financial planning association of central virginia forum 2014 · misleading marketing and...

TRANSCRIPT

Registered Investment AdviserRegulatory Update

Presentation by:

Jim Van Horn, Jr., Co-Managing Partner

Investment Management Practice Group

Hirschler Fleischer, PC

June 5, 2014

Financial Planning Association of Central VirginiaForum 2014

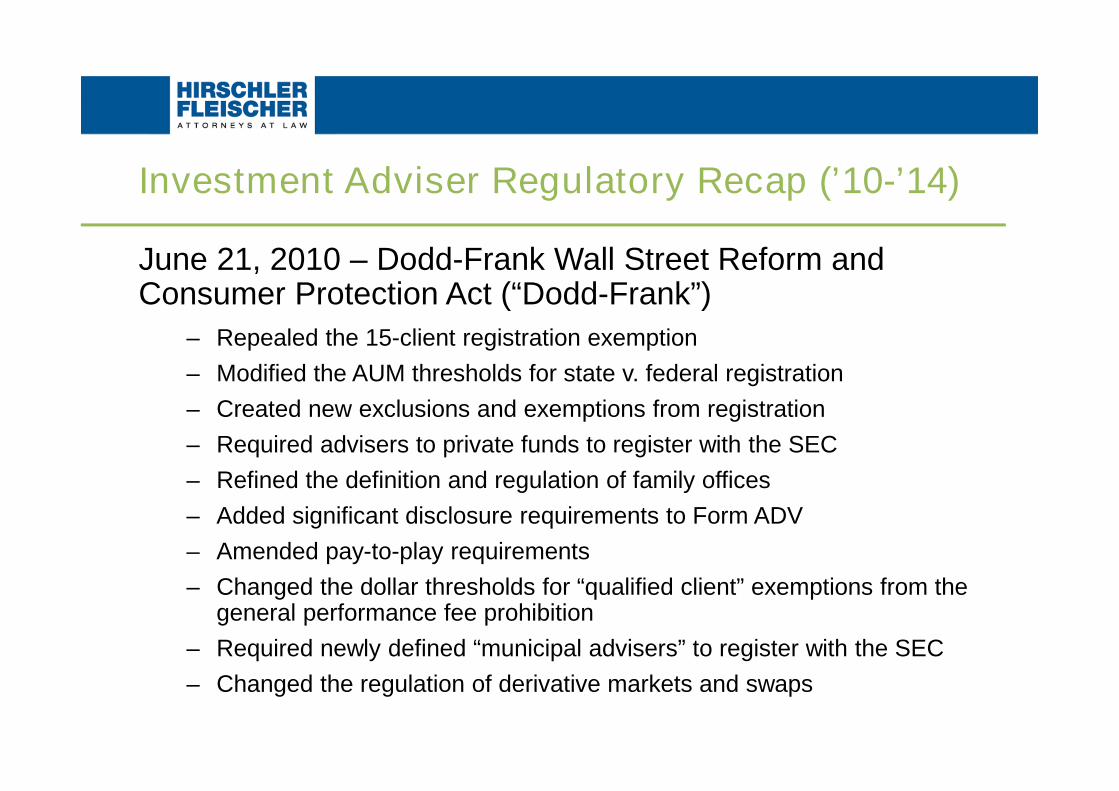

Investment Adviser Regulatory Recap (’10-’14)

June 21, 2010 – Dodd-Frank Wall Street Reform andConsumer Protection Act (“Dodd-Frank”)

– Repealed the 15-client registration exemption

– Modified the AUM thresholds for state v. federal registration

– Created new exclusions and exemptions from registration

– Required advisers to private funds to register with the SEC

– Refined the definition and regulation of family offices

– Added significant disclosure requirements to Form ADV

– Amended pay-to-play requirements

– Changed the dollar thresholds for “qualified client” exemptions from thegeneral performance fee prohibition

– Required newly defined “municipal advisers” to register with the SEC

– Changed the regulation of derivative markets and swaps

Investment Adviser Regulatory Recap (’10-’14)

Rulemaking– Amendments to Form ADV (July 28, 2010)

– Political Contributions by Certain Investment Advisers (Pay-to-Play Rules) (July 1, 2010)

– Rules Implementing Amendments to Investment Advisers Act (June 22, 2011)

– Family Office Definition and Exemption (June 22, 2011)

– Venture Capital Fund, Private Fund Adviser and Foreign Adviser Registration Exemptions (June 22,2011)

– Registration of Private Fund Advisers, Reallocation of Mid-Sized Advisers (i.e., $25mm - $100mm)from SEC to State (June 22, 2011)

– Reporting by Investment Advisers to Private Funds (Form PF) (October 31, 2011)

– Net Worth Standard for Accredited Investors (Dec. 21, 2011)

– Investment Adviser Performance Compensation (Feb. 15, 2012)

– Identity Theft Red Flags (April 10, 2013)

– Eliminating the Prohibition Against General Solicitation and General Advertising in Rule 506and Rule 144A Offerings (Jul. 10, 2013)

