financial management report on agency theory

DESCRIPTION

Financial Management Report on agency theoryTRANSCRIPT

Arjun Patel: PAT11239405 07/11/2012

Contents

Introduction...........................................................................................................................................1

The tasks performed by the Finance Directors/ Chief financial officers................................................1

Steward.............................................................................................................................................2

Operator............................................................................................................................................3

Strategist...........................................................................................................................................4

Catalyst..............................................................................................................................................5

How have the tasks performed by the CFO changed in the present climate?.......................................6

Communicating with the CEO............................................................................................................8

Contributing to more than purely a financial role.............................................................................8

Adopting a new method for identifying and training talent..............................................................8

Improving business knowledge.........................................................................................................9

How do issues of agency theory and information asymmetry impact on the firm?............................10

What is agency theory?...................................................................................................................10

The conflicts between shareholders and managers........................................................................10

Costs of the management and shareholder conflict........................................................................11

Methods for managing shareholder and manager conflicts............................................................11

Agency conflict between stockholders and creditors......................................................................12

Conclusion...........................................................................................................................................12

References:..........................................................................................................................................13

Bibliography:.......................................................................................................................................15

Arjun Patel: PAT11239405 07/11/2012

Introduction

The on-going financial crisis has led to greater regulation expanding dramatically coupled

with heightened uncertainty about the future, this has directly had an impact on the scope

of responsibilities of a chief financial officer (CFO). In addition to being a leader of a complex

and diverse finance function (Ernst and Young, 2011 p.8). This report will look into the

functions and the new challenges a chief financial officer may now encounter, as well as

how the issues of agency theory and information asymmetry impact on the firm.

The tasks performed by the Finance Directors/ Chief financial officers

In todays’ economic uncertainty the role of the chief financial officer (CFO) is continuously

under scrutiny from both external and internal pressure from the company. This pressure

comes from financial reaffirmations, heightened regulatory requirements due to a weaker

