 2009 (In thousands of reais) Profi reserves Additional

Capital stockCapital

reserves Treasury shares

Equity adjustment Legal reserve

Expansion reserves

Treasury shares

Proposed dividends

dividends proposal Total

Balance in December 31, 2008 181,566 203,508 (200,000) (861) 6,118 39,143 (21,883) - - 207,591

Adjustment to the CPC's/IFRS suitability - - - - - (68,502) - - - (68,502) Balance in December 31, 2008 (adjusted) 181,566 203,508 (200,000) (861) 6,118 (29,359) (21,883) - - 139,089

Repurshase of shares - - - - - - (818) - - (818) Stock option plan - 1,783 - - - - - - - 1,783 Equity adjustment – Financial applications - - - 2,111 - - - - - 2,111 Net income of the period - - - - - - - 62,015 - 62,015 Allocation of net income Legal reserves - - - - 2,380 - - (2,380) - - Mandatory dividends (R$ 102.62 per

thousand chares, excluding treasury shares) - - - - - - - (11,308) - (11,308)

Destination of expansion reserve - - - - - 45,118 - (45,118) - - Balance in December 31, 2009 181,566 205,291 (200,000) 1,250 8,498 15,759 (22,701) 3,209 - 192,872

Destination of accumulated profits Additional dividends proposal - - - - - - - (803) 803 - Destination of expansion reserve - - - - - 2,406 - (2,406) - - Capital increase 925 - - - - - - - - 925 Repurshase of shares Stock option plan - 2,516 - - - - - - - 2,516 Sale of treasury shares - - - - - (2,012) 4,070 - - 2,058 Equity valuation adjustment – Financial

applications - - - (630) - - - - - (630) Net income of the period - - - - - - - 33,587 - 33,587 Allocation of net income Legal reserves - - - - 1,134 - - (1,134) - - Mandatory dividends (R$ 163.43 per

thousand chares, excluding treasury shares) - - - - - - - (5,383) - (5,383)

Destination of expansion reserve - - - - - 27,070 - (27,070) - Balance in December 31, 2010 182,491 207,807 (200,000) 620 9,632 43,223 (18,631) - 803 225,945

The explanatory notes are integral part of the financial statements.

9

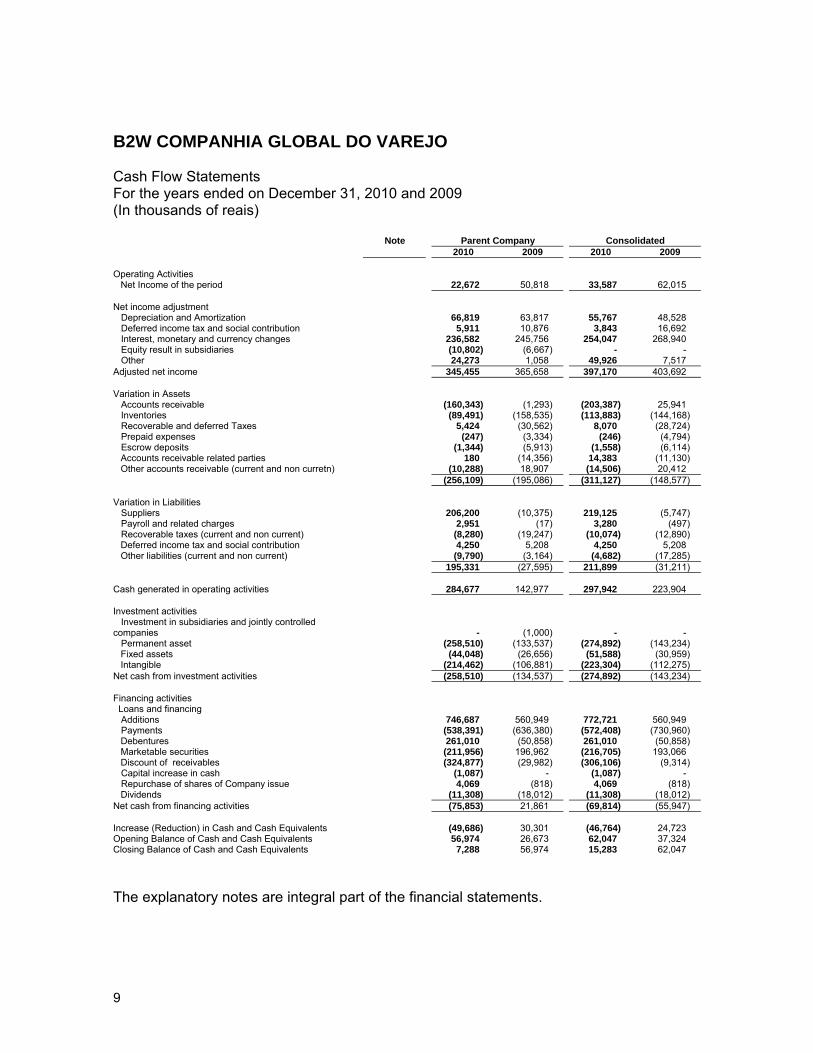

B2W COMPANHIA GLOBAL DO VAREJO Cash Flow Statements For the years ended on December 31, 2010 and 2009 (In thousands of reais) Note Parent Company Consolidated 2010 2009 2010 2009 Operating Activities

Net Income of the period 22,672 50,818 33,587 62,015 Net income adjustment Depreciation and Amortization 66,819 63,817 55,767 48,528 Deferred income tax and social contribution 5,911 10,876 3,843 16,692 Interest, monetary and currency changes 236,582 245,756 254,047 268,940 Equity result in subsidiaries (10,802) (6,667) - - Other 24,273 1,058 49,926 7,517 Adjusted net income 345,455 365,658 397,170 403,692 Variation in Assets Accounts receivable (160,343) (1,293) (203,387) 25,941 Inventories (89,491) (158,535) (113,883) (144,168) Recoverable and deferred Taxes 5,424 (30,562) 8,070 (28,724) Prepaid expenses (247) (3,334) (246) (4,794) Escrow deposits (1,344) (5,913) (1,558) (6,114)

Accounts receivable related parties 180 (14,356) 14,383 (11,130) Other accounts receivable (current and non curretn) (10,288) 18,907 (14,506) 20,412

(256,109) (195,086) (311,127) (148,577) Variation in Liabilities Suppliers 206,200 (10,375) 219,125 (5,747) Payroll and related charges 2,951 (17) 3,280 (497) Recoverable taxes (current and non current) (8,280) (19,247) (10,074) (12,890)

Deferred income tax and social contribution 4,250 5,208 4,250 5,208 Other liabilities (current and non current) (9,790) (3,164) (4,682) (17,285)

195,331 (27,595) 211,899 (31,211) Cash generated in operating activities 284,677 142,977 297,942 223,904 Investment activities Investment in subsidiaries and jointly controlled companies - (1,000) - - Permanent asset (258,510) (133,537) (274,892) (143,234)

Fixed assets (44,048) (26,656) (51,588) (30,959) Intangible (214,462) (106,881) (223,304) (112,275)

Net cash from investment activities (258,510) (134,537) (274,892) (143,234) Financing activities Loans and financing Additions 746,687 560,949 772,721 560,949 Payments (538,391) (636,380) (572,408) (730,960)

Debentures 261,010 (50,858) 261,010 (50,858) Marketable securities (211,956) 196,962 (216,705) 193,066 Discount of receivables (324,877) (29,982) (306,106) (9,314)

Capital increase in cash (1,087) - (1,087) - Repurchase of shares of Company issue 4,069 (818) 4,069 (818)

Dividends (11,308) (18,012) (11,308) (18,012) Net cash from financing activities (75,853) 21,861 (69,814) (55,947) Increase (Reduction) in Cash and Cash Equivalents (49,686) 30,301 (46,764) 24,723 Opening Balance of Cash and Cash Equivalents 56,974 26,673 62,047 37,324 Closing Balance of Cash and Cash Equivalents 7,288 56,974 15,283 62,047

The explanatory notes are integral part of the financial statements.

10

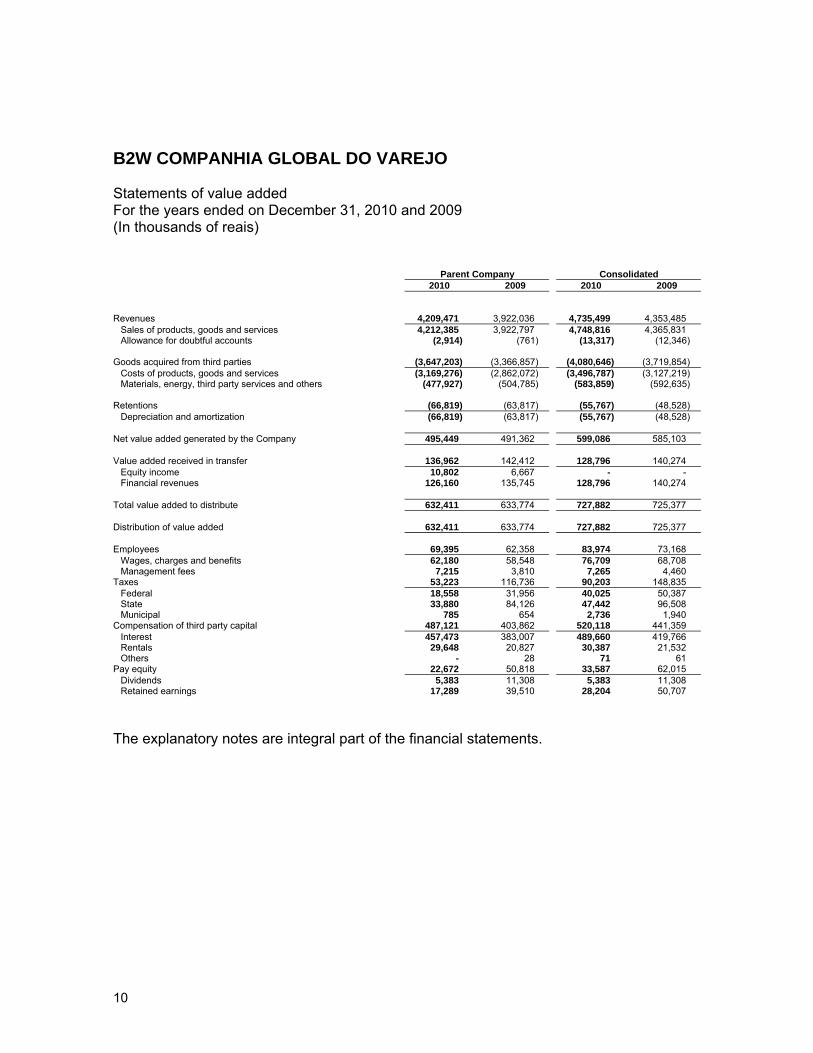

B2W COMPANHIA GLOBAL DO VAREJO Statements of value added For the years ended on December 31, 2010 and 2009 (In thousands of reais)