– Disqualifications of Felons and Other “Bad Actors” from Rule 506 Offerings (Jul. 10, 2013)

– Broker-Dealer Reporting and Financial Responsibility Rules (Jul. 30, 2013)

Investment Adviser Regulatory Recap (’10-’14)

FAQs

– Staff Responses to Questions about Part 2 of Form ADV (March 18, 2012)

– Frequently Asked Questions Regarding Mid-Sized Advisers (June 28, 2011)

– Staff Responses to Questions about the Custody Rule (December 13, 2011)

– Staff Responses to Questions about the Family Office Rule (April 27, 2012)

– Staff Responses to Questions about the Pay-to-Play Rule (July 27, 2012)

– Frequently Asked Questions about Form ADV (August 30, 2012)

– Frequently Asked Questions about Form PF (April 25, 2013)

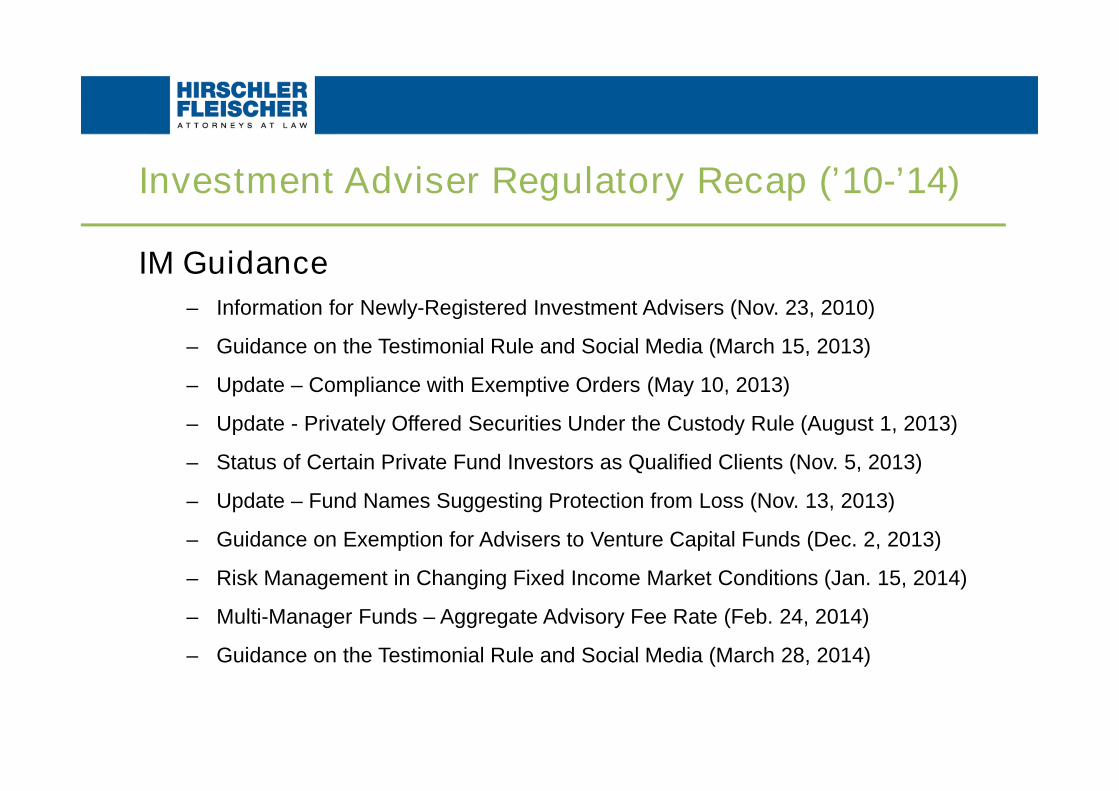

Investment Adviser Regulatory Recap (’10-’14)

IM Guidance

– Information for Newly-Registered Investment Advisers (Nov. 23, 2010)

– Guidance on the Testimonial Rule and Social Media (March 15, 2013)

– Update – Compliance with Exemptive Orders (May 10, 2013)

– Update - Privately Offered Securities Under the Custody Rule (August 1, 2013)

– Status of Certain Private Fund Investors as Qualified Clients (Nov. 5, 2013)

– Update – Fund Names Suggesting Protection from Loss (Nov. 13, 2013)

– Guidance on Exemption for Advisers to Venture Capital Funds (Dec. 2, 2013)

– Risk Management in Changing Fixed Income Market Conditions (Jan. 15, 2014)

– Multi-Manager Funds – Aggregate Advisory Fee Rate (Feb. 24, 2014)

– Guidance on the Testimonial Rule and Social Media (March 28, 2014)