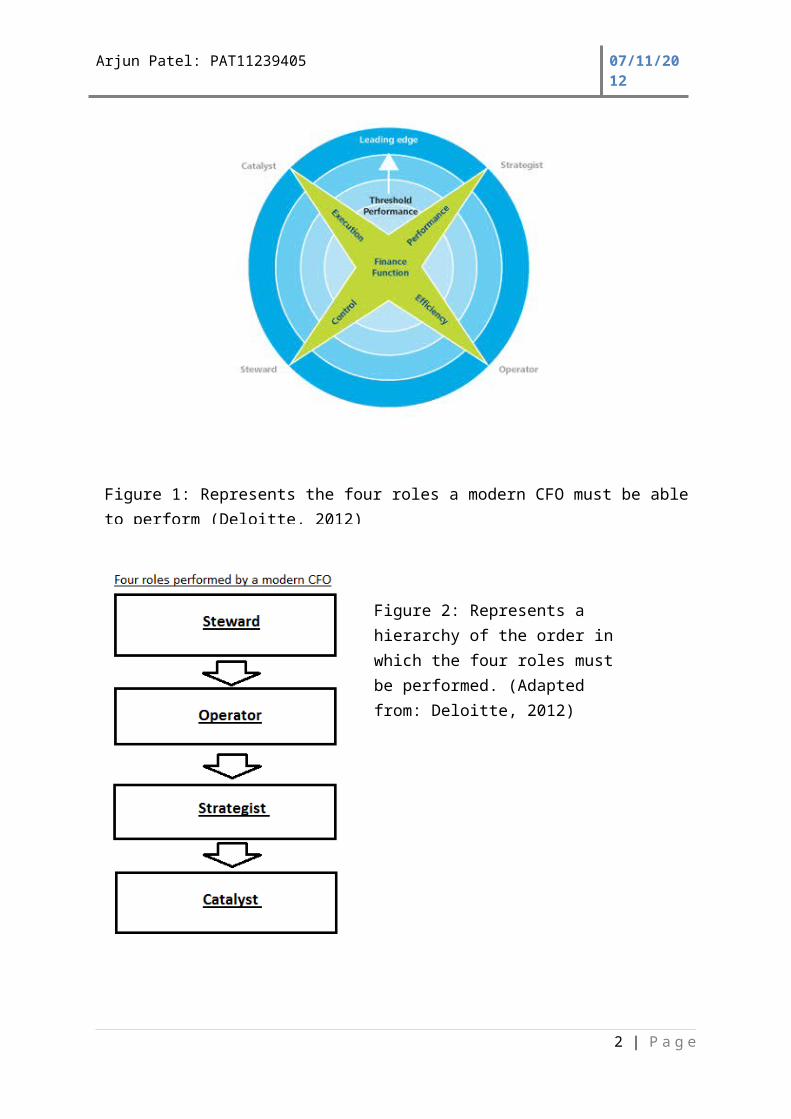

global economy and further pressure from investors. Deliotte (2012) have concluded that in

todays’ modern era the roles CFOs are expected to perform are divided into four categories

these are represented in figure 1, these include steward, operator, strategist and catalyst.

1 | P a g e

Figure 1: Represents the four roles a modern CFO must be able to perform (Deloitte, 2012)

Arjun Patel: PAT11239405 07/11/2012

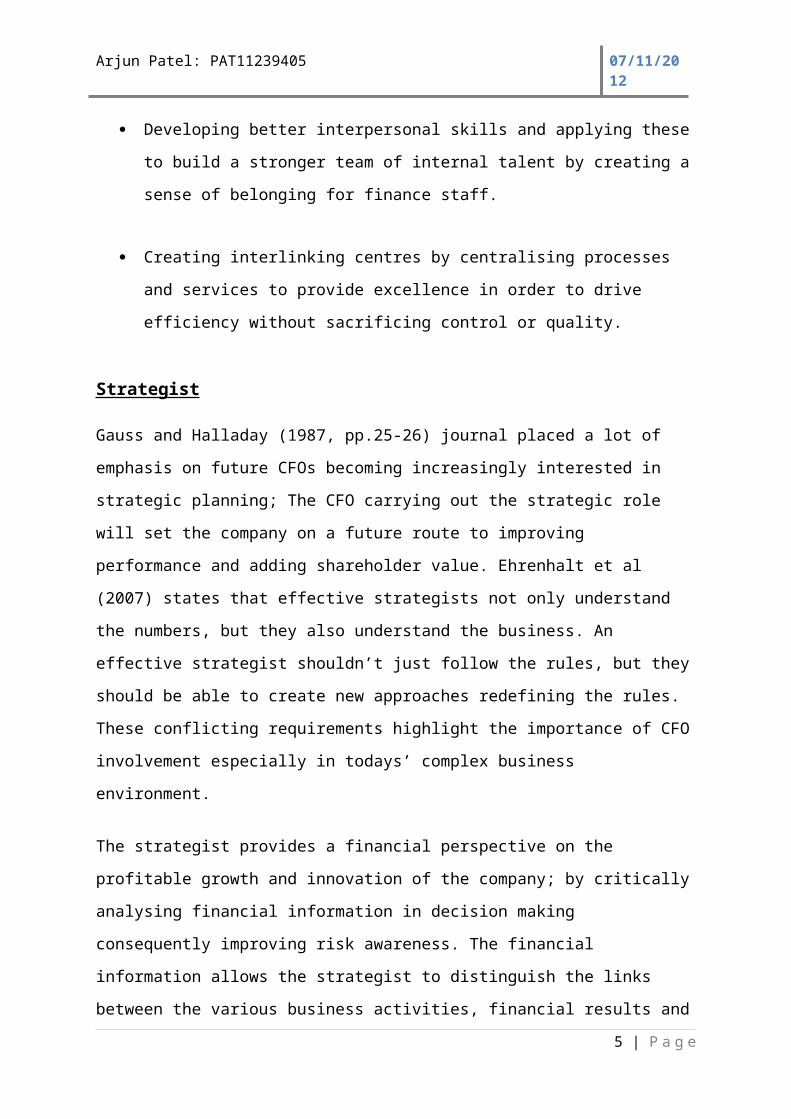

Figure 2 illustrates the order in which a CFO must perform these four modern roles. CFOs

that carry out the wrong order are likely to find themselves moving out rather than up.