Parent Company Consolidated 2010 2009 2010 2009 Revenues 4,209,471 3,922,036 4,735,499 4,353,485

Sales of products, goods and services 4,212,385 3,922,797 4,748,816 4,365,831 Allowance for doubtful accounts (2,914) (761) (13,317) (12,346)

Goods acquired from third parties (3,647,203) (3,366,857) (4,080,646) (3,719,854)

Costs of products, goods and services (3,169,276) (2,862,072) (3,496,787) (3,127,219) Materials, energy, third party services and others (477,927) (504,785) (583,859) (592,635)

Retentions (66,819) (63,817) (55,767) (48,528)

Depreciation and amortization (66,819) (63,817) (55,767) (48,528)

Net value added generated by the Company 495,449 491,362 599,086 585,103

Value added received in transfer 136,962 142,412 128,796 140,274 Equity income 10,802 6,667 - - Financial revenues 126,160 135,745 128,796 140,274

Total value added to distribute 632,411 633,774 727,882 725,377 Distribution of value added 632,411 633,774 727,882 725,377 Employees 69,395 62,358 83,974 73,168

Wages, charges and benefits 62,180 58,548 76,709 68,708 Management fees 7,215 3,810 7,265 4,460

Taxes 53,223 116,736 90,203 148,835 Federal 18,558 31,956 40,025 50,387 State 33,880 84,126 47,442 96,508 Municipal 785 654 2,736 1,940

Compensation of third party capital 487,121 403,862 520,118 441,359 Interest 457,473 383,007 489,660 419,766 Rentals 29,648 20,827 30,387 21,532 Others - 28 71 61

Pay equity 22,672 50,818 33,587 62,015 Dividends 5,383 11,308 5,383 11,308 Retained earnings 17,289 39,510 28,204 50,707

The explanatory notes are integral part of the financial statements.

11

B2W - COMPANHIA GLOBAL DO VAREJO Notes to the financial statements Years ended December 31, 2010 and 2009 (In thousands of reais except where otherwise mentioned) 1. Operating Context

B2W - Companhia Global do Varejo ("B2W" or "Company") is a publicly traded corporation, with head offices at Rua Sacadura Cabral, 102, in city and state of Rio de Janeiro, incorporated through the merger of Americanas.com S.A. - Comércio Eletrônico (Americanas.com) and Submarino S.A. (merger approved by their shareholders on December 13, 2006), with shares traded on the Brazilian Securities Exchange (BM&FBOVESPA), under the ticker symbol BTOW3. B2W is controlled by Lojas Americanas S.A. ("LASA" and/or "Parent Company"), a public company with shares traded on the São Paulo Stock Exchange under the ticker symbols LAME3 - ON and LAME4 - PN. The Company and its subsidiaries are engaged in retail and wholesale of goods and products in general through various sales channels, particularly through the Internet; the rental of movies and related items; the intermediation and distribution of theater and movie tickets, tickets for transportation and public events, entrance to theme parks and events in general; the import of products for resale; promotional services, marketing development and the offering of credit products; and various other products and services for the general consumer. B2W's portfolio contains the Americanas.com, Shoptime, Submarino, Submarino Finance, B2W Viagens, Ingresso.com and Blockbuster Online brands, which offer hundreds of thousands of products and services in various categories through distribution through the Internet, catalogs, television sales and kiosks. B2W also offers outsourced e-commerce services for some of the leading consumer products companies (business-to-business to consumer - B2B2C).

2. Presentation of financial statement

The financial statements of the Company for the years ended on December 31, 2010 and 2009,and as of January 1, 2009 were prepared in accordance with accounting practices adopted in Brazil which include rules of the Brazilian Securities Exchange Commission (CVM) and Accounting Standards Board Pronouncements Committee (CPC), and the Consolidated Financial Statements were prepared in accordance with accounting practices adopted in Brazil which include rules of the Brazilian Securities Exchange Commission (CVM) and Accounting Standards Board Pronouncements Committee (CPC), as well as are in conformity with the International Accounting Standards (IFRS) issued by the International Accounting Standards Board (IASB). The Financial Statements were approved by Board of Directs´ Meeting held on March 16, 2011.

12

The Parent Company and Consolidated financial statements were prepared based on assumptions and estimates by management that impact the assets and liabilities balances. Management judgment involves making estimates related to the probability of future events, actual results may differ from those estimates. Those areas involving a higher level of judgment and/or the use of estimates and assumptions relevant to the financial statements are disclosed in Note 3. As a result, the settlement of transactions comprising these estimates may be materially different from those recorded in the financial statements due to the probabilistic treatment inherent to the estimation process. The Company reviews the estimates and assumptions, at least once a year. The Company has adopted all the standards, standards reviews and interpretations issued by the Accounting Pronouncement Committee (CPC),by IASB and regulatory agencies that were in effect on December 31, 2010. The financial statements were prepared using the historical cost as the value basis, except for the valuation of certain assets, such as financial instruments (measured at their fair value). The values of assets and/or liabilities that represent items subject to fair value hedges, which alternatively, would be recorded at amortized cost, are adjusted to show the changes in fair value attributable to the hedged risks. The effects of adopting IFRS and new pronouncements issued by the CPC are presented in Note 4. Pursuant to current Brazilian Corporate Law, the individual financial statements present an appraisal of investments in subsidiaries and jointly controlled subsidiaries by the equity accounting method, while under IFRS these investments should be valued at cost or fair value, as well as maintenance of the existing balance of deferred charges on December 31, 2008, which has been amortized, whereas under IFRS these expenses do not qualify for recognition as assets. Consequently, these individual financial statements are not considered to be in compliance with IFRS. Criteria for Consolidation The consolidated financial statements include the financial statements of the Parent Company, B2W - Companhia Global do Varejo and those companies that the Company controls (directly or indirectly), as well as those in which control is shared, as detailed in Note 10. Fiscal years of subsidiaries and jointly controlled affiliates included in the consolidation are compatible with the Company and the accounting practices and policies were consistently applied over consolidated companies. As anticipated in Technical Pronouncement CPC 19 (IAS 31) - Investments in Jointly Controlled Ventures ("Joint Ventures"), the consolidation of Submarino Finance Promotora de Credito Ltda. ("Submarino Finance") was done proportionally to the Parent Company's ownership interest in the capital of that Company (50%),

13

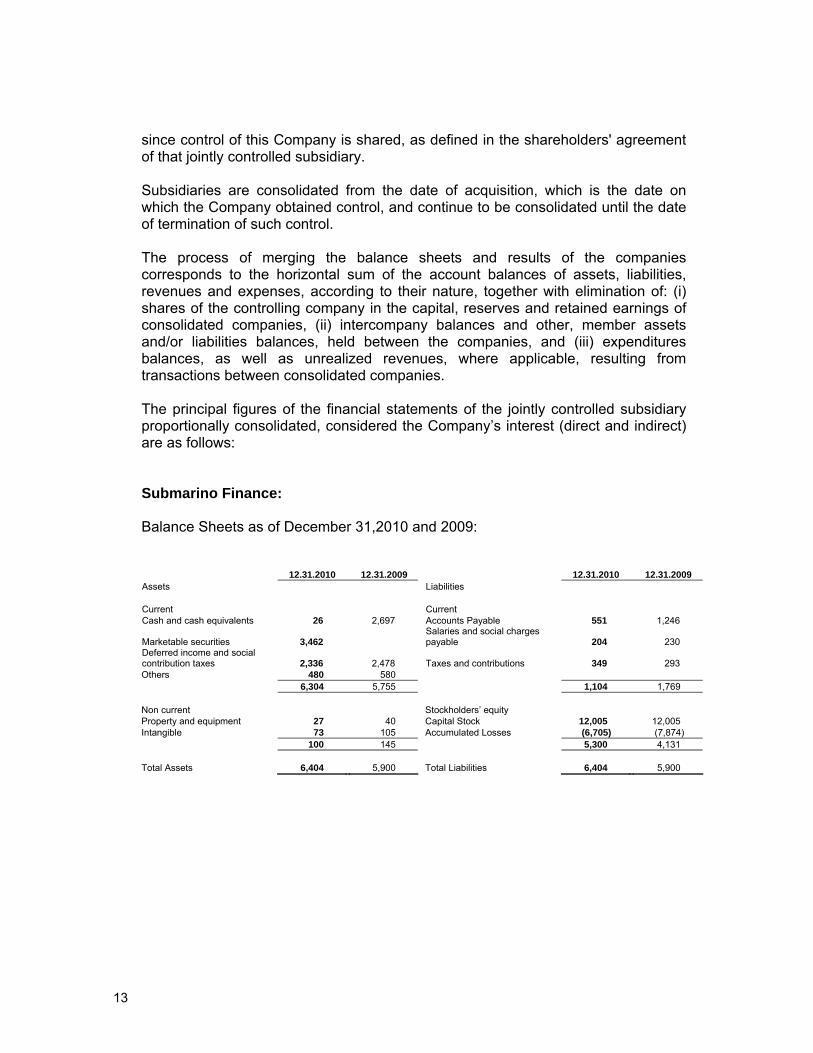

since control of this Company is shared, as defined in the shareholders' agreement of that jointly controlled subsidiary. Subsidiaries are consolidated from the date of acquisition, which is the date on which the Company obtained control, and continue to be consolidated until the date of termination of such control. The process of merging the balance sheets and results of the companies corresponds to the horizontal sum of the account balances of assets, liabilities, revenues and expenses, according to their nature, together with elimination of: (i) shares of the controlling company in the capital, reserves and retained earnings of consolidated companies, (ii) intercompany balances and other, member assets and/or liabilities balances, held between the companies, and (iii) expenditures balances, as well as unrealized revenues, where applicable, resulting from transactions between consolidated companies. The principal figures of the financial statements of the jointly controlled subsidiary proportionally consolidated, considered the Company’s interest (direct and indirect) are as follows: Submarino Finance: Balance Sheets as of December 31,2010 and 2009:

12.31.2010 12.31.2009 12.31.2010 12.31.2009 Assets Liabilities Current Current Cash and cash equivalents 26 2,697

Accounts Payable 551 1,246

Marketable securities 3,462 Salaries and social charges payable 204 230

Deferred income and social contribution taxes 2,336 2,478

Taxes and contributions 349 293 Others 480 580 6,304 5,755 1,104 1,769 Non current Stockholders’ equity Property and equipment 27 40 Capital Stock 12,005 12,005 Intangible 73 105 Accumulated Losses (6,705) (7,874) 100 145 5,300 4,131 Total Assets 6,404 5,900 Total Liabilities 6,404 5,900

14

Income statement for the years ended on December 31, 2010 and 2009: 12.31.2010 12.31.2009 Net revenue 3,337 3,169 Selling, administrative and general expenses (2,325) (2,703) Net financial result 1,014 940 Other operational expenses (396) (39) Deferred income and social contribution taxes - current (320) (121) Deferred income and social contribution taxes - deferred (142) (270) Net income for the year 1,168 976

3. Summary of principle accounting practices

a) Significant judgments, estimates and assumptions

Judgments

The preparation of the Parent Company and Consolidated financial statements requires that the management make judgments, estimates and adopt assumptions that affect revenues, expenses, assets and liabilities figures, as well as disclosures of contingent liabilities as of the date of its financial statements. However, the uncertainty associated with these assumptions and estimates could lead to results that require a significant adjustment to the book value of the affected assets or liabilities in future periods.