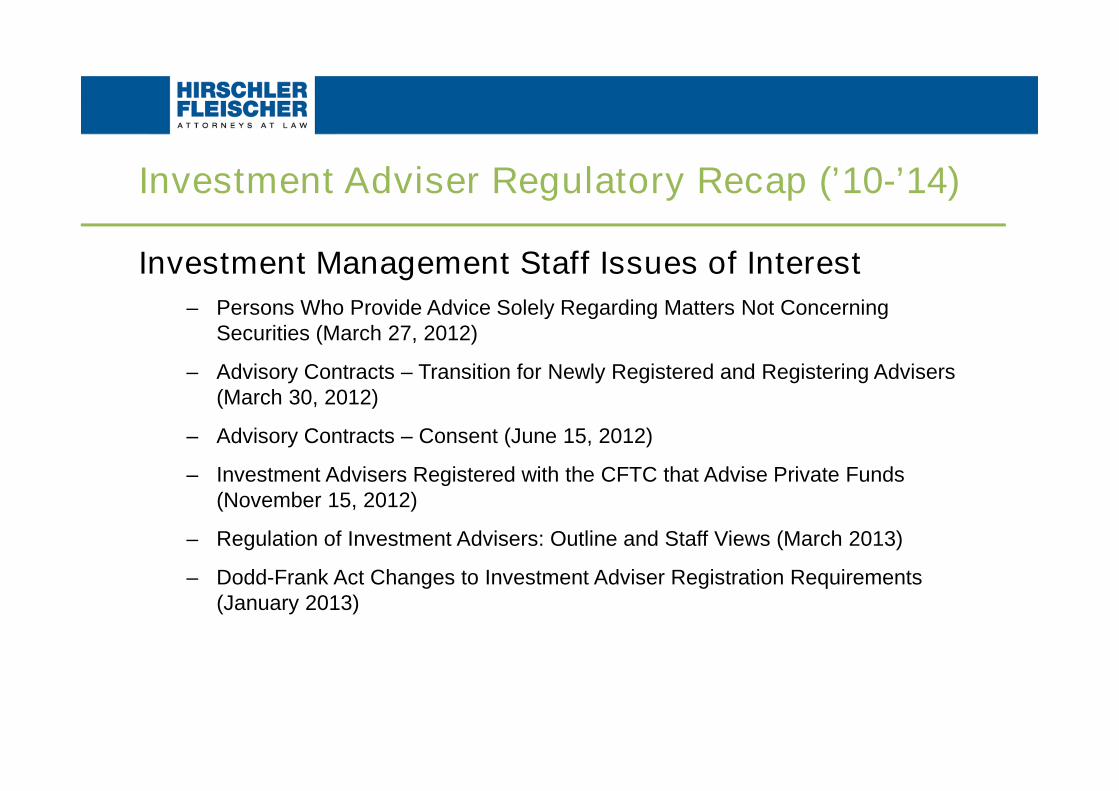

Investment Adviser Regulatory Recap (’10-’14)

Investment Management Staff Issues of Interest

– Persons Who Provide Advice Solely Regarding Matters Not ConcerningSecurities (March 27, 2012)

– Advisory Contracts – Transition for Newly Registered and Registering Advisers(March 30, 2012)

– Advisory Contracts – Consent (June 15, 2012)

– Investment Advisers Registered with the CFTC that Advise Private Funds(November 15, 2012)

– Regulation of Investment Advisers: Outline and Staff Views (March 2013)

– Dodd-Frank Act Changes to Investment Adviser Registration Requirements(January 2013)