Steward

This involves protecting the interests’ of the business by balancing the claims created by

people outside the business. Preservation of the company's assets and resources, managing

risk as well as the use of accounting and control are at the heart of the stewardship role.

The steward must also ensure the company abides by the regulations and legislation of the

company in terms of financial reporting and control requirements; the CFO must also

monitor financial statements to make sure they are timely and relevant thus ensuring its

quality. Ehrenhalt et al (2007) supports that performing the role of stewardship effectively,

requires CFOs to be able to display a variety of different abilities these include:

Not only presenting, but also interpreting the companies information provided by

the financial controller and management accountant on the financial reporting risks.

2 | P a g e

Figure 2: Represents the hierarchy of the order in which the

Figure 2: Represents a hierarchy of the order in which the four roles must be performed. (Adapted from: Deloitte, 2012)

Arjun Patel: PAT11239405 07/11/2012

These include going concern and liquidity risk, then to focus on the critical controls.

The CFO must be able to focus on the critical controls of the business.

The CFO must clarify responsibilities by reinforcing Finance’s authority to make

decisions.

Taking greater responsibility for accounting data by effectively communicating with

the Chief Information Officer, then taking responsibility for the collection and

management of financial and management reporting information this can be in the

form of annual reports.

Focus on talent management by hiring knowledgeable experienced accountants,

therefore avoiding restatements of financial information which can be time

consuming and result in further errors being made.

Create standards throughout the company for processes, data and systems therefore

avoiding conflict.

Operator

This role primarily focuses on efficiency and service levels; the key to reaching this is to

create an operating model for finance which balances between service levels and cost

without sacrificing quality such as outsourcing as a method of reducing costs. CFOs that

have demonstrated this role effectively have shown their ability to:

Improve management performance by creating effective programs and measuring

the performance of finance personnel.

Developing better interpersonal skills and applying these to build a stronger team of

internal talent by creating a sense of belonging for finance staff.

3 | P a g e

Arjun Patel: PAT11239405 07/11/2012

Creating interlinking centres by centralising processes and services to provide

excellence in order to drive efficiency without sacrificing control or quality.

Strategist

Gauss and Halladay (1987, pp.25-26) journal placed a lot of emphasis on future CFOs

becoming increasingly interested in strategic planning; The CFO carrying out the strategic

role will set the company on a future route to improving performance and adding

shareholder value. Ehrenhalt et al (2007) states that effective strategists not only

understand the numbers, but they also understand the business. An effective strategist

shouldn’t just follow the rules, but they should be able to create new approaches

redefining the rules. These conflicting requirements highlight the importance of CFO

involvement especially in todays’ complex business environment.

The strategist provides a financial perspective on the profitable growth and innovation of

the company; by critically analysing financial information in decision making consequently

improving risk awareness. The financial information allows the strategist to distinguish the

links between the various business activities, financial results and to show how company

growth can be achieved profitably and reliably. An effective CFO performing this role will be

able to;

Continuously evaluate strategic decisions such as investment as well as the ability to

make tough decisions when necessary.

Create reports specifically aimed to meet the requirements of critical decisions that

need to be made.

Analyse the company's operations to display how actions and daily decisions can

affect shareholder value.

Arrange improvement projects by importance using value-based portfolio

management.

4 | P a g e

Arjun Patel: PAT11239405 07/11/2012

Catalyst

The Catalyst is an agent for change, primarily focused on creating a value attitude

throughout the organisation (Deliotte, 2012). This role helps the company execute its

strategies whilst monitoring the task throughout its process to ensure completion. A

challenge this role may face is obtaining the approval of other executives that the role of

catalyst finance should be undertaking. Other executives will soon realise the value of

finances contribution to the company and gradually turn to the CFO for support and

assistance with execution.

CFOs demonstrating their ability to be an effective catalyst have shown the following

capabilities:

Recruiting qualified staff and supporting them grow, as well as allowing them to

migrate between the different functions within the company.

Driving financial thinking and thoroughness throughout the company by promoting

value discipline and monetary literacy.