Estimates and assumptions The key assumptions regarding the sources of uncertainty for future estimates and other important sources of uncertainty for estimates on the balance sheet date, involving significant risk of causing a major adjustment to the book value for assets and liabilities in following reported period are discussed below.

Provision for doubtful accounts This provision is based on analysis of historical losses monitored by management, which are provided for an amount considered sufficient to cover probable losses on accounts receivable. Provision for losses in inventories The provision for losses in inventories is based on estimates, which take into account historical data for losses in the annual, physical inventories in the distribution centers, as well as the sale of items below their cost of acquisition. This provision is considered sufficient by management to cover probable losses in the turnover of their inventories.

15

Useful life of fixed and intangible assets Depreciation and amortization of fixed and intangible assets are considered the best estimate of the management on the use of these assets over the course of their useful life. Changes in economic conditions and/or the consumer market may require revision of these useful life estimates.

Impairment of non-financial assets

Management annually reviews the net accounting value of assets with the objective of identifying events or changes in economic, operating or technological circumstances that could indicate the deterioration or loss of their recoverable value. If such evidence is identified and the net accounting value of an asset exceeds its recoverable value, an impairment allowance adjusts the net accounting value to the recoverable value. The recoverable value of an asset or a particular cash-generating unit is defined as the greater value between the remaining useful life and net sales value. In estimating assets value in use, estimated future cash flows are discounted to present value using a discount rate before taxes, reflecting weighted average cost of capital for the industry in which the cash-generating unit operates. The net sales price is determined, whenever possible, based on firm sales contract in a transaction on arm´s length basis, between well informed and willing parties, adjusted by expenses attributable to asset sale or, when there is no firm sales contract, based on the market price in a active market or the most recent transaction price with similar assets. The following criterion is also applied to evaluate impairment losses: i) Goodwill paid for expected future profitability This goodwill is tested annually for impairment or when circumstances indicate loss due to depreciation of its book value. ii) Intangible assets Indefinite-life intangible assets are tested annually for impairment, either individually or at the level of the cash-generating unit depending on the case, or when circumstances indicate loss due to depreciation of their book value. When this evidence is identified and the net book value exceeds the recoverable value, an impairment allowance is booked, adjusting the net book value adjusted to the recoverable value, when applicable.

16

Taxes

Deferred income and social contribution tax assets are recognized only to the extent that it is probable that there will be taxable income for which temporary differences and tax losses can be utilized. The recovery of the deferred tax asset is reviewed at end of each fiscal year and when it is not probable that future taxable profits will be available to allow recovery of all or part of the asset, the asset balance is adjusted by the amount expected to be recovered. Significant management judgment is required to determine the value of deferred tax assets that can be recognized, based upon the likely timing and level of future taxable profits, along with future strategic fiscal planning.

Provision for tax, civil and labor risks

The Company recognizes a provision, which involve considerable management judgment, for tax, labor and civil risks resulting from past events, when it is probable that an outflow of resources embodying economic benefits will result from the settlement of an obligation and the amount at which the settlement will take place can be reasonably measured. The Company is also subject to legal, civil and labor claims related to matters that arise through the normal course of the activities of its business. The assessment of probability of loss includes evaluating available evidence, the hierarchy of laws, available case law, recent court decisions and their relevance in the legal system, as well as the assessment of outside counsel. Provisions are reviewed and adjusted to take into account changes in circumstances, such as the applicable limitation period, conclusions of tax inspections or additional exposures identified based upon new issues or decisions of courts. Actual results may differ from estimates. The basis and nature of provision for contingencies are described in Note 18. The settlement of transactions involving these estimates may result in amounts significantly different from those recorded in the financial statements due to the inaccuracies inherent to the process of their determination. The Company reviews its estimates and assumptions at least quarterly.

b) Results of operations

The results of operations are determined in accordance with the accrual basis of accounting, highlighting the following:

Revenues from the sales of goods and services, which include the freight

charges to customers, are recorded upon transfer of ownership and the risk to third parties by their gross values, deducting unconditional discounts and returns, and adjusting the current calculated value of term sales and sales taxes. Approved sales orders for credit card administrators, whose products have not yet been billed or shipped to customers, and the sales of gift certificates that are in the hands of customers and that will be used in

17

the future are recorded as “Other Obligations” under current liabilities;

The cost of goods sold and services rendered includes the cost of acquisition of goods and the cost of services, deducting for supplier subsidies received, as applicable;

Advertising expenses are recorded in the results when their effective

placement was reduced by the participation of suppliers;

Freight expenses related to the delivery of goods to consumers are classified as sales expenses.

c) Foreign currency

The functional currency of the Company and its subsidiaries based in Brazil is the Brazilian Real (R$), the same currency used in the preparation and presentation of the Parent Company and Consolidated financial statements. Transactions in foreign currency, i.e. all those not made in the functional currency, at exchange rates prevailing on the dates of the transactions. Assets and liabilities in foreign currencies are converted into the functional currency using the exchange rate on the balance sheet closing date. Gains and losses, from changes in the exchange rates, on assets and liabilities are recorded in the results statements. Non-monetary assets and liabilities acquired or contracted in foreign currency, as applicable, are converted using the exchange rates on the dates of transactions or at fair value, on the dates of review, when it is used.

d) Cash and cash equivalents

Cash and cash equivalents include cash, positive balances in bank accounts and investments redeemable within 90 days from the signing date, and with insignificant risk of change in market value. These investments are valued at cost plus income earned to the date of the balance sheet, which do not exceed their market or realizable value.

e) Accounts receivable from clients

Accounts receivable from credit card administrators are shown at net adjusted present value, calculated on the portion of the sales and the depreciation allowance for doubtful accounts. Sales through corporate loyalty programs and trade agreements are recorded under “other receivables”.

f) Inventories

Inventories are shown at average acquisition cost, adjusted to the present value from suppliers (forward purchases) and, when applicable, subsidies received from suppliers, that do not exceed their net realizable value.

18

g) Investments in subsidiaries and jointly controlled subsidiaries

For the purposes of the Company’s financial statements, the investments in subsidiaries and jointly controlled subsidiaries are valued by the equity method, in accordance with Technical Pronouncement CPC 18 (IAS 28). The accounting practices used by subsidiaries and jointly controlled subsidiaries are the same as those used by the Company and the financial statements database used in the calculation of equity is the same as that used by the Company. Based on the equity method, investments in subsidiaries and jointly controlled subsidiaries are calculated on the Company’s balance sheet at cost, adding such changes following the acquisition of shares in those companies. The equity interest in subsidiaries and jointly controlled subsidiaries is presented in the Parent Company’s income statement as equity accounting, shown as net profit attributable to the shareholders of the investee.

h) Fixed assets

Fixed assets are recorded at cost of acquisition, less the respective depreciation and impairment losses, if applicable. Depreciation is calculated on a straight-line basis at the rates described in Note 12, which takes into consideration the useful economic life of these assets. Amortization of the improvements in leased properties is calculated on the basis of the respective time periods for the lease contracts. Costs subsequent to initial recognition are incorporated into the residual value of the fixed asset or recognized as a specific item, as appropriate, only if the economic benefits associated with these items are probable and whose value can be reliably measured. The carrying amount of an item being replaced is de-recognized. Other repairs and maintenance are recognized directly in the results as they were incurred. The residual values and useful life of assets are reviewed and adjusted, as appropriate, at the end of each fiscal year. As a result of the changes in Brazilian accounting practices to completely adhere to the process of convergence with international accounting practices, in the first time adoption of Technical Pronouncement CPC 27 (IAS 16) and,Interpretation of Initial Application to Fixed Assets ICPC 10, there is an option to record adjustments in the initial balances similar to that permitted under international financial reporting standards by using the concept of deemed cost, as indicated in Technical Statements CPC 37 (IFRS 1) and CPC 43. The Company opted not to evaluated its fixed assets at fair value as attributed cost considering that (i) the cost method, minus allowance for losses, is the best method for evaluating the Company's fixed assets, (ii) the Company's

19

fixed assets is broken down into well-defined classes related to its only operational activities, which is recoverable values and useful life estimates are frequently revised, and (iii) the Company has effective controls over fixed assets that allow it to identify impairment losses and changes to the useful life estimates.

i) Intangible

The goodwill registered on the acquisition of investments, including that recorded from the merger, are based on the expectation of future profitability and were amortized through December 31, 2008 using periods of 5 to 10 years, according to the proportion of future profits expected from the investments. The goodwill according to the expectation of future profitability is no longer amortized as of January 1, 2009, and its recoverable value is tested annually, or whenever deemed necessary. The expenses related to the development of websites (the main sales channel of the Company), as well as the development of operating applications, technological infrastructure (purchase and internal development of software and the installation of applications on the sites), as well as graphics development are recorded as intangibles, in accordance with Technical Pronouncement CPC 04 (IAS 38), is amortized on a straight-line basis taking into account the estimated term stipulated for their use and the benefits that will be reported (Note 13). Other intangibles, such as use licenses and software licensing rights, are recorded at their acquisition cost, less amortization, calculated on a straight-line basis according to the useful life of those intangible assets (Note 13).

j) Commercial Leasing

Financial leases

Financial lease contracts substantially transfer to the Company the risks and benefits inherent to the asset ownership. These contracts are characterized as capital lease contracts and the assets are recorded at fair value or the present value of minimum payments foreseen in the contracts. The items recorded as assets are depreciated at depreciation rates applicable to each asset group, according to Note 12. Finance charges relating to capital lease contracts are noted in the results over the term of these contracts, based on the amortized cost method and the effective interest rate.