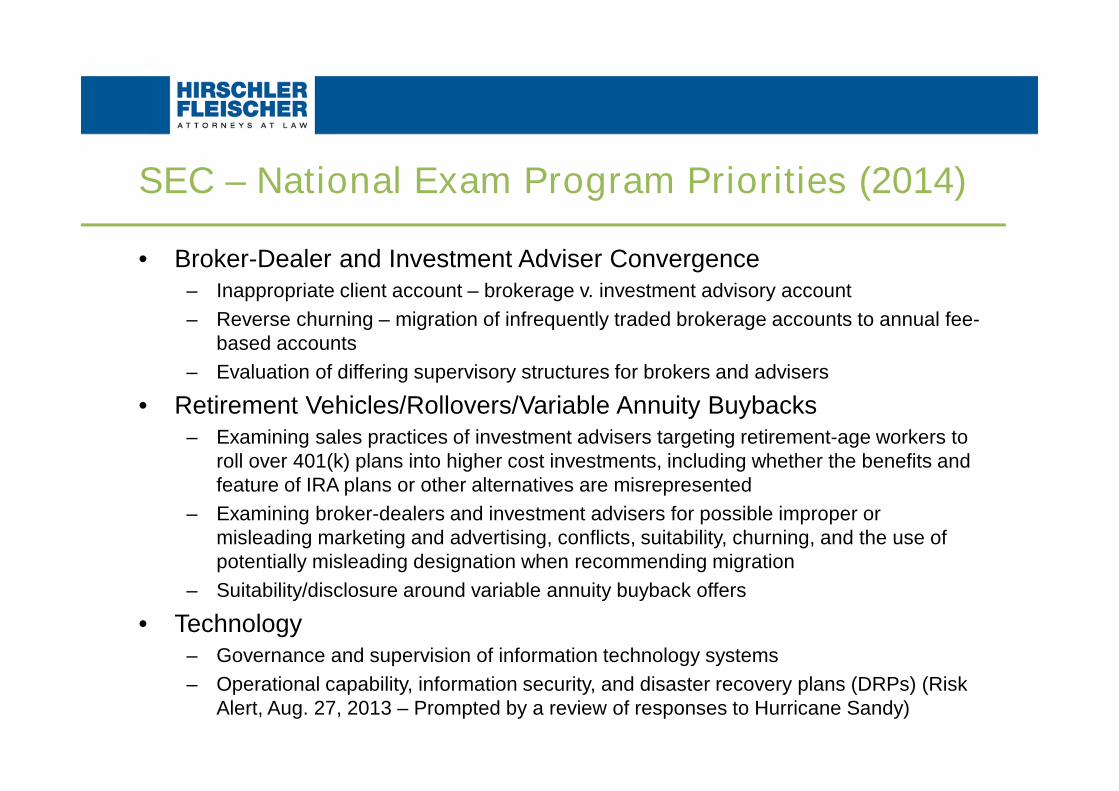

SEC – National Exam Program Priorities (2014)

• Broker-Dealer and Investment Adviser Convergence– Inappropriate client account – brokerage v. investment advisory account

– Reverse churning – migration of infrequently traded brokerage accounts to annual fee-based accounts

– Evaluation of differing supervisory structures for brokers and advisers

• Retirement Vehicles/Rollovers/Variable Annuity Buybacks– Examining sales practices of investment advisers targeting retirement-age workers to

roll over 401(k) plans into higher cost investments, including whether the benefits andfeature of IRA plans or other alternatives are misrepresented

– Examining broker-dealers and investment advisers for possible improper ormisleading marketing and advertising, conflicts, suitability, churning, and the use ofpotentially misleading designation when recommending migration

– Suitability/disclosure around variable annuity buyback offers

• Technology– Governance and supervision of information technology systems

– Operational capability, information security, and disaster recovery plans (DRPs) (RiskAlert, Aug. 27, 2013 – Prompted by a review of responses to Hurricane Sandy)

SEC – National Exam Program Priorities (2014)

• Rule 506(c) Offerings– Review of marketing activities used in a new Rule 506(c) offering

– Adherence to “Bad Actor” rules

– Evaluate the due diligence conducted by broker-dealers and investment advisersused to verify “accredited investor” status of investors

• Safety of Assets and Custody– Failure to recognize when an adviser has custody (e.g., the adviser serves as

trustee, is authorized to write or sign checks for clients, or is authorized to makewithdrawals from a client’s account as part of bill-paying services)

– Failure to meet the custody rule’s surprise examination requirements

– Failure to engage independent accountants for audit pooled investment vehicles

– Failure to satisfy the custody rule’s qualified custodian requirements (e.g.,commingling client, proprietary, and employee assets in a single account, orlacking a reasonable basis to believe that a qualified custodian is sendingquarterly account statements to the client)

– Handling of physical stock certificates (especially private stock certificates)