Driving accountability through personal leadership, dedication and measurement.

Understanding what it takes to achieve tasks within the company and applying that

knowledge to continuously drive execution.

5 | P a g e

Arjun Patel: PAT11239405 07/11/2012

How have the tasks performed by the CFO changed in the present climate?

In Wu (2011, pp.840-843) journal he elucidates that the past 20 years have been led by

macro-economic uncertainty, economic globalisation and increasingly complex environment

business, which has caused CFOs to adapt and perform different roles. CFOs who want to

get ahead can't afford to ignore any of the four roles. The modern CFO continues to include

the traditional areas of financial stewardship but, has now moved to the more progressive

areas of strategic and business leadership, strategy and overseeing operations which include

growth of the company.

The recent global financial crisis has brought all CFOs on the spotlight more than ever

before. CFOs are primarily evaluated by the company’s overall performance, when company

performance falls short the CFO is usually the scapegoat as in the case of Sir Fred Goodwin

(Goff, 2012) who was predominantly blamed for the collapse of the Royal Bank of Scotland,

despite his decisions being made as a group in the boardroom. Along with new pressures of

continuously being under scrutiny, the modern CFO has now had to undertake additional

responsibility this includes corporate governance, operational and strategic decisions of the

company. The old era of only supplying financial information has moved on, now the CFO is

also providing business advice.

In a recent survey by Ernst and Young (2012) 530 CFOs were asked how important it was to

have experience in a range of roles for a future CFO to perform, selecting only their top

three. The results are summarised in figure 3. CFOs rated that having a wider range of

finance roles, international exposure and embarking on a major strategic change project

where among the top three. This further supports the CFOs roles adapting over the past 20

years.

6 | P a g e

Arjun Patel: PAT11239405 07/11/2012

The CFO now partakes more in an active role by taking roles such as talent management,

contributing to areas beyond finance, and assuming the role of CEO designate (Kalra, 2011).

The CFO is now required to contribute to three main areas these include:

Improving the company’s compliance with new legislation.

Providing guidance as well as strategic business advice to the CEO.

Ensuring cost efficiency of the accounting and finance function.

Clements (2005, p.1) suggests that the greater demand on the modern CFO has adapted

them to perform many roles these now also include:

7 | P a g e

Figure 3: represents a survey questioned to 530 CFOs on the importance of having experience in a range of roles for a future CFO. (Ernst & Young, 2012)

Arjun Patel: PAT11239405 07/11/2012

Communicating with the CEO

Able to convert business objectives into business enablers; this includes knowing when to

outsource finance and accounting functions. Clements (2005, p.1) explains that this can give

greater flexibility in the market place due to it helping maintain profitability.

Taking a greater proactive role; being the driving force behind systems, processes and

employee motivation.

With the CFO being the external face of the company; he needs to ensure consistency and

transparency as well as be knowledgeable in foreign laws and develop skills on change

management, so he can be the main point of contact for the CEO.

Contributing to more than purely a financial role

Performing the role of public relations officer; helping to resolve imbalances between the

external and internal stakeholders this ensures there is balance in the board, consequently

resulting in joint effort to achieve company growth.

Communicating with the various functions in the organisation; helping to improve staff

morale, recruitment and team development this also adds to the importance of being a

good listener and communicator.

Adopting a new method for identifying and training talent

Providing the opportunity for team members to migrate from the finance function;

therefore producing an individual with greater experience in the different areas of the

company as well as higher job satisfaction.

8 | P a g e

Arjun Patel: PAT11239405 07/11/2012

Providing greater structured internal training; training courses such as leadership

management can give finance members the ability to be more confident with progressing

within the more senior positions within the company, as well as giving them correct skills for

success in the future.

Give employees training in field; this provides employees with a complete perspective of the

business.

Managing the changing expectations of young and new people entering the market; reduction of staff in the middle management levels has led to new staff taking up these new

roles responsibilities their ability to adapt to these are vital for their survival.

Improving business knowledge

Focusing more on the foundations of business rather than accounting controlling; this can

be achieved by delegating routine tasks such as maintaining books therefore creating more

time for the CFO to look at the strategic and corporate sections of the company.