Operating leases

Payments made under operating leases are recognized in fiscal year results on a straight-line basis over the lease term, in accordance with accrual accounting methodologies for the fiscal years.

20

k) Borrowing costs

The costs of finance charges on non-specific purpose loans, which are used to acquire and/or construct an asset that requires a substantial period of time to be completed ("qualifying asset"), are capitalized during the period required to complete and prepare the asset for its intended use. Capitalized loan finance charges are obtained by applying the weighted average interest rate on loans that were in force during the period in which investments were made to obtain the qualifying asset, not to exceed the amount of borrowing costs incurred during the period.

l) Deferred assets

In connection to Law 11941/09 and CPC 43, the Company opted to maintain, under Deferred Assets, the balances related to pre-operating expenses that showed signs of recoverability, for amortization during the period of anticipated benefits. The effect of maintaining the Deferred Assets balance is totally eliminated in the preparation and presentation of the consolidated financial statements (Notes 4 and 14).

m) Income tax and social contribution

Expenditure on income tax and social contribution are the sum of current and deferred taxes.

Current taxes

Provisions for income tax and social contribution are based on taxable income for the fiscal year. The income tax was set at the rate of 15%, plus an additional 10% on taxable income exceeding R$240. The social contribution was calculated at the rate of 9% on the adjusted net income. Taxable income differs from income presented in the income statement because it excludes taxable revenues or expenditures deductibles from other fiscal years, and excludes permanently non-taxable or non-deductible items. Provisions for income tax and social contribution are calculated individually (by a Group company) based on the prevailing rates at the close of the fiscal year.

Deferred taxes

Income tax and social contribution taxes are recognized in their entirety, in accordance with the concept described in Technical Pronouncement CPC 32 (IAS 12) regarding the differences between assets and liabilities recognized for tax purposes and their corresponding values in the financial statements. Deferred income tax and social contribution amounts are determined by the prevailing rates (and laws) at the time of preparation of financial statements and applicable when the respective, deferred income tax and social contribution payments are made.

21

Current and deferred taxes are recognized in the results, except when they correspond to items recorded as "Other accumulated income," or directly as equity, in which case the current and deferred taxes are also recognized as "Other accumulated income" or directly as equity, respectively. Deferred tax assets and liabilities are presented as net only if there is a legal or contractual right to offset tax assets against tax liabilities and the deferred taxes are related to the same, taxable entity and subject to the same tax authority.

n) Adjustment at present value

The operations of long-term transactions, primarily from suppliers of goods and services, were adjusted to their present value taking into account the maturities of these transactions. We used the average rate of 11.70% per year on December 31, 2010 (12.60% per year and 13.33% per year on December 31, 2009 and January 1, 2009, respectively), with a minimum of 10.59% per year on December 31, 2010 (10.59% per year and 11.94% per year on December 31, 2009 and January 1, 2009, respectively) and the maximum of 12.63% per year on December 31, 2010 (15.97% per year and 15.96% per year on December 31, 2009 and January 1, 2009, respectively), based on funding for the respective fiscal years. The constitution of present value adjustment of purchases is recorded under “Suppliers” and “Inventory” (Note 7) and their counterpart reversals are shown under the heading “Financial Expenses,” to the time of maturity, in the case of suppliers, and for the realization of inventories turnover with regard to the values recorded under the heading “Cost of goods sold.” The operations of long-term transactions, at the same previously-agreed prices as represented, mainly, through credit cards installment sales, were brought to their present value taking into account the payment deadlines of the aforementioned transactions. The same treatment was given to the taxes on those sales, considering the effective rate on them. We used the average rate of 10.68% per year on December 31, 2010 (11.76% per year and 14.25% per year on December 31, 2009 and January 1, 2009, respectively), with a minimum of 9.45% per year on December 31, 2010 (9.27% per year and 11.76% per year on December 31, 2009 and January 1, 2009, respectively) and a maximum of 11.70% per year on December 31, 2010 (17.79% per year and 19.03% per year on December 31, 2009 and January 1, 2009, respectively), receivables discounts being based upon their respective base dates. The present value adjustment of installment sales has a counterpart under the heading “Accounts receivable from clients” (Note 6) and its performance is recorded under “Financial income” to the maturity of the term.

22

o) Financial instruments

The Company’s financial instruments are represented by cash and cash equivalents, marketable securities, accounts receivable, accounts payable, debentures, loans and financing and derivatives. Financial instruments are initially recorded at fair value plus transaction costs that are directly attributable to their acquisition or issue, except for financial assets and liabilities classified at fair value, through profit or loss, when such costs are recorded directly in fiscal year results. Their subsequent measurement occurs as of each date of financial statements, in accordance with classification of financial instruments in the following financial assets and liabilities categories: (i) financial assets or financial liabilities measured at fair value through profit or loss, (ii) investments held to maturity, (iii) loans and receivables, (iv) financial assets available for sale.

Financial assets at fair value through profit or loss: Financial assets at fair value through profit or loss include financial assets held-for-trading and financial assets designated upon initial recognition at fair value through profit or loss. Financial assets are classified as held-for-trading if they are acquired for the purpose of selling in the near term. Gains and losses on liabilities held-for-trading are recognized in the income statement. Financial liabilities at fair value through profit or loss: Financial liabilities at fair value through profit or loss include financial liabilities held-for-trading and financial liabilities designated upon recognition at fair value though profit or loss. Gains and losses on liabilities held-for-trading are recognized in the income statement. Held-to-maturity investment: Financial assets with fixed or determinable payments and fixed maturity dates, which the Company has the intention and ability to hold until maturity, are classified in this category. Financial assets held-to-maturity are measured at amortized cost using the effective interest rate method, less provision for impairment loss of recoverable (“impairment”) value. Interest income is recognized by applying the effective interest method. Loans and receivables: After initial recognition, loans and receivables subject to interest are subsequently measured at amortized cost, using the effective interest method. Gains and losses in liabilities and assets are recognized in the income statement at the time of its closing, as well as during the amortization process by the effective interest rate method.

Available-for-sale financial assets: Available-for-sale financial assets are those that are non-derivative and are designated as available for sale or are not classified in the aforementioned categories. Available-for-sale financial assets are measured at fair value. Interest, restatement, and exchange rates, as applicable, are recognized in the income statement, when incurred. The variations arising from valuation at fair value are recognized, when incurred, as a separate component of equity in the income statement when they are held in cash or determined to be unrecoverable.

23

The Company is exposed to market risks arising from its operations and uses derivative financial instruments to minimize its exposure to these risks, such as swap contracts to protect it from the risks of exchange rates. Derivative financial instruments are measured at fair value (market value) on each balance sheet disclosure date. Given that the Company and its subsidiaries make use of derivatives for protection (“hedge”), it adopted the accounting practice of accounting for hedging instruments (“hedge accounting”). Loans and financing are initially measured at fair value net of incurred transaction costs. Loans and financing not covered by hedging instruments are subsequently measured at amortized cost using the effective interest method, while those that are covered subject to hedge accounting are adjusted for the effects of the fair value of the covered risks. The Company and its subsidiaries have neither cash flow hedges nor overseas investment hedges. The current and noncurrent liabilities are stated at known or estimated amounts, as applicable to the corresponding charges, monetary variations and/or exchange rates incurred through the balance sheet date.

p) Stock option plans

The fair value of the respective equity instruments is calculated on the grant date of the stock option plans, based on pricing models usually adopted by the market. These models are calculated using assumptions, such as market value of the stock, the option exercise price, price volatility of the Company’s stock (calculated on a historical stock price basis), risk-free interest rate, term of the contract (“vesting period”) and anticipated distribution of dividends. The compensation costs associated with these plans are recorded on a straight-line basis over the service period to the beneficiary beneficial, in consideration of an anticipated withdrawal. The assumptions and models used to estimate the fair value of share-based payments are disclosed in Note 20.

q) Other assets and liabilities

An asset is recorded on the balance sheet when it is treated as a resource controlled by the Company as a result of past events and from which future economic benefits are expected to flow. A liability is recorded on the balance sheet when the Company has a legal obligation or an obligation has come about as a result of a past event, where it is probable that an economic resource will be required to liquidate it.

24

r) Earnings per share

In accordance with Technical Pronouncement CPC 41 (IAS 33), net income is calculated and presented in a basic format and diluted, as described in Note 24.

s) Statements of Cash Flows

The statements of cash flows have been prepared by the indirect method and are presented in accordance with Technical Pronouncement CPC 03 (IAS 7).

t) Information per segment

Operating segments are defined as components of an enterprise for which separate financial information is regularly available and evaluated by the chief operating decision-maker in deciding how to allocate resources to an individual segment and in assessing the performance of the segment. The Company’s activities are concentrated in the marketing of products and delivery of services by various means of distance marketing, especially the Internet. Despite the diversity of products sold and services provided by the Company (retail and wholesale trade, movie rentals, sale and distribution of theater and movie tickets, tickets for transportation and public events, entrance to theme parks and events in general, among others), such activities are not controlled and managed by the Management as independent operational segments, as their accompanying results are monitored, tracked and evaluated in an integrated manner. Thus, Management understands that the Company is organized, basically, in a single business unit. The Company also operates in the area of financial products through the jointly controlled subsidiary, Submarino Finance, which, because does not achieve the minimum quantitative and qualitative parameters, is not being presented as a separate operating segment.

u) Value Added Statement (VAS)

This statement aims to highlight the wealth created by the Company, its subsidiaries and jointly controlled subsidiaries, and its distribution channels during a specific fiscal year, and is presented as required by Brazilian corporate law, as part of its individual financial statements and as supplemental information to the consolidated financial statements, yet it is not a planned or compulsory statement in accordance with the IFRS. The VAS has been prepared based on information obtained from accounting records that serve as the basis for preparation of financial statements and following the provisions contained in Technical Pronouncement CPC 09. The first part introduces the wealth created by the Company, represented by revenue (gross sales revenue, including the taxes levied on it, other revenue and the effects of the allowance for doubtful accounts), the inputs acquired from third parties (cost of sales and purchases of materials, energy and services from third parties, including taxes included at the time of acquisition, the effects

25

of loss and recovery of asset values, and depreciation and amortization) and the received value added from third parties (the result of equity, financial income and other revenue). The second part of VAS shows the distribution of wealth between personnel, taxes, fees and contributions, remuneration of third party capital, and pay equity.