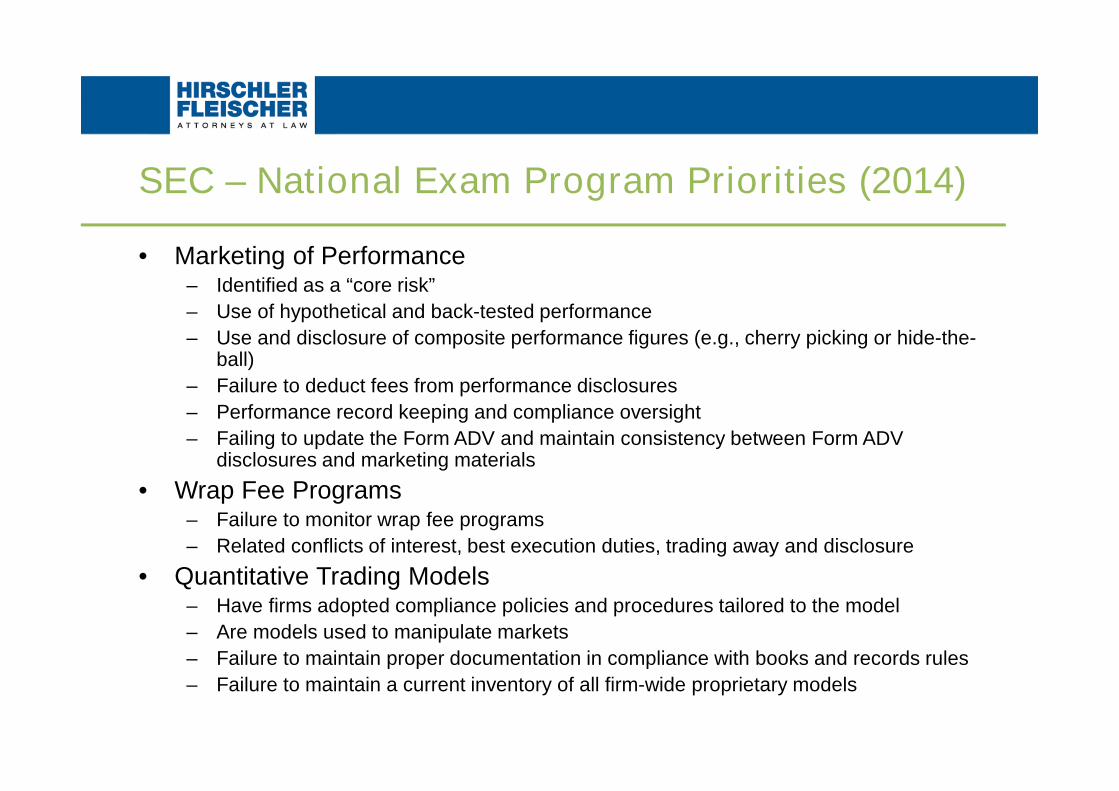

SEC – National Exam Program Priorities (2014)

• Marketing of Performance– Identified as a “core risk”

– Use of hypothetical and back-tested performance

– Use and disclosure of composite performance figures (e.g., cherry picking or hide-the-ball)

– Failure to deduct fees from performance disclosures

– Performance record keeping and compliance oversight

– Failing to update the Form ADV and maintain consistency between Form ADVdisclosures and marketing materials

• Wrap Fee Programs– Failure to monitor wrap fee programs

– Related conflicts of interest, best execution duties, trading away and disclosure

• Quantitative Trading Models– Have firms adopted compliance policies and procedures tailored to the model

– Are models used to manipulate markets

– Failure to maintain proper documentation in compliance with books and records rules

– Failure to maintain a current inventory of all firm-wide proprietary models

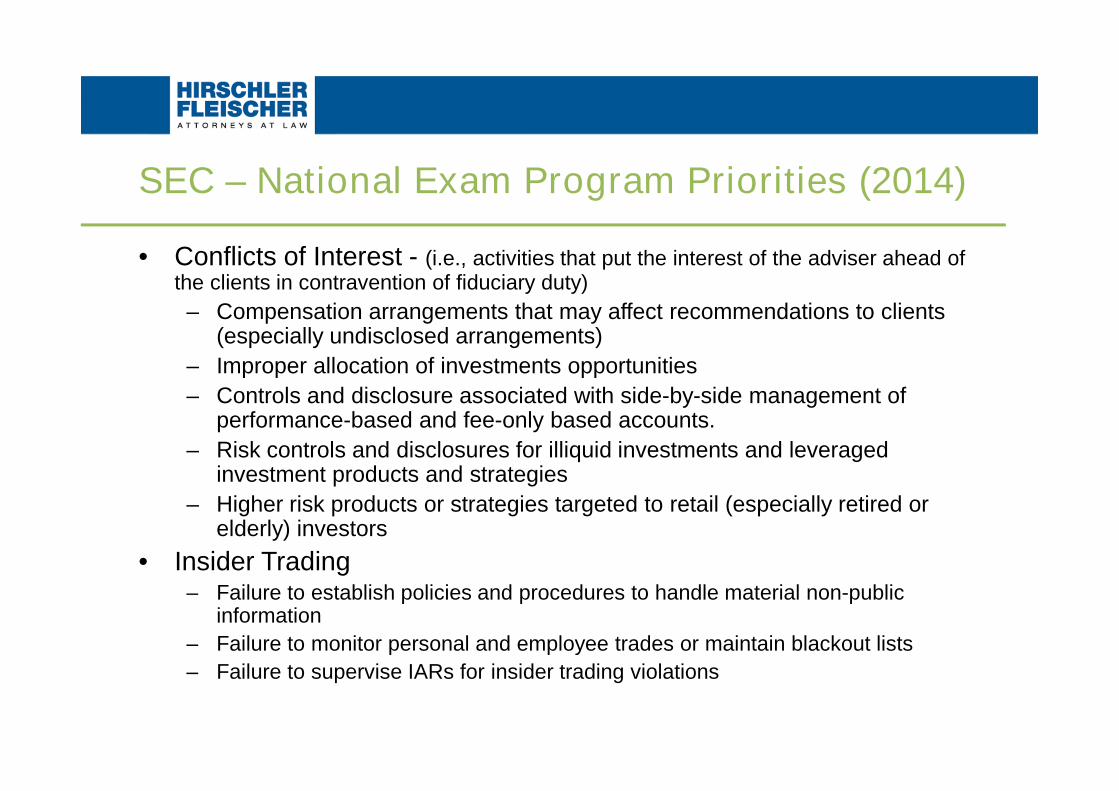

SEC – National Exam Program Priorities (2014)

• Conflicts of Interest - (i.e., activities that put the interest of the adviser ahead ofthe clients in contravention of fiduciary duty)

– Compensation arrangements that may affect recommendations to clients(especially undisclosed arrangements)

– Improper allocation of investments opportunities

– Controls and disclosure associated with side-by-side management ofperformance-based and fee-only based accounts.