Adding more layers to strategy and decision-making; this means thinking about creating

value in the company rather than just profit and allocating more time to manage external

stakeholder expectations rather than just internal stakeholders. This also means keeping

external stakeholders well-informed. After British Petroleum Company (BP), oil disaster it

sparked concerns amongst investors however, the annual report of BP (2011), highlights

that they want to continue keeping their external stakeholders well-informed about their

future strategies and how they are going to achieve them.

Keep up-to-date and have access to information continuously; with the modern

technological era the CFO should be easily able to access information about the

organisation, keeping on top of all developments as well as the ever changing external

environment such as competitors, markets and the economy.

In Shelton (1987, pp.40-42) journal he explains the importance of looking into the past in

order to understand and face the challenges of the future, there is no doubt that the past

9 | P a g e

Arjun Patel: PAT11239405 07/11/2012

few years have led to a vast transformation on the roles of a CFO. The time dedicated to the

CFO’s routine administration jobs have now been focused on the larger strategic matters of

the organisation.

How do issues of agency theory and information asymmetry impact on the firm?

What is agency theory?

This is a theory explaining the relationship between principals such as agents and

shareholders. An agent such as a company executive is a person authorised by the principal

such as a shareholder to act on his or her behalf. It is part of an Agents responsibility to try

to act at all times in the best interests of his or her principal. But putting that into the

context of the relationship between the managers of the company and its shareholders and

you have what is known as the "agency problem”. Campbell, Stonehouse and Houston

(2002) elucidate that the agency theory suggests that agents (Managers) may seek to

maximise their own benefit at the expense of their principles (Shareholders).

Today's managers have wider responsibilities to employees, to the environment as well as

the government and these are often in conflict with their responsibility to shareholders

(Hindle 1994, p.31-32). As responsibility faces further down the management ladder these

other responsibilities include more and more into the agency relationship.

The conflicts between shareholders and managers

Agents are likely to have dissimilar motives to principals. They may be influenced by other

factors these may include financial rewards, labour market opportunities, and relationships

with other parties that are not directly relevant to principals (ICAEW, 2012). This can

consequently cause agents to be more hopeful about the company performance as well as

their own; these differing interests amongst both parties can cause agents to have an

enticement to provide bias information. Agents have more knowledge about the overall

10 | P a g e

Arjun Patel: PAT11239405 07/11/2012

operations and finance of the company therefore they are in a greater position for gathering

information, which principles do not have the access to. Principles may raise their concerns

about information asymmetries as agents are usually in a more knowledgeable position.

Costs of the management and shareholder conflict

Managers may award themselves and staff with greater terms and conditions, consequently

adding as an expense, reducing overall profit therefore lowering shareholder returns. This in

turn may cause a reduction in shareholder returns, causing shareholders to sell their own

shares. The conflict of interest between the two parties may cause agency costs to arise,

these are defined as the costs incurred to maintain an effective agency relationship between

shareholders and managers, an example is bonuses dependant on management

performance, Rosen (1995, pp.12-15) described their sole purpose as a form of

encouragement to managers to maximise shareholder wealth rather than their own

interests.

The three main types of agency costs include:

Opportunity costs lost due to share-holder conflicts, such as shareholder votes

required to carry out certain company issues.

Extra expenses due to monitoring managerial activities these include audit

expenditure.

Restructuring the company to hinder adverse managerial behaviour, this can involve

recruiting outside board members however, it can restrict managerial power.

11 | P a g e

Arjun Patel: PAT11239405 07/11/2012

Shareholders attempts to prevent undesirable managerial behaviour can also incur a loss on

shareholder wealth, due to incorrect managerial decisions being made. The opportunity

costs of these restrictions have to be balanced in order to improve shareholder wealth.

Methods for managing shareholder and manager conflicts

The methods used for controlling shareholder and manager agency conflicts include:

Providing performance based plans with marginal monitoring therefore encouraging

managers to act in shareholders' interests, most of today’s publicly traded companies now

offer performance shares to their managers.

Direct intervention by shareholders this can be in the form votes to carry out

particular decisions.

The threat of discharging the manager and appointing a new one.