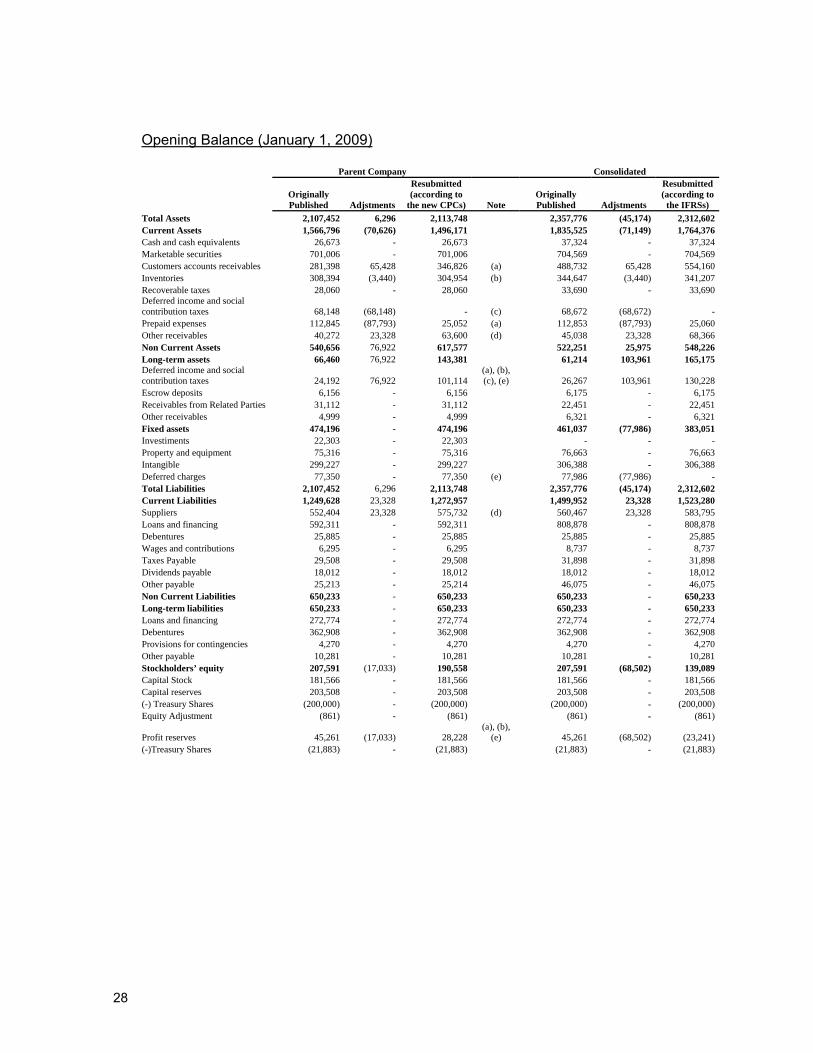

4. First time adoption of International Accounting Standards

The Company’s financial statements (Parent Company and Consolidated) up to December 31, 2009 were prepared based on the accounting practices adopted in Brazil, additional rules of CVM, technical pronouncements of CPC issued up December 31, 2008 and provisions in the Brazilian Corporate Law (BRGAAP). The Company has prepared its opening balance sheet with a transition date of January 1, 2009. Therefore, it has adopted the mandatory exceptions and certain optional exemptions of full retrospective adoption, according to Technical Pronouncements, Interpretations and Guidelines issued by the CPC and approved by the CVM for Individual (Parent Company) and Consolidated Financial Statements according to the International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB) for Consolidated Financial Statements. The CPC 37R (IFRS 1) requires that an entity to develop accounting policies based on CPC and IASB standards and interpretations effective on the closing date of the first Parent Company´s and Consolidated financial statements, and such policies shall be applied the transition date and during all periods presented in the first CPC (application of all rules) and the IFRS statements. The Company´s transition date is January 1, 2009. The Company has adopted all the pronouncements, guidelines and interpretations of the CPC issued up as of December 31, 2010 and, therefore the consolidated financial statements aligned with the International Accounting Standards issued by IASB and approved by CPC. The main differences between the accounting practices adopted on the transition date, including the Shareholders’ Equity and income reconciliations, and the practices adopted for the presentation of comparative financial information are described below. The individual financial statements for the year ended December 31, 2010 are the first one presented consideration the full application of the CPCs and the consolidated financial statements, also are the first one considering the full application of CPCs and in accordance with the International Financial Reporting Standards (IFRS).

26

Mandatory exceptions and exemptions to retrospective to retrospective adoption The CPC 37R (IFRS 1) allows companies to adopt certain voluntary exemptions. The Company has analysis of all voluntary exemptions. Below are the results of such analysis on its operations and the treatment given by the Company indicating the corresponding international standard: The following exemptions apply to operations: a) Exemption for business combinations:

The Company adopted CPC Pronouncement 15 (IFRS 3R) as of the year beginning on January 1, 2009;

b) Exemption for presenting the fair value of a fixed asset at acquisition cost:

The Company has chosen not to measure its fixed assets on the transition date at fair value. Instead it has chosen to maintain the acquisition cost to BRGAAP as the value for its fixed asset, considering reviews of balance related items and the relevant of this criteria;

The following exemptions do not apply to operations and do not impact financial statements on the date of initial adoption:

a) Employee benefits, Technical Pronouncement CPC 33 (IAS 19):

The Company does not have private pension plans characterized as a defined benefit plan;

b) Insurance contracts, Technical Pronouncement CPC 11 (IFRS 4):

The standard is not applicable to the Company’s operations;

c) Concession contracts, ICPC 01 (IFRIC 12):

The Company has no public service concession operations;

d) Effects of changes in exchange rates and conversion of financial statements,

Technical Pronouncement CPC 02 (IAS 21):

The rule does not apply to the Company’s operations.

e) Exemption on the measurement of compound financial instruments:

The Company does not have any operations with compound financial liabilities.

27

f) Investments in subsidiaries, assets and liabilities of subsidiaries, liabilities from the deactivation and transfer of customer assets:

These rules, which briefly allow adoption of a different transition date from January 1, 2009 for these issues, do not bring practical impacts for the first adoption of the CPCs by the Company.

In addition to voluntary exemptions, the CPC 37R (IFRS 1) also prescribes expressly prohibits adjustment of certain transactions on the first adoption, since the adoption in these areas require management to analyze past events after the results of such transactions. The mandatory exceptions include:

a) Accounting for assets and liabilities write-offs:

The Company has not retrospectively adjusted its financial assets and liabilities for the first adoption of the CPC;

b) Registration of hedge transactions:

The CPC 37R (IFRS 1) prohibits the retrospective application of hedge accounting methodology. However, since all of the Company’s hedge instruments have already been properly designated as such on the date of transition, this prohibition does not generate effects for the initial application of CPCs;

c) Changes in estimates:

Estimates taken in the transition to the CPC are consistent with estimates adopted by previous accounting standards;

d) Derecognition of financial assets and liabilities:

The Company has no operations that were subject to these standards.

Reconciliations of accounting practices adopted in teh preparation of financial statement previously disclosed

Pursuant to the CPC 37R (IFRS 1), the Company presents the reconciliation of the assets, liabilities, results, equity and cash flows, for the Parent Company and Consolidated, information previously disclosed for the periods of January 1, 2009 (transition date) and December 31, 2009, originally prepared based on practices adopted in Brazil (BRGAAP), in effect up to December 31, 2009, and international rules considering the CPCs in effect in 2010.

28

Opening Balance (January 1, 2009) Parent Company Consolidated

Originally Published Adjstments

Resubmitted (according to

the new CPCs) Note Originally Published Adjstments

Resubmitted (according to

the IFRSs) Total Assets 2,107,452 6,296 2,113,748 2,357,776 (45,174) 2,312,602 Current Assets 1,566,796 (70,626) 1,496,171 1,835,525 (71,149) 1,764,376 Cash and cash equivalents 26,673 - 26,673 37,324 - 37,324 Marketable securities 701,006 - 701,006 704,569 - 704,569 Customers accounts receivables 281,398 65,428 346,826 (a) 488,732 65,428 554,160 Inventories 308,394 (3,440) 304,954 (b) 344,647 (3,440) 341,207 Recoverable taxes 28,060 - 28,060 33,690 - 33,690 Deferred income and social contribution taxes 68,148 (68,148) - (c) 68,672 (68,672) - Prepaid expenses 112,845 (87,793) 25,052 (a) 112,853 (87,793) 25,060 Other receivables 40,272 23,328 63,600 (d) 45,038 23,328 68,366 Non Current Assets 540,656 76,922 617,577 522,251 25,975 548,226 Long-term assets 66,460 76,922 143,381 61,214 103,961 165,175 Deferred income and social contribution taxes 24,192 76,922 101,114

(a), (b), (c), (e) 26,267 103,961 130,228

Escrow deposits 6,156 - 6,156 6,175 - 6,175 Receivables from Related Parties 31,112 - 31,112 22,451 - 22,451 Other receivables 4,999 - 4,999 6,321 - 6,321 Fixed assets 474,196 - 474,196 461,037 (77,986) 383,051 Investiments 22,303 - 22,303 - - - Property and equipment 75,316 - 75,316 76,663 - 76,663 Intangible 299,227 - 299,227 306,388 - 306,388 Deferred charges 77,350 - 77,350 (e) 77,986 (77,986) - Total Liabilities 2,107,452 6,296 2,113,748 2,357,776 (45,174) 2,312,602 Current Liabilities 1,249,628 23,328 1,272,957 1,499,952 23,328 1,523,280 Suppliers 552,404 23,328 575,732 (d) 560,467 23,328 583,795 Loans and financing 592,311 - 592,311 808,878 - 808,878 Debentures 25,885 - 25,885 25,885 - 25,885 Wages and contributions 6,295 - 6,295 8,737 - 8,737 Taxes Payable 29,508 - 29,508 31,898 - 31,898 Dividends payable 18,012 - 18,012 18,012 - 18,012 Other payable 25,213 - 25,214 46,075 - 46,075 Non Current Liabilities 650,233 - 650,233 650,233 - 650,233 Long-term liabilities 650,233 - 650,233 650,233 - 650,233 Loans and financing 272,774 - 272,774 272,774 - 272,774 Debentures 362,908 - 362,908 362,908 - 362,908 Provisions for contingencies 4,270 - 4,270 4,270 - 4,270 Other payable 10,281 - 10,281 10,281 - 10,281 Stockholders’ equity 207,591 (17,033) 190,558 207,591 (68,502) 139,089 Capital Stock 181,566 - 181,566 181,566 - 181,566 Capital reserves 203,508 - 203,508 203,508 - 203,508 (-) Treasury Shares (200,000) - (200,000) (200,000) - (200,000) Equity Adjustment (861) - (861) (861) - (861)