– Risk controls and disclosures for illiquid investments and leveragedinvestment products and strategies

– Higher risk products or strategies targeted to retail (especially retired orelderly) investors

• Insider Trading– Failure to establish policies and procedures to handle material non-public

information

– Failure to monitor personal and employee trades or maintain blackout lists

– Failure to supervise IARs for insider trading violations

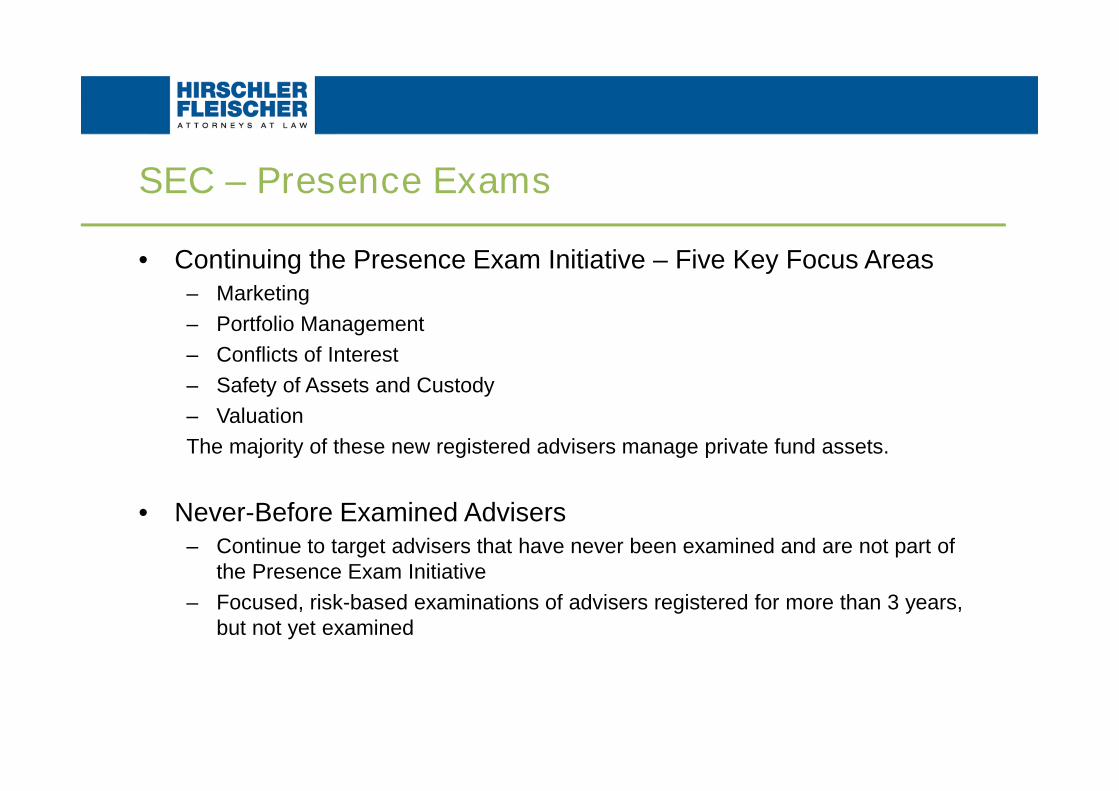

SEC – Presence Exams

• Continuing the Presence Exam Initiative – Five Key Focus Areas– Marketing

– Portfolio Management

– Conflicts of Interest

– Safety of Assets and Custody

– Valuation

The majority of these new registered advisers manage private fund assets.

• Never-Before Examined Advisers– Continue to target advisers that have never been examined and are not part of

the Presence Exam Initiative

– Focused, risk-based examinations of advisers registered for more than 3 years,but not yet examined