Agency conflict between stockholders and creditors

Shareholders and managers borrow money expecting a return larger than the interest paid

on the loan. Creditors review their risk of the venture and determine their rate of return.

The primary issue causing conflict between these parties is trust. Shareholders attempt to

take risky projects with bondholders’ money through the work of managers; this is because

they have more to gain and only an equal amount to lose from a failed project. The

managers and shareholders must work together to determine how much to deceive

creditors in order to gain the finance.

Conclusion

The role of the modern CFO has undergone numerous changes in the past 20 years; he is no

longer only involved in capital expenditure decisions. The CFOs advice is now required for

matters throughout the organisation, the demands of his job have now diversified due to

new challenges he now faces, he has moved from the routine administrative functions to

12 | P a g e

Arjun Patel: PAT11239405 07/11/2012

dedicating himself in more strategic issues. However, the CFO also needs to find the correct

balance in keeping shareholders well informed in order to avoid information asymmetries

and agency problems arising. Only when he realises how to adapt and become an effective

collaborator, partner and change-driver that his CEO and the entire company expect, he will

be able to effectively perform his new modern roles expected of him today.

.

References:

BP (2011) Annual report and form 20-F 2011 [WWW] BP Available from:

http://www.bp.com/assets/bp_internet/globalbp/globalbp_uk_english/set_branch/

STAGING/common_assets/bpin2011/downloads/

BP_Annual_Report_and_Form_20F_2011.pdf

Campbell, D. and Stonehouse, G. and Houston B. (2002) Business Strategy: an introduction.

2nd ed. Oxford: Elsevier Butterworth Heinemann.

Clements, S. (2005) The changing role of the CFO. As demands on CFOs continue to grow,

outsourcing can be a viable form of support, 5 (2) p.1.

Deliotte (2012) Four faces of the CFO [WWW] Deliotte. Available from:

http://www.deloitte.com/view/en_US/us/Insights/browse-by-role/Chief-Financial-Officer-

CFO/Four-Faces-of-the-CFO-Chief-Financial-Officer/index.htm

Ehrenhalt et al (2007) Financial Executive: Mastering the four key roles of the CFO [WWW]

Farlex. Available from: http://www.thefreelibrary.com/Mastering+the+four+key+CFO

%27s+roles%3A+the+job+of+CFO+is+quite+different...-a0166979247

13 | P a g e

Arjun Patel: PAT11239405 07/11/2012

Ernst & Young (2012) Finance Forte; The future of finance leadership [WWW] Ernst & Young.

Available from:

http://www.ey.com/Publication/vwLUAssets/Finance_forte_The_Future_of_Finance_Leade

rship_2011/$FILE/The-Future-of-Finance-Leadership.pdf

Gauss, J.W. and Halladay, D.A. (1987) Today’s stronger, tougher, smarter financial manager.

Healthcare Financial Management: Journal of the Healthcare Financial Management

Association, 41 (8) pp.25-26.

Goff, S. (2012) Rise and fall of Fred Goodwin. [WWW] Financial times. Available from:

http://www.ft.com/cms/s/0/347318fc-4c3c-11e1-b1b500144feabdc0.html#axzz2DwpZk1aU

Hindle, T. (1994) Pocket strategy. New York: Penguin Group.

ICAEW (2012) Agency theory and the role of audit [WWW] ICAEW. Available from

https://www.icaew.com/~/media/Files/Technical/Audit-and-assurance/audit-quality/audit-

quality-forum/agency-theory-and-the-role-of-audit.pdf

Kalra, D. (2011) The changing roles of today’s CFOs [WWW] Egon Zehnder International.

Available from:

http://www.egonzehnder.com/global/practices/functionalpractices/financialofficers/

publication/id/17500363

Rosen, R. (1995) Strategic Management: An Introduction. London: Pitman Publishing.

Shelton, R.M. (1987) The evolution of the CFO: looking into the past helps face the future.

Healthcare Financial Management: Journal of the Healthcare Financial Management

Association, 41 (8) pp.40-42.