Profit reserves 45,261 (17,033) 28,228 (a), (b),

(e) 45,261 (68,502) (23,241) (-)Treasury Shares (21,883) - (21,883) (21,883) - (21,883)

29

Balance Sheet on December 31,2009

Parent Company Consolidated

Originally Published

Adjstments

Resubmitted (according to the

new CPCs) Note Originally Published

Adjstments

Resubmitted (according to the

IFRSs) Total Assets 2,144,629 18,230 2,162,859 2,320,210 (16,274) 2,303,936 Current Assets 1,486,566 (36,386) 1,450,180 1,685,297 (38,864) 1,646,433 Cash and cash equivalents 56,974 - 56,974 62,047 - 62,047 Marketable securities 540,010 - 540,010 547,832 - 547,832 Customers accounts receivables 237,352 34,913 272,265 (a) 389,374 34,913 424,287 Inventories 468,511 (4,828) 463,683 (b) 490,397 (4,828) 485,569 Recoverable taxes 58,992 0 58,992 64,221 - 64,221 Deferred income and social contribution taxes 36,896 (36,896) - (c) 39,373 (39,373) - Prepaid expenses 71,334 (58,940) 12,394 (a) 72,802 (58,940) 13,862 Other receivables 16,498 29,364 45,862 (d) 19,251 29,364 48,615 Non Current Assets 658,063 54,616 712,679 634,913 22,590 657,503 Long-term assets 106,480 46,706 153,186 96,137 75,698 171,835 Deferred income and social contribution taxes 44,784 46,706 91,490

(a), (b), (c), (e) 44,784 75,698 120,483

Escrow deposits 12,069 - 12,069 12,289 - 12,289 Receivables from Related Parties 45,794 - 45,794 33,744 - 33,744 Other receivables 3,833 - 3,833 5,319 - 5,319 Fixed assets 551,583 7,910 559,493 538,776 (53,108) 485,668 Investiments 29,970 - 29,970 - - - Property and equipment 88,011 - 88,011 92,826 - 92,826 Intangible 373,183 7,910 381,093 (f) 384,932 7,910 392,842 Deferred charges 60,419 - 60,419 (e) 61,018 (61,018) - Total Liabilities 2,144,629 18,230 2,162,859 2,320,210 (16,274) 2,303,936 Current Liabilities 796,003 29,364 825,367 971,584 29,364 1,000,948 Suppliers 538,878 29,364 568,242 (d) 551,569 29,364 580,933 Loans and financing 182,491 - 182,491 327,929 - 327,929 Debentures 17,835 - 17,835 17,835 - 17,835 Salaries and social charges security 6,278 - 6,278 8,240 - 8,240 Taxes Payable 10,261 - 10,261 19,009 - 19,009 Dividends payable 11,308 - 11,308 11,308 - 11,308 Other payable 28,952 - 28,952 35,694 - 35,694 Non Current Liabilities 1,101,659 2,689 1,104,348 1,101,658 8,459 1,110,116 Long-term liabilities 1,101,659 2,689 1,104,348 1,101,658 8,459 1,110,116 Loans and financing 710,181 - 710,181 710,181 - 710,181 Debentures 363,244 - 363,244 363,244 0 363,244 Deferred income and social contribution taxes 5,208 2,689 7,897 (f) 5,208 8,458 13,666 Provisions for contingencies 13,517 - 13,517 13,517 - 13,517 Other payable 9,509 - 9,509 9,508 0 9,508 Stockholders’ equity 246,968 (13,824) 233,144 246,968 (54,096) 192,872 Capital Stock 181,566 - 181,566 181,566 - 181,566 Capital reserves 205,291 - 205,291 205,291 - 205,291 (-) Treasury Shares (200,000) - (200,000) (200,000) - (200,000) Equity Adjustment 1,250 - 1,250 1,250 - 1,250

Profit reserves 81,562 (17,033) 64,529 (a), (b), (e), (f) 81,562 (57,305) 24,257

(-)Treasury Shares (22,701) - (22,701) (22,701) - (22,701) Total Assets - 3,209 3,209 - 3,209 3,209

30

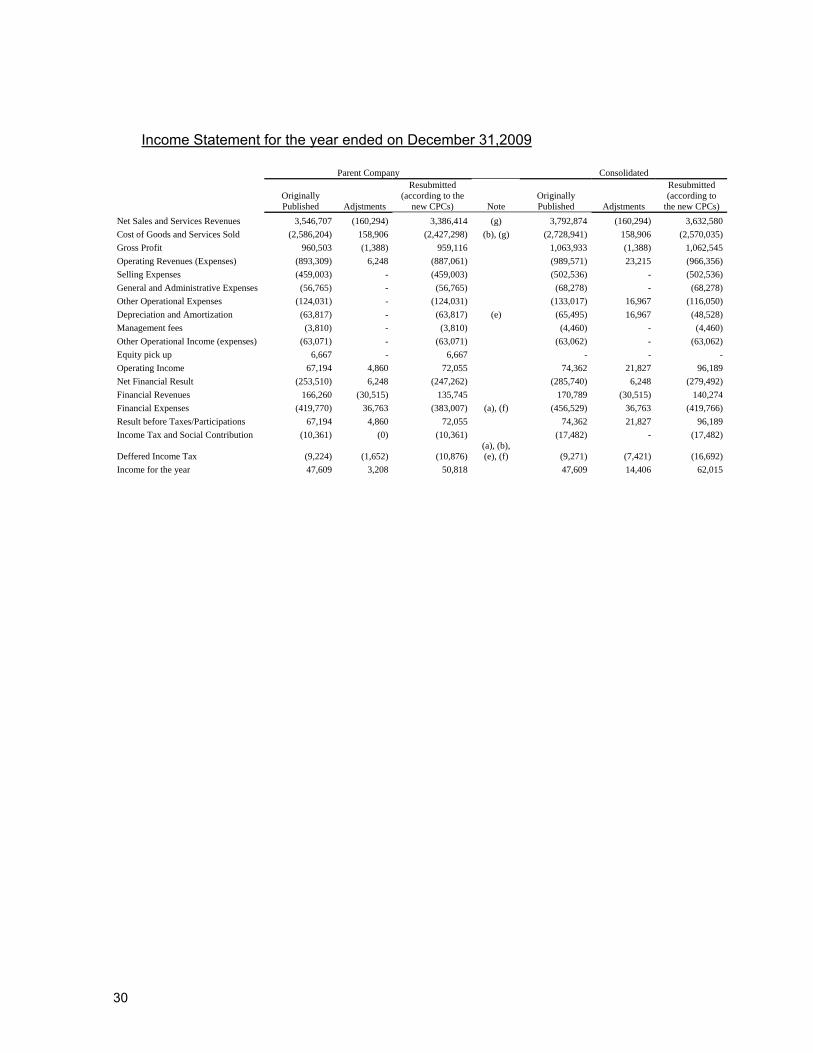

Income Statement for the year ended on December 31,2009

Parent Company Consolidated

Originally Published Adjstments

Resubmitted (according to the

new CPCs) Note Originally Published Adjstments

Resubmitted (according to

the new CPCs) Net Sales and Services Revenues 3,546,707 (160,294) 3,386,414 (g) 3,792,874 (160,294) 3,632,580 Cost of Goods and Services Sold (2,586,204) 158,906 (2,427,298) (b), (g) (2,728,941) 158,906 (2,570,035) Gross Profit 960,503 (1,388) 959,116 1,063,933 (1,388) 1,062,545 Operating Revenues (Expenses) (893,309) 6,248 (887,061) (989,571) 23,215 (966,356) Selling Expenses (459,003) - (459,003) (502,536) - (502,536) General and Administrative Expenses (56,765) - (56,765) (68,278) - (68,278) Other Operational Expenses (124,031) - (124,031) (133,017) 16,967 (116,050) Depreciation and Amortization (63,817) - (63,817) (e) (65,495) 16,967 (48,528) Management fees (3,810) - (3,810) (4,460) - (4,460) Other Operational Income (expenses) (63,071) - (63,071) (63,062) - (63,062) Equity pick up 6,667 - 6,667 - - - Operating Income 67,194 4,860 72,055 74,362 21,827 96,189 Net Financial Result (253,510) 6,248 (247,262) (285,740) 6,248 (279,492) Financial Revenues 166,260 (30,515) 135,745 170,789 (30,515) 140,274 Financial Expenses (419,770) 36,763 (383,007) (a), (f) (456,529) 36,763 (419,766) Result before Taxes/Participations 67,194 4,860 72,055 74,362 21,827 96,189 Income Tax and Social Contribution (10,361) (0) (10,361) (17,482) - (17,482)

Deffered Income Tax (9,224) (1,652) (10,876) (a), (b), (e), (f) (9,271) (7,421) (16,692)

Income for the year 47,609 3,208 50,818 47,609 14,406 62,015

31

Cash Flow Statement for the year ended on December 31,2009

Parent Company Consolidated

Originally Published Adjstments

Resubmitted

(according to the new CPCs)

Originally Published Adjstments Adjstments

Resubmitted (according to

the new CPCs) Operating Activities: Net Income of the period 47,609 3,209 50,818 47,609 14,406 62,015 Adjust for non cash and non operating items: Present Value Adjustment (16,281) 16,281 - (a) (16,281) 16,281 - Depreciation and amortization 63,817 - 63,817 (e) 65,495 (16,967) 48,528

Deferred income tax and social contribution 9,224 1,652 10,876 (a), (b), (e),

(f) 9,271 7,421 16,692 Interest, monetary and currency changes 252,004 (6,248) 245,756 (a), (f) 275,188 (6,248) 268,940 Equity result in subsidiaries (6,667) - (6,667) - - -