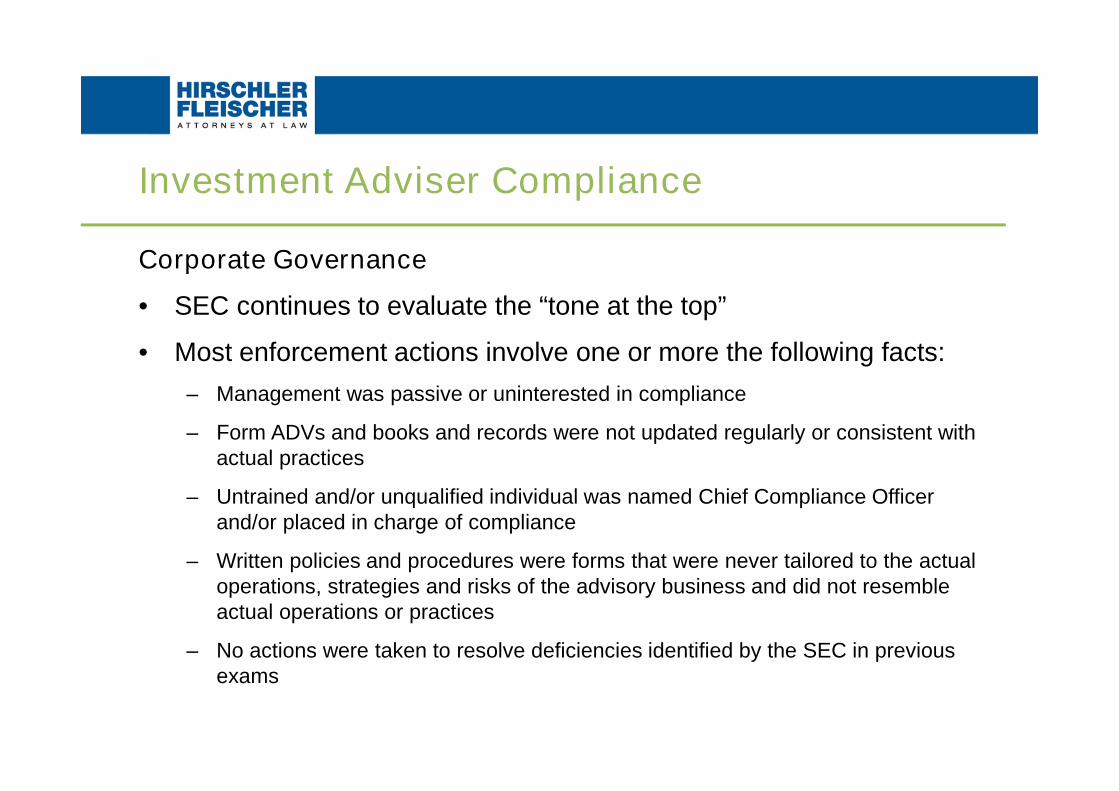

Investment Adviser Compliance

Corporate Governance

• SEC continues to evaluate the “tone at the top”

• Most enforcement actions involve one or more the following facts:

– Management was passive or uninterested in compliance

– Form ADVs and books and records were not updated regularly or consistent withactual practices

– Untrained and/or unqualified individual was named Chief Compliance Officerand/or placed in charge of compliance

– Written policies and procedures were forms that were never tailored to the actualoperations, strategies and risks of the advisory business and did not resembleactual operations or practices

– No actions were taken to resolve deficiencies identified by the SEC in previousexams

Compliance

• Rule 206(4)-7 – Written Policies and Procedures

– Tailor to the actual business practices of the adviser

– Review for adequacy and effectiveness at least annually

– Designate a qualified individual to be Chief Compliance Officer

– Maintain a compliance calendar with important dates highlighted to prompt action

• Rule 204(A)-1 –Code of Ethics

– Reflects the fiduciary obligations and compliance with federal securities laws

– Require initial and annual securities holding reports and at least quarterly transaction reportsof all personal securities transactions

– Require pre-clearance before a supervised person acquires any security

– Establish prohibitions on personal trading in securities the adviser is recommending

– Maintain a record of all written acknowledgements of receipt of the Code for eachsupervised person

– Maintain a record of any violation of the Code and the actions taken in response

– Maintain records of all personal securities holdings/transactions reports

Compliance

• Conduct an annual compliance review to test the effectiveness andadequacy of your compliance program

– Create a customized assessment of the firm’s specific business operations, practices andrelationship and how they have evolved since the last review

– Maintain a clear understanding of potential risks and conflicts and how they may arise

– Document all positive and negative findings

– Address and document the method of mitigating any negative findings

– Revised policies and procedures to make them effective, especially where the written policyor procedure did not work as designed

• Conduct a periodic review of all marketing and advertising materials

• Seek help!

– Compliance consultants

– Qualified attorneys

– Qualified accountants

Enforcement

0

20

40

60

80

100

120

140

160

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Year-by-Year SEC Enforcement Statistics

Broker-Dealer Investment Adviser/Investment Co.

686 cases in FY 2013

140 RIA/RIC cases(147 in FY 2012)

121 BD cases(134 in FY 2012)

$3.4 billion indisgorgement andpenalties(10% increase v FY 2012)(22% increase v FY 2011)

Enforcement Actions

• Compliance programs and supervisory structure– Northern Lights Compliance Services, LLC (May 2, 2013)

– Carl D. Johns (Aug. 27, 2013)

– Chariot Advisors LLC (Aug. 21, 2013)

– Institutional Shareholder Services Inc. (May 23, 2013)

– Modern Portfolio Management, Inc. (Oct. 23, 2013)

– Equitas Capital Advisors, LLC (Oct. 23, 2013)

– Stephen Derby Gisclair (Oct. 23, 2013)

Enforcement Actions

• Failure to disclose allocation errors; cross trades– Western Asset Management Company (Jan. 27, 2014)

• Performance and background claims– Oppenheimer Asset Management Inc. (Mar. 11, 2013)

– ZPR Investment Management, Inc. (Apr. 4, 2013)

• Best execution– Manarin Investment Counsel Ltd. (Oct. 2, 2013)

– A.R. Schmeidler & Co., Inc. (July 31, 2013)

– Goelzer Investment Management, Inc. (July 31, 2013)

• Soft dollar payments– Instinet, LLC (Dec. 26, 2013)

Enforcement Actions

• Custody– Further Lane Asset Management, LLC (Oct. 28, 2013)

– GW & Wade, LLC (Oct. 28, 2013)

– Knelman Asset Management Group, LLC (Oct. 28, 2013)

Enforcement Actions

• Modern Portfolio Management, Inc. (Oct. 23, 2013)– Owners failed to correct ongoing compliance violations at the firm despite prior

warnings from SEC examiners.