14 | P a g e

Arjun Patel: PAT11239405 07/11/2012

Wu, J. (2011) CFO complex characteristic, agency costs and corporate value: Based on

financial engineering cube concept. Business management and electronic information, (May)

pp.840-843.

Bibliography:

BP (2011) Annual report and form 20-F 2011 [WWW] BP. Available from:

http://www.bp.com/assets/bp_internet/globalbp/globalbp_uk_english/set_branch/

STAGING/common_assets/bpin2011/downloads/

BP_Annual_Report_and_Form_20F_2011.pdf

BT (2012) BT Group plc Annual Report & Form 20-F 2012 [WWW] BT. Available from:

http://www.btplc.com/Sharesandperformance/Annualreportandreview/pdf/

BTAnnualReport2012_smart.pdf

Gore, C. and Murray, K. and Richardson, B. (1992) Strategic Decision-Making. London:

Cassell.

Campbell, D. and Stonehouse, G. and Houston B. (2002) Business Strategy: an introduction.

2nd ed. Oxford: Elsevier Butterworth Heinemann.

15 | P a g e

Arjun Patel: PAT11239405 07/11/2012

Clements, S. (2005) The changing role of the CFO. As demands on CFOs continue to grow,

outsourcing can be a viable form of support, 5 (2) p.1.

Deliotte (2012) Four faces of the CFO [WWW] Deliotte. Available from:

http://www.deloitte.com/view/en_US/us/Insights/browse-by-role/Chief-Financial-Officer-

CFO/Four-Faces-of-the-CFO-Chief-Financial-Officer/index.htm

Ehrenhalt et al (2007) Financial Executive: Mastering the four key roles of the CFO [WWW]

Farlex. Available from: http://www.thefreelibrary.com/Mastering+the+four+key+CFO

%27s+roles%3A+the+job+of+CFO+is+quite+different...-a0166979247

Ernst & Young (2012) Finance Forte; The future of finance leadership [WWW] Ernst &

Young. Available from:

http://www.ey.com/Publication/vwLUAssets/Finance_forte_The_Future_of_Finance_Leade

rship_2011/$FILE/The-Future-of-Finance-Leadership.pdf

Gauss, J.W. and Halladay, D.A. (1987) Today’s stronger, tougher, smarter financial manager.

Healthcare Financial Management: Journal of the Healthcare Financial Management

Association, 41 (8) pp.25-26.

Goff, S. (2012) Rise and fall of Fred Goodwin. [WWW] Financial times. Available from:

http://www.ft.com/cms/s/0/347318fc-4c3c-11e1-b1b500144feabdc0.html#axzz2DwpZk1aU

Hindle, T. (1994) Pocket strategy. New York: Penguin Group.

Hannagan, T. (2005) Management: Concepts & Practices. 4th ed. Essex: Pearson Education

Limited.

ICAEW (2012) Agency theory and the role of audit [WWW] ICAEW. Available from

16 | P a g e

Arjun Patel: PAT11239405 07/11/2012

https://www.icaew.com/~/media/Files/Technical/Audit-and-assurance/audit-quality/audit-

quality-forum/agency-theory-and-the-role-of-audit.pdf

Kalra, D. (2011) The changing roles of today’s CFOs [WWW] Egon Zehnder International.

Available from:

http://www.egonzehnder.com/global/practices/functionalpractices/financialofficers/

publication/id/17500363

McManus, J. and White, D. and Botten, N. (2008) Managing Global Business Strategies: A

twenty-first-century perspective. Oxford: Chandos Publishing.

Rosen, R. (1995) Strategic Management: An Introduction. London: Pitman Publishing

Raghavan, K. (2007) International Journal of Disclosure and Governance. A survey of

corporate governance and overlapping regulations in banking (August) pp.181-194

Shelton, R.M. (1987) The evolution of the CFO: looking into the past helps face the future.

Healthcare Financial Management: Journal of the Healthcare Financial Management

Association, 41 (8) pp.40-42.

Wu, J. (2011) CFO complex characteristic, agency costs and corporate value: Based on

financial engineering cube concept. Business management and electronic information, (May)

pp.840-843.

17 | P a g e

Arjun Patel: PAT11239405 07/11/2012

18 | P a g e