Others 15,952 (14,894) 1,058 (a), (b), (e),

(f) 22,410 (14,893) 7,517 Adjusted Net Income (Cash Earnings) 365,658 - 365,658 403,692 - 403,692 (Increase) decrease in assets: Accounts receivable (14,606) 13,313 (1,293) (a) 12,628 13,313 25,941

Inventory (158,535) - (158,535) (144,168) - (144,168) Taxes recoverable (30,562) - (30,562) (28,724) - (28,724) Prepaid expenses (3,334) - (3,334) (4,794) - (4,794) Escrow deposits (5,913) - (5,913) (6,114) - (6,114) Accounts receivable related parties - (14,356) (14,356) - (11,130) (11,130) Other accounts receivable (current and non-current) (18,234) 43,177 24,943 (a) (14,456) 40,904 26,448 (231,184) 42,134 (189,050) (185,628) 43,087 (142,541) (Increase) decrease in liabilities: Suppliers 24,717 (41,128) (16,411) (a) 29,345 (41,128) (11,783) Salaries and social charges security (17) - (17) (497) - (497) Taxes recoverable (current and non-current) (19,247) - (19,247) (12,890) - (12,890) Related parties payables 2,183 (2,183) - 2,183 (2,183) -

Deferred income tax and social contribution - 5,208 5,208 (a), (b), (e),

(f) - 5,208 5,208 Other liabilities (current and non-current) 2,043 (5,207) (3,164) (12,077) (5,208) (17,285) 9,679 (43,310) (33,631) 6,064 (43,311) (37,247) Cash flow from operating activities 144,153 (1,176) 142,977 224,128 (224) 223,904 Investing Activities Investment in subsidiaries and jointly controled compananies (1,000) - (1,000) - - - Fixed Assets (133,537) - (133,537) (143,234) - (143,234) Property and equipment (26,656) - (26,656) (30,959) - (30,959) Intangible (106,881) - (106,881) (112,275) - (112,275) Cash Flow from investing activities (134,537) - (134,537) (143,234) - (143,234) Financing Activities Loans and financing Additions 560,949 - 560,949 560,949 - 560,949 Payments (636,380) - (636,380) (730,960) - (730,960) Debentures (51,082) 224 (50,858) (51,082) 224 (50,858) Marketable Securities 196,962 - 196,962 193,066 - 193,066 Discount of receivables (30,934) 952 (29,982) (a) (9,314) - (9,314) Shares repurchase (818) - (818) (818) - (818) Dividends paid (18,012) - (18,012) (18,012) - (18,012) Cash Flow from financing activities 20,685 1,176 21,861 (56,171) 224 (55,947) Changes in cash balance 30,301 30,301 24,723 24,723 Beginning Cash Balance 26,673 26,673 37,324 37,324 Ending Cash Balance 56,974 56,974 62,047 62,047

32

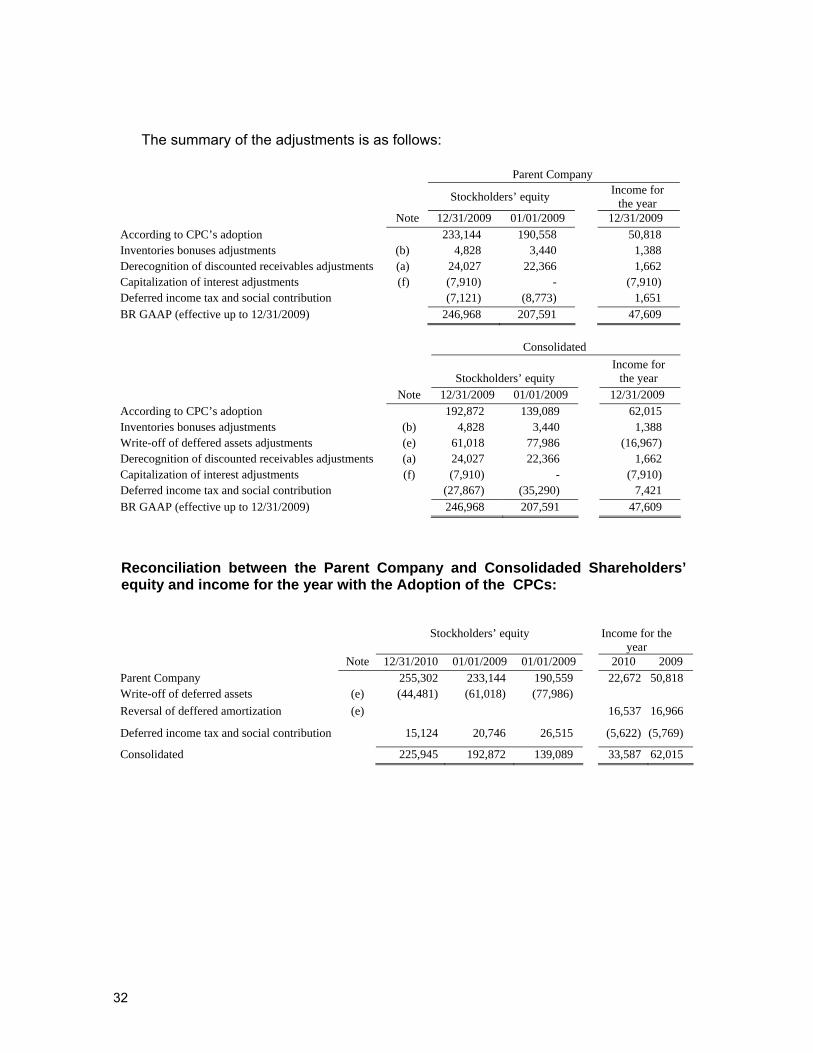

The summary of the adjustments is as follows:

Parent Company

Stockholders’ equity Income for the year

Note 12/31/2009 01/01/2009 12/31/2009 According to CPC’s adoption 233,144 190,558 50,818 Inventories bonuses adjustments (b) 4,828 3,440 1,388 Derecognition of discounted receivables adjustments (a) 24,027 22,366 1,662 Capitalization of interest adjustments (f) (7,910) - (7,910) Deferred income tax and social contribution (7,121) (8,773) 1,651 BR GAAP (effective up to 12/31/2009) 246,968 207,591 47,609

Consolidated

Stockholders’ equity Income for

the year Note 12/31/2009 01/01/2009 12/31/2009 According to CPC’s adoption 192,872 139,089 62,015 Inventories bonuses adjustments (b) 4,828 3,440 1,388 Write-off of deffered assets adjustments (e) 61,018 77,986 (16,967) Derecognition of discounted receivables adjustments (a) 24,027 22,366 1,662 Capitalization of interest adjustments (f) (7,910) - (7,910) Deferred income tax and social contribution (27,867) (35,290) 7,421 BR GAAP (effective up to 12/31/2009) 246,968 207,591 47,609

Reconciliation between the Parent Company and Consolidaded Shareholders’ equity and income for the year with the Adoption of the CPCs:

Stockholders’ equity Income for the

year Note 12/31/2010 01/01/2009 01/01/2009 2010 2009 Parent Company 255,302 233,144 190,559 22,672 50,818 Write-off of deferred assets (e) (44,481) (61,018) (77,986) Reversal of deffered amortization (e) 16,537 16,966

Deferred income tax and social contribution 15,124 20,746 26,515 (5,622) (5,769)

Consolidated 225,945 192,872 139,089 33,587 62,015

33

The main adjustments and reclassifications are described below:

a) Derecognition of accounts receivable:

Receivables discounted with credit card operators, previously recorded as a reduction of accounts receivable balance, qualified for derecognition in accordance with the CPC 38. Accordingly, the present value adjustment previously calculated on the total receivables balance was recalculated to disregard the portion of the derecognized assets, resulting in the acceleration of their realization, which was recorded as “Financial income.” Similarly, interest incurred on prepayment of receivables with the credit card administrators, previously recorded as prepaid expenses and charged to income in accordance with the original maturities of discounted receivables, was fully recognized as “Financial expense.”

b) Vendor allowances:

In accordance with the CPC 16, trade discounts, rebates, subsidies and/or other revenues received from suppliers are deducted to determine the cost of inventory and are only recognized in the income statement upon sale of the product to which they are linked. This adjustment relates to the reversal of the funds received from suppliers, whose linked product has not yet been sold on the base date of preparation of financial statements.

c) Reclassification of deferred taxes to non-current assets:

The CPC 26 prohibits the classification of deferred taxes as current assets and/or liabilities.

d) Receivables from vendors:

The receivables from vendors, before being presented as a reduction of accounts payable to suppliers, was reclassified to current assets, in accordance with the CPC 26, which prevents the netting of assets and liabilities, except when a legal condition exists to make their payment in this manner.

e) Write-off of deferred assets:

The adjustment refers to the write-off of deferred assets, as well as a reversal of its corresponding amortization expense in consolidated financial statements, as required by the CPC 43 (R1), such that these financial statements are in compliance with IFRS.

f) Capitalization of interest:

The CPC 20 requires the capitalization of borrowing costs attributable to the acquisition, construction and/or production of a qualifying asset. The adjustment

34

in question refers to the capitalization of borrowing costs related to developments of software and websites for the Company.

g) Net revenue:

Piece of the income from subsidies, previously registered as sales revenue, was reclassified as a reduction in the cost of the sales of goods.

Restatement of 2010 quarterly reports, compared with 2009, also adjusted by the CPCs in effect on December 31, 2010.

As permitted by CVM Resolution 656 of January 25, 2011, the Company chose to restate the quarterly reports for the quarters ended on March 31, June 30 and September 30, 2010 up to the quarterly report for the quarter ending on March 31, 2011. Thus, in accordance with the requirement of CVM Resolution, the Company presents below the effects on income and equity for the quarters ended March 31, June 30 and September 30, 2010 and 2009, resulting from the adoption of the CPCs in effect on December 31, 2010.