– One location on MPM’s website misleadingly represented that the firm had morethan $600 million in assets. However, on its Form ADV filing to the SEC duringthat same time period, it reported that the firm’s assets under management were$359 million or less.

– The firm failed to conduct any compliance review in at least two years,notwithstanding the mandate of Advisers Act Rule 206(4)-7 that requires such areview and deficiency letters identifying the shortcoming.

– Owners failed to determine whether the designated chief compliance officer wasfamiliar with SEC guidance governing performance advertising, but nonethelessmade the chief compliance officer responsible for the review and approval ofsuch advertising.

– Owners agreed to be censured and pay a total of $175,000 in penalties.Owners must complete 30 hours of compliance training, and MPM has agreed todesignate someone other than owners or the prior CCO to be its chiefcompliance officer.

Enforcement Actions

• Western Asset Management Company (Jan. 27, 2014)– WAM purchased $50 million of the initial offering of a $500 million private placement. The

preliminary prospectus stated that an eligible purchaser excluded employee benefit planssubject to ERISA.

– Through a coding error (changing the security type from “asset-backed security” to“corporate debt”, WAM’s automated compliance system, relied on to ensure compliance withrestrictions regarding the type of securities that could be acquired for various accounts,incorrectly stated that the private securities were ERISA eligible.

– In October 2008 the firm learned from an email sent by a former institutional client that theprivate securities were not ERISA eligible.

– WAM identified the accounts impacted but did not immediately correct the error or notify theclients. Eventually the securities were sold at a loss. Clients were never informed.

– SEC alleged that the should have promptly disclosed the error to clients no later thanDecember 2008 and that WAM had violated Section 206(2) (anti-fraud provision) and Rule206(4)-7 (policies and procedures rule).

– The firm also failed to have adequate compliance policies and procedures requiring thenotification of clients.

– To resolve the matter the firm agreed to implement a series of undertakings and consentedto the entry of a cease and desist order, a censure and an agreement to pay disgorgementof $8,111,582, prejudgment interest and a civil money penalty of $1 million.

Enforcement Actions

• Klein and Michael Shechtman (September 20, 2013)– Klein runs an RIA and was charged by the SEC in September 2013 with insider trading of

King Pharmaceutical (King) stock prior to Pfizer’s acquisition of the company.

– Klein learned about the planned acquisition from an attorney who worked for King.

– The attorney and Klein were friends and the attorney was a client of Klein’s investment firm.

– The insider tip was allegedly conveyed at a dinner at the attorney’s home.

– Klein bought shares of King for himself and 46 clients, including the attorney.

– After the acquisition was announced, Klein sold the King stock for himself and his clients,netting over $300,000 in profits.

– SEC did not demand that Klein or his firm be barred from the securities industry in the initialcomplaint

Enforcement Actions

• The Broken Windows Policy– The theory that when a window is broken and later fixed, this

signals that disorder will not be tolerated. When a brokenwindow is not fixed, it sends a signal that breaking windows willbear no consequences.

– Chairman Mary Jo White (2013) – “The same theory can beapplied to our securities markets – minor violations that areoverlooked or ignored can feed bigger ones, and, perhaps moreimportantly, can foster a culture where laws are increasinglytreated as toothless guidelines.”

Available for Questions

Hirschler Fleischer, PC - multispecialty law firm headquartered in Richmond, Virginia. Attorneysat Hirschler Fleischer focus in specific specialty areas law such as investment management,commercial real estate, mergers and acquisitions, and alternative energy. Serving clients acrossthe United States, Hirschler Fleischer prides itself on providing clarity in an increasingly complexmaze of structural, financial, legal and regulatory dynamics surrounding each of these areas.

Jim Van Horn, Jr. - Jim is co-chair of the IM Practice Group and he focuses his practice onrepresenting institutional investors, private investment funds and other market participants inconnection with a variety of transaction and compliance matters. Jim also advises investmentadvisers, wealth managers and broker-dealers concerning federal and state regulatory complianceand industry best practices. He can be reached at the following:

James W. Van Horn, Jr.Hirschler Fleischer, PCThe Edgeworth Building2100 East Cary StreetRichmond, VA 23223(T): 804-771-9541(E): [email protected]

Legal Disclaimer

This material is provided as a general information service to clients and friends of Hirschler Fleischer, PC.It does not constitute, and should not be construed as, legal advice on any specific matter, nor does itcreate an attorney-client relationship. You should not act or refrain from acting on the basis of thisinformation. This material may be considered Attorney Advertising in some states. Any prior resultsdiscussed in the material do not guarantee similar results or outcomes in the future. Links provided fromoutside sources are subject to expiration or change.

© 2014 Hirschler Fleischer, PC. All Rights Reserved.