35

Reconciliation of the Shareholders’ equity:

09/30/2010 06/30/2010 03/31/2010 09/30/2009 06/30/2009 03/31/2009 Restated Shareholders’ equity (according to the new CPCs)

276,976 259,641 243,947 223,189 216,736 214,801

Inventories bonuses adjustments

3,890 5,153 3,729 4,272 4,186 5,350 Derecognition of discounted receivables adjustments

11,226 17,426

23,335 31,539 21,320 (1,782)

Revision of the useful life of fixed and intangible assets

(18,883)

(12,424)

(6,183) - - -

Capitalization of interest adjustments

(17,644)

(15,462)

(10,720)

(5,732)

(3,712) (2,036)Deferred income tax and social contribution

7,280 1,805

(3,454)

(10,227)

(7,410) (521)

Shareholders’ equity originally published

262,845 256,139 250,654 243,041 231,120 215,812

Reconciliation of the quarter’s net income:

09/30/2010 06/30/2010 03/31/2010 09/30/2009 06/30/2009 03/31/2009 Restated Net Income (according to the new CPCs)

13,156 15,239 11,326 4,653 16,712 9,280

Inventories bonuses adjustments

(1,263) 1,424

(1,099) 86

(1,164) 1,910 Derecognition of discounted receivables adjustments

(6,200)

(5,909)

(692) 10,219 736

(1,782)

Revision of the useful life of fixed and intangible assets

(6,459)

(6,241)

(6,183) - - -

Capitalization of interest adjustments

(2,182)

(4,742)

(2,810)

(2,020)

(1,676)

(2,036)Deferred income tax and social contribution

5,475 5,259 3,667

(2,817) 716 648

Net Income originally published

2,527 5,030 4,209 10,121 15,324 8,020

36

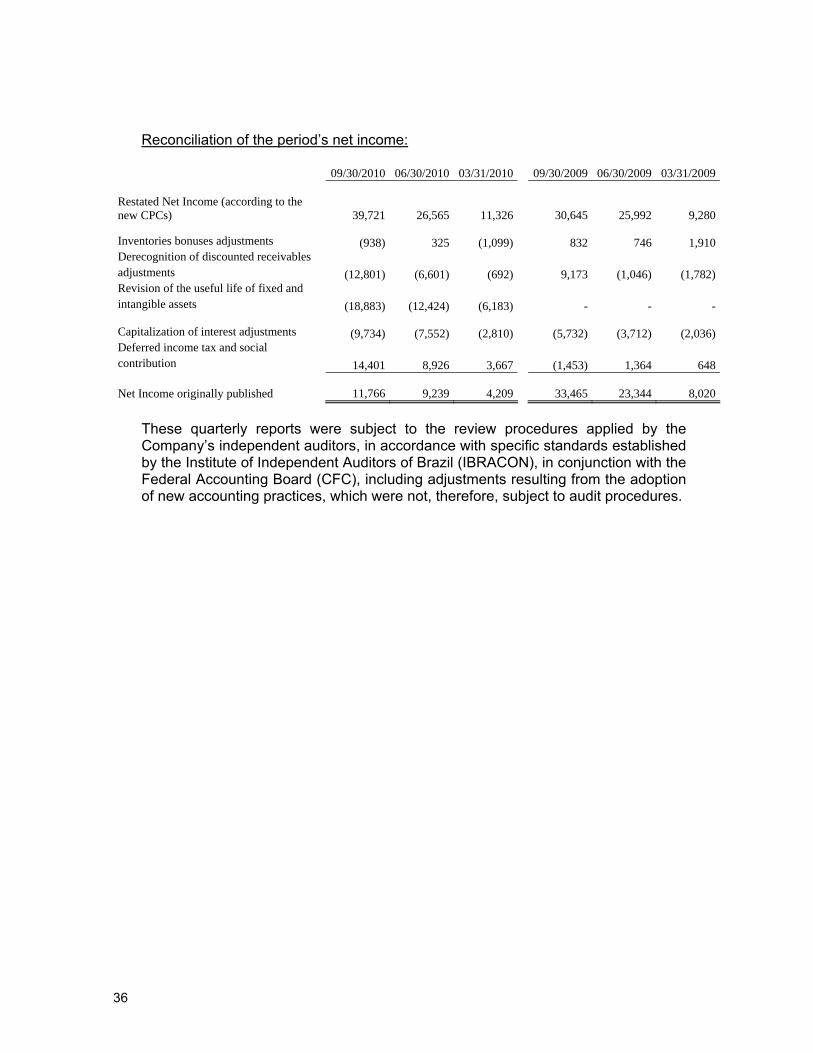

Reconciliation of the period’s net income:

09/30/2010 06/30/2010 03/31/2010 09/30/2009 06/30/2009 03/31/2009 Restated Net Income (according to the new CPCs)

39,721 26,565 11,326 30,645 25,992 9,280

Inventories bonuses adjustments

(938) 325

(1,099) 832 746 1,910 Derecognition of discounted receivables adjustments

(12,801)

(6,601)

(692) 9,173

(1,046)

(1,782)

Revision of the useful life of fixed and intangible assets

(18,883)

(12,424)

(6,183) - - -

Capitalization of interest adjustments

(9,734)

(7,552)

(2,810)

(5,732)

(3,712)

(2,036)Deferred income tax and social contribution

14,401 8,926 3,667

(1,453) 1,364 648

Net Income originally published

11,766 9,239 4,209 33,465 23,344 8,020

These quarterly reports were subject to the review procedures applied by the Company’s independent auditors, in accordance with specific standards established by the Institute of Independent Auditors of Brazil (IBRACON), in conjunction with the Federal Accounting Board (CFC), including adjustments resulting from the adoption of new accounting practices, which were not, therefore, subject to audit procedures.

37

New IFRS and IFRIC interpretations

The new accounting procedures from the International Accounting Standards Board (IASB), and interpretations from the International Financial Reporting Interpretations Committee (IFRIC), have been published and/or revised. Their adoption is optional or mandatory for the years beginning on January 1, 2010, not yet comment or related modifications by CPC. It is expected that the Brazilian standards will be modified to converge to international standards by the time the standards will be enforced. Below are some of the principal standards published but not yet in effect, as well as the expected impact on the Company’s Financial Statements:

IFRS 9 Financial Instruments - Classification and Measurement - The IFRS 9

concludes the first part of the project for the substitution of the “IAS 39 Financial Instruments: Recognition and Measurement”. IFRS 9 uses a simple approach to determine whether a financial asset is measured at amortized cost or fair value, based on the way in which an entity manages its financial instruments (its business model) and the typical contractual cash flows of financial assets. The standard also requires the adoption of only one method for determining the amount of losses of recoverable assets. This standard becomes effective for fiscal years beginning January 1, 2013. The Company does not expect this change to have a significant impact on its financial statements.

IFRIC 14 Prepayments of a Minimum Funding Requirement – This amendment

applies only to those situations where an entity is subject to minimum requirement funding contributions and advances to cover these requirements. The change allows the entity to account for the benefit of such prepayment as an asset. This amendment is effective for fiscal years beginning on or after January 1, 2011. The Company will not suffer any impact from this interpretation.

IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments – The IFRIC

19 was issued in November 2009 and became effective on July 1, 2010, and early implementation was allowed. This interpretation clarifies the requirements of the International Financial Reporting Standards (IFRS) when an entity renegotiates the terms of a financial obligation and the lender agrees to accept this and the actions of the entity or other equity instruments to settle the financial obligation in whole or in part. The Company does not expect that IFRIC 19 would have a significant impact on its Financial Statements.

IFRS Improvements - The IASB issued improvements to the IFRS standards

and amendments in May 2010 and the amendments will be effective from January 1, 2011. The main changes that could impact the Company are shown below:

IFRS 3 - Business Mergers IFRS 7 - Financial Instruments Disclosures IAS 1 - Presentation of Financial Statements IAS 27 - Consolidated and individual Financial Statements IFRIC 13 - Customer Loyalty Program

38

The Company does not expect the changes to have a significant impact on its Financial Statements.

5. Marketable Securities

Parent Company Consolidated 12/31/2010 12/31/2009 1/1/2009 12/31/2010 12/31/2009 1/1/2009

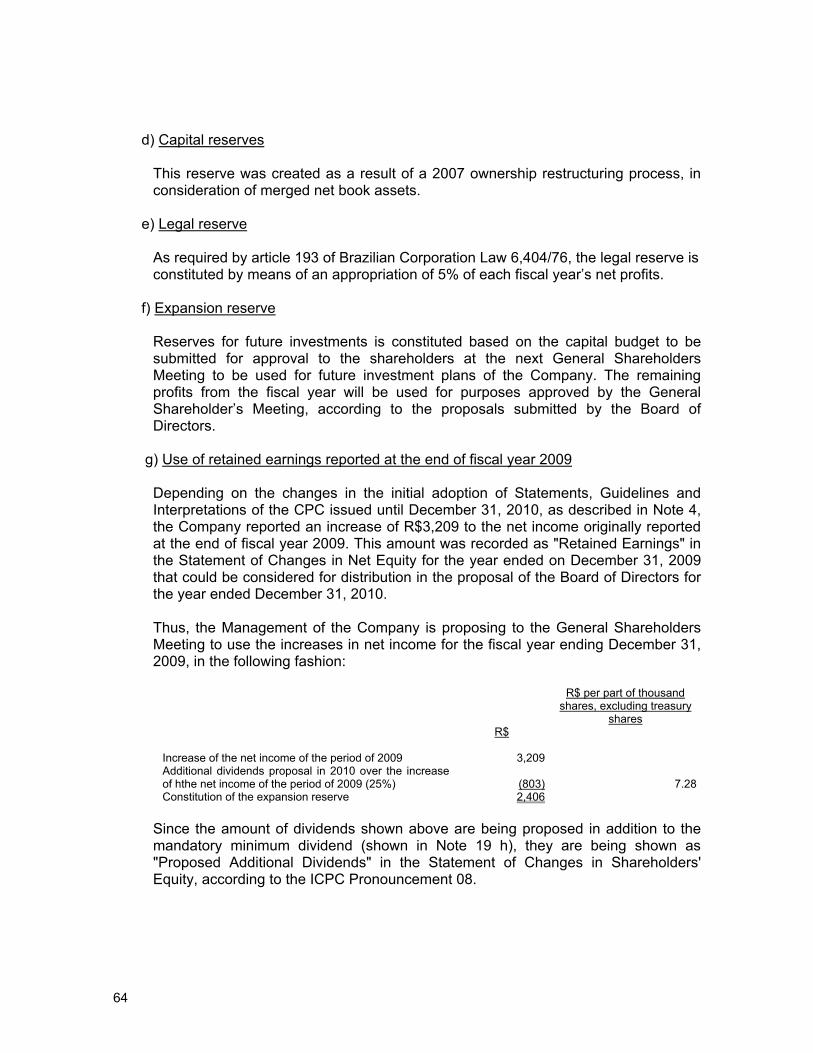

Certificates of bank – deposits - CDBs 582,632 238,537 336,293 594,761 241,230 338,732Debentures 194,341 301,473 364,713 195,946 306,602 365,837 776,973 540,010 701,006 790,707 547,832 704,569